International Gemological Institute: The Alchemy of Trust and the Private Equity Masterclass

I. Introduction & The Masterstroke of Private Equity Arbitrage

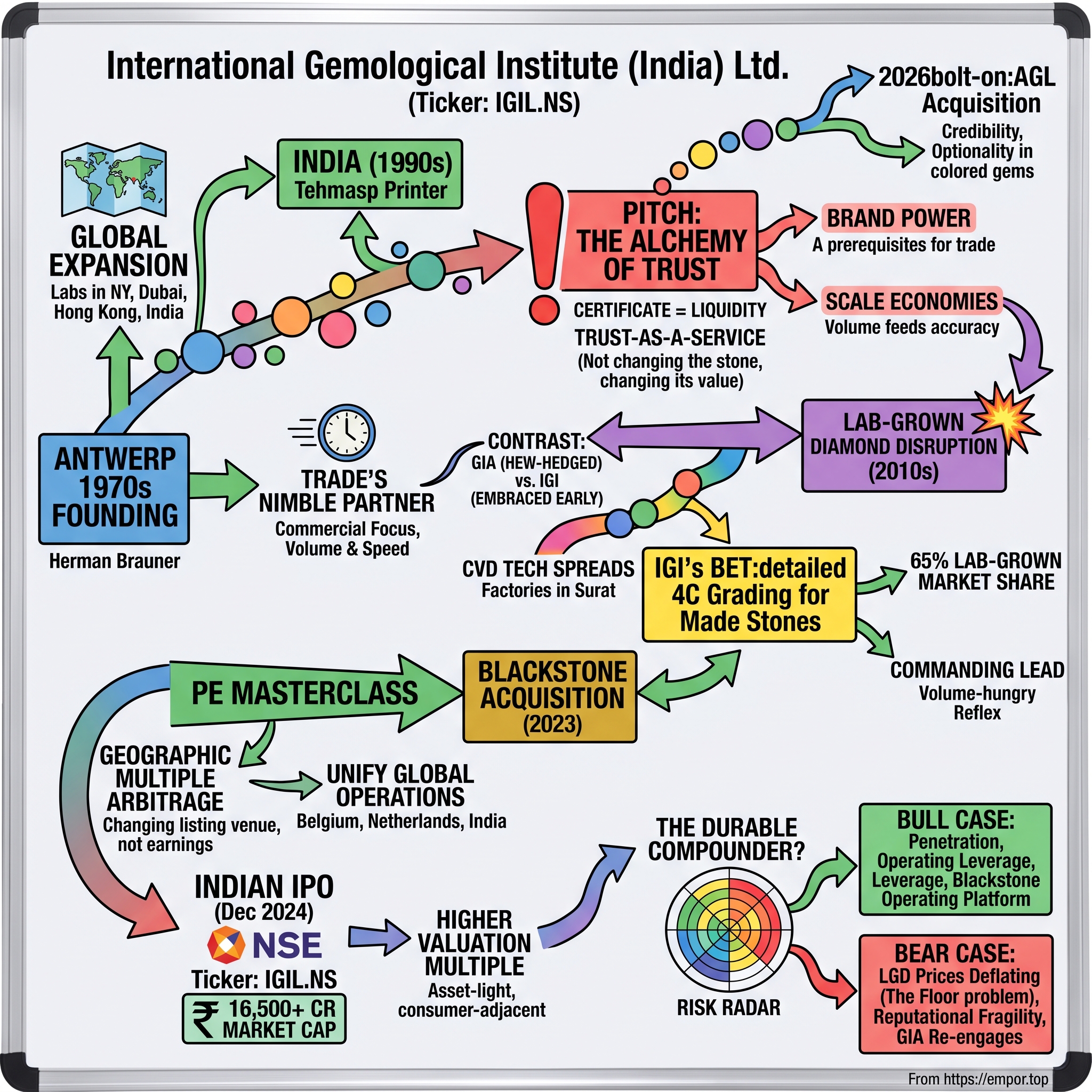

On a Mumbai trading floor in December 2024, a diamond dealer who had spent thirty years buying and selling stones by the fistful watched something he never expected to see: the laboratory that grades his inventory was ringing the opening bell as a listed company. For decades, gem certification had been the invisible plumbing of the jewelry trade — a fee you paid, a paper you filed, a stamp that let a stone move. Now that plumbing had a market capitalization of more than ₹16,500 crore, roughly two billion dollars, and its majority owner was one of the largest private equity firms on earth.

The story of how it got there is one of the cleaner private equity round-trips of the decade. In May 2023, funds managed by 黑石 Blackstone acquired the International Gemological Institute — a global gem-testing group founded in Antwerp — for about $570 million.12 Just eighteen months later, in December 2024, Blackstone floated the consolidated business on the National Stock Exchange of India as International Gemological Institute Limited, ticker IGIL.NS, in an offering that valued the company at an implied ₹16,545 crore.3 On paper, the value of a business that grades rocks had roughly tripled and a half in under two years. The obvious question — the one that animates this entire episode — is how.

Part of the answer is that gem certification is a strange and wonderful business. The physical object being certified does not change when the certificate is issued. A one-carat diamond is chemically identical before and after it passes through a laboratory. And yet the certificate is not a description of the asset — it is the asset's liquidity. Strip away the independent grading report and a polished diamond becomes an untradeable pebble that no dealer will finance, no retailer will display, and no consumer will trust. Certification is the closest thing the luxury world has to a supreme court: a third party whose verdict on carat, color, clarity, and cut settles what a stone is worth. That is a peculiar kind of power — the power to price something you do not own.

The second part of the answer is geography and multiples. The business Blackstone bought was headquartered in Belgium and the Netherlands, sold into a fragmented global trade, and would have been valued by European or American public markets as a sleepy testing-services company. But the center of gravity of the diamond world had moved. India cuts and polishes the overwhelming majority of the world's diamonds, and the Indian public market pays generously for asset-light, high-margin consumer-adjacent franchises. So Blackstone did not merely buy a company and sell it; it moved the company. It relisted a European testing group in Mumbai, next door to the world's dominant cutting-and-polishing ecosystem, and let a higher-multiple market re-rate the same cash flows. Call it geographic multiple arbitrage — the art of not changing what a business earns, only where it is priced.

There is a third layer worth naming up front, because it colors everything that follows: timing. Blackstone did not invent the lab-grown diamond boom, nor did it build IGI's fifty-year brand. What it did was recognize, in 2023, that three trends were about to converge — the explosion of Indian lab-grown manufacturing, the maturation of Indian public capital markets, and the world's growing appetite for asset-light "trust-as-a-service" franchises — and then position a single asset at the exact intersection of all three. Great private equity is often less about operational wizardry than about being early to a re-rating that others will only see in hindsight. The IGI trade is a case study in that discipline, and it is instructive precisely because so little about the underlying business changed. The stones still flowed. The labs still hummed. The reports still cost what they cost. Only the wrapper — and the wrapper's price tag — was transformed.

But a neutral observer has to resist being dazzled by the round-trip. A brilliant entry and a brilliant exit tell you that the seller and the structurer did well. They do not, by themselves, tell you that the business bought at ₹417 a share in December 2024 will compound for the patient investor who is still holding it years from now. Those are different questions with different answers, and keeping them separate is the whole discipline of this piece.

This episode walks through the whole arc: why gemology behaves like a software business with almost no marginal cost; the fifty-year rivalry with the Gemological Institute of America that shaped both firms; the single controversial bet on lab-grown diamonds that handed IGI a global lead; the financial engineering of the Indian listing; and, because Empor is not a shareholder letter, the skeptical stress test of whether any of this is durable. Because underneath the two-billion-dollar valuation sits an uncomfortable fact the bulls prefer not to dwell on — the very product driving IGI's volumes has been collapsing in price. We will get there. But first, the physics.

II. The Physics of Gemology: Why Grading is "Trust-as-a-Service"

Hold two one-carat stones in your palm. One was pulled from a mine in Botswana over a billion years after it formed. The other was grown in a stainless-steel reactor in Gujarat over about four weeks. Under a jeweler's loupe, in ordinary light, neither you nor a seasoned wholesale dealer can reliably tell them apart. Add a third stone that has been fracture-filled or laser-drilled to hide its flaws, and the confusion deepens. This is the central, uncomfortable truth of the gem trade: the buyer almost never knows what he is holding.

Economists have a term for this — asymmetric information — and in most markets it is a nuisance. In luxury goods it is the whole game. The classic academic treatment is George Akerlof's "market for lemons," which showed that when buyers cannot verify quality, they rationally assume the worst, offer only average prices, and thereby drive the best goods out of the market until only "lemons" remain. Diamonds are the platonic lemons problem: enormously valuable, visually indistinguishable across a huge quality and authenticity range, and increasingly imitable by machine. The seller knows the stone's true nature; the buyer does not; and without a trusted referee, the market should, in theory, unravel.

What prevents that unraveling is the certificate. An independent grading report converts a private secret into a public fact. It tells every subsequent buyer — the wholesaler, the retailer, the bride's father — exactly what the stone is, on a standardized scale everyone accepts. The report does not make the diamond more beautiful. It makes the diamond sellable. And crucially, the value of that report scales with how widely its issuer is trusted: a certificate from a lab no one has heard of solves nothing, because the next buyer down the chain will not accept it either. Trust in certification is therefore self-reinforcing in a way that looks a lot like a standard — the more the trade relies on a particular lab's reports, the more every participant must rely on them too, simply to transact with everyone else.

What actually happens inside the lab

It is worth demystifying the science, because the instruments are the reason the moat is not trivially copied. Distinguishing a natural diamond from a lab-grown one, or a treated stone from an untreated one, is not something the human eye can do — the atoms are the same. Instead, gemologists read the stone's fingerprint in light. Fourier-transform infrared spectroscopy (FTIR) shines infrared light through the stone and measures which wavelengths it absorbs, revealing trace impurities and growth features that betray a diamond's origin. Raman and photoluminescence spectroscopy excite the stone with a laser and read the faint light it re-emits, exposing the microscopic defects that natural and synthetic growth leave behind like tool-marks. Think of it as forensic ballistics for carbon: the stone looks identical, but the machine reads the signature of how it was made. These rigs are costly, the interpretation demands trained specialists, and both must be deployed at scale to be economic — which is exactly why grading concentrated in a handful of well-capitalized laboratories rather than dispersing across thousands of jewelers.

The certificate is the liquidity

This is why the industry treats a lab report the way finance treats a credit rating. A dealer in Surat financing inventory on a short-term line cannot afford to hold uncertified goods, because uncertified goods cannot be pledged, moved, or sold at a known price. The grading report is what turns a box of stones into working capital. That single dynamic — certificate as liquidity — is the source of nearly every advantage the certification business enjoys, and it deserves to be understood before any of the numbers, because all the numbers flow from it.

Two economic moats follow directly. The first is switching costs rooted in speed. Cutters and polishers operate on borrowed money and razor-thin turnaround windows; every day a parcel sits waiting for a certificate is a day of interest with no revenue. A laboratory that returns results in days rather than weeks, with a branch physically down the road, becomes woven into the manufacturer's financing calendar. Ripping it out to save a few rupees per stone would jam the whole production line. The switching cost, in other words, is not measured in the certification fee — which is small — but in the working capital that gets stranded when goods sit idle. That is a far stickier hold than any contract could provide.

The second moat is scale. Those spectroscopic rigs are expensive, and their cost is largely fixed. A laboratory grading millions of stones spreads that cost to almost nothing per report; a regional upstart grading thousands cannot. High volume is not just nice to have — it is the cost structure. And there is a subtler compounding effect: the more stones a lab grades, the larger its proprietary database of spectral signatures grows, which in turn makes its detection of new treatments and synthesis methods faster and more reliable than a smaller rival's. Volume feeds accuracy, and accuracy feeds trust, and trust feeds volume. It is not a network effect in the classic two-sided sense, but it rhymes with one.

Software-like margins, with a caveat

Put those together and you get economics that look less like a testing lab and more like a software company. The marginal cost of grading one additional stone, once the building and machines exist, is trivial — a few minutes of a trained gemologist's time and some electricity. Revenue is a fee per report. So as volume climbs, an enormous share of each incremental rupee drops to profit. IGI's disclosed financials bear this out: for the fifteen-month reporting period ended March 31, 2026, the consolidated business generated roughly ₹15,976 million of revenue at a group EBITDA margin near 61%, and in its January–March 2026 quarter the EBITDA margin ran just under 61% on quarterly revenue of about ₹3,686 million.45 These are margins most industrial companies can only dream about, and they are the real reason a rock-grading business can command a software-like valuation.

The caveat — and we will return to it with force — is that this beautiful operating leverage runs in both directions. It rewards rising volume spectacularly, and it punishes falling volume just as hard, because those fixed costs do not shrink when the parcels stop coming. For now, hold onto the mechanism: trust is the product, the certificate is the liquidity, and volume is the engine. To understand how IGI came to sit at that engine's controls, we have to go back to a cobblestoned street in Belgium.

III. The Antwerp Roots & Setting the Commercial Standard

Antwerp in the 1970s was the beating heart of the diamond world — a few dense blocks near the central railway station where an estimated majority of the planet's rough and polished stones changed hands, often on a handshake and the Yiddish-Flemish word mazel. Trust in that district was personal, tribal, and centuries old. Into this world, in 1975, Herman Brauner founded the International Gemological Institute, betting that the trade needed something the handshake could not scale: an independent, consistent, commercially minded laboratory sitting right where the diamonds already were.1

To appreciate why that was a real bet, you have to meet the incumbent. The Gemological Institute of America had been founded in 1931 by Robert M. Shipley, a Wichita jeweler turned evangelist who was appalled that his own profession had no scientific standards and, by many accounts, ashamed of how little he himself had known when he first sold gems. Shipley set out to professionalize the trade the way medicine and law had been professionalized — through education, credentials, and a common vocabulary. GIA invented the language the entire industry now speaks. The 4Cs — carat, color, clarity, and cut — were GIA's coinage, as was the D-to-Z color scale and the Flawless-to-Included clarity scale that grew from it. Owning the vocabulary is a quiet but profound form of power: it made GIA the reference point against which every other lab, including IGI, would forever be measured.

But GIA built itself as a nonprofit with the gravitas of a university — and, crucially, the pace of one too. It graded the stones that went to auction houses, estate sales, and the world's grandest retailers, and it optimized relentlessly for authority rather than throughput. It was rigorous, prestigious, expensive, and slow. If you were selling a rare stone to a collector, GIA's paper was worth the wait and the premium. If you were a working dealer trying to move mid-market goods on a financing clock, the wait itself was the problem. That single mismatch — between the prestige grader's cadence and the working trade's cash-flow reality — was the seam IGI was built to exploit.

The commercial attack

That gap was IGI's opening, and the Lorie family — who came to steward and scale the institute — drove straight through it. IGI positioned itself not as the austere academy but as the trade's nimble commercial partner. Where GIA measured turnaround in weeks, IGI promised days. Where GIA charged academic premiums suited to museum pieces, IGI priced for high volume and the mid-market wholesale trade that made up the vast bulk of the world's actual diamond business. It was a classic disruption from below: take the segment the prestige incumbent found unglamorous — fast, cheap, high-volume grading — and serve it so well that the incumbent chooses not to fight for it.

This is worth pausing on, because it defined IGI's DNA in a way that mattered decades later. GIA optimized for prestige and treated speed as a compromise. IGI optimized for the working trade and treated speed as the product. Neither was wrong. But the two firms were building fundamentally different reflexes — one cautious and reputation-guarding, the other commercial and volume-hungry — and when a genuinely disruptive technology arrived, those reflexes would send them in opposite directions.

There is a deeper structural point hiding in this contrast, and it will echo through the rest of the story. GIA's business model depended on prestige and on the natural-diamond establishment that valued that prestige. IGI's business model depended on volume and on the working trade that valued speed and price. A company's earliest customers shape its reflexes permanently. GIA learned to protect a reputation; IGI learned to chase throughput. Neither reflex is superior in the abstract — but when a technology arrives that the prestige establishment finds threatening and the volume trade finds thrilling, those two reflexes point in opposite directions. Hold that thought.

Through the 1980s and 1990s, IGI followed the diamonds outward, opening laboratories in the trade's other great hubs — New York, then the fast-growing centers of Dubai and Hong Kong — and, in the late 1990s, into India. That last move looked minor at the time and turned out to be the most important decision in the company's history. The manager IGI backed to build its Indian presence was a young, aggressive gemologist named Tehmasp Printer, who would spend the next quarter-century turning a small office into the country's dominant grading engine — and who, decades on, would run the whole company.6 He arrived at a moment when India was transforming from a place that cut cheap melee diamonds into the workshop of the entire diamond world, and he built IGI's Indian network laboratory by laboratory, relationship by relationship, until an IGI report became the default reference for the Indian trade. India was where the diamonds were increasingly being cut. Soon it would be where an entirely new kind of diamond was being made. And IGI, thanks to two decades of patient groundwork, was standing right there when it happened.

IV. The Lab-Grown Diamond Disruption: Pivot of the Century

For most of human history, the sentence "this diamond was manufactured in a factory last month" would have been a contradiction in terms. A diamond's romance — and its price — rested on scarcity and geological time. Then, over the 2010s, that romance ran headfirst into physics. Two technologies matured to the point where they could produce flawless, gem-quality diamonds on an industrial schedule: High-Pressure High-Temperature synthesis, which mimics the crushing conditions deep in the earth, and Chemical Vapor Deposition, which grows a diamond atom by atom from a carbon-rich gas inside a reactor. The stones that came out were not fakes or simulants. They were real diamonds — same carbon lattice, same hardness, same sparkle — that happened to have been born in a machine.

It helps to understand the two methods, because the difference explains why the supply exploded. In HPHT synthesis, a tiny diamond seed is placed in a chamber and subjected to pressures and temperatures that replicate conditions roughly a hundred miles beneath the earth's surface, coaxing carbon to crystallize onto the seed. It is essentially a brute-force imitation of geology, compressed from a billion years into days. CVD is more elegant and, ultimately, more scalable: a seed sits in a vacuum chamber filled with a carbon-rich gas like methane, which is energized into a plasma so that carbon atoms rain down and build the diamond layer by microscopic layer, like a slow, atomic 3D printer. CVD reactors are cheaper to run at scale, easier to cluster in a factory, and well suited to producing the large, clean crystals the jewelry market wants. Once the process was industrialized, the marginal cost of a new gem-quality diamond began a long slide toward the cost of the electricity and gas to grow it — which is the root of both IGI's opportunity and, later, its central risk.

This posed an existential question for the certification industry, and the two rivals answered it in opposite ways. The answer each gave, more than any strategy deck, explains why IGI is worth two billion dollars today.

GIA's blind spot, IGI's gamble

GIA hesitated. For an institution whose prestige was bound up with natural diamonds — and whose deepest relationships ran through the natural-mining establishment, De Beers foremost among them — lab-grown stones looked less like an opportunity than a threat to the mystique that made its paper valuable. GIA worried, reasonably, that applying its hallowed 4C scale to factory diamonds would blur the line between the mined and the made and cannibalize the very product that anchored its brand. So for years it kept lab-grown grading at arm's length, issuing simplified reports rather than the full, granular 4C treatment it lavished on natural stones. To the emerging lab-grown industry, that reluctance read as condescension.

The tell was in the details of GIA's caution. Rather than apply its hallowed color-and-clarity nomenclature to synthetics, GIA for years issued lab-grown reports that used descriptive language instead of the precise 4C grades, a distinction that read, to the manufacturers pouring stones out of Surat, as a refusal to take their product seriously. Even De Beers, the very embodiment of the natural-diamond establishment, tried to fence lab-grown off as a cheap, unbranded novelty through its Lightbox venture — a signal of how deeply the incumbents wanted lab-grown to stay in a separate, lesser category. That was the consensus IGI chose to defy.

IGI did the opposite, and did it fast. Under Roland Lorie and Tehmasp Printer, the company decided that a lab-grown diamond deserved exactly the same rigorous, detailed 4C grading as a mined one — because from the consumer's point of view, the question "how good is this stone?" is identical regardless of where it was born. That decision looks obvious in hindsight and was anything but at the time. It meant betting the brand on a product the industry's most prestigious player was actively snubbing, a product that might have turned out to be a fad, and a product that threatened the mined-diamond ecosystem many of IGI's own clients still depended on. There was a real risk that by embracing synthetics, IGI would taint its natural-diamond credibility and alienate the mining-aligned part of the trade. IGI made the bet anyway. It treated lab-grown not as a threat to be managed but as a volume opportunity to be won — and in doing so, it effectively told the fast-growing synthetic industry: we will take you seriously when no one else will. For a product whose entire commercial future depended on consumer confidence, that message was worth more than any marketing.

The Surat connection and a commanding lead

The bet paid off because of where the manufacturing landed. The global epicenter of CVD lab-grown diamond production became Surat, in the Indian state of Gujarat — the same cutting-and-polishing capital where IGI, thanks to Tehmasp Printer's two decades of groundwork, already had deep physical infrastructure. As Surat's reactors began turning out grown diamonds in staggering volume, the laboratories best positioned to certify them, fast and locally, were IGI's. The company rode that wave to a commanding position: industry and company disclosures credit IGI with roughly a 65% share of the global lab-grown diamond certification market, alongside about a 33% share of overall diamond certification and close to a 50% share within India across diamonds, studded jewelry, and colored stones.78

The analytical point is not simply that IGI got lucky with Surat. It is that IGI's commercial DNA — the same volume-hungry, speed-first, trade-partnering instinct forged in the Antwerp of the 1970s — made it constitutionally willing to embrace a disruptive, faintly disreputable technology that its prestige-guarding rival could not stomach. First-mover advantage in a trust business is unusually sticky, because once the lab-grown trade standardized on IGI's reports as the reference, switching the whole ecosystem to anyone else became a coordination problem no single dealer could solve. That lead is the crown jewel Blackstone would later buy. The story of how it changed hands — twice — is where the money gets interesting.

V. Fosun, Blackstone, & the Indian Listing: A Masterclass in Geographic Multiple Arbitrage

Every great arbitrage needs a seller who does not fully see what they are holding. IGI's ownership history features two private equity batons and a valuation that multiplied several times over as it passed between hands that each understood a different piece of the puzzle.

The Chinese phase

The first baton pass came in 2018, when the Chinese conglomerate 复星国际 Fosun — through its Shanghai-listed tourism-and-retail arm 上海豫园 Shanghai Yuyuan — acquired a controlling stake of roughly 80% in IGI from Roland Lorie and Marc Brauner, with the founding Lorie family retaining a minority holding.92 The reported price for that control stake was in the neighborhood of $108 million, implying a value for the whole business of only around $130 million. Fosun's logic was consumption-led: fold a trusted global certification brand into its sprawling Chinese lifestyle empire and ride Asian jewelry demand. What Fosun mostly did, in practice, was hold the asset while the lab-grown wave it sat atop quietly compounded.

By the early 2020s Fosun itself was under pressure — the conglomerate was working to reduce debt and rationalize a famously eclectic portfolio — and a clean, cash-generative, globally branded asset like IGI was exactly the kind of thing a delevering parent puts up for sale.9 That created the opening for a buyer who understood not just the business but the venue in which it could be revalued.

The Blackstone play

In May 2023, Blackstone acquired IGI — buying out both Fosun's Yuyuan and Roland Lorie — for approximately $570 million.12 At the time the group ran 29 laboratories and 18 schools of gemology across ten countries.1 On its face, Blackstone paid roughly four times what Fosun had paid five years earlier, which sounds like buying high. But Blackstone was not underwriting the same thing Fosun had underwritten. Fosun had bought a certification company. Blackstone had spotted a mispricing between two capital markets.

Here was the insight. The explosive volume growth in Indian lab-grown certification was, by 2023, plainly visible in IGI's numbers. And the Indian public market — hungry for asset-light, high-margin, consumer-facing franchises — was assigning those characteristics valuation multiples that no European or American market would extend to a "testing services" company. In Europe, a certification business is a respectable but unexciting industrial; the market thinks of TÜV or SGS and applies mid-teens earnings multiples. In India, a fast-growing, capital-light franchise with 60% margins and a dominant share of a booming category is the sort of story retail and institutional investors will pay thirty, forty, or more times earnings to own. Same cash flows; wildly different price tags. Blackstone's play was to marry the two: take a business whose earnings were increasingly Indian in origin, package it as an Indian listed company, and let the higher-multiple market do the revaluation. The cash flows would barely change. The multiple on them would change enormously.

This is the part worth sitting with, because it is easy to admire as cleverness and easy to miss as risk. Multiple arbitrage is real value creation only to the extent the higher multiple is deserved and durable. If Indian investors are paying forty times earnings for growth and margins that turn out to be cyclical — tied to a lab-grown boom that fades — then the arbitrage transferred risk from Blackstone to the Indian public rather than creating value from nothing. The genius of the trade for Blackstone and the wisdom of the trade for a new shareholder are not the same proposition. A neutral analyst has to keep asking: is the Mumbai multiple a permanent feature of a better business, or a temporary feature of an enthusiastic market?

The engineering of the Indian IPO

The execution is worth studying, because it is a small masterclass in structuring. Blackstone used its Indian entity — International Gemmological Institute (India) Ltd. — as the public vehicle. In December 2024 that entity launched a ₹4,225 crore IPO, priced in a band of ₹397–417 per share, open from December 13 to 17 and listed on December 20.310 The offer had two parts: a ₹1,475 crore fresh issue of new shares, and a ₹2,750 crore offer for sale in which existing owners cashed out.310

The clever part was the fresh issue. Rather than earmarking the new money for reactors or buildings, the prospectus stated that the ₹1,475 crore of fresh proceeds would be used by the listed Indian company to acquire the other arms of the global group — IGI Belgium and IGI Netherlands — from an entity controlled by Blackstone itself.113 In plain English: Indian public-market investors funded the consolidation of the worldwide business under the Indian listed company, buying the foreign operations from the same promoter that was selling them the shares. It was internally consistent and fully disclosed — but it also meant new investors' cash flowed, in part, to a Blackstone-controlled seller to unify assets under the roof they were buying into.

The market's initial verdict was enthusiastic. The IPO drew heavy demand across investor categories, and the stock listed at a healthy premium to its ₹417 issue price on December 20, 2024 — a validation, at least in the short term, of the entire multiple-arbitrage thesis.310 Enthusiasm at listing, of course, tells you what the market felt on one December morning, not what the business will earn over a decade; IPO pops are a notoriously poor guide to long-run returns. But it did confirm the core Blackstone bet: the Indian market was, indeed, willing to pay a price for IGI's cash flows that no European exchange would have entertained.

When the dust settled, the consolidated entity carried that implied ₹16,545 crore valuation, Blackstone had extracted substantial cash through the offer for sale, and it retained a roughly 76%–77% super-majority stake — locking in a paper gain of several times its 2023 cost in about eighteen months while still controlling the company.3 For a skeptical investor, the structure raises the obvious flags we will test later: a promoter selling the foreign business to the company at a promoter-set price, and a controlling shareholder whose remaining stake looms over the stock. The related-party fresh-issue mechanism, in particular, deserves neither reflexive alarm nor a free pass — it was disclosed in the prospectus and is legal and common in Indian promoter-led listings, but it did route a portion of new investors' money to a Blackstone-controlled seller, and the price at which the foreign arms changed hands was set inside the same corporate family. As financial engineering, the whole package was close to immaculate. The question now becomes whether the underlying business — segment by segment — justifies the multiple that engineering unlocked.

VI. Under the Hood: Key Segments, Margins, and the Economics of Scale

Strip away the deal glamour and IGI is, at its core, a machine that turns stones into reports and reports into fees. Understanding where those fees come from — and how durable each stream is — matters more to a long-term investor than any single quarter's growth rate.

The four revenue streams

The engine room is loose diamond certification, covering both natural and lab-grown stones, which drives the clear majority of consolidated revenue — on the order of 70% or more.7 This is the high-volume, rapid-turnaround B2B business: parcels from Surat cutters and global wholesalers flowing through IGI's labs on a financing clock, priced per report. It is where the operating leverage lives, and it is where the lab-grown boom shows up most directly. It is also, not coincidentally, the segment most exposed to the lab-grown price dynamics that form the heart of the bear case.

The fastest-growing and strategically richest stream is studded jewelry certification — grading finished retail pieces rather than loose stones. This is a subtler and, in many ways, better business. As retail chains and brands increasingly certify every mounted piece to protect themselves from mixed-stone and misrepresentation liability, certification pushes downstream from the trading floor to the shop counter. Certifying a finished necklace with dozens of stones is more involved than grading a single loose diamond, and it attaches IGI's brand directly to the consumer transaction. That makes studded jewelry both lucrative and defensively valuable, though its volumes are more tied to retail cycles than the wholesale grading base.

Two smaller streams round out the picture. Colored stones — rubies, emeralds, sapphires — are low in volume but high in average selling price and complexity, since grading them can require verifying geographic origin, a specialized science that commands premium fees. This is the smallest of the diamond-and-jewelry segments today, but it is strategically the one with the most untapped headroom, which is exactly why the AGL acquisition later in the story matters more than its price tag suggests. And gemological education, run through a network of schools, is financially immaterial as a revenue line but does real strategic work: it trains the next generation of gemologists on IGI's standards and seeds the trade with people fluent in IGI's system. Every graduate who learns to grade "the IGI way" becomes a small reinforcement of the standard. It is a brand-and-trust recruitment mechanism dressed as a business unit, and treating it as a cost center to be trimmed would be a category error.

A word of caution on the segment picture is warranted for the honest analyst: IGI's disclosure as a newly listed company is still maturing, and the granularity investors will eventually want — segment-level margins, volumes split cleanly between natural and lab-grown, geographic revenue mix, average revenue per report by category — is not yet fully and consistently broken out in public materials. That opacity is normal for a company barely eighteen months into its public life, but it is a reason to hold conclusions about the durability of the mix loosely until several more reporting cycles fill in the texture.

What the unit economics reveal

The through-line across all four is a predictable fee-per-report model with a cost base that barely moves as volume rises. Once a laboratory and its instruments are in place, depreciation and fixed overhead shrink relentlessly as a share of sales with every additional stone graded, which is precisely how the group sustains EBITDA margins in the high-50s to low-60s.4 For a long-term investor, the honest reading is two-sided. On the upside, this is a genuinely capital-light compounder: growth throws off cash rather than consuming it, and returns on capital are structurally high. On the downside, that same fixed-cost leverage means the margin story is only as safe as the volume story — and the volume story rests heavily on a single, deflating product category. Which brings the analysis, unavoidably, to the people steering the machine and how their incentives are set.

VII. Executive Power & Alignment: The Tehmasp Printer & Blackstone Era

Every business this dependent on trust eventually comes down to the person whose name is on the standard. At IGI, that person is Tehmasp Printer — the young manager IGI sent to build India in the late 1990s, now the group's Global CEO and Managing Director. His career is, in effect, the Indianization of IGI told through one biography: he took a company that grades stones in Antwerp and made India the place where the grading — and increasingly the value — actually happens.

From Mumbai office to the corner office

Printer spent roughly a quarter-century inside IGI, most of it building and running the Indian subsidiary from a modest operation into the country's dominant gem-grading engine.612 When Blackstone took control, it faced the classic private equity question of whether to import an outside operator or elevate the insider who understood the trade's plumbing. It chose the insider. On August 9, 2023, Blackstone announced that Printer would succeed Roland Lorie — a nearly five-decade IGI veteran — as Global CEO, effective October 1, 2023.126 The symbolism was pointed: leadership of a business founded in Belgium passed to the man who had built its Indian heart, just as the whole company prepared to relist in Mumbai.

The compensation puzzle

Here the governance picture gets genuinely interesting, and a neutral observer should sit with the tension rather than smooth it over. Printer does not own the company in any founder-like sense. Company disclosures describe him holding a single equity share — a nominal position, with real ownership resting overwhelmingly with the Blackstone-controlled promoter, BCP Asia II TopCo Pte. Ltd.3 He is, in ownership terms, a hired steward, not a proprietor.

To align a steward who lacks equity, you pay him — and Blackstone paid. Disclosures around the listing indicated Printer's remuneration ran to roughly ₹24 crore (on the order of $2.9 million) in the relevant period, an unusually large package by the standards of an Indian company of this size.1811 For investors, that figure cuts two ways. Read charitably, it is Blackstone putting serious cash behind the one executive whose credibility underpins the brand, tying his fortunes tightly to aggressive margin-expansion and growth targets in the absence of a founder's equity stake. Read skeptically, a very large cash package for a nominal shareholder is exactly the arrangement that rewards hitting short-horizon targets — the kind a private equity owner sets ahead of an exit — rather than compounding value over decades the way a true owner-operator would. Both readings can be true at once, and the honest conclusion is that Printer's incentives are powerfully aligned with Blackstone's objectives, which may or may not be identical to those of a minority shareholder buying the stock today.

Execution to watch

There is also the matter of what Blackstone itself brings, and here the record is genuinely a mark in the company's favor. Blackstone runs one of the largest and most sophisticated operating platforms in private equity, with in-house capabilities in data, pricing, procurement, and — increasingly — technology and automation that a family-owned certification lab could never have afforded. In a business whose margins are driven by throughput and whose accuracy is driven by data, an owner that can push automation into the grading pipeline and squeeze cost out of the back office is not a passive financial sponsor but an operational one. The professionalization of governance, the imposition of formal reporting rhythms, and the disciplined approach to bolt-on M&A are all recognizably Blackstone's fingerprints. For minority investors, this cuts in a reassuring direction: whatever one thinks of the exit incentives, the day-to-day operator is competent and well-resourced.

On the execution side, the management team has so far done the unglamorous things competently: it navigated the shift from a calendar-year to an April–March fiscal cycle to fit Indian regulatory norms — the reason its recent results span an awkward fifteen-month transition period — while continuing to report brisk organic volume growth.5 That is a point in management's favor, though a mild one; changing a fiscal year-end is administratively fiddly but not strategically revealing, and the fifteen-month reporting period does make clean year-over-year comparison harder for outsiders, which is worth noting. The real test of credibility is still ahead, because it will be measured not in a rising market but in a falling one — and the market for IGI's single most important product has, in fact, been falling. The clearest window into how this team allocates capital under pressure came in early 2026, with a small but revealing acquisition.

VIII. Playbook: M&A, Integration, and the 2026 AGL Acquisition

On January 31, 2026, IGI announced its first notable acquisition as a listed company — and the striking thing about it was how small it was. Through its US subsidiary, IGI agreed to acquire 100% of American Gemological Laboratories for $13.2 million, structured as $9 million in cash at closing and up to $4.2 million in post-closing earnouts.131415 For a company valued at roughly two billion dollars, this was a rounding error. That is precisely what makes it worth examining, because how a company spends small money often tells you more than how it spends large money.

The target

AGL, led by its president and chief gemologist Christopher Smith, is the most respected independent colored-gemstone laboratory in the United States.1416 Colored-stone grading is a different and harder craft than diamond grading. Diamonds are graded against a single, well-codified scale that GIA standardized decades ago; colored stones have no such universal grammar. A ruby's value turns on subtle judgments of hue, saturation, and the presence or absence of heat treatment, and — most consequentially — on origin determination, the scientific detective work of establishing whether a ruby came from Burma or Mozambique, or whether a sapphire is from Kashmir. Those distinctions are not academic: a Kashmir sapphire or an unheated Burmese ruby can command many multiples of the price of a chemically similar stone from a less storied source. Getting origin wrong is not a rounding error; it can misprice a stone by hundreds of thousands of dollars. That is why colored-stone authority is scarce, deeply reputational, and painfully slow to build. AGL had spent decades building exactly that credibility, and a reputation like Smith's cannot be manufactured with capital — it can only be bought.

The discipline the deal signals

IGI could have tried to buy volume — a large competitor to bolt on grading capacity. Instead it spent a disciplined $13.2 million to acquire not scale but credibility in a niche where credibility is the entire product.13 Under the terms, Smith stays on as president and chief gemologist and AGL remains headquartered in New York, operating independently under its own brand — a deliberate choice to preserve the specialist reputation IGI was paying for rather than dissolve it into the parent.16 The strategic logic is a textbook bolt-on: take AGL's gold-standard colored-stone science and distribute it through IGI's global footprint of, as of the announcement, 35 laboratories and 21 schools of gemology across ten countries.16 A premium brand with limited reach gains reach; a high-volume network with limited premium-colored-stone authority gains authority.

For an investor gauging management, the AGL deal is a useful early data point. The earnout structure ties part of the price to post-closing performance, which is disciplined; the decision to buy specialty rather than volume suggests capital allocation aimed at optionality rather than empire-building; and the small size means the downside is negligible even if integration disappoints. It is exactly the kind of move a Blackstone-owned company should make to build a second growth leg in colored stones — genuine optionality — while the diamond core faces its reckoning. Whether that reckoning proves survivable is the question that separates the bulls from the bears, and it is time to war-game it properly.

IX. The Competitive Moat: Porter's Five Forces & Hamilton Helmer's Seven Powers

Before weighing bull against bear, it helps to name the sources of IGI's advantage precisely, because a moat you cannot articulate is a moat you cannot underwrite. Two frameworks do the work well: Hamilton Helmer's 7 Powers and Michael Porter's Five Forces. Used honestly, they explain both why IGI is hard to dislodge and where the walls are thinner than the company would like.

Helmer's 7 Powers

Three of Helmer's seven powers clearly apply. The first and most important is branded differentiation. In certification, the brand is not marketing gloss layered on a product — the brand is the product. An unbranded grading report is worthless paper; a stone's tradeability depends on whose name is on the certificate. IGI's brand has become a prerequisite for trading lab-grown stones and mid-market natural jewelry, which is a far deeper form of brand power than mere preference. It is closer to a passport: without the right stamp, the goods do not move.

The second is switching costs, already met in the physics of the trade. Surat's manufacturers have wired IGI's fast turnaround into their credit-financed production schedules; substituting a slower certifier would strand working capital across the whole line. The switching cost here is not a fee — it is operational friction measured in interest and time.

The third is scale economies. IGI's concentration of grading volume and testing data lets it hold unit costs well below what regional challengers can achieve, which both protects margin and funds the instruments that keep its grading credible. Regional labs — an SGL or a local competitor — can undercut on price in a single geography, but they cannot match IGI's cost-per-report across the whole network, and they lack the brand recognition to command the same trust downstream.

Notably, IGI does not obviously possess several of Helmer's other powers, and being clear-eyed about their absence is as important as celebrating those present. It has no classic two-sided network effect of the kind that locks in a marketplace. It has no cornered resource — no patent or exclusive input a rival could never obtain, since the instruments are commercially available and gemologists can be trained anywhere. Its process power — proprietary ways of working that competitors cannot replicate even with effort — is arguable but not proven. What this means practically is that IGI's moat, while real, is a trust-and-scale moat rather than a structural-lock-in moat. It is durable as long as the brand stays clean and the volume stays high, but it is not the kind of moat that survives a self-inflicted reputational wound or a sustained collapse in throughput. That is a more contingent form of protection than the bull case sometimes implies.

Porter's Five Forces

Porter's lens sharpens the picture. Bargaining power of buyers is low: individual cutters and retailers cannot meaningfully negotiate fees, because a reputable certificate is non-optional for selling the stone onward, and no single customer represents enough volume to dictate terms. Threat of new entrants is very low: the one thing a new competitor cannot buy at any price is a fifty-year record of clean, consistent grading, and trust in this industry is accumulated slowly and destroyed quickly.

But two forces run against IGI, and they are where the bear case breeds. Bargaining power of suppliers is not the classic worry — IGI's key "supply" is skilled gemologists and instruments — but its true dependency is on volume from the diamond trade itself, and that trade's health is outside IGI's control. And the threat of substitutes is real and rising: cheap, consumer-facing diamond-screening devices, and a growing willingness among some buyers to purchase inexpensive lab-grown stones with minimal or no certification at all, both chip at the premise that every stone needs a paid report. Rivalry, meanwhile, is intensifying from a direction IGI once dismissed — its old rival has stopped snubbing lab-grown diamonds. That competitive re-entry is where the stress test begins.

X. The Skeptical Stress Test: Bull vs. Bear Case & Risk Radar

A neutral platform owes readers both cases with equal seriousness. IGI is genuinely excellent and genuinely exposed, and a sophisticated investor has to hold both facts at once.

The bull case — why it wins from here

The bull case is straightforward and rests on evidence, not slogans. IGI is the undisputed leader in the fastest-growing corner of its industry — roughly two-thirds of global lab-grown certification and around half of the Indian market — with a brand that functions as a prerequisite to trade.78 Its financial profile is the kind investors pay up for: EBITDA margins near 60%, capital-light cash generation, high returns on capital, and operating leverage that turns volume growth into disproportionate profit growth.4 And it now sits inside Blackstone's operational apparatus, which has professionalized governance, imposed disciplined capital allocation (the AGL bolt-on being Exhibit A), and demonstrated a willingness to build colored-stone optionality alongside the diamond core. If lab-grown volumes keep climbing and studded-jewelry certification keeps penetrating retail, the compounding is real and durable.

The most compelling piece of the bull thesis is the volume-versus-price distinction, because it is the bulls' answer to the bears' loudest objection. IGI is paid per certificate, not as a percentage of the stone's value, so a collapse in lab-grown prices does not mechanically collapse IGI's revenue — what matters is the number of stones flowing through the labs, and cheaper stones can, up to a point, mean more stones as lab-grown diamonds democratize into new price segments and new markets. A world in which lab-grown becomes an affordable, everyday luxury that millions of first-time buyers purchase is, in principle, a world with more certificates to issue, not fewer. The bull case is that IGI is levered to penetration, not to price, and penetration is still early. The results through the fifteen-month period to March 2026, with double-digit revenue and profit growth even as lab-grown prices fell sharply, are the strongest evidence for this reading — so far, volume has outrun deflation.45

Myth versus reality

It is worth puncturing the framing that made the headlines — the notion that Blackstone conjured a "3.5x gain in eighteen months on a business that grades rocks." The reality is more sober and more useful. Blackstone did not triple the business; it triple-re-rated the valuation multiple by changing the listing venue and riding a genuine earnings boom, then sold a chunk and marked the rest at the new market price. The paper gain is real, but it is a market-priced mark on a majority stake Blackstone still holds, not fully realized cash, and it embeds the assumption that Mumbai's multiple sticks. Equally, the popular story that "the certificate is 100% of the value, so IGI has infinite pricing power" overstates the case: IGI's fee is a tiny fraction of a stone's price, which is precisely why it has had pricing latitude historically — but that same smallness flips into vulnerability once the stone's value falls toward the fee itself. The moat is trust and scale, not magic. Understanding exactly what was and was not created is the difference between admiring a trade and underwriting a stock.

The bear case — what could break it

The bear case is equally grounded, and it starts with the uncomfortable fact the bulls skate past: the price of IGI's flagship product is collapsing. Lab-grown diamond retail prices have fallen dramatically — on the order of 74% from their 2020 levels, with one-carat lab-grown stones that once fetched thousands now selling for a few hundred dollars.[^17] IGI's economic model is volume-driven, which offers partial insulation: a certificate fee is charged per stone regardless of the stone's price, so falling prices do not automatically fall through to IGI's revenue. But there is a floor problem. If a one-carat lab-grown diamond's wholesale value keeps sinking toward the price of costume jewelry, at some point wholesalers will simply refuse to pay a meaningful certification fee to grade a near-disposable stone — and as lab-grown diamonds drift culturally from "engagement ring" toward "fashion accessory," the whole premise that each one warrants a paid, rigorous report erodes. Because of IGI's fixed-cost leverage, a plateau or decline in certified volume would hit margins hard and fast.

The second threat is GIA's response, and it is more nuanced than a simple counterattack. After years of holding lab-grown at arm's length, GIA re-engaged with the category — but in 2025 it moved away from the traditional 4C scale for lab-grown stones, replacing granular color-and-clarity grades with simplified descriptive tiers such as "premium" and "standard," on the reasoning that the overwhelming majority of lab-grown diamonds now cluster in a tiny quality band where fine gradations are meaningless.17 This is a double-edged development for IGI. On one hand, GIA's move implicitly validates the idea that lab-grown diamonds are becoming commoditized — which is the bear thesis. On the other, if the market comes to accept cheaper, simpler lab-grown reports as sufficient, that pressures both pricing and the perceived value of IGI's full-4C treatment. Either way, GIA's prestige is now pointed at the category IGI dominates.

The third risk is the one that could undo everything overnight: reputational fragility. Grading is inherently a matter of expert judgment, and the entire franchise rests on the market's belief that IGI's judgment is honest and consistent. Any credible allegation of "grading inflation" — softening standards to please the high-volume manufacturers who are IGI's largest customers — would strike directly at the trust that is the whole product. This is not a hypothetical genre of risk; the diamond-grading industry has weathered grading-consistency controversies before, and even perceptions that one lab grades "softer" than another circulate constantly in the trade. The structural hazard is built into the business model: IGI's paying customers are the very manufacturers whose stones it judges, which creates a permanent, quiet incentive to be generous. Managing that conflict — being strict enough to stay credible with the buyers who rely on the certificate, while fast and accommodating enough to keep the sellers who pay the fee — is the central tension of the entire enterprise. A trust business can survive a bad quarter. It cannot easily survive a scandal, and the asymmetry is brutal: trust is accumulated over fifty years and can be destroyed in a single well-documented episode.

A fourth, quieter risk belongs on the radar: substitution and disintermediation from below. As lab-grown stones commoditize, a growing slice of the market may simply stop paying for full certification — buying screened-but-ungraded stones, or relying on cheap consumer-facing diamond testers that verify "real vs. synthetic" for a few dollars without any lab involvement. IGI does not need lab-grown diamonds to disappear to be hurt; it only needs the trade to decide that a rigorous paid report is no longer worth it for a large share of low-value stones. That is a subtler and, in some ways, more probable erosion than a dramatic price crash. There is also a data and cybersecurity dimension that is easy to overlook: IGI's reports are increasingly verified digitally, and its grading databases are a core asset; a breach that allowed forged certificates to circulate, or that compromised the integrity of its verification system, would attack trust at its technological root.

A fifth dimension is macro and geopolitical, and it deserves a mention precisely because IGI's fortunes are so concentrated. The company's volume base is heavily tied to a single manufacturing cluster — Surat — and a single fast-growing category. That concentration cuts both ways: it is the source of the dominance and a source of fragility. A downturn in the natural-diamond cycle (which drives a large share of the higher-value grading work), a shift in US or European consumer sentiment toward diamonds of any kind, trade friction or import duties affecting the gem trade, or disruption to the Indian cutting-and-polishing hub would all flow through to IGI's throughput with little to offset them. The company does not control the health of the trade it serves; it can only take its toll on whatever volume the trade produces. For a business valued as a secular growth compounder, that cyclicality and concentration are easy to underweight in good times and painful to rediscover in bad ones.

The activist's ledger — governance and overhang

Finally, a skeptical long/short investor would train fire on the ownership structure. Blackstone controls roughly three-quarters of the company, which creates a large structural overhang: a private equity promoter is, by definition, a temporary owner, and the market knows that at some point Blackstone will sell down its remaining stake, an eventual supply of stock that can cap the share price regardless of operating performance. Add the related-party mechanics of the IPO — where the listed company used public money to buy the foreign operations from a Blackstone entity at a promoter-set valuation — and a nominal-shareholder CEO on a large cash package, and you have a governance profile that demands ongoing scrutiny rather than blind faith.311 None of this is disqualifying, and none of it is hidden. But it is exactly the set of issues that separate a business one admires from a stock one has fully underwritten. The way to keep that underwriting honest is to watch a very short list of numbers.

XI. Epilogue & Key KPIs to Watch

Peel back the frameworks, the deal structuring, and the fifty years of Antwerp history, and IGI comes down to a single elegant, fragile proposition: it sells trust in a market that cannot function without it, at software-like margins, adjacent to the world's diamond-cutting capital. The bull and bear cases are really an argument about one thing — whether the volume of stones flowing through IGI's labs keeps rising fast enough to outrun the deflation in what those stones are worth. Everything else is detail.

That makes the monitoring discipline unusually clean. Three metrics, tracked over time, will tell an investor almost everything about whether the thesis is holding.

First, certification volumes. Because IGI charges per report, the number of stones and pieces it grades — not their underlying price — is the true top-line driver. The single most important question each period is whether volume growth is holding up despite the severe deflation in lab-grown retail prices. Rising volumes mean the "fashion accessory" fear is premature; stalling volumes would be the first hard evidence that the floor problem is real.

Second, average revenue per report. This is the pricing-power gauge. If a re-engaged GIA or hungry regional challengers force IGI to discount its fees, or if the mix shifts toward cheaper, lighter reports for commoditized stones, it will show up here before it shows up anywhere else. A stable or rising figure would suggest the brand still commands its premium; a persistent slide would signal that certification itself is commoditizing.

Third, consolidated EBITDA margin. This is the summary statistic for the whole operating-leverage story. Holding a margin in the high-50s to low-60s while volumes grow would confirm that scale economies remain intact; a meaningful erosion — particularly if high-margin studded-jewelry volumes wobble — would reveal that the fixed-cost leverage has begun working in reverse.4

Two secondary signals are worth watching alongside those three, not as headline KPIs but as early-warning lights. One is the trajectory of Blackstone's stake: any move to sell down further, and the price and manner in which it does so, will speak volumes about both the overhang and the insiders' own read on value. The other is the mix shift within diamond certification — how quickly, if at all, the market drifts toward cheaper, lighter-touch reports for commoditizing lab-grown stones, which would show up first in average revenue per report and only later in margin. An investor who tracks volumes, ARPR, and margin, and keeps half an eye on the promoter's selling and the report-mix, will know whether the thesis is intact long before it shows up in a headline profit number.

Two durable lessons outlast whatever the stock does next. The first is the power of the early, controversial pivot: IGI won its most valuable franchise not by being the most prestigious grader but by being the one willing to embrace a disruptive, faintly disreputable technology while its cautious rival hesitated — a reminder that in trust businesses, the incumbent's greatest asset, its reputation, can also be the reason it freezes. The second is the mechanics of geographic multiple arbitrage: Blackstone created enormous value without changing what the business earned, simply by moving where it was priced — relisting a European trust franchise in the high-multiple market that sits next door to its operational heart. Both lessons are real. Whether they compound into a durable public company, or merely a brilliantly executed private equity exit, is the story the next few years of volumes, pricing, and margins will tell.

References

-

Blackstone Acquires International Gemological Institute (IGI) — Blackstone Press Release, 2023-05-21 ↩↩↩↩

-

Blackstone Officially Inks Deal to Acquire IGI — National Jeweler, 2023-05 ↩↩↩

-

International Gemological Institute (India) Ltd IPO — Price Band, Dates and Details — Groww, 2024-12 ↩↩↩↩↩↩↩↩

-

International Gemological Institute Delivers Robust Growth with 21% Revenue Surge (Q4 FY26) — InvestyWise, 2026 ↩↩↩↩↩

-

International Gemological Institute Financial Results for Fifteen-Month Period Ended March 31, 2026 — InvestyWise, 2026 ↩↩↩

-

Tehmasp Printer to Replace Roland Lorie as IGI CEO — Rapaport News, 2023-08 ↩↩↩

-

International Gemmological Institute (India) Ltd — Company Financials and Key Insights — Screener.in ↩↩

-

International Gemmological Institute India IPO — Details, Price, Dates & Subscription — IPOJI, 2024-12 ↩↩↩

-

Blackstone-owned IGI India files DRHP with SEBI to raise Rs 4,000 crore — Business Standard, 2024-08-23 ↩↩↩

-

Blackstone-Backed International Gemological Institute (IGI) Appoints New Global CEO — PR Newswire, 2023-08-09 ↩↩

-

IGI Acquires American Gemological Laboratories for $13.2 Million — JCK, 2026-01-31 ↩↩

-

IGI to Acquire American Gemological Laboratories — National Jeweler, 2026-01-31 ↩↩

-

IGI Acquires American Gemological Laboratories — BSE Disclosure, 2026-01-31 ↩

-

IGI Acquires AGL, Expanding its Global Footprint in Colored Gemstone Certification — PR Newswire, 2026-01-31 ↩↩↩

-

GIA Redefines Its Lab-Grown Diamond Grading Report — Natural Diamonds, 2025 ↩

-

Tehmasp Printer Nariman — Director Salary History (DIN: 01306226) — Trendlyne ↩

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube