IDBI Bank: From Development Pioneer to LIC's Banking Gambit

Introduction & Episode Setup

On a humid Mumbai morning in January 2019, something unprecedented happened in Indian banking. The Life Insurance Corporation of India, the country's insurance behemoth that had quietly backstopped the nation's capital markets for decades, officially became a banker. Not through a license application or a greenfield venture, but by acquiring control of one of India's most troubled lenders—IDBI Bank. The moment LIC's stake crossed 51%, regulators performed an accounting sleight of hand: a bank majority-owned by two government entities was reclassified as "private sector." It was financial alchemy that would make even the most creative investment banker pause.

Today, IDBI Bank stands as one of India's largest commercial banks, with a balance sheet exceeding ₹4.11 trillion, operating through 2,100 branches and 3,700 ATMs across the country. Walk into any branch, and you'll find the usual banking bustle—customers depositing checks, applying for loans, updating passbooks. Nothing hints at the existential drama that nearly destroyed this institution, or the controversial rescue that saved it. The bank commands a market capitalization of ₹96,223 crore, positioning it among India's mid-cap banking stocks—substantial enough to matter, yet small enough to remain a takeover target. The central paradox of IDBI's existence crystallizes in its ownership structure: LIC holds 49.24% while the Government of India retains 45.48%, yet through regulatory gymnastics, it's classified as a "private sector bank." This classification defies common sense—when 95% of your equity sits with government entities, calling yourself private requires exceptional suspension of disbelief.

But this contradiction merely scratches the surface of a deeper transformation story. How did India's premier development finance institution, established to fuel the nation's industrial dreams, become a cautionary tale of bad loans and regulatory forbearance? Why did LIC, an insurance company with no banking expertise, step in to rescue a sinking ship? And most intriguingly, how did this unlikely marriage produce one of Indian banking's most dramatic turnarounds?

The IDBI saga encompasses the entire arc of Indian financial history—from socialist nation-building through liberalization's creative destruction to the current era of digitization and consolidation. It's a story of institutional hubris, political interference, and ultimately, redemption through radical surgery. As the government and LIC prepare to exit through a high-stakes disinvestment, with bidders including Fairfax Financial, Emirates NBD, and Kotak Mahindra Bank circling the waters, IDBI stands at yet another inflection point.

This is not just a banking story. It's a meditation on how institutions evolve, how cultures clash when development meets commerce, and what happens when the safety net of government ownership both enables and constrains. It's about the price of transformation—measured not just in capital infusions but in careers disrupted, strategies abandoned, and identities reimagined. As we'll discover, IDBI's journey from development pioneer to distressed asset to profitable bank reveals fundamental truths about India's economic evolution and the complex choreography between state and market.

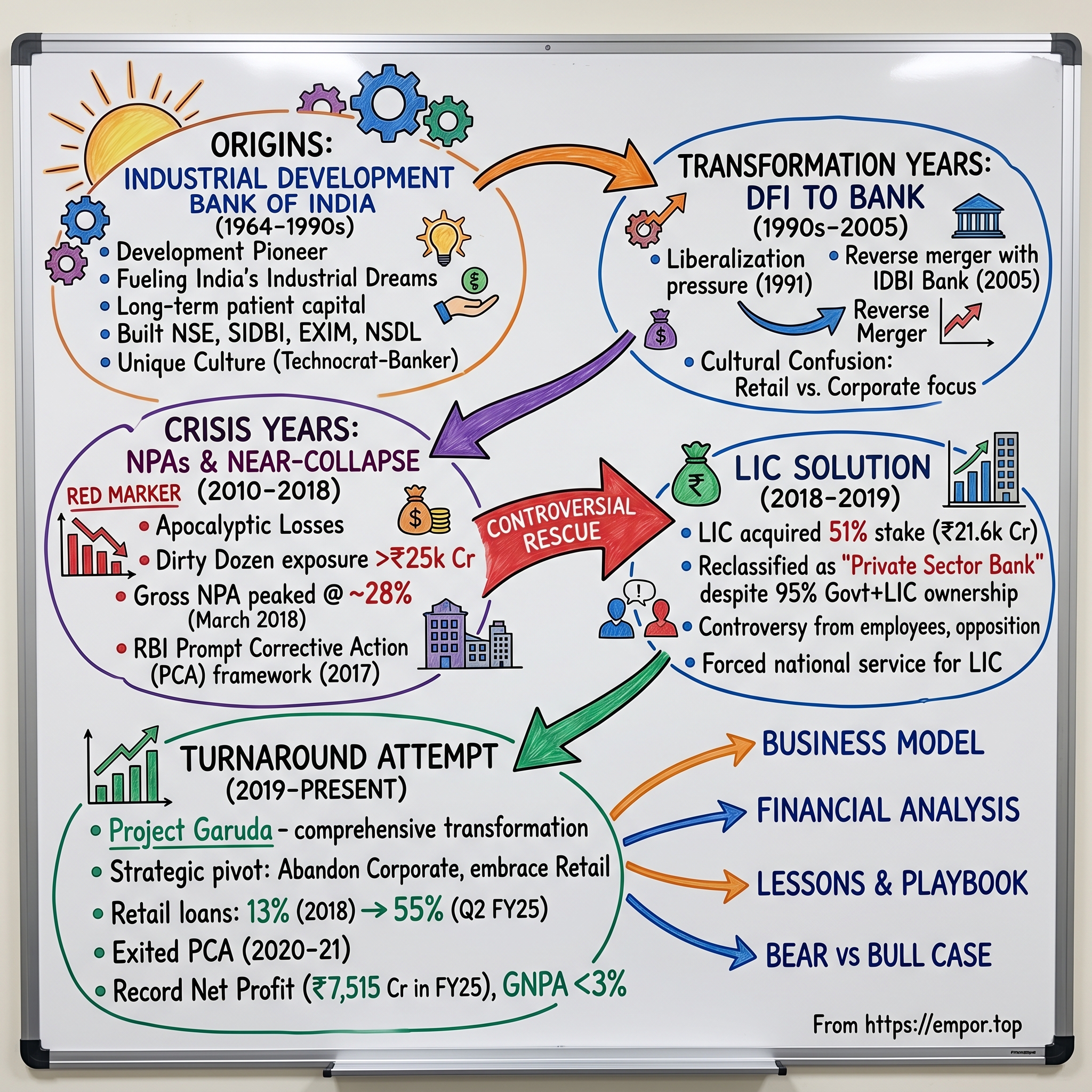

Origins: Industrial Development Bank of India (1964–1990s)

The monsoon had failed again in 1964. As Parliament convened in New Delhi that July, the specter of another drought loomed over a nation still finding its industrial feet seventeen years after independence. It was against this backdrop of agricultural uncertainty that Finance Minister T.T. Krishnamachari rose to announce the creation of the Industrial Development Bank of India. "We cannot remain hewers of wood and drawers of water," he declared, channeling Nehru's vision of an industrialized India. IDBI would be the financial catalyst for this transformation.

The institution emerged not from the Finance Ministry's corridors but from the Reserve Bank of India itself, established as a wholly-owned subsidiary through an Act of Parliament. This wasn't merely administrative convenience—it was strategic design. By housing IDBI within the central bank, the government ensured it would have the gravitas, credibility, and access to capital that private institutions couldn't match. The initial authorized capital of ₹100 crore seemed modest, but in an economy where the entire banking system's deposits totaled less than ₹3,000 crore, it represented serious commitment.

R.K. Hazari, IDBI's first chairman, understood the weight of his mandate. A former deputy governor of RBI, Hazari had witnessed firsthand how British banks in India systematically starved Indian enterprise of capital, preferring the safety of financing trade over the risks of building industry. "We are not just lending money," he told his early recruits. "We are building the sinews of a modern economy." This wasn't hyperbole—in a nation where term lending barely existed, where stock markets were primitive, and where entrepreneurs relied on traditional moneylenders charging usurious rates, IDBI represented a revolution in finance.

The early projects read like a roster of India's industrial ambitions. When the Birlas needed long-term capital to expand Gwalior Rayon, IDBI stepped in with a ₹5 crore loan—the largest industrial loan in Indian history at that point. When Dhirubhai Ambani, then a small-time textile trader, envisioned backward integration into petrochemicals, traditional banks laughed. IDBI saw possibility. The institution didn't just provide capital; it provided validation, technical expertise, and crucially, patience. Unlike commercial banks obsessed with quarterly results, IDBI could wait seven years for a steel plant to generate returns, understanding that nation-building operated on different timelines than profit-making.

The institutional culture that developed was unique—part banker, part technocrat, part nation-builder. IDBI officers weren't just credit analysts; they were expected to understand blast furnace operations, petrochemical processes, and power generation technologies. The recruitment process favored engineers who could learn finance over financiers who might learn engineering. This produced a cadre of professionals who could engage with industrialists as equals, challenging project assumptions and improving proposals rather than merely stamping approvals.

By the 1970s, IDBI had become the spawning ground for India's financial architecture. When the government recognized the need for specialized institutions, it turned to IDBI's talent pool and institutional memory. The Small Industries Development Bank of India (SIDBI) emerged in 1990 as IDBI's subsidiary, taking over the small-scale sector portfolio that had grown too large to manage alongside major industrial projects. The Export-Import Bank of India (EXIM Bank) was carved out to handle the specialized needs of foreign trade financing. Even more remarkably, IDBI played midwife to India's capital markets infrastructure—the National Stock Exchange, SEBI, and the National Securities Depository Limited all trace their origins to IDBI's initiatives. The institution's most visionary contribution came in the early 1990s when capital market reform became urgent. IDBI played a pioneering role in establishing institutions like the Securities and Exchange Board of India (SEBI), National Stock Exchange of India (NSE), the National Securities Depository Limited (NSDL), and the Stock Holding Corporation of India Limited (SHCIL). The NSE project, in particular, showcased IDBI's ability to think beyond traditional banking. When the Harshad Mehta scam exposed the BSE's archaic practices in 1992, IDBI led a consortium to create a modern, transparent, electronic exchange. NSDL was promoted by Industrial Development Bank of India (IDBI), Unit Trust of India (UTI), and National Stock Exchange (NSE), creating India's first electronic depository system that would revolutionize securities trading.

The numbers told a story of remarkable institutional success. By 1990, IDBI had sanctioned cumulative assistance exceeding ₹20,000 crore to over 2,600 projects. Its loan book read like a directory of Indian industry—Tata Steel's modernization, Reliance's petrochemical complex, Maruti's automobile revolution. But more importantly, IDBI had created an ecosystem. Its project appraisal methodologies became industry standard. Its training programs produced generations of industrial financiers. Its technical assistance helped Indian companies negotiate technology transfers and joint ventures with foreign partners.

Yet beneath this success lay the seeds of future crisis. The very strengths that made IDBI effective as a development institution—patient capital, relationship lending, willingness to take risks on unproven sectors—would prove devastating when applied to commercial banking. The officers who excelled at evaluating steel plants struggled with retail credit scoring. The culture that celebrated nation-building through infrastructure finance couldn't adapt to the quick decisions and customer service demanded by commercial banking.

More troublingly, IDBI's success had created a moral hazard. Industrialists came to view IDBI finance not as commercial debt but as quasi-equity, something to be serviced when convenient. Political pressure to support "sick" industries meant loans were often restructured rather than recovered. The institution's very purpose—development—became an excuse for poor credit discipline. As one retired IDBI executive would later reflect, "We were so focused on building India that we forgot we were also running a bank."

The 1990s would test every assumption IDBI held dear. Economic liberalization didn't just change the rules; it changed the game itself. Foreign banks entered with sophisticated products. Private sector banks emerged with aggressive strategies. The cozy world of directed lending and administered interest rates gave way to market competition. IDBI, designed for a different era, would have to transform or perish.

The Transformation Years: From DFI to Bank (1990s–2005)

Yashwant Sinha stood before Parliament on February 28, 2003, his voice betraying none of the turmoil this announcement would cause. "The distinction between development finance institutions and banks has become increasingly blurred," the Finance Minister declared. "IDBI must transform into a universal bank to survive in the new economy." With those words, he signed the death warrant of development banking in India and forced IDBI into an identity crisis from which it would never fully recover.

The pressure had been building since 1991. When Manmohan Singh unveiled economic reforms that July, he didn't just liberalize industry—he fundamentally altered the logic of industrial finance. Suddenly, companies could raise money from capital markets, access foreign currency loans, and choose between multiple funding sources. The monopoly on long-term finance that had made IDBI indispensable evaporated almost overnight. Between 1993 and 2003, IDBI's share of industrial term lending plummeted from 72% to less than 15%.

Inside IDBI's Nariman Point headquarters, the transformation felt like organizational schizophrenia. S.H. Khan, who served as Chairman during this crucial period, faced an impossible balancing act. "We had officers who spent decades perfecting project finance suddenly asked to sell credit cards," he would later recall. The Industrial Development Bank (Transfer of Undertaking and Repeal) Act, 2003, formally converted IDBI into a limited company—IDBI Ltd. In September 2004, the Reserve Bank of India incorporated IDBI as a 'scheduled bank' under the RBI Act, 1934.

The most dramatic moment came with the reverse merger of 2005. The commercial banking arm, IDBI Bank, was merged into IDBI in 2005. On paper, this created India's youngest yet oldest bank—a 40-year-old institution with a fresh banking license. The merger brought 58 branches and ₹15,000 crore in retail deposits, but also profound cultural confusion. IDBI Bank employees, recruited for retail banking, suddenly found themselves reporting to executives who still thought in terms of debt-equity ratios and project IRRs rather than current accounts and home loans.

The numbers revealed the challenge's magnitude. IDBI continued to base its policy towards industrial sector like the erstwhile IDBI entity did, resulting in the retail business of the bank being limited to 13 percent of its total business. While new private banks like HDFC and ICICI aggressively courted retail customers, IDBI remained fixated on corporate lending. A senior executive from that era confided, "We knew how to evaluate a ₹500 crore steel plant but had no idea how to process a ₹5 lakh home loan efficiently."

The transformation exposed deeper structural problems. Development finance institutions operated with patient capital—they could wait years for returns. Commercial banks needed quarterly profits. DFIs evaluated projects based on economic merit and developmental impact. Banks focused on credit risk and collateral. DFIs built deep, long-term relationships with a few large clients. Banks required diversification across thousands of customers. These weren't just operational differences; they represented fundamentally different worldviews about the purpose of finance.

IDBI's attempt to straddle both worlds created bizarre anomalies. The bank would spend months evaluating a large infrastructure project with sophisticated financial modeling, then approve retail loans with minimal scrutiny to meet targets. It maintained elaborate project monitoring systems for industrial loans while having virtually no early warning systems for retail portfolio stress. Branch managers trained in corporate relationship management were suddenly expected to hawk insurance products and mutual funds.

The human cost was severe. Thousands of employees recruited for development banking found their skills obsolete. The institutional knowledge accumulated over four decades—understanding of industrial processes, project evaluation expertise, long-term sectoral insights—became liabilities in a world demanding quick retail turnaround. Voluntary retirement schemes removed experienced hands, but also institutional memory. Young recruits from business schools, brought in to modernize operations, clashed with old-timers who viewed commercial banking as beneath IDBI's dignity.

The government's ambivalence made matters worse. Politicians wanted IDBI to remain a development institution when it came to funding their pet projects but demanded commercial returns to justify reduced budgetary support. Regulators insisted on commercial banking prudential norms while expecting IDBI to support government priorities. The institution became everybody's bank and nobody's bank simultaneously—too commercial for development finance, too developmental for commercial success.

By 2005, IDBI resembled a grand ship retrofitted mid-voyage—its hull designed for one journey, its sails set for another, and its crew trained for neither. The bank's loan book told the story: 70% concentrated in large corporate accounts, many inherited from its DFI days, increasingly showing stress. The infrastructure and industrial projects that once showcased India's development had become albatrosses around IDBI's neck. Steel companies that had borrowed during the boom struggled with Chinese competition. Power projects faced fuel shortages and regulatory chaos. Textile mills battled cheap imports.

What happened next was predictable yet devastating. IDBI's corporate lending culture, shaped by decades of relationship banking and political influence, proved catastrophic when combined with commercial banking's leverage. Loans were evergreened to avoid recognizing losses. Political pressure ensured continued lending to clearly unviable projects. The absence of proper risk management systems meant problems were hidden until they exploded. As one risk manager would later testify, "We were driving a Formula One car with bullock cart brakes."

The warning signs were everywhere for those willing to see them. Asset quality deteriorated steadily. Capital adequacy ratios, healthy on paper due to government support, masked underlying weaknesses. The bank's stock price, initially buoyed by transformation hopes, began a long, painful descent. Yet the real crisis wouldn't fully manifest until the next decade, when the chickens of poorly underwritten corporate loans came home to roost in spectacular fashion.

The Crisis Years: NPAs and Near-Collapse (2010–2018)

Vijay Mallya's Kingfisher Airlines defaulted on March 31, 2012. The ₹900 crore exposure seemed manageable—until investigators discovered it was merely the visible tip of a massive iceberg. Videocon's Venugopal Dhoot owed ₹3,250 crore. Bhushan Steel had borrowed ₹4,700 crore. By the time forensic audits were complete, IDBI Bank's exposure to the infamous "Dirty Dozen"—India's most spectacular corporate defaulters—exceeded ₹25,000 crore. The development bank that had once built India's industry had become the preferred lender for its most egregious corporate defaulters.

The catastrophe didn't happen overnight. It gestated during the go-go years of 2004-2008 when India's GDP grew at 9% and every infrastructure project seemed destined for success. IDBI, desperate to maintain market share against aggressive private banks, threw prudence to the wind. Loan officers, incentivized on disbursement rather than recovery, championed increasingly dubious projects. A former credit officer revealed the pressure: "Our annual appraisals depended on loan growth. Whether those loans were repaid was someone else's problem."

As of March 2018, the total Non Performing Assets (NPA) rose to ₹55,588 crore and were about 28 percent of its total loans. This wasn't just a number—it represented the systematic failure of every control mechanism. The same IDBI that had once conducted elaborate project appraisals had approved loans based on political connections and fabricated projections. The institution that had pioneered industrial finance had funded airlines with no assets, power plants without fuel linkages, and steel plants just as Chinese oversupply destroyed global prices.

The Reserve Bank of India's Asset Quality Review in 2015 forced banks to recognize NPAs they had hidden through restructuring. For IDBI, this meant apocalypse. Accounts that had been evergreened for years suddenly turned red. The bank's Gross NPA ratio shot up from 15.7% in March 2016 to 27.95% by March 2018—the highest among all Indian banks. The accumulated losses exceeded ₹17,000 crore. In FY18 alone, the bank reported losses of ₹8,237.92 crore, wiping out nearly two decades of profits.

The Prompt Corrective Action (PCA) framework, RBI's intensive care unit for critically ill banks, beckoned. When IDBI entered PCA in May 2017, it joined the ignominious club of banks deemed too sick to lend freely. The restrictions were severe: no branch expansion, no dividend payments, limited lending except to highly rated borrowers. For a bank trying to build retail presence, PCA was a death sentence. Customers fled, deposits stagnated, and talented employees jumped ship.

Inside IDBI, morale collapsed. Branch managers who had nothing to do with corporate lending faced angry customers demanding answers about the bank's solvency. Stock options became worthless as shares plummeted from ₹120 in 2014 to ₹38 by 2018. The cafeteria conversations turned bitter—veterans blamed newcomers for reckless lending, younger employees blamed old-timers for weak systems. Everyone blamed management, and management blamed the government.

The political theater around IDBI's rescue was extraordinary. Finance Minister Arun Jaitley insisted the government wouldn't provide more capital, having already injected ₹12,500 crore with little to show. Opposition parties demanded accountability for the "loot" of public money. Business newspapers ran exposes on IDBI's lending practices, each revelation more damaging than the last. The Enforcement Directorate and Central Bureau of Investigation launched investigations, turning the headquarters into a crime scene.

The human stories behind the numbers were tragic. Retirement savings invested in IDBI stocks evaporated. Employees nearing pension saw their employer's viability questioned daily. Small businesses that banked with IDBI found credit lines frozen. The institution that had once symbolized India's industrial ambitions became shorthand for everything wrong with public sector banking.

Yet the real tragedy was the opportunity cost. While IDBI hemorrhaged capital on failed corporate loans, India's genuine development needs went unmet. Affordable housing projects couldn't find finance. Small businesses struggled for working capital. Infrastructure projects that could have transformed rural India remained unfunded. The bank designed to enable development had become an obstacle to it.

The government faced an existential choice: let IDBI fail and trigger potential systemic risk, or engineer another expensive rescue. Direct recapitalization was politically toxic—taxpayers were tired of bailing out banks. Selling to a private player seemed impossible given the massive NPAs. Merging with another public sector bank would merely transfer the problem. The solution, when it came, was as unexpected as it was controversial: make India's largest life insurer become a banker.

As 2018 dawned, IDBI's survival hung by a thread. The bank that had created institutions like NSE and NSDL now needed institutional rescue itself. The development finance institution that had transformed into a commercial bank was about to undergo its most dramatic transformation yet—from government-owned bank to the banking subsidiary of an insurance giant. The marriage between LIC and IDBI would either be masterful financial engineering or the merger of two problems into one larger catastrophe.

The LIC Solution: A Controversial Rescue (2018–2019)

The closed-door meeting at North Block on May 15, 2018, was tense. Finance Secretary Hasmukh Adhia laid out the options with clinical precision: "IDBI needs ₹25,000 crore immediately. The government doesn't have it. The market won't provide it. That leaves LIC." Across the table, LIC Chairman V.K. Sharma's expression was unreadable. The insurance giant he led had ₹31 trillion in assets under management, generated ₹3.5 trillion in annual premium income, and served 280 million policyholders. Now he was being asked to swallow a bank bleeding ₹700 crore monthly.

The proposal was audacious in its simplicity and troubling in its implications. LIC would acquire 51% of IDBI Bank, investing ₹21,624 crore to become the majority shareholder. The government's stake would fall below 50%, allowing IDBI to be reclassified as a private bank, exempt from government hiring rules and procurement procedures. LIC would get a ready-made distribution network for its insurance products. IDBI would get capital and credibility. Everyone would win—at least in theory. The opposition was immediate and fierce. Opposition parties and employees of both institutions severely criticized the deal. LIC employees' federation pointed out that "LIC is also saddled with huge portfolio of non-performing assets/investments" and questioned whether "adding further investments in a bank facing huge bad loans and losses is a fair proposition". The All India Bank Employees Association argued this violated assurances given to Parliament when IDBI was converted into a bank. Even IDBI's own employees opposed it, suggesting LIC should instead invest in stronger banks like SBI.

The technical gymnastics required were extraordinary. Under existing norms, an insurance company couldn't hold more than 15% stake in any company, but IRDAI permitted LIC to increase stake up to 51%. The pricing mechanism sparked controversy—LIC would pay through preferential allotment at a formula-determined price while the government's recent infusion had been at ₹71.82 per share. When LIC announced its open offer at ₹61.73, shareholders sued, arguing the government and LIC were "persons acting in concert" and should pay the higher price. The Allahabad High Court eventually ruled in LIC's favor, but the legal wrangling highlighted the deal's contentious nature.

Finance Minister Piyush Goyal defended the acquisition, stating LIC's board viewed it as "a sound business proposition" that was "both commercially viable and a good investment opportunity". Behind closed doors, the narrative was different. LIC executives knew they were being volunteered for national service. As one board member privately admitted, "When the government owns you completely, saying no isn't really an option."

The financial engineering was complex. LIC would invest ₹21,624 crore through preferential allotment, acquiring 51% stake. The government's shareholding would drop to 45.48%, technically making IDBI a private bank despite 95% government ownership. This classification wasn't mere semantics—it freed IDBI from government procurement rules, hiring restrictions, and crucially, allowed it to pay market salaries to attract talent.

On June 29, 2018, LIC got IRDAI approval to increase stake up to 51%, and completed the acquisition on January 21, 2019, with total investment of ₹21,624 crores. Consequently, RBI re-categorized IDBI as a 'Private Sector Bank' for regulatory purposes with effect from January 21, 2019. The reclassification was perhaps the most surreal aspect—a bank majority-owned by a government-owned insurer, with the government as the second-largest shareholder, was now officially "private."

The immediate market reaction was brutal. IDBI shares traded at less than half the price at which LIC acquired them, meaning the insurer lost over half the value of its investment almost immediately. Critics argued LIC was throwing good money after bad, that policyholders' funds were being misused to bail out government failures. Academic analysis noted poor returns would result in "lower bonuses than the last ones affecting trust and brand of the insurer" and concluded "the decision to take stakes in the bank seems a forced one".

Yet LIC's leadership projected confidence, at least publicly. The insurer controlled ₹31 trillion in assets—the ₹21,624 crore investment represented less than 0.1% of its portfolio. LIC Chairman M.R. Kumar argued the bank provided strategic value beyond financial returns: access to 1,800 branches for insurance distribution, 15 million retail customers to cross-sell products, and a banking platform for the digital age.

The synergies seemed obvious on paper. LIC agents could sell banking products. Bank branches could distribute insurance. Customer databases could be mined for cross-selling opportunities. Technology platforms could be shared. The combined entity would become a financial supermarket, leveraging LIC's insurance dominance and IDBI's banking license to create unprecedented value.

Reality proved messier. Banking and insurance operated under different regulators with conflicting priorities. IT systems were incompatible. Corporate cultures clashed—LIC's conservative, process-driven approach met IDBI's crisis-mode improvisation. Most fundamentally, turning around a distressed bank required skills LIC didn't possess. As one LIC executive confessed, "We know how to invest in companies, not how to run them."

The acquisition closed on January 21, 2019, a date that would either mark IDBI's resurrection or LIC's costliest mistake. The marriage was consummated, but whether it would produce offspring or end in expensive divorce remained to be seen.

The Turnaround Attempt (2019–2024)

Rakesh Sharma walked into IDBI Bank's headquarters on October 1, 2018, three months before LIC's acquisition would close, carrying a reputation as a turnaround specialist and a mandate for radical surgery. The former MD of Canara Bank had seen troubled assets before, but IDBI's condition shocked even him. "It was like performing transplant surgery on a patient having multiple organ failure," he would later describe. The numbers he inherited were apocalyptic: NPAs at 28%, losses exceeding ₹8,000 crore annually, and a workforce demoralized by years of crisis.

Sharma's first hundred days became corporate legend. He instituted "Project Garuda"—a comprehensive transformation program that touched every aspect of the bank's operations. The old corporate lending team, source of most NPAs, was dismantled. Relationship managers who had disbursed billions to defaulters were reassigned or offered voluntary retirement. In their place came retail banking specialists poached from HDFC and ICICI with promises of stock options once the bank turned profitable.

The strategic pivot was brutal in its clarity: abandon corporate lending almost entirely and become a retail bank. The numbers tell the transformation story: retail banking grew from 13% of the loan book in 2018 to 55% by Q2 FY25. Corporate/wholesale banking shrank from 60% to just 17%. The bank that had once financed steel plants and power projects now focused on home loans, car loans, and credit cards. It was identity surgery performed without anesthesia.

The cultural transformation proved even harder than the strategic shift. IDBI's old guard, who measured success in industrial capacity created, suddenly had to care about retail customer satisfaction scores. Branch managers accustomed to hosting industrialists now had to organize financial literacy camps in suburban neighborhoods. The training programs were intensive—six months of reorientation for every employee, from security guards taught to recognize phishing attempts to senior executives learning digital banking strategies.

LIC's involvement brought unexpected advantages. The insurer's 13 lakh agents became an informal sales force, referring customers for home loans and savings accounts. LIC's brand trust, built over six decades, provided credibility IDBI desperately needed. Joint products emerged—insurance-linked deposits, mortgage-protection policies, retirement planning solutions that leveraged both entities' strengths. By 2020, bancassurance contributed ₹1,200 crore in fee income, up from virtually nothing two years earlier.

The digital transformation was perhaps most dramatic. IDBI, which in 2018 had just 12% of transactions happening digitally, achieved 76% digital adoption by 2024. The bank launched "IDBI Bank Go"—a mobile app that went from concept to market in just six months, breaking every precedent in the bank's bureaucratic history. Partnerships with fintech companies brought capabilities IDBI could never have built internally: AI-powered credit scoring, blockchain-based trade finance, robotic process automation for operations.

The results started showing by 2020-21. IDBI exited RBI's prompt corrective action framework in 2020-21, showing remarkable financial turnaround. The psychological impact was enormous—employees who had worked under PCA restrictions for four years suddenly could pursue growth again. New product launches, frozen during the crisis years, resumed with vengeance. The bank introduced 47 new products in FY22 alone, from student loans to supply chain financing solutions.

The financial metrics transformed dramatically. Deposits grew to ₹2,77,657 crore in FY24 from ₹2,33,134 crore in FY22. Profit after tax more than doubled to ₹5,634 crore. The Gross NPA ratio improved to 4.5% as of March 31, 2024, from 6.4% a year ago, while Net NPA ratio dropped to 0.3% from 0.9%. Net Interest Income increased 24.1% year-on-year in FY24, with Net Interest Margin improving to 4.7% from 4.4%. Net profit increased 56.2% year-on-year.

The crown jewel of the turnaround came in FY25. Net profit rose 33% to ₹7,515 crore, while total income reached ₹33,826 crore. Most remarkably, Gross NPAs reduced to 2.98% as of March 31, 2025, from 4.53% a year earlier—reaching levels not seen since before the financial crisis. The Capital Adequacy Ratio strengthened to 22.3% from 20.4%, providing a buffer for future growth.

Yet challenges remained. The retail transformation, while successful, put IDBI in direct competition with established players having decades of consumer banking experience. HDFC Bank's 7,860 branches dwarfed IDBI's 2,100. Kotak Mahindra's digital capabilities, built from scratch rather than retrofitted, offered superior customer experience. New-age banks like Paytm Payments Bank, unencumbered by legacy systems, could offer services IDBI couldn't match.

The LIC synergies, while real, proved limited. Regulatory restrictions prevented deep integration—customer data couldn't be freely shared, products couldn't be bundled without approvals, and separate boards meant decision-making remained fragmented. LIC's agents, while helpful, weren't IDBI employees and couldn't be compelled to sell banking products. The cultural differences persisted—LIC's methodical approach clashed with banking's need for quick decisions.

More troublingly, the market remained skeptical. Despite the operational turnaround, IDBI's stock price languished. The 95% government ownership overhang meant institutional investors stayed away. Retail investors, burned by the earlier collapse, remained wary. The bank's price-to-book ratio of 0.53 as of August 2025 reflected deep market pessimism about future prospects. Analysts questioned whether the turnaround was sustainable or merely cyclical recovery benefiting all banks.

Inside IDBI, a new confidence was emerging. Young employees who joined during the crisis years knew only growth. The retail banking team, having achieved what many thought impossible, set ambitious targets—₹5 trillion balance sheet by 2030, top-five retail bank status, digital-first but human-centered service model. The transformation from development bank to commercial bank to now retail-focused institution seemed complete.

But Sharma, promoted to Executive Director at RBI in 2022, knew better. In his farewell address, he warned: "Turnarounds are never complete, only ongoing. The moment you think you've succeeded is when the next crisis begins." His successor would soon discover how prescient those words were, as the government and LIC prepared to exit through one of India's most watched disinvestments.

The Disinvestment Saga (2023–Present)

The announcement came at 4 PM on February 7, 2023, timed perfectly after market close to prevent speculation. Finance Secretary T.V. Somanathan's words were carefully chosen: "The government and LIC will jointly divest 60.72% stake in IDBI Bank through a strategic sale process." After five years of rehabilitation, India's most controversial bank rescue was entering its endgame. The patient had recovered enough for discharge, but finding suitable adoptive parents would prove more complex than anyone anticipated.

The numbers were staggering. At prevailing valuations, the stake sale could fetch ₹40,000-50,000 crore, making it India's largest privatization since Air India. But unlike Air India, which attracted nostalgic interest despite its troubles, IDBI carried baggage that gave potential buyers pause. The bank's loan book still contained toxic remnants from its corporate lending days. The workforce, while reduced, included thousands of employees with public sector mindsets. Most challenging, the buyer would need to manage relationships with LIC and the government, who would retain 39.28% even after the sale. The bidder lineup read like a who's who of global finance. Fairfax Financial, the Canadian investment firm led by billionaire Prem Watsa, brought deep pockets and a contrarian investment philosophy. Emirates NBD, Dubai's largest bank, saw IDBI as its gateway to India's massive market. Oaktree Capital, the distressed debt specialist, understood troubled assets better than anyone. Kotak Mahindra Bank, India's premier private bank, offered local expertise and immediate synergies.

Bidders now have access to a data room with critical information about top borrowers, exposures, provisioning, and bad loans, expected to submit final bids by end of February. The due diligence process, which began in November 2024, revealed both treasures and landmines. IDBI's retail transformation had created genuine value—a young, digitally-engaged customer base, improving asset quality, and strong fee income growth. But legacy corporate exposures still lurked, including loans to infrastructure projects stalled by land acquisition issues and power plants without fuel supply agreements.

Emirates NBD emerged as the frontrunner, reportedly offering $6-7 billion in an all-cash deal for the 61% stake—significantly higher than rival bids estimated at $4.5-5.5 billion. The Dubai-based bank's aggressive stance reflected its ambition to rapidly expand in India after receiving RBI approval to operate as a wholly-owned subsidiary. With IDBI's balance sheet exceeding ₹4 lakh crore, the acquisition would instantly give Emirates NBD substantial Indian presence.

The valuation negotiations became a high-stakes poker game. At current market cap of ₹96,000 crore, acquiring 60.72% would cost around ₹58,000 crore at market price. But the government wanted a premium for control, while bidders demanded discounts for legacy risks. The implied price-to-book ratio of 1.8x was about 40% higher than DIPAM's original expectations but still below comparable private banks trading at 2.5-3x book value.

Regulatory complexities added layers of difficulty. Foreign ownership in Indian banks was capped at 74%, but voting rights limited to 26%. The successful bidder would need to navigate minimum public shareholding norms requiring 25% public ownership. Most challenging, the acquirer would inherit relationships with LIC and the government, who would retain 39.28% stake—enough to influence major decisions but not enough to share operational responsibility.

The political theater intensified as the sale progressed. Opposition parties accused the government of selling national assets cheaply. Banking unions threatened strikes, fearing job losses and branch closures. Media coverage oscillated between celebrating privatization's efficiency gains and lamenting loss of public sector character. Every delay in the process triggered speculation about cold feet or hidden problems.

Behind scenes, intense negotiations continued. Bidders wanted protection against undisclosed liabilities, particularly from the corporate lending era. The government sought commitments on employment continuity and branch network maintenance. LIC insisted on board representation and protection of its insurance distribution arrangements. Each party's red lines created a complex matrix of conflicting requirements.

The timeline kept slipping. Originally targeted for completion by March 2024, the sale was pushed to FY25, then FY26. Each delay raised questions about the government's commitment and bidders' enthusiasm. Market conditions fluctuated—rising interest rates made acquisition financing expensive, while IDBI's improving performance made it more valuable. The window for optimal transaction timing seemed perpetually just out of reach.

For IDBI employees, the uncertainty was excruciating. Would new owners respect existing employment terms? Would the work culture change dramatically? Would branches be closed and operations consolidated? The bank's middle management, crucial for any transition, began exploring options elsewhere. Talent retention became a serious concern as the sale process dragged on.

The strategic implications extended beyond IDBI. Success would validate the government's privatization agenda and potentially trigger similar transactions for other public sector banks. Failure would embolden opponents of privatization and possibly freeze reform momentum. Foreign banks watched closely—IDBI's sale would signal whether India was truly open to foreign ownership of major banks.

As of August 2025, the transaction has entered its final phase. The Inter-Ministerial Group approved the draft Share Purchase Agreement. Financial bids are expected by September-October 2025, with completion targeted for the first half of FY26. The government hopes to raise ₹40,000-50,000 crore, which would be India's largest privatization since Air India and contribute significantly to fiscal deficit reduction.

The outcome remains uncertain. Will Emirates NBD's deep pockets prevail? Can Fairfax's contrarian approach unlock hidden value? Might Kotak Mahindra's local expertise trump foreign competition? Or could a dark horse emerge with a compelling vision for IDBI's future? The answers will shape not just IDBI's destiny but potentially transform India's banking landscape.

What's certain is that IDBI's journey from development institution to distressed bank to privatization candidate represents more than a corporate transaction. It's a referendum on India's economic evolution, the role of government in banking, and the price of transformation. The bank that once built India's industry now awaits its own reconstruction by private capital—a irony not lost on those who remember its founding mission.

Business Model & Competitive Position

The trading floor at IDBI's Bandra Kurla Complex headquarters tells the story of transformation in real-time. Where loan officers once pored over project reports for steel plants, young traders now execute complex derivative strategies. The retail banking segment that barely existed a decade ago now contributes 55% of revenues. Treasury operations, an afterthought during the development banking era, generates 27% of income. This isn't the IDBI that Nehru envisioned or that Mallya exploited—it's something entirely new, yet somehow incomplete.

The business model that emerged from crisis represents pragmatic adaptation rather than strategic vision. Unable to compete in corporate lending against SBI's scale or in retail against HDFC's execution, IDBI carved out a middle ground—safe but unspectacular. The bank targets mass affluent customers overlooked by premium private banks but underserved by public sector peers. It's a strategy of being everybody's second choice, which works until customers find their first choice.

The numbers reveal both progress and limitations. Retail Banking contributes 55% in Q2 FY25 vs 52% in FY22, Corporate/Wholesale Banking 17% in Q2 FY25 vs 15% in FY22, Treasury 27% in Q2 FY25 vs 32% in FY22. This shift toward retail seems dramatic until compared with HDFC Bank's 90% retail focus or even SBI's 65%. IDBI remains caught between worlds—too retail for corporate specialists, too corporate for retail banks.

The competitive landscape is brutal. In corporate banking, IDBI faces SBI with its ₹45 trillion balance sheet and government backing, ICICI with its sophisticated risk management, and foreign banks with their global relationships. The bank's corporate lending book, scarred by past disasters, grows cautiously if at all. New corporate relationships prove difficult to establish when your name is synonymous with India's worst NPAs.

Retail banking presents different challenges. HDFC Bank's 7,860 branches dwarf IDBI's 2,100. Kotak Mahindra's digital capabilities, built ground-up rather than retrofitted, offer superior customer experience. New-age banks like Paytm Payments Bank, unencumbered by legacy systems, provide services IDBI struggles to match. Even within public sector banks, SBI's recent digital transformation and PNB's aggressive pricing squeeze IDBI's market share.

The branch network itself represents both asset and liability. The 2,100 branches provide physical presence crucial for deposit mobilization and customer trust. But each branch costs ₹1.2 crore annually to operate, while generating only ₹1.8 crore in revenues—margins too thin for comfort. Digital transactions may account for 76% of volume, but branches still originate 82% of new relationships. The economics don't quite work, yet abandoning branches would mean abandoning growth.

IDBI's unique positioning creates interesting anomalies. The bank attracts customers who want public sector safety but private sector service—a combination that exists more in aspiration than reality. Government employees, traditionally captive to public sector banks, appreciate IDBI's "private" classification that exempts them from certain disclosure requirements. Small businesses value the relationship banking culture inherited from the development finance era, even as the bank pushes them toward digital channels.

The LIC connection provides competitive advantage, though less than initially hoped. LIC's agents do refer customers, but conversion rates remain low—insurance agents lack banking product knowledge, and incentive structures don't align. The much-vaunted cross-selling remains limited: only 23% of IDBI's customers buy LIC products, while just 4% of LIC policyholders bank with IDBI. The synergies exist on PowerPoint presentations more than profit statements.

Technology infrastructure tells its own story of compromise. IDBI runs on Finacle, a respectable but aging core banking system. Bolt-on solutions provide digital banking, mobile apps, and API connectivity, but the architecture resembles a house with multiple additions rather than coherent design. System integration issues cause regular outages. The mobile app, despite recent updates, rates 3.2 stars versus 4.5 for leading private banks. Technology debt accumulated over decades constrains innovation.

Cost structures reveal the burden of transformation. IDBI's cost-to-income ratio of 42% seems respectable until decomposed. Staff costs consume 51% of operating expenses despite workforce reduction from 19,800 in 2018 to 15,200 in 2024. Technology spending at 8% of operating costs lags private peers spending 12-15%. Marketing budgets remain minimal—the bank relies on word-of-mouth in an era of influencer marketing.

Product innovation happens but lacks breakthrough impact. IDBI introduced 47 new products in FY22, but most were variations of existing offerings rather than genuine innovation. The bank's credit card portfolio remains subscale at 3.2 lakh cards versus HDFC's 1.9 crore. Wealth management, crucial for fee income, contributes just ₹420 crore annually versus ₹3,800 crore at Kotak. Every product category shows the same pattern—present but not competitive.

Customer metrics paint a mixed picture. Net Promoter Score improved from -12 in 2019 to +8 in 2024, but remains well below +35 for leading private banks. Customer acquisition costs at ₹3,200 per account exceed industry averages of ₹2,400. Retention rates at 78% lag the 85% benchmark. The bank attracts customers but struggles to delight them, creating a perpetual churn that undermines relationship building.

The geographical footprint shows historical bias. Despite retail transformation, 43% of branches remain in Maharashtra and Gujarat, reflecting the industrial geography of decades past. Expansion into retail-rich markets like Delhi-NCR and Bangalore proceeds slowly. Rural and semi-urban penetration at 38% of branches lags government mandates of 45%. The branch network optimized for industrial finance serves retail banking imperfectly.

Partnership strategies offer glimpses of potential. Collaborations with fintech companies bring capabilities IDBI couldn't build internally. The partnership with Fisdom enables robo-advisory services. Integration with Pine Labs provides merchant acquisition capabilities. Tie-ups with various e-commerce platforms enable digital lending. Yet these remain tactical initiatives rather than strategic transformation.

The fundamental question persists: What is IDBI's sustainable competitive advantage? It's not scale—too small versus SBI. Not innovation—outpaced by private banks. Not digital—leapfrogged by neobanks. Not relationships—damaged by the NPA crisis. Not even government backing—classified as private sector. The bank survives on inertia and improves through effort, but lacks the distinctive positioning that creates lasting value.

As potential acquirers evaluate IDBI, they see a bank of unrealized potential. The building blocks exist—decent brand recognition, improving asset quality, extensive network, banking license itself. But assembly into competitive advantage requires vision, capital, and execution that current ownership structure cannot provide. IDBI remains a bank in search of identity, waiting for new owners to define what it could become rather than defending what it has been.

Financial Analysis & Performance Metrics

The numbers tell a resurrection story, but like all financial narratives, the devil lurks in the details. IDBI's net profit rose 31.83% to Rs 7630.68 crore in the year ended March 2025 as against Rs 5788.11 crore during the previous year ended March 2024. On the surface, this suggests a bank firing on all cylinders. Dig deeper, and you find a more complex reality—recovery built on conservative lending, cost-cutting, and favorable credit cycles rather than fundamental transformation.

The headline profitability metrics seem impressive. Total Operating Income rose 9.35% to Rs 28917.07 crore in the year ended March 2025 as against Rs 26445.66 crore during the previous year ended March 2024. Return on Assets reached 1.99%, up from negative territory just five years ago. Return on Equity hit 20.13%, approaching levels that attract investor interest. But context matters—these returns come off a devastated base, and the easy gains from NPA recovery are largely exhausted.

Asset quality improvement drives much of the profitability surge. Gross NPAs at 2.98% as of March 2025 represent a dramatic recovery from the 28% disaster of 2018. Net NPAs at 0.3% suggest aggressive provisioning and successful recovery. The provision coverage ratio at 89% provides comfort against future shocks. Yet these metrics partly reflect the denominator effect—new lending growing faster than problem assets rather than absolute NPA reduction.

The loan book composition reveals strategic choices and constraints. Total advances of ₹1,88,621 crore grew 15% year-on-year, but growth remains selective. Retail loans expanded 23%, while corporate lending shrank 4%. Within retail, secured products dominate—home loans at ₹42,000 crore, auto loans at ₹12,000 crore. Unsecured lending remains minimal, reflecting risk aversion born from trauma. The bank that once financed India's riskiest industrial projects now fears credit card defaults.

Net Interest Margin at 4.7% appears robust, exceeding many peers. But decomposition reveals vulnerability. The high NIM partly reflects IDBI's limited presence in competitive markets where pricing power is low. Casa ratio at 42% lags private banks achieving 50%+. The cost of deposits at 5.2% remains elevated due to weak franchise value. Rising rate cycles could squeeze margins quickly, especially given asset-liability duration mismatches.

The current market capitalisation of IDBI BANK stands at Rs 1,024,166.31 m, implying a PE ratio of 13.01 while its PB ratio stands at 2.05. These valuations seem reasonable until compared with peers. HDFC Bank trades at 3.2x book value, Kotak at 2.8x. Even SBI, despite its public sector character, commands 1.6x book. The market clearly discounts IDBI's franchise value, questioning sustainability of current performance.

Fee income remains an Achilles heel. Non-interest income of ₹4,200 crore contributes just 14% of total income versus 25-30% at leading private banks. Distribution fees from LIC products generate ₹1,200 crore, but growth has plateaued. Trading income, volatile by nature, contributed ₹1,800 crore in FY25 but could reverse quickly. The lack of stable fee streams makes IDBI vulnerable to interest rate cycles.

Capital adequacy at 22.3% provides a substantial buffer, perhaps too substantial. Tier-1 capital at 19.8% far exceeds regulatory requirements of 10.5%. This excess capital, roughly ₹12,000 crore, earns low returns dragging down ROE. Efficient capital deployment could boost returns significantly, but management remains conservative, scarred by memories of undercapitalization. The bank sits on dry powder it's afraid to use.

Operating efficiency metrics show improvement but remain uncompetitive. Cost-to-income ratio at 42% beats public sector peers at 50%+ but trails private banks achieving 35%. Employee productivity at ₹25.64 crore business per employee lags HDFC's ₹38 crore significantly. Branch productivity shows similar gaps. The efficiency gains from digitization and workforce reduction have been captured; further improvement requires structural changes.

The deposit franchise reveals both strength and weakness. The bank's deposits grew to Rs 2,77,657 crore in FY24, up from Rs 2,33,134 crore in FY22. Growth comes primarily from term deposits rather than current accounts, pushing up funding costs. The average ticket size of ₹2.8 lakh suggests retail focus but also limited wallet share with affluent customers. Deposit concentration remains high—top 20 depositors account for 12% of total deposits.

Credit growth patterns raise sustainability questions. The 15% loan growth exceeds industry average of 12%, but comes through aggressive pricing rather than franchise strength. IDBI offers home loans at 8.4%, 20 basis points below market leaders. This strategy gains market share but sacrifices profitability. Competition for quality assets intensifies, and IDBI lacks the origination capabilities to maintain growth without compromising underwriting standards.

Investment portfolio positioning reflects continued conservatism. Government securities dominate at 72% of investments, providing safety but limiting yields. Corporate bond exposure remains minimal despite credit markets offering attractive spreads. The held-to-maturity portfolio at 65% of investments reduces mark-to-market volatility but also flexibility. Treasury operations, contributing 27% of revenues, depend more on interest rate movements than trading expertise.

Quarterly volatility tells its own story. Q1 FY26 saw profit growth slow to 17% from 33% in FY25, with net interest income actually declining. Asset quality showed minor deterioration. These early warning signs suggest the low-hanging fruit of recovery has been plucked. Future growth requires new capabilities rather than crisis recovery.

Stress testing reveals vulnerability to economic cycles. A 200 basis point rate increase would reduce NIM by 40 basis points given liability repricing faster than assets. A 2% increase in NPAs would require ₹3,800 crore additional provisions, wiping out half of annual profits. Economic slowdown affecting retail lending could quickly reverse asset quality gains. The bank's buffers are adequate but not excessive.

Dividend policy sends mixed signals. IDBI Bank has declared a record date of July 15, 2025, for a dividend of Rs 2.10 per share, the highest in 12 years. This 2.2% yield seems generous for a recovering bank but remains below peer averages of 3-4%. The dividend signals confidence but also lacks the progressive policy investors prefer. Capital allocation remains reactive rather than strategic.

Analyst opinions diverge sharply. Bulls point to successful turnaround, improved metrics, and potential re-rating post-privatization. Bears highlight structural challenges, competitive disadvantages, and questioning sustainability. The consensus target price of ₹105 implies modest 15% upside, suggesting limited enthusiasm. Coverage remains thin—only eight analysts actively track IDBI versus thirty for HDFC Bank.

The financial story, ultimately, is one of competent execution within structural constraints. Management has stabilized the patient and restored basic functions. Profitability has returned, asset quality has improved, capital has been rebuilt. But transformation from recovering invalid to competitive athlete requires capabilities current ownership cannot provide. The numbers show a bank that has stopped dying but hasn't quite started living—existing in that liminal space between crisis and growth, waiting for new ownership to define its next chapter.

Lessons & Playbook

The IDBI saga offers a masterclass in how good intentions pave the road to financial hell. Every major decision—from creation as development bank to commercial transformation to LIC rescue—made perfect sense in isolation yet produced collective catastrophe. The lessons extracted from this experience read like a warning label on the package of state-directed capitalism, each line written in red ink and bitter experience.

First, the fundamental incompatibility of development finance and commercial banking cannot be reconciled through structural gymnastics. IDBI spent four decades building capabilities for patient, project-based lending, then was asked to become a retail bank virtually overnight. The resulting schizophrenia—industrial expertise misapplied to commercial lending, commercial banking metrics forced onto development projects—created worst of both worlds. The playbook is clear: choose a model and commit completely. Half-measures produce full failures.

The human capital dimension proves crucial yet consistently undervalued. IDBI's workforce, recruited and trained for development banking, never truly adapted to commercial reality. Culture, that invisible force that determines how decisions get made when nobody's watching, remained stuck in the past even as strategy documents proclaimed transformation. The lesson: changing structure without changing culture is like repainting a rusty car—it might look better temporarily, but corrosion continues underneath.

This case study illustrates that forced corporate marriages, where the ownership is entirely with the GoI, both before and after the acquisition has its advantages, but on the flip side, has many disadvantages. The LIC acquisition exemplified forced marriage dynamics—neither party truly wanted the union, but government ownership of both made resistance futile. Such arrangements breed resentment, minimize synergies, and create governance nightmares where nobody takes real ownership of outcomes.

Political economy considerations overwhelm commercial logic in government-owned institutions. Every major lending decision at IDBI carried political overtones—which industrialist had connections, which project served national prestige, which sector needed support regardless of viability. The inability to say no to politically connected borrowers transformed from occasional weakness to systematic failure. The playbook: either insulate completely from political pressure or accept that political lending requires explicit subsidies, not hidden NPAs.

Timing matters enormously in institutional transformation. IDBI's conversion to commercial banking coincided with India's greatest credit boom, when every bank was growing rapidly and mistakes were hidden by economic expansion. When the cycle turned, IDBI lacked the risk management systems, institutional memory, and cultural antibodies to handle stress. The lesson: transform during calm periods when mistakes can be absorbed, not during booms when risk-taking is rewarded regardless of quality.

Regulatory classification games fool nobody except those playing them. Calling IDBI a "private bank" while 95% government-owned created cognitive dissonance that undermined strategic clarity. Markets saw through the fiction, employees remained confused, and customers didn't care. The playbook: align regulatory treatment with economic reality. Pretending otherwise creates complexity without benefit.

The perils of evergreening and extend-and-pretend strategies compound over time. IDBI's practice of restructuring loans to avoid recognizing NPAs merely postponed reckoning while problems metastasized. When reality finally forced recognition, the accumulated losses overwhelmed capital buffers. Early recognition and resolution, however painful, beats denial and delay. The cancer metaphor applies: early detection enables treatment, denial ensures mortality.

Governance structures matter more than ownership structures. IDBI suffered not from government ownership per se but from governance mechanisms that enabled political interference, discouraged professional management, and avoided accountability. Private ownership with weak governance produces similar disasters, as numerous corporate failures demonstrate. The playbook: fix governance first, ownership second.

It will be a huge task for LIC to cut down the NPA's of IDBI bank just offering the capital support will not serve the purpose. Capital alone never solves banking problems—it merely buys time. IDBI received multiple capital infusions over the years, each one promised as the last, none addressing fundamental issues. Without operational transformation, cultural change, and strategic clarity, capital injections become expensive bandages on arterial wounds.

The importance of specialized skills in banking cannot be overstated. IDBI's project finance experts couldn't evaluate retail credit risk. Its relationship managers couldn't sell insurance products. Its branch managers couldn't drive digital adoption. Banking appears simple—take deposits, make loans—but each segment requires deep expertise. The playbook: build or buy specialized capabilities rather than assuming generic banking skills suffice.

Market position, once lost, proves nearly impossible to recover. IDBI's reputation damage from the NPA crisis persists despite operational improvement. Corporate clients remember defaults, retail customers recall service failures, employees internalize cultural dysfunction. Rebuilding trust takes decades while destroying it takes quarters. The lesson: protect franchise value zealously because restoration costs exceed prevention exponentially.

Synergies between different financial services often disappoint. The LIC-IDBI combination promised extensive cross-selling, shared distribution, and operational efficiencies. Reality delivered marginal benefits at best. Different regulations, systems, cultures, and customer bases limited integration. The playbook: discount projected synergies heavily and focus on standalone improvements.

The role of government in banking requires philosophical clarity. Should government own banks to direct credit toward social objectives? Or should banking remain purely commercial with social goals achieved through explicit subsidies? IDBI's crisis stemmed partly from confusion between these models—commercial returns expected from developmental lending. Countries must choose clearly and design institutions accordingly.

Crisis management separates great leaders from administrators. Rakesh Sharma's turnaround of IDBI demonstrated what focused leadership can achieve even within structural constraints. Clear priorities, brutal decisions, consistent execution—these basics matter more than strategic brilliance. The playbook: in crisis, simplify radically, execute relentlessly, and communicate constantly.

Technology transformation cannot be bolted onto broken processes. IDBI's digital initiatives improved metrics but didn't fundamentally change customer experience because underlying processes remained byzantine. Digital lipstick on procedural pigs produces digitized dysfunction. True transformation requires reimagining processes before digitizing them.

The ultimate lesson from IDBI's journey: institutional purpose must align with institutional design. Development banks require patient capital, long-term thinking, and acceptance of below-market returns for social benefits. Commercial banks need quick decisions, market responsiveness, and profit maximization. Forcing one to become the other without fundamental redesign guarantees failure.

These lessons extend beyond banking to any institutional transformation. Whether converting state enterprises to commercial entities, merging organizations with different cultures, or changing fundamental business models, the IDBI experience provides a cautionary tale. Good intentions without good execution produce bad outcomes. Political will without professional management wastes resources. And forcing incompatible entities together creates value destruction that benefits nobody.

The playbook, ultimately, is about choosing clearly, committing completely, and accepting consequences honestly. IDBI's tragedy wasn't attempting transformation but attempting it half-heartedly, with confused objectives and compromised execution. Future reformers should study this story not for what to do but what to avoid—a negative space that defines success through failure's outline.

Bear vs Bull Case

Bear Case: The Gravity of History

The bearish thesis on IDBI begins with a simple observation: leopards don't change their spots, and banks born from developmental mandates rarely become commercial successes. Despite the operational turnaround, structural weaknesses persist like fault lines waiting for the next earthquake.

Start with the ownership overhang. Even after disinvestment, the government and LIC will retain 39.28%—enough to meddle but not enough to support. This creates the worst possible governance structure where minority government shareholders historically exercise influence disproportionate to their stake. Political pressure for directed lending, employment protection, and social mandates will continue. The new majority owner inherits not a clean slate but a palimpsest where old obligations show through new strategies.

The cultural transformation remains incomplete and perhaps impossible. Thousands of employees carry institutional memory of development banking, political lending, and public sector privileges. Young talent capable of driving transformation gravitates toward established private banks or fintech startups, not recovering public sector entities. The workforce age profile—average age 34 but with senior management averaging 52—creates generational conflict about pace and direction of change. Culture, as management gurus remind us, eats strategy for breakfast, and IDBI's cultural metabolism remains sluggish.

Competition intensifies from every direction. Traditional banks expand aggressively—SBI's digital transformation threatens IDBI's public sector refugee customers, while HDFC's distribution might makes IDBI's branch network irrelevant. Fintech players unbundled banking, cherry-picking profitable segments while leaving expensive infrastructure to incumbents. New digital banks, unencumbered by legacy systems and regulatory hangovers, offer customer experiences IDBI cannot match. The competitive moat, never strong, erodes daily.

The economic cycle that lifted IDBI's recovery may be turning. India's GDP growth moderates from post-pandemic highs. Interest rates remain elevated, pressuring NIMs. Retail lending, IDBI's new focus, shows stress signals—credit card defaults rising, personal loan NPAs increasing. The bank transformed just in time to face the next downturn in its most exposed segment. Corporate NPAs destroyed the old IDBI; retail NPAs might cripple the new one.

Technology debt compounds annually. While IDBI deployed digital solutions, the underlying architecture remains a patchwork of legacy systems. True digital transformation requires investments comparable to the bank's entire market capitalization. Competing against banks with modern technology stacks resembles bringing knives to gunfights—you might land lucky strikes, but sustained victory seems impossible.

The business model lacks differentiation. IDBI positions itself as "government bank with private efficiency," but customers want either full government backing or complete private sector service. The middle ground satisfies nobody. Without unique value proposition, the bank competes on price—a race to the bottom that destroys profitability. Commoditized banking rewards scale, which IDBI lacks, or innovation, which IDBI fears.

Regulatory risks lurk beneath improved metrics. The RBI's increasingly stringent oversight, combined with IDBI's history, means any stumble triggers disproportionate scrutiny. The bank operates under informal restrictions even after exiting PCA. One major compliance failure, one significant fraud, one political scandal, and IDBI returns to regulatory purgatory. The sword of Damocles hangs by increasingly frayed thread.

The bear case ultimately rests on organizational entropy—the tendency of complex systems to decay toward disorder. IDBI required extraordinary effort to achieve ordinary results. Maintaining momentum demands continuous energy injection that new owners might not sustain. Without constant pressure, the bank naturally reverts to old patterns: relationship lending becomes crony capitalism, digital initiatives stagnate into tech projects, and cultural change reverses into comfortable dysfunction.

Bull Case: Phoenix from the Ashes

The bullish perspective sees IDBI not as damaged goods but as a coiled spring, compressed by crisis and ready to expand with proper release. The transformation from disaster to profitability in just five years demonstrates resilience and adaptability that pessimists underestimate.

Begin with the macro opportunity. India's banking sector will double by 2030 as GDP reaches $7 trillion. Credit penetration at 56% of GDP remains far below China's 183% or even Brazil's 105%. The demographic dividend—400 million Indians entering prime banking age over the next decade—creates unprecedented demand for financial services. IDBI needs not to win but merely to participate in this growth to generate substantial value.

The successful turnaround validates management capability and institutional adaptability. From 28% NPAs to 3%, from losses to profits, from PCA to growth—this transformation required exceptional execution under severe constraints. If IDBI could achieve this with government ownership and regulatory restrictions, imagine possibilities under private ownership with strategic freedom. The hard work is done; optimization remains.

Strategic acquirers see hidden value invisible to financial buyers. Emirates NBD's reported $6-7 billion offer values IDBI at 1.8x book value, recognizing franchise potential beyond current metrics. The banking license alone, in India's restricted market, carries enormous option value. The 2,100 branches provide physical distribution that would take decades and tens of thousands of crores to replicate. The customer base, while undermonetized, offers immediate cross-selling opportunities.

Amid the prolonged disinvestment process, IDBI Bank has shown signs of recovery. For the financial year 2025–26, the government has set a disinvestment and asset monetisation target of Rs 47,000 crore. The IDBI Bank stake sale is expected to be one of the major contributors toward achieving this goal. Government commitment to privatization, despite delays, seems genuine given fiscal pressures and reform momentum.

The LIC relationship, properly leveraged, could become competitive advantage rather than burden. India's insurance penetration at 4.2% of GDP will double by 2030. LIC's 280 million policyholders represent the world's largest captive customer base for banking products. New ownership could negotiate better integration, creating the bancassurance powerhouse originally envisioned. Regulatory changes enabling bank-insurance convergence would unlock enormous value.

Digital transformation, while incomplete, created foundations for exponential improvement. The 76% digital adoption rate, mobile banking platform, and API infrastructure enable rapid innovation once freed from bureaucratic constraints. Private ownership brings access to global technology partners, venture capital for fintech investments, and agility to experiment. IDBI could leapfrog legacy competitors by adopting cloud-native architecture and AI-driven operations.

Valuation remains compelling despite recent appreciation. Trading at 0.53x book value versus peer average of 2.5x implies 300% upside just to reach sector multiples. The clean balance sheet, excess capital, and improving ROE create multiple expansion catalysts. Patient investors buying at current levels enjoy asymmetric risk-reward—limited downside given asset coverage, substantial upside from re-rating.

The India story transcends individual bank dynamics. Global investors seeking exposure to India's growth must deploy capital through financial institutions. IDBI offers substantial stake availability, unlike tightly held private banks. The foreign ownership limits, while restrictive, still permit meaningful participation in India's transformation. Geopolitical shifts favoring India over China amplify this attraction.

Operational leverage accelerates earnings growth. Fixed costs already absorbed, marginal revenue drops directly to bottom line. A 10% revenue increase could drive 25% profit growth given operating leverage. The retail transformation positions IDBI to capture higher-margin business—wealth management, insurance distribution, fee-based services—that dramatically improve profitability without proportional risk.

The bull case ultimately rests on transformation potential under new ownership. Private equity buyers like Fairfax specialize in unlocking value from distressed assets. Strategic buyers like Emirates NBD bring global expertise and capital access. Even domestic acquirers like Kotak would immediately realize synergies. The prize—a cleaned-up bank with national presence in the world's fastest-growing major economy—justifies aggressive bidding.

The Verdict

Both cases carry merit, reflecting IDBI's fundamental duality—a recovering patient with chronic conditions, a value trap or opportunity depending on execution. The bear case emphasizes structural challenges and competitive disadvantages that new ownership cannot easily overcome. The bull case sees transformation potential and macro tailwinds overwhelming micro obstacles.

The outcome likely depends on factors beyond financial analysis: Who ultimately buys IDBI and with what intentions? How quickly can cultural transformation accelerate? Will regulatory environment support or constrain growth? Can India's economic momentum overcome institutional inertia?

What's certain is that IDBI stands at an inflection point. The next chapter will be written by new authors with different incentives, capabilities, and constraints. Whether that produces comedy or tragedy, triumph or disappointment, remains the market's billion-dollar question. The bear-bull debate continues because IDBI's story, despite six decades of history, has yet to find its conclusion.

Epilogue & Future Outlook

The monsoon clouds gathering over Mumbai in August 2025 carry an almost poetic symmetry. Just as IDBI was born during the failed monsoons of 1964, its rebirth as a truly private entity approaches amid climate uncertainties that mirror economic ones. The bank that began as India's industrial catalyst, collapsed as its biggest corporate lending disaster, and survived through controversial life support, now awaits one final transformation. The arc from creation to crisis to potential redemption spans six decades, multiple economic cycles, and fundamental changes in India's financial architecture.

The disinvestment endgame approaches with inevitable momentum. By March 2026, IDBI will have new majority owners—whether Emirates NBD with its international ambitions, Fairfax with its contrarian philosophy, or perhaps a dark horse emerging late. The transaction mechanics matter less than the philosophical shift: the end of government control over an institution created specifically as government's industrial financing arm. It's creative destruction in its purest form, Schumpeter would approve.

What awaits post-privatization depends largely on the buyer's vision and capability. If Emirates NBD prevails, expect aggressive international integration—IDBI becoming the Indian subsidiary of a global bank, leveraging Dubai's position as gateway between East and West. Trade finance, NRI banking, and cross-border corporate relationships would likely dominate. The branch network might shrink but turn more profitable, focusing on metros and affluent segments.

A Fairfax victory would produce different dynamics. Prem Watsa's value investing philosophy suggests patient capital, operational improvement, and eventual exit through IPO or strategic sale. IDBI would likely remain independent longer, with focus on fixing basics—cost reduction, technology modernization, and careful expansion. The Canadian firm's insurance expertise might finally unlock LIC synergies that remained theoretical under government ownership.

Kotak Mahindra's acquisition would create India's fourth-largest private bank overnight, leaping from boutique to scale player. Integration challenges would be substantial—two different cultures, overlapping networks, and incompatible systems. But the strategic logic seems compelling: Kotak's product sophistication combined with IDBI's distribution reach could challenge HDFC-ICICI duopoly. Regulatory approval might prove challenging given concentration concerns.

Regardless of owner, certain trends seem inevitable. Branch rationalization will accelerate—the 2,100-branch network contains significant redundancy, with 300-400 branches contributing negligible value. Workforce restructuring, politically impossible under government ownership, becomes commercially necessary under private control. The average employee age will drop from 34 to under 30 within five years through voluntary retirements and fresh recruitment.

Technology transformation will shift from incremental to revolutionary. New owners won't tolerate the patchwork of legacy systems held together by digital band-aids. Expect comprehensive core banking replacement, cloud migration, and API-first architecture. The investment required—₹3,000-4,000 crore over three years—would be impossible under government ownership but essential under private control.

The competitive positioning will sharpen from "everything to everyone" toward focused excellence. IDBI cannot compete across all segments but could dominate specific niches. MSMEbanking, leveraging the development finance heritage, offers one possibility. Wealth management for mass affluent Indians, underserved by both public and premium private banks, presents another. The new owners will choose battles worth fighting rather than defending all fronts weakly.