Jyothy Labs: The Blue Revolution & The David vs. Goliath Pivot

I. Introduction & The "Four Drops" Hook

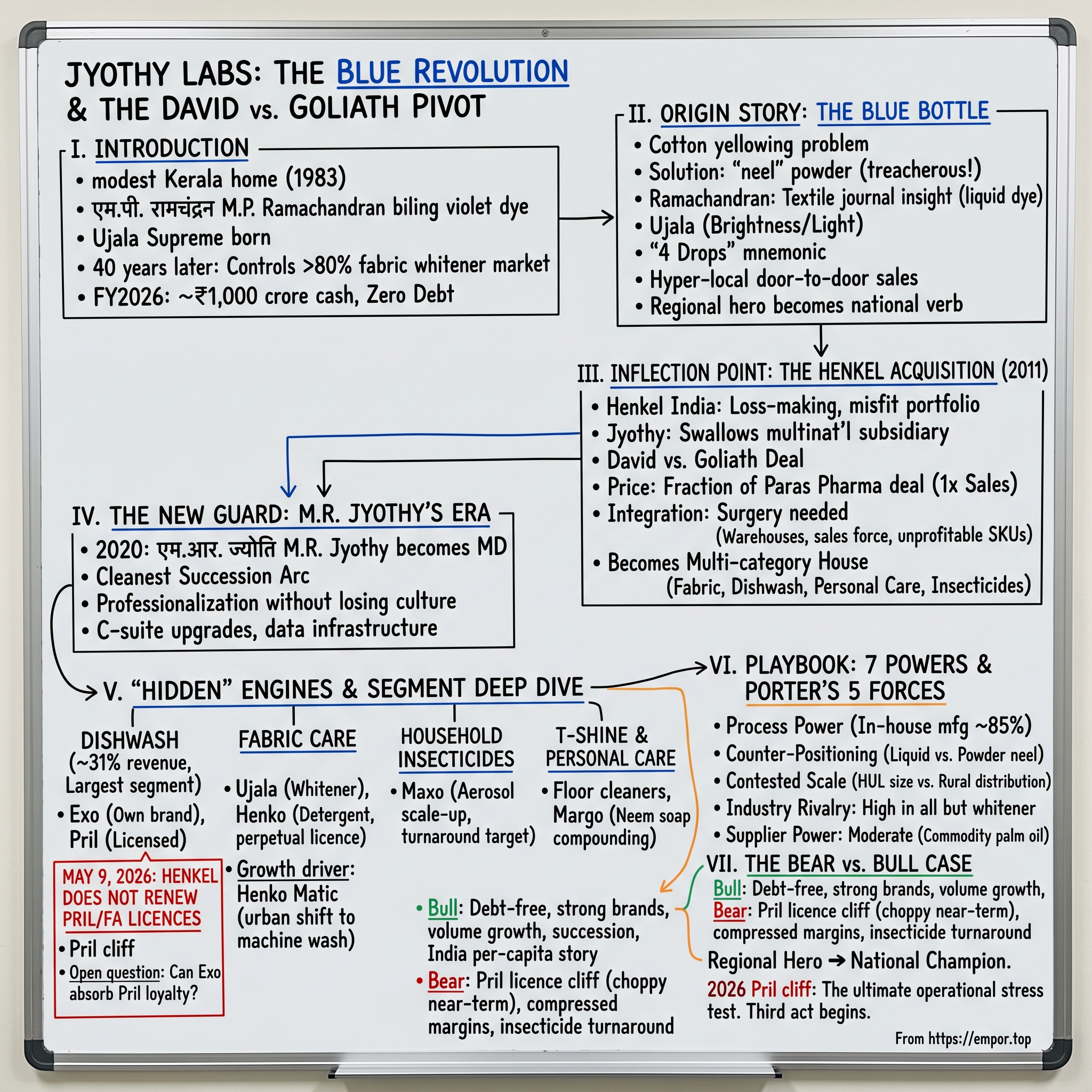

Picture a kitchen in a modest Kerala home in 1983. The monsoon is heavy outside, the kind of slanting rain that turns red laterite into rust. Inside, a man in his early thirties, a chartered accountant by training, is bent over a stove. He is not cooking. He is boiling a violet dye in a stainless steel pot, stirring it with the methodical patience of someone reconciling a balance sheet. He has been at this for almost a year. His wife thinks he has lost his mind. His brother has just lent him ₹5,000, roughly sixty US dollars at the time, to set up a "factory" on a sliver of family land in Thrissur.1

The man is एम.पी. रामचंद्रन Moothedath Panjan Ramachandran. The pot contains the first batch of what would later be called Ujala Supreme — a liquid fabric whitener. And the company he is about to name after his eldest daughter, Jyothy, will, four decades on, control over 80% of India's organised fabric whitener market and command a balance sheet that, as of FY2026, sits on roughly ₹1,000 crore of cash with zero debt.2

This is the story of Jyothy Labs Limited — listed on the NSE as JYOTHYLAB, on the BSE as 532926 — an Indian consumer goods company that started life as a kitchen experiment, scaled into a regional cult brand, then, in 2011, did the unthinkable: a South Indian "single-product" company swallowed the Indian subsidiary of one of Germany's largest multinationals. Henkel India, owner of Pril, Henko, Margo and Fa, came under the Jyothy umbrella. The "David vs. Goliath" framing was almost too cinematic — but the numbers backed it up.

The arc gets more interesting from there. Founder transitions in Indian family-run FMCG are notoriously bumpy — for every successful handover, there are three sagas of cousins suing each other in the Bombay High Court. Yet in April 2020, Ramachandran handed the Managing Director's chair to his daughter एम.आर. ज्योति M.R. Jyothy, slipped quietly into the role of Chairman Emeritus, and walked off-stage with the kind of grace usually reserved for retiring cricketers.3 By 2026, M.R. Jyothy had assumed the Chairperson role as well, completing one of the cleanest succession arcs in the Indian केंद्रीय बजट Union Budget-watching FMCG cosmos.4

And then, on May 9, 2026 — twelve days before this article was written — the company filed a regulatory disclosure that wiped 11% off its market cap in a single session. Henkel had decided not to renew the Pril and Fa brand licences beyond May 31, 2026, ending a fifteen-year arrangement that had given Jyothy access to two of its most recognisable dishwash and personal care names.56

So the company finds itself, on the cusp of a license cliff, with three things working in its favour and one open question. The favours: a debt-free balance sheet, an in-house manufacturing footprint of 23 plants, and a founder-led culture that has been professionalised without being neutered. The open question: can the Exo brand, which Jyothy fully owns, absorb the loyalty that two generations of Indian households built up around Pril?

This is the Acquired-style deep dive. From a stainless steel pot in Thrissur to a multi-category house with ₹2,944 crore in FY26 revenue, the story of Jyothy Labs is a study in how regional heroes become national champions — and what happens when the licence that built half your moat suddenly walks away.7 Let's start where every good Indian consumer story starts: with a problem, a household, and a man who refused to accept the status quo.

II. The Origin Story: M.P. Ramachandran & The Blue Bottle

Ramachandran was, by the standards of 1980s Kerala, an extremely odd kind of entrepreneur. He was a B.Com from St. Thomas College in Thrissur, had worked as a chartered accountant, and could have settled into the comfortable career path of a Malayali finance professional in the Gulf.1 Instead, he became obsessed with a domestic problem so unglamorous that no MBA case study had ever bothered to consider it: the white shirt.

In every Indian household of that era, a white shirt was a battlefield. Cotton turned yellow with age, sweat, hard water, and the iron in groundwater pipes. The standard solution was "neel" — a synthetic indigo powder you dissolved in water and dunked the final rinse into. It was cheap, sold in grocery shops in small paper sachets, and absolutely treacherous. Too much, and your शर्ट shirt came out patchy blue. Too little, and there was no whitening effect. Dissolve it incorrectly, and you would get streaks. Every Indian mother in the early 1980s had, at some point, ruined an entire load of school uniforms with neel.

Ramachandran, in his words, was tired of doing his own laundry badly. He came across a textile industry journal — a niche publication he had no professional reason to read — that described how purple-spectrum dyes were used by mills to achieve the brightest whites in cotton fabric.8 The insight was technical but the implication was domestic: if a textile mill could solve the patchy-blue problem at the manufacturing stage with a liquid dye, why couldn't a household do the same with a liquid whitener instead of a powder?

For nearly a year, his kitchen became a laboratory. He boiled, diluted, mixed, tested on his own clothes. He has talked, in subsequent interviews, about the particular ratio that mattered — too concentrated and the dye stained, too dilute and it disappeared into the rinse water.8 When he finally settled on the formula, the result was, to his mind, miraculous: four small drops in a bucket of water, swirled with the hand, and the rinse turned the colour of a Mumbai monsoon sky. Cotton came out brilliantly white.

He named the product Ujala — Hindi for "brightness" or "light" — and the company Jyothy, after his daughter. The early distribution was almost theatrical. Six women, hired from villages around Thrissur, walked door-to-door with sample bottles. They were not selling — they were demonstrating. The "4 drops" mnemonic was a marketing genius hiding inside a logistical necessity: when your sales force is six women on foot and your customers have never seen a liquid whitener before, you need a usage instruction so simple it cannot be misunderstood. "चार बूँदें Char boondein" — four drops — became a domestic incantation across South India.1

What's worth pausing on here is the un-FMCG-ness of the early strategy. Hindustan Lever, the company that would later become हिंदुस्तान यूनिलीवर HUL Hindustan Unilever, was at the same time pouring tens of crores into national television advertising for Surf and Rin. Jyothy Labs didn't have a tenth of one percent of that budget. So Ramachandran did the opposite of what an MBA would have prescribed: instead of mass media, he went hyper-local. Instead of dealer networks, he went door-to-door. Instead of trying to convert every consumer at once, he focused on Kerala first, then Tamil Nadu, then Karnataka. By the time the marketing departments at HUL noticed, Ujala already owned the South.1

By the late 1990s, the product had crossed the Vindhyas. By 1997, Ujala was a household verb in much of urban India — you didn't whiten clothes, you "Ujala-ed" them.1 Market psychology helped enormously. In an Indian context, "whiteness" is not just about clean cotton. It is a proxy for स्वच्छता swachhata — cleanliness, dignity, and social legibility. A white shirt at a job interview, a white veshti at a temple, a white school uniform — these are not aesthetic choices, they are signals. Ramachandran was not selling a chemical, he was selling a small piece of social capital, four drops at a time.

By the mid-2000s, Jyothy Labs had quietly expanded into mosquito coils (Maxo), detergent powders (Ujala Stiff & Shine), and a handful of soap-adjacent products. The company went public in 2007, but it was still, fundamentally, "the Ujala people." A one-product wonder, regional in feel, with a founder who answered his own phone. That would change abruptly in 2011, when an opportunity none of them had even considered came walking through the door wearing a German nameplate.

III. The Inflection Point: The Henkel India Acquisition

In early 2011, Henkel AG — the Düsseldorf-based maker of Persil detergent, Loctite adhesive and Schwarzkopf hair care, with annual revenues then north of €15 billion — was in an awkward place in India. Its Indian subsidiary, Henkel India Limited, had been losing money for years. It owned a portfolio that looked, from a German boardroom, like a misfit collection: Pril dishwash liquid, Henko detergent, Margo neem soap (acquired from Calcutta Chemicals), Fa deodorant, and Mr. White. National distribution but bleeding margins. Henkel wanted out.

The official version is that several Indian FMCG players ran the numbers. Reckitt Benckiser, Wipro Consumer, Marico, Dabur — the usual suspects in any large Indian consumer M&A — were rumoured to have looked. None bit. Henkel India was a fixer-upper, and at the price the German parent wanted, the math didn't pencil for the bigger players, who would have to integrate a national distribution mess into their own already-functioning national systems.

For Ramachandran, the calculus was completely different. Jyothy was South-and-East strong but underweight in the North and West. Henkel India had exactly the opposite footprint. Henkel's brand portfolio overlapped with Jyothy's in places (dishwash) but extended into adjacencies Jyothy didn't yet play in (deodorants, neem soap, detergent for top-loading machines). The German parent's losses were, in Ramachandran's view, mostly a structural problem of too much overhead servicing too little volume — the kind of thing a hungrier owner could fix by ripping out the corporate skeleton and grafting the brands onto Jyothy's already-efficient distribution.

The deal mechanics were elegant. On May 31, 2011, Jyothy Laboratories acquired 5.94 crore shares of Henkel India, representing a 50.97% stake, at ₹20 per share — an aggregate cheque of roughly ₹118.7 crore.9 Combined with a 14.9% slug Jyothy had earlier picked up from the Indian co-promoter Tamilnadu Petroproducts for about ₹60 crore, Jyothy ended up with 65.86% of Henkel India.9 The mandatory open offer that followed — under SEBI's takeover regulations — was for another 20% at ₹41.20 per share, an outlay of roughly ₹96 crore.10 Total deal value, including debt assumption and the open offer, came in at approximately ₹774 crore.9

Was that expensive? Here is where the benchmarking gets interesting. Henkel India was loss-making, so P/E was meaningless and EV/EBITDA wasn't far behind. The cleanest metric was EV/Sales, and at roughly 1x trailing sales, Jyothy was buying brands at a fraction of what the listed Indian FMCG comp set traded at. To put it in contemporary context, Reckitt Benckiser had acquired Paras Pharmaceuticals — owner of Moov and D'Cold — just months earlier for roughly ₹3,260 crore, valuing Paras at something close to 8x sales.11 On a relative basis, Jyothy was paying for Henkel India's brands at a discount of roughly 85% to where Reckitt was paying for Paras's. The difference, of course, was that Paras was growing and profitable, while Henkel India was neither. But Ramachandran's bet was that brands of this calibre — Henko, Pril, Margo, Fa — wouldn't trade at distress multiples for long once the parent stopped subsidising structural inefficiency.

The integration was harder than the headline price suggested. The "hidden cost" of the acquisition was the absorption of Henkel India's debt (roughly ₹250 crore), a sclerotic distribution network that had been optimised for the wrong SKUs in the wrong cities, and a workforce that had grown comfortable inside a German subsidiary's cost discipline. Jyothy spent the better part of 2012 to 2015 doing surgery: consolidating warehouses, retraining the sales force, redesigning packaging, killing unprofitable SKUs. Margo, the neem soap with a cult Bengali following, got a relaunch. Henko got repositioned for top-loading washing machines. Pril, the most valuable single brand in the basket, was kept largely intact — at the time, nobody at Jyothy was thinking about what would happen if Henkel one day decided not to renew the licence.

The strategic significance, in hindsight, was less about the brands themselves and more about what the deal did to Jyothy's category mix. Pre-Henkel, Jyothy was effectively a fabric whitener company with a side bet in mosquito coils. Post-Henkel, it was a multi-category house: fabric care, dishwash, personal care, household insecticides. That mix is what allowed the company, in subsequent years, to weather the volatility in any single category — and, crucially, to position itself as a "small HUL" in the minds of institutional investors. The re-rating that followed wasn't accidental. By the late 2010s, Jyothy was trading on FMCG multiples, not single-product multiples. The Henkel deal had bought Jyothy the right to be valued like a portfolio.

That re-rating set up the next chapter — but it also planted a seed of vulnerability that wouldn't sprout for fifteen years. We'll come back to that. First, succession.

IV. The New Guard: M.R. Jyothy's Professionalization Era

In early 2019, Ramachandran began signalling, gently, that he was going to step back. He was already in his mid-sixties. He had spent thirty-six years building the company. And he had a daughter who had been embedded in the business for over a decade, learning the trade from the inside.3 The succession announcement, when it came in May 2019, was almost anticlimactic — and that was the point.

M.R. Jyothy is not, by Indian family-business standards, a parachuted-in heiress. She joined Jyothy Labs in the mid-2000s and worked her way through marketing roles, eventually becoming Chief Marketing Officer and a Whole-Time Director. She was the executive most directly responsible for integrating the Henkel brands — Pril, Henko, Margo — into the Jyothy distribution and marketing apparatus after 2011.3 By the time her father formally handed her the Managing Director title on April 1, 2020, she had already been running the front office of the business for years.

The succession structure deserves a closer look because it tells you something about how the family thinks about governance. Three pieces are worth flagging.

First, the split of Chairman and MD roles. For most of its public life, Jyothy Labs had a combined Chairman-and-Managing Director — Ramachandran himself. On April 1, 2020, the roles were split: M.R. Jyothy became MD, and Ramachandran moved to Chairman Emeritus.3 The split is a small but meaningful corporate-governance signal. Combined Chair/CEO roles concentrate authority and reduce board independence; splitting them tells institutional investors that the company is willing to put structural checks on executive power. For an Indian promoter family doing succession, the split is also a way to keep the founder in the room without making him the deciding vote.

Second, the compensation structure. M.R. Jyothy's executive pay package is almost entirely fixed — the variable and stock-linked components are minimal compared to peer FMCG MDs at HUL, Godrej or Dabur. The signal is unusual: in an industry where CEOs typically have large performance-linked option pools, Jyothy's structure essentially says "the family's wealth comes from owning the company, not from the option grants." When 62.89% of the company is held by the promoter group as of late 2025, the incentive to maximise long-term value is already maxed out — adding short-term option grants would just add quarterly volatility to decision-making.12

Third, the family trust architecture. The promoter group holding of roughly 63% is not held by any single family member. M G Shanthakumari — Ramachandran's wife — holds the largest individual slice at around 39%, while M.R. Jyothy holds a smaller direct stake of approximately 2.8%, with the balance distributed across other family members and family trust vehicles.12 This structure does two things: it makes it nearly impossible for any single individual to act unilaterally on the equity, and it keeps the family's long-term alignment with minority shareholders structurally intact.

In terms of what M.R. Jyothy actually changed once she took the chair, the answer is less "revolution" and more "professionalisation." The C-suite was upgraded — CFOs and senior marketing hires were brought in from larger FMCG players. Data infrastructure for sales-force productivity, distributor management and consumer analytics was rebuilt. The "founder-led emotional" culture that had taken the company from kitchen to ₹2,000 crore in revenue was preserved, but layered with the kind of operating discipline that lets you run twenty-three plants and seven brand families without dropping balls.

In April 2024, the succession completed another stage: M.R. Jyothy assumed the Chairperson role as well, with the MD function transitioning to a separately appointed senior executive.4 The family had pulled off the rarest of Indian succession outcomes — a multi-generational handover with no court cases, no public family feud, no abrupt cultural break, and no spike in attrition at the senior management level. The continuity was so smooth that most investors only noticed it in hindsight when the next quarterly result came out.

Which brings us to the operating engine itself — because while the headline narrative was Ujala and the Henkel takeover, the actual financial result of Jyothy Labs in 2026 has very little to do with either.

V. The "Hidden" Engines & Segment Deep Dive

If you walked into a Jyothy Labs investor meeting in 2020 and asked "where does your money come from?" the answer would have been a slightly defensive lecture about how Ujala had stopped growing because the powder-to-liquid conversion had played out and the company had to lean on the other categories. Six years later, the picture is dramatically different. Three of the four operating segments — Dishwash, Fabric Care, Household Insecticides — are bigger contributors than Ujala. The "side bets" became the business.

Let's go segment by segment.

Dishwash. This is, by some distance, the most strategically important and most psychologically loaded segment in the company right now. As of Q4 FY26, dishwash contributed roughly 31% of total revenue, making it the single largest category in the portfolio.7 The lineup is Exo (Jyothy's own brand, originally a South Indian dishwash bar), Pril (Henkel-licensed, dominant in liquid), and Mr. White. For FY26, the dishwash segment generated approximately ₹959 crore in revenue, marginally below FY25's ₹972 crore, while segment profit fell from ₹183 crore to ₹151 crore — a 17.9% decline that reflects the gross margin compression across the FMCG sector through the year.13

And then, on May 9, 2026, the floor moved. Henkel formally notified Jyothy that the licence agreements for Pril and Fa would not be renewed beyond May 31, 2026.56 After fifteen years, the German parent had decided to recall two of the most recognisable brand names in the Jyothy portfolio. The market reaction on May 11 was brutal — the stock fell 11% in a single session.14

What's worth understanding is what the non-renewal does and does not do. It does not affect Mr. White or Henko — those are perpetual licences with no royalty obligations, meaning Jyothy effectively owns the economic interest in them in India regardless of what Düsseldorf decides next.7 It does end Jyothy's right to manufacture, market, and sell Pril and Fa beyond May 2026. The company's response, announced on the same day, was to accelerate the migration of Pril's liquid dishwash users to the homegrown Exo Liquid range, leaning into Exo's existing distribution and the fact that Jyothy controls the in-store shelf in many of the markets where Pril is strong.7

The bet, which is the central operational question of the next eighteen months, is whether Exo can hold the share that Pril built. Exo has the manufacturing, the formulation capability, the distribution and the trade relationships. What it doesn't have is fifteen years of mass-media equity in the liquid dishwash category. The honest answer is: nobody knows. Brand migrations of this scale have a mixed track record in India. The Pril name is owned by Henkel; once Henkel takes it back, the question is whether Henkel itself can keep the brand alive in India without Jyothy's distribution muscle — and whether Jyothy can convert Pril loyalists faster than Henkel can find a new Indian partner.

Fabric Care. This is the segment that has been quietly carrying the company for the last three years. Within it sits Ujala (the original liquid whitener, still around 80% share of the organised fabric whitener market) and Henko (the laundry detergent the company picked up from Henkel and now operates under perpetual licence). The hidden growth driver is Henko Matic — the front-load and top-load machine detergent variant — which has tripled in revenue over recent years from a small base, riding the secular shift in urban India from handwash to machine wash. In Q4 FY26, the fabric care segment posted a 17.8% value growth, the strongest of any segment for the quarter.7

The structural tailwind here is simple: liquid detergent in India is where powder was in 2005. Penetration is low (single-digit by volume), urbanisation is high, and washing-machine ownership is climbing. HUL and Procter & Gamble have been spending heavily on Surf Excel Matic and Ariel Matic, which is, perversely, good news for Henko Matic — the category gets pulled along by the giants' advertising while Henko captures share at a more affordable price point. This is the rare FMCG category in India where a mid-sized player can ride the slipstream of two multinationals.

Household Insecticides. Maxo, the mosquito coil and aerosol brand Jyothy launched in the early 2000s and aggressively expanded in the 2010s, has been one of the most volatile parts of the portfolio. For years, the segment was a drag on consolidated profitability — losses of around ₹25 crore in some years, driven by intense competition from Godrej's Goodknight and SC Johnson's All Out, both of which had deeper pockets for category advertising.

The turnaround has been gradual but real. In FY26, the Household Insecticide segment posted a 12.6% value increase in the most recent quarter, driven primarily by the scale-up of Maxo Aerosol, even as the legacy coil business declined.15 The full-year performance was mixed — the segment is still working through a category-level structural challenge, namely that mosquito coils are being slowly displaced by liquid vaporisers and aerosols in urban India, while rural penetration remains the volume base. Management has explicitly framed FY27 as the "targeted turnaround year" for this segment.15

T-Shine and Personal Care. These are the smaller bets — floor cleaners, dishwash bars, hair oil — but they matter because they're where the next leg of growth is being seeded. T-Shine, the floor cleaner brand, has been growing in the 30%+ range, helped by modern trade and direct-to-consumer channels where Jyothy historically underindexed. Margo, the neem soap acquired through the Henkel deal, has been quietly compounding inside the "naturals" sub-segment of personal care, which is the fastest-growing slice of the Indian soap market.

The point of this segment tour is that Jyothy in 2026 is not the Ujala company. It is a four-engine business where the original engine — fabric whitener — is one of the smaller engines, and the most strategically important engine (dishwash) is at the centre of a brand-migration question that will define the company's next three years.

VI. Playbook: 7 Powers & Porter's 5 Forces

If you apply Hamilton Helmer's 7 Powers framework to Jyothy Labs, three of the seven show up clearly and a fourth is contested.

Process Power. This is the strongest of Jyothy's structural advantages and the one that doesn't get nearly enough airtime in sell-side reports. Jyothy manufactures roughly 85% of its product volume in-house, across 23 plants spread across India.16 By comparison, HUL outsources a substantially higher share of its mid-tier brand production to third-party converters. Procter & Gamble India runs an even more outsourced model. Godrej Consumer Products is somewhere in between. For a company in Jyothy's revenue band — under ₹3,000 crore in FY26 sales — owning that much manufacturing is unusual and, frankly, the kind of thing financial analysts have historically penalised companies for, on the assumption that capital-light is always better than capital-heavy.7

The "process power" argument runs the other way. When you own your manufacturing, you control your gross margin, your formulation flexibility, your speed-to-market on new SKUs, and your ability to handle the volatility of raw material prices. In 2026, with palm oil, soda ash, and packaging material inflation all in motion at different cadences, the in-house plants gave Jyothy the ability to pass through price increases faster than its outsourced peers — and to absorb shocks without breaking promises to distributors. The downside, of course, is fixed-cost leverage: when volume slows, the plants underutilise, and the operating margin gets compressed. That is exactly what happened in FY26, when gross margins fell roughly 400 basis points to 45.2% and EBITDA margins compressed to 13.5%.7 But the same operating leverage works in the other direction when volume recovers.

Branding. The Ujala "4 drops" mnemonic is, in marketing terms, a cognitive asset of the highest order — a piece of consumer language that operates as a usage instruction, a brand attribute, and an emotional shorthand simultaneously. Most FMCG brands spend decades trying to manufacture exactly this kind of language and never get there. Ujala backed into it because it was originally a literal instruction for a confused consumer. Forty years on, "char boondein" is a phrase that needs no explanation in much of urban and rural India.1 In economic terms, this kind of brand asset shows up as low advertising-to-sales ratios in the legacy fabric whitener business — Jyothy doesn't need to remind consumers what Ujala is for, only that it still exists.

Counter-Positioning. This one is more historical than current. In the late 1980s and through the 1990s, Ujala's liquid-versus-powder positioning was a textbook counter-position: HUL and the other incumbents had vast investments in powdered "neel" packaging, distribution and marketing, and they could not easily switch to liquid without cannibalising their own business. Jyothy, with no powder legacy, just walked into the liquid category and owned it. The counter-positioning has largely played out — the powder market for fabric whiteners has shrunk to near-zero — but the share of voice that Jyothy built during that window is still paying dividends.

Scale Economies. This is the contested one. Against HUL, Godrej Consumer, ITC, or Dabur, Jyothy is sub-scale on advertising spend, sub-scale on R&D, and sub-scale on category-level brand investment. Where it punches above its weight is in rural distribution — particularly in South India — where its multi-decade reach into smaller towns and "बाज़ार bazaar" markets creates a local-density advantage that is genuinely hard for the multinationals to replicate. So scale economies cut both ways: at the national mass-media level, Jyothy is a midget; at the village-cluster distribution level, it is a giant.

Pulling out to Porter's 5 Forces:

Threat of new entrants — high in any individual SKU (an Indian D2C startup can launch a dishwash liquid tomorrow), low in the established mass-market categories where distribution is the moat. The recent rise of D2C cleaning brands has nibbled at the premium end but barely touched the volume base in fabric care or dishwash bars.

Bargaining power of suppliers — moderate. Palm oil, packaging plastics, and surfactants are the dominant raw material categories, and all three are commodity markets with relatively transparent pricing. The exposure to international palm oil prices is the most acute pass-through risk and was the proximate cause of FY26's margin compression.

Bargaining power of buyers — split. Modern trade (Reliance Retail, DMart, Big Bazaar-successor formats) has real pricing power and increasingly demands trade margins above what general trade requires. General trade — the kirana store network — remains the dominant volume channel and is more relationally negotiated than purely transactional. Jyothy's general-trade strength is part of why its margin compression in FY26 was smaller than it would have been for a company with higher modern-trade exposure.

Threat of substitutes — low in fabric whitener (no economically viable substitute), moderate in dishwash (bar versus liquid versus paste), high in household insecticides (coils, liquids, aerosols, repellent creams, electric vaporisers, and increasingly mosquito nets are all in active competition for the same household budget).

Industry rivalry — high in every category except fabric whitener. HUL, Procter & Gamble India, Godrej Consumer, ITC, Reckitt Benckiser, Marico, and Dabur are all present in at least one of Jyothy's main segments. The intensity is most acute in dishwash liquid (Vim from HUL, Pril from Henkel) and in household insecticides (Goodknight from Godrej, All Out from SC Johnson).

The takeaway from the framework exercise is that Jyothy's competitive position is strong but uneven: very strong in fabric care and rural distribution, structurally good in in-house manufacturing, contested in dishwash, and structurally challenged in household insecticides. The Pril licence loss is, in framework terms, an erosion of one specific brand asset within an otherwise intact moat — painful, but not structural.

VII. The Bear vs. Bull Case & Conclusion

There is a version of Jyothy Labs you can tell entirely in bullish terms. A four-decade-old FMCG company, debt-free, with roughly ₹1,000 crore of cash on the balance sheet, run by the founder's daughter through one of the cleanest Indian succession transitions on record, sitting on a portfolio of brands that the largest FMCG companies in India would happily pay 5–6x sales for in a private market transaction.24 Volume growth in the core categories has been outpacing the broader FMCG industry for several quarters, and the company has demonstrated repeatedly that it can take legacy brand assets — Henko, Margo, Maxo — and re-platform them under its own distribution muscle.7 If you believe in India's per-capita consumption story — and most foreign institutional investors who own Indian FMCG stocks do — Jyothy is a mid-cap proxy that hasn't yet been bid up to large-cap multiples.

And there is the bearish version. Two thirds of the company's value sits in two segments — dishwash and fabric care — and one of those two is in the middle of a brand-licence cliff that will see two of the most recognisable names in the portfolio leave the building on May 31, 2026.56 The Pril migration to Exo is operationally credible but commercially unproven. Margins are compressed, the household insecticides segment is still working through its turnaround, and the FY26 profit print declined roughly 12% even though revenue grew.14 If raw material inflation persists into FY27 or if Henkel finds a strong Indian partner for Pril, the next few quarters could be choppier than the bull case admits.

The two views aren't actually in conflict — they are time-scoped versions of the same underlying business. The bullish case is a three-to-five-year frame in which the Exo migration succeeds, the household insecticides segment turns, and the cash on the balance sheet either gets returned to shareholders or gets deployed into a meaningful M&A move. The bearish case is a one-to-eighteen-month frame in which the Pril exit creates a revenue and margin air pocket that takes time to close.

Myth vs reality. A few consensus narratives are worth fact-checking. Myth: Jyothy is still primarily a fabric whitener company. Reality: as of FY26, Ujala-led fabric whitener is a minority of revenue; dishwash is the largest segment at ~31%, and fabric care (which includes Ujala plus the much larger Henko detergent franchise) is the growth engine.7 Myth: The Henkel relationship has been a liability for years. Reality: for fifteen years it was a substantial asset, contributing both volume and brand depth; the relationship only became a liability at the moment of non-renewal, and even now, two of the four Henkel brands (Henko, Mr. White) remain under perpetual licence with no royalty.7 Myth: The succession from M.P. Ramachandran to M.R. Jyothy was a soft, ceremonial transition. Reality: M.R. Jyothy had been operationally embedded in the company for over a decade before the title change, and the post-transition period has seen meaningful upgrades to the C-suite, data infrastructure and governance architecture.3

KPIs to track. Three things matter most for monitoring this company's trajectory going forward. First, the dishwash segment volume share — specifically, how much of the Pril liquid franchise migrates to Exo through FY27. Second, the fabric care segment growth rate — Henko Matic in particular is the cleanest read on whether the secular liquid-detergent shift is being captured. Third, the consolidated EBITDA margin — given the in-house manufacturing model, operating leverage works both ways, and the margin trajectory is the cleanest single indicator of whether volume is recovering against the cost base. Beyond these three, the cash deployment question — what does the company do with ₹1,000 crore? — will become a major narrative driver if it turns into an acquisition rather than a buyback or special dividend.

Light overlays worth flagging. The Pril non-renewal has, by definition, a regulatory disclosure dimension — the matter was disclosed under SEBI's Regulation 30 of the LODR Regulations following the May 9, 2026 board meeting, and the company has signalled near-term revenue and margin impact while characterising the medium and long-term fundamentals as intact.5 Auditor and accounting signals through FY26 have been clean. On the ESG side, in-house manufacturing of 85%+ of volume is a double-edged disclosure — high control over labour, environmental and effluent management, but also concentrated capex obligations across 23 plants. Promoter pledges as of late 2025 were not material. There has been no notable 13F-type shift in concentrated institutional ownership — domestic mutual funds remain the dominant non-promoter holders, and FII ownership has been range-bound around its historical levels.12

The final reflection is the one that frames the whole arc. Jyothy Labs is, at its core, a study in what happens when a regional hero gets serious about being a national champion. The 2011 Henkel deal was the foundational bet, the 2020 succession was the cultural test, and the 2026 Pril cliff is the operational stress test. The company has passed the first two. The third one starts on June 1, 2026 — eleven days from the date of this writing — when the Pril shelf becomes Exo's to defend. Whatever happens next, the four drops in that Thrissur kitchen forty-three years ago turned into one of the more durable second acts in Indian consumer goods, and the third act is just beginning.

References

References

-

From Rs.5000 to Rs.1800 Cr: MP Ramachandran's Success with Ujala & Maxo — YourStory, 2023-10 ↩↩↩↩↩↩

-

Jyothy Labs Ltd (BOM:532926) Q2 2026 Earnings Call Highlights — Yahoo Finance ↩↩

-

Jyothy Lab announces succession plan, to appoint M R Jyothy as MD — Business Standard, 2019-05-10 ↩↩↩↩↩

-

Henkel to Conclude Pril and Fa Brand Licensing Agreement with Jyothy Labs — ChemAnalyst ↩↩↩

-

Jyothy Labs Q4 FY26 Results: Strategic Growth and Performance — InvestyWise ↩↩↩↩↩↩↩↩↩↩

-

Jyothy Laboratories to acquire majority stake in Henkel India — Moneylife ↩↩↩

-

Jyothy completes buyout of Henkel India — Business Today, 2011-06-02 ↩

-

Reckitt Benckiser acquires Paras Pharmaceuticals — Business Standard, 2011 ↩

-

Jyothy Labs Q4 Revenue Up 7.7%, PAT Dips 12% on Inflation — Tradebrains ↩

-

Jyothy Labs shares plunge 11% as Henkel ends PRIL, Fa licencing deal — Business Standard, 2026-05-11 ↩↩

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube