Jubilant FoodWorks: The Master Franchisee That Built India's Pizza Empire

I. Introduction & Episode Roadmap

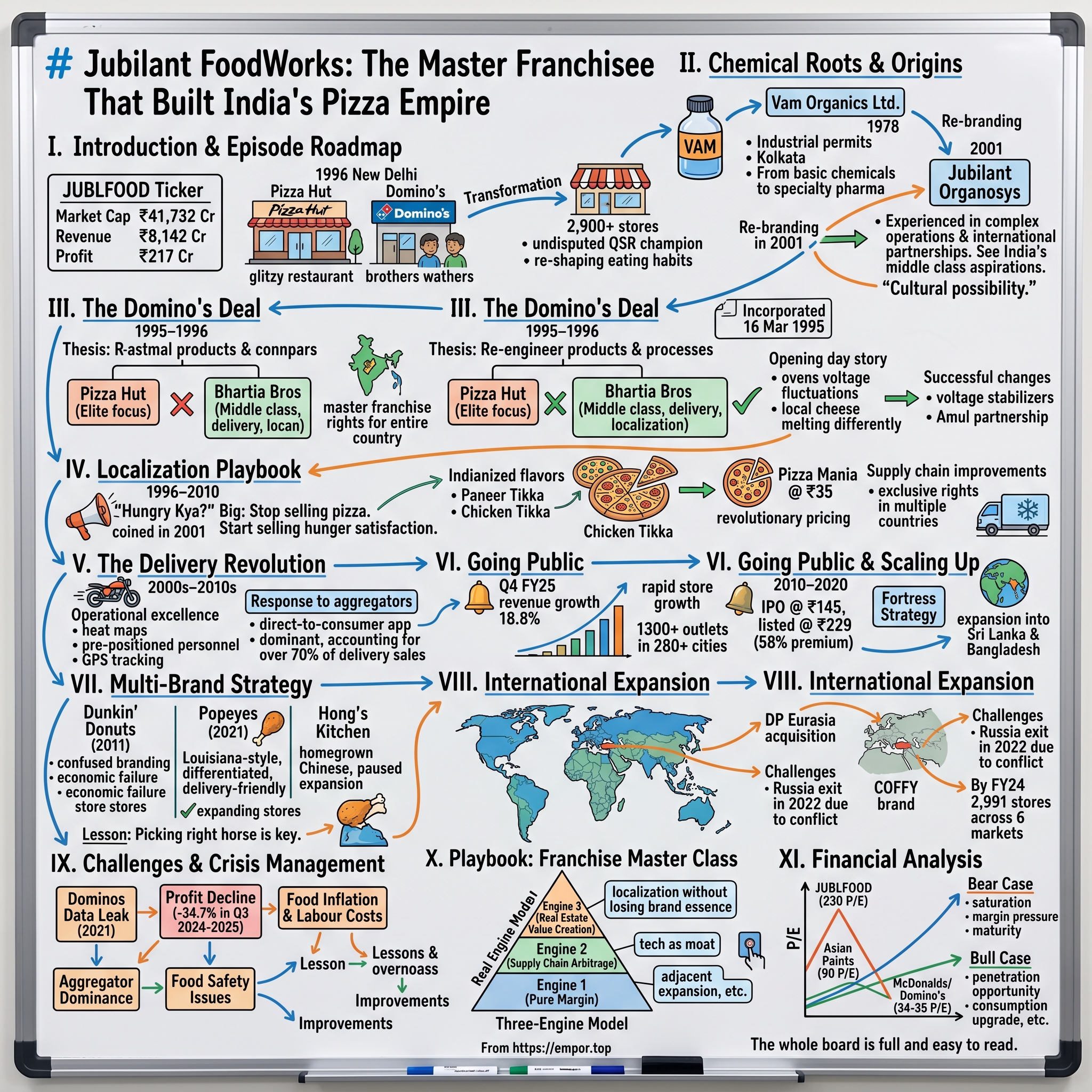

Picture this: It's 1996 in New Delhi. Pizza Hut has just opened its glitzy restaurant in Connaught Place, complete with salad bars and table service. Meanwhile, in a modest corner of the same city, two brothers from a chemical manufacturing background are nervously watching customers trickle into India's first Domino's Pizza outlet. Nobody—not even the brothers themselves—could have imagined that their venture would grow into a ₹41,732 crore behemoth that would fundamentally reshape how 1.4 billion Indians think about fast food. Today, Jubilant FoodWorks stands as India's undisputed quick-service restaurant (QSR) champion. With a market capitalization of ₹41,732 crore, revenue of ₹8,142 crore, and profit of ₹217 crore, it's not just numbers that tell the story—it's the transformation of Indian eating habits. The company that introduced the concept of home-delivered hot pizza has become one of India's largest food service companies, holding master franchise rights for Domino's Pizza and Dunkin' Donuts, and operating Popeyes.

But here's what makes this story remarkable: The protagonists aren't restaurant veterans or hospitality magnates. They're chemical engineers who spotted an opportunity where others saw cultural impossibility. Their journey from vinyl acetate monomer to mozzarella cheese is a masterclass in franchise management, localization strategy, and the patient art of building consumer habits in emerging markets.

This is the story of how Shyam Sundar Bhartia and Hari Bhartia turned a single outlet in Delhi into a 2,900+ store empire spanning six countries. It's about betting on India's middle class before the middle class knew it wanted pizza. It's about creating a supply chain for a product that didn't exist in Indian consciousness. And ultimately, it's about the power of the master franchise model—a business structure that allowed entrepreneurs to build billion-dollar companies on the shoulders of global brands while maintaining the agility to innovate locally.

The key themes we'll explore mirror the company's evolution: from chemical roots to food service empire, the art of localization without losing brand essence, building technology moats in a traditionally low-tech industry, and the delicate dance of multi-brand portfolio management. We'll dissect how Jubilant cracked the code that eluded Pizza Hut, why their 30-minute delivery promise became cultural shorthand for reliability, and what their recent struggles reveal about the limits of the franchise model in the age of food aggregators.

II. Jubilant Bhartia Group Origins & The Chemical Roots

The year was 1978. India was still a decade away from economic liberalization, operating under the suffocating embrace of the License Raj. In this environment of industrial permits and production quotas, two brothers in their twenties made a counterintuitive move. While their peers chased secure government jobs or traditional trading businesses, Shyam Sundar and Hari Bhartia decided to manufacture chemicals.

The brothers came from modest merchant stock. Their father, Mohan Lal Bhartia, ran a steel wire trading business in Kolkata, supplementing it with what seemed like an odd side venture—importing and selling Rolex watches. It was this combination of industrial goods and luxury retail that would unconsciously shape the brothers' future approach to business: technical excellence married to consumer aspiration.

On June 21, 1978, armed with seed capital from their father's trading profits, the brothers incorporated Vam Organics Limited. The company name wasn't born from creativity but from acronym pragmatism—VAM stood for vinyl acetate monomer, the chemical compound they planned to manufacture. This naming convention—functional, direct, unpretentious—would characterize their business approach for decades.

The 1980s were grinding years. While India's software pioneers were beginning to tap into global markets, the Bhartia brothers were dealing with the unglamorous realities of chemical manufacturing: environmental clearances, industrial safety protocols, volatile raw material prices. But they were also learning something crucial—how to operate in highly regulated environments, manage complex supply chains, and maintain quality standards that met international specifications.

The game-changer came with India's economic liberalization in 1991. Suddenly, the protective walls around Indian industry crumbled. Multinationals could enter, imports became easier, and critically for Vam Organics, Indian companies could now aspire to become suppliers to global pharmaceutical and chemical giants. The company that had survived on domestic contracts began winning international ones, moving up the value chain from basic chemicals to specialty pharmaceuticals.

By 2001, the transformation was complete enough to warrant a rebranding. Vam Organics became Jubilant Organosys, marking not just a name change but a shift in ambition. "Jubilant" captured the optimism of post-liberalization India, while "Organosys" signaled systematic, organized growth. The company was no longer just a chemical manufacturer—it was becoming a conglomerate.

But why would chemical engineers venture into food service? The answer lay in a confluence of factors that the brothers observed in the mid-1990s. First, their chemical business had generated substantial cash flows and, more importantly, given them experience in managing complex operations. Second, they had learned how to partner with international companies, understanding the nuances of technology transfer, brand licensing, and quality control. Third, and perhaps most importantly, they saw what others missed: India's middle class wasn't just growing in numbers but in aspirations.

The brothers had a thesis that would prove prescient. They believed that as Indians traveled more, watched more international content, and integrated with the global economy, their consumption patterns would converge with global norms—but with distinctly Indian characteristics. Food, being both universal and deeply cultural, represented the perfect testing ground for this hypothesis.

A chance encounter in 1994 would crystallize this thinking. A friend who held pizza franchises in Southeast Asia mentioned that Domino's was looking for an India partner. Pizza Hut had just entered India with much fanfare, opening a 140-seat restaurant in Bangalore. The conventional wisdom was clear: Indians would eat pizza occasionally, in upscale restaurants, as an exotic experience.

The Bhartia brothers saw it differently. They didn't see pizza as a luxury product to be consumed in restaurants. They saw it as convenience food that could be delivered to homes—if they could crack the price, taste, and logistics equation. Their chemical business had taught them that success came not from copying existing models but from re-engineering products and processes for local conditions.

The negotiation with Domino's International would test everything they had learned about international partnerships. But unlike their chemical joint ventures, where technology transfer was paramount, this deal would require something more complex: cultural translation. They weren't just licensing a brand; they were importing a business model that had never been tested in a market where cheese was an acquired taste, ovens were rare, and home delivery meant the neighborhood grocery store sending a boy on a bicycle.

The brothers' approach to the negotiation revealed their strategic thinking. While Pizza Hut's partners were focused on real estate and restaurant ambiance, the Bhartias were asking different questions: Could they source mozzarella locally? What would delivery logistics look like in cities without proper addressing systems? How could they price a pizza to compete not with Western restaurants but with local fast food?

This chemical engineering mindset—breaking down complex problems into components, optimizing each element, then reassembling them into something new—would become the foundation of their food service empire. They weren't trying to bring American pizza to India; they were using American pizza as a starting point to create something uniquely Indian.

III. The Domino's Deal: Getting the Master Franchise (1995–1996)

The conference room at the Oberoi Hotel in New Delhi had seen many business negotiations, but perhaps none as culturally ambitious as the one unfolding in late 1994. On one side sat executives from Domino's International, armed with binders full of operational standards, temperature specifications, and time-motion studies. On the other, the Bhartia brothers, who had never operated a restaurant but came prepared with something more valuable: a thesis on how to make pizza Indian.

Tom Monaghan's Domino's had built its empire on a simple promise: hot pizza delivered in 30 minutes or less. By 1994, the company had conquered America and was expanding internationally. But India presented unique challenges. The Domino's executives had already met with several potential partners—established restaurant groups, hotel chains, even Bollywood celebrities looking to diversify. Each pitch followed the same script: We'll open restaurants in five-star hotels and upscale malls, targeting the elite who've traveled abroad.

The Bhartias' pitch was radically different. "Forget the elite," they argued. "Target the emerging middle class. Forget dine-in restaurants. Focus on delivery. Forget authentic American pizza. Create Indian flavors." The Domino's executives were intrigued but skeptical. Every other international market had succeeded by maintaining brand standards. Why would India be different?

To answer this, Shyam Sundar Bhartia pulled out a simple chart. It showed the price of a Pizza Hut meal (₹400-500 per person) versus the average middle-class family's monthly eating-out budget (₹500-1000). "At these prices," he explained, "pizza will remain a quarterly indulgence. We need to make it a weekly habit." His target: ₹100 per pizza, delivered hot to the customer's door. The negotiation intensified as Domino's executives probed deeper. How would they maintain the 30-minute delivery promise in Indian traffic? The brothers had already mapped delivery zones in Delhi, calculating that with strategically placed stores and motorcycle delivery (instead of cars), they could actually beat American delivery times. What about vegetarian requirements? They'd already identified local suppliers who could provide vegetarian cheese and planned separate preparation areas—something even Domino's US hadn't implemented.

But the masterstroke came when discussing franchise economics. Most international brands entering India demanded high upfront fees and strict royalty structures. The Bhartias proposed a different model: lower initial fees but a commitment to aggressive expansion. They wanted master franchise rights not just for Delhi or North India, but eventually the entire country. More audaciously, they wanted the flexibility to modify products for local tastes while maintaining quality standards.

On the recommendation of a friend who owned other foreign pizza licences, Shyam Sunder Bhartia and Hari Bhartia of the Jubilant Bhartia Group entered into a master franchise partnership with Domino's Pizza. Domino's Pizza India Private Ltd. was incorporated on 16 March 1995, and began operations in 1996.

The deal structure that emerged was unique in Domino's international operations. The Bhartias would pay a royalty of 3% of sales (versus the standard 5.5%) but commit to opening 100 stores within five years—an aggressive target considering Pizza Hut had managed only three stores in its first year. They also negotiated unprecedented menu flexibility, with the understanding that at least 50% of offerings could be localized.

The first Domino's Pizza in India opened in New Delhi in January 1996. The location choice was deliberate—not the upscale markets of South Delhi where Pizza Hut had positioned itself, but a middle-class neighborhood where the real volume lay. The 1,200-square-foot store was modest by restaurant standards but revolutionary in concept: 70% of the space was dedicated to the kitchen and delivery operations, with only a small counter for walk-in customers.

Opening day was a disaster that would become company legend. The ovens imported from Italy couldn't handle the voltage fluctuations common in Delhi. The cheese, sourced from a local dairy, melted differently than expected. Most critically, the delivery boys—hired from local restaurants—didn't understand the urgency of the 30-minute promise. The first day saw exactly 24 pizzas sold, most to friends and family.

But failure taught valuable lessons. Within weeks, the company installed voltage stabilizers and backup generators—infrastructure that would become standard in all future stores. They partnered with Amul, India's dairy cooperative giant, to develop a special mozzarella blend that could withstand Indian heat and humidity. Most importantly, they began training delivery personnel not as "boys" but as "delivery experts," with uniforms, safety gear, and performance incentives.

The competition with Pizza Hut was fascinating to watch. While Pizza Hut focused on creating an "American dining experience" with salad bars, large restaurants, and even wine service in some locations, Domino's quietly built a delivery infrastructure. By the end of 1996, Pizza Hut had five elegant restaurants and negligible delivery sales. Domino's had three modest stores but was delivering 100+ pizzas daily.

The real validation came from an unexpected source. In late 1996, a senior executive from Domino's International made an unannounced visit to the Delhi store. He ordered a pizza at 8:47 PM—peak traffic time in one of the world's most congested cities. The pizza arrived at his hotel room at 9:11 PM—24 minutes. When he bit into it, expecting standard pepperoni, he tasted something different: tandoori chicken with Indian spices. Instead of being upset about the menu deviation, he was intrigued. This wasn't American pizza forced onto Indian plates; this was pizza reimagined for Indian palates.

The executive's report back to Domino's headquarters would prove pivotal. He recommended not just continuing but accelerating the India experiment. The phrase he used would become prophetic: "They're not trying to make Indians eat pizza. They're making pizza Indian."

By early 1997, the foundation was set. The Bhartias had their master franchise, a proven (if still small) operating model, and most importantly, validation that their localization strategy worked. But the real challenge lay ahead: scaling from three stores to 300, from one city to dozens, from experimental venture to market dominance.

IV. The Localization Playbook: Making Pizza Indian (1996–2010)

The year 1997 began with a stark reality check. Despite initial optimism, Domino's India was hemorrhaging money. The average Indian customer visited once every three months, treating pizza as an exotic indulgence rather than regular food. At a management meeting in February, a junior marketing executive presented a devastating insight: In customer interviews, pizza was consistently described as "party food"—something you ordered for special occasions, like birthday cake. The business model required pizza to be "everyday food." The gap seemed unbridgeable. The solution came from an unlikely source. A young brand manager, fresh from selling soaps at Hindustan Lever, made a radical proposal: "Stop selling pizza. Start selling hunger satisfaction." This insight would birth one of Indian advertising's most memorable campaigns.

In 2001, when the brand was launched nationally, the tagline, 'Hungry Kya?', was coined. The genius of "Hungry Kya?" wasn't in its catchiness but in its cultural resonance. In Hindi, it literally meant "Are you hungry?" but the colloquial usage made it feel like a friend asking if you wanted to grab a bite. Domino's came out with an innovative advertisement campaign in 2001. It was titled the "Hungry Kya?" campaign that went on to create a legacy and something which can be recalled even today.

The campaign's execution was deliberately provocative. One ad showed a pregnant woman's baby kicking; she calms it by eating pizza. Another featured a sultry woman asking a leering man "Hungry Kya?"—cleverly conflating desire with appetite. These weren't selling Italian cuisine; they were positioning pizza as the answer to a basic human need.

But advertising alone wouldn't crack the code. The real innovation happened in the kitchen. When Jubilant's R&D team analyzed why Indians weren't repeat customers, they discovered something Pizza Hut had missed: Indians didn't dislike pizza; they disliked Western pizza. The cheese was too bland, the toppings too alien, the base too thick. Indians wanted spice, familiarity, and value.

The product innovation that followed was systematic and radical. First came the vegetarian revolution. While Domino's USA offered two vegetarian options, Domino's India launched with eight, eventually expanding to over 20. But these weren't token vegetables thrown on cheese—they were careful recreations of Indian flavors. The Peppy Paneer used the cottage cheese beloved in North Indian cuisine. The Deluxe Veggie mimicked the vegetable preparations found in Indian homes.

The masterstroke was the Indian Pizza range. Chicken Tikka Pizza took the flavors of tandoori chicken—a dish every Indian recognized—and married it with the pizza format. Keema Do Pyaaza adapted a Mughlai mutton dish. The spice levels were calibrated to Indian palates, with extra oregano and chili flakes becoming standard accompaniments.

Pricing strategy was equally revolutionary. In 2006, recognizing that the ₹200+ price point limited their market, Jubilant launched Pizza Mania at ₹35-45—cheaper than a movie ticket. Domino's launched the Fun Meal pizza range at Rs 45 in 2006 and then the Pizza Mania range in 2008 at Rs 35. This wasn't just discounting; it was a separate product line with smaller sizes, simpler toppings, but the same quality standards. Suddenly, college students could afford pizza twice a week instead of once a month.

The supply chain transformation was less visible but equally critical. The company is a leading player in the pizza segment, holding exclusive rights to operate Domino's Pizza outlets in India, Sri Lanka, Bangladesh, Nepal, Turkey, Azerbaijan, and Georgia. Unlike the US, where Domino's could rely on established food service suppliers, India required building from scratch. Jubilant created a cold chain network when none existed. They partnered with local farmers to grow specific varieties of vegetables. They worked with Amul to develop a mozzarella that maintained stretch at Indian temperatures.

The commissary system they developed was unique. Instead of fully finished products, they created a hub-and-spoke model where dough and sauce were centrally prepared but vegetables were cut fresh at stores. This balanced quality control with local freshness—critical for Indian consumers who were used to buying vegetables daily.

Store design evolved to match Indian conditions. Kitchens were configured for vegetarian-non-vegetarian separation, with color-coded equipment and separate preparation areas. Delivery bags were insulated for Indian weather—maintaining heat in air-conditioned malls and preventing spoilage in 45-degree summer heat.

The technology adoption, though less sophisticated than today's systems, was pioneering for its time. In 2001, when most Indians had never ordered food by phone, The launch of 'Hungry Kya?' campaign coincided with Domino's tie-up with Mahanagar Telephones Nigam Ltd. (MTNL) for the 'Hunger Helpline'. The helpline enabled the customers to dial a toll-free number (1600-111-123) from any place in India. This system automatically routed calls to the nearest outlet—revolutionary in an era before smartphones and GPS.

Employee training became a differentiator. While competitors hired delivery "boys" casually, Domino's created "Delivery Experts"—uniformed, trained, and incentivized based on delivery times and customer satisfaction. They weren't just delivering food; they were brand ambassadors entering customers' homes.

By 2010, the transformation was complete. What started as 24 pizzas sold on opening day had become a 400+ store network generating over ₹600 crore in revenue. More importantly, pizza had transformed from exotic indulgence to comfort food. The phrase "Let's order pizza" had entered the Indian lexicon.

The metrics told the story: average order frequency increased from once per quarter to twice per month. Customer retention rates exceeded 70%. Most remarkably, 65% of sales came from vegetarian pizzas—unheard of in any other Domino's market globally.

The localization playbook would become the template not just for Jubilant's future expansion but for every international QSR brand entering India. The lesson was clear: success in emerging markets didn't come from imposing global products but from using global frameworks to create local solutions. As one Domino's International executive later remarked, "We went to India to teach them about pizza. Instead, they taught us about adaptation."

V. The Delivery Revolution & Technology Play (2000s–2010s)

At 7:23 PM on a Friday evening in Mumbai, 2008, a Domino's call center received an order that would become company folklore. The customer lived on the 23rd floor of a high-rise in Worli, notorious for its single, slow elevator. Traffic was at its peak monsoon worst. The store manager looked at the address and shook his head—impossible in 30 minutes. But the delivery expert, a young man named Rajesh, grabbed the order and said, "Give me 22 minutes." He made it in 21, having memorized that the building's service elevator was faster and that taking a specific back lane cut seven minutes from the route. This wasn't just delivery; it was urban warfare logistics.

The 30-minute delivery promise, inherited from Domino's global playbook, took on mythical proportions in India. While Domino's USA had discontinued the guarantee in 1993 after safety concerns, India not only maintained it but made it the cornerstone of their brand identity. The operational excellence required to deliver this promise in Indian conditions—chaotic traffic, missing street signs, monsoon floods—would forge capabilities that became Jubilant's most powerful moat.

The delivery infrastructure that emerged was part military operation, part technology platform. Each store maintained a "heat map" showing delivery times to every neighborhood within their radius. Delivery experts weren't assigned randomly but matched to routes they knew intimately. During peak hours, stores pre-positioned delivery personnel at strategic intersections. Some Mumbai stores even maintained boats during monsoon season to reach flooded areas. The technology evolution began modestly but accelerated rapidly. In 2005, Jubilant launched one of India's first food ordering websites—primitive by today's standards but revolutionary when most Indians had never bought anything online. By 2010, they had mobile apps before most Indians had smartphones, betting correctly on the coming mobile revolution.

But the real technology innovation happened behind the scenes. Jubilant built India's first integrated restaurant management system, connecting ordering, kitchen display, inventory, and delivery dispatch. When a customer called, their phone number triggered their order history, preferred items, and delivery address. The system calculated preparation time, assigned the optimal delivery route, and tracked performance—all in real-time.

In Q4 FY25, Domino's India witnessed a revenue growth of 18.8 per cent, led by strong order growth of 24.6 per cent. The brand recorded a like-for-like (LFL) growth of 12.1 per cent, driven by a delivery LFL growth of 21.9 per cent. The delivery channel revenue for Domino's India was up by 27.1 per cent, with the delivery channel mix now at 72.9 per cent.

The rise of food aggregators—Swiggy and Zomato—in the 2010s presented an existential challenge. These platforms promised customers choice and convenience while taking 20-25% commissions from restaurants. Many QSR chains capitulated, becoming dependent on aggregators for customer acquisition.

Jubilant's response was contrarian and brilliant. Instead of fighting aggregators or surrendering to them, they built a parallel direct-to-consumer infrastructure. They invested heavily in their own app and website, offering exclusive deals not available on aggregator platforms. They maintained presence on Swiggy and Zomato but ensured direct orders remained more profitable through smart pricing and promotions.

The data advantage this created was enormous. While competitors saw customers through the aggregator lens, Jubilant knew everything: order patterns, flavor preferences, price sensitivity. They could predict demand spikes during cricket matches, adjust inventory before festivals, and personalize offers at individual level.

The franchisee model within India added another layer of complexity and capability. Unlike the US where most Domino's are franchised, Jubilant operated a hybrid model—company-owned stores in metros and tier-1 cities, franchised stores in smaller markets. This allowed rapid expansion while maintaining quality control in crucial markets.

The franchise structure was unique. Instead of traditional area development agreements, Jubilant created a "hub and spoke" model. A company-owned commissary would supply multiple franchised stores, ensuring quality while allowing local entrepreneurs to focus on operations and customer service. Franchisees were selected not just for capital but for local market knowledge—often successful local businesspeople who understood their communities.

Training became almost militaristic in its intensity. Every delivery expert underwent a two-week program covering not just delivery logistics but customer psychology, conflict resolution, and brand values. They learned to read addresses in multiple scripts, navigate without GPS, and handle everything from angry customers to aggressive dogs.

The numbers validated the strategy. By March 31, 2025, the company had opened 52 new stores and entered nine new cities, reaching a network of 2,179 stores across 475 cities. Delivery times averaged 22 minutes in metros, 25 minutes in tier-2 cities. Customer satisfaction scores consistently exceeded 90%. Most impressively, direct orders through Domino's own channels accounted for over 70% of delivery sales—far higher than any competitor.

The operational metrics were even more impressive. Each store could handle 300+ orders during peak hours. Delivery experts averaged 6-8 deliveries per shift, with top performers managing 12. The company maintained a delivery fleet of over 20,000 motorcycles, each equipped with insulated bags designed specifically for Indian conditions.

Innovation continued relentlessly. Domino's introduced GPS tracking before Uber made it ubiquitous. They launched voice ordering in regional languages. They created a "pizza tracker" that showed customers exactly where their order was in the preparation process. Each innovation was copied by competitors, but Jubilant always stayed one step ahead.

The COVID-19 pandemic became an unexpected validation of these investments. While dine-in restaurants struggled, Domino's delivery infrastructure seamlessly handled the surge in demand. They introduced "zero-contact delivery" within days of the first lockdown. Their technology platform, built over two decades, proved more resilient than newer, venture-funded competitors.

By 2020, what started as boys on bicycles had evolved into one of India's most sophisticated logistics operations. The company that had struggled to deliver 24 pizzas on opening day was now delivering over 3 million pizzas monthly. The delivery revolution wasn't just about speed—it was about building capabilities that would become the foundation for everything that followed: new brands, new markets, and new possibilities.

VI. Going Public & Scaling Up (2010–2020)

February 8, 2010. The Bombay Stock Exchange floor buzzed with unusual energy. Jubilant FoodWorks was going public at ₹145 per share, and the IPO had been oversubscribed 30 times. Institutional investors who had initially scoffed at "a pizza delivery company" were scrambling for allocations. Shyam Sundar Bhartia, ringing the opening bell, allowed himself a brief smile. The chemical engineer who had started making pizzas as a side venture was now heading a ₹3,000 crore public company. The IPO had been priced at ₹145 per share and listed at ₹229—a 58% premium that vindicated years of patient building. Jubilant Foodworks IPO listed at a listing price of 229.00 against the offer price of 145.00. The company went public in 2010 with IPO price of Rs 145 and it currently trades at around Rs 2900 with all-time high of around Rs 3200.

The IPO timing was perfect. India's consumption story was gaining global attention. The Commonwealth Games were coming to Delhi. The middle class was exploding. Most importantly, Jubilant had proven that QSR could work in India—not as an occasional indulgence but as regular consumption.

But going public brought new challenges. The market demanded quarter-on-quarter growth. Analysts questioned everything: Why were margins lower than global QSR players? Could the 30-minute promise scale? What about competition from McDonald's aggressive expansion?

The post-IPO strategy was ambitious and calculated. First, accelerate store expansion. The target: 500 stores by 2012, 1000 by 2015. This wasn't just about numbers—it was about achieving density before competitors could establish footholds. The company adopted a "fortress strategy" in key cities, opening multiple stores to create delivery networks so dense that competitors couldn't match service levels.

Second, expand beyond metros. While Pizza Hut focused on tier-1 cities, Jubilant began entering tier-2 and tier-3 markets. Cities like Nashik, Surat, and Coimbatore got Domino's before they got McDonald's. The thesis was simple: create pizza habits before consumers knew alternatives existed.

The execution was remarkable. The first Domino's Pizza in India opened in New Delhi in January 1996. By 2015, the company had exceeded its target. Now, the numbers above show why Domino's is the largest QSR chain in India. It has 1300+ outlets spread over 280+ cities. This shows that the company has not only grown in metro cities but has also expanded its presence in tier 2 and tier 3 towns of the country.

International expansion began cautiously but strategically. Jubilant FoodWorks Lanka Pvt. Limited operates Domino's Pizza outlets in Sri Lanka. The first Domino's outlet opened in Colombo in February 2011. Sri Lanka offered similar dynamics to India—price-conscious consumers, vegetarian preferences, developing infrastructure. The learnings from India translated directly.

Bangladesh followed a different model. Jubilant Golden Harvest Ltd., a wholly owned subsidiary of Jubilant FoodWorks, operates Domino's Pizza outlets in Bangladesh. Jubilant Golden Harvest Ltd. was established in early 2019 with Jubilant holding a 51% stake, and Bangladeshi company Golden Harvest Group holding the remaining 49%. The first Domino's Pizza outlet opened in Dhaka in February 2019.

Leadership transition marked a crucial evolution. The founders, recognizing that scaling required professional management, began recruiting senior executives from FMCG and retail. Ajay Kaul, who joined as CEO in 2005, brought discipline from Hindustan Lever. His successor, Pratik Pota, came from the telecom industry, bringing technology expertise crucial for the digital age.

The professionalization wasn't without friction. Early employees, used to entrepreneurial decision-making, struggled with corporate processes. Store managers who had operated like independent businessowners now reported through multiple layers. But the systems that emerged—standardized training, performance metrics, career progression paths—enabled scale that entrepreneurial chaos couldn't achieve.

Financial discipline became a hallmark. Despite pressure for growth, the company maintained positive cash flows. Store-level economics were scrutinized obsessively. New stores had to achieve profitability within 12 months or face closure. This discipline meant that while competitors opened flashy stores that bled money, Jubilant's network generated consistent returns.

The same-store sales growth (SSG) metric became the north star. While new stores drove top-line growth, SSG indicated health. Jubilant consistently delivered 15-20% SSG through the early 2010s—extraordinary in global QSR terms. This came from a combination of ticket size growth (customers ordering more), frequency increase (ordering more often), and customer base expansion (new customers trying pizza).

Technology investments accelerated post-IPO. By 2015, over 30% of orders came through digital channels—mobile apps and websites. This wasn't just convenience; it was data. Digital customers ordered 20% more, ordered 30% more frequently, and provided invaluable preference data.

Supply chain sophistication reached new levels. The company built mega-commissaries that could service 100+ stores. They backward-integrated into sauce manufacturing, dough production, and even farming contracts for vegetables. The vertical integration provided quality control, cost advantages, and importantly, the ability to maintain consistency across an exploding store network.

Competition intensified through the decade. McDonald's accelerated expansion. Burger King entered India. Local players like Faaso's and Box8 emerged. But Jubilant's first-mover advantage in delivery, combined with technology and supply chain moats, proved difficult to overcome.

By 2020, the transformation was complete. The company that went public with 200 stores operated over 1,300. Revenue had grown from ₹500 crore to over ₹4,000 crore. More remarkably, they had maintained market leadership despite intense competition. The company that had started as a franchisee had become a case study in emerging market QSR operations.

VII. The Multi-Brand Strategy: Beyond Domino's

The boardroom was divided. It was late 2010, and Jubilant's leadership faced their biggest strategic decision since acquiring the Domino's franchise. With Domino's crossing 300 stores and generating robust cash flows, the question wasn't whether to expand beyond pizza, but how. One camp argued for launching their own Indian QSR brand. Another pushed for acquiring local chains. But Hari Bhartia, drawing from their chemical business experience, made a different argument: "We're not in the food business. We're in the franchise excellence business. "This philosophy would guide their multi-brand journey. On 24 February 2011, Jubilant FoodWorks signed a master franchise agreement with American coffeehouse chain Dunkin' Donuts to operate the brand in India. The master franchise agreement called for Jubilant FoodWorks to develop, sub-franchise, and operate more than 500 Dunkin' Donuts restaurants throughout India over the next 15 years.

The Dunkin' opportunity seemed perfect. Coffee consumption was exploding in India, driven by Café Coffee Day's pioneering work. The breakfast category was nascent but growing. Most importantly, Dunkin' offered what Domino's couldn't—a sit-down experience, a social space, a different daypart (morning versus evening).

Jubilant FoodWorks opened India's first Dunkin' Donuts outlet in Connaught Place, New Delhi in April 2012. The location was symbolic—the heart of Delhi, where Domino's had started 16 years earlier. But the execution revealed the first cracks in the multi-brand strategy.

The localization that had worked brilliantly for Domino's proved more complex for Dunkin'. Indians didn't eat donuts for breakfast—they ate parathas, idlis, poha. Coffee meant either instant Nescafe at home or expensive cappuccinos at cafés—not the American filter coffee Dunkin' was known for. The brand positioning was confused: Was it a donut shop? A coffee place? A breakfast restaurant?

Jubilant tried everything. They added Indian breakfast items—samosas, sandwiches, even burgers. They positioned it as "Dunkin' Donuts & More," trying to be all things to all people. They opened 77 stores at peak, burning cash in prime real estate locations. But the economics never worked. Average store sales were a fraction of Domino's. Customer frequency was low. The breakfast opportunity they'd bet on didn't materialize—Indians still preferred eating breakfast at home.

By 2018, reality hit hard. Jubilant FoodWorks eventually brought down the number of stores to 37. They had shut their most unprofitable stores, cut back on restaurant operating costs and overheads. The dream of 500 stores had collapsed to barely 20 by 2023. Jubilant FoodWorks operates 21 Dunkin' Donuts outlets across 6 Indian cities as of 30 June 2023.

But failure taught valuable lessons. The company realized that not every global brand could be localized successfully. Some categories had cultural barriers too high to overcome. Most importantly, they learned that their core competency wasn't just operating franchises—it was specifically delivery-focused, high-frequency food. The Popeyes opportunity emerged from lessons learned. On 24 March 2021, Jubilant FoodWorks announced that it had entered into a master franchise and development agreement with Restaurant Brands International to operate Popeyes restaurants in India, Bangladesh, Nepal and Bhutan. The company opened India's first Popeyes outlet at Koramangala, Bangalore on 20 January 2022.

This time, the approach was different. Chicken, unlike donuts, was already a massive category in India. KFC had proven the market existed. Popeyes offered differentiation—Louisiana-style fried chicken versus KFC's original recipe. More importantly, it was a delivery-friendly product, aligning with Jubilant's core strength.

The execution showed institutional learning. Instead of rapid nationwide expansion, Popeyes followed a cluster approach—saturating Bangalore before moving to Chennai, building density before breadth. Popeyes made its debut in India with the opening of its first restaurant in Bengaluru in January 2022, followed by rapid expansion to 12 restaurants in Bengaluru.

The menu localization was more nuanced. While maintaining signature items like the chicken sandwich, they added Indian flavors—Sweet Chilli, Smoky Pepper. Critically, they created a completely separate vegetarian kitchen, learning from the challenges Domino's had faced with vegetarian customers' concerns about cross-contamination.

Early results were promising. Jubilant FoodWorks is focusing on expanding its Popeyes and Domino's brands, with plans to open 30-50 Popeyes stores annually and a target of ₹1,000 crore revenue for Popeyes. The brand's average daily orders were reportedly higher than Domino's in comparable locations.

The homegrown brand experiments reflected both ambition and pragmatism. The company launched its first homegrown brand called Hong's Kitchen, offering fast casual Chinese dining, with the first restaurant opening at Eros Mall in Gurugram on 13 March 2019. Chinese food, like pizza, had been successfully Indianized. The casual dining format targeted a different occasion than Domino's quick service.

But Hong's Kitchen struggled with identity. Was it competing with local Chinese restaurants or trying to create a new category? After opening 15 stores, expansion slowed. The company has paused expansion of Dunkin and Hongs Kitchen to reassess their value.

The multi-brand strategy revealed a fundamental truth: franchise excellence wasn't universally transferable. What worked for delivery-focused, high-frequency products didn't necessarily work for dine-in, experiential brands. The capabilities that made Jubilant brilliant at pizza—supply chain efficiency, delivery logistics, value engineering—were necessary but not sufficient for building a cafe culture or creating dining destinations.

By 2023, the portfolio strategy had crystallized. Domino's remained the cash cow, generating the vast majority of profits. Popeyes showed promise as the next growth engine. Dunkin' had been right-sized to sustainable operations. The homegrown experiments had provided valuable learning but hadn't achieved breakthrough success.

The lesson was clear: in the franchise business, picking the right horse was as important as riding skill. Jubilant had proven they could ride brilliantly—but only certain horses would win in the Indian market.

VIII. The International Expansion: Turkey & Beyond

The PowerPoint slide showed a map of Turkey overlaid with pizza consumption data. It was February 2021, and Jubilant's board was considering their boldest move yet—acquiring a stake in DP Eurasia, the master franchisee for Domino's in Turkey, Russia, Azerbaijan, and Georgia. The price tag: £24.80 million. The opportunity: entering markets with 200 million consumers. The risk: operating in geographies as complex as Turkey and as volatile as Russia.

On 19 February 2021, the company announced that it would acquire complete ownership of Netherlands-based Fides Food Systems Coöperatief UA for £24.80 million. The acquisition marks Jubilant FoodWorks entry into the Eurasian market. Fides held a 32.81% stake in DP Eurasia NV, which is the master franchisee for Dominos Pizza in Turkey, Russia, Azerbaijan and Georgia.

The Turkey opportunity was compelling for specific reasons. Unlike India where Jubilant had to create the pizza market, Turkey already had robust pizza consumption—among the highest globally per capita. The market was fragmented with local players but lacked a dominant national chain. Most intriguingly, DP Eurasia had built something Jubilant hadn't: a successful coffee chain called COFFY that competed with Starbucks.

The acquisition wasn't just about geographic expansion—it was about capability acquisition. DP Eurasia operated on a franchise model where 80% of stores were franchised versus Jubilant's 90% company-owned model in India. This capital-light approach offered lessons for Jubilant's next phase of growth. Through the acquisition of DP Eurasia, the company has entered Turkey's high-frequency coffee consumption market under the "COFFY" brand, which ranks as the 8th largest café brand in Turkey.

The execution of the acquisition revealed Jubilant's evolution as a global player. They didn't attempt a full takeover initially, instead taking a strategic stake and gradually increasing it. Jubilant announced the completion of the merger of Fides Food Systems Coeratief UA with Jubilant Foodworks Netherlands BV on 2 March 2022, and stated that it now owned 41.32% of DP Eurasia NV.

The cultural integration proved fascinating. Turkish Domino's had innovations Jubilant had never considered—pide (Turkish flatbread) pizzas, extensive breakfast menus, even pizza boats for Bosphorus delivery. The average order value was lower than India, but frequency was higher. Turkish consumers ordered pizza weekly, sometimes multiple times.

COFFY presented an unexpected opportunity. Where Dunkin' had failed in India, COFFY succeeded in Turkey by being local-first—Turkish coffee preparations, local pastries, neighborhood café ambiance. It wasn't trying to be American; it was authentically Turkish while using modern QSR operations. The lessons for Jubilant's struggles with Dunkin' were obvious and painful.

The geopolitical complexity hit almost immediately. Russia's invasion of Ukraine in 2022 created massive challenges. The Russian operations, which had been growing rapidly, faced sanctions, currency volatility, and supply chain disruptions. Jubilant had to navigate the ethical and practical challenges of operating in a sanctioned market while protecting employees and franchisees.

In FY24, it had a "record opening of 356 stores", taking JFL Group Network to 2,991 stores across six markets India, Turkey, Bangladesh, Sri Lanka, Azerbaijan and Georgia. But the growth masked underlying challenges. Managing operations across time zones, currencies, and regulatory regimes stretched management bandwidth. The company that had perfected Indian operations now had to become truly multinational.

The strategic rationale, however, remained sound. Turkey offered a playbook for other emerging markets—high-growth, young populations, rising disposable incomes, underpenetrated organized food service. The learnings from managing Turkish franchisees could be applied to accelerating franchise expansion in India.

More subtly, international expansion provided negotiating leverage with brand partners. Jubilant was no longer just an Indian operator but a multi-country platform. When negotiating with Restaurant Brands International for Popeyes or discussing terms with Domino's International, they brought scale and sophistication that commanded respect.

The financial architecture of international expansion showed sophistication. Instead of using Indian cash flows directly, Jubilant created holding structures in Netherlands and other jurisdictions, optimizing tax efficiency and regulatory compliance. They raised local currency debt in Turkey, avoiding forex risk. The CFO organization that had once managed rupee operations now dealt in lira, manat, and lari.

By 2024, the international operations contributed significantly to the narrative if not yet to profits. The company network comprises 3,316 stores across six markets – India, Turkey, Bangladesh, Sri Lanka, Azerbaijan and Georgia. The geographic diversification provided resilience—when Indian operations faced headwinds, Turkey compensated, and vice versa.

The challenges of multi-country operations forced organizational evolution. Jubilant created regional leadership structures, with country CEOs reporting to regional heads. Technology platforms had to be modified for local requirements while maintaining global standards. Supply chain strategies that worked in India's vegetarian markets had to be reimagined for meat-heavy Turkish preferences.

The Russia exit decision in 2022 demonstrated maturity. Despite significant investments and growth potential, Jubilant chose to exit rather than navigate increasing sanctions and reputational risks. The write-off was painful but the decision was swift—a sign of institutional confidence that short-term pain was acceptable for long-term positioning.

The international expansion thesis was ultimately about optionality. Turkey might become another India-sized opportunity. Azerbaijan and Georgia were small but profitable markets that provided learning laboratories. Bangladesh, despite political volatility, offered a 170-million-person market with Indian-like consumption patterns.

Most importantly, international expansion transformed Jubilant's identity. They were no longer an Indian QSR company but an emerging markets QSR platform. This positioning attracted different investors, enabled different conversations with global brands, and most importantly, provided a growth narrative beyond India's eventual saturation.

The Turkey acquisition also revealed the limits of the franchise model. While DP Eurasia had built a successful business, margins were structurally lower than India due to higher franchisee share. The challenge became balancing growth through franchising with profitability through company operations—a tension that would define Jubilant's next chapter.

IX. Challenges & Crisis Management

The WhatsApp message spread like wildfire through Mumbai's tech community in April 2021: "Don't order from Domino's. Hackers have your credit card details." Within hours, #DominosDataLeak was trending on Twitter. Jubilant FoodWorks suffered a security breach in April 2021 and hackers reportedly obtained 13 terabytes of data including 180 million order details. The crisis that unfolded would test every muscle the company had built over 25 years. The data breach was catastrophic in scope but the response revealed institutional maturity. Within hours of confirmation, Jubilant had activated a crisis management team, engaged cybersecurity experts, and begun customer communication. The CEO personally addressed the media, taking responsibility while outlining remedial measures. Credit card companies were notified immediately, limiting actual financial damage to customers.

But data breaches were just one type of crisis. The more insidious challenge came from changing consumer behavior and intensifying competition. Jubilant Foodworks Ltd's net profit fell -34.7% since last year same period to ₹42.91Cr in the Q3 2024-2025. On a quarterly growth basis, Jubilant Foodworks Ltd has generated -33.01% fall in its net profits since last 3-months.

The profit decline reflected multiple pressures converging simultaneously. Food inflation, particularly cheese and chicken prices, squeezed margins. Minimum wage increases across states raised labor costs. Most critically, the competitive landscape had fundamentally shifted. Cloud kitchens could now deliver pizza at ₹99, undercutting Domino's pricing. Aggregators promoted private labels, using data from Domino's own orders to identify opportunities.

The response required rethinking fundamental assumptions. The 30-minute delivery promise, sacred for two decades, was shortened to 20 minutes in select areas—not because customers demanded it but because competitors were getting faster. The pricing strategy shifted from premiumization to value, with aggressive offers that protected market share but compressed margins.

Food safety crises periodically erupted. In May 2016, the Centre for Science and Environment (CSE) reported that Domino's pizza bread was laced with toxins and carcinogens such as potassium bromate and potassium iodate. The response was swift—reformulation of recipes, transparent communication about ingredients, and third-party certifications. But each incident eroded trust that took years to rebuild.

The aggregator dilemma intensified yearly. Swiggy and Zomato commanded 60% of food delivery orders, wielding enormous power over restaurants. Their private label initiatives—Swiggy's "The Bowl Company," Zomato's various brands—competed directly with established QSRs while having access to their data. Jubilant's response was nuanced: maintain presence on platforms for customer acquisition while building direct channels for retention.

Competition from new-age brands proved particularly challenging. Brands like EatFit, Faasos, and Box8 didn't just compete on price—they offered healthier options, customization, and variety that resonated with younger consumers. These weren't traditional QSRs but tech companies that happened to make food, with different unit economics and investor expectations.

The COVID-19 pandemic, initially seen as an opportunity for delivery-focused businesses, revealed unexpected vulnerabilities. While delivery volumes surged, the absence of dine-in revenue exposed the importance of that higher-margin channel. Supply chain disruptions made maintaining menu variety difficult. Most challengingly, customer expectations permanently shifted—they now expected contactless delivery, detailed safety protocols, and complete transparency as standard, not premium, features.

Managing franchise relationships during crises required delicate balancing. When company-owned stores could absorb losses during promotional periods, franchisees—operating on thinner margins—struggled. Jubilant had to provide support through reduced royalties, extended payment terms, and marketing support, impacting their own profitability but preserving network integrity.

The talent crisis was less visible but equally threatening. As startups and tech companies offered astronomical salaries and stock options, Jubilant struggled to retain technical talent. The company that had pioneered food tech in India suddenly found itself competing with Swiggy and Zomato for engineers. Store-level attrition exceeded 100% annually, requiring constant recruitment and training.

Regulatory challenges multiplied. GST implementation required system overhauls. State-level regulations on plastic use forced packaging changes. Labor law reforms impacted scheduling flexibility. Each change, individually manageable, cumulatively stressed operations and margins.

The brand perception challenge was subtle but persistent. Domino's, once seen as aspirational, risked becoming commoditized. Younger consumers saw it as their parents' pizza brand—reliable but boring. Attempts at premiumization through gourmet ranges struggled against the value positioning that had defined the brand for decades.

Crisis management evolved from reactive to proactive. Jubilant established a dedicated risk management committee, scenario planning exercises, and crisis simulation drills. They built redundancy into supply chains, diversified supplier bases, and created financial buffers for unexpected shocks.

The learning from crisis was clear: market leadership provided no immunity from disruption. The capabilities that enabled dominance—operational efficiency, supply chain excellence, brand recognition—were necessary but not sufficient. Survival required constant reinvention, painful cannibalization of existing business, and acceptance that yesterday's moats could become today's anchors.

By 2024, Jubilant had survived multiple existential threats but emerged scarred. Margins were structurally lower, competition more intense, and growth more expensive. But they had also developed crisis management muscles that would prove essential for navigating an increasingly volatile future.

X. Playbook: The Franchise Master Class

If you dissect Jubilant FoodWorks' journey, you find not one business model but three interconnected engines, each generating different returns but reinforcing the others. This is the architecture that transformed a single Delhi pizza outlet into a ₹40,000+ crore enterprise.

The Three-Engine Model

Engine One: Franchise fees and royalties—the obvious revenue stream. Jubilant pays 3-5% of sales to global brands, charges sub-franchisees 5-8%. The spread seems thin until you realize it's pure margin on billions in system sales, requiring no working capital.

Engine Two: Supply chain arbitrage—the hidden gold mine. Jubilant buys mozzarella at ₹180/kg through centralized procurement, sells to franchisees at ₹220/kg. Multiply this across every ingredient, every consumable, every piece of equipment. The commissary isn't just quality control; it's a 15-20% margin business disguised as operational necessity.

Engine Three: Real estate and territory value creation—the long game. Every store opened, whether company-owned or franchised, increases territory value. Dense networks create delivery moats. Market leadership commands premium valuations. The Turkey acquisition wasn't about Turkish operations; it was about owning Domino's rights in a 85-million-person market.

Localization Without Losing Brand Essence

The localization playbook seems obvious in retrospect but required extraordinary discipline in execution. The rule: Change everything except the core. For Domino's, the core was hot pizza, delivered fast. Everything else—toppings, sizes, sides, pricing—was negotiable.

The paneer innovation illustrates this perfectly. Paneer tikka pizza sounds like bastardization to purists. But it maintains the fundamental Domino's architecture: standardized dough, consistent sauce base, predictable cooking time. The Indianization happens at the topping level, where customization doesn't disrupt operations.

Pricing localization went deeper than just being cheap. Jubilant discovered Indians have different price elasticity for different occasions. A ₹99 pizza for casual dinners, ₹500 feast for celebrations. The same customer, different contexts, 5x price differential. This insight drove menu architecture that extracted maximum value from heterogeneous consumption patterns.

Multi-Brand Portfolio Management

The portfolio strategy failures taught more than successes. Dunkin' failed because Jubilant tried to replicate the Domino's playbook in a category that required different capabilities. Coffee shops aren't about operational efficiency; they're about experience creation. The very strengths that made Jubilant brilliant at pizza—speed, standardization, delivery focus—became weaknesses in café culture.

Popeyes succeeded because it aligned with core capabilities while offering differentiation. Fried chicken travels well, has high delivery attachment, allows pricing power. More importantly, it leveraged existing infrastructure—delivery fleet, technology platform, supplier relationships—while accessing a new category.

The portfolio lesson: Adjacent expansion works only when adjacency is defined by capabilities, not categories. Jubilant could succeed in biryani delivery but would struggle with fine dining, even though both are "food service."

Technology as Competitive Advantage

Jubilant's technology edge wasn't in cutting-edge innovation but in systematic application. While competitors experimented with AI and blockchain, Jubilant focused on basics: accurate location mapping, predictive demand forecasting, dynamic delivery routing.

The customer data platform, built over two decades, became the real moat. Knowing that Customer A orders extra cheese on weekends, Customer B price-shops but values speed, Customer C orders only during cricket matches—these insights enabled personalization that aggregators couldn't match.

The technology investment philosophy: Build what's strategic, buy what's commodity. Jubilant built customer-facing applications and operational systems but bought infrastructure and tools. This focus prevented technology sprawl while maintaining differentiation.

Supply Chain as a Moat

The supply chain moat has three layers, each harder to replicate:

Layer 1: Physical infrastructure—commissaries, cold chain, distribution centers. Replicable with capital but requires massive upfront investment.

Layer 2: Supplier relationships—exclusive contracts, backward integration, quality protocols. Built over decades, these relationships ensure consistency and cost advantages.

Layer 3: Operational knowledge—understanding that Tamil Nadu stores need different spice levels than Punjab, that Mumbai's humidity requires different dough formulation than Delhi's dry heat. This tacit knowledge, encoded in processes but residing in people, is irreplicable.

Capital Allocation Framework

Jubilant's capital allocation revealed strategic clarity: - 40-50% to new store expansion (growth) - 20-25% to technology and infrastructure (capability building) - 15-20% to existing store renovation (maintenance) - 10-15% to new ventures/acquisitions (optionality) - Remainder as dividends/buybacks (shareholder returns)

This allocation remained remarkably consistent across cycles, resisting both over-expansion in good times and under-investment in bad times.

Managing the Founder-Professional Transition

The transition from founder-led to professionally-managed happened gradually but deliberately. The founders remained as strategic architects but ceded operational control. Professional CEOs brought process discipline but were given freedom to challenge sacred cows.

The key was aligning incentives. Management compensation tied to long-term metrics (5-year revenue CAGR, return on capital) not quarterly earnings. Significant equity components ensured thinking like owners, not employees. The board composition—independent directors with retail, technology, and franchise experience—provided governance without micromanagement.

The Playbook Distilled

-

Choose the right franchise: Success depends more on category selection than execution excellence. Pizza worked; donuts didn't.

-

Localize aggressively but systematically: Change everything except the core. Test, measure, scale.

-

Build infrastructure before you need it: Commissaries, technology platforms, training systems—all were built ahead of demand.

-

Density before diversity: Dominate Delhi before entering Mumbai. Saturate India before attempting Turkey.

-

Control the strategic, franchise the operational: Own the brand, technology, and supply chain. Franchise real estate and labor management.

-

Compete on different metrics: While others optimize for GMV, optimize for unit economics. While others chase customer acquisition, focus on retention.

-

Accept portfolio failures: Not every brand will work. Kill failures quickly, double down on winners.

-

Build for the long term: Accept lower margins today for market position tomorrow. Infrastructure investments pay off over decades, not quarters.

This playbook, refined over 30 years, is Jubilant's true asset—more valuable than stores, brands, or technology. It's a system for building food service businesses in emerging markets, proven across categories and geographies.

XI. Financial Analysis & Valuation

The numbers tell a story of transformation, but also reveal uncomfortable truths about the limits of growth and the price of market leadership. With a Market Cap of ₹41,732 Crore, Revenue of ₹8,142 Cr, and Profit of ₹217 Cr, Jubilant FoodWorks presents a paradox: undisputed market leadership with increasingly challenged economics. The valuation paradox is stark. Jubilant Foodworks trades at a P/E ratio of 230. To give you a perspective, Asian Paints has grown at a CAGR of 20% for 5 decades and it trades at a P/E ratio of 90. The QSR chains listed in the US like McDonald's and Domino's itself trade at a much lower P/E of 34-35. The P/E ratio of Jubilant FoodWorks Ltd is 208.19 times as on 26-May-2025.

This extreme valuation reflects both promise and peril. The promise: India's QSR market, at $4 billion, is a fraction of China's $60 billion, suggesting massive headroom. The peril: growth requires capital, competition is intensifying, and margins are compressing.

Unit Economics Deep Dive

The unit economics reveal the structural challenges. A typical Domino's store in India: - Investment: ₹50-60 lakhs (equipment, interiors, deposits) - Monthly revenue: ₹25-30 lakhs - Food cost: 28-30% (up from 24% five years ago) - Labor: 18-20% (up from 15%) - Rent: 10-12% (stable) - Other operating: 15-18% - Store EBITDA: 20-25% (down from 28-30%)

The margin compression is structural, not cyclical. Food inflation, particularly cheese and chicken, shows no signs of abating. Labor costs will only increase as India develops. Delivery costs, once absorbed by customers through delivery charges, are increasingly subsidized to match aggregator pricing.

Same-Store Sales Growth Trends

SSG tells the real story. After years of 15-20% growth, SSG has moderated to single digits, occasionally turning negative. The Q3 FY25 12.5% SSG seems healthy but came from aggressive discounting that compressed margins. The trade-off between growth and profitability has become increasingly unfavorable.

The composition of SSG has also shifted. Previously driven by transaction growth (more customers), it's now primarily ticket size growth (inflation pass-through). This is concerning—price-led growth has limits, especially in price-sensitive markets.

Capital Efficiency Metrics

Return on capital employed (ROCE) has declined from 35% to under 20%. This isn't just margin compression—it's asset intensity increasing. New stores in tier-2/3 cities generate lower sales. International acquisitions diluted returns. Technology investments, while necessary, don't generate immediate returns.

The cash conversion cycle has elongated. While Domino's globally operates on negative working capital (customers pay before suppliers), India's franchise model means extending credit to franchisees. International operations add forex complexity and trapped cash in certain markets.

Bear Case: The Structural Challenges

The bear case writes itself:

-

Market saturation: Metro cities are saturated. Tier-2/3 expansion is capital-intensive with lower returns.

-

Competition intensification: Every QSR brand is expanding aggressively. Cloud kitchens offer similar products at 50% prices.

-

Margin pressure: Input cost inflation, delivery subsidization, and promotional intensity create a structural margin ceiling.

-

Aggregator dominance: Swiggy and Zomato control customer relationships. Their private labels compete directly using Jubilant's own data.

-

Category maturity: Pizza's novelty has worn off. Younger consumers want variety, health, and authenticity—not standardized fast food.

-

Execution complexity: Managing 3,000+ stores across six countries, multiple brands, and various formats stretches management bandwidth.

The bear case suggests Jubilant is a mature business trading at growth multiples, setting up inevitable disappointment.

Bull Case: The Platform Opportunity

The bull case requires imagination:

-

Penetration opportunity: From ~465 cities in early 2025 to targeting 700 cities by 2028, the company is executing aggressive tier‑2 tier‑3 city expansion. Domino's is slated to reach 3,000 stores, while Popeyes aims for 200–250 outlets within three years.

-

Consumption upgrade: As India's per capita income doubles, food service spending could triple. The shift from unorganized to organized food service is still early innings.

-

Technology moat: The investments in technology, while dilutive short-term, create long-term competitive advantages in personalization and efficiency.

-

Multi-brand leverage: Infrastructure built for Domino's can support multiple brands at marginal cost. Popeyes is proving this thesis.

-

International optionality: Turkey could become as large as India. Other emerging markets offer similar dynamics.

-

Financial flexibility: Debt-free balance sheet, consistent cash generation, and proven capital allocation provide options during downturns.

The bull case sees Jubilant not as a pizza company but as an emerging markets QSR platform, with the current valuation justified by long-term compounding opportunity.

Valuation Framework

At current prices, the market is pricing in: - 15-20% revenue CAGR for 5 years - Margin expansion to historical levels - Successful multi-brand execution - No major competitive disruption

This seems optimistic but not impossible. The key sensitivity: every 100 basis points of margin improvement/deterioration impacts valuation by 15-20%. The stock is essentially a leveraged bet on execution excellence in an increasingly difficult environment.

For fundamental investors, Jubilant presents a classic dilemma: a high-quality business at a price that leaves no room for error. The margin of safety that value investors seek is absent. The growth that growth investors desire is decelerating. The moat that quality investors prize is eroding.

The investment case ultimately rests on faith—faith in management's ability to navigate complexity, faith in India's consumption story, faith that pizza will remain relevant in a rapidly changing food landscape. At 230x earnings, that's expensive faith.

XII. Future Strategy & "If We Were CEOs"

The strategy presentation at the 2024 investor day was polished, comprehensive, and oddly predictable. More stores, more brands, more technology. But what if the future requires not more of the same but fundamental reimagination?

Jubilant FoodWorks is focusing on expanding its Popeyes and Domino's brands, with plans to open 30-50 Popeyes stores annually and a target of ₹1,000 crore revenue for Popeyes. The official strategy is clear: double down on what works, fix what doesn't, explore adjacent opportunities.

But if we were CEOs, we'd ask different questions. Not "How do we grow?" but "What business are we really in?" Not "How do we compete with aggregators?" but "How do we make aggregators irrelevant?" Not "How do we improve margins?" but "How do we change the game so margins don't matter?"

The Cloud Kitchen Revolution We'd Lead

Forget fighting cloud kitchens—become the infrastructure for them. Jubilant operates commissaries that could service hundreds of virtual brands. Why limit this to owned brands? Create "Jubilant Cloud"—a platform offering kitchen space, supply chain, technology, and fulfillment to entrepreneurs. Take 20% of revenues, no upfront investment. Let a thousand pizza brands bloom, powered by Jubilant infrastructure.

This isn't cannibalization; it's evolution. The future isn't 3,000 Domino's stores but 10,000 virtual restaurants operating from 500 ghost kitchens. Jubilant provides the picks and shovels for the gold rush.

The Private Label FMCG Play

Jubilant sells 3 million pizzas monthly. That's 3 million interactions with customers who trust the brand. Why stop at restaurant food? Launch Domino's frozen pizzas in retail. Domino's pasta sauces in supermarkets. Domino's cheese in modern trade. The supply chain exists. The brand equity exists. The distribution partnerships can be built.

McDonald's generates billions from retail products. Starbucks sells more coffee in supermarkets than stores. Jubilant has the same opportunity but hasn't seized it. The FMCG play isn't a side business—it could be bigger than restaurants within a decade.

The Subscription Economy Embrace

Netflix changed entertainment. Amazon Prime changed commerce. What's the Domino's Prime? ₹299 monthly for unlimited free delivery, 20% discount on all orders, exclusive menu items. At 2 million subscribers, that's ₹600 crore in high-margin recurring revenue before selling a single pizza.

But go further. Create tiers. ₹599 monthly includes birthday cakes. ₹999 monthly includes weekly meal plans. Turn transactional customers into subscribers. The lifetime value transformation would be extraordinary.

Technology Investments That Matter

Forget incremental app improvements. Build the AI that predicts what customers want before they know. License this to other QSRs globally. Become the Shopify of food service—powering thousands of restaurants with Jubilant technology.

Create the autonomous delivery network. Partner with drone companies, invest in robotics. The first QSR to crack autonomous delivery drops delivery cost to near zero. That's not an operational improvement; it's a new business model.

International Expansion 2.0

Stop thinking countries, start thinking communities. There are 30 million Indians abroad, concentrated in 50 cities globally. Launch Domino's India in Dubai, London, New York—serving exact Indian recipes to nostalgic diaspora. The market is smaller but margins are 3x.

Then flip the model. Bring global flavors to India through virtual brands. Turkish pide from the Turkey operations. American deep dish from Chicago recipes. Use the international presence for R&D, not just expansion.

The Dark Store Revolution

Merge stores and warehouses. Create 10,000-square-foot "dark stores" that service 20,000 households with 20-minute delivery of not just pizza but groceries, essentials, anything. Domino's becomes the trusted rapid delivery brand, not just food.

This isn't mission creep—it's recognizing that customers don't think in categories. They want speed, reliability, value. Domino's has built these capabilities. Why limit them to pizza?

Acquisition Targets We'd Pursue

Buy a cloud kitchen operator for infrastructure and expertise. Acquire a D2C food brand for FMCG capabilities. Purchase a last-mile logistics company for delivery independence. Each acquisition isn't just growth—it's capability building for the platform future.

But the boldest move: acquire an aggregator. Not Swiggy or Zomato, but a regional player. Transform it into Jubilant's own aggregation platform, featuring Jubilant brands prominently but open to others. Control the customer relationship instead of ceding it.

The Uncomfortable Decisions

Exit Dunkin' completely—accept the failure, free up resources. Sell the Turkish operations if returns don't improve within 18 months. Shut unprofitable stores ruthlessly, even if it means negative growth temporarily.

Convert 50% of company-owned stores to franchises, improving capital efficiency. Yes, margins compress, but return on capital expands. Use freed capital for technology and new ventures with higher returns.

The Cultural Revolution Required

The hardest change isn't strategic but cultural. Jubilant succeeded by being operationally excellent. The future requires being innovatively aggressive. This means accepting more failures, rewarding bigger bets, hiring different talent.

Create an internal venture fund. Give employees ₹100 crore annually to launch new concepts. Most will fail. Some will become billion-dollar businesses. The cost of not innovating exceeds the cost of failed experiments.

The Metrics Revolution

Stop managing to same-store sales growth—it encourages discounting. Instead, measure customer lifetime value growth. Stop focusing on store count—measure market share of stomach. Stop optimizing for quarterly earnings—measure capability building.

Public markets won't understand initially. The stock might underperform. But building for 2035, not 2025, requires accepting short-term pain.

The Ultimate Vision

In 10 years, Jubilant shouldn't be India's largest QSR company but India's largest food platform. Restaurants are one channel. Retail is another. Subscriptions, technology licensing, ghost kitchens, autonomous delivery—all channels serving the same mission: feeding India profitably.

The precedent exists. Amazon started selling books. Alibaba started connecting buyers and sellers. The biggest companies start narrow then expand relentlessly. Jubilant has the foundation—brand trust, operational excellence, financial strength. What's missing is imagination and courage.

The risk isn't in this transformation—it's in not transforming. Because while Jubilant debates incremental improvements, a startup in Bangalore is building the food platform of the future. The question isn't whether the QSR industry will be disrupted but whether Jubilant will be the disruptor or the disrupted.

This strategy won't be popular with analysts focused on next quarter's earnings. It won't be comfortable for management used to predictable operations. It won't be easy for a culture built on execution excellence.

But it's necessary. Because the alternative—managing decline while maintaining the fiction of growth—is the slow death that killed Kodak, Blockbuster, and countless market leaders who confused temporary dominance with permanent moat.

The future belongs to platforms, not products. To ecosystems, not companies. To those who reimagine, not those who optimize. Jubilant has the assets, capabilities, and opportunity to lead this transformation.

The only question is whether they have the courage.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube