ICICI Prudential Life Insurance: India's Insurance Pioneer Goes Public

I. Introduction & Episode Thesis

The Mumbai stock exchange floor erupted in applause on September 29, 2016. For the first time in Indian capital markets history, a life insurance company had gone public. ICICI Prudential Life Insurance, born from the ashes of a government monopoly just 16 years earlier, was now worth ₹48,000 crores at listing—a valuation that would nearly double to ₹90,000 crores within eight years.

But this wasn't just another IPO story. This was the culmination of India's great financial liberalization experiment, a testament to what happens when global expertise meets local distribution muscle, and proof that in a country of 1.4 billion people, selling promises about the future could build one of the most valuable franchises in financial services.

The central question that drives this narrative: How did a post-liberalization joint venture, starting from literally zero customers in December 2000, become India's first listed life insurer and create more value than most of the country's established industrial conglomerates?

ICICI Prudential Life's journey began in fiscal year 2001, when insurance in India meant one thing: Life Insurance Corporation (LIC), the state-owned behemoth that had monopolized the sector since 1956. Today, the company manages over ₹3.2 trillion in assets, serves millions of customers across 2,500 branches, and has maintained a perfect track record—zero non-performing assets across 21 years of market cycles.

This is a story about timing, about recognizing when regulatory walls are about to fall. It's about the power of distribution in a trust-based business. And ultimately, it's about how two unlikely partners—a transformed development bank and a British insurer with century-old Asian ambitions—created something neither could have built alone.

So what for investors: The ICICI Prudential story offers a masterclass in identifying and capitalizing on regulatory discontinuities. When governments deregulate monopolies, the first movers who combine local trust with global expertise often capture disproportionate value—a playbook worth studying as India continues liberalizing sectors from healthcare to education.

II. The Pre-History: Insurance in India & Liberalization

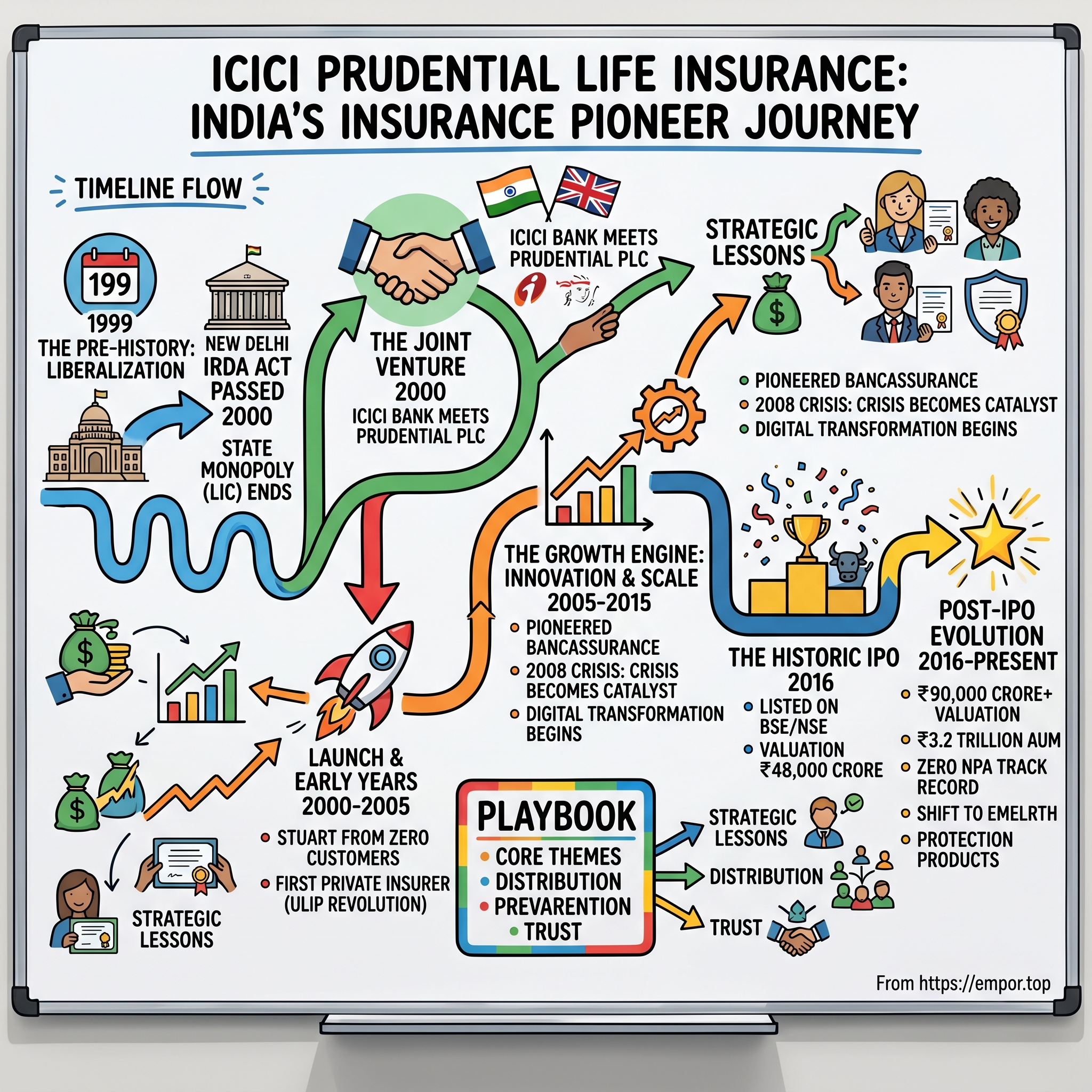

Picture India in 1999: Y2K fears grip global markets, the Kargil conflict dominates headlines, and in the corridors of North Block in New Delhi, bureaucrats are drafting legislation that would end a 43-year-old monopoly. The Insurance Regulatory and Development Authority (IRDA) Act was about to transform how Indians thought about death, savings, and financial security.

To understand the magnitude of this shift, you need to grasp what insurance meant in pre-liberalization India. Since 1956, when the government nationalized 245 insurance companies into Life Insurance Corporation, buying life insurance was like visiting a government ration shop—long queues, limited products, take-it-or-leave-it service. LIC's agents, often retired government employees, sold policies like postal savings schemes. Innovation meant changing the font on policy documents.

The monopoly wasn't just administrative; it was philosophical. Insurance was seen as a social obligation, not a financial product. LIC channeled policyholder funds into government securities and public sector enterprises. Returns were an afterthought. Customer service was an oxymoron. Yet Indians saved through LIC because there was literally no alternative. The transformation began with the Malhotra Committee, set up in 1993 under RN Malhotra, former Governor of RBI, to propose recommendations for reforms in the insurance sector. The committee's 1994 report was revolutionary: it recommended that the private sector be permitted to enter the insurance industry. For an economy still recovering from the 1991 balance of payments crisis, this was audacious.

The IRDA Bill was passed in December 1999 and became an Act in April 2000. The speed of implementation was breathtaking: in July 2000, immediately after the first meeting of the Insurance Advisory committee, 11 essential regulations were notified, and by October 2000, six licenses to new players in the life and non-life sectors were issued.

But why did liberalization matter so fundamentally? In a nation where less than 20% of the population had any form of life insurance, the potential was staggering. The middle class was growing, nuclear families were replacing joint family systems, and financial literacy was slowly improving. Yet the insurance products available were archaic—endowment policies that mixed insurance with low-return savings, sold by agents who barely understood what they were selling.

Enter Prudential Corporation Asia, a company with a fascinating backstory. Prudential Corporation Asia had a presence in the continent since 1923 when an overseas agency for life assurance was created in India. After independence and nationalization forced them out, they'd spent decades planning their return. When the doors finally opened in 2000, Prudential wasn't just ready—they'd been preparing for this moment for 77 years.

The regulatory framework that emerged was carefully calibrated. Foreign companies were allowed ownership of up to 26%—enough to ensure technology and expertise transfer, but not enough to dominate. This wasn't just market opening; it was controlled liberalization, designed to create Indian champions with global capabilities.

Myth vs Reality Box: Myth: Insurance liberalization was primarily about bringing foreign capital into India. Reality: The capital requirements were modest. The real import was expertise—in product design, actuarial science, risk management, and customer service. The 26% foreign ownership cap ensured knowledge transfer while maintaining Indian control.

The stage was set for a transformation. As one IRDAI official noted: "I do not think there is any other sector in this country where the transition from state monopoly to free market has been as hassle free as the insurance sector". This smooth transition would prove crucial for what came next—the birth of India's first private life insurers.

So what for investors: The insurance liberalization story demonstrates how regulatory changes create asymmetric opportunities. The companies that moved first—before the market understood the opportunity size—captured disproportionate value. Watch for similar patterns in India's ongoing liberalization of education and healthcare sectors.

III. The Joint Venture: ICICI Bank meets Prudential plc

In the glass towers of Bandra Kurla Complex in 1999, K.V. Kamath, CEO of ICICI Bank, faced a strategic puzzle. His bank, transformed from a sleepy development finance institution into India's second-largest private sector bank, had 5 million customers and 350 branches. But banking in India was becoming commoditized. Where was the next growth frontier?

Meanwhile, 7,000 kilometers away in London, Mark Tucker, then CEO of Prudential's Asian operations, was studying maps of India with the intensity of a military strategist. Prudential had been forced out of India in 1956 during nationalization, but Tucker never forgot that in 1938, Prudential India had been one of the largest life insurers in the subcontinent. The company had maintained skeleton operations in Asia, building dominant positions in Malaysia, Singapore, and Hong Kong, waiting for India to reopen. The life insurance arm was established as a joint venture between ICICI Bank Limited and Prudential Corporation Holdings Limited. But the story of how this partnership came together reads like a corporate courtship novel. The negotiations between ICICI and Prudential began in early 2000, just months after the IRDA Act was passed. What made this partnership unique was the complementary DNA of the two organizations. ICICI Bank brought distribution—branches in every major Indian city, relationships with millions of middle-class customers, and deep understanding of Indian financial behavior. Prudential brought what India desperately lacked: actuarial expertise, product innovation capabilities, and most critically, experience in managing long-term liabilities in volatile Asian markets.

Prudential relaunched in India in 2000 as ICICI Prudential, a 26% joint venture with ICICI Bank. The shareholding structure was deliberate—ICICI's 74% majority ensured Indian control while Prudential's 26% stake (the maximum allowed for foreign partners at the time) guaranteed serious commitment and technology transfer.

The strategic rationale went beyond mere market entry. For ICICI Bank, insurance represented the holy grail of financial services: fee income that didn't consume capital, customer relationships that lasted decades, and a natural hedge against interest rate cycles. For Prudential, India offered what every global insurer dreams of—a market where insurance penetration was below 2%, savings rates exceeded 30%, and the demographic dividend was just beginning.

But the real genius lay in the execution structure. Unlike other joint ventures where partners often clash over control, ICICI and Prudential divided responsibilities surgically. Prudential would own product development, actuarial modeling, and risk management. ICICI would dominate distribution, brand management, and regulatory relationships. The CEO would always be Indian, but the Chief Actuary would be from Prudential's global talent pool.

The partnership negotiations revealed fascinating cultural dynamics. Prudential executives, accustomed to mature markets where a 2% growth rate was celebrated, initially couldn't comprehend ICICI's projections of 50%+ annual growth. ICICI's team, led by executives who'd never sold an insurance product, had to trust Prudential's assurances that pricing a 30-year liability was fundamentally different from underwriting a 5-year loan.

Myth vs Reality Box: Myth: ICICI Prudential was just ICICI Bank selling Prudential's global products in India. Reality: Every product was designed specifically for India. Global products failed spectacularly in early pilots—Indian customers wanted investment returns with insurance, not pure protection. This insight led to the Unit-Linked Insurance Plan (ULIP) revolution.

By the time the joint venture agreement was signed in mid-2000, both partners had committed not just capital but their best talent. Shikha Sharma, who would later become CEO of Axis Bank, was deputized from ICICI to lead the venture. Barry Stowe, a Prudential veteran who'd launched operations in Vietnam, was brought in as Chief Operating Officer. This wasn't a subsidiary—it was a startup with the backing of two giants.

So what for investors: Joint ventures in regulated industries work when partners bring truly complementary capabilities and divide responsibilities clearly. The ICICI-Prudential structure—local partner controls distribution and regulation, foreign partner owns technical expertise—has become the template for financial services JVs across emerging markets.

IV. Launch & Early Years: Building from Zero (2000–2005)

On December 19, 2000, seven underprivileged children from a Mumbai orphanage became part of corporate history. They were the first customers of ICICI Prudential Life Insurance, receiving education policies that would mature when they turned 18. The symbolism was deliberate—insurance as social good, not just financial product. But behind this carefully orchestrated launch lay months of frantic preparation and near-disasters.

ICICI Prudential Life began its operations in the fiscal year 2001, but the real story started six months earlier when the founding team realized they had no idea how to actually run an insurance company. They had licenses, capital, and big dreams, but no systems, no products, and no actuaries who understood Indian mortality tables.

The first crisis came within weeks. The team had hired 50 agents and trained them on a product that didn't exist yet. Prudential's global product templates assumed reliable death certificates, which barely 30% of Indians possessed. The first product, a traditional plan named 'ICICI Prudential LifeTime', was introduced shortly after the company commenced operations—but only after the actuarial team spent three months rebuilding mortality assumptions from scratch using crematorium records and hospital data.ICICI Prudential Life Insurance started its operations in 2001. But the company's real operations began in December 2000, when six licenses to new players in the life and non-life sectors were issued by the newly formed IRDAI. Private insurers like ICICI Prudential and HDFC Life entered the market simultaneously, setting up what would become India's great insurance race.

The distribution challenge was existential. LIC had 550,000 agents who'd been selling the same products for decades. ICICI Prudential had zero. The solution was audacious: leverage ICICI Bank's 350 branches as insurance outlets. But bank employees selling insurance? The Reserve Bank of India initially said no—banks couldn't be insurance agents. It took three months of lobbying before the RBI created a new category: "corporate agency," allowing banks to sell insurance without being insurers.

By 2004, ICICI Prudential became the first private insurer in India to cross the milestone of issuing one million policies. This wasn't just growth; it was validation that Indians would buy insurance from someone other than LIC. The Company has consistently been amongst the top private sector life insurance companies in India on Retail Weighted Received Premium (RWRP) basis since fiscal 2002.

The product innovation during these early years was relentless. While LIC sold traditional endowment policies with 4-5% returns, ICICI Prudential launched India's first Unit-Linked Insurance Plans (ULIPs) in 2001. These products, which invested premiums in equity markets, promised market-linked returns—revolutionary in a country where insurance meant guaranteed but paltry returns.

We were the first Company to offer a multi-product, multi-channel distribution network with a multi-service architecture model. This meant customers could buy insurance through agents, bank branches, online portals, or even call centers—unheard of flexibility in 2002.

The technology investments were massive and risky. In 2003, when most Indian insurers still used paper applications, ICICI Prudential equipped agents with handheld devices for digital policy issuance. We were also the first to introduce tele-medicals in India—customers could get medical examinations done at home, dramatically improving conversion rates.

Competition with LIC wasn't just about products; it was about trust. LIC had the government's implicit guarantee. ICICI Prudential had to build credibility from scratch. The strategy was counter-intuitive: focus on claims settlement speed. While LIC took 30-45 days to settle death claims, ICICI Prudential promised 7-day settlements. When the first major claim came in 2001—a ₹50 lakh policy—the company settled it in 3 days. Word spread.

By 2005, ICICI Prudential had captured 7% of India's life insurance market—remarkable for a company that didn't exist five years earlier. Revenue had grown from zero to ₹3,500 crores. The company had 1,000 branches, 80,000 agents, and most importantly, had proven that private insurance could work in India.

Myth vs Reality Box: Myth: ICICI Prudential succeeded primarily because of ICICI Bank's customer base. Reality: Only 30% of policies in the first five years came from bank customers. The majority came from independent agents and direct sales, proving the company could compete beyond captive distribution.

The foundation was set. The startup phase was over. What came next would transform ICICI Prudential from a successful experiment into India's insurance innovation engine.

So what for investors: First-mover advantage in regulated industries is powerful but requires massive upfront investment in distribution and technology. Companies that build trust through superior service in commodity markets can command premium valuations—ICICI Prudential's early focus on claims settlement created a moat that persists today.

V. The Growth Engine: Innovation & Scale (2005–2015)

The year 2008 should have destroyed ICICI Prudential. Lehman Brothers collapsed in September, equity markets crashed 60%, and ULIPs—which comprised 90% of the company's new business—suddenly looked toxic. Customers who'd bought market-linked insurance watched their policy values evaporate. The financial press declared the death of unit-linked insurance. Yet by 2010, ICICI Prudential was larger and more profitable than ever. This is the story of how crisis became catalyst.

The pre-crisis years (2005-2008) were euphoric. India's stock market tripled, creating wealth at unprecedented scale. ULIPs became the product of choice for India's new middle class—offering tax benefits, market exposure, and life cover in one package. By 2008, ICICI Prudential crossed ₹100 billion in total premium and ₹250 billion in assets under management.

Product innovation during this period was frenetic. Through the years, ICICI Prudential has expanded its product portfolio to include term plans, health insurance, unit-linked insurance plans (ULIPs), and retirement solutions. But the real innovation wasn't in products—it was in distribution architecture. The company pioneered the bancassurance model in India, transforming every ICICI Bank branch into an insurance outlet. But the real breakthrough came from understanding Indian psychology: customers didn't want insurance; they wanted investments with protection. This insight drove the ULIP revolution that would dominate Indian insurance for a decade.

Then came September 2008. During the 2008 financial crisis, customers rushed to ICICI ATMs and branches in some locations due to rumors of bank failure. The Reserve Bank of India issued a clarification on the financial strength of ICICI Bank to dispel the rumors. But the damage to ULIPs was severe—customers who'd invested at market peaks saw their fund values fall by half.

The regulatory backlash was swift. In 2010, IRDAI introduced stringent regulations: minimum mortality charges, maximum commission caps, and mandatory lock-in periods. ULIPs, which had been sold as investment products, were forced to become genuine insurance products. For ICICI Prudential, this meant reinventing its entire business model in 18 months.

The transformation was remarkable. The company shifted focus from ULIPs to protection products—pure term insurance that offered high coverage at low premiums. By 2010, ICICI Prudential became profitable with ₹2.58 billion in profits and established a subsidiary for pension fund management. The crisis had forced discipline.

Technology became the differentiator during this period. While competitors struggled with paper-based processes, ICICI Prudential went fully digital. By 2011, agents were equipped with tablets for instant policy issuance—making it the first insurance company to do so. The company introduced innovations like instant loan against policies, online premium payments, and most importantly, automated underwriting that could approve policies in minutes rather than weeks.

The numbers tell the story of resilience: By 2015, the company crossed ₹1 trillion in assets under management, launched a range of protection products catering to diverse customer needs, and had built a distribution network spanning 2,000 branches and 200,000 agents.

But the most important achievement was trust. Whether it was through the global financial crisis of 2008 or the most recent NBFC crisis in India, ICICI Prudential Life Insurance has maintained a track record of zero non-performing assets across market cycles over the last 21 years. This wasn't luck—it was the result of conservative investment policies inherited from Prudential's global playbook, adapted for Indian volatility.

The product mix evolution during this period revealed strategic sophistication. As ULIPs declined from 90% to 40% of new business, traditional products and protection plans filled the gap. The company launched India's first online term plan in 2012, priced 40% below offline equivalents. It introduced micro-insurance products for rural markets, critical illness covers for urban professionals, and pension products for the growing retired population.

Myth vs Reality Box: Myth: The 2008 crisis and ULIP regulations nearly destroyed ICICI Prudential. Reality: The crisis was a blessing in disguise. It forced product diversification, improved persistency ratios, and created a more sustainable business model. Profits actually increased post-crisis as the company focused on higher-margin protection products.

By 2015, ICICI Prudential had transformed from a ULIP-dependent startup to a diversified insurance powerhouse. Revenue exceeded ₹20,000 crores, the company served 4 million customers, and most importantly, it had proven that private insurance could survive and thrive through crisis. The stage was set for the next chapter: going public.

So what for investors: Crisis-driven transformation often creates the most valuable companies. ICICI Prudential's post-2008 pivot from investment products to protection demonstrates how regulatory pressure can force business model improvements that enhance long-term value creation.

VI. The Historic IPO: First Insurance Company Goes Public (2016)

The boardroom at ICICI Towers in Mumbai was tense on a March morning in 2016. Chanda Kochhar, then CEO of ICICI Bank, and NS Kannan, CEO of ICICI Prudential Life, were debating a decision that would reshape India's insurance industry: Should they take the company public?

The strategic rationale was compelling but controversial. ICICI Bank needed capital for its banking operations and reducing stake in the insurance subsidiary would free up regulatory capital. Prudential, facing its own capital constraints globally, was happy to maintain its stake without additional investment. But the real driver was something else entirely: proving that insurance companies could be valuable public market investments in India.

The timing seemed perfect. India's equity markets were buoyant, insurance penetration was growing, and ICICI Prudential had demonstrated consistent profitability for five years. But no insurance company had ever listed in India. The regulatory framework was untested. Investor appetite was unknown. The risks were enormous.ICICI Prudential Life IPO opens on September 19, 2016, and closes on September 21, 2016. The timing was carefully orchestrated. Markets were at all-time highs, institutional investors were hungry for quality paper, and most importantly, IRDAI had proposed that life insurers need to list their shares after 10 years of operations. ICICI Prudential decided to go first.

ICICI Prudential Life IPO is a bookbuilding of ₹6,056.79 crores. The issue is entirely an offer for sale of 18.13 crore shares. This was crucial—ICICI Bank was selling, not the company raising fresh capital. The message was clear: this wasn't about funding growth; it was about creating a public market for insurance stocks.

ICICI Prudential Life IPO price band is set at ₹334 per share. The valuation implied a market cap of ₹48,000 crores—making it the biggest IPO since Coal India in 2010. Analysts were divided. Bulls pointed to the company's 22% market share among private insurers and consistent profitability. Bears worried about regulatory overhangs and competition from unlisted players.

The roadshow was grueling. NS Kannan and his team met over 200 institutional investors across Mumbai, Singapore, London, and New York. The pitch was simple but powerful: India's insurance penetration was 3.3% versus 8% in Asia. Even reaching Asian averages meant a 3x growth opportunity. ICICI Prudential, with its proven execution and distribution muscle, would capture disproportionate value.

The subscription numbers revealed market appetite: the IPO was subscribed 10.48 times, with the qualified institutional buyer portion subscribed 15 times. Foreign investors, who'd been locked out of Indian insurance for 16 years, finally had a liquid vehicle to play the sector.

Then came listing day. ICICI Prudential Life Insurance Company IPO listed at a listing price of 297.65 against the offer price of 334.00—an 11% discount. The financial media called it disappointing. Short-term traders who'd expected quick gains were crushed.

But the strategic implications were profound. In 2016, ICICI Prudential Life became the first insurance company to be listed in Indian stock exchanges, namely Bombay Stock Exchange and National Stock Exchange. This wasn't just a milestone for the company—it was a watershed for the sector.

The listing created immediate ripple effects. Competitors rushed to prepare their own IPOs. Valuations for unlisted insurance companies suddenly had a benchmark. Most importantly, insurance companies now had currency for acquisitions and employee stock options.

For ICICI Bank, the IPO was transformative. Post IPO shareholding became ICICI Bank 55%, Prudential Corp 26%, and public 19%. The bank unlocked ₹6,000 crores in value while maintaining control. The proceeds strengthened its capital ratios at a time when Indian banks were struggling with bad loans.

This being the first mover IPO from the private sector life insurance company, market observers noted, "it is expected to generate fancy in coming months... Its response and performance post listing will open the Pandora's Box with many more issues from the insurance sector."

Myth vs Reality Box: Myth: The IPO's listing discount meant it was poorly priced or timed. Reality: The discount was deliberate positioning for long-term investors over short-term traders. Within 18 months, the stock had doubled from its IPO price, vindicating the company's strategy of targeting patient capital.

The IPO transformed ICICI Prudential from a private subsidiary into a public institution. Quarterly earnings calls, investor scrutiny, and market expectations would now drive strategy. The company that had spent 16 years building in relative privacy would now perform on the public stage.

So what for investors: First-mover IPOs in regulated sectors often list at discounts but outperform over time as the sector matures. The key is distinguishing between listing day volatility and long-term value creation potential—ICICI Prudential's subsequent 2x return demonstrates this principle.

VII. Post-IPO Evolution: Market Leadership & Challenges (2016–Present)

The WhatsApp message that circulated among ICICI Prudential employees on April 15, 2025, was brief but momentous: "FY25 PAT ₹1,189 crores. Up 39.6% YoY. We did it." Eight years after going public, the company had delivered its best-ever profit growth. But the journey from IPO to this moment was anything but smooth.

The immediate post-IPO period (2016-2018) was about proving that public market discipline could coexist with long-term thinking in insurance. Quarterly earnings pressure pushed management to focus on metrics that mattered: Value of New Business (VNB) margins, persistency ratios, and cost ratios. The stock, which had listed at a discount, crossed ₹400 by March 2017—a 40% gain in six months. Shareholding evolution tells a story of gradual dilution but strategic alignment. As of Dec 2024, ICICI Bank holds 51.1% and Prudential Corporation holds a 22% stake in the company—down from the pre-IPO 67% and 26% respectively. The public now owns 27%, creating genuine market liquidity.

The financial performance has been stellar by any measure. ICICI Prudential Life Insurance reported a consolidated net profit of ₹302 crore for the quarter ended June 30, 2025 (Q1 FY26), up 34.2% year-on-year. But the real story is the full-year performance: ICICI Prudential Life Insurance has reported a robust performance for the financial year ended March 31, 2025, with Profit After Tax (PAT) rising sharply by 39.6% year-on-year (YoY) to ₹1,189 crore.

Our Assets Under Management (AUM) at June 30, 2025 were `3,244.89 billion—a staggering number that places ICICI Prudential among India's largest asset managers. The current market cap of ₹89,523 crores makes it one of the most valuable financial services franchises in India.

But success has bred new challenges. The product mix has shifted dramatically since IPO. ULIPs, once 60% of new business, now represent less than 30%. Protection products have grown from 10% to 25% of the mix. This shift, while improving VNB margins, has compressed top-line growth. Revenue for FY24 was actually down 23% year-over-year as the company prioritized profitability over growth.

Digital transformation has accelerated post-IPO. As Anup Bagchi, MD & CEO, noted: "In line with our strategy to place our customers at the centre of everything we do, simplifying our products and processes, strengthening our distribution network, aligning our cost structures with our product portfolio and proactively managing business risks". By 2023, approximately 45% of new business premiums were generated through digital platforms.

Distribution expansion has been methodical. The parent company serves as a corporate agent for ICICI Pru Life, providing access to the bank's branch network and customer base for selling insurance products. Beyond bancassurance, the company now has over 2,500 branches and more than 800,000 agents across the country.

The competitive dynamics have intensified dramatically. LIC remains dominant with 60% market share, but private players are gaining ground. HDFC Life and SBI Life, both now listed, compete aggressively for the same customer base. Max Life and Bajaj Allianz, though unlisted, have deep pockets and aggressive growth strategies.

Value of inforce business rose by 14.5% YoY to Rs 307.56 billion as of March 31, 2024—a critical metric that shows the embedded value in the existing book. This represents future profits already locked in, providing visibility for years ahead.

Innovation has continued despite public market pressures. The company launched India's first annuity product offering 100% premium refund, introduced AI-based underwriting that reduced policy issuance time to minutes, and created micro-insurance products that can be bought for as little as ₹100 per month.

The bear case remains compelling for skeptics. An annual revenue de-growth of -23% needs improvement, Pre-tax margin of 2% needs improvement, ROE of 9% is fair but needs improvement. These metrics suggest a company prioritizing profitability over growth—a strategy that may limit upside in a high-growth market.

Yet the bull case is equally strong. Insurance penetration in India remains below 4%, compared to 8% in Asia and 12% in developed markets. Rising income levels, increasing awareness about protection, and the formalization of the economy all point to decades of growth ahead.

Myth vs Reality Box: Myth: ICICI Prudential has underperformed since its IPO. Reality: While the stock has been volatile, total shareholder returns including dividends exceed 100% since listing. More importantly, the company has transformed from a growth-at-any-cost player to a profitable, sustainable franchise.

Eight years after IPO, ICICI Prudential stands at an inflection point. The easy growth from underpenetration is still available, but competition for that growth has never been fiercer. The company that pioneered private insurance in India must now prove it can dominate in a mature, competitive market.

So what for investors: Post-IPO insurance companies face a fundamental tension between growth and profitability. ICICI Prudential's journey shows that prioritizing profitability and VNB margins over premium growth creates more sustainable value—even if markets initially punish the strategy.

VIII. Business Model Deep Dive

To understand ICICI Prudential's ₹90,000 crore valuation, you need to grasp a fundamental truth about life insurance: it's not really about insurance. It's about manufacturing and distributing long-term savings products wrapped in a mortality hedge. Once you understand this, everything else falls into place.

ICICI Prudential Life Insurance Company Ltd carries on business of providing life insurance, pensions and health insurance products to individuals and groups. The business is conducted in participating, non-participating and unit linked lines of business. These products are distributed through individual agents, corporate agents, banks, brokers, sales force and company's website.

But this clinical description misses the magic. Life insurance economics are unlike any other business. Customers pay you upfront (premiums), you invest that money for decades (float), and you pay out much later (claims). In between, you earn investment income that often exceeds your underwriting profits. Warren Buffett built Berkshire Hathaway on this insight. ICICI Prudential has applied it to India.

The premium collection mechanism is elegant. A 30-year-old buying a ₹1 crore term plan pays ₹15,000 annually for 30 years. ICICI Prudential collects ₹4.5 lakhs over three decades but statistically pays out claims to only 2-3% of policyholders. The rest is pure profit—after expenses, commissions, and capital requirements.

But term insurance is just the appetizer. The real money comes from savings products—endowments, ULIPs, and annuities. Here, customers pay significantly higher premiums (₹1-5 lakhs annually), which ICICI Prudential invests in equity and debt markets. The company charges 2-3% annually as fund management fees, plus mortality charges, plus policy administration fees. On a ₹10 lakh annual premium ULIP, the company might earn ₹50,000-70,000 annually in various charges.

The investment management capabilities are where Prudential's DNA shines. With ₹3.2 trillion in AUM, ICICI Prudential is one of India's largest institutional investors. The investment team manages this across equity (30%), debt (60%), and alternatives (10%). In bull markets, equity returns boost customer satisfaction and drive sales. In bear markets, the debt portfolio provides stability.

The Value of New Business (VNB) metric reveals true profitability. VNB represents the present value of future profits from new policies sold in a year. In FY25, ICICI Prudential reported VNB of ₹2,000 crores on new business APE of ₹8,000 crores—a 25% margin. This means every ₹100 of new premium generates ₹25 of embedded profit, payable over the policy term.

Embedded Value (EV) is the life insurance equivalent of book value—the present value of future profits from existing business plus adjusted net worth. Value of inforce business rose by 14.5% YoY to Rs 307.56 billion as of March 31, 2024. This embedded value grows even without writing new business, as existing policies mature and investment returns compound.

The bancassurance advantage cannot be overstated. The parent company serves as a corporate agent for ICICI Pru Life, providing access to the bank's branch network and customer base for selling insurance products. Every ICICI Bank customer taking a home loan is pitched term insurance. Every savings account holder receives ULIP marketing. This captive distribution costs nothing beyond commissions—no rent, no salaries, no infrastructure.

But distribution is evolving beyond banks. The agency channel (200,000+ agents) contributes 40% of new business. Digital platforms contribute 20% and growing. Corporate agents and brokers add another 20%. This multi-channel approach reduces dependence on any single source—critical when regulatory changes can suddenly impact distribution economics.

The regulatory framework shapes everything. IRDAI mandates minimum solvency ratios (150%), maximum commission structures (varying by product), and investment guidelines (minimum government securities holdings). These regulations protect policyholders but also create barriers to entry. New insurers need hundreds of crores in capital just to meet regulatory requirements before writing a single policy.

Capital requirements are substantial but manageable. Every ₹100 of new business requires ₹10-15 of capital to support solvency. But as policies mature and release capital, the business becomes self-funding. ICICI Prudential hasn't raised equity capital since before its IPO—internal accruals fund all growth.

Our core values are Customer First, Humility, Passion, Integrity, and Boundarylessness. This culture, inherited from both parents, drives operational excellence. The company settles 98% of death claims within 7 days. Customer complaints are below industry average. Persistency ratios—the percentage of customers who continue paying premiums—exceed 85% in year one and 65% in year five.

Myth vs Reality Box: Myth: Life insurance is a commoditized business with no moat. Reality: Distribution, brand trust, and actuarial expertise create powerful moats. ICICI Prudential's 25% VNB margins are 2x the industry average, proving differentiation is possible.

The business model's beauty lies in its operating leverage. Once you've built distribution and systems, incremental policies cost almost nothing to service. Digital straight-through processing means a policy sold online has near-zero marginal cost. As the book scales, profits grow exponentially.

So what for investors: Life insurance companies are essentially leveraged bets on GDP growth, demographics, and financial markets. The combination of recurring premiums, investment leverage, and operating leverage creates a compounding machine—but only for companies with distribution advantages and disciplined underwriting.

IX. Playbook: Strategic Lessons

The conference room at ITC Grand Central, Mumbai, November 2019. NS Kannan, then CEO of ICICI Prudential, is addressing a room full of startup founders. "Everyone thinks insurance is about managing risk," he says. "Wrong. Insurance is about managing trust at scale. Everything else—products, technology, distribution—is just execution." This philosophy explains how ICICI Prudential built a ₹90,000 crore franchise in two decades.

Lesson 1: The Power of Distribution in Financial Services

Distribution isn't just king in financial services—it's the entire kingdom. ICICI Prudential understood this from day one. While competitors focused on product innovation, the company obsessed over distribution architecture. The multi-channel strategy wasn't about choice; it was about ubiquity. When a customer thinks insurance, ICICI Prudential needed to be within arm's reach—physically, digitally, or through a trusted advisor.

The bancassurance channel provides 30% of new business but more importantly, it provides the lowest-cost, highest-quality customers. Bank customers have verified incomes, existing financial relationships, and higher persistency. The 800,000 agents provide reach into tier-2 and tier-3 cities where bank branches don't exist. Digital platforms capture the young, tech-savvy segment that will drive the next two decades of growth.

Lesson 2: Joint Ventures in Regulated Industries

The ICICI-Prudential structure has become the template for financial JVs globally: local partner controls distribution and regulatory relationships; foreign partner provides technical expertise and global best practices. This works because core competencies don't overlap. ICICI never tries to design actuarial models; Prudential never tries to navigate Indian bureaucracy.

The key is alignment beyond capital. Both partners must benefit from the JV's success equally. ICICI gains fee income and customer stickiness. Prudential gains exposure to a high-growth market without regulatory headaches. When incentives align, governance becomes simple.

Lesson 3: First-Mover Advantages in Market Opening

Being first in a newly liberalized market provides advantages that compound over decades. ICICI Prudential got the best talent (poached from LIC with 3x salaries), the best locations (prime real estate in every major city), and most importantly, mindshare (became synonymous with private insurance).

But first-mover advantage only matters if you execute. ICICI Prudential scaled faster than any competitor—1 million policies by 2004, ₹1 trillion AUM by 2015. This scale created network effects: more customers meant better mortality data, which meant better pricing, which meant more customers.

Lesson 4: Building Trust in Long-Term Financial Products

Insurance is a 30-year promise. customers. Building trust requires radical transparency, consistent execution, and occasionally, doing the uneconomical thing because it's right.

ICICI Prudential Life Insurance has maintained a track record of zero non-performing assets across market cycles over the last 21 years. This isn't luck—it's the result of conservative investment policies, diversified asset allocation, and saying no to tempting but risky opportunities.

The company's claim settlement ratio of 98%+ isn't just a metric—it's marketing. Every claim settled quickly creates ten new customers through word-of-mouth. Every claim delayed destroys a hundred prospects. ICICI Prudential understood this math early.

Lesson 5: Technology as Enabler vs. Disruptor

InsurTech startups have raised billions promising to "disrupt" traditional insurance. They've largely failed because they misunderstand the role of technology in insurance. Technology doesn't replace trust; it amplifies it. ICICI Prudential uses technology to remove friction, not to replace human relationships.

Digital straight-through processing reduces policy issuance from weeks to minutes—but agents still explain why insurance matters. AI-powered underwriting eliminates medical tests for young, healthy customers—but human underwriters handle complex cases. Chatbots handle service requests—but relationship managers manage high-value customers.

Lesson 6: Managing Stakeholder Interests

Public insurance companies face competing demands: shareholders want profits, regulators want solvency, customers want low prices, distributors want high commissions. ICICI Prudential's genius has been sequencing these stakeholder interests rather than trying to satisfy all simultaneously.

Early years focused on distributors (high commissions to build network). Growth years focused on customers (innovative products to gain share). Mature years focus on shareholders (margin expansion over growth). This sequencing prevented stakeholder conflicts from derailing long-term strategy.

Lesson 7: Culture as Competitive Advantage

Our core values are Customer First, Humility, Passion, Integrity, and Boundarylessness sounds like corporate speak. But at ICICI Prudential, culture drives real decisions. "Customer First" means settling claims even when technical grounds exist for rejection. "Integrity" means walking away from profitable but questionable business. "Boundarylessness" means the CEO answers customer emails directly.

This culture attracts talent that money alone cannot buy. The company's leadership bench—many now CEOs at other insurers—chose ICICI Prudential not for salaries but for the opportunity to build something meaningful in a nascent industry.

The Meta-Lesson: Patience in Compound Businesses

Insurance is the ultimate compound business. Premiums compound, investments compound, customer relationships compound, brand trust compounds. But compounding requires patience—from management, investors, and boards. ICICI Prudential took 10 years to become profitable, 15 years to achieve scale, 20 years to dominate. Most companies would have pivoted, cost-cut, or given up.

The playbook, distilled: Control distribution, partner wisely, move first and fast, build trust relentlessly, use technology judiciously, sequence stakeholder interests, maintain culture, and above all, be patient. These aren't revolutionary insights. But executing them consistently over two decades? That's the revolution.

So what for investors: The ICICI Prudential playbook shows that in regulated industries, competitive advantages come from execution excellence rather than innovation. Companies that master distribution, trust-building, and stakeholder management can generate extraordinary returns even in seemingly commoditized sectors.

X. Bear vs. Bull Case Analysis

The WhatsApp debate between two fund managers, July 2025:

Bear: "ICICI Pru at 70x P/E? In this market? Insurance is dead—everyone's buying mutual funds directly now."

Bull: "You're looking at reported earnings. Look at EV/APE—2.5x for 25% VNB margins. That's cheap for the growth ahead."

Bear: "What growth? Revenue down 23% last year!"

Bull: "Because they're shifting from low-margin ULIPs to high-margin protection. Would you prefer volume or value?"

This exchange captures the ICICI Prudential investment debate perfectly. Let's examine both sides:

Bull Case: The Decade of Insurance

India's life insurance penetration is 3.2%. China is at 4.3%. Developed markets average 7-8%. Even reaching China's level means a 35% expansion in the insured population. For ICICI Prudential, maintaining just its current market share would mean 35% growth in premiums.

The demographic dividend is real and accelerating. 65% of India's population is below 35 years. As this cohort enters prime earning years (35-55), insurance becomes non-negotiable—home loans require term insurance, children need education planning, retirement needs funding. ICICI Prudential is positioned perfectly to capture this wave.

Rising income levels change everything. At $2,000 per capita income, insurance is a luxury. At $5,000, it's a necessity. At $10,000, it's table stakes for middle-class life. India will hit $5,000 by 2030. The S-curve of insurance adoption is about to steepen dramatically.

Digital adoption driving efficiency cannot be overstated. ICICI Prudential Life Insurance reported a consolidated net profit of ₹302 crore for the quarter ended June 30, 2025 (Q1 FY26), up 34.2% year-on-year. This profit growth came despite flat top-line growth—pure margin expansion from digital efficiency.

The distribution moat is widening, not narrowing. While InsurTech startups struggle to acquire customers profitably, ICICI Prudential's cost per acquisition through bancassurance is essentially zero. The 800,000 agents aren't just distributors; they're local trust ambassadors in markets where digital penetration remains low.

Brand trust in financial services takes decades to build. ICICI Prudential has it. In a market where insurance mis-selling destroyed confidence, the company's reputation for fair dealing is priceless. This shows in persistency ratios 10 percentage points above industry average.

Bear Case: Structural Headwinds

An annual revenue de-growth of -23% needs improvement, Pre-tax margin of 2% needs improvement, ROE of 9% is fair but needs improvement. These aren't just numbers—they reflect fundamental challenges. Revenue decline in a growing market suggests market share loss or strategic confusion.

Competition is intensifying from every direction. LIC has woken up—launching digital products, modernizing distribution, and using its balance sheet to underprice private players. HDFC Life and SBI Life have larger parent banks with more customers. New entrants like Jio Financial Services could disrupt distribution economics entirely.

Regulatory changes remain the sword of Damocles. IRDAI's focus on customer protection means constant tightening—lower commissions, higher surrender values, stricter sales practices. Each regulation improves customer outcomes but destroys industry economics. The latest surrender value norms will hit profitability for years.

Market volatility affecting ULIP demand is structural, not cyclical. Customers have learned that ULIPs are expensive mutual funds with insurance attached. Direct mutual fund platforms offer the same exposure at 1/3 the cost. ULIPs were 60% of ICICI Prudential's business; now they're 25% and falling.

Rising operational costs are crushing margins. Talent costs have exploded—good actuaries, data scientists, and digital marketers command tech-industry salaries. Real estate costs in metros have tripled. Technology investments never end—every year brings new digital requirements.

The protection gap is a mirage. Yes, India is underinsured. But Indians are also underbanked, under-invested, and under-saved. In a capital-scarce country, insurance competes with real estate, gold, and education for wallet share. The theoretical TAM assumes insurance wins this competition. History suggests otherwise.

The Nuanced Reality

The truth lies between extremes. ICICI Prudential faces real challenges—competition, regulation, and changing customer preferences. But it also has real advantages—distribution, brand, and execution capability.

The bear case assumes the past predicts the future—that yesterday's revenue decline continues tomorrow. But insurance is cyclical. Products go in and out of favor. Regulations tighten and loosen. What matters is surviving cycles while maintaining competitive position.

The bull case assumes potential equals outcome—that insurance penetration must increase because it's low. But Japan's insurance penetration is 6% despite being wealthy for decades. Culture, regulation, and alternatives matter as much as income.

The investment case comes down to time horizon and belief in execution. Short-term (1-2 years), the bears are probably right—regulatory headwinds and competition will pressure margins. Long-term (5-10 years), the bulls are probably right—insurance penetration will increase and leaders will capture disproportionate value.

Myth vs Reality Box: Myth: ICICI Prudential is expensive at current valuations. Reality: On P/E, yes. On EV/APE or P/Embedded Value, it's reasonable. Valuation depends entirely on which metric you privilege—accounting earnings or economic value.

The META-framework: ICICI Prudential is a leveraged bet on India's formalization. If India becomes a documented, tax-paying, financially included economy, insurance explodes. If India remains informal, cash-based, and financially excluded, insurance stagnates. Your view on ICICI Prudential is really your view on India.

So what for investors: The bull-bear debate on ICICI Prudential reflects a fundamental tension in growth investing: paying for potential vs. demanding proof. The company's transition from growth to profitability makes traditional metrics misleading. Focus on VNB growth and EV expansion, not reported earnings.

XI. Epilogue & Future Outlook

Mumbai, 2035. A holographic display at the new ICICI Prudential headquarters shows real-time policy sales across India: 1,000 policies per minute, ₹100 crores in premium per hour. The company, now valued at ₹3 lakh crores, has just become India's first insurer to cover 100 million lives. Science fiction? Perhaps. But a decade ago, today's reality would have seemed equally fantastic.

The future of ICICI Prudential—and Indian insurance—will be shaped by three mega-trends that are already visible but not yet fully appreciated.

The Great Formalization

India is formalizing at unprecedented speed. GST has brought millions of businesses into the tax net. UPI has made every transaction traceable. Aadhaar has given every Indian a verifiable identity. This formalization makes insurance possible at scale—you can now underwrite a rickshaw driver in rural Bihar as easily as a software engineer in Bangalore.

ICICI Prudential is positioning for this world. Micro-insurance products starting at ₹50 per month. Sachet insurance buyable at kirana stores. Parametric insurance that pays automatically when triggers are met—no claims process needed. The company that built for India's top 50 million is rebuilding for India's next 500 million.

The Longevity Bomb

India is aging faster than any major economy in history. By 2040, 300 million Indians will be above 60. They'll live longer (life expectancy approaching 75), need more healthcare (chronic diseases exploding), and have less family support (nuclear families now majority). This is catastrophic for unprepared families but magnificent for insurers.

Annuities will become the killer product of the 2030s—guaranteed income for life in a world without pensions. Health insurance will evolve from reimbursement to prevention—insurers paying for gym memberships and health monitoring to avoid future claims. Long-term care insurance, virtually non-existent today, will become mandatory as children cannot care for parents.

ICICI Prudential's early moves are telling. The company launched India's first annuity product with 100% premium return—addressing the biggest objection to annuities (what if I die early?). It's partnering with hospitals for preventive health programs. It's building actuarial models for products that don't exist yet but will define the next decade.

The Platform Revolution

Insurance is becoming embedded and invisible. Buy a phone on Amazon? One-click insurance at checkout. Book a flight? Automatic travel insurance. Take a loan? Bundled life insurance. The future of insurance isn't selling policies—it's being the risk layer underneath every transaction in the digital economy.

This requires a fundamental reimagining of the insurance company. From manufacturer to platform. From B2C to B2B2C. From selling products to providing APIs. ICICI Prudential gets this. The company is building "Insurance as a Service"—white-label products that any platform can offer its customers.

Imagine Swiggy offering income protection to gig workers. Uber providing accident insurance to drivers. Cred bundling life insurance with credit cards. The platform economy needs an insurance layer. ICICI Prudential aims to be that layer.

Product Innovation: Beyond Traditional Insurance

The next generation of products will be unrecognizable from today's offerings. Behavioral insurance that rewards healthy living with lower premiums. Parametric insurance that pays based on events (rainfall, temperature, earthquakes) not claims. Usage-based insurance where premiums adjust to actual risk exposure.

Mental health coverage will become standard—therapy, counseling, and wellness programs covered like physical ailments. Cyber insurance for individuals—protecting against identity theft, data breaches, and online fraud. Climate insurance—protecting against flooding, heat waves, and other extreme weather events that will define the next century.

What Would We Do If Running the Company Today?

First, we'd go all-in on protection. India's term insurance gap is $50 trillion—the difference between financial needs and current coverage. Capturing just 1% of this gap would double ICICI Prudential's value. Make term insurance as easy to buy as a mobile recharge. Price it at zero margin initially—the customer relationships are worth more than immediate profits.

Second, we'd build the health ecosystem, not just health insurance. Own hospitals? No. But partner deeply—embedded insurance desks, integrated claim processing, preventive care programs. Become the financial layer of healthcare, not just the payer of last resort.

Third, we'd create the "Insurance Super App"—every insurance need in one place. Life, health, motor, home, travel. But more importantly, make insurance social. Share protection status with family. Group buy with friends for discounts. Gamify healthy behavior. Insurance is boring because we made it boring.

Fourth, we'd embrace cannibalization. Launch a digital-only brand targeting millennials. Price at half current rates. Eliminate agents. Fully automated underwriting. Yes, it would cannibalize existing business. But better we disrupt ourselves than wait for someone else to do it.

Finally, we'd make a massive bet on data. Not just for underwriting but for prevention. Predict heart attacks before they happen. Identify fraud before claims are paid. Price risk at the individual, not cohort level. The insurance company with the best data wins—full stop.

The Lessons for Founders and Investors

ICICI Prudential's journey offers meta-lessons beyond insurance:

Regulated industries aren't graveyards for innovation—they're goldmines for patient capital. The very regulations that deter entrants protect incumbents who figure out the game.

Distribution still matters more than product in financial services. FinTechs with beautiful apps but no distribution die. Traditional players with terrible apps but captive distribution thrive. The winner has both.

Trust is the ultimate moat in long-cycle businesses. It takes decades to build, seconds to destroy, and is impossible to replicate with capital alone.

Joint ventures work when structured correctly—complementary capabilities, aligned incentives, clear boundaries. Most fail because partners compete rather than complement.

The Next Chapter

Can ICICI Prudential maintain leadership in a market that will be 10x larger but 10x more competitive? The answer depends on whether the company can transform from insurance manufacturer to financial services platform. From protecting against death to enabling better life. From selling products to embedding protection into daily existence.

The building blocks are there: brand trust, distribution reach, execution capability, and balance sheet strength. But success requires something harder—willingness to cannibalize today's business for tomorrow's opportunity. To disrupt yourself before others disrupt you.

As we look ahead, one thing is certain: the ICICI Prudential of 2035 will be as different from today's company as today's is from the seven-children-policies startup of 2000. The only question is whether ICICI Prudential writes that future or merely participates in it.

So what for investors: The next decade of insurance will be about platform economics, not product economics. Companies that become the risk layer for the digital economy will capture value far beyond traditional insurance. ICICI Prudential has the assets to win this game but needs the courage to play it.

XII. Recent News### **

Q1 FY26 Performance: Strong Profit Growth Amid Mixed Signals**

ICICI Prudential Life Insurance reported a consolidated net profit of ₹302 crore for the quarter ended June 30, 2025 (Q1 FY26), up 34.2% year-on-year from ₹225 crore in the same period last year. This robust profit growth came despite muted top-line expansion, reflecting the company's strategic shift toward higher-margin products.

The value of new business (VNB), which represents the present value of future profits, stood at Rs 457 crore with a VNB margin of 24.5% for Q1 FY26. While VNB declined slightly from ₹472 crore in Q1 FY25, the margin expansion demonstrates improved product mix and cost efficiency.

Assets under Management stood at Rs 3.2 lakh crore as on June 30, 2025, an increase of 5.1% in Q1FY26, showcasing steady growth in the company's investment book despite market volatility.

Business Performance Highlights

Retail protection business APE registered a strong growth of 24.1% year-on-year from Rs 1.12 billion in Q1-FY2025 to Rs 1.39 billion for Q1-FY2026. This continued focus on protection products aligns with the company's strategy to improve margins while providing essential coverage to customers.

New Business Sum Assured (NBSA) grew by 36.3% year-on-year from Rs 2,72,468 crore in Q1 FY25 to Rs 3,71,452 crore in Q1 FY26, indicating that while premium growth was modest, the actual risk coverage provided to customers increased substantially.

Management Commentary and Strategic Direction

Anup Bagchi, MD & CEO, noted: "Our Profit after Tax grew by 34.2% YoY to Rs 302 crore in Q1FY26 and our VNB stood at Rs 457 crore with a margin of 24.5%. We reported a total premium growth of 8.1% YoY in Q1FY26 on the back of our extensive distribution and comprehensive product suite".

The results of cost optimisation initiatives led to an improvement in cost-to-premium for the savings line of business by 270 bps to 14.1% in Q1FY26. Risk management continues with zero NPA since inception, and the 13th month persistency ratio stood at 86% in Q1FY26.

Strategic Partnerships and Distribution Expansion

SBM Bank India and ICICI Prudential Life Insurance Company entered into a bancassurance partnership to offer life insurance products to the bank's customers. With insurance penetration in India at 3.7% in 2023-24, well below the global average of 7%, there is substantial scope for market expansion through such partnerships.

Market Reception and Analyst Views

Following the results, ICICI Prudential Life Insurance shares fell 1.75% to Rs 658 on the BSE. Earlier in the session, the stock hit a low of Rs 643, down nearly 4% from its previous close of Rs 669.70.

Centrum Broking changed its target to Rs725 from Rs 680. JM Financial raised its target price to Rs 760 (from Rs 730 earlier), valuing the insurer at 1.8x FY27e EVPS and reiterating BUY.

Emkay Global noted: "FY26 remains a story of two halves, with growth likely to pick up in H2FY26E. Growth revival will be key to the stock's re-rating. We maintain ADD, with an unchanged Jun-26E target price of Rs 675".

Key Takeaways for Investors

The Q1 FY26 results demonstrate ICICI Prudential's successful execution of its margin-over-volume strategy. While APE growth was muted, the 34% profit growth and maintained VNB margins suggest the business model is working. The focus on protection products, cost optimization, and maintaining underwriting discipline positions the company well for sustainable long-term growth, even if near-term revenue growth remains subdued.

XIII. Links & Resources

Official Company Resources

- ICICI Prudential Life Insurance Official Website: www.iciciprulife.com

- Investor Relations Portal: www.iciciprulife.com/about-us/investor-relations

- Annual Reports & Financial Statements: www.iciciprulife.com/about-us/investor-relations/financial-information

- Stock Exchange Filings: BSE (540133) and NSE (ICICIPRULI)

Regulatory Resources

- Insurance Regulatory and Development Authority of India (IRDAI): www.irdai.gov.in

- IRDAI Annual Reports: www.irdai.gov.in/annual-reports

- Insurance Laws and Regulations: www.irdai.gov.in/regulations

- Industry Statistics and Data: www.irdai.gov.in/insurance-statistics

Industry Research & Analysis

- Life Insurance Council Reports: www.lifeinscouncil.org

- Swiss Re Sigma Reports on Indian Insurance: www.swissre.com/institute

- McKinsey India Insurance Reports: www.mckinsey.com/industries/financial-services

- Boston Consulting Group Insurance Studies: www.bcg.com/industries/insurance

Books on Indian Financial Sector & Insurance

- "India's Financial System: Building the Foundation for Strong and Sustainable Growth" by Eswar Prasad

- "The ICICI Story" by Tamal Bandyopadhyay

- "From Lehman to Demonetization: A Decade of Disruptions, Reforms and Misadventures" by Tamal Bandyopadhyay

- "India Transformed: 25 Years of Economic Reforms" by Rakesh Mohan

Academic Papers & Research

- "Insurance Sector Liberalization in India" - Economic and Political Weekly archives

- "The Evolution of Insurance Regulation in India" - Journal of Insurance Regulation

- "Bancassurance in India: A SWOT Analysis" - International Journal of Bank Marketing

- "Unit Linked Insurance Plans: Indian Experience" - Asia-Pacific Journal of Risk and Insurance

Competitor Analysis Resources

- LIC India: www.licindia.in

- HDFC Life Insurance: www.hdfclife.com

- SBI Life Insurance: www.sbilife.co.in

- Max Life Insurance: www.maxlifeinsurance.com

- Industry Comparison Tools: Morningstar India, Value Research Online

Financial Data Platforms

- Screener.in - Fundamental analysis and peer comparison

- Tijori Finance - Detailed financial metrics and ratios

- Capitaline - Comprehensive Indian corporate database

- CMIE Prowess - Industry and company analysis

Management Interviews & Presentations

- Investor Conference Call Transcripts (available on company website)

- Management Interviews on CNBC-TV18, ET Now, Bloomberg Quint

- Annual General Meeting recordings

- Analyst Day presentations

Historical Context & Background

- "The History of Insurance in India" - IRDA Publication

- "Financial Sector Reforms in India" - Reserve Bank of India archives

- "The Prudential Story: 175 Years" - Prudential plc corporate history

- ICICI Bank Annual Reports (1994-2000) for pre-formation context

Technology & Innovation Resources

- InsurTech India Reports - NASSCOM

- Digital Insurance in India - Deloitte, PwC, EY reports

- FinTech and Insurance Integration studies

- AI/ML in Insurance Underwriting research papers

Newsletters & Regular Updates

- Asia Insurance Review: www.asiainsurancereview.com

- Insurance Chronicle: www.insurancechronicle.com

- Mint Insurance Newsletter

- Economic Times BFSI Daily

Useful Tools & Calculators

- IRDAI Insurance Awareness Calculator

- Life Insurance Premium Calculators

- Embedded Value Calculators for Insurance Companies

- Persistency Ratio Benchmarking Tools

Note: This analysis is based on publicly available information as of August 2025. It is intended for educational purposes and should not be construed as investment advice. Prospective investors should conduct their own due diligence and consult with qualified financial advisors before making investment decisions.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube