Ion Exchange (India): The Water Empire Nobody Talks About

I. Introduction & Episode Setup

Picture this: It's 2024, and Chennai's IT corridor is running out of water. Again. Tech giants are trucking in tankers while their engineers debug code. Hotels are rationing showers. The irony is thick—India's silicon valley brought to its knees not by competition or regulation, but by something as basic as H2O.

Here's the staggering reality: India houses 18% of the world's population but controls only 4% of its freshwater resources. By 2030, demand will be twice the available supply. This isn't just an environmental crisis—it's an economic time bomb worth $600 billion in lost GDP annually by some estimates.

Yet buried in this crisis narrative is a company most investors have never heard of: Ion Exchange (India) Limited. Trading at ₹500 on the NSE with a market cap of ₹6,514 crore, it generated ₹2,753 crore in revenue last year with ₹212 crore in profit. Not exactly software margins, but here's what's fascinating—this company has quietly built India's most comprehensive water treatment empire, touching everything from the water in your Coke bottle to the cooling systems in nuclear power plants. The puzzle deepens when you realize this isn't some venture-backed startup or a multinational subsidiary anymore. It's a 60-year-old company controlled by employee welfare trusts—a structure virtually unheard of in corporate India. Think of it as India's answer to an ESOP-owned firm, except this happened in 1984, decades before ESOPs became cool.

Revenue grew 13% YoY, and EBIT rose 26% YoY in Q1 FY25 supported by steady medium-sized job orders and international contracts. The company expects faster execution of large EPC jobs in the coming quarters. Yet the stock has been brutalized, down 21.91% over the last six months despite water becoming India's most critical resource challenge.

This is a story about how a British colonial subsidiary transformed into India's water infrastructure backbone, built on a foundation of chemistry that most MBAs couldn't explain if their lives depended on it. It's about riding three megatrends simultaneously: industrial growth, environmental regulation, and water scarcity. And it's about why, in a world obsessed with software and platforms, sometimes the most valuable moats are built with polymers and membranes.

The themes we'll explore cut to the heart of industrial capitalism: How do you build technical moats in commoditized industries? What happens when employees own the company? And perhaps most importantly—why does a company processing the most essential resource on earth trade at industrial multiples while loss-making food delivery apps command software valuations?

II. Origins: The Permutit Connection (1964–1984)

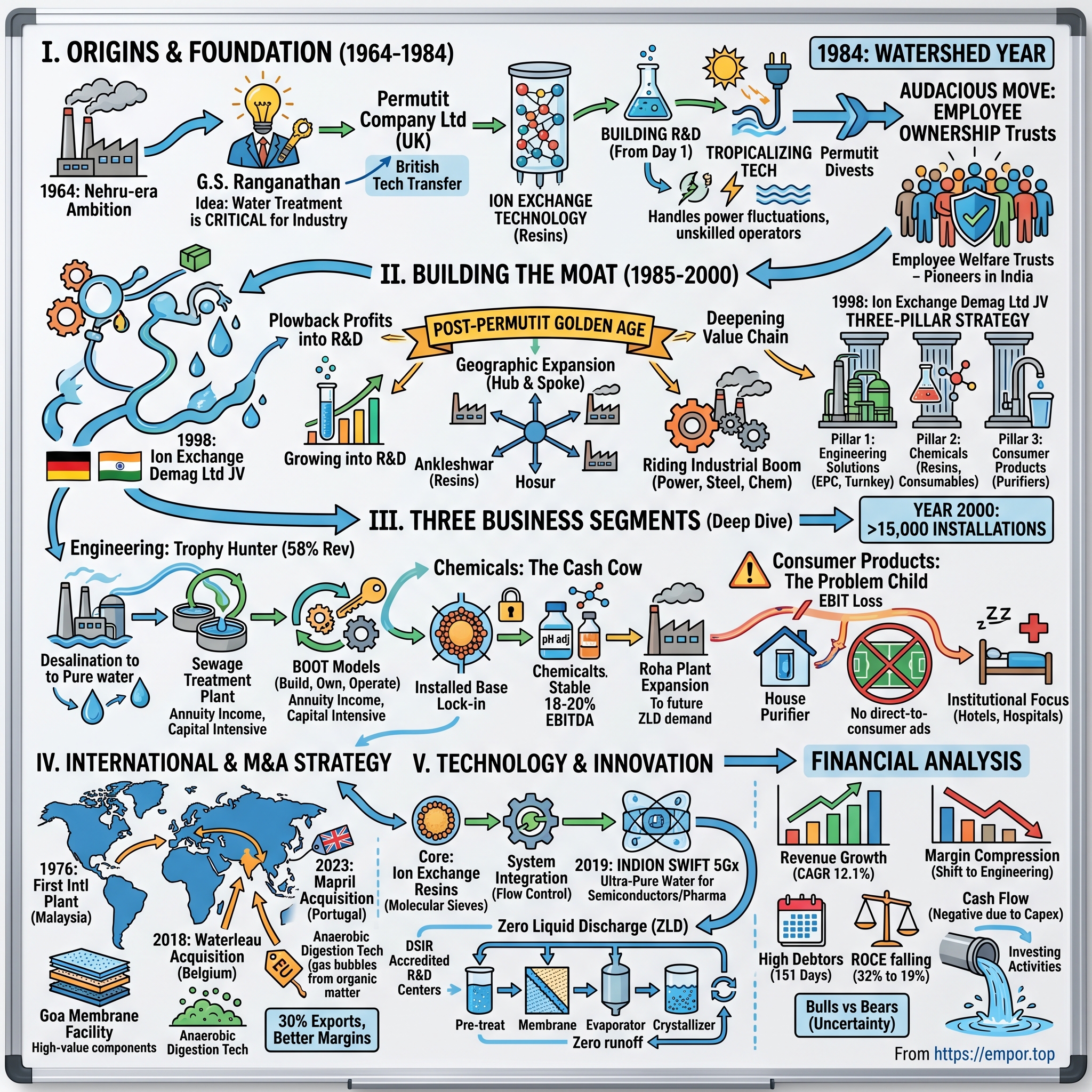

The year is 1964. Jawaharlal Nehru has been dead for three months. India's third Five Year Plan is stumbling. The country is importing everything from steel to toothpaste. In this environment of industrial ambition colliding with technical incompetence, a chemical engineer named G.S. Ranganathan spots an opportunity that would define the next six decades of Indian industrial development.

Ranganathan wasn't your typical Indian entrepreneur of that era—no textile mills, no trading houses. He was a technocrat who understood something fundamental: India's industrial dreams would die without water treatment. Every steel plant, every refinery, every power station needed treated water. And nobody in India knew how to do it properly.

Enter Permutit Company Limited, a British firm that had pioneered ion exchange technology—essentially chemistry's answer to water purification. Think of ion exchange like a molecular bouncer at a nightclub, selectively letting good ions in while kicking out the troublemakers. Permutit had been using this technology globally since the 1920s, but India was virgin territory.

The partnership structure was classic post-colonial: Permutit provided technology and initial capital, Indians provided market access and local knowledge. Ion Exchange (India) was born as a subsidiary, with Ranganathan as the operational head. But here's what made it different from hundreds of similar ventures—Ranganathan insisted on building R&D capabilities from day one, not just assembling imported components. The founder and chairman emeritus G. Shankar Ranganathan passed away in March 2013, but his legacy shaped the company's DNA. Ion Exchange was formed in 1964 as a subsidiary of UK company Permutit on Ranganathan's initiative and recommendation.

The company's first facility came up in Mumbai, manufacturing ion exchange resins—those magical polymer beads that could swap ions like molecular trading cards. The early customer list reads like a who's who of India's industrial revolution: Bharat Heavy Electricals for their power plants, Indian Oil for their refineries, SAIL for their steel plants. Each installation was a vote of confidence in indigenous capability over imported solutions.

But the real genius wasn't in the technology transfer—it was in Ranganathan's understanding of the Indian context. Western water treatment systems assumed consistent power supply, skilled operators, and regular maintenance. India had none of these. So Ion Exchange started tropicalizing the technology: designing systems that could handle power fluctuations, training local operators, building redundancy into critical components.

By 1976, just twelve years after inception, the company was confident enough to set up its first international plant in Malaysia—a stunning reversal of the typical technology flow from West to East. This wasn't just manufacturing; it was innovation tailored to emerging market realities.

Then came 1984, the watershed year. Permutit decided to divest its holding, seeing limited growth potential in the Indian market. Most subsidiaries in this situation either shut down or get acquired by local business houses. But Ranganathan did something unprecedented: he advocated and set up employee welfare trusts, a pioneering concept for India.

Think about the audacity of this move. In an era when Indian companies were either family-owned or government-controlled, here was a company owned by its employees through trusts. Not ESOPs that vest over time, not phantom equity—actual ownership through welfare trusts. The structure was so unusual that regulators didn't know how to classify it.

This ownership transition coincided with India's industrial boom. The 1980s saw massive capacity additions in power, steel, and chemicals—all water-intensive industries. Ion Exchange was perfectly positioned: it had the technology, the local manufacturing capability, and most importantly, a motivated employee base that thought like owners because they were owners.

III. Building the Technical Moat (1985–2000)

The post-Permutit era should have been a disaster. The company lost its technology pipeline, its global brand association, and its financial backstop. Instead, it became Ion Exchange's golden age—a masterclass in building technical moats in unglamorous industries.

The new employee-owned structure created an interesting dynamic. Without a promoter family to pay dividends to, profits were plowed back into R&D. Ranganathan expanded the company's technology base through R&D, joint ventures, licensing and representative agreements making Ion Exchange one of the few companies worldwide with the entire spectrum of technologies, products and services.

The R&D story deserves special attention. While software companies get celebrated for spending 10% of revenue on R&D, Ion Exchange was spending similar percentages on polymer chemistry research in the 1980s. The company's R&D center, accredited by the Department of Scientific and Industrial Research (DSIR) since 1965, wasn't just adapting foreign technology—it was creating new applications for Indian conditions.

Consider the problem of chromium in tannery effluents—a massive issue in Tamil Nadu's leather belt. Western solutions involved expensive chemical precipitation. Ion Exchange developed a selective ion exchange resin that could extract chromium for reuse, turning a waste problem into a resource recovery opportunity. This wasn't published in Nature, but it saved hundreds of tanneries from closure.

Geographic expansion followed a hub-and-spoke model. Manufacturing facilities were set up not in SEZs for tax benefits, but close to customer clusters. A resin plant in Ankleshwar to serve Gujarat's chemical belt. A facility in Hosur for South India's industrial corridor. Each location became a mini-R&D center, solving local water problems that would later have global applications.

The 1990s brought liberalization and competition. Suddenly, global giants like GE Water (now Suez) and Nalco could enter India. The conventional wisdom was that Indian companies would get steamrolled. Instead, Ion Exchange thrived by going deeper into the value chain.

In 1998, a pivotal joint venture materialized: Ion Exchange Demag Ltd, a 50:50 partnership with Mannesmann Demag of Germany. This wasn't desperation—it was strategic chess. While competitors were fighting over commodity resin sales, Ion Exchange was moving into high-value engineered systems.

The three-pillar strategy that defines the company today emerged during this period:

Pillar 1: Engineering Solutions - Complete water treatment plants, not just components. This meant taking on EPC (Engineering, Procurement, Construction) risk but also capturing 3-5x higher margins than product sales.

Pillar 2: Chemicals - Not just resins but the entire chemical value chain for water treatment. When a customer needed pH adjustment, coagulants, and resins, Ion Exchange could supply everything.

Pillar 3: Consumer Products - The audacious move into B2C with home water purifiers, leveraging industrial credibility for consumer trust.

By 2000, Ion Exchange had over 15,000 installations across India. More importantly, it had something no competitor could easily replicate: two decades of operational data from Indian conditions. Every failed membrane in Rajasthan's hard water, every resin fouled by Mumbai's monsoon runoff, every pump that survived Uttar Pradesh's voltage fluctuations—all of this became institutional knowledge.

The numbers tell the story: revenue grew from approximately ₹50 crore in 1985 to over ₹400 crore by 2000. But the real moat wasn't in the financials—it was in the thousands of customer relationships, the library of proprietary solutions, and the network of trained operators across India who knew Ion Exchange systems inside out.

IV. The Three Business Segments Deep Dive

To understand Ion Exchange's economics, you need to think of it as three different companies under one roof, each with distinct dynamics, margins, and growth trajectories. This isn't diversification for its own sake—it's vertical integration masquerading as business segments.

Engineering Segment: The Trophy Hunter

The Engineering segment (58% of revenue in Q1 FY25) provides integrated services and solutions in water & wastewater treatment including Sea Water desalination, Recycle and Zero liquid discharge plants to diverse industries.

This is where Ion Exchange flexes its technical muscle. We're talking about ₹100-500 crore projects: a zero liquid discharge system for a textile park, a 100 MLD sewage treatment plant for a smart city, or a seawater desalination plant for a refinery. These aren't commodity installations—each one is essentially a custom-engineered solution.

The business model here is fascinating. Ion Exchange operates across the entire spectrum: turnkey projects where they handle everything, EPC contracts where they're the prime contractor, and increasingly, BOOT (Build, Own, Operate, Transfer) models where they finance, build, and operate plants for 10-25 years.

BOOT deserves special attention because it's transforming the segment's economics. Instead of lumpy project revenues with 12-15% EBITDA margins, BOOT provides annuity income at 20-25% margins. The catch? It's capital intensive and ties up the balance sheet. But in a water-scarce world, owning water infrastructure is like being a toll collector on an essential highway.

Revenue grew 13% YoY, and EBIT rose 26% YoY in Q1 FY25 supported by steady medium-sized job orders and international contracts. The company expects faster execution of large EPC jobs in coming quarters.

The international piece is crucial. Ion Exchange isn't just competing for Indian projects anymore—they're winning contracts in Bangladesh, Sri Lanka, and Africa, leveraging their emerging market expertise against developed market competitors who over-engineer solutions.

Chemicals Segment: The Cash Cow

This is the misunderstood gem of the portfolio. Everyone focuses on the engineering segment's large projects, but chemicals is where the real economic moat lies.

Ion exchange resins are consumables—they need replacement every 3-7 years depending on usage. Once you've installed an Ion Exchange system, you're essentially locked into their resins unless you want to re-engineer the entire plant. It's the razors-and-blades model, except the blades cost lakhs of rupees.

Beyond resins, the segment includes specialty chemicals for water treatment: coagulants, flocculants, antiscalants, biocides. These aren't sexy products, but they're essential. A power plant can't run without water treatment chemicals any more than a car can run without oil.

The Roha plant expansion is particularly interesting. Ion Exchange is adding capacity not just for current demand but anticipating the zero liquid discharge mandate that's coming to all industries. When every textile mill and paper plant needs ZLD systems by 2027, they'll need specialized resins that only a handful of companies worldwide can produce.

Margins in this segment are attractive—18-20% EBITDA—and more importantly, predictable. It's essentially a subscription business disguised as chemical manufacturing.

Consumer Products: The Problem Child

The consumer products division struggled with an EBIT loss, prompting management to implement structural changes.

This segment is Ion Exchange's biggest strategic puzzle. The logic seemed impeccable: leverage industrial credibility to sell water purifiers to homes. "If we're good enough for nuclear power plants, we're good enough for your kitchen."

But B2C is a different game. Kent and Aquaguard spend crores on cricket sponsorships while Ion Exchange relies on word-of-mouth. The direct-to-consumer water purifier market is brutally competitive with 60+ brands fighting for share.

Where Ion Exchange has found success is in the institutional segment: hotels, hospitals, schools. These customers care more about technical specifications than brand advertisements. A 500-bed hospital needs reliable water treatment, not Shah Rukh Khan's endorsement.

The structural changes being implemented focus on this B2B2C approach—selling to institutions and communities rather than individual homes. It's less sexy than D2C but plays to Ion Exchange's strengths.

V. International Expansion & M&A Strategy

The international story begins in 1976, just twelve years after inception, when Ion Exchange set up its first international plant in Malaysia. This wasn't just contract manufacturing—it was a full-fledged production facility. For context, this was when Indian companies needed government permission to travel abroad, let alone set up factories.

The international expansion followed water scarcity, not GDP growth. Middle East countries with oil wealth but no water became natural markets. Singapore, despite being rich, has always been paranoid about water security. African countries needed low-cost, robust solutions that wouldn't break down when the German engineer flew home.

But the real acceleration came post-2010 when Ion Exchange shifted from organic expansion to acquisitions. The 2018 watershed moment was the Waterleau acquisition. Waterleau Group N.V., a Belgium-based company with 800+ reference plants worldwide, became a wholly owned subsidiary effective from August 20, 2018. This wasn't just buying technology—it was acquiring European market access, anaerobic digestion expertise, and most importantly, credibility in developed markets.

The Waterleau story illustrates Ion Exchange's M&A philosophy: buy distressed or undervalued assets with complementary technology, integrate the IP, and leverage the combined portfolio globally. Waterleau had great technology but was struggling financially. Ion Exchange had cash flow and emerging market expertise but needed developed market credentials.

Then came 2023's masterstroke: the MAPRIL acquisition in Portugal. Ion Exchange acquired 100% stake in MAPRIL - Produtos Químicos e Maquinas Para a Industria, Lda for approximately ₹24 crore. This seems tiny, but MAPRIL gave Ion Exchange something priceless—a manufacturing base inside the EU.

Post-Brexit, having an EU manufacturing entity became crucial for serving European markets without tariff complications. The company stated this synergy will give them a strong footing in the European market. It's regulatory arbitrage disguised as geographic expansion.

The 2018 membrane manufacturing facility in Goa deserves special mention. Inaugurated as a state-of-the-art facility to manufacture world-class membranes, this wasn't just another factory. Membrane technology is to water treatment what semiconductors are to electronics—the highest value-add component. Only a handful of companies globally can manufacture high-quality RO membranes. Ion Exchange joining this club changed the competitive dynamics.

The international strategy has paid off: exports now account for 30% of sales, up from less than 10% a decade ago. More importantly, international projects command better margins because Ion Exchange's emerging market expertise is genuinely differentiated. A German company might build a technically perfect plant in Nigeria, but Ion Exchange builds one that actually works when the power goes out.

VI. Technology Evolution & Innovation

"We're not a water company," an Ion Exchange engineer once told me, "we're a chemistry company that happens to work with water." This distinction is crucial to understanding their competitive advantage.

The technology journey reads like a materials science textbook. It started with ion exchange resins—polymer beads that could selectively remove dissolved ions from water. Think of these as molecular sieves, each designed to catch specific contaminants. The company has completed over 100,000 installations worldwide using variations of this core technology.

But resins were just the beginning. The real innovation came in system integration. A modern water treatment plant is essentially a chemical factory in reverse—instead of making products, it's removing them. This requires understanding not just chemistry but fluid dynamics, process control, and increasingly, data analytics.

The 2019 launch of INDION SWIFT 5Gx exemplified this evolution. Designed to meet growing requirements of high purity water systems for pharmaceutical, power, semiconductor and electronic industries, this wasn't just a better resin—it was a complete system optimized for ultra-pure water production.

The semiconductor connection is fascinating. Making chips requires water so pure that it's essentially an insulator—18.2 megohm-cm resistivity, for the technically inclined. Ion Exchange's ability to deliver this consistently made them critical suppliers to India's nascent semiconductor ambitions. Every fab needs a water treatment partner, and Ion Exchange positioned itself as the only Indian company capable of meeting these specifications.

Zero Liquid Discharge (ZLD) technology represents the current frontier. As environmental regulations tighten, industries can't just treat and discharge wastewater—they need to eliminate liquid discharge entirely. This means evaporating all water and recovering it, leaving only solid waste. It's energy-intensive, technically complex, and absolutely mandatory for new industrial projects in water-scarce regions.

Ion Exchange's ZLD systems combine multiple technologies: preliminary treatment to remove easy contaminants, membrane systems for concentration, evaporators for water recovery, and crystallizers for salt recovery. It's not elegant—it's brute force chemistry. But it works, and more importantly, it works in Indian conditions with Indian operators.

The digital transformation story is still being written. IoT sensors now monitor treatment plants remotely, AI algorithms optimize chemical dosing, and predictive maintenance prevents failures before they happen. But this isn't Silicon Valley-style disruption—it's careful integration of digital tools into industrial processes where failure means factories shut down. The R&D infrastructure is impressive: centers accredited by the Department of Scientific and Industrial Research (DSIR) since 1965, making it one of the oldest water research facilities in India. With an investment of around INR 300 million, the R&D Centre will develop new resins, membranes, polymers and speciality chemical technologies.

But the real technology story isn't in the labs—it's in the field. Every failed installation teaches something. Every customer complaint drives innovation. Ion Exchange's technology evolution isn't driven by PhDs publishing papers but by engineers solving real problems in real factories with real constraints.

VII. Financial Analysis & Unit Economics

The financial story of Ion Exchange is a tale of two businesses fighting for the same balance sheet. On one side, you have the chemicals business—predictable, cash-generative, with attractive returns. On the other, the engineering business—lumpy, working capital intensive, but essential for growth.

Let's start with the headline numbers: revenues stood at Rs 23,940 m in FY24, up from Rs 15,152 m in FY20. Over the past 5 years, revenue has grown at a CAGR of 12.1%. Not bad for an industrial company, but the margin story is more complex.

Operating profit margins witnessed a fall and stood at 11.7% in FY24 as against 13.0% in FY23. Net profit margins during the year declined from 9.8% in FY23 to 8.3% in FY24. This margin compression tells you everything about the business mix shift toward engineering projects.

The working capital situation is the Achilles heel: Company has high debtors of 151 days. Think about what this means—Ion Exchange delivers a ₹100 crore water treatment plant and waits five months to get paid. Meanwhile, they're paying suppliers, workers, and interest costs. It's essentially providing free financing to customers.

Return on capital employed (ROCE) has deteriorated: "Around five years ago returns on capital were 32%, but since then they've fallen to 19%." This isn't necessarily bad management—it's the price of growth through capital-intensive BOOT projects.

The segment-wise performance reveals the underlying dynamics:

Engineering (58% of revenue): Growing fast but margin-dilutive. The shift to BOOT models means Ion Exchange is essentially becoming an infrastructure company, trading margins for annuity revenues.

Chemicals: The cash cow being milked to fund engineering growth. Stable 18-20% EBITDA margins, but growth limited by capacity until the Roha plant comes online.

Consumer Products: The problem child burning cash. Management's "structural changes" are code for "we're trying to stop the bleeding."

Cash flow from operating activities during FY24 stood at Rs 1 billion, an improvement of 107.2% YoY. Cash flow from investing activities stood at Rs -2 billion. Cash flow from financial activities stood at Rs 84 million. Overall, net cash flows stood at Rs -217 million.

The cash flow statement reveals the core challenge: even with improved operating cash flow, heavy capex for expansion means the company remains cash-negative. This isn't necessarily bad—Amazon was cash-negative for years while building infrastructure—but it does mean Ion Exchange needs either strong profits or external financing to fund growth.

The capital allocation debate is fascinating. Should they double down on high-margin chemicals? Pursue more BOOT projects that tie up capital but provide predictable returns? Or fix the consumer business that's destroying value?

Management seems to be choosing all three simultaneously, which either shows confidence or confusion. The market clearly thinks it's the latter, given the stock's underperformance despite water becoming India's most critical resource challenge.

VIII. Competitive Landscape & Market Position

The competitive dynamics in Indian water treatment resemble trench warfare more than blitzkrieg. Everyone knows everyone, margins are fought over basis points, and switching costs create mini-monopolies within customer accounts.

Over the last 5 years, market share decreased from 61.24% to 51.54%. Ion Exchange trades at a P/E (TTM) multiple of 25x vs a 5-year median multiple of 18x. Competitors like Va Tech and Antony trade at P/E (TTM) multiple of 13x and 9x respectively.

The market share erosion is concerning but needs context. The denominator has expanded dramatically as new players entered, particularly Chinese companies offering cut-rate solutions. Ion Exchange chose to defend margins rather than market share—probably the right call given their technology advantages.

The competitive set breaks into distinct categories:

Global Giants: Suez (formerly GE Water), Veolia, and others bring global technology but struggle with Indian market realities. Their solutions are often over-engineered and over-priced for Indian conditions.

Indian Engineering Conglomerates: L&T, Thermax have water divisions but treat them as adjacencies to their core businesses. They compete on projects but lack Ion Exchange's chemical integration.

Pure-Play Water Companies: Va Tech Wabag is the closest comparable, focused purely on water treatment. But they lack Ion Exchange's chemical manufacturing, making them more project executors than technology companies.

Chinese Entrants: The real threat. Chinese companies are flooding the market with cheap membranes and systems. Quality is questionable, but for price-sensitive municipal projects, "good enough" often wins.

Ion Exchange's competitive moat comes from three sources:

-

Installed Base Lock-in: Those 100,000+ installations need consumables, and switching resin suppliers means re-engineering the entire system.

-

Integrated Offering: Being able to supply everything from chemicals to complete plants gives Ion Exchange pricing power and bundling opportunities competitors can't match.

-

Local Manufacturing: While competitors import membranes and resins, Ion Exchange manufactures locally, providing cost advantages and supply chain resilience.

But moats are eroding. The wastewater treatment solutions segment is forecasted to grow at a CAGR of 9.2% from FY21 to FY31. The India water purifier market size reached USD 2.8 billion in 2022, expected to reach USD 5 billion by 2028. This growth is attracting everyone from Tata to Adani, each seeing water as the next infrastructure play.

The regulatory environment is Ion Exchange's best friend. Stricter discharge norms, zero liquid discharge mandates, and groundwater restrictions all drive demand for sophisticated treatment systems. When the government mandates ZLD for textile mills, Ion Exchange doesn't compete on price—they're often the only company that can deliver a working solution.

IX. Playbook: Lessons for Founders & Investors

After six decades, Ion Exchange offers a masterclass in building technical moats in commoditized industries. The lessons aren't always pretty, but they're instructive for anyone trying to build an industrial business in emerging markets.

Lesson 1: Chemistry Beats Software In an age obsessed with asset-light models, Ion Exchange shows the power of owning the full stack. Their resin manufacturing isn't just a business—it's a competitive moat. When you control the consumables, you control the customer relationship. Software companies dream of 90% gross margins; Ion Exchange achieves similar economics through installed base lock-in.

Lesson 2: Emerging Market Engineering is Different Western companies fail in India not because their technology is inferior but because it assumes Western conditions. Ion Exchange succeeded by "tropicalizing" technology—designing for power cuts, unskilled operators, and monsoon flooding. This isn't dumbing down; it's intelligent adaptation.

Lesson 3: Employee Ownership Actually Works The 1984 transition to employee trusts created alignment rarely seen in Indian companies. No promoter siphoning cash through related party transactions. No sons-in-law in corner offices. Just professional management focused on building value. The 25.7% promoter holding might worry some investors, but it's feature, not bug.

Lesson 4: Vertical Integration vs. Focus MBA textbooks preach focus, but Ion Exchange's three-pillar strategy makes strategic sense. Chemicals provide stable cash flow, engineering drives growth, and consumer products... well, two out of three isn't bad. The integration creates cross-selling opportunities and reduces customer acquisition costs.

Lesson 5: The Infrastructure Trap BOOT projects are seductive—predictable revenues, long-term contracts, infrastructure asset creation. But they're also capital intensive and create asset-liability mismatches. Ion Exchange is learning what power and road companies learned a decade ago: infrastructure returns require infrastructure capital structures.

Lesson 6: B2B2C is Harder Than B2B or B2C The consumer products struggle shows the difficulty of straddling markets. B2B buyers care about specifications and service. B2C buyers care about brand and convenience. Trying to serve both with the same organization and mindset usually serves neither well.

Lesson 7: Technical Moats Require Continuous Investment Ion Exchange's R&D spending might seem excessive for an industrial company, but it's table stakes for maintaining technical leadership. The moment you stop innovating, Chinese competitors will copy your last innovation and sell it at 50% discount.

Lesson 8: Market Timing Matters Less Than Market Structure Ion Exchange entered water treatment when India had barely any industry to treat water for. They survived because they bet on market structure (India would industrialize) rather than market timing (when it would happen).

For investors, the Ion Exchange story offers a framework for evaluating industrial companies in emerging markets: Do they own the technology or just license it? Can they manufacture locally or do they assemble imports? Do they sell products or solutions? Are they building assets or capabilities?

X. Bear vs. Bull Case

The Bear Case: Why Ion Exchange Could Struggle

The bears have compelling arguments, starting with the ownership structure. Promoter holding is low: 25.7%. In Indian markets, low promoter holding often signals either lack of confidence or vulnerability to hostile takeovers. Without a strong promoter, who drives long-term strategy versus quarterly earnings?

The financial deterioration is undeniable. ROCE falling from 32% to 19% over five years isn't a rounding error—it's value destruction. The company is generating lower returns on incrementally higher capital, the definition of destroying economic value.

Working capital management remains abysmal. Those 151-day receivables mean Ion Exchange is essentially a bank that happens to make water treatment equipment. In a rising rate environment, financing customers becomes increasingly expensive.

The consumer products division is a disaster. Continuing to burn cash in a segment where you have no competitive advantage is either stubbornness or stupidity. Management's "structural changes" feel like rearranging deck chairs on the Titanic.

Competition is intensifying from every direction. Global giants are localizing, Indian conglomerates are entering water, and Chinese companies are dumping products. Ion Exchange's market share erosion from 61% to 51% might accelerate.

The technology disruption risk is real. New membrane technologies, biological treatment methods, or even atmospheric water generation could obsolete traditional treatment methods. Ion Exchange's heavy investments in conventional technology could become stranded assets.

Valuation looks stretched. Trading at 25x P/E versus competitors at 9-13x assumes execution perfection. Any disappointment—a delayed project, a bad debt, a failed product launch—could trigger multiple compression.

The ESG paradox is particularly troubling. Ion Exchange enables water treatment but their chemical manufacturing has its own environmental footprint. As ESG criteria tighten, chemical companies face increasing scrutiny and compliance costs.

The Bull Case: Why Ion Exchange Could Soar

The bulls see a different movie, starting with the inexorable water crisis. India can treat 44% of sewage while only 28% is actually treated. There is huge headroom to grow as industrialization increases and Government focuses on reducing open sewage disposal.

This isn't cyclical demand—it's structural. Every new factory needs water treatment. Every existing factory faces tighter discharge norms. Every city needs sewage treatment. The TAM isn't just large; it's mandatory.

The international expansion is hitting inflection. With 30% of revenue from exports and European manufacturing through MAPRIL, Ion Exchange is becoming a genuine multinational. International revenues carry higher margins and provide currency diversification.

The technology portfolio is genuinely differentiated. Few companies globally can offer everything from basic resins to zero liquid discharge systems. This isn't commodity manufacturing—it's sophisticated chemical engineering with decades of IP accumulation.

Government initiatives are massive tailwinds. Jal Jeevan Mission, Namami Gange, Smart Cities—every major government program has water treatment components. Ion Exchange's experience with government contracts, while painful for working capital, provides competitive advantages in execution.

The replacement cycle is accelerating. Those 100,000 installations don't last forever. Resins need replacement every 3-7 years. Membranes fail. Systems need upgrades. This installed base is an annuity disguised as a project business.

The Roha plant expansion could be transformative. Adding resin capacity just as ZLD mandates kick in positions Ion Exchange to capture outsized market share. The operational leverage from higher capacity utilization could drive significant margin expansion.

Climate change is the ultimate catalyst. As water becomes scarcer, treatment becomes more valuable. As regulations tighten, compliance becomes mandatory. As industries grow, water demand explodes. Ion Exchange sits at the intersection of all three trends.

The valuation discount to potential is significant. If Ion Exchange can stabilize ROCE at 25%, fix consumer products, and maintain 15% revenue growth, the stock could double. The market is pricing in execution failure, creating opportunity if management delivers.

XI. Recent Developments & Future Outlook

The stock market has been brutal to Ion Exchange, despite the promising fundamentals. After reaching an all-time high of ₹768.40 on July 26, 2024, the stock has corrected sharply, showing a -35.10% decrease over the last year. This isn't company-specific weakness—it's the market repricing industrial stocks amid global uncertainty.

Net profit of Ion Exchange rose 8.32% to Rs 48.70 crore in Q1 FY25 versus Rs 44.96 crore in Q1 FY24. Sales rose 2.75% to Rs 583.19 crore. The modest growth masks underlying strength in order bookings and international expansion.

For March 2025, consolidated net sales rose 6.75% to Rs 834.56 crore. However, net profit fell 12.97% to Rs 63.35 crore. The profit decline reflects investment in growth rather than operational weakness—classic J-curve dynamics.

The future trajectory depends on several key variables:

Regulatory Evolution: The zero liquid discharge mandate for industries could be Ion Exchange's iPhone moment—a regulatory change that creates massive, mandatory demand. If implemented as planned, every textile mill, tannery, and chemical plant needs ZLD systems by 2027.

Technology Disruption: Ion Exchange must navigate the transition from chemical to biological treatment, from manual to automated operations, from standalone systems to integrated platforms. Their R&D investments suggest they understand this, but execution remains uncertain.

Capital Structure Optimization: The current debt-equity mix isn't optimal for an infrastructure-style business. Ion Exchange needs patient capital—perhaps private equity or infrastructure funds—to finance BOOT projects without destroying ROCE.

Geographic Diversification: The European acquisition provides a beachhead, but real international success requires winning projects against established competitors. Ion Exchange's emerging market expertise could be the differentiator, particularly in Africa and Southeast Asia.

Industrial Growth: India's manufacturing ambitions—from semiconductors to solar panels—all require sophisticated water treatment. If India achieves even half its manufacturing targets, water treatment demand could surprise dramatically to the upside.

The management seems cautiously optimistic, expecting "faster execution of large EPC jobs in coming quarters." This isn't promotional language—Ion Exchange management has historically been conservative in guidance.

The key monitorables for investors: order book growth (leading indicator), working capital days (operational efficiency), ROCE trajectory (capital allocation), and segment-wise margins (business mix). If Ion Exchange can show improvement in any two of these four metrics, the stock could re-rate significantly.

The water crisis isn't getting solved anytime soon. If anything, it's accelerating. The question isn't whether Ion Exchange will benefit, but whether they can execute fast enough to capture the opportunity. After 60 years of building capabilities, the next decade could be their defining moment.

The story of Ion Exchange is ultimately about the intersection of chemistry and capitalism, of solving essential problems with unglamorous solutions. In a world chasing the next software unicorn, there's something refreshing about a company that makes its money ensuring humans have clean water to drink and industries have treated water to operate.

Whether Ion Exchange becomes India's water infrastructure champion or remains a solid but unspectacular industrial company depends on execution over the next few years. The pieces are in place—technology, relationships, manufacturing capacity, and most importantly, a water crisis that demands solutions.

For long-term investors, Ion Exchange offers exposure to one of humanity's most fundamental challenges with a company that has spent six decades building capabilities to address it. The stock may not double overnight, but in a world running out of water, owning the company that knows how to treat it might be the ultimate defensive investment.

The employee-owned structure that seemed anachronistic in 1984 might prove prescient in 2025. Without promoter pressures for dividends or related-party transactions, Ion Exchange can focus on long-term value creation. In an era of quarterly capitalism, that patience could be their greatest competitive advantage.

As India stumbles toward water day zero—the day when taps run dry—Ion Exchange stands ready with solutions developed over six decades. They may not be the sexiest company in your portfolio, but when the water stops flowing, they might be the most essential.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube