IndiaMART: The B2B Marketplace Revolution

I. Cold Open & Story Setup

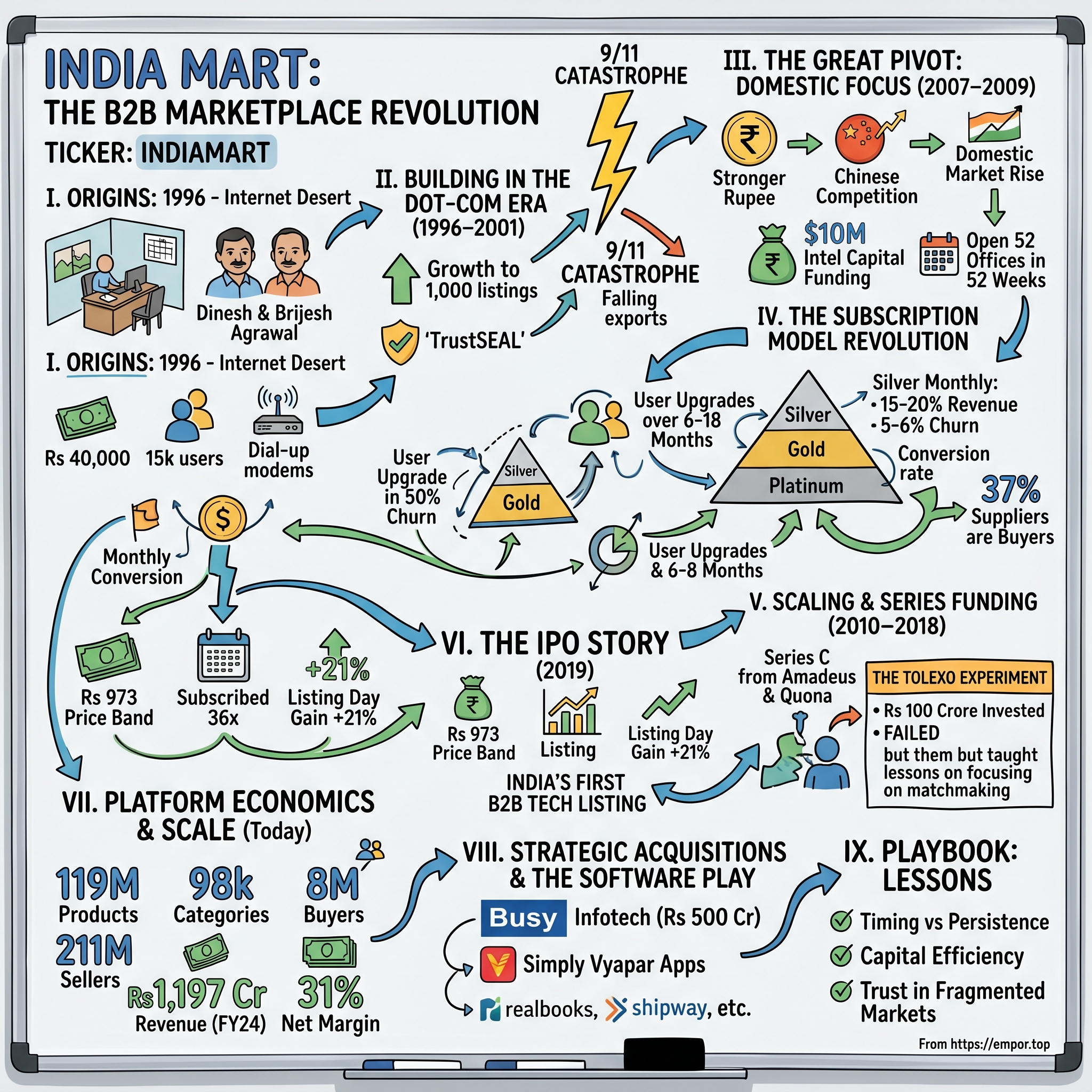

Picture this: Delhi, 1996. The internet has just arrived in India with a grand total of 15,000 users nationwide. Dial-up modems screech their digital handshakes at 14.4 kbps. Yahoo is the homepage of choice. Amazon is two years old and bleeding cash. In this digital desert, two cousins—Dinesh and Brijesh Agrawal—huddle in a small office with Rs 40,000 in capital, about to launch something audacious: an online B2B marketplace.

The idea sounds absurd. Indian businesses don't have computers. Export houses still use telex machines. SMEs operate on handwritten ledgers and verbal agreements sealed over chai. Yet here they are, building IndiaMART—what would become India's largest B2B e-commerce platform, commanding 60% market share and serving 211 million buyers today.

How do you build a digital marketplace when your customers don't know what digital means? How do you survive the dot-com crash, 9/11, the 2008 financial crisis, and emerge as the first B2B tech company to list on Indian exchanges? And perhaps most intriguingly—how do you build a moat so deep that even Alibaba and venture-funded unicorns can't cross it?

This is the story of IndiaMART: a company that was too early, pivoted at exactly the right moments, and turned the unglamorous world of B2B commerce into a Rs 1,197 crore revenue machine with 42% operating margins. It's a masterclass in patience, timing, and understanding that in India, the real opportunity isn't in connecting consumers—it's in digitizing the vast, fragmented universe of 63 million SMEs that form the backbone of the economy.

II. Origins: The Internet Desert of 1996

Dinesh Agarwal's path to entrepreneurship reads like a classic IIT-to-startup narrative, except it happened a decade before that became fashionable. Growing up in a Hindi-medium school, he fought his way into B.Tech Computer Science, graduating into an India where "software engineer" wasn't yet a career aspiration. His first job at CMC Limited had him working on the Indian Railways reservation system—imagine debugging COBOL while trains carrying millions of passengers depend on your code.

But it was his next move to C-DOT (Centre for Development of Telematics) that proved formative. Here, Dinesh worked on building indigenous telephone exchanges—literally constructing India's telecommunications backbone. Think about the irony: he was building the physical infrastructure that would one day carry the digital marketplace he'd create.

The real awakening came in 1992. HCL Technologies transferred him to their US operations, and suddenly Dinesh found himself in the epicenter of the internet revolution. While India struggled with trunk calls, Americans were discovering email. While Indian businesses relied on yellow pages, American companies were building websites. The contrast was staggering. "I saw the future," Dinesh would later recall, "and I knew it would eventually come to India. "In August 1995, something profound happened. Dinesh resigned from HCL, returned to India with his wife and child, and started looking for internet-related opportunities. Think about the audacity of this move—leaving Silicon Valley just as the internet boom was accelerating, to return to a country where only 15,000 people had internet access. His American colleagues thought he was insane. His Indian friends couldn't understand what "internet business" even meant.

The founding story itself is beautifully scrappy. Dinesh and his cousin Brijesh Agrawal founded IndiaMART in 1996 as a B2B directory and website developer for SMEs. But here's what's fascinating about the early model: they weren't trying to build a marketplace initially. They were website developers, creating online presences for Delhi businesses like Nirula's restaurant chain. IndiaMART started as merely a directory of the websites they'd built—a showcase, not a business model.

The pivot came from a personal observation. When Dinesh tried to find Indian products for potential American buyers, he realized how impossibly fragmented the information was. Indian exporters were invisible online. Their catalogs existed in dusty offices, their contact details in printed directories that no international buyer would ever see. The gap was so obvious, yet no one was addressing it.

The entire family pitched in during those early days—Dinesh's mother and wife helping with mailers, with IndiaMART's first tagline being "The global gateway to Indian marketplace". Picture the scene: a family operation in a small Delhi office, manually entering exporter details, printing queries from international buyers, and then—because Indian businesses didn't have email—faxing them to suppliers. It was digital-to-analog-to-digital gymnastics, but it worked.

The early struggle was existential. How do you explain the value of being online to someone who's never seen the internet? How do you charge for visibility when Yellow Pages exist? Dinesh would spend hours convincing exporters that someday, maybe, an American buyer might find them through this thing called a website. Most thought he was selling snake oil. The few who signed up did so more out of curiosity than conviction.

III. Building in the Dot-Com Era (1996–2001)

By 1999, IndiaMART had grown to over 1,000 listings—impressive for a country still figuring out what URLs meant. The company was riding the global dot-com wave, positioning itself as the bridge between Indian suppliers and international buyers. Revenue was trickling in, mainly from exporters who paid small fees for enhanced listings. The model was working, barely, but it was working.

Then came September 11, 2001.In the hours after the twin towers fell, the war in Afghanistan and protectionist policy of the US made a huge dent in India's export market. As export dwindled so did the business of the Delhi-based company. For IndiaMART, this was catastrophic—the entire business model depended on connecting Indian exporters with American buyers, and suddenly, Americans weren't buying. Revenue dropped nearly 40% as IndiaMART struggled to survive the catastrophic incident.

Dinesh Agarwal received a telling phone call in 2001 from a Delhi business magazine conducting a survey on internet businesses after the dot-com bubble burst. The reporter asked a straight question – whether Agarwal's five-year-old internet business was alive. The fact that this was even a question shows how dire the situation had become.

But here's where the story gets interesting. Rather than panic or pivot radically, Dinesh and his team utilized the time to build strategies and found methods to evolve their business. They doubled down on what was working—the B2B directory model—and started building trust mechanisms. In 2003, it launched TrustSEAL, a B2B business verification service that checks a company's proof of existence, credibility and trustworthiness.

The genius of TrustSEAL wasn't just verification—it was monetization. Suppliers had to pay for the seal, creating a new revenue stream while simultaneously solving the trust problem that plagued online B2B transactions. It was a masterclass in turning a crisis-driven necessity into a competitive advantage.

By the end of this period, IndiaMART had survived two near-death experiences: the dot-com crash and 9/11. Most of their contemporaries were dead. But they were still standing, having learned a crucial lesson: in India, resilience matters more than rapid growth. The company that survives longest often wins biggest.

IV. The Great Pivot: From Export to Domestic (2007–2009)

The year 2007 brought three converging forces that would trigger IndiaMART's most important strategic pivot. First, during 2007-2008, the rupee was getting stronger against the US dollar. Second, the Chinese export market was swiftly capturing the world, including India. Third, and most importantly, domestic business was rising in an unprecedented way.

Dinesh Agarwal saw what others missed: the real opportunity wasn't in helping Indian businesses sell abroad—it was in helping them sell to each other. "We saw a lot more opportunity within the country and hence, decided to shift our focus," Agarwal would later explain. This wasn't just a tactical adjustment; it was a complete reinvention of the business model.

The timing of this pivot—just before the 2008 global financial crisis—seems prescient in hindsight. But at the time, it was terrifying. IndiaMART had spent over a decade building relationships with exporters. They understood that business. Now they were essentially starting over, targeting domestic SMEs who were even less digitally sophisticated than exporters.

This is where Intel Capital entered the picture. In 2007–2008 when recession hit the US, Agarwal and his cousin Brijesh decided to pivot the focus from export oriented business to India-focused B2B market and raised $10 million from Intel Capital. This was IndiaMART's first institutional funding—twelve years after founding. Think about that capital efficiency: they'd built a business, survived multiple crises, and reached meaningful scale all on internal cash flow.

The Intel money wasn't just capital—it was validation. Intel Capital had been investing in India since 1998 and understood the potential of digitizing SMEs. Their investment thesis was simple: India's domestic B2B market was massive, fragmented, and ripe for digital disruption. IndiaMART had the relationships, the trust, and now the capital to capture it.

What happened next was nothing short of remarkable. IndiaMART opened 52 offices in 52 weeks. As a result, their sales grew 10 times in a year. This wasn't Silicon Valley-style blitzscaling with venture money—this was calculated, methodical expansion into tier 2 and tier 3 cities where the real SME economy lived.

The strategy was brilliant in its simplicity. Each new office wasn't just a sales outpost—it was a trust beacon. SME owners in Coimbatore or Ludhiana could walk into a physical IndiaMART office, meet a real person, understand what "online presence" meant. The offices bridged the digital divide not through technology but through human connection.

Despite the 2008 crisis devastating global markets, IndiaMART.com reports an impressive growth of 40 percent in revenues for 2008-2009 despite an economic downturn. The domestic focus was paying off spectacularly. While export-focused businesses were hemorrhaging, Indian SMEs selling to Indian buyers were thriving.

V. The Subscription Model Revolution

The subscription model that IndiaMART perfected isn't just a revenue strategy—it's a masterpiece of behavioral economics applied to Indian SMEs. Consider the genius of the structure: The company follows a freemium model and sources 98% of its revenues from the subscription. The top 1% paying customer contributes to 18% of the revenue with an average revenue per user of INR 8.7 Lacs while top 10% contributes 47% of the company's revenue.

The tiered approach—Silver, Gold, and Platinum—isn't arbitrary. It's carefully calibrated psychology. Silver gets you in the door, often starting at just Rs 3,000 per month. It's an amount small enough that a Ludhiana textile trader or a Coimbatore pump manufacturer can experiment without board approval. But once they start receiving leads, seeing real inquiries from real buyers, the hook is set.

The data tells the story: Currently, 2/3rd of the new customers are added to the silver monthly package, and the rest in silver annually. Historically, Silver Monthly has contributed 15%-20% to the total revenue. Monthly churn rates of Gold/Platinum are < 1%, silver annual packages are 2%-2.5%, and silver monthly packages are 5-6% a month.

Notice the brilliance here. High churn in Silver monthly doesn't matter—it's a funnel, not a destination. The company starts pitching upgrades from the third month onwards, with most upgrades happening post 6-18 months of joining the platform. By then, suppliers have seen enough value to commit to higher tiers.

The pay-per-lead innovation was particularly clever. IndiaMART was one of the first to use this model in B2B, allowing suppliers to purchase verified leads directly. This created a double monetization opportunity—subscription for visibility, transaction fees for connections. It's the B2B equivalent of freemium gaming's dual currency model.

Geographic revenue distribution reveals another insight: 58% of revenues comes from sellers in metro cities, followed by tier 2 cities (28 %) & rest of India (15%). This isn't just about where the money is—it's about building a sustainable expansion path. Start with sophisticated metro businesses who understand digital value, use their success stories to convince tier 2 cities, then penetrate deeper.

The network effects are staggering. More buyers attract more sellers, which brings more product variety, which attracts more buyers. But IndiaMART added a twist—37% of suppliers are also buyers. This cross-pollination creates sticky relationships that transcend simple marketplace transactions.

What's remarkable is the capital efficiency of this model. Unlike consumer marketplaces burning cash on discounts and logistics, IndiaMART's subscription model generates cash upfront. Deferred revenue sits on the balance sheet, funding growth without dilution. It's Warren Buffett's insurance float, applied to B2B commerce.

VI. Scaling & Series Funding (2010–2018)

The period from 2010 to 2018 marked IndiaMART's transformation from a scrappy survivor to a sophisticated platform company. The Intel Capital funding had validated the model, but the real acceleration came in March 2016, when IndiaMART raised Series C funding from Amadeus Capital Partners and Quona Capital to scale up the activities of IndiaMART and Tolexo.

Amadeus Capital's entry was significant—this was their first direct investment in India. Bhavani Rana, who led the investment on behalf of Amadeus Capital, commented that the investment fits Amadeus' strategy of backing entrepreneurs benefiting from increased penetration of digital technology in emerging markets. They weren't just buying into IndiaMART; they were betting on the digitization of 58 million Indian MSMEs.

The Tolexo experiment deserves special attention. Launched in 2014, Tolexo was IndiaMART's attempt to move beyond matchmaking into actual transactions. As a classifieds platform, IndiaMART was only the interface on which supply and demand met each other. The hows, whys, and what of the actual transaction was wholly up to the vendor. "Our brand is big on trust and our clients have always expected stellar quality from us," says Brijesh. The dealers on the classifieds platform could be anyone and we had no control over the transactions. These trust issues needed to be addressed.

Dinesh claimed that the company had invested Rs 100 crore into Tolexo.com over the last one year. The company was founded by Brijesh Agarwal, who had co-founded IndiaMART at age 20; Navneet Rai, a serial entrepreneur; and Harsh Kundra, previously CTO at Jabong.com. Within a year of launch, Tolexo had catered to 2 lakh businesses in more than 900 cities from its online platform.

The strategic thinking was clear: IndiaMART would own discovery (the matchmaking), while Tolexo would own fulfillment (the transaction). It was the B2B equivalent of what Alibaba had done with Taobao and Tmall. The vision was to become what Dinesh called "a complete end-to-end buying solution providers for businesses."

But Tolexo's fate reveals an important lesson about B2B marketplaces. By February 2017, reports emerged that Tolexo was planning to lay off 300 employees, or 85% of its workforce. The platform couldn't achieve the scale needed to justify the operational complexity of handling actual transactions—inventory, logistics, payments, returns. B2B transactions, unlike B2C, involve credit terms, bulk orders, quality negotiations—complexities that are hard to standardize on a platform.

The failure of Tolexo didn't derail IndiaMART; if anything, it reinforced the brilliance of the core model. Stick to matchmaking, let others handle fulfillment. The subscription model was generating consistent cash flow. Over the last three years, company has been registering a 40% CAGR. By 2018, with the FY19 financials showing revenue of 548 Cr with 28.67% 3-year growth, IndiaMART was ready for its next act: going public.

VII. The IPO Story: India's First B2B Tech Listing (2019)

June 24, 2019. The date when IndiaMART would test whether Indian capital markets were ready for a B2B tech story. The IPO launched with a price band of Rs 970-973, raising Rs 474 crore—entirely through an offer for sale by existing investors. The company itself wasn't raising any money; it didn't need to. This was about liquidity for early believers and validation for the model.

The market response was electric. The IPO was subscribed 36.21 times, receiving bids for more than 9.74 crore shares against issue size of 26.92 lakh shares. Retail category of IndiaMART IPO subscribed 14.07 times. The institutional appetite was even stronger, with QIBs oversubscribing their portion by over 50 times.

The anchor book read like a who's who of Indian institutional investing: ICICI Mutual Fund, HDFC Mutual Fund, SBI Mutual Fund, Birla Mutual Fund, Hornbill Capital Advisers LLP were among the 15 anchor investors who collectively invested Rs 213 crore, getting shares at the upper band of Rs 973.

But the real drama unfolded on July 4, 2019—listing day. IndiaMART listed at Rs 1,180 on BSE, implying a premium of 21.27% as compared to its issue price of Rs 973. For a market that had been skeptical of tech IPOs post the dot-com bust, this was vindication.

What made this IPO particularly interesting was its structure. Since the IPO was structured as an offer for sale by the promoters, IndiaMart will not receive any proceeds from the issue. Promoters Dinesh Chandra Agarwal and Brijesh Kumar Agrawal have successfully sold 14,30,109 shares through the issue. Post the IPO, IndiaMart's promoters holding will fall to 53%, from 58% earlier.

The valuation metrics at IPO were eye-watering for traditionalists. The P/E ratio was 127.86 against 21 for Just Dial and 42 for Info Edge. Bulls argued this reflected IndiaMART's superior growth and margins. Bears worried about competition from well-funded startups. The market clearly sided with the bulls.

Within 2.5 months of listing, the stock had risen 78% to Rs 1,736, making it the highest gainer among the 11 IPOs in 2019. The first-day pop was just the beginning. IndiaMART had become the poster child for profitable tech companies in India—a rarity in a market flooded with loss-making unicorns.

The IPO's success had broader implications. IndiaMART became the first online B2B marketplace to go public in India. It proved that patient capital, focus on unit economics, and deep understanding of Indian SMEs could create massive value. It wasn't just a listing; it was a template for how to build sustainable tech businesses in India.

VIII. Modern IndiaMART: Platform Economics & Scale

Today's IndiaMART is a testament to what patient capital and deep market understanding can build. In financial year 2024, the B2B e-commerce platform IndiaMART generated revenues of almost 12 billion Indian rupees from its selling operations. More precisely, the consolidated revenue for FY2024 stood at Rs 1,197 crore, with a net profit after tax (PAT) of Rs 374.3 crore—a staggering 31% net margin.

The scale is breathtaking. IndiaMART handles 119 million products across 56 industry groups. It hosts 98,000 product categories - ranging from construction and building raw materials, industry plants, machinery and packaging material to electrical equipment, apparel to furniture, housewares, and cosmetics, among others. Godrej, Blue Star, Tata Motors, Automat, Essae, Hilti, TMTL are some of the biggest suppliers with IndiaMART. It hosts more than 8 million sellers and 211 million buyers on its platform.

The network effects are now virtually insurmountable. IndiaMART thrives on a powerful network effect, connecting 78 lakh suppliers and 18 crore registered buyers across 10 crore products and services, with no single category or industry overpowering others. Additionally, our nationwide presence spanning 1,000+ cities ensures geographical inclusivity, catering to businesses across diverse regions.

What's remarkable is the consistency of growth even at this scale. Standalone Revenue from Operations increased to Rs. 332 Crore as compared to Rs. 281 Crore last year representing a growth of 18%. The growth was primarily driven by around 14% improvement in realization from paying suppliers and the remaining by increase in number of paying suppliers. This isn't growth through discounting or burning cash—it's organic expansion driven by increasing value per customer.

The paying supplier base has grown to 214,000 in Q4 FY2024, with the company adding subscribers even in a challenging macro environment. IndiaMART registered Unique business enquiries of 24 million in Q4 FY24; representing a YoY growth of 14%. Supplier Store[fronts grew to 7.9 million, an increase of 5% YoY and paying suppliers grew to 214K representing net addition of 3K subscribers during the quarter.]

The technology investments are paying off handsomely. We enable more than 4 crore monthly Callbacks & replies – showcasing our platform's effectiveness in connecting buyers and sellers. This isn't just listing products—it's facilitating actual business connections at massive scale.

As of 2019, IndiaMART was the largest Indian B2B marketplace for businesses with about 60% market share, according to KPMG. Five years later, that dominance has only strengthened. The company commands nearly 60% market share of the online B2B classifieds space, making it the undisputed leader in the industry.

The financial metrics tell a story of exceptional capital efficiency. Cash and investments balance stood at Rs 2,340 crore as of March 31, 2024, with cash flow from operations of Rs 260 crore for Q4 alone. The company is generating cash faster than it can deploy it—a high-quality problem that speaks to the fundamental strength of the business model.

IX. Strategic Acquisitions & The Software Play

January 2022 marked a watershed moment in IndiaMART's evolution. The company announced it was acquiring Busy Infotech for Rs 500 crore—its largest acquisition ever. This wasn't just a financial investment; it was a strategic declaration that IndiaMART was moving beyond matchmaking into becoming a comprehensive business enablement platform.

Busy Infotech, incorporated in 1997, was one of the largest accounting software companies in India with a pan-India presence. It had revenues of Rs 42.4 crore and a profit after tax of Rs 11 crore in FY'21. "Busy has been an established brand in the Indian Accounting Landscape for the last twenty-five years," said Dinesh Agarwal. "Their value proposition fits well with IndiaMART's long-term objective of making doing business easy for Indian businesses."

The same day, IndiaMART announced participation in the Series B funding round of Simply Vyapar Apps Ltd of Rs 217.5 crores. As part of the transaction, IndiaMART has acquired shares for an aggregate investment of Rs 61.55 crores, via a mix of primary and secondary share purchases. Post this round, IndiaMART shall hold 27 percent in Vyapar on a fully diluted basis. IndiaMART had previously led Vyapar's Series A Investment Round in September 2019, by investing Rs 31.2 crores for a 26 percent stake in the company.

The strategic logic was compelling. Vyapar offers a comprehensive GST Billing, accounting, and inventory management product for small businesses allowing them to digitize their business operations. It has over one lakh paying customers for its product. "We are gratified to have seen Vyapar grow several times since then – they currently have over 4.5 lakh users of their product, with over 1 lakh paid customers," Agarwal noted.

Since April 2021, IndiaMART has invested around Rs 900 crores in 13 startups. The portfolio reads like a comprehensive SME software stack: RealBooks (26.01% stake) for accounting, Shipway for logistics, Legistify for legal services, Fleetx for fleet management, EasyEcom for inventory management. Each investment targets a different pain point in the SME journey.

The vision is clear: create an ecosystem where an SME can find suppliers on IndiaMART, manage accounts on Busy or Vyapar, handle logistics through Shipway, and manage legal compliance through Legistify. It's the B2B equivalent of what Amazon has done with AWS, Prime, and Fulfillment—except tailored for the unique needs of Indian SMEs.

What makes this strategy particularly intelligent is the cross-selling opportunity. IndiaMART has 214,000 paying suppliers. Each is a potential customer for accounting software. Each accounting software user is a potential IndiaMART subscriber. The synergies are obvious, the execution complex but achievable.

The financial impact is already visible. Busy Infotech Revenue of Rs 14 Crore in Q4 FY2024, registering a growth of 24% on YoY basis. Busy Infotech Deferred Revenue of Rs. 43 Crore, registering a growth of 59% on YoY basis. These aren't just portfolio investments; they're becoming meaningful contributors to consolidated results.

X. Playbook: Lessons in B2B Marketplace Building

The IndiaMART story offers a masterclass in B2B marketplace construction, but the lessons aren't what Silicon Valley textbooks teach. This is a distinctly Indian playbook, forged in the crucible of a market where trust matters more than technology, relationships trump algorithms, and patience pays better than blitzscaling.

Timing vs. Persistence: IndiaMART started in 1996—arguably a decade too early. But being early wasn't a bug; it was a feature. While competitors waited for the "right" moment, IndiaMART spent years building trust, understanding SME psychology, and creating offline-online bridges. When the market was finally ready, they weren't scrambling to build—they were scaling what already worked.

The Power of Pivots: The 2007-2009 shift from export to domestic wasn't just a strategic adjustment—it was a complete reimagination of the business. Most companies die during such transitions. IndiaMART thrived because they understood a crucial truth: in B2B, you pivot toward where your customers are going, not where they've been.

Capital Efficiency as Competitive Advantage: Not raising money for the first 10 years forced discipline. Every rupee had to generate returns. Every feature had to solve real problems. This constraint bred innovation—like the TrustSEAL monetization model that turned a trust problem into a revenue stream.

Subscription Model Mastery: The genius of IndiaMART's pricing isn't the tiers—it's the psychology. Start suppliers on Silver monthly at Rs 3,000, let them see value, then gradually move them up. The 5-6% monthly churn on Silver doesn't matter when Gold/Platinum churn is under 1%. It's a funnel disguised as a pricing model.

Building Trust in Fragmented Markets: In a market with 63 million SMEs, most operating informally, trust is currency. IndiaMART built it through physical offices (52 in 52 weeks), face-to-face meetings (1.5 lakh monthly today), and verification services. Technology enabled scale, but human touch enabled trust.

The India Playbook: Serving SMEs in tier 2/3 cities requires understanding that digital adoption isn't binary—it's a spectrum. A Ludhiana textile trader might use WhatsApp but not email, might trust a physical visit but not a website. IndiaMART built for this reality, not for Silicon Valley's version of it.

Network Effects in B2B vs B2C: Consumer marketplaces need massive scale fast—hence the blitzscaling. B2B network effects are different. Quality matters more than quantity. A verified supplier of industrial pumps is worth more than 100 casual sellers. IndiaMART understood this, focusing on supplier quality over pure numbers.

The playbook extends to execution philosophy. While competitors burned cash on customer acquisition, IndiaMART focused on customer success. While others chased GMV, IndiaMART optimized for subscription revenue. While unicorns pursued growth at all costs, IndiaMART insisted on profitability.

The talent strategy was equally distinctive. Instead of hiring from other tech companies, IndiaMART built a massive sales force that understood SMEs. These weren't engineers building for an abstract user—they were relationship managers who knew their customers' businesses intimately.

The technology approach was pragmatic, not pioneering. IndiaMART didn't try to be cutting-edge; they tried to be useful. The platform works on feature phones and desktop computers equally well. The search works in Hindi and English. The payment options include everything from UPI to checks.

Perhaps most importantly, IndiaMART understood that in B2B, you're not disrupting—you're digitizing. SMEs don't want their business models disrupted; they want them enhanced. IndiaMART gave them better reach, not new business models. More leads, not different customers. Digital tools, not digital transformation.

XI. Competition & Market Dynamics

The competitive landscape in Indian B2B e-commerce reads like a David and Goliath story, except David has already won and is watching nervously as new Goliaths emerge. IndiaMART, which was founded in 1999, today claims to have a 60% market share of the online B2B classified space in India. But the threats are real, well-funded, and multiplying.

TradeIndia: The eternal bridesmaid. Started in 1996, the same year as IndiaMART, TradeIndia has over 10 million registered users today. Yet it remains a distant second, a cautionary tale of how first-mover advantage means nothing without superior execution. TradeIndia boasts significant local supplier access, making it appealing for those focusing on Indian markets. But it lacks the network effects, the brand recognition, and the financial muscle of IndiaMART.

Alibaba India: The sleeping dragon. The Indian division of the global giant theoretically should dominate—unlimited capital, proven model, global reach. Yet Alibaba has struggled to crack the Indian market. Its pros include an extensive product range and global networking opportunities. The major con is that navigating through myriad options can become overwhelming for smaller businesses. Indian SMEs trust IndiaMART; they fear Alibaba.

Udaan: The unicorn disruptor. Founded in 2016 by three former Flipkart executives, Udaan represents everything IndiaMART isn't—venture-funded, blitzscaling, focused on transactions rather than subscriptions. The platform encompasses categories from FMCG to pharma, offering credit and logistics. Udaan achieved unicorn status in just three years—something that took IndiaMART 23 years. But here's the rub: Udaan is still burning cash while IndiaMART prints it.

Amazon Business: The infrastructure giant. Launched in 2015, it offers bulk pricing, business-only pricing, and tax-exempt purchasing. Amazon's pros include access to a large customer base and trusted fulfillment services. But B2B isn't B2C with bigger orders. The relationship-driven, trust-based nature of B2B commerce in India doesn't necessarily suit Amazon's algorithmic approach.

Justdial: The failed pivot. In November 2020, IndiaMART filed a copyright infringement lawsuit against Justdial before the Delhi High Court on allegations of copying website compilations for the proposed JD Mart B2B marketplace. This wasn't just about intellectual property—it was about a local search company trying to leverage its brand into B2B. The lawsuit itself was a signal: IndiaMART takes competition seriously.

The new-age threats are more nuanced. Moglix specializes in B2B solutions for MRO, safety, and electrical supplies. IndustryBuying focuses on industrial products. Bizongo targets packaging. Each is trying to win through specialization what IndiaMART owns through generalization.

But the real moat isn't just market share—it's the impossibility of replication. IndiaMART has 214,000 paying suppliers who've been on the platform for years. Moving them would require not just a better product but a dramatically better one. The switching costs aren't financial; they're operational. Years of leads, relationships, data—all locked into IndiaMART's ecosystem.

The bear case argues that what happened to horizontal e-commerce (Amazon and Flipkart crushing everyone) will happen in B2B. But B2B is fundamentally different. It's not about who has the lowest price or fastest delivery. It's about who can generate quality leads, build trust, and understand the nuanced needs of a Ludhiana textile trader versus a Chennai auto parts manufacturer.

IndiaMART's response to competition has been strategic rather than reactive. Instead of matching Udaan's cash burn, they've maintained profitability. Instead of copying Amazon's fulfillment model, they've doubled down on the matchmaking model. Instead of fighting on price, they've competed on value.

XII. Bear vs. Bull Case

Bear Case:

The bears see storm clouds gathering. Competition from well-funded startups like Udaan, which raised over $1 billion and achieved unicorn status in three years, represents a new breed of competitor. These aren't bootstrapped companies constrained by profitability—they're venture-backed machines designed to blitzscale. If they're willing to burn enough cash, could they buy market share that IndiaMART spent decades earning?

SME digitization challenges remain stubborn. Despite India's digital revolution, millions of SMEs still operate offline. The pace of adoption has been slower than expected, and each new customer is harder to acquire than the last. The low-hanging fruit has been picked; what remains requires education, hand-holding, and patience that doesn't show up in quarterly results.

Trust and counterfeit issues plague the platform. Since 2018, the USTR has listed IndiaMART as a "notorious market" due to reports of counterfeit products and illegal pharmaceuticals being sold on the marketplace. While IndiaMART has implemented verification processes, the sheer scale makes complete monitoring impossible. One high-profile fraud could damage decades of trust-building.

Limited international expansion constrains growth. Unlike Alibaba, which built a global empire, IndiaMART remains firmly focused on India. This concentration risk becomes acute if India's economy slows or regulatory environments change. The company has shown little appetite for international expansion, potentially capping its addressable market.

The subscription model, while profitable, may be reaching saturation. With 214,000 paying suppliers out of 8 million total, the conversion rate is just 2.7%. Moving this needle significantly requires either dramatic product improvements or market education—both expensive propositions. The fear is that IndiaMART has already captured everyone willing to pay, leaving only the perpetual free users.

Bull Case:

The bulls see a different picture entirely. 60%+ market share dominance isn't just a number—it's a network effect moat that compounds daily. Every new buyer makes the platform more valuable to sellers, every new seller attracts more buyers. Competitors aren't fighting IndiaMART; they're fighting metaeconomics.

42.23% operating profit margins tell a story of exceptional unit economics. While Udaan burns cash, IndiaMART generated Rs 374.3 crore in PAT from Rs 1,197 crore in revenue. This isn't growth at all costs; it's sustainable, profitable growth. In a world where capital is no longer free, profitability is the ultimate moat.

The massive untapped SME market represents decades of growth. India has 63 million SMEs; IndiaMART has 214,000 paying subscribers. Even capturing 1% of the total market would double their paying base. As digital adoption accelerates post-COVID, as GST forces formalization, as younger entrepreneurs take over family businesses, the addressable market expands.

Software ecosystem synergies are just beginning. The Busy acquisition, Vyapar investment, and other software plays create multiple monetization opportunities. An SME might start with IndiaMART for leads, add Busy for accounting, Shipway for logistics. Each product strengthens the others, creating switching costs that make customers sticky for life.

Strong unit economics and cash generation provide infinite runway. With Rs 2,340 crore in cash and investments, IndiaMART can weather any storm. They can acquire competitors, invest in technology, or simply return cash to shareholders. This financial strength means they control their destiny in ways venture-funded competitors don't.

The COVID accelerator effect is still playing out. The pandemic forced digital adoption that might have taken a decade to happen naturally. SMEs that never considered online presence were forced online. This behavioral change is permanent, and IndiaMART is the primary beneficiary.

Geographic expansion within India remains massive. While 58% of revenue comes from metros, tier 2 and tier 3 cities are just awakening to digital commerce. As infrastructure improves, as internet penetration deepens, as digital payments become ubiquitous, IndiaMART's addressable market multiplies.

The platform economics are beautiful at scale. Unlike e-commerce companies dealing with inventory and logistics, IndiaMART's marginal cost of serving an additional customer approaches zero. Every rupee of revenue beyond break-even falls almost directly to the bottom line.

The Verdict:

The truth, as always, lies somewhere in between. IndiaMART faces real challenges—competition is intensifying, growth is slowing, international expansion seems unlikely. But the company's strengths—market dominance, profitability, cash generation, network effects—provide substantial protection.

The key question isn't whether IndiaMART will face challenges—it will. The question is whether its moats are deep enough to survive them. History suggests they are. The company survived the dot-com crash, 9/11, the 2008 crisis, and COVID. Each crisis made them stronger, not weaker.

For investors, IndiaMART represents a rare combination: a tech company with real profits, a growth story with downside protection, a market leader with expansion potential. It's not without risks, but in the casino of Indian tech stocks, it's one of the few where the house doesn't always win.

XIII. What's Next: The Vision Forward

The next decade for IndiaMART isn't about revolution; it's about evolution at scale. The SME digitization opportunity in India is a generational transformation, and IndiaMART is positioned as the primary beneficiary. With internet users expected to reach 900 million by 2025 and SME formalization accelerating under GST, the company sits at the intersection of multiple tailwinds.

Payment and financing services expansion represents the next frontier. IndiaMART has the data on millions of transactions—who buys what, from whom, how often, at what price. This data is gold for credit underwriting. While the company has been cautious about lending directly, partnerships with financial institutions could unlock massive value. Imagine pre-approved working capital loans for verified suppliers, or trade credit for regular buyers. The opportunity is measured in thousands of crores.

International market potential remains deliberately unexplored. Unlike Alibaba's global ambitions, IndiaMART has chosen depth over breadth. But the Indian diaspora worldwide, particularly in the Middle East, Africa, and Southeast Asia, represents a natural expansion opportunity. Indian products, from textiles to pharmaceuticals, have global demand. IndiaMART could facilitate this trade without the operational complexity of entering new markets—simply by enabling cross-border transactions on the existing platform.

AI and automation in B2B commerce is where IndiaMART's data advantage becomes decisive. With 24 million unique business enquiries generated monthly, the company has the largest dataset on Indian B2B buying behavior. Machine learning can optimize lead matching, predict purchase intent, personalize recommendations. The company that started with manual fax machines could become an AI-powered prediction engine for B2B commerce.

The integration story is perhaps most compelling. As IndiaMART's software acquisitions mature, the vision of an integrated SME operating system becomes clearer. Start your business on IndiaMART, manage accounts on Busy, handle logistics through Shipway, ensure legal compliance via Legistify. It's not just cross-selling; it's creating switching costs so high that leaving becomes inconceivable.

The next decade of B2B marketplaces will be defined by who can move beyond matchmaking to enablement. IndiaMART's evolution from a directory to a marketplace to a platform to an ecosystem maps this journey. The end state isn't just connecting buyers and sellers—it's powering the entire lifecycle of B2B commerce.

But perhaps the most exciting opportunity is the simplest: deeper penetration of existing markets. IndiaMART has 214,000 paying suppliers out of 63 million SMEs. Even reaching 1 million paying suppliers—less than 2% of the market—would represent 5x growth. This isn't about finding new markets or building new products; it's about executing the existing model at greater scale.

The cultural transformation of Indian business also plays to IndiaMART's strengths. As family businesses transition to younger generations, as English-speaking, digitally-native entrepreneurs take charge, the resistance to online B2B commerce evaporates. What required education and evangelism for the parent's generation becomes obvious for the children.

The regulatory environment, often a challenge, could become a tailwind. As the government pushes digitization, as GST compliance requires better record-keeping, as credit flows increasingly through formal channels, IndiaMART becomes not just useful but essential. The company that survived despite the government could thrive because of it.

The vision forward isn't about disruption—it's about integration. Not about replacing traditional B2B commerce—but digitizing it. Not about building a tech company—but creating a technology-enabled business ecosystem. IndiaMART's next decade will be defined not by what it builds, but by what it enables others to build.

In Dinesh Agarwal's words, the mission remains unchanged: "Make doing business easy." Twenty-eight years after starting with Rs 40,000, that simple vision continues to drive a company now worth Rs 15,000+ crore. The tools have evolved from fax machines to AI, the scale from 70 listings to 119 million products, but the core insight remains: Indian businesses need help connecting, transacting, and growing.

The next decade will test whether IndiaMART can maintain its dominance while evolving its model, whether it can fight off competitors while serving customers, whether it can grow profitably while investing for the future. Based on history, betting against them seems unwise. This is a company that has survived everything the market could throw at it and emerged stronger each time.

For long-term investors, IndiaMART represents something rare in Indian tech: a profitable, dominant, growing platform with massive untapped potential. It's not without risks, but in a market full of story stocks, here's one with an actual story—and the numbers to back it up.

XIV. Recent News

The most recent developments paint a picture of steady execution amid market volatility. In Q2 FY2025 (ended September 2024), IndiaMART reported consolidated revenue of Rs 348 crore, representing 18% year-over-year growth. However, the market reaction was harsh—shares fell 19% despite a 48% increase in profit, as concerns emerged about subscriber growth slowing.

The subscriber addition challenge has become the key focus for investors. Net additions have moderated from 34,000 in FY23 to just 9,000 in the first nine months of FY24. Management attributes this to the lingering effects of COVID-era churn stabilizing, but skeptics worry about market saturation.

Jefferies downgraded the stock to "underperform" in October 2024, citing weak subscriber growth and elevated churn rates. Nomura followed with a downgrade to "reduce" with a price target of Rs 1,900, suggesting 10% downside. The bear thesis centers on whether IndiaMART has picked all the low-hanging fruit in terms of customer acquisition.

Yet the fundamental business remains robust. EBITDA margins reached 36% in Q2 FY2025, with net profit margins at 32%. Cash generation continues unabated, with Rs 2,449 crore in cash and investments as of September 2024. The company maintains its guidance of returning to 20-25% collection growth once subscriber additions normalize.

The software ecosystem continues to expand. Recent investments include a 10% stake acquisition in IDfy (identity verification), additional funding in Fleetx (logistics), and deeper integration of Busy's accounting capabilities into the IndiaMART platform. The vision of a comprehensive SME operating system is steadily taking shape.

Regulatory scrutiny remains a watching brief. The USTR's continued inclusion of IndiaMART on its "notorious markets" list for counterfeit concerns hasn't resulted in material business impact, but represents a reputational risk that management continues to address through enhanced verification processes.

XV. Links & Resources

Primary Sources: - IndiaMART Investor Relations: investor.indiamart.com - Annual Reports FY2020-2024: BSE/NSE filings - Quarterly Earnings Transcripts: Available on investor portal - DRHP (Draft Red Herring Prospectus) 2019: SEBI website

Industry Reports: - KPMG India B2B E-commerce Report 2019 - RedSeer Consulting: Indian B2B Commerce Market Analysis - Bain & Company: India's SME Digitization Journey - Google-BCG: Digital SME Report India

Founder Interviews & Talks: - Dinesh Agarwal at TiE Global Summit - Prime Venture Partners Podcast with Dinesh Agarwal - YourStory Conversations: Building IndiaMART - Economic Times Startup Awards Keynotes

Books on Indian Internet Ecosystem: - "The Rise of Digital India" by Ravi Agrawal - "Billionaire Raj" by James Crabtree (context on Indian business) - "From Pony to Unicorn" by Sanjeev Aggarwal (Indian startup ecosystem)

Competitor Analysis: - Udaan: Industry reports and funding announcements - TradeIndia: Company website and media coverage - Alibaba India Strategy: Various analyst reports

SME Digitization Studies: - Ministry of MSME Annual Reports - India Brand Equity Foundation (IBEF) SME Reports - Omidyar Network: Indian SME Credit Gap Analysis

B2B Marketplace Analysis: - Bessemer Venture Partners: B2B Marketplace Playbook - Andreessen Horowitz: B2B Marketplace Metrics Guide - McKinsey: B2B Digital Commerce Reports

Technology in Indian E-commerce: - NASSCOM Reports on Indian Tech Adoption - Google India Digitization Reports - Facebook/Meta India Business Survey

Indian Capital Markets: - SEBI regulations for tech company listings - NSE/BSE historical data on IndiaMART - Institutional investor reports (HDFC Securities, Motilal Oswal, etc.)

The IndiaMART story is far from over. What started as two cousins with Rs 40,000 trying to put Indian exporters online has evolved into India's dominant B2B platform, a profitable tech company in a sea of loss-makers, and a blueprint for building sustainable digital businesses in emerging markets. The next chapter—whether it's about defending dominance or extending it—will be equally fascinating to watch unfold.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube