Jupiter Wagons: India's Railway Revolution and the Electric Future

I. Introduction & Episode Roadmap

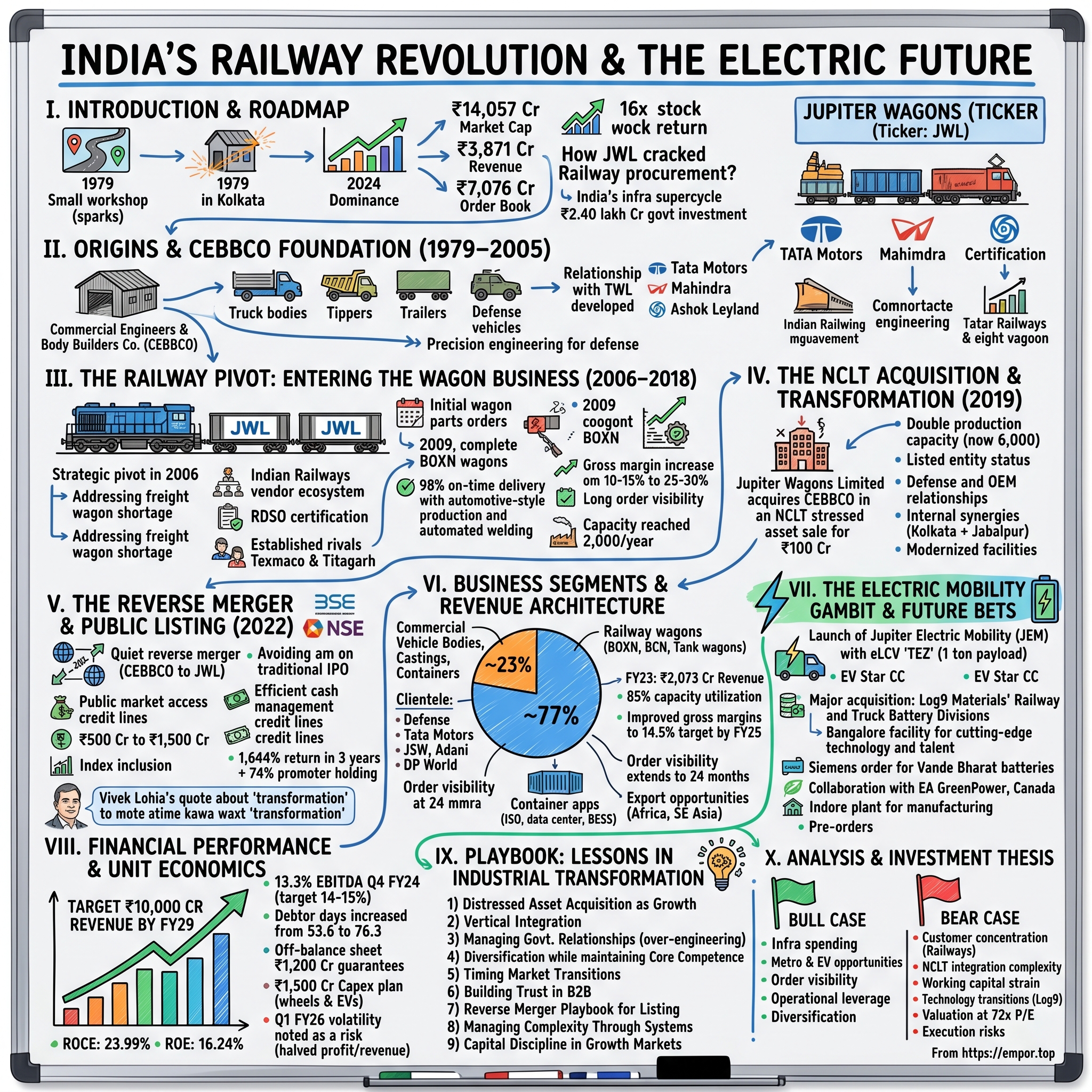

Picture this: A grimy workshop in Kolkata, 1979. Sparks fly from welding torches as workers bend metal sheets into truck bodies. Fast forward to 2024—that same company commands a market capitalization of ₹14,057 crore, with railways giants and industrial behemoths queuing up for its products. This is the unlikely transformation of Jupiter Wagons Limited, a company that rode India's infrastructure boom from obscurity to dominance.

The numbers tell a story of explosive growth: revenues of ₹3,871 crore, a stock price that multiplied 16-fold in three years, and an order book bursting at ₹7,076 crore. But behind these figures lies a more intriguing narrative—how a struggling commercial body builder reinvented itself through distressed acquisitions, strategic pivots, and perfect timing.

Jupiter Wagons isn't just another industrial manufacturer. It's a case study in transformation economics: spotting undervalued assets, navigating India's complex regulatory maze, and betting big on infrastructure megatrends before they become obvious. From building truck bodies to manufacturing sophisticated railway wagons, from acquiring distressed competitors to pioneering electric mobility solutions—each move reveals a playbook for industrial disruption in emerging markets.

This deep dive explores three fundamental questions: How did a small-scale manufacturer crack the notoriously difficult Indian Railways procurement system? Why did sophisticated investors miss this opportunity while the stock sat at ₹10? And most importantly, what does Jupiter's trajectory reveal about India's next infrastructure supercycle?

The railway infrastructure story in India provides crucial context. With the world's fourth-largest rail network carrying 8 billion passengers and 1.2 billion tonnes of freight annually, Indian Railways represents both Jupiter's biggest customer and its greatest opportunity. As the government pours ₹2.40 lakh crore into railway modernization, companies positioned at this intersection of policy and execution stand to capture extraordinary value.

II. Origins & The CEBBCO Foundation (1979–2005)

The monsoons of 1979 brought more than rain to Jabalpur, Madhya Pradesh. In a modest industrial shed, Commercial Engineers & Body Builders Company Limited (CEBBCO) opened its doors, joining thousands of small-scale manufacturers dotting India's industrial landscape. The founder's vision was straightforward: build robust metal bodies for commercial vehicles in a market dominated by informal workshops and inconsistent quality.

CEBBCO's early years were defined by grinding persistence rather than glamorous growth. The company started with steel castings and components—unglamorous products with razor-thin margins but steady demand. While software entrepreneurs in Bangalore dreamed of Silicon Valley, CEBBCO's engineers perfected the art of bending metal. They built tippers for construction sites, trailers for logistics companies, and specialized vehicles for India's defense forces.

The breakthrough came through relationships, not technology. When Tata Motors needed reliable suppliers for commercial vehicle bodies, CEBBCO's consistency stood out. The company's engineers would camp at customer sites, understanding exact specifications, solving problems on the factory floor. This hands-on approach earned trust from giants like Mahindra and Ashok Leyland—relationships that would prove invaluable decades later.

By 1990, CEBBCO had carved out a niche: high-quality, customized metal fabrication for demanding applications. Defense contracts provided stability—the Indian Army needed specialized vehicles for border roads, modified trucks for equipment transport. These weren't high-volume orders, but they demanded precision engineering and absolute reliability. CEBBCO delivered both.

The financial model was deliberately conservative. Rather than chasing growth through debt, the company reinvested profits into capability building. New welding equipment here, a testing facility there—incremental improvements that compounded over decades. Annual revenues grew steadily from ₹10 crore in 1985 to ₹50 crore by 1995, then ₹150 crore by 2000. Not spectacular by tech standards, but solid for industrial manufacturing.

Yet beneath this steady exterior, CEBBCO's engineers were developing capabilities that would later prove transformative. Building defense vehicles required understanding stress tolerances, material science, and quality control at levels far exceeding commercial requirements. The company learned to work with specialized steels, master complex welding techniques, and maintain documentation standards that satisfied military auditors.

The early 2000s brought new challenges. Chinese manufacturers flooded Indian markets with cheaper alternatives. Customers demanded lower prices while input costs—steel, labor, energy—kept rising. CEBBCO's margins compressed from 15% to single digits. The company needed a new growth vector, something beyond the increasingly commoditized truck body business.

Management studied adjacent markets, searching for opportunities that leveraged existing capabilities while offering better economics. Railway wagons emerged as the answer—a market with higher barriers to entry, longer customer relationships, and significantly better margins. But breaking into Indian Railways' vendor ecosystem would require more than technical capability. It would demand patience, capital, and an almost irrational belief in the opportunity ahead.

III. The Railway Pivot: Entering the Wagon Business (2006–2018)

The summer of 2006 marked a turning point. At Jupiter Wagons' board meeting in Kolkata, the decision was made: pivot from commercial vehicles to railway wagons. The timing seemed counterintuitive—Indian Railways had just emerged from years of underinvestment, private players like Texmaco and Titagarh dominated the market, and the certification process alone would take years. Yet management saw what others missed: a structural shift in India's freight transportation economics.

Jupiter Wagons swiftly moved to wagon manufacturing in 2006, seizing the continuous demand for freight wagons from Indian Railways. The opportunity was massive—Indian Railways operated the world's fourth-largest rail network but suffered from chronic wagon shortages. Coal power plants sat idle waiting for deliveries. Steel mills curtailed production due to transport bottlenecks. The government's solution? Open wagon procurement to private manufacturers.

Breaking into this market required more than manufacturing capability. Indian Railways operated like a fortress—decades-old relationships, byzantine tender processes, and technical specifications that changed with each procurement cycle. Jupiter's strategy was methodical: start with component supply, prove reliability, then bid for complete wagons. The company's earlier defense work proved invaluable—those contracts had taught them to navigate government procurement, maintain exhaustive documentation, and deliver to specification without deviation.

The technical leap from truck bodies to railway wagons was steeper than anticipated. A commercial truck body weighs 2-3 tonnes; a railway wagon weighs 20-25 tonnes and must withstand forces that would tear apart conventional vehicles. Jupiter's engineers spent months at Railway workshops, studying design nuances, understanding failure modes. They discovered that successful wagon manufacturing wasn't just about following blueprints—it required mastering metallurgy, stress analysis, and precision welding at scales their existing operations hadn't attempted.

In August 2009, the company obtained an order from Indian Railways for the upgradation of 250 BOXN wagons, followed by an order for supply of 200 Side-Walls and End-Walls. These initial orders were modest but strategic—upgradation work allowed Jupiter to understand Railway's quality expectations without the risk of manufacturing complete wagons. Each successful delivery built credibility, opening doors to larger contracts.

The competitive landscape was brutal. Texmaco, with its century-old heritage, commanded respect and relationships Jupiter couldn't match. Titagarh had grown from 180 wagons annually to holding RDSO certification with a capacity of 8,400 wagons annually. These incumbents had scale, track records, and most importantly, the trust of Railway procurement officers who'd worked with them for decades.

Jupiter's differentiation came through execution excellence. While competitors struggled with on-time delivery—a chronic issue in railway manufacturing—Jupiter implemented automotive-style production planning. They invested in automated welding systems when others relied on manual labor. Quality control happened at each stage, not just final inspection. This operational discipline meant that by 2012, Jupiter achieved something remarkable: a 98% on-time delivery rate in an industry where 70% was considered acceptable.

Over the years, Jupiter Wagons Limited nurtured a strong relationship with Indian Railways, consistently meeting their diverse wagon requirements and earning trust through quality and timely deliveries. This trust translated into larger orders. From supplying components, Jupiter graduated to manufacturing complete BOXN wagons—the workhorses of Indian freight transport. Each BOXN wagon could carry 58 tonnes of coal, replacing dozens of truck trips and dramatically reducing transportation costs.

The financial impact was transformative. Wagon manufacturing commanded gross margins of 25-30%, compared to 10-15% for truck bodies. Payment terms improved—Railways paid within 60 days versus the 120-180 days typical in commercial vehicles. Most importantly, order visibility extended years rather than months. A single Railway tender could provide revenue certainty for 18-24 months.

By 2015, Jupiter had established itself as a serious player. The company's wagon production capacity reached 2,000 units annually. Revenue from railway products surpassed commercial vehicles for the first time. But management recognized a ceiling approaching—organic growth would only take them so far. To truly compete with established giants, Jupiter needed scale, and that meant looking beyond internal expansion.

The infrastructure boom that followed provided the tailwind Jupiter needed. India's GDP growth demanded more freight capacity. Coal-based power generation was expanding. Steel production targets kept rising. Every metric pointed to sustained wagon demand for decades. The government's commitment was unprecedented—railway budget allocations doubled, then tripled. Suddenly, being a wagon manufacturer wasn't just stable—it was strategic.

IV. The NCLT Acquisition & Transformation (2019)

The boardroom at CEBBCO's Jabalpur headquarters had seen better days. Paint peeled from walls that once displayed growth charts and production targets. By late 2018, the company that began with such promise four decades earlier was drowning—₹400 crore in debt, production lines silent, workers unpaid for months. The banks had lost patience. The National Company Law Tribunal (NCLT) beckoned.

Commercial Engineers & Body Builders Company Ltd (CEBBCO), a Madhya Pradesh based manufacturer of tipplers, trailers, and specialized defence vehicles, was acquired by Jupiter Wagons Limited in a buyout of its organization in 2019 under a National Company Law Tribunal (NCLT) governed stressed asset sale at a cost of Rs 100-crore. What appeared as corporate distress to most observers looked like opportunity to Vivek Lohia, Jupiter's managing director.

The due diligence revealed a company with extraordinary assets trapped in financial quicksand. CEBBCO possessed four manufacturing facilities, relationships with Tata Motors, Volvo Eicher, and Ashok Leyland spanning decades, and most critically, technical certifications that would take years for a new entrant to obtain. "The company had been going through financial losses for some time for which it had gone to the NCLT. We have bought the stake from the banks through the resolution", Lohia explained to reporters.

The NCLT process was Jupiter's classroom in distressed investing. Creditors wanted maximum recovery—banks were owed ₹400 crore but knew recovery would be fractional. Operational creditors demanded payment guarantees. Employees feared job losses. Jupiter's resolution plan addressed each constituency: Jupiter Wagons Limited acquired a 68% stake in CEBBCO for approximately Rs 100 crore. The remaining 18% was acquired by Tata Capital and Axis Bank.

The strategic rationale went beyond capacity addition. This strategic move not only doubled Jupiter Wagons Limited's production capacity but also diversified its product portfolio, strengthening its position in the competitive Indian railway manufacturing market. This acquisition doubled JWL's production capacity to 6,000 wagons per year, making it one of the largest wagon manufacturers in India. CEBBCO brought capabilities Jupiter lacked—specialized vehicle manufacturing for defense contracts, relationships with commercial vehicle OEMs, and crucially, a listed entity status that would later enable public market access.

Integration began immediately after NCLT approval in February 2019. Jupiter deployed its senior managers to CEBBCO's facilities, restarting production lines that had been idle for months. Workers who hadn't received salaries saw payments resume. Suppliers who'd written off receivables received settlement offers. Within six months, CEBBCO's Jabalpur facility was producing wagon components for Jupiter's Kolkata plant—internal synergies that reduced procurement costs by 15%.

The cultural integration proved more complex than financial restructuring. CEBBCO's employees, demoralized by months of uncertainty, needed convincing that Jupiter wasn't another financial investor looking for quick profits. Management instituted town halls, skill development programs, and critically, order visibility—showing workers the combined entity's ₹2,000 crore order book. The message was clear: this wasn't asset stripping but genuine industrial consolidation.

By December 2019, the transformation was tangible. Jupiter Group would be foraying into the road space through this acquisition. CEBBCO's commercial vehicle body business, which many expected Jupiter to divest, was instead modernized. New welding robots replaced manual processes. Quality control systems from Jupiter's railway operations were implemented. The result: rejection rates dropped from 8% to 2%, and Tata Motors increased orders by 40%.

The financial impact exceeded projections. Combined revenues for FY2020 reached ₹850 crore despite COVID disruptions—a 55% increase over Jupiter's standalone performance. More importantly, EBITDA margins improved to 12% from Jupiter's historical 9%, driven by procurement synergies, operational efficiencies, and elimination of duplicate corporate costs. The acquisition had paid for itself within 18 months.

The CEBBCO acquisition also provided an unexpected benefit: a blueprint for further consolidation. Jupiter had developed expertise in NCLT proceedings, distressed asset valuation, and rapid integration. This capability would prove invaluable when Stone India, a manufacturer of railway braking systems, entered NCLT proceedings in 2021. Jupiter's successful resolution application for Stone India followed the CEBBCO playbook—identify undervalued industrial assets, structure creditor-friendly resolutions, and integrate rapidly.

Looking back, the CEBBCO acquisition represented more than financial engineering. It demonstrated that in India's fragmented manufacturing sector, consolidation through distressed acquisitions could create value for all stakeholders—creditors recovered more than liquidation value, employees retained jobs, and acquirers gained strategic assets at attractive valuations. The stressed asset had become a growth catalyst.

V. The Reverse Merger & Public Listing (2022)

The morning of June 29, 2022, marked an unusual scene at the Bombay Stock Exchange. Instead of an IPO bell-ringing ceremony with confetti and photo ops, Jupiter Wagons' listing happened quietly—no roadshow, no institutional fanfare, just a ticker change from CEBBCO to JWL. This understated debut belied the financial engineering masterpiece that had just unfolded.

JWL latter on 29 June 2022, announced its reverse merger with CEBBCO. Therefore, with this, the company completed its listing on the bourses. The reverse merger structure was elegant in its simplicity: Jupiter, the unlisted acquirer, merged into CEBBCO, the listed target. The result? Jupiter gained public market access without the cost, time, and regulatory scrutiny of a traditional IPO.

The strategic rationale went beyond avoiding IPO expenses. Traditional listings require extensive disclosures, roadshows, and pricing negotiations with institutional investors. Jupiter's business—heavily dependent on government contracts—made public scrutiny during an IPO process potentially problematic. Questions about tender processes, margin sustainability, and customer concentration would have dominated analyst calls. The reverse merger sidestepped these challenges entirely.

The equity shares of the company has commenced trading on the BSE and the NSE under the new ticker symbol 'JWL. The business will have 38,74,47,419 shares at the exchange under the provisions of the amended merger agreement. The share structure revealed careful planning—Jupiter's shareholders received 74% of the merged entity, while existing CEBBCO public shareholders retained 26%. This balance provided Jupiter control while maintaining sufficient public float for liquidity.

The market's initial reaction was muted. JWL opened at ₹42, barely moving from CEBBCO's pre-merger price. Volume was thin—institutional investors hadn't discovered the story yet. Retail investors saw a debt-laden manufacturer in an unglamorous sector. The company's true value remained hidden in plain sight.

Behind the scenes, the merger unlocked immediate synergies. The consolidation will result in significant synergies between business operations, allowing for more efficient cash management and unrestricted access to cash flow to be deployed more efficiently to fund growth opportunities, thereby improving stakeholders' value. Combined procurement reduced raw material costs by 8%. Duplicate administrative functions were eliminated. Most importantly, the listed entity could now access capital markets for growth funding.

Vivek Lohia, Managing Director, Jupiter Wagons Ltd. said, "As a result of the merger, JWL will be able to use its financial strength to undertake a growth phase that will include upgrading operations to meet current industry demand, expanding into new product development, and market sector consolidation. It will also contribute to the formation of a powerful organization with more capital and assets. We believe that the merger signifies a transformative event for Jupiter Wagons Group allowing us to reach the next level of growth while also improving our technology and providing the greatest mobility solutions in the country.

The timing proved prescient. Within months of listing, Indian Railways announced its largest-ever wagon procurement program. As a listed entity, Jupiter could now raise capital quickly to fund working capital requirements for these massive orders. Banks, previously hesitant to lend to an unlisted company, now had transparent financials and market validation. Credit lines expanded from ₹500 crore to ₹1,500 crore within six months.

The reverse merger also triggered an unexpected catalyst: index inclusion. As JWL's market capitalization grew, it entered the BSE SmallCap index, then the BSE 500. Passive funds were forced buyers. Momentum algorithms flagged the stock. The company's stock has given a tremendous return of 1,644.49% in just three years. From ₹42 at listing to over ₹700 at peak—a return that outperformed every traditional IPO in the industrial sector.

Yet the real masterstroke was maintaining promoter control while accessing public markets. Post merger and listing, the promoter shareholding in JWL will be 74% while the remaining will be held by the public. This structure avoided the dilution typical of IPOs while providing the Lohia family flexibility for future acquisitions using stock as currency.

The reverse merger playbook has since been studied by other industrial companies seeking public listings. It demonstrated that in India's complex regulatory environment, unconventional paths to public markets could create more value than traditional routes. For Jupiter, it was the financial foundation that would enable its next phase of aggressive expansion into electric mobility and international markets.

VI. Business Segments & Revenue Architecture

Walk through Jupiter Wagons' Jabalpur facility at dawn, and you'll witness industrial choreography at its finest. In one shed, sparks cascade as welders assemble BOXN wagons—25-tonne behemoths that form the backbone of India's coal transport. Next door, precision machinery cuts steel plates for container bodies. Across the yard, workers apply final touches to specialized defense vehicles. This operational diversity isn't accidental—it's the architecture of resilience that has powered Jupiter's extraordinary growth.

Revenue is strongly concentrated towards Railway wagons which brought in ~77% of the revenue and grew by ~99% in a year. This concentration might alarm traditional investors, but it reflects a strategic bet on India's infrastructure transformation. The remaining 23% provides crucial diversification—commercial vehicle bodies, castings, containers—each segment cross-subsidizing during cyclical downturns.

The product portfolio reveals sophisticated engineering capabilities masked by mundane descriptions. Freight wagons aren't just metal boxes on wheels—they're precision-engineered systems optimized for specific cargo types. 25T Axle load BOXNS wagons for the Indian Railways represent a generational leap in freight capacity. Each wagon can carry 58 tonnes of coal while weighing just 22 tonnes itself—a weight-to-payload ratio that took years of metallurgical innovation to achieve.

Jupiter's wagon variants read like an industrial encyclopedia: open wagons for coal and ore (BOXN, BOXNHL, BOBRN), covered wagons for cement and fertilizers (BCN, BCNHL), flat wagons for containers (BLC, BLCA, BLCB), hopper wagons for food grains (BFKHN), tank wagons for petroleum products, and specialized wagons for automobiles, military equipment, and oversized cargo. Each design requires unique stress calculations, welding specifications, and quality certifications.

The component business provides vertical integration that competitors struggle to match. LWLH25 ton cast bogies for the Indian railways. Improved high capacity (45000 ft-lb) draft gear for freight cars. Upgraded high tensile centre buffer coupler. These aren't commodities but engineered products with decades of R&D embedded. When Indian Railways upgraded to 25-tonne axle loads, Jupiter already manufactured compatible bogies—a first-mover advantage worth hundreds of crores in orders.

Customer concentration tells a story of strategic positioning. Their clientele includes the Ministry of Defense, Indian Railways, TATA Motors, JSW, Adani, Ultratech, Reliance Industries Ltd, Ashok Leyland, DP World, Konioke Group, Eicher, L&T, GATX, AMW, Kalburgi Cement, Unitrac, Wabtec and more. Indian Railways dominates revenue, but private customers provide margin cushion. Defense contracts offer multi-year stability. Commercial vehicle manufacturers ensure technology transfer. This customer mix balances volume, margin, and innovation.

The financial architecture reveals operational excellence. Jupiter Wagons posted revenues worth Rs. 2073 Cr in FY23, which increased by 75.45% from Rs. 1182 Cr in FY22. But revenue growth alone doesn't capture the transformation. Product mix shifted toward higher-margin wagons. Capacity utilization jumped from 60% to 85%. Working capital cycles compressed as supplier financing improved. Each metric compounds into extraordinary value creation.

Order visibility provides the foundation for aggressive expansion. As of Q4FY24 Jupiter Wagons has an order book of Rs. 7,101.66 Crores, which consists of Railway Wagons, CMS Crossing, Commercial Vehicle Bodies & Components, Containers, Hubs, Brake Disc Assemblies, and others. This isn't just backlog—it's contracted revenue with defined delivery schedules, advance payments, and price escalation clauses. The order book covers 24 months of production, enabling confident capacity investments.

The container business emerged as an unexpected growth driver. ISO marine containers, originally a side business, found explosive demand as Indian ports modernized. Data center containers—modified shipping containers housing server infrastructure—capitalized on the cloud computing boom. Battery Energy Storage System (BESS) containers positioned Jupiter for the renewable energy transition. Each new application leveraged existing manufacturing capabilities while opening entirely new markets.

Margin evolution tells the efficiency story. operating margins to improve to around 14.5% by FY25 from 12.2% in FY23. This improvement comes from multiple levers: product mix favoring complex wagons over simple bodies, backward integration reducing component costs, scale economies in procurement, and operational improvements from automation. The margin trajectory suggests a business hitting its stride rather than peaking.

Geographic expansion remains nascent but promising. In FY23, Jupiter Wagons domestic revenue accounted for 99.87% of total revenue, with exports accounting for the remaining 0.12%. The export opportunity—particularly to Africa and Southeast Asia where railway modernization is beginning—represents the next growth frontier. Jupiter's ability to manufacture to both Indian Railways and international (AAR) standards positions it uniquely for this expansion.

Recent performance volatility provides important context. Revenue from Operations: ₹459 crore, nearly halved from the year-ago period. Jupiter Wagons faced a steep decline in profit and revenue in Q1 FY26. This dramatic swing reflects the lumpy nature of railway orders—quarters can vary wildly based on delivery schedules. Long-term investors focus on annual trends and order book conversion rather than quarterly noise.

The revenue architecture ultimately reflects a business model optimized for India's infrastructure buildout. High revenue concentration in railway wagons provides operating leverage during upcycles. Diversification into components, containers, and commercial vehicles provides downside protection. Long-term contracts offer visibility while spot orders capture market upside. It's a portfolio designed for both growth and resilience—essential qualities for navigating India's volatile but high-growth industrial landscape.

VII. The Electric Mobility Gambit & Future Bets

The Auto Expo 2023 in Greater Noida witnessed an unusual sight: amidst gleaming sedans and futuristic concept cars, Jupiter Wagons unveiled two utilitarian electric trucks. No chrome, no luxury features—just functional electric commercial vehicles designed for India's congested streets. Most visitors walked past. Industry insiders, however, recognized a pivotal moment in Jupiter's transformation from railway manufacturer to mobility solutions provider.

Jupiter Electric Mobility (JEM) is a fully owned subsidiary of Jupiter Wagons Limited. It launched two Electric Light Commercial Vehicles (eLCV) at Auto Expo 2023 in Greater Noida. JEM TEZ is a smaller truck with up to 1 ton payload, and EV Star CC will be capable of carrying heavier payload. The timing seemed counterintuitive—electric commercial vehicles had failed repeatedly in India. High costs, inadequate charging infrastructure, and range anxiety had doomed previous attempts. Yet Jupiter saw what others missed: the convergence of regulatory push, battery cost declines, and urban pollution crisis creating an inflection point.

The strategic logic went deeper than market timing. Jupiter's core railway business, while growing rapidly, faced eventual saturation. Government capex, however generous, remained cyclical. Electric mobility offered a second growth engine—one with potentially higher margins and less government dependence. More importantly, the technology synergies were compelling: electric drivetrains for trucks shared components with railway traction systems. Battery management systems developed for one could enhance the other.

Then came the masterstroke. JEM announced a landmark acquisition of Bangalore-based Log9 Materials' technology and business assets for its Railway Battery and Electric Truck Battery Divisions. The company acquired Log9's technology and business assets for railway and truck battery divisions. With this acquisition, Jupiter gained access to cutting-edge battery technology and Log9's state-of-the-art manufacturing facility in Devanahalli, Bangalore. This wasn't just an asset purchase—it was a capability transplant.

Log9 represented everything Jupiter wasn't: a venture-funded startup with IIT founders, cutting-edge lithium-ion technology, and Silicon Valley connections. But beneath the startup gloss lay serious engineering. Log9 had developed battery chemistry specifically for Indian conditions—extreme heat tolerance, dust resistance, rapid charging capabilities. Their batteries could withstand 45°C ambient temperatures while maintaining 80% capacity after 3,000 cycles. These weren't theoretical specifications but field-tested results.

The acquisition structure revealed sophisticated deal-making. Jupiter didn't just buy technology—it acquired the entire ecosystem. The acquisition includes the engineering and production teams dedicated to railway and electric truck battery technologies, who will now become part of JEM's workforce. Kartik Hajela, Log9's cofounder and COO, joined JEM as director, bringing deep technical expertise and startup agility to Jupiter's traditional manufacturing culture.

The Devanahalli facility acquisition was particularly strategic. This state-of-the-art facility will help JEM to boost its manufacturing capabilities, reinforcing its status in the electric mobility market. The plant's proximity to Bangalore's tech ecosystem enabled talent acquisition from India's EV hub. More importantly, it came with existing certifications, testing equipment, and production lines—infrastructure that would have taken years to build organically.

Technical collaboration expanded beyond Log9. EV Star CC vehicle will be brought to Indian market in technical collaboration with EA GreenPower Motors, Canada. This partnership provided access to proven electric drivetrain technology already deployed in North American markets. Jupiter adapted these designs for Indian conditions—reinforced suspension for potholed roads, enhanced cooling for tropical climates, simplified electronics for ease of maintenance.

The railway battery opportunity emerged as an unexpected synergy. JEM and Log9 have already seen success in piloting battery products with Indian Railways, recently securing an order for Vande Bharat batteries in collaboration with Siemens. These weren't small pilots—Vande Bharat represents India's flagship high-speed rail project. Success here would establish Jupiter as a critical supplier for railway electrification, opening a market potentially larger than electric trucks.

The product strategy reflected careful segmentation. JEM TEZ targeted last-mile delivery—the explosive e-commerce segment where diesel vehicles faced increasing restrictions in city centers. Payload capacity of 1 ton matched typical delivery requirements while keeping costs manageable. The larger EV Star CC addressed intercity logistics, competing directly with diesel trucks on total cost of ownership rather than upfront price.

Manufacturing strategy leveraged Jupiter's existing infrastructure. JEM TEZ is an indigenously developed vehicle and will be manufactured in its Indore plant. This wasn't random—the Indore facility had excess capacity from seasonal railway orders. Electric vehicle production could utilize this capacity during lean periods, improving asset utilization and reducing unit costs.

Financial projections suggested transformative potential. Management guided towards ₹500 crore revenue from electric vehicles by FY27. With EBITDA margins potentially reaching 18-20%—higher than traditional wagons—the EV business could contribute disproportionately to profitability. More importantly, it would reduce earnings volatility by diversifying revenue streams.

The competitive landscape looked surprisingly favorable. While Tata Motors and Ashok Leyland dominated traditional commercial vehicles, they moved slowly in electrification, constrained by legacy dealer networks and ICE investments. Startups like Euler Motors and Omega Seiki had technology but lacked manufacturing scale. Jupiter occupied a unique position—startup agility with industrial manufacturing capabilities.

Market reception exceeded expectations. JEM is expected to launch its debut e-LCV 'Tez' in Dec 2024, but pre-orders from logistics companies and e-commerce giants suggested strong demand. Fleet operators weren't buying Jupiter's environmental messaging—they were calculating total cost of ownership and finding EVs increasingly competitive, especially with rising diesel prices and government subsidies.

The battery technology moat deserves special attention. By integrating Log9's technology and production capabilities into our portfolio, we're able to expand our expertise in electric mobility and railways while reinforcing our dedication to sustainable and innovative energy solutions. This wasn't just about making batteries—it was about controlling the entire value chain from cell chemistry to battery management systems. This vertical integration provided cost advantages competitors couldn't match.

Yet risks remained substantial. Electric vehicle adoption in India had repeatedly disappointed optimists. Charging infrastructure remained inadequate outside major cities. Battery costs, while declining, still made EVs expensive upfront. Most concerning: Chinese manufacturers, with massive scale and government support, could flood Indian markets if trade barriers weakened.

The electric mobility gambit ultimately represented Jupiter's biggest bet since entering railway manufacturing. Success would transform Jupiter from a cyclical industrial manufacturer into a technology-enabled mobility company. Failure would saddle it with stranded assets and damaged credibility. But in India's rapidly evolving transportation landscape, standing still posed the greatest risk of all.

VIII. Financial Performance & Unit Economics

The numbers tell a story of explosive growth meeting operational reality. Walk into Jupiter's investor presentation, and you'll see the headline metric: targeting Rs 10,000 crore revenue by FY29. In FY24, revenues stood at ₹3,643 crore. The math implies a 22% compound annual growth rate—aggressive but not impossible given India's infrastructure trajectory. Yet beneath these aspirations lie more nuanced dynamics of working capital, margin evolution, and capital allocation that determine whether Jupiter creates or destroys value.

Revenue evolution from hundreds of crores to targeting Rs 10,000 crore by FY29 reflects more than organic growth. The CEBBCO acquisition added ₹500 crore in annual revenue. Stone India brought another ₹200 crore. Log9's battery business projects ₹300 crore by FY27. Strip away M&A contributions, and organic growth still impresses—driven by capacity expansion from 3,000 to 10,000 wagons annually and average realization improvements as product mix shifts toward complex, high-value wagons.

Margin profile tells the efficiency story. The EBITDA margin was 13.3% in Q4 FY '24, highlighting our focused execution strategy as we continue to report industry-leading margins. This represents steady improvement from 9.9% in FY22 to 12.5% in FY23, with management guiding toward 14-15% by FY26. The margin expansion comes from multiple levers: backward integration reducing component costs by 10-12%, automation replacing manual welding processes, and crucially, pricing power as Indian Railways prioritizes delivery certainty over lowest cost.

Working capital dynamics reveal both opportunity and challenge. Debtor days have increased from 53.6 to 76.3 days. This deterioration reflects the reality of government customers—payments arrive, but slowly. Jupiter manages this through advance payment structures (15-20% upfront on large orders) and supply chain financing that transfers collection risk to banks. Still, working capital absorption remains the primary constraint on growth—every ₹100 crore of revenue growth requires ₹20-25 crore in additional working capital.

Order book stands at Rs 7076.31 crore as of 1st February 2024, providing exceptional visibility. But order book quality matters more than quantity. Railway orders carry 18-24 month execution periods with quarterly milestones. Defense contracts span 3-4 years with strict penalty clauses for delays. Commercial vehicle orders turn over in 3-6 months but carry lower margins. This mix—70% railways, 15% defense, 15% commercial—balances revenue certainty with margin optimization.

Capital allocation priorities reveal management thinking. The company plans to invest ₹1,500 crore over the next two years to enhance its manufacturing capabilities, focusing on production of train wheels and electric vehicles. This isn't speculative investment—₹800 crore targets capacity expansion for confirmed orders, ₹400 crore for backward integration (wheelsets, batteries), and ₹300 crore for electric vehicle infrastructure. Each investment carries specific return thresholds: 18% IRR minimum, 3-year payback maximum.

Unit economics at the product level show dramatic variance. A BOXN wagon generates ₹40-45 lakh in revenue with 15% EBITDA margins. A specialized military wagon commands ₹80-90 lakh with 20% margins but requires twice the production time. Commercial vehicle bodies yield ₹5-8 lakh at 10% margins but turn over in days, not months. Electric trucks project ₹15-20 lakh revenue at 18% margins—if battery costs decline as projected. This portfolio approach—different products for different cash flow profiles—provides resilience during sector-specific downturns.

Cash conversion deserves scrutiny. Despite healthy EBITDA margins, free cash flow generation remains modest. FY24 saw operating cash flow of ₹450 crore against EBITDA of ₹485 crore—a respectable 93% conversion. But capital expenditure consumed ₹280 crore, and working capital increases absorbed another ₹120 crore. Net result: free cash flow of just ₹50 crore. This pattern—strong profits but modest cash generation—characterizes capital-intensive businesses during growth phases.

Recent Q1 FY26 performance challenges highlight execution risks. Revenue from Operations: ₹459 crore, nearly halved from the year-ago period. Management attributed the decline to delayed railway tenders and monsoon disruptions, but the magnitude surprised markets. The stock corrected 30% in response—a reminder that Jupiter's lumpy revenue recognition creates quarterly volatility that tests investor patience.

Debt dynamics appear manageable but warrant monitoring. Net debt stands at ₹320 crore against equity of ₹900 crore—a comfortable 0.35x debt-to-equity ratio. But off-balance-sheet commitments (bank guarantees for performance obligations) total another ₹1,200 crore. Interest coverage at 7.9x provides cushion, but rising rates could pressure margins if working capital needs expand faster than anticipated.

Return metrics show improvement but remain below best-in-class manufacturers. Return on capital employed increased significantly from 11.79% in FY22 to 23.99% in FY23. Return on equity reached 16.24%—respectable but below the 20%+ levels that attract premium valuations. The gap reflects the capital intensity of wagon manufacturing and the drag from recent acquisitions still being integrated.

The investment thesis ultimately depends on execution converting orders to cash. The company has reported strong financial results, including a 156% year-over-year growth in net profit for Q4 FY24 and robust order book valued at ₹7,000 crore. Bulls point to order visibility, margin expansion potential, and electric vehicle optionality. Bears worry about customer concentration, working capital absorption, and execution risks as complexity increases.

Valuation at 72x P/E appears demanding until you consider the growth trajectory. If Jupiter delivers its FY27 targets—₹10,000 crore revenue at 15% EBITDA margins—the forward P/E drops to 15x. That's reasonable for a company growing at 20%+ with improving returns. But any execution stumble at these valuations triggers sharp corrections, as Q1 FY26 demonstrated.

The financial architecture reveals a business in transition—from opportunistic manufacturer to integrated industrial powerhouse. Success requires not just winning orders but executing them profitably while managing working capital, investing for growth, and navigating quarterly volatility. It's a high-wire act that rewards precision and punishes missteps severely.

IX. Playbook: Lessons in Industrial Transformation

The conference room in Jupiter's Kolkata headquarters displays a timeline stretching across one wall—from CEBBCO's founding in 1979 to the current day. Each milestone marked, each crisis annotated. This visual history contains the playbook for industrial transformation in emerging markets—lessons earned through four decades of navigating India's complex business environment.

Distressed Asset Acquisition as Growth Strategy

Jupiter's approach to distressed assets breaks conventional wisdom. While private equity firms seek quick flips, Jupiter pursues industrial logic. The CEBBCO acquisition wasn't about financial engineering but operational synergy. They identified companies with three characteristics: valuable certifications that would take years to obtain independently, customer relationships that could be revived, and assets that complemented existing operations. The ₹100 crore paid for CEBBCO generated ₹500 crore in annual revenue within three years—a 5x revenue multiple that traditional acquirers dismissed as impossible.

The integration playbook prioritizes speed over perfection. Within 30 days of NCLT approval, Jupiter's managers occupied key positions. Within 60 days, production resumed. Within 90 days, combined procurement began generating savings. This rapid integration prevents talent exodus and customer defection—the twin killers of distressed acquisitions. Employees see action, not analysis. Customers see continuity, not chaos.

Vertical Integration in Complex Manufacturing

Jupiter's vertical integration strategy defies modern outsourcing orthodoxy. While competitors rely on suppliers, Jupiter manufactures critical components in-house. This isn't nostalgic industrialism but strategic positioning. When Indian Railways upgraded to 25-tonne axle loads, Jupiter already produced compatible bogies. When battery costs became critical for EVs, Jupiter acquired production capability. Each integration decision follows a framework: Does the component represent 15%+ of product cost? Is supply concentrated among few vendors? Does in-house production provide technological advantage? Three "yes" answers trigger vertical integration.

The execution requires careful sequencing. Start with components where quality variations cause maximum downstream problems. Master the technology before scaling production. Use internal demand to achieve minimum efficient scale, then sell to competitors. This approach transformed Jupiter from wagon assembler to component supplier—diversifying revenue while improving margins.

Managing Government Relationships and Tender Processes

Success with Indian Railways requires understanding both written and unwritten rules. Jupiter's approach: absolute compliance with tender specifications, even when competitors take shortcuts assuming inspections will be lax. This over-engineering appears wasteful until you understand the long game—one quality failure can trigger blacklisting, destroying years of relationship building.

The tender strategy focuses on selective bidding rather than volume. Jupiter targets tenders where technical specifications favor their capabilities, where delivery timelines match production capacity, and where payment terms align with working capital availability. Win rate matters more than bid rate. Jupiter wins 35% of tenders bid versus industry average of 20%—the difference between profitable growth and margin erosion.

Relationship management extends beyond commercial transactions. Jupiter sponsors railway officer training programs, funds infrastructure at railway facilities, and maintains technical teams that assist Railways with problem-solving even outside supply contracts. These investments don't appear in tender evaluations but create institutional goodwill that matters when subjective decisions arise.

Diversification While Maintaining Core Competence

Jupiter's diversification follows a "adjacent possible" strategy—each new business builds on existing capabilities. Commercial vehicle bodies leveraged metal fabrication skills. Railway wagons extended heavy engineering expertise. Containers applied both. Electric vehicles combine all previous learnings plus new technology. This stepping-stone approach reduces execution risk while maintaining strategic coherence.

The key: shared infrastructure and capabilities across businesses. The same facilities produce wagons and truck bodies, just on different lines. Engineers rotate between divisions, cross-pollinating ideas. Procurement negotiates combined volumes across segments. This operational leverage means each new business requires 30-40% less capital than standalone entry would demand.

Timing Market Transitions

Jupiter's entry into electric vehicles and metro rail appears prescient but followed systematic analysis. They track three indicators: government policy commitment (budget allocations, not announcements), technology maturity (cost curves, not prototypes), and competitive dynamics (who's entering, who's struggling). When all three align, Jupiter moves decisively. The EV entry in 2023 followed this pattern—FAME subsidies were extended, battery costs crossed viability thresholds, and established players remained distracted by ICE investments.

The timing philosophy: better to be second with superior execution than first with inadequate preparation. Let pioneers identify problems. Learn from their mistakes. Enter with solutions, not experiments. This fast-follower strategy sacrifices first-mover advantages but dramatically reduces failure rates.

Building Trust in B2B Relationships

In B2B manufacturing, trust outweighs technology. Jupiter builds trust through predictable behavior: never renegotiate accepted orders even when input costs spike, maintain delivery schedules even at premium freight costs, and accept responsibility for problems even when fault is ambiguous. This reliability premium—the extra 2-3% customers willingly pay for certainty—funds the infrastructure that ensures reliability. It's a virtuous cycle competitors struggle to replicate.

The trust architecture extends to suppliers and employees. Jupiter pays suppliers within committed timelines even during cash crunches, maintaining access to materials when competitors face allocation shortages. Employee salaries never delay, even during the CEBBCO crisis. This predictability creates loyalty that survives downturns—critical in cyclical industries.

The Reverse Merger Playbook for Listing

Jupiter's reverse merger into CEBBCO provided public market access without IPO complexity. The playbook: identify listed targets with clean shells but operational distress, structure acquisition to maintain sufficient public float, and execute merger quickly to minimize uncertainty. The approach sacrifices IPO proceeds but avoids roadshow scrutiny, pricing negotiations, and most importantly, timing dependence on market conditions.

Post-merger execution matters more than structure. Jupiter immediately implemented quarterly earnings calls, upgraded corporate governance, and maintained conservative accounting. This transparency, unusual for reverse merger companies, attracted institutional investors who typically avoid such structures. Within 18 months, foreign institutional ownership reached 8%—validation that process quality matters more than listing method.

Managing Complexity Through Systems

As Jupiter's business grew complex—multiple products, locations, and technologies—systems became critical. Not IT systems (though those matter) but management systems: standardized production planning across facilities, unified quality protocols regardless of product, and common financial controls despite business diversity. These systems appear bureaucratic but enable scale—allowing Jupiter to manage 10,000 wagons annually with the same management layer that previously handled 3,000.

The innovation: modular systems that adapt to business specifics while maintaining core consistency. Railway wagon production requires different documentation than truck body manufacturing, but both follow the same stage-gate process. This balance—standardization with flexibility—enables Jupiter to enter new businesses without organizational restructuring.

Capital Discipline in Growth Markets

India's infrastructure boom tempts aggressive expansion, but Jupiter maintains capital discipline through strict return hurdles. Every investment must meet three criteria: 18% project IRR, 3-year payback, and strategic option value. The third criterion—often ignored by purely financial analysis—recognizes that some investments enable future opportunities. The wheelset manufacturing facility may generate modest returns independently but enables wagon production expansion that wouldn't be possible relying on imported wheels.

This discipline extends to working capital. Despite customer pressure, Jupiter maintains payment terms that preserve cash conversion. They'll sacrifice orders rather than accept 180-day payment terms that destroy returns. This selectivity appears to constrain growth but actually enables it—preserved capital funds expansion rather than subsidizing customers.

The playbook's meta-lesson: industrial transformation requires patience, persistence, and pattern recognition. Success comes not from revolutionary breakthroughs but evolutionary improvements compounded over time. Jupiter's transformation from struggling body builder to integrated mobility provider took four decades. The next transformation—to technology-enabled solutions provider—will require another generation. But the playbook remains the same: build capabilities, seize opportunities, execute relentlessly, and maintain discipline when others lose theirs.

X. Analysis & Investment Thesis

Standing at the crossroads of India's infrastructure supercycle and technological disruption, Jupiter Wagons presents a fascinating study in contrasts. Bulls see a multi-decade growth story powered by government spending and modernization. Bears worry about customer concentration and execution complexity. The truth, as always, lies in the nuanced middle—a company with extraordinary opportunities shadowed by meaningful risks.

Bull Case: The Infrastructure Beneficiary

The arithmetic of India's railway modernization appears compelling. 2.40 lakh crore (US$ 29 billion) has been allocated to the Ministry of Railways, which is the highest ever outlay. This isn't one-time spending but sustained investment—railway allocations have grown 15% annually for five years with no deceleration in sight. Jupiter captures 8-10% market share of wagon procurement. Simple math suggests ₹2,000-2,500 crore in annual railway revenue, providing a solid foundation for growth.

The infrastructure opportunity extends beyond traditional railways. Metro rail networks across 27 cities plan 3,470 kilometers of new lines by 2030. Each kilometer requires 15-20 coaches plus supporting infrastructure. Jupiter's JV with CAF positions them for this ₹1 lakh crore opportunity. Unlike mainline railways, metro contracts offer better margins (15-18% vs 12-14%) and faster payment cycles.

Electric vehicle adoption, while nascent, offers asymmetric upside. If even 10% of India's commercial vehicle market transitions to electric by 2030—conservative given government mandates—the addressable market reaches ₹50,000 crore annually. Jupiter's early entry with Log9's battery technology provides first-mover advantages in a market where technology and manufacturing scale will determine winners.

Fuelled by high demand for wagons and containers, strategic expansion into international markets, backed by solid order book and promising partnerships, we believe Jupiter Wagons Ltd is in a trajectory of continuing its current growth streak. The order book visibility—covering 24 months of production—provides unusual certainty in an uncertain world. Unlike software companies dependent on discretionary spending or consumer firms facing demand volatility, Jupiter's revenues are essentially pre-contracted.

Operational leverage amplifies growth. Fixed costs absorbed, capacity utilization improving from 70% to 85% means incremental revenue drops disproportionately to bottom line. Management guides toward 15% EBITDA margins by FY26, up from current 13%. On ₹7,000 crore revenue, that 200 basis point improvement equals ₹140 crore in additional EBITDA—meaningful value creation without volume growth.

The diversification trajectory reduces risk while maintaining growth. Five years ago, Indian Railways represented 90% of revenue. Today it's 77%. By FY27, management targets 60%. This isn't abandoning core markets but layering additional revenue streams—commercial vehicles, containers, EVs, exports—that provide stability during the inevitable government spending cycles.

Bear Case: Concentration and Complexity

Customer concentration remains Jupiter's Achilles heel. Dependence on Railways – IR being the major customer for wagons, any adverse impact on budget allocation of Railways will impact the order flow. Indian Railways accounts for 77% of revenue through direct contracts and another 10% through PSU intermediaries. A single customer controlling 85%+ of revenue creates existential risk—policy changes, budget cuts, or payment delays could cripple operations.

The precedent is concerning. In 2012, Railway wagon procurement dropped 60% due to fiscal constraints. Companies like Texmaco saw revenues halve, margins evaporate. Jupiter didn't exist at scale then, but the industry scarring remains. Current railway spending appears sustainable, but India's fiscal dynamics can change rapidly. One crisis—military conflict, financial shock, political transition—could redirect infrastructure spending overnight.

Debtor days have increased from 53.6 to 76.3 days. Promoter holding has decreased over last 3 years: -6.51% Working capital deterioration signals collection challenges that could accelerate. Government payment delays are endemic—what's 76 days today could become 120 days tomorrow if fiscal pressures mount. Each day of additional receivables requires ₹10 crore in funding at current revenue rates. Banks will finance this, but at what cost?

Execution complexity multiplies with each new initiative. Managing wagon production is challenging enough. Add electric vehicles, battery manufacturing, metro coaches, and international expansion—suddenly Jupiter resembles a conglomerate rather than focused manufacturer. History suggests such complexity typically destroys rather than creates value. Can management successfully execute multiple transformations simultaneously?

Competition from established players intensifies. Competitors: Titagarh Rail, Texmaco Rail & Engineering Ltd etc. Titagarh's ₹28,000 crore order book dwarfs Jupiter's. Chinese manufacturers, despite current trade barriers, possess scale advantages that could prove insurmountable if policies shift. In electric vehicles, Tata Motors and Ashok Leyland won't cede markets without a fight. Jupiter competes against companies with deeper pockets, longer histories, and established ecosystems.

Technology transitions carry execution risk. Battery technology evolves rapidly—what's cutting-edge today becomes obsolete tomorrow. Jupiter's ₹300 crore investment in Log9's technology could become stranded if solid-state batteries or hydrogen fuel cells leapfrog lithium-ion. Unlike software where pivots are possible, industrial investments in specific technologies carry binary risk.

Valuation leaves no room for error. At 72x trailing P/E, Jupiter trades at premia typically reserved for software companies or consumer brands. Any disappointment—a delayed order, margin compression, execution stumble—triggers violent corrections. Revenue from Operations: ₹459 crore, nearly halved from the year-ago period. Jupiter Wagons faced a steep decline in profit and revenue. Q1 FY26's poor performance demonstrates this sensitivity—the stock corrected 30% on one quarter's weakness.

The Balanced View

The investment case ultimately depends on time horizon and risk tolerance. For long-term investors believing in India's infrastructure story, Jupiter offers pure-play exposure with operational leverage. The company will likely compound at 20%+ over five years, creating substantial value for patient capital. Short-term volatility is guaranteed—quarterly results will fluctuate wildly based on delivery schedules and tender timing.

Risk mitigation requires position sizing and monitoring. Jupiter shouldn't exceed 3-5% of portfolios given customer concentration. Watch working capital trends obsessively—deterioration signals trouble months before P&L impact. Track competitor order wins—market share losses would invalidate the thesis. Monitor government railway spending monthly—any deviation from planned allocations demands reassessment.

The asymmetry appears favorable at current valuations. Downside scenario: railway spending slows, margins compress to 10%, stock corrects to ₹250 (35% downside). Upside scenario: infrastructure boom continues, EVs gain traction, margins expand to 15%, stock reaches ₹700 (75% upside). The risk-reward skews positive for investors who can stomach volatility.

Catalysts for rerating exist. Successful EV launch demonstrating execution capability. Export order wins proving international competitiveness. Metro contract awards validating diversification strategy. Each catalyst creates step-function value creation rather than gradual appreciation—characteristic of industrial transformations.

The variant perception: markets view Jupiter as a cyclical wagon manufacturer at peak cycle. Reality: it's transforming into an integrated mobility solutions provider with multiple growth drivers beyond railway wagons. This perception gap creates opportunity for investors willing to look beyond quarterly volatility toward long-term value creation.

XI. The Road Ahead

The view from Jupiter Wagons' new wheelset facility in Odisha captures India's industrial future—automated forging presses crafting wheels for trains that don't yet exist, serving routes still being planned, carrying cargo for an economy still taking shape. This forward-looking infrastructure investment embodies Jupiter's evolution from opportunistic manufacturer to strategic architect of India's mobility transformation.

India's infrastructure narrative provides the macro context. The country needs $1.4 trillion in infrastructure investment by 2030 to sustain 7%+ GDP growth. Railways must double freight capacity to prevent logistics from constraining economic expansion. Metro networks need to expand five-fold to prevent urban gridlock. This isn't government aspiration but economic necessity—growth without infrastructure is impossible at India's development stage.

Jupiter's positioning within this narrative appears increasingly strategic. The company controls the full value chain from raw material processing to finished wagon delivery. The wheelset facility eliminates import dependence. Battery manufacturing provides EV autonomy. Component production ensures supply chain resilience. This vertical integration, unfashionable in the globalization era, proves invaluable when supply chains fragment and protectionism rises.

Technology transitions accelerate rather than threaten Jupiter's prospects. High-speed rail requires specialized bogies and couplers—products Jupiter now manufactures. Railway electrification needs advanced braking systems—capabilities acquired through Stone India. Freight optimization demands GPS-tracked, sensor-equipped smart wagons—technologies Jupiter is developing with international partners. Each transition creates upgrade cycles that multiply revenue opportunities beyond simple capacity addition.

Jupiter Wagons aims for a topline of Rs 10,000 crore and an EBITDA margin of 27% by FY27, driven by new facilities and entry into the EV truck segment. These targets appear aggressive but decompose logically. Railway wagons contribute ₹5,000 crore (10,000 units at ₹50 lakh average). EVs add ₹1,500 crore (10,000 vehicles at ₹15 lakh). Components and services provide ₹2,000 crore. Containers and commercial bodies fill the remainder. Each segment exists today—scaling rather than creating is the challenge.

International expansion possibilities multiply. Africa's railway renaissance—Kenya's SGR, Ethiopia's light rail, Nigeria's modernization—requires 50,000 wagons over five years. Southeast Asian metros—Jakarta, Manila, Bangkok—need 10,000 coaches by 2030. Jupiter's ability to manufacture at 30% lower cost than European competitors while meeting international quality standards positions them uniquely for these opportunities.

The partnership ecosystem strengthens competitive positioning. Technical collaborations with Tatravagónka (Slovakia), DAKO-CZ (Czech Republic), Kovis (Slovenia), Talleres Alegria (Spain), and CAF (Spain) provide technology access without development costs. These aren't passive licensing arrangements but active partnerships—joint product development, shared manufacturing, combined bidding for international tenders. Each partnership opens doors that would take decades to unlock independently.

Key metrics to watch reveal execution progress. Monthly wagon production run rate—target 1,000 by FY26 versus current 700. Order book composition—diversification beyond railways toward private sector. Working capital days—improvement from current 70 toward 60 days. EBITDA margins—progression toward 15% despite mix changes. Each metric provides early warning of thesis confirmation or deterioration.

The biggest risks require constant monitoring. China's infrastructure export ambitions could flood markets with subsidized alternatives. Technology disruption—hyperloop, autonomous trucks, drone delivery—could obsolete traditional transportation. Financial crisis triggering government austerity would devastate capital-intensive manufacturers. Climate change regulations might disadvantage certain product lines. These aren't probable but possible—tail risks that demand contingency planning.

Yet the opportunities overshadow risks for those with appropriate time horizons. India's demographic dividend—400 million people entering middle class by 2030—guarantees sustained infrastructure demand. Urbanization—200 million rural-to-urban migrants—necessitates mass transit expansion. Manufacturing renaissance—PLI schemes, China+1 strategies—requires logistics capacity multiplication. These are structural trends immune to short-term volatility.

Jupiter's cultural evolution enables continued transformation. The engineering excellence inherited from CEBBCO's defense heritage. The entrepreneurial energy from startup acquisitions like Log9. The operational discipline from railway manufacturing. The innovation mindset from EV development. This cultural synthesis—rare in traditional manufacturing—provides the adaptive capacity essential for navigating discontinuous change.

Management's capital allocation framework demonstrates maturity. Growth investments in capacity and technology. Productivity investments in automation and digitalization. Strategic investments in partnerships and acquisitions. But also returning capital—dividends when appropriate, buybacks if undervalued. This balanced approach suggests confidence in cash generation beyond growth requirements.

The competitive dynamics increasingly favor Jupiter's integrated model. Pure-play wagon manufacturers struggle with component availability. Component suppliers lack system integration capabilities. New entrants face certification barriers. Foreign competitors carry cost disadvantages. Jupiter's positioning at the intersection of capability and opportunity creates sustainable competitive advantages.

ESG considerations, often overlooked in industrial companies, provide additional tailwind. Railway transportation emits 75% less CO2 than road freight. Electric vehicles eliminate local emissions entirely. Modal shift from road to rail aligns with climate commitments. Jupiter enables rather than resists the green transition—a positioning that attracts ESG-focused capital and government support.

The institutional ownership evolution validates the transformation. From zero institutional ownership pre-listing to 8% foreign institutional and 12% domestic institutional today. Sophisticated investors recognize the structural growth story beyond cyclical volatility. As execution continues and complexity resolves, institutional ownership should reach 30-35%—typical for quality mid-caps—providing valuation support.

The final reflection returns to that Jabalpur workshop where CEBBCO began in 1979. What started as small-scale metal fabrication has evolved into integrated mobility solutions. The next chapter—technology-enabled, internationally competitive, sustainably focused—is being written now. For investors willing to partner through this transformation, Jupiter Wagons offers not just returns but participation in building the infrastructure foundation of India's economic emergence.

The road ahead stretches long, with inevitable bumps and detours. But the destination appears clear: a company that helps move a nation forward, literally and figuratively. In the grand narrative of India's development, Jupiter Wagons claims a essential role—not as protagonist but as crucial infrastructure, the rails on which progress runs.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube