JSW Holdings: India's Investment Powerhouse and the Art of Conglomerate Capital Allocation

I. Introduction & Episode Roadmap

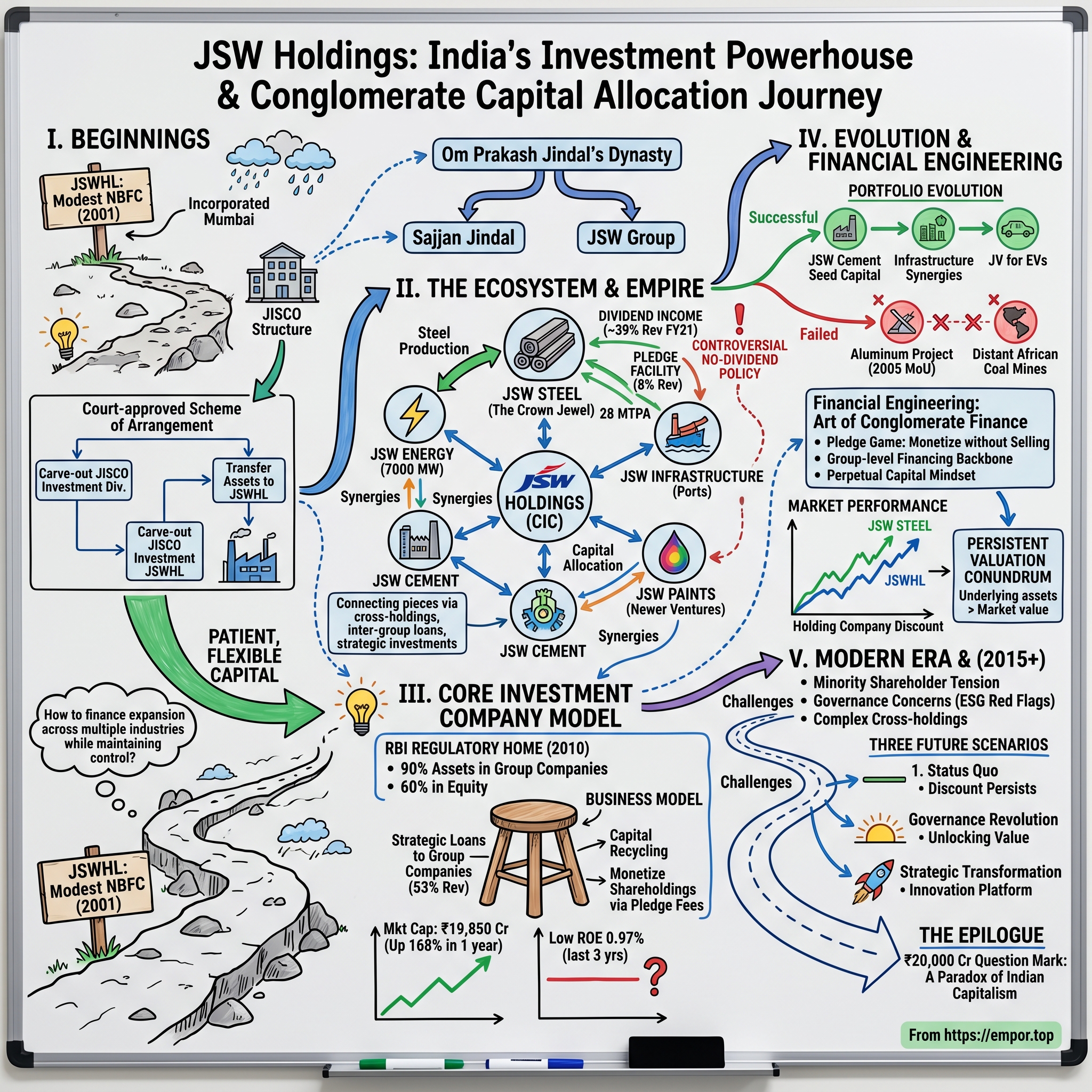

Picture this: A company sitting on ₹19,000 crores worth of JSW Steel shares, virtually debt-free, yet trading at a market cap that barely reflects its holdings. Welcome to the enigmatic world of JSW Holdings Limited—a financial architect that has quietly orchestrated one of India's most ambitious conglomerate expansions while remaining largely invisible to retail investors.

In the labyrinthine structure of Indian business houses, holding companies often serve as the hidden puppeteers, pulling strings across empires worth billions. JSW Holdings Limited, the core investment company of the $23 billion JSW Group, represents perhaps the purest expression of this model—a company whose primary business is owning pieces of other businesses, lending to them, and collecting dividends like a patient landlord of corporate equity.

The central question that drives our exploration today: How did a strategic holding company, born as a modest NBFC in 2001, transform into a ₹20,000 crore behemoth while maintaining an almost debt-free balance sheet—and why does the market still value it at a significant discount to its holdings? This story isn't about steel plants or cement factories. It's about something far more subtle—the art of managing money within money, the architecture of corporate control, and how a family-run business house built a financial fortress that would become both its greatest strength and most misunderstood asset.

Our journey traverses two decades of Indian capitalism's evolution, from the early 2000s liberalization boom through commodity supercycles, regulatory overhauls, and the peculiar dynamics of Core Investment Companies (CICs)—a uniquely Indian regulatory innovation that allows certain holding companies to operate with minimal oversight while wielding enormous financial influence.

We'll explore how JSW Holdings transformed from a simple Non-Banking Financial Company into the strategic nerve center of one of India's most ambitious industrial groups, accumulating stakes worth thousands of crores while paradoxically refusing to pay dividends to its own shareholders—a decision that has created both immense paper wealth and profound shareholder frustration.

The numbers tell a story of extremes: Market cap of ₹19,850 Crore (up 168% in 1 year), yet the company has a low return on equity of 0.97% over last 3 years. A stock that has multiplied over 200 times since listing, yet trades at a persistent discount to its holdings. A company that is almost debt free, yet refuses to share its wealth with minority shareholders.

This is the paradox we'll unpack: How does a company that essentially owns pieces of other companies become so valuable? Why does the market simultaneously love and hate holding companies? And what does the JSW Holdings story teach us about the unique dynamics of Indian capitalism, where family control, regulatory arbitrage, and patient capital converge to create structures that defy conventional financial logic?

II. The JSW Empire: Understanding the Ecosystem

To understand JSW Holdings, you must first understand the empire it serves. Picture the scorching heat of a Vijayanagar steel plant, the limestone quarries of Karnataka, the power plants dotting India's coastline—all connected by invisible threads of ownership that converge in a nondescript Mumbai office where JSW Holdings operates.

The story begins not with JSW, but with a man who embodied India's entrepreneurial awakening. Om Prakash Jindal, a farmer's son from Haryana, ventured into the steel business in the 1950s when independent India was just finding its industrial feet. By the time of his death in a helicopter crash in 2005, he had built an empire that would be divided among his four sons—each inheriting a piece of what would become separate business dynasties.

Sajjan Jindal, the youngest son, inherited what would become the JSW Group. Unlike his brothers who focused on specific sectors, Sajjan had grander ambitions. He envisioned not just a steel company, but a conglomerate that would span the commanding heights of India's economy—steel, energy, infrastructure, cement, and beyond.

The group's foundational moment came in 1982 when Jindal acquired a struggling re-rolling mill in Tarapur, Maharashtra, from the Piramal Group. This wasn't just any acquisition—it was a statement of intent. The mill, renamed Jindal Iron and Steel Company (JISCO), would become the seed from which the JSW empire would grow. That same year, they established their first integrated steel plant in Vasind, near Mumbai, marking the transition from trading to manufacturing.

But here's where the story gets interesting from a structural perspective. As the group expanded through the 1990s—adding power plants, port facilities, mining operations—Sajjan Jindal faced a classic conglomerate challenge: How do you finance rapid expansion across multiple capital-intensive industries without losing control?

The traditional route—diluting equity in operating companies—would have meant gradually ceding control to outside investors. Bank financing alone couldn't support the ambitions. Foreign partners wanted operational control. The solution that emerged was elegant in its simplicity: create a holding company structure that could raise capital, provide inter-group financing, and maintain family control while allowing individual businesses to scale independently.

This wasn't unique to JSW. The Tatas had Tata Sons, the Birlas had their investment companies, the Ambanis would later create similar structures. But what made JSW's approach distinctive was its timing and execution. They were building this structure just as India's financial markets were maturing, as foreign investment was liberalizing, and as a new class of institutional investors was emerging hungry for exposure to India's growth story.

The JSW Group that exists today—valued at over $23 billion—is actually a carefully orchestrated network of listed and unlisted companies, joint ventures, and special purpose vehicles. At the operational level, you have the flagship JSW Steel, the crown jewel that produces over 28 million tonnes per annum and ranks among India's largest steel producers. There's JSW Energy with over 7,000 MW of power generation capacity. JSW Infrastructure operates ports and terminals handling over 170 million tonnes of cargo annually. The newer ventures—JSW Paints challenging Asian Paints' monopoly, JSW Cement targeting 25 million tonnes capacity, JSW One pioneering steel e-commerce—represent the group's continued evolution.

But connecting all these pieces is a complex web of cross-holdings, inter-company loans, and strategic investments. JSW Steel owns stakes in JSW Energy. JSW Energy has investments in JSW Infrastructure. Various group companies provide loans and guarantees to each other. At the center of this web sits JSW Holdings—not as an operating company, but as a financial architect, a patient provider of capital, and crucially, a vehicle for the promoter family to maintain control without having to directly own majority stakes in every group company.

The genius of this structure becomes apparent when you consider the mathematics of control. Through a combination of direct holdings, cross-holdings, and the strategic use of JSW Holdings' investments, the Jindal family maintains effective control over a $23 billion empire while owning far less than 50% of the total equity across all companies. It's leverage, but not the debt kind—it's control leverage through clever structuring.

This ecosystem approach also created natural synergies. The steel plants needed power—JSW Energy provided it. The power plants needed coal—JSW Infrastructure's ports handled the imports. The infrastructure needed steel—JSW Steel supplied it. Each business supported the others, creating an internal economy that could weather external shocks better than standalone companies.

The family dynamics added another layer of complexity. Unlike the bitter public feuds that characterized some Indian business family splits, the Jindal brothers' separation was relatively amicable. They agreed to non-compete arrangements, divided territories and sectors, and occasionally collaborated on specific projects. Sajjan Jindal's JSW focused on western and southern India initially, while brothers operated in other regions. This geographic and sectoral division allowed each to grow without fratricidal competition.

Understanding this ecosystem is crucial because JSW Holdings cannot be analyzed as a standalone entity. Its value, its strategy, its very existence is intertwined with the broader JSW Group's fortunes. When steel booms, Holdings benefits through dividends and appreciation. When new ventures need capital, Holdings provides it. When banks need comfort for group-level borrowings, Holdings' shares serve as collateral.

This symbiotic relationship would shape every major decision JSW Holdings would make over the next two decades—from its transformation into a Core Investment Company to its controversial dividend policies, from its investment strategies to its relationship with minority shareholders. The holding company wasn't just a financial vehicle; it was the circulatory system of an industrial empire, moving capital to where it was needed most, when it was needed most.

III. Origins: From NBFC to Core Investment Company (2001–2010)

July 12, 2001, marked an inflection point in the JSW Group's evolution, though few recognized it at the time. On that monsoon day in Mumbai, a new entity was quietly incorporated—Jindal South West Holdings Limited, registered as a Non-Banking Financial Company with the Reserve Bank of India. The timing was no coincidence. India had just survived the dot-com bust, the economy was liberalizing at breakneck speed, and industrial groups were scrambling to position themselves for what everyone sensed would be a prolonged boom.

The creation of this NBFC wasn't born from a boardroom epiphany but from practical necessity. By 2001, Sajjan Jindal's steel ambitions had outgrown the original JISCO structure. The Vijayanagar plant in Karnataka was consuming massive capital, competing steel projects needed funding, and the group was eyeing opportunities in power and infrastructure. Traditional bank financing came with covenants and restrictions. Capital markets wanted quarterly performance. What Jindal needed was patient, flexible capital that could move quickly between group companies without regulatory friction.

The NBFC structure offered elegant solutions to multiple problems. Unlike regular companies, NBFCs could lend to group entities with fewer restrictions. They could take deposits from group companies, effectively creating an internal banking system. They could invest in securities, providing a mechanism for the group to consolidate its various shareholdings. Most importantly, they could do all this while maintaining a lighter regulatory touch than actual banks.

But the real masterstroke came through a complex scheme of arrangement that would define JSW Holdings' DNA. Through a court-approved restructuring between Jindal Iron and Steel Company, the newly formed Holdings company, and Jindal Vijayanagar Steel, the entire investment division of JISCO was carved out and transferred to the Holdings company. This wasn't just moving assets between pockets—it was creating a dedicated vehicle whose sole purpose was to manage the group's strategic investments and provide financial flexibility.

The early portfolio was modest but strategic. The holdings included stakes in group companies that were still finding their feet—nascent infrastructure ventures, small cement operations, international trading arms. But the crown jewel was always the stake in what would become JSW Steel. Even in those early days, it was clear that steel would be the engine that powered the group's ambitions.

The 2000s were transformative years for Indian industry, and JSW Holdings had a front-row seat. China's insatiable commodity demand was driving a global supercycle. Indian infrastructure spending was exploding. Credit was flowing freely. In this environment, the Holdings company served as the group's war chest, providing bridge financing for acquisitions, funding new ventures before they could access external capital, and occasionally taking positions in non-group companies that offered strategic value.

One fascinating episode from this period illustrates the Holdings company's role. In 2005, the company signed a memorandum of understanding with the Andhra Pradesh government to set up aluminum refinery and smelter plants near Visakhapatnam. This wasn't JSW's core business—they were steel people. But aluminum was experiencing its own boom, and the Holdings company provided the risk capital to explore this opportunity. The venture ultimately didn't materialize as envisioned, but it demonstrated the Holdings company's mandate: to be the group's scout, its risk-taker, its option holder on future opportunities.

The regulatory landscape was evolving rapidly during this period. The Reserve Bank of India, scarred by previous NBFC failures, was tightening oversight. New capital requirements were introduced. Lending norms were strengthened. Activity restrictions were imposed. For many NBFCs, these regulations were suffocating. But for JSW Holdings, they presented an opportunity to transform into something more suited to its actual role.

Enter the concept of Core Investment Companies (CICs)—a regulatory innovation that seemed tailor-made for JSW Holdings' business model. The RBI recognized that some NBFCs weren't really in the business of lending to the public or taking public deposits. They were investment holding companies, providing financial services primarily to their group companies. These entities needed different regulations—lighter in some areas, more specific in others.

The transition from NBFC to CIC wasn't automatic. It required restructuring the business model, ensuring compliance with specific asset-liability ratios, and accepting certain restrictions on activities. But for JSW Holdings, it was a natural evolution. The company was already functioning as a CIC in practice; now it would be recognized as one in regulation.

By 2010, JSW Holdings had established its essential character. It was a patient provider of capital, funding long-gestation projects while public markets focused on quarterly earnings. It was a strategic consolidator, holding stakes that gave the group flexibility in structuring and control. It was a financial bridge, connecting group companies through loans and guarantees. And increasingly, it was becoming valuable in its own right as the stakes it held—particularly in JSW Steel—began appreciating dramatically.

The first decade had been about building the foundation. The Holdings company had accumulated strategic stakes, established its lending relationships with group companies, and found its regulatory home as a CIC. But the real value creation was yet to come. The commodity supercycle was approaching its peak, JSW Steel was about to embark on massive expansions, and the Holdings company's patient bets were about to pay off in ways that would transform it from a supporting player to a major source of value in its own right.

IV. The Core Investment Company Model

The Reserve Bank of India's 2016 Master Direction on Core Investment Companies reads like a regulatory manual, but hidden within its technical provisions is a fascinating acknowledgment: India's conglomerates needed their own specialized financial architecture. JSW Holdings had found its regulatory home, and understanding this CIC model is crucial to grasping both its power and limitations.

A Core Investment Company, in essence, is a non-banking financial company that exists primarily to hold investments in group companies. Think of it as a specialized investment fund, but instead of investing in public markets for returns, it invests in related companies for control and strategic value. The regulations recognize this unique role with a carefully calibrated framework—lighter touch in some areas, specific restrictions in others.

For JSW Holdings, the CIC classification was transformative. Under the regulations, as long as it maintained 90% of its assets in the form of investments in equity shares, preference shares, bonds, debentures, or loans to group companies, and had at least 60% in equity investments, it could operate without seeking registration from the RBI. This wasn't just regulatory convenience—it was recognition that the company's systemic risk was different from a typical NBFC lending to the public.

In FY21, interest on loans accounted for ~53% revenues, followed by dividend income (39%) and pledge fees (8%). This revenue breakdown reveals the three-legged stool of the CIC business model, each leg serving a different strategic purpose.

The lending business—accounting for the majority of revenues—wasn't about maximizing interest income. These were strategic loans to group companies, often provided at crucial moments when external financing was either unavailable or came with unacceptable conditions. When JSW Steel needed bridge financing for an acquisition, when JSW Energy required working capital before project financing came through, when new ventures needed seed capital—JSW Holdings was there, lending at rates that balanced commercial returns with group strategic needs.

The dividend income stream told another story. Unlike typical investors who chase dividend yields, JSW Holdings' dividend income was about capital recycling within the group. When JSW Steel or other group companies declared dividends, a portion flowed back to Holdings, creating a pool of capital that could be redeployed elsewhere in the group. It was an elegant internal capital market, allowing successful mature businesses to fund nascent ventures without external dilution.

But perhaps the most innovative revenue stream was the pledge fees—a uniquely Indian financial innovation born from the intersection of promoter financing needs and regulatory constraints. Here's how it worked: JSW Holdings owned valuable shares, particularly in JSW Steel. Group companies or promoters needing loans could borrow from banks using these shares as collateral. JSW Holdings would charge a fee for providing this pledge facility. It was leverage without debt on Holdings' own books—a way to monetize shareholdings without selling them.

The capital allocation philosophy embedded in this model was fundamentally different from a typical investment company. A mutual fund or private equity firm would constantly evaluate whether to hold or sell, seeking to maximize returns. But for JSW Holdings, the calculus was more complex. Selling JSW Steel shares might realize immediate gains, but it would reduce group control, eliminate future dividend streams, and remove pledge capacity. The value of holding wasn't just financial—it was strategic.

This philosophy extended to how the company evaluated new investments. When JSW Cement was launched, Holdings provided crucial early capital, not because cement offered the best risk-adjusted returns, but because it fit the group's infrastructure ecosystem. When international ventures needed funding, Holdings participated not for diversification, but to support the group's globalization agenda.

The CIC model also came with constraints that shaped behavior. Leverage limits meant Holdings couldn't borrow excessively against its investments. Investment concentration rules meant it couldn't put all eggs in one basket, even if that basket was JSW Steel. These regulations forced a discipline that, in retrospect, served the company well—preventing excessive leverage during boom times that could have been catastrophic during downturns.

The regulatory framework also created interesting tax dynamics. Inter-company dividends enjoyed favorable tax treatment. Interest on loans to group companies was deductible for the borrowers while taxable for Holdings, creating opportunities for tax-efficient structuring. The ability to provide corporate guarantees without being classified as a banking activity opened doors for group-level financing arrangements.

But the CIC model wasn't without its critics, particularly among minority shareholders. The structure essentially meant JSW Holdings existed to serve the broader group's interests, not necessarily to maximize returns for Holdings' own shareholders. This tension—between group strategic value and minority shareholder returns—would become a defining challenge.

The model also created valuation complexities. How do you value a company whose primary assets are stakes in related parties, whose lending is strategic rather than commercial, whose dividend policy is subordinated to group capital needs? Traditional valuation metrics struggled with these questions, contributing to the persistent holding company discount that plagued JSW Holdings' stock price.

Yet for the JSW Group, the CIC model was near-perfect. It provided a regulated framework for doing what they needed—moving capital efficiently within the group, maintaining control without excessive equity dilution, and creating financial flexibility for an ambitious conglomerate. The fact that the company's market cap grew to ₹19,850 Crore while remaining almost debt free validated the model's effectiveness, even if the market didn't fully appreciate it.

V. The Crown Jewel: JSW Steel Stake

The conference room at JSW Centre in Mumbai bears witness to countless strategic decisions, but few carried the weight of those concerning the JSW Steel shareholding. As of March 31, 2024, JSW Holdings' 7.42% stake in JSW Steel commanded a market value approaching ₹19,000 crores—a position that essentially defines the holding company's entire worth and existential purpose. To truly understand the significance of this stake, we need to travel back to the mid-2000s when JSW Steel was still consolidating its various steel operations. The 2005 merger of JISCO and Jindal Vijayanagar Steel Limited created JSW Steel Limited—a unified entity that would become India's steel powerhouse. JSW Holdings, through the complex restructuring we discussed earlier, emerged with a strategic stake in this combined entity.

In the year 2005, JISCO and JVSL merged to form JSW Steel Limited. What seemed like a routine corporate restructuring would prove to be one of the most valuable financial decisions in Indian corporate history. The stake that Holdings retained—initially larger but diluted over time through various capital raises—would appreciate beyond anyone's wildest projections.

The mathematics of this appreciation tells a story of India's industrial transformation. As of July 2023, the installed with a production capacity of 29.7 MTPA in India and the United States, with the company aiming to boost the total steel production capacity to 38.5 MTPA by the financial year 2025. Each capacity expansion, each new plant, each acquisition added value not just to JSW Steel but multiplicatively to Holdings' stake.

Consider the trajectory: From a regional steel producer with a few million tonnes capacity in 2005 to becoming India's largest private sector steel company. The Vijayanagar plant alone, the Company's 12 MTPA manufacturing unit in Vijayanagar, Karnataka is the largest single-location steel-producing facility in India. The Dolvi expansion doubled capacity from 5 to 10 MTPA. The acquisition of Bhushan Power and Steel added another 3.5 MTPA. Each milestone pushed JSW Steel's valuation higher, and with it, the value of Holdings' stake.

But the strategic importance of this holding transcends mere financial appreciation. The stake serves multiple critical functions in the group's financial architecture. First, it provides the collateral backbone for group-level financing. When JSW companies need to raise debt for new projects, Holdings' shares in JSW Steel—liquid, valuable, and easily pledgeable—serve as prime collateral. Banks love this security because JSW Steel shares trade actively, have clear market values, and represent ownership in a profitable, growing business.

The dividend stream from this stake represents another crucial dimension. JSW Steel, as a mature, cash-generating business, regularly declares dividends. For Holdings, these dividends aren't just income—they're the lifeblood that funds new ventures, provides bridge loans to group companies, and maintains Holdings' own operations without requiring external capital. It's a perpetual money machine, as long as steel markets remain healthy.

Yet this crown jewel has also become Holdings' greatest source of controversy with minority shareholders. The fundamental tension is stark: Holdings owns shares worth ₹19,000 crores, its market cap is around ₹20,000 crores, yet it refuses to pay dividends to its own shareholders. The company's repeated profits haven't translated into shareholder distributions, creating a situation where minority investors own shares in a company that owns valuable shares but won't share the wealth.

The pledge game adds another layer of complexity. At various points, significant portions of JSW Steel shares held by Holdings have been pledged for group borrowings. This creates a curious dynamic—the shares generate pledge fees (income for Holdings), enable group companies to borrow (strategic value), but also create risk (if loans default, shares could be sold). It's financial engineering at its most sophisticated, using the same asset to generate multiple streams of value while maintaining ultimate control.

The debates in Holdings' boardroom about whether to sell portions of the JSW Steel stake have been intense. Selling would realize immediate gains, provide cash for dividends or new investments, and potentially reduce the holding company discount. But it would also reduce control, eliminate future dividend streams, decrease pledge capacity, and signal a retreat from the core business that defines the group. The decision to hold, despite market pressure, reflects a fundamental belief that JSW Steel's best days are ahead.

This belief isn't unfounded. JSW Steel targets to expand its capacity to 38 MTPA by 2024 from the present 23 MTPA, with massive investments planned. The expansion will add another 5 million tonnes of capacity at the Dolvi plant, raising its total capacity to 15 million tonnes per annum by September 2027. Nationwide, JSW Steel aims for a total production capacity of 42 million tonnes by then. Each tonne of additional capacity potentially adds value to Holdings' stake.

The international ambitions add another dimension. In March 2024, JSW Steel Italy SRL inked an MoU with the Government of Italy to invest €140 million in restarting production at the Piombino plant. However, this new agreement aims to double rail-making capacity to 600,000 tonnes per year in Piombino. The company's forays into specialty steels, green steel production, and downstream value addition all potentially multiply the value of Holdings' stake.

But perhaps the most fascinating aspect of this crown jewel is how it exemplifies the Indian approach to corporate control. Through a 7.42% stake—seemingly modest—combined with the promoter family's direct holdings and other cross-holdings, the group maintains effective control over a company worth hundreds of thousands of crores. It's not about owning everything; it's about owning the right pieces in the right structures.

The market's valuation of Holdings essentially reduces it to its JSW Steel stake plus a bit more. This reductionist view misses the strategic value—the ability to provide patient capital, the flexibility to support group ventures, the option value on future businesses. But it also reflects a harsh reality: without the JSW Steel stake, Holdings would be worth a fraction of its current value. The crown jewel isn't just valuable; it's existential.

VI. Portfolio Evolution & Strategic Investments

Beyond the towering presence of JSW Steel, JSW Holdings' investment portfolio reads like a map of the group's ambitions—each stake representing a bet on India's infrastructure future, some flourishing into billion-dollar businesses, others serving as expensive lessons in the perils of diversification.

The portfolio strategy was never about building a diversified investment fund. Instead, each investment served the larger group architecture—creating synergies, securing raw materials, entering adjacent markets, or providing strategic options for future expansion. The company's stated philosophy was clear: focus on strategic investments in new ventures promoted by the JSW Group, with steel sector investments forming the core given the sector's growth trajectory.

Take the cement venture, for instance. When JSW Cement was conceived in 2009, India's infrastructure boom was creating insatiable demand for building materials. For a group already producing steel for construction, cement was a logical adjacency. Holdings provided crucial seed capital, not because cement offered superior returns to steel, but because it completed the group's construction materials portfolio. Today, JSW Cement targets 25 million tonnes capacity, validating that early bet.

The international ventures tell a more complex story. Holdings established a Singapore subsidiary to facilitate overseas investments and trading operations. This wasn't just about geographic diversification—it was about creating a platform for international fund-raising, managing forex risks, and establishing presence in global commodity trading hubs. The subsidiary facilitated investments in coal mines in Africa, iron ore projects in South America, and trading relationships across Asia.

But not all international forays succeeded. The eventual wind-down of certain Singapore operations reflected hard-learned lessons about the challenges of managing distant assets, navigating foreign regulatory environments, and competing against established global players. The capital tied up in these ventures could have been deployed more productively in India, where the group had natural advantages.

The 2005 aluminum ambition deserves special attention as a case study in strategic optionality. The Company signed a Memorandum of Understanding (MOU) with the Government of Andhra Pradesh (AP) in July, 2005, envisaging aluminum refinery and smelter plants near Visakhapatnam. This represented a bold diversification—aluminum and steel serve similar markets but require completely different technical competencies, raw materials, and energy profiles.

The aluminum venture never materialized as planned, but the episode revealed Holdings' role as the group's scout, willing to commit capital to explore opportunities that operating companies couldn't justify. The MOU gave JSW an option on entering aluminum if conditions became favorable. When they didn't—due to bauxite availability issues, power costs, and competitive dynamics—the group could walk away without damaging core operations. Holdings absorbed the exploration costs, protecting listed entities from venture risks.

The infrastructure investments proved more successful. As JSW Steel's production scaled, the need for dedicated logistics infrastructure became critical. Holdings participated in funding port projects, railway sidings, and material handling systems. These weren't standalone profitable ventures but strategic enablers that reduced logistics costs for the entire group. A captive port that saves Rs 100 per tonne on iron ore imports across millions of tonnes creates value far exceeding its standalone profitability.

The power sector investments followed similar logic. Steel plants are energy-intensive, consuming massive amounts of electricity. By investing in JSW Energy through Holdings and other structures, the group secured reliable, cost-effective power for its steel operations while also building a standalone power business. The synergies were obvious—JSW Energy's plants could be located near JSW Steel's facilities, sharing infrastructure and reducing transmission losses.

The newer ventures—paints, sports, e-commerce platforms—represented evolution in Holdings' investment philosophy. These weren't traditional infrastructure plays but attempts to leverage the JSW brand into consumer-facing businesses. The paints venture, challenging established players like Asian Paints, required patient capital willing to accept losses during market entry. Holdings, with its long-term orientation and no quarterly earnings pressure, was the ideal funding source.

Throughout this portfolio evolution, certain patterns emerged. Successful investments shared common characteristics: clear synergies with existing businesses, leverageable group capabilities, and large addressable markets. Failed ventures typically lacked one or more of these elements—international projects without local knowledge, sectors without synergies, or markets without scale.

The portfolio composition also evolved with India's economic transition. Early investments focused on basic infrastructure—steel, power, ports. As India's economy matured, investments shifted toward value-added products and services. The latest ventures in electric vehicles, green hydrogen, and digital platforms reflect bet on India's next economic phase.

The funding pattern for these investments reveals Holdings' financial flexibility. Sometimes it provided direct equity, becoming a shareholder in new ventures. Other times it extended loans, generating interest income while maintaining option to convert to equity. Occasionally it provided guarantees, enabling ventures to borrow without depleting Holdings' capital. This toolkit allowed customized support based on each venture's needs.

But this portfolio evolution wasn't without criticism. Minority shareholders questioned why Holdings' capital was deployed in nascent ventures with uncertain returns rather than distributed as dividends. Why fund a paint company's losses when you own shares worth ₹19,000 crores in a profitable steel company? The answer lay in the group's vision of building an industrial conglomerate, not maximizing near-term shareholder returns.

The regulatory environment also shaped portfolio decisions. As a Core Investment Company, Holdings had to maintain specific asset compositions—90% in group investments, 60% in equity form. These requirements prevented excessive diversification into third-party investments but also constrained flexibility. The company couldn't simply become a hedge fund or private equity investor even if such strategies promised higher returns.

VII. Financial Engineering & Market Performance

The story of JSW Holdings' market journey begins with a puzzle: How does a company transform from a stock price of ₹115 at listing to ₹27,740 at its peak—a mind-bending 240x return—while maintaining one of the most controversial dividend policies in Indian capital markets? The 2005 listing journey marked JSW Holdings' entry into public markets. Listing date: 21 Jun, 2005, the company went public in an era when Indian capital markets were just beginning to appreciate the value of financial holding companies. The initial reception was lukewarm—investors struggled to understand a company whose primary business was owning stakes in other companies.

Lowest end of day price: 2.5103688398283 INR ($0.05480 USD) on 2006-06-14—adjusted for corporate actions, this represents one of the most spectacular value creation stories in Indian markets. The journey from these depths to Highest end of day price: 310.24356592985 INR ($3.64 USD) on 2025-04-17 (adjusted for splits) wasn't linear but punctuated by periods of explosive growth and painful corrections.

The stock's performance can be divided into distinct phases, each reflecting broader market dynamics and group developments. The 2005-2008 period saw modest appreciation as markets tried to value this unusual entity. The global financial crisis of 2008-2009 crushed valuations, with Holdings trading at massive discounts to its underlying assets as investors fled to safety.

The 2010-2017 period brought steady appreciation as JSW Steel's capacity expansions bore fruit and commodity markets recovered. But the real fireworks began in 2020. The combination of pandemic-era liquidity, India's infrastructure push, and JSW Steel's aggressive expansion plans created perfect conditions for a rerating. JSWHL has showed a 213.70% increase over the last year alone, with the stock touching lifetime highs repeatedly.

Mkt Cap: 19,850 Crore (up 168% in 1 year)—this explosive growth reflects not just asset appreciation but a fundamental reassessment of holding companies' value in India's evolving market structure. Yet paradoxically, this same company maintains Stock P/E 113, a valuation that seems astronomical for a holding company but perhaps justified by the growth trajectory of its underlying assets.

The financial engineering that enabled this performance deserves scrutiny. Company is almost debt free—a remarkable achievement for a company sitting at the center of a capital-intensive conglomerate. This wasn't accidental but reflected deliberate choices. Rather than leverage Holdings' balance sheet for acquisitions or expansions, the group chose to keep it pristine, using it as collateral provider rather than direct borrower.

The dividend paradox stands out starkly: Though the company is reporting repeated profits, it is not paying out dividend. This decision has created tremendous shareholder frustration. With Promoter Holding: 66.3%, the promoter family essentially decides dividend policy unilaterally. Their choice to reinvest rather than distribute reflects a fundamental philosophy—Holdings exists to support group growth, not maximize shareholder returns.

The revenue model reveals sophisticated financial structuring. In FY21, interest on loans accounted for ~53% revenues, followed by dividend income (39%) and pledge fees (8%). Each revenue stream serves dual purposes—generating returns while maintaining group financial flexibility. The interest income isn't just about returns; it's about providing patient capital when banks won't lend. The dividend income isn't just cash flow; it's about recycling capital from mature to growing businesses.

The pledge fee innovation deserves special attention. By charging fees for allowing shares to be pledged for group borrowings, Holdings monetizes its assets without selling them or borrowing against them directly. It's a uniquely Indian financial innovation, born from the intersection of promoter funding needs and regulatory constraints.

Company has a low return on equity of 0.97% over last 3 years—a metric that would doom most companies but makes sense for Holdings given its model. The company isn't trying to maximize ROE through leverage or aggressive investing. It's maintaining a fortress balance sheet while supporting group expansion. The low ROE reflects huge equity base from accumulated profits never distributed as dividends.

The valuation conundrum persists despite stellar stock performance. The market values Holdings at roughly its JSW Steel stake plus a small premium, essentially assigning zero value to its lending business, other investments, and strategic importance to the group. This holding company discount—typical globally but particularly pronounced in India—reflects several factors: complexity in valuation, lack of control over underlying assets, dividend uncertainty, and regulatory constraints.

Market participants have evolved different views on Holdings. Long-term investors see it as a discounted play on JSW Steel with optionality on new ventures. Traders love its volatility, with the stock often moving 5-10% in single sessions based on JSW Steel's performance. Institutional investors remain wary, concerned about governance and minority shareholder treatment. Retail investors, attracted by the JSW brand and spectacular returns, often misunderstand the business model.

The stock's correlation with JSW Steel is nearly perfect—when Steel rises, Holdings follows; when Steel falls, Holdings falls harder due to its leveraged exposure. This creates interesting arbitrage opportunities for sophisticated investors who can trade the spread between Holdings' market value and its net asset value.

VIII. Modern Era: Challenges & Opportunities (2015–Present)

The modern chapter of JSW Holdings' story begins with a paradox that would define its trajectory: unprecedented asset value growth coupled with persistent questions about corporate governance and shareholder value distribution. Post-2015, as India entered its infrastructure supercycle and JSW Steel embarked on its most ambitious expansion phase, Holdings found itself at the center of intensifying debates about minority shareholder rights and holding company structures.

The valuation metrics tell a story of extremes. With Stock P/E at 113, the market is essentially pricing in decades of future growth—unusual for a holding company that primarily owns mature assets. This stretched valuation reflects the market's struggle to reconcile Holdings' strategic value with its shareholder-unfriendly policies. The company has a low return on equity of 0.97% over last 3 years, yet investors continue bidding up the stock, betting on eventual value unlocking.

The regulatory landscape shifted significantly during this period. The Reserve Bank of India's enhanced scrutiny of Core Investment Companies brought new compliance requirements. Holdings had to navigate evolving regulations around related-party transactions, ensure arm's length pricing for inter-company loans, and maintain detailed disclosures about its investment portfolio. These changes, while adding compliance burden, actually strengthened Holdings' position by creating barriers to entry for new CICs.

The cross-holding complexities intensified as the JSW Group's structure became more intricate. Holdings owns JSW Steel shares, JSW Steel owns stakes in JSW Energy, JSW Energy has investments in infrastructure projects—creating a web of interdependencies that makes valuation challenging. Each entity's value depends on others, creating circular references that confound traditional sum-of-parts analysis.

The minority shareholder tension reached new heights during this period. With promoter holding at 66.3%, minority investors found themselves in a peculiar position—owning shares in a company with valuable assets but no say in capital allocation. Shareholder meetings became forums for expressing frustration about the no-dividend policy. Proxy advisory firms regularly recommended voting against resolutions, though with limited practical impact given promoter control.

The debate crystallized around a simple question: Why shouldn't a company with ₹19,000 crores in liquid investments and minimal debt pay dividends? The management's response—that capital was needed for group expansion—rang hollow to minorities watching the stock trade at huge discounts to asset value. Some investors argued for a special dividend, share buyback, or even voluntary delisting to unlock value.

The capital allocation decisions during this period reflected strategic priorities over financial optimization. Holdings continued funding new ventures—JSW Paints' aggressive rollout, infrastructure projects with long gestation periods, international expansions with uncertain returns. Each investment made strategic sense for the group but diluted Holdings' return metrics. The company essentially operated as the group's venture capital arm, accepting lower returns for strategic value.

The COVID-19 pandemic created an unexpected test of Holdings' model. As credit markets froze and banks turned cautious, Holdings' ability to provide emergency liquidity to group companies proved invaluable. While listed companies struggled with covenant breaches and rating downgrades, JSW Group entities could tap Holdings for bridge financing. The debt-free balance sheet, long criticized as inefficient, became a strategic asset during crisis.

Post-pandemic recovery brought extraordinary circumstances. Commodity prices soared, infrastructure spending exploded, and JSW Steel's profitability reached record levels. Holdings' stake value multiplied, yet the company maintained its conservative stance—no dividends, no buybacks, no value unlocking. The stock's 168% rise in one year reflected market optimism about eventual value realization rather than fundamental changes in shareholder treatment.

The emergence of new investment themes added complexity. Green energy, electric vehicles, digital platforms—each required patient capital that traditional lenders wouldn't provide. Holdings found itself funding ventures far removed from its steel-cement-infrastructure heritage. These investments, while offering optionality on India's economic transformation, further complicated Holdings' investment case.

International scrutiny increased as foreign investors discovered Holdings. Global funds, attracted by India's growth story and JSW's execution track record, struggled with Holdings' governance model. ESG concerns, particularly around minority shareholder treatment, became prominent. Some funds explicitly excluded Holdings despite its attractive valuation, citing governance red flags.

The competitive dynamics among Indian holding companies evolved during this period. Tata Sons' legal battles highlighted risks in complex holding structures. Reliance's corporate restructuring showed possibilities for value unlocking. Bajaj Holdings' consistent dividends demonstrated alternative approaches. These comparisons put pressure on JSW Holdings to reconsider its model, though management remained unmoved.

Technology began playing a larger role in Holdings' operations. Digital platforms for inter-company transactions, automated compliance systems, real-time portfolio tracking—Holdings modernized its operations even as its fundamental model remained unchanged. The company explored blockchain for inter-company settlements and AI for credit assessment, showing willingness to innovate operationally if not strategically.

The future investment priorities became clearer as the decade progressed. Green steel, renewable energy, electric vehicles, specialty chemicals—Holdings positioned itself to fund the group's transition to sustainability. Each new venture required patient capital willing to accept J-curve returns, perfectly suited to Holdings' mandate but challenging for public market investors seeking predictable returns.

As we stand today, JSW Holdings embodies the contradictions of Indian capitalism—enormous value creation alongside questionable value distribution, strategic brilliance coupled with governance concerns, market outperformance despite structural disadvantages. The company remains almost debt free, sitting on invaluable assets, yet trading at persistent discounts, refusing to share wealth with minorities who've been part of the journey.

IX. Playbook: The Art of Conglomerate Finance

If you were to distill JSW Holdings' two-decade journey into actionable lessons, you'd find a masterclass in patient capital deployment, regulatory arbitrage, and the delicate balance between group interests and public market expectations. The playbook that emerges isn't just about financial engineering—it's about building enduring competitive advantages through structure.

Lesson 1: Patient Capital as Competitive Moat

In a market obsessed with quarterly earnings, JSW Holdings' ability to provide patient capital became its defining advantage. When JSW Paints needed five years to break even while challenging Asian Paints, when JSW Cement required decade-long investments before achieving scale, when international ventures demanded upfront capital with uncertain returns—Holdings was there, unfazed by J-curve dynamics that would terrify public market investors.

This patience wasn't just philosophical; it was structural. Without external shareholders demanding quarterly performance, without analyst calls questioning every investment, Holdings could take positions that wouldn't make sense for publicly-listed operating companies. The ability to fund a steel plant expansion that takes three years to complete, or a port that needs five years to reach capacity utilization, created competitive advantages that pure operational efficiency couldn't match.

Lesson 2: The Indian Context Changes Everything

What works in developed markets doesn't necessarily work in India, and Holdings exemplifies this principle. In the US or Europe, holding company discounts often exceed 30-40% because of double taxation, lack of control premium, and efficient capital markets that reduce the value of internal capital allocation. But in India, where credit markets remain shallow, where regulatory permissions can take years, where relationships matter as much as collateral—a holding company that can navigate these complexities becomes invaluable.

The Core Investment Company regulation itself is uniquely Indian, recognizing that business houses need specialized financial vehicles. Unlike Western markets where holding companies are largely tax or control plays, Indian holding companies serve operational purposes—providing credit when banks won't lend, offering guarantees that enable project financing, maintaining strategic stakes that ensure management continuity.

Lesson 3: Cross-Subsidization as Strategy

The ability to move capital from profitable mature businesses to nascent ventures—without market scrutiny or regulatory friction—enabled JSW to build businesses that standalone entities couldn't. When JSW Steel generated cash, Holdings could redirect it to fund JSW Infrastructure's port expansion. When JSW Energy needed growth capital, Holdings could provide it without diluting public shareholders.

This internal capital market operated more efficiently than external markets could. Holdings understood group businesses better than any bank, could price risk more accurately than external lenders, and could be flexible on terms in ways that arm's length transactions couldn't. The interest rate might be commercial, but the patience, the covenant flexibility, the willingness to restructure when needed—these created value beyond the financial terms.

Lesson 4: Managing Regulatory Constraints as Opportunity

Every regulatory constraint Holdings faced became an opportunity for innovation. When RBI limited leverage, Holdings innovated with pledge fees—monetizing assets without borrowing. When related-party transaction rules tightened, Holdings formalized its lending processes, actually improving credit discipline. When CIC regulations required portfolio composition ratios, Holdings used them to justify strategic investments to shareholders.

The mastery lay in understanding that regulations aren't just constraints—they're competitive barriers. Every compliance requirement that Holdings mastered became a moat that prevented new entrants. The complexity of managing a CIC, maintaining regulatory ratios, ensuring proper documentation—these created barriers that simple investment companies couldn't replicate.

Lesson 5: The Pledge Financing Innovation

Perhaps Holdings' most innovative contribution to Indian corporate finance was perfecting the pledge model. By allowing promoters and group companies to pledge its shares for borrowings while charging fees, Holdings created a triple win: borrowers got financing, lenders got liquid collateral, and Holdings generated income without balance sheet risk.

This wasn't just financial engineering; it was solving a real problem. Indian promoters often have wealth locked in illiquid shares. Banks want to lend but need collateral. Holdings' shares—liquid, valuable, easily monitored—bridged this gap. The pledge fees might seem small at 8% of revenues, but the strategic value of enabling billions in group borrowings was immense.

Lesson 6: When to Hold vs. When to Sell

Holdings' unwavering commitment to holding its JSW Steel stake—despite massive appreciation and persistent holding company discount—teaches important lessons about strategic vs. financial value. A pure financial investor would have sold portions during peak valuations, crystallizing gains and reducing concentration risk. But Holdings understood that the stake's value transcended its market price.

The control premium, the dividend stream, the pledge capacity, the signaling effect—these created value that selling couldn't capture. Moreover, in Indian business culture, selling core holdings signals distress or retreat. By never selling, Holdings signaled confidence in JSW Steel's future, actually enhancing the stake's value.

Lesson 7: Building for Perpetuity, Not Exit

Unlike private equity or venture capital, Holdings operates with no exit horizon. This perpetual capital mindset fundamentally changes investment decisions. A PE fund might avoid steel because of cyclicality; Holdings embraces it because cycles average out over decades. A VC might demand rapid scaling; Holdings accepts gradual capacity building.

This perpetual orientation enabled investments that financial investors couldn't make. Funding a cement plant that takes seven years to optimize, supporting a paint brand that needs a decade to gain market share, maintaining stakes through commodity downturns—these require not just patient capital but perpetual capital.

Lesson 8: The Governance Trade-off

Holdings exemplifies a fundamental trade-off in emerging market capitalism: accepting governance concerns for strategic flexibility. The no-dividend policy, the related-party transactions, the cross-holdings—each creates governance questions but enables strategic value creation. In mature markets with deep capital pools and strong institutions, such trade-offs might not be necessary. But in India's context, they might be essential for building industrial scale.

The lesson isn't that governance doesn't matter—it clearly affects valuations and access to capital. Rather, it's that governance is one variable among many, and optimizing for Western governance standards might sub-optimize for Indian business building.

X. Analysis & Investment Case

Standing at a market capitalization of ₹19,850 crores, JSW Holdings presents one of the most complex investment puzzles in Indian markets. The bull and bear cases are equally compelling, reflecting fundamental tensions between strategic value and shareholder returns, between group interests and minority rights, between potential and reality.

The Valuation Framework Dilemma

Traditional sum-of-parts valuation suggests Holdings should trade at least at the value of its JSW Steel stake (₹19,000 crores) plus its other investments and lending business. Yet the market stubbornly values it barely above the Steel stake alone. This holding company discount reflects multiple factors, but primarily the market's skepticism about value realization.

The P/E ratio of 113 seems astronomical, but it's misleading for a holding company whose earnings don't reflect asset appreciation. Book value per share of ₹28,209 (as per recent data) suggests the stock trades at 0.62 times book—seemingly cheap until you realize the book doesn't capture market values of listed investments. Every valuation metric tells a different story, reflecting the complexity of valuing a company whose worth depends on assets it won't sell and dividends it won't distribute.

The Bear Case: Structural Disadvantages

The pessimistic view starts with governance. With promoter holding at 66.3%, minority shareholders are essentially along for a ride they can't influence. No dividends despite profits, no share buybacks despite cash, no value unlocking despite discounts—management's track record suggests minority interests will remain subordinated to group strategy.

The return metrics paint a sobering picture. Return on equity of 0.97% over three years would be unacceptable for any normal business. Yes, the debt-free balance sheet and unlevered model explain low ROE, but investors seeking returns have better options. Why own Holdings when you could directly own JSW Steel without the holding company discount?

The concentration risk looms large. With essentially all value tied to JSW Steel, Holdings is a leveraged bet on one company in one cyclical sector. If steel markets turn, if China dumps capacity, if Indian growth slows—Holdings would suffer disproportionately. The diversification into cement, paints, and infrastructure doesn't meaningfully reduce this concentration.

The opportunity cost argument resonates. In a market offering numerous growth opportunities, why lock capital in a holding company with structural disadvantages? The same capital invested in quality mid-caps or even JSW Steel directly would likely generate superior returns without governance concerns.

The Bull Case: Hidden Value and Optionality

The optimistic view sees Holdings as one of India's most undervalued assets. Trading at a 30-40% discount to just its JSW Steel stake, investors get the lending business, other investments, and strategic value essentially for free. This discount won't persist forever—eventually, through dividends, buybacks, or restructuring, value will be unlocked.

The debt-free balance sheet provides enormous flexibility. In a crisis, Holdings could leverage up, unlock billions in capital without selling assets. This dry powder, combined with proven execution capabilities, positions Holdings to capitalize on distressed opportunities or fund aggressive expansion when others can't.

The earnings trajectory supports optimism. JSW Steel's capacity expansion from 29.7 MTPA to 42 MTPA by 2027 should drive significant value appreciation. Every tonne of capacity added, every efficiency improvement, every market share gain directly benefits Holdings. With steel demand expected to grow with India's infrastructure buildout, the best years may be ahead.

The optionality on new ventures offers asymmetric upside. JSW Paints could become a multi-billion dollar business. Green hydrogen and electric vehicle plays could transform portfolios. The infrastructure assets could be monetized through InvITs. Holdings provides exposure to these options without the execution risk borne by operating companies.

Comparative Analysis: Learning from Peers

Comparing Holdings to other Indian conglomerates' holding companies provides context. Tata Investment Corporation trades at similar discounts despite the Tata pedigree. Bajaj Holdings offers regular dividends but still trades below NAV. International comparisons—Berkshire Hathaway, Investor AB, Pargesa—show holding company discounts persist globally but narrow with improved governance and capital allocation.

The key differentiator is Holdings' strategic role within JSW Group. Unlike pure investment holdings, it actively enables group expansion through lending and guarantees. This operational involvement, while creating governance concerns, also generates value beyond passive investing.

Scenario Analysis: Potential Catalysts

Several scenarios could unlock value:

- Dividend Declaration: Even a modest dividend would signal shareholder-friendliness, potentially narrowing the discount significantly.

- Stake Sale: Partial sale of JSW Steel stake to fund dividends or new ventures would crystallize value and improve liquidity.

- Restructuring: Merging Holdings with JSW Steel or spinning off the lending business could eliminate the holding structure discount.

- Governance Improvements: Independent board members, minority shareholder protections, transparent capital allocation could rerate the stock.

Conversely, several scenarios could worsen the discount:

- Steel Downturn: A prolonged steel bear market would disproportionately impact Holdings given its concentration.

- Governance Deterioration: More aggressive related-party transactions or value-destructive investments would further alienate minorities.

- Regulatory Changes: Tighter CIC regulations or tax changes could impair Holdings' business model.

The Investment Decision Framework

For long-term fundamental investors, Holdings presents a complex proposition. Those believing in India's infrastructure story, JSW's execution capabilities, and eventual value unlocking might find the current discount attractive. The key is time horizon—this isn't a quarter or even year play, but a decade-long bet on Indian industrialization.

For governance-focused investors, Holdings remains uninvestible regardless of valuation. The track record of minority shareholder treatment, the structural subordination to group interests, and the lack of clear value unlocking path make it incompatible with ESG mandates.

For traders and arbitrageurs, Holdings offers opportunities. The high correlation with JSW Steel but higher beta creates pair trading possibilities. The persistent but variable discount enables mean reversion strategies. The low liquidity and high volatility suit nimble traders.

XI. Epilogue & Future Scenarios

As monsoon clouds gather over Mumbai's skyline, the JSW Holdings story enters its third decade with more questions than answers. The company that began as a modest NBFC has evolved into a ₹20,000 crore entity sitting at the nexus of one of India's most ambitious industrial expansions. Yet its future remains as complex as its structure—pulled between the competing forces of strategic value creation and shareholder value realization.

The next chapter is already being written in boardrooms and steel plants across India. JSW's aggressive push into electric vehicles through partnerships and joint ventures will require patient capital that traditional lenders won't provide. The group's green energy ambitions—from hydrogen production to renewable power generation—demand upfront investments with uncertain returns. The infrastructure opportunities emerging from India's $1.4 trillion national infrastructure pipeline present possibilities that only patient, flexible capital can capture.

Holdings finds itself uniquely positioned for this future. Its debt-free balance sheet provides firepower for new ventures. Its proven ability to support long-gestation projects offers competitive advantages in sectors where others fear to tread. Its strategic stakes in mature businesses generate cash flows to fund tomorrow's growth engines.

Yet the fundamental tensions remain unresolved. How long can Holdings maintain its no-dividend policy as institutional ownership increases? Will regulatory evolution force greater transparency and minority protection? Can the holding company discount persist as India's capital markets mature?

Three scenarios could define Holdings' evolution:

Scenario 1: The Status Quo Persistence Holdings continues its current model—funding group expansion, maintaining strategic stakes, ignoring minority concerns. The stock continues trading at discounts, but absolute value creation from underlying asset appreciation rewards patient shareholders. This scenario sees Holdings as a perpetual enabler, valuable to the group but frustrating to minorities.

Scenario 2: The Governance Revolution Pressure from institutional investors, proxy advisors, and regulators forces change. Holdings initiates regular dividends, improves disclosure, perhaps even considers strategic alternatives like merging with JSW Steel or spinning off businesses. The holding company discount narrows dramatically, unlocking billions in value. This scenario transforms Holdings from group vehicle to shareholder-friendly investment.

Scenario 3: The Strategic Transformation Holdings evolves beyond its traditional role, becoming JSW's vehicle for new economy investments. It leads the group's ventures into technology, sustainability, and consumer businesses. The market rerates Holdings not as a steel proxy but as an innovation platform. This scenario sees Holdings transcending its industrial heritage to become a bridge to JSW's digital future.

The lessons from JSW Holdings extend beyond one company or group. They illuminate fundamental questions about Indian capitalism: How do family-owned businesses balance control with capital access? Can governance standards evolve without sacrificing entrepreneurial flexibility? Will India's holding companies remain anachronisms or become sophisticated capital allocators?

For founders building conglomerates, Holdings offers both inspiration and caution. The structure enabled JSW to build scale without losing control, to take risks without endangering operating companies, to be patient in a market demanding immediacy. But it also created persistent valuation discounts, governance concerns, and stakeholder tensions that limit access to capital and talent.

The role of holding companies in emerging markets remains contested but crucial. In markets where credit is scarce, regulations are complex, and relationships matter, holding companies provide solutions that pure market mechanisms cannot. They enable industrial development that dispersed shareholding might prevent. They provide stability that quarterly capitalism might destroy.

As India aims to become a $10 trillion economy by 2035, companies like JSW Holdings will play pivotal roles. They'll channel domestic savings into productive assets. They'll enable infrastructure development that transforms economic potential into reality. They'll bridge the gap between family enterprises and professional corporations.

The JSW Holdings story ultimately isn't about steel or cement or even money. It's about the architecture of ambition—how financial structures enable or constrain industrial dreams. It's about the tensions inherent in public markets—between concentration and diversification, control and governance, patience and performance.

As we close this analysis, JSW Holdings remains what it's always been: a paradox wrapped in an enigma, delivering spectacular returns while frustrating shareholders, creating enormous value while trading at persistent discounts, essential to its group while misunderstood by markets. Perhaps that's the most important lesson—in emerging markets, the most interesting companies are often the most complex, defying simple narratives while building extraordinary value.

The market will eventually resolve these tensions through price discovery, regulatory evolution, or strategic action. Until then, JSW Holdings stands as a testament to both the possibilities and perils of conglomerate finance in India—a ₹20,000 crore question mark that embodies the complexities, contradictions, and tremendous potential of Indian capitalism itself.

For investors, entrepreneurs, and students of business, JSW Holdings offers no easy answers but invaluable lessons. It reminds us that value creation and value capture are different things, that strategic worth and market price can diverge for decades, and that in the grand chess game of building industrial empires, the holding company might just be the most powerful piece on the board—even if it's also the most misunderstood.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube