INFIBEAM AVENUES: The Story of India's Payment Infrastructure Pioneer

I. Introduction & Episode Roadmap

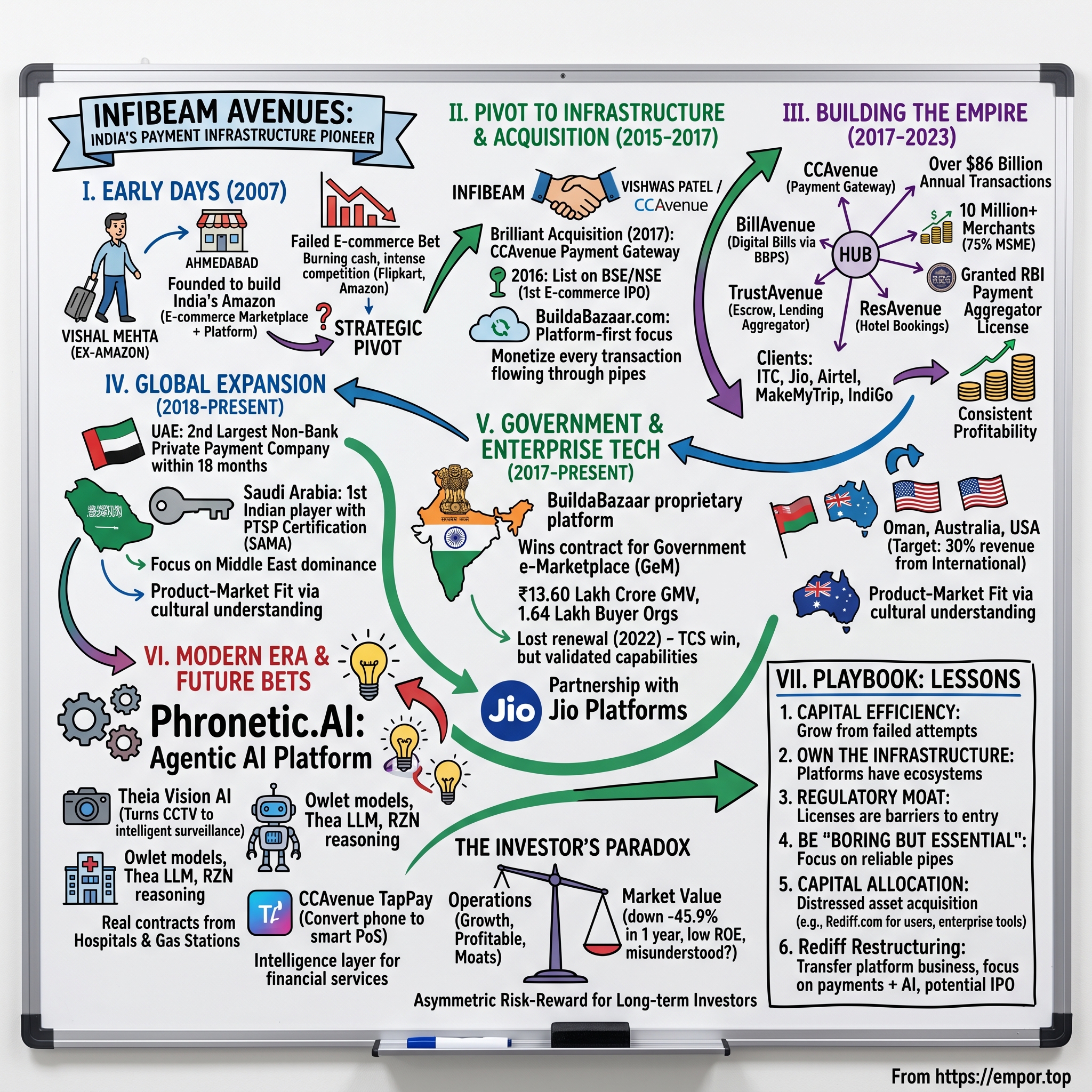

Picture this: It's 2007, and while Silicon Valley veterans are typically cashing out their stock options and retiring to Palo Alto estates, one ex-Amazon executive is boarding a flight to India with a radically different plan. Vishal Mehta isn't just leaving behind a decade at one of the world's most successful tech companies—he's betting his entire career on building something in a market where only 3% of the population has credit cards and e-commerce barely exists.

Today, that bet has transformed into Infibeam Avenues, a financial technology powerhouse that processes over $86 billion in transactions annually and powers the payment infrastructure for more than 10 million merchants across India and the Middle East. Through its flagship brand CCAvenue, the company ranks among India's top three B2B payment gateways. In the UAE, it achieved something even more remarkable: becoming the second-largest non-bank private payment company within just 18 months of serious operations.

But here's what makes this story fascinating for investors and founders alike: Infibeam didn't win by playing the typical venture capital game. While competitors like Flipkart raised billions and grabbed headlines, Vishal Mehta built his empire on a philosophy of capital efficiency that seemed almost quaint in the era of blitzscaling. The company went public in 2016 with minimal dilution, maintaining founder control while building critical infrastructure that would become the backbone of India's digital economy.

This is a story of strategic pivots done right—from e-commerce marketplace to payment infrastructure, from domestic focus to international expansion, from pure payments to full-stack fintech. It's about building boring but essential infrastructure in emerging markets, where the real money isn't in the flashy consumer apps but in the pipes that make everything else possible.

Over the next few hours, we'll unpack how an MIT Sloan graduate who helped revitalize Amazon's technology stack came back to India to build what would become one of the most important—yet underappreciated—pieces of the country's digital infrastructure. We'll explore the failed e-commerce bet that almost killed the company, the brilliant acquisition that saved it, and the international expansion that nobody saw coming. And we'll analyze why, despite processing transactions worth billions and maintaining consistent profitability, the market values Infibeam at just ₹4,810 crore—down 45.9% over the past year—while loss-making competitors command premium valuations.

II. The Amazon Alumni Story & Founding Vision

The conference room at Amazon's Seattle headquarters buzzed with the controlled chaos typical of a Jeff Bezos-era strategy session. It was 2005, and Vishal Mehta, armed with degrees in Operations Research from Cornell and management from MIT Sloan, was presenting a financial model that would reshape how Amazon thought about international expansion. For nearly a decade, Mehta had been instrumental in revitalizing the e-commerce giant's technology infrastructure and spurring growth in finance and corporate development. But as he looked at the projections for emerging markets, particularly India, a different vision began to crystallize. Mehta's decade at Amazon headquarters, from 1997 to 2007, working in technology revitalization, finance, and corporate development roles, provided him with a front-row seat to one of the greatest scaling stories in corporate history. But by 2006, something was pulling him back to India—not the usual immigrant's nostalgia, but a strategic insight that would define the next chapter of his career.

"The question wasn't whether to stay or return," Mehta would later reflect in interviews. Like most Indians who had gone abroad, the question of whether to stay back in the U.S. or return to their motherland with the aim of contributing to the growth story started to trouble Mehta. But for him, it was more calculated. India's GDP was growing at 9% annually, mobile phone adoption was exploding from 90 million to what would become 300 million users by 2008, and yet e-commerce penetration was virtually non-existent.

The pivotal moment came during a 2006 trip to India when Mehta visited local retailers in Ahmedabad. Store owners were eager to sell online but had no idea how to begin. The infrastructure simply didn't exist—no payment gateways that worked reliably, no logistics networks for last-mile delivery, no platforms that could handle Indian languages and payment preferences. Where others saw obstacles, Mehta saw a blueprint for an entire ecosystem waiting to be built.

After spending ten years in the US, he returned to India in 2007 with several colleagues from Amazon and founded Infibeam. This wasn't a solo venture—it was an orchestrated movement of talent. He brought along careers—both his and those of his mates at Amazon who had joined hands to venture into entrepreneurship. The team that assembled in Ahmedabad in 2007 included engineers who had built core systems at Amazon, operations experts who understood scale, and product managers who knew how to think platform-first rather than product-first.

The original vision was audacious yet logical: build India's Amazon. It was always a two-pronged strategy: Infibeam.com sold everything from books and electronics to home and lifestyle products, while simultaneously renting out the technology platform that powered the portal. This dual approach—marketplace plus infrastructure—would prove both prescient and problematic. It was prescient because infrastructure would eventually become the company's moat. It was problematic because in 2007, trying to do both meant doing neither particularly well.

The India these ex-Amazonians returned to was vastly different from the Seattle they'd left behind. Internet penetration stood at a mere 4%. Credit card ownership was below 3%. Cash-on-delivery wasn't just preferred—it was essential for 80% of transactions. The ecosystem that made Amazon possible in the U.S. simply didn't exist. They would have to build it from scratch.

III. The CCAvenue Acquisition & Payment Gateway Pivot

The year was 2015, and Infibeam was hemorrhaging money on its e-commerce operations. In a nondescript office building in Mumbai, Vishwas Patel was running CCAvenue, a payment gateway he had founded back in 2001—long before anyone in India truly understood what digital payments could become. Mr. Vishwas Patel is the founder of the payment gateway brand, CCAvenue, founded in the year 2001. The two companies were about to converge in what would become one of the most consequential mergers in Indian fintech history.CCAvenue, founded in 2001 by Vishwas Patel, was processing payments for millions of businesses worldwide when most Indians didn't even know what a payment gateway was. By 2016, it had quietly become one of India's most profitable fintech companies, processing over ₹15,000 crores of transactions for around 100,000 merchants—all while maintaining a low profile that kept it off most investors' radars.

The courtship between Infibeam and CCAvenue began in June 2016, when Infibeam picked up 3.85% for around ₹50 crore through its subsidiary NSI Infinium Global. This wasn't just a financial investment—it was a strategic probe, a way for Mehta to understand whether the cultural and operational fit would work. By February 2017, Infibeam was ready to make its move, signing an agreement to invest ₹150 crore to acquire 7.5% stake.

The acquisition valued CCAvenue at a net worth of Rs 123.54 crores, while valuing Infibeam at a consolidated net worth of Rs 781.82 crores, as on March 31st 2017. But here's where it gets interesting: Avenues merged with Infibeam for about Rs 2,000 crore but the fair value was valued only Rs 134 crore. Remaining Rs 1,846 crore worth stock was paid for intangible assets including software, trademark, goodwill, and customer relationship. This massive goodwill component—93% of the total acquisition amount—would later raise auditor eyebrows and become a point of controversy.

The merger itself was structured as an all-stock deal: 260 shares of Infibeam being given for every 100 shares of CCAvenue. For Vishwas Patel and the CCAvenue team, this wasn't an exit—it was a transformation. Patel would become Joint Managing Director of the combined entity, bringing his two decades of payment expertise to complement Mehta's platform vision.

What made this merger brilliant wasn't just the financials—though CCAvenue was growing at a CAGR of more than 45% to 50% year-over-year and would add another ₹200 crores to Infibeam's services revenue portfolio. It was the strategic logic. As Mehta explained in earnings calls: "Platform with payment is a very, very interesting asset... It allows us to provide a very seamless experience for merchants to onboard and to be able to transact and gain customers online".

The Digital Payment Platform that emerged from this merger operates through the flagship brand CCAvenue as a PCI DSS 3.2.1 compliant payment gateway platform. With over 240 payment options connecting more than 55 Indian banks on a real-time basis, CCAvenue became one of India's largest direct debit engines. It processes payments through net-banking, all types of credit cards, debit cards, and digital wallets, including the then-nascent UPI payments.

But the real genius of the acquisition was timing. This was 2017—a year after demonetization had forced millions of Indians to experiment with digital payments for the first time, but before the UPI revolution had fully taken hold. Payment gateways were about to become critical infrastructure for India's digital economy, and Infibeam had just acquired one of the best at a fraction of what it would be worth just a few years later.

The transformation was immediate. Instead of bleeding cash on customer acquisition for its e-commerce marketplace, Infibeam could now monetize every transaction flowing through its payment gateway. Instead of competing with Flipkart on who could offer the biggest discounts, it could focus on providing the infrastructure that every e-commerce player—including its former competitors—would need.

IV. The Failed E-commerce Bet & Strategic Pivot

The conference room in Infibeam's Ahmedabad headquarters was silent except for the whir of the air conditioning. It was late 2014, and Vishal Mehta was staring at a spreadsheet that told a story no founder wants to hear. While Flipkart had just raised $1 billion at a $7 billion valuation and Amazon had committed $2 billion to its India operations, Infibeam's e-commerce marketplace was burning through cash with no path to profitability in sight.

Vishal Mehta has had limited success as an online retailer with Infibeam.com. But he is back in the hunt with e-commerce infrastructure provider BuildaBazaar.com. This understated assessment from Business Today barely captured the existential crisis the company faced. The marketplace that was supposed to be India's Amazon was instead becoming a cautionary tale about the perils of capital efficiency in a blitzscaling world.

There was a time when Flipkart and Infibeam were almost head to head, according to Niren Shah, Managing Director at Norwest Venture Partners. "In the past Infibeam was very focused on capital efficiency, and so it did not raise large sums of money. Unfortunately, the Indian market has chosen winners based on scale and the lack of fund raising may have impeded Infibeam's progress."

The numbers told the brutal truth. While Infibeam prided itself on running a lean operation, competitors were spending hundreds of crores on marketing alone. When other e-tailers invested heavily in offline and online marketing, Infibeam chose to stay low-profile. Flipkart and Snapdeal had become household names through celebrity endorsements and primetime TV ads. Infibeam? Most Indians had never heard of it.

But the problem went deeper than just marketing spend. An industry expert noted: "Infibeam is an online marketplace which could never build itself into a shopping destination. It offers discounts but why would someone go there instead of Snapdeal or Amazon who also offer heavy discounts. If an e-tailer doesn't have a proposition for consumers, it is very difficult to sustain the onslaught of large players".

Mehta's philosophy was fundamentally different from his competitors'. Those who worked with Mehta say he was mostly averse to external funding and hefty marketing spends. Most investors who approached Mehta sought a high stake in the start-up, so he decided to run the show on his own. His reasoning was logical, even admirable: private equity money comes with costs and riders.

"They had the first-mover advantage but they compromised on growth due to this approach," says an online retailer. This first-mover advantage was real—Infibeam had launched in 2007, three years before Flipkart pivoted from books to general merchandise, and six years before Amazon entered India. But in the winner-take-all dynamics of e-commerce, being early meant nothing without the capital to defend your position.

The irony was that Mehta understood the economics better than anyone. "Businesses are not built to lose money but to make money," grins Mehta in interviews from that period. He wasn't wrong—Flipkart wouldn't turn profitable for another decade, and many of the high-flying e-commerce companies of that era would eventually shut down or sell for pennies on the dollar. But being right about unit economics didn't help when customers were flocking to competitors offering deeper discounts and faster delivery.

By 2015, the writing was on the wall. Infibeam's e-commerce GMV was stagnating while infrastructure costs kept rising. The company needed to make a choice: raise massive amounts of capital to compete in the e-commerce wars, or pivot to something where capital efficiency could actually be an advantage.

The pivot, when it came, was both dramatic and subtle. Infibeam wouldn't abandon e-commerce entirely—that would be admitting defeat. Instead, it would flip the model. Rather than competing to be THE e-commerce platform, it would become the infrastructure provider for thousands of e-commerce platforms. BuildaBazaar, which had always been the second prong of Infibeam's strategy, would now become the primary focus.

This wasn't just a business model pivot—it was a philosophical one. Instead of B2C, think B2B. Instead of acquiring customers, acquire merchants. Instead of fighting for market share in a winner-take-all market, become the arms dealer in a market where everyone needs weapons. The lessons from the failed e-commerce bet would shape everything that came next: stay capital efficient, avoid competition with deep-pocketed players, and focus on boring but essential infrastructure that others couldn't easily replicate.

V. Building the Payment Infrastructure Empire

The year 2016 marked a defining moment for Infibeam—not because of any single product launch or acquisition, but because of a strategic decision that would transform it from a struggling e-commerce player into an infrastructure powerhouse. The company was listed on the BSE and the NSE in 2016, becoming the first Indian e-commerce company to go public. While competitors were raising private rounds at inflated valuations, Mehta chose the discipline of public markets. The IPO filing revealed something remarkable: from Rs 337 crore revenue and Rs 8.8 crore profit at the time of listing, Infibeam would go on to post Rs 839 crore revenue with Rs 88 crore profit in FY18—a 10x increase in profitability in just two years. This wasn't the typical cash-burning e-commerce story investors were used to. This was infrastructure building at its finest.

By March 2023, the transformation was complete. The company made 91.4% of its total operating revenue via its payment gateway and infrastructure business, which grew 58% to Rs 1,793 crore during FY23 from Rs 1,134 crore in FY22. The e-commerce platform that had once been the company's identity now contributed just 8.6% of revenues.

The network effects were staggering. It had a network of 9.2 million merchants as of March 2023. Among these, approximately 6 million use the company's software platforms, while the remaining 3 million engage with the company's payment platforms. More than 75% of these merchants belong to the micro, small, and medium enterprises category—the backbone of India's economy that had been historically underserved by traditional financial institutions.

Under his leadership, the company has grown into one of the largest fintech, software, and payment infrastructure provider, processing over $86 billion in transactions annually across more than 10 million merchants. This wasn't just about payment processing—it was about creating an entire ecosystem.

The product suite expansion told the story of infrastructure dominance. Beyond CCAvenue, the company launched BillAvenue in November 2017, a digital bill payments platform built over the Bharat Bill Payment System (BBPS) infrastructure. ResAvenue handled hotel bookings and travel payments. TrustAvenue provided escrow services. Each product wasn't competing for consumer mindshare—they were embedding themselves into the operational DNA of businesses.

The regulatory moat deepened significantly when, in 2022, Infibeam Avenues was granted the payment aggregator licence by the Reserve Bank of India for CCAvenue. This wasn't just a permit—it was a competitive fortress. The RBI had tightened regulations after years of loose oversight, and only companies with robust compliance, technology, and capital could qualify. Smaller competitors would struggle to match this regulatory clearance.

The net take rate evolution revealed the business model's brilliance. The company's payment net take rates experienced a significant increase in Q2 FY24, up 25% YoY to 9.3 basis points, primarily due to a substantial influx of small merchants. Small merchants paid higher rates than large enterprises but were stickier customers with lower churn. This wasn't a race to the bottom on pricing—it was strategic customer selection.

By Q4 FY25, the scale had become breathtaking. In Q4 FY25, the company clocked INR 2.41 Lakh Cr in transaction processing value (TPV), up 7% from INR 2.26 Lakh Cr in the year-ago quarter. To put this in perspective, Infibeam was processing more in a quarter than many banks process in a year.

The platform's technical capabilities had evolved far beyond simple payment processing. The payment acquiring business includes a front-end Payment Gateway (PG) for acquiring or processing digital payment transaction through 200+ payment methods categorized into debit and credit cards, net banking, wallets, EMI and UPI. This wasn't just about accepting payments—it was about giving merchants every possible way to get paid, reducing cart abandonment, and maximizing conversion rates.

What made this infrastructure empire particularly defensible was its enterprise focus. It caters to marquee clients across industries, such as ITC, MakeMyTrip, IndiGo, Vistara, Taj, Jio, Airtel, Myntra, Indian Oil. These weren't price-sensitive SMBs that could be poached with discounts. These were enterprises that valued reliability, compliance, and integration capabilities over marginal cost savings.

The transformation from e-commerce marketplace to payment infrastructure had created something rare in Indian tech: a profitable, defensible, scalable business that grew stronger with each passing quarter. While the market still valued Infibeam like a second-tier e-commerce player, the company had quietly become one of India's most important pieces of financial infrastructure.

VI. International Expansion & Middle East Dominance

The Dubai International Financial Centre gleamed under the desert sun as Vishal Mehta signed the papers that would transform Infibeam from an Indian payment company into a regional powerhouse. It was 2018, and while most Indian fintechs were still fighting for domestic market share, Mehta was executing a contrarian strategy: dominate the Middle East before the competition even noticed the opportunity. The company earlier expanded into the United Arab Emirates (UAE) in 2013 through the BuildaBazaar platform, marking one of the first Indian e-commerce players to venture overseas. But the real game-changer came when it launched CCAvenue payments in the UAE later in 2018. What happened next defied all conventional wisdom about Indian companies expanding internationally.

Within 18 months, CCAvenue became the second-largest non-bank private payment company in the UAE. Let that sink in: a company from India, competing against established Western and Middle Eastern players, captured the number two position in one of the world's most sophisticated financial markets. As a pure-play online payment solutions provider, in the UAE, we rank second in payments processed among all the non-bank players.

The secret wasn't just technical capability—it was cultural understanding. The Middle East, particularly the UAE, had a unique mix of local merchants, expatriate businesses, and international corporations. Each had different needs: local merchants wanted Arabic interfaces and Sharia-compliant payment options, expatriate businesses needed multi-currency processing, and international corporations demanded enterprise-grade reliability. CCAvenue delivered all three. The Oman expansion in 2020 showcased the company's Middle East playbook perfectly. Infibeam Avenues also collaborated with Bank Muscat, the largest financial services provider in Oman, in 2020. It also partnered with Bank Dhofar, the second-largest financial services provider in Oman, to offer CCAvenue Payment Gateway Service. This quick one-two combination of a tie-up with the top two banks of Oman meant that a lion's share of Oman's processing volumes would now flow through Infibeam Avenues systems.

The numbers in the UAE were staggering. CCAvenue processed payments at an annual run rate of AED 12 billion in FY 2022-23. This figure increased to over AED 14 billion in the current fiscal year and was projected to reach AED 18 billion by year-end 2024. Over the past six years, CCAvenue.ae claimed to have processed transactions totalling AED 24.5 billion, with approximately 23.5 million transactions to date.

But the real masterstroke came with Saudi Arabia. Infibeam Avenues has become the first Indian player to receive PTSP (Payment Technical Service Provider) Certification from SAMA (Saudi Arabian Monetary Authority). This distinction allows them to operate as a full-fledged payment processor within the Kingdom. This wasn't just a license—it was a competitive moat. Being the first Indian payment gateway to secure this certification gave Infibeam first-mover advantage in a market where trust and regulatory compliance are everything.

The U.S. expansion in 2020 represented a different challenge altogether. Infibeam Avenues Australia Pty Ltd (Australian market), AI Fintech Inc. (USA market), and Infibeam Avenues Saudi Arabia for Information Systems Technology were all consolidated under Vavian International Ltd, its UAE-based wholly-owned subsidiary. This restructuring wasn't just corporate housekeeping—it was strategic positioning to attack developed markets from a position of strength in emerging ones.

The international strategy revealed something crucial about Infibeam's approach: while Indian competitors were burning cash trying to win the domestic market, Infibeam was quietly building a global payments network. Currently, the international business contributes 6% to Infibeam Avenues Ltd's total revenue, but the company's ambitions were much larger. Management targeted international business to contribute 30% of total revenue within the next couple of years.

What made the international expansion particularly brilliant was the product-market fit. In India, Infibeam competed with well-funded players like Razorpay and PayU. In the Middle East, it faced less competition from Indian players and could leverage its experience with similar infrastructure challenges. The company understood that markets like Oman, with nearly 150% mobile penetration and over 80% internet usage, were primed for digital payment adoption.

The technical capabilities that powered this expansion were formidable. The multi-channel, multi-lingual and multi-currency, allows us to launch our payment solutions anywhere across the globe. This wasn't just about translation—it was about understanding local payment methods, regulatory requirements, and merchant needs in each market.

By 2023, the transformation was complete. Infibeam wasn't just an Indian payment company with some international operations—it was a regional payments powerhouse with operations across India, UAE, Saudi Arabia, Oman, Australia, and the United States. The company that had failed to dominate Indian e-commerce had succeeded in building something far more valuable: critical payment infrastructure across multiple high-growth markets.

VII. The Platform Business: BuildaBazaar & Government Tech

The meeting at the Ministry of Commerce in New Delhi was tense. It was 2017, and the Indian government was about to make a decision that would revolutionize how ₹3 lakh crore worth of government procurement happened annually. On one side sat representatives from global tech giants—IBM, Accenture, TCS. On the other, a consortium led by Infibeam, the company that most bureaucrats had never heard of. When the results were announced, the underdogs had won. Technology Platform via the brand name 'BuildaBazaar' for enterprises and government provide cloud-based, end-to-end software-as-a-service (SaaS) platforms that allow corporate clients to transact online, manage the back-end (orders, inventory and logistics), make digital payments, undertake online marketing and so on. BuildaBazaar proprietary platform also hosts one of the largest online market for government procurement called Government of India e-Marketplace (GeM).

The GeM win was David beating multiple Goliaths. While Intellect beat TCS and Sify, Infibeam won the bid over players like Flipkart and Amazon. TCS roped in Tata Group ecommerce firm Tata CLiQ and Sify partnered with Amazon Web Services to form a stronger consortium. Yet the consortium led by Intellect Design Arena and Infibeam emerged as the lowest bidder.

The five-year contract, worth around Rs 1,000 crore, wasn't just about the money. Procurement by the central and state governments has been estimated to be worth around $77.65 Bn – $108.72 Bn (INR 5 Lakh Cr-INR 7 Lakh Cr) each year. This was about controlling the infrastructure through which trillions of rupees in government procurement would flow.

What made Infibeam's bid successful wasn't just price—it was understanding. While Amazon and Flipkart saw GeM as another marketplace, Infibeam understood it was fundamentally different. Government procurement needed different workflows, approval hierarchies, audit trails, and compliance mechanisms. BuildaBazaar had been quietly building these capabilities for years, serving enterprise clients who had similar complex requirements.

The impact was immediate and massive. As of 1st May, 2025, GeM has crossed ₹13.60 Lakh Crore in GMV with a total order volume of more than 2.86 Crore. The portal has over 1.64 Lakh Buyer Organisations and over 23 Lakh Sellers & Service Providers, of which more than 10.42 Lakhs are MSE Sellers & Service Providers and 30,866 are Startup Suppliers.

But the GeM contract also revealed the vulnerabilities of platform businesses. When the contract came up for renewal in 2022, Infibeam Avenues Ltd was disqualified during the tender evaluation as the company was not able to submit the Capability Maturity Model Integration (CMMI) certificate which is mandatory for IT projects. TCS won the renewal, and Infibeam lost one of its crown jewels.

The loss stung, but it also validated the strategy. Infibeam had proven it could compete with—and beat—the biggest names in Indian tech. More importantly, it had shown that BuildaBazaar wasn't just an also-ran e-commerce platform but sophisticated enterprise software that could handle nation-scale deployments.

The enterprise SaaS strategy extended beyond government. The company entered into an agreement with Jio Platforms to offer its enterprise software licence and enterprise digital payments platform to Jio Platforms' internal businesses. This wasn't a small vendor contract—this was Reliance, India's largest conglomerate, choosing Infibeam's technology to power its digital ambitions.

The platform business model had evolved far from its e-commerce roots. BuildaBazaar now offered: - Multi-tenant marketplace infrastructure - Inventory and warehouse management systems - Digital catalog management - Vendor onboarding and verification - Complex approval workflows - Analytics and reporting dashboards - Integration with payment gateways (naturally, CCAvenue)

Each component was battle-tested at scale through GeM and enterprise deployments. While competitors built for the happy path of consumer e-commerce, BuildaBazaar was built for the complex reality of B2B and G2B transactions.

The numbers told the story of transformation. Platform business, which had once been the failed e-commerce marketplace, now contributed hundreds of crores in high-margin SaaS revenues. Enterprise clients paid annual contracts, reducing the volatility of transaction-based revenue. The capital-light model meant minimal marginal costs for each new deployment.

The government tech play had another strategic benefit: credibility. Being trusted to run GeM, even temporarily, gave Infibeam credentials that money couldn't buy. When pitching to enterprises or international governments, "we built and ran India's national procurement platform" carried weight that no marketing campaign could match.

VIII. The Rediff Acquisition & Consumer Play

The boardroom at Rediff.com's Mumbai headquarters felt like a time capsule. Founded in 1996 by Ajit Balakrishnan, Rediff was one of India's oldest internet companies—a pioneer that had somehow survived the dot-com bust, the social media revolution, and the mobile disruption, but hadn't quite thrived through any of them. In August 2024, Vishal Mehta walked into that boardroom not as a competitor but as a savior, armed with a vision that would transform both companies. In August 2024, Infibeam Avenues acquired a 54.1% stake in internet business firm Rediff.com for just INR 25 crore—roughly $3 million. For a company that had once been valued at over $600 million on Nasdaq at its peak in 2000, this was a humbling valuation. But for Infibeam, it was a strategic masterstroke.

Rediff wasn't just any acquisition. Founded in 1996, it was the first Indian internet firm to list on Nasdaq back in the year 2000. It had 55 million monthly visitors—a user base that most companies would spend hundreds of crores to acquire through marketing. For INR 25 crore, Infibeam was getting not just traffic but trust, brand recognition, and decades of user data.

The strategic rationale was brilliant. Infibeam plans to integrate its digital payment services, platform offerings, and AI solutions with Rediff.com to boost user engagement and create new revenue streams. With Rediff.com's 55 million monthly visitors, Infibeam will cross-sell financial products such as loans, insurance, and investments using AI.

But there was a deeper play here. Rediff wasn't just about its consumer traffic—it was about its enterprise services. Rediff's cloud-based enterprise email storage, instant messaging platform, and content distribution services gave Infibeam entry into spaces it hadn't touched before. This wasn't just acquiring users; it was acquiring capabilities.

Vishal Mehta, the founder of Infibeam, became the chairman and managing director of Rediff.com. This wasn't a passive investment—Mehta was taking direct control. Ajit Balakrishnan, Rediff's founder, would continue to advise, but the baton had been passed. "I am delighted to pass on this iconic brand and its legacy into the capable hands of Vishal Mehta," Balakrishnan said, with the grace of someone who knew when it was time to let go.

The financial engineering was clever. The acquisition for Rs 50 crore would be equally divided into equity and debt—Rs 25 crore for the 54% stake and Rs 25 crore as debt. This structure minimized dilution for Infibeam shareholders while giving the company control of an asset that could be leveraged across its ecosystem. But the story took an unexpected turn in August 2025. Just a year after acquiring Rediff, Infibeam sells ecommerce platform to Rediff for INR 800.39 Cr, retaining 82% stake, focusing on payments and AI. This wasn't a retreat—it was financial engineering at its most sophisticated.

The slump sale valued the platform business at ₹800.39 crore—a business that generated just ₹180 crore in revenue and contributed only 4.83% to Infibeam's topline. The deal structure was clever: ₹400 crore in cash and ₹400.39 crore via issuance of new equity shares in Rediff. Post-deal, Infibeam's stake in Rediff increased from 54% to 82%.

The strategic logic was brilliant. By transferring the platform business to Rediff, Infibeam could: 1. Focus exclusively on high-margin payments and AI businesses 2. Maintain control of the platform business through its 82% stake in Rediff 3. Create a cleaner story for investors focused on fintech pure-plays 4. Set up Rediff for a potential IPO with a more coherent business model

Rediff was also evaluating capital-raising opportunities, including a potential initial public offering (IPO). The addition of the e-commerce platform made Rediff a more complete enterprise software story—Rediffmail for enterprise email, RediffPay for payments, the e-commerce platform for digital commerce, and content for traffic generation.

The consumer financial services play through Rediff was already showing promise. The company was preparing to debut RediffPay, a UPI payments app that would mark Infibeam's entry into the consumer-facing payments market. This would complement its CCAvenue B2B payment gateway business. With 55 million monthly visitors as a captive audience for cross-selling, the potential was enormous.

The Rediff acquisition and subsequent restructuring revealed Mehta's sophistication as a capital allocator. He wasn't just buying assets—he was creating structures that maximized value while maintaining control. The failed e-commerce marketplace had been transformed into a valuable enterprise platform, which was then packaged with Rediff's consumer assets to create something neither company could have built alone.

IX. Modern Era: AI, Fintech Evolution & Future Bets

The demonstration room at Infibeam's GIFT City headquarters looked more like a scene from Minority Report than a typical fintech office. On multiple screens, real-time transaction data flowed through neural networks, flagging potential fraud with an accuracy that would have seemed impossible just years earlier. This was Phronetic.AI, Infibeam's ambitious bet that the future of payments wasn't just about processing transactions—it was about intelligence.A standout initiative is Phronetic, a pioneering Vision AI business leveraging artificial intelligence to revolutionize how organizations process visual data. Phronetic enhances operational efficiency and decision-making across industries, positioning itself as a cornerstone of AI-driven solutions and enabling businesses to unlock new possibilities through intelligent automation.

The AI strategy wasn't just about adding buzzwords to investor presentations. Phronetic.AI, launched as Infibeam's wholly-owned subsidiary, was building genuine innovation. The company's Theia Vision AI technology could transform any existing CCTV infrastructure into intelligent surveillance systems within five minutes—no hardware changes required. This wasn't theoretical—by 2024, Phronetic had secured contracts with leading hospital chains and international gas station chains, with combined contract values of $1 million per annum over five-year terms.

The vision extended far beyond simple computer vision. Infibeam was building what Mehta called an "agentic AI platform"—infrastructure that would allow anyone to build, deploy, and monetize intelligent agents without writing code. The company's Owlet vision-language models, Thea LLM for visual processing, and RZN reasoning engine formed a comprehensive AI stack that could handle everything from fraud detection to facility management.

On 7 September 2022, Infibeam Avenues launched its omni-channel mobile app CCAvenue TapPay that allows businesses and entrepreneurs to convert any NFC-enabled Android phone into smart PoS terminals. This wasn't just another payment app—it was democratization of payment acceptance. Any small merchant with an Android phone could now accept card payments without expensive POS hardware.

The competitive landscape had evolved dramatically. Razorpay, backed by Tiger Global and Sequoia, had raised over $741 million and was valued at $7.5 billion. PayU, owned by Prosus, had deep pockets and global expertise. Paytm, despite its struggles post-IPO, still dominated consumer payments through UPI. Yet Infibeam had carved out its niche: the unsexy but essential B2B infrastructure that powered enterprise payments.

The lending opportunity was particularly intriguing. Through TrustAvenue, its lending aggregation platform, Infibeam wasn't trying to become a lender itself—it was becoming the infrastructure through which lending happened. With transaction data from millions of merchants, the company could underwrite credit better than traditional banks. This wasn't competing with banks—it was enabling them.

The data center play revealed another dimension of the strategy. Infibeam provides data center-as-a-service, and built a Tier-III data center in GIFT City, Gandhinagar. This wasn't just about hosting—it was about data sovereignty. As regulations tightened around data localization, having domestic data center capabilities became a competitive advantage.

The international AI expansion showed global ambitions. In February 2024, Infibeam acquired a 20% stake in US-based AI company XDuce for $10 million. This wasn't just an investment—it was a beachhead for taking Indian AI capabilities global. XDuce's enterprise AI solutions combined with Infibeam's payment data could create unique fraud detection and risk management products for the US market.

The modern era strategy was crystallizing: become the intelligence layer for financial services. While others fought over transaction volumes and take rates, Infibeam was building the AI and infrastructure that would power the next generation of financial products. Every payment processed, every fraud detected, every loan underwritten added to the data moat that would be increasingly difficult for competitors to replicate.

X. Playbook: Business & Investing Lessons

The conference room fell silent as the young founder finished his pitch. "We're going to be the Flipkart of our category," he declared with confidence. Across the table, Vishal Mehta smiled knowingly. "Let me tell you about the time we tried to be Flipkart," he began, "and why being boring made us more money than being sexy ever could."

Lesson 1: Capital Efficiency vs. Growth - The False Dichotomy

The conventional wisdom says you must choose: either grow fast with massive capital or stay small and profitable. Infibeam proved this is false. The company grew from ₹337 crore revenue at IPO to over ₹4,500 crore while maintaining profitability. The secret? Sequential pivots that built on existing capabilities rather than moon shots that required starting from scratch.

When the e-commerce marketplace failed, the technology wasn't abandoned—it became BuildaBazaar. When BuildaBazaar struggled to scale, it pivoted to government tech. Each failure became the foundation for the next success. This is capital efficiency: not doing less, but wasting less.

Lesson 2: Platform vs. Product - The Infrastructure Advantage

Products have customers; platforms have ecosystems. CCAvenue isn't just a payment gateway—it's the rails on which thousands of businesses run. When a merchant integrates CCAvenue, switching costs aren't just technical—they're operational. Years of transaction data, reconciliation processes, and customer payment preferences create lock-in that price competition can't break.

The platform strategy extends beyond payments. BuildaBazaar for enterprises, BillAvenue for bill payments, TrustAvenue for lending—each is a platform that others build upon. The lesson: in emerging markets, own the infrastructure, not the applications.

Lesson 3: The Regulatory Moat

In 2022, when Infibeam received its payment aggregator license from the RBI, competitors dismissed it as paperwork. They missed the point. In regulated industries, licenses aren't just permission—they're barriers to entry. Every new regulation that makes compliance harder makes Infibeam's position stronger.

The company didn't just comply with regulations—it anticipated them. Building a Tier-III data center before data localization became mandatory. Getting SAMA certification in Saudi Arabia before competitors even entered the market. Regulatory foresight created competitive advantage.

Lesson 4: Building in Emerging Markets - Infrastructure Before Demand

When Infibeam launched CCAvenue in markets like Oman, digital payments barely existed. Critics said they were too early. But being early meant shaping the market rather than competing in it. By the time demand materialized, Infibeam had relationships with every major bank and thousands of merchants.

The lesson: in emerging markets, build for where the market will be, not where it is. The first-mover advantage isn't about being first—it's about being embedded in the ecosystem before it becomes an ecosystem.

Lesson 5: Why Payment Companies Are Sticky Businesses

Payments are the ultimate sticky business for three reasons: 1. Switching costs are enormous - Not just technical integration but training, process changes, and historical data migration 2. Trust takes years to build - One payment failure can destroy a merchant's business; they won't risk switching for marginal savings 3. Network effects compound - More merchants attract more payment methods, which attract more merchants

Infibeam's 75% merchant retention rate after five years proves this. Merchants might complain about fees, but they rarely leave.

Lesson 6: The Value of Being "Boring but Essential"

While the media celebrated consumer unicorns, Infibeam quietly built infrastructure that processed ₹13.60 lakh crore through GeM. No viral marketing campaigns, no celebrity endorsements, just reliable infrastructure that worked.

Being boring has advantages: - Less competition (talented engineers want to work on sexy problems) - Better unit economics (B2B customers pay for value, not entertainment) - More predictable growth (enterprises don't churm like consumers) - Higher multiples eventually (infrastructure commands premium valuations in mature markets)

The Capital Allocation Masterclass

The Rediff acquisition and restructuring was a masterclass in capital allocation: - Acquire distressed assets with hidden value (₹25 crore for 55 million users) - Inject capabilities that multiply value (payment integration, AI tools) - Financial engineering to maintain control (82% stake post-restructuring) - Set up for multiple exit options (IPO, strategic sale, or continued operation)

This wasn't financial engineering for its own sake—it was value creation through strategic combination.

The Investor's Paradox

Here's the puzzle: Infibeam processes $86 billion annually, ranks among India's top 3 payment gateways, dominates Middle East markets, yet trades at just ₹4,810 crore market cap—down 45.9% in the past year. Why?

The market struggles to value Infibeam because it doesn't fit neat categories. It's not a pure payment company like Razorpay. It's not a platform company like Salesforce. It's not an AI company like OpenAI. It's all three, which means it's valued as none.

For investors, this creates opportunity. The company trades at less than 1x revenue while growing 30%+ annually. It's profitable while competitors burn cash. It has regulatory moats while others face compliance challenges. The market's confusion is the investor's opportunity.

XI. Analysis & Bear vs. Bull Case

The numbers tell a story of transformation. Infibeam's revenue from operations flourished 51.6% to Rs 1,962 crore during the fiscal year ending March 2023 as compared to Rs 1,294 crore in FY22. The net profit after tax for FY23 was ₹136.7 crore compared to ₹83.7 crore during the previous year. In FY23, the earnings before interest, tax, depreciation and amortisation (EBITDA) increased to ₹179.6 crore from the previous year's ₹145 crore.

But beneath these headline numbers lies a more complex reality.

The Bear Case: Why the Market Is Skeptical

Market Cap: ₹4,810 Crore (down -45.9% in 1 year). Company is almost debt free. Company has a low return on equity of 5.05% over last 3 years. These metrics paint a troubling picture for momentum investors.

The bear case rests on several pillars:

-

UPI Disruption: The elephant in the room is UPI's dominance. With zero MDR (Merchant Discount Rate) on UPI transactions, payment gateways' traditional revenue model is under threat. While Infibeam processes billions, if those billions shift to UPI, what happens to revenues?

-

International Concentration Risk: The company's Middle East success is impressive but creates concentration risk. Political instability, regulatory changes, or economic downturns in the UAE or Saudi Arabia could disproportionately impact growth.

-

Technology Platform Challenges: The loss of the GeM contract renewal to TCS exposed vulnerability. If Infibeam can lose its crown jewel platform contract, what does that say about competitive positioning?

-

Corporate Governance Concerns: The complex Rediff transaction—acquiring for ₹25 crore, then selling the platform business back for ₹800 crore while maintaining control—raises questions about related party transactions and value transfer.

-

Competition from Global Giants: Stripe, Adyen, and PayPal are entering India. These players have deeper pockets, better technology, and global merchant relationships. Can Infibeam compete?

-

Low Return on Equity: At 5.05% over three years, ROE is anemic for a technology company. This suggests the company isn't efficiently using shareholder capital.

The Bull Case: Why This Could Be a Multi-Bagger

The bull case is equally compelling:

-

Misunderstood Business Model: The market values Infibeam like a payment gateway, missing the platform and AI businesses. The company made 91.4% of its total operating revenue via its payment gateway and infrastructure business, which grew 58% to Rs 1,793 crore during FY23. But this includes high-margin platform revenues that deserve higher multiples.

-

The AI Opportunity: Phronetic.AI isn't vaporware. With real contracts worth $1 million annually from hospitals and gas stations, the AI business could be worth more than the current market cap if valued like pure-play AI companies.

-

Hidden Asset Value: Rediff's 55 million monthly visitors, enterprise email clients including ICICI Bank and HDFC Life, and potential IPO create unrecognized value. The 82% stake in Rediff alone could be worth ₹2,000+ crore post-IPO.

-

Regulatory Moats Deepening: As regulations tighten, smaller players will struggle with compliance costs. Infibeam's licenses in India, UAE, and Saudi Arabia become more valuable as barriers to entry rise.

-

Cross-Selling Opportunity: With 10 million merchants and 55 million Rediff users, the lending and insurance cross-sell opportunity is massive. Even 1% penetration at ₹10,000 average ticket would generate ₹1,000 crore in loan disbursements.

-

International Growth Runway: International business contributed less than 10% to Infibeam Avenues Ltd's total revenue and we plan to grow international business to 30% of total revenue in the next couple of years. At current growth rates, international revenue could exceed ₹1,500 crore by FY26.

Financial Projections & Valuation

Infibeam Avenues reported a 18.3% jump in its consolidated profit after tax to INR 54.7 Cr in Q4 FY25 from INR 46.2 Cr in Q4 FY24. In Q4 FY25, the company clocked INR 2.41 Lakh Cr in transaction processing value (TPV), up 7% from INR 2.26 Lakh Cr in the year-ago quarter. Alongside, payments net take rate or NTR (net earnings per transaction) improved 16% to 10.6 basis points (bps) in the quarter under review from 9.2 bps in the year-ago period.

If we project forward: - TPV growing at 25% CAGR reaches ₹6 lakh crore by FY27 - Net take rate expanding to 12 bps (still below industry average of 15-20 bps) - Revenue reaches ₹7,200 crore - At 25% EBITDA margins, EBITDA of ₹1,800 crore - At 15x EV/EBITDA (discount to global payment companies at 20-25x), enterprise value of ₹27,000 crore

This suggests 5-6x upside from current levels—if execution delivers.

The Verdict: Asymmetric Risk-Reward

The bear case is real: UPI disruption, competition, and governance concerns are legitimate risks. But at current valuations, much of this is priced in. The company trades at: - 1x revenue (vs. 3-5x for payment companies) - 25x P/E (vs. 40-50x for profitable tech companies) - Below book value when adjusting for Rediff stake

For long-term investors, Infibeam presents asymmetric risk-reward. The downside is limited—the company is profitable, debt-free, and growing. The upside is substantial if any of the following materialize: - AI business gains traction - International expansion accelerates - Rediff IPO unlocks value - Cross-selling drives new revenue streams

The market's skepticism has created opportunity. Sometimes the best investments are in companies the market doesn't understand. Infibeam might be one of them.

XII. Epilogue & "If We Were CEOs"

As 2025 unfolds, Infibeam stands at an inflection point. The company that failed at e-commerce, pivoted to payments, expanded internationally, and now pioneers AI has proven its adaptability. But what comes next?

Recent developments suggest accelerating momentum. The rights issue of ₹700 crore, oversubscribed 1.4x, provides war chest for AI investments. The Rediff restructuring creates cleaner equity story for different investor bases. The Phronetic.AI contracts validate the technology. Yet the stock languishes, creating a fascinating disconnect between operational progress and market perception.

If we were CEO, here's what we'd do:

1. Create Tracking Stocks or Spin-offs The conglomerate discount is real. Infibeam is valued less than the sum of its parts because investors can't properly value disparate businesses. Create three distinct entities: - Infibeam Payments: Pure-play payment infrastructure (CCAvenue, BillAvenue) - Infibeam Platforms: Enterprise software and government tech (BuildaBazaar) - Phronetic.AI: AI and data services

Each would command category-appropriate multiples.

2. Double Down on Embedded Finance With transaction data from millions of merchants, Infibeam should become the infrastructure layer for embedded finance. Don't compete with banks—enable them. White-label lending, insurance, and wealth products that banks can offer through Infibeam's pipes.

3. Build the India Stack for Other Markets India's digital public infrastructure (Aadhaar, UPI, GST) is being replicated globally. Infibeam should package its experience running GeM and payment infrastructure into turnkey solutions for emerging market governments.

4. Acquire Distressed Assets Aggressively The Rediff playbook works. Identify undervalued digital assets with user bases or capabilities that multiply value when combined with Infibeam's infrastructure. Roll them up, integrate payments and AI, unlock value.

5. Create Developer Ecosystem Stripe's valuation comes from developers loving their APIs. Infibeam should invest heavily in developer experience, documentation, and tools. Make CCAvenue the default choice for Indian developers.

The Future of Payments in India

The payments landscape is evolving rapidly. Central Bank Digital Currency (CBDC) trials are underway. Blockchain-based cross-border payments are gaining traction. Embedded finance is exploding. AI is transforming fraud detection and risk management.

Infibeam is positioned at the intersection of these trends. Its payment infrastructure processes transactions. Its AI detects fraud. Its platform enables embedded finance. Its government relationships position it for CBDC infrastructure.

The biggest surprise in researching this story? How a company that failed at its original vision became essential infrastructure for India's digital economy. Infibeam's journey from failed e-commerce marketplace to payment infrastructure giant offers profound lessons:

For Founders: Sometimes the best businesses emerge from failed attempts at sexier ones. The capabilities you build while failing become the foundation for eventual success.

For Investors: The market's inability to properly categorize complex businesses creates opportunity. Companies that don't fit neat boxes often trade at discounts to intrinsic value.

For India: The country needs more Infibeams—companies that build boring but essential infrastructure. Not every startup needs to be a unicorn. Sometimes being a workhorse that processes billions reliably is more valuable than being a show horse that attracts headlines.

XIII. Outro & Links

As we close this deep dive into Infibeam Avenues, it's worth reflecting on what makes this story unique in the pantheon of Indian tech companies. This isn't a story of blitzscaling to unicorn status. It's not about disrupting industries or creating new consumer behaviors. It's about something rarer and perhaps more valuable: building essential infrastructure that others depend upon.

Infibeam's journey reminds us that in the rush to celebrate the visible—the consumer apps we use daily—we often overlook the invisible infrastructure that makes everything possible. Every UPI payment, every government procurement, every cross-border transaction flows through infrastructure built by companies like Infibeam.

The company's story is far from over. As India's digital economy grows from $1 trillion to potentially $5 trillion by 2030, the infrastructure processing these transactions becomes exponentially more valuable. Whether Infibeam captures this value for shareholders remains to be seen. But what's certain is that the company has already played a crucial role in building India's digital economy—even if most Indians have never heard of it.

For those interested in diving deeper, key resources include: - Infibeam Avenues investor presentations (quarterly updates on ia.ooo) - RBI payment aggregator regulations and compliance requirements - McKinsey Global Payments Report for industry context - GeM portal statistics for government procurement trends - Middle East payment market reports from SAMA and UAE Central Bank

The Infibeam story teaches us that sometimes the best businesses are hiding in plain sight, processing billions in transactions while everyone else chases the next hot thing. In a world obsessed with disruption, there's value in building the rails on which disruption runs.

XIV. Recent News

Recent developments continue to reshape the Infibeam narrative:

August 2025: Infibeam Avenues Limited's board approve a Business Transfer Agreement (BTA) with Rediff.com India Limited to divest its Platform Business Undertaking through a slump sale. The deal, valued at ₹800.39 crore, will see Infibeam transfer its Ecommerce Platform Technology Infrastructure business to Rediff, while holding an 82% stake in the company after this transaction.

Q1 FY26 Results: 72% revenue growth year-over-year, demonstrating accelerating momentum despite broader market challenges.

AI Traction: Phronetic.AI secures multiple enterprise contracts, validating the AI strategy with real revenue rather than just promises.

International Expansion: Continued growth in Middle East markets, with Saudi Arabia operations scaling rapidly post-SAMA certification.

The story of Infibeam Avenues is ultimately about the value of patience, persistence, and pivoting intelligently. In a market that rewards growth over profitability and hype over substance, Infibeam chose a different path. Whether that path leads to eventual recognition by the market remains to be seen. But for those willing to look beyond the noise, Infibeam represents something increasingly rare: a profitable, growing, essential business trading at a discount to intrinsic value.

The infrastructure builders rarely get the glory. But they often get the returns.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube