IIFL: India's Financial Services Transformation Story

I. Introduction & Episode Roadmap

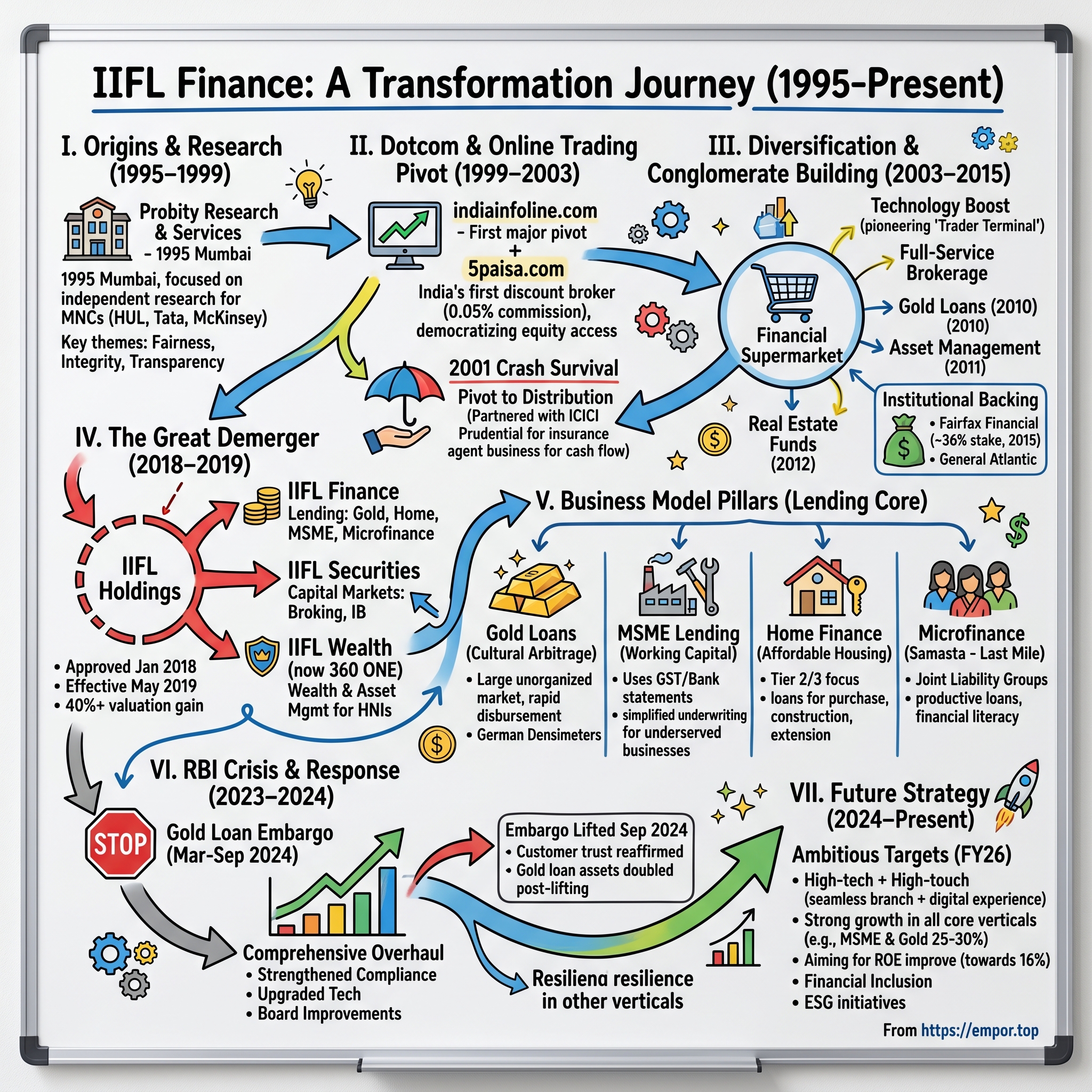

The year is 1995. India's economy is just four years into liberalization, and the old certainties of the License Raj are crumbling. In a modest Mumbai office, a young IIM Ahmedabad graduate named Nirmal Jain is about to make a bet that will transform him from a research analyst into one of India's most successful financial entrepreneurs. This is the story of IIFL Finance Limited—how a two-person research firm became a financial powerhouse ranked among India's top seven financial conglomerates, survived multiple crises, split into three listed entities, and emerged from regulatory storms stronger than ever.

What makes IIFL's journey remarkable isn't just its scale—though managing ₹78,341 crore in assets across 4,900 branches is impressive. It's the sheer audacity of transformation: from producing research reports for multinationals to pioneering online trading at 5 paisa when competitors charged 100 times more, from selling insurance as agents to lending against gold in rural India, from a single entity to three specialized listed companies. This is entrepreneurship in the crucible of modern India—navigating liberalization, technology disruption, regulatory upheaval, and the eternal challenge of serving a billion aspirations.

Our narrative unfolds across three decades of Indian capitalism. We'll explore how Nirmal Jain spotted opportunity in information asymmetry, why he pivoted from research to trading during the dotcom boom, how IIFL survived the 2001 crash by becoming India's first corporate insurance agent, and the strategic logic behind the dramatic 2019 demerger. We'll dissect the four-pillar lending model—gold loans to rural India, MSME credit in tier-2 cities, affordable home finance, and microfinance through Samasta. And we'll confront the elephant in the room: the 2024 RBI embargo that halted gold loans for six months, slashed profits by 71%, and tested whether three decades of trust-building could withstand regulatory censure.

This isn't just IIFL's story—it's a window into India's financial democratization. From research house to conglomerate to focused entities, each transformation mirrors the evolution of Indian capitalism itself. Let's begin where it all started: with a simple observation about the hunger for information in a newly liberalized economy.

II. Origins & The Research House Beginning (1995–1999)

October 18, 1995. The Bombay Stock Exchange is still recovering from Harshad Mehta's securities scam three years prior. Foreign institutional investors are tentatively entering Indian markets. And Nirmal Jain, armed with an IIM Ahmedabad degree and experience at Hindustan Lever, incorporates a company called Probity Research and Services Private Limited. The name itself—Probity, meaning integrity and uprightness—hints at the founding ethos that would later crystallize as "FIT": Fairness, Integrity, Transparency.

Jain wasn't trying to build a financial conglomerate. His vision was narrower but profound: produce high-quality, unbiased, independent research on the Indian economy, businesses, industries, and corporates. In 1995, this was revolutionary. The License Raj had just ended in 1991, and information was still hoarded, manipulated, or simply unavailable. Foreign investors needed reliable data on Indian companies. Indian corporates needed sectoral analysis to navigate newly competitive markets. The government's monopoly on economic intelligence was cracking, creating a vacuum that private research could fill.

The early days were lean but promising. Working from a small office with minimal staff, Jain began producing what would become Probity's signature products: the Probity 200 Company Reports—comprehensive analyses of India's leading corporations; Economy Probe—macroeconomic assessments of India's liberalizing economy; and detailed Sector Reports covering everything from textiles to telecommunications. The quality caught attention. Within two years, marquee clients lined up: Hindustan Lever (Jain's former employer), multiple Tata Group companies seeking competitive intelligence, CRISIL needing specialized research support, McKinsey requiring local market insights, and even public sector giants like State Bank of India and foreign banks like Citibank. What set Jain apart was his unique combination of credentials—a rank-holder Chartered Accountant, Cost Accountant, and PGDM from IIM Ahmedabad. After starting his career in 1989 with Hindustan Unilever as a commodities trader, he understood both the operational complexities of Indian business and the information gaps that plagued decision-making. His research wasn't academic theorizing—it was practical intelligence designed for executives making real capital allocation decisions.

The late 1990s context is crucial. India's GDP was growing at 6-7% annually, foreign direct investment had jumped from $103 million in 1990-91 to $3.5 billion by 1997-98, and the number of listed companies on BSE had doubled. Yet reliable information remained scarce. Government statistics lagged by months. Company disclosures were minimal. Brokerage research was often compromised by investment banking relationships. Probity positioned itself as the antidote—independent, rigorous, and timely.

By 1999, Jain sensed a bigger opportunity. The internet was arriving in India—only 0.2% of Indians were online, but that meant 2 million potential users in a billion-person market. Financial markets were evolving—the National Stock Exchange had launched electronic trading in 1994, dematerialization of shares began in 1996, and retail participation was growing. The research firm had built credibility and relationships, but Jain saw that merely analyzing markets wasn't enough. The real opportunity lay in participating in them, in democratizing access to financial services the way liberalization had democratized access to consumer goods.

The decision to pivot from pure research to becoming a market participant would transform everything. In 1999, as Y2K fears gripped global markets and India's Kargil conflict rattled investors, Jain registered the domain indiainfoline.com. The research house was about to enter the arena it had been studying. What happened next would either vindicate his vision or destroy the credibility Probity had painstakingly built.

III. The Dotcom Era & Online Trading Revolution (1999–2003)

The Mumbai headquarters buzzed with a different energy in 1999. Engineers hunched over computers, debugging code. Customer service representatives fielded calls about internet connections. And at the center of it all, Nirmal Jain was orchestrating one of India's first major pivots from offline to online. The website indiainfoline.com went live that year—not just as a digital brochure for Probity's research, but as a portal to democratize financial information and, soon, financial transactions themselves.

The timing seemed perfect. The NASDAQ was soaring, reaching 5,048 points by March 2000. Indian IT stocks were discovering their global potential—Infosys had listed on NASDAQ in 1999, Wipro was expanding aggressively. The Indian middle class, estimated at 300 million people, was beginning to view equity investment not as gambling but as wealth creation. And internet penetration, while still minimal, was doubling annually. Into this ferment, IIFL launched what would become its signature disruption: 5paisa.

The name itself was audacious. In 2000, traditional brokers charged 1-1.5% commission on trades. For a ₹10,000 transaction, that meant ₹100-150 in fees. IIFL's 5paisa platform charged 0.05%—just ₹5 for the same trade. This wasn't a marginal improvement; it was a 95% cost reduction that made small trades economically viable for the first time. A schoolteacher could buy 10 shares of Reliance without fees eating her returns. A small businessman could build a portfolio gradually without hemorrhaging money to intermediaries. The validation came quickly. CDC was the first private equity firm to invest in India Infoline, funding US$1 Mn—modest by today's standards but transformative for a five-year-old company trying to build India's financial infrastructure. Intel and other investors provided growth capital, attracted by the audacious vision of democratizing equity markets in a country where less than 2% of the population invested in stocks.

But 2001 brought catastrophe. The NASDAQ crashed from 5,048 to 1,114 points—a 78% decline. Indian tech stocks collapsed. Retail investors who'd mortgaged homes to buy Himachal Futuristic and Zee Telefilms watched their wealth evaporate. For IIFL, which had bet everything on online trading adoption, "sustaining became tough". The company was burning cash, the 5paisa model wasn't generating sufficient revenue at such low volumes, and the entire premise of retail equity participation seemed flawed.

Jain's response revealed the strategic flexibility that would define IIFL's next two decades. Rather than doubling down on a failing model or shutting down, he pivoted to distribution. The organisation decided to tie-up with ICICI Prudential, thus putting to use its distribution network and becoming India's first corporate agent for insurance. This wasn't glamorous—selling life insurance policies through the same network built for equity trading—but it generated cash flow, kept the lights on, and most importantly, maintained customer relationships through the downturn.

The insurance pivot taught IIFL a crucial lesson: Indian consumers needed a full spectrum of financial products, not just equity trading. A middle-class family might trade stocks occasionally, but they needed insurance regularly, loans periodically, and wealth management eventually. The dotcom crash, rather than destroying IIFL, forced it to evolve from a mono-line online broker into something more ambitious—a financial supermarket serving all of India's emerging financial needs.

By 2003, as markets recovered and India's GDP growth accelerated past 7%, IIFL was ready for its next transformation. The company had survived the dotcom bust, built a distribution network during the downturn, and learned to cross-sell multiple products. Now it was time to go from survival mode to expansion mode, from being a distributor of others' products to creating its own financial offerings.

IV. Expansion & Diversification: Building the Financial Supermarket (2003–2015)

The trading floor at IIFL's Mumbai headquarters in 2003 looked nothing like the sterile research office of 1995. Screens flickered with real-time prices, phones rang with client orders, and in a glass-walled room, engineers put finishing touches on what would become a game-changer: the 'Trader Terminal', pioneering technology built over 3 years. This wasn't just software—it was IIFL's declaration that it could compete with global financial firms on technology, bringing Bloomberg-like capabilities to retail investors at Indian price points.

The Trader Terminal epitomized IIFL's expansion strategy: democratize institutional-grade tools for retail clients while building capabilities to serve institutions directly. As India's economy roared—GDP growth averaged 8.5% between 2003-2007—IIFL transformed from a scrappy survivor into a diversified financial conglomerate. The company became a full-service broker, offering research, trading, and wealth management. But Jain saw a bigger opportunity: lending.

The entry into lending wasn't random. IIFL's distribution network—built during the dotcom bust to sell insurance—gave it presence in tier-2 and tier-3 cities where banks barely operated. These weren't Mumbai and Delhi elites trading derivatives; they were small businessmen needing working capital, families buying first homes, and farmers whose only asset was ancestral gold. In 2010, IIFL entered the gold loan market—a ₹600 billion industry growing at 31% annually, dominated by unorganized pawnbrokers charging usurious rates. By 2011, it incorporated IIFL Asset Management, and by 2012, it was releasing real estate investment instruments.

The transformation accelerated with institutional backing. In 2015, Canadian billionaire Prem Watsa's Fairfax Financial made an open offer for IIFL shares, acquiring ~26% stake, with post-offer aggregate shareholding going to 35.7%. Watsa, known as "Canada's Warren Buffett," saw in IIFL what he'd seen in other emerging market financial services plays—a trusted brand serving an underbanked population in a rapidly growing economy. The Fairfax investment, along with backing from General Atlantic and CDC Group, provided not just capital but credibility.

By 2015, IIFL had evolved far from its research house origins. It was simultaneously an online broker competing with ICICI Direct, a wealth manager serving high-net-worth individuals, a gold loan company competing with Muthoot Finance, a home finance provider targeting affordable housing, and an institutional broker serving foreign investors. The company operated across the entire financial services value chain—from a farmer pledging gold jewelry in rural Karnataka to a hedge fund trading Indian equities from Connecticut.

This conglomerate structure had advantages: cross-selling opportunities, diversified revenue streams, and economies of scale. A client who took a gold loan might open a trading account; a wealth management client might need a home loan. But by 2017, the structure was showing strain. Each business had different capital requirements, regulatory oversight, and growth trajectories. The gold loan business needed branch expansion and working capital. The wealth management business needed technology and talent. The capital markets business needed regulatory compliance and risk management systems.

More fundamentally, each business served different customer segments with different needs. The rural customer pledging gold had nothing in common with the ultra-high-net-worth individual seeking portfolio management. The MSME owner needing working capital operated in a different universe from the institutional investor seeking equity research. IIFL was trying to be everything to everyone, and increasingly, that was becoming impossible. The solution would be radical: split the company into three focused entities, each with its own management, strategy, and stock listing.

V. The Great Demerger: Creating Three Listed Entities (2018–2019)

January 31, 2018. The boardroom at IIFL's headquarters witnessed one of Indian finance's most ambitious corporate restructurings. After months of deliberation, the directors approved a plan that would essentially destroy the conglomerate they'd spent two decades building—to create something better. The strategy: split IIFL Holdings into three independent listed companies, each laser-focused on its core competency.

The logic was compelling. Each core business had acquired critical mass requiring flexibility and independence; distinct customer sets; different ways of working, culture and critical success factors. The wealth management business, serving India's ultra-rich, needed a boutique culture, personalized service, and global investment capabilities. The capital markets business, competing with discount brokers and fintechs, needed technology, speed, and scale. The lending business, operating in rural markets and urban slums, needed physical presence, credit assessment capabilities, and collection infrastructure.

Under the conglomerate structure, these businesses were cannibalizing each other's resources and management attention. Capital allocation decisions became political battles. Regulatory requirements for one business constrained others. The market couldn't properly value such a complex entity—was IIFL a lending company trading at book value or a wealth manager deserving premium valuations? The demerger would solve these problems by creating pure-play entities that investors could evaluate independently.

The execution was complex corporate gymnastics. IIFL Holdings would be renamed IIFL Finance Limited, retaining the lending businesses—gold loans, home finance, business loans, and microfinance. IIFL Wealth Management would house the wealth and asset management businesses, targeting India's growing millionaire class. IIFL Securities would contain capital markets operations—broking, distribution, and investment banking. Each entity would get proportionate assets, liabilities, and employees. Shareholders would receive shares in all three companies, maintaining their economic interest while gaining focused exposure.

Regulatory approvals took over a year. The Reserve Bank of India had to approve the NBFC restructuring. SEBI had to clear the capital markets separation. The National Company Law Tribunal had to bless the scheme of arrangement. By May 13, 2019, the reorganization became effective. IIFL Securities Limited and IIFL Wealth Management Limited were demerged and independently listed in September 2019. IIFL Holdings Limited was renamed as IIFL Finance Limited.

The market reaction validated the strategy. Post-demerger, the combined market capitalization of the three entities exceeded the pre-demerger valuation by over 40%. IIFL Wealth, rebranded as 360 ONE, commanded premium valuations as a pure-play wealth manager. IIFL Securities could pursue aggressive digital strategies without worrying about lending regulations. And IIFL Finance could focus on its core lending verticals without the complexity of managing unrelated businesses.

For Nirmal Jain, the demerger represented philosophical evolution. The entrepreneur who'd built a conglomerate to capture India's financial services opportunity now recognized that focused execution trumped diversified presence. In interviews, he compared it to raising children—at some point, they need independence to reach their potential. The demerger wasn't dismantling IIFL's legacy; it was unleashing it.

VI. Business Model Deep Dive: The Four Pillars

Walk into any of IIFL Finance's 4,900 branches and you'll witness India's financial inclusion in action. In a Rajasthan village, a farmer pledges gold jewelry inherited from his grandmother to fund his daughter's engineering education. In a Mumbai suburb, a small garment manufacturer gets working capital without the weeks-long documentation banks demand. In Tamil Nadu, a daily wage worker receives a microfinance loan to buy a sewing machine. These aren't just transactions—they're the building blocks of IIFL Finance's four-pillar lending model, each targeting massive, underserved markets.

Gold Loans: The Cultural Arbitrage

Indians own 25,000 tonnes of gold—roughly $1.5 trillion at current prices, more than the GDP of Australia. This isn't just investment; it's cultural identity, social security, and intergenerational wealth. Indians regard gold as vital symbol of social status, financial security; households prefer using gold as collateral rather than liquidating. IIFL recognized that this cultural attachment created a massive lending opportunity. Families would never sell ancestral gold, but they'd temporarily pledge it for liquidity.

The gold loan market exploded from ₹600 billion in FY2009-10 to ₹9,000 billion in FY2019-20, a 31.1% CAGR. IIFL differentiated through speed and trust. While unorganized pawnbrokers took days and charged 36-48% interest, IIFL disbursed loans in 30 minutes at 12-24% rates. The company built specialized branches with German-manufactured Densimeter machines for instant gold purity testing, fireproof vaults with biometric access, and trained relationship managers who understood that they weren't just handling collateral—they were safeguarding family heritage.

MSME Lending: Solving the Working Capital Crisis

India has 63 million MSMEs contributing 30% of GDP, yet 80% operate outside formal credit channels. Banks find them too risky; loan amounts too small to justify underwriting costs. This creates an unmet credit demand of ₹20-25 lakh crore, forcing businesses to borrow from informal lenders at crushing rates or stunting growth for lack of capital.

IIFL's MSME lending leverages its distribution network and simplified underwriting. Instead of demanding three years of audited financials, IIFL uses GST returns, bank statements, and on-ground verification. Loan officers visit businesses, assess inventory, talk to suppliers and customers. It's high-touch, relationship banking that technology alone can't replicate. During FY25, despite regulatory challenges, IIFL achieved ₹9,430 crore in new MSME disbursals, proving the model's resilience.

Home Finance: Affordable Housing Revolution

IIFL Home Finance targets a specific segment: families earning ₹25,000-50,000 monthly, buying homes worth ₹15-50 lakhs, often in tier-2 cities or urban peripheries. These aren't slum redevelopment projects or luxury apartments—they're modest flats for teachers, clerks, and small businessmen achieving their middle-class dream. Traditional banks find these tickets too small; housing finance companies find these customers too risky. IIFL found opportunity in this gap.

The home finance vertical doesn't just provide purchase loans but also construction finance for self-built homes and loans for extension and improvement. In rural areas where land ownership is clear but construction quality varies, IIFL's technical teams assess property value beyond standard metrics. They understand that a home isn't just collateral—it's aspiration crystallized in concrete.

Microfinance: The Last Mile

Through IIFL Samasta (formerly Samasta Microfinance), IIFL reaches India's poorest—daily wage workers, vegetable vendors, and cottage industry operators. These loans average ₹30,000-40,000, requiring weekly collection and intensive customer engagement. 93% of loans are directed toward productive purposes, with 86% of customers from economically weaker sections having annual incomes below ₹3 lakh.

The microfinance model depends on joint liability groups—five women cross-guarantee each other's loans, creating social pressure for repayment. IIFL Samasta's field officers conduct weekly center meetings, not just for collection but for financial literacy training. They teach budgeting, savings, and basic accounting. It's labor-intensive, low-margin business that requires massive scale to generate returns. But it's also IIFL's most direct contribution to financial inclusion—bringing formal credit to those who've never entered a bank.

Each pillar serves different demographics, geographies, and needs, but they share common threads: focus on underserved segments, leverage of physical distribution, and emphasis on relationship over pure technology. While fintechs promise algorithmic lending, IIFL Finance proves that in India's diverse, complex markets, human judgment and physical presence remain irreplaceable.

VII. The RBI Crisis & Recovery (2023–2024)

March 4, 2024. The Reserve Bank of India's press release landed like a bombshell: IIFL Finance was barred from disbursing gold loans with immediate effect. No new customers, no fresh loans against gold, no increasing limits on existing loans. For a company generating significant revenue from gold lending, this wasn't just regulatory action—it was an existential crisis. The stock crashed 20% in minutes. Competitors circled like vultures. And in branches across India, customers and employees wondered if three decades of trust-building had evaporated overnight.

The RBI's action followed concerns about supervisory compliance, particularly around gold loan practices and valuation methods. While the specific violations weren't publicly detailed, market whispers suggested issues with loan-to-value ratios, gold valuation practices, and cash disbursements. For IIFL, which prided itself on the "FIT" philosophy—Fairness, Integrity, Transparency—the regulatory censure was particularly stinging.

But this wasn't IIFL's first crisis. The company had survived the dotcom crash, the 2008 financial crisis, demonetization, and COVID-19. Each time, it emerged stronger by addressing root causes rather than symptoms. The RBI embargo triggered a comprehensive overhaul: strengthening compliance systems, upgrading technology infrastructure, retraining staff, and implementing additional checks and balances. Management didn't just fix problems—they rebuilt processes from the ground up.

The financial impact was severe. FY25 consolidated PAT fell 71% from FY24, with ROE dropping to 3.4%. Gold loan disbursements went to zero for six months. Customers migrated to competitors. Employee morale plummeted. Yet IIFL Finance didn't resort to fire sales or panic cost-cutting. Instead, it used the embargo period to strengthen other verticals—MSME lending grew 25%, home finance expanded steadily, and the company maintained its distribution network intact.

September 19, 2024, marked redemption. The RBI lifted the embargo after IIFL demonstrated compliance improvements. What happened next stunned skeptics: gold loan assets doubled in six months following the lifting of embargo. Customers who'd stayed away during the embargo returned in droves. The gold loan business surged to new peaks in loan AUM, reaffirming customer trust. By Q4FY25, the recovery was remarkable: loan AUM reached ₹78,341 crore, growing 10% QoQ, with PAT of ₹251 crore representing a 208% increase quarter-on-quarter.

The crisis also catalyzed governance improvements. IIFL strengthened its board with independent directors, enhanced risk management frameworks, and implemented real-time monitoring systems. The company adopted a "compliance-first" culture where regulatory adherence trumped growth targets. Regular audits, mystery shopping exercises, and whistleblower mechanisms ensured early detection of potential issues.

Interestingly, IIFL's response contrasted with typical corporate crisis management. There were no aggressive public relations campaigns, no blame games, no litigation against regulatory action. Instead, the company acknowledged shortcomings, fixed problems systematically, and let results speak. This approach—humble, methodical, focused—resonated with stakeholders who'd seen too many financial firms deflect responsibility during crises.

The RBI episode, while painful, ultimately strengthened IIFL Finance. It forced introspection, drove operational improvements, and demonstrated resilience. Most importantly, it proved that customer relationships built over decades could survive regulatory storms if the underlying business model remained sound and management responded with integrity.

VIII. Current State & Future Strategy (2024–Present)

Stand outside IIFL Finance's branch in Nashik on a Monday morning, and you'll see the future of Indian lending. Farmers queue with gold ornaments, using the new QR-code based queue management system. Small factory owners upload GST returns through the mobile app for instant loan approval. First-time homebuyers video-call loan officers for documentation guidance. This seamless blend of physical presence and digital capability defines IIFL's current strategy—high-tech and high-touch, serving India's diverse financial needs.

The numbers tell a story of remarkable recovery and ambitious growth. Post-embargo, IIFL Finance has roared back to life. The company's network of approximately 4,900 branches across 500+ cities gives it one of India's widest financial services footprints outside the public sector banks. But unlike traditional NBFCs that choose between physical and digital, IIFL invests aggressively in both—branches for trust and service, technology for efficiency and scale.

The growth targets for FY26 reflect management's confidence: home loans growing 15-18%, gold loans and MSME loans expanding 25-30% each, and microfinance growing 5-10%. These aren't arbitrary numbers—they reflect massive market opportunities. India's housing shortage exceeds 20 million units. MSME credit gap remains above ₹20 trillion. Gold loans penetration is still below 15% of pledgeable gold. IIFL is targeting ROE improvement from 3.4% in FY25 to approximately 16% in FY26—a return to historical profitability levels but with stronger governance and risk management.

Technology investments focus on three areas: customer acquisition, risk assessment, and operational efficiency. The company's mobile app allows instant gold loan applications with doorstep service in select cities—upload gold photos, get preliminary valuation, and have an executive visit for final assessment and disbursement. For MSME loans, artificial intelligence analyzes GST returns, bank statements, and bureau data to generate instant credit scores. Robotic process automation handles routine documentation, freeing relationship managers for customer engagement.

But technology isn't replacing IIFL's human-centric model—it's amplifying it. Branch managers still visit MSME clients' businesses. Gold loan officers still handle family heirlooms with reverence. Microfinance field officers still conduct weekly group meetings. Technology handles the routine; humans handle the relationships. This hybrid model proves particularly effective in India, where trust matters as much as convenience.

Competition has intensified across all segments. In gold loans, Muthoot Finance and Manappuram remain formidable, while banks are becoming aggressive. In MSME lending, fintech lenders like Kinara Capital and Lending Kart offer instant digital loans. In home finance, Bajaj Housing Finance and banks dominate. Yet IIFL's diversified model provides resilience—when gold loans faced embargo, other verticals sustained growth. When COVID hit microfinance, gold loans boomed.

The company's ESG initiatives deserve mention. IIFL Finance serves 10 million customers, with significant representation from economically weaker sections. Its financial literacy programs have trained over 500,000 individuals. The company's rural presence brings formal credit to villages where moneylenders previously monopolized lending. This isn't corporate social responsibility as marketing—it's business model as social impact.

Looking ahead, IIFL Finance faces both opportunities and challenges. India's formal credit penetration remains below 30%, suggesting massive growth potential. Rising income levels, urbanization, and digitalization create favorable tailwinds. But regulatory scrutiny has intensified post-COVID, asset quality concerns persist in unsecured lending, and competition from banks and fintechs is escalating. Success requires balancing growth with governance, innovation with prudence, and scale with service quality.

IX. Playbook: Business & Investing Lessons

Three decades, multiple crises, and a transformation from research house to split conglomerate—IIFL's journey offers a masterclass in building financial services businesses in emerging markets. These aren't theoretical frameworks from business schools but battle-tested strategies that worked in India's chaotic, competitive, and high-growth environment.

Lesson 1: Survive First, Thrive Later

When the dotcom bubble burst in 2001, IIFL could have stubbornly stuck to online trading, burning cash until bankruptcy. Instead, Jain pivoted to insurance distribution—unglamorous but cash-generative. When demonetization killed cash transactions in 2016, IIFL accelerated digital adoption. When COVID struck, the company shifted to work-from-home while maintaining branch operations for essential services. Each crisis became a catalyst for evolution rather than extinction.

The survival instinct shapes capital allocation too. IIFL maintains higher liquidity buffers than regulations require, diversifies funding sources across banks, capital markets, and international investors, and never bets the company on a single product or segment. This conservatism might reduce returns during boom periods but ensures survival during busts—and in financial services, survival is the prerequisite for compound growth.

Lesson 2: The Demerger Decision Matrix

IIFL's 2019 split provides a framework for when conglomerates should divide: when business units serve fundamentally different customers (rural gold loan borrowers vs. ultra-HNI wealth clients), when regulatory requirements conflict (RBI rules for NBFCs vs. SEBI rules for brokers), when capital needs diverge (asset-heavy lending vs. asset-light broking), and when management bandwidth becomes a constraint. The demerger wasn't failure—it was evolution, recognizing that focused execution beats diversified presence.

Lesson 3: Trust as Moat

In financial services, trust is the ultimate competitive advantage. Technology can be replicated, products commoditized, and prices matched—but trust takes decades to build and seconds to destroy. IIFL's "FIT" philosophy—Fairness, Integrity, Transparency—isn't just corporate rhetoric. It manifests in refusing to mis-sell insurance for higher commissions, maintaining gold loan collateral even when customers default, and accepting regulatory actions without deflection or litigation.

The trust dividend compounds over time. Customers who took gold loans in 2010 now seek home loans. Entrepreneurs who borrowed for working capital now need wealth management. Second-generation family members inherit not just assets but relationships with IIFL. In India's relationship-driven society, this trust creates switching costs that pure digital players can't overcome with convenience alone.

Lesson 4: Physical + Digital, Not Physical vs. Digital

While fintechs preached "digital-only" and traditional lenders defended branches, IIFL chose both. Branches provide trust, service, and local knowledge—crucial when lending against gold jewelry or assessing MSME creditworthiness. Digital provides convenience, efficiency, and scale—essential for acquiring younger customers and reducing operational costs. The hybrid model proves particularly effective in India, where smartphone penetration coexists with preference for face-to-face financial interactions.

Lesson 5: Regulatory Navigation

Operating in India's heavily regulated financial sector requires a specific mindset: view regulations as features, not bugs. RBI rules prevent reckless lending that could destroy the system. SEBI regulations protect retail investors from exploitation. Rather than regulatory arbitrage, IIFL practices regulatory partnership—engaging with regulators, implementing guidelines proactively, and accepting enforcement actions as learning opportunities.

The RBI embargo, while painful, demonstrated this philosophy. Instead of legal challenges or public confrontation, IIFL fixed problems, strengthened compliance, and emerged stronger. This approach builds long-term regulatory relationships that matter more than short-term wins.

Lesson 6: Capital Allocation in Lending

IIFL's four-pillar model demonstrates sophisticated capital allocation. Gold loans offer high returns but face regulatory scrutiny. MSME loans provide growth but carry credit risk. Home loans generate stable returns but require patient capital. Microfinance serves social purposes but operates on thin margins. The portfolio approach—balancing risk, return, and social impact—creates resilience that mono-line lenders lack.

X. Analysis & Bear vs. Bull Case

Strip away the narrative and examine IIFL Finance purely as an investment proposition. You find a recovered NBFC trading at relatively modest valuations, operating in markets with massive growth potential, but facing regulatory overhangs and competitive pressures. The investment case isn't straightforward—it requires weighing exceptional opportunities against non-trivial risks.

Bull Case: The Demographic Dividend Play

India's financial services penetration tells a story of enormous untapped potential. Formal credit reaches less than 30% of the population. Only 3% of Indians have used organized gold loans despite holding $1.5 trillion in gold. MSME credit gap exceeds ₹20 trillion. Housing shortage surpasses 20 million units. These aren't incremental growth opportunities—they're generational expansion possibilities.

IIFL Finance's positioning captures this opportunity uniquely. Its 4,900-branch network provides physical presence where digital-only players can't operate. Its technology investments enable efficiency that traditional NBFCs lack. Its diversified lending model provides resilience that mono-line players miss. Post-embargo, the company has demonstrated both operational improvement and customer loyalty, with gold loans surging to record levels.

The financial trajectory supports optimism. Management guides ROE improvement from 3.4% to 16% in FY26—not through aggressive lending but through normalized operations post-embargo. The loan book can compound at 20-25% annually for years given market opportunities. Operating leverage should expand margins as technology investments mature. And valuation remains reasonable compared to historical levels and peer multiples.

Consider the competitive moat: 30-year brand reputation in financial services, relationships with 10 million customers across income segments, integrated physical-digital distribution platform, and demonstrated ability to survive multiple crises. While fintechs grab headlines, IIFL quietly compounds—adding branches, acquiring customers, and deepening relationships.

Bear Case: The Regulatory Sword

The RBI embargo wasn't IIFL's first regulatory issue. In June 2023, SEBI passed an order restraining IIFL from accepting new clients for two years and imposing a ₹2 crore penalty for mixing clients' funds with own funds and using credit balance clients' funds to fund trades of debit balance clients and own trades. Though the Securities Appellate Tribunal set aside SEBI's order, reduced the penalty to ₹20 lakh, and said there was no misuse of client funds, the pattern suggests aggressive growth sometimes conflicts with regulatory compliance.

Indian financial regulation is tightening post-COVID. The RBI worries about NBFCs' systemic risk, periodically adjusting risk weights, provisioning norms, and exposure limits. Any future regulatory action could again halt growth, damage reputation, and destroy shareholder value. For investors, this regulatory sword of Damocles hangs perpetually.

Competition intensifies across all segments. Banks, flush with deposits, are aggressively entering gold loans and MSME lending. Fintech lenders, backed by venture capital, offer instant loans through apps. Large NBFCs like Bajaj Finance expand into IIFL's territories. Payment companies like Paytm morph into lenders. The competitive intensity suggests margin compression and market share battles ahead.

Asset quality remains concerning, particularly in unsecured lending. While IIFL's secured focus provides comfort, economic downturns affect all lenders. India's household debt is rising, informal sector employment remains fragile, and global economic uncertainty persists. A serious recession could spike non-performing assets across the portfolio.

Execution risk looms large. Expanding from ₹78,341 crore to ₹100,000+ crore loan book requires originating quality assets, maintaining collection efficiency, managing operational complexity, and avoiding regulatory missteps. The planned ROE expansion assumes flawless execution—a heroic assumption given IIFL's recent challenges.

Comparative Analysis

Against pure-play gold loan companies like Muthoot Finance (trading at 2.5x book) and Manappuram (2x book), IIFL Finance appears reasonably valued at around 1.5x book. However, Muthoot operates 5,800+ branches focused solely on gold loans, suggesting deeper expertise. Against diversified NBFCs like Bajaj Finance (trading at 6x book), IIFL looks cheap, but Bajaj's superior ROE (25%+) and track record justify premium valuations.

The investment decision ultimately depends on three beliefs: India's financial inclusion story remains intact despite near-term challenges; IIFL has genuinely strengthened governance post-embargo; and diversified lending models outperform mono-line strategies over cycles. If you believe all three, IIFL Finance offers compelling risk-reward. If any seem questionable, better opportunities exist elsewhere.

XI. Epilogue & Reflections

Walk through Mumbai's financial district today and you'll find IIFL's three entities occupying different buildings, pursuing independent strategies, competing for different customers. The research house that Nirmal Jain founded in 1995 has metamorphosed so completely that its original form seems almost mythical. Yet the thread connecting Probity Research to today's IIFL Finance isn't just corporate history—it's a mirror reflecting India's economic transformation.

When Jain started producing research reports for multinational clients, India's GDP was $360 billion. Today it exceeds $4 trillion. When 5paisa launched online trading at 5 paise, fewer than 2 million Indians invested in stocks. Today, over 100 million hold demat accounts. When IIFL entered gold loans, the organized market was ₹600 billion. Today it surpasses ₹9 trillion. Each transformation in IIFL's journey paralleled India's evolution from a closed, socialist economy to an open, aspirational market.

The 30-year arc from research house to conglomerate to focused entities teaches profound lessons about entrepreneurship in emerging markets. First, timing matters more than strategy. Jain didn't create demand for financial services—he recognized and captured demand that liberalization unleashed. Second, pivots aren't admissions of failure but adaptations to reality. The shift from research to trading to lending to demerger reflected changing market conditions, not managerial indecision.

Third, and perhaps most importantly, financial services in emerging markets is ultimately about trust, not technology. While Silicon Valley celebrates algorithmic lending and blockchain disruption, IIFL proves that in India, relationships matter. The branch manager who knows three generations of a family, the gold loan officer who handles jewelry with reverence, the microfinance field officer who conducts weekly meetings—these human connections create value that algorithms can't replicate.

The regulatory challenges IIFL faced—and survived—highlight another crucial lesson: in regulated industries, compliance isn't a cost center but a competitive advantage. Companies that view regulations as obstacles to arbitrage eventually face enforcement actions. Those that view regulations as frameworks for sustainable growth build lasting franchises. IIFL's response to the RBI embargo—fixing problems rather than fighting regulators—exemplifies this mature approach.

For investors, IIFL's story offers a framework for evaluating emerging market financial services. Look beyond growth rates to governance quality. Assess not just current profitability but crisis survival capability. Value distribution networks and customer relationships as much as technology platforms. And recognize that regulatory actions, while painful short-term, can catalyze long-term improvements if management responds appropriately.

The future of lending in India remains extraordinarily promising. Credit penetration will double over the next decade. Millions will enter the formal financial system. Technology will enable previously impossible lending models. But success won't come from technology alone or traditional methods alone—it will come from thoughtful integration of both, serving India's diverse population with products suited to their specific needs.

As we reflect on IIFL's three-decade journey, from Nirmal Jain's two-person research firm to three listed companies serving millions, the larger narrative emerges. This isn't just a corporate success story—it's a testament to India's economic potential, entrepreneurial energy, and financial democratization. The research house that began by analyzing India's economy became a participant in that economy's transformation, enabling millions to access credit, build wealth, and achieve aspirations.

The story continues to unfold. IIFL Finance, focused purely on lending, pursues aggressive growth while maintaining governance discipline. Will it achieve its ambitious targets? Can it avoid future regulatory issues? Will competition erode margins? These questions remain unanswered. But if history provides guidance, betting against IIFL's ability to adapt, survive, and thrive seems unwise.

In the end, IIFL's greatest achievement isn't its financial performance or market capitalization. It's the democratization of financial services—making stock trading affordable for middle-class investors, providing credit to MSMEs ignored by banks, enabling rural families to monetize gold without losing it, and bringing millions into the formal financial system. That transformation, more than any financial metric, defines IIFL's legacy and India's future.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube