The Bed Linen King: Indo Count Industries Limited (ICIL)

I. Introduction: The Silent Giant in Your Bedroom

Walk into a Costco in Sacramento on a Saturday morning. Navigate past the rotisserie chickens, the pallets of Kirkland water, the unreasonable quantities of toilet paper. Eventually you arrive at the soft-goods aisle, where stacks of cotton sheets sit in clear plastic sleeves, marked with thread counts like trophies — 600, 800, 1000. Pick one up. Flip it over. Look at the small print at the bottom of the label.

There is a roughly one-in-five chance that the sheets in your hand were manufactured at a sprawling facility in कोल्हापुर Kolhapur, a city of around a million people in western Maharashtra better known for jaggery, leather sandals, and a notoriously spicy mutton curry called तांबडा-पांढरा रस्सा. The same is true if you bought your sheets from Target in Plano, from Macy's in Manhattan, from Walmart's vast e-commerce engine, or — increasingly — from Amazon's home category. The bed sheet is one of the most invisible consumer products in the modern home. You touch it for eight hours a night and never look at it. You replace it once every three to five years. You almost never know who made it.

The company is Indo Count Industries Limited — ICIL on the National Stock Exchange of India. It is, by capacity, the largest bed-linen-only manufacturer in the world, with a finished-goods capacity of roughly 153 million metres a year and customers in fifty-four-plus countries.12 Its sheets find their way onto beds in Walmart, Target, Macy's, Amazon, and Costco — names that, between them, account for a meaningful share of every dollar Americans spend on home textiles.3

But this is not a story about a Costco sheet. It is a story about a man who, in 1988, started a humble export-oriented cotton-spinning unit in a state that was famous for cotton and almost nothing else, and who — over the next three-and-a-half decades — quietly built a company that turned a commodity (yarn) into a consumer product (the thing you sleep on) and, in doing so, captured more global market share in a single category than any other Indian textile player in modern history.

The thesis we want to chase in this episode is deceptively simple: how does a mid-tier Indian spinning mill, born in the worst possible decade for Indian textiles, end up dictating the bed linen aisle at Walmart? The answer involves a humiliating commodity trap, a counter-intuitive pivot, a son educated at Babson College, a 596-crore acquisition that doubled capacity overnight, and the cold-eyed purchase of a 178-year-old American brand from a bankruptcy estate for $10.25 million.45

It also involves a series of smaller, less glamorous decisions — the choice not to vertically integrate when everyone else did, the choice not to enter apparel when the rest of the industry stampeded toward it, the choice to invest in a 100-person design studio before there was a customer who explicitly asked for one, the choice to stay focused on a single product category when conglomerate-style diversification was the default Indian business playbook. Each individual decision looks ordinary in retrospect. Together they describe a company that has compounded itself into a position that nobody else in Indian textiles currently occupies.

In a country where the textile industry is famous for being many things — fragmented, cyclical, capital-hungry, politically protected, occasionally scandalous, often subsidy-dependent — ICIL stands out as something rarer: a focused operator that figured out, very early, that the prize was not the loom but the relationship with the retailer. The asset-right model. The slow accumulation of design capabilities. The patient pivot from selling cotton at $2 a kilo to selling finished bed linen at $15 a kilo.6

Why does this matter to anyone who is not a textile specialist? Because ICIL is, in many ways, a case study in how Indian manufacturing actually transitions from the bulk-commodity era to the value-added export era — the same transition that the country's policymakers have been trying to engineer at scale for two decades, with mixed success. Bedsheets are a particularly clear lens because the product is simple, the demand is durable, the customers are well-known, and the competitive set is finite. If you want to understand the China-plus-one trade, the post-Bed-Bath-and-Beyond redrawing of US home retail, and the future of Indian export manufacturing in a single sitting, ICIL is as good a place to start as any.

In the next two hours, we will trace exactly how that happened — and what it tells us about manufacturing in modern India, about the China-plus-one trade, and about the unglamorous, deeply unsexy business of selling people sheets they touch only at night and forget about by morning. Let us begin where every Indian industrial story seems to begin: in the 1980s, with a man, a license, and a piece of land outside a small city.

II. Founding & The Commodity Trap

The year is 1988. India is still four years away from liberalising its economy. The Licence Raj is intact. The rupee is non-convertible. A typical entrepreneur in Maharashtra spends as much time placating government inspectors as he does running his business, and the textile industry — once the crown jewel of Indian manufacturing — is in the middle of a slow, generational decline. The great Bombay textile strike of 1982 has already broken the unions of गिरणगाव Girangaon. The mills of central Mumbai are months away from being shuttered and sold for real estate that would, two decades later, become the most expensive zip codes in the country. Lower Parel will be condominiums and office towers. The looms will be gone.

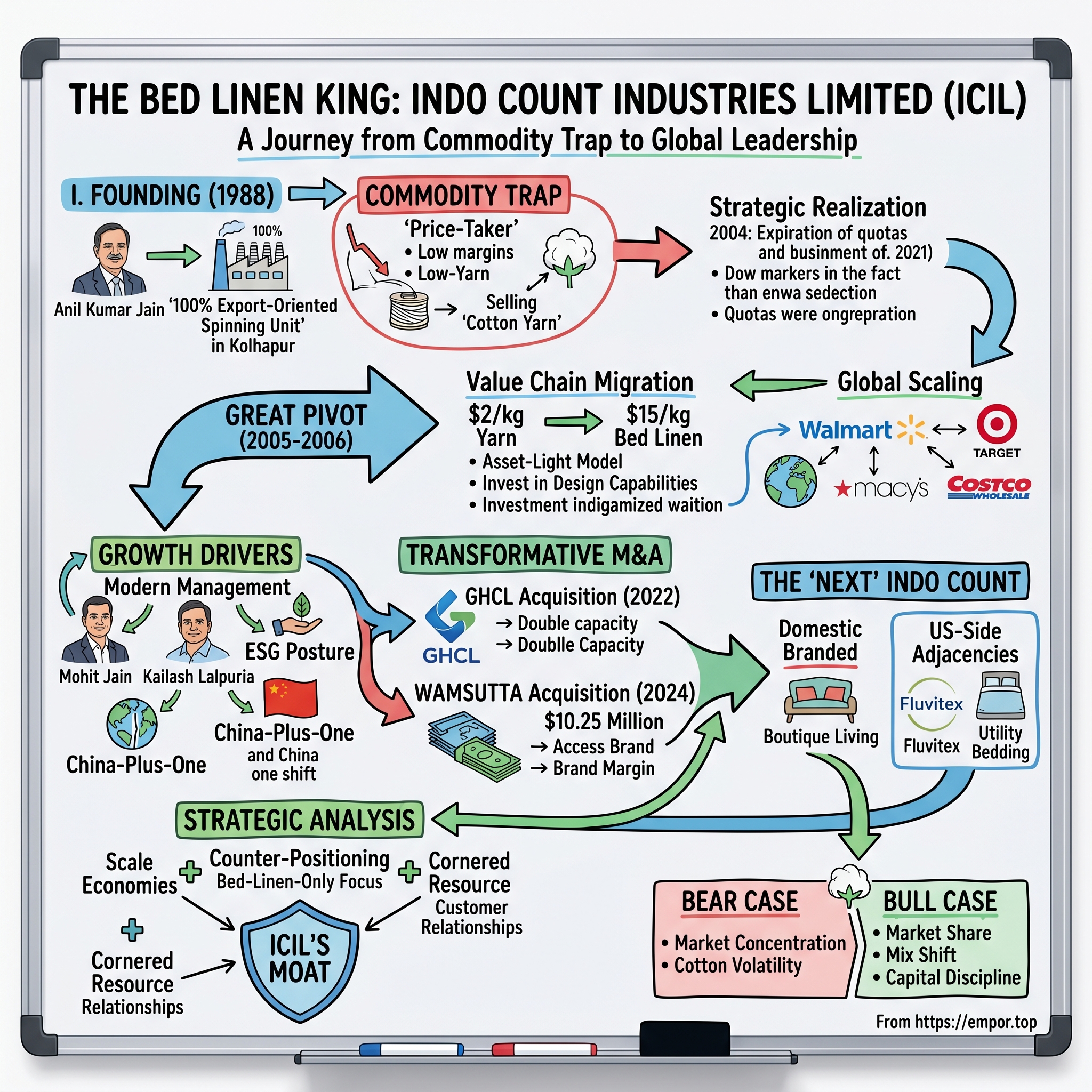

Into that landscape walked Anil Kumar Jain, a textile entrepreneur with patience that bordered on stubbornness. On November 7, 1988, he incorporated Indo Count Industries Limited as a 100%-export-oriented combed cotton yarn spinning unit, headquartered in Mumbai with its plant in Kolhapur.[^7] The choice of Kolhapur was not romantic. It was geographically deliberate — the city sits at the edge of the cotton-growing belt of Maharashtra, close enough to the ports of Mumbai and JNPT to ship containers westward, and far enough from Bombay's labour militancy to keep operations clean. The state of Maharashtra was, at the time, offering land at concessional rates to export-oriented units in tier-two cities, partly to push industrial activity out of the over-congested Mumbai metropolitan region and partly to absorb the displaced labour from the dying mill economy.

Jain's instinct was to set up a 100% Export Oriented Unit (EOU) — a regulatory category that, under the prevailing rules, allowed duty-free import of capital equipment and raw materials in exchange for the requirement to export the entirety of finished output.[^7] The EOU classification was, in 1988, one of the few credible ways for an Indian manufacturer to access world-class machinery — without it, even buying a modern Rieter spinning frame from Switzerland was prohibitively expensive. The trade-off was that everything had to be shipped abroad. That constraint, which would have looked like a curse to a domestic-focused entrepreneur, was the founding gift of Indo Count: from day one, the company never had a domestic market to fall back on, never developed the soft habits of a protected manufacturer, and never built a customer base that was not, at some level, ruthlessly competitive on price and quality.

For the first decade and a half of its existence, Indo Count did what every other Indian spinning mill of its era did. It bought raw cotton bales, opened and carded the fibre, drew it into rovings, and spun it into yarn — combed cotton yarn, specifically, the higher-quality variety that goes into shirts, sheets, and the better grades of woven fabric. The yarn was then shipped, mostly to East Asia, where weaving mills in Korea and Taiwan and (later) China would turn it into fabric for someone else's brand. The Indian export earned was almost always a few percentage points lower than the global market price, because Indian yarn carried a faint quality discount in those years — a stigma that the better mills, including Indo Count, slowly worked to erase.

This is what people in the industry call "the commodity trap." A spinning mill, no matter how well run, is a price-taker. Its inputs — raw cotton — move with global commodity cycles. Its outputs — yarn — are priced off the same global benchmarks. The mill has almost no pricing power. When cotton prices fall sharply, you carry inventory written down. When they rise, your customers push back on contracted yarn prices. Margins of two to four percent on revenue are considered a good year. Margins of nothing — or worse — are common. The Indian spinning industry alone has seen multiple generations of family businesses go through cycles of expansion, debt accumulation, restructuring, and quiet absorption into larger groups, all within a quarter-century.

Through the 1990s, ICIL ran this business with operational discipline but no obvious differentiation. It diversified gingerly into knitted fabric, the kind that goes into innerwear and t-shirts, and it kept its export-oriented status, which gave it some duty drawback and tax benefits. By the early 2000s, the company was profitable in the sense that it survived. But it was also a textbook example of what India's policy makers would, a decade later, start calling "trapped capital" — businesses with real assets, real workforces, real customers, and almost no ability to grow earnings faster than the cost of capital. A balance sheet that looked solid on a snapshot basis was running on a treadmill that never quite went anywhere.

There is a quiet lesson in this period that gets lost when people tell the ICIL story in retrospect. The spinning years were not wasted. They taught the Jain family two things that would prove decisive a decade later. First: a global view. Because they sold every kilo of yarn abroad, they learned what an export contract looked like, how letters of credit worked, what an L/C amendment cost when shipment dates slipped, and — crucially — what foreign buyers actually wanted. They learned the language of Incoterms, the rhythm of seasonal demand from Northern Hemisphere buyers, the peculiar way that container availability tightens just before Chinese New Year. Second: cost obsession. When you operate at low single-digit margins, every fraction of a rupee on power, on cotton wastage, on labour per shift becomes existential. That muscle memory of running a tight ship would, later, become a moat — because when ICIL eventually moved into bed linen, it carried into the new business a manufacturing discipline that pure-play home textile entrants did not have.

By 2004, however, the writing on the wall was hard to miss. The Multi-Fibre Arrangement — the global quota system that, since 1974, had artificially protected Indian textile exports by guaranteeing access to Western markets at predetermined volumes — was scheduled to expire on January 1, 2005. China would no longer be quota-constrained. Pakistan would compete head-on. Bangladesh would surge in apparel. Vietnam would emerge as a credible alternative in knitwear. The cosy bilateral world in which an Indian spinner could plan with confidence three years out was about to evaporate. Margins in plain yarn were going to compress, not expand.

If Indo Count was going to be anything other than another mid-sized spinner watching the wave wash over it, the next move had to be different. It had to be up the value chain. And it had to be soon. In one of the more cited internal moments from this period, Anil Kumar Jain reportedly framed the choice for his board in stark terms: either the company moved decisively into a finished-goods product where margins were structurally higher, or it accepted that, over the next decade, it would either be acquired, restructured, or quietly liquidated. There was no third option. The choice that was made — into bed linen — would define everything that came next.

III. The Great Pivot: 2005–2006

If you visit Kolhapur today, the original spinning unit is still there, but it is dwarfed by what was built next to it: a fully integrated bed linen complex with weaving, processing, printing, cut-and-sew, and packaging — the kind of facility that takes a bale of cotton in at one end and delivers a folded, polybagged, retail-ready sheet set out the other. That complex did not exist in 2004. It was, at that point, a gleam in Anil Kumar Jain's eye and a series of arguments at the board table.

The pivot to bed linen, which began in fiscal 2006, is the single most important business decision in the company's history. It is also one of the more interesting case studies of a commodity manufacturer trading up.[^7]7 The question Jain asked, with the kind of clarity that only comes from staring at twenty years of two-percent margins, was this: where in the textile value chain is the gap between input cost and end-customer price the widest, and is that gap defensible?

The answer, after some homework, was bed linen. Specifically, finished bed linen — sheet sets, pillowcases, duvet covers, comforters — sold under retailer private labels into the United States and Europe. Why bed linen and not, say, apparel or curtains or rugs?

Several reasons, which the company has elaborated in investor presentations over the years and which any thoughtful observer can reconstruct. Apparel is fashion. Apparel cycles are short, designs change every season, and inventory risk is borne almost entirely by the manufacturer if it gets the season wrong. If a navy-blue spring collection does not move in March, the discounts come in April, and the chargebacks from the retailer arrive in May. The bullwhip effect in apparel is brutal. Curtains and rugs, by contrast, are sold less frequently — the household replacement cycle stretches to a decade or more, which means market sizing is small relative to the cost of building scale. Towels are towels, but towel-making is dominated by terry-weaving capacity that is hard to add cheaply, and the leading Indian player (Welspun) had already built such a deep position that contesting it head-on was unattractive.

Bed linen sat in the sweet spot. It is replaced roughly every three to five years by a typical American household. It is dictated more by colour and pattern than by silhouette. The "fashion content" is real but moderate — buyers refresh print collections seasonally, but the underlying garment construction does not change. And, perhaps most importantly, the supply chain into US big-box retail was already structured: a handful of large importers were already buying tens of millions of meters of finished sheets every year, mostly from China and Pakistan, and they were always looking for a credible third source to give them sourcing diversification.

The economics looked very different from yarn. A kilo of combed yarn might sell for two dollars at the gate. A kilo of finished bed linen — woven, dyed, printed, finished, and stitched into a retail-ready pack — could sell for fifteen dollars, sometimes more.7 Even after the additional capex, the labour, the waste, the dye chemicals, the energy, the margin profile was structurally different. You were no longer a price-taker. You were, in the language of the industry, a "vendor of record" to a retailer. You had a brief. You had a relationship that had to be earned with samples and audits and on-time shipments, and that, once earned, was sticky in a way that yarn business never was.

The execution choice ICIL made in those early years is, in hindsight, the move that made everything else possible. Rather than build a fully owned, vertically integrated bed-linen complex from day one — which would have required hundreds of crores of capex and probably broken the balance sheet — the company adopted what it later called an "asset-light" model. It put up its own weaving and finishing capacity at scale, but in the early years it also worked with processors and converters on a job-work basis. The intellectual capital — design, sampling, customer relationship, quality control, logistics — stayed in-house. The non-differentiating commodity steps were rented.

This is a more important strategic choice than it might sound. Most Indian textile mills, when they trade up, instinctively build everything. They confuse vertical integration with control. They put up power plants when grid power becomes expensive, they put up captive water treatment when local supply gets unreliable, they put up packaging units when corrugated box prices spike. By the time they are done, the balance sheet looks like an industrial conglomerate and the return on capital looks like one too. ICIL's insight was that, in textiles, the part that the customer pays for is design and reliability — not capacity. Capacity can be procured. A relationship with Walmart's softlines buyer cannot. So Indo Count invested ahead in design studios in Kolhapur and, later, in customer-facing offices in the US, while letting the metal of the supply chain accumulate more gradually.

The numbers tell the rest of this chapter. From a base of around 36 million meters in the late 2000s, capacity scaled to 68 million meters by 2014–15 and roughly 90 million meters by the time the company was getting ready for its next, much larger move.7 The mix shifted decisively: by the mid-2010s, bed linen — not yarn — accounted for the overwhelming majority of revenue, and the customer book had filled out with the names that would later define the franchise: Walmart, Target, Macy's, Bed Bath & Beyond, Costco, JCPenney.3 India, which had been a minor player in US bed-linen imports in 2005, was by 2018 the second-largest source country after China. A meaningful share of that shift was Indo Count's doing.

The 2008 global financial crisis, which broke just as ICIL's bed-linen ramp was hitting its stride, did exactly what one might expect to a heavily export-oriented Indian textile company: it almost killed it. US demand fell, payment terms stretched, working capital exploded, and the rupee — counterintuitively — appreciated in the early months of the crisis before falling back. The company carried significant debt through the late-2000s and had to undergo a corporate debt restructuring in the years that followed. That episode is worth flagging because it explains an enduring trait of ICIL's leadership: an almost institutional caution about debt, a preference for organic capacity builds over leveraged acquisitions, and a long-standing focus on net cash positions. The bed linen company that emerged on the other side of 2010 was the same company strategically but a much more conservative one financially.

By the late 2010s, the question for the company was no longer whether the pivot had worked. The question was who would run it next.

IV. Modern Management & Incentive Structures

Founders, in Indian industrial families, are often described in cinematic terms — the patriarch, the visionary, the man who saw it before anyone else. Anil Kumar Jain, who has spent more than forty-five years in the textile industry, is genuinely all of those things. But the second act of any family business is almost always defined by the next generation, and the second act of Indo Count is, in many ways, defined by Mohit Jain.8

Mohit Jain is the Executive Vice Chairman of ICIL. He studied at Babson College in Massachusetts — the small Wellesley school famous for producing entrepreneurs rather than bankers — and majored in economics, finance, and entrepreneurial studies.8 Babson is an interesting school for a textile heir to have chosen. It is one of the few American business schools that builds its curriculum around the act of starting and running a company rather than around the act of analysing one. The student who graduates from Babson tends to think of business as an exercise in product-market fit and operational throughput rather than as an exercise in financial structuring. That cast of mind is visible in how Mohit Jain has spoken about ICIL across the last decade.

If you watch his television appearances over the years, the through-line is striking. Jain talks about ICIL not as a textile company but as a partner to global retail.[^10] He talks about design pipelines, replenishment cycles, drop schedules, and the importance of being able to swap a print SKU in six weeks rather than six months. He sounds, in other words, more like someone running a private-label home goods business than someone running a 38-year-old Maharashtrian spinning mill. He returned to India with the global lens that his father's generation had developed organically through decades of L/C amendments, and he combined it with something that the senior generation did not always have: an instinctive understanding of how American retailers actually buy, of the choreography between a category manager and an open-to-buy budget, of the politics of vendor scorecards.

The other half of the executive duo is Kailash Lalpuria, Executive Director and CEO, who has been with Indo Count since October 2010 and has more than thirty-five years of textile experience.9 Lalpuria is the operator — the one who runs the plants, the export pipeline, the customer servicing engine. He had spent the bulk of his career before joining ICIL in senior commercial roles at other large textile groups, which means he came in with established relationships across the US retail buyer community. The textbook division of labour between a strategic vice-chairman and a hands-on CEO is rare in Indian promoter-run firms, where the founder typically keeps both functions and the next generation either inherits both or none. At ICIL, the division has functioned with the kind of stability that, in family businesses, is often the difference between scaling and stagnating.

The professionalisation of the management layer is mirrored in the cap table. As of the most recent disclosed shareholding pattern, promoters owned 58.74% of the company, split between foreign promoter entities at 33.95% and Indian promoters at 24.78%.10 This is a controlling stake but not an absolute one. The remaining 41% is widely held — domestic mutual funds, foreign portfolio investors, retail. The company is, in every sense, an institutional-grade name on the Indian small-and-mid-cap circuit, with active sell-side coverage and a long history of investor relations material that is, by Indian textile-industry standards, unusually disclosed.11

The skin-in-the-game story is important for a particular reason. In commodity-adjacent businesses with long capex cycles, the temptation to "diworsify" — to use cash flow from the core business to buy adjacent but unrelated assets — is almost a law of nature. Indian textile companies have, historically, been some of the worst offenders. They have bought power plants, hotels, retail chains, real estate, even, in one infamous case, a feed-corn business. The temptation is obvious: a textile business in good years throws off more cash than it can sensibly reinvest, the promoter family looks for a place to put it, and the next thing you know there is a Mediterranean restaurant chain on the consolidated balance sheet. ICIL has, over the same period, stayed remarkably narrow: bed linen, more bed linen, and adjacencies that look like bed linen (utility bedding, branded bedding, hospitality linen). The promoter holding is large enough that the family carries most of the consequence of capital decisions. That alignment shows up in the boring details — the auditor reports, the related-party disclosures, the absence of strange off-balance-sheet vehicles, the relatively short list of subsidiaries.

Two other elements of the modern management story deserve mention. The first is the ESG posture. American retailers are, increasingly, not allowed to be cavalier about where their cotton comes from — the Uyghur Forced Labor Prevention Act in the US has, since 2022, materially raised the cost of compliance for cotton sourced from Xinjiang.[^14] Major US retailers have, as a result, been quietly de-risking their supplier base toward countries where the cotton provenance question is cleaner. ICIL has leaned hard into being an alternative: it sources cotton predominantly from Indian and US growers, has invested in third-party sustainability certifications including OEKO-TEX and BCI (Better Cotton Initiative), and has built the kind of traceability documentation that lets a Target compliance officer sleep at night. In a world where the upstream cotton question has become a board-level issue for US retailers, that posture is worth quiet money.

The second is the increasingly explicit "Complete Comfort" positioning — the idea that ICIL is not selling a sheet but a sleep experience. That sounds like marketing fluff, and on a given Tuesday it probably is. But strategically, it is the language that gives the company permission to extend into adjacencies — utility bedding, mattress protectors, fashion bedding, hospitality. It is the difference between being a sheet vendor and being a category partner. When a retailer is allocating shelf space for the entire bedding category and looking for a single supplier who can fulfil sheets, comforters, mattress pads, and pillows under one container, the manufacturer who has positioned itself as a "complete comfort" partner is the one who wins the category review. That, in turn, is the strategic logic behind Fluvitex USA, Modern Home, and the broader US-side adjacency build that we will come to shortly.

It is also worth noting the more pedestrian governance signals that come with a company of this profile. ICIL's audited accounts have been clean across multiple cycles. Its disclosure schedule is on the more rigorous end of Indian small-mid cap. Its credit ratings have been investment-grade and stable across the most recent cycle, with CARE Ratings continuing to affirm its rating profile in the most recent annual review.20 None of these are exciting signals individually. But for a manufacturing business with international working capital cycles, the cumulative effect is meaningful. The cost of capital advantage is real, even if invisible.

Which brings us to how the company moved from organic growth to acquisitions — and how the financial discipline of the post-2010 years gave it the balance-sheet room to make a transformative bet when the opportunity finally arrived.

V. M&A: The GHCL Acquisition & Wamsutta

By 2021, Indo Count had reached the limit of what organic capacity expansion could comfortably do. The Kolhapur complex had been pushed close to its operating ceiling. Adding more weaving lines, processing capacity, and stitching capability on the same site would have taken eighteen to twenty-four months at best, and incremental capacity at that pace was not going to be enough to absorb what was, by then, a once-in-a-generation demand shift. The global tailwind — the post-pandemic surge in home textile demand, the China-plus-one sourcing shift, the slow-motion bankruptcy of Bed Bath & Beyond's supplier base, the realisation by every US retailer that single-country sourcing was a strategic risk — was happening now. Capacity that arrived in 2024 would miss the window. Capacity that arrived in 2022 could capture it.

On December 6, 2021, ICIL announced a deal that would change the shape of the company. It agreed to acquire the Home Textile Business of GHCL Limited — a Delhi-based listed company best known for soda ash but with a substantial home textile arm based in Vapi, Gujarat — for an aggregate consideration of approximately ₹596 crore, including the identified assets of GHCL's US subsidiary, Grace Home Fashions.[^15]12 The pure home textile business in India was valued at ₹539 crore on a debt-and-cash-free basis (₹340 crore fixed plus ₹199 crore towards net current assets), with an additional roughly ₹20 crore expected from the Grace Home Fashions piece.12

The numbers behind the deal are interesting once you sit with them. GHCL's home textile business had reported revenue of around ₹435 crore in the most recent full year before the announcement.12 The headline price of around ₹596 crore therefore valued the asset at roughly 1.4x sales — but a meaningful chunk of that was working capital, which meant the enterprise-value-to-sales on the operating business itself was closer to 0.8x. By the standards of the global home textile space — where Welspun India and Himatsingka Seide traded at considerably higher revenue multiples at the time — this was a deeply attractive entry. The reason was straightforward: GHCL had been a perennially under-invested home textiles business inside a conglomerate that was, increasingly, focused on its chemicals franchise. Bed linen was a stepchild. The parent did not have the strategic patience to keep funding capex in a business that did not move the needle for its overall profile. For ICIL, that same business was the main event.

The acquisition completed in April 2022.13 In one stroke, ICIL roughly doubled its installed capacity, picking up an additional ~45 million meters of bed-linen capacity at Vapi, an entirely new customer book that overlapped only partly with its own, and a US distribution arm that gave it direct presence on American soil.1314 The post-deal capacity footprint of around 153 million meters made ICIL the largest dedicated bed-linen company in the world by capacity.2 In a global market for woven home textiles where China is still the volume leader in aggregate, India had quietly produced a single-product champion that was bigger than any single Chinese factory complex.

The integration of the GHCL business — and this is the part that is easy to skim past in a press release — was not trivial. Two different manufacturing systems, two different cost structures, two overlapping customer books, two sets of compliance regimes. The Vapi plant ran a different product mix from Kolhapur, with a different print finishing process and a different stitching configuration. Cross-pollinating customer accounts (taking a Walmart program from Kolhapur and offering capacity to a Macy's program at Vapi) required commercial agreements that did not exist on day one. The first eighteen months after closing were spent in operational consolidation work that does not show up in any quarterly print but that determines whether an acquisition compounds or stagnates. By FY24, the integrated business was running close to combined capacity utilisation in the 80%-plus range, which is the operational signal that the deal had landed cleanly.

But the more interesting move, strategically, came two years later. On April 18, 2024, through its US subsidiary Indo Count Global Inc. — a Delaware-incorporated entity established for exactly this kind of transaction — the company acquired the WAMSUTTA brand and related intellectual property from Beyond, Inc. — the successor company to the bankrupt Bed Bath & Beyond — for $10.25 million.45

To understand why this matters, you need to understand what Wamsutta is. The brand traces its origins to 1846 in Massachusetts, when the Wamsutta Steam Mills were established to weave fine cotton goods — making it one of the oldest continuously used home-textile brand names in the United States.4 For the better part of the twentieth century, "Wamsutta sheets" was American consumer shorthand for premium percale. The brand had been folded under Springs Industries, then divisional, then eventually licensed and warehoused by Bed Bath & Beyond when it was at its retail peak. When Bed Bath & Beyond filed for Chapter 11 in 2023, its IP was carved up. Wamsutta sat as an asset, waiting for a buyer who knew what to do with it.

ICIL knew exactly what to do with it. For an Indian manufacturer that had spent two decades quietly producing sheets that landed on US shelves under someone else's name, owning a 178-year-old premium American home-textile brand was less a vanity purchase than a structural upgrade. It gave ICIL, for the first time, the right to sell into the US at a brand margin rather than a vendor margin. Wamsutta could be deployed onto Amazon, Wayfair, Macy's, and selectively into off-price channels, with ICIL capturing both the manufacturing margin (which it always had) and the brand margin (which it had always given away). At a price of $10.25 million — less than a single quarter of the company's EBITDA in a normal year — this was, in capital allocation terms, the cheapest brand in modern American retail.

There is a more interesting capital allocation lesson hiding in the Wamsutta number than the price. A 178-year-old US home textile brand with documented consumer recognition was effectively trading at fire-sale prices because the asset was, for the bankruptcy estate, illiquid. Brands without an operating business attached are very hard to monetise. The Beyond Inc. estate wanted to convert IP into cash. ICIL was, perhaps, the only buyer in the world who could deploy Wamsutta immediately onto an existing supply chain at scale. That asymmetry of strategic fit — common buyer, idiosyncratic value — is exactly the situation in which M&A creates the most value, and the fact that ICIL had the discipline, the cash, and the operating engine to act on it within a year of the Bed Bath & Beyond bankruptcy filing is a testament to the company's deal readiness.

What is interesting about the two deals taken together is the philosophical evolution they reveal. ICIL spent the 2005–2020 period evangelising the "asset-light" model — keep design and customer ownership in-house, rent the metal. By the early 2020s, it was openly using the phrase "asset-right" to describe its posture: owning the metal when it gave it cost and reliability advantages, owning the brand when it gave it margin, and outsourcing the rest. The GHCL deal was an asset-heavy bet; the Wamsutta deal was an asset-brand bet. Both were, in different ways, attempts to capture more of the value chain. Neither was the kind of empire-building acquisition that a less disciplined promoter would have done; both passed the basic test of whether the asset was strategically additive at a price that left a meaningful margin of safety.

The acquired engine, however, is only half the story. The other half is what ICIL has been quietly building inside India.

VI. Hidden Gems: The "Next" Indo Count

If you ask any retail visitor to a Bengaluru or Pune or Hyderabad upper-middle-class neighbourhood about Indian home textile brands, the names that surface — Bombay Dyeing, D'Décor, Welspun's Spaces — have been around for decades. Boutique Living, ICIL's domestic flagship, is one of the newer entrants, but it is doing something the older brands largely did not: building a directly Indo-Count-controlled premium bed linen line for the Indian market rather than licensing the brand to a department store.15

Boutique Living sits at a deliberate price point — typically ₹2,000 to ₹4,000 per sheet set — that targets aspirational urban households who have stopped buying mill-gate sheets at neighbourhood textile stores and have not yet jumped to imported European brands.15 The brand sells through company-operated outlets, larger format retailers, and increasingly through D2C channels on Amazon India and Flipkart. The product line has progressively expanded from the original sheet sets into duvets, comforters, decorative pillows, and a "Pure Earth" sustainable line that targets environmentally conscious consumers. ICIL has not disclosed precise revenue numbers for Boutique Living independently — but management commentary across earnings calls suggests the domestic branded business has grown at a 20%-plus annual rate from a small base.[^20]

In the context of overall ICIL revenue, domestic still accounts for less than 10% of the business — roughly 90% of revenue continues to come from exports.16 But the strategic significance of the domestic piece is out of proportion to its size. Domestic branded business carries margins that are structurally higher than private-label export business, because the company keeps the entire retail margin stack rather than handing it to Walmart. As Indian household formation accelerates, as the urban consumer trades up, and as e-commerce removes the distribution disadvantage that mid-sized brands always faced versus department stores, the domestic line item should — in theory — grow at a multiple of GDP for the next decade.

There is a slightly contrarian sub-thesis here that is worth airing. The Indian premium home textile market has historically been described as small, fragmented, and price-sensitive. That description was accurate ten years ago. It is increasingly inaccurate now. The Indian household at the top quintile of income has been consolidating spending toward branded categories with a velocity that retail data does not yet fully capture, and the bed linen category — perhaps because it sits at the intersection of "personal" and "aspirational" — is one of the under-penetrated targets of that shift. Whether Boutique Living captures that move or watches it be captured by an international entrant (a Brooklinen, a Parachute, a Casper at scale) is one of the open questions for the next five years.

The second hidden area is the US-side adjacency build. Through subsidiaries Fluvitex USA and Modern Home, ICIL has been pushing into the utility bedding category — comforters, pillows, mattress pads — which sits adjacent to its core sheet competence but addresses a category that turns over more frequently than top-of-bed.17 Utility bedding is interesting because the unit economics are different — it is less about high thread count and complex prints and more about fill quality, stitching reliability, and packaging. Margins per unit are lower; volume per household is higher. As of the most recent disclosures, the utility bedding subsidiaries were operating at roughly 50% capacity utilisation, which is both a statement of current under-utilisation and a measure of the operating leverage that could come if volumes ramp.17

The third quiet growth lever is the technical and value-added end of the bed linen market. This is the side of the business that nobody markets in a glossy investor deck but that quietly contributes to ASP — anti-microbial finishes, thermal-regulating treatments, hypoallergenic constructions, hospitality and institutional linen for hotels and hospitals. Each of these sub-categories is its own micro-market with its own buying logic, but they share the feature that the product carries a functional claim, which the customer pays a premium for. Anti-microbial treatments became a mainstream consumer ask in the post-COVID world; thermal-regulating sheets followed a wave of consumer interest in sleep optimisation; hypoallergenic constructions cater to the steady upward trend in allergy-aware households.

The institutional channel in particular — five-star hotel chains, premium hospitals, large corporate guest houses — is a sticky, contract-driven business that carries lower volatility than retail and that benefits enormously from the fact that ICIL is one of the few Indian players with the certifications and the scale to bid on multi-year supply contracts. A Marriott or an IHG, when standardising linen procurement across a national or regional footprint, runs an extensive vendor qualification process; once a supplier is in, the business is multi-year, the volumes are predictable, and the working capital cycle is shorter than retail.

Pulling these threads together, the structural story of "next" ICIL is the story of mix change. Today, the revenue base is heavily skewed to private-label US exports, which is a wonderful business when the US consumer is buying, a difficult one when she isn't. The bull case for the next decade is that the mix will progressively diversify — branded export (Wamsutta) into one bucket, branded domestic (Boutique Living) into another, utility bedding into a third, institutional into a fourth. Each of those carries either margin advantages or volatility advantages over the base business. None of them needs to be a home run individually. The compounding effect of even modest growth in each is what would shift the company's earnings profile from cyclical-exporter to diversified-home-textile-platform.

There is also a meta-thesis hiding in the segment data that does not get enough airtime. ICIL is, today, almost certainly under-monetising its manufacturing footprint. A 153-million-meter capacity base, if run at full utilisation on a higher-mix product profile, would generate materially higher EBITDA per meter than the current blend. The capacity exists. The customer relationships exist. What needs to happen is the gradual rotation of the order book toward higher-value SKUs and the gradual ramp of the branded businesses to absorb capacity that would otherwise sit idle in soft demand quarters. The Q4 FY25 print, in which volume dipped and ASP compressed simultaneously, was a reminder that this rotation has not yet structurally completed.19

This sets up the broader competitive question. If ICIL is doing all of this, why don't the competitors do the same — and what is actually defensible about its position?

VII. Strategic Analysis: 7 Powers & Porter's 5 Forces

Hamilton Helmer's 7 Powers framework asks a deceptively simple question for any business: what is the persistent differential that lets you earn returns above the cost of capital? For a textile company — and especially a globally export-led one — most of the seven powers are unavailable. There is no network effect on a bed sheet. There are no meaningful switching costs for a Walmart buyer who decides to dual-source, because the cost of bringing in a second vendor is small relative to the program. Brand power exists, but for the most part the brand belongs to the retailer, not the manufacturer. Process power, in the Toyota sense, is real but slow to compound in commodity textiles. So what is left?

Three of the seven, in particular, are worth examining carefully for ICIL.

Scale economies. This is the most obvious one. At 153 million meters of capacity, ICIL is the largest single-name bed-linen specialist in the world.2 Scale shows up in less obvious places than the manufacturing line. It shows up in container logistics — ICIL is large enough that it can fill multiple ocean containers a week to single retailers, which gets it preferential freight rates and lane stability, especially valuable through the Red Sea disruption and the subsequent rerouting around the Cape of Good Hope. It shows up in cotton procurement — being the largest single buyer of certain Maharashtra cotton grades gives it bargaining leverage against ginners that smaller mills do not have. It shows up in design pipelines — the company can afford to staff a design studio that produces tens of thousands of SKU concepts annually, which a smaller competitor cannot match. The scale moat is real, but it is also bounded; Welspun is bigger overall (though more diversified), and a determined entrant could, with enough capital, reach a comparable size in a five-to-seven-year window.

Counter-positioning. This is where the ICIL story is more interesting. Counter-positioning, in Helmer's framework, is when a smaller competitor adopts a business model that the larger incumbent cannot copy without cannibalising itself. The textbook example is Vanguard versus Fidelity. The ICIL version: by focusing exclusively on bed linen, ICIL forces every diversified competitor — Welspun (towels + bath + flooring), Himatsingka (drapery + licensed brands like Tommy Hilfiger and Calvin Klein), Trident (towels + paper), Bombay Dyeing (everything from polyester to denim to real estate) — to allocate management attention and capital across multiple categories. In a category where being the partner that a US retailer can call at 11 p.m. with a flash demand shift matters, single-category focus is a real advantage. None of the diversified Indian incumbents can replicate that without unwinding businesses they own for other reasons. The ICIL bed linen platform is, in effect, the only one in India that does nothing else.

Cornered resource. This one is partial. India is the world's largest cotton producer, and Maharashtra and Gujarat — the two states where ICIL's plants sit — are among the most productive cotton-growing belts globally. That is a geographic advantage but not strictly a cornered one, because the same cotton is available to every Indian competitor. The cornered resource argument is more about cumulative customer relationships: a multi-year audited supplier relationship with Walmart, Target, and Costco is not something that can be replicated quickly even with the right capacity. Compliance pipelines, vendor scorecards, and chargeback history accumulate slowly. New entrants spend years getting onto approved-vendor lists before they ship a single container. ICIL has been on those lists for over a decade in most cases.

The other four powers — branding, network effects, process power, switching costs — are present in faint form, but none of them is the load-bearing wall of the moat. Branding is something ICIL is actively buying with Wamsutta; until that brand is built into a material revenue line, it remains potential rather than realised. Network effects do not exist in this product. Process power is a slow grinder rather than a step change. Switching costs are minimal for retailers, although the implicit cost of vendor onboarding and audit creates a small friction that benefits incumbents.

Turning to Porter's 5 Forces, the most interesting story is on the buyer side. Bargaining power of buyers in this industry is structurally high — Walmart, Target, and Costco are oligopsonists in US home textile retail, and they squeeze suppliers ruthlessly. Indo Count's defence is not pricing power but rather what one might call the design + reliability halo: by being the supplier that the buyer trusts to deliver a complex print run on time, with full traceability and zero compliance flags, ICIL has earned a small but meaningful margin over rotational vendors. It is not a quoted premium; it is a who-gets-the-call premium. Over time, that premium compounds into share.

Bargaining power of suppliers is moderate. Cotton growers and ginners in India are highly fragmented; no single supplier has bargaining power against a large mill. But Indian cotton policy — Minimum Support Prices, occasional export restrictions, government procurement through the Cotton Corporation of India — introduces a kind of government-as-supplier dynamic that can be opaque and occasionally disruptive. In years where the MSP is set materially above international prices, Indian mills are forced to buy domestic cotton at a structural disadvantage to global peers in Vietnam or Egypt.

Threat of new entrants is moderate. The capital cost of building a 50-million-meter bed linen complex from scratch is north of ₹1,500 crore today, and the lead time to recoup is long. But it is not infinite — and Vietnam, Bangladesh, and Egypt are all credible alternatives that have been growing share, even if slowly. New Indian entrants are limited; the consolidation that took place during the COVID years left fewer mid-sized players with the appetite to scale up.

Threat of substitutes is genuinely low. No one has yet invented a credible non-textile alternative to a cotton sheet. There is incremental substitution within the textile category — bamboo viscose, microfiber, lyocell — but these remain niche products in the US bed linen market, and ICIL itself has the capacity to participate in those mixes if and when they scale.

Rivalry, the fifth force, is the one that has shifted most decisively in ICIL's favour over the past five years. The single biggest shift in global home textile sourcing has been 中国加一 China-plus-one — the explicit policy by US retailers to dual-source out of China to manage geopolitical and tariff risk. Combined with Pakistan's domestic economic difficulties (high inflation, currency volatility, energy supply issues), which have hobbled its largest home textile exporters, India has been the primary structural beneficiary of this shift.[^14]18 ICIL has, in a very real sense, been positioned at the receiving end of two macro tailwinds simultaneously — and has compounded that with its own operational execution.

A second-layer diligence aside on competition: among Indian peers, the comparison set is small but important. Welspun India is bigger overall but has roughly half its revenue in towels and bath; Himatsingka Seide carries licensed brand rights for premium fashion bedding (Tommy Hilfiger, Calvin Klein, Bellora) and has historically operated with higher leverage; Trident is primarily a paper-and-towel story with a meaningful but secondary home textile presence; Sutlej Textiles, Vardhman, and others operate in adjacent yarn and fabric verticals. The closest like-for-like competitor is, in some ways, GHCL itself before its home textile arm was sold to ICIL. With that competitor effectively absorbed, ICIL has been operating in an environment of consolidated rather than fragmented competition.

This setup — strong tailwinds, real but bounded competitive moat, exposure to a single end-market (US retail), commodity input risk — is the perfect frame for the bull/bear discussion that any long-term investor must run.

VIII. The Playbook & Bear/Bull Case

Myth vs Reality

Before the bull and bear cases, a quick fact-check on the consensus narratives around this business — the kind of stories that get repeated on financial television and that, on close inspection, are partly right and partly wrong.

Myth: "Indo Count is a beneficiary of a one-time bedding boom from US pandemic stimulus." Reality: The company's volume growth has continued past the post-pandemic normalisation. FY25 sales volume of 106.4 million meters was up 9.8% year-on-year — well past the post-COVID cliff — even as US discretionary spending softened.19 The volume growth is the cleanest tell that the China-plus-one share gain is structural rather than cyclical, because in a pure cyclical episode the volume line would have already rolled over.

Myth: "It's a private-label commodity manufacturer with no pricing power." Reality: Average selling price compressed in FY25 by roughly 6% in Q4 due to mix shift toward lower-priced offerings — but the deliberate move into branded (Wamsutta) and utility bedding is explicitly a play to take ASP and margin back over time.19 The pricing power question is therefore not a static one. The current snapshot is a low point; the structural mix shift is the path off of it.

Myth: "Cotton volatility makes the earnings stream unforecastable." Reality: Cotton volatility absolutely creates quarterly noise, but the company's full-year EBITDA margin has remained range-bound between roughly 13% and 17% across multiple cotton cycles — meaning the operational business absorbs the volatility better than peers.1920 The full-year frame is the right one; quarterly snapshots can be misleading.

Myth: "Wamsutta is a vanity purchase that will not move the needle." Reality: The acquisition cost of $10.25 million is small.5 But the deployment opportunity — premium branded sheets on Amazon, Wayfair, Macy's, and selectively in off-price — has structural margin potential that, even at modest revenue contribution, could meaningfully shift the consolidated mix. The question is execution, not strategic fit.

The Bull Case

The bull case for ICIL rests on three pillars. The first is market share. India's share of US home textile imports has been rising secularly, and within India, ICIL has been a disproportionate gainer thanks to its single-category focus. Even modest further share gains, on a base that already represents roughly 20% of US bed linen imports from India, translate into meaningful absolute volume.[^14]18 The runway from China-plus-one is unlikely to close in the next five years; if anything, the political appetite in the US for diversifying away from Chinese sourcing has intensified, not eased.

The second is margin expansion from mix. The Wamsutta deal, the Boutique Living domestic brand, the utility bedding push, and the institutional channel each carry margin profiles structurally above private-label export. As mix shifts, even modestly, EBITDA margin should drift upward over a multi-year window. Management has guided to a return to historical margin bands as branded mix grows.19 The mix shift does not need to be dramatic; even a 200-basis-point improvement on a 13-14% base is a meaningful absolute earnings move.

The third is capital allocation discipline. The promoter family controls 58.74% of the equity, the M&A track record (GHCL at a structurally cheap multiple, Wamsutta at a comically cheap multiple) is strong, and the absence of "diworsification" into unrelated sectors is itself a positive. Few Indian textile names can claim the same.10124 Capital that comes off the operating business is reinvested into the operating business; cash flows that exceed reinvestment needs are returned through dividends rather than vanity acquisitions.

There is a fourth, more subtle pillar that deserves a sentence: the manufacturing chassis. A 153-million-meter bed linen capacity base, geographically split between Kolhapur and Vapi, is a strategic asset that cannot be replicated in under five years even with full capital availability. As global retail continues to consolidate its supplier base toward fewer, larger, more reliable vendors, the structural advantage of being one of those vendors becomes self-reinforcing.

The Bear Case

The bear case is equally crisp. First, end-market concentration risk. Roughly 90% of revenue comes from exports, and a large share of that lands in US retail. A US consumer recession, or a sharp tariff event on Indian textile imports, would hit revenue in a non-linear way. The Q4 FY25 print — revenue down 5.9%, EBITDA down 47% — was an early reminder that this business is operationally levered to US consumer demand.19 The non-linearity matters: a 6% volume decline became a 47% EBITDA decline because operating leverage runs both ways.

Second, cotton price volatility. Indian cotton prices have been more volatile than global cotton in recent years thanks to domestic policy interventions, weather variability, and MSP-related distortions.20 In any given quarter, raw material can swing 15–20%, and that runs through the P&L. The company hedges and contracts where it can, but a sustained spike in cotton prices that cannot be passed through to retailers compresses margin for two to three quarters at a stretch.

Third, shipping and logistics. The Red Sea crisis of 2024–25 — Houthi attacks on commercial shipping forcing rerouting around the Cape of Good Hope — added weeks of transit time and meaningful freight cost for Indian exporters. Any prolonged disruption of the Suez or Cape route disproportionately hurts an exporter whose end market is on the wrong side of the Indian Ocean. The structural shift in shipping cost from the COVID era never fully reverted, and a fresh disruption could re-impair margins quickly.

Fourth, brand execution risk on Wamsutta. The math on the acquisition is brilliant. The execution — building a brand-led D2C and wholesale presence in the US from an Indian manufacturer's organisation — is harder than the math, and historically Indian companies have under-delivered on US brand bets. Building a brand requires a different muscle set than running a private-label factory: marketing spend cadence, retail channel management, e-commerce media buying, customer service infrastructure. The risk is not that Wamsutta destroys value; the risk is that it underperforms its potential while consuming management attention.

Fifth, the tariff scenario. US trade policy has become structurally less predictable in 2024 and 2025. While the China-plus-one tailwind has been a positive, the same dynamic could reverse direction in a single executive order if the US administration decides to impose broad tariffs on Indian textile imports. The legal framework exists; the political will is variable. This is a tail risk rather than a base case, but it is not zero.

KPIs to Track

For a long-term investor following ICIL, three operational metrics are worth keeping a quiet running track of, and they tell you most of what you need to know about whether the bull case is playing out:

1. Volume in million meters per quarter and full year. This is the cleanest single read on demand. Revenue can swing with ASP and mix; volume tells you whether the underlying franchise is gaining or losing share. The FY25 print of 106.4 million meters is the base from which to watch the next several years.19 Sustained growth above the global home-textile-trade growth rate is the share-gain signal.

2. Share of branded + value-added revenue in total revenue. This is the proxy for the mix-shift thesis. Today it is in single digits; the inflection — if it comes — will show up here first. The Wamsutta deployment ramp, the Boutique Living domestic growth, and the utility bedding US subsidiary utilisation are the three sub-components that aggregate into this metric. Management discloses these to varying degrees on calls; the trajectory matters more than any single point.

3. EBITDA margin (consolidated, full-year basis). This is where the cotton cycle, the mix shift, and the operational leverage all settle. The historical band has been 13%–17%; sustained margin above the upper end would suggest the structural story is working. Sustained margin below the lower end would suggest that either cotton has become structurally adverse or that operating leverage from utility bedding and other US adjacencies is failing to materialise.

Closing Reflection

At the start of this episode we asked whether ICIL was a textile company or, in some sense, a supply-chain-as-a-service operation for global retail. The honest answer, after walking through the story, is that it has been both at different points in its history, and that the most interesting decade ahead may be the one in which it tries to be neither — to become, in the slow Indian way, a category brand with a manufacturing backbone rather than the other way around. The Wamsutta deal, the Boutique Living push, the utility bedding subsidiaries, the institutional channel: these are not separate bets. They are, in aggregate, a single bet that the next phase of Indo Count is about earning a brand margin on a manufacturing chassis.

Whether that bet pays off is the story of the next ten years. The first thirty-eight years suggest it is at least worth watching, very quietly, from the spinning floor in कोल्हापुर to the boutique aisle in बेंगलुरु and, perhaps, to a Bed Bath replacement store somewhere off an Interstate in Ohio with a Wamsutta sheet set on the endcap that nobody knows was made in India.

The deeper lesson, if there is one, is about the patience of Indian manufacturing. The instinct in modern markets is to think in two- and three-year horizons — what is the next quarter, what is the next product launch, what is the next deal. The ICIL story is not legible in those horizons. It is legible only in decades. The pivot from yarn to bed linen took five years to plan and ten years to consolidate. The GHCL acquisition was the result of a balance sheet repair effort that began after the 2008 crisis and concluded with the cash position that made the 2021 deal possible. The Wamsutta brand purchase was the culmination of a brand-strategy conversation that had been on the board agenda for at least half a decade before the Bed Bath & Beyond bankruptcy made the asset available.

In an industry obsessed with the quarterly cotton tick and the latest shipping rate, holding that long-horizon orientation is itself a competitive advantage. Whether the next chapter of Indo Count writes itself into the global category-brand pantheon, or remains the quiet manufacturing chassis behind other people's labels, is going to be answered slowly, in the cadence that this company has always preferred: one container at a time, one design cycle at a time, one shelf endcap at a time, in cities where the people sleeping under the sheets have never heard the name and probably never will.

References

References

-

Indo Count Industries Limited corporate profile — Indo Count ↩

-

Indo Count emerging global leader in home textiles — The Textile Magazine ↩↩↩

-

Indo Count Industries Limited (ICIL) stock business overview — Bitget ↩↩

-

Indo Count Acquires US Premium National Brand WAMSUTTA — BusinessWire, 2024-04-19 ↩↩↩↩

-

Indo Count Industries Ltd. acquires Wamsutta brand from Beyond, Inc. for $10.25 Million — In Fashion Business, 2024-04 ↩↩↩

-

This father-son duo built their cotton yarn spinning unit into a global bed linen powerhouse — YourStory ↩

-

After exporting bed linen for almost three decades, Anil Jain of Indo Count is now creating his own brands — Business Today, 2016-12-12 ↩↩↩

-

Kailash R. Lalpuria - Executive Director & CEO at Indo Count — The Org ↩

-

Indo Count buys GHCL's home textiles business, IP, inventory for Rs 576 cr — Business Standard, 2021-12-06 ↩↩↩↩

-

Indo Count soars 10% on completing acquisition of home textile biz of GHCL — Business Standard, 2022-04-04 ↩↩

-

Indo Count wraps up multi-million-dollar deal — Home Textiles Today ↩

-

Indo Count Industries Q4 FY25 Earnings Call Highlights — Yahoo Finance, 2025 ↩↩

-

China, India, Pakistan Dominate U.S. Home Textiles Imports — WWD/Sourcing Journal ↩↩

-

Indo Count Industries Q4 & FY25 Earnings Call Transcript — Indo Count, 2025-06-02 ↩↩↩↩↩↩↩

-

Corporate Rating Report: Indo Count Industries Limited — CARE Ratings, 2025-09 ↩↩↩

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube