JM Financial: The Making of India's Capital Markets Powerhouse

I. Introduction & Episode Roadmap

Picture this: It's October 2024, and India's capital markets are on fire. The Hyundai Motor India IPO—the largest in the country's history at ₹27,870 crores—has just closed for subscription. Behind the scenes, orchestrating this massive financial event alongside the global giants, stands a homegrown investment bank that most international investors have never heard of. Yet this firm commands a staggering 47% market share in IPOs and 38% in QIPs, capturing 80% of the top 10 IPOs by size in fiscal 2024.

How did two cousins from a traditional Gujarati business family build what would become India's capital markets powerhouse from scratch? How did they navigate the labyrinthine License Raj, survive regulatory investigations, orchestrate a generational transition, and emerge as the go-to advisor for India Inc's biggest deals?

This is the story of JM Financial—a ₹16,934 crore market cap institution that in FY24 generated ₹4,412 crores in revenue and ₹1,045 crores in profit. But those numbers barely scratch the surface of what makes this company fascinating. At its core, this is a tale about building in emerging markets, where relationships trump algorithms, where regulatory complexity creates moats, and where patient capital can compound through multiple cycles of boom and bust.

The narrative arc spans five decades and touches on every major inflection point in India's economic history: the socialist era of the 1970s, the liberalization revolution of 1991, the dot-com boom and bust, the 2008 financial crisis, the digital transformation wave, and now, India's emergence as the world's fastest-growing major economy. Through it all, JM Financial didn't just survive—it thrived by understanding a fundamental truth about emerging markets: in environments where trust is scarce and information asymmetry is high, the firms that can bridge those gaps become indispensable.

What makes JM Financial particularly compelling is how it defied conventional wisdom at every turn. While global investment banks parachuted into India with their playbooks, JM built from first principles. While others focused on technology disruption, they doubled down on relationship capital. While competitors specialized, they built a conglomerate. And while the industry consolidated globally, they remained fiercely independent, with the Kampani family still holding over 15% of the shares directly and promoters controlling 56.5% of the company.

This episode explores four interconnected themes that explain JM Financial's unlikely rise. First, the art of building financial infrastructure in a low-trust environment—how do you create capital markets in a country where most businesses are family-owned and transparency is viewed with suspicion? Second, the dynamics of conglomerate evolution in emerging markets—why does diversification work in India when it fails in developed markets? Third, the delicate dance of generational transition in family businesses—how do you modernize without losing your soul? And finally, the mechanics of capital markets transformation—what happens when a $3.5 trillion economy decides to financialize at warp speed?

The timing of this story couldn't be more relevant. As global investors scramble to understand India's moment—with the country crossing $4 trillion in market capitalization and foreign portfolio investors pouring in $21 billion in 2024 alone—JM Financial sits at the epicenter of this transformation. They're not just participants; they're architects of India's capital markets renaissance.

But this isn't a victory lap. The firm faces existential questions about its future: Can relationship-based investment banking survive in an age of algorithms and automation? Will the next generation of Indian entrepreneurs value the same things their fathers did? Can a domestic player compete with the unlimited balance sheets of global banks? And perhaps most critically: Is being the biggest fish in the Indian pond enough when the ocean of global finance beckons?

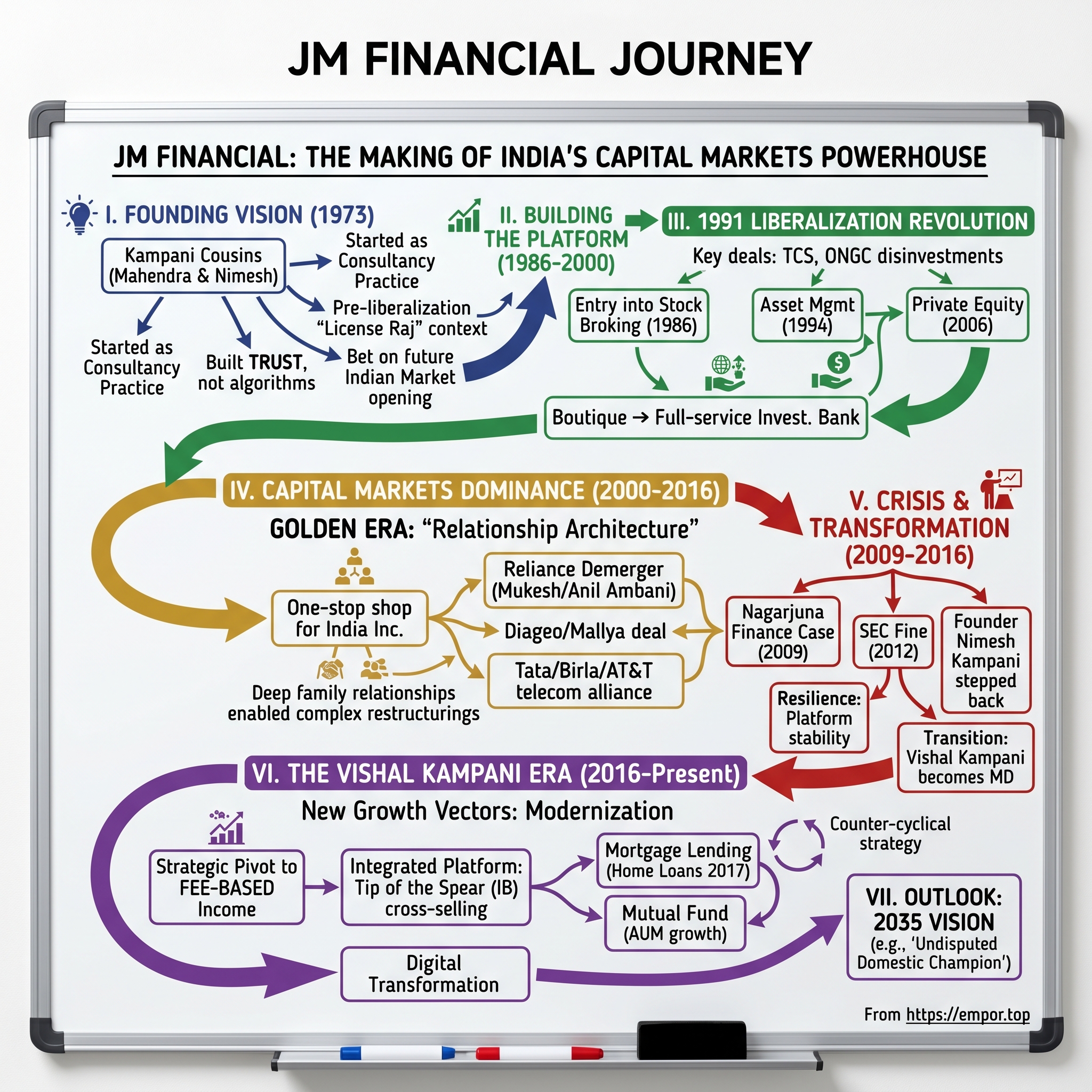

II. The Kampani Origin Story & Founding Vision

The year was 1973. India was a different universe—a socialist economy where private enterprise was viewed with suspicion, where getting a telephone connection required political connections, and where the idea of a stock market was as foreign to most Indians as space travel. In this unlikely environment, two cousins—Mahendra and Nimesh Kampani—made a decision that would seem either prescient or insane depending on your perspective: they would build an investment bank.

But this wasn't a startup in the modern sense. The Kampanis weren't fresh-faced MBAs with a PowerPoint deck. They were spinning out from Jamnadas Morarjee Securities, where they had been running the investment banking arm—itself a curious anomaly in an era when "investment banking" in India meant helping companies navigate the Byzantine maze of government licenses and permits. The firm started as a consultancy practice, a deliberately modest positioning that reflected both the regulatory constraints of the time and the Kampanis' understanding that in India, you build trust before you build businesses. To understand Nimesh Kampani, you have to understand pre-liberalization India. A commerce graduate from Sydenham College and a Chartered Accountant from ICAI, Nimesh wasn't a typical financier. He was an architect of markets that didn't yet exist. His vision wasn't just to build an investment bank—it was to make JM Financial into one of India's largest financial institutions. This might sound like standard entrepreneurial ambition, but in 1973 India, it was borderline revolutionary.

The License Raj era was a peculiar beast. Every business decision required government approval. Want to expand production? Get a license. Want to import machinery? Get a license. Want to raise capital? Get permission, then get a license. In this kafkaesque bureaucracy, the Kampanis saw opportunity where others saw obstacles. They understood that Indian businesses desperately needed guides through this regulatory labyrinth—advisors who could speak both the language of bureaucrats and businessmen.

The firm was originally set up as a consultancy practice, a deliberately understated beginning that reflected the Kampanis' understanding of Indian business culture. You didn't burst onto the scene; you earned your place through patient relationship-building and consistent delivery. The cousins brought complementary skills—Mahendra with his operational acumen and Nimesh with his strategic vision and relationship management capabilities that would later make him legendary in Indian business circles.

What's remarkable about the founding vision is how prescient it was. The Kampanis were betting that India would eventually open up, that capital markets would matter, that businesses would need sophisticated financial advice. Remember, this was a time when the Bombay Stock Exchange had fewer than 2,000 listed companies, daily trading volumes that would be considered a rounding error today, and when most Indians kept their savings in gold or real estate because they didn't trust financial instruments.

The family business DNA ran deep. This wasn't just about making money—it was about building an institution that would outlast them. The Kampani family's combined direct and indirect equity ownership would eventually reach between 60% and 65%, but more importantly, they instilled a culture that balanced entrepreneurial aggression with conservative risk management. This duality—ambitious in vision, cautious in execution—would become JM Financial's signature trait.

The early challenges were immense. How do you build trust in a market where trust is scarce? How do you convince family-owned businesses, often secretive about their finances, to open up to external advisors? How do you create financial products for a market that doesn't understand why it needs them? The Kampanis' answer was radical patience. They would spend months, sometimes years, cultivating relationships before seeing any business. They would educate clients about capital markets, often with no immediate payoff. They were playing an infinite game in a market full of finite players.

One early insight that shaped the firm's trajectory: in India, relationships weren't just important—they were everything. While Western investment banks could rely on standardized products and processes, in India every deal was bespoke, every client relationship was personal, and trust, once earned, could span generations. The Kampanis understood that they weren't just building a financial services firm; they were building a trust network that would compound in value over decades.

The timing of the founding—1973—is itself fascinating. This was the year of the oil crisis, when global markets were in turmoil. India, already isolated from global capital flows, became even more insular. Yet the Kampanis saw this isolation not as a permanent condition but as a temporary phase. They were building for an India that didn't yet exist—one that would embrace markets, welcome foreign capital, and need sophisticated financial intermediaries. It would take 18 years for that India to emerge with the 1991 liberalization, but when it did, JM Financial was ready.

III. Building the Platform: From Broker to Bank (1986–2000)

The transformation of JM Financial from a consultancy to a full-fledged financial institution reads like a masterclass in platform building. In 1986, the firm was incorporated as a private limited company to engage in the business of stock-broking—a move that might seem incremental but was actually revolutionary. This was the Kampanis' first major bet on the formalization and growth of India's capital markets. But 1991 changed everything. P. V. Narasimha Rao took over as Prime Minister in June, and appointed Dr Manmohan Singh as the Finance Minister. The Narasimha Rao government ushered in several reforms that are collectively referred to as liberalisation in the Indian media. The reforms formally began on 1 July 1991 when RBI devalued the rupee by 9% and by a further 11% on 3 July. This wasn't just policy change—it was revolution. The reforms specified deregulation, increased foreign direct investment, liberalisation of the trade regime, reforming domestic interest rates, strengthening capital markets (stock exchanges), and initiating public enterprise reform. For JM Financial, which had listed on the Bombay Stock Exchange just months before in 1991, the timing was exquisite.

The liberalization unleashed animal spirits that had been caged for decades. India's GDP grew from $266 billion in 1991 to $2.3 trillion in 2018, and JM Financial rode this wave with remarkable prescience. They expanded into asset management in 1994, just as Indian households were beginning to discover mutual funds. They launched private equity operations in 2006, anticipating the coming boom in risk capital. Each move wasn't just opportunistic—it was strategic, building capabilities before the market fully understood it needed them. The landmark deals that established JM Financial's credibility read like a who's who of India Inc. They played a key role in taking Tata Consultancy Services and Bharti Airtel public, assisted the Indian government in raising $2.4 billion through the partial sale of the Oil and Natural Gas Corporation. These weren't just transactions—they were nation-building exercises. The TCS IPO in 2004, which raised ₹5,400 crores, wasn't just India's largest IPO at the time; it was a statement that Indian IT had arrived on the global stage. The ONGC disinvestment demonstrated that India could execute complex public sector sales with the sophistication of any developed market.

The secondary listing on NSE in 2006 marked another evolution. By this point, JM Financial had transformed from a boutique advisory firm into a full-service investment bank. The expansion into asset management in 1994 and private equity in 2006 weren't random diversifications—they were calculated moves to capture different pools of capital at different stages of India's financial evolution. When Indian households started moving savings from gold to financial assets, JM was there with mutual funds. When entrepreneurs needed growth capital, JM was there with private equity.

What's fascinating about this period is how JM Financial built its platform through relationships rather than technology. While Western investment banks were investing billions in trading systems and quantitative models, JM was investing in understanding the psyche of Indian business families. They knew that in India, deals weren't won in boardrooms but over chai in living rooms. They understood that trust, once earned from a patriarch, could unlock decades of business across multiple group companies.

The network effects were powerful and compounding. Every successful IPO brought five new mandates. Every M&A deal opened doors to both the acquirer's and target's ecosystems. Every family that trusted them with one transaction would return for the next generation's needs. This wasn't just relationship banking—it was relationship architecture, building interconnected webs of trust that would prove invaluable when markets turned volatile.

The 2008 financial crisis, rather than destroying JM Financial, actually strengthened its position. While global banks retreated from India, cutting staff and closing offices, JM doubled down. They understood something fundamental: crises in emerging markets create opportunities for those with patient capital and strong relationships. As credit dried up globally, JM's deep understanding of Indian businesses allowed them to provide liquidity when others couldn't or wouldn't. This countercyclical expansion would pay dividends for years to come.

IV. The Golden Era: Capital Markets Dominance (2000–2016)

The period from 2000 to 2016 represents JM Financial's golden era, when they weren't just participating in India's capital markets boom—they were orchestrating it. The deals during this period read like a greatest hits album of Indian capitalism. Kampani advised Mukesh Ambani on the demerger of Reliance Industries following the split with his brother Anil Ambani, and later negotiated the deal between Diageo and Vijay Mallya. Kampani facilitated major business alliances, including a telecommunications partnership involving Ratan Tata, Kumar Mangalam Birla, and AT&T.

The Reliance demerger in 2005 was perhaps the most complex corporate restructuring in Indian history. When Dhirubhai Ambani died in 2002 without a clear succession plan, the ensuing battle between his sons Mukesh and Anil threatened to tear apart India's largest business empire. The charge of this complex affair was given to Dhirubhai's personal banker K. V. Kamath of ICICI Bank and Nimesh Kampani of JM Financials. This wasn't just about dividing assets—it was about surgically separating intertwined businesses while maintaining operational continuity and shareholder value.

The trust that enabled such deals wasn't built overnight. It came from decades of discrete counsel, from being in the room during crisis moments, from never betraying confidences even when the stakes were astronomical. When you're dividing a $25 billion empire between feuding brothers, you need someone both sides trust implicitly. That was Nimesh Kampani's superpower—the ability to be everyone's banker without being anyone's enemy.

The integrated financial services model that JM Financial built during this period was revolutionary for India. While global banks typically specialized—Goldman Sachs in M&A, Morgan Stanley in equity capital markets, JPMorgan in debt—JM understood that Indian businesses needed a one-stop shop. The same family that needed help taking their company public would also need private wealth management, real estate financing for their factories, and eventually succession planning for the next generation.

By 2016, JM Financial had evolved into four distinct but synergistic pillars. Investment banking generated the relationships and deal flow. Mortgage lending provided steady, predictable income. Alternative and distressed credit allowed them to take contrarian bets when markets panicked. And asset management created recurring fee income while deepening client relationships. Each vertical reinforced the others—a private equity exit might lead to an IPO mandate, which would generate wealth management opportunities, which could fund real estate investments.

The network effects were extraordinary. In India's relationship-driven business environment, every successful transaction created a multiplier effect. Help a promoter take his company public, and you'd get introductions to his entire business network. Manage a complex restructuring successfully, and distressed companies across the country would seek you out. The trust compound interest that JM Financial earned during this period would prove invaluable when storms hit.

But beneath the success, fault lines were developing. The very relationships that enabled JM's rise would also create vulnerabilities. The concentration of power in Nimesh Kampani's hands meant that the institution's reputation was inextricably linked to one man's conduct. And in India's politically charged business environment, being too close to certain business houses could make you a target. These vulnerabilities would soon be exposed in ways that would test the firm's resilience.

V. Crisis, Controversy & Transformation (2009–2016)

The year 2009 marked the beginning of JM Financial's trial by fire. In 2009, JM Financial Founder, chairman and managing director, Nimesh Kampani was under police investigation for alleged involvement of defrauding depositors by Hyderabad-based Nagarjuna Finance Ltd. Kampani was reported hiding in Dubai temporarily to avoid arrest. In April 2009, the Supreme Court of India granted a stay on the arrest for Kampani. After two years, Kampani returned to India but stepped back from daily operations.

The Nagarjuna Finance case was a classic example of how India's business-politics nexus could ensnare even the most careful operators. Kampani had served as an independent director on Nagarjuna Finance's board until 1999—a decade before the company's collapse. Yet when the firm defaulted, leaving depositors in the lurch, investigators came after former board members. The timing was suspicious—many believed it was politically motivated, a way to pressure Kampani given his close relationships with certain business houses that had fallen out of political favor.

The image of one of India's most respected investment bankers reportedly in Dubai to avoid arrest sent shockwaves through the financial community. Here was a man who had advised on some of India's largest deals, who had the trust of the country's biggest business families, now unable to return to his own country. For JM Financial, it was an existential crisis. How do you maintain client confidence when your founder and face of the firm is under investigation? The troubles compounded in 2012 when the U.S. Securities and Exchange Commission (SEC) fined JM Financial and three other Indian securities firms, US$1.8 million for violating registration rules. The firms solicited and provided brokerage services to U.S. investors without being registered with the SEC as required under the federal securities laws. While the fine was relatively small by global standards, the reputational damage was significant. Here was one of India's premier investment banks being sanctioned by the world's most powerful securities regulator.

What's remarkable about this period is not that JM Financial faced challenges—every major financial institution does—but how they responded. Rather than circle the wagons or deny responsibility, the firm embarked on a comprehensive governance overhaul. They strengthened compliance systems, brought in independent directors, and most importantly, began planning for succession.

The decision for Nimesh Kampani to step down as Managing Director in 2016 was both painful and necessary. In 2016, Kampani stepped down as the managing director (MD) of JM Financial, with his son Vishal succeeding him as MD and Kampani continuing as non-executive chairman. This wasn't just a generational transition—it was an institutional transformation. The firm that had been synonymous with one man's relationships and reputation had to prove it could survive and thrive without him at the operational helm.

The lessons from this period are profound. First, in emerging markets where institutions are weak, the line between legitimate business and political persecution can be razor-thin. Second, governance matters more when trust is your primary asset—one scandal can undo decades of relationship-building. Third, succession planning in founder-led firms isn't just about transferring ownership; it's about transferring trust, relationships, and institutional memory.

The period also revealed the resilience of JM Financial's business model. Despite the controversies, clients didn't abandon them en masse. The integrated platform—with multiple revenue streams across investment banking, lending, and asset management—provided stability when one area faced headwinds. The deep relationships built over decades proved their worth when the firm needed support most.

Most importantly, this crisis forced JM Financial to evolve from a founder-driven firm to an institution. The compliance improvements, governance reforms, and succession planning weren't just responses to immediate challenges—they were investments in the firm's ability to survive beyond its founders. This transformation would prove crucial as the firm entered a new era under Vishal Kampani's leadership.

VI. The Vishal Kampani Era: New Growth Vectors (2016–Present)

When Vishal Kampani took over as Managing Director in 2016, he faced a challenge that would define his leadership: how do you modernize a 43-year-old institution without losing what made it successful? Since joining JM Financial in 1997, he has been integral in expanding the group's operations across various financial services, including the launch of JM Financial Home Loans Limited in 2017. But the real transformation would go much deeper than adding new business lines.

Vishal brought a different sensibility to JM Financial. A Master of Finance from London Business School who had worked with Morgan Stanley in New York, he understood both the global best practices and the unique requirements of the Indian market. His approach wasn't to impose Western models wholesale but to synthesize the best of both worlds—maintaining the relationship-driven core while building technology-enabled scale.

The digital transformation under Vishal's leadership has been nothing short of revolutionary. "Many of the new companies that you see probably have not seen cycles, and they are in rapid expansion mode. I think learnings really come when you go through a cycle. As a firm, we've seen many cycles," Vishal noted in a recent interview. This perspective—combining the wisdom of experience with the urgency of innovation—has defined his strategic approach. The numbers speak to the success of this transformation. Q2 FY25 deals: BRLM for Bajaj HFC IPO (₹6,560 Cr), Vedanta QIP (₹8,500 Cr), Nexus Select Trust Block Deal (₹4,554 Cr). Investment Bank segment revenue grew 55% between FY22 and FY24. These aren't just transactions—they're validations of JM Financial's evolved model that combines traditional relationship banking with modern execution capabilities.

The expansion into mortgage lending through JM Financial Home Loans in 2017 was particularly strategic. While everyone was chasing the digital lending boom, Vishal recognized that real estate financing—backed by hard assets and requiring deep local knowledge—played to JM's strengths. This wasn't about competing with fintech startups on their turf; it was about leveraging decades of relationships with developers, understanding of local markets, and risk assessment capabilities that algorithms couldn't replicate.

The mutual fund business transformation has been equally impressive. Mutual Fund AUM increased 2x to ₹6,189 crores (March 2024), equity schemes grew 4x, current AUM crossed ₹8,000 crores. This wasn't achieved through aggressive pricing or distribution muscle alone. JM Financial took a contrarian approach—focusing on sophisticated products for informed investors rather than vanilla offerings for the mass market.

Vishal's perspective on the changing investment landscape is particularly insightful: "I don't think the younger generation will be interested in really owning properties, managing them. Their free time on a weekend is not going to go into having three properties, figuring out if they're managed, if my rent is coming on time. They much rather own yielding properties through capital market instruments." This understanding of generational shifts has informed JM's product development and client engagement strategies.

The strategic pivot to fee-based income represents perhaps the most important transformation under Vishal's leadership. While lending provides scale and relationships, fee income from advisory, asset management, and wealth management provides higher margins and lower capital requirements. This isn't just financial engineering—it's a fundamental reimagining of what an investment bank can be in the Indian context.

What's remarkable is how Vishal has managed this transformation while preserving JM Financial's cultural DNA. The firm still values relationships over transactions, still maintains the patient, long-term approach that defined its early years. But now these traditional strengths are amplified by technology, scale, and institutional capabilities. It's not disruption—it's evolution.

VII. Business Model Deep Dive: The Four Pillars

Understanding JM Financial's business model requires appreciating how four distinct pillars create a sum greater than their parts. In H1 FY25, the Investment Bank contributed 39% of revenues, but that number understates its strategic importance. This division isn't just a revenue generator—it's the tip of the spear that opens doors, builds relationships, and creates opportunities for every other business line.

The Investment Banking pillar encompasses capital markets, M&A advisory, institutional equities, private wealth, portfolio management services (PMS), and private equity funds. Each sub-vertical reinforces the others. An M&A mandate might lead to a capital markets transaction post-merger. A successful IPO creates wealth that flows into private wealth management. Private equity exits generate investment banking fees. This isn't diversification for its own sake—it's strategic integration where each business multiplies the value of others.

The Mortgage Lending pillar—encompassing commercial and residential real estate finance, housing finance, and educational institution lending—provides the ballast for the entire operation. While investment banking revenues can be volatile, mortgage lending offers predictable, asset-backed returns. But more importantly, it deepens relationships with real estate developers who are also major consumers of investment banking services. When a developer needs project finance, JM is there. When the same developer wants to go public, JM already understands their business intimately.

The Alternative & Distressed Credit pillar, including asset reconstruction and alternative credit funds management, represents JM's contrarian bet on India's bad loan problem. While others saw NPAs as toxic waste, JM saw opportunity. By acquiring distressed assets at deep discounts and either restructuring or liquidating them efficiently, they've created a highly profitable business that also positions them as problem-solvers for banks and corporates dealing with stress.

The Asset Management & Wealth pillar ties everything together. With offerings ranging from mutual funds to alternative investment funds to portfolio management services, JM can serve clients across the wealth spectrum. But the real genius is how this business creates stickiness. A client who trusts you with their wealth management is more likely to give you their investment banking mandates. A fund that invests in your IPOs becomes a strategic partner in future transactions.

The synergies between these pillars are extraordinary. Consider a typical client journey: A entrepreneur gets project finance from JM's mortgage lending arm. As the business grows, they tap JM's private equity funds for expansion capital. When ready for an IPO, JM's investment bank takes them public. Post-IPO, JM manages the promoter's wealth through private banking. If the company later faces stress, JM's distressed credit team provides solutions. This isn't just cross-selling—it's lifecycle partnership.

The capital allocation across these pillars reflects sophisticated risk management. Investment banking requires minimal capital but generates high ROE when markets are buoyant. Mortgage lending requires significant capital but provides stable returns through cycles. Distressed credit is opportunistic—deploying capital when assets are cheap and harvesting when markets recover. Asset management is capital-light but requires patient investment in distribution and technology. Together, they create a portfolio that can generate returns through different market conditions.

The platform economics are compelling. Client acquisition costs are amortized across multiple products. Regulatory compliance infrastructure serves all businesses. Brand equity built in investment banking enhances asset gathering in wealth management. Risk management capabilities developed for lending inform investment decisions in distressed credit. These shared economies of scale and scope create competitive advantages that are hard to replicate.

VIII. Playbook: Building in Emerging Markets

JM Financial's success offers a masterclass in building financial services businesses in emerging markets, where the rules are fundamentally different from developed economies. The playbook they've developed over five decades challenges conventional wisdom while offering insights relevant far beyond India's borders.

The first principle: relationship capital trumps everything else in low-trust environments. In markets where information asymmetry is high, legal systems are weak, and business practices are opaque, trust becomes the ultimate currency. JM understood that in India, you don't win mandates through pitchbooks—you win them through decades of discrete counsel, through being there during crises, through understanding not just the business but the family dynamics behind it. This isn't about schmoozing—it's about becoming an indispensable counselor to business families navigating generational transitions, regulatory changes, and market volatility.

Managing regulatory complexity in emerging markets requires a different mindset. Rather than viewing regulations as constraints, JM treated them as moats. Every new compliance requirement that global banks found onerous became an opportunity for JM to deepen its competitive advantage. They invested heavily in understanding not just the letter but the spirit of regulations, building relationships with regulators, and often helping shape policy. When foreign banks retreated due to regulatory challenges, JM expanded.

The approach to political risk is particularly sophisticated. Unlike Western firms that try to remain apolitical, JM understood that in India, business and politics are inextricably linked. But instead of aligning with particular parties or individuals, they built relationships across the political spectrum, focusing on technocrats and institution-builders rather than politicians. This enabled them to navigate regime changes, policy shifts, and political vendettas without becoming collateral damage.

Long-term conviction in the India growth story, despite short-term valuation concerns, has been a defining characteristic. While foreign investors oscillated between irrational exuberance and excessive pessimism about India, JM maintained steady conviction. They understood that India's growth wouldn't be linear—there would be crises, setbacks, and periods of stagnation. But the secular trends—demographics, urbanization, formalization, financialization—were irreversible. This long-term perspective enabled them to invest during downturns and harvest during upturns.

Capital allocation in volatile markets requires nerves of steel and deep pockets. JM's approach was counter-cyclical by design. When markets crashed and competitors retreated, JM deployed capital aggressively. When markets boomed and everyone was expanding, JM consolidated and built reserves. This wasn't contrarianism for its own sake—it was recognition that in volatile markets, the best opportunities come during distress and the biggest risks emerge during euphoria.

The conglomerate advantage in India deserves special attention. While conglomerates have fallen out of favor in developed markets, they thrive in emerging markets for good reasons. In environments where specialized suppliers are unreliable, capital markets are shallow, and talent is scarce, vertical integration makes sense. JM's evolution into a financial conglomerate wasn't sprawl—it was strategic integration that created internal markets for capital, talent, and information.

Building trust in low-trust environments requires different strategies. JM understood that in India, trust is personal, not institutional. That's why the Kampani family's continued involvement mattered—it signaled skin in the game. They also understood that trust is built through consistent behavior over decades, not through marketing campaigns. Every promise kept, every confidentiality maintained, every crisis navigated together added to their trust bank account.

The network effects in investment banking are particularly powerful in emerging markets. In developed markets with transparent information and efficient markets, relationships matter less. But in India, where information is closely held and deals happen through introductions, network effects are everything. JM's network wasn't just about knowing people—it was about understanding the complex web of relationships, rivalries, and alliances that define Indian business.

IX. Competition & Market Position Analysis

The competitive landscape of Indian investment banking reveals JM Financial's unique positioning. Benchmarking against Kotak, ICICI Securities, Axis Capital shows that while these firms have greater balance sheet strength or broader retail distribution, none match JM's combination of deep corporate relationships, execution track record, and integrated platform capabilities.

Kotak Mahindra, often seen as JM's closest domestic competitor, took a different path—building from a non-banking finance company into a universal bank. This gives Kotak advantages in terms of funding costs and regulatory flexibility, but it also means they're more constrained by banking regulations. JM's decision to remain primarily a non-banking financial company gives them more flexibility in capital allocation and risk-taking.

ICICI Securities benefits from being part of India's second-largest private bank, with access to a massive retail customer base and cheap funding. But this also makes them more bureaucratic, less entrepreneurial, and often conflicted when dealing with competitors of their parent bank. JM's independence allows them to work with anyone, creating a broader addressable market.

Axis Capital, formed from the acquisition of Enam Securities, represents the consolidation trend in Indian investment banking. While they've gained scale, the integration challenges and cultural differences have prevented them from fully capitalizing on the combination. JM's organic growth approach, while slower, has preserved cultural coherence and execution capabilities.

The foreign bank competition—Goldman, Morgan Stanley, JPMorgan—presents a different challenge. These firms bring global expertise, unlimited capital, and marquee brand names. But they also suffer from several structural disadvantages in India. Regulatory restrictions limit their ability to deploy capital freely. Distance from headquarters means slow decision-making. And most critically, the revolving door of expat bankers means they never build the deep, multi-generational relationships that define Indian business.

Mergermarket League tables usually ranked JM Financial in the top 10 for India deals, with their 2021 rank being No. 4. But league tables don't tell the full story. JM often works on complex, relationship-driven transactions that don't make headlines but generate significant fees and deepen client relationships. They're less focused on league table rankings and more on profitability and strategic value.

The moat that protects JM Financial's position is multi-layered. Local relationships built over decades can't be replicated quickly. Regulatory expertise in navigating India's complex financial laws creates barriers to entry. The execution track record—having successfully completed hundreds of transactions across market cycles—builds trust that money can't buy. And increasingly, the integrated platform creates switching costs for clients who value the convenience of one-stop shopping.

Market share dynamics in Indian investment banking are fascinating. During boom times, foreign banks gain share as they're willing to underwrite larger deals and accept lower fees. During downturns, domestic banks like JM gain share as foreign banks retreat and clients value relationships over just pricing. This cyclicality actually benefits JM—they use boom times to build capabilities and downturns to gain market share.

Fee compression is a real challenge, particularly in vanilla products like IPOs and QIPs. But JM has responded by moving up the value chain—focusing on complex restructurings, cross-border M&A, and structured products where relationships and expertise matter more than price. They've also expanded into recurring fee businesses like asset management and wealth management to reduce dependence on transactional revenues.

X. Bear vs. Bull Case & Future Outlook

The bear case for JM Financial starts with the numbers that can't be ignored. Poor sales growth of 5.06% over five years, low ROE of 5.67% over 3 years—these metrics suggest a business that's struggling to generate adequate returns despite operating in one of the world's fastest-growing economies. Critics argue that JM Financial is a melting ice cube, dependent on relationships that matter less each year as markets become more transparent and technology democratizes financial services.

Regulatory risks loom large in the bear narrative. The Indian financial sector faces constant regulatory changes, and JM's history of regulatory issues—from the Nagarjuna Finance case to the SEC fine—suggests vulnerability. As regulators become more stringent and compliance costs rise, smaller players like JM could find themselves squeezed between compliance burdens and competitive pressures.

The competitive threats are multiplying. Global banks are becoming more committed to India, hiring local talent and building permanent infrastructure. Domestic banks are consolidating, creating larger competitors with better funding access. Technology platforms are disintermediating traditional investment banks, offering direct listing platforms and automated advisory services. In this environment, what's JM's sustainable competitive advantage?

The cyclical nature of capital markets business creates inherent volatility. Investment banking revenues can swing wildly based on market conditions. A prolonged bear market or global crisis could devastate profitability. Unlike universal banks with stable deposit franchises, JM lacks the ballast to weather extended downturns.

Governance concerns persist despite improvements. The concentrated promoter holding of 56.5% raises questions about minority shareholder rights. The family-run nature of the business, while providing stability, could also limit professional management and strategic flexibility. Will the next generation of Kampanis have the same commitment and capability as their predecessors?

But the bull case for JM Financial is equally compelling, starting with the macro opportunity. India is, as Vishal Kampani puts it, "the most interesting and exciting market in the world." With a $3.5 trillion economy growing at 7-8% annually, corporate credit growing at 12-15%, and capital markets deepening rapidly, the pie is expanding fast enough for everyone to eat well.

The strong promoter holding of 56.5%, rather than being a governance concern, signals skin in the game and long-term commitment. In a market where trust matters, having promoters with their wealth tied to the company's success aligns interests and provides stability. This isn't a hired-gun management team optimizing for quarterly earnings—it's a family building for generations.

Platform synergies are just beginning to manifest. As Indian businesses become more sophisticated, they need integrated financial solutions—not just an IPO banker or a loan provider, but a comprehensive financial partner. JM's ability to provide everything from early-stage capital to public market access to wealth management creates competitive advantages that grow stronger over time.

India's capital market deepening opportunity is massive. With market cap to GDP still below 100% compared to 150%+ in developed markets, household financial savings at just 7% of GDP versus 15%+ in developed economies, and corporate bond markets at 15% of GDP against 50%+ globally, the growth runway is decades long. JM Financial is perfectly positioned to capture this financialization wave.

The network effects are accelerating. Every successful transaction adds to JM's reputation capital. Every new relationship opens doors to others. Every market cycle survived adds to institutional knowledge. These intangible assets—impossible to replicate quickly—become more valuable as markets grow more complex.

The digital transformation under Vishal's leadership positions JM for the next generation of financial services. They're not trying to out-tech the fintechs but rather combining technology with relationships to create a hybrid model that serves sophisticated clients who value both efficiency and expertise.

Looking ahead to 2035, success for JM Financial would mean several things. First, becoming India's undisputed domestic investment banking champion—the firm that every Indian company turns to for their most important transactions. Second, successfully transitioning to a fee-based model where recurring revenues from asset and wealth management provide stability through cycles. Third, institutionalizing beyond the Kampani family while maintaining the cultural values that made them successful.

The path forward requires navigating several challenges. Succession planning beyond Vishal's generation needs careful consideration. Technology investments must accelerate without losing the human touch. Regulatory compliance must be bulletproof to avoid reputation-damaging incidents. And most critically, JM must prove it can generate acceptable returns on equity while maintaining its relationship-first approach.

XI. Epilogue: The Next Decade Vision

As 2024 draws to a close, India's capital markets are experiencing a moment that would have seemed fantastical just a decade ago. $21 billion raised in IPOs in 2024, including Hyundai's biggest-ever listing—these aren't just statistics but markers of a fundamental transformation in how Indian businesses access capital and create wealth. At the center of this transformation stands JM Financial, no longer the scrappy outsider but an institution whose next decade will help define India's financial future.

The $3 trillion market cap opportunity thesis isn't just about numbers—it's about what those numbers represent. Every billion dollars of market cap created means jobs generated, innovations funded, and wealth distributed. JM Financial's role in this isn't just as an intermediary but as an architect of India's capital markets architecture. They're not just facilitating transactions; they're building the pipes through which capital flows from savers to entrepreneurs.

The digital transformation reshaping financial services presents both existential threats and unprecedented opportunities. Fintech unicorns with billion-dollar valuations but no profits, algorithmic trading replacing human judgment, blockchain promising to eliminate intermediaries—in this brave new world, what role does a traditional investment bank play? JM's answer is nuanced: technology is a tool, not a strategy. The future belongs to firms that can combine algorithmic efficiency with human insight, digital reach with personal touch.

The competitive dynamics are evolving rapidly. Global banks, after years of false starts, are finally cracking the India code by hiring local talent and committing patient capital. Domestic banks are consolidating, creating formidable competitors with massive balance sheets. Technology platforms are democratizing access to capital markets. In this environment, JM's competitive advantage isn't scale or technology—it's trust, earned over decades and deployable instantly when clients face their most critical decisions.

Succession planning remains the elephant in the room. Vishal Kampani has successfully modernized JM Financial while preserving its cultural core, but what happens next? Will the third generation of Kampanis have the same commitment to the business? Can the institution survive and thrive beyond its founding family? These questions don't have easy answers, but the firm's systematic institutionalization—strengthening of professional management, improvement in governance standards, and building of systems and processes—suggests awareness of the challenge.

The vision for 2035 is ambitious yet achievable. JM Financial as India's premier homegrown investment bank, respected globally for its execution capabilities and deep market knowledge. A firm that's successfully navigated the digital transformation while maintaining its relationship-driven core. An institution that's outlived its founders while preserving their values. A platform that serves everyone from first-generation entrepreneurs to third-generation business families, from retail investors to sovereign wealth funds.

What would success look like in concrete terms? Perhaps ₹50,000 crores in market cap, reflecting the value created for shareholders. Maybe ₹25,000 crores in AUM, representing trust earned from millions of investors. Certainly presence in every major Indian corporate transaction, validation of their position at the apex of Indian investment banking. But beyond the numbers, success would mean having played a meaningful role in India's transformation from a $3.5 trillion economy to a $10 trillion one.

The challenges ahead are formidable. Regulatory scrutiny will only intensify as financial services become more systemic. Technology disruption will accelerate, requiring constant innovation and adaptation. Global competition will strengthen as India becomes too important to ignore. Market volatility—an inevitable feature of emerging markets—will test resilience repeatedly. And always, the challenge of maintaining culture and values while scaling and modernizing.

Yet the opportunities dwarf the challenges. India's demographic dividend—500 million people entering the workforce over the next two decades—ensures sustained growth. The formalization of the economy—from cash to digital, from unorganized to organized—creates massive opportunities for financial intermediation. The globalization of Indian business—both companies going abroad and foreign capital coming in—demands sophisticated financial advisory. And the wealth creation underway—potentially $10 trillion over the next decade—needs professional management.

JM Financial's journey from a two-person consultancy to a ₹17,000 crore financial services conglomerate isn't just a corporate success story—it's a testament to the power of patient capital, relationship building, and long-term thinking in emerging markets. It's proof that in markets where trust is scarce, those who can build and maintain it become invaluable. It's validation that even in an age of algorithms and automation, human judgment and relationships matter.

As India stands on the cusp of its demographic dividend, infrastructure boom, and digital revolution, JM Financial is positioned not just as a beneficiary but as an enabler of this transformation. The next decade will test whether they can maintain their relationship-driven core while embracing technological change, whether they can institutionalize beyond their founding family while preserving entrepreneurial spirit, whether they can generate adequate returns while maintaining ethical standards.

The story of JM Financial is far from over. In many ways, it's just beginning. The firm that Nimesh and Mahendra Kampani started in 1973 with a vision of building India's capital markets has evolved into something larger than they might have imagined—an institution whose success is intertwined with India's economic destiny. As India marches toward becoming the world's third-largest economy, JM Financial's role in financing that journey, enabling entrepreneurship, and creating wealth will only grow more critical.

For investors evaluating JM Financial, the question isn't just about financial metrics or competitive positioning—it's about belief in the India story itself. If you believe India will continue its economic ascent, that capital markets will deepen, that businesses will need sophisticated financial advice, then JM Financial represents a way to participate in that transformation. If you're skeptical about emerging markets, worried about governance, or convinced that technology will eliminate traditional financial intermediaries, then JM Financial embodies those risks.

The ultimate judgment on JM Financial won't come from quarterly earnings or stock price movements but from its contribution to India's economic transformation. Did they help build world-class companies? Did they enable entrepreneurship and innovation? Did they create wealth responsibly and sustainably? Did they maintain their values while adapting to change? These are the questions that will define JM Financial's legacy.

As this analysis concludes, it's worth reflecting on what JM Financial represents in the broader context of emerging market finance. In a world increasingly dominated by global mega-banks and technology platforms, JM Financial proves that there's still room for institutions built on local knowledge, long-term relationships, and patient capital. They demonstrate that in markets where information is imperfect and trust is scarce, intermediaries who can bridge those gaps create enormous value.

The lessons from JM Financial's journey are relevant far beyond India's shores. For entrepreneurs in emerging markets, it shows the value of building for the long term rather than optimizing for quick exits. For investors, it highlights the importance of understanding local context rather than applying global templates. For regulators, it demonstrates how domestic institutions can be nurtured to compete with global giants. And for students of business, it offers a masterclass in building sustainable competitive advantages in challenging environments.

The next chapter of JM Financial's story will be written by a new generation of leaders, shaped by new technologies, and tested by new challenges. But if history is any guide, the firm will adapt, evolve, and continue to play a central role in India's economic story. The DNA of patient relationship-building, conservative risk management, and entrepreneurial opportunism that defined the firm's first fifty years will likely define its next fifty as well.

For those watching from the sidelines—investors, competitors, clients, or simply students of business—JM Financial offers a front-row seat to one of the most exciting economic transformations in human history. As India rises, so too will the institutions that enable its ascent. And among those institutions, JM Financial has earned its place through five decades of trust-building, crisis-navigating, and opportunity-seizing.

The story that began with two cousins and a vision in 1973 continues today with thousands of employees, millions of clients, and billions in capital under management. But at its core, it remains the same story—of building trust in a low-trust environment, of seeing opportunity where others see risk, of believing in India's future when others doubted. That story, still being written, makes JM Financial not just an investment opportunity but a window into India's economic soul.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube