ITD Cementation India: Building India's Infrastructure Backbone

I. Introduction & Cold Open

Picture this: 30 meters beneath Kolkata's bustling streets, where the air is thick with humidity and the ground water pressure threatens to burst through at any moment, engineers are carving out what will become one of India's deepest metro stations. The year is 2019, and ITD Cementation's teams are working round the clock at Esplanade, creating a five-tier underground marvel spanning 4.3 lakh square feet. Above ground, the city moves on, oblivious to the engineering ballet playing out below—a dance that ITD Cementation has been perfecting for over nine decades.

Today, ITD Cementation India stands as a ₹13,000+ crore market cap infrastructure giant, delivering ₹9,258 crore in revenue while providing end-to-end EPC services across India's most critical infrastructure projects. But here's what makes this story extraordinary: this is a company that has survived the British Empire's collapse, navigated post-independence nationalism, endured five different foreign owners, and emerged as Thailand's strategic gateway to India's infrastructure boom.

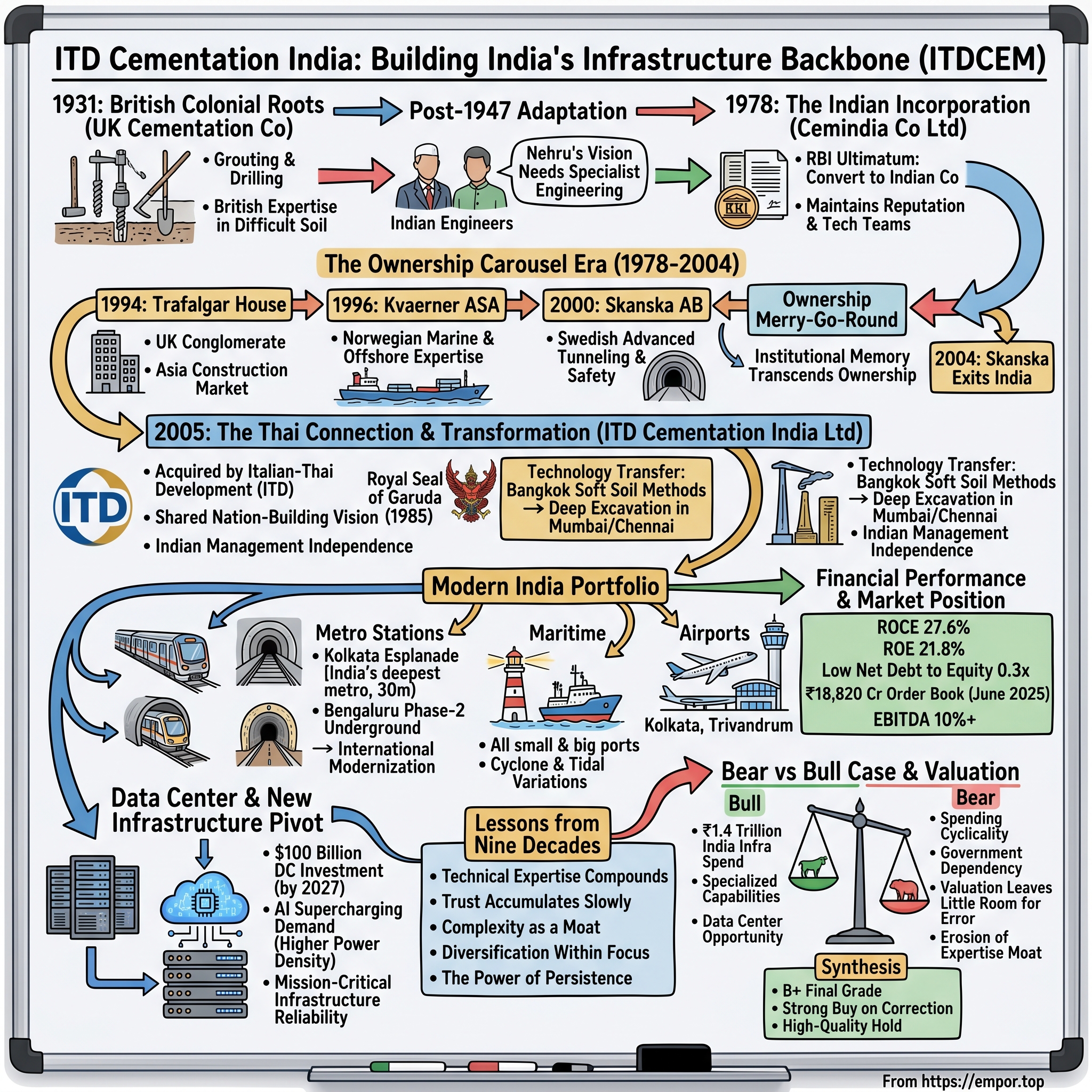

The company's DNA traces back to 1931, when The Cementation Company Limited of UK established its Indian branch for "extensive grouting and drilling works to hydraulic structures"—colonial-era engineering speak for the unglamorous but essential work of making things stand up straight and not sink into the ground. What started as a British firm helping build the Raj's infrastructure would transform into something far more remarkable: a testament to corporate resilience across three distinct empires—British, Indian, and now Thai.

This is not just another infrastructure company story. It's the tale of how specialized engineering knowledge, painstakingly accumulated over decades of working in India's challenging soil conditions, became the foundation for something much larger. While flashier tech companies grab headlines, ITD Cementation has been quietly mastering the art of making India's ambitious infrastructure dreams physically possible—from metro systems that snake beneath ancient cities to airports that connect the subcontinent to the world.

The central question isn't how a construction company survived for 90 years—plenty have done that. The real mystery is how a firm managed to maintain its technical edge and market position through the chaos of decolonization, the musical chairs of multinational ownership, and the complete transformation of India's economy. The answer lies in understanding that in infrastructure, reputation compounds over decades, technical expertise creates genuine moats, and sometimes the best business strategy is simply refusing to die.

II. The British Colonial Roots (1931–1978)

The story begins not in a boardroom but in the muddy foundations of pre-independence India. When The Cementation Company Limited arrived from Britain in 1931, India was still the jewel in the crown, and British firms dominated the engineering landscape. Cementation wasn't building monuments to empire—they were doing something far more essential: figuring out how to make structures stand in India's notoriously challenging geology.

Consider the technical challenge: India's soil conditions range from the alluvial plains of the Ganges—where you can dig 100 meters and still not hit bedrock—to the hard granite of the Deccan plateau. The monsoons bring water tables that fluctuate wildly. The company's early specialty in grouting and drilling for hydraulic structures meant they were literally injecting cement into the earth to create stable foundations where none existed naturally. This wasn't glamorous work, but it was the kind of expertise that would prove invaluable when India began its infrastructure journey.

Post-independence in 1947 changed everything. Suddenly, British firms weren't just foreign—they were symbols of colonial exploitation. Yet Cementation survived where others fled or were nationalized. Why? Because newly independent India had grand infrastructure ambitions but limited technical expertise in specialized foundation engineering. Nehru's vision of modern India needed dams, bridges, and industrial plants, all requiring the exact expertise Cementation had accumulated.

The company adapted brilliantly to the new reality. They began training Indian engineers, transferring technology that had previously been closely guarded. By the 1960s, Cementation wasn't seen as a British firm operating in India but as an Indian firm with British parentage—a crucial distinction in the License Raj era. They worked on projects that defined modern India: the foundations for steel plants in Bhilai and Rourkela, hydroelectric projects in the Himalayas, ports along both coasts.

But by 1978, the Reserve Bank of India's patience with foreign ownership had limits. The RBI issued an ultimatum: convert to an Indian company or cease operations. On paper, this looked like the end of the British chapter. In reality, it was just the beginning of Cementation's transformation. The company incorporated as Cemindia Company Limited in 1978, maintaining its technical teams, project pipeline, and most importantly, its reputation. The British had left, but the engineering knowledge remained—now thoroughly Indianized and ready for the next phase.

This period established a pattern that would define ITD Cementation's future: the ability to separate ownership from operations, to maintain technical continuity through corporate upheaval. In infrastructure, where projects span years and reputations take decades to build, this stability amid change would prove to be their greatest asset.

III. The Ownership Carousel Era (1978–2004)

If the British period was about establishing roots, the next quarter-century was about proving that those roots could survive being transplanted—repeatedly. Between 1978 and 2004, Cemindia would have five different owners, each bringing their own vision, capital, and occasionally, chaos. Yet somehow, the company not only survived but expanded its capabilities with each transition.

The carousel began spinning in 1994 when Trafalgar House, the British conglomerate that owned everything from Cunard cruise lines to the Ritz Hotel, acquired Cemindia, renaming it Trafalgar House Construction India Limited. Trafalgar House wasn't particularly interested in Indian foundation engineering—they wanted a foothold in what they saw as Asia's next big construction market. But before they could execute any grand strategy, they themselves were acquired.

Enter the Norwegians. In 1996, Kvaerner ASA, the Norwegian engineering giant, swallowed Trafalgar House whole. Suddenly, Cemindia—now renamed Kvaerner Cementation India Limited—found itself part of a Scandinavian engineering empire. Kvaerner brought something new: expertise in offshore engineering and complex marine structures. Under Norwegian ownership, the Indian operations began working on ports and marine facilities, adding saltwater to their repertoire of challenges.

But Kvaerner's global ambitions exceeded their financial capacity. By 2000, they were divesting non-core assets, and Swedish construction giant Skanska AB picked up the Indian operations. Another rebrand, another set of corporate priorities. Skanska, however, was different. They saw India not as a sideshow but as a strategic market. They invested in training, brought in advanced tunneling technology, and most importantly, gave the Indian management real autonomy.

During this ownership merry-go-round, something remarkable happened at the operational level. While corporate parents changed, the core team—the engineers who knew every soil type from Kashmir to Kanyakumari, the project managers who had relationships with every state PWD, the workers who had perfected techniques for monsoon construction—remained. They became the institutional memory that transcended ownership.

Each owner inadvertently added layers to the company's capabilities. Trafalgar House brought international project management standards. Kvaerner added marine and offshore expertise. Skanska contributed advanced tunneling technology and safety protocols that exceeded Indian standards. By 2004, when Skanska decided to exit India to focus on more developed markets, they were selling not just a construction company but a unique amalgamation of British colonial knowledge, Norwegian marine expertise, and Swedish engineering precision—all thoroughly Indianized through decades of local execution.

The company had also learned a meta-skill: how to be acquired. They knew how to present themselves to new owners, maintain operational independence, extract technical knowledge, and prepare for the inevitable next transition. This would prove invaluable when the Thais came calling.

IV. The Thai Connection & Transformation (2004–2015)

The arrival of Italian-Thai Development (ITD) in 2004 wasn't just another ownership change—it was a meeting of kindred spirits separated by geography but united by history. To understand why this acquisition finally stuck, we need to first understand ITD's own origin story, which reads like a movie script.

In 1954, an Italian engineer named Giorgio Berlingieri and a Thai entrepreneur named Chaijudh Karnasuta met over a salvage operation for a sunken dredger in the Chao Phraya River. Their partnership worked so well that by 1958, they had founded Italian-Thai Development, combining Italian engineering prowess with Thai market knowledge. Over the next four decades, ITD built much of modern Thailand—airports, highways, mass transit systems, industrial plants. By 2004, they weren't just contractors; they were nation-builders wearing hard hats.

ITD saw in the Indian operations something familiar: a company that had survived colonialism, adapted to local conditions, and accumulated irreplaceable ground-level expertise. The acquisition from Skanska wasn't about financial engineering or market entry—it was about finding a platform that could execute ITD's vision for India. The company was renamed ITD Cementation India Limited in 2005, and for the first time in decades, it had an owner who understood infrastructure as a calling, not just a business.

The Thai parentage brought unexpected advantages. Unlike European owners who saw India through a "developing market" lens, ITD understood the realities of building in monsoons, dealing with complex bureaucracies, and managing projects where ground conditions could change every hundred meters. They had built Bangkok's Skytrain through flooding streets and Jakarta's towers on swampland. India's challenges weren't exotic—they were familiar variations on Southeast Asian themes. More than just another owner, ITD brought credibility through its own royal connections. ITD had been awarded the Royal Seal of the Garuda by His Majesty the King of Thailand on 22nd November 1985—Thailand's highest corporate honor, granted only to companies demonstrating exceptional service to the nation. This wasn't corporate window dressing; in Southeast Asia, royal endorsement translates to trust, access, and the ability to navigate complex government relationships.

The technology transfer was immediate and practical. ITD brought techniques for building in Bangkok's notoriously soft soil—methods for deep excavation below water tables, concrete formulations that could withstand tropical humidity, project management systems designed for monsoon disruptions. The Indian operations absorbed these like a sponge, adapting Thai solutions to Indian problems. When Mumbai needed deep excavations for metro stations, the teams applied Bangkok Skytrain techniques. When Chennai's soil proved unstable, they used Thai ground improvement methods.

But the real transformation was cultural. For the first time, ITD Cementation's Indian management had genuine autonomy. ITD's philosophy was simple: they provided capital, technology, and strategic direction, but execution was local. The parent company held approximately 47% of equity—enough to control but not enough to dominate. This balance created an unusual dynamic: a subsidiary with real independence backed by a parent with real expertise.

By 2015, a decade into Thai ownership, ITD Cementation had transformed from a foreign subsidiary cycling through owners into something unique: an Indian company with Thai DNA, combining nine decades of Indian field experience with Southeast Asian engineering innovation. The company had found its forever home not in Europe or America, but in another Asian nation that understood infrastructure as nation-building. The ownership carousel had finally stopped spinning.

V. Building Modern India: The Project Portfolio

To understand ITD Cementation's true capabilities, forget the corporate timeline and focus on what they've actually built. The Esplanade Metro Station in Kolkata, completed in 2019, tells you everything about their technical evolution. This isn't just a deep station—at 30 meters below ground, it's an engineering response to Kolkata's unique challenge: building modern infrastructure beneath a colonial city while the Hooghly River's water table presses against every wall. The five-tier structure required continuous dewatering, specialized waterproofing, and construction techniques that allowed the city to function normally just meters above active excavation.

The numbers are staggering: 4.3 lakh square feet of underground space, but the real achievement was maintaining structural integrity while boring through layers of Kolkata's notoriously unstable alluvial soil. Every meter down increased water pressure exponentially. The solution involved freezing soil sections, creating temporary ice walls to hold back groundwater—a technique borrowed from their Thai parent's experience building Bangkok's underground, adapted for Kolkata's specific geology.

Their metro portfolio reads like a tour of India's urban ambitions. The Underground Yard Cum Depot for Kolkata Metro's Airport Line earned a Chairman Commendation Award not for its size but for its complexity—imagine building a massive maintenance facility entirely underground, with tracks, service bays, and administrative offices, all below the water table. In Bangalore, they're constructing Phase-2 underground sections, navigating not just soil but the city's infamous traffic while ensuring zero disruption to the IT corridor above.

The airport modernization work showcases a different skill set. At Kolkata Airport, they weren't just pouring concrete but integrating complex systems—ensuring runways could handle new aircraft loads, building terminals that could process millions while maintaining security protocols, all while keeping the airport operational. The Trivandrum International Airport project required working in Kerala's coastal environment, where salt air corrodes standard materials and monsoons can flood a construction site in hours.

But it's in maritime engineering where their eight-decade expertise truly shows. "Working in all small & big ports" undersells what this means: building structures that must withstand cyclones, tidal variations, and constant salt water exposure while supporting massive loads. Port construction isn't just civil engineering—it's a battle against the ocean itself. Foundations must go deep enough to hit bedrock through underwater silt, concrete must be specially formulated to resist salt intrusion, and every structure must account for forces most buildings never face.

The technical capabilities compound across projects. The deep excavation expertise from metro work applies to port foundations. The water management techniques from marine projects help with underground construction. The project management skills from keeping airports operational during renovation transfer to maintaining city traffic flow during metro construction. Each project doesn't just add to the portfolio—it adds to the institutional knowledge that makes the next project possible.

What emerges from this portfolio isn't just a construction company but an organization that has solved India's hardest infrastructure problems. They're not building in greenfield sites with perfect conditions—they're threading modern infrastructure through ancient cities, unstable soils, and extreme weather, all while millions of people continue their daily lives meters away. This is the unglamorous expertise that actually enables India's growth story.

VI. Financial Performance & Market Position

The numbers tell a story of consistent outperformance that most investors miss because infrastructure isn't sexy. Q4 FY24 saw net profit jump 26.9% to ₹113.55 crore while revenue climbed 9.8% year-over-year to ₹2,479.72 crore. But the headline figures obscure the real story: this is a company generating 27.6% ROCE and 21.8% ROE in an industry where double digits are considered excellent. The stock trades at a P/E of 31.8—seemingly expensive until you consider the growth trajectory. Over the last 5 years, revenue has grown at 25.9% yearly versus the industry average of 10.19%. This isn't financial engineering or multiple expansion—it's genuine operational outperformance driven by execution excellence and strategic positioning in high-growth segments.

The consolidated order book stood at ₹18,820 crore as of 30 June 2025, providing visibility for the next 2-3 years of revenue. More importantly, the order mix has shifted toward higher-margin, technically complex projects. The company has transitioned away from older, lower-margin legacy orders, now nearly phased out, paving the way for improved EBITDA margins with newer, more lucrative contracts.

The working capital intensity—often the Achilles heel of construction companies—is remarkably well-managed. The company maintains a low net debt to equity ratio at 0.3x, providing financial flexibility to bid for larger projects without diluting shareholders or taking excessive leverage. This conservative balance sheet is a competitive advantage in an industry where many players are perpetually capital-constrained.

Management's guidance reflects confidence without overreach. For FY25, they're targeting 20% plus revenue growth and order inflow of ₹8,000 to ₹10,000 crores. The margin outlook remains conservative—maintaining 10% plus EBITDA margins, which management views as sustainable for the construction industry—but given the shift in project mix, there's potential for positive surprises.

The competitive landscape provides context for ITD Cementation's performance. While larger players like L&T dominate headline-grabbing mega-projects, ITD Cementation has carved out profitable niches in specialized segments where technical expertise matters more than balance sheet size. Their success rate in marine projects—35% win rate in marine tenders—demonstrates this focused approach's effectiveness.

What's particularly impressive is the capital efficiency. Generating nearly 28% ROCE in a capital-intensive business suggests either exceptional project selection, superior execution, or both. The company isn't chasing growth at any cost—they're being selective, focusing on big jobs in the ₹1,000-3,000 crore range that provide better revenue visibility and execution efficiency.

The financial performance isn't just about the past—it's setting up the future. With India's infrastructure spending expected to accelerate, a proven execution track record, and a balance sheet that can support growth without stress, ITD Cementation is positioned to capture disproportionate value in the coming infrastructure super-cycle. The market is beginning to recognize this, but at current valuations, the company still offers compelling risk-reward for patient investors who understand that infrastructure is ultimately about execution, not promises.

The Data Center & New Infrastructure Pivot

The surge in India's data center ecosystem isn't just another infrastructure trend—it's a fundamental rewiring of the country's digital nervous system. India's data centre market continues to experience robust growth driven by digital transformation, increased internet penetration, policy enablers, rising data consumption, and artificial intelligence (AI) adoption. The numbers are staggering: India's total DC capacity reached approximately 1,255 MW between January and September and is projected to expand further to around 1,600 MW by the end of 2024.

For ITD Cementation, this represents a strategic pivot that leverages their eight decades of foundation engineering expertise in an entirely new vertical. Data centers aren't just buildings with servers—they're precision-engineered fortresses that must maintain exact temperatures, withstand seismic events, manage massive power loads, and operate 24/7 without interruption. Every competency ITD Cementation has developed—from deep excavation to specialized concrete formulations to managing complex MEP systems—translates directly to data center construction.

India's digital infrastructure is poised for unprecedented growth, with investment commitments in the data center industry expected to exceed $100 billion by 2027. This investment surge reflects the country's strategic importance as a global digital hub. Between 2019 and 2024 alone, India attracted nearly $60 billion in data center investment commitments, with Maharashtra and Tamil Nadu emerging as preferred destinations.

The AI revolution is supercharging this growth. The India data center colocation market is expected to grow at a CAGR of 24.68% from 2023 to 2029. More critically, the average rack power density in India is around 3-5 kW, which is likely to increase to 12-14 kW by 2029 through the increased deployment of Big data, IoT, AI, and ML workloads. This isn't just more of the same—it's a complete reimagining of what data centers need to be.

The construction challenges are formidable. Traditional data centers required precision; AI-enabled facilities demand perfection. The cooling requirements alone are revolutionary—where a standard server rack might generate 5kW of heat, an AI cluster can produce 30kW or more. The structural requirements change completely: floors must support exponentially higher loads, power systems must deliver unprecedented density, and cooling systems must remove heat at rates that would have been unimaginable five years ago.

ITD Cementation's timing couldn't be better. They're entering this market just as it transitions from traditional builds to next-generation facilities. Their experience with mission-critical infrastructure—where a millimeter's deviation in a metro tunnel could be catastrophic—positions them perfectly for data center construction where uptime is measured in "nines" of reliability (99.999% uptime means less than 5 minutes of downtime per year).

The company isn't just chasing a trend. They're recognizing that India's infrastructure future isn't just about moving people and goods—it's about moving data. The rapid adoption in 5G technology has catapulted monthly data usage from 2GB to an average of 25GB per user in India. This surge in data consumption coincides with India's achievement of surpassing one billion smartphone users. Additionally, Indian banks are witnessing an unparalleled level of compute usage due to the immense volume of UPI transactions, potentially surpassing the combined activity of numerous European countries.

What makes this pivot particularly clever is that data centers aren't replacing their traditional infrastructure work—they're complementing it. A new metro line needs data centers for operations control. Airports require edge computing facilities for real-time processing. Smart cities need distributed data infrastructure. ITD Cementation can now offer integrated solutions: build the physical infrastructure and the digital backbone that makes it smart.

The competitive dynamics in data center construction differ from traditional infrastructure. While metro projects might see 10-15 bidders, specialized data center construction has fewer qualified players. The technical requirements—from understanding computational fluid dynamics for cooling to managing electromagnetic interference—create natural barriers that favor experienced engineering firms over pure construction companies.

This isn't speculation about distant possibilities. The data center boom is happening now, and ITD Cementation is positioning to capture it. With their proven ability to execute complex projects, relationships with major corporations and government entities, and technical expertise that translates perfectly to data center requirements, they're not just participating in India's digital transformation—they're building its physical foundation.

VIII. Playbook: Lessons from Nine Decades

After tracking ITD Cementation through British colonialism, Indian independence, five ownership changes, and now a digital revolution, clear patterns emerge that transcend any single era or owner. This isn't luck or coincidence—it's a playbook for survival and growth in one of the world's most challenging business environments.

Lesson 1: Technical Expertise Compounds Over Generations

The company's origin story—British engineers figuring out how to make structures stand in Indian soil—established a principle that remains true 93 years later: in infrastructure, deep technical knowledge creates lasting competitive advantages. Every project adds to an institutional memory that can't be replicated by new entrants. When Kolkata needed someone to dig 30 meters below ground without flooding the city, ITD Cementation didn't consult manuals—they drew on decades of experience doing exactly this kind of work. This expertise compounds: marine construction knowledge helps with underground water management, tunneling experience applies to deep foundations, airport work informs data center construction.

Lesson 2: Ownership Is Temporary, Capability Is Permanent

Between 1978 and 2004, the company changed hands five times. Each transition could have been fatal—new owners often gut acquisitions, impose their culture, or redirect strategy. Yet ITD Cementation survived by maintaining a core identity separate from ownership. The engineers building projects in 1995 under Trafalgar House were largely the same ones working in 2000 under Skanska. This continuity meant that while corporate strategies shifted, project execution remained consistent. Clients trusted the company not because of who owned it, but because of who operated it.

Lesson 3: International Parentage as Competitive Advantage

In emerging markets, foreign ownership can be either an asset or liability depending on execution. ITD Cementation turned it into an asset by using international connections for technology transfer while maintaining local operations. Each owner—British, Norwegian, Swedish, now Thai—brought different capabilities that layered onto existing expertise. But crucially, the company never became a foreign firm operating in India; it remained an Indian firm with foreign backing. This balance is delicate but powerful: international credibility with local execution.

Lesson 4: Trust Accumulates Slowly, Pays Dividends Forever

Infrastructure is ultimately a trust business. Governments entrust you with projects that affect millions of citizens. A single high-profile failure can end a company. ITD Cementation has built trust through consistent delivery across decades. When they bid for a project today, they're not just offering a price—they're offering 93 years of successful execution. This trust becomes self-reinforcing: successful projects lead to more opportunities, which build more trust, creating a virtuous cycle that new entrants can't easily break.

Lesson 5: Complexity as a Moat

The company consistently moved toward more complex projects rather than competing on price in commoditized segments. Building a simple warehouse is a commodity; constructing an underwater metro station is art. By focusing on projects that require specialized knowledge—marine structures, deep excavations, tunneling—they've avoided the race to the bottom that plagues much of construction. Complexity doesn't just mean higher margins; it means fewer competitors and stronger client relationships.

Lesson 6: Adapt Technology, Don't Chase It

Despite operating in a traditional industry, ITD Cementation has consistently adopted new technologies—but always in service of core capabilities rather than as ends in themselves. They didn't become a "tech company"; they became a construction company that uses technology exceptionally well. When tunneling technology advanced, they adopted it to dig better tunnels. When project management software evolved, they used it to deliver projects faster. Technology amplified existing strengths rather than replacing them.

Lesson 7: Diversification Within Focus

The company's portfolio spans metros, airports, ports, tunnels, and now data centers—seemingly diverse but actually variations on a theme: complex infrastructure requiring specialized engineering. They didn't diversify into real estate development or manufacturing; they stayed within infrastructure but broadened their definition of what infrastructure means. This focused diversification provides resilience without diluting expertise.

Lesson 8: Government Relations Are Infrastructure

In a sector where the government is often the primary client, relationships matter as much as capabilities. ITD Cementation has mastered the art of being apolitical while being deeply connected—working with governments across party lines and regime changes. They understand that in infrastructure, you're not just a contractor; you're a partner in nation-building. This positioning transcends individual projects and creates lasting institutional relationships.

Lesson 9: Financial Conservatism in a Capital-Intensive Business

Despite operating in an industry notorious for leverage and working capital stress, ITD Cementation maintains remarkably conservative finances. Their net debt to equity ratio of 0.3x isn't just a number—it's a philosophy. In infrastructure, financial stress can force you to take bad projects or accept poor terms. By maintaining a strong balance sheet, they can be selective, walking away from projects that don't meet their criteria.

Lesson 10: The Power of Persistence

Perhaps the most important lesson is simply showing up, year after year, decade after decade. While flashier companies captured headlines and then disappeared, ITD Cementation kept building. They survived the License Raj, economic liberalization, the global financial crisis, and COVID-19. This persistence creates its own momentum—clients know they'll be around to honor warranties, employees build careers rather than taking jobs, and expertise accumulates rather than dissipating.

These lessons aren't just historical curiosities—they're the operating manual for building a sustainable infrastructure business in emerging markets. They explain why a company that started as a colonial-era engineering firm is now positioned to build India's digital future. The specific projects change, the technologies evolve, but the fundamental playbook remains remarkably consistent: accumulate expertise, build trust, manage complexity, and above all, survive long enough for compounding to work its magic.

IX. Bear vs. Bull Case & Valuation

The investment case for ITD Cementation presents a fascinating study in contrasts—a company with undeniable operational excellence trading at valuations that make both bulls and bears uncomfortable. At 31.8x P/E and 7.4x book value, the market is pricing in significant growth, but is it justified?

The Bull Case: India's Infrastructure Renaissance

The bulls see ITD Cementation as perfectly positioned for India's next decade. Start with the macro: India needs to spend $1.4 trillion on infrastructure by 2025 to sustain economic growth. This isn't aspirational—it's essential. The government has committed ₹10 lakh crore for infrastructure in FY25 alone. With GDP growth targeted at 7-8% annually, infrastructure spending must keep pace.

ITD Cementation's specialized capabilities create genuine moats. There are perhaps a dozen companies in India capable of building metro stations 30 meters underground. Fewer still can construct marine structures that withstand cyclones. The company isn't competing on price in commoditized segments—they're providing solutions where technical expertise determines success. Their 35% win rate in marine projects demonstrates this specialized edge.

The financial metrics support the optimism. Generating 27.6% ROCE in a capital-intensive industry suggests exceptional capital allocation. Revenue growing at 25.9% annually versus 10.19% industry average isn't just market share gain—it's category creation. They're not just growing; they're growing profitably, with margins expanding as they exit legacy low-margin projects.

The Thai parentage provides unique advantages. Unlike financial sponsors seeking exits, ITD is a strategic owner understanding infrastructure's long cycles. The parent's royal endorsement in Thailand translates to credibility across Southeast Asia. Technology transfer continues—from Thai expertise in soft soil construction to regional project management capabilities.

The new growth vectors are particularly compelling. Data center construction could be a multi-decade opportunity as India builds digital infrastructure. The shift from 5kW to 12-14kW rack densities means existing facilities need upgrading—a massive replacement cycle. With few competitors possessing both construction expertise and understanding of mission-critical facilities, ITD Cementation could dominate this niche.

Management's execution track record inspires confidence. They've consistently met or exceeded guidance, suggesting either conservative forecasting or exceptional execution—likely both. The order book at ₹18,820 crore provides 2+ years of revenue visibility, unusual in construction.

The Bear Case: Structural Challenges and Cyclical Risks

The bears counter with sobering realities. Infrastructure spending is inherently cyclical, tied to government finances and political priorities. A global recession, fiscal crisis, or political shift could dramatically reduce project flow. The company survived previous downturns, but past performance doesn't guarantee future resilience.

Government dependency creates multiple risks. Payment delays are endemic in Indian infrastructure—even successful projects can stress working capital. Policy changes can strand investments: witness the toll road crisis or stalled power projects. When your largest customer is also your regulator, pricing power is limited.

Competition is intensifying from multiple directions. Larger players like L&T have deeper pockets and political connections. Chinese companies, despite current restrictions, could re-enter with aggressive pricing. New technologies like modular construction could disrupt traditional methods. The moats might be narrower than they appear.

The valuation leaves little room for error. At 31.8x P/E, the market expects perfection. Any execution stumbles, margin compression, or growth deceleration could trigger significant multiple contraction. The stock has already appreciated significantly—how much upside remains?

Working capital management remains challenging despite improvements. Construction is inherently working capital intensive—growth requires funding. While the current 0.3x debt to equity seems conservative, rapid growth could strain the balance sheet. One bad project or delayed payment could cascade into broader financial stress.

The human capital challenge is underappreciated. Infrastructure engineering expertise takes decades to develop. As experienced engineers retire, can the company maintain technical excellence? India's tech boom offers talented engineers better-paying, less demanding careers than construction sites. The expertise moat could erode through attrition.

Technological disruption is a wildcard. While ITD Cementation has adapted historically, the pace of change is accelerating. Building Information Modeling (BIM), artificial intelligence in project management, robotic construction—each could fundamentally alter competitive dynamics. Traditional expertise might matter less if software eats construction.

The Valuation Debate

Current valuations reflect optimism but not euphoria. Comparing to global infrastructure players, ITD Cementation trades at a premium justified by superior growth. Versus Indian peers, the valuation is in-line with quality players but expensive versus the broader sector.

The DCF models are highly sensitive to assumptions. Bull cases reaching ₹1,200-1,500 assume sustained 20%+ growth and margin expansion. Bear cases around ₹400-500 factor in cyclical downturns and margin pressure. The wide range reflects genuine uncertainty about India's infrastructure trajectory. Analyst sentiment remains mixed but generally positive. According to analysts, ITDCEM price target is 593.50 INR with a max estimate of 633.00 INR and a min estimate of 554.00 INR. These targets suggest limited upside from current levels, though the wide range reflects uncertainty about execution and market conditions.

The Synthesis

The truth likely lies between extremes. ITD Cementation is a high-quality operator in an essential industry with demonstrated execution capability and strong growth prospects. The valuation is demanding but not unreasonable given the track record and opportunity set. The key question isn't whether the company will grow—it's whether growth will meet elevated expectations.

For investors, the decision hinges on time horizon and risk tolerance. Short-term traders face valuation risk and potential volatility. Long-term investors can look through near-term fluctuations to the structural growth story. The company offers exposure to India's infrastructure buildout with proven execution—valuable but not without risks.

The most balanced view: ITD Cementation is a strong company at a full price. The business quality justifies premium valuation, but the margin of safety is limited. Investors should size positions accordingly—meaningful enough to matter if the bull case plays out, modest enough to survive if reality disappoints. In infrastructure investing, as in infrastructure building, the key is not to bet the foundation on any single pillar.

X. Power & Grading

After examining ITD Cementation through every conceivable lens—historical, operational, financial, and strategic—it's time to render judgment. Not on whether the stock will go up or down tomorrow, but on the fundamental question: is this a great business, and if so, at what price does greatness matter?

The Power Analysis

In the Acquired.fm framework, "power" refers to a company's ability to generate persistent differential returns. ITD Cementation demonstrates multiple forms of power:

Scale Economies: The company's ability to bid for and execute ₹1,000-3,000 crore projects creates a natural advantage. Smaller competitors can't marshal the resources, bonding capacity, or technical expertise for such projects. But this isn't traditional scale—it's "complexity scale" where size enables tackling problems others can't solve.

Switching Costs: Once ITD Cementation is midway through building your metro station 30 meters underground, switching contractors isn't really an option. But more subtly, the switching costs are reputational—government officials who choose ITD Cementation are making a safe choice backed by 93 years of history.

Network Effects: Not in the traditional sense, but there's a "reputation network effect." Each successful project makes the next sale easier. Each government relationship opens doors to others. Each technical challenge solved adds to institutional knowledge that helps win future projects.

Counter-Positioning: By focusing on technically complex, lower-volume projects, ITD Cementation has positioned itself where larger competitors like L&T might not compete aggressively. It's more profitable to be the best at building specialized infrastructure than the fifth-best at building highways.

The Execution Grade: A-

On pure execution, ITD Cementation earns top marks. Ninety-three years of continuous operation through colonial collapse, economic crises, and ownership chaos demonstrates remarkable resilience. The technical capabilities are undeniable—from marine structures to deep excavations to emerging data center expertise.

Financial execution has been stellar recently: 27.6% ROCE in a capital-intensive industry, revenue growing at 2.5x the industry rate, margins expanding despite inflation. Management consistently meets guidance, suggesting either conservative forecasting or exceptional project management—both positives.

The only deduction comes from the historical volatility in margins and returns during ownership transitions. While recent performance is excellent, the long-term track record shows periods of struggle. The question is whether current excellence is sustainable or cyclical.

The Strategy Grade: B+

Strategically, ITD Cementation has made smart choices. The focus on technical complexity over scale is correct for their capabilities. The pivot to data centers shows strategic foresight. Maintaining financial conservatism provides flexibility.

But there are strategic questions. Why hasn't the company expanded internationally more aggressively given parent company connections? Why remain subscale in certain segments rather than consolidating? Is the current strategy differentiated enough when competitors are also upgrading capabilities?

The Thai ownership is strategically valuable but underutilized. There should be more technology transfer, more regional expansion, more leveraging of ITD's Southeast Asian relationships. The company seems content being a strong Indian player rather than a regional champion.

The Market Position Grade: B

In the Indian infrastructure landscape, ITD Cementation occupies a strong but not dominant position. They're the clear leader in certain niches—marine construction, complex foundations—but lack the scale to influence industry dynamics.

The ₹13,000+ crore market cap makes them significant but not essential. They're large enough to matter but small enough to be acquired. This middle position provides flexibility but also vulnerability.

The competitive moat exists but isn't insurmountable. Technical expertise can be developed, relationships can be built, and execution track records can be established by determined competitors. The moat is more like a series of defensive positions than an impregnable fortress.

The Valuation Context: C+

Here's where enthusiasm meets reality. At 31.8x P/E and 7.4x book value, the market is pricing ITD Cementation like a high-growth technology company, not an infrastructure contractor. Yes, the growth rate justifies a premium, but how much?

The valuation implies several assumptions: continued 20%+ growth, sustained margin expansion, no execution hiccups, and favorable government spending. These aren't unreasonable, but they're optimistic. The risk-reward is skewed—more downside from disappointment than upside from exceeding expectations.

The Final Grade: B+

ITD Cementation is a very good business trading at a price that assumes it's excellent. The company deserves credit for exceptional execution, smart strategic positioning, and remarkable resilience. In the universe of infrastructure companies, it's clearly above average.

But greatness requires more than competence—it requires competitive advantages that compound over time, creating widening moats and accelerating returns. ITD Cementation has advantages, but they're more like skilled craftsmanship than structural superiority.

For investors, this grade translates to a simple framework: ITD Cementation is a high-quality hold at current prices, a strong buy on any significant correction, and a potential trim if valuations become even more extended. The company will likely continue executing well and growing steadily—the question is whether that's enough to justify today's premium valuation.

The power in ITD Cementation isn't the explosive kind that creates ten-baggers. It's the steady, compound power of a business that shows up every day for 93 years and builds things that matter. In a world obsessed with disruption, there's underappreciated value in construction. The grade reflects that reality—very good, not quite great, but absolutely worth watching as India builds its future, one foundation at a time.

XI. Recent NewsCorporate Developments & Strategic Shifts

The most significant development in 2024 has been the potential ownership transition. ITD Cementation announced on July 3, 2024, that its promoter Italian Thai Development Public Company Limited is exploring a potential divestment of its investments in the company. This triggered intense speculation, with the stock rallying 35% in two weeks on reports that Adani Group is eyeing to acquire a promoter stake.

On September 20, ITD Cementation informed that there was no conclusion to the proposed divestment of ITD's investments, but the speculation continues. The stock performance reflects this uncertainty and opportunity: thus far in calendar year 2024, the stock price has more than doubled, or zoomed 122%.

Record-Breaking Order Book & Execution

The operational momentum remains exceptional. ITD Cementation reported a robust order book of INR 18,820 crores as of June, with new orders of over INR 2,900 crores in Q1 and INR 1,300+ crores in July. More impressively, the company is also L1 (lowest bidder) on INR 1,400 crores of additional orders.

Management's outlook is bullish. Order inflow for the year is expected at INR 15,000 to 16,000 crores, with about 35% coming from group entities. The strategic shift toward larger projects is notable—management sees a pipeline of INR 87,000 to INR 90,000 crores in opportunities, emphasizing a shift toward fewer but larger projects.

Financial Performance Continues to Shine

Q1 FY25 delivered another strong quarter. The company posted robust operational performance with the highest ever quarterly revenue of Rs 2,381 crore (up 30% YoY) and profit after tax at Rs 100 crore (up 91% YoY). EBITDA grew 36% YoY to Rs 237 crore.

Management maintained guidance for 20–25% revenue growth and 10% EBITDA margin for FY '26. The margin resilience is particularly impressive: EBITDA margins remained steady at 10% despite industry labor shortages and margin pressure seen by peers. Management attributed this to a balanced mix of contracts, with about 70% being variable price contracts.

Contract Wins & Strategic Positioning

Recent contract wins demonstrate continued execution strength. ITD Cementation India shares soared 6% to a new high of ₹860.95, driven by a robust order book and significant contract wins totaling ₹1,853 crore in June. The company anticipates continued revenue growth and improved margins, supported by government infrastructure spending.

ITD Cementation has won a significant contract worth approximately ₹893 crore for the construction of berth and breakwater structures in Odisha, enhancing its maritime infrastructure portfolio. This aligns with their strategic focus on marine structures, where they maintain industry-leading capabilities.

Leadership Changes & Governance Updates

ITD Cementation undergoes significant leadership changes, including new appointments and resignations, alongside alterations to its Articles of Association due to acquisition by Renew Exim DMCC. The governance changes reflect the ongoing ownership transition dynamics.

Shareholders approved company name change to Cemindia Projects and amended Articles reflecting new promoter Renew Exim DMCC, suggesting the ownership transition may be progressing behind the scenes despite official statements about no conclusion.

Market Recognition & Analyst Sentiment

The market's recognition of ITD Cementation's quality is evident in the stock performance. Shares hit a new high of Rs 634, surging 18% in Thursday's intra-day trade amid heavy volumes in an otherwise weak market, surpassing its previous high of Rs 614.30.

Management highlighted the government's significant emphasis on improving connectivity through projects such as Bharatmala Pariyojana for road development, Sagarmala for port-led development and several other initiatives. This demonstrated the government's commitment to fostering growth in the construction sector and enhancing the overall quality of urban and rural life in India. All these initiatives are directed at attracting investments, improving project execution and creating employment opportunities.

The recent developments paint a picture of a company at an inflection point—strong operational performance meeting potential ownership transformation. The speculation around Adani Group's interest adds complexity but also validates ITD Cementation's strategic value. Whatever the ownership outcome, the underlying business continues to execute exceptionally, positioning itself for India's infrastructure super-cycle.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube