Kalyan Jewellers: From Kerala Gold Shop to Pan-India Empire

I. Cold Open & The Big Question

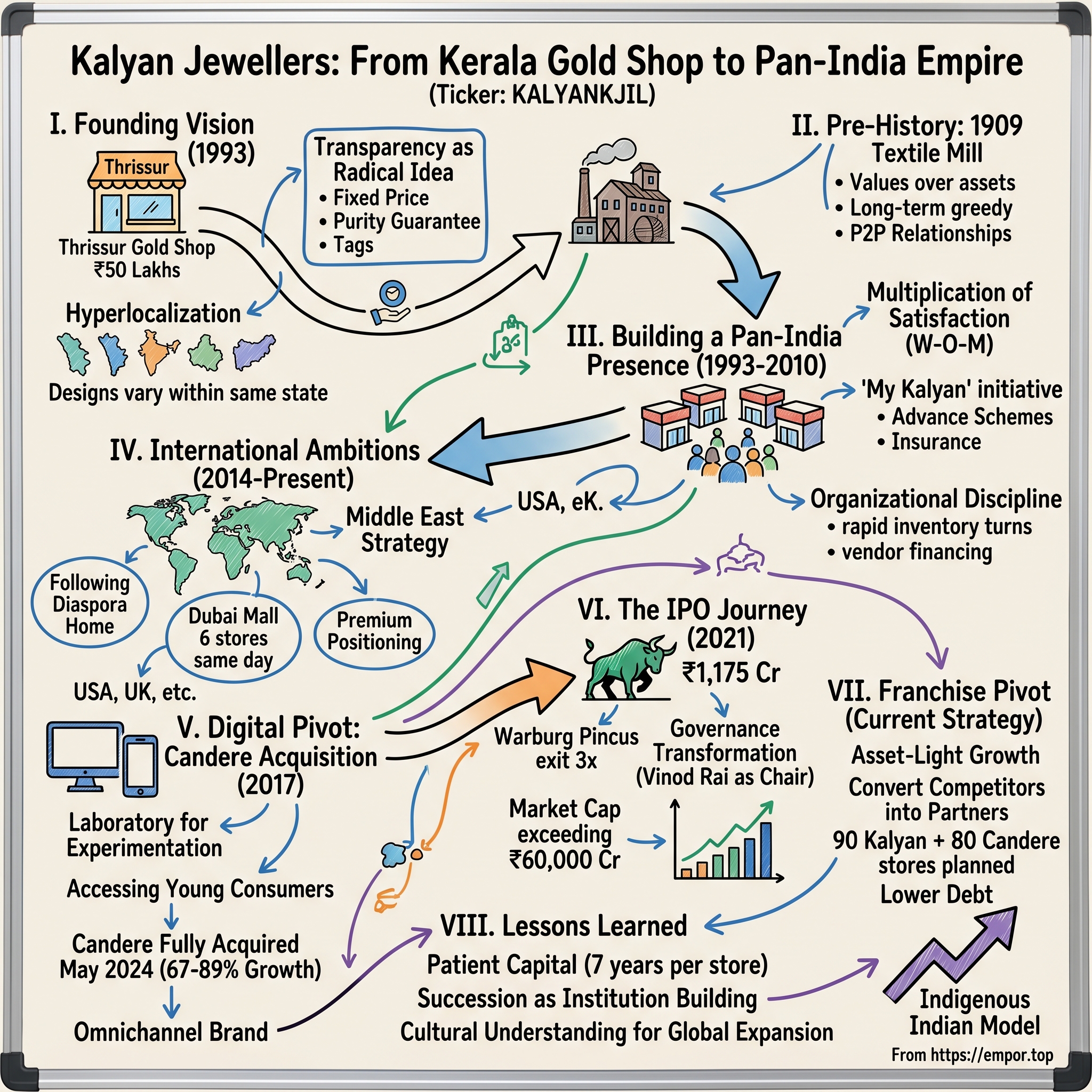

Picture this: A single 4,000-square-foot jewelry store opens in Thrissur, Kerala in 1993. The founder has ₹50 lakhs in capital and a radical idea—what if buying gold jewelry could be as transparent as buying groceries? Fast forward three decades, and that store has morphed into an empire spanning three continents, with over 315 showrooms and a market capitalization exceeding ₹60,000 crores.

The question that should haunt every retail strategist in India is deceptively simple: How did T.S. Kalyanaraman transform a regional gold shop into India's second-largest jewelry retailer, all while competing against Titan's marketing muscle, thousands of family jewelers with century-old relationships, and the most price-sensitive luxury consumers on earth? The answer lies not in a single breakthrough moment, but in a patient accumulation of counter-intuitive decisions: spending seven years perfecting one store before opening a second, launching six Middle East locations on the same day, acquiring an e-commerce startup when everyone said jewelry couldn't sell online, and most audaciously—choosing transparency in an industry that has thrived on opacity for millennia.

This is the story of how a priest's grandson from Kerala built a jewelry empire by doing exactly what the industry said couldn't be done. It's a masterclass in hyperlocalization at scale, family succession without destruction, and most importantly, how to transform a commodity business into a trust business. As of July 2025, Kalyan Jewellers operates more than 315 showrooms across India, Middle East and the US, making it a rare Indian retail success story that crossed both domestic state boundaries and international waters.

What makes Kalyan's ascent particularly fascinating for investors is that it happened in plain sight, yet few understood what they were witnessing until the company's ₹60,000 crore market cap forced them to pay attention. The themes we'll explore—hyperlocal customization, trust-building in high-ticket retail, franchise-model pivots, and diaspora-focused international expansion—aren't just Kalyan's story. They're a blueprint for how Indian consumer brands can scale in the 21st century.

II. The Pre-History: A Century of Kalyan Group

The year is 1909. India is still under British rule, the Wright brothers had flown just six years earlier, and in the temple town of Thrissur, Kerala, a Brahmin priest named Kalyanaraman Iyer makes a decision that would echo through four generations. He would become an entrepreneur.

This wasn't just unusual—it was revolutionary. In early 20th century Kerala, Brahmins occupied the apex of the caste hierarchy, their lives devoted to ritual, scripture, and spiritual guidance. Commerce was considered beneath them, the domain of other castes. Yet Kalyanaraman Iyer saw something others didn't: that building businesses could be a form of nation-building, that creating employment and prosperity was its own kind of service.

His vehicle? A textile mill in Thrissur. The choice was strategic—textiles were the backbone of Indian commerce, both a daily necessity and a cultural touchstone. Every Indian family, regardless of wealth, needed cloth. The business prospered through the tumultuous decades of independence struggle, partition, and the early years of the Indian republic. But then came the 1960s and India's romance with socialism. The government, in its infinite wisdom, decided that certain successful private enterprises should be "taken over" for the greater good. The Kalyan textile mill was nationalized.

For most business families, this would have been the end. A century of work erased by a bureaucratic decree. But the Iyers had something more valuable than assets—they had values. And those values, crystallized through adversity, would become the operating system for everything that followed.

T.K. Seetharamaiyer, Kalyanaraman's son, absorbed these lessons and passed them to his son, T.S. Kalyanaraman. The family philosophy was deceptively simple: business wasn't about quick profits but about building institutions that outlasted individuals. Trust wasn't a marketing slogan but a generational asset that took decades to build and seconds to destroy. And most importantly, setbacks weren't endings but transitions.

The nationalization of the textile mill taught the family a crucial lesson: never build a business that's too attractive to politicians. Stay under the radar. Grow quietly. Build trust locally before expanding nationally. These weren't just strategies—they were survival mechanisms honed over decades of navigating India's treacherous business environment.

By the 1980s, the family had diversified into various trading activities, but young T.S. Kalyanaraman was restless. Working with his father from age 12, he had absorbed not just the mechanics of business but its deeper rhythms. He understood something fundamental: in India, business wasn't B2B or B2C—it was P2P, person to person. Every transaction was a relationship. Every sale was a promise.

The foundation mythology of Kalyan Group wasn't about a single eureka moment or a technological breakthrough. It was about patient capital in the truest sense—not just financial patience but cultural patience, the willingness to wait generations for the right opportunity. That opportunity would come in 1993, when T.S. Kalyanaraman would take a century of accumulated wisdom and pour it into 4,000 square feet of retail space in Thrissur.

III. The Founding Story: T.S. Kalyanaraman's Vision (1993)

Walk into any traditional Indian jewelry store in 1992, and you'd encounter a peculiar ritual. The shopkeeper would pull out a worn booklet, flip through pages of designs, and ask you to point at what you liked. The actual jewelry? Locked away in a back room safe, brought out piece by piece, shrouded in ceremony and suspicion. Prices? Negotiable, which meant nobody ever knew if they got a fair deal. Quality? Trust us, sahib.

T.S. Kalyanaraman saw this charade and recognized an opportunity hiding in plain sight. Indians weren't buying jewelry—they were navigating an obstacle course of opacity, hoping they wouldn't get cheated on one of the most emotionally significant purchases of their lives. He started his first jewellery shop named Kalyan Jewellers in Thrissur City in 1993 with a capital of ₹50,00,000.

But Kalyanaraman's insight went deeper than just transparency. He understood that jewelry in India wasn't merely an economic transaction—it was a cultural sacrament. Every piece carried meaning: the mangalsutra that sealed a marriage, the bangles that announced a new bride, the gold coin given to a newborn. These weren't products; they were milestones made tangible.

His father had always dreamt of organizing the jewelry segment. "Earlier, there used to be small shops where jewelry was not stocked. People used to go by the booklet and trust the seller while buying expensive ornaments," Kalyanaraman would later recall. "My father wanted to bring in complete transparency into the business."

The solution was radical for its time: a 4,000-square-foot showroom where every piece of jewelry was displayed, tagged with a non-negotiable price, and backed by a purity guarantee. Customers could browse, compare, and choose without the psychological warfare of negotiation. It was the departmentalization of trust.

But the real genius was in what Kalyanaraman didn't do. He didn't try to change Indian jewelry preferences or impose a singular aesthetic. Instead, he recognized that India wasn't one market but thousands of micro-markets, each with distinct preferences passed down through generations. Jewellery is a complicated product, because tastes vary even within the same state. A Bengali bride's jewelry differed from a Punjabi bride's, which differed from a Tamil bride's—not just in style but in significance.

The first Kalyan store became a laboratory for this hyperlocal approach. Kalyanaraman would spend hours observing customers, noting which designs attracted women from different communities, which gold purities were preferred by different economic segments, how purchasing patterns changed with seasons and festivals. This wasn't market research—it was anthropology.

The early years were brutal. Established jewelers dismissed him as an upstart. Customers, conditioned by centuries of negotiation culture, were suspicious of fixed prices. Suppliers were reluctant to extend credit to an unknown player. But Kalyanaraman had something his competitors didn't: patience inherited from three generations of building and rebuilding.

He also had an unusual strategy for building trust. Instead of aggressive marketing, he focused on what he called "the multiplication of satisfaction." Every customer who left happy would tell ten others. Every complaint resolved generously would convert a skeptic into an evangelist. In a business where word-of-mouth could make or break you, Kalyanaraman was playing a different game—he was building a network effect before Silicon Valley had coined the term.

The masterstroke was the "My Kalyan" initiative—a customer service network that went beyond mere sales. The services provided by My Kalyan includes jewelry purchase advance schemes, gold insurance, wedding purchase planning, advance booking of purchases to protect against price increases, sale of gift vouchers and gold buying tips and education. This wasn't just customer service; it was customer partnership. Kalyan wasn't selling jewelry; it was managing life's golden moments.

By the late 1990s, the Thrissur store had become a phenomenon. Families would travel from neighboring districts specifically to shop at Kalyan. The store's annual revenue exceeded that of jewelers who had been in business for centuries. But Kalyanaraman did something unexpected—he didn't immediately expand. For seven years, he ran just one store, perfecting the model, understanding its economics, building the supply chain. This wasn't conservatism; it was strategic patience.

IV. The Expansion Playbook: Building a Pan-India Presence (1993-2010)

Seven years. That's how long T.S. Kalyanaraman resisted the siren song of expansion. While venture capitalists would later call this "product-market fit," Kalyanaraman was practicing something more fundamental: he was learning how to scale trust.

The second store finally opened in 2000, not in a metropolis but in Palakkad, another Kerala town just 80 kilometers from Thrissur. The choice puzzled industry observers. Why not Kochi? Why not Bangalore? The Palakkad store would teach Kalyanaraman his most valuable lesson about Indian retail.

Despite being in the same state, speaking the same language, and being just an hour's drive away, Palakkad customers had distinctly different jewelry preferences from Thrissur. The designs that flew off shelves in Thrissur gathered dust in Palakkad. The gold purity preferences were different. Even the average ticket sizes varied. "Localisation in the jewellery industry is very important," Ramesh Kalyanaraman would later explain. "What is sold in one region may not do well in another region even if the customers have migrated, as the tastes and preferences vary."

This revelation would become the cornerstone of Kalyan's expansion strategy. Instead of replicating a standard template across locations—the McDonald's model—Kalyan would create what was essentially a federation of local jewelry stores, united by trust and systems but differentiated by inventory. Kalyan's biggest strength is in these craftsmen who create unique designs just for us from every nook and corner of India.

Following the success of the initial store, Kalyanaraman's sons, Rajesh Kalyanaraman and Ramesh Kalyanaraman, joined the family business. This wasn't nepotism—it was strategic succession. Rajesh brought financial acumen; Ramesh understood operations. Together with their father, they formed a triumvirate that could execute expansion without losing the essence of what made Kalyan special.

The expansion that followed was methodical, almost musical in its rhythm. First, saturate Kerala—by 2005, Kalyan had stores across the state. Then, follow the Malayalam diaspora—Bangalore, Chennai, Mumbai. Each new market was entered not with one store but with a cluster, allowing for economies of scale in marketing and operations.

But the real innovation was in how Kalyan solved the working capital puzzle that had constrained Indian jewelers for centuries. Gold is expensive. Holding inventory across multiple stores requires massive capital. Traditional jewelers either stayed small or took on crushing debt. Kalyan pioneered a different model: vendor financing combined with rapid inventory turns. Suppliers would provide gold on credit, Kalyan would sell quickly, pay suppliers, and repeat. It was the Dell model applied to Indian jewelry.

The company also revolutionized jewelry retail marketing in India. Massive marketing campaigns and launches, path-breaking ads which were never-before seen in jewellery advertising, multi-storey large format jewellery showrooms, same-day multi-launch ceremonies and events. While competitors whispered, Kalyan shouted. But it was strategic shouting—every campaign was tied to a cultural moment, a festival, a wedding season.

The customer acquisition strategy was equally sophisticated. Kalyan didn't just want customers; it wanted families. The purchase advance schemes weren't just financial products—they were relationship builders. A family would start a scheme when their daughter was 15, accumulating gold for her wedding. By the time she married, Kalyan wasn't just a store—it was part of the family story.

By 2010, Kalyan had crossed an inflection point. It was no longer a Kerala jeweler with stores outside; it was a pan-Indian player with particular strength in South India. The company had cracked the code that had eluded Indian retailers for decades: how to be simultaneously hyperlocal and nationally scaled.

The numbers told the story. From one store generating perhaps ₹50 crores annually in 2000, Kalyan had grown to dozens of stores generating thousands of crores. But the more important metric was trust. In an industry where customers traditionally bought from the same jeweler their parents and grandparents had used, Kalyan had convinced millions to switch. They hadn't just built a retail chain; they had engineered a behavioral change.

V. International Ambitions: The Middle East Strategy (2014-Present)

The Dubai Mall, 2014. Six Kalyan Jewellers stores open simultaneously across the Gulf Cooperation Council (GCC) countries—a choreographed display of ambition that would make even the most aggressive Silicon Valley growth hacker take notes. But this wasn't about blitzscaling. It was about following your customers home.

Here's what most people miss about Indian international expansion: the first wave isn't about conquering foreign markets—it's about serving your diaspora. The GCC countries host over 8 million Indians, many from Kerala, Karnataka, and Tamil Nadu—Kalyan's core markets. These weren't new customers; they were existing customers who happened to live abroad.

The math was compelling. An Indian family in Dubai earned in dirhams but measured wealth in gold. They bought jewelry for themselves locally but also for family back in India. They wanted Indian designs, Indian customs, Indian trust—but with international convenience. Kalyan wasn't entering a foreign market; it was extending its domestic market across geography.

The execution was theatrical. "India's largest jewellery retailer, Kalyan Jewellers, has added $200m annually to its bottom line since opening its first store in the GCC in 2014," the company would later report. "When Kalyan launched in the GCC two-and-a-half years ago, it did so by opening six stores on the same day in Dubai."

But why six stores on the same day? This wasn't vanity—it was strategic signaling. In the Middle East, size matters. Opening one store makes you a player; opening six makes you an institution. It was a $50 million bet that paid off spectacularly. The stores were profitable from year one, a rarity in international retail expansion.

The Middle East taught Kalyan valuable lessons about premium positioning. In India, Kalyan competed on trust and transparency. In Dubai, where gold souks had existed for centuries and competition was fierce, they needed a different edge. The answer: experience. The Middle East stores weren't just bigger; they were theatrical. Multiple floors, VIP sections, dedicated wedding planning areas. It was jewelry retail as entertainment.

With these launches, Kalyan Jewellers' presence in the UAE now spans 22 locations, strengthening its position as one of the most prominent jewellery retailers in the region. The expansion continued methodically: UAE, Qatar, Oman, Kuwait. Each market was slightly different—Kuwait preferred heavier pieces, Qatar wanted more diamonds—but the core proposition remained consistent: Indian jewelry with international service standards.

The financial impact was substantial. The Middle East operations contributed approximately 12-15% of overall revenues but, more importantly, higher margins. The average ticket size in Dubai was three times that of India. The customers were less price-sensitive, more brand-conscious. It was Kalyan's finishing school in premium retail.

But the real strategic value of the Middle East wasn't just revenue—it was learning. Kalyan learned how to operate in developed markets, how to deal with international regulations, how to manage foreign currency risk. These lessons would prove invaluable as the company eyed its next frontier: the United States.

The U.S. expansion, launched in 2018, was different. This wasn't about serving the diaspora alone—though the 4.5 million Indian Americans were certainly the beachhead market. This was about testing whether an Indian jewelry brand could compete globally. The early results were mixed. American consumers didn't understand the Indian jewelry categories. The regulatory environment was complex. The working capital requirements were massive.

Kalyan Jewellers will enter the UK this fiscal. "Our overseas expansion will be focused on the US, UK and the Middle East till next fiscal. We are getting inquiries from countries like Australia, Malaysia, and Singapore, having a large Indian diaspora; however, our overseas expansion will be very calibrated", management recently indicated.

The international expansion strategy revealed something profound about Kalyan's ambitions. This wasn't just about growth—it was about building a global Indian brand. In a world where Indian companies often succeeded by being the back-office or the manufacturer, Kalyan wanted to be the front-end, the brand that customers chose.

VI. The IPO Journey & Capital Markets Story (2021)

March 2021. The Indian stock market is in the midst of a pandemic-driven digital frenzy. Tech startups with no profits are commanding billion-dollar valuations. And here comes Kalyan Jewellers—a traditional retailer selling the most ancient store of value—asking public markets for ₹1,175 crores.

The timing seemed off. The context was worse. COVID-19 had decimated retail. Weddings were postponed. Gold prices were volatile. Yet Kalyan's IPO would become a masterclass in how traditional businesses can access capital markets by telling a growth story wrapped in governance.

The IPO structure itself was revealing: ₹800 crores in fresh capital for expansion, ₹375 crores as an offer for sale by promoters and Warburg Pincus. This wasn't a cash-out; it was a capital structure optimization. The fresh funds would fuel the next phase of growth while the partial promoter exit would improve free float and liquidity.

Warburg Pincus's involvement added institutional credibility. They had invested $200 million in 2014 at a valuation of roughly $600 million. Seven years later, they were partially exiting at a valuation north of $2 billion. A 3x return in traditional retail? In India? This wasn't supposed to happen.

The IPO roadshow revealed Kalyan's equity story: organized jewelry retail in India was just 35% of the market. The shift from unorganized to organized was accelerating, driven by GST implementation, hallmarking regulations, and changing consumer preferences. Kalyan, as the second-largest organized player, was positioned to capture disproportionate share gains. The IPO was oversubscribed 2.61 times, with particularly strong demand from retail investors who subscribed 2.82 times their allocated portion. The institutional response was measured but positive—QIBs subscribed 2.76 times, suggesting cautious optimism from smart money.

But here's what made Kalyan's IPO truly remarkable: the post-IPO governance transformation. In 2022, the company onboarded Vinod Rai as its chairperson and independent non-executive director. Think about that—the former Comptroller and Auditor General of India, the man who exposed the 2G spectrum scandal, joining a family-run jewelry company. This wasn't window dressing; it was a signal that Kalyan was serious about institutional governance.

The market's initial reaction was lukewarm. The stock listed at a modest premium to its issue price of ₹87. But what followed was more interesting—a gradual rerating as investors began to understand the story. The company, with a market capitalization of Rs 60,959 crore today, has delivered spectacular returns to IPO investors.

The IPO proceeds deployment strategy was textbook capital allocation. ₹600 crores went straight to working capital—essentially funding inventory for new stores without taking on debt. This wasn't financial engineering; it was using equity capital to fund growth while maintaining balance sheet strength.

The public listing also forced operational discipline. Quarterly reporting meant management couldn't hide behind annual numbers. Every festival season, every gold price movement, every new store opening was now scrutinized. This transparency, initially seen as a burden, became a competitive advantage. Competitors were still operating in opacity while Kalyan was building institutional credibility quarter by quarter.

The shareholding pattern post-IPO revealed another strategic insight. The promoters retained 62.8% stake—enough to maintain control but not so much as to concern minority investors. Warburg's continued holding (even after partial exit) provided comfort to institutional investors. This wasn't a dump-and-run IPO; it was a long-term value creation story.

VII. The Digital Pivot: Candere Acquisition & E-commerce

Silicon Valley wisdom says jewelry can't be sold online. It's too personal, too expensive, too dependent on touch and feel. Someone forgot to tell Kalyan Jewellers, which in 2017 made a contrarian bet by acquiring a majority stake in Candere, an e-commerce jewelry platform that was burning cash and struggling to find product-market fit.

The acquisition price wasn't disclosed, but industry sources suggested it was a distress sale—Candere had raised venture capital but was running out of runway. For Kalyan, this wasn't just about buying technology or talent. It was about acquiring an option on the future of jewelry retail.

The integration strategy was unconventional. Instead of immediately merging Candere into the main brand, Kalyan let it operate independently, learning from its mistakes and successes. Candere became Kalyan's laboratory for experimentation—testing new designs, new price points, new customer acquisition strategies without risking the parent brand.

The real insight came when Kalyan realized that Candere wasn't competing with physical stores—it was accessing an entirely different customer. The average Candere customer was 28 years old, buying their first piece of "real" jewelry, comfortable with online shopping but intimidated by traditional jewelry stores. This wasn't cannibalization; it was market expansion.

In May 2024, Kalyan Jewellers fully acquired Candere, which now operates as a retail brand offering jewellery through both its website and retail stores. The full acquisition signaled a strategic shift—Candere was no longer an experiment but a core part of the growth strategy.

The transformation of Candere from pure-play e-commerce to an omnichannel brand was masterful. Instead of forcing online customers into stores or store customers online, Kalyan created a hybrid model. Customers could browse online, try in store, customize online, pick up in store. It was the kind of seamless experience that Amazon was still trying to figure out. The numbers validate the strategy. Candere recorded a revenue growth of approximately 89% during Q3 FY2025 as compared to the same period during the last year. The digital platform Candere recorded 67% revenue growth during Q1 of FY26. This wasn't just growth—it was proof that traditional retailers could successfully pivot to digital.

The Candere playbook revealed a deeper truth about Indian e-commerce: online isn't about replacing offline; it's about creating new consumption occasions. A 25-year-old software engineer might not walk into a Kalyan showroom to buy a ₹15,000 ring for his girlfriend, but he'd happily order it online from Candere. That same customer, when buying wedding jewelry worth lakhs, would want the full Kalyan showroom experience.

The lifestyle positioning was crucial. Candere wasn't competing with Kalyan; it was competing with fashion accessories, with gifting alternatives, with impulse purchases. The average order value was a fraction of Kalyan's, but the frequency was higher. It was jewelry as fashion, not jewelry as investment.

The company is planning to open 170 showrooms in 2025-26, of which 90 will be Kalyan and 80 stores under its lifestyle jewellery brand Candere. Think about that ratio—almost equal expansion between the traditional brand and the digital-first brand. This wasn't a side project anymore; it was a parallel growth engine.

VIII. Financial Deep Dive & Business Model

The numbers tell a story of transformation. Revenue: 26,794 Cr, Profit: 801 Cr for FY24. But raw numbers without context are just digits. The real story is in the trajectory and the underlying business model evolution.

KALYAN JEWELLERS' revenue has grown from Rs 101,810 million in FY20 to Rs 186,314 million in FY24. Over the past 5 years, the revenue of KALYAN JEWELLERS has grown at a CAGR of 16.3%. During a period when COVID decimated retail, when gold prices went haywire, when consumer sentiment oscillated wildly, Kalyan grew revenue at 16.3% CAGR. That's not luck—that's operational excellence.

The profitability evolution is even more impressive. The net profit of KALYAN JEWELLERS stood at Rs 5,963 million in FY24, which was up 38.1% compared to Rs 4,319 million reported in FY23. The margin expansion story isn't about pricing power—jewelry is a commodity business with transparent pricing. It's about operational leverage, inventory turns, and mix improvement.

The working capital story deserves its own case study. Jewelry retail is fundamentally a working capital business. You're financing gold inventory, customer credit (through purchase advance schemes), and store build-outs. Traditional jewelers either stayed small or leveraged themselves to bankruptcy. Kalyan found a third way.

The vendor financing model was elegant. Suppliers provided gold on credit, typically 60-90 day terms. Kalyan turned inventory in 45-60 days. This negative working capital cycle meant growth actually generated cash rather than consuming it. It's the same model that made Dell famous, applied to Indian jewelry retail.

But the real financial innovation was the franchise pivot. Jewellery retailer Kalyan Jewellers plans to open 170 stores through a franchise model in domestic and overseas markets this fiscal, which will help reduce its debt liabilities. This wasn't just about capital efficiency—it was about risk distribution.

In the franchise model, the franchisee bears the inventory risk, the real estate risk, the local market risk. Kalyan provides the brand, the systems, the procurement leverage. It's asset-light growth—the holy grail of retail. The company essentially becomes a jewelry brand licensor and supply chain manager rather than a traditional retailer.

The unit economics are compelling. A typical Kalyan store requires ₹15-20 crores in inventory, ₹3-5 crores in fit-out costs, and generates ₹50-70 crores in annual revenue. At 7-8% EBITDA margins, that's ₹3.5-5.6 crores in annual EBITDA. For a franchisee, that's a 15-20% ROI. For Kalyan, it's pure margin with zero capital employed.

The gold price volatility management is sophisticated. Kalyan doesn't speculate on gold prices—it hedges. When a customer places an advance order, Kalyan immediately hedges the gold price exposure. The company makes money on making charges and retail margins, not on gold price movements. This discipline is why Kalyan's margins are stable despite gold volatility.

The revenue mix evolution shows strategic focus. India operations contribute 85%, Middle East 12-15%, and Candere is rapidly growing. Within India, non-South markets are growing faster than South markets, proving the pan-India strategy is working. Studded jewelry (diamonds) is growing faster than plain gold, improving margins.

Stock is trading at 11.5 times its book value, which might seem expensive for a traditional retailer. But Kalyan isn't a traditional retailer anymore—it's a brand-driven, asset-light, omnichannel platform. The valuation reflects future cash flows, not historical book value.

IX. Growth Strategy & Future Expansion Plans

The numbers are audacious: Kalyan Jewellers plans to open 170 new showrooms via a franchise model, aiming to reduce debt liabilities... It is set to establish 90 Kalyan stores and 80 Candere lifestyle jewellery outlets in the 2025-26 fiscal. That's nearly a 50% increase in store count in a single year. In retail, this kind of expansion typically precedes either spectacular success or spectacular failure.

But Kalyan's expansion isn't reckless—it's methodical. The focus on franchise model means the capital risk is distributed. The 90:80 split between Kalyan and Candere shows portfolio thinking—betting on both traditional and modern formats. The geographic targeting reveals strategic precision.

The non-South expansion is particularly interesting. South India, despite being just 20% of India's population, accounts for nearly 40% of gold consumption. It's also Kalyan's stronghold. Moving North and West means entering markets with different consumption patterns, different competition, different cultural nuances. It's not just geographic expansion—it's cultural translation.

The tier 2/3/4 city focus is counter-intuitive but brilliant. While everyone chases metro consumers, Kalyan is going where the growth is. These smaller cities have lower real estate costs, less organized competition, and increasingly affluent consumers. A family in Hubli or Salem might have the same jewelry budget as one in Bangalore, but with fewer options to spend it.

The international strategy is evolving from diaspora-focus to mainstream ambition. Kalyan Jewellers will enter the UK this fiscal. Our overseas expansion will be focused on the US, UK and the Middle East till next fiscal. We are getting inquiries from countries like Australia, Malaysia, and Singapore, having a large Indian diaspora; however, our overseas expansion will be very calibrated.

The UK entry is strategic. London is not just home to a large Indian diaspora but also a global luxury hub. Success in London provides credibility for expansion into other Western markets. It's the same playbook Chinese brands like Huawei and Xiaomi used—prove yourself in demanding developed markets to build global credibility.

The manufacturing strategy is evolving too. The company has contract manufacturers, and as of now, it is focused on front-end retailing. We are working on improving the back-end and developing the roadmap for strengthening the back-end that will include setting up a contract manufacturing hub in Thrissur before the end of this financial year.

This isn't backward integration for the sake of it. It's about quality control, design differentiation, and margin improvement. The contract manufacturing hub model—where multiple manufacturers operate from a single location—provides scale benefits without capital intensity.

The digital integration continues to evolve. It's not just about Candere anymore—it's about making every Kalyan store digitally enabled. Virtual try-ons, online booking with store pickup, digital catalogs—the physical and digital are merging into what Kalyan calls "phygital."

The capital allocation framework is disciplined. Every new store must meet hurdle rates. Every market entry must have a path to profitability. Every acquisition must be accretive. This isn't the venture capital model of growth at any cost—it's the old-school retail model of profitable growth.

The competitive response strategy is nuanced. Against Titan, Kalyan emphasizes local customization and family legacy. Against regional players, it leverages scale and systems. Against unorganized players, it offers transparency and trust. It's not trying to beat everyone at everything—it's choosing battles carefully.

The risk management is sophisticated. Geographic diversification reduces regional risk. Format diversification (Kalyan vs. Candere) reduces segment risk. Franchise model reduces capital risk. International expansion reduces country risk. It's a portfolio approach to retail expansion.

X. Competitive Landscape & Market Position

The company is among India's top 5 gold jewellery retailers, accounting for about 6% of the total organised market share. In any other industry, 6% market share would be a rounding error. In Indian jewelry retail, it makes you a giant.

The competitive landscape in Indian jewelry is unlike any other retail category. At the top sits Titan (Tanishq), the Tata Group company that pioneered organized jewelry retail in India. With over 400 stores and a ₹40,000 crore market cap, Tanishq is the undisputed leader. But leadership in Indian retail is always provisional.

The real competition isn't other organized players—it's the unorganized sector that still controls 65% of the market. These are the family jewelers, some operating for centuries, with deep community relationships and flexible business practices. They don't file taxes properly, they don't follow labor laws, they negotiate prices, they offer unofficial credit. How do you compete with that?

Kalyan's answer: you don't compete, you co-opt. The franchise model isn't just about capital efficiency—it's about converting competitors into partners. That successful family jeweler in Coimbatore? Instead of competing with him, make him a Kalyan franchisee. He brings local relationships; Kalyan brings brand and systems.

The regional players present a different challenge. Joyalukkas in Kerala, Lalitha in Tamil Nadu, Senco in Bengal—each has deep regional roots and loyal customers. They speak the local language, literally and figuratively. Kalyan's response: be more local than the locals. Our biggest differentiator is not only the ability to understand local, think local and act local, but at the same time bring in our vast experience and sourcing strength out of operating in multiple markets. Jewellery is a complicated product, because tastes vary even within the same state.

The hyperlocal strategy goes beyond inventory. Store managers are local, marketing campaigns feature local celebrities, designs incorporate regional motifs. A Kalyan store in Amritsar feels Punjabi; one in Kolkata feels Bengali. It's McDonald's in reverse—instead of standardizing globally, Kalyan customizes hyperlocally.

The brand ambassador strategy reveals competitive positioning. While Tanishq goes for Bollywood A-listers with national appeal, Kalyan signs regional stars—Telugu actors for Andhra, Tamil stars for Tamil Nadu. It's more expensive to manage multiple ambassadors, but it creates deeper regional connect.

The marketing philosophy is distinctly different from competitors. Massive marketing campaigns and launches, path-breaking ads which were never-before seen in jewellery advertising, multi-storey large format jewellery showrooms, same-day multi-launch ceremonies and events. While Tanishq whispers elegance, Kalyan shouts celebration.

The pricing strategy is surgical. Kalyan isn't the cheapest—that's the unorganized sector. It isn't the most premium—that's Tanishq. It sits in the sweet spot: 5-10% premium over unorganized for the trust factor, 5-10% discount to Tanishq for the value proposition. It's the Goldilocks pricing—just right.

The product strategy emphasizes breadth over depth. While boutique jewelers specialize in specific categories, Kalyan offers everything. Wedding jewelry, daily wear, investment pieces, fashion jewelry through Candere—it's the department store model applied to jewelry.

The trust-building mechanisms are systematic. BIS hallmarking, buyback guarantees, transparent pricing, lifetime maintenance—each element reduces purchase anxiety. In a category where trust is everything, Kalyan institutionalizes trust.

The digital competition is evolving. New players like BlueStone and CaratLane (now owned by Titan) are digital-first. Kalyan's response through Candere shows it can play the digital game while leveraging physical store advantages.

XI. Investment Thesis & Risk Analysis

The bull case for Kalyan Jewellers writes itself. India's jewelry market is expected to grow from $80 billion to $150 billion by 2030. The shift from unorganized to organized will accelerate, driven by GST compliance, consumer awareness, and generational change. Kalyan, as the second-largest organized player with just 6% market share, has massive headroom for growth.

The franchise model transformation is a game-changer. It converts Kalyan from a capital-intensive retailer to an asset-light brand owner. Think of it as the Domino's model applied to jewelry—franchise fees, supply chain margins, zero inventory risk. The return on invested capital (ROIC) improves dramatically.

The international expansion provides optionality. If India grows at 15% and international at 20%, the blended growth rate supports premium valuations. The Middle East is proven profitable; the US and UK are options on global brand building.

Market share grows every year in the range of over 1 per cent for Kalyan. The company's current market share in the organised segment is around 8-9 per cent. At this rate, Kalyan could double its market share in 8-10 years, implying a 3-4x revenue opportunity just from share gains.

The Candere acquisition is bearing fruit with 67-89% growth rates. If Candere becomes a ₹1,000 crore brand (currently ~₹150 crores), it adds significant value at minimal capital cost.

But the bear case has teeth too. Gold price volatility can destroy working capital management. A sudden spike in gold prices could freeze consumer demand, strand inventory, and crush margins. Kalyan hedges, but hedging isn't perfect.

Execution risk is real. Opening 170 stores in a year requires flawless execution. Finding franchisees, training staff, managing inventory, maintaining quality—any slip could damage the brand. Rapid expansion has killed many retailers.

Competition is intensifying. Titan isn't sitting still—CaratLane is growing aggressively, Tanishq is expanding internationally. Regional players are consolidating. New digital players are entering. The comfortable duopoly might not last.

Regulatory risk lurks. Jewelry retail attracts regulatory attention—money laundering concerns, cash transaction limits, import duties. One adverse regulation could disrupt the business model.

Regional concentration remains high. Despite pan-India presence, South India still contributes over 50% of revenues. Any regional disruption—political instability, natural disasters, economic slowdown—disproportionately impacts Kalyan.

The valuation demands perfection. Stock is trading at 11.5 times its book value. At these multiples, any disappointment in growth or margins could trigger a sharp correction.

The franchise model, while capital-efficient, reduces control. A few bad franchisees could damage brand reputation. Managing franchise relationships at scale is complex.

Currency risk in international operations is meaningful. Middle East currencies are dollar-pegged, but any depeg could impact profitability. The UK and US operations add developed market currency exposure.

The investment thesis ultimately rests on a simple question: Can Kalyan execute its ambitious expansion while maintaining brand integrity and financial discipline? The track record suggests yes, but past performance, as they say, doesn't guarantee future results.

For long-term investors, Kalyan represents a play on Indian consumption, retail consolidation, and brand building. It's not without risks, but in Indian retail, what is?

XII. Lessons & Takeaways

The Kalyan Jewellers story offers masterclasses in multiple dimensions of business building. But perhaps the most important lesson is about time horizons. In an era of quarterly capitalism, Kalyan spent seven years perfecting one store. That's not patience—that's strategic conviction.

The power of patient capital manifests throughout Kalyan's journey. The family operated in textiles for decades before entering jewelry. They spent years understanding local preferences before expanding nationally. They built trust customer by customer before leveraging it into a brand. In venture capital terms, this is the ultimate "long-term greedy" approach.

The hyperlocalization playbook challenges conventional retail wisdom. While global retailers pursue standardization for efficiency, Kalyan proves that customization can scale. Every part of India has its unique jewellery, the expertise to create those exist only in that region, passed on through generations. Kalyan's biggest strength is in these craftsmen who create unique designs just for us from every nook and corner of India. The lesson: in diverse markets, one size doesn't just not fit all—it fits none.

Family business succession is where most Indian companies fail. The founder builds an empire; the children destroy it fighting over inheritance. Kalyan shows another way. T.S. Kalyanaraman brought in his sons Rajesh and Ramesh not as inheritors but as partners. Each had defined roles, complementary skills, and mutual respect. The lesson: succession is not about inheritance but about institution building.

Building trust in high-value transactions requires more than marketing—it requires systematic trust architecture. Every element of Kalyan's model—transparent pricing, hallmarking, buyback guarantees, lifetime service—reduces transaction anxiety. In categories where trust is the product, you can't just claim trustworthiness; you must engineer it.

The importance of cultural understanding in international expansion cannot be overstated. Kalyan didn't just export Indian jewelry to the Middle East; it understood that Gulf Indians wanted to display success differently than homeland Indians. The designs were bigger, the stores grander, the experience more luxurious. Global expansion isn't about replication but translation.

The franchise pivot demonstrates strategic flexibility. When capital became a constraint, instead of slowing growth or diluting equity, Kalyan changed the model. The lesson: your business model is not your strategy—it's a tool to execute strategy. When the tool doesn't work, change the tool, not the strategy.

The Candere acquisition shows how traditional companies can embrace disruption. Instead of fighting e-commerce, Kalyan bought an option on the future. Instead of forcing integration, they let Candere evolve independently. The lesson: sometimes the best way to manage disruption is to own it but not control it.

The IPO journey illustrates how family businesses can access capital markets without losing soul. The Vinod Rai appointment, the Warburg partnership, the governance improvements—each step built institutional credibility while maintaining entrepreneurial spirit. The lesson: going public isn't about exit but about evolution.

The competitive strategy proves that in fragmented markets, you don't need to dominate—you need to consolidate. Kalyan isn't trying to crush competition but to organize it. The franchise model converts competitors into partners. The lesson: in Indian retail, cooperation scales better than competition.

The financial discipline throughout shows that growth and profitability aren't trade-offs but complements. Kalyan grew at 16% CAGR while improving margins. The lesson: sustainable growth comes from operational excellence, not financial engineering.

For investors, Kalyan demonstrates that boring can be beautiful. Jewelry retail isn't sexy like tech or innovative like pharma. But it's steady, scalable, and sustainable. In a world chasing the next big thing, sometimes the best investment is in the oldest thing done in a new way.

The meta-lesson might be the most important: Indian business isn't about copying Western models but creating indigenous ones. Kalyan didn't try to be Tiffany or Cartier. It created a distinctly Indian model for a distinctly Indian market. In a globalizing world, the most successful companies might be the most local ones.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube