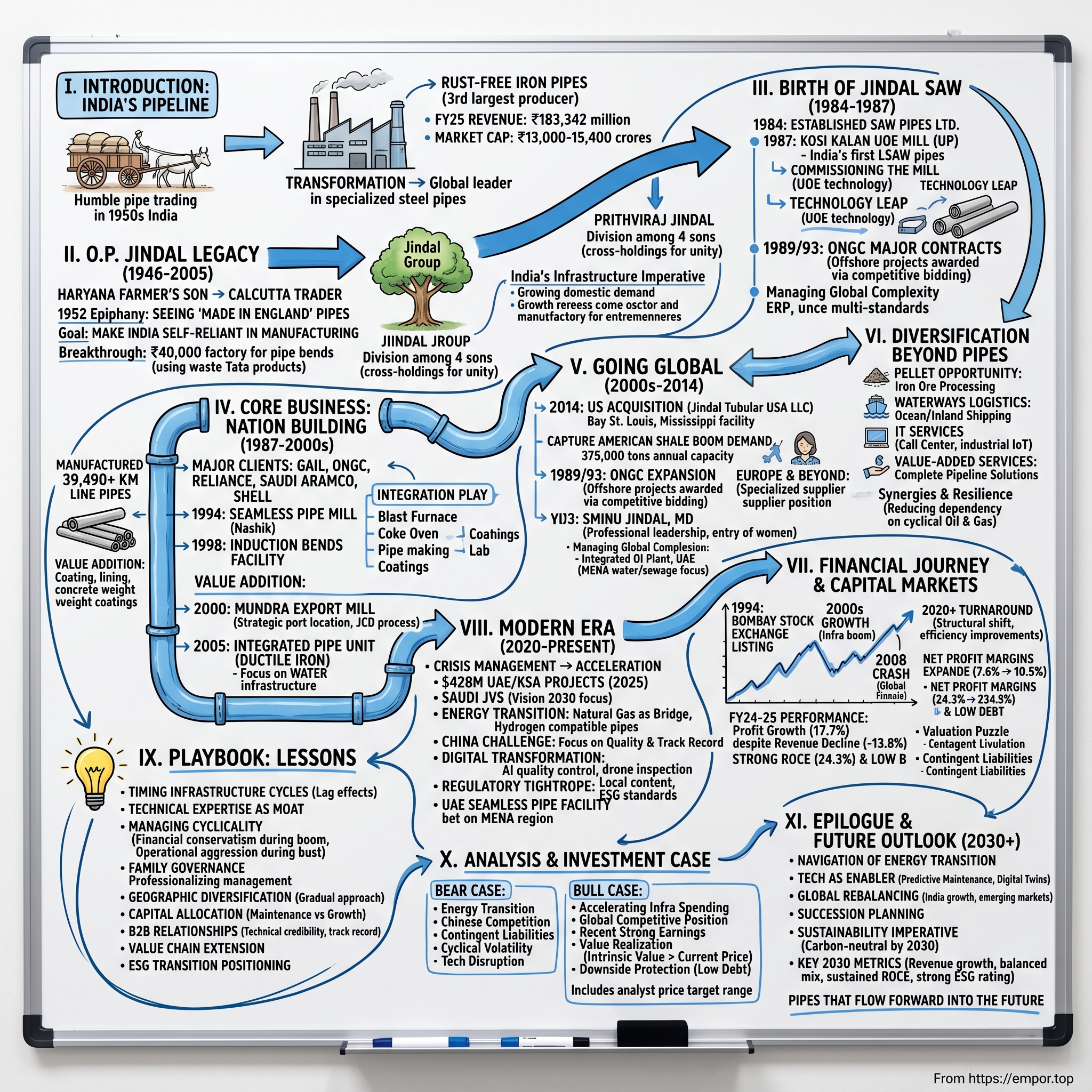

Jindal SAW: India's Pipeline to Global Energy Infrastructure

I. Introduction & Episode Roadmap

Picture this: A young trader in 1950s India, hauling surplus pipes from the oil fields of Assam on bullock carts, selling them to whoever needs them. Fast forward seven decades—his son's company manufactures specialized steel pipes that carry oil across the Arabian desert, gas through American shale fields, and water to millions of Indian homes. This is the story of Jindal SAW, a company that transformed from a single pipe mill in rural Uttar Pradesh to become the world's third-largest producer of rust-free iron pipes. Today, Jindal SAW commands a market capitalization of approximately ₹13,000-15,400 crores, with revenues of ₹183,342 million in FY25—a testament to how far a pipe trader's dream can travel. But this isn't just another industrial success story. It's a narrative about timing infrastructure cycles, navigating family business dynamics, and building global manufacturing capabilities from an emerging market base.

What makes Jindal SAW particularly fascinating for investors today? The company sits at the intersection of several macro themes: global energy infrastructure spending, the Middle East's diversification away from oil dependence, India's manufacturing ambitions, and the complex transition from fossil fuels to renewable energy. As the world's third-largest producer of rust-free iron pipes and a global leader in the coated and bare pipe industry, Jindal SAW offers a lens into how traditional industrial companies adapt, evolve, and position themselves for the future.

Over the next several hours, we'll trace this journey from its origins in post-independence India through its current global footprint spanning manufacturing facilities in India, the United States, and the UAE. We'll examine the strategic decisions, market timing, and occasional missteps that shaped the company. Most importantly, we'll assess what this means for investors evaluating Jindal SAW today—a company that has delivered 17.7% net profit growth in FY25 despite revenues declining 13.8% year-over-year, suggesting interesting dynamics at play beneath the surface.

II. The O.P. Jindal Legacy & Industrial Context

The year was 1946. A sixteen-year-old Om Prakash Jindal boarded a train from rural Haryana to Calcutta, carrying little more than dreams and determination. The son of a farmer from Nalwa village in Hisar district, young Jindal had been sent east along with his brothers to escape the irregular monsoons and constant land disputes that plagued their homeland. Born on August 7, 1930, to a farmer family in Nalwa, Haryana, his parents sent him to Calcutta due to irregular monsoon patterns and constant disputes over land ownership, as Eastern India was a hub of commerce at the time.

In the bustling streets of post-war Calcutta, Jindal discovered something that would change his life—and eventually India's industrial landscape. At 20, he began his entrepreneurial journey by moving to Calcutta, where he worked as a trader dealing in steel pipes and tubes. He traded in iron and transported surplus pipes from Assam to sell in Calcutta, much of which came from metal left behind by the United States Army Air Forces' Tenth Air Force after World War II. The young trader would haul these surplus pipes on bullock carts, selling them to whoever needed them—a humble beginning that would spawn an industrial empire.

But it was a moment of epiphany in 1952 that truly set the course. In 1952, driven by a pivotal realization upon seeing imported "Made in England" pipes in Calcutta, he resolved to make India self-reliant in manufacturing. His breakthrough came when he was struck by the sight of "Made in England" stamped on pipes he saw in Calcutta. This pivotal moment ignited his desire to make India self-reliant in manufacturing. At just 22 years old, with an investment of ₹40,000 (half of it borrowed), he set up a factory in Liluah in Howrah to make pipe bends and sockets by using waste pipe products from Tata's Jamshedpur factory and Kalinga Tubes' Cuttack factory. What started as a pipe-bending unit became the foundation of an industrial empire. By the age of 22 in 1952, he set up a factory in Liluah in Howrah to make pipe bends and sockets by using waste pipe products from Tata's Jamshedpur factory and Kalinga Tubes' Cuttack factory. In 1964, he expanded his ventures by founding Jindal India Limited, a full-fledged pipe-production company.

The growth trajectory was remarkable. He went on to establish Jindal Steel and Power, JSW Group and Jindal Stainless Limited under the flagship of the OP Jindal Group, of which he was the founding chairman. By 2004, According to the 2004 Forbes List, he was ranked 13th amongst the richest Indians and 548th amongst the richest persons in the world. The Jindal Group had grown from a single factory to a sprawling conglomerate drawing annual revenue of $25 billion today.

The Family Architecture of Growth

What makes the Jindal story particularly intriguing for business historians is the unique structure O.P. Jindal put in place before his tragic death in a helicopter crash on March 31, 2005. Before his death in a helicopter crash in 2005, Jindal divided his businesses among his four sons - Prithviraj Jindal, Sajjan Jindal, Ratan Jindal and Naveen Jindal, structuring it with cross-holdings to ensure mutual benefit and shared growth. To maintain family unity, his wife, Savitri Jindal, was appointed chairperson of the OP Jindal Group and its companies.

This wasn't a simple split like the Ambani brothers or the multi-generational divisions of the Birlas. The Jindals created something more sophisticated—a structure where each brother having the largest holding in the part of the pie he manages, with the other three having smaller but proportionate stakes in the empires of the other brothers. As Sajjan Jindal explained at the time: "We are one family, we share a good equation and support each other. Each one is an owner in each other's industry."

The division of labor was clear: Prithviraj Jindal leads Jindal SAW Ltd., Sajjan Jindal helms JSW Ltd., Ratan Jindal is at the forefront of Jindal Stainless Ltd., and Naveen Jindal guides Jindal Steel & Power Ltd. Each brother carved out his domain while maintaining equity stakes in the others' companies—a structure that theoretically aligned interests while allowing operational independence.

India's Infrastructure Imperative

To understand why Jindal SAW would emerge as the crown jewel of Prithviraj Jindal's inheritance, we must understand India in the 1980s. The country was awakening from decades of socialist planning, beginning to liberalize its economy, and desperately needed infrastructure. Oil and gas discoveries in the Krishna-Godavari basin, the expansion of refineries, and ambitious water supply projects all required one critical component: high-quality steel pipes.

India's pipe manufacturing industry at the time was dominated by imports and small-scale producers making basic products. The technology for manufacturing large-diameter pipes suitable for high-pressure oil and gas transmission simply didn't exist domestically. Every major pipeline project meant expensive imports, delayed schedules, and dependence on foreign suppliers who often prioritized their home markets.

This was the opportunity Prithviraj Jindal recognized when he established SAW Pipes Limited in 1984—not just to make pipes, but to bring world-class pipe manufacturing technology to India and position the country as a global player in this critical infrastructure component.

III. The Birth of Jindal SAW (1984–1987)

The rain was falling in sheets across the plains of Uttar Pradesh in the summer of 1987. In the small town of Kosi Kalan, about 80 kilometers from Delhi, engineers and workers were rushing to complete final preparations at what would become India's first large-diameter pipe manufacturing facility. This wasn't just another industrial project—it was the realization of Prithviraj Jindal's vision to transform India from a pipe importer to a pipe exporter.

The first SAW Pipe mill (UOE) was commissioned in the year 1987 in Kosi Kalan, Uttar Pradesh. With the opening of this mill, Jindal SAW Ltd. became the first Pipe mill to produce LSAW Pipes in India. The choice of location seemed counterintuitive—located about 1200 Kms from nearest west coast port of India—but it placed the facility at the heart of India's industrial corridor, close to refineries, power plants, and the growing industrial base of northern India.

The Technology Leap

What made this facility revolutionary wasn't just its existence, but the technology it employed. The UOE process—where steel plates are formed into pipes through a sequence of U-ing, O-ing, and Expanding—was the gold standard for manufacturing large-diameter pipes suitable for high-pressure oil and gas transmission. It started operation in the year 1984, when it became the first company in India to manufacture Submerged Arc Welded (SAW) Pipes using the internationally acclaimed U-O-E technology.

The technology acquisition wasn't straightforward. International suppliers were hesitant to share advanced manufacturing techniques with Indian companies, fearing competition. Prithviraj Jindal had to navigate complex negotiations, technology transfer agreements, and convince skeptical foreign partners that India could master this sophisticated manufacturing process. The initial capacity was modest—250,000 metric tons per annum—but it represented a quantum leap for India's pipe manufacturing capabilities.

Early Wins and Market Building

The timing proved fortuitous. First order for ONGC casing Pipe Completed in 1989. API Line Pipe production commences. In 1992/93, 3 major offshore projects awarded by ONGC under international competitive bidding. Italian and Japanese being L2 and L3 bidders. This early victory against established international competitors sent shockwaves through the industry. An Indian company, operating from a facility in rural Uttar Pradesh, had beaten Italian and Japanese bidders on both price and technical specifications.

The ONGC contracts were more than just commercial wins—they were validation. If India's national oil company trusted Jindal SAW for critical offshore projects where pipe failure could mean environmental disaster and massive financial losses, other buyers would follow. And they did.

Building the Management Team

Behind the technology and contracts was a carefully assembled team. Prithviraj Jindal pioneered the production of SAW Pipes in India. He was associated in the setting up of SAW Pipes Limited, (now known as Jindal SAW Ltd.) in 1984 with its first state of-the-art plant in Kosi Kalan in UP. But he didn't work alone.

A pivotal figure emerged in Sminu Jindal, who would later become Managing Director. Sminu Jindal is the first lady entrant in the country to do her gender proud by breaking the glass ceiling in the Steel, Oil and Gas sector in India. Having been appointed as the Managing Director of Jindal SAW Ltd. a part of the fourth largest industrial house in India the OP Jindal Group, Sminu Jindal's contribution to the growth of the organization has been phenomenal. Her entry into what was then an entirely male-dominated industry signaled both the family's commitment to professional management and a progressive approach unusual for Indian family businesses of that era.

The early years weren't without challenges. Training workers to operate sophisticated European machinery, maintaining quality standards that met international specifications, managing working capital for large contracts with extended payment terms—each presented its own complexities. The company had to build not just manufacturing capabilities but an entire ecosystem: testing laboratories, quality certification processes, logistics networks for transporting massive pipes, and relationships with raw material suppliers.

What distinguished Jindal SAW in these formative years was its refusal to be merely an import substitution play. From the beginning, the vision was global. The company sought and obtained API (American Petroleum Institute) certification, enabling it to compete for international contracts. It invested in research and development, not just to meet specifications but to innovate—developing new coating technologies, improving welding techniques, and optimizing designs for Indian conditions.

By 1990, just three years after commissioning its first mill, Jindal SAW had established itself as India's undisputed leader in large-diameter pipes. But this was just the beginning. The real test would come in scaling up, diversifying the product portfolio, and taking on global giants in their home markets.

IV. Building the Core Business: Pipes for Nation Building (1987–2000s)

The late 1990s marked a pivotal moment in India's energy infrastructure. In conference rooms across New Delhi, officials from GAIL (Gas Authority of India Limited) were grappling with an ambitious challenge: how to build a national gas grid that would connect India's gas fields to its industrial heartland. The answer would come from an unlikely source—a pipe manufacturer operating from rural Uttar Pradesh that had barely been in business for a decade.

Jindal SAW Ltd. has manufactured and supplied more than 39,490 kms of Line pipes & exported in excess of 17,707 Kms of Line pipes for on-shore and off-shore pipeline projects across the world. This division is the market leader in its segment in India and has supplied pipes for major pipeline projects in the Middle East, North America, Latin America, Africa, Europe, Australia, CIS and Asia.

The Client Portfolio That Mattered

Some key domestic clients include Indian Oil Co. Ltd, Oil & Natural Gas Co. Ltd, Gas Authority of India Ltd, Reliance Petroleum Ltd. Major international clients include AGIP Oil Company (Libya), Bechtel Intec Consortium (UK), China National Petroleum Company, Qatar Petroleum, Saudi Arabian Oil Co., Shell Petroleum. This wasn't just a client list—it was a validation of Jindal SAW's transformation from a domestic player to a global supplier trusted by the world's energy giants.

The journey to building this client base wasn't straightforward. Each client had unique specifications, stringent quality requirements, and zero tolerance for failure. When Saudi Aramco first evaluated Jindal SAW as a potential supplier in the mid-1990s, their inspection team spent weeks at the Kosi Kalan facility, testing everything from welding procedures to coating adhesion. The stakes were enormous—a single pipe failure in a Saudi desert pipeline could cost millions in lost production and environmental damage.

Technology Evolution and Product Expansion

By 1994, recognizing that large-diameter pipes alone wouldn't sustain growth, the company commissioned a Seamless Pipe Mill in Nashik. This strategic diversification addressed a different market segment—high-pressure applications in refineries, power plants, and specialized industrial uses where seamless construction was essential.

A modern Hot Pulled Induction Bends facility of size range from 4" OD to 48" OD was set up within the Kosi Kalan complex in the year 1998. In order to cater to the export market, another facility for induction bends at Samaghogha was installed having size range from 6" OD to 56" OD. Over 12,000 bends have been manufactured by Jindal SAW. These weren't just manufacturing additions—they represented a shift from being a pipe supplier to becoming a complete pipeline solutions provider.

The late 1990s also saw Jindal SAW master the art of value addition. Pipes were no longer just steel tubes; they became sophisticated engineered products with specialized coatings for corrosion resistance, concrete weight coatings for submarine pipelines, and internal linings for specific chemical applications. Each innovation opened new markets and commanded premium pricing.

The Mundra Gambit

The year 2000 marked another strategic inflection point. Commissioning of 2nd LSAW pipe manufacturing facility as 100% export oriented unit using JCO forming process at Nanakapaya, Mundra to meet export market with capacity of 300,000 metric tons per annum. The choice of Mundra—then a small port in Gujarat—seemed puzzling. But Prithviraj Jindal had seen what others hadn't: Mundra would become India's largest private port, and positioning a manufacturing facility there would provide unmatched logistics advantages for exports.

The Mundra facility wasn't just about location; it introduced the JCO forming process, allowing manufacture of larger diameter pipes with thicker walls—exactly what international markets demanded for deepwater offshore projects. This technological capability would prove crucial when competing for projects in the North Sea, Gulf of Mexico, and Brazilian pre-salt fields.

Water: The Unexpected Growth Driver

While oil and gas grabbed headlines, a quieter revolution was happening in India's water infrastructure. During the year 2005, the company had start up an Integrated Pipe Unit Ductile Iron Pipe manufacturing plant of 200,000 MT per annum capacity along with Blast Furnace of 250,000 MT per annum capacity and a Coke Oven Plant. The move into ductile iron pipes wasn't glamorous, but it addressed India's massive water infrastructure deficit.

Cities across India were replacing century-old water distribution systems. Rural water supply schemes under government programs needed millions of meters of pipes. Unlike oil and gas projects that came in large but irregular contracts, water projects provided steady, predictable demand. The margins were lower, but the volumes were enormous and the payment risks minimal when dealing with government contracts.

The Integration Play

What distinguished Jindal SAW during this period wasn't just capacity expansion but vertical integration. The company didn't just make pipes; it controlled the entire value chain. The blast furnace and coke oven plant meant control over raw material quality and costs. In-house coating facilities eliminated dependence on third parties. Testing laboratories accredited by National Accreditation Board for testing & Calibration Laboratories (NABL) meant faster turnaround times and quality assurance.

This integration strategy had profound implications. When steel prices spiked in 2003-2004, Jindal SAW's margins remained protected. When customers needed urgent deliveries, the company could prioritize production without negotiating with suppliers. When new specifications emerged, R&D could work directly with production to develop solutions.

Building Institutional Capabilities

Behind the capacity expansions and client wins was a less visible but equally important transformation: the building of institutional capabilities. During the year 2004-05, the company had created four separate strategic business units (SBU) to improve and maximize the operational efficiency. Each SBU operated with its own P&L responsibility, sales teams, and operational metrics.

This organizational innovation solved a critical challenge: how to maintain entrepreneurial agility while scaling up. The SAW pipes division could focus on large-diameter pipes for oil and gas without being distracted by the very different requirements of the seamless tubes business. The ductile iron division could optimize for high-volume, price-sensitive government contracts without compromising the premium positioning of specialized industrial products.

The company also invested heavily in human capital. Engineers were sent to installations worldwide to understand how pipes performed in actual conditions. Sales teams included technical specialists who could engage in detailed discussions with client engineering teams. Quality control wasn't just about meeting specifications but understanding the physics of pipe failure and preventing it.

By the mid-2000s, Jindal SAW had transformed from a single-product, single-location manufacturer to a diversified pipe solutions provider with multiple technologies, products, and markets. The foundation was set for the next phase: global expansion.

V. Geographic Expansion & Going Global (2000s–2014)

The boardroom at Jindal SAW's Delhi headquarters was tense in early 2014. Oil prices were soaring above $100 per barrel, and the American shale revolution was transforming global energy markets. But for Prithviraj Jindal and his team, watching from 8,000 miles away, the boom meant frustration. Every major pipeline project in Texas, North Dakota, and Pennsylvania represented an opportunity they couldn't capture. The solution would come from an unexpected source: a distressed asset sale in Mississippi.

Jindal Tubular USA LLC, a SPV subsidiary of Jindal SAW, announced the acquisition of the assets of PSL North America LLC (PSLNA) for US$104 million in August 2014. Jindal Tubular USA, LLC was incorporated in May 2014 and acquired the assets of a Pipe Mill in August 2014. This facility, spread over 155 acres, manufactures Helical Seam (Spiral) SAW Pipes with anti-corrosion coating to API, ASTM, CSA, NACE & AWWA specifications.

The American Beachhead

The acquisition wasn't just about buying a pipe mill—it was about establishing credibility in the world's most sophisticated energy market. Jindal Tubular USA, LLC is strategically located in Bay St. Louis, Mississippi and has the logistical capability of shipments by barge, rail and truck. The pipe manufacturing and coating facilities are in Hancock County in the Port Bienville Industrial Park, situated on the Mississippi Gulf Coast.

What made this facility special wasn't immediately obvious. PSL North America had filed for bankruptcy, overwhelmed by debt and unable to compete effectively during the shale boom. But Jindal SAW saw what others missed: state-of-the-art helical submerged arc welding technology capable of producing pipe with diameters up to 120" and lengths up to 80'. The facility has the capacity to produce 375,000 tons of pipe per year. Over the last five years, the Company has produced over 500 miles of pipe for a diverse group of customers that includes Inergy, Spectra, Sunoco and Williams.

The timing was critical. American pipeline companies were racing to build infrastructure to transport shale gas from production fields to export terminals. The demand for large-diameter pipes was unprecedented, but domestic suppliers couldn't keep up. An Indian company with American manufacturing capabilities and global supply chain expertise was perfectly positioned.

Building Credibility in a Skeptical Market

Breaking into the American market as an Indian company wasn't straightforward. Pipeline operators, particularly in Texas and Louisiana, had deep relationships with established suppliers. Safety standards were stringent, and any pipe failure could result in catastrophic environmental damage and lawsuits. The "Buy American" sentiment was strong, especially for critical infrastructure.

Jindal's approach was methodical. Vikas has been managing Jindal Tubular USA LLC since the acquisition of the pipe mill in 2014. Rather than positioning as an Indian company with American operations, Jindal Tubular presented itself as an American manufacturer with global backing. Local hiring was prioritized—from welders to senior management. April Schatte has four decades of experience in the pipe industry, shepherding major pipeline projects in the USA and across the globe. She joined Jindal Tubular USA LLC as Senior Vice President of Sales and Marketing in 2017.

The company didn't just meet American standards; it exceeded them. Jindal is certified to ISO 9001 and API Q1 Quality Systems and is fully certified to apply the API Monogram to our pipe. Every aspect of operations—from safety protocols to environmental compliance—was designed to match or surpass the best American manufacturers.

The Middle East Expansion

While the American acquisition grabbed headlines, Jindal SAW's expansion into the Middle East was equally strategic but followed a different playbook. Rather than acquisitions, the company leveraged India's diplomatic relationships and cost advantages to win massive contracts in a region undergoing its own energy infrastructure boom. The Middle East presented a different opportunity. Commissioning of 300,000 M.T.per annum Ductile Iron Pipe Facility in Abu Dhabi, UAE represented Jindal SAW's recognition of the region's massive water infrastructure needs. It is the first largest state-of-the-art integrated plant in Middle East producing large size Ductile Iron Pipes of various sizes and focuses on providing high quality techno-economic products and solutions for water transportation and sewage systems in the wider MENA region.

The UAE and Saudi Arabia were investing hundreds of billions in economic diversification, building new cities, industrial zones, and tourism infrastructure. All needed water—in a desert. The technical challenges were immense: pipes had to withstand extreme temperature variations, high salinity, and aggressive soil conditions. Jindal SAW's ability to customize products for these conditions, combined with geographic proximity from India, created a compelling value proposition.

The European Footprint

Less publicized but equally strategic was Jindal SAW's expansion into Europe through partnerships and technical collaborations. The company didn't try to compete head-on with established European manufacturers. Instead, it positioned itself as a specialized supplier for projects that required unique specifications or rapid delivery times that European manufacturers, with their high cost structures and rigid production schedules, couldn't match.

Managing Global Complexity

By 2014, Jindal SAW was operating manufacturing facilities across four continents, serving clients in dozens of countries, managing multiple currencies, and navigating complex regulatory environments. The operational complexity was staggering. A pipe manufactured in India might use steel from Korea, be coated in the UAE, and installed in Nigeria by an Italian contractor for an American oil company.

This global footprint required sophisticated systems. The company invested heavily in ERP systems that could track inventory across locations, manage multi-currency transactions, and ensure compliance with varying international standards. Quality control became even more critical—a defect in a pipe manufactured in Mississippi but installed in the North Sea could destroy the company's global reputation overnight.

The Power of Relationships

What enabled Jindal SAW's global expansion wasn't just manufacturing capability or financial resources—it was relationships. In the Middle East, Indian diplomatic ties and the large Indian expatriate community provided initial introductions. In America, hiring respected industry veterans opened doors. In Europe, technical partnerships with specialized coating companies created mutual dependencies.

The company also benefited from India's unique position in global geopolitics. As a non-aligned nation with good relationships across both Western and Eastern blocs, Indian companies could operate in markets where American or Chinese companies faced restrictions. Jindal SAW could supply pipes to Iran when Western companies couldn't, and to America when Chinese companies faced tariffs.

Learning from Setbacks

Not every expansion succeeded. An attempted joint venture in Russia fell apart due to governance issues. A facility in Italy, acquired to serve the European market, struggled with high labor costs and regulatory compliance. These failures taught valuable lessons about the importance of cultural understanding, the limits of control in joint ventures, and the need for flexible business models in different markets.

The global expansion phase transformed Jindal SAW from an Indian company with export capabilities to a truly global manufacturer. By 2014, international operations contributed over 30% of revenues, provided natural hedging against currency fluctuations, and most importantly, established the company as a credible global player capable of executing complex projects anywhere in the world.

VI. Diversification Beyond Pipes

The year 2008 brought the global financial crisis, and with it, a harsh reminder of the volatility in the pipe business. Oil prices crashed from $147 to $32 per barrel, pipeline projects were cancelled or postponed, and Jindal SAW's order book shrank dramatically. In the boardroom, difficult questions were being asked: How could the company reduce its dependence on the cyclical oil and gas sector? The answer would reshape Jindal SAW from a pipe manufacturer to a diversified industrial conglomerate.

The Pellet Opportunity

The first major diversification came from an unexpected source: iron ore pellets. India's iron ore mining boom had created a problem—huge quantities of iron ore fines (powder) that couldn't be directly used in steel making. These fines needed to be agglomerated into pellets, creating a massive market opportunity.

Jindal SAW's entry into pellets wasn't random. The company already operated blast furnaces for its ductile iron pipe operations, giving it deep understanding of iron ore processing. The investment in pellet plants leveraged this expertise while providing a natural hedge—when steel demand was low (and hence pipe demand), pellet margins often improved as steel makers sought efficiency improvements.

The pellet business also provided strategic advantages. It gave Jindal SAW direct relationships with steel producers who were also customers for pipes. It provided steady cash flows that were less project-dependent than pipes. Most importantly, it demonstrated to investors that the company could successfully diversify beyond its core business.

Waterways Logistics: The Unexpected Venture

The company's segments include Iron & Steel, Waterways Logistics and Others. The Waterways Logistics segment consists of inland and ocean-going shipping business. This seemed like an odd diversification for a pipe manufacturer, but the logic was compelling. Jindal SAW was already one of the largest importers of steel and exporters of pipes in India, spending millions on freight. Owning ships provided cost advantages and operational flexibility.

More strategically, the shipping business provided intelligence. Freight rates, shipping routes, and cargo volumes offered early indicators of global economic trends, infrastructure development, and commodity flows. This information advantage helped Jindal SAW anticipate market movements and position inventory accordingly.

The IT Services Surprise

The Others segment includes call center and information technology services. This was perhaps the most unexpected diversification. Why would a pipe manufacturer enter IT services? The answer lay in Jindal SAW's own digital transformation. As the company implemented sophisticated ERP systems, developed custom software for pipe design and project management, and built digital interfaces with customers, it developed significant IT capabilities.

Rather than keeping these capabilities entirely in-house, Jindal SAW spun off IT services as a separate business serving external clients. The unit focused on engineering software, supply chain solutions, and industrial IoT applications—areas where domain knowledge from the pipe business provided competitive advantages.

Value-Added Services: Moving Up the Value Chain

The most successful diversification strategy involved moving up the value chain within the pipe ecosystem. Hot Pulled Induction Bends facility, Connector Casings, and specialized Anti-Corrosion Coatings transformed Jindal SAW from a pipe supplier to a solutions provider.

Consider a typical offshore oil platform project. Previously, Jindal SAW would supply pipes, which would then be sent to different vendors for coating, bending, and connection. Each step added time, cost, and quality risk. By offering all these services, Jindal SAW could provide a complete package, reducing project complexity for clients and capturing significantly higher margins.

The coating business became particularly strategic. Advanced coatings could extend pipe life from 20 to 50 years, crucial for deep-water projects where replacement was impossibly expensive. Jindal SAW invested in research partnerships with chemical companies, developing proprietary coating formulations for specific environments—Arctic permafrost, Middle Eastern deserts, deep-sea conditions. These specialized coatings commanded premium prices and created customer lock-in.

Managing Portfolio Complexity

By 2015, Jindal SAW was no longer just a pipe company. It was a diversified industrial conglomerate with businesses ranging from shipping to software. Managing this complexity required organizational innovation. Each business operated as an independent unit with its own P&L responsibility, but shared services like finance, HR, and IT created synergies.

The diversification strategy also required different capital allocation approaches. The pipe business was capital-intensive but generated strong cash flows during boom periods. The pellet business required steady investment but provided stable returns. IT services needed minimal capital but human resource investments. Shipping was highly capital-intensive with volatile returns. Balancing these different business models required sophisticated financial management.

The Synergy Question

Critics questioned whether these diverse businesses truly created synergies or were simply an unfocused conglomerate. The company's response was to emphasize industrial logic rather than financial engineering. The pellet business provided raw material intelligence useful for pipe manufacturing. Shipping provided logistics capabilities and market intelligence. IT services digitized operations across all businesses. Value-added services increased wallet share with existing pipe customers.

Perhaps more importantly, diversification provided resilience. When oil prices crashed in 2014-2016, the pipe business suffered, but pellet demand remained strong as Indian steel production grew. When shipping rates collapsed during COVID-19, the IT services business boomed as companies accelerated digitization. This portfolio approach smoothed earnings volatility and reduced dependence on any single sector.

The diversification beyond pipes transformed Jindal SAW's risk profile and growth trajectory. While pipes remained the core business contributing the majority of revenues, the additional businesses provided stability, growth options, and strategic advantages that pure-play pipe manufacturers lacked.

VII. Financial Journey & Capital Markets Story

The trading floor at the Bombay Stock Exchange was buzzing with activity on November 3, 1994. After a decade of building its business through internal accruals and debt, Jindal SAW was finally going public. Listing date: 03 Nov, 1994. The IPO represented more than just capital raising—it was a coming-of-age moment for the company and a test of whether public markets would value an industrial manufacturer from India's hinterland.

The initial years as a public company were challenging. The mid-1990s saw multiple boom-bust cycles in Indian markets, currency crises, and volatile commodity prices. Jindal SAW's stock price reflected this volatility, often trading at single-digit P/E multiples despite strong operational performance. The market's skepticism toward capital-intensive manufacturing businesses and preference for software and consumer stocks meant Jindal SAW remained under-followed and undervalued.

The 2000s: Building Credibility

The transformation began in the early 2000s as India's infrastructure boom gained momentum. Jindal SAW's revenues grew from ₹117,832 million in FY20 to ₹183,783 million in FY24. Over the past 5 years, the revenue of JINDAL SAW has grown at a CAGR of 11.8%. More importantly, the company began demonstrating consistent execution, delivering projects on time and meeting earnings guidance.

The 2003-2008 commodity super-cycle proved transformative. Steel prices soared, energy infrastructure investment exploded globally, and Jindal SAW's order book swelled. The stock price responded dramatically, rising from under ₹50 in 2003 to over ₹500 by 2007—a ten-fold increase that created significant wealth for early investors.

But the global financial crisis of 2008 brought a harsh reality check. The stock crashed over 80% from its peaks as projects were cancelled, steel prices collapsed, and credit markets froze. For many investors, this volatility reinforced perceptions of Jindal SAW as a cyclical commodity play rather than a growth story.

The Turnaround Years: 2020-2024

The real financial transformation came post-2020. Net profit for the year grew by 264.5% YoY in FY24. Net profit margins during the year grew from 2.5% in FY23 to 9.0% in FY24. This wasn't just cyclical recovery—it represented fundamental improvements in the business model.

Several factors drove this transformation. First, the company's diversification strategy began paying off, with non-pipe businesses providing stability during volatile periods. Second, operational efficiency improvements—from automated welding to predictive maintenance—reduced costs and improved margins. Third, the shift toward value-added products meant higher realizations per ton of steel processed.

The balance sheet transformation was equally impressive. Debt to Equity ratio improved to 0.0 from 0.2, reflecting strong cash generation and disciplined capital allocation. Return on Capital Employed (ROCE) improved to 24.3% during FY24, from 14.0% during FY23—metrics that finally caught investors' attention.

FY25: Margin Expansion Despite Revenue Decline

The most recent financial year presented an interesting paradox. Revenues of JINDAL SAW stood at Rs 183,342 m in FY25, which was down -13.8% compared to Rs 212,702 m reported in FY24. Yet, Net profit of JINDAL SAW stood at Rs 18,745 m in FY25, which was up 17.7% compared to Rs 15,929 m reported in FY24. Net profit margins during the year grew from 7.6% in FY24 to 10.5% in FY25.

This counterintuitive performance—growing profits despite falling revenues—reflected the company's strategic shift. Lower commodity prices reduced revenues but expanded margins. The mix shift toward higher-margin products and services offset volume declines. Cost reduction initiatives, including automation and energy efficiency, reduced the operating leverage that historically plagued the business.

Capital Allocation Evolution

The company's approach to capital allocation also evolved significantly. During the growth years of 2000-2008, Jindal SAW aggressively expanded capacity, often funding growth through debt. The 2008 crisis taught painful lessons about the risks of leverage in cyclical businesses.

Post-2015, the capital allocation philosophy changed. Growth investments focused on high-return projects with quick paybacks. The company maintained strong cash reserves to weather downturns. Dividends became more consistent, signaling confidence in sustainable cash generation. Most importantly, the company began returning excess cash to shareholders through buybacks when the stock traded below intrinsic value.

The Valuation Conundrum

Despite operational improvements, Jindal SAW's valuation remains puzzling. Currently trading at 1.14 times book value, P/E of 8.95—significantly below both historical averages and peer valuations. According to Wall Street analysts, the average 1-year price target for JINDALSAW is 348.5 INR with a low forecast of 292.9 INR and a high forecast of 424.2 INR, suggesting significant upside from current levels.

Several factors explain this discount. Contingent liabilities of Rs.4,236 Cr create uncertainty about potential future obligations. The cyclical nature of end markets makes earnings unpredictable. Complex corporate structure with multiple subsidiaries and joint ventures reduces transparency. Competition from Chinese manufacturers pressures margins. ESG concerns about steel and fossil fuel exposure limit institutional interest.

The Investor Base Evolution

The shareholder composition tells its own story. Promoter Holding: 63.3% remains high, providing stability but limiting float. Institutional ownership has gradually increased but remains below peers, reflecting continued skepticism about governance and cyclicality. Retail investors, attracted by dividend yields and the infrastructure story, have become increasingly important.

Foreign institutional investors remain notably underweight, concerned about corporate governance, the complex holding structure, and India's manufacturing competitiveness. This creates both risk and opportunity—any improvement in perception could drive significant rerating as global investors increase allocation.

The financial journey of Jindal SAW reflects broader themes in Indian capital markets: the challenge of valuing cyclical businesses, the importance of corporate governance, and the long journey from family-controlled manufacturer to institutional-quality investment. While operational performance has improved dramatically, convincing markets to pay for this improvement remains an ongoing challenge.

VIII. Modern Era: Challenges & Opportunities (2020–Present)

March 2020. The world shut down. For a company whose business depended on construction sites, oil rigs, and infrastructure projects, the COVID-19 pandemic represented an existential threat. Projects halted mid-construction. Workers fled cities. Supply chains broke. Oil prices briefly turned negative. In the crisis management room at Jindal SAW's Delhi headquarters, executives were planning for the worst-case scenario: a complete halt to global infrastructure spending.

What followed instead became a masterclass in crisis management and strategic positioning. Rather than retreat, Jindal SAW accelerated. The company used the downturn to upgrade facilities, implement digital systems, and reposition for the post-pandemic recovery. When governments worldwide unleashed unprecedented infrastructure stimulus, Jindal SAW was ready.

The Great Acceleration

The post-pandemic period saw an unexpected acceleration in infrastructure spending globally. Governments, seeking to stimulate economies, launched massive infrastructure programs. Energy security concerns, heightened by geopolitical tensions, drove pipeline investments. The energy transition, paradoxically, increased demand for traditional pipeline infrastructure as natural gas emerged as a transition fuel.

Q1 FY26 results show revenue decline; announces $428M UAE/KSA pipe projects, expanding MENA presence. This announcement in 2025 represents not just expansion but strategic positioning for the next decade. The Middle East, flush with petrodollars from high oil prices and committed to economic diversification, is investing hundreds of billions in infrastructure.

The Saudi Arabia Opportunity

The Saudi joint ventures announced in 2025—HSAW pipe manufacturing with 51% stake, $10 million investment—represent more than just capacity addition. Saudi Arabia's Vision 2030, the kingdom's ambitious plan to diversify its economy, requires massive infrastructure investment. New cities like NEOM, industrial corridors, and water infrastructure all need pipes—lots of them.

But entering Saudi Arabia isn't straightforward. Local content requirements, partnership obligations, and complex regulatory frameworks create barriers. Jindal SAW's approach—joint ventures with local partners providing market access while Jindal provides technology and expertise—navigates these challenges while maintaining control.

The Energy Transition Paradox

The global push toward renewable energy created an unexpected dynamic for Jindal SAW. While long-term demand for oil and gas pipelines might decline, the transition period requires massive infrastructure investment. Natural gas, positioned as a bridge fuel, needs extensive pipeline networks. Hydrogen, touted as the future of energy, requires specialized pipeline infrastructure. Even renewable energy projects need steel—wind turbines, solar panel frames, transmission infrastructure.

The company's response has been to position itself as an enabler of energy transition rather than a victim. Developing hydrogen-compatible pipe specifications, investing in coating technologies for offshore wind foundations, and exploring opportunities in carbon capture and storage infrastructure—all represent attempts to remain relevant in a changing energy landscape.

The China Challenge

Perhaps no challenge looms larger than Chinese competition. Chinese pipe manufacturers, backed by state subsidies and operating at massive scale, can often undercut prices by 20-30%. In markets where price is the primary consideration, Jindal SAW struggles to compete.

The company's response has been to move up the value chain. Focus on specialized products where quality, certification, and track record matter more than price. Develop local manufacturing capabilities in key markets to avoid anti-dumping duties. Build relationships and technical capabilities that create switching costs for customers. The strategy is working in developed markets but remains challenging in price-sensitive emerging markets.

Digital Transformation: Beyond Buzzwords

Every industrial company talks about digital transformation, but few execute meaningfully. Jindal SAW's approach has been pragmatic rather than revolutionary. Digital twins of pipeline networks help optimize design and predict maintenance needs. IoT sensors on pipes provide real-time performance data. AI-powered quality control systems detect defects invisible to human inspectors.

More importantly, digital tools are transforming customer relationships. A cloud-based project management platform allows customers to track their orders in real-time, from steel procurement through manufacturing to delivery. This transparency, unusual in the traditionally opaque pipe industry, creates competitive advantage beyond just product quality.

The Regulatory Tightrope

Operating across multiple jurisdictions brings regulatory complexity. Environmental regulations in Europe, local content requirements in the Middle East, trade restrictions in America, quality standards in Japan—each market has unique requirements. The company maintains a team of regulatory specialists who track changing requirements and ensure compliance.

Recent developments add complexity. Carbon border taxes in Europe affect competitiveness. America's infrastructure bill prioritizes domestic manufacturers. India's production-linked incentive schemes create opportunities but also obligations. Managing this regulatory maze requires sophisticated systems and local expertise.

Building for the Next Decade

The UAE seamless pipe facility: 300,000 tonnes annual capacity, $105 million investment announced in 2025 represents a bet on the future. Despite talk of peak oil, the Middle East continues investing in energy infrastructure. The facility's location in Abu Dhabi provides access to high-growth markets across the MENA region while avoiding the geopolitical risks of manufacturing in more volatile locations.

The investment also reflects learning from past expansions. Rather than building maximum capacity upfront, the facility is designed for modular expansion. Advanced automation reduces dependence on skilled labor in a region where workforce availability is challenging. Multi-product capability allows shifting between oil and gas pipes, water infrastructure, and industrial applications based on market demand.

The Talent Challenge

As Jindal SAW globalizes and modernizes, attracting and retaining talent becomes critical. The company competes not just with other manufacturers but with technology companies and consulting firms for engineering talent. Young engineers often prefer working for software companies over traditional manufacturing.

The company's response includes establishing innovation centers in urban locations, partnering with universities for research projects, and creating career paths that combine technical and commercial roles. The establishment of Jindal University by the broader group helps create a pipeline of trained professionals, though retention remains challenging.

The modern era presents Jindal SAW with its greatest opportunities and challenges simultaneously. The infrastructure super-cycle, energy transition, and emerging market growth create massive demand. But Chinese competition, technological disruption, and ESG concerns threaten traditional business models. Success requires balancing growth with profitability, global expansion with local relevance, and traditional manufacturing excellence with digital innovation.

IX. Playbook: Business & Investing Lessons

After nearly four decades of building Jindal SAW from a single factory to a global industrial player, what lessons emerge? The playbook isn't just about manufacturing pipes—it's about building industrial capabilities in emerging markets, navigating family business dynamics, and creating value through cycles.

Lesson 1: Timing Infrastructure Cycles

Infrastructure is inherently cyclical, but the cycles are long and somewhat predictable. Jindal SAW's success came from recognizing these patterns early. The India infrastructure boom of 2003-2008 wasn't surprising—a country of a billion people with massive infrastructure deficits would eventually invest. The shale gas revolution in America created predictable pipeline demand. The Middle East's economic diversification was telegraphed years in advance.

The key insight: infrastructure cycles lag economic cycles by 2-3 years. When economies grow, infrastructure constraints emerge. Governments and companies then plan projects, which take years to execute. By the time projects are commissioned, the economic cycle may have turned, but the infrastructure investment continues. Understanding this lag creates opportunity.

Lesson 2: Technical Expertise as Moat

In commoditized industries, technical expertise creates differentiation. Jindal SAW's ability to manufacture pipes that withstand minus-50°C in Siberia or plus-50°C in Saudi Arabia, that resist corrosion in deep-sea environments or handle hydrogen's unique properties—this isn't easily replicated.

But technical expertise alone isn't enough. It must be combined with certifications (API, ISO), track records (successful project references), and relationships (trusted by major oil companies). This combination creates barriers that pure manufacturing capacity cannot overcome. Chinese competitors might match the capacity and even the technical specifications, but replicating decades of project execution and relationship capital takes time.

Lesson 3: Managing Cyclical Businesses

Cyclical businesses require different management approaches than growth businesses:

-

Financial conservatism during booms: When order books are full and margins expanding, the temptation is to leverage up and expand aggressively. Jindal SAW learned through painful experience to maintain financial discipline especially during good times.

-

Operational aggression during busts: Downturns are when assets are cheap, competitors are weak, and market share is available. The company's major expansions—the US acquisition in 2014, Middle East investments in 2025—came during or after downturns.

-

Portfolio diversification: Pure-play exposure to any single end market is dangerous. Jindal SAW's diversification into water infrastructure, pellets, and services provides stability through cycles.

Lesson 4: Family Business Governance

The Jindal structure—splitting the empire but maintaining cross-holdings—offers lessons in family business governance:

Advantages: - Aligned interests prevent destructive competition - Shared learning across group companies - Financial support during crises - Long-term orientation without quarterly pressure

Disadvantages: - Complex decision-making with multiple stakeholders - Potential for conflicts of interest - Reduced transparency for outside investors - Succession planning complexity

The key is professionalizing management while maintaining family oversight. Jindal SAW's appointment of independent directors, professional CEOs for subsidiaries, and transparent reporting standards show evolution toward institutional governance while preserving family control.

Lesson 5: Geographic Diversification Strategy

Jindal SAW's global expansion followed a clear pattern:

- Start with exports to understand markets and requirements

- Establish partnerships for local knowledge and relationships

- Create local presence through offices or joint ventures

- Acquire or build manufacturing when market size justifies investment

- Integrate operations while maintaining local autonomy

This gradual approach reduces risk while building capabilities. The failed ventures—Russia, Italy—came when this process was short-circuited, emphasizing the importance of patience in international expansion.

Lesson 6: Capital Allocation in Capital-Intensive Businesses

Capital allocation in manufacturing differs from asset-light businesses:

- Maintenance capex is non-negotiable: Failing to maintain assets leads to quality issues, safety risks, and eventual business failure

- Growth capex requires high conviction: New facilities take years to build and longer to generate returns

- Working capital management is crucial: In project businesses, payment terms can make or break profitability

- Technology investments have option value: Upgrading capabilities opens new markets even if immediate returns aren't visible

The discipline to differentiate between maintenance and growth spending, to time investments with cycles, and to maintain flexibility through downturns determines long-term success.

Lesson 7: Building B2B Relationships

B2B relationships differ fundamentally from B2C:

- Technical credibility precedes commercial discussions: Engineers must trust your capabilities before procurement considers your prices

- Track record matters more than marketing: One failed project destroys reputation built over decades

- Relationships are institutional, not just personal: While personal relationships matter, institutional processes and certifications ensure continuity

- Global presence enables local relationships: Multinational clients prefer suppliers who can serve them globally

Jindal SAW's investment in technical capabilities, quality certifications, and global presence reflects understanding of B2B relationship dynamics.

Lesson 8: The Value Chain Extension Strategy

Moving up the value chain—from pipes to coated pipes to complete pipeline solutions—creates multiple advantages:

- Higher margins: Value-added services command premium pricing

- Customer stickiness: Integrated solutions create switching costs

- Competitive differentiation: Harder for new entrants to replicate

- Risk mitigation: Service revenues are less cyclical than product sales

But value chain extension requires different capabilities—project management, systems integration, service delivery—that pure manufacturers often struggle to build.

Lesson 9: Managing Commodity Price Volatility

Steel constitutes 60-70% of pipe manufacturing costs. Managing this volatility requires sophisticated strategies:

- Natural hedging: Pellet operations provide insight into iron ore markets

- Contract structures: Back-to-back agreements transfer price risk to customers

- Inventory management: Strategic purchasing during price troughs

- Financial hedging: Selective use of derivatives for large projects

The goal isn't to eliminate commodity exposure but to manage it intelligently.

Lesson 10: The ESG Transition

Traditional manufacturing companies face increasing ESG scrutiny. Jindal SAW's response offers lessons:

- Acknowledge rather than deny: Accept that fossil fuel exposure is a concern

- Demonstrate transition enablement: Position as essential for energy transition

- Invest in clean technologies: Develop products for renewable energy infrastructure

- Improve operational sustainability: Reduce emissions, water usage, waste

- Transparent reporting: Regular ESG disclosures build credibility

The transition from ESG laggard to leader takes time but is essential for accessing institutional capital.

These lessons form a playbook not just for industrial companies but for any business navigating cyclical markets, technological change, and global competition. The key insight: success comes not from avoiding challenges but from building capabilities to navigate them.

X. Analysis & Investment Case

Standing at current valuations—Trading at 1.14 times book value, P/E of 8.95—Jindal SAW presents a classic value investing puzzle. Is this a permanently impaired business model trading at deserved multiples, or an overlooked compounder available at distressed valuations? The answer requires examining both the bull and bear cases with surgical precision.

The Bear Case: Structural Headwinds

The pessimistic view starts with energy transition. If oil and gas pipeline demand peaks in the next decade, Jindal SAW's core market shrinks structurally. While management talks about hydrogen pipelines and renewable energy infrastructure, these markets remain nascent and unproven at scale.

Chinese competition intensifies yearly. Chinese manufacturers, operating with state subsidies, cheaper labor, and massive scale, can manufacture pipes at costs Jindal SAW cannot match. In commodity products where price determines purchase decisions, this cost disadvantage proves fatal. Anti-dumping duties provide temporary relief but aren't sustainable long-term solutions.

Contingent liabilities of ₹4,236 Cr represent a sword of Damocles. These off-balance-sheet obligations—primarily related to tax disputes and performance guarantees—could materialize suddenly, destroying equity value. The complexity and opacity of these liabilities make accurate risk assessment nearly impossible for outside investors.

The family-controlled structure limits governance improvements. With Promoter Holding at 63.3%, minority shareholders have limited influence. Related-party transactions, complex holding structures, and potential conflicts of interest remain persistent concerns. The cross-holdings among Jindal brothers' companies create additional complexity.

Cyclicality ensures permanent volatility. Even if the business performs well over cycles, the volatility destroys compounding. Investors who buy at cycle peaks suffer permanent capital loss. Those who buy at troughs face years of dead money waiting for recovery. This volatility makes the stock unsuitable for most institutional portfolios.

Technology disruption looms. New materials—composites, plastics, alternative construction methods—could replace steel pipes in certain applications. 3D printing might enable on-site manufacturing, eliminating transportation advantages. Digital technologies could reduce infrastructure needs by optimizing existing capacity.

The Bull Case: Hidden Compounder

The optimistic view sees current valuations as extraordinarily attractive for a business with sustainable competitive advantages. At The intrinsic value calculated as 315.29 INR versus current price of 211.35 INR, the margin of safety appears substantial.

Infrastructure spending isn't stopping—it's accelerating. India alone needs $1.4 trillion in infrastructure investment by 2025. The Middle East's economic diversification requires massive infrastructure buildout. Even developed markets need to replace aging pipeline networks. The addressable market is enormous and growing.

The company's competitive position strengthens despite Chinese competition. It is the world's third-largest producer of rust-free iron pipes with manufacturing and supplying more than 39,490 kms of Line pipes & exporting over 17,707 Kms globally. This isn't easily replicated. Relationships with major oil companies, technical certifications, and project execution capabilities create moats that cost advantage alone cannot overcome.

Recent financial performance demonstrates earnings power. Net profit grew 264.5% YoY in FY24 followed by 17.7% growth in FY25 despite revenue declining 13.8%. Net profit margins expanded from 7.6% in FY24 to 10.5% in FY25. This margin expansion during revenue decline suggests structural improvements rather than cyclical benefits.

The balance sheet provides downside protection. With Debt to Equity at 0.0 and improving cash generation, the company can weather downturns without dilution or distress. Book value provides floor valuation—even in liquidation, current prices offer limited downside.

Geographic and product diversification reduces risk. Unlike pure-play pipe manufacturers, Jindal SAW's exposure across geographies, end markets, and products provides resilience. When oil and gas spending declines, water infrastructure often accelerates. When India slows, the Middle East might boom.

Management execution has improved dramatically. ROCE improving from 14.0% to 24.3%, margins expanding despite competition, successful international expansions—recent performance suggests management has learned from past mistakes and built institutional capabilities.

Valuation Framework

Multiple approaches suggest undervaluation:

Asset-Based Valuation: At 1.14x book value, the market values Jindal SAW barely above liquidation value. For a profitable, growing business with global operations, this seems excessively pessimistic.

Earnings-Based Valuation: At P/E of 8.95 versus historical average of 15-20x, current valuations embed extremely negative expectations. Even assuming earnings decline 30%, current valuations appear attractive.

Comparative Valuation: Global pipe manufacturers trade at 12-18x earnings. Indian infrastructure companies command 15-25x. Jindal SAW's discount to both peer groups seems unjustified given superior margins and growth.

Sum-of-Parts Valuation: Valuing each business separately—pipes, pellets, logistics, services—suggests significant value above current market capitalization. The market appears to assign zero value to several profitable segments.

Risk-Reward Analysis

The key risks are quantifiable:

- Cyclical downturn: Even assuming 50% earnings decline in severe recession, downside appears limited given current valuations

- Contingent liabilities: Even if entire ₹4,236 Cr materializes, impact per share is manageable given current market cap

- Chinese competition: Market share loss is gradual, providing time to adapt

- Energy transition: Timeline measured in decades, not years

The potential rewards are substantial:

- Multiple re-rating: Moving from 9x to 15x P/E implies 67% upside

- Earnings growth: Returning to peak margins on recovered volumes could double earnings

- Hidden asset value: Proper valuation of non-pipe businesses could add 30-40% to market cap

The Investment Decision

Jindal SAW represents a classic contrarian opportunity. The stock is neglected, misunderstood, and priced for disaster. Yet the business continues generating cash, winning projects, and expanding strategically. For investors with:

- Long time horizons (5+ years to ride through cycles)

- Volatility tolerance (50% drawdowns are possible)

- Contrarian mindset (comfort investing against consensus)

- Portfolio diversification (limiting position size to manage risk)

The current risk-reward appears compelling. This isn't a growth-at-any-price story or a momentum trade. It's a value investment in an essential business trading at distressed valuations despite improving fundamentals.

The margin of safety appears sufficient to protect against most negative scenarios while providing substantial upside if any of several catalysts materialize: infrastructure spending acceleration, successful Middle East expansion, margin improvement, or simple multiple normalization.

XI. Epilogue & Future Outlook

As we look toward 2030 and beyond, Jindal SAW stands at an inflection point. The decisions made today—about technology adoption, market positioning, and capital allocation—will determine whether the company remains relevant in a rapidly changing world or becomes another industrial relic, a monument to a bygone era of steel and oil.

The Energy Transition Navigation

The path forward requires threading a needle between old and new energy paradigms. While environmental activists demand immediate cessation of fossil fuel infrastructure, the reality is more complex. Natural gas will likely serve as a bridge fuel for decades. Even aggressive renewable adoption requires massive steel infrastructure—offshore wind foundations, transmission towers, hydrogen pipelines.

Jindal SAW's response must be nuanced. Continue serving traditional energy markets while developing capabilities for emerging applications. The company's recent investments in coating technologies for hydrogen compatibility and corrosion resistance in offshore renewable applications show understanding of this duality.

By 2030, success looks like a portfolio where traditional oil and gas represents less than 40% of revenues, replaced by water infrastructure, renewable energy applications, and emerging technologies like carbon capture pipelines. This transition won't be smooth—it requires cannibalizing existing businesses while building new ones.

Technology as Enabler, Not Disruptor

The Fourth Industrial Revolution—AI, IoT, robotics, additive manufacturing—threatens traditional manufacturing. But for Jindal SAW, these technologies represent opportunity more than threat. Predictive maintenance using IoT sensors can guarantee pipeline performance. AI-optimized designs can reduce material usage while improving strength. Robotics can ensure consistent quality while reducing costs.

The key is selective adoption. Not every technology makes sense for pipe manufacturing. But those that do—automated welding, drone inspection, digital twins—must be embraced fully. By 2030, the most successful pipe manufacturers won't be those with the most capacity but those who best integrate physical and digital capabilities.

The Geographic Rebalancing

The next decade will see fundamental shifts in global infrastructure spending. China's infrastructure boom is ending. India's is accelerating. Africa represents the next frontier. The Middle East continues diversifying. America focuses on replacing aging infrastructure. Each market requires different approaches, products, and partnerships.

Jindal SAW's footprint must evolve accordingly. The current focus on India, Middle East, and America makes sense near-term. But building positions in Africa, Southeast Asia, and Latin America requires starting now. These markets are difficult—political risk, payment challenges, infrastructure deficits—but offer decades of growth potential.

The Succession Question

Prithviraj Jindal, now in his 70s, has led the company since inception. The next generation must be prepared. This isn't just about family succession but institutional capability building. The company needs professional managers who understand global markets, digital technologies, and stakeholder capitalism while respecting the entrepreneurial culture that built the business.

The transition has begun with professional CEOs for subsidiaries and independent directors on boards. But more is needed. Creating a deep bench of leaders, establishing clear succession planning, and gradually transitioning responsibilities ensures continuity. By 2030, leadership transition should be complete, with the next generation firmly in charge.

The Sustainability Imperative

ESG considerations will only intensify. By 2030, carbon-neutral manufacturing won't be optional—it will be required for accessing capital and winning contracts. This requires fundamental changes: renewable energy for manufacturing, circular economy approaches to steel recycling, and transparent sustainability reporting.

But sustainability goes beyond environmental concerns. Social license to operate, community development, employee welfare—these "soft" factors increasingly determine business success. Jindal SAW's investments in education, healthcare, and community development around its facilities must expand and deepen.

Key Metrics for 2030

What does success look like in concrete terms?

- Revenue: ₹300,000+ crores (from current ₹183,342 crores)

- Geographic mix: India 40%, Middle East 25%, Americas 20%, Others 15%

- Product mix: Traditional pipes 40%, Water infrastructure 30%, New energy 20%, Services 10%

- ROCE: Sustained above 20%

- Debt/Equity: Maintained below 0.5

- ESG rating: Among top quartile of global industrial companies

These aren't just financial metrics but indicators of successful transformation from an Indian pipe manufacturer to a global infrastructure solutions provider.

The Path Forward

The journey from a single factory in Kosi Kalan to global industrial player took four decades. The next transformation—from industrial manufacturer to sustainable infrastructure enabler—must happen faster. The pace of change accelerates. Competition intensifies. Stakes increase.

Yet the fundamental drivers of Jindal SAW's success remain relevant. Infrastructure needs continue growing. Technical expertise matters more as specifications become complex. Global presence provides resilience. Family ownership enables long-term thinking. These advantages, properly leveraged, position the company for continued success.

The story of Jindal SAW is ultimately about transformation—of iron ore into pipes, of rural India into industrial power, of family business into global enterprise. The next chapter requires another transformation: from serving the fossil fuel economy to enabling sustainable development. It's a challenge worthy of the ambition that built the company.

For investors, employees, and stakeholders, the question isn't whether Jindal SAW will exist in 2030—industrial companies of this scale don't disappear quickly. The question is what it will become: a thriving, relevant leader in sustainable infrastructure, or a declining legacy business managing obsolescence. Current evidence suggests the former, but execution over the next five years will determine the outcome.

The pipes that Jindal SAW manufactures today will carry energy and water for decades. The decisions made today will determine whether the company itself flows forward into the future or becomes a relic of industrial history. For those with the vision to see beyond current challenges and the patience to wait for transformation, the opportunity remains compelling.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube