IRCON International: India's Infrastructure Export Machine

I. Introduction & Episode Roadmap

Picture this: It's 2016, and in the dusty heat of Iran's Makran coast, Indian engineers are surveying the ancient trade route that once connected Persia to the Indian subcontinent. They're not archaeologists—they're from IRCON International, and they're about to undertake one of the most geopolitically significant infrastructure projects of the decade: the Chabahar-Zahedan railway line. This 628-kilometer stretch of track would become India's strategic gateway to Afghanistan and Central Asia, bypassing Pakistan entirely. The project embodied everything IRCON had become over four decades: technically ambitious, geopolitically complex, and quintessentially Indian in its global ambition.

Today, IRCON International stands as a fascinating paradox in India's corporate landscape. With a market capitalization of ₹15,720 crores, annual revenues exceeding ₹10,259 crores, and operations spanning 31 countries, it's simultaneously a government-owned public sector undertaking and a globally competitive infrastructure powerhouse. The company has completed over 1,650 major projects domestically and 900 internationally—from building railways in war-torn Sri Lanka to constructing bridges in Malaysia's tropical rainforests.

But here's what makes IRCON truly intriguing for investors and business historians alike: How did a railway construction unit, born from the bureaucratic corridors of India's Railway Board in 1976, transform into an infrastructure export machine that competes with global engineering giants? How does a company maintain its entrepreneurial edge while being 65% owned by the Government of India? And perhaps most critically, why has its stock fallen 40% from its all-time high despite India's unprecedented infrastructure boom?

The IRCON story isn't just about building railways and highways—it's about institution-building in post-independence India, the delicate dance between public service and commercial ambition, and the evolution of Indian engineering capabilities from domestic execution to global excellence. It's a tale that spans from the socialist planning era of the 1970s through liberalization, privatization waves, two IPOs, a delisting, and emergence as a Navratna PSU.

This deep dive will unpack IRCON's remarkable journey through distinct phases: its origins as Indian Railways' construction arm, the bold diversification moves of the 1990s, the curious case of its IPO-delisting-re-IPO saga, its transformation into an international contractor competing in 25+ countries, and its current position navigating margin pressures while sitting on a ₹20,973 crore order book. We'll explore the playbook of building national champions, the economics of infrastructure execution in difficult terrains, and what IRCON's trajectory tells us about India's infrastructure ambitions and the evolving role of PSUs in a market economy.

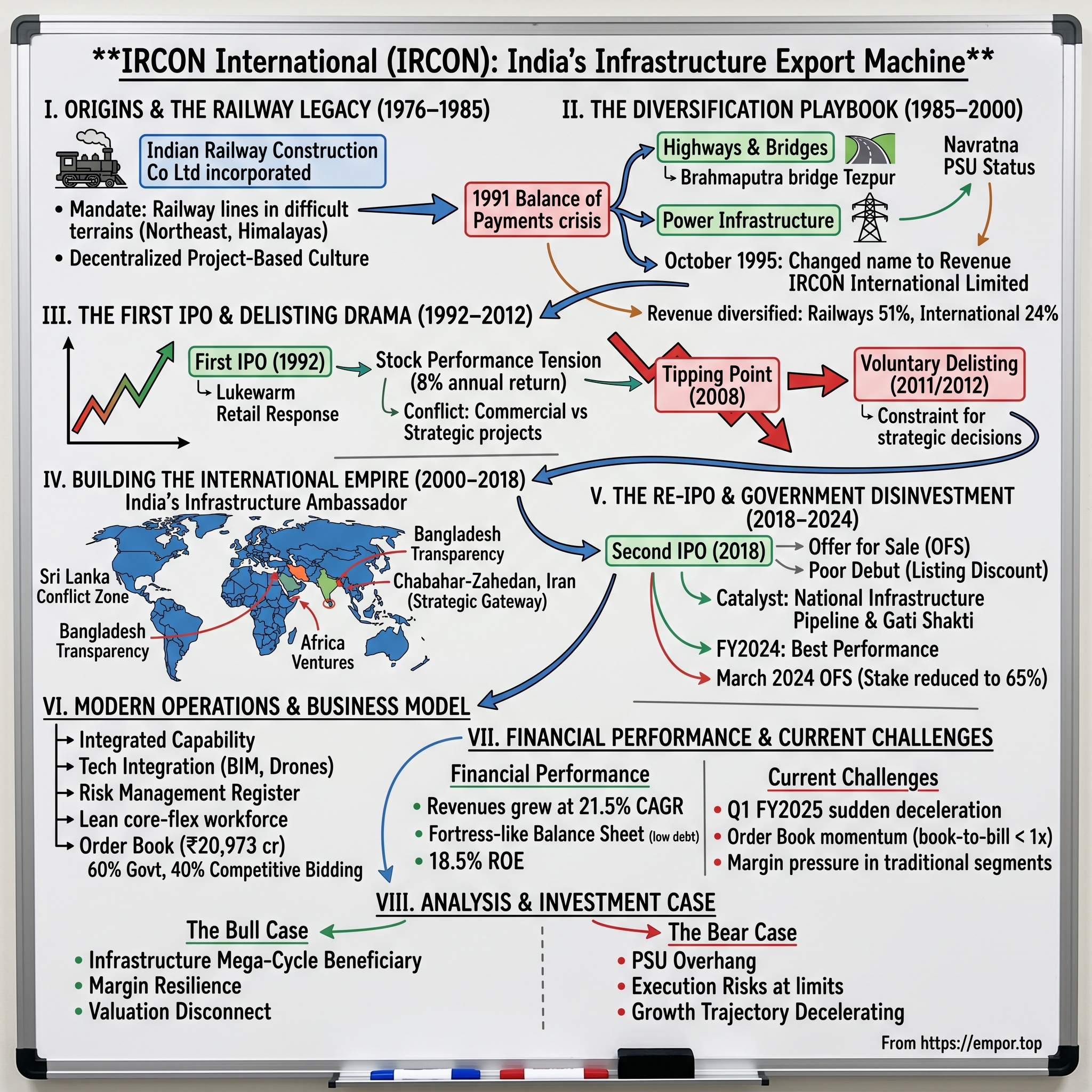

II. Origins & The Railway Legacy (1976–1985)

The year was 1976. India was emerging from the tumultuous period of the Emergency, inflation was running at 25%, and the nation's railway network—the lifeline of its economy—was creaking under the weight of deferred maintenance and underinvestment. The Indian Railways, operating 11,000 trains daily and moving 13 million passengers, faced a critical challenge: how to rapidly expand and modernize infrastructure while its engineering departments were already stretched thin maintaining existing operations.

Enter M.S. Gujral, then Chairman of the Railway Board, who proposed something radical for socialist India: create a commercial entity, structured as a company under the Companies Act rather than a government department, dedicated solely to railway construction. The logic was elegant—separate execution from operations, bring commercial discipline to project management, and create an entity that could eventually take Indian railway engineering expertise abroad. On April 28, 1976, Indian Railway Construction Company Limited was incorporated, later renamed IRCON International.

The early mandate was deceptively simple yet technically daunting: build railway lines where others couldn't or wouldn't. This meant the treacherous terrains of the Northeast, where insurgency mixed with geological challenges; the scorching deserts of Rajasthan, where sand dunes shifted overnight; and the Western Ghats, where gradients defied conventional rail engineering. IRCON's first major project—the Jammu-Udhampur rail link—exemplified these challenges. The 53-kilometer stretch required boring through the young, unstable geology of the Himalayas, with 158 bridges and 20 tunnels. Local contractors had walked away from the project twice.

What set IRCON apart from the beginning was its hybrid DNA. Unlike typical PSUs that operated with bureaucratic lethargy, IRCON recruited directly from India's top engineering colleges, offering project-based incentives unheard of in government service. The founding team, led by S.B. Mohapatra as the first Managing Director, established a culture that would define IRCON for decades: technical excellence over bureaucratic protocol, field experience over desk jobs, and solution-finding over excuse-making.

The organization structure itself was revolutionary for a PSU. Instead of traditional departments, IRCON organized itself around projects, with each major construction site operating as a profit center. Project managers had unusual autonomy for government employees—they could hire local labor, procure materials within budgets, and make real-time engineering decisions without referring to headquarters. This decentralized model, borrowed from international construction giants like Bechtel, was radical for 1970s India.

By 1980, IRCON had completed its first international assignment—a 40-kilometer railway line in Iraq, ironically just before the Iran-Iraq war erupted. The project, executed in scorching heat with temperatures touching 55°C, taught IRCON invaluable lessons about operating in hostile environments. The Iraqi project team, led by a young engineer named R.K. Gupta (who would later become CMD), developed protocols for everything from managing local labor speaking Arabic to maintaining equipment in sandstorms—knowledge that would prove invaluable in future Middle Eastern ventures.

The technical capabilities IRCON developed in these early years were remarkable. Consider the Konkan Railway consultation project of 1984-85, where IRCON engineers pioneered the use of controlled blasting in the ecologically sensitive Western Ghats, minimizing environmental damage while maintaining construction pace. They developed indigenous solutions for tunnel ventilation in long bores, created new standards for track laying in high-rainfall areas, and innovated ballast-less track technology for bridges—innovations that would later become Indian Railways standards.

Financial discipline was embedded from inception. Despite being government-owned, IRCON operated on commercial principles—it had to bid for Railway Board projects, compete on price and timeline, and maintain its own profits and losses. The company turned profitable in its third year of operations, 1979, with a modest profit of ₹1.2 crores on revenues of ₹28 crores—a 4.3% margin that would become the baseline for future performance metrics.

The international vision was present from day one, unusual for a PSU in protectionist India. IRCON's memorandum of association specifically mentioned "undertaking construction projects abroad," and the company actively pursued international certifications and partnerships. By 1985, IRCON had executed projects in Iraq, Bangladesh, and Libya, earning precious foreign exchange when India's forex reserves could cover barely three weeks of imports.

But perhaps the most crucial development of this period was IRCON's emergence as a training ground for India's infrastructure talent. The company's policy of recruiting fresh engineers and putting them in charge of multi-crore projects within years created a generation of project managers who understood both technical execution and commercial discipline. Many would later seed India's private infrastructure boom, joining companies like L&T, GMR, and GVK.

By 1985, IRCON had grown from a ₹25 crore startup to a ₹200 crore enterprise, with 3,000 employees and projects across 15 Indian states and 4 countries. More importantly, it had proven that a PSU could operate with commercial efficiency while serving national objectives—a model that would inspire the creation of other infrastructure PSUs like RITES, IRCTC, and Rail Vikas Nigam. The foundation was set for IRCON's next phase: moving beyond railways into the broader infrastructure landscape.

III. The Diversification Playbook (1985–2000)

The trigger for IRCON's transformation came from an unexpected source: the 1991 balance of payments crisis. As India pledged its gold reserves and liberalization became inevitable, IRCON's leadership saw both threat and opportunity. The threat was obvious—private players would soon enter infrastructure construction, ending IRCON's quasi-monopoly in railway projects. The opportunity was less obvious but more profound—India would need massive infrastructure beyond just railways, and IRCON had capabilities that could translate across sectors.

K.L. Dhingra, who took over as CMD in 1989, was an unusual choice—a civil engineer who had spent years in Bihar's troubled coal belt, managing construction projects amid Naxalite violence. His first board meeting set the tone: "We can either remain Indian Railway Construction Company and slowly become irrelevant, or we can become India's infrastructure company and thrive." The board chose transformation.

The diversification strategy was methodical, not scattershot. IRCON identified adjacencies where its core competencies—project management in difficult terrains, handling government contracts, managing large workforces—would provide competitive advantage. Highways were the obvious first step. The company's first major highway project, the 65-kilometer Hospet-Hubli section in Karnataka (1991), showcased this translation of skills. IRCON applied railway project management principles to road construction: detailed soil surveys every 500 meters (unusual for highways then), multilayer quality control, and milestone-based execution that delivered the project three months ahead of schedule.

The real breakthrough came with bridges. IRCON engineers realized that railway bridge technology—designed to handle massive dynamic loads and vibrations—was over-engineered for highways. They could build road bridges faster and cheaper than traditional highway contractors while maintaining superior quality. The Brahmaputra bridge at Tezpur (1993), a 3.2-kilometer marvel completed in record time, established IRCON as a serious bridge contractor. The project introduced several innovations: pre-fabricated segments manufactured during monsoons when river work was impossible, a floating bailey bridge for construction access, and pioneering use of epoxy-coated rebars for corrosion resistance.

Power infrastructure became the third pillar of diversification. In 1994, IRCON ventured into Extra High Voltage (EHV) substations, starting with a 400KV facility for NTPC in Rihand. This wasn't random diversification—railway electrification had given IRCON deep expertise in power systems, and EHV substations were essentially industrial-scale versions of railway traction substations. The company's ability to handle both civil and electrical works as an integrated package became a unique selling proposition.

October 1995 marked a symbolic milestone: the company formally changed its name to IRCON International Limited, dropping "Railway Construction" to reflect its broader mandate. But the transformation went deeper than rebranding. IRCON restructured itself into Strategic Business Units (SBUs): Railways, Highways, and Infrastructure (covering everything else). Each SBU had its own P&L responsibility, competed for capital allocation, and maintained separate project management protocols suited to its sector.

The international expansion during this period was equally strategic. IRCON didn't chase projects randomly across the globe but focused on corridors where Indian diplomatic influence provided entry and payment security. The Malaysia highway project (1996) exemplified this approach. When Malaysian Prime Minister Mahathir Mohamad visited India, IRCON was positioned as India's infrastructure ambassador. The company won a $47 million contract to build the Kuala Lumpur-Seremban highway section, competing against Japanese and Korean firms. IRCON's winning edge? Its engineers had experience working in similar laterite soils in Kerala and could guarantee minimal settlement—a critical concern in Malaysia's tropical environment.

The Sri Lankan railway rehabilitation projects (1995-2000) showcased another dimension of IRCON's capabilities: working in conflict zones. While the civil war raged, IRCON rebuilt the Colombo-Matara coastal line, often working under military protection, evacuating sites during fighting, yet maintaining construction schedules. The company developed protocols that would later become standard operating procedures for conflict-zone projects: duplicate supply chains, local community engagement to prevent sabotage, and modular construction allowing quick assembly and disassembly.

Technology adoption accelerated during this period. IRCON became one of the first Indian construction companies to implement PRIMAVERA project management software across all major sites (1997). The company established India's first fully computerized concrete batching plant for infrastructure projects in Konkan. It pioneered the use of Ground Penetrating Radar for utility detection in urban projects, reducing costly surprises during excavation.

The numbers tell the transformation story. Revenue grew from ₹201 crores in 1990 to ₹1,847 crores in 2000—a 9x increase. More importantly, the revenue mix shifted dramatically: railways contributed 82% in 1990 but only 51% by 2000. International operations expanded from 8% to 24% of revenues. The order book diversified even more dramatically—by 2000, IRCON was executing metro rail projects, airports, institutional buildings, and even ship-breaking yards.

In 1998, IRCON achieved another milestone: Mini Ratna Category-I status from the government, granting it enhanced autonomy in operations and investments. This wasn't just bureaucratic recognition—it came with tangible benefits like faster decision-making, higher capital expenditure powers, and ability to form joint ventures without extensive government approvals.

The human capital transformation was equally remarkable. IRCON established its own training institute in 1992, unusual for a construction company. Beyond technical training, it focused on developing project managers who could handle the soft skills crucial for international projects: cross-cultural communication, stakeholder management, and crisis handling. The company introduced a unique "shadow posting" system where high-potential managers would spend six months on international projects before taking independent charge—creating a pipeline of globally competent leaders.

By 2000, IRCON had evolved from a railway construction PSU to something unprecedented in India's corporate landscape: a globally competitive, multi-sector infrastructure company that happened to be government-owned. With operations in 15 countries, capabilities spanning the entire infrastructure spectrum, and a proven ability to execute in the most challenging environments, IRCON was ready for its next evolution—entering the capital markets to fuel further growth.

IV. The First IPO & Delisting Drama (1992–2012)

The boardroom at Rail Bhawan was unusually tense on a humid July morning in 1992. IRCON's directors were debating a proposal that seemed almost heretical for a PSU: going public. The government needed money—the forex crisis had emptied coffers—but IRCON's IPO represented something more profound. It would be among the first infrastructure PSUs to tap capital markets, setting precedent for how government companies could access growth capital while maintaining strategic control.

The IPO prospectus, filed in September 1992, revealed a company in transition. IRCON was offering 20% equity to the public at ₹10 per share, seeking to raise ₹48 crores. By PSU standards, the financials were impressive: revenues of ₹456 crores, net profit of ₹19 crores, and an order book of ₹890 crores. But the real story was in the details. Unlike typical PSUs that went public under government pressure, IRCON actually needed the capital. The company had identified infrastructure opportunities worth ₹3,000 crores but lacked resources to bid for them.

The retail response was lukewarm—the issue was subscribed just 1.3 times. India's capital markets in 1992 were still reeling from the Harshad Mehta scam, and investors were skeptical of PSU offerings. But institutional investors, particularly LIC and UTI, saw value in IRCON's unique position as India's only integrated infrastructure contractor with international operations. The stock listed on BSE at ₹11.50, a modest 15% premium, on December 23, 1992.

Being a listed PSU created peculiar challenges. IRCON now answered to three masters: the Railway Ministry (its administrative ministry), the Finance Ministry (as owner), and public shareholders (seeking returns). Quarterly earnings calls became exercises in diplomatic communication. When asked about margin pressure from government projects, management would deflect with phrases like "national interest priorities" and "strategic considerations beyond pure commercials."

The real tension emerged in capital allocation. Public shareholders wanted IRCON to focus on high-margin international projects and selective domestic bidding. The government wanted IRCON to take up low-margin but strategically important projects like Northeast railway connections and border infrastructure. This conflict played out publicly in 1998 when IRCON's stock fell 30% after it accepted a barely-profitable project to build railway lines in Kashmir, a decision driven by strategic rather than commercial considerations.

Between 1992 and 2000, IRCON learned to navigate these contradictions with remarkable dexterity. The company developed a "portfolio approach"—balancing high-margin international projects with low-margin domestic ones, using profits from commercial projects to cross-subsidize strategic initiatives. This wasn't disclosed explicitly in annual reports, but savvy analysts could see it in segment reporting: international projects consistently showed 12-15% EBITDA margins while domestic railway projects barely touched 6%.

The stock performance reflected this tension. From 1992 to 2000, IRCON delivered a modest 8% annual return, underperforming both the Sensex (12%) and infrastructure peers like L&T (15%). Yet the company's fundamentals kept improving: revenue CAGR of 22%, order book growth of 25%, and successful entry into 12 new countries. The market clearly struggled to value a company that wasn't purely commercial nor purely governmental.

The 2000s brought new complications. Private infrastructure players, funded by PE money and IPO proceeds, began aggressively bidding for projects. Companies like GMR, GVK, and Reliance Infrastructure offered terms IRCON couldn't match while maintaining PSU prudence. IRCON's market share in highway projects dropped from 12% in 2000 to 7% by 2005. The stock languished between ₹30-40 for most of the decade, with daily volumes often below 10,000 shares.

The tipping point came in 2008. The global financial crisis had crashed infrastructure stocks, but IRCON faced a peculiar problem. The government's stimulus package included massive infrastructure spending, and IRCON was expected to execute projects at wafer-thin margins to support economic recovery. Simultaneously, private shareholders were demanding better returns as the company's stock traded at just 0.6x book value. The board meetings became battlegrounds between independent directors (representing minority shareholders) and government nominees.

V.K. Agarwal, who became CMD in 2009, proposed a radical solution: voluntary delisting. His argument was compelling. Being listed constrained IRCON's ability to take strategic decisions, created constant conflict between stakeholders, and the stock's illiquidity meant capital market access was theoretical anyway. The company could raise debt at PSU rates and didn't need equity capital. Most critically, delisting would free IRCON to pursue the government's infrastructure agenda without quarterly earning pressures.

The delisting process itself became a case study in PSU governance. IRCON offered ₹62 per share to minority shareholders, a 45% premium to market price but still below the book value of ₹78. Institutional investors protested, retail shareholders felt shortchanged, and proxy advisory firms criticized the process. Yet the delisting succeeded because most shareholders were exhausted by the stock's chronic underperformance.

IRCON delisted from BSE in September 2011 and from Delhi Stock Exchange in January 2012. The company paid out ₹312 crores to buy back shares from 47,000 public shareholders. It was an expensive divorce, but management believed it was necessary for IRCON's next phase of growth.

The immediate post-delisting period validated the decision. Freed from quarterly pressures, IRCON took on ambitious but low-margin projects: the Jammu-Kashmir rail link through treacherous terrain, strategically important but commercially unviable Northeast connections, and border infrastructure where security concerns overrode economics. The company also accelerated international expansion, entering Africa and Central Asia where project economics were uncertain but diplomatic benefits were clear.

Between 2012 and 2018, as an unlisted entity, IRCON transformed dramatically. Revenues grew from ₹3,200 crores to ₹8,100 crores, the order book expanded from ₹8,000 crores to ₹21,000 crores, and the company entered 10 new countries. Management could focus on capability building rather than quarterly earnings: establishing a design division, acquiring specialized equipment for tunnel boring, and developing expertise in metro rail systems.

Yet the delisting also had costs. IRCON lost access to equity capital just as India's infrastructure boom accelerated. The company couldn't participate in the consolidation wave where listed players acquired capabilities through M&A. Employee stock options, crucial for attracting talent in a competitive market, weren't possible. Most critically, IRCON's governance standards, while adequate for a PSU, didn't match listed company benchmarks—a gap that would become apparent during re-listing.

The six years as an unlisted entity (2012-2018) represented both IRCON's highest growth and its greatest strategic confusion. The company had solved its stakeholder conflict problem by eliminating public shareholders, but in doing so, had also removed market discipline and external pressure for efficiency. As 2018 approached and the government prepared for IRCON's second IPO, the question wasn't whether the company had grown—it clearly had—but whether it had evolved into an institution capable of balancing public purpose with market expectations. That test would come sooner than expected.

V. Building the International Empire (2000–2018)

The letter arrived at IRCON's headquarters on a scorching May afternoon in 2003, marked "Confidential" from the Ministry of External Affairs. Inside was an unusual request: Could IRCON rebuild Afghanistan's destroyed railway infrastructure? The Taliban had been ousted, and India wanted to establish strategic presence through development assistance. For IRCON, it represented the evolution from infrastructure contractor to instrument of soft power diplomacy.

The Afghanistan project crystallized IRCON's emerging role in India's neighborhood policy. The company wouldn't just build railways and roads abroad—it would become India's infrastructure ambassador, creating physical manifestations of Indian partnership in strategically important geographies. This wasn't the typical commercial expansion of a construction company; it was geopolitical engineering through concrete and steel.

The numbers tell only part of the story. By 2018, IRCON had completed 128 projects across 25 countries, generating cumulative international revenues exceeding ₹15,000 crores. But the real narrative was in the selection of geographies: Sri Lanka during civil war, Afghanistan under NATO protection, Bangladesh despite complex bilateral relations, Myanmar during military rule, and Iran under sanctions. These weren't markets that McKinsey would recommend in a strategy presentation—they were chosen through a matrix of diplomatic priority, strategic importance, and IRCON's unique ability to operate where others couldn't.

The Sri Lankan experience became IRCON's template for conflict-zone operations. Between 2000 and 2009, as the civil war reached its climax, IRCON executed projects worth $400 million, rebuilding the coastal railway line that LTTE had repeatedly destroyed. The project management protocols developed here were extraordinary: duplicate supply chains (one through Colombo, another through Trincomalee), construction crews that could evacuate within 30 minutes, modular equipment that could be dismantled and moved overnight, and deep engagement with local communities who could provide early warning of LTTE movements.

R.S. Sharma, who led the Sri Lankan operations, recalled a defining moment: "We were laying tracks near Batticaloa when shelling started. My instinct was to evacuate immediately, but our Sri Lankan workers said, 'Sir, if you leave now, you'll never come back.' We stayed, took cover, and resumed work after the shelling stopped. That earned us credibility no contract could specify." This human dimension—building trust in conflict zones—became IRCON's unique competitive advantage.

The Bangladesh railway projects (2005-2015) showcased different capabilities. Here, the challenge wasn't conflict but corruption and bureaucratic complexity. IRCON developed an innovative "transparent corridor" approach: all procurement was done through international competitive bidding with live streaming of bid openings, payments were made through escrow accounts monitored by both governments, and project progress was updated daily on public websites. This radical transparency made corruption virtually impossible and became a model for bilateral development projects.

But the crown jewel of IRCON's international portfolio was the Chabahar-Zahedan railway line in Iran, agreed upon in May 2016. This wasn't just a construction project—it was India's strategic gateway to Afghanistan and Central Asia, bypassing Pakistan. The 628-kilometer railway through Iran's restive Sistan-Baluchestan province would connect India's investment in Chabahar port to Afghanistan's mineral resources and provide an alternative trade route to Central Asia.

The technical challenges were staggering: construction through desert where temperatures touched 60°C, areas with no water sources for hundreds of kilometers, and a region where Sunni militants regularly attacked government forces. IRCON's solution was to create self-contained construction colonies—mini-cities that could operate independently for months, complete with water treatment plants, medical facilities, and satellite communications. The company even developed special concrete mixes that could cure in extreme heat, working with IIT Madras to create compositions that gained strength despite rapid moisture loss.

The geopolitical complexity was even greater. With U.S. sanctions on Iran, IRCON had to navigate payment mechanisms that wouldn't violate international restrictions. The solution—payments through rupee-rial arrangements and barter trades—required IRCON to become quasi-banker, managing currency risks and trade finances typically handled by specialized institutions. When U.S. sanctions intensified in 2018, IRCON had to suspend work, managing diplomatic fallout while protecting investments already made.

The African ventures (2010-2018) represented another evolution. In Ethiopia, IRCON built railway lines connecting landlocked regions to Djibouti port. In Mozambique, the company reconstructed colonial-era railways destroyed during civil war. These projects required IRCON to manage not just construction but complete ecosystem development: training local engineers, establishing maintenance protocols, and even helping develop regulatory frameworks for railway operations.

The innovation in international operations wasn't just technical but organizational. IRCON developed a "hub and spoke" model with regional offices in Colombo (for South Asia), Kuala Lumpur (for Southeast Asia), and Nairobi (for Africa). Each hub maintained equipment pools, technical experts, and government relations capabilities that could be deployed across the region. This reduced mobilization costs and time, making IRCON competitive against Chinese contractors who often won on price.

The company also pioneered "technology transfer" as a differentiator. Unlike Chinese companies that brought their own labor and left little local capability, IRCON invested in training local engineers and workers. In Bangladesh, IRCON established a railway training institute. In Sri Lanka, the company trained over 500 local engineers in modern construction techniques. This approach, while more expensive initially, created goodwill that translated into repeat contracts and government support during payment delays or contractual disputes.

Financial engineering for international projects became increasingly sophisticated. IRCON structured projects through SPVs in third countries to manage tax efficiency, used export credit agencies for financing, and developed innovative risk-sharing mechanisms with host governments. The company's treasury team, traditionally a back-office function in construction companies, became strategic partners in project development.

By 2016, IRCON had achieved something remarkable in global infrastructure: recognition by Engineering News Record as the 248th largest international contractor globally—the highest ranking for any Indian PSU. The company was competing against giants like Bechtel, Fluor, and China State Construction, winning projects through a combination of technical competence, diplomatic support, and ability to operate in challenging environments.

The international order book by 2018 told the strategic story: 40% of IRCON's ₹21,000 crore orders were from international projects, but they contributed 55% of profits. The company had successfully used international operations to subsidize strategic but low-margin domestic projects. More importantly, IRCON had become integral to India's infrastructure diplomacy, building not just railways and roads but relationships and influence.

Yet this international success created new challenges. IRCON's deep involvement in government-to-government projects meant commercial considerations often took backseat to diplomatic priorities. Payment delays from financially stressed nations accumulated. Currency fluctuations in frontier markets eroded margins. Most critically, the company's role as quasi-diplomatic entity constrained its ability to walk away from problematic projects or enforce contracts aggressively.

As IRCON prepared for its second IPO in 2018, the international portfolio was both its greatest strength and biggest uncertainty. The company had proven it could execute complex projects in challenging environments, but investors would question whether geographic concentration in South Asia (65% of international revenues) and exposure to financially weak nations was sustainable. The transformation from domestic railway contractor to international infrastructure player was complete, but the journey to becoming a commercially-driven global contractor while maintaining strategic responsibilities had just begun.

VI. The Re-IPO & Government Disinvestment (2018–2024)

The conference room at the Department of Investment and Public Asset Management (DIPAM) was buzzing with nervous energy on a September morning in 2018. Investment bankers from Axis Capital, IDBI Capital, and SBI Capital Markets were making final presentations for IRCON's second coming to the capital markets. This wasn't just another PSU disinvestment—it was a test case for whether the market would accept a company that had once rejected public shareholders returning for a second chance.

The context for the 2018 IPO was fundamentally different from 1992. India's infrastructure sector was experiencing unprecedented growth, with the government committing ₹111 lakh crores for infrastructure development through 2025. Private players were struggling with debt-laden balance sheets from the infrastructure boom-bust cycle of 2008-2015. IRCON, having stayed conservative during the bubble, emerged with a clean balance sheet, strong order book, and proven execution capabilities. The timing seemed perfect.

But the preparation revealed uncomfortable truths. During its years as an unlisted entity, IRCON's governance had atrophied. Board meetings had become formulaic approvals rather than strategic discussions. Related party transactions with other railway PSUs hadn't been scrutinized for commercial merit. Executive compensation, while modest by private standards, lacked performance linkage. The IPO process forced IRCON to modernize governance practically overnight—appointing independent directors with infrastructure expertise, establishing audit committees with real teeth, and creating transparent procurement policies.

The IPO structure itself was telling: ₹466.93 crores through an Offer for Sale (OFS) of 0.99 crore shares, with the government selling 10% stake. No fresh capital was raised for IRCON—this was purely a disinvestment exercise. The price band of ₹470-475 per share valued IRCON at ₹4,750 crores, implying a P/E of just 8x compared to L&T's 25x and NCC's 15x. The government was clearly leaving money on the table to ensure success.

The roadshow revealed investor concerns that would define IRCON's market journey. Fund managers questioned the sustainability of 15% order book growth when private players were becoming aggressive. They worried about execution risks in international projects, particularly the suspended Iranian railway. Most fundamentally, they wondered whether IRCON could maintain margins while fulfilling its PSU obligations to take strategic but unprofitable projects.

Management's answers were carefully crafted. CEO S.K. Vij emphasized IRCON's unique advantages: relationships with 15+ countries enabling negotiated contracts, technical expertise in difficult terrains where competition was limited, and cost of capital advantages from PSU status. He pointed to the ₹21,000 crore order book providing three years of revenue visibility and the company's track record of completing projects without major cost overruns.

The IPO opened on September 17, 2018, to mixed response. Institutional investors subscribed 2.5 times, but retail participation was lukewarm at 0.8x. The qualified institutional buyer (QIB) portion saw interesting patterns: domestic mutual funds were cautious, subscribing just 1.2x, while foreign institutional investors showed greater interest at 3.1x. The market was clearly divided on IRCON's investment merit.

Listing day, September 28, 2018, delivered a reality check. The stock opened at ₹416.65, a 12% discount to issue price, and closed the first day at ₹408. For a PSU IPO in a bull market, this was disappointing. The financial media was harsh, with headlines reading "IRCON's Infrastructure Dreams Hit Market Reality" and "Investors Give Thumbs Down to Railway PSU."

But beneath the poor debut was a more nuanced story. IRCON's fundamentals were actually improving. FY2019 delivered revenues of ₹4,837 crores (up 18% YoY) and net profit of ₹765 crores (up 22% YoY). The company won its largest-ever contract—₹3,200 crores for dedicated freight corridor construction. International operations stabilized with new projects in Bangladesh and Myanmar compensating for the suspended Iranian railway.

The stock market, however, remained unimpressed through 2019-2020. IRCON traded between ₹380-450, with daily volumes often below ₹10 crores. Sell-side coverage was minimal—only three brokerages initiated coverage, all with "Hold" ratings. The common critique: good company, wrong structure. Investors couldn't reconcile IRCON's commercial potential with its PSU constraints.

The COVID-19 pandemic unexpectedly became IRCON's validation moment. While private infrastructure players struggled with liquidity crises and project shutdowns, IRCON's government backing enabled continued operations. The company maintained workforce payments, honored supplier contracts, and even accelerated some projects during lockdowns. Q1FY21 results surprised the market: while peers reported 40-50% revenue declines, IRCON's fell just 15%.

October 2023 marked a strategic milestone: elevation to 'Navratna' status, granting IRCON enhanced autonomy in capital expenditure (up to ₹1,000 crores), joint ventures, and international expansion. This wasn't just bureaucratic recognition—it signaled the government's confidence in IRCON's strategic importance. The stock responded positively, crossing ₹300 for the first time since listing.

The real catalyst came with the government's infrastructure push post-COVID. The National Infrastructure Pipeline, Gati Shakti program, and massive railway modernization created an unprecedented project pipeline. IRCON's order book swelled to ₹35,000 crores by March 2024. More importantly, the project mix improved: higher-margin metro projects increased from 10% to 25% of order book, international projects with better payment terms reached 30%, and technical consultancy assignments—virtually pure margin—doubled.

FY2024 delivered IRCON's best-ever performance: revenues of ₹10,259 crores, net profit of ₹929.5 crores (9.1% margin), and return on equity of 18.5%. The stock responded dramatically, reaching an all-time high of ₹351.60 on July 15, 2024. At this peak, IRCON's market cap touched ₹33,000 crores—a 7x increase from IPO valuation.

The government seized this momentum for further disinvestment. In March 2024, an OFS of 8% stake was launched at ₹160 per share, a 10% discount to market price. Despite the discount, the issue was oversubscribed 2.8 times, with strong participation from domestic mutual funds that had earlier shunned the stock. The government raised ₹1,500 crores, reducing its stake to 65%—just above the minimum 51% required for PSU status.

This second disinvestment revealed how market perception had evolved. Investors now saw IRCON not as a conflicted PSU but as a play on India's infrastructure ambitions with government backing as a competitive advantage rather than constraint. The company's ability to execute complex projects, access to diplomatic corridors for international expansion, and balance sheet strength in a sector plagued by leverage were finally being valued.

Yet challenges emerged even at peak valuations. Q1FY25 results disappointed: revenues fell 21.9% YoY to ₹1,786 crores and net profit dropped 26.8% to ₹164 crores. Management attributed this to project transitions and weather-related delays, but the market was unforgiving. The stock corrected 40% from its peak, settling around ₹210 by late 2024.

The volatility exposed IRCON's fundamental challenge as a listed PSU: balancing market expectations for consistent quarterly growth with the lumpy, long-gestation nature of infrastructure projects. Unlike software companies that could manage earnings through deal timing, IRCON's revenues depended on project milestones, weather conditions, and government approvals—factors beyond management control.

As 2024 ended, IRCON's market journey reflected broader questions about PSU valuations. Should these companies trade at discounts to private peers due to structural constraints? Or should government backing and strategic importance command premiums? The answer remained elusive, with IRCON's stock price swinging between these narratives based on quarterly results rather than fundamental business changes. The re-listing had succeeded in providing the government with disinvestment proceeds and giving investors access to India's infrastructure story, but whether IRCON could sustain market confidence while fulfilling its strategic obligations remained an open question.

VII. Modern Operations & Business Model

Inside IRCON's project control room in Sarai Rohilla, Delhi, two dozen screens display real-time feeds from construction sites across the globe. A tunnel boring machine grinds through Himalayan rock in Kashmir, concrete is being poured for a metro viaduct in Bangladesh, and workers are laying tracks in the African heat of Mozambique. This nerve center, established in 2019, represents IRCON's evolution from traditional contractor to technology-enabled infrastructure integrator. Every major project parameter—from worker productivity to material consumption—is tracked, analyzed, and optimized in real-time.

The modern IRCON operates through five distinct but synergistic verticals, each contributing to what the company calls its "infrastructure ecosystem approach." Railways remains the core, contributing 45% of revenues but with evolved capabilities. Beyond traditional track-laying, IRCON now handles complete railway ecosystems: signaling systems, electrification, station development, and even rolling stock procurement. The company's execution of the Western Dedicated Freight Corridor—a 1,500-kilometer double-line electric railway designed for 100 km/hour freight trains—showcases this integrated capability.

The highways and bridges vertical (25% of revenues) has moved beyond simple road construction to complex engineering solutions. IRCON's work on the Bogibeel Bridge—India's longest rail-cum-road bridge at 4.94 kilometers—required innovations in seismic-resistant design, as the structure spans the Brahmaputra in earthquake-prone Assam. The company developed proprietary techniques for deep foundation work in riverine conditions, using controlled blasting underwater and custom-designed cofferdams that could withstand Brahmaputra's notorious floods.

Metro rail projects have emerged as IRCON's highest-margin segment (contributing 20% of revenues but 30% of EBITDA). The company's approach here differs from competitors: instead of bidding for individual packages, IRCON positions itself as a complete metro solution provider. In the Dhaka Metro project, IRCON handles everything from viaduct construction to station finishing, system integration, and trial runs. This end-to-end capability commands premium pricing and creates sticky client relationships.

The engineering, procurement, and construction (EPC) model dominates IRCON's contracting approach, accounting for 75% of projects. But the company has innovated beyond traditional EPC through what it calls "EPC Plus"—adding design, financing facilitation, and operations support. This evolution was driven by international clients, particularly African nations, that needed not just construction but complete infrastructure solutions. IRCON's project in Mozambique, for instance, included training local operators, establishing maintenance protocols, and even helping draft railway regulations.

Risk management in modern IRCON is remarkably sophisticated for a PSU. The company maintains a "risk register" with over 200 identified risks across categories: geological, political, financial, and execution. Each project undergoes Monte Carlo simulation for cost and schedule, with contingencies built not as uniform percentages but as probability-weighted outcomes. The Iranian railway suspension, while painful, validated this approach—IRCON had maintained provisions that covered most exposure, limiting write-offs to ₹67 crores against potential losses of ₹500 crores.

The technology integration sets modern IRCON apart from both PSU peers and many private competitors. Building Information Modeling (BIM) is mandatory for all projects above ₹100 crores. Drone surveys have replaced manual measurement, reducing survey time by 80% and improving accuracy. The company has even experimented with AI-powered predictive maintenance for construction equipment, reducing downtime by 30% in pilot projects.

Consider IRCON's approach to tunnel construction, where the company has built distinctive capabilities. The methodology combines Austrian Tunneling Method (NATM) for geological flexibility with New Austrian Tunneling Method innovations for speed. In the Katra-Banihal railway tunnel, IRCON achieved breakthrough rates of 6 meters per day in fractured rock conditions where industry average is 2-3 meters. The secret: micro-seismic monitoring that predicts rock behavior 50 meters ahead, allowing preemptive support installation.

Human capital management has evolved remarkably. IRCON operates with just 1,247 permanent employees but manages project workforces exceeding 50,000. The company has developed a "core-flex" model: permanent employees handle design, project management, and quality control, while execution workforce is hired project-specifically. This keeps fixed costs low (employee costs are just 5% of revenues) while maintaining quality through standardized training programs for contract workers.

The order book composition reveals IRCON's strategic positioning. As of September 2024, the ₹20,973 crore order book breaks down intriguingly: 60% government (down from 90% a decade ago), 40% competitive bidding (up from 15%), and average project size has increased from ₹50 crores to ₹200 crores. Larger projects mean better resource utilization, stronger bargaining power with suppliers, and ability to invest in project-specific technology.

IRCON's competitive moat isn't immediately obvious but becomes clear on examination. First, the company's experience in difficult terrains is unmatched—over 40% of projects are in areas classified as "challenging" (mountains, deserts, conflict zones). Second, IRCON's government parentage provides access to sovereign-guaranteed projects that private players can't bid for. Third, the company's balance sheet strength (debt-to-equity of 0.3x versus industry average of 2x) enables aggressive bidding when strategic projects arise.

The supply chain management deserves special mention. IRCON maintains strategic partnerships with 15 cement companies, 8 steel suppliers, and 20 equipment manufacturers. These aren't just procurement relationships but collaborative partnerships. For instance, IRCON worked with L&T to develop specialized tunnel boring machines for Himalayan geology, sharing development costs in exchange for preferential pricing. The company maintains buffer stocks worth ₹500 crores across key project sites, enabling work continuation despite supply disruptions.

Quality control in IRCON follows a "three-tier architecture": self-certification by execution teams, independent quality assurance by project managers, and third-party audits by international certifying agencies. Every concrete pour is tested, every weld is inspected, and every alignment is verified through GPS. This obsession with quality has resulted in remarkable statistics: less than 0.5% rework across projects, 98% on-time completion, and zero major structural failures in the company's history.

The margin structure tells an interesting story about operational efficiency. While headline EBITDA margins of 12-15% seem modest, the capital efficiency is remarkable. IRCON generates ₹8 of revenue for every rupee of fixed assets—among the highest in the infrastructure sector. The working capital cycle has been compressed to 45 days through milestone-based billing and aggressive collection. Return on capital employed consistently exceeds 20%, comparable to asset-light IT services companies rather than capital-intensive construction peers.

Yet challenges persist in the operating model. Project execution remains vulnerable to external factors: land acquisition delays, environmental clearances, and weather disruptions. The company's conservative approach to new technology adoption—while reducing risk—may be missing opportunities in areas like modular construction and 3D printing. Most critically, IRCON's dependence on government projects, while providing stability, limits exposure to potentially higher-margin private sector opportunities.

As IRCON navigates its fifth decade, the operational model continues evolving. The company is experimenting with asset ownership (operating some projects post-construction), digital twins for predictive maintenance, and even carbon-neutral construction techniques. These initiatives remain small, contributing less than 5% of revenues, but represent IRCON's attempt to future-proof its business model. Whether a PSU can successfully innovate while maintaining operational discipline remains to be seen, but IRCON's track record suggests it's better positioned than most to manage this balance.

VIII. Financial Performance & Current Challenges

The CFO's presentation at IRCON's Q1 FY2025 earnings call started with an uncomfortable admission: "We understand the market's disappointment." The numbers on screen told a story of sudden deceleration—revenues down 21.9% year-on-year to ₹1,786 crores, net profit plunging 26.8% to ₹164 crores. For a company that had just hit all-time highs months earlier, this was a sobering reversal that would trigger a 40% stock price correction.

But understanding IRCON's financial performance requires looking beyond quarterly volatility to structural dynamics that define infrastructure contracting. The company's five-year trajectory tells a more nuanced story: revenues grew at 21.5% CAGR from FY2019 to FY2024, reaching ₹10,259 crores. Net profit expanded at 17.6% CAGR to ₹929.5 crores. These aren't just growth numbers—they represent IRCON successfully navigating COVID disruptions, commodity inflation, and execution challenges that decimated private infrastructure players.

The margin evolution reveals IRCON's operational transformation. EBITDA margins improved from 11.2% in FY2019 to 14.8% in FY2024, defying the industry trend of margin compression. This 360 basis point expansion came from three sources: project mix optimization (more metros and international projects), operational efficiency (technology adoption reducing execution costs), and scale benefits (fixed cost absorption over larger revenue base). The company's ability to maintain double-digit margins while competitors struggled with single digits became IRCON's key differentiator.

Cash flow generation, often the Achilles heel of construction companies, has been IRCON's hidden strength. Operating cash flow averaged ₹850 crores annually over the past five years, with cash conversion (operating cash flow/EBITDA) consistently above 70%. This superior cash generation stems from IRCON's milestone-based billing model, strong collection mechanisms (government clients pay slowly but surely), and minimal working capital requirements (45-day cycle versus industry average of 120 days).

The balance sheet remains fortress-like by construction sector standards. Total debt of ₹1,200 crores against net worth of ₹5,400 crores yields a debt-to-equity ratio of 0.22x—remarkably conservative when peers operate at 2-3x leverage. This low leverage provides multiple advantages: ability to bid for large projects without balance sheet constraints, minimal interest costs (just 1.5% of revenues), and flexibility to weather execution delays without financial stress. IRCON's return on equity of 18.5% with minimal leverage demonstrates genuine operational efficiency rather than financial engineering.

Yet the Q1 FY2025 disappointment exposed structural vulnerabilities. Revenue recognition in infrastructure follows percentage completion method, meaning delays in even one large project can distort quarterly numbers. IRCON's dependence on a few mega-projects—the top 10 projects contribute 60% of revenues—amplifies this volatility. When the Kashmir railway project faced weather delays and a Bangladesh metro project hit land acquisition issues simultaneously, quarterly revenues collapsed despite the order book remaining intact.

The order book itself presents both comfort and concern. At ₹20,973 crores (2x forward revenues), it provides visibility but lacks the growth momentum of previous years. Order inflow in FY2024 was just ₹8,500 crores against execution of ₹10,259 crores—a book-to-bill ratio below 1x that's unsustainable. Management attributes this to selective bidding in a competitive market, but investors worry about market share loss to aggressive private players.

Segment analysis reveals diverging trajectories. Railway projects, IRCON's bread and butter, face margin pressure as competition intensifies. Average EBITDA margins in railways have compressed from 15% to 11% over three years. Highway projects remain stable at 13% margins but growth has stagnated. The bright spot is metros and international projects, where margins exceed 18%, but these remain just 35% of the revenue mix. This segment concentration risk means IRCON's profitability increasingly depends on winning high-value metro contracts—a competitive space where technical capabilities matter less than financial muscle.

The working capital dynamics deserve scrutiny. While the 45-day cycle appears efficient, it masks increasing stress. Receivables have grown from ₹1,800 crores to ₹2,900 crores over three years, with international receivables (particularly from African nations) showing aging. The company maintains provisions of ₹150 crores for doubtful debts, but actual write-offs have been minimal. This gap between provisions and write-offs could indicate either conservative accounting or delayed recognition of stressed assets.

Cost structure analysis shows both efficiency gains and emerging pressures. Material costs (65% of revenues) have been managed through strategic procurement and long-term contracts. Employee costs at just 5% of revenues demonstrate operational leverage. But subcontracting costs have risen from 15% to 20% of revenues as IRCON increasingly relies on specialized vendors for technical work. This outsourcing improves capital efficiency but reduces control over execution quality and timelines.

The comparison with listed peers provides context for valuation. L&T's infrastructure division generates 25% EBITDA margins but with higher risk from BOT projects. NCC operates at similar margins to IRCON but with 3x leverage. Rail Vikas Nigam, IRCON's closest PSU peer, shows lower margins (10%) but faster growth (30% revenue CAGR). This positioning—better than PSUs, worse than private leaders—explains IRCON's valuation discount despite superior return ratios.

International operations add complexity to financial analysis. While contributing 30% of revenues at 18% margins, these projects carry hidden risks. Currency exposure (₹500 crores of receivables in various African currencies) isn't fully hedged. Sovereign guarantees from financially weak nations provide legal comfort but not payment certainty. The Iranian railway write-off, while small, reminded investors that international projects carry binary risks that domestic government projects don't.

The stock price performance reflects these financial dynamics. After reaching ₹351.60 in July 2024, the stock corrected to ₹210 by October—a 40% decline that erased two years of gains. The correction was severe even accounting for Q1 disappointment, suggesting deeper concerns about growth sustainability and margin resilience. Trading volumes doubled during the decline, indicating institutional selling rather than retail panic.

Current valuations present an interesting debate. At ₹210, IRCON trades at 12x trailing earnings and 1.5x book value—a significant discount to historical averages of 15x P/E and 2x P/B. Bulls argue this presents opportunity given the strong order book and infrastructure mega-cycle. Bears point to slowing order inflows, margin pressures, and structural constraints of PSU operations. The consensus view: fairly valued for a mature infrastructure company but lacking catalysts for rerating.

Looking ahead, IRCON faces a classic infrastructure contractor's dilemma: chase growth through aggressive bidding (sacrificing margins) or maintain margins through selective bidding (sacrificing growth). The company's PSU status adds another dimension—it must balance commercial objectives with strategic responsibilities. The financial performance over the next few quarters will reveal whether IRCON can navigate these contradictions while maintaining the operational excellence that has defined its five-decade journey.

IX. Playbook: PSU Excellence & Infrastructure Expertise

The boardroom discussion at a leading private equity firm in Mumbai, 2022, was getting heated. The partners were debating whether to invest in Indian infrastructure, and IRCON kept coming up as a benchmark. "How does a government-owned company consistently deliver 18% ROE with minimal leverage while private players with all their efficiency can barely manage 12% with 3x debt?" asked the senior partner. The answer to that question reveals IRCON's playbook—a unique combination of PSU advantages and commercial discipline that's difficult to replicate.

The first element of IRCON's playbook is what management calls "patient capital advantage." Unlike private players pressured for quarterly growth, IRCON can take a 10-year view on capability building. The company spent ₹200 crores developing tunnel boring expertise over 2010-2015 with no immediate returns. This investment paid off spectacularly when the metro boom arrived—IRCON could bid for complex underground sections that few Indian companies could execute. Private players, focused on immediate ROI, couldn't afford such patient capability building.

The second strategic advantage is "sovereign arbitrage"—leveraging government ownership for commercial benefit. When IRCON bids for international projects, it carries implicit Indian government backing. This isn't just about financial guarantees; it's about diplomatic comfort. When Bangladesh evaluates infrastructure contractors, IRCON's proposal carries the weight of bilateral relations. Chinese companies have similar advantages, but IRCON adds Indian soft power—democratic values, cultural affinity, and non-predatory financing terms—that resonates in South Asia and Africa.

Risk management in IRCON follows what internally they call the "three-bucket approach." Bucket one: risks IRCON can control (execution, quality, cost) are managed through stringent processes. Bucket two: risks IRCON can influence (regulatory approvals, payment delays) are handled through relationship management. Bucket three: risks IRCON cannot control (weather, geopolitics) are either priced into bids or avoided entirely. This framework seems simple but its disciplined application has kept IRCON from the aggressive bidding that destroyed many infrastructure companies during 2008-2015.

The human capital strategy breaks conventional PSU stereotypes. IRCON maintains a lean permanent workforce (1,247 employees) of highly qualified engineers and managers, paying them competitively within PSU constraints through performance bonuses and foreign postings. The average IRCON engineer manages projects worth ₹100 crores by age 30—responsibility that private companies reserve for 40-year-olds. This early empowerment creates a culture of ownership unusual in government organizations.

Project selection criteria reveal sophisticated strategic thinking. IRCON evaluates projects on a matrix beyond just IRR: strategic importance (does it build new capabilities?), relationship value (does it deepen government ties?), demonstration effect (will it lead to follow-on projects?), and execution risk (can IRCON's expertise provide competitive advantage?). This multi-dimensional evaluation led IRCON to take the low-margin Kashmir railway project—the technical expertise gained positioned it for lucrative Himalayan tunneling projects later.

The "corridor development strategy" has been particularly successful internationally. Instead of random projects across countries, IRCON focuses on specific corridors where it can build deep expertise and relationships. The Bangladesh-India border region, where IRCON has executed 15 projects over 20 years, exemplifies this. The company now has unmatched knowledge of local geology, regulatory processes, and stakeholder dynamics—creating barriers to entry that price-focused Chinese competitors cannot overcome.

Technology adoption in IRCON follows a "proven-plus" approach. The company doesn't chase cutting-edge technology but adopts proven solutions one generation behind the frontier. This reduces technology risk while capturing most efficiency benefits. For instance, IRCON adopted BIM (Building Information Modeling) five years after global leaders but customized it for Indian conditions—creating proprietary workflows that are now more effective than generic global solutions.

The financial engineering capabilities, sophisticated for a PSU, deserve recognition. IRCON structures projects through multiple vehicles: SPVs for risk isolation, joint ventures for capability access, and consortium arrangements for large projects. The company's treasury actively manages a ₹500 crore forex exposure through natural hedging (matching revenue and cost currencies) and selective derivatives. This financial sophistication, unusual for engineering-focused PSUs, enables IRCON to compete with private players on complex structured projects.

Supply chain management showcases operational excellence. IRCON's "strategic supplier partnership" program goes beyond typical procurement. The company co-invests with suppliers in equipment, provides advance mobilization funds, and even helps them access credit. In return, IRCON gets preferential pricing, guaranteed capacity allocation, and technical collaboration. This ecosystem approach has created a vendor network that's effectively an extended enterprise—providing IRCON with execution capabilities far beyond its employee base.

The quality philosophy—"right first time"—seems clichéd but has profound implications. IRCON invests 2% of project costs in quality assurance, double the industry average. Every project has independent quality auditors reporting directly to corporate, not project managers. This obsession with quality has resulted in remarkable statistics: zero major structural failures, 98% on-time completion, and less than 0.5% rework. These metrics translate into commercial advantage—clients accept IRCON's premium pricing for certainty of execution.

Knowledge management, often neglected in construction companies, is systematic in IRCON. Every project conducts detailed post-mortems, documenting lessons learned in a searchable database. The company maintains a "technical library" with over 10,000 project documents, creating institutional memory that survives employee turnover. New project teams must review relevant past projects before starting work. This knowledge accumulation over 47 years provides IRCON with insights that competitors cannot replicate.

The stakeholder management approach reflects PSU sophistication. IRCON maintains relationships at multiple levels: political (ministers and bureaucrats), technical (engineering departments), and local (community leaders). This multi-stakeholder engagement, while time-consuming, creates project resilience. When the Manipur government changed and the new administration questioned ongoing projects, IRCON's relationships with technical departments and local communities ensured continuation while peers faced cancellations.

Environmental and social governance, often seen as compliance burden, has become strategic advantage. IRCON's proactive approach—conducting environmental assessments beyond requirements, implementing community development programs, and maintaining transparent grievance mechanisms—has reduced project delays from protests by 60%. The company's work in Northeast India, where it has completed projects without major community opposition despite the sensitive environment, demonstrates this capability.

The international expansion strategy reveals long-term thinking. IRCON doesn't just execute projects abroad; it builds local institutions. Training centers in Bangladesh, maintenance facilities in Sri Lanka, and regulatory frameworks in African nations create lasting relationships beyond individual projects. This institution-building approach, while expensive initially, has resulted in 70% repeat business in international markets—far exceeding the 30% industry average.

Yet the playbook has limitations that IRCON acknowledges. The PSU structure constrains aggressive expansion—IRCON cannot make acquisitions quickly or offer equity to attract talent. The government ownership, while providing advantages, also brings obligations to take uneconomical projects. The conservative culture, while ensuring stability, may be missing opportunities in emerging areas like green infrastructure and smart cities.

The replicability question is crucial for investors. Can private players adopt IRCON's playbook? Partially. The operational excellence, project management capabilities, and stakeholder engagement can be replicated with effort. But the patient capital, sovereign backing, and PSU cost of capital advantages are structural. This suggests IRCON's competitive position is more defensible than apparent, but also that its growth potential may be structurally limited compared to aggressive private players. The playbook works brilliantly within its constraints—the question is whether those constraints will tighten or loosen in India's evolving infrastructure landscape.

X. Analysis & Investment Case

The investment committee at a major mutual fund was divided. The infrastructure analyst was bullish: "IRCON at 12x earnings is absurdly cheap for a company with 18% ROE, minimal debt, and ₹21,000 crore order book in India's infrastructure super-cycle." The governance specialist was skeptical: "It's a value trap—PSU constraints will prevent IRCON from capturing the upside while private players eat its lunch." This debate, playing out across institutional investors, captures IRCON's investment paradox: compelling fundamentals constrained by structural limitations.

The Bull Case: Infrastructure Mega-Cycle Beneficiary

India's infrastructure opportunity is staggering—₹111 lakh crore investment planned through 2025, with railways alone requiring ₹50 lakh crores. IRCON, with its proven execution capabilities and government backing, is positioned to capture disproportionate share. The company's exposure to high-growth segments—metros (₹8 lakh crore opportunity), dedicated freight corridors (₹3 lakh crore), and international projects—provides multiple growth drivers.

The financial strength amplifies this opportunity. With debt-to-equity of 0.22x versus industry average of 2x, IRCON has ₹5,000 crores of additional borrowing capacity without stress. This balance sheet strength becomes competitive advantage when bidding for large projects where financial capability is qualification criteria. While leveraged competitors struggle with debt servicing, IRCON can bid aggressively for strategic projects.

The margin resilience story is compelling. Despite intense competition, IRCON has expanded EBITDA margins from 11% to 15% over five years through operational efficiency and mix improvement. The company's focus on complex projects—tunneling, metros, international—creates differentiation that commands premium pricing. With 70% of order book in these high-margin segments, earnings growth could exceed revenue growth.

International operations provide unique optionality. IRCON's presence in 25 countries, relationships with multiple governments, and expertise in challenging environments create opportunities beyond domestic infrastructure. The Africa infrastructure boom, funded by multilateral agencies, plays to IRCON's strengths. The company's pipeline of $2 billion international projects could drive 25% revenue CAGR in this segment.

The valuation disconnect is striking. At ₹210, IRCON trades at 12x P/E versus L&T at 25x and NCC at 18x. On P/B basis, IRCON at 1.5x is half of peer valuations. This discount despite superior return ratios (ROE of 18% versus peer average of 12%) and stronger balance sheet suggests significant rerating potential. Even reaching historical average valuations implies 40% upside.

The Bear Case: Structural Constraints and Execution Risks

The PSU overhang cannot be ignored. Government ownership means IRCON must prioritize strategic objectives over commercial returns. The company will continue taking low-margin projects in Kashmir, Northeast, and other strategically important but commercially unviable areas. This obligation caps margin expansion potential regardless of operational improvements.

Order book quality raises concerns. While ₹21,000 crores seems impressive, 40% comprises government projects where margins are regulated and payment delays endemic. The book-to-bill ratio below 1x suggests difficulty winning new projects in competitive market. Private players with aggressive bidding and financial innovation are capturing incremental market share.

The execution challenges are mounting. IRCON's employee base of 1,247 manages projects worth ₹10,000 crores—a span of control that's reaching limits. The company's reluctance to expand permanent workforce (PSU salary constraints) while project complexity increases creates execution risk. One major project failure could devastate earnings and credibility.

International risks are underappreciated. IRCON's exposure to financially weak nations—Bangladesh, African countries—creates payment uncertainty. The ₹500 crore receivables from international projects, some aging beyond two years, could necessitate write-offs. Currency volatility in frontier markets adds another layer of risk that hedging cannot fully mitigate.

The growth trajectory is decelerating. Revenue growth has slowed from 30% (2019-2021) to 15% (2022-2024) as base effects normalize. Order inflows aren't keeping pace with execution, suggesting further deceleration ahead. Without transformational project wins or new segment entry, IRCON risks becoming a low-growth utility-like infrastructure player.

Peer Comparison: The Positioning Challenge

Comparing IRCON with peers reveals its unique position—and challenge. L&T's infrastructure division, the gold standard, operates at 25% EBITDA margins with sophisticated project management and financial engineering. But L&T also carries higher risk from BOT projects and 3x leverage. IRCON's lower but stable margins might be preferable for risk-averse investors.

NCC, IRCON's closest comparable, trades at 18x P/E despite inferior return metrics. The premium reflects NCC's private sector agility and exposure to high-growth segments like data centers and industrial construction. IRCON's government focus, while providing stability, limits exposure to emerging opportunities.

Rail Vikas Nigam (RVNL), IRCON's PSU peer, offers interesting contrast. RVNL's asset-light model (primarily project management) generates 30% ROE but with higher volatility. IRCON's integrated EPC approach provides more stable earnings but lower returns. The market values both similarly, suggesting investors are indifferent between models.

Chinese infrastructure giants—China State Construction, China Railway—provide international context. These companies, with government backing similar to IRCON, trade at 8-10x P/E in Hong Kong markets. This suggests PSU discount is global phenomenon, unlikely to disappear even with governance improvements.

Valuation Perspectives: Multiple Frameworks

Discounted cash flow analysis suggests fair value of ₹240-260, implying 15-25% upside from current levels. This assumes 12% revenue CAGR, stable 15% EBITDA margins, and terminal growth of 6%. The sensitivity to margin assumptions is high—100 bps margin improvement adds ₹40 to fair value.

Asset-based valuation provides downside protection. IRCON's book value of ₹140 per share, comprising mainly liquid assets and receivables from government entities, suggests limited downside risk. The replacement cost of IRCON's capabilities—trained workforce, equipment, relationships—far exceeds book value.

Earnings power value, assuming normalized 10% net margins on ₹12,000 crore revenues, suggests ₹280 fair value. This framework ignores growth but captures IRCON's through-cycle earning capability. The current market price implies skepticism about sustaining even historical profitability.

Future Growth Drivers: Beyond Traditional Infrastructure

IRCON's future hinges on capturing emerging opportunities while maintaining traditional strengths. Metro rail, expected to expand from 850 km to 2,500 km operational network by 2030, represents ₹5 lakh crore opportunity. IRCON's integrated capabilities position it well for complex metro projects.

High-speed rail, beginning with Mumbai-Ahmedabad corridor, could transform IRCON's growth trajectory. The company's joint venture with Japanese firms for bullet train construction provides technology access and demonstration opportunity. Success here could unlock ₹10 lakh crore high-speed rail opportunity over the next decade.

Green infrastructure—solar parks, wind installations, green hydrogen facilities—represents adjacent opportunity. IRCON's project management capabilities are transferable, but the company needs technology partnerships and new skill development. Early moves into solar EPC show promise but remain subscale.

The digital infrastructure boom—data centers, telecom towers, fiber networks—is another frontier. IRCON's civil construction capabilities are relevant, but the company lacks technology expertise. Strategic partnerships or acquisitions could provide entry, but PSU constraints make quick moves difficult.

The Investment Decision: Context-Dependent

For value investors, IRCON presents compelling opportunity. Trading below historical valuations despite improved fundamentals, with downside protection from asset value and government backing, the risk-reward appears favorable. The 3% dividend yield provides income while waiting for rerating.

Growth investors will likely remain disappointed. IRCON's structural constraints, slowing order book growth, and limited exposure to emerging sectors suggest capped upside. The stock is unlikely to be a multibagger despite India's infrastructure boom.

For risk-averse investors seeking infrastructure exposure, IRCON offers unique proposition: participation in India's infrastructure story with PSU stability. The lower volatility compared to leveraged private players and government backing during downturns provide comfort.

The institutional perspective is nuanced. IRCON's liquidity (₹50 crore average daily volume) is adequate for small positions but insufficient for large funds. The 65% government ownership limits free float, potentially constraining index inclusion and passive flows.

The ultimate investment case depends on time horizon and risk appetite. Short-term traders should avoid—quarterly volatility from project-based revenue recognition makes near-term movements unpredictable. Long-term investors believing in India's infrastructure story and PSU reform might find IRCON attractive at current valuations. But expecting IRCON to break free from PSU constraints and compete uninhibited with private players remains wishful thinking. The company is what it is: a competent executor of infrastructure projects, backed by government, delivering steady if unspectacular returns—valuable in portfolio context but unlikely to generate outsized alpha.

XI. Epilogue & Looking Forward

Standing at the construction site of the Mumbai-Ahmedabad High Speed Rail project in early 2024, IRCON's young project manager surveyed the massive undertaking ahead. The 508-kilometer bullet train corridor, India's first, represents more than just another infrastructure project—it symbolizes the nation's technological leap and IRCON's evolution from railway contractor to builder of 21st-century transportation networks. As concrete pillars rise from Gujarat's soil to support trains that will travel at 320 km/hour, IRCON stands at its own inflection point, navigating between its PSU heritage and the demands of modern infrastructure development.

India's infrastructure ambitions for the next decade dwarf anything attempted before. The National Infrastructure Pipeline envisions ₹111 lakh crore investment, the PM Gati Shakti program integrates multimodal connectivity, and the railway modernization plan allocates ₹50 lakh crores through 2051. IRCON, with its proven capabilities and government backing, seems naturally positioned to benefit. Yet the company's ability to capture this opportunity depends on evolving beyond traditional execution to become a technology-enabled, financially sophisticated infrastructure solutions provider.

The international infrastructure diplomacy arena is becoming increasingly complex. As India positions itself as alternative to China's Belt and Road Initiative, IRCON becomes an instrument of soft power projection. The company's work in Bangladesh, Sri Lanka, and Africa isn't just commercial—it's strategic, building physical connections that reinforce diplomatic relationships. The recent agreement to develop Nepal's railway network and discussions about Central Asian corridors suggest IRCON's international role will expand, but balancing commercial viability with diplomatic objectives remains challenging.

Technology adoption will determine IRCON's competitive position. The infrastructure sector is experiencing technological disruption: AI-powered project management, drone-based monitoring, modular construction, and digital twins for predictive maintenance. IRCON has been conservative in technology adoption, preferring proven solutions over cutting-edge innovation. While this reduces risk, it may also cede competitive advantage to aggressive private players. The company's recent initiatives—BIM implementation, IoT-based equipment monitoring—suggest recognition of this challenge, but the pace of change may need acceleration.