IRCTC: India's State-Granted Monopoly on Wheels

I. Introduction & Episode Roadmap

Picture the numbers first, because they anchor everything that follows. In the financial year ended March 2025, IRCTC generated roughly ₹4,675 crore of revenue and about ₹1,315 crore of net profit — a net margin near 28%, expanding from the prior year's 26%.12 That is a software-company margin profile attached to a business that, on the surface, sells train tickets, packs lunches, and bottles water. For most of the period since its 2019 listing, the market treated IRCTC as a rare public-sector jewel: a state enterprise that behaved like a high-quality consumer-internet platform. The stock became a retail-investor darling, and then, over the year leading into mid-2026, it gave back roughly a third of its value — a reminder that "monopoly" and "share price you can rely on" are not synonyms.

What makes this such a rich case study is that it inverts the usual relationship between quality and risk. In most businesses, a wide moat and a low-risk profile travel together: the more defensible the franchise, the safer the earnings. IRCTC breaks that link. Its franchise is about as defensible as any on Earth — competition is literally prohibited — and yet the earnings are subject to a form of risk most great businesses never face: the risk that your owner, regulator, and supplier are the same entity, and that entity has a budget to balance. A Coca-Cola or a Visa builds its moat brick by brick over decades and answers to no one who can unilaterally reprice its product. IRCTC was handed its moat fully formed and answers to a controlling shareholder who can, and once did, try to take the best of it. Understanding IRCTC means holding those two facts — extreme defensibility and unusual top-down fragility — in the same thought without letting either cancel the other.

The central question is deceptively simple. How much of IRCTC's economics is a genuine business moat — something durable, defensible, and earned — and how much is a policy favour that the government could revoke or reprice on a Tuesday afternoon? In October 2021, that question stopped being academic. The Ministry of Railways announced it would help itself to half of IRCTC's online convenience-fee revenue; the stock cratered close to 25% in a single session; and then, in less than a day, the Ministry reversed itself.3 That 19-hour round trip is the closest thing to a controlled laboratory experiment on minority-shareholder risk in a government-controlled monopoly that Indian markets have produced, and we will return to it in depth.

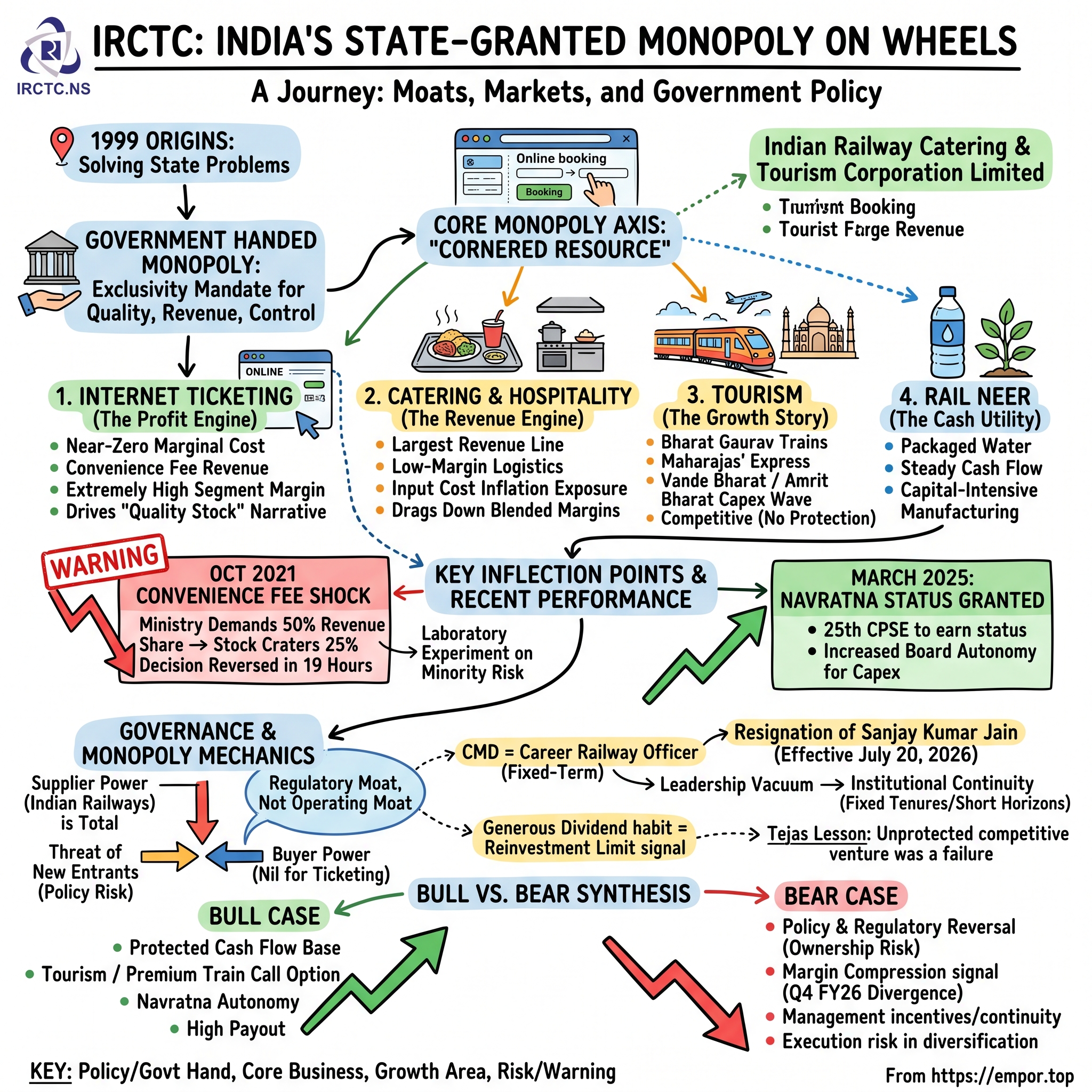

Here is the roadmap. We start with why India built a state ticketing monopoly in the first place. We then dissect the four engines of the business as it exists today — catering, ticketing, tourism, and packaged water — because they have wildly different economics and only one of them explains the "quality stock" narrative. We examine the actual mechanics of the monopoly and the governance stress test that exposed its fragility. We walk through the 2019 IPO and the slow sell-down of a sovereign stake. We weigh the growth bets — the tourism wave riding India's rail-capex supercycle — against the cautionary tale of Tejas Express, the one time IRCTC tried to run a train rather than just ticket it. We look hard at management incentives in a company with no founder and no owner-operator. We map the competitive landscape, which is airtight at the core and genuinely contested at the edges. And we close with the risk radar and the bull-versus-bear synthesis. The through-line: an investor in IRCTC is not underwriting a competitive strategy. They are underwriting government policy continuity. Let us see why.

II. Origins: Why India Built a State Ticketing Monopoly

To understand IRCTC, rewind to the India of the late 1990s, when buying a train ticket meant a physical queue that could swallow half a day, and eating on a train meant taking your chances with catering of famously uneven quality. Indian Railways was — and remains — one of the largest transport systems on the planet, a lattice of tracks carrying tens of millions of passengers a day. But it was a colossus optimized for moving people, not for the retail experience of buying, boarding, and being fed. The catering was decentralized, inconsistent, and the subject of persistent complaints about hygiene and overcharging. Ticketing was a paper-and-clerk operation straining under demand it could not gracefully meet.

The government's answer, in 1999, was administrative rather than market-based: carve out a separate corporate entity, wholly owned by the Ministry of Railways, and hand it a defined set of exclusive mandates.5 Indian Railway Catering & Tourism Corporation was incorporated to professionalize catering, to develop rail-linked tourism, and — almost as an afterthought at the time — to drag ticketing into the internet age. The choice to create a single wholly controlled monopoly, rather than license a competitive field of vendors, was deliberate. It gave the state revenue capture, centralized quality control after years of food-safety embarrassment, and administrative simplicity across a network of that scale. It also, not incidentally, kept the money inside the family.

It helps to remember the wider backdrop. The late 1990s and early 2000s were the years India was cautiously corporatizing pieces of its sprawling public sector — spinning off ministerial functions into arm's-length companies that could carry commercial discipline without being fully privatized. IRCTC fit that mould exactly: a company with a corporate balance sheet and a profit motive, but with the government's hand firmly on the tiller and the government's mandate as its entire reason for being. The catering brief in particular carried real political weight. Onboard food had become a recurring source of passenger anger and parliamentary questions; centralizing it under a single accountable entity was as much about defusing a chronic public-relations sore as about commerce. That the same entity would, within a few years, stumble into becoming a technology pioneer was nobody's plan.

Then came the underrated origin fact. In 2002, IRCTC launched its online ticketing portal, irctc.co.in.5 Consider the timing. This was years before Flipkart existed, before Amazon had an India business, before the smartphone reordered Indian commerce. A state-owned railway subsidiary quietly became one of the country's earliest and highest-volume e-commerce properties — arguably one of India's first internet businesses to operate at genuine national scale. It did not set out to be a technology pioneer. It became one because it sat on top of the largest captive transactional demand in the country: everyone needs a train ticket, and IRCTC was the only place online to get one. That accident of positioning — enormous demand, funnelled through a single mandated channel — is the seed of everything that later made the ticketing segment so extraordinarily profitable.

Consider how counterintuitive this was in its moment. India's private internet economy would spend the next two decades and untold billions of venture capital trying to manufacture what IRCTC possessed from day one: a captive national audience that transacted repeatedly, out of necessity, with no meaningful alternative. Flipkart had to subsidize customers into shopping online; Paytm had to bankroll cashbacks to teach India to pay digitally. IRCTC never had to acquire a single customer. The customer arrived because the customer needed a train, and the train ticket lived nowhere else. In the language of internet economics, IRCTC's customer-acquisition cost was structurally near zero and its retention was effectively mandated — the two most expensive problems in consumer technology, solved not by product genius but by the terms of a government charter. The irony that would define the company's investment case was already baked in at birth: the very thing that gave it world-class economics also meant those economics were never truly its own to keep.

The deeper point for an investor is that the monopoly was never an earned competitive victory. It was a design decision by a government solving for its own problems: quality, revenue, and control. That origin explains why the structure is so politically entrenched — dismantling it would mean the state voluntarily surrendering both a revenue stream and a lever of control over a strategically important network — and it also explains the permanent vulnerability. A privilege granted by policy can be modified by policy. Keep that in mind as we turn from why the monopoly exists to what, exactly, it produces today.

III. The Business Today: Four Engines, Very Different Economics

Walk into IRCTC's income statement expecting a single clean monopoly and you will instead find four businesses stapled together, each with a distinct personality. The trap — the one that management's own framing sometimes encourages — is to treat them as one homogeneous "railway platform." They are not. One engine drives the revenue, a different engine drives the profit, a third is the growth story management most wants to sell you, and a fourth is a quiet cash-generating utility. Getting the proportions right is the single most important analytical act in understanding this company.

Start with catering and hospitality, the revenue engine. Onboard meals, station food plazas, refreshment rooms, base kitchens — this is the largest revenue line, and it is fundamentally a logistics-and-vendor-management business, not a software business. In the quarter ending March 2025, catering revenue was roughly ₹531 crore, growing around 34% year over year.2 By the March 2026 quarter, catering alone contributed nearly 46% of total revenue.3 Big top line, but structurally the lowest-margin segment: you are buying ingredients, paying cooks and outsourced labour, managing food safety across thousands of trains, and absorbing input-cost inflation. Every rupee of catering revenue drags a heavy cost tail behind it. When you hear that IRCTC has "software-like margins," catering is emphatically not the reason.

The reason is internet ticketing — the crown jewel, and the segment that explains almost the entire re-rating of IRCTC into a quality stock. Here the economics invert. The marginal cost of processing one additional e-ticket is close to nothing; the infrastructure is built, and each incremental booking is nearly pure contribution. The proof is in the segment disclosures. For the nine months ending December 2025, internet ticketing threw off roughly ₹1,257 crore of segment profit on about ₹1,554 crore of segment revenue — a segment-level profitability so high that ticketing accounted for over 86% of IRCTC's total segment profit.17 Read that again: a segment that is not even the largest by revenue produces the overwhelming majority of the profit. That is the near-zero-marginal-cost toll booth doing its work. This is the closest IRCTC comes to a true platform business, and it is where the "quality" thesis lives or dies.

It is worth understanding exactly where the ticketing profit comes from, because it is subtler than "IRCTC sells tickets." The face value of the ticket belongs to Indian Railways, not to IRCTC. What IRCTC keeps is the convenience fee — a modest per-transaction charge layered on top of the fare for the service of booking online. Multiply a small fee by hundreds of millions of transactions a year against a cost base that barely moves whether volumes rise 5% or 15%, and you have manufactured operating leverage of a rare kind. This is why management, on recent calls, has consistently pointed to booking-volume growth and the mix between the higher-fee air-conditioned classes and the lower-fee non-AC classes as the real levers on the segment.[^18] It also explains why the 2021 attempt to skim half of that fee was so existentially alarming to the market: the convenience fee is not a side revenue line, it is the profit engine's fuel. A change to it does not dent IRCTC; it reprices the entire company. Hold that thought for the governance section.

Tourism is the growth story. Domestic and international holiday packages, hotel and air bookings, pilgrimage circuits, and the flagship theme trains — Bharat Gaurav trains and the ultra-premium Maharajas' Express. Historically around 15–16% of revenue, it is the fastest-growing segment and the one management promotes most energetically. But note the flip side visible in the same nine-month segment data: tourism generated roughly ₹281 crore of revenue yet only about ₹14 crore of segment profit.17 It is a real, expanding business, but it is thin-margined and — crucially — the one segment where IRCTC has no legal protection and must actually compete. More on that later.

Finally, Rail Neer, the packaged-water business, is the utility-like tail: the smallest and most capital-intensive engine, running bottling plants at high utilization across hundreds of stations to serve captive onboard and platform demand.5 It is the one segment that behaves like a conventional manufacturing operation — you build a plant, you run it near full capacity, you truck bottles to stations, and you earn a steady spread. The strategic logic is partly defensive: standardizing the water sold on trains under a single quality-controlled brand was itself a response to years of complaints about dubious bottled water being passed off on passengers. It is steady, low-drama, low-optionality cash. It will not make anyone rich, and it will not blow up. For an investor, its main function is to remind you that even IRCTC's "boring" segment exists because of the same captive-demand logic that underwrites everything else here.

The investor implication of this four-engine structure is that IRCTC should never be valued as a single blended entity, because the blend hides everything that matters. A sum-of-the-parts lens is the only honest one: the ticketing engine deserves a rich, platform-like multiple because of its margin structure and near-zero incremental cost; the catering and Rail Neer engines deserve modest, utility-to-industrial multiples befitting their thin, cost-exposed economics; and the tourism engine deserves whatever premium you are willing to pay for an option that is growing fast but has not yet proven it can grow profitably. Collapse all of that into one price-to-earnings number and you will either overpay — treating the whole company as if it were the ticketing segment — or underappreciate the crown jewel by dragging it down with the catering business. The market's habit of oscillating between euphoria and disappointment on IRCTC is, in part, a symptom of exactly this: investors repeatedly re-rating the entire company on the strength or weakness of whichever engine is in the headlines that quarter.

So the honest map is this: ticketing is the profit engine, catering is the revenue engine, tourism is the growth pitch, and Rail Neer is the stable tail. The full-year FY25 result — revenue up about 10% to ₹4,675 crore, net profit up roughly 18% to ₹1,315 crore, with net margin widening toward 28% — looked like the platform thesis vindicated.14 But the March 2026 quarter flashed the first warning in years, and it deserves to be named here rather than buried: revenue grew about 15% year over year to ₹1,460 crore, yet consolidated net profit fell nearly 9% to ₹326 crore, as PAT margin compressed from roughly 27% to 22% in a single quarter.3 Costs, in other words, grew faster than sales for the first time in a long while. Whether that is a one-off or the start of a trend is one of the most important questions an IRCTC investor now faces — and it points us straight at the mechanics of the monopoly itself, and who really controls the economics.

IV. The Monopoly Mechanics — and the Governance Stress Test That Exposed Them

Let us be precise about what the exclusivity actually covers, because vague talk of a "monopoly" obscures where the walls are. IRCTC holds the sole right to sell Indian Railways tickets online; the sole mandate for onboard catering across the network; and the exclusive right to sell packaged drinking water on trains and at stations. At the supply layer — the actual issuance of the e-ticket, the cooking of the meal, the bottling of the water — no licensed competitor exists. Not a weak competitor. None. Competition, at that layer, is simply not permitted.

The cleanest way to classify this is through Hamilton Helmer's 7 Powers. IRCTC's advantage is not Network Economies (the platform does not get more valuable to me because you also use it), nor Counter-Positioning (there is no clever business model incumbents can't copy), nor Scale Economies in the classic sense. It is a Cornered Resource: a single entity's exclusive control of a uniquely valuable asset — here, the government-granted mandate itself. Through Porter's Five Forces, the picture sharpens further and turns slightly menacing. The threat of new entrants is essentially zero commercially but entirely a function of policy. Buyer power is negligible for ticketing, because the buyer has no alternative. And supplier power is total — because the supplier is Indian Railways, which is also the regulator, which is also the majority shareholder. The uncomfortable implication is that the same power that grants IRCTC its moat sits on both sides of every negotiation. The risk vector is not customer switching or a startup disruptor. It is the owner.

To feel the shape of this power, run the counterfactual. Imagine the government tomorrow licensed three private companies to issue Indian Railways e-tickets alongside IRCTC. What would happen? The face-value fare would not change — that is Railways' to set — but the convenience fee would collapse toward zero as licensees competed for bookings, and IRCTC's crown-jewel margin would evaporate almost overnight. Nothing about IRCTC's technology, brand, or customer relationships would save it, because in the ticketing layer it has never had to build a defensible one; the mandate did the defending. That thought experiment is the tell: a moat you would lose the instant competition were merely permitted is not an operating moat at all. It is a legal enclosure. Enclosures can last for decades — and this one is politically well-fortified — but the risk they carry is binary and top-down, not gradual and competitive.

Which brings us to October 2021, and the single most instructive 24 hours in the company's public life. The Ministry of Railways issued a directive that IRCTC would share 50% of the convenience fee it charged on online bookings with the government.9 The convenience fee is high-margin money — a small charge on hundreds of millions of transactions, flowing almost entirely to the bottom line. Halving it was a direct hit to the crown-jewel segment. The market's reaction was violent and immediate: the stock plunged close to 25% intraday, erasing thousands of crores of value, as investors repriced the monopoly for the discovery that its owner could reach in and take half the best cash flow by fiat.9 And then, within roughly 19 hours, the Ministry withdrew the decision, and the shares recovered.9

There are two ways to read that episode, and a serious investor should hold both. The optimistic reading, argued at the time in a widely discussed Forbes India piece, is that the state — through the Department of Investment and Public Asset Management (DIPAM), which shepherds the government's shareholdings — effectively acted as a protector of minority investors, forcing a correction in under a day.10 The market itself, with no external activist in sight, played the activist role and won a near-instant reversal. That is genuinely rare price discipline over a sovereign owner. The pessimistic reading is harder to dismiss: the arrangement governing how the convenience fee and its revenue are split has reportedly been altered several times over just a few years,10 which means the 2021 shock was not an aberration but a recurring feature. The reversal proved the government can be checked; it did not prove the government won't try again. Both readings are true, and the tension between them is exactly the risk an IRCTC shareholder carries.

Zoom out and the convenience-fee arrangement has been tinkered with repeatedly — reportedly altered on the order of four times across roughly six years, oscillating between the fee being charged, waived, restored, and its split renegotiated.10 Each individual change was small; the cumulative signal is not. It tells you that the single most important variable in IRCTC's profit engine is treated by its owner as an adjustable policy dial, not a settled commercial contract. Contrast that with how a normal company's core pricing works: a private business sets its own prices and defends them; the market, not a ministry, decides whether they hold. IRCTC does not have that autonomy over the very fee that generates most of its profit. For a long-term investor, this is the crux of the "regulatory moat, not operating moat" distinction made concrete. You are not analyzing a company that controls its own economics and happens to be regulated. You are analyzing a company whose economics are, at the most fundamental level, set by the counterparty on the other side of every transaction — and that counterparty answers to fiscal and political pressures that have nothing to do with IRCTC's business performance.

Now, the evidence for the "monopoly equals moat" claim. It is overwhelming — on its own terms. IRCTC processes the underlying volume for essentially all online Indian Railways bookings, a figure that runs to hundreds of millions of e-tickets a year, and it commands north of 90% of the underlying rail-ticket volume that flows through the digital channel.611 But here is the analytical discipline the number demands: this is a regulatory moat, not an operating one. You do not need to invoke brand, switching costs, superior product, or network effects to explain IRCTC's dominance, because you don't need any of them when competition is illegal. That is a strength — regulatory moats can be extraordinarily durable — but it is a strength of a completely different character than, say, a payments network or a search engine. It cannot be competed away. It can only be legislated away. And the entity holding the pen is also the entity that took the company public, which is where the story turns next.

V. The 2019 IPO and the Slow Sell-Down of a Sovereign Stake

On October 14, 2019, IRCTC did something a state-owned catering-and-ticketing subsidiary had no business doing: it delivered one of the best stock-market debuts India had seen in years. The IPO had been priced at ₹320 per share, with the government offloading about 12.6% of its stake in an offer for sale.78 When the stock opened, it listed around ₹644 on the BSE — roughly double the issue price on day one — and briefly touched ₹743 before the dust settled.8 Retail investors who had been allotted shares woke up with a 100%-plus gain by lunchtime. For a public-sector undertaking, this was not supposed to happen; PSU listings were the unloved corner of the Indian market. IRCTC broke the pattern so decisively that it became the template for how investors would come to view "guaranteed monopoly cash flows" — arguably pricing them too richly, too fast.

Why the euphoria? Because the market took one look at the near-zero-marginal-cost ticketing engine and the legally protected demand base and concluded, correctly, that this was a structurally high-margin, capital-light cash machine. The mistake was not in identifying the quality of the cash flows; it was in underweighting the fragility of their ownership — a lesson the 2021 convenience-fee episode would deliver two years later.

Since the IPO, the more important capital-markets story has not been anything IRCTC did — it has done essentially no acquisitions, no transformational M&A, nothing to benchmark against industry deal comps. The story has been what the government did to its own stake. From roughly 87.5% immediately after the IPO, the state has steadily reduced its holding to around 62.4% through a series of offer-for-sale tranches under India's PSU disinvestment program.[^19] This is, functionally, IRCTC's M&A story: a repeating sequence of secondary sell-downs. And the analytically useful frame is that each tranche is a signal about government fiscal priorities, not company strategy. When the state needs to plug a budget gap or hit a disinvestment target, an OFS appears; the float expands, index weights shift, and the flows that move the stock — from foreign and domestic institutions — get rebalanced. An IRCTC investor is therefore always, in part, forecasting the timing of the government's own cash needs. That is an unusual variable to carry on a "quality compounder."

There is a second-order consequence worth naming, because it drives a lot of the stock's day-to-day volatility. Each sell-down enlarges the public float, and a larger float changes IRCTC's weight in the indices that passive and quasi-passive money tracks, which in turn changes the automatic, price-insensitive flows into and out of the name.18 Layer on the fact that IRCTC became a genuine retail-investor phenomenon — one of the most widely held and heavily traded stocks among Indian individual investors — and you have a security whose price can move far more on sentiment, index mechanics, and disinvestment headlines than on any change in the underlying cash flows. The roughly one-third drawdown in the stock over the year into mid-2026 owed at least as much to that sentiment cycle unwinding as to anything the business did. For a long-term investor, the discipline is to separate the durability of the cash flows (high, policy permitting) from the stability of the share price (demonstrably not high). They are not the same question, and conflating them is how people get hurt in names like this.

Then, in March 2025, came the closest thing IRCTC has had to a genuine capital-allocation unlock. The government conferred Navratna status on the company — making it the 25th central public-sector enterprise to earn the designation.12 In plain terms, Navratna status raises the board's autonomy: management can commit up to ₹1,000 crore, or 15% of net worth, to a single investment without running to the ministry for prior approval, and it can more easily form international joint ventures.12 For a company whose defining constraint has always been that it is an arm of the state, this is meaningful headroom. But — and this is the neutral-platform discipline — autonomy is an input, not a result. Navratna status gives IRCTC the ability to deploy capital more freely; it says nothing about whether management will deploy it well. To judge that, we have to look at what happens when IRCTC steps outside its protected lane. Which is the story of the tourism wave and the Tejas lesson.

VI. Growth Bets and Capital Deployment: The Tourism Wave versus the Tejas Lesson

Begin with a fact that reframes the entire capital-allocation discussion: IRCTC has done no material M&A. There is no acquisition to dissect, no purchase multiple to critique, no integration to grade. Its capital-deployment story is almost entirely organic — capex into kitchens, bottling plants, and tourism products — plus a notably generous dividend habit. In FY26 the company paid a first interim dividend of ₹2.50 per share in November 2025, followed by a second interim dividend of ₹3.50 per share (a 175% payout on the ₹2 face value) in early 2026, and then recommended a ₹0.50 final dividend alongside its year-end results.173 For a business that generates far more cash than it can sensibly reinvest, returning much of it to shareholders is rational — but it also tells you something: management is not sitting on a pipeline of high-return internal projects large enough to absorb the profit. The payout is the capital-allocation strategy.

The bull-case growth vector is tourism, and it is genuinely attractive in structure. On its recent earnings calls, management has guided to something like 20% tourism growth, mid-teens catering growth, and high-single-digit ticketing growth looking ahead.16 The tourism ambition rides a wave IRCTC does not have to create: India is in the middle of a rail-capex supercycle — Vande Bharat trains, the coming Vande Bharat Sleeper class, Amrit Bharat trains, and a planned rollout of a couple hundred Bharat Gaurav theme trains over the next several years. The elegance of this bet is that IRCTC does not need to win share from a competitor to grow tourism on the back of new premium trains; it grows as the network grows. That is real optionality layered on top of monopoly cash flow, and it is the single most credible part of the growth story.

The Bharat Gaurav model deserves a closer look because it shows IRCTC playing to its actual strength rather than its Tejas weakness. Under this scheme, themed tourist trains — circuits built around pilgrimage routes, heritage trails, or regional culture — are run as packaged experiences where IRCTC bundles the transport, accommodation, sightseeing, and meals into a single-price product. Crucially, the demand is aspirational and experiential rather than point-to-point commuter travel, which means IRCTC is not competing on fare against an airline or a bus; it is selling a curated journey to a customer who wants the journey itself. That is a far more defensible place to compete than a Tejas-style shuttle, and it leans on the one genuine asset IRCTC has outside the mandate: privileged access to the rail network and the operational plumbing to run trains on it. If the tourism thesis works, this is the mechanism through which it works — not by out-discounting MakeMyTrip on a Goa package, but by selling experiences only a railway insider can assemble.

The honest caveat is that all of this rides a capex wave the company does not fund and cannot control. The Vande Bharat and Amrit Bharat rollouts are decisions of the Ministry of Railways and the Union Budget, not of IRCTC's board. So the growth vector is real, but it is borrowed — IRCTC is a highly leveraged bet on the government's continued willingness to pour capital into premium and long-distance rail. That is probably a good bet given India's stated infrastructure priorities. But it is another instance of the recurring pattern: the best parts of the IRCTC story are things the government does for it, not things the company does for itself.

The premiumization proof point is the Maharajas' Express, IRCTC's ultra-luxury tourist train, which has drawn strong inbound-tourism interest at the top of the market — a small but genuine signal that the tourism segment can move upmarket, capturing high-margin foreign spend, rather than only adding thin-margin domestic volume. It is the kind of product that suggests the tourism engine could, over time, become more than the low-margin appendage the current segment numbers show.

And now the counter-example, which balance demands we tell in full: Tejas Express. This was IRCTC's attempt to do something it had never done — not merely ticket a train, but operate one, as a semi-private service with IRCTC bearing the commercial risk. Two Tejas routes launched with fanfare. Both bled money for three straight years. The Ahmedabad–Mumbai Tejas, for instance, reportedly lost around ₹2.9 crore, then about ₹16.4 crore, then roughly ₹16 crore in successive years before operations were suspended in November 2020.13 Part of the problem was self-inflicted: a dynamic-pricing model that, on peak days, pushed Tejas fares above the airfare for the same route — asking price-sensitive rail passengers to pay a premium to the plane.13 The pandemic delivered the final blow, but the losses predated it.

Sit with the dynamic-pricing detail for a moment, because it is more revealing than the losses themselves. Airlines invented surge pricing for a good reason: a plane seat is perishable inventory with a hard departure deadline, and yield-management software squeezes the last rupee out of it. IRCTC imported that logic to a train — but a train competes on a completely different value proposition. People choose rail over air precisely because it is cheaper, more flexible, and does not require airports. Pricing a premium train above the plane on busy days did not just lose money; it revealed a conceptual misread of who the customer was and why they were on the platform in the first place. That is the kind of error a seasoned competitive operator, scarred by real market feedback, tends not to make — and it is exactly the kind of error an organization accustomed to captive, price-inelastic demand might make when suddenly asked to win customers on the merits.

Why does a suspended train with a rounding-error P&L matter so much? Because it is the one clean, uncontaminated data point on IRCTC's ability to run a business outside its regulatory monopoly. Inside the monopoly, the mandate does the work and execution quality is hard to isolate. Tejas stripped that away and asked a simple question — can IRCTC compete on price, service, and demand forecasting when it is not the only option? — and the answer, on the available evidence, was no. That should shape how much credit an investor extends to any future unprotected venture: the floated idea of a hotel-sector entry, new tourism formats, international expansion. Treat each as unproven until there is a second, more successful data point. The tourism wave may well work because it rides the network rather than competing head-on. But the moment IRCTC has to out-execute a real rival rather than ride a mandate, the track record is one loss. That asymmetry — protected businesses that print money, unprotected ones that have struggled — is the crux of how to think about who runs this company, which is next.

VII. Current Management: Incentives, Continuity, and Credibility

Here is the structural fact that should govern how you weigh everything management says: IRCTC has no founder, no owner-operator, and no leader with meaningful personal equity in the outcome. The Chairman and Managing Director is a career Indian Railway Traffic Service officer on a fixed-term government posting. There is no visionary-founder story to tell, no "skin in the game" narrative, no equity-aligned operator betting their net worth on the next decade. That absence is not a scandal — it is simply the nature of a central public-sector enterprise — but it must recalibrate how much weight you place on any single leader's "vision," and it should push your attention toward the things that are observable: operational execution, guidance discipline, and how candidly management explains a miss.

The current occupant of the chair is Sanjay Kumar Jain, a 1990-batch IRTS officer and a chartered accountant, who took charge as CMD in February 2024.14 During his tenure, IRCTC was upgraded from Schedule B to Schedule A and elevated to Navratna status, and it posted record financials, with FY26 revenue reaching roughly ₹5,215 crore.143 But the live, unresolved development — the one an investor tracking this company in mid-2026 cannot ignore — is that Jain resigned on personal grounds, and the Ministry of Railways accepted the resignation effective July 20, 2026.14 The company disclosed that the Ministry would issue separate orders assigning interim additional charge for the CMD post until a permanent successor is named.14 So as this is written, IRCTC is days away from a leadership vacuum at the top, to be filled — as is the PSU custom — by bureaucratic appointment rather than a planned internal succession.

The predecessor context matters mainly to establish the pattern. Rajni Hasija, who led IRCTC before this period, is credited in the business press with steering an earlier operational turnaround, particularly on the tourism and catering side.15 But notice what the sequence reveals: continuity at IRCTC comes not from a single enduring operator but from the bureaucracy itself — a rotating cast of career officers, each on a fixed tenure, with the institution carrying the strategy across handovers. This is a fundamentally different credibility test than a founder-led firm. You are not betting on one person's genius compounding over twenty years. You are betting on the durability of an institutional mandate and the competence of whichever capable administrator the system next installs.

This structure cuts both ways, and an honest assessment holds both edges. On the reassuring side, a mandate-driven institution is less exposed to key-person risk than a founder-led firm: no single departure can gut the strategy when the strategy is, in effect, "operate the monopoly competently and grow the tourism book." The business does not depend on one person's irreplaceable insight. On the worrying side, fixed tenures create short horizons. A CMD posted for a few years has limited incentive to make bets that pay off a decade out, and every genuine reason to optimize for the metrics that look good during their watch — revenue growth, headline profit, a Navratna upgrade to put on the résumé. There is no equity vesting over ten years to align a leader with the long arc; the incentive is bureaucratic advancement, set by government pay committees, not shareholder value compounding. When you evaluate any strategic ambition management voices — hotels, international tourism, new train formats — factor in that the person announcing it may well have rotated out before the results are in. Accountability in such a structure is inherently diffuse, which is exactly why the observable behaviors — guidance kept or missed, misses explained honestly or fudged — carry so much weight. They are the only real scorecard.

That reframing tells you exactly where to point the microscope: not at grand strategy, but at execution and honesty in the numbers. And that is where the current moment gets interesting. On the FY25 earnings call in May 2025, management laid out specific FY27 growth targets across the segments.16 An investor should now hold those targets against what actually printed — and, more pointedly, watch how management explains the March 2026 quarter, where profit fell almost 9% even as revenue grew 15%.3 The credibility tell is simple. Does management name a specific, controllable driver — a mix shift toward lower-margin catering, a defined input-cost spike, a one-time payment to the railway authority, a higher effective tax rate — or does it wave at "macro conditions" and "cost pressures" without pinning the cause? Independent analysis of the quarter could only attribute the compression to unspecified "systemic cost pressures," which is precisely the kind of vagueness a skeptical investor should want management to replace with specifics on the next call.3 In a company with no owner-operator alignment, the quality of that explanation is one of the few real windows into management accountability. Which raises the question of who, if anyone, is competing for IRCTC's economics — and where the company is genuinely exposed.

VIII. Competitive Landscape: A Monopoly at the Core, Real Competition at the Edges

War-game IRCTC's competitive position and you quickly discover you are fighting on two completely different battlefields with two completely different rulebooks. On the first — the core supply layer of ticket issuance, onboard catering, and station water — there is no battle at all. There is no licensed competitor, and there cannot be one, because the mandate is exclusive. This is not a hard-won position; it is a legal fact. Any competitive analysis of the core is therefore short: the incumbent cannot be dislodged by a better product because a better product is not permitted to reach the field.

The second battlefield — the distribution layer — is where things get genuinely competitive, and it is widely misunderstood. When you book a train ticket through MakeMyTrip, ixigo, or Cleartrip, you might think you are using an IRCTC competitor. You are not, at least not where it counts. Every one of those bookings still routes through IRCTC's system for the actual ticket issuance; the online travel agencies compete for the customer relationship and the convenience layer on top, not for the underlying processing economics.11 MakeMyTrip holds roughly half of India's overall online-travel market, and in rail bookings specifically ixigo has built a commanding share of the OTA rail niche, with Cleartrip pushing further into train bookings.11 But their success is a fight over who owns the front-end relationship with the passenger — and who collects the convenience economics on that relationship — while IRCTC keeps the back-end toll. As one incisive analysis put it, the OTAs and payment aggregators simply cannot escape the IRCTC "bogie-man": they are structurally dependent on the very platform they appear to compete with.11 It is a distribution fight, not an existential one.

But do not dismiss that fight as irrelevant to IRCTC, because it has a subtle economic edge. The OTAs are effectively arguing, over time, that they deserve a slice of the convenience economics for owning the customer, the app experience, the fare alerts, and the loyalty relationship — while IRCTC keeps the mandated processing fee. ixigo in particular built a large share of the rail-booking niche not by circumventing IRCTC but by wrapping a slicker, faster, more forgiving interface around it, monetizing the passenger through ancillary services and advertising that IRCTC's utilitarian portal never captured.11 The strategic question this raises for IRCTC is whether, over a decade, the passenger relationship migrates decisively to third-party front-ends, leaving IRCTC as an invisible back-end utility — profitable, but commoditized and stripped of any ability to upsell tourism, hotels, or premium services to a customer it no longer "owns." That is not a threat to the ticket-processing monopoly. It is a threat to IRCTC's ambition to be more than a toll booth. The two things are easy to conflate and important to keep apart.

There is, however, exactly one arena where IRCTC competes on level, unprotected ground: tourism. Its holiday packages, pilgrimage circuits, and hotel-and-air bundles go head-to-head with MakeMyTrip, Yatra, Thomas Cook India, and a long tail of operators for the same discretionary spend. Here IRCTC has no mandate, no exclusivity, and — candidly — a far weaker position than in its monopoly lines. The thin segment margins we saw earlier are partly the signature of that real competition. This is the honest way to size tourism: a genuine, competitive, small business with real growth potential, not an extension of the moat. Conflating the two is the most common error in the bull case.

Return to Porter's Five Forces for the synthesis, because it clarifies where the actual threat lives. Rivalry is nonexistent at the core and fierce in tourism. Buyer power is nil for ticketing, moderate for tourism. Supplier power — Indian Railways — is absolute. And the threat of new entry is not commercial but political: the only thing that can introduce competition into IRCTC's protected lines is a policy decision to license private operators. India has flirted with exactly this before — a 2020 tender invited private players to run passenger trains on a hundred-plus routes — even though it has not, to date, touched IRCTC's specific exclusivities on ticketing, catering, or water. The lesson stands: for this company, the competitor that matters does not sit in a boardroom in Gurgaon. It sits in the Ministry of Railways. And that reframes the entire risk map.

IX. Risk Radar: What Could Actually Break the Thesis

The temptation with a monopoly is to assume the risks are trivial. IRCTC's risks are real; they just do not look like a normal company's risks, and they cluster in unusual places.

Policy and regulatory reversal is the single largest risk, full stop. The government that created the monopoly can reprice or dilute it, and the 2021 convenience-fee episode is the proof of concept — a decision that, had it stood, would have permanently impaired the crown-jewel segment's economics.9 The instructive historical analogy is India's state telecom monopolies, MTNL and BSNL, which were reliably profitable until liberalization ended their protection and exposed them to real competition, after which they struggled for survival. IRCTC is not MTNL — rail exclusivity is far more entrenched than telephony ever was — but the mechanism is identical: a protected PSU's earnings power is only as durable as the policy fence around it. An investor who models IRCTC's regulated cash flows as "safe" without pricing this in has mis-specified the risk.

The cybersecurity and fraud arms race is a persistent, escalating operational cost. Bot-driven scalping of Tatkal (last-minute quota) tickets is a chronic problem, and the scale of the countermeasures tells you how serious it has become: IRCTC has reported deactivating tens of millions of suspicious user IDs and blocking billions of malicious bot requests, deploying an AI-based detection system built with academic researchers to fight back. This is not a one-time fix; it is a permanent, compounding cost and a standing reputational exposure. A visible failure here — a booking system gamed so badly that ordinary passengers cannot get tickets — damages public trust in the very platform that is the monopoly. The moat and the fraud target are, once again, the same object.

There is a political dimension to this that a purely financial analysis would miss. Because IRCTC is a state entity handling a mass-transit necessity, a booking-system failure is not merely a customer-service problem; it becomes a parliamentary and media event, the kind of thing that generates ministerial statements and public anger. That elevates cybersecurity from an IT line item to a reputational and quasi-political risk. It also, perversely, cuts against the company commercially: the more IRCTC clamps down on bots and scalpers, the more friction ordinary users experience — captchas, verification steps, tighter Tatkal rules — which is precisely the friction that pushes some passengers toward the smoother third-party OTA front-ends discussed earlier. Fighting fraud well and keeping the user experience frictionless are in genuine tension, and IRCTC has to manage both under a public microscope that a private company would never face. It is a standing operating cost with no finish line, and it is the kind of unglamorous liability that "it's a monopoly, it prints money" narratives conveniently ignore.

Execution risk in diversification has already been demonstrated once. Tejas Express is the cautionary precedent for any venture where IRCTC operates rather than merely tickets, and the same skepticism should apply to the floated hotel-sector entry and any new tourism format until real unit economics appear.13 The Navratna autonomy makes it easier for management to write larger cheques into unproven ventures — which is a benefit only if the execution muscle exists, and the one clean test to date suggests caution.

The margin-compression signal is the newest entry on the radar and the one that most deserves live monitoring. The March 2026 quarter's divergence — revenue up 15%, profit down nearly 9%, PAT margin falling from about 27% to 22% — needs a clear, named explanation.3 If the next couple of quarters attribute it to a defined, controllable driver, it is likely a blip. If the explanation stays vague or shifts to macro blame, that is a governance and credibility flag in the standard PSU playbook.

Finally, two lower-order items worth tracking as pattern rather than magnitude. IRCTC has faced minor compliance friction — a GST show-cause notice of roughly ₹3.93 crore relating to an earlier year, and an income-tax demand in the tens of lakhs for a recent assessment year — each financially immaterial on its own but collectively a small input on governance hygiene. And the leadership transition: the CMD's departure effective July 20, 2026 creates near-term interim uncertainty.14 Given the bureaucratic-continuity model, it is not thesis-breaking. But for anyone underwriting near-term execution, an unfilled top job during a margin wobble is not the ideal configuration. Put all of it together and a coherent bull-and-bear picture emerges.

X. Bull vs. Bear

The bull case is clean and, on its own terms, strong. IRCTC owns a legally protected monopoly on a captive, structurally growing volume base — India's rail ridership rises, the premium-train rollout accelerates, and IRCTC processes all of it. The ticketing engine carries near-zero marginal cost, so incremental volume converts to profit at exceptional rates and can drive margin expansion over time, as the near-90%-margin segment economics demonstrate.17 On top of that durable base sits a genuine multi-year growth option — the Vande Bharat Sleeper, Amrit Bharat, and Bharat Gaurav trains feeding a tourism segment that rides network expansion rather than fighting for share, with the Maharajas' Express proving the segment can reach premium, high-margin customers. Navratna status adds capital-allocation autonomy, the dividend payout is high and PSU-generous, and if the FY27 guidance is met, a re-rating case exists; the most bullish sell-side targets have run well above the current price on exactly that logic.

The bear case is equally coherent and, crucially, is not the mirror image of the bull case — it attacks a different axis. The bull argues about growth and margins; the bear argues about ownership and control. The moat is a government favour, not an earned advantage, and October 2021 proved it can be repriced without warning.9 The March 2026 quarter shows margin pressure arriving even as revenue grows, undercutting the "margins only expand" premise.3 Management operates on fixed tenure with bureaucratic incentives and no owner-operator alignment, and the top seat is, as of this writing, about to turn over with no named successor.14 The one time IRCTC tried to run a competitive business outside its monopoly — Tejas — it failed.13 And the single growth vector everyone points to, tourism, is also the only segment facing real competition, where IRCTC is a weak player. Bearish targets have sat far below the bull case, reflecting a view that much of the stock's valuation rests on sentiment and institutional flows rather than fundamentals alone.

It is worth asking what a genuinely skeptical activist — the short-selling kind who writes forty-page decks — would attack here, because the answer is instructive precisely for how little of it is the usual fare. There is no leverage to speak of; IRCTC runs an almost debt-free, cash-generative balance sheet. There is no sprawling conglomerate of related-party transactions to untangle, no opaque subsidiaries hiding losses, no aggressive revenue recognition — the accounting is, by all appearances, clean and simple. The classic activist playbook mostly misfires. What a sharp critic would instead zero in on is threefold: first, disclosure and governance asymmetry — a controlling shareholder who is also the regulator, with the 2021 episode as Exhibit A that minority interests can be subordinated to fiscal convenience; second, capital allocation by default — a company returning cash largely because it lacks the demonstrated ability to reinvest it at high returns outside the mandate, dressed up as shareholder friendliness; and third, the quality of the growth narrative — the risk that "tourism will compound at 20%" is a story sold to justify a premium multiple while the segment remains structurally thin-margined and competitively exposed. None of those are fraud. All of them are reasons to demand a discount to the multiple a "clean compounder" would earn.

Run it through the two analytical frameworks and the verdict is nuanced. In Helmer's terms, IRCTC has exactly one Power — a Cornered Resource — and it is a powerful one, but Cornered Resources held at the pleasure of a controlling regulator are a fragile species of the genus. In Porter's terms, the company is insulated from every competitive force except the two that matter most here: supplier power and the political threat of entry, both embodied in the same sovereign owner. There is no Network Economies flywheel, no Counter-Positioning, no Brand power doing meaningful work. The moat is one wall, very high, that the landlord can lower.

The honest synthesis: IRCTC is less a "growth compounder" and more a "regulated utility with a call option." The base monopoly cash flow is durable for as long as policy holds — that is the utility. The tourism-and-premium-train wave is the option value on top. What an investor is really underwriting is not competitive dynamics, market share, or product superiority. It is government policy continuity, and the government's ongoing willingness to treat minority shareholders as a constraint worth respecting rather than a source of cash worth tapping. Everything else is secondary. That framing yields some durable lessons.

XI. Durable Business & Investing Lessons

IRCTC is a case study precisely because its economics and its risk profile are so mismatched to intuition, and a few lessons generalize well beyond this one stock.

First, a government-granted monopoly can produce truly excellent unit economics while carrying a risk profile that looks nothing like a normal moat. The ticketing segment's margins would be the envy of most software companies, yet the durability of those margins depends on a policy decision, not on customer love or switching costs. The discipline this demands is to model policy risk explicitly — as its own line in the analysis — rather than mentally filing regulated cash flows under "safe." Safe from competitors is not the same as safe from your own controlling shareholder.

Second, watch what a company does the one time it steps outside its protected lane. Tejas Express is worth more, analytically, than its trivial P&L, because it is the only clean read on management's operating skill absent the mandate. When a business is protected, you cannot tell whether results come from execution or from the moat doing the work. The unprotected experiment is where the truth leaks out — and here it argued for humility about IRCTC's ability to win a fair fight.

Third, in state-controlled companies, the market can occasionally act as a fast, effective check on the majority owner. The 19-hour reversal in 2021 is a rare, almost pristine example of price discipline working without a formal activist — the stock's collapse was the activist campaign, and it succeeded overnight. That is a genuinely useful thing to know about how sovereign owners of listed entities behave when confronted with the cost of their own decisions. It is not a guarantee. But it is evidence that even a majority state owner is not entirely indifferent to the share price.

Fourth, segment-level materiality discipline is everything. The easy narrative lets the small, fast-growing, exciting segment — tourism — dominate the story, when a much larger, slower segment (catering) and a much higher-margin segment (ticketing) are doing the real economic work. Get the proportions wrong and you will misprice the whole company. The most important skill in analyzing IRCTC is refusing to let the loudest segment become the biggest number in your model. With the lessons drawn, the practical question is what to actually monitor from here.

XII. What to Watch Going Forward

If you track only a handful of things on IRCTC, track these. The internet-ticketing segment profit margin is the clearest read on the core engine — it is where near-all of the profit is made, and any erosion there (from a convenience-fee change, a mix shift, or a cost surprise) matters more than movement in any other line.17 Second, tourism segment revenue growth and, critically, its profitability against the roughly 20% growth ambition — this is the direct test of the option-value thesis, and the segment's thin margins mean growth alone is not enough; it has to become more profitable to justify the narrative weight placed on it.16 Third, the catering segment's margin trend, because it is the largest revenue base and the most exposed to food-input inflation and outsourced-labour costs — and it is the prime suspect in the March 2026 margin compression.3

On catalysts and near-term watch-items: the resolution of the CMD succession after July 20, 2026; the next one or two quarters' explanation for the margin divergence — specifically, whether management replaces "systemic cost pressures" with a named, controllable cause; and any concrete move on the floated hotel-sector entry or other Navratna-enabled capital deployment, which will be the first real test of whether the new autonomy is used with discipline or drifts toward the kind of unprotected venture that Tejas warned against.

One further discipline is worth adopting for anyone following this name across quarters: read the segment table, not the headline. IRCTC's consolidated numbers can mislead in either direction because the engines move independently — a strong catering quarter can flatter revenue while margins quietly compress, and a soft-looking top line can mask a ticketing segment still minting cash. The single most information-rich page in each result is the segment breakdown, where the ticketing segment's profit margin either holds its remarkable level or begins to slip. Pair that with management's commentary on the earnings call — specifically whether the explanations for any margin move are concrete and mechanism-based or vague and macro-flavored — and you have a far better read on the business than the profit-after-tax figure the newspapers print. The 2021 shock, the 2026 margin wobble, and the leadership change are all, in the end, variations on the same instruction: watch the parts, watch the policy, and treat the consolidated headline as the least interesting number in the release.

The closing frame is the one to carry out the door. IRCTC's next decade will be decided far less by competitive strategy than by two forces largely outside the company's control: how India's rail network and its premium-train rollout expand — the tide that lifts every one of IRCTC's engines — and whether the government continues to treat its minority shareholders as a constraint it respects rather than an afterthought it can tap. The business will keep printing monopoly cash flow as long as the policy fence holds. The interesting question, and the one no earnings call can fully answer, is whether the people who built the fence will always choose to leave it standing.

References

-

IRCTC reports robust Q4 FY25 performance, net profit soars 26% to ₹358 crore — BW Businessworld, 2025 ↩↩

-

IRCTC Q4FY25 segment-wise revenue analysis — Medianama, 2025-06 ↩↩

-

IRCTC Q4 FY26: Profit slips despite revenue growth as margins contract — MarketsMojo, 2026-05 ↩↩↩↩↩↩↩↩↩↩

-

State-run IRCTC delivers India's best trading debut in 2 years — TechCrunch, 2019-10-14 ↩

-

IRCTC share delivers more than 100% returns on market debut — Business Today, 2019-10-14 ↩↩

-

Railway Ministry withdraws decision on sharing IRCTC convenience fee, shares recover losses — National Herald India, 2021-10-29 ↩↩↩↩↩

-

Reversal of IRCTC convenience fee: DIPAM, the new protector of minority investors? — Forbes India, 2021 ↩↩↩

-

Payments companies, OTAs can't escape the IRCTC bogie-man — The Ken ↩↩↩↩↩

-

Centre grants 'Navratna' status to IRCTC and IRFC — Business Standard, 2025-03-03 ↩↩

-

Halting of Tejas Express raises doubts on viability of private trains — Business Standard, 2020-11-22 ↩↩↩↩

-

IRCTC CMD Sanjay Kumar Jain resigns; railways ministry accepts exit effective July 20 — Business Today, 2026-06-24 ↩↩↩↩↩↩

-

How Rajni Hasija spearheaded IRCTC's turnaround — Business Today, 2024-04-01 ↩

-

IRCTC Q4 & FY25 earnings call transcript, 2025-05-29 — Trendlyne ↩↩↩

-

IRCTC Q3 FY26 results: net profit surges 22% to ₹325 crore; declares second interim dividend of ₹3.50/share — Indian Masterminds, 2026-02 ↩↩↩↩↩

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube