Indegene: India's Digital-First Life Sciences Unicorn

I. Introduction & Episode Setup

Picture this: It's May 9, 2024, and the Indian stock markets are witnessing something extraordinary. A company that most retail investors have never heard of—Indegene—lists on the NSE at ₹655, a stunning 45% premium to its IPO price of ₹452. Investors who got allotments are seeing ₹6,699 gains per lot within minutes. The financial press scrambles to explain who this company is and why institutional investors bid 197 times the shares available to them.

Here's the fascinating part: Indegene isn't your typical tech unicorn story. No flashy consumer app, no viral growth hacks, no celebrity endorsements. Instead, five engineers from IIT and IIM spent 26 years quietly building the digital backbone for how the world's largest pharmaceutical companies develop, test, and sell drugs. Today, they serve all top 20 global pharma companies, helping them navigate the $1.5 trillion life sciences industry's digital transformation.

The company operates at the intersection of healthcare and technology, but not in the way you might expect. While everyone was chasing telemedicine and fitness apps, Indegene was building AI systems to automate clinical trial documentation for Pfizer. While startups were burning cash on customer acquisition, they were signing decade-long contracts with AstraZeneca and Novartis. Their business? Digital-first healthcare solutions that help biopharmaceutical, emerging biotech, and medical device companies develop products and get them to market faster, cheaper, and more effectively. The central question driving this story: How did five IIT/IIM engineers build a global life sciences commercialization powerhouse that today manages critical drug development operations for the world's largest pharmaceutical companies? This isn't just another Indian IT services success story. They have 63 active clients and work with all the top 20 global pharmaceutical companies, and 69% of their revenues come from the top 20 Pharma companies.

What makes Indegene particularly fascinating is their timing and strategic positioning. They entered the pharma services market when it was dominated by massive CROs (Contract Research Organizations) and traditional IT vendors. Instead of competing head-on, they carved out a unique niche: digital-first commercialization. While Accenture and IBM were selling enterprise software to pharma companies, Indegene was embedding itself into the actual drug development and commercialization workflow.

The numbers tell a remarkable story. Company has delivered good profit growth of 67.9% CAGR over last 5 years and is almost debt free. For FY2024, revenue crossed INR 2,500 crore with a 12.3% increase in revenue, a 28.6% rise in EBITDA, and a 26.5% surge in profit after tax.

Our episode roadmap takes us from a 1998 startup operating out of Bangalore to becoming the digital backbone of global pharma. We'll explore how they survived the dotcom crash without VC funding, built relationships with skeptical pharma giants, and positioned themselves perfectly for the AI revolution in drug development. Most importantly, we'll understand why a company you've probably never heard of might be one of the most important players in how new drugs reach patients worldwide.

The story begins in the late 1990s, when the internet was just starting to transform industries, and five engineers decided that healthcare—specifically pharmaceutical commercialization—was ripe for disruption.

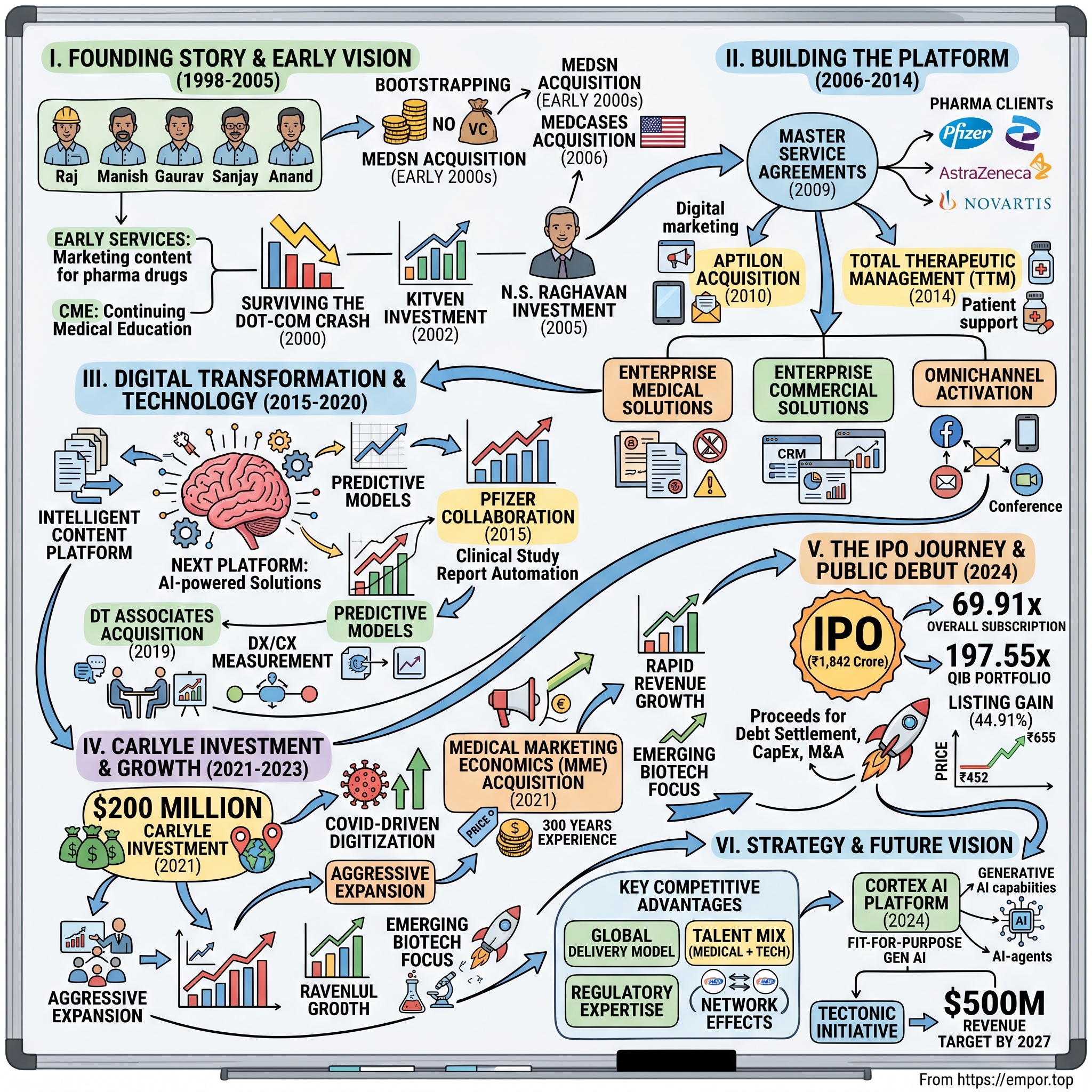

II. The Founding Story & Early Vision (1998-2005)

The year is 1998. The Vajpayee government has just conducted nuclear tests at Pokhran, the Indian economy is liberalizing, and in Bangalore's Electronic City, the IT boom is creating millionaires overnight. But in a modest office space, five engineers are having a different conversation. They're not talking about e-commerce or portals or B2B marketplaces—the hot topics of the era. Instead, they're discussing something decidedly unsexy: pharmaceutical marketing materials.

Indegene was founded in 1998 by Dr. Rajesh Nair, Manish Gupta, Gaurav Kapoor, Dr. Sanjay Parikh and Anand Kiran. The founding team brought together an unusual combination of credentials—IIT engineering backgrounds mixed with IIM business training, but more importantly, they shared a contrarian vision. While their batchmates were joining Infosys and Wipro or launching dot-com startups, these five saw opportunity in the intersection of healthcare and technology.

Dr. Rajesh Nair, who would become the intellectual architect of Indegene's healthcare strategy, had spent time understanding how pharmaceutical companies operated. He noticed something peculiar: despite being among the world's most profitable industries, pharma companies were remarkably inefficient in how they communicated with doctors and patients. Sales representatives would carry physical binders of clinical data. Medical information was disseminated through expensive conferences. Clinical trial documentation was entirely paper-based. The industry that created cutting-edge molecules was using stone-age methods to commercialize them.

Manish Gupta, who would later become CEO, brought the operational discipline. An IIM Ahmedabad alumnus, he understood that breaking into pharma wouldn't be about technology alone—it would require building trust with an industry notorious for being conservative and risk-averse. The strategy they developed was elegant in its simplicity: start as a services company creating marketing content for pharmaceutical drugs, learn the industry inside-out, then gradually move up the value chain.

The early days were tough. Unlike software services where you could demonstrate value quickly, pharmaceutical companies moved slowly. Very slowly. Sales cycles stretched for months. Compliance requirements were Byzantine. The founders would joke that getting a meeting with a pharma executive was harder than getting funding from a VC—except they weren't actually trying to get VC funding.

This brings us to one of the most remarkable aspects of Indegene's story: the conscious decision to bootstrap. In an era when every startup was raising money, burning it on Super Bowl ads, and hoping to IPO before the music stopped, Indegene chose a different path. They would grow organically, reinvest profits, and build for the long term. This wasn't just financial prudence—it was strategic. Pharmaceutical companies valued stability and longevity. A bootstrapped company that had been profitable from day one sent a powerful signal: we're here to stay.

Indegene's first acquisition was Medsn, a company that provided medical education. Medsn continued to operate under the same name in the United States. This wasn't just about buying revenue; it was about acquiring credibility. Medsn gave them a foothold in the US market and more importantly, relationships with American pharmaceutical companies who were the global decision-makers.

Then came 2000, and with it, the dot-com crash. Companies that had raised millions were shutting down overnight. The NASDAQ crashed 78% from its peak. In India, IT companies saw their valuations decimated. But Indegene, having never relied on external capital, kept building. While competitors retrenched, they hired. While others pivoted to "safer" industries, they doubled down on pharma.

The post-9/11 world brought new challenges. US companies became more insular, travel became difficult, and offshore vendors were viewed with suspicion. But Indegene had spent three years building relationships. They weren't just another Indian vendor; they were becoming domain experts in pharmaceutical commercialization. They understood FDA regulations, knew the nuances of direct-to-consumer pharmaceutical advertising, and could speak the language of medical affairs teams.

By 2002, they caught the attention of KITVEN (Karnataka Information Technology Venture Capital Fund), which made a small investment. This wasn't about the money—KITVEN's check was modest. It was about validation from a government-backed fund that added credibility when dealing with risk-averse pharma companies.

In 2006, Indegene acquired MedCases, a continuing medical education company based in the United States. This acquisition was transformative. Continuing Medical Education (CME) is how doctors stay updated on the latest treatments and therapies. By owning a CME platform, Indegene wasn't just creating content for pharma companies; they were directly influencing how doctors learned about new drugs. They were moving from being a vendor to becoming a strategic partner.

The year 2005 marked another milestone when N.S. Raghavan, the legendary co-founder of Infosys, made a personal investment in Indegene. Raghavan wasn't just bringing capital; he was bringing the playbook of how to build a global services company from India. His mentorship would prove invaluable as Indegene prepared for its next phase of growth.

What's remarkable about this period is what Indegene didn't do. They didn't chase the generic drug opportunity that was making Dr. Reddy's and Sun Pharma wealthy. They didn't try to become a clinical research organization like Quintiles or Covance. They didn't even try to become a pure-play IT services company for pharma. Instead, they stayed focused on their niche: helping pharmaceutical companies communicate and commercialize better.

By 2005, Indegene had survived the dot-com bust, 9/11, and the general skepticism about Indian companies in healthcare. They had made strategic acquisitions, brought on board credible investors, and most importantly, had begun to establish themselves as domain experts rather than just service providers. The foundation was set for what would come next: the transformation from a services company to a platform player.

III. Building the Platform: From Services to Solutions (2006-2014)

The scene is a pharmaceutical conference in Philadelphia, 2009. The global financial crisis has just decimated budgets. Lehman Brothers has collapsed, AIG has been bailed out, and pharmaceutical companies—despite their recession-resistant revenues—are under pressure to cut costs. In a hotel conference room, Manish Gupta is presenting to six pharmaceutical executives. What happens next will transform Indegene from a vendor to a strategic partner.

In 2009, Indegene signed a master service agreement with six pharmaceutical companies. This wasn't just another contract win. It was a fundamental reimagining of how pharma companies could work with service providers. Instead of project-based engagements, Indegene was proposing something radical: become the exclusive digital commercialization partner for multiple therapeutic areas across multiple geographies. The pharma executives, desperate to reduce costs while maintaining quality, said yes.

The master service agreement model was brilliant in its simplicity. Rather than competing for every project, Indegene would be the default partner for a defined scope of work. This gave them predictable revenue, deep domain expertise, and most importantly, the ability to invest in long-term capabilities. They could hire specialized talent, build proprietary tools, and develop intellectual property knowing they had guaranteed demand.

In 2010, Indegene acquired Canada-based Aptilon, a multichannel marketing firm, for $4 million. Aptilon brought something Indegene desperately needed: expertise in digital marketing for pharmaceuticals. Remember, this was 2010—the iPad had just launched, physicians were beginning to use smartphones, and the entire healthcare industry was grappling with how to engage digitally-savvy doctors and patients. Aptilon's multichannel marketing capabilities meant Indegene could now orchestrate campaigns across email, web, mobile, and traditional channels—a integrated approach that pharma companies were desperately seeking.

The integration of Aptilon revealed Manish Gupta's operational philosophy: acquire for capability, not just capacity. Every acquisition target was evaluated on three criteria: Does it add a new capability? Does it deepen our domain expertise? Does it give us access to new client relationships? If the answer to any of these was no, they walked away. This discipline would serve them well as they built their platform.

By 2012, Indegene had evolved from a content creation company to something much more sophisticated. They had developed three distinct business segments that would define their strategy for the next decade:

Enterprise Medical Solutions: This wasn't just medical writing anymore. They were now managing entire medical affairs operations for pharmaceutical companies—everything from clinical trial documentation to regulatory submissions to pharmacovigilance. They had teams of doctors, pharmacists, and life sciences professionals who could speak peer-to-peer with their clients' medical teams.

Enterprise Commercial Solutions: The old model of pharma sales—representatives visiting doctors' offices with glossy brochures—was dying. Indegene was building the digital infrastructure for the new world: customer relationship management systems tailored for healthcare, analytics platforms that could track prescription patterns, and engagement tools that could deliver personalized content to physicians based on their specialty and prescribing behavior.

Omnichannel Activation: This was the secret sauce. While competitors could offer medical or commercial services, Indegene could orchestrate campaigns across every channel—from medical journals to social media to medical conferences. They weren't just executing tactics; they were designing integrated strategies that could move a drug from clinical trials to blockbuster status.

The 2014 acquisition of Atlanta-based Total Therapeutic Management (TTM) marked another strategic evolution. TTM specialized in patient support programs—the services that help patients navigate insurance, afford medications, and adhere to treatment regimens. This wasn't just about adding another service line. Indegene recognized that the future of pharmaceutical commercialization wasn't just about convincing doctors to prescribe; it was about ensuring patients could access and stay on therapy.

What made this period remarkable was how Indegene managed growth while maintaining quality. They developed what they called the "Centers of Excellence" model—specialized teams focused on specific therapeutic areas or capabilities. The oncology center of excellence, for instance, didn't just understand cancer drugs; they understood the entire oncology ecosystem—from tumor boards to treatment pathways to reimbursement challenges. This depth of expertise made them indispensable to clients.

The financial trajectory during this period tells its own story. Revenue grew from approximately $30 million in 2006 to over $90 million by 2014. But more important than the top-line growth was the client quality. By 2014, they were working with 18 of the top 20 pharmaceutical companies. Client retention rates exceeded 120%—meaning existing clients were not just renewing but expanding their engagement year over year.

The "boring" strategy, as some Silicon Valley types might call it, was actually brilliant. While health-tech startups were trying to "disrupt" healthcare with consumer apps and failing spectacularly (remember Google Health?), Indegene was embedding itself into the critical workflows of pharmaceutical commercialization. They weren't trying to replace pharma companies; they were making them more effective.

There's an interesting contrast here with the typical tech playbook. No blitzscaling, no winner-take-all dynamics, no network effects in the traditional sense. Instead, Indegene was building something more valuable: switching costs through deep integration, competitive moats through domain expertise, and recurring revenue through multi-year contracts. It was textbook enterprise software economics, except they were delivering it through a services model.

By 2014, Indegene had completed its transformation from a services company to a solutions provider. They weren't just executing tasks; they were solving business problems. They weren't just vendors; they were partners. Most importantly, they had built the foundation for what would come next: the integration of artificial intelligence and machine learning into pharmaceutical commercialization. The boring strategy was about to become very exciting.

IV. Digital Transformation & Technology Platform (2015-2020)

Picture a Pfizer executive in 2015, staring at a wall of printed clinical trial documents that literally reached the ceiling. Each page required manual review, cross-referencing, and validation. A single Phase 3 trial could generate 100,000 pages of documentation. The executive turns to her team: "There has to be a better way." That better way would come from an unlikely source—a Bangalore-based company that had been quietly building AI capabilities while everyone else was still debating digital transformation.

The period from 2015 to 2020 would see Indegene transform from a technology-enabled services company to a technology-first platform player. This wasn't just about adopting new tools; it was about fundamentally reimagining how pharmaceutical companies could leverage data and artificial intelligence to accelerate drug development and commercialization.

The catalyst for this transformation was the convergence of several trends. First, the pharmaceutical industry was generating unprecedented amounts of data—from clinical trials, real-world evidence, social media, and connected devices. Second, regulatory agencies were becoming more receptive to digital submissions and AI-assisted analysis. Third, and most importantly, the cost of drug development had spiraled to an average of $2.6 billion per approved drug, forcing companies to seek radical productivity improvements.

Indegene's response was to build what they called the NEXT platform—a suite of AI-powered solutions that could automate routine tasks while augmenting human decision-making. But unlike Silicon Valley startups that would announce their AI ambitions with great fanfare, Indegene built quietly, tested extensively, and only launched when they had proven value with lighthouse clients.

The first breakthrough came in clinical documentation. Working with Pfizer, Indegene developed an Intelligent Content Platform that could auto-generate clinical study reports, regulatory submissions, and safety documentation. The system didn't just template documents; it could extract relevant data from multiple sources, identify inconsistencies, and even suggest narrative text based on statistical results. What previously took medical writers weeks could now be done in days, with higher accuracy and complete audit trails.

But the real innovation wasn't the technology itself—it was how Indegene deployed it. Rather than selling software licenses and walking away, they embedded their AI tools within managed services engagements. Clients didn't have to worry about implementation, training, or maintenance. They simply got better, faster, cheaper outcomes. This "AI-as-a-Service" model was perfectly suited for pharmaceutical companies that wanted the benefits of AI without the complexity of building it themselves.

The machine learning capabilities extended beyond documentation. Indegene built predictive models that could identify which physicians were most likely to prescribe a new drug, optimize the sequence of marketing messages, and even predict which patients were at risk of discontinuing therapy. They called this the "Multichannel Maturity Framework"—a systematic approach to evolving pharmaceutical marketing from mass broadcast to personalized engagement. In September 2019, Indegene entered into an agreement to acquire a majority stake in London-based DT Associates, a consulting company exclusively focused on helping pharmaceutical companies achieve excellence in Customer Experience (CX) and Digital Operations (DX). Indegene paid $10 million for a majority stake in the company. This wasn't just another acquisition for geographic expansion. Since being founded in 2014, DT Associates successfully helped large pharmaceuticals around the world identify, plan for and capture the commercial opportunity behind their DX/CX transformation, and developed proprietary solutions for the objective measurement of Customer Experience (CX) and Digital Maturity (DX). Its client roster includes companies such as Pfizer, Sanofi, AstraZeneca, Takeda, Novo Nordisk and more.

The DT acquisition was strategic on multiple levels. First, it gave Indegene credibility in digital transformation consulting—the ability to not just execute but to advise at the C-suite level. Second, it provided European presence with offices in London, Switzerland, and Ireland. Third, and most importantly, DT brought methodologies for measuring digital maturity—something pharmaceutical companies desperately needed but didn't know how to quantify.

The Centers of Excellence model evolved during this period into something more sophisticated. Rather than just having therapeutic area expertise, Indegene built specialized units for emerging capabilities: Real-World Evidence analytics, Social Media listening for pharmacovigilance, and Digital Therapeutics integration. Each center wasn't just a cost center providing services; they were innovation hubs developing intellectual property that could be leveraged across clients.

Consider the scale of transformation happening inside pharmaceutical companies during this period. A typical large pharma company might have 50,000 sales representatives globally, each making 8-10 physician visits per day. The traditional model—where reps showed up at doctors' offices with printed materials—was dying. Physicians were busier, less accessible, and increasingly getting their information digitally. Indegene's Omnichannel Activation platform didn't just digitize the old model; it reimagined it. Using AI to analyze physician behavior, they could predict the optimal channel (email, webinar, peer-to-peer program), timing, and message for each interaction.

The financial performance during this period validated the strategy. Revenue grew from approximately $90 million in 2014 to over $180 million by 2019, with EBITDA margins expanding as technology leverage increased. Client concentration actually decreased even as revenue grew—a sign that Indegene was winning new logos, not just expanding existing relationships.

But perhaps the most important development during this period was something that wouldn't show up in financial statements: the accumulation of healthcare data and the algorithms to process it. Every clinical trial they supported, every marketing campaign they executed, every physician interaction they facilitated was generating data. And unlike their competitors who treated data as exhaust, Indegene was treating it as fuel for their AI engines.

The stage was set for the next phase. Indegene had built the technology platform, established credibility with consulting capabilities, and demonstrated the ability to drive outcomes. What they needed now was capital—not to survive, but to accelerate. The conversation with private equity was about to begin, and it would transform Indegene from a successful services company to a potential unicorn.

V. The Carlyle Investment & Growth Acceleration (2021-2023)

February 2021. The world is still reeling from COVID-19. Pharmaceutical companies, having developed vaccines in record time, are heroes. Digital adoption in healthcare, which typically moved at glacial pace, has accelerated by a decade in twelve months. In a virtual meeting room, executives from The Carlyle Group—one of the world's largest private equity firms with $260 billion in assets—are listening to Manish Gupta present Indegene's vision. By the end of the call, they would commit to leading a $200 million investment that would value Indegene at over a billion dollars. The Carlyle Group (NASDAQ: CG), Brighton Park Capital and Indegene announced that Carlyle and Brighton Park Capital will acquire minority stakes in the company for US$200 million. The transaction consists of a secondary sale from existing shareholders of Indegene and a primary investment into the company. This has enabled the company to grow at more than 25% revenue CAGR over a decade. With more than 3,000 employees across North America, Europe, China, Japan and India, Indegene provides technology platforms and commercialization services to pharmaceutical, biotechnology, and medical device companies. 18 of the top 20 global biopharma organizations lean on its domain experts for an agile, customized, enduring partnership.

The Carlyle investment wasn't just about money—though $200 million certainly helped. It was validation that Indegene's vision of AI-powered pharmaceutical commercialization was not just viable but inevitable. Neeraj Bharadwaj, Managing Director of the Carlyle Asia advisory team, said: "We have been impressed by the strong entrepreneurial energy of the management team at Indegene and their technology-led, data driven, differentiated global delivery model, as well as by their ability to scale relationships with global healthcare enterprises."

But what really mattered was what happened next. COVID-19 had fundamentally changed how pharmaceutical companies operated. Sales representatives couldn't visit doctors. Medical conferences went virtual. Clinical trials had to be conducted remotely. Every pharmaceutical company was scrambling to digitize operations that had remained unchanged for decades. And Indegene, having spent 20 years preparing for this moment, was perfectly positioned to help. In August 2021, Indegene announced the acquisition of Medical Marketing Economics, LLC (MME), a global leader in Pricing, Reimbursement and Market Access (PRMA) services for approximately $10 million. MME specialises in advising life sciences organisations and emerging biotech companies on determining pricing and reimbursement, contracting strategy, tactics and custom payer market research to optimise market value for their innovations. Emerging Biotech organizations today contribute about 75% of the products in pipeline and this is only expected to grow. Biotech originators are creating over $251 billion in innovation value.

This acquisition was particularly strategic. The shift in drug development from big pharma to smaller biotech companies created a massive opportunity. These emerging biotechs had brilliant science but lacked commercialization expertise. They could develop breakthrough therapies for rare diseases but had no idea how to price them, get insurance coverage, or navigate the complex web of global reimbursement systems. MME's team has a cumulative 300 years of pharma market access, pricing and reimbursement experience—exactly what these biotechs needed.

The growth during this period was explosive. Topline growth in 2020-21 was about 45% and is expected to grow over 50% this year to post about $200 million revenue. Revenue grew from approximately $90.8 million in FY2020 to $223.8 million in FY2022—a remarkable acceleration driven by the perfect storm of COVID-driven digitization, the Carlyle investment enabling aggressive expansion, and the fundamental shift in how pharmaceutical companies operated.

But what's most impressive about this period is what Indegene didn't do. They didn't chase every shiny object. They didn't pivot to telehealth or direct-to-consumer healthcare apps—the hot areas that attracted billions in venture funding. They stayed focused on their core: helping pharmaceutical companies commercialize drugs more effectively. Every acquisition, every new service line, every technology investment was aligned with this mission.

The client metrics during this period tell the real story. Client retention rates soared to 122.83% in FY2023, 159.89% in FY2022, and 129.90% in FY2021—meaning not only were clients staying, they were dramatically expanding their engagements. When a retention rate exceeds 100%, it means existing clients are buying more services than the previous year—a powerful indicator of value creation.

The financial strength was equally impressive. The company spent about $30-40 million in acquisitions and majority of these funds were mobilised from internal accruals. Despite rapid growth and acquisitions, Indegene remained almost debt-free—a remarkable achievement in an era of cheap capital and aggressive leverage.

By 2023, Indegene had transformed from a services company with some technology to a technology company that delivered through services. They had AI platforms generating clinical documentation, predictive models optimizing marketing spend, and digital infrastructure supporting thousands of pharmaceutical sales representatives globally. The stage was set for the ultimate validation: going public.

VI. The IPO Journey & Public Market Debut (2024)

The boardroom at Indegene's Bangalore headquarters, December 2023. The five founders, now in their fifties, are having a debate they never thought they'd have. After 25 years of building without external validation, without quarterly earnings calls, without the scrutiny of public markets, they're discussing whether to take Indegene public. Manish Gupta later recalled: "We always said we want to remain private. But the market opportunity ahead of us, the investments needed in AI, the need to provide liquidity to early employees—everything pointed to one direction. "The IPO structure was ambitious: ₹1,842 crore issue, with a fresh issue of ₹760 crore and an offer for sale of ₹1,082 crore. The price band was set at ₹430-452 per share. The IPO opened on May 6, 2024, and closed on May 8, 2024.

What happened next stunned even the optimists. The IPO was subscribed 69.91 times overall. But the real story was in the category-wise subscription: the QIB (Qualified Institutional Buyer) portion was subscribed 197.55 times—meaning institutions were willing to buy nearly 200 times the shares available to them. This wasn't just interest; it was overwhelming conviction from the world's smartest money managers. The shares got listed on BSE, NSE on May 13, 2024. The public issue of Indegene IPO was offered at ₹452.00 per share and the ipo was listed at ₹655.00. It has delivered listing gain of 44.91%. For investors who got allotments, the IPO has offered Rs 6699.00 per lot return on listing.

The grey market had been buzzing with anticipation. The GMP, as per the latest reports, hovered at around ₹301 per share. Combining the GMP with the upper price band of the IPO – ₹452 per share – the expected listing price stands at ₹753. But even the grey market underestimated the actual demand.

The subscription numbers tell an extraordinary story. Qualified Institutional buyers placed applications for 155.98 crore equity shares against the quota of 78.95 lakh shares, resulting in oversubscription of 197.55 times. Non Institutional Investors' portion was booked 54.70 times. Bids for 33.90 crore equity shares were placed against 61.97 lakh equity shares on offer. Even Retail Individual Investors' category was booked 5.74 times. Bids for 11.04 crore equity shares were received against 1.44 crore shares on offer.

The anchor investor round before the IPO had already set the tone. Indegene IPO raises ₹548.78 crore from anchor investors. The list of anchor investors read like a who's who of global institutional investing—marquee names betting big on Indegene's future.

Post-listing, Indegene's market capitalization stood at approximately ₹13,750 crore, instantly making it one of India's most valuable healthcare technology companies. The founders, who had bootstrapped for years and taken minimal external capital, were now paper billionaires. But more importantly, thousands of employees who had stuck with the company through its journey were now holding valuable stock options.

The IPO proceeds were earmarked for strategic purposes. The company plans to allocate ₹3,913.35 million for settling the debt of ILSL Holdings, Inc., a significant subsidiary. ₹1,029.16 million will be allocated for covering the capital expenditure needs of both the Company and another major subsidiary, Indegene, Inc. The remaining funds would be used for general corporate purposes and potential inorganic growth opportunities—code for more strategic acquisitions.

What made the IPO particularly interesting was the founder dynamics. Unlike typical tech IPOs where founders cash out significantly, the Indegene founders sold minimally. The offer for sale included modest amounts from the founders—a signal that they believed the best was yet to come. This wasn't an exit; it was a new beginning.

The public market debut also brought scrutiny. Analysts pored over the numbers, questioning the sustainability of growth rates, the concentration of revenue from top clients, and the competitive threats from both global giants and emerging startups. But the overwhelming consensus was positive. Indegene had proven that an Indian company could build a global leadership position in a specialized, high-value segment of healthcare technology.

The listing success was particularly sweet for those who had been with Indegene from the early days. Employees who had joined when the company was a small Bangalore startup were now seeing life-changing wealth creation. The company's ESOP pool, carefully managed over the years, had created hundreds of crorepatis overnight.

For the Indian startup ecosystem, Indegene's IPO sent a powerful message: you don't need to be a consumer internet company to create massive value. You don't need to burn billions in venture capital. You can build a global leader by focusing on a niche, developing deep domain expertise, and executing consistently over decades. It was validation for the "boring" businesses—the ones that don't make headlines but quietly build empires.

VII. Business Model & Competitive Advantages

To understand why institutional investors bid 197 times for Indegene's shares, you need to understand the economics of their business model. It's a masterclass in building recurring revenue, creating switching costs, and generating operating leverage—all while appearing to be "just a services company."

The company enjoys client relationships with all the 20 largest pharmaceutical companies globally in terms of revenue for FY 2023. But the real story isn't just who their clients are—it's how sticky these relationships are. Client retention rates of 122.83% (FY2023), 159.89% (FY2022), 129.90% (FY2021) mean that not only do clients stay, they dramatically expand their spending year over year. When your retention rate exceeds 100%, you've achieved the holy grail of enterprise software economics through a services model.

The business is structured around four core segments, each addressing different parts of the pharmaceutical value chain:

Enterprise Commercial Solutions: This isn't just sales and marketing support. Indegene embeds itself into the commercial operations of pharmaceutical companies, managing everything from customer relationship management to sales force effectiveness. They don't just provide tools; they run entire commercial operations. Once a pharma company outsources its commercial operations to Indegene, switching to another provider would be like performing heart surgery while running a marathon—theoretically possible but practically suicidal.

Omnichannel Activation: In a world where a physician might see a drug advertisement on LinkedIn, attend a virtual medical conference, receive personalized emails, and interact with sales reps—all for the same drug—someone needs to orchestrate this symphony. Indegene's omnichannel platform ensures that every touchpoint is coordinated, personalized, and compliant with regulations. 69% of our revenues come from the top 20 Pharma companies, and these companies don't trust their multi-billion dollar drug launches to anyone but the best.

Enterprise Medical Solutions: This is where Indegene's medical expertise shines. They manage medical affairs, regulatory submissions, and pharmacovigilance for their clients. When a new adverse event is reported for a drug anywhere in the world, Indegene's teams are often the ones processing it, analyzing it, and ensuring regulatory compliance. This isn't work you hand over to the lowest bidder.

Enterprise Clinical Solutions: The newest and potentially most lucrative segment. Clinical trials are the most expensive part of drug development, often costing hundreds of millions of dollars. Indegene's AI-powered solutions can reduce these costs by 20-30% while accelerating timelines. In an industry where getting to market six months earlier can mean billions in additional revenue, this value proposition is irresistible.

The revenue model is elegantly simple yet powerful. Indegene primarily uses a Full-Time Equivalent (FTE) model where clients pay for dedicated resources, supplemented by transaction-based pricing for specific technology modules. This creates predictable, recurring revenue while allowing for upside from increased usage. It's the best of both worlds: the stability of services revenue with the scalability of software.

Indegene had 65 active clients as of December 2023 and runs offices in India as well as North America, Europe and Asia. But unlike traditional IT services companies that chase hundreds of clients, Indegene focuses on depth over breadth. They'd rather have 65 clients spending $3 million each than 650 clients spending $300,000 each. This concentration allows them to develop deep expertise and become indispensable.

The global delivery model is another competitive advantage. With the majority of their workforce in India, Indegene enjoys significant cost arbitrage. But unlike traditional outsourcing, they're not competing on cost—they're using the cost advantage to invest in technology and domain expertise. A pharmaceutical company might pay Indegene 70% of what they'd pay a US-based competitor, but Indegene delivers 120% of the value through their technology leverage and domain expertise.

Company is almost debt free. Company has delivered good profit growth of 67.9% CAGR over last 5 years. This financial strength allows them to invest aggressively in R&D and acquisitions without diluting shareholders or taking on debt. In a capital-intensive industry, being debt-free is like bringing a gun to a knife fight.

The talent strategy is particularly clever. Indegene hires life sciences graduates—doctors, pharmacists, biotechnologists—and trains them in technology and business. This creates a unique workforce that can speak the language of their pharmaceutical clients while understanding the technology needed to transform their operations. Try finding that combination at TCS or Accenture.

The acquisition strategy we discussed earlier—buying specialized capabilities rather than revenue—has created a portfolio effect. Each acquisition adds a new capability that can be cross-sold to existing clients. When they acquired MME for market access expertise, every existing client became a potential buyer of market access services. When they acquired DT Associates for digital transformation consulting, they could now lead strategic engagements rather than just execute them.

But perhaps the most underappreciated competitive advantage is regulatory expertise. Healthcare is one of the most regulated industries in the world. Every piece of content, every customer interaction, every data point must comply with complex regulations that vary by country and change frequently. Indegene has built this compliance into their platforms and processes. A competitor trying to enter this space would need years to develop similar capabilities.

The network effects, while subtle, are powerful. As Indegene works with more pharmaceutical companies, they accumulate more data and insights about what works and what doesn't. This knowledge, anonymized and aggregated, makes their AI models smarter and their recommendations more valuable. Every client makes Indegene better for every other client.

VIII. AI Strategy & Future Vision

Standing in Indegene's innovation lab in Bangalore, you might mistake it for a Silicon Valley startup. Data scientists huddle around screens showing neural network architectures. Product managers debate API designs. Engineers deploy code to cloud infrastructure. But look closer, and you'll see something different: medical degrees on the walls, pharmaceutical journals on desks, and discussions peppered with terms like "pharmacokinetics" and "real-world evidence." This is where healthcare meets artificial intelligence, and it's the foundation of Indegene's billion-dollar bet on the future.

The Pfizer collaboration that began in 2015 has evolved into something remarkable. The Intelligent Content Platform that started as a tool to automate clinical documentation has become a comprehensive AI suite that touches every aspect of drug development and commercialization. Consider the scale: a single Phase 3 clinical trial generates millions of data points. Traditionally, humans would spend months analyzing this data, writing reports, and ensuring compliance. Indegene's AI can do it in days, with higher accuracy and complete audit trails.

But the real innovation isn't the speed—it's the intelligence. The system doesn't just process data; it understands context. When analyzing adverse events, it can differentiate between a headache caused by the drug and one caused by stress. When reviewing clinical trial data, it can identify patterns that humans might miss—subtle correlations between patient genetics and drug efficacy that could lead to personalized treatment protocols.

The Cortex AI platform, launched in 2024, represents the next evolution. While the Intelligent Content Platform focused on documentation, Cortex aims to transform decision-making across the pharmaceutical value chain. It launched Cortex, a fit-for-purpose Generative AI platform for the life sciences industry. Imagine a pharmaceutical executive asking, "Which physicians should we target for our new oncology drug?" Cortex doesn't just provide a list; it analyzes prescription patterns, research publications, clinical trial participation, and social media influence to identify the physicians most likely to become early adopters and influence their peers.

The platform leverages large language models (LLMs) but with crucial modifications for healthcare. Generic LLMs like GPT-4 might hallucinate medical information—a potentially fatal flaw in healthcare. Indegene's models are trained on verified medical literature, regulatory documents, and real-world evidence. They're not just accurate; they're traceable. Every recommendation can be traced back to its source, critical for regulatory compliance.

The commercial applications are perhaps even more transformative. Pharmaceutical sales and marketing have traditionally been relationship-driven and intuition-based. Indegene's AI brings science to the art of selling. Their models can predict which marketing messages will resonate with specific physician segments, optimize the timing and channel of communications, and even generate personalized content at scale.

Consider the example of a new diabetes drug launch. Traditional approach: Create one marketing campaign, blast it to all endocrinologists, hope for the best. Indegene's approach: AI analyzes each physician's prescribing history, research interests, patient demographics, and communication preferences. It then generates thousands of personalized campaigns—different messages for researchers versus clinicians, different channels for digital natives versus traditional physicians, different timing based on prescription cycles. The result: 3x higher engagement rates and 2x faster adoption curves.

Q1 FY26 results: 1.8% USD revenue growth, stable margins, $1M revenue from new AI-driven Tectonic initiative. The Tectonic initiative represents Indegene's bet on autonomous AI agents. Rather than just providing insights, these agents can execute tasks independently—scheduling medical conference presentations, responding to physician queries, even drafting regulatory submissions. It's moving from AI as a tool to AI as a colleague.

The $500 million revenue target by 2027 isn't just ambitious—it's a statement of intent. Indegene believes that AI will fundamentally restructure the pharmaceutical industry, and they intend to be the infrastructure layer for this transformation. They're not trying to replace pharmaceutical companies; they're trying to make them exponentially more effective.

The competitive moat around their AI strategy is multi-layered. First, data: decades of working with pharmaceutical companies has given them access to patterns and insights that newcomers can't replicate. Second, trust: pharmaceutical companies won't hand over their most sensitive data to just anyone. Third, integration: Indegene's AI isn't a standalone product but integrated into workflows that pharma companies already depend on.

The ethical considerations are taken seriously. Healthcare AI can literally be a matter of life and death. Indegene has established an AI Ethics Board, including external medical ethicists and patient advocates. Every AI model is tested not just for accuracy but for bias—ensuring that recommendations don't inadvertently discriminate based on race, gender, or socioeconomic status.

Looking forward, Indegene is betting on three major trends. First, the convergence of AI and real-world evidence. As wearables and digital health tools generate continuous patient data, Indegene's platforms will analyze this information in real-time to optimize treatment protocols. Second, the rise of precision medicine. As genetic testing becomes routine, their AI will help pharmaceutical companies develop and market drugs for increasingly specific patient populations. Third, the digitization of clinical trials. COVID-19 showed that many aspects of clinical trials can be conducted remotely. Indegene's platforms will make decentralized trials the norm, not the exception.

The unicorn trajectory isn't just about financial metrics—it's about becoming indispensable to the pharmaceutical industry's future. When every drug is developed with AI assistance, when every marketing campaign is AI-optimized, when every physician interaction is AI-enhanced, Indegene intends to be the platform powering it all.

IX. Playbook: Lessons in Building Without Hype

There's a moment in every Indegene board meeting that captures the company's philosophy perfectly. Before discussing new initiatives, Manish Gupta asks a simple question: "Will this still matter in 10 years?" It's a question that would seem absurd in most startups, where the focus is on the next quarter or at best, the next funding round. But for Indegene, thinking in decades isn't just strategy—it's survival.

The "boring" strategy, as Silicon Valley might dismissively call it, is actually a masterclass in company building. While contemporaries were raising rounds every 18 months, pivoting business models, and optimizing for valuation metrics, Indegene was optimizing for something else entirely: permanence.

Consider the founding team dynamics. Indegene was founded in 1998 by Dr. Rajesh Nair, Manish Gupta, Gaurav Kapoor, Dr.Sanjay Parikh and Anand Kiran. Twenty-six years later, all five founders are still actively involved. In an industry where founder departures are common and often acrimonious, this continuity is remarkable. They didn't stay together because they had to—by 2010, any of them could have cashed out for generational wealth. They stayed because they were building something bigger than individual ambitions.

The capital strategy deserves its own business school case study. Indegene raised minimal external capital until the Carlyle round in 2021—23 years after founding. This wasn't because they couldn't raise money. Post-2010, venture capitalists were literally queuing up to invest. But each time, the founders asked: "What would we do with the money that we can't do with our profits?" Usually, the answer was nothing valuable.

This patient capital approach had profound implications. Without the pressure of venture returns, Indegene could make decisions that wouldn't pay off for years. They could invest in building domain expertise that had no immediate monetization path. They could say no to clients that wanted to squeeze margins. They could retain employees through downturns instead of conducting layoffs to preserve runway.

The acquisition strategy exemplifies their disciplined approach. The company spent about $30-40 million in acquisitions and majority of these funds were mobilised from internal accruals. Each acquisition was small, strategic, and immediately integrated. No trophy hunting, no empire building. Compare this to competitors who made flashy billion-dollar acquisitions that later had to be written down or divested.

The value creation through these acquisitions was multiplicative, not additive. When they acquired DT Associates for $10 million, they didn't just get $3-4 million in revenue. They got the capability to lead digital transformation engagements, which opened doors to C-suite relationships, which led to larger contracts, which generated 10x the acquisition price in incremental revenue within three years.

The cultural elements are equally important. Indegene cultivated what they call "intellectual humility"—the recognition that in healthcare, what you don't know can literally kill people. This manifested in hiring practices (preferring domain expertise over pure technical brilliance), client interactions (listening more than talking), and product development (extensive testing over rapid deployment).

The employee value proposition was different too. While competitors offered stock options that might make employees rich if the company IPO'd or got acquired, Indegene offered something else: the opportunity to work on problems that mattered, stable employment, and steady wealth creation through profit-sharing. It attracted a different type of person—those who valued purpose and stability over lottery tickets.

Risk management at Indegene deserves special attention. They consistently avoided the fashionable risks that destroyed many contemporaries. When everyone was building platforms, they stuck to services. When everyone pivoted to services, they started building platforms. When everyone chased consumer healthcare, they stayed focused on enterprise. When everyone went remote-first, they maintained physical offices. This contrarian approach wasn't stubbornness—it was strategic patience.

The client relationship philosophy was transformative. Instead of the typical vendor mindset ("How can we maximize this contract?"), Indegene adopted a partner mindset ("How can we make this client successful?"). This sometimes meant recommending competitors for work outside Indegene's expertise. It sometimes meant reducing contract values when clients faced budget pressures. Short-term pain, long-term gain.

The geographic expansion strategy was similarly patient. Rather than the typical "land and expand" approach of opening offices everywhere, Indegene waited until they had anchor clients in each geography. The European expansion came only after they had deep relationships with European pharmaceutical companies. The China office opened only when they had confirmed multi-year contracts.

Perhaps most importantly, Indegene understood the power of compound growth. While a 25% annual growth rate might seem pedestrian compared to startups growing 300% annually, compounded over 26 years, it creates extraordinary value. Moreover, profitable growth compounds not just financially but operationally—each year's profits fund next year's investments, creating a virtuous cycle.

The lesson for entrepreneurs isn't to avoid venture capital or grow slowly. It's to be intentional about the type of company you're building. If you're building for a quick flip, optimize for growth metrics and valuation multiples. But if you're building for permanence, optimize for sustainability, profitability, and strategic position.

X. Risk Analysis & Future Challenges

Every success story has its shadows, and Indegene is no exception. For all its strengths, the company faces structural challenges that could derail its unicorn trajectory. Smart investors aren't just buying the growth story—they're pricing in these risks.

The subsidiary dependency is perhaps the most immediate concern. The majority of Indegene's revenue flows through international subsidiaries, particularly in the United States. This creates multiple vulnerabilities: regulatory changes in foreign jurisdictions, transfer pricing scrutiny, and currency fluctuations. If the US government decided to restrict outsourcing of healthcare data processing—not impossible given rising data nationalism—Indegene's business model would face an existential crisis.

Client concentration remains a double-edged sword. 69% of our revenues come from the top 20 Pharma companies. This concentration provides stability and deep relationships, but it also creates vulnerability. Pharmaceutical companies are consolidating—there were 30 major pharma companies in 2000, today there are 20, and by 2030 there might be 15. Each merger reduces Indegene's client base and potentially puts contracts at risk as merged entities rationalize vendors.

The competitive landscape is intensifying from multiple directions. Traditional IT services giants like Accenture and IBM are building healthcare practices, bringing massive resources and existing enterprise relationships. Healthcare-native competitors like IQVIA have deeper clinical trial expertise. Technology giants like Microsoft and Google are entering healthcare with AI solutions that could disintermediate Indegene's value proposition. Most threatening are the pharmaceutical companies themselves, who are building in-house digital capabilities—Roche acquired Flatiron Health, Novartis is building its own AI lab.

The technology disruption risk cuts both ways. While Indegene is betting big on AI, the pace of change in artificial intelligence is unprecedented. Large language models are improving exponentially. Open-source alternatives are democratizing capabilities that were previously proprietary. If AI becomes commoditized—if any company can build pharmaceutical-grade AI solutions using off-the-shelf tools—Indegene's competitive advantage erodes significantly.

Regulatory changes pose constant challenges. Healthcare regulations vary dramatically across geographies and change frequently. The EU's AI Act, for instance, classifies healthcare AI as "high-risk," requiring extensive compliance measures. India's proposed Data Protection Bill could restrict cross-border data transfers. The US FDA is still figuring out how to regulate AI in healthcare. Each regulatory change requires expensive adaptation and potentially makes existing solutions obsolete.

The talent challenge is becoming acute. It employs more than 4,500 people across North America, Europe, China, Japan and India. But the competition for talent that combines healthcare expertise with technology skills is fierce. Google can pay 3x what Indegene offers. Startups offer equity upside that a post-IPO company can't match. As Indegene grows, maintaining its culture and talent quality becomes exponentially harder.

The economic sensitivity of pharmaceutical spending is often underestimated. While drug demand is relatively recession-proof, pharmaceutical companies' operational spending—where Indegene makes its money—is not. In a severe recession, pharma companies could slash marketing budgets, delay digital transformation initiatives, and insource work to preserve jobs. Indegene's growth assumes continued healthy pharmaceutical industry spending.

Cybersecurity and data privacy risks are existential in healthcare. Indegene handles some of the most sensitive data in the world—clinical trial results, patient information, proprietary drug development data. A single major breach could destroy decades of trust-building. The SolarWinds hack showed how supply chain attacks can compromise even the most security-conscious organizations. As a vendor to multiple pharmaceutical companies, Indegene is an attractive target for state-sponsored hackers and criminal organizations.

The innovation dilemma is subtle but real. Indegene's business model depends on deep, long-term client relationships. But innovation often requires disrupting existing relationships and cannibalizing current revenue. Can Indegene truly innovate while keeping existing clients happy? History suggests this is one of the hardest challenges for successful companies.

Market saturation is approaching in core services. Indegene already works with all top 20 pharmaceutical companies. Where does growth come from when you've captured the entire addressable market? The answer—emerging biotech and medical devices—comes with its own challenges: smaller deal sizes, higher client acquisition costs, and increased revenue volatility.

The post-IPO pressure is already visible. Q1 FY26 results: 1.8% USD revenue growth, stable margins shows slowing growth rates. Public markets are unforgiving. They expect consistent quarterly growth, margin expansion, and guidance beats. This pressure could force Indegene to make short-term decisions that compromise long-term value creation.

The geopolitical risks are escalating. US-China tensions could force Indegene to choose sides, potentially losing access to one of the largest pharmaceutical markets. India-Pakistan tensions could disrupt operations. The rise of healthcare nationalism—countries wanting healthcare data and operations to remain domestic—could fragment Indegene's global delivery model.

Yet for all these risks, Indegene has demonstrated remarkable resilience. They survived the dot-com crash, 9/11, the 2008 financial crisis, and COVID-19. Each crisis made them stronger. The question isn't whether challenges will come—they will. The question is whether the company that built itself through patient execution can maintain that discipline under the harsh spotlight of public markets.

Epilogue: The Boring Revolution

As we close this deep dive into Indegene, it's worth reflecting on what this company represents for Indian entrepreneurship and the global healthcare industry. In an era obsessed with disruption, Indegene chose evolution. In a time of blitzscaling, they chose patient growth. While others chased valuations, they chased value creation.

The story of Indegene is ultimately a story about the power of focus, patience, and execution. Five engineers from India's premier institutions could have built anything—a consumer internet company, an e-commerce platform, a fintech startup. Instead, they chose one of the most complex, regulated, and slow-moving industries in the world. And through 26 years of disciplined execution, they built something remarkable: a company that is indispensable to how modern pharmaceutical companies operate.

Market Cap ₹ 13,748 Cr might seem modest compared to consumer tech unicorns. But Indegene's value isn't just in its market capitalization—it's in the drugs that reach patients faster because of their clinical trial automation, the physicians who make better treatment decisions because of their medical education platforms, and the healthcare costs that are lower because of their efficiency improvements.

The next chapter of Indegene's story is being written now. Will they achieve their $500 million revenue target? Will AI transform them from a services company to a product company? Will they maintain their culture and execution discipline as a public company? These questions remain open.

But one thing is certain: Indegene has proven that you can build a global technology leader from India without following the Silicon Valley playbook. You can create massive value without burning massive capital. You can revolutionize an industry without disrupting it. Sometimes, the most radical thing you can do is execute the basics extraordinarily well, consistently, for decades.

For investors evaluating Indegene, the question isn't whether it's a good company—it clearly is. The question is whether the qualities that made it successful in the past—patience, discipline, focus—will be assets or liabilities in the AI-accelerated future of healthcare. The answer to that question will determine whether Indegene becomes India's first healthcare technology decacorn or remains a successful but ultimately limited regional player.

The boring revolution continues. And sometimes, boring changes the world.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube