JBM Auto: From Auto Components to India's Electric Bus Revolution

I. Introduction & Episode Roadmap

Picture this: In the sprawling industrial outskirts of Gurugram, a massive 100-acre facility hums with activity. Electric buses roll off assembly lines every few hours, their bright green livery symbolizing India's sustainable transport revolution. This isn't a Chinese BYD factory or a Tesla facility—it's JBM Auto's crown jewel, the world's largest dedicated integrated electric bus manufacturing ecosystem outside China. A company that started four decades ago making simple metal cylinders now commands 30-35% of India's electric bus market, with half a million auto components rolling out of its factories daily.

The transformation of JBM Auto reads like a masterclass in industrial evolution. From a modest components supplier inspired by Intel's "Intel Inside" model to create "JBM Inside" for Indian vehicles, to becoming the backbone of India's electric mobility revolution—this is a story of vision meeting opportunity at precisely the right moment.

What makes JBM's journey particularly fascinating isn't just the pivot from traditional auto components to electric vehicles. It's how they've built an entire ecosystem—from lithium-ion batteries to charging infrastructure, from power electronics to complete bus manufacturing. While global giants were still debating electric vehicle strategies, JBM was quietly assembling the pieces of what would become India's most comprehensive e-mobility platform.

The numbers tell part of the story: ₹14,360 crore market capitalization, ₹5,582 crore in revenue, contracts worth ₹5,500 crore under the government's PM-eBus Sewa Scheme. But the real narrative lies in how a family-run conglomerate from North India outmaneuvered established players to capture the commanding heights of India's electric bus market—a market that barely existed a decade ago.

This episode unpacks three critical transformations: First, how JBM built one of India's most successful auto component businesses through the liberalization era. Second, their prescient pivot to electric vehicles just as India's pollution crisis reached critical mass. And third, their vertical integration strategy that created competitive moats even Tata Motors and Ashok Leyland struggle to breach.

For investors, JBM represents a fascinating paradox: a traditional manufacturing company trading at tech-like valuations (P/E of 69.9), a government contractor with Silicon Valley ambitions, and an Indian company building global technology capabilities. As we'll explore, understanding JBM requires rethinking conventional frameworks about emerging market industrials.

What follows is the untold story of how a cylinder manufacturer became India's electric bus champion—and why their next decade might be even more transformative than their last four.

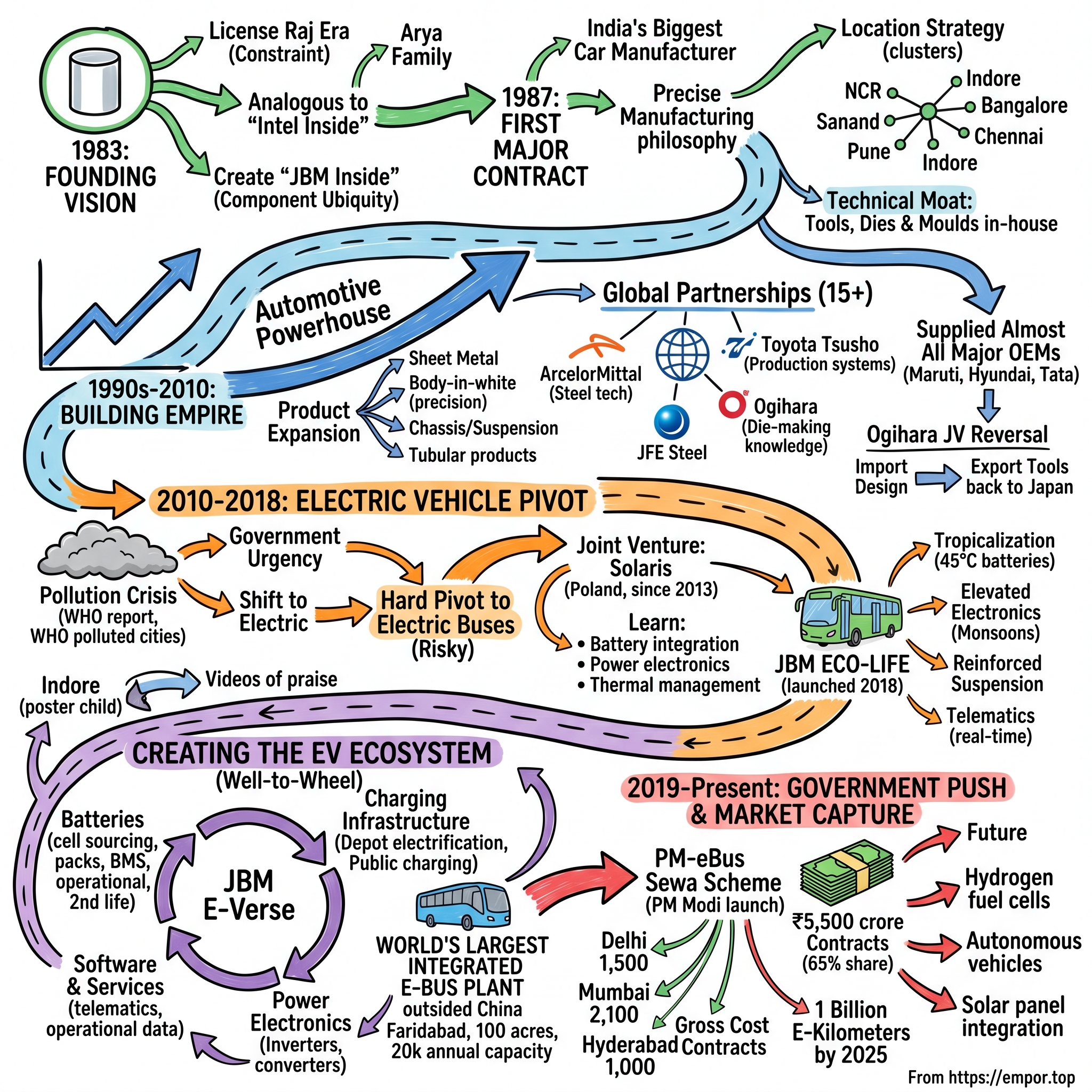

II. The JBM Group Origins & Founding Vision (1983–1990s)

The year was 1983. India was still deep in the License Raj era, where every industrial decision required government approval and entrepreneurship meant navigating Byzantine bureaucracy. In this constrained environment, the Arya family founded JBM Group with a simple manufacturing unit producing cylinders. But the founder had been struck by a powerful analogy from the computer industry—Intel's "Intel Inside" campaign that had made a hidden component famous worldwide.

"Why couldn't there be a 'JBM Inside' for Indian vehicles?" This wasn't just marketing aspiration; it was a strategic vision that would guide every major decision for the next four decades. The idea was audacious for its time: become so integral to India's automotive supply chain that JBM components would be ubiquitous, even if invisible to end consumers.

The breakthrough came in 1987 when JBM secured its first major contract with India's biggest car manufacturer. This wasn't just another supplier relationship—it was validation of JBM's manufacturing philosophy: deliver consistent quality at scale while maintaining cost competitiveness. In an era when Indian manufacturing was synonymous with compromise, JBM was betting on precision.

Location strategy became crucial early on. Rather than concentrate operations in one industrial hub, JBM began establishing facilities near automobile manufacturing clusters: Delhi-NCR for the northern market, Sanand to serve Gujarat's emerging auto hub, Pune for western India's manufacturing belt, and later expanding to Indore, Nasik, Bangalore, and Chennai. This distributed model meant higher capital costs but provided two critical advantages: proximity to customers reduced logistics expenses, and geographic diversification reduced dependency on any single market.

The late 1980s and early 1990s were formative in another way—JBM began developing deep expertise in tools, dies, and moulds. This might seem like unglamorous work, but it was strategic genius. Tools and dies are the DNA of manufacturing; whoever controls them controls production flexibility and cost structure. While competitors outsourced this capability, JBM built it in-house, creating a technical moat that would prove invaluable decades later.

By the early 1990s, JBM had evolved from a single-product company to a diversified auto component manufacturer. The portfolio expanded systematically: first sheet metal components (the body panels and structural parts), then more complex assemblies, and eventually entire subsystems. Each expansion followed the same playbook: start with simple parts, prove reliability, then move up the value chain.

The economics of this period were compelling. India's automotive market was growing at 15-20% annually as economic liberalization unleashed pent-up consumer demand. Every new car model needed hundreds of components, and localization requirements meant foreign automakers needed Indian suppliers. JBM positioned itself perfectly—sophisticated enough for global OEMs, cost-effective enough for Indian manufacturers.

What distinguished JBM from hundreds of other component suppliers wasn't just manufacturing capability—it was their approach to partnerships. Rather than viewing OEM relationships transactionally, JBM invested in understanding their customers' long-term product roadmaps. When Maruti Suzuki needed suppliers for their next-generation models, JBM had already developed the capabilities. When global automakers entered India, JBM spoke their language of quality certifications and process controls.

The 1990s also saw JBM's first international forays. Exports began modestly—tools and dies to Southeast Asian markets where Indian engineering was respected but not yet premium-priced. These early international experiences would prove crucial; they exposed JBM to global quality standards and manufacturing practices that would later differentiate them in the domestic market.

By the decade's end, JBM had transformed from a single factory in Gurugram to a multi-location conglomerate generating hundreds of crores in revenue. The "JBM Inside" vision was becoming reality—their components were in virtually every major vehicle brand sold in India. But this was just the foundation for what would come next.

III. Building the Auto Components Empire (1990s–2010)

The turn of the millennium marked JBM's transformation from a successful component supplier to an automotive powerhouse. India's auto industry was experiencing a golden age—car sales doubled between 2000 and 2005, and global automakers were making India a manufacturing hub for small cars. JBM didn't just ride this wave; they anticipated and shaped it.

The company's core business crystallized around three segments that would generate massive cash flows: sheet metal components, tools/dies/moulds, and an OEM division for buses. Each segment reinforced the others in a virtuous cycle. The sheet metal business provided volume and steady revenue, tools and dies offered high margins and technical differentiation, while the bus OEM division served as a testing ground for integrated manufacturing capabilities.

Product portfolio expansion during this period was methodical yet ambitious. Body-in-white (BIW) components—the skeletal frame of vehicles before painting—became a specialty. These weren't simple stamped parts but complex assemblies requiring precision welding and dimensional accuracy measured in fractions of millimeters. JBM's chassis and suspension systems evolved from basic components to complete modules. Pedal boxes, seemingly simple but safety-critical, showcased their ability to meet global crash-test standards. Tubular products for exhaust systems demonstrated mastery of different manufacturing processes.

The real strategic coup came through global partnerships. Between 2000 and 2010, JBM formed alliances with over 15 international organizations. The partnership with ArcelorMittal brought advanced steel technology. Toyota Tsusho provided access to Toyota's legendary production systems. JFE Steel from Japan offered materials expertise. Ogihara, a Japanese tooling giant, transferred critical die-making knowledge. Each partnership was carefully chosen—not just for immediate technology transfer but for long-term capability building.

Consider the Ogihara partnership in detail. Japanese tooling companies were considered the gold standard globally, with capabilities Indian firms couldn't match. Rather than compete, JBM partnered, establishing a joint venture that brought Japanese precision to Indian cost structures. The venture started with imported designs and expatriate technicians but gradually developed local capabilities. Within five years, the JV was exporting tools back to Japan—a reversal that stunned industry observers.

By 2010, JBM supplied "almost all major OEMs in India"—a claim that sounds hyperbolic but was literally true. Maruti Suzuki, Hyundai, Tata Motors, Mahindra, Honda, Toyota, Volkswagen—every major assembly line had JBM components. The economics were staggering: a typical car might have 50-100 JBM parts, from critical safety components to simple brackets. Multiply that by millions of vehicles, and you understand the scale.

The business model during this period was deceptively simple but hard to replicate. JBM would co-locate facilities with major OEMs, reducing logistics costs and enabling just-in-time delivery. They'd invest upfront in customer-specific tooling, creating switching costs. They'd commit to annual price reductions, forcing continuous productivity improvements. And they'd maintain quality levels that exceeded customer specifications, building trust that transcended contracts.

Being a Tier-1 supplier in India's auto boom wasn't just about manufacturing—it was about financial engineering. OEMs demanded extended payment terms while raw material suppliers wanted quick payment. JBM mastered working capital management, using supply chain financing and inventory optimization to generate cash despite challenging payment cycles. Return on capital employed consistently exceeded 20%, remarkable for a capital-intensive manufacturing business.

The international expansion accelerated during this period. Exports grew from a few million dollars to hundreds of millions. But more importantly, JBM began establishing overseas facilities. A plant in South Africa to serve the local auto industry. Technical centers in Europe to work with global OEMs on next-generation designs. Each international presence enhanced credibility back home—Indian automakers took notice when JBM won contracts from demanding German manufacturers.

Technology absorption was another differentiator. While competitors focused on low-cost production, JBM invested in advanced manufacturing technologies. Robotic welding lines, automated painting systems, real-time quality monitoring—capabilities that seemed excessive for the Indian market but positioned JBM for the next evolution. They weren't just making parts; they were building a platform for whatever came next.

The 2008 financial crisis tested this model. Auto sales crashed globally, and India wasn't immune. But JBM's diversification across customers, products, and geographies provided resilience. While single-product suppliers went bankrupt, JBM used the downturn to consolidate market share, acquiring distressed assets and hiring talent from struggling competitors. By 2010, they emerged stronger, with capabilities that would prove perfectly suited for the next transformation.

The numbers from this era tell the story: revenue grew from under ₹500 crore in 2000 to over ₹3,000 crore by 2010. Manufacturing facilities expanded from 10 to 40+. Employee count rose from hundreds to tens of thousands. But the most important metric wasn't financial—it was the institutional knowledge accumulated. JBM now understood every aspect of automotive manufacturing, from design to delivery. This expertise would soon find an unexpected application.

IV. The Electric Vehicle Pivot: Vision Meets Opportunity (2010–2018)

In 2015, a World Health Organization report sent shockwaves through India's policy establishment: 14 of the world's 20 most polluted cities were in India. Delhi's air quality had become an international embarrassment, with winter smog so thick it grounded flights. Transport contributed 40% of urban air pollution, and within that, diesel buses were the worst offenders—each one equivalent to 25 cars in emissions. Yet India had less than 2 buses per 1,000 population, compared to 8 in China and 12 in developed countries. The math was brutal: India needed more public transport but couldn't afford more pollution.

This crisis created an unexpected opportunity for JBM. While the company had been manufacturing bus bodies through their OEM division since the early 2000s, these were conventional diesel vehicles—reliable but unremarkable. The pollution crisis changed everything. Suddenly, there was government urgency, public awareness, and international pressure to transform urban transport. JBM's leadership made a decision that seemed risky at the time but would define their next decade: pivot hard into electric buses.

The strategic logic was compelling once you looked past the immediate challenges. Electric buses solved multiple problems simultaneously—zero local emissions addressed the pollution crisis, lower operating costs appealed to cash-strapped state transport corporations, and the technology shift created an opportunity to leapfrog established players. While Tata Motors and Ashok Leyland dominated conventional buses with 70%+ market share, electric buses were a new game with new rules.

JBM's entry into electric vehicles wasn't a moonshot bet—it was methodical preparation meeting sudden opportunity. Since 2013, they'd been quietly building capabilities through their joint venture with Poland's Solaris, Europe's leading electric bus manufacturer. This wasn't widely publicized, but JBM engineers were in Poland learning battery integration, power electronics, and thermal management—technologies completely different from mechanical engineering.

The 2016 announcement of JBM's electric bus program surprised the industry. Competitors dismissed it as publicity-seeking from a component supplier overreaching into OEM territory. But JBM had done their homework. They'd studied Chinese electric bus manufacturers like BYD and Yutong, analyzed European operators' experiences, and most importantly, understood Indian conditions—extreme heat, monsoon flooding, potholed roads, and overloaded vehicles.

JBM ECO-LIFE, launched in 2018, wasn't just India's first indigenous electric bus—it was purpose-built for Indian conditions. Two variants (9-meter and 12-meter) offered flexibility for different route requirements. The design philosophy was "tropicalization"—batteries with advanced thermal management for 45°C summers, elevated electronics for monsoon waterlogging, and reinforced suspension for Indian road conditions. Where Chinese buses failed in Indian trials due to overheating batteries or water ingress, JBM's buses ran reliably.

The technology stack JBM assembled was comprehensive. Lithium-ion batteries sourced initially through partnerships but with clear localization roadmaps. Power electronics that could handle India's unstable grid conditions. Regenerative braking systems that captured energy from frequent stops. Telematics for real-time monitoring. Air conditioning that didn't devastate range. Each component was optimized for total cost of ownership rather than just purchase price.

Early customer wins validated the strategy. Indore became the poster child—the city deployed JBM electric buses and saw immediate improvements in air quality and passenger satisfaction. The buses were quiet, smooth, and air-conditioned—luxuries in Indian public transport. Videos of passengers praising the experience went viral, creating pull demand from other cities. Mumbai, Delhi, and Hyderabad took notice.

The business model innovation was as important as the technology. JBM didn't just sell buses—they offered complete solutions. Financing packages that addressed state transport corporations' capital constraints. Maintenance contracts that guaranteed uptime. Training programs for drivers and technicians. Even charging infrastructure installation and management. This wasn't product sales; it was transport-as-a-service before the term became fashionable.

By 2018, the electric bus market was still tiny—fewer than 500 electric buses operated across India compared to 150,000 diesel buses. But the direction was clear. The government announced ambitious targets: 7,000 electric buses by 2020, 50,000 by 2025. Every major city drafted electric mobility plans. International funding from World Bank and Asian Development Bank specifically targeted electric bus procurement. The market was about to explode, and JBM had first-mover advantage.

The decision to focus exclusively on electric buses rather than electric cars or two-wheelers proved prescient. Buses offered better economics—higher utilization meant faster battery cost amortization. Government procurement meant fewer customers to manage. Public transport alignment meant policy support. And most importantly, the competitive landscape was manageable—unlike electric cars where every global automaker was competing, electric buses had fewer serious players.

The transformation wasn't without challenges. Developing electric vehicle capabilities required massive investment—hundreds of crores in R&D, new facilities, and talent acquisition. The technology was evolving rapidly, creating obsolescence risks. Early buses had teething problems—range anxiety, charging time concerns, and service network gaps. But JBM persisted, iterating quickly based on operational feedback.

What's remarkable in retrospect is the timing. JBM entered electric buses just as the market was about to transform from science project to commercial reality. Earlier would have been too early—battery costs were prohibitive and infrastructure nonexistent. Later would have been too late—established players would have locked up the market. The 2016-2018 period was the sweet spot, and JBM seized it completely.

V. Creating the EV Ecosystem: The "Well-to-Wheel" Strategy

While competitors were still debating build-versus-buy strategies for electric vehicle components, JBM was executing something far more ambitious: constructing an entire electric mobility ecosystem under one roof. They called it "JBM E-Verse"—a term that might sound like corporate buzzword bingo but represented genuine vertical integration at a scale unprecedented in India's automotive industry.

The ecosystem strategy emerged from a simple insight: electric buses weren't just vehicles with different powertrains; they were nodes in an integrated energy and transport system. The bus needed batteries, the batteries needed charging infrastructure, the charging infrastructure needed power management, and everything needed real-time monitoring and optimization. Controlling any single element meant being hostage to other suppliers. Controlling everything meant owning the customer relationship entirely.

JBM E-Verse began with batteries—the most expensive and critical component, representing 40-50% of an electric bus's cost. Rather than simply importing battery packs like competitors, JBM established comprehensive battery operations. This included cell sourcing partnerships with global suppliers, pack assembly facilities with automated production lines, battery management system development with proprietary algorithms, and even second-life applications for degraded batteries in stationary energy storage.

The battery strategy was particularly sophisticated. JBM recognized that different applications required different chemistry optimizations. City buses with frequent stops needed power-dense batteries for regenerative braking. Intercity buses needed energy-dense batteries for range. Depot charging could use different chemistry than opportunity charging. By 2020, JBM offered multiple battery configurations, each optimized for specific use cases—flexibility competitors couldn't match.

Charging infrastructure became the next frontier. JBM didn't just supply charging equipment; they became a Charge Point Operator, establishing and operating charging sites across major cities. This included depot electrification for bus operators, public charging stations for commercial vehicles, and even exploring battery swapping for specific applications. The infrastructure business had different economics than vehicle sales—recurring revenue, software margins, and network effects that improved with scale.

The power electronics capability deserves special attention. JBM developed in-house expertise in inverters, converters, and onboard chargers—components that seem mundane but determine vehicle efficiency and reliability. Their power electronics were designed for Indian conditions: wide voltage fluctuations, harmonic distortions, and grid instabilities that would fry imported components. This localization created a genuine technical moat.

Vertical integration extended beyond hardware into software and services. JBM's telematics platform monitored every bus in real-time—battery health, driver behavior, route optimization, and predictive maintenance. The data was staggering: thousands of parameters from hundreds of buses generating gigabytes daily. But the insights were valuable: which routes stressed batteries most, which drivers maximized regenerative braking, which charging patterns optimized battery life.

The "Well-to-Wheel" philosophy meant thinking about energy holistically. JBM ventured into solar panel integration for bus depots, reducing electricity costs and carbon footprint. They explored vehicle-to-grid applications where parked buses could supply power back to the grid during peak demand. They even developed energy storage systems for commercial and industrial customers, leveraging battery expertise beyond transportation.

Manufacturing scale became a competitive weapon. JBM's facility in Faridabad emerged as the world's largest integrated electric bus plant outside China—100 acres, 20,000 buses annual capacity, and complete vertical integration from battery assembly to final vehicle testing. The scale economics were powerful: shared overhead across multiple products, bulk purchasing power for raw materials, and learning curve benefits that reduced costs with each unit produced.

The ecosystem approach created powerful lock-in effects. Once a transport operator bought JBM buses, they typically bought JBM charging infrastructure for compatibility. Once they installed JBM chargers, they preferred JBM energy management systems for optimization. Once they used JBM telematics, switching to another vendor meant losing historical data and operational insights. The ecosystem wasn't just products—it was a platform that became stickier with use.

Financial implications of vertical integration were complex but compelling. Higher capital intensity meant lower returns initially, but better margins once scale achieved. Controlling the entire value chain meant capturing more value per bus sold—not just vehicle margins but battery margins, charging margins, and service margins. The lifetime revenue per bus could be 2-3x the initial sale price through batteries, charging, and maintenance over 10-12 years.

The innovation engine supporting this ecosystem was substantial. Five engineering and design centers across India employed hundreds of engineers. R&D spending exceeded 3% of revenue, high for an automotive company. Patents filed covered everything from battery cooling systems to charging algorithms. Partnerships with academic institutions created talent pipelines. The investment was massive but necessary—technology evolution in electric vehicles was too rapid to rely on external suppliers.

By 2020, JBM's ecosystem was fully operational. They could deliver a complete electric bus solution—from vehicles to charging infrastructure to operational support—as a turnkey package. No other Indian company had comparable capabilities. Even global players like BYD or Yutong would need local partners for various elements. JBM's vertical integration wasn't just operational efficiency; it was strategic positioning for market dominance.

The ecosystem strategy also provided resilience. When semiconductor shortages hit the auto industry in 2021, JBM's multiple product lines allowed component reallocation. When battery prices spiked, in-house assembly provided buffer. When charging standards evolved, integrated development ensured compatibility. The ecosystem wasn't just about capturing value—it was about managing risk in a rapidly evolving industry.

VI. The Government Push & Market Capture (2019–Present)

On August 16, 2023, Prime Minister Modi launched the PM-eBus Sewa Scheme with an allocation of ₹57,613 crore—the largest single commitment to electric buses globally. For JBM, this wasn't just another government program; it was validation of a decade-long bet. The scheme targeted deploying 10,000 electric buses across 169 cities, with integrated infrastructure support. JBM emerged as the biggest winner, capturing contracts worth ₹5,500 crore, approximately 65% of the total buses in major tenders.

The government's electric mobility push had been building since 2015's FAME (Faster Adoption and Manufacturing of Electric Vehicles) scheme, but PM-eBus Sewa was different in scale and structure. Rather than simple purchase subsidies, it offered comprehensive support: capital subsidies covering up to 60% of bus costs, operational support for 12 years, and infrastructure development funding. The program design seemed almost tailor-made for JBM's integrated ecosystem approach.

JBM's tender wins read like a sweep of India's major cities. Delhi: 1,500 buses. Mumbai: 2,100 buses. Bangalore: 921 buses. Hyderabad: 1,000 buses. Each win wasn't just about lowest price—state transport corporations evaluated total cost of ownership, technology roadmaps, and execution capability. JBM's existing operational track record—100 million electric kilometers already logged, 1 billion passenger trips served—provided credibility competitors couldn't match.

The Asian Development Bank partnership announced in early 2024 demonstrated international validation. ADB committed INR 3.6 billion for 650 electric buses in Haryana and Odisha, with JBM as the primary supplier. This wasn't just financing—ADB's technical due diligence validated JBM's technology and operations. International development banks backing JBM buses sent powerful signals to state governments and private operators.

The competitive dynamics during this period were fascinating. Tata Motors, despite being India's largest commercial vehicle manufacturer, struggled to match JBM's electric bus capabilities. Their electric buses, while technically competent, lacked the ecosystem integration. Ashok Leyland partnered with multiple technology providers but couldn't match JBM's vertical integration benefits. Olectra, backed by Chinese technology from BYD, faced skepticism amid anti-China sentiment. International players like Volvo and Mercedes found Indian price points unviable.

JBM's "1 billion e-kilometers" promise by 2025 seemed audacious when announced but now appears conservative. With 100 million kilometers already achieved and thousands of buses in the pipeline, the target will likely be exceeded. Each kilometer represents real-world validation—batteries performing in Indian heat, motors surviving monsoon floods, and passengers choosing electric buses over private vehicles. The operational data generated provides continuous improvement insights no amount of testing could replicate.

The market capture wasn't just about winning tenders—it was about shaping market structure. JBM pushed for gross cost contracts where operators paid per kilometer rather than buying buses outright. This model, common globally but new to India, aligned incentives—JBM profited from reliability and efficiency rather than just sales. State transport corporations preferred it as it converted capital expenditure to operational expenditure, easing budget constraints.

Government policy alignment extended beyond direct subsidies. GST rates favored electric vehicles (5%) over conventional vehicles (28%). State governments offered additional incentives—road tax waivers, parking fee exemptions, and priority lane access. Some cities mandated electric vehicle quotas for fleet operators. Each policy change expanded the addressable market and improved electric bus economics versus diesel alternatives.

The execution of large government contracts revealed JBM's operational maturity. Delivering hundreds of buses to a city required complex coordination—manufacturing scheduling, logistics planning, driver training, depot preparation, and charging infrastructure installation. JBM developed playbooks for rapid deployment, reducing delivery times from months to weeks. Their ability to scale operations faster than competitors created positive feedback loops—successful deployments led to more orders.

Financial structuring of government contracts was sophisticated. JBM partnered with financial institutions to offer lease financing, reducing upfront capital requirements for cash-strapped state transport corporations. They accepted deferred payment terms backed by government guarantees. They even explored innovative structures like battery-as-a-service, where batteries were leased separately from buses. Each structure addressed specific customer constraints while maintaining JBM's return targets.

The market share mathematics by 2024 was staggering. From virtually zero electric buses in 2018, India had over 7,000 operational, with JBM commanding 30-35% share. But more importantly, JBM dominated new orders—over 65% of recent large tenders. With the electric bus market expected to reach 50,000 units by 2030, JBM's current position suggests potential revenues exceeding ₹25,000 crore from buses alone, plus recurring revenues from charging and services.

Risk management during this growth phase was crucial. Government contracts meant payment delays and political risks. JBM diversified across states to avoid concentration. They maintained strong balance sheets to handle working capital needs. They invested in government relations and policy advocacy. They even developed private market segments—corporate shuttles, airport buses, and intercity operators—to reduce government dependence.

The international expansion began gaining momentum. Export orders transitioned from diesel to electric buses. Sri Lanka, Nepal, and Bangladesh showed interest in Indian electric bus technology. African markets, facing similar urbanization and pollution challenges, emerged as prospects. JBM's cost-competitive technology developed for India proved relevant for other emerging markets—a potential second growth vector beyond domestic demand.

VII. Technology & Innovation Engine

Inside JBM's Faridabad technical center, a team of engineers huddles around computer screens displaying thermal imaging from a bus battery pack undergoing stress testing—45°C ambient temperature, full acceleration loads, and rapid charging simultaneously. This scene, repeated across five engineering centers, represents JBM's transformation from a manufacturing company to a technology company that happens to manufacture.

The JBM ECO-LIFE platform—offered in 9-meter and 12-meter variants—represents five years of iterative development specifically for Indian conditions. Where global designs failed, JBM succeeded through obsessive localization. The batteries feature dual-circuit liquid cooling that maintains optimal temperature even in Delhi's 47°C summers. The air suspension adapts to passenger loads that routinely exceed design capacity by 50%. The regenerative braking system captures energy from India's stop-start traffic, extending range by 15-20%.

The "Think Global, Act Local" initiative goes deeper than marketing slogans. JBM's engineers studied global best practices—European safety standards, Japanese reliability processes, and Chinese manufacturing efficiency—then adapted them for Indian realities. The result: buses that meet European crash-test standards while surviving Indian pothole tests, achieving Japanese-level uptime while operating in Indian pollution levels, and matching Chinese costs while exceeding quality expectations.

The material innovation partnership with Jindal Stainless for lightweight, corrosion-resistant bus bodies exemplifies JBM's approach to technology development. Conventional buses use mild steel that rusts in monsoons and adds weight that reduces efficiency. JBM pioneered stainless steel monocoque construction—30% lighter yet stronger, corrosion-proof for 15+ year life, and recyclable at end-of-life. The weight savings alone improve range by 8-10%, critical for electric vehicles where every kilogram matters.

Battery technology remains the core innovation focus. JBM's battery labs test different cell chemistries—LFP (Lithium Iron Phosphate) for safety and longevity, NMC (Nickel Manganese Cobalt) for energy density, and emerging chemistries like sodium-ion for cost reduction. The proprietary battery management system uses machine learning algorithms trained on millions of kilometers of operational data to optimize charging patterns, predict failures, and extend battery life beyond industry standards.

The software stack powering JBM buses deserves recognition. The vehicle control unit runs proprietary firmware that orchestrates hundreds of sensors and actuators. The telematics platform processes real-time data from thousands of buses—location, speed, battery state, passenger count, and driver behavior. The fleet management system provides operators with actionable insights—route optimization suggestions, maintenance predictions, and energy consumption analytics. This isn't just hardware with software; it's software-defined vehicles where updates improve performance post-purchase.

R&D investment numbers tell the commitment story: over ₹150 crore annually, 300+ engineers across centers, 50+ patents filed, and 15+ university partnerships. But more impressive is the R&D focus—not just improving existing products but anticipating future requirements. Teams work on autonomous driving capabilities for fixed-route buses. Others explore hydrogen fuel cells as alternative zero-emission technology. Some investigate vehicle-to-grid applications where buses become mobile power banks.

The global engineering presence—36 countries—provides technology access and market intelligence. The European center tracks regulatory evolution and safety standards. The Japanese office monitors battery developments and quality processes. The Chinese team studies manufacturing automation and cost reduction. This distributed intelligence network ensures JBM isn't surprised by technology shifts or market changes.

Collaborative innovation accelerates development. The partnership with IIT Delhi created an electric vehicle research lab on campus. Collaboration with TERI (The Energy and Resources Institute) focuses on sustainable materials. Work with defense laboratories explores ruggedized electric vehicles for military applications. Each partnership expands capabilities while sharing costs and risks.

The testing and validation infrastructure rivals global OEMs. Environmental test chambers simulate everything from Ladakh's -40°C to Rajasthan's 50°C. Vibration test rigs replicate decades of Indian road conditions in weeks. Battery abuse testing pushes cells to failure to understand safety margins. Electromagnetic compatibility labs ensure electronics work despite India's electrical noise. This testing rigor explains why JBM buses achieve 95%+ uptime compared to 85% industry average.

Manufacturing technology adoption keeps pace with product innovation. Robotic welding ensures consistent quality across thousands of joints. Automated guided vehicles move components through assembly lines. Digital twins simulate production before physical implementation. Predictive maintenance prevents equipment failures. Industry 4.0 isn't buzzword compliance—it's operational reality delivering 20% productivity improvements annually.

The innovation culture extends beyond formal R&D. Shop floor workers suggest process improvements through kaizen programs. Service technicians feedback field issues for design updates. Even drivers provide input on ergonomics and usability. This distributed innovation model means improvements come from everywhere, not just engineers. The best ideas often emerge from unexpected sources—a mechanic's suggestion reduced battery installation time by 40%.

Intellectual property strategy balances protection with speed. Core technologies like battery management algorithms are patented. Manufacturing processes are kept as trade secrets. Software is continuously updated to stay ahead of copies. The approach recognizes that in fast-moving industries, execution speed matters more than perfect protection.

Future technology bets reveal strategic thinking. Autonomous capabilities make sense for fixed-route buses with dedicated lanes. Hydrogen fuel cells could serve long-distance routes where battery weight becomes prohibitive. Solar panels integrated into bus roofs could extend range and reduce charging frequency. Vehicle-to-grid could turn idle buses into revenue generators. Each bet is optionality for different future scenarios.

The technology transformation impacts talent requirements. JBM now recruits software engineers alongside mechanical engineers. Data scientists work beside welding specialists. Battery chemists collaborate with assembly line workers. The workforce evolution from blue-collar manufacturing to mixed-collar technology company creates cultural challenges but competitive advantages.

VIII. Financial Performance & Capital Allocation

The numbers tell a story of transformation: From ₹3,000 crore revenue in 2010 to ₹5,582 crore in 2024. From commodity component supplier to technology company commanding a ₹14,360 crore market capitalization. From industrial valuations to tech-like P/E ratio of 69.9. But understanding JBM's financial performance requires looking beyond headlines to the underlying drivers and capital allocation decisions that created this value.

The 2024 financial snapshot reveals a business at an inflection point. Revenue of ₹5,582 crore grew 9.17% year-over-year—solid but not spectacular. However, earnings of ₹220 crore jumped 12.91%, indicating margin expansion. The market values JBM at 10.6x book value, suggesting investors see assets that accounting doesn't capture—technology, market position, and growth optionality. The recent stock split from ₹2 to ₹1 face value improved liquidity, enabling broader retail participation.

Revenue composition has shifted dramatically. Traditional auto components still contribute 60% of sales but grow at GDP rates. Electric vehicles and new energy businesses contribute 40% but grow at 30%+ annually. By 2027, the mix will likely invert—electric mobility dominating revenues with legacy businesses providing stable cash flows. This transition explains the valuation premium—investors are paying for the future business, not the current one.

Margin structure reveals operational leverage. Gross margins expanded from 12% to 15% as product mix shifted toward higher-value electric buses. EBITDA margins reached 8%, impressive for a manufacturing business but with room for improvement as scale efficiencies materialize. Net margins of 4% seem thin but are expanding as interest costs decline and tax benefits from green investments flow through.

Capital allocation strategy has been aggressive but disciplined. Over ₹2,000 crore invested in electric vehicle capabilities since 2015—new factories, R&D centers, and technology development. Working capital intensity increased as government contracts require extended payment terms. But return on capital employed maintained at 15%+, suggesting investments are value-accretive despite the transition period.

The balance sheet strength enables growth ambitions. Debt-to-equity ratio of 0.8x is conservative for a capital-intensive business. Interest coverage of 4x provides cushion for additional leverage. Cash generation from legacy businesses funds new investments without excessive dilution. The financial flexibility means JBM can pursue opportunities without being constrained by capital availability.

Working capital management in government-dominated business requires sophistication. Receivable days extend to 120+ as state transport corporations delay payments. Inventory turns are lower as electric bus production requires longer cycles. But JBM manages through supply chain financing, government-backed receivables discounting, and milestone-based payment structures. The working capital intensity is structural but manageable.

Capital expenditure patterns reveal strategic priorities. ₹500 crore allocated for capacity expansion in electric buses. ₹200 crore for battery manufacturing capabilities. ₹150 crore for charging infrastructure. ₹100 crore for R&D facilities. The capex intensity will remain elevated through 2025-26 but should moderate as facilities reach optimal utilization.

The valuation puzzle deserves examination. At P/E of 69.9, JBM trades like a high-growth technology company rather than an auto manufacturer. Bulls argue this reflects electric vehicle leadership, government contract visibility, and international expansion potential. Bears worry about government dependence, competition intensifying, and technology obsolescence. The truth likely lies between—valuable but not without risks.

Peer comparison provides context. Tata Motors trades at P/E of 15, Ashok Leyland at 20, but both are predominantly conventional vehicle manufacturers. Global electric bus makers like BYD (P/E 25) or Proterra (before bankruptcy) show sector volatility. JBM's premium reflects India's growth potential and first-mover advantages but seems optimistic relative to global benchmarks.

Cash flow analysis reveals quality. Operating cash flows turned positive in 2022 after years of investment. Free cash flow remains negative due to growth capex but should inflect positive by 2025-26. Cash conversion cycles are extending but manageable. The business generates real cash, not just accounting profits—critical for sustainability.

Shareholder returns have been spectacular for early investors. The stock is up 400% over five years, 150% over three years, and 75% year-to-date. Dividend policy remains conservative—₹2 per share—as profits are reinvested for growth. But total shareholder returns including price appreciation exceed 50% annually over five years—venture capital-like returns from an industrial company.

The capital structure evolution shows maturation. Initial growth funded through internal accruals and debt. Recent equity dilution minimal despite massive investments. Preference for debt over equity reflects confidence in cash generation. The structure optimizes cost of capital while maintaining flexibility.

Segment reporting provides granular insights. Auto components: steady 8% growth, 12% EBITDA margins, cash generative. Electric vehicles: 40% growth, currently loss-making but approaching breakeven. Energy storage: nascent but high-margin potential. The portfolio provides both growth and stability—important for managing transition risks.

Forward-looking metrics suggest acceleration. Order book of ₹8,000+ crore provides 18-month revenue visibility. Pipeline of tenders worth ₹15,000 crore offers growth runway. International opportunities not yet quantified but potentially significant. The growth trajectory seems sustainable through 2027 at minimum.

Risk factors warrant consideration. Customer concentration with government at 70%+ of electric bus sales. Technology evolution potentially making current investments obsolete. Competition intensifying as market grows. Regulatory changes affecting economics. Input cost inflation pressuring margins. Each risk is real but manageable with proper hedging strategies.

IX. Playbook: Business & Strategic Lessons

The JBM story offers a masterclass in how emerging market companies can transcend their origins. The playbook isn't about any single brilliant move but rather a series of interconnected strategies executed over decades. For founders and investors studying industrial transformation, JBM's journey from component supplier to electric vehicle leader provides actionable insights rarely found in business school cases.

The Power of Vertical Integration in Emerging Markets works differently than in developed economies. Where Western companies often outsource for flexibility, JBM integrated for control. In India's unreliable supplier ecosystem, vertical integration wasn't just about margins—it was about existence. When battery suppliers couldn't guarantee quality, JBM built battery plants. When charging infrastructure didn't exist, JBM became an infrastructure company. This isn't textbook strategy; it's survival evolution that created competitive moats.

Consider how JBM's integration strategy evolved: Starting with simple components where integration meant cost savings, moving to complex assemblies where integration meant quality control, then to complete vehicles where integration meant customer ownership, and finally to entire ecosystems where integration meant market definition. Each stage built on previous capabilities while opening new opportunities. The lesson: vertical integration in emerging markets isn't binary but evolutionary.

Timing Market Transitions requires patience and preparation. JBM didn't randomly pivot to electric buses in 2018—they prepared for years through international partnerships, technology investments, and capability building. When the market inflected, they were ready. But equally important was what they didn't do—chase every trend. No electric cars despite Tesla hype. No two-wheelers despite huge markets. Focus on buses where their capabilities aligned with market needs.

The timing lesson extends deeper. JBM entered each new segment just as economics became viable but before competition intensified. Sheet metal when Indian auto manufacturing took off. Modules when global OEMs arrived. Electric buses when battery costs dropped below viability thresholds. The pattern: prepare during technology development, enter during early commercialization, and dominate during scaling. Too early means bleeding capital; too late means competing on price.

Building Competitive Moats Through Ecosystem Play represents modern strategic thinking. JBM didn't just build better buses—they created customer lock-in through ecosystem dependence. Once a city adopts JBM buses, they need JBM charging infrastructure for compatibility, JBM service networks for maintenance, and JBM software for operations. Switching costs compound with each additional element. The moat isn't any single product but the integration between products.

ESG as Strategy, Not Compliance differentiates JBM from traditional manufacturers. Gender action plans that put women in welding roles. Safety protocols exceeding international standards. Environmental initiatives beyond regulatory requirements. These aren't cost centers but talent attraction tools, customer differentiation factors, and regulatory risk mitigation. In markets where ESG is often greenwashing, authentic commitment creates real advantages.

The human capital strategy deserves emphasis. JBM invests in multi-year training programs for engineers. They sponsor employees for international certifications. They create career paths from shop floor to management. In India's tight talent market, developing rather than just hiring talent creates loyalty and capability advantages. The 30,000+ employees aren't just workers but institutional knowledge repositories.

Managing Conglomerate Complexity While Maintaining Focus is JBM's hidden capability. With 60+ facilities, multiple business lines, and thousands of products, complexity could destroy value. But JBM maintains focus through clear portfolio rules: every business must leverage existing capabilities, serve automotive or adjacent markets, and generate cash or strategic value. Diversification within boundaries rather than unlimited expansion.

Navigating Government Policy and Public Sector Sales requires different skills than B2B sales. JBM mastered the art of aligning with policy objectives, building relationships across political parties, and maintaining reputation through execution excellence. They don't just respond to tenders—they shape tender specifications through technical committees. They don't just serve government customers—they become policy partners in achieving national objectives.

The government relations strategy is sophisticated. JBM maintains relationships at multiple levels—national policymakers for framework policies, state governments for implementation, and city administrators for operations. They invest in policy research, participate in standard-setting committees, and provide technical expertise to regulators. This isn't lobbying but collaborative policy development that happens to benefit JBM's position.

The "Frugal Engineering" Approach to Cost Leadership distinguishes Indian innovation. JBM's electric buses cost 50% less than European equivalents while meeting similar performance standards. This isn't about cutting corners but fundamental redesign for cost optimization. Smaller batteries with better thermal management rather than larger batteries with basic cooling. Mechanical solutions where others use electronics. Local materials where others import. The result: products affordable for emerging markets but competitive globally.

Capital allocation discipline despite growth ambitions shows maturity. JBM could have raised massive equity funding to accelerate expansion. Instead, they grew at sustainable rates funded by internal cash flows and modest debt. This preserved founder control, avoided dilution, and enforced discipline. The lesson: in capital-intensive businesses, the cost of capital matters more than growth rates.

International Expansion Through Capability Export rather than just product export creates sustainable advantages. JBM doesn't just sell buses abroad—they transfer manufacturing technology, establish local partnerships, and develop market-specific products. The international strategy builds on domestic strengths while adapting to local requirements. This isn't colonial export but collaborative development that creates win-win outcomes.

The partnership philosophy permeates everything. Rather than acquiring capabilities, JBM partners to access them. Rather than competing with global players, JBM collaborates selectively. Rather than defending against new entrants, JBM co-opts them through joint ventures. The result: faster capability building, lower capital requirements, and reduced execution risks. But partnership management—aligning incentives, managing conflicts, and capturing value—becomes a core competency itself.

Risk management in volatile markets requires portfolio thinking. JBM's mix of stable component businesses and high-growth electric vehicles provides balance. Geographic diversification across Indian states and international markets reduces concentration. Customer diversification across government and private reduces policy dependence. Technology diversification across battery-electric and potentially hydrogen reduces obsolescence risk. The portfolio approach enables aggressive bets while maintaining overall stability.

X. Bear vs. Bull Case & Competitive Analysis

The investment community remains sharply divided on JBM. At investor conferences, you'll find tables of believers citing the electric vehicle revolution and tables of skeptics questioning valuations. Both sides make compelling arguments, and understanding the bear-bull debate is crucial for anyone evaluating JBM's future.

The Bull Case starts with market dominance in a massive growth market. India needs 200,000 electric buses by 2030 to meet climate commitments—current penetration is under 10,000. At 35% market share, JBM could deliver 70,000 buses worth ₹35,000 crore in vehicle sales alone. Add batteries, charging, and services over the 12-year bus life, and the revenue potential exceeds ₹100,000 crore. The PM-eBus Sewa Scheme provides policy visibility through 2036. State transport corporations have no choice but to electrify given pollution levels and operating cost advantages.

The moat appears unassailable. JBM's integrated ecosystem can't be replicated quickly—it took them eight years and ₹2,000 crore to build. Competitors face a chicken-and-egg problem: they need scale for economics but economics for scale. Meanwhile, JBM's learning curve advantages compound—each bus delivered improves their data, processes, and costs. The 100 million e-kilometers already logged provide operational insights no amount of testing can replicate.

International expansion offers a second growth vector. Electric bus markets in Southeast Asia, Africa, and Latin America are 3-5 years behind India. JBM's frugal engineering approach—50% lower costs than Western alternatives—positions them perfectly for these price-sensitive markets. Export revenues could match domestic revenues by 2030. Unlike Chinese competitors facing geopolitical headwinds, Indian companies benefit from neutral positioning.

The technology platform extends beyond buses. The same batteries, power electronics, and software powering buses can serve trucks, tractors, and industrial vehicles. The energy storage market for grid stabilization and renewable integration is nascent but massive. Vehicle-to-grid applications could turn bus fleets into distributed power plants. Each adjacency leverages existing capabilities while opening new TAMs (Total Addressable Markets).

Valuation might actually be reasonable given growth potential. At ₹14,360 crore market cap and potential ₹100,000 crore revenue opportunity, JBM trades at 0.14x potential sales—cheap for a technology company. Earnings will inflect dramatically as scale efficiencies materialize and lifecycle revenues compound. Comparable global electric vehicle companies trade at higher multiples despite slower growth. The India premium for fastest-growing major economy seems justified.

The Bear Case centers on unsustainable valuations and execution risks. P/E of 69.9 for a manufacturing company with 4% net margins seems detached from reality. The market is pricing in perfect execution for a decade—any disappointment could trigger massive derating. The stock has already appreciated 400% in five years; how much good news is already priced in?

Government dependence creates existential risks. Over 70% of electric bus sales come from government contracts notorious for payment delays, renegotiations, and political interference. The PM-eBus Sewa Scheme could be modified or delayed by future governments. State transport corporations are financially weak—many can't pay for diesel buses, let alone expensive electric buses. What happens when subsidies end or reduce?

Competition is intensifying rapidly. Tata Motors is investing heavily in electric vehicles and has deeper pockets. Ashok Leyland partnered with Switch Mobility brings international technology. BYD and Yutong from China have global scale advantages. New entrants like TVS and Mahindra are exploring electric buses. Tesla or Rivian could enter with breakthrough technology. JBM's first-mover advantage is real but temporary.

Technology risk looms large. Battery technology evolves rapidly—solid-state batteries could obsolete current lithium-ion investments. Hydrogen fuel cells might prove superior for heavy vehicles. Autonomous vehicles could change business models entirely. JBM's ₹2,000 crore investment in current technology could become stranded assets. The pace of change in electric vehicles makes long-term competitive advantages questionable.

Execution challenges multiply with scale. Delivering thousands of buses requires massive working capital. Quality issues could destroy reputation overnight. Managing government relationships across political parties and states is complex. International expansion requires local knowledge and partners. The company that excelled at hundreds of buses annually might struggle with thousands.

Competitive Benchmarking reveals JBM's unique position but also vulnerabilities:

Tata Motors brings massive resources—₹40,000 crore revenue, global R&D centers, and Jaguar Land Rover technology access. Their electric bus offering is improving rapidly. But they lack JBM's singular focus and integrated ecosystem. Tata treats electric buses as one segment among many; for JBM, it's existential.

Ashok Leyland with Switch Mobility combines Indian manufacturing with British technology. They're targeting premium segments with advanced features. But their higher costs make them uncompetitive in price-sensitive government tenders. The partnership structure also creates decision-making complexity.

BYD India has global scale—they're the world's largest electric bus manufacturer. Their technology is proven across continents. But anti-China sentiment, localization requirements, and higher costs limit their Indian market access. They're winning some contracts but struggling to scale.

Olectra Greentech partners with BYD for technology while maintaining Indian ownership. They're JBM's most direct competitor with similar cost structures. But they lack vertical integration, depending on BYD for critical components. Their 15% market share makes them credible but not dominant.

The competitive dynamics suggest a maturing market structure. JBM will likely maintain leadership but at lower margins as competition intensifies. Market share might decline from 35% to 25% but on a much larger base. Pricing power will erode forcing continuous cost reduction. Technology differentiation will matter more requiring sustained R&D investment.

The verdict depends on time horizon and risk tolerance. Short-term traders should beware—the stock is priced for perfection and vulnerable to disappointment. Long-term investors might find opportunity—the electric vehicle transition is real and JBM is positioned to capture value. The bear and bull cases aren't mutually exclusive; both could be right at different times.

XI. The Road Ahead: Future Strategy & Vision

Standing at JBM's Faridabad facility, watching electric buses roll off the assembly line destined for cities across India and beyond, you can feel the company at an inflection point. The next decade will determine whether JBM becomes India's BYD—a global electric vehicle champion—or remains a successful but regional player. The strategic choices being made today in boardrooms and engineering centers will echo for decades.

International expansion has moved from aspiration to execution. JBM's buses now operate in Nepal, Sri Lanka, and Bangladesh—markets with similar operating conditions but less competitive intensity. The real prize lies in Africa and Latin America, where rapid urbanization creates massive public transport demand but limited electric vehicle supply. JBM is establishing local assembly partnerships in Kenya and exploring opportunities in Nigeria, Ethiopia, and South Africa. The strategy isn't just export but localization—knockdown kits assembled locally creating jobs and government support.

The technology roadmap reveals ambitious bets on multiple futures. Artificial intelligence integration is advancing from concept to deployment. Predictive maintenance algorithms now anticipate component failures days in advance. Route optimization systems reduce energy consumption by 12%. Driver assistance features improve safety and efficiency. But the real AI opportunity lies in autonomous capabilities—fixed-route buses with dedicated lanes are ideal for automation. JBM is testing Level 2 autonomy with plans for Level 4 by 2027.

The hydrogen question can't be ignored despite JBM's battery-electric focus. For routes exceeding 300 kilometers, hydrogen fuel cells offer advantages—faster refueling, lighter weight, and longer life. JBM is hedging through a partnership with Indian Oil Corporation to develop hydrogen buses for intercity routes. The investment is modest—₹50 crore—but provides optionality if hydrogen economics improve. The strategy: dominate battery-electric for urban routes while exploring hydrogen for long-distance.

Vehicle-to-Grid (V2G) technology could transform electric buses from cost centers to profit centers. A typical bus sits idle 6-8 hours daily with 200+ kWh of battery capacity. At peak electricity rates of ₹10/kWh, each bus could generate ₹2,000 daily by feeding power back to the grid. For a fleet of 1,000 buses, that's ₹60 crore annual revenue from assets already owned. JBM is piloting V2G with utilities in Delhi and Mumbai. If successful, it changes electric bus economics fundamentally.

Manufacturing scale ambitions are staggering. Current capacity of 20,000 buses annually will expand to 50,000 by 2027. But this isn't just replicating existing facilities. Next-generation factories will use digital twins for virtual commissioning, collaborative robots for flexible automation, and AI-powered quality control. The goal: reduce manufacturing costs by 30% while improving quality. The investment required—₹3,000 crore—is massive but necessary for global competitiveness.

The brand building challenge is unique. JBM is well-known in B2B circles but invisible to consumers who ride their buses daily. This is changing through subtle branding on buses, digital campaigns highlighting sustainability impact, and partnerships with environmental organizations. The goal isn't consumer sales but policy influence—when citizens demand electric buses, governments respond. JBM is investing ₹100 crore annually in brand building, unusual for a B2B company but strategic for market development.

Adjacency expansion follows logical progression. Electric trucks for last-mile delivery leverage the same powertrain technology. School buses offer a massive market with different duty cycles. Agricultural equipment electrification aligns with rural development priorities. Each adjacency is evaluated through three filters: technology leverage from existing capabilities, market size exceeding ₹5,000 crore, and competitive dynamics favoring new entrants.

The partnership ecosystem continues expanding. Collaboration with Maruti Suzuki explores small electric commercial vehicles. Joint venture with a European company (unnamed due to NDAs) targets advanced battery technology. Strategic investment in startups working on charging infrastructure, fleet management software, and battery recycling. The approach: build core capabilities internally while accessing complementary technologies through partnerships.

Capital allocation for growth requires balance. JBM needs ₹5,000 crore over five years for capacity expansion, technology development, and working capital. The funding strategy combines internal accruals (₹2,000 crore), debt financing (₹2,000 crore), and potential equity raise (₹1,000 crore). The equity component remains uncertain—founders resist dilution but recognize capital needs. An IPO of the electric vehicle subsidiary is under consideration, potentially unlocking value while maintaining control.

What Success Looks Like in 2030 is becoming clear through strategic planning exercises. JBM envisions: 50,000 electric buses operational globally with JBM supplying 40%, revenue exceeding ₹25,000 crore with 15% EBITDA margins, international sales comprising 40% of total revenue, and energy storage and adjacent businesses contributing 30% of profits. The stock market value could exceed ₹50,000 crore if execution succeeds.

But success isn't just financial metrics. JBM's vision includes: preventing 10 million tons of CO2 emissions annually, providing safe, comfortable transport for 100 million daily passengers, creating 50,000 direct and indirect jobs, and establishing India as a global electric vehicle manufacturing hub. The societal impact amplifies financial returns—purpose-driven growth that attracts talent, customers, and investors.

The risks are real and acknowledged. Technology disruption could obsolete current investments. Chinese competitors could enter aggressively if geopolitical tensions ease. Government support could waver with political changes. Execution complexity could overwhelm management capacity. But JBM's track record suggests they'll adapt and overcome as they have for four decades.

The next chapter is being written now. Every strategic decision—which technology to develop, which market to enter, which partner to choose—shapes the outcome. JBM stands at the intersection of India's development needs and global sustainability imperatives. The opportunity is massive, the competition is intensifying, and the stakes couldn't be higher.

XII. Epilogue & Final Reflections

The JBM story defies conventional business wisdom. A family-run conglomerate from North India shouldn't be able to out-innovate global giants. A component supplier shouldn't successfully become an OEM. A traditional manufacturer shouldn't transform into a technology company. Yet JBM did all three, creating ₹14,000 crore of market value while revolutionizing Indian public transport.

The biggest surprise isn't JBM's success but how they achieved it. No massive venture funding or celebrity CEO. No breakthrough technology or first-mover advantage in absolute terms. Instead, methodical capability building over decades, strategic patience to wait for the right moment, and operational excellence in execution. JBM proves that industrial transformation doesn't require Silicon Valley playbooks—emerging market companies can chart their own paths.

For founders contemplating pivoting established businesses, JBM offers crucial lessons. First, pivots work best when building on existing capabilities rather than abandoning them. JBM's component expertise enabled bus manufacturing which enabled electrification. Second, timing matters more than being first—prepare during technology development but commercialize when economics align. Third, ecosystem control creates competitive advantages that pure technology doesn't—JBM's integration is their moat.

The India opportunity extends beyond JBM. Manufacturing for the world from India is finally becoming reality after decades of promise. The combination of scale domestic market, engineering talent, government support, and cost advantages creates unique conditions. Electric vehicles are just the beginning—renewable energy, semiconductors, and advanced materials offer similar potential. JBM's success validates the India manufacturing story.

Why timing and government alignment matter becomes clear through JBM's journey. They entered electric buses just as battery costs dropped below viability thresholds, pollution became a political priority, and funding became available. Earlier would have meant bleeding capital on immature technology. Later would have meant competing against entrenched players. The lesson: in regulated industries, swimming with policy currents beats swimming against them.

The sustainable transportation future looks increasingly electric, connected, and shared. Electric powertrains will dominate urban transport within a decade. Connected vehicles will optimize routes and reduce deadheading. Shared mobility will improve asset utilization. JBM is positioned at the confluence of these trends—their buses are electric, their telematics enable connectivity, and their business model supports sharing.

But the future won't be linear progression from today. Breakthrough technologies could disrupt current trajectories. Social preferences might shift from ownership to access. Urbanization patterns could change post-pandemic. Climate events might accelerate or delay transitions. JBM's adaptability—shown through multiple pivots—matters more than any specific strategy.

The human element deserves final emphasis. Behind every strategic decision and technology breakthrough are people—engineers working late to solve battery cooling problems, workers taking pride in building buses that reduce pollution, and managers navigating complex stakeholder relationships. JBM's culture of continuous improvement, customer focus, and social responsibility enables everything else.

The unanswered questions remain fascinating. Will JBM become a global champion or remain regionally focused? Can they maintain leadership as competition intensifies? Will adjacent bets in hydrogen and autonomous vehicles pay off? How will they manage succession as founders age? Will India's electric vehicle ambitions materialize at projected scale? These uncertainties make JBM's next decade as interesting as their last four.

For investors, JBM represents a complex proposition. The growth opportunity is real and massive. The execution capabilities are proven. The market position is strong. But valuations reflect high expectations, risks are material, and competition is intensifying. This isn't a simple buy-or-sell decision but requires nuanced analysis of time horizons, risk tolerance, and belief in India's development trajectory.

The broader implications transcend JBM. Their success demonstrates that emerging market companies can lead global technology transitions. That manufacturing still matters in a digital age. That purpose-driven businesses can create superior returns. That patient capital and long-term thinking beat quarterly optimization. These lessons apply beyond India and beyond automotive.

As our episode concludes, we return to that Faridabad factory where this began. The buses rolling off assembly lines today will transport millions of Indians for the next decade. They'll reduce pollution in cities where children struggle to breathe. They'll provide dignified transport for people who've never experienced air-conditioned commutes. They'll generate data that improves future designs. Each bus is simultaneously a product, a service, and a platform for India's sustainable development.

The JBM story isn't finished—arguably, it's just beginning. The electric vehicle revolution is in early innings. The energy transition will take decades. India's urbanization has centuries to run. JBM's transformation from cylinder manufacturer to electric vehicle leader took 40 years. Their transformation into whatever comes next starts now.

What makes JBM worthy of study isn't just their success but what it represents—the possibility of industrial transformation, the power of strategic patience, and the potential for emerging market companies to shape global industries. In a world obsessed with software and services, JBM reminds us that making physical things that solve real problems still matters. Their buses carry millions of people daily. Their components enable mobility for billions. Their vision of sustainable transport might help save the planet.

That's a story worth understanding, whether you're an investor evaluating opportunities, a founder building companies, or simply someone interested in how businesses evolve. JBM's journey from auto components to electric buses isn't just corporate history—it's a blueprint for industrial transformation in the 21st century.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube