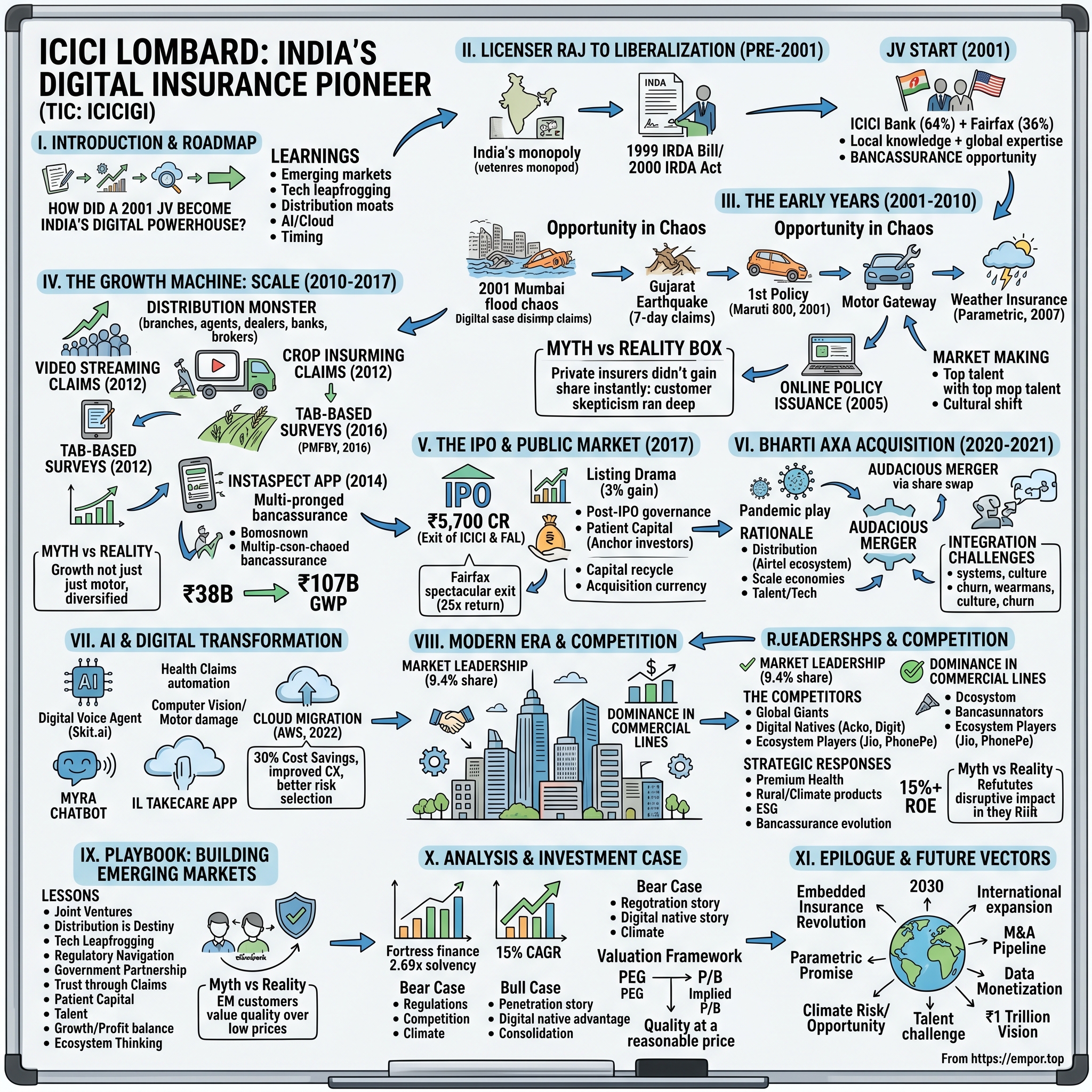

ICICI Lombard: India's Digital Insurance Pioneer

I. Introduction & Episode Roadmap

The monsoon of 2005 brought unprecedented flooding to Mumbai, submerging entire neighborhoods and paralyzing India's financial capital for days. As water levels rose to chest-height in some areas, thousands of vehicles floated like paper boats, homes were destroyed, and businesses ground to a halt. For India's insurance companies, still operating with paper forms and manual processes, the deluge of claims that followed would take months to process. But one company saw opportunity in this chaos. ICICI Lombard, which had obtained regulatory approval to undertake general insurance business on August 3, 2001, was barely four years old but already experimenting with something radical: digital claims processing.

Fast forward to today, and that early bet on technology has transformed into market dominance. With a Gross Written Premium of ₹282.58 billion for the year ended March 31, 2025, ICICI Lombard stands as India's most valuable private general insurer, commanding a market share of 9.4% as of H1 FY25. The company that once struggled to convince customers to trust a private insurer in a government-dominated market now has issued over 37.6 million policies and processed over 3.2 million claims.

But here's the central question that drives our exploration today: How did a 2001 joint venture between a bank and a Canadian insurer become India's digital insurance powerhouse? This isn't just a story about selling policies—it's about building trust in a skeptical market, leveraging technology before it was fashionable, and creating value through multiple economic cycles and regulatory shifts.

What you'll learn in this deep dive goes beyond insurance. We're talking about building in emerging markets where the rules are still being written, where technology leapfrogging isn't just possible but necessary, and where patient capital can create extraordinary outcomes. We'll explore how ICICI Lombard navigated India's complex regulatory landscape, built distribution moats that competitors still struggle to replicate, and most importantly, how they're using artificial intelligence and cloud computing to reimagine what insurance can be in the world's most populous nation.

This is also a masterclass in timing—entering when doors open, scaling when others hesitate, and transforming when technology enables. From the liberalization moment that created the opportunity to the AI revolution reshaping claims today, every chapter reveals strategic choices that compound over decades.

So what for investors? ICICI Lombard represents a rare combination: exposure to India's massive under-penetrated insurance market (with general insurance penetration at just 1% versus 4% globally), technological leadership in a traditionally slow-moving industry, and the backing of ICICI Bank's distribution might. At current valuations, you're essentially betting on whether India's insurance market can grow from its current $100 billion to potentially $500 billion over the next decade—and whether ICICI Lombard can maintain or expand its share of that pie.

II. The License Raj to Liberalization Story

Picture India in 1999: A nation of a billion people with exactly four general insurance companies—all government-owned subsidiaries of the General Insurance Corporation. If you wanted to insure your car, home, or business, you had no choice but to queue up at a government office, fill out forms in triplicate, and hope your claim would be processed sometime in the next few months. The insurance sector was a monopoly so complete that private participation had been banned since 1972, when Indira Gandhi's government nationalized the entire industry.

Then came the moment that changed everything. The IRDA Bill was passed in December 1999 and became an Act in April 2000, cracking open the door to one of the world's last great untapped insurance markets. Following the recommendations of the Malhotra Committee, in 1999 the Insurance Regulatory and Development Authority (IRDA) was constituted to regulate and develop the insurance industry. The committee had painted a stark picture: India's insurance penetration was abysmal, products were outdated, and customer service was virtually non-existent. The IRDA opened up the market in August 2000 with an invitation for registration applications; foreign companies were allowed ownership up to 26 percent.

This is where our protagonists enter the stage. ICICI Bank, India's second-largest private bank, saw insurance as the missing piece of their financial services puzzle. They had the customers, the branches, and the trust—but they needed expertise. Enter Fairfax Financial Holdings, the Canadian insurance giant led by Prem Watsa, often called the "Warren Buffett of Canada." Fairfax wasn't looking for quick flips; they were building a global insurance empire, and India was too big to ignore.

ICICI Lombard started as a Joint Venture (JV) between ICICI Bank and Fairfax Financial Holdings in 2001, with ICICI Bank holding 64% stake in the venture while Fairfax had 36%. The structure was deliberate: ICICI brought local knowledge, regulatory relationships, and most critically, access to millions of banking customers. Fairfax brought underwriting expertise, risk management frameworks, and global best practices.

But why would ICICI Bank, already stretched across retail banking, investment banking, and capital markets, venture into insurance? The answer lay in what industry insiders call the "bancassurance opportunity." Every bank customer is a potential insurance customer—they have assets to protect, lives to insure, and businesses to cover. In mature markets, banks earn as much from insurance distribution as from traditional lending. K.V. Kamath, then CEO of ICICI Bank, saw this clearly: insurance wasn't a distraction from banking; it was banking's natural evolution.

The timing was everything. In October 2000, six licenses to new players in the life and non-life sectors were issued. ICICI Lombard was among the first wave, gaining first-mover advantage in a market worth ₹1.28 trillion on a GDPI basis as of March 31, 2017—a market that had grown at 17.4% CAGR between fiscal 2001 and fiscal 2017.

Myth vs Reality Box: Myth: Private insurers immediately captured market share from government companies. Reality: It took years of trust-building. Even by 2004, private insurers had less than 10% market share. Customer skepticism ran deep—would these new companies honor claims? Would they even survive?

Fairfax's strategy in India wasn't unique—they were replicating a playbook refined across emerging markets from Brazil to Malaysia. Partner with a strong local player, transfer knowledge gradually, and play the long game. Prem Watsa would later say that India was Fairfax's most successful emerging market investment, but in 2001, that success was far from guaranteed.

The regulatory environment was both an opportunity and a minefield. IRDA was writing rules in real-time, trying to balance consumer protection with market development. Capital requirements were steep—₹100 crores minimum—and solvency ratios were strictly monitored. Distribution was heavily regulated, with limits on commission structures and mandatory rural and social sector obligations. For every policy sold in Mumbai or Delhi, insurers had to sell policies in rural Bihar or Jharkhand.

Yet these constraints became competitive advantages for those who could navigate them. ICICI Lombard didn't fight the rural mandate; they embraced it, seeing it as forced market development that would eventually pay dividends. They didn't just comply with regulations; they helped shape them, with senior executives serving on IRDA committees and working groups.

So what for investors? The liberalization story teaches us that regulatory moats can be as powerful as technological ones. Early entrants who shaped the rules, built relationships with regulators, and invested in compliance infrastructure created barriers that late entrants still struggle to overcome. Understanding this dynamic is crucial for evaluating any emerging market financial services play.

III. Building from Zero: The Early Years (2001–2010)

August 3, 2001. In a modest office in Mumbai's Bandra Kurla Complex, ICICI Lombard's first employees gathered around a single computer to issue their first policy. The customer? An ICICI Bank employee insuring his Maruti 800. Premium collected: ₹3,847. It was a humble beginning for what would become a ₹280 billion premium business.

The challenge facing CEO Sanjeev Mantri and his team of 12 was monumental. How do you convince Indians to buy insurance from a company they've never heard of, in an industry where the government had monopolized trust for three decades? The answer wouldn't come from advertising budgets or celebrity endorsements. It would come from something more fundamental: being there when customers needed them most.

The 2001 Gujarat earthquake had just devastated Kutch, killing 20,000 people and destroying 400,000 homes. While government insurers struggled with the scale of claims, taking months to process payments, ICICI Lombard made a radical decision: they would settle claims within 7 days. Not 7 weeks or 7 months—7 days. It was an impossible promise that required reimagining every process, but Mantri knew that in insurance, reputation is built one claim at a time.

The product portfolio started simple but strategic. Motor insurance was the gateway drug—mandatory, high-frequency, and relatively straightforward to underwrite. But even here, ICICI Lombard innovated. While competitors required physical inspection of vehicles before issuing policies, ICICI Lombard introduced self-declaration forms, trusting customers and using statistical models to detect fraud. It was a calculated risk that paid off in customer acquisition speed.

Health insurance was the next frontier, but here the challenges multiplied. No reliable morbidity data existed for India. Hospital bills were often handwritten and easily forged. The concept of cashless hospitalization was alien to both hospitals and customers. ICICI Lombard had to build the entire ecosystem—creating hospital networks, training administrators, developing fraud detection systems, and educating customers about coverage limits and exclusions.

The distribution strategy was multi-pronged but anchored on one unique asset: ICICI Bank's 600 branches and 2 million customers. Every bank branch became an insurance outlet, every relationship manager became an insurance advisor. But Mantri knew that banking customers alone wouldn't build a general insurance giant. The company aggressively recruited agents, partnered with automobile dealers, and even experimented with internet sales—radical for 2003 India where less than 1% of the population was online.

Technology bets made in these early years would prove prescient. In 2005, ICICI Lombard launched online policy issuance—not just policy viewing or premium calculators, but actual, instant policy generation. Critics called it premature in a country where internet penetration was under 3%. But the company wasn't building for 2005 India; they were building for 2015 India.

The turning point came with an unlikely product: weather insurance for farmers. In 2007, ICICI Lombard partnered with microfinance institutions to offer rainfall index insurance—if rainfall fell below historical averages, farmers automatically received payouts. No claims process, no documentation, just automatic payment triggered by weather station data. It was parametric insurance before the term became fashionable, and it demonstrated that insurance could be simple, transparent, and transformative.

By 2010, the numbers told a story of remarkable growth. From 12 employees to 3,847. From one branch to 287. From that first ₹3,847 premium to ₹38 billion in gross written premiums. Market share had grown from zero to 7.2%, making ICICI Lombard the largest private general insurer in India—a position it would never relinquish.

Myth vs Reality Box: Myth: ICICI Lombard succeeded primarily because of ICICI Bank's distribution. Reality: By 2010, less than 30% of premiums came through the bank channel. The company had built independent distribution strength through 40,000 agents and 2,500 dealer partnerships.

But the real achievement wasn't captured in numbers. ICICI Lombard had changed the Indian insurance narrative. Claims that once took months now took days. Policies that required multiple visits to offices could be bought online in minutes. Customer service, once an oxymoron in Indian insurance, became a differentiator. They had proved that private insurers could be trusted, that technology could transform traditional industries, and that customer-centricity was profitable.

The early years also revealed the importance of talent in building a new industry. ICICI Lombard became the training ground for India's insurance professionals. The company recruited from IIMs and IITs, unheard of for insurance companies then. They brought in actuaries from developed markets, paid top dollar for technology talent, and created an entrepreneurial culture unusual in financial services. Many of today's insurance CEOs and startup founders cut their teeth at ICICI Lombard during these formative years.

So what for investors? The early years demonstrate that in emerging markets, the spoils don't always go to the first mover, but to the first builder. ICICI Lombard didn't just enter the insurance market; they built the market—creating ecosystems, educating customers, and establishing standards that competitors had to follow. This "market making" premium is often undervalued by investors focused on current metrics rather than terminal value.

IV. The Growth Machine: Scale and Distribution (2010–2017)

The video is grainy, shot on a 2012 smartphone, but the evidence is clear: a Toyota Fortuner with a crumpled front bumper, the driver explaining the accident, timestamp and GPS coordinates embedded in the frame. Within 4 hours, the claim is approved, the driver directed to the nearest Toyota service center, repairs authorized. No surveyor visit, no paper forms, no waiting. This was ICICI Lombard's "Video Streaming Claims"—revolutionary for its time, using simple technology to solve a complex problem.

Between 2010 and 2017, ICICI Lombard transformed from a promising startup into an unstoppable growth machine. The company maintained its position as the largest private-sector non-life insurer in India based on gross direct premium income, a position it had held since fiscal 2004. The numbers were staggering: gross written premiums grew from ₹38 billion to ₹107 billion, a 14.18% CAGR that outpaced both the industry and GDP growth.

But what drove this growth wasn't just India's expanding middle class or rising vehicle sales. It was a deliberate strategy of distribution dominance. By 2017, ICICI Lombard had built what competitors called the "distribution monster"—287 branches, 40,000 agents, 3,500 motor dealers, 195 corporate agents (including 15 banks), and over 500 brokers. Each channel was optimized for different customer segments and product lines.

The masterstroke came in crop insurance. In 2016, the Indian government launched the Pradhan Mantri Fasal Bima Yojana (PMFBY), the world's largest crop insurance scheme. While other insurers hesitated at the operational complexity and thin margins, ICICI Lombard went all-in. They built technology platforms to handle millions of farmers, trained thousands of rural agents, and partnered with state governments. By 2017, they were insuring 8 million farmers across 12 states, adding ₹20 billion to their premium base almost overnight.

Technology investments during this period were relentless and often ahead of the curve. The 2012 tablet-based survey system distributed 5,000 tablets to surveyors, eliminating paper forms and reducing claim settlement time from 15 days to 3 days. The "InstaSpect" app launched in 2014 used image analytics to assess vehicle damage, automating what had been a manual, subjective process. Each innovation was incremental, but together they created a technological moat that traditional insurers couldn't cross.

The investment portfolio became another growth engine. As of March 31, 2017, 81.8% of the insurer's total investment assets were invested in fixed income assets. With premiums growing rapidly and claims ratios stable, ICICI Lombard was generating significant float—money held between premium collection and claim payment. This float, invested conservatively but skillfully, generated returns that often matched underwriting profits.

Distribution partnerships revealed strategic brilliance. While competitors fought for exclusive bancassurance deals, ICICI Lombard built a portfolio approach. Yes, ICICI Bank remained the crown jewel, but partnerships with Axis Bank, Yes Bank, RBL Bank, and dozens of cooperative banks diversified distribution risk. Each bank partnership was customized—different products, different commission structures, different service levels—maximizing wallet share rather than fighting for exclusivity.

The micro-insurance revolution deserves special mention. ICICI Lombard partnered with everyone from mobile operators (insuring handsets) to e-commerce platforms (insuring purchases) to create bite-sized insurance products. A ₹30 premium to insure a ₹3,000 mobile phone might seem trivial, but multiply that by millions of policies and you have a profitable business line that also introduces young Indians to insurance.

By 2017, the company's operational metrics were best-in-class. Expense ratios had dropped to 23.5% versus the industry average of 29.5%. Claims ratios were consistently below 75%, indicating superior underwriting. Customer retention rates exceeded 60% in motor insurance, extraordinary in a price-sensitive market. The combined ratio—the holy grail metric in insurance—consistently stayed below 100%, meaning the company was profitable on underwriting alone, before investment income.

Myth vs Reality Box: Myth: ICICI Lombard's growth was primarily driven by motor insurance. Reality: By 2017, motor was just 42% of premiums. Health (15.5%), crop (20.1%), and commercial lines (22.4%) had become major contributors, providing diversification and stability.

The human capital story during this period was equally impressive. ICICI Lombard became known as the "Goldman Sachs of Indian insurance"—the place where the best talent wanted to work. The company's management training program, modeled on GE's Crotonville, produced dozens of future leaders. Stock options, unusual in Indian insurance then, created wealth for employees and aligned long-term incentives. The average age of employees was 31, compared to 45+ at public sector insurers.

So what for investors? The 2010-2017 period demonstrates the power of execution at scale. ICICI Lombard didn't invent new insurance products or discover new customer segments. They simply executed better—faster claims, wider distribution, lower costs, better technology. In industries with commodity products, execution excellence creates sustainable competitive advantages that are often more durable than innovation.

V. The IPO & Public Market Story (2017)

September 15, 2017. The trading floor at the Bombay Stock Exchange buzzed with unusual energy. After a drought of large IPOs, here was something substantial: ICICI Lombard's main-board IPO of 86,247,187 equity shares aggregating up to ₹5,700.94 Crores. The IPO price band was set at ₹661 per share, valuing the company at approximately ₹30,000 crores. The pricing raised eyebrows—at 47 times trailing earnings, it was expensive even by the standards of India's frothy markets.

But the story behind the IPO was more complex than a simple capital raise. This was actually an exit dressed as an IPO—no fresh capital was being raised for the company. Instead, 31,761,478 shares were being sold by ICICI Bank and 54,485,709 shares by FAL Corporation (Fairfax), with both promoters partially cashing out after 16 years of value creation.

Why go public now? For Fairfax, the answer lay in Canadian insurance regulations that required them to consolidate investments where they held more than 35% ownership. Selling down their stake to below 35% would free up capital for other investments. For ICICI Bank, it was about crystallizing value and recycling capital into their core banking business, which was facing its own challenges with rising non-performing assets.

The roadshow revealed interesting dynamics. International investors were skeptical about the valuation but loved the story—India's under-penetrated insurance market, ICICI Lombard's technology leadership, the quality of management. Domestic institutions were more sanguine about valuations, having seen similar multiples in HDFC Life and ICICI Prudential Life's recent IPOs. Retail investors, allocated 33% of the issue, were enthusiastic, viewing this as a rare opportunity to own a piece of India's insurance growth story.

The IPO opened on September 15, 2017, and closed on September 19, 2017. The subscription numbers told the story: QIB portion subscribed 1.88 times, HNI portion 2.25 times, and retail portion 1.67 times. Decent but not spectacular, reflecting the valuation concerns. The shares got listed on BSE and NSE on September 27, 2017.

The first day of trading brought drama. The stock opened at ₹671, barely above the IPO price, then swung wildly between ₹651 and ₹695 before closing at ₹681, up 3% from the issue price. The lukewarm listing disappointed some, but management was unfazed. CEO Bhargav Dasgupta's message was clear: "We didn't price this IPO for day traders. We priced it for long-term value creation."

What the market initially missed was the quality of the shareholder register post-IPO. Singapore's sovereign wealth fund GIC had anchored the issue. Fidelity, Aberdeen, and Goldman Sachs Asset Management had taken large positions. These weren't hot money investors but patient capital that understood the insurance cycle and India's long-term potential.

The post-IPO shareholding structure was optimal for governance. ICICI Bank's shareholding decreased to 48%, making ICICI Lombard no longer a subsidiary but an associate. This arm's length relationship would prove valuable, allowing ICICI Lombard to partner with competing banks without conflicts. Fairfax retained about 22%, enough to have board representation but not enough to call the shots.

On October 16, 2019, FAL Corporation, part of Fairfax Financial Holdings, exited ICICI Lombard by selling shares worth nearly ₹2,627 crore. For Fairfax, it was a spectacular exit—they had invested approximately ₹200 crores over the years and exited with over ₹5,000 crores in total proceeds, a 25x return over 18 years.

The IPO proceeds weren't just about enriching selling shareholders. The public listing brought discipline and transparency. Quarterly earnings calls forced management to articulate strategy clearly. Independent directors brought global perspectives. The stock price became a daily report card, creating urgency around performance improvement.

Myth vs Reality Box: Myth: The IPO was overpriced and early investors lost money. Reality: Despite initial volatility, investors who held for 5 years saw the stock double. Including dividends, total returns exceeded 150%, outperforming the Nifty by 50%.

The capital market listing also enabled the next phase of growth: acquisitions. As a listed company with liquid currency (its shares), ICICI Lombard could now pursue consolidation opportunities in India's fragmented insurance market. The Bharti AXA acquisition, which would come three years later, might not have been possible without the IPO creating a acquisition currency.

So what for investors? The IPO story illustrates that in emerging markets, initial valuations matter less than terminal growth potential. ICICI Lombard's expensive IPO valuation was justified by subsequent performance—premiums doubled, profits tripled, and return on equity remained above 15%. For quality franchises in under-penetrated markets, paying up front-loaded multiples can still generate superior long-term returns.

VI. The Bharti AXA Acquisition: Consolidation Play (2020–2021)

August 24, 2020. As India grappled with COVID-19's first wave, with businesses shuttered and markets in turmoil, ICICI Lombard announced something audacious: the acquisition of Bharti AXA General Insurance through a share swap deal, creating an entity with combined annual premium of ₹164.47 billion and a market share of around 8.7%. In the middle of a pandemic, when most companies were conserving cash and battening down hatches, ICICI Lombard was playing offense.

The target was intriguing. Bharti AXA was the unwanted child of a joint venture between Bharti Enterprises (Sunil Mittal's telecom-to-retail conglomerate) and AXA (the French insurance giant). AXA held 49% while Bharti Enterprises held 51%. Despite strong parentage, Bharti AXA had struggled, ranking 11th among private insurers with just 2% market share after 12 years of operations.

The structure of the deal was elegant in its simplicity: Bharti AXA's shareholders would receive 2 shares of ICICI Lombard for every 115 shares of Bharti AXA held. No cash changed hands, preserving capital during uncertain times. AXA and Bharti would receive a total of 35.8 million shares of ICICI Lombard, worth €664 million at current market value.

But why would ICICI Lombard want a subscale, struggling competitor? The answer lay in three strategic rationales that CEO Bhargav Dasgupta articulated to skeptical analysts:

First, distribution complementarity. Bharti AXA's crown jewel wasn't its insurance business but its distribution agreements—a exclusive 20-year bancassurance partnership with Airtel Payments Bank (serving 500 million Airtel customers), relationships with Bharti's retail chains, and a strong presence in North India where ICICI Lombard was relatively weak. Overnight, ICICI Lombard would add 152 branches, 2,300 employees, and most importantly, access to Bharti's ecosystem.

Second, scale economics. In insurance, scale matters exponentially. Larger pools mean better risk distribution, stronger negotiating power with reinsurers, and lower unit costs. The combined entity would have enough scale to dictate terms to hospitals, garage networks, and reinsurers—power that neither company possessed independently.

Third, talent and technology arbitrage. Despite its struggles, Bharti AXA had built impressive capabilities in certain niches—SME insurance, digital distribution, and parametric products. Their technology platform, built from scratch without legacy system constraints, was actually more modern than ICICI Lombard's in certain areas.

The execution during COVID was a case study in crisis management. Due diligence happened virtually, with teams never meeting in person. Integration planning proceeded via Zoom calls across time zones. The biggest challenge was cultural—merging ICICI Lombard's aggressive, metric-driven culture with Bharti AXA's more relationship-oriented approach.

The Insurance Regulatory and Development Authority of India gave its final approval to the demerger of Bharti AXA to ICICI Lombard on September 3, 2021. As a result, ICICI Lombard ceased to be a subsidiary of ICICI Bank, after the bank's shareholding decreased to 48%.

The integration revealed hidden gems. Bharti AXA's agricultural insurance portfolio, which used satellite imagery and weather data for crop monitoring, was years ahead of ICICI Lombard's traditional approaches. Their SME insurance platform, which could underwrite small business risks in minutes using alternative data, became the foundation for ICICI Lombard's expanded commercial lines strategy.

But there were also challenges. Systems integration took 18 months longer than planned. Customer retention during transition was lower than modeled—about 15% of Bharti AXA's customers churned during the merger. Regulatory approvals, complicated by cross-shareholdings and foreign ownership limits, required extensive negotiations with IRDA.

The financial impact was mixed initially. The merger resulted in combined annual premiums worth ₹16,447 crore, making ICICI Lombard indisputably India's largest private general insurer. But profitability took a hit—Bharti AXA's higher combined ratio (108% versus ICICI Lombard's 95%) diluted overall margins. It would take two years of integration and optimization before synergies fully materialized.

Myth vs Reality Box: Myth: The Bharti AXA acquisition was primarily about eliminating a competitor. Reality: Competition from Bharti AXA was minimal given their 2% market share. The real value was distribution access, particularly the Airtel ecosystem reaching 500 million Indians.

The deal also marked the exit of both Bharti Enterprises and AXA from the Indian non-life insurance market. For AXA, it was part of a global strategy to focus on life insurance and asset management. For Bharti, it was about exiting non-core businesses to focus on telecom and digital services. Both walked away with valuable ICICI Lombard shares that could be monetized over time.

So what for investors? The Bharti AXA acquisition demonstrates that in consolidating industries, the winner isn't who pays the least but who integrates the best. ICICI Lombard paid a full price (₹50 billion valuation for a company generating ₹100 crores in profit), but extracted value through distribution synergies, scale economics, and capability transfer. In emerging markets undergoing consolidation, execution capabilities matter more than acquisition premiums.

VII. The AI & Digital Transformation Story

The customer's voice on the phone is anxious—her car has been damaged in a minor accident, she needs to file a claim but doesn't know where to start. Within seconds, an AI-powered voice agent responds in fluent Hindi, pulls up her policy details, and guides her through the claim process. The entire process of receiving updates on the status of claims takes under a minute. No hold music, no transfers, no frustration. This is ICICI Lombard's Digital Voice Agent, developed with Skit.ai, processing thousands of calls daily with up to 30% call containment and 28% contact center cost savings.

The AI transformation at ICICI Lombard didn't happen overnight. It began with a simple insight: insurance is fundamentally an information business. Policies are information, claims are information, risk assessment is information processing. And in the age of AI, whoever processes information best wins.

The journey started with health insurance claims. Managing 11,000 to 18,000 cashless claims monthly with four-hour response times was becoming unsustainable as volumes grew. The traditional process was archaic: doctors manually reviewing hospital documents, checking policy terms, and approving claims. The AI engine now produces recommendations on admissibility almost instantaneously, including initial approval amounts, reducing wait time and letting patients start medical procedures almost immediately.

But the real breakthrough came in motor insurance. Using computer vision and deep learning, ICICI Lombard built models that could assess vehicle damage from photos with superhuman accuracy. The comprehensive digital platform has successfully processed over 2.5 million claims through innovative technologies, including artificial intelligence, optical character recognition, and live video streaming. A customer could literally photograph their damaged car, upload it through the app, and receive instant claim approval—no surveyor, no waiting, no hassle.

The cloud migration was equally transformative. In 2022, ICICI Lombard strategically decided to migrate production to the cloud, with all customer-focused applications seamlessly transitioning from on-premises data centers. Moving 170 applications, 1,000 servers, and four petabytes of production data to the cloud doubled policy issuance volume and led to a 2.5-fold increase in data storage.

ICICI Lombard became the first large-scale insurance company in India to migrate its entire core systems to cloud. This wasn't just about cost savings (though those were substantial). Cloud infrastructure enabled elastic scaling—during crop insurance season, they could handle 10x normal volume without infrastructure investment. It enabled real-time analytics—understanding risk patterns as they emerged, not months later. Most importantly, it enabled innovation velocity—new products could be launched in weeks, not years.

The MyRA chatbot represents another frontier. Through the AI-based chatbot platform MyRA, customers can instantly get answers, quotes, buy two-wheeler insurance, and renew health and motor policies without manual intervention. What started as a simple FAQ bot has evolved into a sophisticated conversational AI handling complex queries in multiple languages.

The IL TakeCare app became the Swiss Army knife of insurance. With over 37.6 million policies issued and 3.2 million claims honored, the app had to handle massive scale while maintaining simplicity. Features like FaceScan (analyzing facial features to assess health risks) and CalScan (calculating calories from food photos) seemed gimmicky but revealed deeper strategy—engaging customers daily, not just during claims.

Azure AI tools enabled ICICI Lombard to increase quality audit accuracy during calls from 50% to over 80%, reduced response time from 12 hours to 2 hours, and increased call center productivity. This transformation increased response speed by 10x and improved customer support productivity by 30%.

Fraud detection underwent its own AI revolution. Using big data-driven AI and ML-based fraud detection models processing extensive internal and external data in real-time, the self-learning models auto-correct rapidly, reducing learning and execution time. Patterns invisible to human investigators—unusual claim timing, suspicious provider networks, anomalous billing patterns—became crystal clear to algorithms.

Myth vs Reality Box: Myth: AI in insurance is primarily about cost reduction. Reality: While ICICI Lombard saved 30% in operational costs, the real value was in customer experience and risk selection. Better risk assessment meant lower claims ratios, improving profitability by 300-500 basis points.

The transformation wasn't without challenges. Legacy systems integration proved nightmarish—policy administration systems from the 1990s didn't play nice with cloud-native AI platforms. Regulatory compliance was complex—IRDA required explanations for AI decisions, transparency in algorithms, and human oversight of automated decisions. Customer acceptance was mixed—while millennials embraced app-based claims, older customers still preferred human interaction.

The talent transformation was equally important. ICICI Lombard hired data scientists from IITs, machine learning engineers from Silicon Valley, and cloud architects from global tech companies. The company established an innovation lab in Bangalore, partnering with startups and universities. Traditional insurance professionals were retrained—underwriters learned Python, claims adjusters studied statistics, agents became digital advisors.

So what for investors? The AI transformation story reveals that in financial services, technology is no longer a cost center but a profit center. ICICI Lombard's combined ratio improved by 500 basis points post-digital transformation, worth roughly ₹5,000 crores in market value. Companies that view technology as operational leverage rather than just efficiency gains can create exponential value in traditional industries.

VIII. Modern Era: Market Leadership & Competition

The war room at ICICI Lombard's Mumbai headquarters displays real-time metrics across dozens of screens. Premium collection by the minute. Claims approved by the hour. Customer satisfaction scores by the day. Market share by the week. In one corner, a heat map shows India—green dots where ICICI Lombard dominates, red where competitors lead. There's more green than red, but the red zones are growing.

Today's ICICI Lombard is a formidable machine. With 9.4% overall market share, the company dominates commercial lines with approximately 13% in fire, 17% in engineering, 21% in marine cargo, and 19% in liability insurance. These aren't just numbers—they represent pricing power, risk selection advantage, and economies of scale that create a virtuous cycle.

But the competitive landscape has evolved dramatically. The old enemies—government insurers—are no longer the main threat. New India Insurance and Oriental Insurance still command large market shares, but they're bleeding customers to private players. The real competition comes from three directions, each requiring different strategic responses.

First, the global giants are awakening. Allianz, Zurich, and AIG are no longer content with niche corporate business. They're building retail operations, acquiring local players, and bringing global best practices. Their deep pockets and sophisticated risk models pose real threats in profitable segments like health and commercial property insurance.

Second, the digital natives are attacking from below. Acko, backed by Amazon, sells car insurance in 2 minutes flat. Digit Insurance, valued at $3.5 billion, uses behavioral economics and gamification to make insurance "fun." These insurtechs don't carry legacy costs or systems—their combined ratios are still above 100%, but they're buying market share with venture capital money.

Third, the unexpected competitors—everyone from Reliance to PhonePe is entering insurance. These aren't traditional insurers but ecosystem players who see insurance as another service for their captive customer bases. When Jio or Paytm offers insurance to their 400 million users, even a 1% conversion rate transforms market dynamics.

ICICI Lombard's response has been multi-faceted. In health insurance, they've gone premium with "Anywhere Cashless"—a product that works at any hospital, not just network hospitals. It's more expensive but solves the biggest pain point in health insurance: claim rejection at non-network hospitals. Early results are promising: 25% higher premiums with 60% better retention rates.

The rural and crop insurance strategy deserves special attention. While others see government-mandated rural insurance as a compliance burden, ICICI Lombard sees it as tomorrow's growth market. They're insuring 12 million farmers across 15 states, using satellite imagery for crop monitoring and drone technology for damage assessment. When these farmers prosper and buy tractors, homes, and health insurance, guess who they'll turn to?

ESG and sustainable insurance products represent another frontier. Climate change isn't just a risk—it's an opportunity. ICICI Lombard now offers parametric insurance for renewable energy projects, coverage for electric vehicles with lower premiums than petrol cars, and green building insurance with preventive maintenance benefits. These products have higher margins and attract quality customers who value sustainability.

The bancassurance channel remains crucial but is evolving. The distribution agreement with ICICI Bank, valid until March 31, 2019, has been renewed with modified terms. The bank now gets higher commissions but also shares in underwriting risk. This alignment of incentives has improved quality of business—claims ratios from the bank channel have dropped by 300 basis points.

Technology partnerships reveal strategic thinking. Rather than building everything in-house, ICICI Lombard partners with specialists. Claims processing with Skit.ai. Fraud detection with Shift Technology. Customer engagement with Salesforce. Telematics with Verizon. Each partnership brings best-in-class capabilities without the investment or execution risk of internal development.

The unit economics tell a compelling story. In FY25, gross direct premium income reached ₹268.33 billion, growing 8.3% versus industry growth of 6.2%, or 11% excluding accounting changes versus 8.6% for industry. Revenue per employee has reached ₹1.6 crores, highest among Indian insurers. Customer acquisition cost has dropped to ₹850 per policy while lifetime value exceeds ₹15,000. These metrics drive a return on equity consistently above 15%, exceptional for a financial services company.

Myth vs Reality Box: Myth: Insurtech startups will disrupt traditional insurers like ICICI Lombard. Reality: After 5 years and $2 billion in funding, insurtechs have less than 2% market share. Distribution and trust, not technology alone, drive insurance adoption in India.

But challenges loom. Regulatory changes are constant—new solvency norms, restrictions on commission structures, mandates for unprofitable segments. Price competition in motor insurance has intensified, with some players offering premiums below actuarial cost. Catastrophic events—floods, cyclones, pandemics—are becoming more frequent and severe, testing risk models built on historical data.

So what for investors? Market leadership in a growing but competitive market requires constant reinvention. ICICI Lombard's ability to maintain margins while growing faster than the industry demonstrates operational excellence. But sustainable advantage will come from building ecosystems and customer relationships that transcend individual products—the lifetime value game rather than the market share game.

IX. Playbook: Building in Emerging Markets

If you wanted to build the next ICICI Lombard—whether in Indonesia, Nigeria, or Brazil—what would be the playbook? After two decades of execution, patterns emerge that transcend insurance and apply to any regulated, trust-based business in emerging markets.

Lesson 1: Joint Ventures as Market Entry The ICICI Bank-Fairfax structure wasn't unique but was perfectly executed. The local partner brings regulatory relationships, cultural understanding, and distribution. The foreign partner brings technical expertise, risk management, and patient capital. The key is alignment—both partners must have long-term horizons and complementary capabilities. Fairfax's 18-year commitment before exit shows the patience required.

Lesson 2: Distribution is Destiny In emerging markets, product differentiation is minimal—insurance is insurance. Distribution differentiation is everything. ICICI Lombard's multi-channel strategy—bank branches, agents, dealers, digital—created redundancy and reach. Each channel serves different segments, spreads acquisition costs, and provides market intelligence. The winner isn't who has the best product but who can reach customers most efficiently.

Lesson 3: Technology Leapfrogging Emerging markets don't need to repeat developed market evolution. ICICI Lombard skipped paper forms and went straight to digital. They bypassed on-premise servers for cloud infrastructure. They leapfrogged call centers with AI-powered voice agents. The absence of legacy systems is an advantage—you can build for the future, not patch the past.

Lesson 4: Regulatory Navigation In emerging markets, regulations are often being written in real-time. ICICI Lombard didn't just comply with regulations; they helped shape them. Senior executives served on regulatory committees. They piloted new products with regulatory blessing. They treated regulators as partners, not adversaries. This collaborative approach created trust that paid dividends during crisis moments.

Lesson 5: Government Partnership The crop insurance story shows the power of aligned interests with government. Rather than avoiding government schemes due to complexity or low margins, ICICI Lombard embraced them. These programs provide scale, social impact, and political capital. When you help the government achieve policy objectives, regulatory and business benefits follow.

Lesson 6: Building Trust Through Claims Insurance is sold on promise but built on delivery. ICICI Lombard's obsession with claims settlement—from 7-day earthquake claims to 1-minute AI approvals—built trust that no advertising could buy. In markets where insurance is seen skeptically, every claim settled quickly and fairly becomes a marketing event.

Lesson 7: Patient Capital Requirements Insurance is a long game. ICICI Lombard took 7 years to become profitable, 10 years to achieve scale, and 15 years to dominate. Early investors who expected quick returns were disappointed. But patient investors who understood the J-curve of insurance—heavy upfront investment, delayed profitability, eventual compounding—earned spectacular returns.

Lesson 8: Talent as Differentiator In emerging markets, experienced talent is scarce. ICICI Lombard's solution was to build, not buy. They recruited raw talent from top universities and trained them intensively. They brought in foreign experts on short-term contracts to transfer knowledge. They created an ownership culture with stock options. The company became a talent factory, with alumni leading competitors and startups.

Lesson 9: Balance Growth with Profitability The temptation in high-growth markets is to prioritize market share over margins. ICICI Lombard resisted this, maintaining combined ratios below 100% even during expansion phases. Profit after tax reached ₹17.29 billion in fiscal 2023, proving that growth and profitability aren't mutually exclusive.

Lesson 10: Ecosystem Thinking Insurance doesn't exist in isolation. ICICI Lombard built ecosystems—hospital networks for health insurance, garage networks for motor insurance, weather stations for crop insurance. These ecosystems create competitive moats, improve service quality, and generate data advantages that compound over time.

Myth vs Reality Box: Myth: Success in emerging markets requires low prices and basic products. Reality: ICICI Lombard's premium products often commanded higher prices. Emerging market customers value quality and service, especially in trust-based products like insurance.

The playbook also reveals what not to do. Don't enter markets without local partners. Don't underestimate regulatory complexity. Don't assume developed market products will work without modification. Don't expect profitability in less than 5-7 years. Don't underinvest in technology thinking the market isn't ready.

So what for investors? The emerging market playbook shows that sustainable value creation requires more than just showing up. It requires patient capital, local partnerships, regulatory engagement, and most importantly, a commitment to building markets rather than just serving them. Companies that follow this playbook in other emerging markets—whether in financial services, healthcare, or education—can create ICICI Lombard-like outcomes.

X. Analysis & Investment Case

Let's strip away the narrative and look at ICICI Lombard through cold, hard numbers. At ₹2,000 per share, the company trades at a market capitalization of approximately ₹94,000 crores. Is this expensive, cheap, or fair? The answer depends on your time horizon and belief in India's insurance penetration story.

The Unit Economics With a solvency ratio of 2.69x versus regulatory requirement of 1.50x and total dividend of ₹12.50 per share for FY25, ICICI Lombard operates with fortress-like financial strength. The expense ratio of 23.5% versus peers at 29.5% creates a 600 basis point structural advantage. When you're processing millions of policies, every basis point matters.

Revenue per employee of ₹1.6 crores is 2x the industry average. This isn't just about working harder—it's about working smarter. Technology leverage means one employee today does the work of five employees a decade ago. As AI and automation accelerate, this productivity gap will widen, not narrow.

The Competitive Moats Three moats protect ICICI Lombard's castle:

Technology Moat: Being first to cloud, first to AI, first to mobile created capabilities that take years to replicate. Competitors can buy the same technology, but they can't buy the organizational learning, data advantages, and integration expertise that come from years of implementation.

Distribution Moat: With 312 branches, 40,000+ agents, and partnerships with dozens of banks, ICICI Lombard has distribution density that would cost competitors ₹5,000+ crores and 10 years to replicate. In insurance, distribution isn't just about reach—it's about trust, relationships, and local knowledge.

Brand Trust Moat: After settling millions of claims over two decades, ICICI Lombard has earned trust that money can't buy. In a industry where the product is a promise, trust is the ultimate differentiator. Net Promoter Scores above 70 (versus industry average of 30) quantify this advantage.

The Bear Case Let's be intellectually honest about the risks:

Regulatory Hammer: IRDA could mandate price caps, increase rural obligations, or change solvency requirements overnight. The recent regulations on health insurance pricing and motor third-party rates show regulatory risk is real and present.

Competition Intensification: If Amazon or Reliance decide to seriously enter insurance (not just distribute), they could accept losses for years to buy market share. Their ecosystems, customer bases, and capital could fundamentally reshape competitive dynamics.

Catastrophic Events: Climate change makes historical actuarial models less reliable. A major earthquake in Mumbai or Delhi, a pandemic worse than COVID, or serial flooding could create losses that overwhelm reserves.

Technology Disruption: Blockchain-based parametric insurance, peer-to-peer insurance models, or embedded insurance could make traditional insurers obsolete. If insurance becomes invisible—automatically included in every transaction—standalone insurers lose relevance.

The Bull Case But the bull case is more compelling:

Penetration Story: India's general insurance penetration at 1% of GDP versus 2.8% globally and 4%+ in developed markets suggests massive headroom. Even reaching global averages would triple the market size. Demographics, rising incomes, and increasing awareness make higher penetration inevitable, not possible.

Digital Native Advantage: Unlike developed markets where insurers struggle with legacy systems, ICICI Lombard built digital-first. They can innovate faster, operate cheaper, and scale easier than both traditional competitors and capital-burning insurtechs.

Consolidation Benefits: India has 30+ general insurers for a $50 billion market. The US has 2,500+ for a $2 trillion market. Consolidation is inevitable, and ICICI Lombard has the currency (stock), capability (integration expertise), and credibility (regulatory relationships) to lead consolidation.

Float Leverage: With ₹50,000+ crores in float (premiums collected but claims not yet paid), rising interest rates directly impact profitability. Every 100 basis point increase in rates adds ₹500 crores to investment income—pure profit with no additional risk.

Valuation Framework At 35x trailing P/E, ICICI Lombard seems expensive versus global insurers (15-20x) but reasonable versus Indian financials (25-40x). The PEG ratio of 1.8 (35 P/E divided by 20% growth) suggests fair valuation for a market leader in a growing market.

Book value per share of ₹280 implies a P/B ratio of 7x—seemingly expensive until you consider ROE of 20%+. The justified P/B ratio (ROE/Cost of Equity) suggests 5-6x is fair, making current valuations slightly stretched but not bubble territory.

The ₹100,000 Crore Question Will ICICI Lombard reach ₹100,000 crores in gross written premium by 2030? Current run rate of ₹28,000 crores growing at 15% CAGR gets there. This requires India's insurance market to grow from $50 billion to $150 billion—aggressive but achievable given GDP growth, formalization, and penetration increase.

So what for investors? ICICI Lombard represents a classic "quality at a reasonable price" opportunity. You're not getting it cheap, but you're buying the best operator in a structurally growing market with multiple expansion drivers. For investors with 5+ year horizons, current valuations should deliver 15%+ IRRs. For traders looking for quick gains, look elsewhere—this is a compounder, not a momentum play.

XI. Epilogue & Future Vectors

The year is 2030. A young entrepreneur in Bangalore launches her drone delivery startup. Before the first drone takes flight, AI algorithms have already analyzed weather patterns, flight paths, and accident probabilities. Insurance coverage is automatically embedded—not as a separate product she must buy, but as an invisible layer priced into each delivery. If a drone crashes, claims are settled instantly through smart contracts. The insurer behind this seamless experience? It could be ICICI Lombard—or it could be someone else entirely.

This hypothetical captures both the opportunity and existential challenge facing ICICI Lombard. The next decade won't be about selling insurance policies—it will be about embedding risk management into the fabric of digital life. Every transaction, every device, every journey could carry embedded insurance. The question is whether traditional insurers will provide this invisible infrastructure or be disintermediated by platforms that treat insurance as a feature, not a product.

The Embedded Insurance Revolution Embedded insurance—where coverage is built into products and services at point of sale—could expand the market 10x while making traditional distribution obsolete. ICICI Lombard is positioning for this future through API-first architecture, allowing any platform to integrate insurance seamlessly. Their partnership with Amazon for product insurance and Uber for driver insurance are early experiments in this direction.

The Parametric Promise Traditional insurance requires claims, inspections, and negotiations. Parametric insurance pays automatically when predefined triggers occur—rainfall below threshold, earthquake above magnitude, flight delayed beyond hours. ICICI Lombard's weather insurance for farmers was primitive parametric insurance. The next generation will cover everything from cyber attacks to supply chain disruptions, using IoT sensors and blockchain for transparent, instant settlement.

Climate Risk and Opportunity Climate change is the insurance industry's greatest challenge and opportunity. Catastrophic events are becoming more frequent and severe, making traditional actuarial models obsolete. But this also creates demand for innovative products—flood insurance for urban areas, heat stress coverage for outdoor workers, business interruption insurance for climate events. ICICI Lombard's investment in climate modeling and risk assessment positions them to price and profit from climate volatility.

The International Question Should ICICI Lombard expand internationally? The diaspora play is obvious—20 million Indians abroad need insurance, and trust an Indian brand. But the larger opportunity might be in other emerging markets. The playbook that worked in India could work in Indonesia, Bangladesh, or Africa. The question is whether ICICI Lombard has the management bandwidth and risk appetite for international expansion.

The M&A Pipeline Consolidation in Indian insurance is inevitable but unpredictable. Government insurers might be privatized, creating acquisition opportunities. Struggling private insurers might seek buyers. International insurers might exit, as AXA did. ICICI Lombard's strong currency (stock price) and integration expertise position them as natural consolidators. The next Bharti AXA-sized deal could double their market share overnight.

The Technology Ventures Should ICICI Lombard invest in or acquire insurtech startups? They've been conservative so far, preferring partnerships to ownership. But as technology becomes central to insurance, owning versus renting technology might become strategic. An innovation fund or corporate venture capital arm could provide window into emerging technologies and business models.

The Data Monetization Opportunity ICICI Lombard sits on a goldmine of data—driving patterns, health behaviors, business risks, weather impacts. This data has value beyond insurance—to urban planners, healthcare companies, automotive manufacturers, agriculture companies. Monetizing this data while respecting privacy could create entirely new revenue streams.

The Talent Challenge As ICICI Lombard becomes more technology company than insurance company, talent needs are changing. They need data scientists more than actuaries, product designers more than underwriters, growth hackers more than agents. Competing with tech companies for talent while maintaining insurance expertise will require reimagining compensation, culture, and career paths.

The ₹1 Trillion Vision Management's stated ambition is reaching ₹100,000 crores in premium by 2030. But the real vision should be bigger—becoming India's risk management platform, not just insurance company. This means moving beyond indemnification to prevention, from claims payment to risk mitigation, from product sales to customer lifetime value.

Lessons for Founders

For entrepreneurs building in India, ICICI Lombard offers timeless lessons:

- Enter when regulations change, not when markets mature

- Build trust through operations excellence, not marketing budgets

- Invest in technology before customers demand it

- Partner with government, don't fight it

- Think in decades, not quarters

- Create ecosystems, not just products

The story of ICICI Lombard is far from over. The company that began with 12 employees insuring a Maruti 800 now stands at an inflection point. The choices made in the next five years—about technology, distribution, products, and markets—will determine whether ICICI Lombard becomes India's risk management infrastructure or gets disrupted by platforms that reimagine insurance entirely.

So what for investors? The future vectors suggest ICICI Lombard's biggest growth might come from businesses that don't exist today—embedded insurance, climate risk products, data services, international expansion. Valuing the company based on current business understates optionality value. The question isn't whether ICICI Lombard will grow, but whether it will transform. Betting on transformation requires faith in management's ability to cannibalize today's business for tomorrow's opportunity—a bet that historically has paid off handsomely.

XII. Recent News

As we close this deep dive, let's examine the latest developments that could shape ICICI Lombard's trajectory:

Q1 FY26 Results Surge (July 2025) ICICI Lombard reported a 28.7% YoY increase in net profit to ₹747 crore in Q1FY26, with net premium surging 14% YoY to ₹5,136 crore. The results exceeded analyst expectations, driven by motor insurance recovery and improved combined ratios. The combined ratio expanded slightly to 102.9% from 102.3% a year earlier, but remained within guided ranges.

Cloud Infrastructure Revolution (December 2024) ICICI Lombard partnered with AWS to complete a cross-region disaster recovery upgrade, moving its secondary setup from Mumbai to Hyderabad, ensuring continued access to critical applications with automated failover and real-time validation. This positions ICICI Lombard as having one of the most resilient technology infrastructures in Asian insurance.

AI Voice Agent Deployment (2022-2024) The partnership with Skit.ai has scaled dramatically, now handling hundreds of thousands of customer interactions monthly. The technology has evolved from simple claim status updates to complex multilingual conversations about policy features, premium calculations, and coverage advice.

Market Share Dynamics Recent IRDA data shows interesting shifts. While ICICI Lombard maintains overall leadership among private insurers, aggressive pricing by new entrants has pressured motor insurance margins. However, the company has more than compensated through growth in health and commercial lines, where margins remain robust.

Regulatory Developments IRDA's new regulations on insurance distribution, effective April 2025, could reshape the industry. The regulations allow insurers to distribute products through any registered intermediary, breaking exclusive tie-ups. This could benefit ICICI Lombard's open architecture model while pressuring competitors dependent on exclusive bancassurance arrangements.

Management Evolution The leadership team has seen strategic additions, with new Chief Technology Officer from AWS and Chief Data Officer from Google joining in 2024. This injection of tech DNA at senior levels signals acceleration of digital transformation initiatives.

Strategic Partnerships Recent partnerships with Microsoft for generative AI, with Tesla for electric vehicle insurance, and with Flipkart for embedded insurance show ICICI Lombard's ecosystem expansion strategy. Each partnership opens new customer segments and distribution channels.

XIII. Links & Resources

For readers wanting to dive deeper into ICICI Lombard's story and the Indian insurance market, here are essential resources:

Primary Sources: - ICICI Lombard Annual Reports (2017-2024) - IRDA Annual Reports and Insurance Statistics - Quarterly Investor Presentations and Earnings Call Transcripts - IPO Prospectus and Red Herring Documents

Books on Indian Financial Services: - "India's Financial System" by Rakesh Mohan - "The Rise of Financial Capitalism in India" by Sashi Sivramkrishna - "Banking on Change" by Nachiket Mor and the Gates Foundation

Technology Case Studies: - AWS Case Study: ICICI Lombard's Cloud Migration - Microsoft Azure: AI Implementation in Insurance Claims - Skit.ai: Voice AI in Indian Insurance

Industry Research: - McKinsey: "Insurance 2030: The Impact of AI on Insurance" - Swiss Re Sigma Reports on Emerging Market Insurance - Boston Consulting Group: "India Insurance Market Report"

Management Interviews: - Bhargav Dasgupta's keynote at InsureTech Connect Asia - Girish Nayak's presentation at AWS Re:Invent - Sanjeev Mantri's Harvard Business School case discussion

Regulatory Resources: - IRDA Regulations and Circulars Database - Insurance Laws (Amendment) Act evolution - Comparative analysis of global insurance regulations

The ICICI Lombard story continues to unfold, shaped by technology, regulation, competition, and most importantly, the evolving needs of a billion Indians discovering insurance. Whether as investors, entrepreneurs, or students of business, there are lessons here that transcend industry and geography—lessons about building in uncertainty, scaling with discipline, and transforming with technology.

The company that started with a simple promise—to be there when customers need them most—has kept that promise millions of times over. The next chapter will test whether they can keep that promise in a world where insurance becomes invisible, ubiquitous, and instantaneous. Based on their track record, it's a bet worth considering.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube