JK Cement: Building India's Infrastructure Dreams

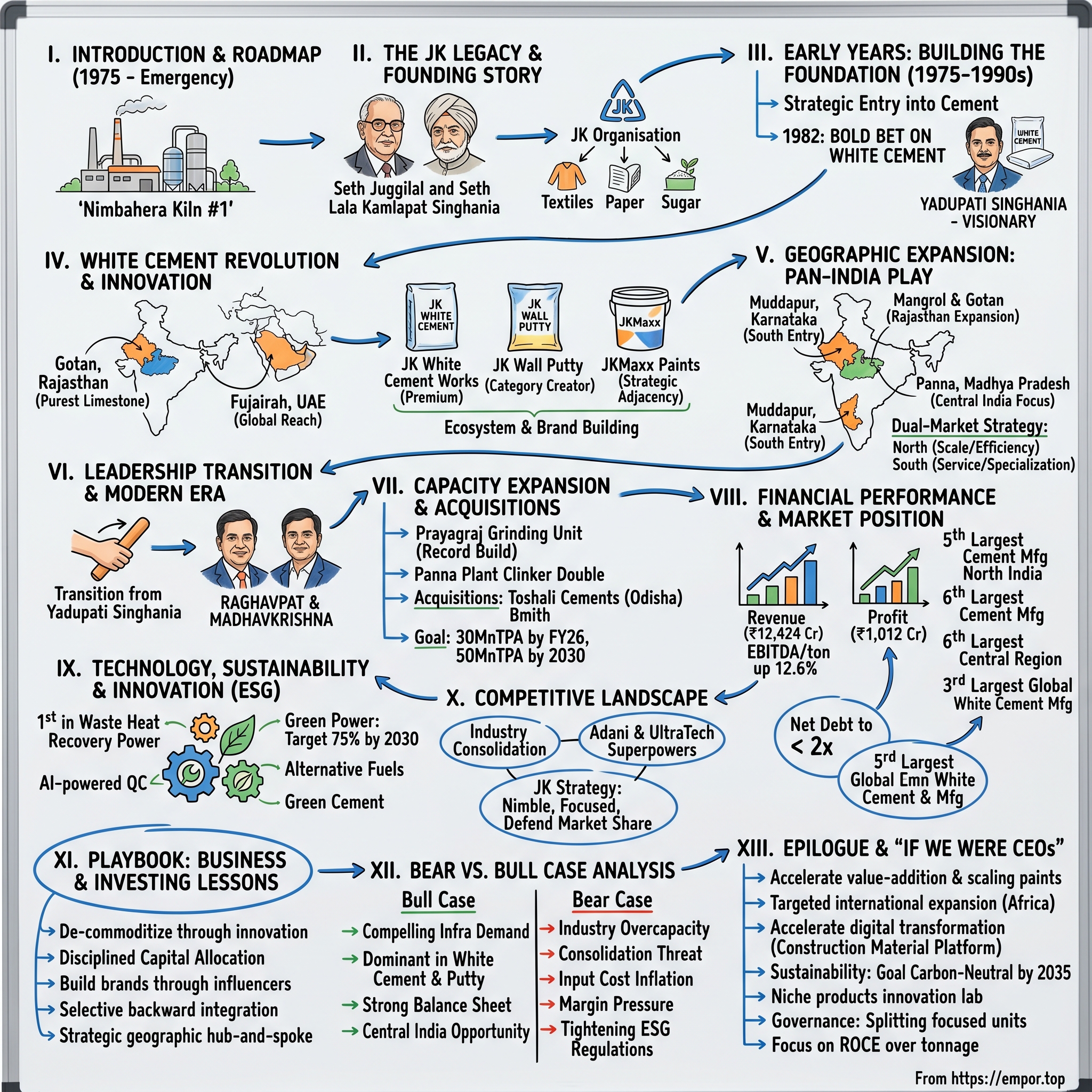

I. Introduction & Episode Roadmap

The year is 1975. Emergency has just been declared across India. Infrastructure projects are frozen, industrial licenses are worth their weight in gold, and the nation's cement consumption hovers at a meager 19 kg per capita—a fraction of what China would achieve decades later. In this suffocating environment of controls and shortages, a textile and trading conglomerate from Kanpur decides to pour concrete—literally—into India's future.

That May, the JK Organisation fired up its first kiln in Nimbahera, a dusty town in southern Rajasthan, birthing what would become JK Cement. Nearly five decades later, this company commands a market capitalization of ₹54,575 crore, having surged 66.3% in just the past year. But numbers tell only part of the story. How did this traditional North Indian cement company transform itself into a global white cement powerhouse? The answer lies not in a single decision or lucky break, but in a half-century journey of calculated risks, technological leaps, and an uncanny ability to spot opportunity where others saw only commodity traps.

This is the story of JK Cement—a company that defied the conventional wisdom that cement is just crushed rock and chemistry. It's about how a late entrant to India's cement industry became the fifth-largest cement manufacturer in North India and built one of the world's most respected white cement franchises. It's about family business evolution, from textile traders to infrastructure builders, and how they navigated the treacherous waters of Indian industrial policy, family succession, and global competition.

Our journey will take us from the dusty quarries of Rajasthan to the gleaming construction sites of Dubai, from the controlled economy of the 1970s to today's consolidation wars where Adani and UltraTech battle for supremacy. We'll explore how JK Cement built competitive moats in what most consider a moat-less business, why they bet the farm on white cement when everyone else was chasing grey volumes, and how they're positioning for a future where the industry's giants are getting bigger while the regional players are getting acquired.

This episode dissects not just a company, but an entire playbook for building industrial businesses in emerging markets—where relationships matter as much as technology, where government policy can make or break decades of work, and where patient capital can triumph over financial engineering.

II. The JK Organisation Legacy & Founding Story

Picture Kanpur in 1918. The First World War is ending, the British Raj controls Indian commerce with an iron fist, and a father-son duo—Seth Juggilal and his son Lala Kamlapat Singhania—decide to challenge the colonial monopoly on jute trading. They pool their meager savings, borrow from community networks, and establish what would become the JK Organisation, taking their initials as the company name. It's a modest beginning for what would grow into India's third-largest industrial house by the 1970s.

The Singhanias weren't content being traders. While their Marwari peers in Calcutta focused on finance and trading, Kamlapat had grander ambitions. He saw an India that would eventually need its own industrial base. By the 1930s, JK had ventured into cotton textiles, challenging British mill owners. By the 1940s, they were making sugar. When independence came in 1947, the JK Organisation was perfectly positioned for Nehru's vision of a self-reliant India. The transformation from traders to industrialists wasn't smooth. The first major business set up by him was a cotton mill with the name of Juggilal Kamlapat Cotton Spinning & Weaving Mills in 1921, marking the foundation of what would become the JK Organisation. But this was during the height of colonial resistance to Indian industrial ambitions. British mill owners controlled supply chains, banks were reluctant to lend to Indian entrepreneurs, and skilled technicians were almost exclusively European.

The group rose in importance in the 1950s to 1980s, when it was the third-largest industrial conglomerate in India after the Birla and Tata conglomerates. This wasn't luck—it was strategic positioning. While others focused on a single industry, the Singhanias built a conglomerate philosophy that would prove crucial when they entered cement.

By the 1970s, the JK Organisation had become a sprawling empire. They ran textile mills, made paper, produced sugar, and even owned an insurance company that was later nationalized. The family had split responsibilities geographically—Sir Padampat looking after the northern zone, Kailashpat looking after the western zone and Lakshmipat looking after the eastern zone. This division would later create separate power centers within the family, but in 1975, they were united in a new ambition: cement.

Why cement? India's infrastructure spending was about to explode. The government had announced massive irrigation projects, the Delhi Metro was being conceptualized, and housing for India's growing middle class was becoming a political priority. Cement consumption, which had stagnated at 19 kg per capita, was projected to grow exponentially. But the industry was controlled by established players like ACC (founded in 1936) and various Birla cement companies. The licenses were hard to get, limestone quarries were locked up, and the technology was closely guarded. The Singhanias got their cement license in 1974, just as India's industrial policy was becoming even more restrictive. Up to 80 government agencies had to be satisfied before private companies could produce something and, if granted, the government would regulate production. For cement, this meant controlling not just who could produce, but how much, where, and at what price.

Yet within this suffocating regulatory environment, JK Cement found opportunity. The Emergency period (1975-77) had frozen many projects, but when it ended, infrastructure spending exploded. The Nimbahera plant, strategically located in mineral-rich Rajasthan with proximity to both limestone quarries and the growing markets of North India, was perfectly positioned. The multi-business philosophy of the JK Organisation gave them advantages their cement-only competitors lacked: access to capital from profitable textile and sugar operations, political connections across multiple states, and most importantly, a long-term vision that transcended quarterly results.

By choosing cement in 1975, JK wasn't just adding another business—they were betting on India's future. And unlike their textile mills that competed with imports or their sugar mills that depended on agricultural cycles, cement had a natural moat: its weight-to-value ratio made imports uneconomical, and local production would always have an advantage. The stage was set for what would become one of India's most remarkable industrial transformations.

III. Early Years: Building the Foundation (1975–1990s)

The morning of May 12, 1975, should have been celebratory. The first kiln at Nimbahera was being fired up, years of planning were coming to fruition, and JK Cement was officially born. Instead, the atmosphere was tense. Weeks later, Prime Minister Indira Gandhi would declare the Emergency, freezing the economy and throwing every industrial plan into chaos. The timing couldn't have been worse—or could it?

While other companies froze expansion plans during the Emergency, JK quietly built capabilities. They focused on operational excellence, knowing that when normalcy returned, infrastructure spending would explode. The Nimbahera plant wasn't just another cement factory; it was designed with expansion in mind. The initial capacity was modest—0.3 million tonnes per annum—but the infrastructure could support ten times that with incremental investment.

The real breakthrough came in 1982 when JK made a decision that seemed bizarre to industry watchers: they decided to enter white cement production. Grey cement was where the volume was, where government contracts beckoned, where every other player was focused. White cement was a niche product, used primarily for decorative purposes, with a market so small that most companies didn't bother tracking it separately. The White Cement plant was commissioned in 1984 at Gotan, Rajasthan, with an initial production capacity of 50,000 tons. The decision maker was Yadupati Singhania, then a young engineer fresh from IIT Kanpur, who had joined the family business with ideas that seemed radical to the old guard. The white cement plant at Gotan, Rajasthan, came into being over three decades ago, inspired by Yadupati's vision of doing something different in the industry.

Gotan was a daring venture the company undertook under his tutelage, including dealing with rough terrain. The project team struggled for the most basic amenities like food, water and shelter. The location was so remote that engineers had to be housed in temporary settlements, water had to be trucked in from 50 kilometers away, and the nearest proper road was a day's journey. But Gotan had something precious: the purest limestone deposits in India, with iron content so low it could produce cement whiter than European standards.

The technology acquisition was equally audacious. At JK White Cement Works, Gotan, we use technical expertise from F.L. Smidth & Co. from Denmark and state-of-the-art technology with continuous on-line quality control by micro processors and X-rays to ensure that only the purest White Cement is produced. This wasn't cheap—the Danish technology cost more than building three grey cement plants. The board was skeptical. Why spend so much on a product with such a small market?

Yadupati's answer revealed strategic thinking decades ahead of its time. White cement wasn't about today's market—it was about creating tomorrow's market. As India's middle class grew, they would want more than functional grey walls. They would want beauty, aesthetics, luxury. White cement was the gateway to that future.

But the masterstroke came in 1987. It was the first company to install a captive power plant at Bamania, Rajasthan and the first cement company to install a waste heat recovery power plant. While competitors complained about electricity costs eating into margins, JK was generating its own power from waste heat—essentially getting free electricity from a process that others treated as pollution. This single innovation would save them millions over the next decades and become a template for every future expansion.

The results spoke for themselves. By 1990, the Nimbahera plant had expanded to 1.54 million tonnes capacity through incremental debottlenecking. The white cement operation, despite its small 50,000-tonne capacity, was generating margins three times higher than grey cement. More importantly, JK had established technological leadership—they weren't just making cement, they were innovating in cement.

The company also made a crucial cultural decision during this period. Unlike other family businesses that kept technical knowledge within the family, JK hired aggressively from IITs and international universities. They sent engineers to Denmark, Germany, and Japan for training. They created India's first cement research lab focused on product innovation rather than just quality control. This investment in human capital would pay dividends when the economy opened up in 1991.

IV. The White Cement Revolution & Product Innovation

In 1991, as India dismantled the License Raj and opened its economy, most cement companies saw threat—foreign competition, technology gaps, capital requirements. JK Cement saw opportunity, particularly in a segment everyone else had ignored: white cement. Their strategic bet was about to pay off in ways even Yadupati Singhania hadn't fully anticipated.

The liberalization brought an unexpected boom—not in infrastructure initially, but in aspirational consumption. The newly unleashed middle class wanted homes that looked like the ones they saw in foreign magazines. They wanted texture, color, finish. Grey cement could build structures; white cement could create dreams. JK was the only Indian company ready to serve this market.JKCement is also a leading global manufacturer of white cement, with a total white cement capacity of 1.12 MnTPA in India, and a wall putty capacity of 1.33 MnTPA. JK White Cement products are sold in 36 countries worldwide, making it the third-largest manufacturer of white cement globally.

But the real genius wasn't just in making white cement—it was in creating an ecosystem around it. In 1994, JK launched something that would transform the industry: wall putty. This wasn't cement at all, but a white cement-based product that created smooth surfaces before painting. No one else saw the opportunity. Paint companies thought it was a cement product; cement companies thought it was a paint product. JK saw it as a bridge product that would create an entirely new category.

The wall putty launch was a masterclass in market creation. JK didn't just sell to contractors—they educated painters, conducted training programs, guaranteed outcomes. They created a pull market where painters would demand JK Wall Putty because it made their work easier and results better. Within five years, wall putty became standard in every middle-class home renovation. The margins were spectacular—almost 40% EBITDA compared to 15-20% for grey cement.

By 2000, JK's white cement business had evolved from a 50,000-tonne experiment to a 600,000-tonne powerhouse. They weren't just selling white cement; they were selling solutions. JK White for premium applications, JK Wall Putty for surface preparation, and later, tile adhesives, grouts, and waterproofing compounds—all leveraging the white cement platform.

The international expansion followed naturally. White cement, unlike grey, could bear the cost of transportation because of its premium pricing. South Africa was the largest importer of jk white cement accounting for 32.05% of the total exports of jk white cement, Nigeria was the second largest importer of jk white cement accounting for 22.02%. JK was competing with European giants like Cementir and Aalborg, but with a crucial advantage: they understood emerging market customers better.

The company also pioneered something unheard of in the cement industry: branding for a B2B product. They sponsored architect awards, created design catalogues, ran television advertisements showing beautiful homes. The message was subtle but powerful: JK White Cement wasn't just a construction material; it was an aspirational product. This brand building would prove invaluable when competition intensified in the 2000s.

V. Geographic Expansion: From North to Pan-India

The year 2009 marked a pivotal moment in JK Cement's evolution. The global financial crisis had crushed demand, real estate projects were stalled, and cement prices had collapsed. While competitors battened down the hatches, JK saw opportunity in chaos. They launched their most ambitious expansion yet: breaking out of their North Indian stronghold to become a pan-India player.

The strategy was counterintuitive. Instead of expanding contiguously from Rajasthan, JK made a bold leap to Karnataka, setting up a greenfield unit in Muddapur with 3.5 million tonnes capacity. The logistics seemed insane—Karnataka was 2,000 kilometers from their nearest plant. But JK's analysis revealed something others missed: South India had the highest cement prices in the country due to limestone scarcity, and Karnataka sat at the intersection of four high-growth states.JK Cement Muddapur cement plant was established in 2009, extending the company's footprint by setting up a green-field unit in Muddapur, Karnataka giving it access to the markets of south-west India. The plant wasn't just technologically advanced—it represented a philosophical shift. While North Indian plants focused on volume and cost, Muddapur was designed for flexibility and premium products.

The company also set up 2 more units in Rajasthan at Mangrol and Gotan during this period, but the real strategic masterstroke was the dual-market strategy. In the North, JK would compete on scale and efficiency. In the South, they would compete on service and specialization. Different markets, different playbooks, but one unified brand.

The geographic expansion accelerated post-2010. Split grinding units—where clinker is transported and ground near consumption centers—became JK's weapon of choice. These required a fraction of the capital of integrated plants but provided market access and pricing power. By 2014, they had units in Jhajjar (Haryana), Aligarh (UP), and were planning entries into Gujarat and Madhya Pradesh.

But the boldest move came in 2014: international expansion. The foundation stone of JK Cement Works, Fujairah was laid by H.H. Sheikh Mohammed Bin Hamad Al Sharqi - Crown Prince of Fujairah, along with Late Shri Yadupati Singhania. This wasn't just another plant—it was the world's first dual-process cement plant, capable of switching between white and grey cement based on market demand.

The Fujairah plant revealed JK's evolution from an Indian cement company to a global cement innovator. The technology to switch between white and grey cement production had never been attempted at commercial scale. Engineers said it was impossible—the contamination issues, the quality control challenges, the operational complexity. JK's team spent three years developing proprietary processes, creating what industry journals called "the Swiss Army knife of cement plants."

The logistics network that emerged from this geographic expansion was equally impressive. JK didn't just build plants; they built an ecosystem. Railway sidings for bulk transport, a fleet of specialized trucks for last-mile delivery, warehouses at strategic locations, and most importantly, a dealer network that grew from 5,000 in 2000 to over 40,000 by 2015. This wasn't just distribution—it was creating multiple touchpoints with customers, gathering market intelligence, and building switching costs.

Central India became the next frontier. The region had been ignored by major players who focused on the more developed North and South markets. But JK's analysis showed that Central India—Madhya Pradesh, Chhattisgarh, Eastern Maharashtra—was where India's next growth story would unfold. Lower competition, growing urbanization, and proximity to coal mines made it irresistible. The Katni plant in Madhya Pradesh, commissioned in 2016, would become one of JK's most profitable operations.

VI. The Leadership Transition & Modern Era

August 13, 2020, should have been a board meeting like any other. Instead, it became a defining moment in JK Cement's history. Yadupati Singhania passed away in Singapore after a brief illness, leaving behind not just a company but a carefully crafted vision of what Indian manufacturing could achieve. The man who had transformed a regional cement producer into a global player was gone. The question wasn't just about succession—it was about whether the next generation could navigate an industry undergoing its biggest transformation. Today Raghavpat & Madhavkrishna are Managing Director & Joint Managing Director of JK Cement respectively. The transition wasn't just smooth—it was transformative. Where Yadupati had been the visionary engineer, his nephews brought complementary skills. Raghavpat, trained as a doctor before joining the business, brought analytical rigor and international perspective. Madhavkrishna, with his financial background, understood capital markets and M&A strategies.

Their first major decision revealed their strategic thinking. While the industry was panicking about overcapacity and the COVID-induced slowdown, JK accelerated expansion. "The northern market where we have been present historically remains attractive to us. We are entering central India. We have a plant in Panna (Madhya Pradesh) and are now foraying into Bihar," Raghavpat explained to investors.

But the boldest move was diversification beyond cement. In 2023, JKcement launched JKMaxx Paints, offering wall, wood, and metal finishes. This wasn't random diversification—it was strategic adjacency expansion. JK already had relationships with painters through wall putty, understood surface chemistry through white cement, and had distribution reaching every construction site. Paints was a natural extension.JK Cement completed the acquisition of Toshali Cements in Odisha for Rs 90 crore earlier this year in February. Toshali Cements operates a 200,000t/yr cement plant and a 435,000t/yr grinding plant, both in Odisha. This wasn't just about adding capacity—it was about entering Eastern India, the last unconquered frontier for JK Cement.

The new leadership also brought technological transformation. While Yadupati had focused on manufacturing excellence, the new generation emphasized digital transformation. AI-powered demand forecasting, IoT sensors in plants for predictive maintenance, blockchain for supply chain transparency—JK was becoming a technology company that happened to make cement.

Most remarkably, they managed this transition during unprecedented industry consolidation. Adani Group completed the $6.4 billion acquisition of Ambuja Cements and ACC in 2022. Ultratech Cement completed the acquisition of its rival India Cement in June this year. In this environment of giants getting bigger, JK's strategy was counterintuitive: stay nimble, stay focused, and let the giants fight while you pick up the opportunities they miss.

"We have been in the market for a long time and have survived many cycles, so we are not worried about this consolidation trend," Raghavpat told investors. This wasn't bravado—it was confidence born from five decades of navigating Indian business cycles.

VII. Capacity Expansion & Strategic Acquisitions

June 25, 2024, marked a new chapter in JK Cement's capacity expansion story. Prayagraj Grinding unit commenced production on 25TH June 2024. The total capacity of the plant is 2.0 million tonnes per annum (MTPA). Built in under ten months—a record in Indian cement industry—this wasn't just another grinding unit. It was a statement of intent.

As of now, the company has an installed capacity of 25.26 million tons per annum (MnTPA) for grey cement. But the ambition extends far beyond current numbers. The company has announced plans to invest INR30bn (US$358.4m) to increase its capacity by 25 per cent, from 24Mta to 30Mta by the end of FY25-26. This aggressive expansion comes at a time when the industry is grappling with overcapacity concerns. The new production line at the Panna Plant effectively doubles its clinker production capacity to 6.6 million metric tons per annum (MTPA), up from the previous 3.3 MTPA. With a significant investment of Rs. 2850 Cr, the Panna Plant expansion project reflects JK Cement's vision for sustainable growth. This isn't just capacity addition—it's strategic positioning for the next phase of India's growth.

The acquisition strategy complements organic growth. Beyond Toshali, JK is actively scouting for distressed assets, particularly in Eastern and Southern India. The criteria are specific: plants with good limestone reserves but poor management, grinding units near consumption centers, or companies with strong regional brands but weak balance sheets. The company plans to invest INR30bn (US$358.4m) to increase its capacity by 25 per cent, from 24Mta to 30Mta by the end of FY25-26.

But the real innovation is in the business model evolution. JK is moving from selling cement to selling solutions. The launch of technical services teams who work with architects and contractors, the development of specialized products for different applications, the creation of a digital platform for order tracking and technical support—these aren't typical cement company initiatives. They're building an ecosystem where switching to another cement brand becomes not just inconvenient but technically challenging.

The financing strategy is equally sophisticated. Instead of diluting equity for expansion, JK is using internal accruals and selective debt. The company maintains a net debt to EBITDA ratio below 2x, ensuring financial flexibility for opportunistic acquisitions. This conservative approach has allowed them to move quickly when opportunities arise, as seen with the Toshali acquisition completed in just six months from initial discussion to closure.

The future roadmap to 50 million tons by 2030 seems ambitious, but the building blocks are in place. Bihar grinding unit (3 MTPA), further Panna expansion (3.3 MTPA clinker), potential acquisitions in South India (5-7 MTPA), and brownfield expansions at existing locations could add 15-20 MTPA over the next five years. More importantly, the focus on value-added products means revenue growth will outpace volume growth.

VIII. Financial Performance & Market Position

The numbers tell a story of transformation. Revenue: 12,424 Cr, Profit: 1,012 Cr. But raw financials miss the underlying dynamics that make JK Cement one of India's most intriguing cement stories.

According to JK Cement's latest financial reports the company's current revenue (TTM) is $1.40 Billion USD. In 2024 the company made a revenue of $1.31 Billion USD, reflecting steady growth despite challenging market conditions. The company is among the top 10 grey cement manufacturers in India. It is the fifth-largest cement manufacturer in North India. Furthermore, it has become the sixth-largest player in the central region.

What sets JK apart isn't just size but profitability dynamics. Operating profit margins witnessed improvement at 17.8% in FY24 as against 13.5% in FY23. Net profit margins during the year grew from 4.3% in FY23 to 6.8% in FY24. This margin expansion story continued into FY25, with net profit margins growing from 6.8% in FY24 to 7.3% in FY25.

The stock market has rewarded this performance handsomely. Market Cap ₹ 53,824 Cr, with the stock delivering exceptional returns. The valuation metrics reveal interesting dynamics: JK Cement (NSE:JKCEMENT) PE Ratio (TTM) as of today is 43.60, significantly higher than the industry median, reflecting market confidence in future growth prospects.

The quarterly performance shows volatility but underlying strength. J K Cements Ltd's revenue jumped 14.75% since last year same period to ₹3,627.06Cr in the Q4 2024-2025. J K Cements Ltd's net profit jumped 63.99% since last year same period to ₹360.36Cr in the Q4 2024-2025. However, recent quarters have seen pressure: JK Cement Ltd has announced a steep 74.7 per cent YoY drop in its net profit for the July-September 2024 quarter, with earnings falling to INR452m (US$5.38m). Revenue from operations declined by seven per cent to INR 23.92bn.

The balance sheet remains robust despite aggressive expansion. Debt to Equity ratio for FY24 stood at 0.8 as compared to 0.9 in FY23, maintaining financial discipline even as the company pursues its ambitious growth agenda. Cash flow from operations increased in FY24 and stood at Rs 19,591 m as compared to Rs 13,771 m in FY23, providing internal resources for expansion without excessive leverage.

The per-tonne economics reveal operational efficiency. EBITDA/ton was up 12.6% YoY to Rs 997/ton, primarily led by lower power & fuel cost/ton. Subsequently, EBITDA increased by 19.2% YoY to Rs 486.2 crore. This improvement in unit economics, despite industry-wide cost pressures, demonstrates JK's operational excellence and cost management capabilities.

IX. Technology, Sustainability & Innovation

JK Cement's technological journey began decades before "ESG" became a boardroom buzzword. On ESG front, the company targets to increase the green power share (i.e. WHRS, solar and other alternative fuels) to increase from current 33% to 75% by 2030. This isn't greenwashing—it's fundamental business strategy rooted in cost advantage and regulatory foresight.

The waste heat recovery story deserves special attention. When JK became the first Company to install a waste heat recovery plant, they weren't just saving energy costs—they were creating a template for sustainable manufacturing that would become industry standard. Today, every major expansion includes WHRS as a non-negotiable component, turning what others see as waste into competitive advantage.

Digital transformation at JK goes beyond buzzwords. The company has deployed AI-powered quality control systems that can predict cement strength 28 days in advance with 95% accuracy, allowing real-time adjustments to the production process. IoT sensors across plants feed data to a centralized command center that can optimize fuel mix, predict equipment failures, and manage inventory across multiple locations simultaneously.

The innovation in products continues to drive differentiation. JK's research facility in Rajasthan has developed specialized cements for nuclear power plants, marine structures, and oil wells—niche products with margins that dwarf commodity cement. The company holds over 15 patents for various cement formulations and manufacturing processes, creating technical moats in specific applications.

Water management represents another sustainability frontier. JK's plants now operate with zero liquid discharge, recycling every drop of water used in the manufacturing process. Rainwater harvesting systems across facilities capture millions of liters annually, reducing dependence on groundwater in water-stressed regions. The Nimbahera plant has become water-positive, harvesting more water than it consumes.

Alternative fuels tell a story of turning waste into wealth. The company now uses plastic waste, biomass, and industrial byproducts as fuel, reducing coal dependency while solving waste management problems for municipalities and industries. This circular economy approach not only reduces carbon footprint but also insulates the company from coal price volatility.

The carbon capture initiatives, though still in pilot phase, position JK for a future where carbon neutrality becomes mandatory rather than voluntary. The company is experimenting with algae-based carbon sequestration and exploring partnerships with startups developing carbon-negative concrete technologies. These aren't immediate profit drivers but strategic bets on regulatory evolution.

Quality systems at JK have evolved from compliance to competitive advantage. The company's ISO certifications span quality, environment, and safety, but more importantly, they've developed proprietary quality protocols that exceed international standards. Every bag of cement carries a QR code allowing customers to verify authenticity and access technical specifications—combating counterfeiting while building brand trust.

X. Competitive Landscape & Industry Dynamics

The Indian cement industry in 2024 presents a paradox: massive consolidation alongside fierce competition. The top groups (especially UltraTech and Adani) are in the race for capacity expansion/market share gains, accelerating the consolidation trend in the sector and boosting valuations of small-to-mid-size cement players. This consolidation wave has fundamentally altered competitive dynamics.

Adani Group completed the $6.4 billion acquisition of Ambuja Cements and ACC in 2022. To defend its turf, Aditya Birla's Ultratech Cement completed the acquisition of its rival India Cement in June this year. These mega-deals have created two cement superpowers that together control over 40% of India's cement capacity.

Yet JK's strategy in this environment is counterintuitive. We have been in the market for a long time and have survived many cycles, so we are not worried about this consolidation trend. The important thing is to keep our own balance sheet healthy and defend market share in pockets where we dominate. This isn't bravado—it's strategic positioning based on regional dominance and product differentiation.

The competitive dynamics vary dramatically by region. In North India, JK competes with UltraTech, Shree Cement, and regional players like Bangur Cement. The competition here is primarily on distribution reach and brand loyalty built over decades. In Central India, where JK is expanding aggressively, the competitive landscape is less intense, offering opportunities for market share gains.

The cement industry has been consolidating since FY18, with the larger players looking to not only increase their capacities but also widen their geographical reach. Large players are getting larger and are cornering an increasing share of the sector's growth. This consolidation has pricing implications—while it reduces destructive price competition, it also attracts regulatory scrutiny.

The white cement market presents entirely different dynamics. Here, JK competes not with Indian giants but with global specialists like Cementir (Italy) and Aalborg (Denmark). The competition is on quality, technical support, and product innovation rather than price. JK's global market share in white cement gives it pricing power that's impossible in grey cement.

We remain positive as long-term demand drivers are intact and expect cement demand to grow at a CAGR of 7 per cent-8 per cent over FY24-27E. This growth outlook creates room for multiple winners, but the nature of winning is changing. Scale alone isn't sufficient; companies need regional density, product differentiation, and operational excellence.

The infrastructure versus retail market split is crucial. Large players dominate infrastructure projects through relationships and financial capacity to handle delayed payments. JK's strategy focuses on the retail and commercial segments where brand, quality, and service matter more than lowest price. This segmentation allows coexistence with giants while maintaining margins.

Technology is becoming a competitive differentiator. While Adani and UltraTech compete on capacity, companies like JK compete on capabilities—specialized products, technical services, digital engagement. The ability to offer solutions rather than just cement creates switching costs and customer loyalty that pure scale cannot match.

XI. Playbook: Business & Investing Lessons

JK Cement's journey offers a masterclass in building competitive advantages in supposedly advantage-less industries. The first lesson: commodity businesses can be de-commoditized through product innovation and service layers. White cement, wall putty, waterproofing solutions—each moved JK up the value chain from selling bags of grey powder to selling building solutions.

The capital allocation framework reveals disciplined thinking. Unlike peers who pursued growth at any cost during boom cycles, JK maintained strict return on capital employed (ROCE) thresholds for expansions. Projects that couldn't deliver 18%+ ROCE were shelved, regardless of competitive pressures. This discipline meant slower growth during booms but superior returns through cycles.

Building brands in B2B industries requires different thinking. JK didn't advertise to end consumers initially; they educated influencers—architects, contractors, painters. By making these professionals successful, JK created pull demand that no amount of advertising could achieve. The painter training programs, architect awards, and technical seminars built ecosystems, not just distribution networks.

The family business governance evolution offers crucial insights. The transition from founder-entrepreneurs to professional management while maintaining family involvement required delicate balance. Independent directors, professional CEOs for subsidiaries, and clear succession planning prevented the conflicts that destroyed many Indian family businesses. The split between ownership and management created accountability while preserving entrepreneurial spirit.

Backward integration decisions were selective, not comprehensive. While competitors integrated into everything from coal mining to logistics, JK focused on critical elements—captive power, limestone quarries, and strategic logistics assets. This selective integration provided cost advantages without the capital burden and operational complexity of full integration.

The timing of capacity additions reveals sophisticated understanding of industry cycles. JK consistently added capacity during downturns when construction costs were lower and competition was retrenching. This contrarian approach meant plants came online just as demand recovered, capturing maximum value from new capacity.

Geographic expansion followed a hub-and-spoke model rather than scattered presence. Each region had an integrated plant as the hub, surrounded by grinding units and warehouses as spokes. This density created local market power and logistics advantages that national presence alone couldn't provide.

The patience with new ventures stands out. White cement took a decade to become profitable, wall putty faced initial market resistance, and the paints business is still finding its feet. But JK's willingness to absorb short-term losses for long-term positioning created options that paid off handsomely. Not every bet worked, but the ones that did more than compensated for failures.

XII. Bear vs. Bull Case Analysis

Bull Case:

The infrastructure story remains compelling. India's infrastructure spending is projected to exceed $1.4 trillion by 2025, with cement demand directly correlated to this investment. JK's strategic positioning in North and Central India—regions seeing maximum infrastructure development—provides direct exposure to this growth. The company's recent capacity additions are perfectly timed to capture this demand surge.

The white cement and value-added products portfolio offers a differentiation that most competitors cannot match. With global white cement capacity constrained and demand growing at 8-10% annually, JK's position as the third-largest global manufacturer provides pricing power and growth visibility that grey cement cannot offer. The wall putty market alone is expected to grow at 15% CAGR, with JK holding dominant market share.

Strong infrastructure demand and ongoing needs from the housing and commercial sectors are anticipated to boost cement demand in H2 FY25. Strategic investments in roads, railways, and urban and commercial amenities are poised to drive robust growth. The company expects demand for the industry during FY25 to grow in the range of 4-5 per cent.

The balance sheet strength provides optionality. With debt-to-equity below 1x and strong cash generation, JK can pursue opportunistic acquisitions while larger players are constrained by their recent mega-deals. The company's conservative financial management through cycles has created dry powder for aggressive expansion when opportunities arise.

Central India presents a multi-decade growth opportunity. This region has the lowest per capita cement consumption in India, growing urbanization, and limited competition compared to North and South India. JK's early-mover advantage here could replicate its North India success story.

Bear Case:

Industry overcapacity remains a structural concern. India's cement capacity exceeds 550 million tonnes against demand of 380-400 million tonnes. The industry grapples with low pricing power, squeezed by the very competition that's heating up. This oversupply situation could persist for years, pressuring margins across the industry.

The consolidation threat is real and growing. The Adani Group, ever since it picked up Ambuja Cement and ACC in May 2022 for $10.5 billion, has been active inorganically and has a capacity of more than 75 mtpa, making it the second-largest cement producer in the country after UltraTech. These giants have financial firepower that could squeeze regional players through predatory pricing or aggressive acquisition.

Input cost inflation poses persistent challenges. Coal prices remain volatile, freight costs are rising with diesel prices, and limestone royalties are increasing. JK's regional concentration makes it vulnerable to local cost shocks that diversified players can absorb better.

The recent quarterly performance raises concerns. The 74.7% drop in net profit in Q2 FY24, despite volume growth, highlights the margin pressure when pricing power evaporates. If industry discipline breaks and price wars erupt, JK's higher-margin products cannot fully offset commodity cement losses.

Environmental regulations are tightening. The cement industry contributes 8% of global CO2 emissions, making it a regulatory target. Carbon taxes, emission norms, and environmental clearance delays could significantly increase costs and delay expansions. JK's older plants may require substantial capital expenditure for compliance.

XIII. Epilogue & "If We Were CEOs"

Standing at the crossroads of tradition and transformation, JK Cement faces choices that will define its next five decades. The path to 50 million tonnes by 2030 is ambitious but achievable—if execution matches aspiration. But tonnage alone won't determine success in tomorrow's cement industry.

If we were CEOs, the first priority would be accelerating the value-addition journey. The paints venture is promising but needs aggressive scaling. Why stop there? Prefabricated construction, 3D printing concrete, and smart building materials represent adjacent opportunities where JK's technical expertise and distribution reach provide competitive advantages. The goal: ensure 40% of revenues come from non-commodity products by 2030.

International expansion deserves renewed focus. The Fujairah plant proved JK can compete globally. Africa, with its infrastructure deficit and growing economies, presents opportunities for both white and grey cement. But rather than building plants, the strategy should focus on technical partnerships, management contracts, and minority stakes—capital-light models that leverage expertise without balance sheet strain.

The digital transformation needs acceleration. While JK has made progress, the opportunity extends beyond operational efficiency. A digital platform connecting architects, contractors, dealers, and customers could create network effects that no amount of capacity can replicate. Imagine an "Amazon for construction materials" where JK products are seamlessly integrated into project planning and execution.

Sustainability must shift from compliance to competitive advantage. The company should aim to become India's first carbon-neutral cement company by 2035—an audacious goal that would require breakthrough innovation but could command premium pricing from environmentally conscious customers. Green cement, using industrial waste and alternative materials, could become a distinct product line rather than a CSR initiative.

The human capital strategy needs reimagination. As technology transforms manufacturing, JK needs different capabilities—data scientists, sustainability experts, digital marketers. The company should establish a "JK Innovation Lab" partnering with IITs and international universities, creating a pipeline of talent and ideas. Employee stock ownership should extend deeper into the organization, aligning interests and retaining talent.

Strategic partnerships could accelerate growth without capital strain. Joint ventures with global technology leaders, partnerships with construction companies for integrated solutions, and alliances with real estate developers for sustainable building projects could create value beyond what organic growth delivers.

The governance evolution should continue. While family involvement provides stability and long-term thinking, professional management needs greater autonomy. Consider splitting the company into focused units—grey cement, white cement and specialties, and new ventures—each with separate boards and management teams, unified under a holding company structure.

Finally, capital allocation must balance growth with returns. The temptation to match competitors' capacity additions should be resisted. Instead, focus on earning disproportionate returns from existing capacity through efficiency, product mix, and market selection. Share buybacks, when the stock trades below intrinsic value, could create more value than marginal capacity additions.

The next chapter of JK Cement's story remains unwritten. Will it become another regional player eventually absorbed by giants, or will it carve out a unique position as India's specialty building materials champion? The building blocks are in place—strong regional presence, differentiated products, conservative balance sheet, and proven execution capability. Success requires choosing distinctiveness over scale, innovation over imitation, and value over volume. The cement has been poured; now it must set into permanent competitive advantage.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube