Intellect Design Arena: The FinTech Transformation Story from Chennai

I. Introduction & Episode Thesis

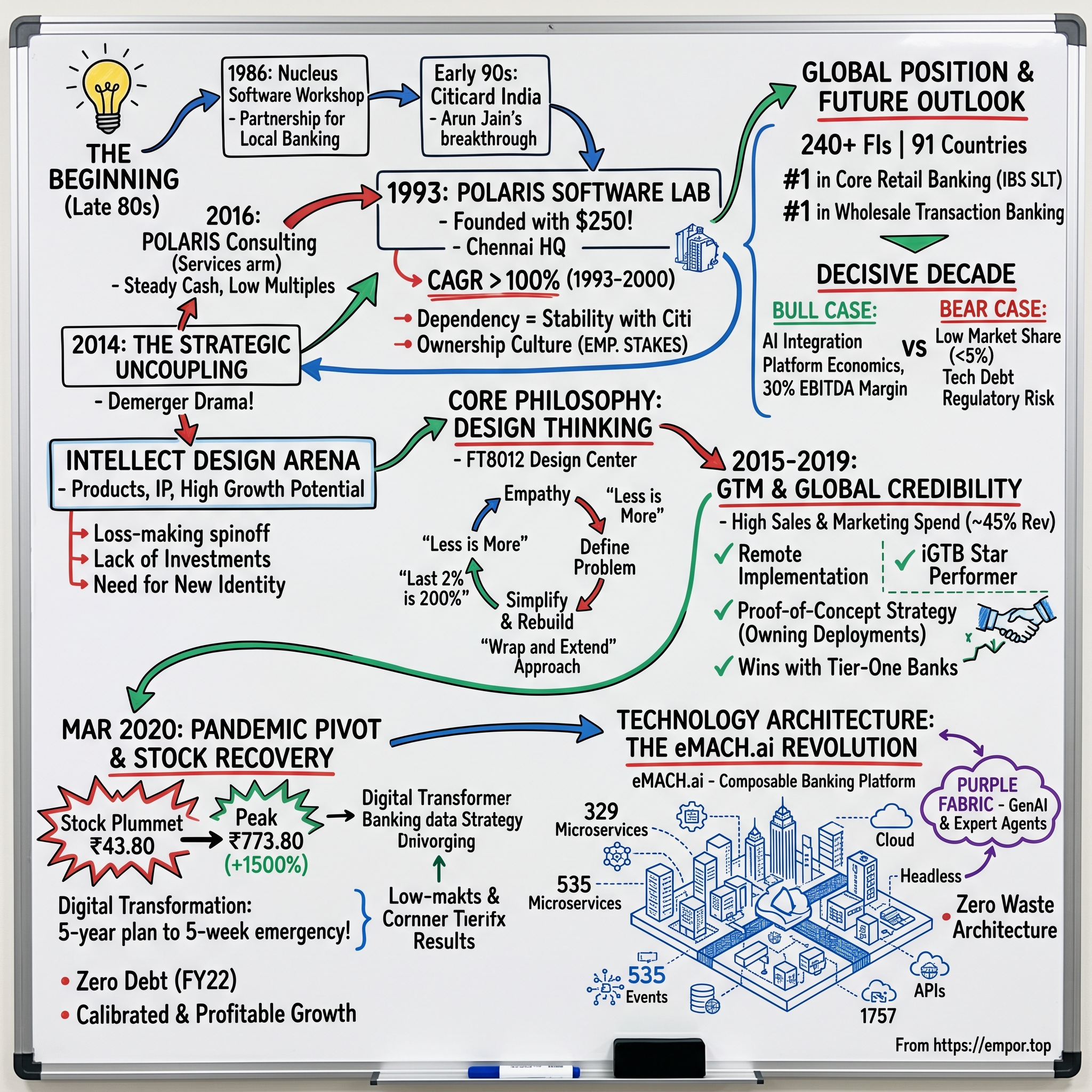

Picture this: It's March 2020, and the world is shutting down. Stock markets are in freefall. In a nondescript office building in Chennai, Arun Jain watches his company's stock price plummet to ₹43.80—an all-time low. Six years after spinning off from Polaris, his bet on building a global fintech product company from India seems to be unraveling. Fast forward twelve months: that same stock touches ₹773.80, delivering 1500%+ returns to those brave enough to buy at the bottom. This isn't just another pandemic recovery story—it's the culmination of a three-decade journey to build something that conventional wisdom said was impossible: a world-class enterprise software company from India that could compete with Silicon Valley and European giants.

Today, Intellect Design Arena commands a market capitalization of ₹12,852 crores, serving over 240 financial institutions across 91 countries. From the largest banks in America to emerging fintech challengers in Africa, Intellect's software processes millions of transactions daily. The company ranks #1 globally in six categories according to IBS Intelligence—not bad for a company that was bleeding money just a decade ago.

But here's what makes this story truly compelling: while India's IT services giants like TCS, Infosys, and Wipro built empires on labor arbitrage and cost advantages, Intellect took the harder path. They chose to build intellectual property, to create products that could stand toe-to-toe with Temenos, FIS, and Finastra. They chose design thinking over body shopping, microservices over monoliths, and composable architecture when everyone else was still selling ERP-style solutions.

The core question we're exploring today isn't just how a Chennai-based company became a global fintech leader—it's how they fundamentally reimagined what financial software could be in an era of digital transformation. This is a story about patience, about burning through hundreds of crores to build something that wouldn't pay off for years, about convincing tier-one banks to trust their core operations to a company most had never heard of.

What you're about to hear is part corporate archaeology, part technology deep-dive, and part meditation on what it takes to build a global product company from an emerging market. We'll trace the journey from Arun Jain's early days at Nucleus Software in the 1980s, through the Polaris years when they built the foundation, to the dramatic 2014 demerger that birthed Intellect, and finally to today where they're betting everything on AI and composable banking.

Along the way, we'll unpack the design thinking philosophy that became their North Star, decode their eMACH.ai platform that comprises 329 microservices and 1757 APIs, and examine why, despite all their success, they still struggle to capture more than 5% of the global market. We'll also explore the financial engineering that took them from losses to profitability, the go-to-market strategy that cracked advanced markets, and the technology bets that could either cement their position or render them obsolete.

This isn't just Intellect's story—it's a playbook for how emerging market companies can compete globally, how to manage the painful transition from services to products, and what it really means to be design-led in enterprise software. So buckle up for a journey that spans four decades, three continents, and one audacious vision: to build the world's most advanced financial technology platform from the streets of Chennai.

II. The Arun Jain Journey: From Nucleus to Polaris

In 1986, three young engineers sat in a cramped office in Delhi's Thyagraj Nagar, hunched over primitive computers, writing code for local banks. Arun Jain, along with Yogesh Andlay and Vishnu Dusad, had just founded Nucleus Software Workshop—a partnership that would eventually reshape India's financial technology landscape. They weren't thinking about global domination then. They were just trying to survive, taking whatever software projects came their way. But Jain, the son of a government servant who had watched his father struggle to educate ten children on a meager salary, carried something more than survival instinct. He carried a vision that India could build world-class software products, not just provide cheap labor to Western companies.

The Nucleus years were formative but limiting. While Andlay and Dusad would continue building Nucleus into a respectable lending software company that would eventually list on the stock exchanges, Jain grew restless. After graduating in electrical engineering from Delhi College of Engineering in 1983, Jain had initially started a company called International Information Systems that undertook software projects. But by the early 1990s, the partners had different visions. The co-founders had grown apart and the company needed a new direction. Jain restructured the company into three separate entities with each partner getting to drive his own business at his own pace.

The real transformation began with a single client and an audacious dream. In 1990, Jain came to Chennai to help set up India's first credit card system for Citibank, which had its back office in the Tamil Nadu capital. This wasn't just another project—it was Jain's introduction to the complexity and scale of global banking operations. He saw an opportunity that others missed: instead of just servicing Citibank's needs, why not build products that could serve banks globally?

In 1993, he founded Polaris Software Lab with an initial capital of $250 (Rs 10,000), which recorded a CAGR of over 100% during 1993-2000. Think about that for a moment—starting a company with the equivalent of a few hundred dollars in an era when software companies needed millions in venture funding. He set up shop with 120 people in an office near the historic Thousand Lights Mosque, just off Mount Road in Chennai—a location that would remain the company's global headquarters through all its transformations.

The Citibank relationship became Polaris's foundation and its first major test. Jain's firm clinched a major deal beating the likes of TCS, Infosys and Mastek. "It was a major breakthrough for me," recalls Jain. But Jain understood something crucial about enterprise relationships—dependency creates stability. For the next five years, he focused on creating a relationship where each party was dependent on the other. The gambit paid off with Citi becoming one of the company's longest-standing clients.

The late 1990s marked Polaris's adolescence—rapid growth, public listing, and geographic expansion. The company went public in 1997, with employees given stakes in the company. This wasn't just about wealth creation; it was about building an ownership culture. As one employee noted: "People work on their own, instead of being asked to work. Jain likes to empower people to take decisions. He won't micro-manage, but when things go wrong, he will step in".

By 2000, Polaris had crossed Rs 100 crore in revenue, but Jain was already thinking bigger. He wanted to look beyond Citibank, set up an IT technology park with global infrastructure, and reduce dependence on one company. Citibank's share dropped to 30% even as Polaris's turnover shot up to over Rs 200 crore. The company was learning to walk on its own, building relationships with banks across the globe.

The 2000s brought scale and complexity. Jain had to take several strategic decisions to speed up growth, including the merger of Polaris with OrbiTech. In 2002, Polaris acquired Citigroup's software business in India, the largest transaction of that year. This wasn't just an acquisition—it was a statement. The vendor had become sophisticated enough to absorb its client's operations.

By the 2010s, Polaris had become a formidable force—12,000+ employees across 25+ countries, serving major global banks. But success brought its own challenges. The company had become a hybrid—part services, part products—trying to be everything to everyone. The services business generated steady cash flows but commanded low multiples. The products business held the promise of exponential growth but required patient capital and different capabilities.

This tension would eventually lead to the most important decision of Jain's career. In March 2016, Virtusa Corporation acquired a majority stake in Polaris Consulting & Services for Rs 1,173 crore—what Jain called the "biggest decision of his life". But this wasn't an exit—it was a strategic uncoupling. Jain had already carved out the products business into a separate entity two years earlier: Intellect Design Arena.

The philosophical underpinnings of Jain's journey reveal themselves in his other ventures. The Ullas Trust, started in 1997, has reached out to over 260,000 children from economically challenged sections. Jain put his personal money into the Polestar awards, arguably the best-known award for IT and business journalism in India—an instance of putting his money where others put their mouth.

Looking back, the journey from Nucleus to Polaris wasn't just about building a company—it was about proving a thesis. That an Indian company could move beyond labor arbitrage, beyond services, beyond being a vendor. The path began with just $250 and a dream, guided by two beliefs: ordinary people coming together to achieve extraordinary results, and the power of organizational subconscious in realizing vision.

As we transition to the birth of Intellect, it's worth noting that Jain's Polaris journey had taught him crucial lessons: the importance of patient capital, the power of design thinking over linear problem-solving, and most importantly, that to build a global product company from India, you sometimes have to destroy what you've built and start anew. The stage was set for the most audacious bet of his career.

III. The Birth of Intellect: Demerger Drama & Design Thinking

The boardroom at Polaris headquarters in Chennai was tense on a humid March morning in 2014. Arun Jain stood before his board with a radical proposal: tear the company in half. After two decades of building Polaris into a 12,000-person powerhouse, he wanted to separate the products business—the very soul of his original vision—from the services arm that generated most of the cash. Boston Consulting Group's advisors had laid out the numbers: the company's product business was investing only 15% in sales and marketing while competition spent 30-50%. Under the services umbrella, the products division would never get the investment it needed to compete globally.

Polaris being an IT services company focused on providing services to IP-led BFSI players was resulting in a conflict as Intellect itself was an IP-led company competing in BFSI space. At the time of demerger, Intellect had revenues of ~550 crores and was making losses. This wasn't just a corporate restructuring—it was an existential bet. Would investors understand? Would customers trust a loss-making spinoff? Would employees stay?

Polaris announced the demerger of its Products (Intellect) business into an independent entity 'Intellect Design Arena Ltd', with a focus on Global Universal Banking, Risk and Treasury Management, Global Transaction Banking and Insurance businesses. The new entity was expected to double its business in the next three years from the current around $100 million. The mechanics were elegant: every shareholder of Polaris Financial Technology would receive one share of Intellect.

But beneath the financial engineering lay a deeper philosophical shift. Jain had become obsessed with design thinking—not as a buzzword, but as a fundamental reimagining of how enterprise software should be built. According to design thinking, asking an appropriate question is more important than getting to a solution. The foundation of design thinking lies in empathy with the customers. This wasn't how Indian IT companies operated. They solved problems handed to them by clients. Jain wanted to discover problems clients didn't even know they had.

The design thinking philosophy had crystallized during Jain's interactions with global banks. He noticed something peculiar: banks would spend millions implementing software that their employees hated using. The software worked—technically—but it felt like torture. Complex workflows, endless screens, cryptic error messages. Banking software had been designed by engineers for engineers, not for the humans who actually used it. The laws of design thinking became Intellect's mantra: 'Less is More'—remove redundancy and focus on what matters most for users, reduce complexity and keep it simple. 'Last 2% is 200%'—empathize with the user, be alert to understand unstated requirements to provide differential service(s).

This philosophy demanded a different organizational structure. Services companies optimize for utilization—keeping engineers billable. Product companies need slack for innovation, time for experimentation, tolerance for failure. The two models were fundamentally incompatible. In one of the initial earnings calls post-demerger, Arun Jain stated that under Polaris, Intellect lacked dedicated thrust and investments in Sales & Marketing. "Our competition invests between 30-50% on Sales & Marketing. We invest 15% in Sales & Marketing. To be globally competitive, we propose to increase these investments in a focused and planned manner".

The demerger wasn't just about freeing up investment capacity—it was about creating a new identity. The new company would have around 3,000 employees, inheriting the product IP but needing to build everything else from scratch: sales teams, marketing muscle, customer relationships, credibility. The services business kept the Polaris brand and the steady cash flows. Intellect got the dreams and the debts.

December 18, 2014, marked Intellect's debut on the stock exchanges. The stock opened at Rs 69.25 and hit a low of Rs 69.25 in early morning trade, before locking in the upper circuit of 5% at Rs 72.70. The market was cautiously optimistic, but the real test lay ahead.

The funding strategy was carefully orchestrated. Intellect received ~300 crores cash as part of the demerger from Polaris. The company also did a rights issue in July 2017 to raise ~198 crores and raised another Rs 100 crores from promoters in September 2018. This war chest would fund the transformation from a captive product division to a global competitor.

But money alone wouldn't solve Intellect's challenges. The company needed to rebuild its entire go-to-market apparatus. Under Polaris, product sales had been an afterthought—something the services team mentioned if a client asked. Now, Intellect needed to convince CIOs to buy software from a company they'd never heard of, competing against Temenos, FIS, and Finastra who had decades of credibility.

The organizational culture also needed rewiring. Jain instituted what he called "First Principles Thinking"—breaking down banking operations to their atomic components and rebuilding from scratch. Every assumption was questioned: Why does a loan application need 47 fields? Why do treasury operations require 15 approvals? Why can't different banking products share the same data models?

This wasn't incremental improvement—it was radical simplification. Where competitors added features to justify upgrades, Intellect removed complexity to improve usability. Where others built monolithic platforms that took years to implement, Intellect created modular components that could go live in weeks.

The design center, FT8012, became the physical manifestation of this philosophy. Located in Chennai, it wasn't just an office—it was a laboratory where bankers, designers, and engineers collaborated to reimagine financial services. Clients weren't just buyers; they were co-creators. Problems weren't just solved; they were reframed.

FY15-FY18 became Intellect's "Go-To-Market stage" with heavy investments in Sales & Marketing. The company was burning cash to build credibility, hiring expensive sales talent from competitors, sponsoring conferences, building proof-of-concepts for skeptical prospects. Every deal was a validation, every loss a learning.

The philosophy extended beyond products to people. Jain's approach to talent was unconventional: hire for curiosity, not credentials. Train for empathy, not just expertise. Reward questions, not just answers. The company's tagline became "Design for Digital"—not just using design thinking for products, but designing the entire organization for a digital future.

By 2018, the transformation was showing results. FY19 saw Intellect reaping benefits with revenues growing nearly 40% to Rs 1,458 crores and turning small profits of ~25 crores. This growth was on the back of iGTB segment gaining market acceptance, with revenues doubling from Rs 343 crores in FY17 to Rs 678 crores in FY19.

The demerger had been painful—like performing surgery on yourself without anesthesia. But it had achieved something remarkable: freeing Intellect from the constraints of quarterly services targets to pursue a longer-term product vision. As Jain would later reflect, Intellect Design Arena Limited was his third venture, in pursuit of his vision to make India the IP Capital towards the next growth wave for the IT Industry. His passion to create a technology product powerhouse from India made Intellect a reality.

The stage was now set for the next phase: taking this design-thinking-led, India-born fintech platform to the world's most sophisticated financial markets. The question was no longer whether Intellect could survive the demerger, but whether it could fulfill its audacious promise—to become the world's most advanced financial technology platform.

IV. The Go-To-Market Years: Building Global Credibility (2015-2019)

London, 2016. Manish Maakan, CEO of Intellect's Global Transaction Banking division, sits across from the Chief Technology Officer of a tier-one European bank. The CTO leans back, skeptical. "You're telling me an Indian company I've never heard of, spun off from another company I've never heard of, can replace our core transaction banking platform that processes €50 billion daily?" Maakan doesn't flinch. "Give us 90 days for a proof of concept. If we fail, we'll cover all your costs." This wasn't just confidence—it was the culmination of Intellect's radical go-to-market strategy.

FY15-FY18 was Go-To-Market stage for Intellect wherein there were heavy investments in Sales & Marketing. Intellect invested heavily for next 3-4 years in Sales & Marketing, which was as high as ~45% of revenues. Even investments in R&D were high at 15-20% of revenues. These heavy investments resulted in Intellect continuing to turn losses from FY15 to FY18.

The numbers tell a story of deliberate, painful investment. They reported net revenue of Rs 636.28 crore in FY15. In less than five years, this revenue became more than its double as revenue worth Rs 1515.24 crore was recorded in FY19. But revenue growth alone doesn't capture the transformation. Intellect was fundamentally rewiring how enterprise software was sold in the financial services industry.

The traditional enterprise sales playbook—wine and dine executives, promise the moon, deploy armies of consultants—wouldn't work for Intellect. They lacked the brand recognition, the reference customers, the decades of trust. So they flipped the model. Instead of selling promises, they would deliver results upfront. Instead of PowerPoints, they would show working software. Instead of hiding behind implementation partners, they would own every deployment.

The product portfolio evolved across four distinct business lines, each targeting a specific pain point in financial services. iGTB (Global Transaction Banking) focused on corporate banking and cash management. iGCB (Global Consumer Banking) tackled retail banking operations. iRTM (Risk, Treasury and Markets) addressed trading and risk management. And Intellect SEEC handled the insurance vertical—a market most banking software vendors ignored.

Each division operated like a startup within Intellect, with dedicated CEOs who had P&L responsibility and the autonomy to make rapid decisions. Jaideep Billa and Venkatesh Srinivasan, Joint CEOs of Global Universal Banking and Risk & Treasury, operated out of Singapore and Mumbai respectively. Pranav Pasricha led the insurance division. This wasn't just organizational design—it was a recognition that different markets required different approaches.

The sales strategy was equally unconventional. Rather than hiring expensive enterprise sales veterans who relied on relationships, Intellect recruited domain experts—former bankers who understood the pain points viscerally. These weren't salespeople selling software; they were practitioners selling solutions to problems they had personally experienced.

The London office, established under Manish Maakan's leadership, became the spearhead for European expansion. But this wasn't a traditional sales outpost. It was a design and innovation center where European banks could co-create solutions. The message was subtle but powerful: Intellect wasn't an Indian vendor selling to European clients; it was a global company building with local partners.

These investments were made from ~300 crores Cash that Intellect received as a part of demerger from Polaris. Intellect also did a rights issue in July'17 to raise ~198 crores. And raise another Rs100 crores from Promoters in Sep'18. This war chest funded not just sales teams but something more ambitious: the ability to say yes to proof-of-concepts that competitors would reject as too risky or expensive.

The proof-of-concept strategy was revolutionary in enterprise software. While competitors demanded million-dollar commitments before showing their software, Intellect would deploy functional systems in weeks, often at their own cost. If the bank liked what they saw, they would buy. If not, Intellect would learn and move on. This approach was expensive—many POCs failed—but the ones that succeeded created unshakeable customer relationships.

The share of License Linked Revenues (License + AMC + SaaS) for Intellect has grown from 32% in FY15 to 54% in FY21. Within this, SaaS+AMC has grown from 18% in FY15 to 32% in FY21. These are good indications as License Linked Revenues, specifically SaaS+AMC provides for higher gross margins and are more secular in nature.

The shift to recurring revenue models wasn't just financial engineering—it represented a fundamental change in how banks thought about software procurement. Traditional licenses required massive upfront investments and multi-year commitments. Intellect's SaaS model allowed banks to start small, prove value, then scale. This lowered the barrier to entry, especially for mid-sized banks that couldn't afford Temenos or FIS's hefty price tags.

The product development philosophy during this period was equally distinctive. While competitors built for the Fortune 500, Intellect designed for the next 5,000. They recognized that tier-two and tier-three banks had the same operational complexities as their larger peers but lacked the resources for lengthy implementations. Intellect's modular architecture allowed these banks to implement specific functions—say, trade finance or liquidity management—without replacing their entire core banking system.

By FY17, the strategy was showing early signs of success. Q2 FY18 revenues grew 21% year-over-year, with license and AMC crossing the 100 crore mark during the quarter. But these numbers understated the qualitative shift. Intellect was winning deals not on price—they were often more expensive than Indian competitors—but on speed of implementation and depth of domain expertise.

The breakthrough came with large digital transformation deals. Unlike traditional "rip and replace" projects that took years, Intellect pioneered the "wrap and extend" approach. Their software would wrap around existing systems, extending functionality without disruption. A European bank could add sophisticated cash pooling capabilities without touching their core banking system. An Asian bank could launch digital lending without replacing their loan origination platform.

FY19 saw Intellect reaping benefits of its investments with revenues growing nearly 40% to Rs1458 crores and Intellect turning small profits (before tax) of ~25 crores (including Capitalized R&D) even though overall investments in R&D continued to expand. The iGTB segment was the star performer, with revenues doubling from Rs 343 crores in FY17 to Rs 678 crores in FY19.

The customer wins during this period read like a who's who of global banking. But more importantly, they represented a validation of Intellect's approach. These weren't peripheral systems or departmental solutions. Banks were trusting Intellect with mission-critical operations—the systems that, if they failed, could bring down the entire institution.

The intellectual property vault grew steadily during these years. By FY19, Intellect had built comprehensive solutions across 30+ products. But unlike competitors who grew through acquisition—buying disparate products and struggling to integrate them—Intellect built everything on a common architecture. This meant a bank could start with trade finance, add supply chain finance, then corporate lending, with all systems sharing the same data models and user experience.

The company's EBITDA (Earnings before interest, tax, depreciation and amortization) surged by more than 10X times from FY17 to FY19. This wasn't just operational leverage—it was validation that the model worked. The heavy investments in sales and marketing were paying off, not just in new customers but in expansion within existing accounts.

The geographic expansion strategy was equally deliberate. Rather than spreading thin across every market, Intellect focused on specific corridors: London for European banks, Singapore for Asian operations, and selective presence in the Americas. Each office wasn't just a sales outpost but a center of excellence that understood local regulations, market practices, and cultural nuances.

Intellect's SaaS revenues have grown from nothing to nearly 12% in FY21 and at current run-rate, it could be as high as 20% in FY22. This increase is another indication of new product lines of iGCB and SEEC gaining traction, as in SEEC 100% deals are SaaS based and iGCB also has most deals on SaaS model.

The insurance vertical (SEEC) emerged as an unexpected success story. While most banking software vendors ignored insurance—seeing it as a different market—Intellect recognized the convergence opportunity. Banks were increasingly selling insurance products. Insurers were offering banking services. The boundaries were blurring, and Intellect's unified platform could serve both.

By the end of FY19, Intellect had achieved something remarkable: credibility without legacy. They weren't burdened by decades-old code that needed constant patching. They weren't defending installed bases against disruption. They were the disruption—but packaged in enterprise-grade reliability that conservative financial institutions could trust.

The sales culture that emerged during these years was distinctive. Win rates mattered less than learning rates. Every lost deal triggered a post-mortem: What did we miss? What couldn't our platform do? What would it take to win next time? This feedback loop drove product development, creating a virtuous cycle where customer rejections became product improvements.

As the go-to-market phase concluded, Intellect had transformed from an unknown spinoff to a credible alternative to established players. The company had over 200 financial institutions as customers, operations in 91 countries, and most importantly, referenceable implementations at tier-one banks. The foundation was set for the next phase of growth—one that would be unexpectedly accelerated by a global pandemic that nobody saw coming.

V. Pandemic Pivot & Platform Evolution (2020-2023)

The Zoom call was scheduled for 8 PM Chennai time, March 24, 2020. India had just announced its first lockdown. Arun Jain stared at his screen, watching his leadership team join from their hastily assembled home offices. The company's stock had crashed to Rs 43.80—an all-time low. Banks were freezing IT budgets. Implementation projects were stalled. Travel—the lifeblood of enterprise software sales—was banned indefinitely. "This," Jain told his team, "is either the end of everything we've built, or the beginning of something extraordinary."

For the first time in these many years, their revenue failed to get past the previous years' mark. In FY20, Intellect declared total revenue of Rs 1,385.10 crore. This can be attributed to the rising case of Covid-19 globally. Even if they failed to beat their previous mark, the fall in the revenue wasn't steep. This shows the strength of fintech companies.

What happened next defied all logic. In March 2020, just like many other stocks, Intellect Design touched its all-time low of Rs 43.80. On 1st April 2021, it touched its all-time high of Rs 773.80. That means in just over a year time frame, it delivered whopping returns of more than 1500%. But this wasn't just a stock market phenomenon—it reflected a fundamental transformation in how financial services viewed technology.

The pandemic didn't create new problems for banks; it exposed existing ones with brutal clarity. Legacy systems that required physical presence. Paper-based processes that couldn't function remotely. Monolithic architectures that took months to modify. Suddenly, digital transformation went from a five-year plan to a five-week emergency. And Intellect was perfectly positioned to capitalize.

The Q2 FY21 numbers tell the story of this transformation. Healthy growth of 131% in License revenues and AMC revenues up by 19% YoY. License linked revenue (License + SaaS/Subscription + AMC) was at 56% of total revenues as against 41% of total revenues in Q2 FY20. Sustained turnaround in profitability with PAT at INR 590 Mn as against a loss of INR 170 Mn in Q2 FY20.

But the real story wasn't in the numbers—it was in how those numbers were achieved. While competitors struggled to deploy software remotely, Intellect's cloud-native architecture and modular design allowed for remote implementation. Banks could go live with new capabilities in weeks, not years. A European bank implemented trade finance capabilities entirely remotely. An Asian institution launched digital lending without a single on-site visit.

Arun Jain commented during this period: "I take great satisfaction in announcing another quarter of steady revenue growth along with sustained expansion in profitability as part of our monetisation strategy announced last quarter. Our brand recognition & superior and deep financial technologies are helping us to drive more consistent deal flows in advanced markets."

The platform strategy that Intellect had been building for years suddenly became essential. As Jain noted in Q2 FY22: "Intellect's technologies have driven calibrated and profitable growth over the last 8 quarters. As committed during the Intellect Technology day in March 2021, we launched two Platforms on Cloud this quarter – iKredit360 and iGTB Cloud – CashPower '22. Both platforms have helped Intellect win 6 platform deals in this quarter. This is the beginning of Intellect's transition from a Product company to a Fintech Platform."

The pandemic accelerated adoption of SaaS models by years. Traditional banks that had insisted on on-premise installations suddenly embraced cloud deployment. Annualised Recurring Revenues (ARR) touched INR 6774 mn on an annual basis by Q2 FY22. SaaS revenue registered 156% growth. The shift wasn't just technological—it was psychological. Banks realized that cloud wasn't just cheaper; it was more resilient.

FY22 marked a financial milestone: Zero debt achievement with cash of INR 2574 Mn. EBITDA margins expanded dramatically—reaching 28.5% of revenue in Q2 FY22. The company's cost optimization program, focusing on rationalization of S&G expenses and tighter R&D spending while increasing license-linked revenue, enhanced margin profile from 6-9% in FY19/FY20 to 24% in FY21 and 25% in FY22.

The operational metrics revealed the underlying strength. Despite visa hurdles and travel restrictions, Intellect went live in 26 financial institutions with 10 new digital transformations across the world during Q2 FY21 alone. The Net Days of Sales Outstanding improved, collections strengthened, and working capital efficiency reached new heights.

Customer wins during the pandemic were particularly strategic. One of the largest multi-faceted global financial services from the US chose iGTB's Liquidity Management Solution. With this deal win, iGTB now had 11 clients in the US out of Intellect's portfolio of 25 in North America, reinforcing its position as partner of choice for large financial institutions in this region.

The recognition from global analysts validated the transformation. IDC Financial Insights announced Intellect Wealth as the winner at the 2020 IDC FinTech Rankings Real Results Award for Digital Wealth Transformation. iGTB was rated as a "Strong Performer" in The Forrester Wave™ in Digital Banking Processing Platforms. Intellect joined BIAN to help revolutionize the API-driven contextual banking technology framework.

By FY23, the momentum was unstoppable. Intellect crossed INR 2000 crore revenue mark, registering 21% growth. Q4 FY23 revenue registered 24% YoY growth. The company wasn't just recovering from the pandemic—it was thriving in the new normal. License-linked revenue (License Platform AMC) reached Rs 1,132 crore, with Annual Recurring Revenue growing 35% YoY.

The geographic mix shifted dramatically during this period. Advanced markets, which had been skeptical pre-pandemic, became the growth drivers. Q2FY25 saw 8 out of 12 deal wins from Americas and Europe, validating the advanced market strategy. As Arun Jain noted: "The fact that 8 out of 12 deal wins in the quarter are from Americas and Europe gives us the confidence that we have the desired market endorsements for our platform to address the needs of western financial institutions."

The platform revenue trajectory was particularly impressive. Platform revenue of LTM Q2 FY23 was Rs 448 crore as against Rs 276 crore in LTM Q2 FY22—growing 62% YoY. This wasn't just growth; it was a fundamental business model transformation. Intellect was no longer selling software; it was providing banking-as-a-platform.

The investment strategy during this period was counter-intuitive but brilliant. While competitors cut R&D spending, Intellect doubled down. Investment of INR 1000 Mn in alternative investment funds, continued product development capitalization of INR 290 Mn quarterly, and sustained investment in new platforms like Purple Fabric. The bet was that the post-pandemic world would need fundamentally different financial technology.

Management's confidence was evident in their guidance. Despite market uncertainty driven by high inflation rates and currency volatility, they projected 20% annual growth visibility for FY23. More ambitiously, they set a long-term EBITDA margin target of 30%—a level that would put them among the most profitable enterprise software companies globally.

The cultural transformation within Intellect was equally profound. Remote work, initially seen as a temporary necessity, became a strategic advantage. The company could now hire talent globally, serve customers 24/7, and iterate on products faster than ever. The traditional enterprise software model—armies of consultants descending on client sites—seemed antiquated.

By the end of FY24, crossing INR 2500 crore revenue mark, Intellect had emerged from the pandemic fundamentally transformed. The company that had struggled to convince banks to try its software pre-pandemic was now turning away business to maintain quality. The stock price recovery—from Rs 43.80 to Rs 773.80—was just the market catching up to a reality that Jain had seen early: the pandemic wasn't a disruption to be endured but an acceleration of inevitable change.

The pandemic years proved that Intellect's bet on cloud-native, API-first, microservices-based architecture wasn't just technically superior—it was existentially necessary. Banks that had resisted digital transformation for decades completed it in months. And Intellect, the company that many had written off in March 2020, emerged as one of the pandemic's biggest winners. The next challenge would be even more ambitious: leveraging artificial intelligence to reimagine banking itself.

VI. The eMACH.ai Revolution & Technology Architecture

The conference room at FinTech 8012, Intellect's design center in Chennai, March 2023. Arun Jain stands before a massive digital wall displaying what looks like the blueprint of a city—except it's not buildings and roads, but microservices and APIs. "Ladies and gentlemen," he announces to the assembled bankers and technologists, "what you're looking at is the most comprehensive deconstruction of banking ever attempted. 329 microservices, 535 events, 1757 APIs. We call it eMACH.ai, and it's going to change everything."

This wasn't hyperbole. With an impressive array of 329 microservices, 535 events and over 1757 APIs, this First Principles Thinking-based Platform enables financial institutions to build future-ready solutions. What Intellect had done was radical: they had broken down every single banking operation—from opening an account to complex derivatives trading—into atomic, reusable components.

Think of traditional banking software as a monolithic cathedral—impressive, but impossible to modify without risking the entire structure. eMACH.ai was more like LEGO blocks—infinitely reconfigurable, each piece self-contained yet designed to work with every other piece. Combining these 4 principles creates a magical name for our Technology – eMACH – Events, Microservices, APIs, Cloud and Headless.

The philosophical underpinning was First Principles Thinking—a concept borrowed from physics where you break down complex problems to their fundamental truths and rebuild from there. Applying first principles thinking, we have elementalised the banking space to a finite number of Events, Microservices and Application Programming Interfaces (APIs) which significantly simplifies any adoption / transformation initiative.

But the real magic wasn't in the decomposition—it was in the recomposition. Enter iTurmeric, the codeless visual composer that allowed business users, not just developers, to create banking solutions. iTurmeric combines the power of integration, process automation, and codeless development in a single platform, enabling banks to build, connect, and deploy solutions at unprecedented speed. A bank's product manager could literally drag and drop microservices to create a new lending product, test it in a sandbox, and deploy it to production—all without writing a single line of code.

The technical architecture was breathtaking in its ambition. Every microservice was designed to be stateless, scalable, and secure. Each API followed strict design principles—RESTful, versioned, with comprehensive documentation. The event-driven architecture meant that changes in one part of the system automatically triggered appropriate responses elsewhere. A loan approval could simultaneously update risk models, notify treasury, adjust capital allocation, and trigger regulatory reporting—all through loosely coupled events.

With 285 pre-built microservices available on the cloud, and access to 1,214 APIs and 200 events, eMACH.ai enables financial institutions to design the future of banks and FIs. The numbers kept growing as Intellect added more capabilities, more integrations, more intelligence.

The platform's composability was its killer feature. eMACH.ai doesn't just offer modularity. It offers co-existence, integrating seamlessly with existing systems, allowing financial institutions to modernise without disruption. Banks didn't need to replace their entire technology stack—they could wrap eMACH.ai around legacy systems, gradually modernizing component by component.

But Jain knew that APIs and microservices alone wouldn't transform banking. The industry needed intelligence—not just automation, but genuine cognitive capabilities. Enter Purple Fabric, what Intellect called the world's first Open Business Impact AI Platform.

Intellect Purple Fabric leverages cutting-edge Generative AI to enable Enterprise-Connected Intelligence. The platform integrates five rich knowledge banks—Structured Data, Document Knowledge, Operations Knowledge, Regulatory Knowledge, and Market Knowledge—with AI Expert Agents.

Purple Fabric wasn't just another AI tool—it was an attempt to encode banking expertise into software. Purple Fabric empowers subject matter experts to swiftly create and implement AI-driven solutions through a low-code, self-service approach, significantly reducing costs and time investment while fostering innovation. By integrating diverse knowledge banks and deploying AI expert agents, the platform unleashes Enterprise Connected Intelligence.

The London Market breakthrough illustrated Purple Fabric's potential. IntellectAI announced a breakthrough agreement with London's premier Market Insurance and Reinsurance Brokerage firm. Under this multi-year engagement, the brokerage firm will deploy Intellect's underwriting ecosystem which consists of Magic Submission and Xponent solutions, built on IntellectAI's proprietary Purple Fabric platform. This INR 200 crore deal validated that even the most sophisticated financial institutions saw value in Intellect's AI approach.

The Zero Waste Architecture philosophy drove every design decision. Traditional enterprise software was bloated—features added over decades, code that nobody understood, integrations held together with digital duct tape. eMACH.ai was ruthlessly efficient. Every microservice had a single responsibility. Every API had a clear contract. Every event had a defined purpose.

We have secured 29 mandates from global banks who have chosen to use eMACH.ai services. We have conducted over 150 eMACH.ai workshops to assist these banks in designing their future strategies around customer opportunities rather than just focusing on technology maximisation and optimisation.

The platform's evolution reflected changing market needs. When Intellect launched eMACH.ai in March 2023, it had 285 microservices. By 2024, this had grown to 329. By early 2025, internal documents suggested over 386 microservices with 2015 APIs. This wasn't feature creep—each addition addressed specific customer requirements identified through their design thinking workshops.

The geographic rollout was strategic. With its extensive offering of 329 microservices, 535 events, and over 1757 APIs, it serves as the most comprehensive Open Finance Platform, enabling the creation of customer-centric solutions instead of traditional product-focused ones. The Canada-ready eMACH.ai Cloud launch in May 2024 demonstrated how the platform could be localized for specific regulatory and market requirements while maintaining its core architecture.

The technical differentiation went beyond architecture. While competitors were still debating cloud strategies, Intellect had built cloud-agnostic capabilities. Banks could deploy on AWS, Azure, Google Cloud, or even on-premise—the platform adapted. While others struggled with API versioning, Intellect had built backward compatibility into its DNA. While rivals required armies of consultants for customization, Intellect's visual tools empowered banks' own teams.

This latest win highlights IntellectAI's strategic investment in creating Purple Fabric platform which brings the power of 217 technologies to deliver cutting-edge Artificial Intelligence solutions. This AI platform gives the opportunity to quickly design and realise the potential of connected intelligence for an organisation to transform its operations.

The business model innovation was equally important. Instead of charging for individual products, Intellect offered platform subscriptions. Banks paid for access to the entire ecosystem—all microservices, all APIs, all updates. This aligned incentives: Intellect succeeded when banks used more of the platform, creating a virtuous cycle of adoption and innovation.

The intellectual property strategy was sophisticated. While the platform was "open" in terms of standards and integrations, the underlying implementations were proprietary. Intellect had essentially created a new operating system for banking—open enough to attract developers and partners, closed enough to maintain competitive advantage.

By 2024, the platform strategy was showing results. Banks weren't just buying Intellect's products; they were building on Intellect's platform. Third-party developers were creating solutions using eMACH.ai's APIs. System integrators were training teams on iTurmeric. Universities were teaching courses on composable banking architecture.

The AI evolution through Purple Fabric represented the next frontier. At IntellectAI, we are not only pushing the boundaries of implementing AI in financial services with our Purple Fabric platform, but we are elevating the intelligence from fragmented to connected. Our platform integrates knowledge bases with domain expertise through targeted use cases, capturing the full potential of AI to enhance business efficiency and ensure seamless last-mile execution.

The investment required was staggering—over 100 crores for Purple Fabric marketing and distribution alone. But Jain saw this as table stakes for the next phase of growth. The company that had started with $250 was now betting hundreds of crores on becoming the intelligence layer for global finance.

As we look at eMACH.ai's architecture today, we see not just a technology platform but a philosophical statement about how banking software should be built. Modular, not monolithic. Composable, not rigid. Intelligent, not just automated. Open, not proprietary. This wasn't incremental improvement—it was a fundamental reimagining of financial technology. The question now wasn't whether banks would adopt this approach, but how quickly Intellect could capture market share before competitors caught up.

VII. Global Expansion & Market Position

The London Shard, 2024. Fifty of the world's most influential banking technology leaders gather for an exclusive dinner. Among them, Arun Jain receives the news that would validate decades of work: Intellect has been ranked #1 in three of its banking offerings by IBS Intelligence, continuing to lead the fintech industry with top rankings in Retail Core Banking for the sixth consecutive year, Transaction Banking for the fifth consecutive year, and Lending for the third consecutive year. The Chennai company that started with $250 was now consistently beating Silicon Valley giants and European incumbents at their own game.

IBSi's Annual Sales League Table is a widely regarded industry benchmark that measures the performance of global banking technology solutions. The SLT has been running for over 20 years and is recognised as a barometer for financial technology supplier sales performance across the banking industry. To understand Intellect's achievement, you need to understand what the IBS rankings mean: they're based on actual new customer wins, not revenue or market cap. It's the truest measure of competitive success in enterprise software.

The geographic footprint tells a remarkable story. Intellect also secured #2 positions in 8 other financial technology categories and retained #3 ranking in "global leadership for geographic spread" for the fourth year in a row. From a Chennai headquarters, Intellect had built a presence spanning 91 countries, serving over 240 financial institutions. But this wasn't just about planting flags—it was about understanding and serving radically different markets.

The Americas breakthrough was particularly significant. With this deal win, iGTB now has 11 clients in the US out of Intellect's portfolio of 25 in North America, reinforcing its position as partner of choice for large financial institutions in this region. Breaking into the US market—where banks traditionally bought from Oracle, FIS, or Fiserv—required not just superior technology but cultural translation. Intellect couldn't sell as an "Indian vendor"; they had to position as a global innovator that happened to be headquartered in India.

The partnership ecosystem became crucial for global expansion. Rather than trying to build direct sales presence everywhere, Intellect cultivated relationships with global system integrators, regional consultancies, and local implementation partners. Each partner brought market knowledge, customer relationships, and crucially, credibility that a Chennai-based company couldn't build overnight.

Robin Amlôt, Managing Editor at IBS Intelligence commented: "For the sixth year in a row, the company retained the top spot in the Retail Core Banking category, performing strongly in the APAC region, followed by Africa and Europe. Intellect Design Arena also racked up its third year as leader of the Wholesale Transaction Banking category. The company was a clear leader here with a nearly equal number of deals from the Americas, Europe, and the Middle East. It was also the second year running that Intellect Design Arena held the top position in InsurTech".

The distribution strategy evolved significantly during this period. Traditional enterprise software sales—expensive field sales teams, long sales cycles, massive RFPs—worked for established players but not for challengers. Intellect pioneered what they called "experience zones"—physical and virtual spaces where banks could actually use the software before buying. No PowerPoints, no demos, actual hands-on experience with their own data.

The competitive landscape was formidable. Temenos, the Swiss giant, had decades of credibility and thousands of implementations. FIS and Fiserv had massive installed bases in North America. Infosys Finacle leveraged the parent company's consulting relationships. TCS BaNCS could undercut on price. Yet Intellect was winning—not every deal, but enough to consistently rank #1.

The differentiation wasn't just technical—it was philosophical. While competitors sold "digital transformation," Intellect sold "composable transformation." Banks didn't need to transform everything at once; they could start small, prove value, then expand. This lowered the risk threshold dramatically, especially for mid-sized banks that couldn't afford massive transformation programs.

Over 60 global banking groups benefit from DTB, which handles 50% of total corporate collections transactions across regions like India, the Middle East, Asia Pacific, Africa, and Europe, setting a new standard in banking efficiency and customer satisfaction. This statistic reveals something profound: in certain segments, Intellect had achieved market-defining scale.

The market share challenge remained real. Even after such good performance in pre-Covid times, Intellect Design failed to increase its market share substantially. Yes, their market share has increased from 3.44% to just 4.66% in the last half-decade. This highlighted the inertia in enterprise software—banks don't switch core systems lightly, and new customer acquisition is expensive and slow.

The regional strategies varied significantly. In Asia-Pacific, Intellect leveraged cost advantages and cultural proximity. In the Middle East, they emphasized Islamic banking capabilities and local presence. In Europe, they focused on regulatory compliance and open banking readiness. In the Americas, they led with innovation and speed of implementation.

Intellect's Global Consumer Banking ranked #1 in the 2022 edition of Regional Leader (ASEAN). The ASEAN dominance wasn't accidental—these markets were digitizing rapidly, had less legacy infrastructure, and were more open to vendors from emerging markets. Vietnam, Thailand, Indonesia became showcase markets where Intellect could demonstrate capabilities to global prospects.

The sales strategy evolved from opportunistic to strategic. Early years were about winning any deal, anywhere. By 2020, Intellect was selective—focusing on "lighthouse" customers whose success would influence others. A tier-one bank win was worth ten tier-three wins, not just in revenue but in market credibility.

Commenting on Intellect's performance, Robin Amlôt, Managing Editor at IBS Intelligence said, "Intellect's continued dominance at the IBSi Sales League Table underscores its pioneering role in the fintech industry. Their commitment to innovation, exemplified by the groundbreaking eMACH.ai platform, continues to set a high benchmark in Retail Core Banking, Transaction Banking, and Lending. Intellect's solutions are not only reshaping the present landscape but are also poised to lead the evolution of financial services globally, driving unprecedented advancements and customer-centric solutions".

The partnership with cloud providers became strategic. Being "Powered by AWS" or "Built on Azure" provided technical credibility and commercial advantages. Cloud marketplaces became a new distribution channel, allowing banks to procure Intellect's software through existing cloud commitments.

Competition from Indian IT majors intensified during this period. Infosys pushed Finacle aggressively. TCS expanded BaNCS capabilities. Tech Mahindra acquired companies to build banking capabilities. But Intellect's pure-play focus—100% dedicated to financial services—became a differentiator. They weren't distracted by other industries or services revenue.

The pricing strategy was nuanced. In emerging markets, Intellect could compete on total cost of ownership. In developed markets, they emphasized value—faster time to market, better user experience, lower operational cost. The shift to subscription models made the software accessible to smaller institutions while providing predictable revenue.

Customer retention became as important as acquisition. Arun Jain noted: "This is a remarkable validation for us, proving how our customers rely on our products and reaffirming their faith in Intellect's Next-Gen FinTech architecture. Our rapid move towards an open finance architecture provides the ability for our customers to adopt a flexible, composable and contextual product design strategy".

The analyst relations strategy was sophisticated. Beyond IBS Intelligence, Intellect engaged with Gartner, Forrester, Celent, and Aite. Each analyst firm had different evaluation criteria, different client bases, different influence spheres. Consistent recognition across multiple analysts built cumulative credibility.

By 2024, Intellect's global position was established but not dominant. They were respected competitors in every market but market leaders in few. The challenge wasn't winning deals—it was winning enough deals, fast enough, to achieve the scale needed for the next phase of growth. The rankings validated the strategy, but market share remained the ultimate scorecard. The next frontier would require not just competing globally but fundamentally changing how banks bought and implemented software.

VIII. Financial Performance & Unit Economics

The CFO's office at Intellect's Chennai headquarters, May 2024. Venkateswarlu Saranu stares at the financial dashboard displaying numbers that would have seemed impossible a decade ago. Intellect had just announced crossing the INR 2500 Crore revenue mark—a milestone that validated the painful transformation from a loss-making spinoff to a profitable global fintech player. But the real story wasn't in the headline numbers; it was in the underlying unit economics that had fundamentally transformed.

The revenue evolution tells a story of deliberate transformation. From losses at demerger when Intellect had revenues of ~550 crores to crossing INR 2000 crore revenue mark, registering 21% growth in FY 2023, and then INR 2500 crore in FY24. But growth alone doesn't capture the qualitative shift in revenue composition. License linked revenue (License + Platform + AMC) had become the dominant driver, fundamentally changing the company's financial profile.

The shift to recurring revenue models was transformative. License linked revenue (License Platform AMC) was Rs 1,132 crore in LTM Q2 FY23 as against Rs 929 crore in LTM Q2 FY22 - grew 22%YoY. This wasn't just about predictability—it was about customer lifetime value. A traditional license sale was a one-time event. A subscription created a 15-20 year relationship with compounding value.

Annual Recurring Revenue - ARR (on an annualised basis) was at Rs 794 crore in LTM Q2FY23 as against 587 crore in LTM Q2FY22 - grew 35% YoY. ARR growth outpacing revenue growth indicated that new deals were increasingly subscription-based, setting up future revenue streams that would compound over time.

The margin story was equally compelling. From 6-9% EBITDA margins in FY19/FY20, Intellect had expanded to sustainable profitability. The company mentioned that the company is designed for 25% EBITDA margins but it continues to invest back 5% into platform journey. This deliberate choice—maintaining 20% reported margins while investing 5% in future capabilities—reflected long-term thinking rare in public markets.

The capital allocation strategy was sophisticated. 2 million person-hours of sustained investments annually and 16 million person-hours during the last 8 years in R&D have catapulted the company from Product to Technology company. eMACH.ai, with its 5 built-in technologies, drives holistic and agile transformation at double the speed and half the costs. This R&D intensity—unusual for an Indian company—was the moat that competitors couldn't easily replicate.

Dividend policy reflected confidence. The company's board of directors has recommended a final dividend of Rs 2.50 per share with a face value of Rs 5 per share for FY23. Maintaining dividend payouts while investing heavily in R&D and maintaining zero debt status demonstrated exceptional cash generation capabilities.

The unit economics at the customer level were particularly attractive. The company mentioned that margin maintenance & improvement will be there once the client is onboarded as the contract is for longer duration of 15-20 years. This long contract duration meant customer acquisition costs could be amortized over decades, creating compelling lifetime value to acquisition cost ratios.

Platform economics were emerging as the game-changer. Platform revenue of LTM Q2 FY 23 is Rs 448 crore as against Rs 276 crore in LTM Q2 FY22 - grew 62% YoY. Platform revenue commanded higher margins, scaled without linear cost increases, and created network effects as more customers adopted the platform.

The geographic mix impacted profitability significantly. Advanced market deals, while harder to win, commanded premium pricing. Emerging market deals provided volume but at lower margins. The optimal mix—roughly 60% emerging, 40% advanced—balanced growth with profitability.

Working capital management had improved dramatically. Days Sales Outstanding (DSO) improvements, better collection processes, and shift to subscription models reduced capital intensity. The company's ability to fund growth from operations without external capital was a testament to improving cash conversion.

The investment thesis for the future was clear. The company, however, mentioned that five years down the line margins will be in the range of 40% aided by increase in AMC business. This wasn't fantasy—enterprise software companies with high recurring revenue regularly achieve such margins. The question was execution, not possibility.

License revenue volatility remained a challenge. License revenue (18% of mix) grew 56.9% QoQ & 39.9% YoY to | 113 crore aiding in the strong revenue growth during the quarter. Quarter-to-quarter swings in license revenue, while positive for growth, created forecasting challenges that the market sometimes misinterpreted.

The cost structure had been optimized but not starved. Employee costs remained the largest expense, but the company had improved revenue per employee significantly. The shift from services to products meant the same headcount could support much higher revenue.

On the future growth outlook, the company mentioned that its business is designed to grow at 20% revenue growth. Intellect aims to grow at 20%+ revenue growth in FY24. This guidance—consistent 20% growth—reflected confidence in the pipeline and market opportunity rather than conservative sandbagging.

The competitive dynamics impacted pricing. Against global giants, Intellect often won on total cost of ownership rather than license fees. Against Indian competitors, they commanded premium pricing based on product superiority. This pricing power—the ability to charge more than competitors—was the ultimate validation of product-market fit.

Investment in partnerships was yielding returns. The company mentioned that it had already entered into a partnership with Microsoft and is now working with Accenture, which gives the company a strong cloud & AI partner and a digital partner. The company further mentioned that its partnership with IBM is also going strong. These partnerships reduced customer acquisition costs and accelerated deal cycles.

The SaaS transition was accelerating. SaaS revenue increased 80 bps to 20.7% of revenue mix and reported revenue of | 461 crore, up 23.3%. SaaS revenue, while lower in absolute dollars per customer initially, provided superior lifetime value through lower churn and automatic renewals.

Cash generation had become robust. The company also mentioned that cash generation in FY24 will higher be compared to FY23 as the investment phase is behind. The ability to generate cash while growing 20%+ and investing in R&D demonstrated the underlying profitability of the business model.

Return on equity remained a concern. Company has a low return on equity of 13.6% over last 3 years. While profitability had improved, the company's asset-light model meant ROE should be higher. This suggested either excess capital on the balance sheet or suboptimal capital allocation—areas for future improvement.

The deal metrics were improving. eMACH.ai was chosen by 16 customers worldwide in Q4 FY 24 (including 8 destiny deals) and 52 customers in FY24 (including 29 destiny deals). "Destiny deals"—large, transformational contracts—were becoming more frequent, indicating movement upmarket to larger, more strategic engagements.

Q1 FY24 revenue registered 19% YoY growth; License revenue grew 46% YoY, EBITDA grew 33% YoY and PAT grew 36%YoY. The operating leverage was evident—revenue growing 19% but profits growing 36% demonstrated the scalability of the platform model.

Looking at the financial trajectory, Intellect had achieved something remarkable: building a profitable, cash-generative, high-growth enterprise software company from India. The unit economics—high gross margins, improving EBITDA margins, strong cash generation, increasing recurring revenue—rivaled global best-in-class. The challenge now wasn't profitability but scale. Could they maintain these economics while growing from 2500 crores to 10,000 crores? The financial foundation suggested yes, but execution would determine reality.

IX. Playbook: Lessons in Building Global FinTech from India

The conference room at IIT Delhi, 2023. Arun Jain addresses a packed auditorium of aspiring entrepreneurs. "Everyone asks me the secret of building a global product company from India," he begins. "The truth is, we did everything wrong before we figured out what was right. Let me tell you what we learned—not from success, but from failure."

Lesson 1: Design Thinking as Competitive Advantage

The fundamental insight that transformed Intellect wasn't technical—it was philosophical. According to design thinking, asking an appropriate question is more important than getting to a solution. The foundation of design thinking lies in empathy with the customers. While competitors focused on features, Intellect focused on problems. While others built what banks asked for, Intellect built what banks actually needed.

The design thinking approach manifested in every interaction. Customer meetings started not with product demos but with questions: What keeps you awake at night? What would you build if you could start over? What do your employees hate about their current systems? This empathy-first approach revealed opportunities competitors missed.

'Less is More': Remove redundancy and focus on what matters the most for users. In other words, reduce complexity and keep it simple. 'Last 2% is 200%': Empathize with the user. Be alert to understand unstated requirements to provide differential service(s). These weren't just slogans—they were engineering principles that drove product decisions.

Lesson 2: Managing the Services-to-Products Transition

The most painful lesson was that services companies and product companies require fundamentally different DNA. Services optimize for utilization—keeping people billable. Products require slack—time to think, experiment, fail. Services celebrate customer customization. Products demand saying no to maintain architectural integrity.

Under Polaris, Intellect lacked dedicated thrust and investments in Sales & Marketing. Our competition invests between 30-50% on Sales & Marketing. We invest 15% in Sales & Marketing. To be globally competitive, we propose to increase these investments in a focused and planned manner. The demerger wasn't just structural—it was cultural liberation.

The transition required patient capital. FY15-FY18 was Go-To-Market stage for Intellect wherein there were heavy investments in Sales & Marketing. Intellect invested heavily for next 3-4 years in Sales & Marketing, which was as high as ~45% of revenues. Even investments in R&D were high at 15-20% of revenues. These heavy investments resulted in Intellect continuing to turn losses from FY15 to FY18.

Lesson 3: Building for Global Markets from Emerging Economy Base

The conventional wisdom was that Indian companies couldn't build global products—they lacked domain expertise, customer proximity, market understanding. Intellect turned these disadvantages into advantages. Being outsiders forced them to question assumptions insiders took for granted.

The cost arbitrage that made Indian IT services successful became a liability in products. Global customers assumed lower price meant lower quality. Intellect had to price at par or premium to global competitors to be taken seriously—then overdeliver on value to justify the price.

Building global products from India required a different talent strategy. Instead of hiring fresh graduates and training them—the IT services model—Intellect hired experienced professionals who had worked in global banks. They paid premium salaries to attract Indians working abroad to return home. Domain expertise couldn't be taught; it had to be acquired.

Lesson 4: The Importance of Patient Capital and Long-Term Vision

2 million person-hours of sustained investments annually and 16 million person-hours during the last 8 years in R&D have catapulted the company from Product to Technology company. eMACH.ai, with its 5 built-in technologies, drives holistic and agile transformation at double the speed and half the costs. This level of sustained investment was only possible because Jain, as founder-promoter, could take a long-term view.

Public market pressure for quarterly results nearly killed the transformation. The stock price volatility—from Rs 43.80 to Rs 773.80—reflected market confusion about Intellect's model. Were they a services company with some products? A product company with services revenue? The market hated ambiguity, but transformation required living in ambiguity for years.

The funding strategy was crucial. Rights issues, promoter funding, retained earnings—every source except debt. Debt would have forced short-term thinking. Equity, while dilutive, provided the flexibility to invest through losses to profitability.

Lesson 5: Creating IP-led Differentiation

The intellectual property strategy was sophisticated but often misunderstood. Intellect didn't patent algorithms or business methods—those were difficult to defend and easy to work around. Instead, they built complexity that competitors couldn't replicate: domain knowledge encoded in software, integration patterns that took years to perfect, and architectural decisions that compounded over time.

With an impressive array of 329 microservices, 535 events and over 1757 APIs, this First Principles Thinking-based Platform enables financial institutions in the Island Nation to build future-ready solutions. Each microservice represented years of learning. Each API encoded regulatory requirements across multiple jurisdictions. The platform wasn't just software—it was crystallized expertise.

Lesson 6: The Platform Mindset

The evolution from products to platform required a fundamental mindset shift. Products were sold; platforms were adopted. Products had features; platforms had ecosystems. Products locked customers in; platforms created network effects that made leaving irrational.

We are working towards moving Intellect Design from product to platform company. This transition will help us to gain a significant market share at the global level. The platform strategy wasn't just about technology—it was about business model innovation.

Lesson 7: Competing with Giants

The David versus Goliath narrative was romantic but misleading. Intellect didn't beat giants by being smaller and more agile. They won by changing the game. While Temenos sold enterprise licenses, Intellect offered subscriptions. While FIS required armies of consultants, Intellect provided self-service tools. While Oracle demanded multi-year commitments, Intellect enabled monthly deployments.

The key was identifying where giants were structurally disadvantaged. Large companies couldn't cannibalize existing revenue streams. They couldn't disrupt their own partner ecosystems. They couldn't take risks that might upset installed bases. Intellect had no such constraints—they could build the future without protecting the past.

Lesson 8: The Importance of Timing

The pandemic accelerated digital adoption by years, but Intellect had been preparing for this moment since 2014. In FY20, Intellect declared total revenue of Rs 1,385.10 crore. This can be attributed to the rising case of Covid-19 globally. Even if they failed to beat their previous mark, the fall in the revenue wasn't steep. This shows the strength of fintech companies.

Being too early was as dangerous as being too late. Intellect's cloud-native architecture, built years before banks were ready for cloud, initially seemed like over-engineering. But when the market turned, they were ready while competitors scrambled to retrofit legacy systems.

Lesson 9: Culture as Strategy

The cultural principles that emerged weren't accidental—they were strategic choices. Empowerment over control. Questions over answers. Learning over knowing. These weren't feel-good values; they were competitive advantages in an industry where innovation speed determined success.

"People work on their own, instead of being asked to work. Jain likes to empower people to take decisions. He won't micro-manage, but when things go wrong, he will step in". This management philosophy—maximum autonomy with selective intervention—enabled innovation while maintaining quality.

Lesson 10: The India Advantage

The final lesson was counterintuitive: being from India was an advantage, not a handicap. Indian engineers understood complexity—they lived it daily. Indian entrepreneurs understood frugality—they had no choice. Indian companies understood diversity—they operated in the world's most heterogeneous market.

More fundamentally, building from India forced discipline. Without access to unlimited venture capital, Intellect had to build sustainable businesses. Without prestigious brands, they had to win on merit. Without home market advantage, they had to think globally from day one.

The playbook that emerged wasn't just about building a fintech company—it was about building a global product company from an emerging market. It required patient capital, design thinking, platform architecture, and most importantly, the audacity to believe that a company from Chennai could compete with anyone, anywhere. The journey from $250 to 2500 crores validated the thesis. The question now was whether this playbook could be replicated, scaled, and evolved for the next generation of Indian product companies.

X. Bear vs. Bull Case & Future Outlook

Bear Case: The Structural Headwinds

The skeptics have compelling arguments. Despite all the accolades and growth, Intellect Design failed to increase its market share substantially. Yes, their market share has increased from 3.44% to just 4.66% in the last half-decade. In enterprise software, market share is destiny. Without scale, R&D investments become unsustainable, talent acquisition becomes harder, and competitive moats erode.

The competition isn't standing still. Temenos, with revenues exceeding $1 billion, spends more on R&D annually than Intellect's total revenue. FIS and Fiserv are consolidating, creating behemoths with unprecedented scale. Cloud-native challengers like Thought Machine and Mambu are raising hundreds of millions in venture capital, competing for the same digital transformation deals.

Company has a low return on equity of 13.6% over last 3 years. For a capital-light software business, this ROE is disappointing. It suggests either inefficient capital allocation or structural profitability challenges that financial engineering can't solve. Compare this to Temenos's 20%+ ROE or even Indian IT services companies generating 25%+ ROE.

The dependency on banking sector health creates systemic risk. Banking IT spending correlates with banking profitability, which correlates with economic cycles. A global recession, credit crisis, or regulatory squeeze could dramatically reduce technology spending. Unlike diversified IT companies, Intellect has no hedge—they're all-in on financial services.

Indian IT majors are awakening to the product opportunity. Infosys is investing heavily in Finacle, leveraging its massive sales force and customer relationships. TCS is expanding BaNCS, using its consulting strength to bundle products with services. These giants have resources Intellect can't match—thousands of salespeople, decades of relationships, unlimited capital.

The advanced market penetration, while improving, remains nascent. Despite recent wins, Intellect has minimal presence in the US—the world's largest banking technology market. Without US success, global leadership remains a dream. And breaking into the US requires investments that could destroy profitability for years.

Technical debt accumulates even in modern architectures. As Intellect's platform grows—now over 329 microservices—complexity increases exponentially. Managing this complexity, maintaining backward compatibility, ensuring security across thousands of APIs—these challenges only intensify with scale.

Customer concentration risk persists. While Intellect has 240+ customers, revenue concentration in top accounts remains high. Loss of a major customer—through consolidation, insourcing, or competitive displacement—could materially impact growth.

The talent challenge is structural, not cyclical. Competing for engineering talent against Google, Microsoft, and Amazon in India. Competing for domain expertise against global banks paying investment banking salaries. Competing for sales talent against companies offering Silicon Valley stock options. The talent war intensifies as the company grows.

Regulatory risks loom large. Banking is becoming more regulated, not less. Data localization requirements, privacy regulations, operational resilience mandates—each adds complexity and cost. A single regulatory failure could destroy decades of reputation building.

Bull Case: The Transformation Trajectory

But the optimists see a different future. Intellect isn't trying to win yesterday's game—they're defining tomorrow's. The shift from monolithic core banking to composable finance isn't a trend; it's an architectural revolution. And Intellect's platform, built on first principles thinking, is positioned perfectly for this future.

Intellect continues to lead the fintech industry with top rankings in Retail Core Banking for the sixth consecutive year, Transaction Banking for the fifth consecutive year, and Lending for the third consecutive year. Consistent market leadership in multiple categories suggests product superiority that's widening, not narrowing.

The recurring revenue transformation fundamentally changes the investment thesis. Annual Recurring Revenue - ARR (on an annualised basis) is at Rs 794 crore in LTM Q2FY23 as against 587 crore in LTM Q2FY22 - grew 35% YoY. ARR growth exceeding revenue growth means future revenue is increasingly predictable and protected.

The fact that 8 out of 12 deal wins in the quarter are from Americas and Europe gives us the confidence that we have the desired market endorsements for our platform to address the needs of western financial institutions. Advanced market success isn't a hope—it's happening. Each win creates references that accelerate future sales.

The AI transformation presents a generational opportunity. This latest win highlights IntellectAI's strategic investment in creating Purple Fabric platform which brings the power of 217 technologies to deliver cutting-edge Artificial Intelligence solutions. This AI platform gives the opportunity to quickly design and realise the potential of connected intelligence for an organisation to transform its operations. While competitors bolt AI onto legacy architectures, Intellect has built AI into its foundation.

Platform economics are just beginning to manifest. As more banks adopt eMACH.ai, network effects accelerate. Each new customer makes the platform more valuable for all customers. Each new integration reduces implementation cost for future customers. Each new microservice expands addressable use cases. This isn't linear growth—it's exponential potential.