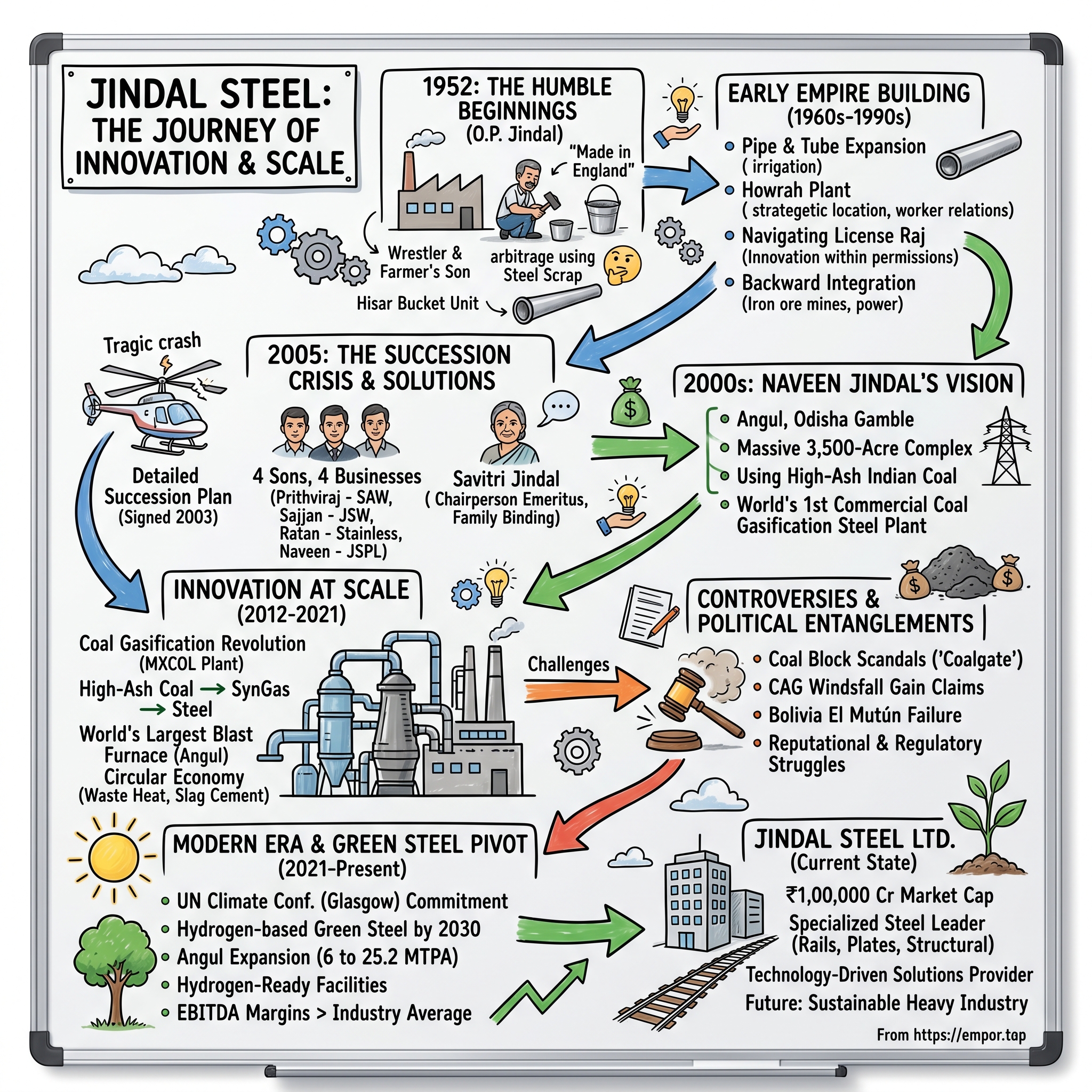

Jindal Steel: From Bucket Manufacturing to India's Steel Innovation Leader

Introduction & Episode Roadmap

The year is 2012, and in the remote district of Angul in Odisha, India, something unprecedented is happening. Inside a sprawling 3,500-acre complex, engineers are firing up the world's first commercial coal gasification-based steel plant. The technology is so radical that industry veterans have called it impossible—making high-quality steel from India's notoriously poor-quality, high-ash coal. As the first molten steel pours from the furnace, Naveen Jindal, the man who bet his company's future on this moonshot, watches from the control room. This moment represents not just a technological breakthrough, but the culmination of a 60-year journey that began with his father hammering out buckets in a small workshop in Haryana.

Today, Jindal Steel Limited commands a market capitalization of over ₹1,00,000 crore, ranking among India's steel titans. The company, which quietly shed "Power" from its name in July 2025 to become simply Jindal Steel Limited, produces everything from railway tracks that carry India's millions to specialized plates that armor the nation's military vehicles. But how did a farmer's son who started with a bucket factory build one of India's most innovative steel companies? How did a family business navigate the treacherous waters of Indian politics, survive a tragic succession crisis, and emerge as a technological leader in one of the world's most commoditized industries?

This is a story of audacious bets, family dynamics that would make a soap opera blush, and the relentless pursuit of turning India's disadvantages into competitive advantages. It's about how the Jindal family transformed from rural entrepreneurs into industrial royalty, and how they're now racing to reinvent themselves for a carbon-conscious future. Along the way, we'll explore the controversies that nearly derailed them, the political entanglements that both propelled and plagued them, and the technological gambles that define them today.

The O.P. Jindal Origin Story & Philosophy

Om Prakash Jindal's hands were not meant for steel. Born in 1930 in the dusty village of Nalwa in Haryana's Hisar district, the young O.P. spent his childhood wrestling in the village akhara, his muscular frame earning him local fame as a teenage bodybuilder. His parents, simple farmers who knew more about wheat harvests than industrial revolution, watched their son's growing obsession with physical strength with a mixture of pride and concern. They had different plans for him—perhaps he could escape the vagaries of agriculture through trade. So in 1947, as India gained independence and partition tore the subcontinent apart, they sent their 17-year-old son to Calcutta with a simple mission: learn the textile business.

But Calcutta in the late 1940s was a city transforming. The former colonial capital was becoming an industrial hub, and young O.P. found himself drawn not to textiles but to the clanging symphony of metal workshops. He would spend hours in the industrial areas, watching sparks fly as workers shaped steel. One particular moment changed everything. Standing in a pipe factory, he picked up a steel pipe and saw stamped on it: "Made in England." The irony struck him like a physical blow—here was independent India, importing basic industrial products from its former colonizer. That pipe became his mission statement.

By 1952, O.P. had saved enough to start a tiny bucket-manufacturing unit in Hisar. The operation was almost comically humble—a few workers, basic tools, and O.P. himself working 18-hour days, his bodybuilder's strength now channeled into hammering metal. But this wasn't just about making buckets. O.P. had discovered something remarkable: India was throwing away massive amounts of steel scrap, considering it worthless, while simultaneously importing finished steel products. He saw an arbitrage opportunity that others had missed—converting this "waste" into useful products.

What set O.P. apart wasn't just his business acumen but his almost mystical relationship with machinery. Workers would later describe how he could diagnose a machine's problems just by listening to it run, earning him the nickname "Machine Whisperer." He would walk through the factory floor, pause near a running lathe or press, cock his head slightly, and announce, "The third bearing needs replacement" or "The alignment is off by two degrees." He was invariably right. This hands-on approach became the cornerstone of what would become the Jindal management philosophy.

The 1950s and 60s saw O.P. methodically expand from buckets to pipes, from pipes to tubes, from tubes to more complex steel products. But his vision extended beyond business. He believed in swadeshi—economic self-reliance—before it became fashionable. Every product his companies made was one less import, one step toward India's industrial independence. He would often tell his sons, "We're not just making steel; we're building a nation."

This philosophy attracted attention beyond the business world. O.P. became increasingly involved in Haryana politics, eventually serving as the state's Power Minister. He understood that in India's controlled economy, political connections weren't just helpful—they were essential for navigating the maze of licenses and permits required to grow an industrial enterprise. Yet he maintained a reputation for straight dealing, unusual in an era where corruption was endemic.

By the early 2000s, O.P. Jindal had built an empire valued at over $2 billion. Forbes ranked him as the 13th richest Indian and 548th globally in 2004. He had transformed from a wrestler's son in rural Haryana to one of India's industrial titans. His four sons—Prithviraj, Sajjan, Ratan, and Naveen—had all been groomed in the family business, each developing expertise in different areas. O.P. had even worked out a detailed succession plan, unusual for Indian family businesses where succession often triggered bitter feuds.

The culmination of O.P.'s philosophy came in his approach to technology and innovation. While his competitors focused on licensing foreign technology, O.P. invested heavily in developing indigenous capabilities. His companies didn't just operate steel plants; they designed and built them. This emphasis on technological self-reliance would prove prophetic, setting the stage for his youngest son Naveen's later gambles on radical new steelmaking technologies. As O.P. often said, "If you always follow others, you'll always be behind."

Building the Steel Empire: The Early Years (1952-1990s)

The India of 1952 was a nation finding its industrial feet. As Nehru spoke of temples of modern India, referring to dams and factories, O.P. Jindal was building his own temple in a modest workshop in Hisar. The transition from buckets to pipes wasn't just a product evolution—it was a masterclass in reading market signals. O.P. had noticed that India's massive irrigation projects needed pipes, lots of them, and they were all being imported. His first major breakthrough came when he figured out how to convert steel strips into pipes using a technique he had modified from what he'd observed in Calcutta's workshops.

The real transformation began when O.P. established Jindal India Ltd. in Howrah, West Bengal. The location was strategic—close to Calcutta's port for raw material imports and in the heart of India's industrial belt. But setting up in Howrah meant navigating West Bengal's notorious labor unions and communist politics. O.P.'s approach was unconventional: instead of confrontation, he embraced the workers, often eating lunch with them on the factory floor, listening to their concerns, and implementing profit-sharing schemes decades before they became fashionable. The factory became known for something remarkable in 1960s India—it never had a strike.

The License Raj era of the 1960s and 70s should have been O.P.'s biggest obstacle. This Byzantine system required government permission for everything from importing machinery to expanding production capacity. Most industrialists spent more time in Delhi's corridors of power than in their factories. O.P. turned this challenge into an opportunity. While his competitors waited months for licenses, he had mastered the art of working within existing permissions, constantly innovating to squeeze more production from licensed capacity. When regulations limited his pipe production, he started making specialized tubes. When tube production was capped, he moved into value-added products.

A defining moment came in 1969 when the government announced plans to nationalize the steel industry. While larger players panicked, O.P. saw an opening. He quickly pivoted to focus on specialized steel products that fell outside the nationalization scope—stainless steel, special alloys, and precision tubes. This wasn't just evasion; it was strategic positioning. By the time the nationalization wave passed, Jindal companies had established themselves in niches that the public sector steel giants couldn't serve effectively.

The 1970s brought O.P.'s first major technological coup. He acquired a secondhand rolling mill from Japan that others had rejected as obsolete. His engineers spent six months rebuilding it, incorporating modifications that O.P. had sketched out on paper napkins during late-night brainstorming sessions. When it finally started production, it could produce specifications that even new mills couldn't match. This became the Jindal way—taking what others discarded and transforming it into competitive advantage.

By the 1980s, the Jindal empire had grown beyond steel pipes and tubes. O.P. had established three major companies that would form the backbone of the family's wealth: Jindal Steel and Power (JSPL), which would focus on large-scale steel production and power generation; JSW Group, which would become a diversified conglomerate; and Jindal Stainless Limited, which would dominate India's stainless steel market. Each company was structured as a separate entity, but with careful cross-holdings that maintained family control while allowing for independent growth trajectories.

The political dimension of O.P.'s empire-building cannot be ignored. His stint as Haryana's Power Minister in the 1980s gave him insights into infrastructure development that his purely business-focused competitors lacked. He understood that India's power shortage was steel's opportunity—every new power plant needed massive amounts of specialized steel. He positioned his companies to benefit from India's infrastructure push, establishing relationships with key decision-makers that would prove invaluable.

What distinguished O.P.'s approach during these formative decades was his insistence on backward integration. While competitors were content to import raw materials and focus on finishing, O.P. methodically built capabilities across the entire value chain. By 1990, Jindal companies owned everything from iron ore mines to specialized finishing units. This integration provided cushion against commodity price volatility and gave them flexibility that pure-play manufacturers lacked.

The late 1980s saw O.P. make his boldest move yet—establishing greenfield plants in industrially backward regions. When he announced plans for a major facility in Odisha, industry watchers were skeptical. The state had minerals but little infrastructure. O.P. saw it differently: Odisha's minerals were the infrastructure. By locating near raw material sources, he could achieve cost advantages that would offset logistical challenges. This insight would later inspire Naveen's massive Angul investment, showing how strategic thinking can span generations.

The Succession Plan & Family Dynamics (2005)

March 31, 2005, began like any other day for the Jindal family. O.P. Jindal, now 75 but still vigorous, boarded his helicopter in Saharanpur for what should have been a routine flight. Accompanying him were his longtime associate Hari Prasad Agarwal and two pilots. The helicopter never reached its destination. When it crashed near Khatima in Uttarakhand, India lost one of its pioneering industrialists, and the Jindal family faced its greatest crisis. But what happened next would become a case study in succession planning done right—a rarity in Indian business families where patriarch deaths often trigger bitter feuds.

Unknown to the public, O.P. had spent the previous two years crafting a detailed succession blueprint. Unlike the Ambani brothers who would spend years in court, or the Birlas whose disputes became public spectacles, the Jindal transition was remarkably smooth. The secret lay in a document O.P. had signed in 2003, dividing his empire among his four sons while he was still alive and commanding absolute authority. Each son received a distinct piece of the empire: Prithviraj got Jindal SAW, Sajjan received JSW, Ratan took Jindal Stainless, and Naveen inherited JSPL.

But the masterstroke was appointing his wife, Savitri Jindal, as the chairperson emeritus of the overarching O.P. Jindal Group. This wasn't mere symbolism. Savitri, who had largely stayed out of business operations, became the family's binding force. Her role was to ensure the brothers supported each other despite running competing businesses—a delicate balance that required maternal authority rather than business acumen. In Indian family business culture, where the mother figure commands unique respect, this arrangement provided stability that no legal document could ensure.

The division itself reflected O.P.'s deep understanding of his sons' personalities and capabilities. Prithviraj, the eldest, steady and methodical, received the pipes and tubes business—mature, stable, requiring operational excellence rather than grand vision. Sajjan, the most ambitious and aggressive, got JSW with its diversification potential. Ratan, technically minded and detail-oriented, took the specialized stainless steel operations. And Naveen, the youngest, most educated (a graduate from the University of Texas at Dallas), and most comfortable with risk, inherited JSPL with its ambitious expansion plans and capital-intensive projects.

What made this succession particularly remarkable was the cross-holding structure O.P. had engineered. While each brother controlled his company, they held small stakes in each other's businesses. This created aligned incentives—when one succeeded, all benefited. More importantly, it made hostile takeovers or family feuds economically irrational. Any brother attempting to undermine another would damage his own wealth. This structure, elegant in its simplicity, would be studied in Indian business schools as the "Jindal Model" of family business succession.

Naveen's inheritance of JSPL was particularly intriguing. Established in 1994, JSPL was the newest and most ambitious of the Jindal companies. O.P. had specifically groomed Naveen for this role, sending him to study in America not just for education but to understand global business practices. Naveen had returned with ideas about technology and scale that seemed fantastical to Indian steel veterans. O.P., rather than dismissing these ideas, had encouraged them, perhaps seeing in his youngest son's ambition an echo of his own youth.

The immediate aftermath of O.P.'s death tested the succession plan. Within days, competitors and corporate raiders began circling, expecting the family to fragment. Investment bankers pitched acquisition proposals, assuming the brothers would want to cash out rather than compete with each other. Instead, the four brothers appeared together at a press conference, standing behind their mother, and announced they would honor their father's vision. Each would grow his company independently but support the others when needed. The market's response was swift—Jindal company stocks, which had crashed on news of O.P.'s death, recovered within weeks.

Savitri Jindal's role evolved beyond just maintaining family harmony. She became one of India's richest women and entered politics, serving multiple terms as a Member of the Legislative Assembly from Haryana. Her political career provided the family businesses with continued access to policy corridors while maintaining the apolitical stance necessary for business operations. This dual approach—business leadership through the sons, political engagement through the mother—proved remarkably effective.

The brothers developed an informal cooperation protocol that went beyond their cross-holdings. They would not compete directly in each other's core markets, shared technical expertise when it didn't compromise competitive advantage, and coordinated on major policy issues affecting the steel industry. When Sajjan's JSW needed specialized stainless steel for a project, Ratan supplied it at favorable terms. When Naveen's JSPL required specific pipes for its power plants, Prithviraj's Jindal SAW got the contract without tender. These arrangements, while raising some corporate governance questions, demonstrated how family businesses could leverage relationships for mutual benefit.

By 2010, five years after O.P.'s death, each brother had grown his inheritance significantly. The combined market value of the four companies had tripled, vindicating O.P.'s succession strategy. Industry observers noted something remarkable: instead of the typical Indian family business pattern where subsequent generations become less entrepreneurial, each Jindal brother seemed more ambitious than their father. Perhaps the greatest tribute to O.P.'s legacy was that his sons didn't just preserve what he built—they transformed it into something he might not have imagined but would certainly have admired.

Naveen Jindal's Vision & The Angul Gamble (2000s-2012)

In 2006, Naveen Jindal stood on a barren stretch of land in Angul, Odisha, surrounded by tribal villages and sal forests, and declared this would become India's largest steel complex. Local journalists who covered the announcement were skeptical—this was one of India's most backward districts, with no rail connectivity, minimal infrastructure, and a history of violent protests against industrialization. When Naveen announced an investment of ₹33,000 crore, making it the largest private sector investment in Odisha's history, even supporters thought he was overreaching. But Naveen saw what others missed: Angul sat atop massive coal reserves, and he had a radical idea about how to use India's poor-quality coal that everyone else considered worthless for steelmaking.

The Angul project represented more than just scale—it was a fundamental bet on technology that didn't yet exist commercially. Traditional steelmaking requires coking coal, which India imports at enormous cost. Indian coal, with ash content often exceeding 40%, was considered useless for steel production. Naveen's vision was to gasify this high-ash coal, converting it to synthesis gas that could then be used to produce Direct Reduced Iron (DRI). If successful, it would transform India's steel economics, turning a disadvantage into competitive advantage.

But first, he had to acquire the land, and this is where the project nearly died. The 3,500 acres Naveen needed were spread across multiple villages, requiring negotiation with thousands of farmers and tribal families. Initially, Naveen tried the traditional approach—government acquisition under eminent domain. This triggered exactly the response he should have expected. By 2011, protests had erupted across the district. The situation deteriorated rapidly, culminating in violent clashes in 2012 that left over 200 people injured. Images of police beating protesters went viral, and suddenly Naveen Jindal became the face of predatory capitalism in activist narratives.

What happened next revealed Naveen's evolution as a leader. Instead of doubling down or retreating, he completely changed approach. He personally began visiting villages, not in convoys with security but often alone or with just one aide. He sat in village squares, listening to concerns, drinking tea from earthen cups, and slowly building trust. The compensation package was restructured to include not just land payment but jobs for family members, infrastructure development for villages, and profit-sharing mechanisms. It took two years, but by 2014, the same villages that had violently protested were celebrating the plant's first production milestone.

The technological challenge was even more daunting than land acquisition. The coal gasification technology Naveen wanted to implement had been tried before—and failed spectacularly. SAIL, India's public sector steel giant, had attempted it in the 1990s and abandoned it as unviable. International technology providers were skeptical. When Naveen approached Siemens and other global engineering firms, they quoted prices that would make the project uneconomical and timelines that stretched beyond a decade. Their message was clear: this was experimental technology with uncertain outcomes.

Naveen's response was audacious—if international firms wouldn't provide the technology at reasonable terms, JSPL would develop it internally. He assembled a team of Indian engineers, many poached from competitors with promises of working on "India's moonshot," and supplemented them with select international experts willing to take the risk. The team spent three years in research and development, building pilot plants, failing repeatedly, and iterating. The breakthrough came when they realized they couldn't simply adapt existing gasification technology—they needed to redesign it specifically for Indian coal's unique characteristics.

The MXCOL (Modified X-Coal) plant that finally emerged was unlike anything in the global steel industry. It could handle coal with up to 45% ash content, converting it to synthesis gas with remarkable efficiency. The engineering was complex—multiple gasifiers working in parallel, sophisticated gas cleaning systems, and integration with the DRI plant that required precision coordination. When the plant produced its first commercial batch in 2012, delegations from China, Korea, and even Germany came to study it. The impossible had been achieved: high-quality steel from India's worst coal.

But technology was only part of Naveen's vision for Angul. He conceived it as an integrated complex where nothing would be wasted. The power plant would use waste heat from steel production. The ash from coal gasification would be converted to cement. Even the slag would be processed into construction materials. This circular economy approach, radical for its time, would later become standard in sustainable manufacturing. By 2012, when the first phase was operational, Angul wasn't just a steel plant—it was an industrial ecosystem.

The financial engineering behind Angul was as innovative as its technology. With Indian banks skeptical and international funding expensive, Naveen structured a complex arrangement involving equipment suppliers' credit, international development finance, and innovative bond structures. He convinced equipment suppliers to take equity stakes, aligning their interests with project success. When traditional project finance proved insufficient, he pioneered infrastructure bonds that retail investors could buy, turning ordinary Indians into stakeholders in industrial development.

The human dimension of Angul often gets overlooked in business analyses. Naveen insisted on hiring locally, even if it meant extensive training programs. JSPL established technical institutes in nearby towns, training tribal youth in industrial skills. The company built hospitals, schools, and roads that served not just employees but entire communities. This wasn't corporate social responsibility as marketing—it was building the ecosystem necessary for a remote industrial complex to thrive. By 2012, Angul employed over 10,000 people directly and supported perhaps 50,000 more indirectly.

As the first molten steel poured from Angul's furnaces in 2012, Naveen had won his first major gamble. But he wasn't celebrating—he was already planning the next phase. The initial capacity of 2 million tonnes per annum was just the beginning. His vision extended to 6 million tonnes, then 12 million, eventually 25 million. Each expansion would incorporate new technology, pushing the boundaries of what was possible. The boy who had returned from Texas with grand ideas had proved they weren't just dreams—they were blueprints for transforming Indian industry.

Innovation at Scale: The Coal Gasification Revolution (2012-2021)

The control room at Angul on a humid August morning in 2015 looked more like NASA mission control than a traditional steel plant. Banks of monitors displayed real-time data from thousands of sensors, algorithms continuously optimized gas flows, and engineers made adjustments with touchscreen precision. At the heart of this operation was the MXCOL plant—four massive gasifiers, each seven stories tall, converting Odisha's high-ash coal into synthesis gas every second of every day. Dr. Rajesh Sharma, JSPL's head of technology, stood before a group of visiting Chinese steel executives and made a statement that would have seemed absurd just five years earlier: "Gentlemen, you're looking at the future of steelmaking, and it was invented in India."

The journey from that first successful batch in 2012 to full-scale operation was anything but smooth. The initial MXCOL plant, while revolutionary, had significant teething problems. The gasifiers would clog with ash, requiring shutdowns every few weeks. The gas cleaning systems, designed for lower ash content, needed constant modification. Most critically, integrating the gasification plant with the Direct Reduced Iron (DRI) facility proved far more complex than anticipated. For every ton of steel produced in 2013, JSPL was spending nearly twice what conventional producers spent.

But Naveen Jindal and his team persisted with an almost obsessive focus on continuous improvement. They instituted a practice unusual in Indian industry—complete transparency about failures. Every problem, every shutdown, every cost overrun was documented and analyzed. Engineers were rewarded not for hiding problems but for identifying and solving them. This culture of radical transparency accelerated learning curves dramatically. By 2014, the interval between shutdowns had extended from weeks to months. By 2015, the plant was achieving availability rates above 90%—remarkable for such novel technology.

The breakthrough innovation wasn't just the gasification technology itself but the entire integrated system JSPL developed around it. Traditional steel plants treat each process—coal handling, iron making, steel making—as separate operations. At Angul, Naveen insisted on complete integration. The synthesis gas from coal gasification didn't just feed the DRI plant; its composition was continuously adjusted based on real-time feedback from the steel quality parameters. This required developing proprietary control systems that could manage complexity beyond what any existing steel plant software could handle.

The numbers tell a remarkable story. The DRI plant at Angul, fed by synthesis gas, achieved a scale unprecedented in global steel industry—2 million tonnes per annum from a single module. To put this in perspective, the largest natural gas-based DRI plants globally produced 1.5 million tonnes. But JSPL wasn't using expensive natural gas; it was using synthesis gas from cheap, high-ash coal that others considered waste. The economic implications were staggering. While competitors importing coking coal faced volatile international prices, JSPL's input costs were stable and predictable.

In 2018, JSPL took the technology to its next evolution with the commissioning of the world's largest blast furnace at Angul—4,554 cubic meters of volume, capable of producing 3 million tonnes of hot metal annually. But this wasn't just about size. The blast furnace was designed to use the same synthesis gas from coal gasification, supplemented with coal injection. This hybrid approach—combining traditional blast furnace technology with innovative gasification—had never been attempted at this scale. Industry experts predicted disaster. Instead, the furnace achieved design capacity within six months, setting new benchmarks for productivity.

The environmental implications of JSPL's innovations often get overlooked in discussions of industrial efficiency. While coal gasification might seem counterintuitive in an era of climate consciousness, the technology actually reduced emissions compared to traditional Indian steel production. The gasification process captured pollutants that would otherwise be released, the synthesis gas burned cleaner than pulverized coal, and the integrated design minimized waste heat. By 2020, Angul's carbon intensity per ton of steel was 20% lower than the Indian industry average—remarkable for a coal-based operation.

The intellectual property JSPL developed became valuable beyond just steel production. The company filed over 100 patents related to coal gasification, gas cleaning, and system integration. International companies began approaching JSPL for technology licenses—a reversal of the traditional flow where Indian companies licensed foreign technology. In 2019, a major Indonesian coal company paid JSPL $50 million for gasification technology rights, marking the first time an Indian steel company had exported core process technology.

But perhaps the most ambitious achievement was the cultural transformation within Indian engineering. JSPL's success at Angul inspired a generation of engineers to believe that India could be a technology creator, not just an adopter. The company's annual technical symposium became a pilgrimage site for engineering students. The "Angul Model"—indigenous technology development, systems integration, continuous improvement—became a case study at IITs. Young engineers who might have gone to software companies instead joined JSPL to work on "real engineering that matters."

By 2021, when Angul achieved its full Phase 1 capacity of 6 million tonnes per annum, it had become more than just a steel plant. It was India's largest single-location steel complex, incorporating technologies that didn't exist a decade earlier. The coal gasification plants were achieving 95% availability. The integrated complex was generating its own power, producing cement from waste, and even capturing CO2 for industrial use. The impossible had not just been achieved—it had been optimized to world-class standards.

The international recognition was unprecedented for an Indian steel company. In 2021, the World Steel Association awarded JSPL its Technology Innovation Award—the first Indian company to receive this honor. Delegations from Brazil, South Africa, and Indonesia—countries with similar high-ash coal challenges—came to study the Angul model. Academic papers analyzing JSPL's gasification technology appeared in journals from MIT to Tokyo Institute of Technology. Naveen Jindal, once dismissed as a dreamer, was invited to speak at the World Economic Forum about "Innovation in Traditional Industries."

The Controversies & Political Entanglements

The registered letter that arrived at JSPL's Delhi headquarters in September 2009 was innocuous-looking, but its contents would trigger one of India's biggest political scandals. The Comptroller and Auditor General (CAG) was questioning the allocation of the Talcher coal field to JSPL—a massive reserve containing 150 crore metric tonnes of coal that was crucial to the Angul plant's economics. What started as a routine audit would snowball into "Coalgate," a scandal that would bring down ministers, trigger Supreme Court interventions, and cast a shadow over Naveen Jindal's reputation that persists to this day.

The Talcher allocation story began in 2005 when JSPL applied for captive coal blocks to feed its proposed Angul plant. The logic was compelling—steel production needed assured coal supply, and captive mining would make the project viable. The Screening Committee, headed by the Coal Secretary, recommended allocation based on JSPL's track record and the Odisha government's support. Everything appeared above board until the CAG began calculating what it called "windfall gains"—the difference between the cost of captive coal and market prices. By this calculation, JSPL's allocation was worth thousands of crores in implied subsidy.

The political dimension exploded when opposition parties discovered that Naveen Jindal was not just an industrialist but also a Member of Parliament from the Congress party. The narrative wrote itself—wealthy industrialist uses political connections to secure valuable natural resources. The fact that Naveen had entered politics in 2004, before the coal allocation, and that the allocation followed established procedures, got lost in the political theater. News channels ran breathless exposés titled "Coal Mines or Gold Mines?" and "The MP-Industrialist Nexus."

The personal toll on Naveen was severe. In Parliament, where he had earned respect for thoughtful interventions on industrial policy, he became a pariah. Opposition members would pointedly walk out when he rose to speak. His advocacy for the right to display the national flag—a cause he had championed for years—was now cynically dismissed as reputation management. The man who had seen public service as complementing business success found himself trapped between two identities, neither fully trusted by the other side.

But Talcher was just one controversy. In 2006, JSPL had secured rights to Bolivia's El Mutún iron ore deposit, one of the world's largest untapped reserves. The deal, signed with Evo Morales's socialist government, promised to transform JSPL into a global player. The company committed to investing $2.3 billion, building a steel plant in Bolivia, and sharing technology with the Latin American nation. It seemed like a coup for Indian industry—until it wasn't. By 2012, the relationship had soured. The Bolivian government accused JSPL of not meeting investment commitments. JSPL countered that Bolivia had failed to provide promised infrastructure and constantly changed terms. The project collapsed in mutual recrimination, with JSPL writing off hundreds of crores in investments.

The El Mutún debacle revealed the challenges Indian companies faced in international expansion. Unlike Chinese firms backed by state power, or Western multinationals with centuries of colonial and post-colonial experience, Indian private companies navigated foreign politics alone. JSPL had assumed business logic would prevail over political considerations—a naive belief in retrospect. The failure became a cautionary tale about the limits of entrepreneurial ambition in geopolitically complex environments.

Back in India, the coal scandal continued to metastasize. In 2014, the Supreme Court delivered a stunning verdict—all coal block allocations since 1993 were illegal. While JSPL's Talcher allocation was eventually upheld on technical grounds, the reputational damage was done. The company had to participate in fresh auctions, paying thousands of crores for resources it thought it already owned. The financial impact was manageable, but the uncertainty had delayed expansion plans and increased capital costs significantly.

The political entanglements weren't limited to coal. In Odisha, JSPL found itself caught in the state's complex tribal politics. Environmental activists accused the company of destroying forests and displacing indigenous communities. While JSPL pointed to its rehabilitation programs and environmental clearances, the narrative of big business versus vulnerable tribals resonated powerfully. International NGOs picked up the cause, leading to embarrassing protests at JSPL's international roadshows. European investors, increasingly sensitive to ESG concerns, began asking uncomfortable questions.

The company's response to these controversies revealed both strengths and weaknesses. On one hand, JSPL's legal team successfully defended against most allegations, winning crucial court battles and maintaining operational continuity. The company's disclosure standards improved, and it began engaging more proactively with civil society. On the other hand, the siege mentality that developed made JSPL insular and defensive. Executives became wary of media, reducing transparency. The company's communications, once open and confident, became legalistic and guarded.

The cost of doing business in India's political economy became starkly apparent. JSPL spent hundreds of crores on legal fees, compliance costs, and regulatory management—resources that could have funded innovation or expansion. More importantly, management attention was diverted from business to firefighting. Naveen Jindal, who should have been focusing on technology and strategy, spent countless hours in court corridors and government offices.

Yet, paradoxically, these controversies also strengthened JSPL in unexpected ways. The constant scrutiny forced the company to develop robust governance systems. The need to defend every decision created exceptional documentation culture. The experience navigating India's investigation agencies and courts built institutional knowledge that became competitive advantage. When competitors faced similar challenges later, JSPL's playbook became the industry template. The company that emerged from these controversies was scarred but also battle-hardened, with a sophistication about political risk that would prove valuable in future ventures.

Modern Era & The Green Steel Pivot (2021-Present)

The announcement came at an unlikely venue—the 2021 United Nations Climate Change Conference in Glasgow. While world leaders debated carbon credits and net-zero targets, Naveen Jindal took the stage at a side event and made a startling commitment: JSPL would produce India's first commercial batch of green steel using hydrogen by 2030. The audience, used to vague corporate sustainability promises, was stunned by the specificity. Here was a company built on coal gasification, whose competitive advantage came from using dirty fuel efficiently, promising to abandon its core technology for an unproven alternative. Either Naveen had lost his mind, or he saw something others didn't.

The strategic logic became clearer in subsequent months. JSPL's leadership had been tracking global steel industry trends and reached an uncomfortable conclusion: coal-based steel production, no matter how efficient, would face escalating carbon taxes, particularly in export markets. The European Union's Carbon Border Adjustment Mechanism, set to be fully implemented by 2026, would impose significant costs on high-carbon steel imports. For JSPL, with ambitions of becoming a global player, continuing with coal-only production was a pathway to obsolescence.

But the green steel pivot wasn't just defensive—it was opportunistic. India had announced the National Hydrogen Mission with ambitious targets for green hydrogen production. Solar power costs in India had plummeted to among the world's lowest. JSPL's Angul complex, with its massive scale and integrated operations, was ideally positioned for hydrogen steel production. The same innovative culture that had cracked coal gasification could potentially solve hydrogen-based steelmaking's challenges.

The technical challenges were formidable. Hydrogen-based steel production existed only in pilot plants globally. The process—using hydrogen instead of carbon to reduce iron ore—was understood theoretically but had never been implemented at commercial scale. The infrastructure requirements were staggering: electrolyzers for hydrogen production, storage systems for a highly volatile gas, and completely redesigned furnaces. The capital investment would match or exceed what JSPL had spent on the entire Angul complex.

JSPL's approach reflected lessons learned from the coal gasification journey. Instead of waiting for perfect technology, the company began with parallel experiments. A pilot hydrogen injection system was installed in one blast furnace, gradually replacing pulverized coal with hydrogen. A small direct reduction plant was modified to use hydrogen-rich gas. Each experiment provided data that informed the next iteration. The company partnered with IIT Bombay and the Indian Institute of Science, creating India's first academic-industry consortium focused on hydrogen metallurgy.

The 2021 expansion announcement—taking Angul from 6 MTPA to 12 MTPA by 2025, then to 25.2 MTPA by 2030—incorporated green steel thinking from the design phase. The new facilities would be "hydrogen-ready," capable of transitioning from coal to hydrogen with minimal modification. This dual-fuel approach hedged technology risk while maintaining expansion momentum. The investment scale was breathtaking—₹1 lakh crore over a decade, making it one of India's largest private sector industrial investments.

The creation of Jindal Steel Odisha Limited (JSOL) as a subsidiary marked a structural innovation. JSOL would house the expansion and green steel initiatives, allowing focused management and potentially separate capital raising. The structure also enabled partnerships that might have been complicated at the parent company level. In 2022, JSOL signed a memorandum with a European green technology firm for hydrogen steel technology transfer—the first such agreement by an Indian steel company.

The market's response to JSPL's green pivot was initially skeptical. Steel analysts questioned the economics, noting that green steel production costs were currently 50% higher than conventional methods. Short-sellers bet against the stock, arguing that JSPL was sacrificing near-term profitability for uncertain long-term gains. But institutional investors, particularly those with ESG mandates, saw it differently. JSPL's bonds, once trading at discounts due to coal exposure, began attracting premium valuations from green funds.

The government's recognition came in 2025 when JSPL was selected for incentives under the Coal Gasification Promotion Scheme—ironically, for the same technology it was planning to eventually replace. This seeming contradiction actually made strategic sense. The coal gasification technology would generate cash flows to fund the hydrogen transition. Moreover, the synthesis gas from coal gasification could be combined with green hydrogen, creating a transitional "blue steel" product with lower carbon intensity than pure coal-based production.

Current financial performance validated the dual-track strategy. In fiscal 2024, JSPL reported revenues of ₹49,765 crore with profits of ₹2,846 crore, demonstrating that green ambitions hadn't compromised operational excellence. The company's EBITDA margins, at 18%, exceeded industry averages despite heavy investment in new technology. The stock price, which had languished during the controversy years, reached all-time highs as investors bet on JSPL's transformation story.

The competitive landscape had also evolved dramatically. Tata Steel, the industry doyen, was pursuing its own green steel initiatives but was constrained by legacy operations. JSW Steel, now run by Naveen's brother Sajjan, had announced similar hydrogen ambitions, creating an ironic situation where brothers competed in sustainability narratives. ArcelorMittal's Indian operations, backed by global resources, posed the most serious challenge. But JSPL's first-mover advantage in indigenous technology development and its proven ability to scale innovations provided confidence.

The human capital transformation paralleled the technological shift. JSPL recruited talent from global steel companies, renewable energy firms, and technology startups. The average age of senior management dropped from 55 to 45 as younger leaders took charge of transformation initiatives. The company established India's first Green Steel Research Center, offering fellowships that attracted PhDs from MIT, Cambridge, and the Max Planck Institute. The same company that had once struggled to attract top talent due to its coal association was now seen as the most exciting place for engineers wanting to solve climate challenges.

Product Portfolio & Market Position

Walk through any major Indian construction site, and you'll likely encounter JSPL steel without knowing it. The massive beams holding up the new terminal at Delhi Airport, the rails carrying Mumbai's suburban trains, the plates armoring military vehicles in Ladakh—JSPL products are ubiquitous yet invisible, the skeleton beneath India's development skin. This invisibility is both JSPL's strength and challenge: while the company has built dominant positions in specialized segments, it lacks the consumer recognition of a Tata Steel or the market visibility of imported steel that often gets specified by brand-conscious architects.

JSPL's product strategy reflects a deliberate choice made in the early 2010s—focus on technically demanding, high-margin products rather than commodity grades where Chinese imports dominate. The crown jewel of this strategy is the rail business. JSPL is one of only two Indian companies (the other being government-owned SAIL) qualified to supply rails to Indian Railways. The qualification process took five years, involving extensive testing, trial runs on actual tracks, and certification of manufacturing processes. But once achieved, it created a near-duopoly in a market consuming over a million tonnes annually.

The rail manufacturing facility at Angul incorporates technology that reads like science fiction. The 120-meter-long rails undergo ultrasonic testing across their entire length, detecting flaws invisible to human inspection. The head-hardening process, using accelerated cooling, creates rails that last 50% longer than conventional ones. When Indian Railways launched its high-speed rail projects, JSPL was the only domestic manufacturer capable of producing rails meeting Japanese specifications. This technical capability translated into pricing power—JSPL's rails command premiums of 15-20% over imported alternatives.

The plate mill tells a different story of market positioning. JSPL produces some of India's widest and thickest plates—up to 5 meters wide and 150mm thick. These aren't just big slabs of steel; they're precisely engineered materials with specific metallurgical properties. The plates for nuclear power plants must maintain strength after decades of radiation exposure. Naval plates must resist corrosion from seawater while maintaining ballistic protection. Boiler plates must withstand extreme pressure and temperature cycles. Each application requires different chemistry, processing, and quality assurance—capabilities that take decades to develop.

The company's position in special grades reveals both opportunity and vulnerability. JSPL is the sole domestic supplier for several critical applications—bulletproof steel for military vehicles, weathering steel for bridges in coastal areas, and high-strength plates for pressure vessels. These monopolistic positions generate exceptional margins but also create dependency risks. When JSPL's plate mill underwent maintenance in 2023, several defense projects faced delays. The government has since pushed for supply source diversification, potentially eroding JSPL's pricing power.

In structural steel, JSPL occupies an interesting middle ground. It's not the largest producer—that distinction belongs to JSW and Tata Steel. But it's often the most profitable, focusing on complex sections and customized solutions. When the new Parliament building required steel that could support massive spans without intermediate columns, JSPL developed a special high-strength grade. When Mumbai's coastal road project needed corrosion-resistant structures, JSPL created a proprietary coating system. This solutions-oriented approach generates margins that commodity producers can't match.

The power and cement businesses, initially developed as adjacencies to steel, have become significant profit contributors. The 3,400 MW power generation capacity, primarily using waste heat and coal gasification byproducts, provides electricity at costs below grid prices. This captive power advantage translates to steel production costs that are ₹2,000-3,000 per tonne lower than competitors buying grid power. The cement business, using slag from steel production, generates nearly ₹1,000 crore in annual revenue with minimal additional investment.

JSPL's global presence, spanning multiple continents, reflects ambitions beyond India. The Australian coal mines provide raw material security. The African operations—in Mozambique, South Africa, and Botswana—offer access to high-grade iron ore. The Indonesian ventures bring coal resources. But international operations have been mixed blessings. While providing resource security, they've also consumed capital that might have generated better returns in India. The Bolivia failure remains a cautionary reminder of international expansion risks.

The market share statistics tell a nuanced story. JSPL is India's third-largest private steel producer with roughly 7% market share—respectable but not dominant. But in specific segments, it's often number one or two. In long rails, it has 45% market share. In heavy plates above 100mm thickness, it commands 35%. In specialized structural sections, it holds 30%. This focused dominance strategy generates returns on capital employed of 15%, well above the industry average of 10-12%.

The customer concentration reveals strategic choices and risks. The top ten customers—including Indian Railways, defense establishments, and major infrastructure companies—account for 40% of revenues. This concentration provides stable demand and pricing power but also creates dependency. When government infrastructure spending slows, as it did during COVID-19, JSPL's revenues decline disproportionately. The company has been diversifying its customer base, but moving away from established relationships proves challenging.

The competitive positioning against the three other major players—Tata Steel, JSW (ironically run by Naveen's brother), and ArcelorMittal—shows distinct strategies. Tata Steel leverages its century-old brand and downstream integration. JSW focuses on scale and cost leadership. ArcelorMittal brings global technology and financial strength. JSPL's differentiation lies in technical capability and innovation—a positioning that works well in specialized segments but may limit mass market potential.

Looking at JSPL's product portfolio evolution reveals a company in transition. The traditional products—rails, plates, structures—remain cash cows. But new products are emerging. The company has started producing steel for electric vehicle batteries, wind turbine towers, and solar panel mounting structures. These green economy products currently contribute less than 5% of revenues but grow at 50% annually. The portfolio transformation mirrors JSPL's broader evolution from a coal-based commodity producer to a technology-driven solutions provider.

Playbook: Business & Investing Lessons

The JSPL story offers a masterclass in turning structural disadvantages into competitive moats—a lesson particularly relevant for emerging market companies. When Naveen Jindal decided to build a steel plant using India's high-ash coal, every consultant and industry expert explained why it would fail. The coal was wrong, the technology didn't exist, the location was remote, and the capital requirements were prohibitive. Yet these very constraints forced innovations that became JSPL's greatest strengths. The lesson isn't just about contrarian thinking—it's about recognizing that in commoditized industries, competitive advantage often comes from solving problems others won't touch.

The power of technological differentiation in commodities deserves special attention. Steel is supposedly the ultimate commodity—Fe is Fe, whether produced in Pittsburgh or Angul. Yet JSPL generates margins significantly above industry averages by making steel differently. The coal gasification technology, initially a desperate workaround for India's poor coal quality, became a proprietary advantage generating hundreds of crores in additional profits annually. For investors, this suggests looking beyond production volumes and market share to understand how companies actually make their products. The most boring industries often hide the most innovative companies.

Family business succession planning, the Indian way, offers lessons extending beyond family enterprises. The Jindal model—dividing the empire while maintaining cross-holdings, appointing a neutral family figurehead, and creating economic incentives against conflict—solved a problem that destroys enormous value in emerging markets. The structure essentially created an internal market where brothers compete yet collaborate, innovate independently yet share resources when logical. Modern corporations attempting to balance divisional autonomy with corporate synergy could learn from this organic solution to organizational design.

Political capital as a business asset—and liability—emerges as a crucial theme. O.P. Jindal's political involvement, and later Naveen's parliamentary role, provided access and influence that accelerated growth. But political entanglement also brought scrutiny, controversies, and reputational damage that persist today. The lesson isn't to avoid politics—in emerging markets, that's impossible—but to manage political relationships with the same rigor as customer relationships. JSPL's experience suggests maintaining multiple political connections, avoiding over-identification with any party, and building institutional rather than personal relationships.

Long-term thinking in capital-intensive industries separates winners from casualties. JSPL's major investments—Angul, coal gasification, now green steel—have payback periods exceeding a decade. In an era of quarterly capitalism, such patience seems anachronistic. Yet this long-term orientation, possibly enabled by family ownership, allowed JSPL to pursue strategies that public market pressure might have killed. The current green steel pivot, requiring massive investment with uncertain returns, would be impossible if JSPL optimized for next quarter's earnings. For investors, this suggests that in capital-intensive industries, ownership structure and time horizon matter more than current financial metrics.

The importance of backward integration in emerging markets reflects infrastructure realities. In developed markets, companies can rely on efficient supply chains and spot markets. In India, JSPL needed to control everything from coal mining to power generation because external dependencies created unacceptable risks. This integration required enormous capital but provided resilience during commodity cycles and supply disruptions. The COVID-19 period validated this approach—while competitors struggled with supply chain disruptions, JSPL's integrated operations continued largely unaffected.

When to bet big on unproven technology remains one of business's hardest questions. JSPL's coal gasification gamble could have destroyed the company. The green steel pivot might still prove premature. Yet both bets reflected a framework: pursue technology that solves fundamental constraints, develop it internally if necessary, and scale aggressively once proven. This approach differs from both conservative incrementalism and Silicon Valley-style disruption. It's about taking calculated risks on technologies that, if successful, create lasting competitive advantages rather than temporary first-mover benefits.

Managing stakeholder complexity—family, government, local communities, investors—requires skills rarely taught in business schools. JSPL simultaneously manages four Jindal family branches with different interests, multiple state governments with changing political leadership, tribal communities with historical grievances, and investors with conflicting time horizons. The company's approach—transparency within the family, regulatory compliance over optimization, community investment beyond CSR requirements, and consistent investor communication—isn't elegant but it works. The lesson is that stakeholder management isn't about optimization but about sustainability.

The value of indigenous innovation capability extends beyond specific technologies. JSPL's ability to develop coal gasification internally created organizational confidence that enables the current green steel push. Engineers who solved "impossible" problems once believe they can do it again. This innovation culture, rare in traditional industries, becomes self-reinforcing. Talented engineers join because interesting problems exist, their solutions create new challenges that attract more talent, and gradually the company's innovation capability becomes its true moat.

Capital allocation in cyclical industries requires countercyclical thinking that's obvious in theory but difficult in practice. JSPL's major expansions occurred during downturns when capital was expensive but assets were cheap. The Angul investment during the 2008-09 financial crisis, the technology development during the 2015-16 steel price collapse, and the current green steel pivot during COVID-19 uncertainty all reflect this pattern. The challenge isn't identifying opportunities but maintaining financial flexibility and organizational courage to act when conventional wisdom counsels caution.

The interplay between business strategy and national development creates opportunities and obligations unique to emerging markets. JSPL's success depended on India's infrastructure growth, but it also contributed to that growth through products, employment, and technology development. This symbiotic relationship—neither pure capitalism nor state direction—might be the most sustainable model for industrial development in democratic emerging markets. For investors, it suggests evaluating companies not just on financial metrics but on alignment with national development priorities.

Analysis & Bear vs. Bull Case

The investment case for JSPL presents a fascinating study in contradictions. Here's a company with world-class technology trading at developing-market multiples, a green steel pioneer built on coal gasification, and a family business with better governance than many professionally managed competitors. The bull and bear cases aren't just about different assumptions—they reflect fundamentally different views on India's industrial future, the pace of energy transition, and the value of technological capability in commodity industries.

The Bull Case rests on five pillars, each compelling individually and potentially transformative collectively. First, the expansion trajectory from 6 MTPA today to 25.2 MTPA by 2030 would make JSPL one of the world's largest single-location steel complexes. This isn't just about scale—concentrated production provides cost advantages through shared infrastructure, logistics optimization, and operational synergies that distributed competitors can't match. If JSPL executes even 70% of planned expansion, the revenue growth would be extraordinary.

Second, the coal gasification technology leadership provides a moat that markets haven't fully valued. While developed markets race toward hydrogen steel, the reality is that coal will remain Asia's primary steelmaking fuel for decades. JSPL's ability to use high-ash coal that others can't process creates a sustainable cost advantage. The technology licensing potential alone—to Indonesia, South Africa, and other countries with similar coal—could generate billions in high-margin revenue. The 2025 government incentive selection validates this technology's strategic value.

Third, the green steel transition positions JSPL for the post-carbon economy. Unlike competitors retrofitting old plants, JSPL is building hydrogen-ready facilities from scratch. The Angul complex's scale makes it ideal for green hydrogen production—renewable energy projects need large, stable customers, exactly what JSPL offers. If green steel commands the premium that analysts project (30-50% above conventional steel), JSPL's early mover advantage could generate extraordinary returns.

Fourth, India's infrastructure spending trajectory supports sustained demand growth. The government's ₹100 lakh crore infrastructure pipeline, the urban development push, and defense modernization all require specialized steel that JSPL produces. Unlike China, where steel demand has peaked, India's per capita steel consumption at 75 kg remains far below the global average of 230 kg, suggesting decades of growth potential.

Fifth, the promoter commitment, evidenced by 62.4% holding despite numerous opportunities to sell down, signals confidence in long-term value creation. The Jindal family's reputation, political connections, and financial resources provide stability that purely professional management might lack. The recent simplification to "Jindal Steel Limited" suggests renewed focus and confidence.

The Bear Case is equally compelling, starting with disappointing historical performance. Five-year revenue growth of 5.59% barely exceeds inflation, suggesting execution challenges or market constraints. The ROE of 10.8% falls well below the 15-20% that quality companies should generate. These numbers suggest that despite technological leadership, JSPL struggles to convert innovation into financial performance—a red flag for investors seeking returns, not just interesting engineering.

The promoter pledge of 39.98% raises serious concerns. Nearly 40% of promoter holdings pledged implies either financial stress or aggressive financial engineering. In a downturn, margin calls could force promoter selling, creating a negative spiral. The pledge also suggests that despite strong operational narratives, the promoters themselves need liquidity—rarely a positive signal.

Commodity cycle vulnerability remains JSPL's Achilles heel. Steel prices move with global economic cycles, and no amount of technology differentiation fully insulates from these swings. The 2015-16 steel crisis saw JSPL's stock lose 80% of value despite its technological advantages. With global recession risks rising and China's property crisis potentially flooding markets with cheap steel, another downcycle seems probable rather than possible.

Environmental regulations and carbon pricing pose existential threats that green steel ambitions might not offset quickly enough. The European Carbon Border Adjustment Mechanism will impose costs that could eliminate export profitability. Domestic carbon taxes, while not immediate, seem inevitable. JSPL's coal-based production, regardless of efficiency, faces structural headwinds that will only intensify. The green transition requires massive capital exactly when carbon taxes will pressure profitability—a challenging combination.

Competition from global giants entering India presents a formidable challenge. ArcelorMittal, the world's second-largest steelmaker, has committed massive investments to Indian capacity. POSCO and Nippon Steel bring superior technology and deep pockets. Chinese producers, despite import duties, find ways to access Indian markets. JSPL's technological edge might prove temporary as global leaders localize production with even better technology.

The execution risk on expansion plans deserves particular scrutiny. Growing from 6 MTPA to 25 MTPA requires everything going right—land acquisition, environmental clearances, technology scaling, market demand, and financing. JSPL's history includes spectacular successes but also notable failures like Bolivia. The probability of flawless execution on such ambitious plans seems low, yet the market valuation appears to assume success.

The family dynamics, while currently stable, introduce governance risks. The cross-holdings between brother's companies create potential conflicts of interest. Savitri Jindal's political career could complicate business operations. The next generation's commitment and capability remain untested. Family businesses often struggle with third-generation transitions, and JSPL's complex structure might amplify these challenges.

Financial leverage remains elevated despite recent deleveraging. The debt-to-equity ratio, while improved, still constrains financial flexibility. Rising interest rates increase debt servicing costs exactly when capital needs for green transition are highest. The company might face choosing between growth investment and balance sheet strengthening—a difficult position in a competitive market.

The technology risk in green steel cannot be ignored. Hydrogen-based steelmaking remains experimental globally. The economics depend on renewable energy costs that might not decline as projected. Alternative technologies like carbon capture or breakthrough battery technologies might obsolete hydrogen steel before JSPL recovers its investment. Betting the company on unproven technology worked once with coal gasification—assuming it works again seems optimistic.

Epilogue & Looking Forward

Standing at the Angul complex in 2025, watching the massive blast furnaces operate while hydrogen electrolyzers are being installed nearby, one witnesses a company—and an industry—in transition. The ₹1 lakh crore that JSPL will invest in Odisha over this decade represents more than capital allocation; it's a bet on India's industrial future and the possibility of sustainable heavy industry. The transformation from family-run enterprise to professional management while maintaining family control, from coal dependency to green ambitions while leveraging coal technology, from domestic focus to global aspirations while deepening local roots—these paradoxes define JSPL's forward trajectory.

The question isn't simply whether Jindal Steel becomes a global champion or remains a domestic leader—it's whether the company can navigate the energy transition while maintaining the innovation culture that enabled its rise. The early indicators are mixed but intriguing. The new generation of Jindal leaders, educated at global universities but grounded in shop floor realities, bring fresh perspectives while respecting institutional knowledge. The R&D spending, now exceeding ₹500 crore annually, suggests continued commitment to technology leadership. The partnerships with international firms indicate openness to external innovation while maintaining core capabilities internally.

Key metrics to watch in coming quarters extend beyond traditional financial indicators. The capacity utilization at Angul, currently around 85%, needs to reach 95% to justify expansion. The debt reduction trajectory, targeting net debt-to-EBITDA below 3x, will determine financial flexibility for green investments. The progress on hydrogen pilots, particularly the percentage of hydrogen successfully substituted in the DRI process, will indicate technical feasibility. The international technology licensing deals, if they materialize at scale, would validate JSPL's innovation premium. The talent retention in critical technical roles, especially in the new Green Steel Research Center, will determine execution capability.

The broader implications of JSPL's journey extend beyond one company's success or failure. If JSPL successfully transitions from coal to green steel while maintaining competitiveness, it provides a template for industrial transformation in emerging markets. If the indigenous technology development model proves sustainable, it challenges assumptions about innovation geography. If the family business structure successfully manages generational transition while scaling operations, it offers lessons for Asian capitalism's evolution. Conversely, if JSPL struggles, it might signal that industrial transformation requires resources and time horizons that even successful emerging market companies can't sustain.

The company that began with O.P. Jindal hammering buckets in Hisar has traveled an extraordinary distance, but the most challenging journey lies ahead. The next five years will determine whether JSPL becomes a case study in successful industrial transformation or a cautionary tale about the limits of ambition in commodity industries. The only certainty is that the story remains unfinished, the engineering challenges unsolved, and the potential—for spectacular success or failure—very real.

Recent Developments at Jindal Steel Signal Strategic Transformation

The company's accelerating transformation from a traditional steelmaker into a technology-driven industrial powerhouse is evident in recent changes. The company officially changed its name from Jindal Steel and Power to Jindal Steel Ltd. on 23 July, 2025, a seemingly minor change that signals a strategic refocusing on its core steel business while shedding the diversification baggage of the past.

The most significant recent development is New Era Cleantech Solution Private Limited, Jindal Steel and Power Limited (JSPL) and Greta Energy Limited are the three companies that have been selected for government incentives under the Coal Gasification Promotion Scheme, with JSPL securing Rs 500 crore. This government validation of JSPL's gasification technology comes at a crucial moment, providing financial support for the company's ambitious expansion plans while acknowledging its technological leadership in converting India's poor-quality coal into valuable industrial products.

The expansion trajectory remains aggressive and on track. JSPL unveiled ambitious plans to inject Rs 1.20 lakh crore for four-fold increase of the capacity of its Angul plant in Odisha to 25.2 MTPA by 2030, creating more than 60,000 direct job opportunities. The intermediate milestone of reaching 12 MTPA by 2025 appears achievable, with the company aiming to expand its current steel-making capacity from 6 million tonnes per annum (MTPA) to 12 MTPA by next year as part of its ongoing Angul facility expansion.

The green steel pivot is gaining momentum beyond rhetoric. JSPL Angul will see an expansion of substantial green steel manufacturing capacity through Hydrogen-based DRI and EAF route. The company's dual-track approach—continuing to optimize coal gasification while preparing for hydrogen—reflects pragmatic planning. The company aims to produce at least 50% of steel capacity through green and environment-friendly technologies, positioning itself for the inevitable carbon-constrained future while maintaining near-term profitability.

Financial performance indicators suggest the strategy is working. Jindal Steel reports FY25 record production, ₹58,044 Cr revenue, ₹2,846 Cr PAT, and AGM on Aug 30, 2025, demonstrating that the technological innovations and expansion investments haven't compromised operational excellence. The market capitalization hovering around ₹100,000 crore reflects investor confidence in the transformation story, though concerns about historical underperformance and promoter pledges persist.

The infrastructure development beyond steel production reveals the scale of JSPL's ambitions. JSPL's Vision 2030 entails substantial investments to develop the iron ore and coal mineral industry and build a world-class logistics infrastructure, including a state-of-the-art Port and a dedicated Railway Line to connect the Port, the Angul facility, the Barbil Pellet Plant and its Raigarh plant in Chhattisgarh. This integrated ecosystem approach transforms JSPL from a steel producer into an industrial infrastructure developer.

The international arbitration setback in Bolivia, while disappointing, appears to be in the rearview mirror. In 2024, the International Court of Arbitration ruled in favor of Bolivia against Jindal Steel Bolivia S.A., dismissing JSB's claims for 100 million dollars compensation. The company seems to have absorbed this loss and refocused on domestic opportunities where it has clearer competitive advantages.

The human capital transformation continues with strategic hiring and skill development initiatives. The company's engagement with educational institutions and its Green Steel Research Center are attracting top talent, crucial for executing the technological transition. The emphasis on local employment and skill development in Odisha demonstrates a sophisticated understanding of the social license needed for massive industrial operations.

Looking ahead, several key milestones will determine JSPL's trajectory. The successful commissioning of the 12 MTPA capacity by 2025 will validate execution capabilities. The pilot hydrogen steel production promised by 2030 will test technological prowess. The ability to maintain margins while investing heavily in green technology will determine financial sustainability. And the navigation of India's evolving environmental regulations will test adaptability.

Links & Resources

Company Resources: - Official Website: www.jindalsteel.com - Investor Relations: BSE: 533719, NSE: JINDALSTEL - Annual Reports: Available on company website and stock exchange filings

Industry Analysis: - World Steel Association: Technology Innovation Awards and industry statistics - India Brand Equity Foundation: Indian steel industry reports - Ministry of Steel, Government of India: Policy documents and industry data

Technology Resources: - Coal Gasification Technology papers from IIT Bombay - Green Steel initiatives: National Hydrogen Mission documentation - MXCOL Technology: Technical specifications available through JSPL

Historical Context: - O.P. Jindal Group history and family business structure - Angul Steel Plant development timeline - Coal allocation controversy: CAG reports and Supreme Court judgments

Sustainability & ESG: - JSPL Sustainability Reports (FY 2024-25) - Carbon footprint reduction initiatives - Community development programs in Odisha

Investment Research: - Stock performance: NSE/BSE historical data - Analyst reports from major brokerages - Credit ratings from CARE, CRISIL

News Sources: - Business Standard, Economic Times for regular updates - Steel industry publications like SteelOrbis - Local Odisha media for plant-specific developments

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube