Interarch Building Solutions: Engineering India's Infrastructure Revolution

I. Introduction & Episode Roadmap

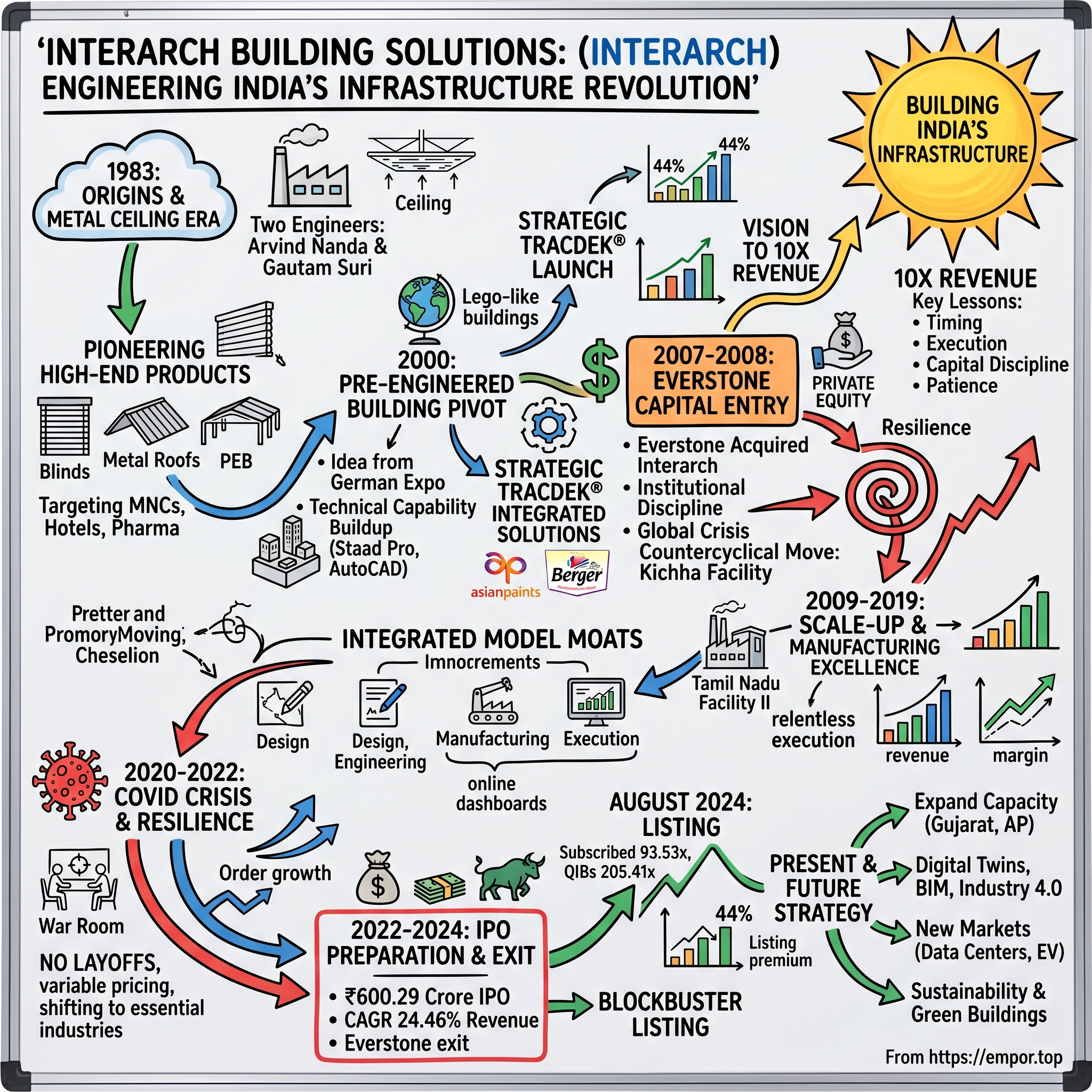

Picture this scene: A rain-soaked construction site in Gujarat, 1983. Two engineers stand surveying an empty warehouse, their hands clutching blueprints for metal ceiling systems nobody in India had seen before. Arvind Nanda turns to Gautam Suri—"If we build it right, they will come." With just two employees and a vision to revolutionize India's construction landscape, they founded what would become Interarch Building Solutions.

Fast forward four decades: The company now operates with over 2,000 employees, five advanced manufacturing facilities, and a robust nationwide presence. Market capitalization as of May 2025 stands at approximately Rs. 3400 crore, with turnover exceeding Rs. 1400 crore annually. But the real story isn't just in these numbers—it's in how a metal ceiling company transformed into India's pre-engineered building powerhouse, riding every wave of the country's infrastructure boom while somehow staying ahead of multinational giants.

Today's journey takes us through boardroom battles with private equity, the gut-wrenching decisions during COVID-19, and a blockbuster IPO that left investors scrambling. We'll decode how Interarch cracked the code on India's fragmented construction market, why Everstone Capital bet big on them in 2007, and what their future holds as India builds its way to becoming the world's third-largest economy.

This isn't just a story about steel and concrete—it's about timing, transformation, and the art of building a business that quite literally builds India.

II. Origins & The Metal Ceiling Era (1983–2000)

The year was 1983. India's construction industry operated like it had for centuries—brick by brick, beam by beam. Founded by visionaries Mr. Arvind Nanda and Mr. Gautam Suri, Interarch Building Solutions Ltd. began as a modest two-employee firm in New Delhi. But these weren't your typical entrepreneurs. Nanda, an IIT Delhi graduate, had seen modern construction techniques abroad. Suri brought deep relationships in Delhi's industrial circles. Together, they spotted what others missed: India's commercial buildings were crying out for modern interior solutions.

The company commenced operations in 1983, with the manufacture and sale of metal suspended ceiling systems under the brand "TRAC®". Think about the audacity—selling metal ceilings in a market that barely understood false ceilings, let alone premium metal ones. Their first factory was more workshop than plant, tucked away in an industrial area of Delhi. Every sale required education, every project a leap of faith from the customer.

By 1984, Interarch had pioneered the high-end metal interior products market in India, being the first mover from metal ceilings to blinds, metal roofing to pre-engineered buildings. The early customers weren't the government buildings or mass developers you'd expect. Instead, they targeted multinational corporations setting up Indian offices, five-star hotels wanting international standards, and pharmaceutical companies needing clean-room specifications.

The challenge wasn't just selling a product—it was selling a concept. Indian architects in the 1980s sketched with concrete and plaster in mind. Interarch's team would sit for hours with designers, showing them international catalogs, explaining acoustic properties, demonstrating installation techniques that seemed almost magical compared to traditional methods. One early employee recalls Nanda personally supervising installations at 2 AM to ensure perfection, knowing that one failed project could destroy their reputation.

By the mid-1990s, something interesting happened. The liberalization of 1991 had opened floodgates of foreign investment. Suddenly, every multinational wanted Grade-A office space. Indian companies, not to be outdone, began upgrading their facilities. Interarch's order book swelled. The TRAC® brand became synonymous with quality metal ceilings—a remarkable achievement in a market that hadn't known the product category existed a decade earlier.

But Nanda and Suri saw beyond ceilings. They watched international construction trends, studied how buildings were going up faster in Southeast Asia, noticed the pre-engineered building revolution happening globally. The metal ceiling business had given them three critical assets: credibility in the construction industry, relationships with large corporations, and most importantly, manufacturing expertise in metal fabrication. The stage was set for a bigger play.

III. The Pre-Engineered Building Pivot (2000–2007)

The new millennium brought a revelation wrapped in opportunity. Nanda had just returned from a construction expo in Germany where he witnessed something that stopped him cold: entire factories being assembled like giant Lego sets. Pre-engineered buildings—structures designed in software, manufactured in factories, and assembled on-site in weeks rather than months. India's booming economy needed infrastructure yesterday, and traditional construction couldn't keep pace.

The pivot wasn't obvious to everyone. Board meetings in 2000 grew heated. Why abandon a profitable ceiling business for an unproven market? But Nanda and Suri had done their homework. India's manufacturing sector was exploding—pharmaceuticals, automobiles, textiles—all needed factories, warehouses, and distribution centers. Traditional construction took 12-18 months for a mid-sized facility. PEBs could do it in 3-4 months.

The technical capability buildup was methodical. First, they hired structural engineers from India's top institutions. Then came investments in design software—expensive licenses for Staad Pro and AutoCAD that cost more than most Indian companies' annual profits. The Pantnagar Manufacturing Facility was set up in 2005, marking their serious entry into PEB manufacturing. This wasn't just another factory; it was a statement of intent.

The TRACDEK® brand launch for metal roofing and cladding systems was strategic genius. Instead of competing head-on with established PEB players, Interarch positioned itself as the complete building envelope solution provider. While competitors sold structures, Interarch sold integrated solutions—structure, roofing, cladding, and interiors. One-stop shopping for industrial construction.

Early customer wins read like a who's who of Indian industry. Asian Paints needed a new plant in record time. Delivered. Berger Paints wanted earthquake-resistant structures. Designed and built. Each successful project became a reference, each satisfied customer a evangelist. The repeat order rate climbed steadily—a metric that would become Interarch's calling card.

The Pantnagar facility undertook production of PEB steel structures, comprising complete PEBs, primary systems (consisting of built-up sections such as H-shaped and I-shaped structures), and secondary framing systems. Unlike trading companies that imported knocked-down kits, Interarch built integrated capabilities. They could design, engineer, manufacture, and erect—controlling quality at every step.

By 2007, revenues had crossed Rs. 500 crore. The order book was bursting. But growth required capital—for new factories, working capital, technology upgrades. The founders faced a crossroads: remain a profitable mid-sized player or bring in external capital to scale aggressively. Private equity firms circled, sensing opportunity. Among them, one stood out with a compelling vision: Everstone Capital.

IV. The Private Equity Chapter: Everstone Entry (2007–2008)

On December 4, 2007, private equity firm Everstone Group acquired Interarch Building Products. The timing seemed perfect—India's infrastructure boom was accelerating, and industrial construction was hitting record highs. But within months, Lehman Brothers collapsed, and the world plunged into financial crisis.

Everstone wasn't a typical private equity firm. Founded in 2006, it primarily operated from Singapore, focusing on mid-market companies with strong fundamentals and growth potential. For Interarch, the attraction went beyond capital. Everstone brought institutional discipline, international best practices, and crucially, the patience to build for the long term rather than flip for quick returns.

The transformation from family business to professionally managed company wasn't painless. Everstone insisted on independent directors, formal board processes, and quarterly performance reviews. For founders accustomed to intuitive decision-making, the new rigor felt constraining. Yet it was precisely this discipline that would help them navigate the approaching storm.

The Kichha Manufacturing Facility was set up in 2008, even as the global financial crisis decimated construction markets worldwide. While competitors froze expansion plans, Interarch doubled down. Steel prices had crashed, making factory construction cheaper. Skilled workers were available as other projects stalled. What looked like terrible timing became a countercyclical masterstroke.

The crisis management playbook that emerged would serve them well in future downturns. First, protect cash flow—they renegotiated payment terms with suppliers while offering discounts for early payment from customers. Second, focus on quality clients—government projects and blue-chip corporations that wouldn't default. Third, use the downturn to build capabilities—training programs, process improvements, technology upgrades that would pay dividends when markets recovered.

Everstone's network opened new doors. International best practices in project management, introductions to global suppliers, and most importantly, the credibility that came with institutional backing. When clients worried about vendor stability during the crisis, Everstone's backing provided reassurance. The PE firm wasn't just writing checks; they were active partners in building the business.

V. Scale-Up & Manufacturing Excellence (2009–2019)

As India emerged from the global financial crisis, infrastructure spending exploded. The government launched ambitious programs—industrial corridors, smart cities, Make in India. Every initiative needed buildings, and fast. Interarch was perfectly positioned.

Tamil Nadu Manufacturing Facility II was set up in Sriperumbudur in 2009. This wasn't just capacity addition; it was strategic positioning in South India's manufacturing hub. The facility's location—close to Chennai port, surrounded by automotive and electronics manufacturers—wasn't accidental. Logistics costs could make or break PEB economics, and Interarch understood the importance of being close to demand centers.

Interarch Building Products ranked 3rd in operating revenue from the PEB business in FY2024 among integrated Indian players. The climb to this position happened during this decade of relentless execution. While competitors struggled with quality issues or focused on trading, Interarch built deep manufacturing capabilities. Five integrated manufacturing facilities gave them flexibility others couldn't match—if one plant was busy, another could take the order.

Technology adoption transformed operations. 3D modeling reduced design errors. Automated welding improved consistency. ERP systems connected design to procurement to production to site execution. A customer could track their building's progress from steel cutting to final erection through online dashboards—transparency that was revolutionary in Indian construction.

The integrated model created powerful moats. When steel prices spiked, traders struggled with margin compression. Interarch's manufacturing efficiency provided a buffer. When customers wanted customization, trading companies had to refuse or outsource. Interarch's design team could modify on the fly. When projects faced site challenges, competitors pointed fingers at subcontractors. Interarch's project managers owned the solution.

Customer diversification was deliberate and strategic. Industrial clients—pharmaceuticals, automotive, FMCG—provided steady base load. Infrastructure projects—airports, metro stations, convention centers—offered large, prestigious contracts. Commercial buildings—warehouses, logistics parks, data centers—emerged as a growth driver as e-commerce exploded. No single sector dominated, insulating them from industry-specific downturns.

The numbers tell the story of operational excellence. Revenue grew steadily, but more importantly, margins expanded. The EBITDA margin improvement from 2% in FY19 to nearly 10% by decade-end wasn't luck—it was operational leverage from higher capacity utilization, better project selection, and improved execution efficiency. Every percentage point of margin represented millions in additional profit, funding further expansion without diluting equity.

VI. COVID Crisis & Supply Chain Resilience (2020–2022)

March 2020. India announced the world's strictest lockdown. Construction sites emptied overnight. For a company whose business was building buildings, the pandemic was an existential threat. Revenue evaporated, but fixed costs remained. The Everstone board convened emergency meetings—virtually, a first for the traditionally in-person leadership team.

The immediate priority was liquidity. CFO-led war rooms modeled cash scenarios—best case, base case, worst case, and what they grimly called "survival case." Every expenditure was scrutinized. But critically, they made a decision that would define their culture: no layoffs. While competitors shed workers, Interarch kept its 2,000-strong workforce intact, even paying partial salaries during complete lockdown.

Net profit of Rs 171 million in FY22 and Rs 64 million in FY21 reflected the pandemic's brutal impact. But these numbers don't capture the operational gymnastics required to achieve even these reduced profits. When lockdowns lifted partially, they had to manage sites with 50% workforce, arrange transportation for workers in bubbles, and establish on-site quarantine facilities. Each project became a complex logistics puzzle.

Steel price volatility turned extreme. Prices doubled in 12 months as global supply chains broke down. For a business where steel constituted 87% of raw material costs, this was potentially catastrophic. The management's response showed strategic thinking under pressure. They shifted to variable pricing contracts where possible, hedged positions through strategic buying, and most importantly, transparently communicated with customers about price pressures, building trust that would pay dividends later.

The recovery strategy was multi-pronged. First, they focused on government infrastructure projects that continued despite lockdowns. Second, they pivoted to essential industries—pharmaceuticals needed COVID vaccine facilities, e-commerce needed warehouses, data centers needed expansion. Third, they accelerated digital transformation—remote project monitoring, virtual customer meetings, digital documentation—changes that improved efficiency even after normalcy returned.

By early 2022, something remarkable had happened. The company that many thought wouldn't survive emerged stronger. The order book swelled as pent-up demand released. Customers who had watched Interarch honor commitments during crisis now preferred them over competitors who had walked away from projects. The crisis had become a differentiator.

VII. The IPO Preparation & Everstone Exit (2022–2024)

The boardroom discussions in early 2022 were intense. After 15 years, Everstone was ready to exit—a typical PE timeline, even for patient capital. But the timing seemed perfect. India's infrastructure spending was hitting record highs, the company had proven its resilience through COVID, and capital markets were hungry for infrastructure plays.

The transformation into Interarch Building Solutions from Interarch Building Products wasn't just cosmetic. It signaled evolution from a product company to a solutions provider. The corporate restructuring that followed was extensive—cleaning up inter-company transactions, streamlining subsidiaries, strengthening governance structures. Every aspect was scrutinized through public market lens.

Revenue grew from Rs 834.94 crore in FY22 to Rs 1,293.30 crore in FY24, achieving a CAGR of 24.46%, PAT rose from Rs 17.13 crore in FY22 to Rs 81.46 crore in FY23, and further to Rs 86.26 crore in FY24. These weren't just recovery numbers—they represented fundamental business strength. The company had emerged from crisis with better customers, improved operations, and stronger market position.

The IPO of ₹600.29 crores was a combination of fresh issue of 0.22 crore shares aggregating to ₹200.14 crores and offer for sale of 0.44 crore shares aggregating to ₹400.15 crores. The structure was carefully calibrated—enough fresh capital for growth without excessive dilution, while providing Everstone its exit. OIH Mauritius Limited (Everstone Capital) would exit through the offer for sale, ending a successful 17-year partnership.

The roadshow presentations told a compelling story. India's pre-engineered building market was projected to grow from ₹195 billion to ₹340 billion by FY29. Interarch was perfectly positioned—second-largest capacity, integrated model, strong brand, proven execution. Institutional investors were particularly impressed by one metric: repeat orders had improved from 59% in FY22 to 81% in FY24. In a project business, such customer stickiness was gold.

The IPO documents revealed fascinating details about the business model. Order mix of 75% fixed contract and 25% variable contract provided balance between margin certainty and risk management. Average order size of Rs. 12 crore with execution time of 4-12 months meant steady cash generation. The qualified pipeline of Rs. 4,000 crore with historical hit rate of 20-27% provided clear revenue visibility.

VIII. The Blockbuster Listing & Market Reception (August 2024)

IPO bidding started from Aug 19, 2024 and ended on Aug 21, 2024. The allotment was finalized on Aug 22, 2024. The shares got listed on BSE, NSE on Aug 26, 2024. But the real action happened in the three days of bidding.

Day one opened with tentative interest. Retail investors, burned by recent IPO failures, approached cautiously. The IPO price band was set at ₹900.00 per share. In the grey market, premiums fluctuated wildly—Rs. 300 in the morning, Rs. 350 by evening. WhatsApp groups buzzed with speculation. Was this another infrastructure story that would disappoint?

Day two changed everything. The issue was booked over 3.20 times on the first day and attracted strong response from wealthy individuals and retail bidders, booking over 7 times by day two with HNI portion booked 19.5 times. High net worth individuals, who had done their homework, piled in. Their logic was simple: at 15x FY24 earnings, this was cheap for a debt-free, high-growth infrastructure play.

The final day saw institutional investors join the party. The issue was booked over 10 times by day two and continued to attract strong response on the third and final day as institutional investors joined, with the issue eventually being subscribed 62x with QIB and HNI portions booked over 100 times. The issue was overall subscribed 93.53 times, with QIBs quota booked 205.41 times.

Listing day, August 26, 2024, arrived with palpable excitement. The company's shares were listed at Rs 1,291 on the BSE, marking a 43.46% premium over the upper end of its issue price of Rs 900. On the NSE, shares opened at Rs 1,299, reflecting a 44.43% premium. Investors saw a return of Rs 399 per share, or over 44%, post-listing.

The market reception wasn't just about listing gains. Analysts dissected the fundamentals. The company was debt-free with surplus cash. Capacity expansion was funded and underway. The order book of Rs. 1,153 crore provided 9-10 months of revenue visibility. In a market starved of quality infrastructure plays, Interarch offered a rare combination: proven execution, strong growth, and reasonable valuations.

Post-listing performance validated investor confidence. The stock held its gains, trading volume remained healthy, and research coverage expanded. Brokerages initiated coverage with buy ratings, citing the infrastructure super-cycle thesis. The successful listing also marked Everstone's profitable exit—a 17-year journey from Rs. 100 crore investment to Rs. 400 crore exit, not counting interim dividends and capital returns.

IX. Current Operations & Competitive Position (2024–Present)

Interarch has the second largest aggregate installed capacity of 1,61,000 mt/annum as of December 2024. But capacity is just one part of the story. The real competitive advantage lies in the integrated model spanning design, engineering, manufacturing, and execution.

The new AP plant at Attivaram was inaugurated on September 4, 2024, equipped with advanced technology and automated machinery. This isn't just another factory. It represents the next generation of PEB manufacturing—Industry 4.0 enabled, with IoT sensors tracking production, AI optimizing cutting patterns, and automated material handling reducing waste. The plant can switch between different building specifications without retooling, providing flexibility that pure traders can't match.

For Q4FY25, net profit rose 25.01% to Rs 107.83 crore, Sales rose 12.41% to Rs 1453.83 crore. The margin expansion tells the deeper story. Despite steel price volatility and competitive pressure, EBITDA margins are expanding. This isn't pricing power—it's operational excellence. Better capacity utilization, improved product mix favoring complex projects, and technology-driven efficiency gains.

The market position as the #3 player in integrated PEB segment might seem modest, but it's deceptive. In the organized sector, only a handful of players have integrated capabilities. Most competitors are either pure traders importing from China or small fabricators without design capabilities. Interarch competes in a different league—complex projects requiring customization, tight timelines demanding execution excellence, blue-chip clients expecting quality assurance.

Customer mix reveals strategic positioning. Industrial clients—Asian Paints, Berger, Timken—provide steady business with multi-location requirements. Infrastructure projects—convention centers, airport hangars, metro depots—offer large-ticket contracts with higher margins. The emerging data center segment, driven by India's digital transformation, represents the future. These aren't just buildings; they're precision-engineered environments requiring specialized expertise.

Technology edge manifests in multiple ways. Design software creates 3D models that clients can walk through virtually before construction begins. Project management systems provide real-time visibility from factory floor to construction site. Quality control uses ultrasonic testing and x-ray inspection—overkill for simple warehouses but essential for critical infrastructure. This technology moat deepens with each project, as learnings get coded into systems and processes.

X. Future Strategy & Growth Vectors

The infrastructure boom thesis isn't hope; it's mathematical certainty. India's construction market is projected to grow by 11.2% annually to INR 25.31 trillion by 2025, with a forecasted CAGR of 8.8% during 2025-2029, expected to reach about INR 39.10 trillion by 2029. For perspective, that's larger than many countries' entire GDP.

The Indian PEB market is valued at approximately ₹195 billion in FY24 and is projected to grow to ₹340 billion by FY29. But the real opportunity lies in market share shift. Currently, unorganized players control 55% of the market. As projects become larger and more complex, as customers demand quality and timelines, the organized sector's share will expand. Interarch doesn't need the market to grow; it just needs to capture share from the unorganized sector.

Capacity expansion follows a hub-and-spoke model. The new facility planned for Gujarat isn't random—it positions them at the heart of India's industrial corridor. Each integrated plant has revenue potential of Rs. 550 crore. With five facilities operational and more planned, the company targets doubling revenue to Rs. 2,500 crore by 2028. Ambitious? Yes. Achievable? The track record suggests so.

New market opportunities read like a technology trends report. Data centers need specialized structures with massive cooling requirements and zero-downtime construction. E-commerce warehouses require clear spans exceeding 100 meters and multi-level configurations. Electric vehicle factories need clean rooms and specialized flooring. Each segment requires expertise that commodity players can't provide.

Technology investments focus on digital twins—virtual replicas of physical buildings that enable predictive maintenance, energy optimization, and future modifications. Building Information Modeling (BIM) integration allows seamless collaboration between architects, engineers, and contractors. These aren't buzzwords; they're competitive differentiators that justify premium pricing.

Sustainability initiatives address tomorrow's requirements today. Green building certifications, solar-ready structures, and rainwater harvesting integration aren't add-ons—they're built into standard designs. As ESG requirements tighten, as carbon taxes loom, buildings that don't meet sustainability standards will face obsolescence. Interarch is positioning for this future.

XI. Playbook: Lessons from the Journey

Building an integrated model in a fragmented industry requires patience that quarterly capitalism rarely permits. Interarch spent two decades vertically integrating while competitors chased quick profits through trading. The integrated model meant lower margins initially but created compounding advantages—quality control, customization capability, and crucially, customer trust that translates to pricing power.

Managing commodity risk in a business where steel constitutes 87% of costs requires sophistication beyond simple hedging. The order mix of 75% fixed contract and 25% variable contract provides natural hedging. When steel prices rise, variable contracts protect margins. When prices fall, fixed contracts lock in profits. This portfolio approach, borrowed from financial markets, provides stability in volatile commodity markets.

Customer retention excellence shows in repeat orders improving from 59% in FY22 to 81% in FY24. In project businesses, customer acquisition costs are massive—bidding expenses, design work, relationship building. A customer retained is worth five customers acquired. Interarch's systematic approach to customer success—dedicated account managers, post-project reviews, proactive maintenance—turns one-time buyers into lifetime partners.

The private equity to public markets transition offers a masterclass in stakeholder management. Everstone's 17-year holding period—exceptional for PE—provided stability for long-term building. The exit through IPO rather than strategic sale preserved company independence. The founders retaining majority stake post-IPO ensures continuity. This isn't financial engineering; it's thoughtful capitalism where all stakeholders win.

Creating value through operational excellence rather than financial leverage distinguishes sustainable businesses from market darlings. Interarch remained virtually debt-free through its growth journey. Every factory was funded through internal accruals or equity. This conservative approach meant slower growth initially but provided resilience during downturns and flexibility during opportunities.

XII. Bear vs. Bull Case Analysis

Bull Case:

The infrastructure super-cycle isn't a thesis; it's happening. India's construction industry is expected to grow by 7.1% in real terms in 2025, with the FY2025-26 Budget outlining total expenditure of INR50.7 trillion ($603 billion), including INR2.9 trillion for highways and INR2.6 trillion for railways. Every rupee of government spending creates multiplier effects—roads need warehouses, railways need stations, ports need storage facilities.

The company is almost debt free and has delivered good profit growth of 22.4% CAGR over last 5 years. In a capital-intensive industry, this financial strength provides enormous flexibility. They can bid for large projects without consortium partners, offer credit terms that cash-strapped competitors can't match, and invest in technology without diluting returns.

The order book and execution capabilities create a virtuous cycle. Strong execution leads to repeat orders, which improves capacity utilization, which enhances margins, which funds expansion, which enables larger projects. With second-largest capacity among organized players and proven project management, Interarch can bid for projects others can't execute.

Market consolidation opportunity remains massive. The unorganized sector's 55% market share will shrink as GST compliance, quality requirements, and project complexity increase. Every percentage point of share gained from unorganized players represents Rs. 20 crore in additional revenue. Interarch doesn't need to beat organized competitors; it just needs to be better than tin-shed fabricators.

Bear Case:

Steel price volatility could destroy margins overnight. While the company has risk management strategies, a sustained spike in steel prices combined with fixed-price contracts could create a perfect storm. The 87% raw material cost exposure means even small fluctuations significantly impact profitability.

Competition from international players, particularly Chinese manufacturers, poses existential threat. If trade barriers reduce or diplomatic relations improve, low-cost Chinese PEB kits could flood the market. Indian manufacturers' cost structure can't compete with Chinese scale and state subsidies.

Working capital intensity remains a structural challenge. Construction businesses require funding projects upfront while collecting payments over extended periods. As the company scales, working capital requirements could balloon, forcing debt or dilution. Current efficiency metrics look good, but larger projects with government clients could stretch payment cycles.

Execution risks multiply with scale. Managing five factories, hundreds of projects, thousands of workers—complexity increases exponentially. One major project failure, one serious accident, one quality issue could damage reputation built over decades. In project businesses, reputation is everything, and it's fragile.

XIII. Power & "What If" Scenarios

What if they hadn't pivoted from metal ceilings to PEB? They'd probably be a profitable Rs. 100 crore company, competing with imports in a commoditizing market. The ceiling business provided the foundation—customer relationships, manufacturing expertise, brand credibility—but PEB provided the growth runway. Timing the pivot before the infrastructure boom was either prescient or lucky, probably both.

What if Everstone hadn't invested in 2007? The company might have remained family-owned, growing organically but slowly. Everstone's capital enabled counter-cyclical expansion during the 2008 crisis, institutional discipline improved operations, and PE backing provided credibility with large customers. The 17-year partnership, rare in PE, provided stability for long-term building.

What if they had gone public during the 2021 IPO boom? They would have achieved higher valuations—the market was paying ridiculous multiples for anything infrastructure-related. But they would have also faced pressure for quick growth, possibly compromising project selection or execution quality. The 2024 IPO, after proving COVID resilience and achieving scale, attracted quality investors rather than momentum traders.

Could they become the "Asian Nucor"? Nucor revolutionized American steel through mini-mills and operational excellence. Interarch could similarly revolutionize Indian construction through technology and integration. The ingredients exist—strong operations, technology focus, financial strength. But it requires sustained execution over decades, resisting temptations for unrelated diversification or financial adventures.

M&A opportunities abound in the fragmented market. Acquiring regional players would provide immediate capacity and market access. Technology companies could add digital capabilities. International partnerships could bring global best practices. But integration challenges have destroyed many ambitious roll-ups. Organic growth might be slower but safer.

XIV. Epilogue & Final Reflections

From two employees to 2000+, from metal ceilings to infrastructure backbone, from family business to public company—Interarch's transformation mirrors India's economic journey. They didn't just ride the infrastructure wave; they helped create it, one building at a time.

Building India's infrastructure, literally, carries profound responsibility. Every factory enables manufacturing, every warehouse supports commerce, every data center powers digital India. Interarch's structures aren't just steel and concrete; they're the physical foundation of economic growth. When historians write about India's rise, the buildings will be footnotes, but they'll be essential footnotes.

Key success factors emerge clearly: timing (entering PEB before the boom), execution (consistent delivery building trust), capital discipline (staying debt-free despite growth temptations), and perhaps most importantly, patience (building capabilities over decades rather than quarters). These aren't easily replicable, which explains why so few have succeeded at scale.

The next decade poses a fascinating question: Can they 10x from here? Growing from Rs. 1,500 crore to Rs. 15,000 crore requires more than linear scaling. It needs new markets (exports?), new products (modular construction?), or consolidation (roll-up strategy?). The foundation exists—brand, balance sheet, and business model. The execution will determine whether Interarch becomes India's construction champion or remains a successful niche player.

The lesson for entrepreneurs and investors is nuanced. Building a successful business in India requires understanding that the country doesn't just need products; it needs solutions. It doesn't just need vendors; it needs partners. It doesn't just need growth; it needs sustainable growth. Interarch succeeded by recognizing these truths early and executing consistently. In a market full of sprinters, they ran a marathon.

As we close this episode, remember that every building tells a story. The next time you drive past a modern factory or warehouse, there's a chance it's an Interarch structure. Behind that steel frame lies four decades of evolution, ambition, and execution. That's the real infrastructure story—not just what gets built, but who builds it and how.

The company that started with two people and a vision for better ceilings now builds the structures that house India's ambitions. From metal ceilings to manufacturing India's future—that's not just business growth; that's nation-building, one pre-engineered beam at a time.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube