India Cements: The Southern Cement Empire That Cricket Built

Introduction & Episode Setup

The Chennai skyline in 2024 tells a story of transformation. Where once stood the proud headquarters of an independent cement empire, now flies the flag of UltraTech—India's cement behemoth. This December day marks not just another corporate acquisition, but the end of a 78-year saga that wove together cement, cricket, and the dreams of post-independence India.

India Cements Limited, founded in 1946, wasn't just another industrial company. It was a testament to Tamil entrepreneurship, a builder of South India's infrastructure, and perhaps most surprisingly, the unlikely owner of one of cricket's most successful franchises—the Chennai Super Kings. How did a cement company end up owning a cricket team? Why did a family that built an empire from the ground up decide to sell? And what does this acquisition tell us about the brutal economics of commodity businesses in modern India?

This is the story of three generations of builders—from S.N.N. Sankaralinga Iyer's post-independence industrial vision to N. Srinivasan's cricket empire to the final handover to Kumar Mangalam Birla's UltraTech. It's a tale that reveals hard truths about family businesses, the perils of diversification, and the inexorable logic of industry consolidation.

At its peak, India Cements stood as the ninth-largest listed cement company in India by revenue. Today, it becomes another chapter in UltraTech's consolidation playbook. But between those bookends lies a fascinating journey through Indian capitalism's evolution—from license raj to liberalization, from industrial production to entertainment empires, from regional champion to acquisition target.

The Foundation Story: Post-Independence India (1946-1960s)

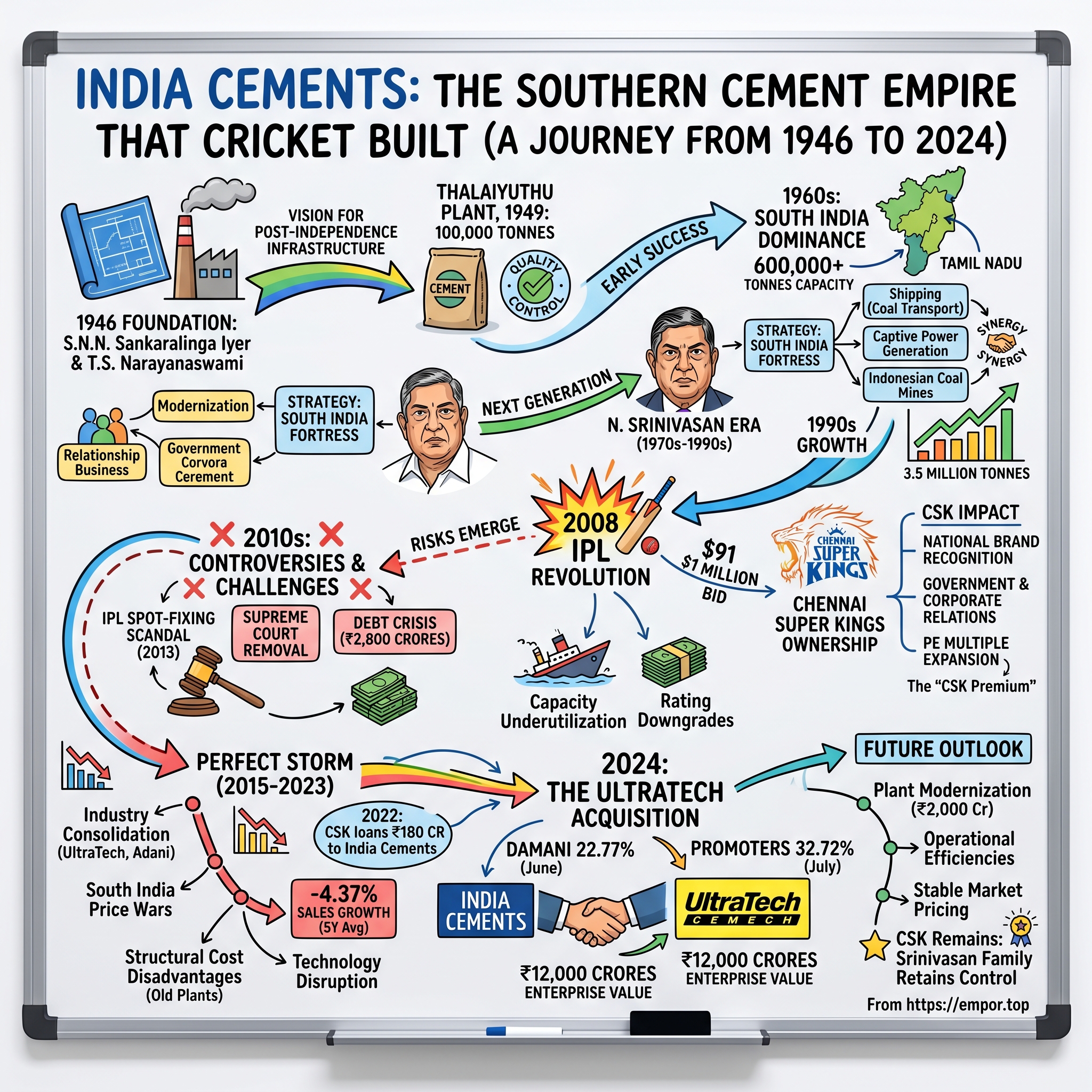

Picture Tamil Nadu in 1946. The British are packing their bags, independence is on the horizon, and two visionaries—S.N.N. Sankaralinga Iyer and T.S. Narayanaswami—are sketching blueprints not just for a company, but for a nation's infrastructure. While Nehru spoke of temples of modern India, these entrepreneurs were quite literally planning to build the foundation.

The timing was audacious. Most industrialists were waiting to see how independent India would shape up. Would it embrace capitalism? Would regional businesses thrive? Sankaralinga Iyer didn't wait for answers. A successful lawyer-turned-industrialist from a traditional Tamil Brahmin family, he had already tasted success in textiles and understood that post-independence India would need cement—lots of it.

The first plant at Thalaiyuthu in Tamil Nadu, commissioned in 1949, was an engineering marvel for its time. Built with a capacity of 100,000 tonnes per annum, it was modest by today's standards but revolutionary for South India. The location wasn't accidental—Thalaiyuthu sat on rich limestone deposits, the primary raw material for cement. But more importantly, it was strategically positioned to serve the infrastructure needs of the emerging Tamil Nadu state.

The early years were marked by what entrepreneurs today would call "doing things that don't scale." Sankaralinga Iyer personally supervised quality control, spending days at the plant. Workers recall him arriving before dawn, checking the kilns, tasting the limestone (yes, literally), and obsessing over the chemistry of cement production. This hands-on approach created a culture of quality that would become India Cements' calling card.

The 1950s saw the company navigate India's nascent regulatory environment. The Industrial Policy Resolution of 1956 could have nationalized cement, but it remained in the private sector—a stroke of luck that Sankaralinga Iyer maximized. By 1958, the company had expanded capacity to 300,000 tonnes, making it the largest cement producer in South India.

What distinguished India Cements wasn't just production capacity but distribution innovation. While competitors relied on rail transport, Sankaralinga Iyer built a fleet of trucks, creating direct dealer relationships across Tamil Nadu. This seemingly simple decision—controlling distribution—would prove prescient. It gave India Cements pricing power and market intelligence that larger, distant competitors lacked.

The founder's philosophy was distinctly regional yet ambitiously modern. He believed Tamil enterprise could match any in India, but it needed to be rooted in local relationships and trust. Every dealer was visited personally, credit was extended based on handshakes, and quality complaints were addressed by senior management. This wasn't just business; it was building a network that would sustain the company through multiple economic cycles.

By the 1960s, India Cements had established two more plants and crossed 600,000 tonnes in annual capacity. But more importantly, it had created a template: technical excellence, regional dominance, and relationship-based business. As Sankaralinga Iyer aged, the question loomed—who would carry this legacy forward? The answer would come from an unexpected quarter: his son-in-law's family, the Srinivasans, who would transform this regional cement company into something far more ambitious—and controversial.

The Srinivasan Era Begins: Second Generation Takes Charge (1970s-1990s)

N. Srinivasan didn't look like a typical cement baron when he joined India Cements in 1979. An engineer from Tamil Nadu's illustrious Annamalai University with a keen analytical mind, he brought something different to the family business—ambition that extended beyond cement. Where the founders saw a regional cement company, Srinivasan envisioned an industrial conglomerate.

His entry coincided with a generational transition. The founders were aging, and the company needed fresh thinking to navigate India's complex license raj. Srinivasan's first major decision revealed his strategic approach: instead of competing head-on with northern giants like ACC and L&T, he would make South India an impregnable fortress.

The 1980s expansion was methodical. While others chased all-India presence, Srinivasan focused on Tamil Nadu and Andhra Pradesh, adding plants at strategic locations—Sankarnagar, Chilamkur, Vishnupuram. Each plant was positioned near limestone deposits but, crucially, also near growing urban centers. Chennai, Hyderabad, Bangalore—the southern metros were booming, and India Cements would feed their growth.

But Srinivasan's masterstroke was vertical integration. While retaining cement as its mainstay, India Cements ventured into shipping, captive power generation, and coal mining—all with purposeful synergy to the core business. The shipping division wasn't a random diversification; it transported coal for the kilns. The power plants weren't just investments; they provided reliable electricity when state grids failed. The coal mines in Indonesia weren't speculation; they were supply chain insurance.

This integration strategy had a hidden benefit: information advantage. Owning ships meant understanding global coal markets. Running power plants meant expertise in energy economics. Operating mines meant direct knowledge of input costs. While competitors relied on suppliers and consultants, India Cements had real-time, ground-level intelligence across the value chain.

The numbers tell the story of successful execution. By 1990, India Cements had grown to 3.5 million tonnes capacity, making it among India's top five cement producers. Market share in Tamil Nadu exceeded 30%, and in some districts, it was effectively a monopoly. The company's EBITDA margins consistently exceeded industry averages by 300-400 basis points—the vertical integration premium.

Yet Srinivasan's management style was distinctly old-school Tamil business. He maintained a small corporate office, knew senior dealers by name, and made quick decisions. Board meetings were brief; execution was everything. This wasn't the MBA-style management becoming fashionable in liberalizing India. It was proprietorial, personal, and incredibly effective in its context.

The 1991 liberalization changed the game. Suddenly, foreign technology was accessible, capital markets were opening, and competition was intensifying. Srinivasan's response was characteristic: he didn't panic or overextend. Instead, he modernized existing plants, improved efficiency, and prepared for the next phase of growth. The company went for major capacity expansion, adding state-of-the-art technology that reduced power consumption by 20% and improved quality consistency.

By the late 1990s, India Cements was generating ₹1,200 crores in revenue with healthy 18% EBITDA margins. The diversifications were contributing 15% of profits while providing strategic benefits. Srinivasan had successfully transitioned from son-in-law to patriarch, from engineer to industrialist. But his greatest gamble—and controversy—lay ahead. The new millennium would bring opportunities in an unexpected arena: cricket.

The IPL Revolution: Cricket Meets Cement (2008-2015)

The Taj Coromandel ballroom in Chennai, January 2008. The IPL auction is underway, and seasoned businessmen are bidding millions for cricket teams—a business no one quite understands yet. When the Chennai franchise comes up, N. Srinivasan raises his paddle. $91 million. The room gasps. A cement company just bought a cricket team for more than most Indian companies' annual profits.

To understand this moment, you need to understand Srinivasan's relationship with cricket. This wasn't a vanity purchase by a cricket-loving billionaire. Srinivasan had been involved with Tamil Nadu Cricket Association since the 1990s, methodically working his way up cricket administration just as he had in cement. He understood something others missed: cricket in India wasn't just sport—it was religion, business, and politics rolled into one.

India Cements directly owned the Chennai Super Kings from 2008, with N. Srinivasan becoming the owner after IPL rules initially prohibited direct ownership by BCCI officials. The franchise immediately became more than a cricket team. It was a marketing platform that no amount of traditional advertising could buy. Every six hit by MS Dhoni, every victory at Chepauk, beamed India Cements into millions of homes. The brand recall was extraordinary—suddenly, a regional cement company had national recognition.

The business model was counterintuitive but brilliant. While the team lost money initially—player salaries, infrastructure, operations—the strategic benefits were enormous. Government relations improved (every politician wanted to be seen with Dhoni), corporate deals accelerated (CEOs loved CSK hospitality boxes), and employee morale skyrocketed (imagine working for the company that owned Dhoni's team).

Srinivasan's management of CSK reflected his cement philosophy: build slowly, dominate completely. He didn't chase the most expensive foreign players. Instead, he invested in talent scouting, coaching infrastructure, and team culture. The retention of core players—Dhoni, Raina, Jadeja—created the consistency that became CSK's hallmark. Three IPL titles and two Champions League titles between 2010-2014 validated the approach.

The numbers were staggering. CSK's brand value grew from $75 million in 2009 to $398 million by 2015. Match-day revenues, merchandising, and sponsorships generated ₹200+ crores annually. But the indirect benefits were larger. India Cements' institutional sales grew 30% faster in the CSK era. Government contracts increased. The company's price-to-earnings multiple expanded from 8x to 12x—the "CSK premium" as analysts called it.

But cricket administration brought Srinivasan something else: power. By 2011, he was BCCI Secretary. By 2013, BCCI President. By 2014, ICC Chairman. The boy from Tamil Nadu now controlled world cricket. This wasn't just business; this was empire-building of a different sort.

The integration between cricket and cement was surprisingly deep. CSK's tagline "Whistle Podu" (blow the whistle) appeared on cement bags. Players visited dealer meets. Construction projects using India Cements got CSK-branded site boards. The cricket team had become a customer acquisition and retention tool that no competitor could replicate.

The separation of CSK from India Cements occurred around 2015, with shares distributed among India Cements shareholders and the Srinivasan family retaining majority control. This restructuring was prompted by regulatory pressure but also financial pragmatism. CSK had served its purpose—building brand and relationships. Now it needed to stand alone.

Looking back, the CSK investment was either genius or madness, depending on your perspective. Financially, it probably broke even. Strategically, it transformed India Cements from regional player to national brand. But it also attracted scrutiny, controversy, and ultimately, may have distracted from the core cement business just as industry dynamics were shifting dramatically.

Controversies and Challenges: The Turbulent 2010s

The Mumbai Police Commissioner's office, May 2013. Investigators are poring over phone records, betting apps, and cricket statistics. The IPL spot-fixing scandal has erupted, and at its center, through his son-in-law Gurunath Meiyappan, is N. Srinivasan. The empire built over decades is about to face its greatest crisis.

The Mudgal Committee report of February 2014 was damning—it accused Gurunath Meiyappan of illegal betting and passing sensitive information to bookies during IPL 2013, stating that India Cements was liable for his actions. Meiyappan wasn't just family; he was CSK's "Team Principal," though Srinivasan would later claim he was merely a "cricket enthusiast."

The scandal revealed the dangerous interconnections Srinivasan had created. As BCCI President, he controlled Indian cricket. As CSK owner, he had a team in the tournament. As India Cements Chairman, he had business interests. When these worlds collided, the conflict of interest was undeniable. The Supreme Court's March 2014 order was scathing, calling it "nauseating" that Srinivasan held onto the BCCI presidency despite judicial censure, ordering him to step down.

But while media focused on cricket scandals, a larger crisis was brewing at India Cements. The company had loaded up on debt during the 2000s boom—₹2,800 crores by 2013. The assumption was that cement demand would grow 8-10% annually forever. Instead, post-2011, growth collapsed. Real estate slowed, infrastructure projects stalled, and suddenly India Cements was burning cash.

The numbers were brutal. Capacity utilization fell to 65%. Prices crashed by ₹50 per bag. Interest costs consumed 40% of EBITDA. The stock price collapsed from ₹150 in 2013 to ₹45 by 2015. Rating agencies downgraded debt to near-junk status. For the first time since the 1970s, India Cements faced existential questions.

Srinivasan's response revealed both his strengths and limitations. He negotiated with banks, extended loan tenures, and sold non-core assets. The shipping business went for ₹200 crores. The Indonesian coal mines were divested. But he wouldn't sell cement plants—that was admitting defeat. Instead, he believed the cycle would turn, demand would return, and India Cements would emerge stronger.

The governance questions were equally challenging. Institutional investors questioned the CSK ownership, the family's role, and corporate governance standards. Proxy advisory firms recommended voting against resolutions. AGMs became battlegrounds. The company that once symbolized Tamil business pride now represented everything wrong with old-school Indian capitalism.

By November 2022, the tables had turned remarkably—CSK extended an ₹180 crore unsecured loan to struggling India Cements, a reversal of the original relationship where the cement company had funded the cricket team. This inter-corporate deposit was legal but optically terrible. The cricket team bailing out the cement company? The irony was lost on no one.

The operational challenges were equally severe. Competitors like UltraTech and Shree Cement had modernized aggressively, achieving costs per tonne 20% lower than India Cements. The regional fortress strategy that worked in the 1990s was failing. Tamil Nadu had excess capacity, Andhra had split into two states creating regulatory confusion, and pan-India players were entering with pricing power India Cements couldn't match.

Employee morale plummeted. The company that once attracted Tamil Nadu's best engineering talent now struggled with attrition. Young managers left for Ambuja, UltraTech, or tech companies. The CSK glamour couldn't compensate for stagnant careers and uncertainty. India Cements was aging—literally and figuratively.

Yet Srinivasan, now in his late 70s, wouldn't let go. This was his life's work, his identity. Selling would be admitting failure, disappointing his late father-in-law's legacy. But mathematics is merciless. By 2023, with accumulated losses mounting and market share declining, even Srinivasan knew the game was ending. The only question was: who would buy, and at what price?

The Perfect Storm: Market Dynamics and Competition (2015-2023)

The data tells a story of slow-motion collapse. India Cements delivered -4.37% sales growth over five years through 2023. In an industry where scale is everything, negative growth is a death sentence. But to understand how India's ninth-largest cement company became an acquisition target, you need to understand the brutal economics of Indian cement.

The 2015-2020 period witnessed unprecedented consolidation. UltraTech acquired JP Associates' plants, then Binani Cement, then Century Textiles' cement division. Adani entered via ACC and Ambuja acquisitions. Suddenly, the top five players controlled 55% market share versus 35% a decade earlier. India Cements, stuck at 2% national share, was increasingly irrelevant.

South India, India Cements' fortress, became the bloodiest battlefield. Tamil Nadu and Andhra Pradesh had 130 million tonnes capacity for 80 million tonnes demand. Utilization rates crashed to 60%. Price wars erupted quarterly. Every player—Ramco, Chettinad, Dalmia, plus the nationals—fought for market share. In this knife fight, India Cements brought a butter knife.

The cost disadvantage was structural. India Cements' plants, averaging 25 years age, consumed 85 kWh power per tonne of cement. Modern plants achieved 65 kWh. At ₹7 per unit power cost, that's ₹140 per tonne disadvantage—roughly the entire EBITDA margin. No amount of management brilliance could overcome physics.

Logistics compounded the problem. UltraTech and Adani had plants across India, optimizing transportation costs. India Cements, concentrated in Tamil Nadu and Andhra, couldn't serve Mumbai or Delhi economically. When infrastructure projects shifted north and west, India Cements couldn't follow. Geography, once an advantage, became a prison.

The 2024 financial results were devastating: revenue of ₹4,149 crores, down 18.85% from the previous year's ₹5,112 crores, with losses of ₹144 crores. For context, UltraTech generated ₹144 crores of profit every five days. The scale differential had become insurmountable.

The working capital situation was equally dire. Dealers demanded credit; India Cements needed cash. Competitors offered 45-day payment terms; India Cements couldn't match without bleeding money. The company that once controlled distribution through relationships now lost dealers to whoever offered better terms. Market share in core districts fell from 35% to 20%.

Technology disruption accelerated the decline. Digital procurement platforms commoditized cement buying. Infrastructure companies used reverse auctions, crushing margins. Brand loyalty evaporated when algorithms chose suppliers. The relationship-based business model Srinivasan perfected became obsolete almost overnight.

Environmental regulations added another burden. New emission norms required ₹500 crores investment India Cements didn't have. Carbon taxes loomed. Alternative materials like fly ash favored players with scale and R&D budgets. The regulatory landscape that once protected regional players now favored consolidation.

The talent exodus accelerated post-2020. India Cements' best plant managers were poached by competitors offering 50% salary increases. The finance team decimated by startups offering stock options. Even CSK couldn't retain talent when the parent company looked terminal. The human capital carefully built over decades evaporated in quarters.

By 2023, the writing wasn't just on the wall—it was in neon lights. India Cements traded at 0.5x book value. Debt exceeded market capitalization. Plants ran at 55% utilization. The only questions were: Would it be bankruptcy or acquisition? And if acquisition, by whom?

The answer came from an unexpected source: Radhakishan Damani, India's retail king and savvy investor. His entry would set the stage for the final act of the India Cements saga.

The UltraTech Acquisition: End of an Era (2024)

The photograph in the Economic Times said everything: N. Srinivasan, 79, shaking hands with Kumar Mangalam Birla, looking relieved rather than triumphant. After months of speculation, the inevitable had happened. The Srinivasan family's 78-year-old cement legacy was passing to India's largest cement maker.

The choreography began in June 2024. UltraTech made a financial investment to acquire 22.77% equity from veteran investor Radhakishan Damani at ₹268 per share, aggregating to ₹1,900 crores. Damani, who had quietly accumulated his stake seeing value in distress, made a clean 40% return in under two years. Classic Damani—buy when there's blood on the streets, sell when strategic buyers appear.

The main transaction followed in July: UltraTech acquired 32.72% from promoters and associates for ₹3,954 crores, triggering an open offer. The math was elegant: ₹390 per share for promoter stakes, valuing India Cements at roughly ₹12,000 crores enterprise value. For 14.45 million tonnes capacity, that's ₹8,300 per tonne—expensive by global standards but reasonable for Indian consolidation.

Why did UltraTech pay this price? The strategic logic was compelling. First, capacity addition through acquisition is faster than greenfield expansion. Building 14 million tonnes would take five years and ₹10,000 crores. Buying India Cements took six months. Second, South India market share. UltraTech was underrepresented in Tamil Nadu; India Cements fixed that overnight. Third, elimination of competition. Every tonne India Cements produced was one tonne of pricing pressure removed.

The synergies were substantial. UltraTech projected ₹400 crores annual cost savings through procurement scale, logistics optimization, and overhead reduction. Revenue synergies from cross-selling and pricing power could add another ₹300 crores. The acquisition pays for itself in eight years—acceptable for patient capital in a century-long business.

For Srinivasan, the sale marked the end of an era, coming just months before his 80th birthday—a pragmatic recognition that the next generation couldn't compete in the new cement landscape. The family retained CSK, now worth more than what they received for India Cements. The cricket team, once a distraction, became the more valuable asset. The irony is perfect.

The employee reaction was mixed relief and anxiety. Relief that salary delays would end and job security would improve under UltraTech. Anxiety about culture change, potential layoffs, and loss of identity. The Chennai headquarters, once buzzing with Tamil conversations and cricket discussions, would become another UltraTech regional office.

For dealers and customers, the transition was seamless. UltraTech honored all contracts, extended credit lines, and improved service levels. The India Cements brand would continue for now, though everyone knew it would eventually disappear into UltraTech's portfolio. Another Indian brand joining the corporate graveyard.

By December 24, 2024, UltraTech communicated completion of the acquisition. The integration began immediately with key appointments: R. Parthasarathy as Head of Integration (Sales & Marketing), Rajesh Sankar as Head of Integration (Manufacturing), and Prakash Pattanshetty realigned as Head of Sales and Marketing. Professional managers replacing family confidants—the modern Indian corporate story.

The market reaction was predictable. UltraTech stock rose 3% on improved market position. India Cements stock found its level around the open offer price. Analysts upgraded the sector citing reduced competition. The consolidation thesis playing out exactly as predicted.

Looking back, was there an alternative? Could India Cements have survived independently? Theoretically yes, with massive capital injection, new technology, and generational leadership change. Practically no. The cement industry's economics—scale, efficiency, distribution—favor consolidation. India Cements fought the tide admirably but inevitably lost. The sale to UltraTech wasn't surrender; it was pragmatism.

Playbook: Business & Strategy Lessons

The India Cements story offers a masterclass in what works—until it doesn't. Every strategic decision that built the empire contained the seeds of its eventual downfall. Understanding these paradoxes is essential for any entrepreneur or investor in commodity businesses.

The Conglomerate Trap: Srinivasan's diversification into shipping, power, and coal made perfect sense in the 1980s-90s. Vertical integration provided cost advantages and supply security. But it also consumed capital that could have modernized cement plants. When the cycle turned, these assets became millstones. The lesson? In commodity businesses, focus beats diversification. Every rupee spent on non-core assets is a rupee not spent on efficiency.

Sports Franchises as Brand Builders: CSK was simultaneously India Cements' greatest marketing coup and biggest distraction. The brand value and government relations were invaluable. But the management attention, regulatory scrutiny, and controversy extracted a heavy toll. The playbook insight: trophy assets work when the core business is strong. When it's struggling, they become dangerous distractions.

Family Business Succession: Srinivasan built India Cements into a regional powerhouse through personal relationships and hands-on management. But this same style prevented institutional evolution. No clear successor emerged, professional managers weren't empowered, and governance remained opaque. The brutal truth: family businesses must professionalize or perish. The skills that build empires rarely sustain them.

Capital Allocation in Cyclical Industries: India Cements borrowed aggressively during the 2005-2010 boom, assuming eternal growth. When demand crashed post-2011, debt became deadly. The playbook lesson is counter-cyclical capital allocation—borrow when times are tough and assets are cheap, deleverage when everyone's euphoric. India Cements did the opposite and paid the price.

Reading Consolidation Waves: The signs were clear by 2015—UltraTech acquiring everyone, Adani entering aggressively, regional players struggling. Yet India Cements held on for another decade, destroying value. The lesson: in consolidating industries, sell early or sell control. Holding on hoping for better terms usually means selling distressed.

The Regulatory-Business Nexus: Srinivasan's cricket administration role initially helped India Cements through government relations and brand building. But when controversy struck, the regulatory backlash was severe. The playbook insight: regulatory capture works until it doesn't. When it unravels, the damage exceeds any benefits accumulated.

Commodity Business Economics: India Cements' story illustrates the brutal math of commodity businesses. Small cost disadvantages—₹140 per tonne from higher power consumption—cascade into existential crises. There's no brand premium, no product differentiation, just ruthless efficiency. The only sustainable advantages are scale, location, and cost. Everything else is temporary.

Technology Adoption Timing: India Cements delayed modernization, believing their old plants could compete through operational excellence. Meanwhile, competitors installed new technology achieving step-changes in efficiency. The lesson: in industrial businesses, technology adoption isn't optional. Late adopters don't catch up; they get acquired.

Market Position Strategy: The regional fortress strategy worked brilliantly for three decades, then failed catastrophically. When transportation costs fell and pan-India players emerged, regional dominance became irrelevant. The strategic lesson: dominant positions in small markets are vulnerable to players with small positions in dominant markets.

The Exit Decision: Perhaps the most important lesson is knowing when to sell. Srinivasan could have sold in 2015 at 2x today's price. But emotional attachment, ego, and hope delayed the inevitable. The playbook is clear: when industry structure changes permanently against you, sell immediately. Waiting for recovery in structural decline is value destruction.

Analysis & Investment Perspective

The UltraTech-India Cements transaction reveals important truths about valuation in consolidating industries. At ₹390 per share, UltraTech paid an enterprise value per tonne significantly higher than recent acquisitions—₹8,300 versus ₹7,070 for Kesoram and ₹6,073 for Century Textiles. Why the premium?

Location value explains much of it. India Cements' plants in Tamil Nadu and Andhra Pradesh are strategically positioned near demand centers. Unlike Kesoram's scattered assets or Century's single large plant, India Cements offers immediate market presence in South India's infrastructure corridor. For UltraTech, weak in the South, this geographic footprint was worth the premium.

The replacement cost arithmetic is compelling. Building 14.45 million tonnes of new capacity would cost ₹12,000-14,000 crores at current prices. UltraTech paid ₹12,000 crores enterprise value for functioning plants with established dealer networks and mining leases. Even accounting for modernization needs, the acquisition is cheaper than greenfield expansion.

The market capitalization of ₹11,505 crores at acquisition reflected deep pessimism about standalone prospects. Trading at 0.7x book value and 15x distressed EBITDA, the market had written off India Cements as a going concern. For UltraTech, buying at distressed valuations with synergy potential was attractive risk-reward.

The South India cement market outlook justifies strategic positioning. Tamil Nadu and Andhra Pradesh will add 60 million tonnes demand by 2030 driven by Chennai-Bangalore industrial corridor, Amaravati capital development, and port expansion. Current oversupply will be absorbed by 2027. Post-consolidation pricing power could improve margins by 500 basis points.

The consolidation impact is already visible. Post-acquisition announcements, cement prices in Tamil Nadu rose ₹15 per bag. With India Cements' 15% market share now part of UltraTech's 23%, the combined entity controls 38% of Tamil Nadu capacity. This concentration allows price leadership previously impossible with fragmented competition.

For remaining independent players—Ramco, Chettinad, Penna—the implications are stark. Scale disadvantages will worsen as UltraTech leverages procurement power. Market share will face pressure from UltraTech's distribution might. The choice is binary: find a buyer or accept permanent subscale status. The consolidation wave isn't ending; it's accelerating.

From an investor perspective, the India Cements saga validates several themes. First, investing in subscale players in consolidating industries is a value trap unless you're playing for acquisition. Second, governance issues and related-party transactions destroy terminal value—CSK's controversies probably cost shareholders ₹1,000 crores. Third, regional champions in commodity businesses are structurally disadvantaged against national players.

The UltraTech acquisition multiple implies 8% unlevered returns assuming modest synergies—acceptable for strategic buyers but unattractive for financial investors. This explains why private equity never bid for India Cements. Without synergies, the math doesn't work. With synergies, only strategic buyers can pay fair value.

Looking forward, UltraTech's integration will be textbook industrial consolidation. Reduce overhead by 40%, improve plant efficiency by 15%, optimize logistics by 20%, and capture pricing benefits. Within three years, India Cements' EBITDA per tonne will match UltraTech's average. The assets were never bad; the ownership structure was.

Epilogue & Future Outlook

Three months after acquisition close, the integration proceeds with military precision. UltraTech's December 24, 2024 communication confirmed completion of the acquisition formalities. The Chennai headquarters, once echoing with cricket discussions and family dynamics, now hosts integration teams mapping synergies. It's efficient, professional, and somehow melancholic.

The plant modernization has begun. UltraTech committed ₹2,000 crores over three years to upgrade India Cements' facilities. Waste heat recovery systems, automation, and AI-powered process optimization will reduce costs by 25%. The plants that struggled to compete will become among India's most efficient. Technology, capital, and scale—the trinity India Cements lacked—arrive in abundance.

For Tamil Nadu's cement market, the integration brings stability after years of price wars. The state's three major players—UltraTech-India Cements, Ramco, and Dalmia—now control 75% capacity. Rational pricing replaces ruinous competition. Infrastructure contractors benefit from supply security. The market works better with fewer, stronger players—economic theory validated by practical outcomes.

The human story is bittersweet. Of India Cements' 3,500 employees, most will remain, but the culture evaporates. Tamil replaced by English in meetings. Cricket posters removed from cafeterias. The family touch replaced by corporate processes. It's nobody's fault—modern business demands standardization. But something ineffable is lost when regional champions become divisional units.

N. Srinivasan, approaching 80, focuses on CSK and cricket administration. The cement business that defined his life for 45 years is history. In interviews, he's philosophical: "Business is about timing. We built something wonderful, but times changed." No bitterness, just acceptance. The next generation will remember him for CSK, not cement. Perhaps that's enough.

The broader implications for Indian business are profound. India Cements joins a long list—Binani, JP, Century—of family cement companies absorbed by larger players. The industry that once had 50+ independent players will soon have five controlling 80% capacity. Efficiency improves, but entrepreneurship diminishes. The economy gains, but something harder to measure is lost.

For investors, the lesson is clear: in mature, capital-intensive industries, consolidation is destiny. Fighting it destroys value; embracing it creates value. The skill is recognizing when industry structure shifts from competition to consolidation. India Cements recognized it too late. Others should learn from their timing mistake.

The India Cements brand will survive another year, maybe two, before disappearing into UltraTech's portfolio. The plants will produce more efficiently than ever. The dealers will prosper under better terms. By every operational metric, the acquisition is successful. Yet, when the last India Cements cement bag is sold, Tamil Nadu will have lost something—an emblem of regional enterprise that cricket alone cannot replace.

What remains is CSK, now worth ₹7,000 crores, more than India Cements ever was. The cricket team that was supposed to market cement became more valuable than the cement company. It's a perfect metaphor for modern India—entertainment exceeding industry, intangible surpassing tangible, dreams defeating reality.

The India Cements story ends not with bankruptcy or scandal but with pragmatic surrender to economic logic. In commodity businesses, scale wins. In family businesses, succession challenges are existential. In diversified conglomerates, focus eventually matters. These aren't moral judgments but mathematical certainties. India Cements fought mathematics for a decade and lost. The surprise isn't that they sold; it's that they lasted so long.

For entrepreneurs studying this saga, the message is sobering but valuable. Build with passion, but sell with pragmatism. Regional champions are temporary; industry structure is permanent. Diversification feels safe but isn't. And sometimes, the side project—like a cricket team—becomes more valuable than the main business. Business, like cricket, is gloriously unpredictable.

The Chennai Super Kings play on, now India's most valuable sports franchise outside cricket. The cement plants produce under new management. N. Srinivasan watches from his Chennai home, perhaps content that his legacy lives in both concrete and cricket. Not a bad epitaph for a cement man who dared to dream beyond gray powder.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube