Jindal Stainless: India's Stainless Steel Pioneer

I. Introduction & Episode Roadmap

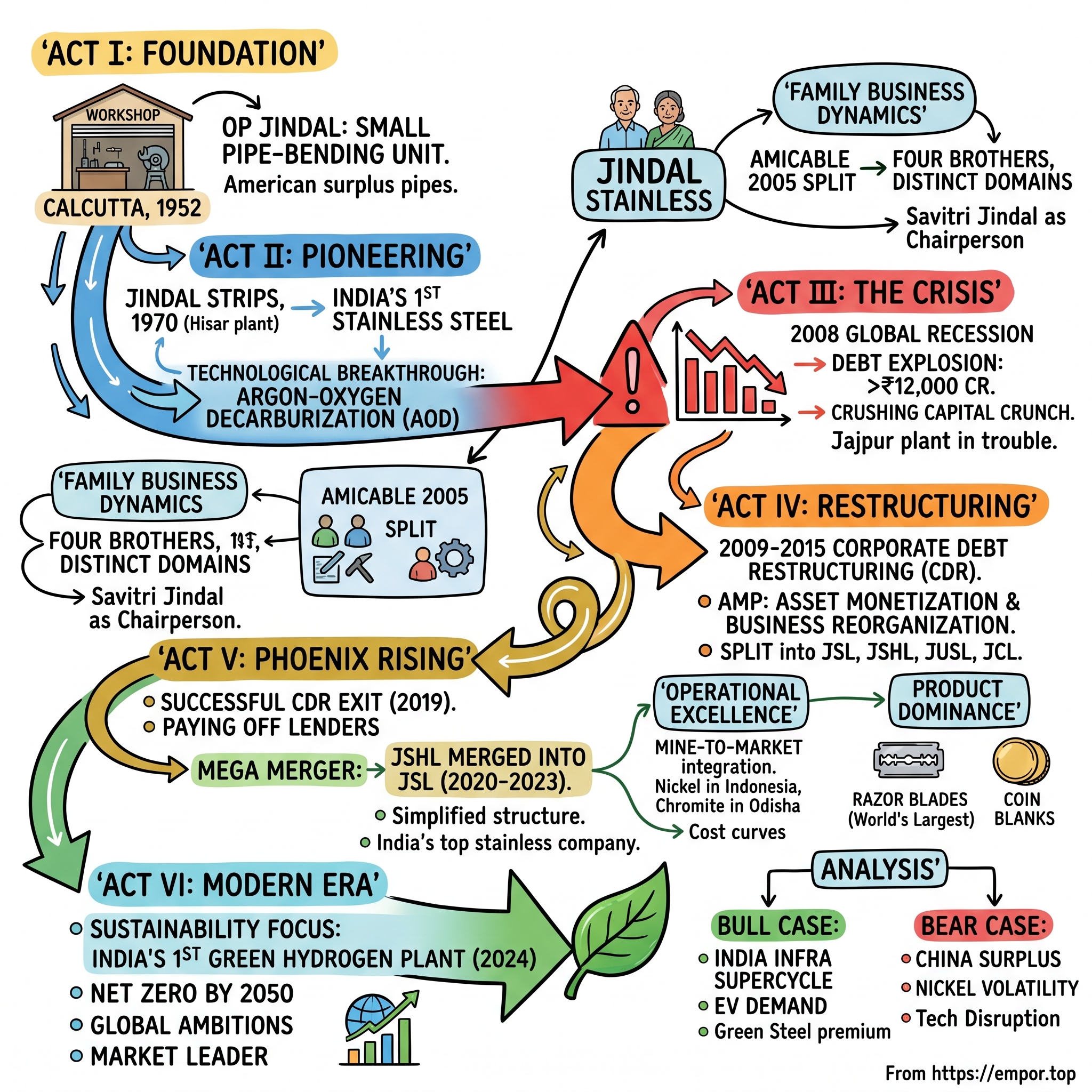

Picture this: A small pipe-bending workshop in Calcutta's industrial suburb of Liluah, 1952. The air thick with coal dust from nearby factories, the clang of metal on metal echoing through corrugated tin walls. A young Om Prakash Jindal, barely 22, watches American surplus pipes being unloaded—remnants of World War II that would become the foundation stones of one of India's greatest industrial empires.

Fast forward seven decades. That humble workshop has morphed into Jindal Stainless Limited, India's undisputed stainless steel champion commanding 52% domestic market share. With ₹40,182 crore in revenue for FY2025 and operations spanning from Haryana to Odisha to Indonesia, JSL sits among the global top ten stainless steel producers. The company transforms 2.9 million tonnes of raw materials annually into everything from razor blades to railway coaches, from kitchen utensils to architectural marvels.

But here's what makes this story particularly fascinating: Unlike the typical Indian conglomerate tale of licenses and connections, this is fundamentally an engineering story. A story of technological breakthroughs, of bringing Argon-Oxygen Decarburization to India when nobody believed it could work, of surviving a crushing debt crisis that would have killed most companies, and ultimately of a complex merger that created a vertically integrated powerhouse.

The question we're exploring today isn't just how a trading operation became a manufacturing giant—it's how a company in one of the world's most capital-intensive, cyclical industries managed to not just survive but thrive through liberalization, globalization, and multiple economic crises. How did they crack the code on competing with Chinese imports while building a green hydrogen plant in Haryana? And what does their journey tell us about the future of Indian manufacturing?

This is a story with four distinct acts: the foundation years under OP Jindal, the technological revolution that created India's stainless steel industry, the near-death experience of overleveraging, and the phoenix-like rise through strategic restructuring. Along the way, we'll meet wrestlers-turned-industrialists, encounter midnight board meetings that saved the company, and discover how a family split actually strengthened rather than weakened the enterprise.

II. The OP Jindal Foundation Story

The year is 1930. In the dusty village of Nalwa in Haryana's Hisar district, a boy named Om Prakash is born into a farming family. His father, Netram Jindal, runs a small trading business on the side. Young Om Prakash shows more interest in the wrestling akhara than the family fields—he becomes a formidable wrestler, his physical strength matched only by his mental toughness. These early morning wrestling sessions, where strategy matters as much as strength, would shape his approach to business decades later.

At seventeen, with partition's chaos engulfing the subcontinent, Om Prakash makes a decision that changes everything: he boards a train to Calcutta with just ₹500 in his pocket. The city in 1947 is a cauldron of opportunity and chaos—refugees pouring in, new businesses sprouting overnight, the British industrial infrastructure suddenly up for grabs. Om Prakash starts small, trading in scrap metal and surplus goods. But his real breakthrough comes in 1952 when he spots an opportunity others missed.

The Americans are liquidating massive stockpiles of military surplus from their World War II operations in the CBI (China-Burma-India) theater. Among the detritus: thousands of tonnes of steel pipes. While others see junk, Om Prakash sees raw material. He doesn't just trade these pipes—he sets up a small unit to bend, cut, and reshape them for India's nascent industrial sector. This isn't mere trading; it's value addition, transformation, manufacturing. The distinction matters because it establishes a pattern: the Jindals would always be makers, not just traders.

By the 1960s, Om Prakash has built a thriving business and a family—four sons who would each inherit a piece of what becomes the Jindal empire. The split, when it comes after his death in 2005, is remarkably amicable by Indian business family standards. Sajjan gets JSW Steel, Prithviraj takes Jindal Steel & Power, Naveen keeps Jindal SAW, and Ratan—the focus of our story—inherits what becomes Jindal Stainless.

But we're getting ahead of ourselves. The real pivot comes in 1970 when Om Prakash makes his boldest move yet. India's steel industry is dominated by government-owned giants like SAIL. Private players are restricted, licenses are hard to come by, and the conventional wisdom says small private companies can't compete in steel. Om Prakash disagrees. He establishes Jindal Strips Limited in Hisar—not in an established industrial hub, but in the heartland of Haryana, close to his roots. The industrial context deserves special attention. In 1970, a mini steel plant is established as Jindal Strips Limited at Hisar, which produces hot rolled carbon steel coils, plates, slabs and blooms. This marks the birth of not just Jindal Stainless, but the entire OP Jindal Group of Companies. India in 1970 is deep in the License Raj—every tonne of production needs government approval, every expansion requires navigating Byzantine bureaucracy. Private players in steel are viewed with suspicion. Yet Om Prakash persists, driven by a simple belief: India needs to make its own steel, not import it.

The family dynamics add another layer. Before his death in a helicopter crash in 2005, Jindal divided his businesses among his four sons with cross-holdings to ensure mutual benefit. To maintain family unity, his wife, Savitri Jindal, was appointed chairperson. Unlike the acrimonious splits that plague many Indian business families, the Jindal division is strategic, almost surgical. Each brother gets a distinct vertical—Sajjan builds JSW into a behemoth, Naveen focuses on power and coal, Prithviraj takes the pipe business, and Ratan inherits what will become the stainless steel crown jewel.

What's remarkable about Om Prakash's journey is how he embodied the post-independence industrial spirit. This wasn't about quick profits or financial engineering—it was nation-building through manufacturing. When he started, India imported virtually all its stainless steel. By the time of his death, the foundations were laid for domestic self-sufficiency. The wrestler from Nalwa had become one of India's industrial titans, but more importantly, he had shown that Indian private enterprise could compete in the most capital-intensive sectors. His legacy wasn't just the companies he built, but the industrial ecosystem he helped create—from raw material suppliers to fabricators, from engineers to metallurgists.

III. Birth of India's Stainless Steel Industry (1970–1980s)

The scene shifts to 1978. Inside the Hisar plant, a group of engineers huddle around a new piece of equipment that looks like something from a science fiction movie—a massive vessel with pipes snaking in every direction, gauges and valves covering every surface. This is India's first Argon-Oxygen Decarburization (AOD) converter, and nobody is quite sure if it will work. PR Jindal, Om Prakash's brother and the technical brain of the operation, has staked his reputation on this German technology that promises to transform regular steel into stainless steel through a precise dance of chemistry and heat.

Under the guidance of OP Jindal, PR Jindal introduces Argon-Oxygen Decarburization (AOD), a major breakthrough in stainless steel technology. India witnesses its first indigenously manufactured stainless steel. The significance of this moment cannot be overstated. Before 1978, every piece of stainless steel in India—from surgical instruments to kitchen utensils—was imported. The foreign exchange drain was massive, the dependence complete.

The AOD process is deceptively complex. You blow oxygen and argon through molten steel at precisely controlled rates, removing carbon while preserving chromium—the element that makes steel "stainless." Get it wrong, and you have expensive scrap. Get it right, and you've cracked the code to one of metallurgy's most valuable transformations. PR Jindal and his team spent months calibrating, failing, adjusting. When the first batch of genuine stainless steel emerged—gleaming, corrosion-resistant, meeting international specifications—it was like watching alchemy turn real.

But making stainless steel was only half the battle. Convincing customers to buy it was another war entirely. Indian manufacturers had grown accustomed to imported steel from Japan and Europe. The Jindal name meant nothing in stainless steel. Quality was questioned at every turn. The company's salespeople faced a standard response: "Why should we risk our production on your experiment?"

The breakthrough came from an unexpected quarter: razor blades. Gillette and other manufacturers needed ultra-thin, ultra-precise stainless steel strips. The tolerances were measured in microns, the quality requirements unforgiving. If Jindal could crack this market, it would prove their technical credentials beyond doubt. By 1981, after countless iterations and quality improvements, they did it. Today, Jindal Stainless is world's largest producer of razor blade grade of stainless steel—but that dominance started with those first tentative shipments to skeptical blade manufacturers.

The Company's stainless steel products gain popularity with quality standards par with imported stainless steel. Company installs and expands its downstream facilities. The 1980s became a decade of steady expansion and credibility building. From razor blades, they moved to coin blanks—another high-precision application where quality failures were immediately visible. The Reserve Bank of India's approval to supply coin blanks was more than a commercial victory; it was a stamp of trust from the nation's most quality-conscious institution.

The technical achievements masked intense financial pressure. Every expansion required capital the company didn't have. Banks were skeptical of private steel ventures. The solution was classic bootstrap financing—plow every rupee of profit back into the business, live lean, think long-term. The Jindal family's lifestyle remained modest even as the business grew. Om Prakash was known to scrutinize every expense, questioning the need for air conditioning in offices while ensuring the factory floor had the best equipment money could buy.

By decade's end, Jindal Strips (as it was still known) had established a template that would define its future: technical excellence over marketing flash, vertical integration over trading margins, and patient capital allocation over quick returns. The company was producing 50,000 tonnes annually—a rounding error by global standards, but a revolution by Indian ones. More importantly, they had proven that India could produce world-class stainless steel. The import substitution dream was becoming reality, one heat at a time.

IV. Scaling Up: From Regional to National Player (1990s–2000s)

July 1991. Finance Minister Manmohan Singh rises in Parliament to present a budget that will reshape India's economic destiny. License Raj is dismantled overnight. Import duties crash. Foreign companies can now enter India. For Jindal Stainless, liberalization is both existential threat and unprecedented opportunity. Suddenly, they're not competing with import duties and quotas—they're competing with Outokumpu, Acerinox, and POSCO on pure merit.

Ratan Jindal, who had taken operational control from his father, saw liberalization differently than his peers. While others feared foreign competition, he saw a chance to learn, to benchmark, to leapfrog. His first move was counterintuitive: instead of circling the wagons, he went on an acquisition spree. In 1992, when Piramal was exiting the steel business, Jindal swooped in, acquiring their stainless steel unit. The price was steep, the debt burden significant, but the strategic logic was clear—scale would be the only defense against global giants.

The IPO in 1986 had already provided some growth capital, but the real transformation came with a series of strategic pivots. First, the company officially became Jindal Stainless Limited in 2002, shedding the generic "Strips" moniker for a name that declared its specialization. This wasn't just rebranding—it was a statement of intent. While competitors diversified into carbon steel, aluminum, and other metals, Jindal would go deep, not wide. The boldest move came in 2003-2004. Ratan Jindal sets the ball rolling for setting up of a 3.2 million tonnes integrated stainless steel project at Kalinga Nagar Industrial Complex in Jajpur District of Odisha. The facilities are installed in two phases over next several years. This wasn't just expansion—it was a bet-the-company move. The Jajpur project would quadruple capacity, but at a cost that would strain every financial sinew. The location choice was strategic: Odisha had iron ore, coal, and chromite. The state government was offering land and incentives. But most importantly, it was virgin territory for stainless steel—no legacy infrastructure to work around, no old mindsets to change.

The international expansion followed a different logic. Jindal Stainless establishes its foothold in the South East Asian & Oceania markets with the acquisition of a stainless steel Cold Rolling Plant in Indonesia. Indonesia had nickel—the critical input for stainless steel. By establishing operations there, Jindal wasn't just accessing markets; they were securing raw material supply chains. This forward-thinking approach to resource security would prove prescient when nickel prices exploded in later years.

The product portfolio evolution tells its own story of ambition. By 1991, Jindal had become the sole manufacturer of stainless steel razor blades in India—a position they leveraged into global dominance. The coin blank business was another masterstroke. Back in 1998, Jindal Stainless Hisar received a call from enquiring if Jindal Stainless would be interested in the Minting Business, that is, in producing Coils for the India Government Mint (IGM). The present Chairman of Jindal Stainless, Mr Ratan Jindal, along with his colleagues, decided to grab the offer with both hands. By 2015, they were supplying to mints globally, including the prestigious French Mint.

The 2000s also saw Jindal embrace a philosophy that would define its next phase: "Mine to Market." This wasn't just about vertical integration—it was about controlling every link in the value chain. They acquired chromite mines in Odisha, set up ferroalloy plants, established service centers across India, and even ventured into lifestyle products through Arttd'inox. Each move reduced dependence on external suppliers and captured more margin.

But beneath this expansion lay a ticking time bomb. The debt taken for the Jajpur project was predicated on certain assumptions about demand growth, steel prices, and interest rates. When the 2008 global financial crisis hit, all three assumptions shattered simultaneously. The ripple effect of the global economic recession of 2008 could be seen on all industries, and stainless was no exemption. Even though the Hisar facility of Jindal Stainless group weathered the storm well, the Jajpur (Odisha) unit of the group, which was in its incipient phase of commissioning and trials, went into the red. The stage was set for the company's darkest hour—and its most dramatic restructuring.

V. The Debt Crisis & CDR Restructuring (2008–2015)

The boardroom at Jindal Stainless headquarters in December 2008 felt like a war room. Balance sheets covered the table, each one painting a grimmer picture than the last. The Jajpur plant, meant to be the crown jewel, had become an albatross. Global stainless steel prices had crashed 40%. Demand evaporated as construction projects worldwide froze. Interest rates spiked. The company's debt stood at over ₹12,000 crore against an EBITDA that was rapidly shrinking.

Ratan Jindal faced a choice that would define his legacy: declare bankruptcy and lose everything his father built, or attempt one of Indian corporate history's most complex restructurings. He chose to fight. The Corporate Debt Restructuring (CDR) framework became JSL's lifeline. The firm had entered the CDR framework back in 2009. But the real drama unfolded between 2014-2015. After having various rounds of discussion with the Corporate Debt Restructuring (CDR) cell, the company and lenders came up with Asset monetization cum business reorganisation plan (AMP) – to split the company into three units through demerger/slump sale(s) and utilization of the proceeds of the slump sale (s) in deleveraging the company by an amount of approx. 5,500 Crore.

The restructuring plan was audacious in its complexity. The Composite Scheme of Arrangement (Scheme) among Jindal Stainless Ltd and Jindal Stainless (Hisar) Ltd and Jindal United Steel Limited and Jindal Coke Ltd and their respective Shareholders and Creditors was approved by the Board of Directors (Board) in its meeting held on 29 December 2014. Essentially, they would split the company into four entities, each taking a portion of the debt:

- Jindal Stainless Limited (JSL) would keep the crown jewel Jajpur stainless steel operations

- Jindal Stainless Hisar Limited (JSHL) would get the Hisar plant, ferro alloys, and mining divisions with ~₹2,600 crore debt

- Jindal United Steel Limited (JUSL) would take the hot strip mill with ~₹2,400 crore debt

- Jindal Coke Limited (JCL) would operate the coke ovens with ~₹500 crore debt

The financial engineering was intricate. JSL will also transfer its business undertaking relating to the Hisar Unit to JSHL for ~Rs 2809 crore. Transfer of Business Undertaking 2 of the Company comprising, inter-alia, the hot strip plant of the Company located at Odisha and vesting of the same with Jindal United Steel Ltd ("JUSL") on a going-concern basis by way of a Slump Sale for a lump sum consideration of ~Rs. 2413 Crs. Transfer of Business Undertaking 3 of the Company comprising, inter-alia, the coke oven plant of the Company located at Odisha and vesting of the same with Jindal Coke Ltd on a going-concern basis by way of a Slump Sale for a lump sum consideration of ~Rs. These weren't just paper transactions—each entity would operate independently, sink or swim on its own merits.

The years 2013-2015 were brutal. Operations continued, but every decision was scrutinized by lenders. Capital expenditure froze. Talent fled to competitors. Market share eroded as customers worried about supply continuity. The promoters showed their commitment by infusing capital multiple times—₹100 crore here, ₹100 crore there—but it felt like throwing water on a forest fire.

Under Jindal's leadership, JSL underwent Corporate debt restructuring (CDR) in 2013 following economic challenges that impacted loan repayments, with debts amounting to nearly ₹8,000 crore. As part of this process, JSL's debt was redistributed among three entities, Jindal Stainless (Hisar) Limited, Jindal United Steel Limited, and Jindal Coke Limited.

What saved them wasn't just financial restructuring but operational excellence. The separated entities could focus on their core competencies. The Hisar plant optimized for specialty grades. The hot strip mill at JUSL started processing carbon steel alongside stainless, improving capacity utilization. The coke ovens doubled output by recycling by-products. Each improvement was marginal, but collectively they transformed the economics.

The human dimension often gets lost in restructuring stories. Ratan Jindal, then in his sixties, personally visited every plant, every shift, explaining why the pain was necessary. Middle managers who could have jumped ship stayed, motivated by a mixture of loyalty and the promise that if they could weather this storm, they'd emerge stronger. The next generation also stepped up—After a brief period as a consultant at Boston Consulting Group (BCG), Jindal joined Jindal Stainless Limited as Vice Chairman in November 2015. Later, Jindal was appointed Managing Director of Jindal Stainless Limited in 2018.

By 2017, the first signs of recovery appeared. Global stainless steel prices recovered. The government imposed anti-dumping duties on Chinese imports. Domestic demand picked up as infrastructure spending increased. Soon the restructuring paid off and in FY 2016-17, JSL declared net profit for the first time in its history. But the CDR overhang remained until that triumphant moment in March 2019.

VI. The Phoenix Rising: Exit from CDR & Mega Merger (2015–2023)

March 31, 2019. The conference room erupts in celebration. Jindal Stainless Limited (JSL), India's largest stainless steel manufacturer, announced its successful exit from the Corporate Debt Restructuring (CDR) framework with effect from March 31, 2019. The company successfully exited the Corporate Debt Restructuring framework on 31 March 2019. A decade of financial purgatory had ended. JSL said it has already re-compensated existing lenders to about Rs 275 crore in cash which will reflect in their income in the current fiscal while it has fully redeemed the outstanding Optionally Convertible Redeemable Preference Shares (OCRPS), which were issued to the lenders in June 2017 paying them around Rs 558 crore in the process. The two put together JSL has paid an aggregate Rs 833 crore to its lenders.

But Ratan Jindal and his team weren't content with mere survival. The restructuring had created an unwieldy corporate structure—multiple listed entities, complex cross-holdings, operational inefficiencies from the forced split. The solution was as bold as the original restructuring: reverse it through a mega-merger. December 29, 2020 marked the beginning of the reversal. The Boards of Jindal Stainless Limited (JSL) and Jindal Stainless (Hisar) Limited (JSHL) today approved the merger of JSHL into JSL in a share swap ratio of 1:1.95. As per the approved share swap ratio, 195 equity shares of JSL will be issued for every 100 equity shares of JSHL. The merger of JSHL in to JSL will induce a simplified capital structure, expanding the turnover of the merged business to Rs 20,000 crore. With 1.9 MTPA melt capacity, the merged entity will be the only Indian company in the league of top 10 stainless steel companies in the world.

The strategic rationale was compelling. The demerger had served its purpose—helping the company survive the debt crisis. But operating as separate entities created inefficiencies. Raw materials couldn't be optimally allocated. Customer relationships were fragmented. Investment decisions lacked coordination. The merger would create an integrated entity with enhanced downstream capabilities, rationalise operational and management efficiency, and create a diversified end-to-end product portfolio including 120+ stainless steel grades.

Abhyuday Jindal, who had been appointed Managing Director of Jindal Stainless Limited in 2018, brought fresh energy to the merger process. He addressed supply chain inefficiencies by implementing a dual inventory management approach, shifting from a 'Made to Order' model to an 'Anticipation of Stock' approach. This wasn't just operational tinkering—it was reimagining how a commodity business could operate like a consumer goods company.

The merger timeline stretched over three years, navigating regulatory approvals, shareholder votes, and court proceedings. JSHL has fixed Thursday, March 9, 2023, as the record date for its merger with JSL. The culmination was anticlimactic in the best way—no drama, just the quiet satisfaction of undoing what crisis had forced upon them. Strategic acquisitions accelerated the transformation. Earlier this year, Jindal Stainless acquired Rathi Super Steel, which was grappling with debt issues, for approximately Rs 2 billion through the debt resolution process. After the successful acquisition of Rathi Super Steel Ltd, Jindal Stainless has begun production in the facility ahead of the planned timelines. Strengthening the Company's solution-oriented approach and widening its product offerings, this move will add Long Products like wire rods and rebars to the Company's existing product portfolio. This wasn't just buying assets—it was entering an entirely new product category targeting infrastructure demand.

The international nickel investment represents perhaps the boldest strategic move. The Collaboration Agreement with New Yaking Pte Ltd made JSL the first Indian company to invest in Nickel Pig Iron abroad (Indonesia), while the merger process of JSL and JSHL also achieved fruition. With nickel prices volatile and supply concentrated in a few countries, securing upstream access was critical for long-term competitiveness.

The financial transformation was equally dramatic. The Company has seen an improvement in the net debt-equity ratio which stood at 1.3 as on December 31, 2019, as compared to 3.2 as on March 2017. From a company gasping under debt to one with the financial flexibility to make strategic acquisitions—the journey was complete. CARE raises Jindal Stainless' credit rating to AA, with a Stable Outlook, reflecting the market's renewed confidence.

By 2023, the restructuring saga had come full circle. Acquisition of 74% holding of JUSL by JSL is also progressing as planned. This will be completed within the committed timelines, post which, JUSL will become a 100% owned subsidiary of JSL. The company that had been forcibly split was being methodically reassembled, but stronger, more focused, and with a clearer strategic vision than ever before.

VII. Modern Era: Sustainability & Global Ambitions (2020s–Today)

The scene opens at the Hisar plant in March 2024. Union Steel Minister Jyotiraditya Scindia stands before a gleaming array of pipes and vessels—India's first green hydrogen plant in the stainless steel sector. No coal, no coke, just water splitting into hydrogen and oxygen through renewable electricity. It's a moment that would have seemed like science fiction to Om Prakash Jindal, yet perfectly embodies his vision of Indian industrial self-reliance. Jindal Stainless (JSL) announced it has commenced the maiden usage of green hydrogen in the company's stainless steel plant in Hisar, Haryana, from what is India's first commercial-scale GH2 plant in the steel sector. JSL has set up a fully automated production unit in association with Hygenco Green Energies, which operates the plant under the build-own-operate model. The facility aims to abate around 54,000 tonnes of CO2 emissions over 20 years through the use of green hydrogen in its manufacturing processes.

The sustainability push isn't just about hydrogen. With a significant reduction of approximately 240,000 tonnes of CO2e over the past two fiscal years (FY22 and FY23), Jindal Stainless is well on its way to achieving its midterm goal of a 50% reduction in carbon emissions well ahead of the 2035 target year and Net Zero by 2050. The company manufactures stainless steel using scrap in an electric arc furnace, the least greenhouse gas emission route since it enables 100% recyclability with no reduction in quality. The financial performance reflects this transformation. On a standalone basis, net revenue rose by 5% YoY, at INR 40,182 crore. Mkt Cap: 58,747 Crore. The market capitalization tells its own story—from near-bankruptcy to becoming one of India's most valuable steel companies. The company recorded sales at 23,73,070 tonnes, a jump of 9% over FY24, demonstrating robust volume growth even as global markets remain volatile.

The product portfolio evolution shows how far the company has come from its razor blade origins. The company's product range includes stainless steel slabs, blooms, coils, plates, sheets, precision strips, wire rods, rebars, blade steel, and coin blanks. Today, they serve everything from satellite launch vehicles to electric buses. JSL's strategic arm, Jindal Defence and Aerospace (JDA), successfully developed and supplied for the first time 3 mm special alloy steel sheets for structural application in the Supersonic Missile-Assisted Release of Torpedo (SMART) system, aimed at enhancing the Indian Navy's anti-submarine warfare capabilities.

The capacity expansion plans are equally ambitious. India's leading stainless-steel manufacturer, Jindal Stainless, had a consolidated annual turnover of INR 38,562 crore (USD 4.7 billion) in FY24 and is ramping up its facilities to reach 4.2 million tonnes of annual melt capacity in FY27. With an investment of approximately INR 715 crore, company has entered a JV to develop and operate a stainless steel melt shop in Indonesia with an annual production capacity of 1.2 million tonnes per annum.

The competitive landscape remains challenging. Chinese and Vietnamese imports continued to challenge India's stainless steel industry, accounting for over 70% of total imports in this fiscal, with low-priced stainless steel often rerouted through ASEAN countries, including Vietnam. While FY25 saw a 7% YoY rise in imports from China, imports from Vietnam surged by 176% in FY25. Yet Jindal's response isn't protectionism but innovation—competing on quality, sustainability, and customer relationships rather than just price.

What's particularly striking is how sustainability has become a competitive advantage rather than a compliance burden. Corporate Carbon Footprints were reduced by ~15% in FY25, achieved through ongoing decarbonisation initiatives. Jindal Stainless published its first Taskforce on Nature-related Financial Disclosure (TNFD) Report in FY25, the first of its kind in the Indian iron and steel sector. In an industry often seen as environmentally problematic, Jindal is positioning itself as part of the solution.

The leadership transition also deserves attention. Abhyuday Jindal, the third generation, brings a different sensibility—Boston University educated, ex-BCG consultant, but equally comfortable on the factory floor. His initiatives like co-branding programmes and loyalty schemes are redefining customer engagement and operational agility. The Stainless Academy initiative, which has successfully trained over 9,000 fabricators across India, shows a sophisticated understanding that in commodities, ecosystem development matters as much as production capacity.

VIII. Playbook: Business & Investing Lessons

The Jindal Stainless journey offers a masterclass in navigating commodity cycles, but the lessons go far beyond the typical "buy low, sell high" platitudes. Let's dissect the strategic moves that separated survivors from thrivers.

The Power of Vertical Integration in Commodities

Most commodity businesses talk about vertical integration; Jindal Stainless weaponized it. When nickel prices spiked 300% in 2007, companies buying on spot markets hemorrhaged cash. Jindal's Indonesian nickel investments, chromite mines in Odisha, and ferroalloy plants weren't just about margin capture—they were about survival during volatility. The lesson: in commodities, your supply chain is your lifeline. Control it or it controls you.

But here's the nuance most miss: vertical integration only works if you can operate each segment at world-class efficiency. Jindal didn't just own mines; they ran them better than mining companies. Their ferroalloy operations compete with specialized producers. Each vertical delivered standalone returns while providing strategic control. That's the difference between conglomerate sprawl and strategic integration.

Surviving and Thriving Through Debt Crises

The 2008-2019 debt crisis could have been a obituary. Instead, it became a case study in financial engineering. The key insight: when you can't pay debt, restructure the business, not just the balance sheet. The demerger wasn't financial shuffling—it created focused entities that could optimize independently. JSHL mastered specialty grades. JUSL maximized asset utilization by adding carbon steel. Each entity's improved economics made the consolidated debt serviceable.

The promoter commitment mattered enormously. The Jindal family infused capital repeatedly when easier options existed—selling to competitors, letting lenders take control, or simply walking away. This skin in the game signaled to lenders that recovery was possible, buying time for operational improvements to deliver results. Patience capital in impatient times.

Family Business Dynamics: Managing Splits and Succession

The 2005 split of the OP Jindal empire could have been catastrophic. Instead, it became multiplicative. Each brother got a domain where they could build without interference. The cross-holdings ensured cooperation where needed but independence where it mattered. Compare this to the Ambani brothers' destructive competition or the Bajaj family feuds.

The succession to third generation—Abhyuday taking over from Ratan—happened smoothly because it was gradual and merit-based. Abhyuday worked at JSW (cousin Sajjan's company), then BCG, before joining the family business. He proved himself before inheriting. The lesson: in family businesses, nepotism is a luxury you can't afford in competitive industries.

Import Substitution to Export Excellence

Jindal's journey from import substitution to global competitiveness offers lessons for industrial policy. They didn't rely on protective tariffs forever. Instead, they used the breathing room to achieve global cost curves and quality standards. When liberalization came in 1991, they were ready to compete, not hide.

The focus on technical excellence over financial engineering matters. While peers played stock market games, Jindal invested in AOD converters, precision rolling mills, and quality certifications. They built capabilities that compound—technical knowledge, customer relationships, operational excellence. These intangibles don't show on balance sheets but determine competitive advantage.

Capital Allocation Through Cycles

The timing of Jindal's major moves reveals sophisticated cycle thinking. The Jajpur expansion in 2003-2004 came during China's commodity boom when funding was available and demand visible. The debt restructuring happened when everyone was distressed, giving them negotiating leverage. The JSHL merger in 2020-2023 occurred when markets recovered but before valuations peaked.

But they also made counter-cyclical moves. Acquiring Rathi Super Steel during bankruptcy, investing in green hydrogen before carbon taxes, expanding in Indonesia before nickel prices recovered—these weren't consensus trades. The pattern: be pro-cyclical on operations (expand when demand is visible) but counter-cyclical on assets (buy when distressed).

The Merger as a Value Creation Tool

The JSHL-JSL merger wasn't just unwinding the demerger—it was value creation through simplification. Public market investors hate complexity. Multiple listed entities, cross-holdings, related-party transactions—all create a "complexity discount." The merger eliminated this, likely adding 20-30% to valuation just through structure simplification.

The 1:1.95 swap ratio was also masterful. JSHL shareholders got a premium, but JSL shareholders got a simpler, larger, more liquid entity. Both won because the pie expanded. This positive-sum thinking in what's often a zero-sum negotiation shows sophisticated deal-making.

ESG as Competitive Advantage in Steel

While peers treat environmental compliance as a cost, Jindal turned it into strategy. The green hydrogen plant isn't just about emissions—it's about being ready for carbon border taxes, attracting ESG-focused customers, and accessing green financing. In a world moving toward carbon pricing, the lowest carbon producer wins, not the lowest cost producer.

The talent angle matters too. The best engineers want to solve climate problems, not just maximize production. By positioning as a sustainability leader, Jindal attracts talent that purely financial incentives can't buy. This human capital advantage compounds over time.

IX. Analysis & Bear vs. Bull Case

Let's step into the ring where bulls and bears duke it out over Jindal Stainless's future. Both sides have compelling arguments, and the truth, as always, lies in the nuanced space between.

Bull Case: The India Infrastructure Supercycle

India's stainless steel consumption per capita stands at 2.8 kg versus 10 kg in China and 15 kg in developed markets. Simple math suggests a 5x opportunity just to reach China's levels. But the bulls see something more profound: a structural shift in material choice.

Consider the government's coastal infrastructure mandate being contemplated—using stainless steel for bridges and structures within 50 km of India's 7,500 km coastline. One policy change could create millions of tonnes of incremental demand. The Mumbai Coastal Road, Chennai Metro, and countless similar projects are already specifying stainless steel over carbon steel for longevity.

The automotive transition accelerates this. EVs require 15-20% more stainless steel than ICE vehicles—battery enclosures, thermal management, lightweighting. India's 2030 target of 30% EV penetration could add 500,000 tonnes of annual demand. Jindal's established relationships with Maruti, Tata Motors, and new players like Ola Electric position them to capture disproportionate share.

Operational leverage amplifies returns. With 2.9 MTPA current capacity heading to 4.2 MTPA, most expansion is brownfield—lower capex, faster execution, higher returns. Fixed costs spread over higher volumes could expand EBITDA margins from current 10-12% to 15%+ at peak utilization. The math is compelling: ₹40,000 crore revenue at 15% margins yields ₹6,000 crore EBITDA.

The global supply chain reorganization helps too. The "China Plus One" strategy isn't just about manufacturing moving to India—it's about supply chains seeking reliability over just cost. Jindal's quality certifications, ESG credentials, and delivery track record make them a natural beneficiary as global buyers diversify from Chinese dependence.

Bear Case: The China Syndrome and Commodity Curse

But bears see storm clouds gathering. Chinese stainless steel capacity exceeds global demand by 30%. As their property market implodes and infrastructure spending slows, this excess capacity must find outlets. Despite anti-dumping duties, Chinese stainless steel finds ways in—routed through Vietnam, Indonesia, or simply accepting the duties to maintain market share.

The nickel dependence is particularly worrying. Indonesia controls 40% of global nickel production and has banned raw ore exports, forcing downstream investment. Jindal's Indonesian JV helps, but they're still price takers in a market Indonesia increasingly controls. A repeat of the 2022 nickel squeeze, when prices hit $100,000/tonne, would devastate margins.

Technology disruption looms larger than most acknowledge. Carbon fiber, advanced composites, and aluminum alloys keep improving their price-performance. Tesla's Cybertruck used ultra-hard 30X cold-rolled stainless steel, but their next generation might use something else entirely. In industrial applications, polymer coatings and galvanized steel are "good enough" for many use cases at half the cost.

The financial leverage, while reduced, remains significant. Net debt of ₹3,900 crore seems manageable, but add the ₹5,400 crore capex commitment, working capital needs, and potential acquisition funding—suddenly you're back to ₹10,000+ crore obligations. One demand shock or margin compression, and the debt spiral returns.

Environmental regulations cut both ways. Yes, green steel commands premiums, but the investment required is staggering. The hydrogen plant is impressive, but scaling to meaningful production volumes requires tens of thousands of crores. Meanwhile, Chinese producers ignore environmental costs, creating an uneven playing field that duties alone can't level.

The Nuanced Reality

The truth incorporates both narratives. Jindal Stainless is simultaneously a beneficiary of secular growth trends and vulnerable to cyclical shocks. The key variables to watch:

-

Government Policy Execution: Infrastructure spending promises are plenty; execution determines reality. Track monthly steel consumption data, not announcement headlines.

-

China's Domestic Recovery: If Chinese domestic demand recovers, export pressure reduces. Watch Chinese PMI, property starts, and infrastructure FAI.

-

Technology Adoption Curves: Green hydrogen, EVs, coastal infrastructure—all depend on adoption rates. Early adopters pay premiums; mass market demands cost parity.

-

Input Cost Dynamics: Nickel, ferrochrome, and power constitute 70% of costs. Even 10% moves significantly impact margins. The Indonesian JV provides some hedge, but not immunity.

-

Competition Response: JSW Steel's stainless ambitions, potential new entrants, and import dynamics will shape pricing power. Market share matters less than pricing discipline.

The investment case ultimately depends on time horizon and risk tolerance. For long-term believers in India's infrastructure story, current valuations offer compelling entry. For traders focused on quarterly earnings, volatility will provide both opportunities and pain.

What's undeniable is that Jindal Stainless has transformed from a debt-laden question mark to a strategic asset in India's industrial landscape. Whether that justifies the current ₹58,747 crore market cap depends on your view of India's next decade. The bulls see ₹100,000 crore potential; bears see reversion to ₹30,000 crore. Both could be right—just at different times.

X. Epilogue & "If We Were CEOs"

Standing at the helm of Jindal Stainless today, with ₹40,000 crore in revenue and ambitions for much more, what strategic choices would define the next decade? The path forward isn't just about making more steel—it's about reimagining what a materials company can be in the 21st century.

The Platform Play

First move: transform from manufacturer to platform. Jindal produces 200+ grades of stainless steel, but customers don't want grades—they want solutions. Create "Jindal Design Studios" in major cities where architects, engineers, and fabricators can prototype, test, and specify stainless steel applications. Think Apple Stores, but for industrial materials.

Build a digital marketplace connecting fabricators, dealers, and end-users directly. Today's supply chain has five middlemen between Jindal and the final customer. Cut it to two. Use blockchain for tracking, AI for demand prediction, and embedded financing for working capital. The data generated would be worth more than the transaction fees.

The Sustainability Moat

Second, make green steel the only steel. The Hisar hydrogen plant is a start, but go all-in. Partner with renewable energy developers for 24/7 green power through round-the-clock renewable energy contracts. Create the world's first "Carbon Negative Steel"—where the CO2 absorbed in recycling and renewable energy exceeds emissions. Price it at 30% premium and watch sustainability-conscious customers line up.

Launch "Jindal Forever"—a steel buyback program. Every tonne sold comes with a guarantee to buy back at 60% of prevailing prices after use. This creates a circular economy, locks in customers, and secures raw material (scrap) supply. The financial engineering would be complex, but the competitive advantage would be insurmountable.

The Capability Expansion

Third, expand beyond stainless. The metals market is converging—customers want multi-material solutions. Acquire or partner for aluminum, titanium, and advanced composites capabilities. Don't compete with these materials; offer them alongside stainless. Become the "materials solutions company" that happens to be great at stainless steel.

Enter the midstream aggressively. Don't just supply steel for EVs; make battery enclosures. Don't just provide steel for kitchens; manufacture modular kitchen systems. Move from B2B to B2B2C. The margins are higher, customer relationships deeper, and differentiation clearer.

The Geographic Arbitrage

Fourth, think global, act regional. The Indonesia JV is smart, but think bigger. Africa is the next infrastructure frontier—establish finishing facilities in Nigeria, Kenya, and Egypt. These markets will grow 10% annually for decades. Being early means defining standards, relationships, and market structure.

In developed markets, acquire distressed assets. European steel companies face energy crisis and emission regulations. Buy their specialty steel units at distressed valuations, retrofit with Indian cost structures and Jindal's green technology. Transform them into export bases serving high-value segments.

The Innovation Engine

Fifth, make R&D a profit center, not a cost center. Partner with IITs and international universities for a "Jindal Advanced Materials Lab." Focus on three areas: ultra-high-strength stainless for aerospace, bio-compatible stainless for medical implants, and smart stainless with embedded sensors for infrastructure monitoring.

Patent everything, license globally. The Japanese model—materials innovation driving industrial advancement—is the template. In 10 years, technology licensing could contribute 10% of profits with 50% margins.

The Capital Revolution

Sixth, reimagine capital structure. Create a Stainless Steel REIT holding industrial real estate and leasing it back. This removes assets from balance sheet, improves returns, and creates a dividend-yielding investment vehicle for different investors.

Launch "Jindal Green Bonds" specifically tied to emission reduction targets. Price them 200 basis points below conventional debt but link management compensation to achieving targets. This aligns incentives and creates accountability.

The Biggest Surprises

Reflecting on Jindal's journey, several surprises stand out:

-

The Debt Crisis as Catalyst: Most companies die in debt restructuring. Jindal emerged stronger. The forced focus, operational discipline, and strategic clarity that crisis brought proved invaluable.

-

Family Harmony in Division: The Jindal brothers' split created value rather than destroying it. Each focused on their strength—Sajjan on scale, Ratan on specialty, Naveen on power, Prithviraj on pipes. The sum exceeded the whole.

-

Technology as Differentiator in Commodities: In an industry where products are supposedly undifferentiated, Jindal's technical superiority in razor blade steel, coin blanks, and specialty grades created monopolistic positions.

-

Green as Growth Driver: Sustainability isn't a cost—it's a revenue driver. Green steel commands premiums, attracts customers, and opens financing options unavailable to polluting peers.

-

Youth as Advantage: Abhyuday Jindal taking charge at 34 brought fresh thinking. His digital initiatives, customer focus, and sustainability drive wouldn't have emerged from traditional steel industry thinking.

The Next Decade

Can JSL become a global top 5 player? The ingredients exist: Indian market growth, operational excellence, sustainability leadership, and financial flexibility. But ingredients don't make a meal—execution does.

The biggest risk isn't Chinese competition or commodity cycles—it's complacency. Success breeds conservatism. The hunger that drove Om Prakash from Haryana to Calcutta, that pushed Ratan through the debt crisis, that motivates Abhyuday's innovation—maintaining that edge while managing a ₹60,000 crore enterprise is the real challenge.

If we were CEOs, the north star would be simple: make stainless steel as ubiquitous as concrete and as profitable as software. The path requires technical excellence, financial sophistication, and strategic courage. But then again, that's exactly what got Jindal Stainless here in the first place.

The story that began with surplus pipes in post-partition Calcutta has become a testament to Indian industrial ambition. Whether the next chapter matches the drama and success of the previous ones depends on choices being made in boardrooms and factory floors today. For investors, customers, and competitors alike, Jindal Stainless remains a company worth watching—and perhaps, worth betting on.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube