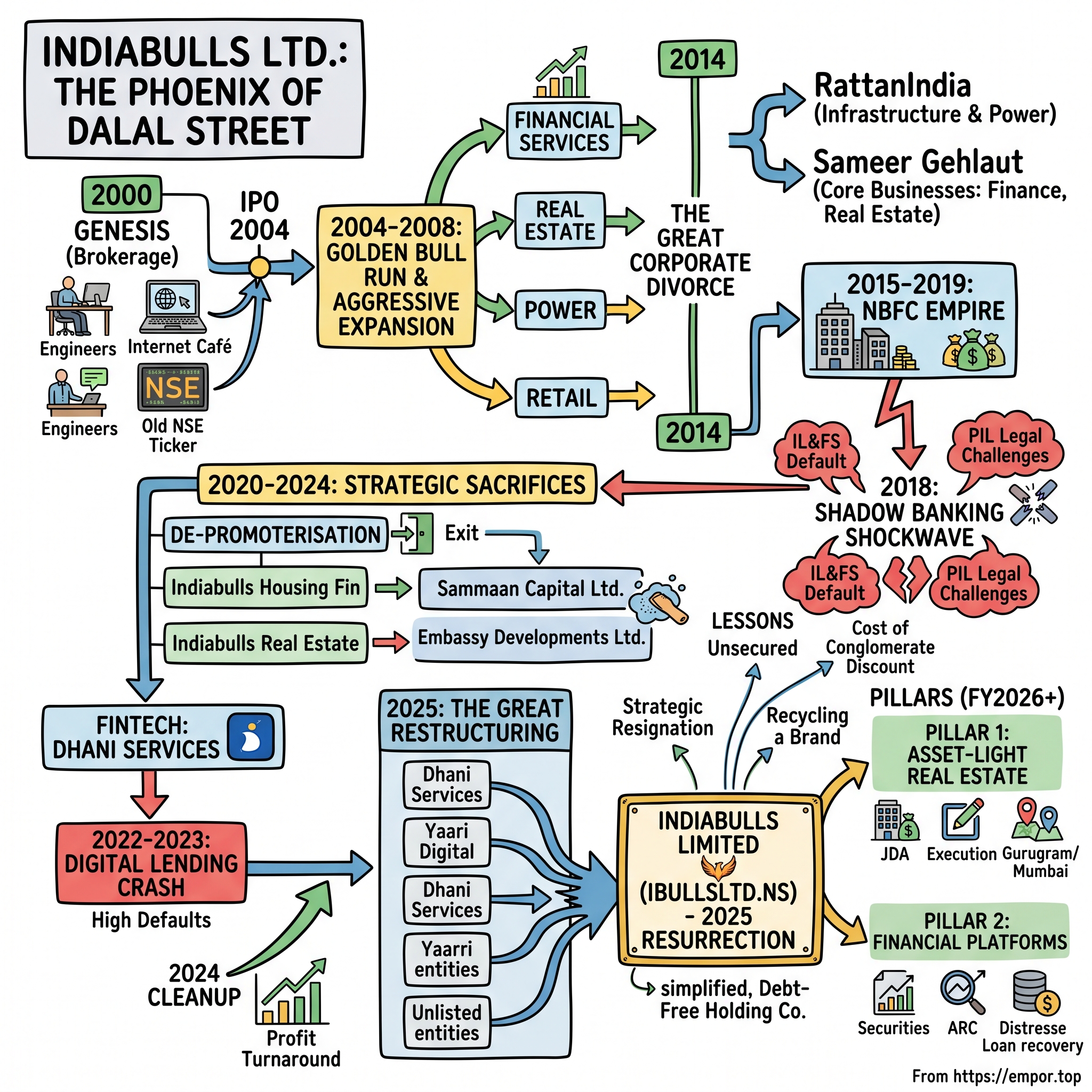

Indiabulls Ltd.: The Phoenix of Dalal Street

There is a peculiar kind of ghost that haunts Indian capital markets: the brand that outlives the company. In the mid-2000s, "Indiabulls" was not a name so much as a mood — the roar of a leveraged, ambitious, slightly reckless new India that had discovered it could borrow against tomorrow to buy today. It built skyscrapers on the bones of dead textile mills, lent home loans to a swelling middle class, and printed money in a bull market that felt like it would never end. Then the tide went out. And when it did, the name did not die so much as scatter — into a housing lender that would eventually erase the word "Indiabulls" from its logo, into a real-estate developer that would be absorbed by a rival, into a power company that ran off with a different family, and into a fintech app that burned through cash chasing India's most dangerous borrowers.

And yet, in the autumn of 2025, the name came home.

I. Introduction & Episode Roadmap

Ask an investor in 2026 to find the original Indiabulls giants, and they will send you on a scavenger hunt. Indiabulls Housing Finance — once India's second-largest private mortgage lender — now trades as Sammaan Capital Limited, a Hindi word meaning "respect" or "dignity," a deliberate act of reputational cleansing.1 Indiabulls Real Estate, the mill-land conqueror of Lower Parel, was swallowed into the Bengaluru-based Embassy Group and now trades as Embassy Developments Limited, the Indiabulls name scrubbed off entirely in February 2025.2 The power business left the family altogether back in 2014, rechristened RattanIndia.3

So who, exactly, is Indiabulls Ltd. — the entity that started trading on the NSE under the ticker IBULLSLTD in late 2025?

Here is the core paradox of this story. The corporate brand that once symbolized high-leverage risk — the brand that had been so carefully retired from the highly regulated worlds of banking and mortgages — was resurrected in the one place it still carried commercial weight. In October 2025, a sprawling composite scheme of arrangement collapsed seventeen group entities into a listed company then called Yaari Digital Integrated Services Limited (which had itself once been called SORIL Holdings). That merged shell promptly renamed itself back into the ultimate legendary identity: Indiabulls Limited.4

It is a resurrection built on selective memory. The most valuable, most scrutinized businesses that carried the name for two decades are gone. What remains is an asset-light real-estate developer, a discount brokerage, an asset-reconstruction arm, and the residue of a fintech dream — all bundled under a debt-free holding company, with the group's original founder, Sameer Gehlaut, once again the dominant hand on the wheel.

This is the twenty-five-year saga of the Indiabulls Group: from an internet-café-incubated online brokerage, to a shadow-banking colossus, through the brutal 2018 NBFC liquidity freeze, through a radical strategy of self-erasure its founder called "de-promoterisation," and finally to the phoenix-like re-emergence of a name that management is betting still means something. The question this article keeps returning to is not whether the story is dramatic — it plainly is — but whether the new Indiabulls is a genuinely different, cleaner business, or the same instincts wearing a fresh coat of paint. Let us begin where every good origin myth begins: with a few young engineers who thought the establishment was beatable.

II. The IIT Delhi Trio & The Genesis of Indiabulls (2000–2004)

Picture the Indian stock market of the late 1990s. To buy shares, you called a broker who belonged to a tight, clubby fraternity that had operated the same way for a century. You paid fat commissions. You waited for physical share certificates to arrive by courier — paper that could be forged, lost, or stuck in settlement limbo for weeks. The whole apparatus was designed, whether by intent or inertia, to keep ordinary Indians out and insiders comfortable. It was, in short, exactly the kind of cozy incumbency that three restless engineers might look at and think: this is begging to be broken.

The three were Sameer Gehlaut, Rajiv Rattan, and Saurabh Mittal — classmates from the mechanical engineering program at IIT Delhi, the country's elite engineering crucible. Gehlaut, born in a village in Haryana, had briefly gone off to work on offshore oil rigs for Schlumberger before deciding that the real gusher was in Indian financial services.5 There is a founding legend, retold often enough to be worn smooth, that the enterprise began when Gehlaut bought a small, struggling brokerage called GPF Securities, and that the trio worked out of cramped quarters wiring together an online trading portal just as the internet was arriving in Indian homes.5

Two pieces of early backing separated Indiabulls from the hundreds of other dot-com-era hopefuls that flamed out. The first was the imprimatur of steel tycoon L.N. Mittal, whose family took an early stake — a signal to a status-conscious market that serious money believed in these unknowns.5 The second was institutional venture capital from the American hedge fund Farallon Capital, which provided the growth equity to scale.5 For a first-generation Indian startup in the early 2000s, foreign hedge-fund capital was rocket fuel and validation in equal measure.

The timing was almost suspiciously perfect. India was in the middle of dematerializing its equity markets — replacing those forgeable paper certificates with electronic "demat" accounts held at central depositories. Think of it as the moment share ownership went from a physical deed you locked in a drawer to a line item on a screen, instantly transferable. That single infrastructural shift did to stockbroking what broadband did to media: it collapsed the cost and friction of participation. Indiabulls built a business precisely on this transition, offering internet-based trading to a rapidly swelling class of retail investors who had never been welcome in the old brokers' offices.

By 2004, the group was ready to tap the public markets, listing Indiabulls Financial Services on the NSE and BSE just as India's legendary 2003–2007 bull market — one of the great wealth-creation booms in the country's history — was shifting into overdrive. The trio had timed their entry to the market with the instinct of people who lived and breathed market cycles. What they would do with the flood of capital that followed would define — and nearly destroy — them. Because a brokerage, however fast-growing, is a modest business. And these were not modest men.

III. The Golden Bull Run: IPO & Aggressive Expansion (2004–2008)

Fresh capital and a soaring share price are a combustible combination in the hands of the ambitious. With Indiabulls trading at valuations that would make any founder feel invincible, Gehlaut looked beyond the brokerage's thin commissions toward the two industries that were, in the mid-2000s, minting India's new fortunes: real estate and lending. He would enter both — aggressively, simultaneously, and with a taste for spectacle.

The real-estate opening arrived in the most cinematic possible form: the ruins of Mumbai's industrial past. Lower Parel had once been the beating heart of the city's cotton-mill economy, but the mills had died, leaving behind vast tracts of prime central-Mumbai land locked inside the state-owned National Textile Corporation. In 2005, the government auctioned some of these mill parcels, and the bidding became a defining moment in the making of modern Mumbai. In March 2005, an Indiabulls subsidiary won the auction for Jupiter Mills, an eleven-acre defunct textile plant in Lower Parel — and that single purchase launched the group's real-estate business.[^6] Months later, it added Elphinstone Mills, another NTC parcel in the same district.[^6]

To grasp why this mattered, understand what Lower Parel became. Over the following decade, those dead mill lands were reborn as the glass-and-steel spine of Mumbai's new corporate district — the towers, malls, and premium offices that turned "Lower Parel" from a synonym for industrial decay into some of the most expensive commercial real estate in the country. Indiabulls had bought at the ground floor, literally and figuratively, and it planted its flag there with developments that announced it as a premium urban builder rather than a suburban plot-seller.

But land is capital-hungry, and construction is slow. To finance both its own projects and the broader building boom, the group established what would become its true engine: Indiabulls Housing Finance, a non-banking financial company (NBFC) built to issue home loans and construction finance. India's mortgage market was structurally underpenetrated — a country where a fast-growing middle class was, for the first time, able to borrow to buy homes rather than saving for decades. An NBFC could originate these loans faster and with less regulatory friction than a traditional bank, funding itself in the wholesale debt markets and lending out at a spread.

Here is the elegant, dangerous logic of the model, worth pausing on because it is the fault line running through the entire Indiabulls story. A bank funds long-term loans with sticky retail deposits. An NBFC like Indiabulls funded long-term mortgages by continuously borrowing short-term money from mutual funds and bond markets — commercial paper that had to be rolled over again and again. As long as the short-term markets stayed open and cheap, the machine spun beautifully, and the spread between cheap borrowing and higher lending rates dropped straight to the bottom line. It was, effectively, a bet that liquidity would always be there when you reached for it. In a bull market, that bet looks like genius. The group was about to learn what it looks like when the bet fails — but not before making one more, even bolder wager.

IV. The First Pivot & The Great Corporate Divorce (2008–2014)

By 2008, the Indiabulls empire had the sprawling, slightly incoherent shape of a conglomerate assembled by men who could not say no to an opportunity. Finance, real estate, brokerage, retail — and now, the biggest swing yet: power. As India's government evangelized a massive infrastructure build-out to fuel its growth story, Gehlaut launched Indiabulls Power in 2008, with plans for enormous thermal power plants at Amravati and Nashik in Maharashtra. The IPO of Indiabulls Power became one of the marquee listings of its era, riding the national conviction that India's electricity demand would grow forever and that whoever built the generating capacity would own the future.

This is the point in the story where ambition curdles into complexity. Running a hyper-diversified empire that spanned mortgages, skyscrapers, stock trading, and coal-fired power plants strained everything — management bandwidth, capital allocation, and, crucially, investor patience. Public markets are notoriously suspicious of conglomerates that lack an obvious logic connecting their parts; they apply a "conglomerate discount," valuing the tangled whole at less than the sum of its pieces because no investor can cleanly own the one business they actually want. And a power plant is about as far from an online brokerage as two businesses can get.

The friction was not only strategic; it was personal. Three founders who had built something extraordinary together now had genuinely different appetites for where to point it. The resolution came in July 2014, and it was remarkably clean for a divorce of this magnitude. The trio split the empire in two.6

Rajiv Rattan and Saurabh Mittal took the heavy, capital-intensive infrastructure assets — Indiabulls Power and Indiabulls Infrastructure — walking away to build an independent energy business.6 Within months, Rattan would consolidate control by buying out Mittal's stake in the infrastructure arm, and the businesses were rebranded under the RattanIndia banner — RattanIndia Power and RattanIndia Infrastructure.7 The terms of the separation carried a telling clause: Rattan and Mittal relinquished all rights to the "Indiabulls" name, barred from using it after December 31, 2014.7 The brand, it was already clear, was understood to be an asset in its own right — and it was staying with Gehlaut.

Sameer Gehlaut, for his part, kept the crown jewels: the financial-services, housing-finance, real-estate, and brokerage businesses — the profitable, cash-generative core.6 On paper, he had won the divorce, retaining the highest-quality assets and the storied name. In hindsight, he had also retained the businesses whose entire model rested on that fragile bet about liquidity always being available. The split simplified the empire and set up what would become the golden age of Indiabulls Housing Finance. It also concentrated all of Gehlaut's chips on the shadow-banking table — right as the group was about to enjoy its most glorious years, and then face its near-death experience.

V. The NBFC Empire & The Shadow Banking Shockwave (2015–2019)

For a few intoxicating years, Indiabulls Housing Finance (IBHFL) was one of the most admired financial companies in India, and it wore its success the way its founders wore everything — conspicuously. It grew into the country's second-largest private housing finance company. It reported enviably low gross non-performing assets, suggesting a loan book of pristine quality. It paid out lavish dividends, a signal to the market that profits were real and cash was abundant. And it commanded a premium valuation, trading at more than three times book value — the kind of multiple markets award only to lenders they believe have cracked the code of growing fast without lending recklessly.

But there was a second engine humming beneath the retail-mortgage story, and it is the one that mattered. IBHFL had built a high-velocity wholesale real-estate lending business, extending large loans to property developers — including, in an arrangement that would later draw intense scrutiny, its own sister concern, Indiabulls Real Estate. This created a tidy, self-reinforcing ecosystem: the lender financed developers, the developers built projects, and the money circulated within a familiar circle. It was enormously profitable while property values rose. It was also exactly the kind of interconnected, related-party lending that looks like synergy in a boom and looks like a conflict of interest in a bust. Independent investors were, in effect, being asked to trust that loans between affiliated companies were struck at arm's length. That trust was about to be tested.

The test arrived in September 2018, and it came from outside. IL&FS — Infrastructure Leasing & Financial Services, a giant, opaque infrastructure-financing conglomerate — abruptly defaulted on its debts. Because IL&FS was considered blue-chip, its collapse detonated a confidence crisis across India's entire shadow-banking sector. This was the Indian NBFC world's Lehman moment: mutual funds and banks, suddenly terrified of what other hidden defaults lurked, simply stopped lending to NBFCs overnight.

Recall the fragile mechanism from earlier — long-term loans funded by short-term borrowing that had to be constantly rolled over. When the refinancing window slammed shut, every NBFC dependent on wholesale funding faced the same nightmare: maturing short-term debt that needed repaying, and no fresh money to repay it with. This asset-liability mismatch — borrowing short to lend long — went from being an invisible feature of the model to an existential threat. IBHFL, one of the largest players, was squarely in the crosshairs. It survived the immediate squeeze, but the market's faith had cracked, and the premium valuation began to bleed away.

Then came the legal onslaught. In 2019, a public-interest litigation filed by an outfit called the Citizens Whistle Blower Forum alleged financial irregularities, round-tripping of funds, and siphoning by the promoters.8 The allegations — amplified by news articles, magazine pieces, and pointed tweets from a member of parliament — hit an already jittery stock, contributing to a crash that erased the vast majority of IBHFL's market value.8 A proposed merger with Lakshmi Vilas Bank, which would have converted the NBFC into a full bank with access to stable deposits, was rejected by the Reserve Bank of India, closing off the cleanest escape route.

It is worth being precise about how this legal cloud ultimately resolved, because it cuts against the simplest villain narrative. In February 2024, the Delhi High Court dismissed the 2019 petition, finding "no merit" in the allegations, and pointedly noted that shareholders had been "made to suffer huge losses" from the media campaign around the claims.9 The company was, in the end, legally vindicated. But vindication arrived five years too late to matter for the stock, and by then Gehlaut had already concluded that the mere presence of a controversial promoter was itself the problem to be solved. The most radical chapter of the Indiabulls story was not forced by a court. It was chosen.

VI. The Strategic Sacrifices: "De-Promoterisation" & Rebranding (2020–2024)

Most founders fight to the last share to keep control of what they built. Sameer Gehlaut did something that still reads as counterintuitive: he decided the most valuable thing he could do for his companies was to remove himself from them. If the market and regulators no longer trusted a promoter-run Indiabulls, then the businesses would have to stop being promoter-run — and stop being called Indiabulls. He named the strategy "de-promoterisation," and it amounted to a deliberate, staged act of self-erasure.

The logic was cold and, arguably, correct. A housing-finance company lives and dies on its cost of funds; lenders and bondholders must trust it enough to keep the short-term money flowing. As long as the enterprise was fused to a founder trailing PILs, magazine exposés, and governance questions, that trust — and therefore that funding — carried a permanent risk premium. Institutionalizing the business, handing it to a professional board and blue-chip global investors, was a way to buy back credibility at the cost of control.

On the housing-finance side, the divestment came in tranches. Gehlaut systematically sold down his stake, including a major block placement in December 2021, and by 2023 he had exited entirely. He resigned from the IBHFL board in March 2022 and reclassified himself from "promoter" to ordinary "public shareholder" — a legally meaningful demotion that formally severed his control.10 Into the vacuum stepped global institutional capital, most consequentially the Abu Dhabi–based International Holding Company (IHC), whose affiliate acquired a large stake, effectively anchoring the reconstituted, board-run lender.1 The final act was symbolic but total: in July 2024, the company shed the Indiabulls name altogether and rebranded as Sammaan Capital Limited — "dignity" — completing the transformation from a founder's fiefdom into an asset-light, professionally governed NBFC.1 (The name change was not entirely frictionless; the group's holding entity was later fined a small sum by the exchanges over a procedural lapse in a related renaming, a reminder that even reputational housekeeping generates paperwork.)11

The real-estate exit followed a parallel logic but a messier path. Gehlaut divested his interest in Indiabulls Real Estate by merging it into the Bengaluru-based Embassy Group, folding in Embassy's Nam Estates and other Blackstone-backed property assets to create a pan-India developer combining Indiabulls' northern footprint with Embassy's southern strength. The deal nearly died in the tribunals: in May 2023, the Chandigarh bench of the National Company Law Tribunal stalled the merger over objections from the Income Tax Department, freezing it for roughly eighteen months.12 It took the National Company Law Appellate Tribunal, which overruled the tax objections in January 2025, to revive it; the merger became effective on January 24, 2025.12 The renaming happened in two steps — first to the placeholder "Equinox India Developments" in mid-2024, and then, once the Embassy deal closed, to Embassy Developments Limited on February 13, 2025 — erasing the Indiabulls name from Indian real estate for good.2

By early 2025, then, Gehlaut had voluntarily given away the two businesses that had made him famous. He had traded control for survival and value preservation — a genuinely rare act of founder discipline. But a founder who has just methodically dismantled his own empire is rarely done. He had kept one thing back. And that one thing was, at the time, a burning wreck.

VII. The Rise, Stall, and Rebirth of Dhani Services (2017–2024)

While Gehlaut was busy giving away mortgages and skyscrapers, his real energy — and his personal capital — flowed into a very different bet: consumer fintech. The vehicle was Indiabulls Ventures, the group's brokerage-and-lending arm, which in October 2020 was rechristened with a name meant to evoke prosperity: Dhani Services Limited. Dhani was to be Gehlaut's answer to the question of what a de-promoterised founder does next — build something new, digital, and entirely his own.

The vision was a "super-app," that seductive and treacherous category that has tempted so many. Dhani would bundle instant personal loans, stockbroking through Indiabulls Securities, an e-pharmacy, and telehealth into a single phone-based platform — a financial-and-health services hub for aspirational India. For a moment, during the pandemic-era digital boom, it looked like it might work. Customer acquisition soared as Dhani offered instant, app-based credit to millions who had never had access to formal loans.

But here the story runs headlong into one of the hardest truths in emerging-market finance, and it is worth stating plainly: lending money is easy; getting it back is the entire business. Dhani's engine was aggressive, unsecured consumer credit — small-ticket personal loans with no collateral behind them. In a country with thin credit histories and limited recourse against defaulters, unsecured lending at scale is a knife-edge. Acquire customers too fast, underwrite too loosely, and you are not building a loan book; you are subsidizing strangers. That is roughly what happened. Default rates climbed, non-performing assets ballooned, and then the Reserve Bank of India tightened the screws on the entire digital-lending industry, cracking down on the app-based lending practices that firms like Dhani had ridden. The combination was brutal, and Dhani's parent posted heavy consolidated net losses across FY23 and FY24.

The one genuinely creditable part of this chapter is the cleanup. Rather than simply writing the business off, the group's lending arm, Dhani Loans and Services, rebuilt its underwriting and — critically — its in-house digital collections machinery, the unglamorous plumbing of chasing down borrowers. The results in the numbers were real: the lending entity swung from a net loss of roughly ₹144 crore in FY23 to a profit of about ₹74 crore in FY24, as impairment costs collapsed from around ₹77 crore to just ₹7.5 crore on sharply better asset quality.13 Management has pointed to gross NPAs falling from 4.11% to 1.88% over that span as evidence the collections rebuild worked.13 The turnaround was real, but so is the cautionary lesson embedded in it: the profitability came less from brilliant growth than from shrinking, tightening, and cleaning up a book that had been allowed to run wild. A chastened Dhani, its lending ambitions curbed and its losses stemmed, was now a candidate not for expansion but for consolidation. And consolidation, on a grand scale, was exactly what Gehlaut had in mind.

VIII. The Great 2025 Restructuring: The Birth of the New Indiabulls Ltd.

By 2025, the Gehlaut universe had become a genuine puzzle even for professionals: a scatter of listed and unlisted entities — Dhani Services, Indiabulls Enterprises, an old holding shell called SORIL that had been renamed Yaari Digital Integrated Services, plus a long tail of digital, healthcare, insurance, and brokerage subsidiaries — each with its own compliance costs, its own board, its own sliver of the story. This is the conglomerate discount in its purest form: value trapped inside complexity that no rational investor wants to underwrite. The solution was to take all of it and force it through a single legal funnel.

That funnel was a composite scheme of arrangement, the most consequential piece of financial engineering in the group's recent history. It merged seventeen group entities — including Dhani Services and Indiabulls Enterprises, alongside a raft of unlisted digital, healthcare, and insurance subsidiaries — into the listed Yaari Digital shell, while simultaneously carving out a real-estate undertaking through a demerger.4 Approved by the Chandigarh bench of the National Company Law Tribunal and given a retrospective appointed date of April 1, 2023, the scheme became effective on October 14, 2025.14 The mechanics were vast: the surviving company allotted roughly 2.22 billion new equity shares, ballooning its share count from about 100 million to over 2.3 billion.15

For Dhani's shareholders, the swap converted their holdings into the new consolidated stock. The exchange ratio depended on the paid-up status of the shares — holders of Dhani's partly paid-up shares (paid up to ₹1.10) received 162 fully paid shares of Yaari for every 100 they held, with fully paid holders receiving proportionally more.16 Whatever the precise ratio for a given holder, the effect was uniform: dozens of overlapping equity claims across a confusing family of companies were compressed into a single, tradable currency.

Then came the flourish. On October 17, 2025, the merged Yaari Digital renamed itself Indiabulls Limited, and the stock began trading under the ticker IBULLSLTD.4 The legendary identity, so carefully retired from banking and mortgages, was resurrected — this time wrapped around a simplified, essentially debt-free listed holding company. The strategic rationale management offered was threefold and, on its face, reasonable: eliminate the redundant compliance and listing costs of running multiple public companies; pool the group's cash, brokerage assets, and property into one balance sheet; and present public markets with a single, legible vehicle instead of a maze.

But an independent reading has to name the fourth rationale that management naturally soft-pedals: consolidation is also re-promoterisation. The same founder who had spent five years methodically demoting himself to "public shareholder" and stripping his name off regulated lenders was now, through this scheme, re-emerging as the dominant, hands-on promoter of a single vehicle bearing the old name. That is not a criticism so much as an observation with sharp edges. The de-promoterisation of 2020–2024 was sold as permanent institutionalization. The consolidation of 2025 quietly reverses part of that logic. Which version represents the "real" Gehlaut strategy is precisely the question a serious investor now has to answer — and the answer depends heavily on what this new company actually does.

IX. The Modern Core: Asset-Light Real Estate & Financial Platforms (FY2026–Today)

Walk into the story of the new Indiabulls and the first thing to understand is that it has, at least rhetorically, renounced the sin that nearly killed the old one: debt-fueled, capital-heavy empire-building. The company today rests on two pillars, and the larger of the two is designed to generate profit without ever again betting the balance sheet.

Pillar one — real-estate development — is the declared profit engine, targeted by management to deliver the large majority of earnings. But the model is the inverse of the 2000s land grab. Rather than buying prime parcels outright and financing them with borrowed money — the Lower Parel playbook — Indiabulls now pursues an asset-light developer model built on Joint Development Agreements (JDAs). In a JDA, the landowner contributes the land, and Indiabulls contributes execution, project management, marketing muscle, and the "Indiabulls" brand, sharing the proceeds without taking on the debt or the land-acquisition cost. This is the entire strategic bet made concrete: the belief that the name is worth enough to a landowner that it can be swapped for a share of a project in lieu of capital. It is a genuinely capital-light way to build — but it also means the company controls neither the land nor, entirely, the timeline, a vulnerability we will return to.

The scale management points to is not trivial. The company has guided to a gross development value potential of over ₹21,000 crore across roughly 110 lakh square feet (about 11 million square feet) of sellable area in markets including Gurugram, Mumbai, and Ludhiana.17 Layered on top is an annuity shield: the commercial "Indiabulls Tower" in Mumbai throws off recurring rental income, the kind of steady, high-margin cash flow that cushions a developer against the brutal cyclicality of residential sales. GDV, it must be said, is a potential-sales figure spread over many years and many approvals; it is a measure of ambition, not of money in the bank.

Pillar two — financial and digital services — is the scalable platform, and it is a deliberately humbler collection than the mortgage colossus of old. It houses the discount-brokerage business, Indiabulls Securities, which attempts to monetize the group's historical customer database against ferocious modern competition. It includes an Asset Reconstruction Company (ARC) — a counter-cyclical business that buys distressed loan portfolios from banks at a discount and profits by recovering more than it paid, effectively turning banking-sector cleanups into an opportunity. And it retains fintech and payments infrastructure — wallets, payment gateways, insurance distribution — having pointedly exited the capital-destructive unsecured-lending business that nearly sank Dhani.

The first post-merger financial year gave the market its first real look at the assembled machine, and the headline numbers were striking. For FY2026, Indiabulls reported consolidated revenue of roughly ₹880 crore and profit after tax of about ₹346 crore — a net margin near 39%.18 The fourth quarter was especially strong, with revenue of about ₹418 crore and PAT of ₹194 crore, up more than 46% — and real estate was explicitly the primary driver, contributing roughly ₹143 crore at the operating level in the quarter.[^20] For the full year, the company recorded sales bookings of about ₹2,752 crore across 909 units and 21.6 lakh square feet, against a stated operational target of ₹3,000+ crore in annual residential pre-sales.18

Here the independent lens has to work harder than the press release. A ~39% net margin and a swing from years of losses to healthy profit is genuinely impressive on its face — but a first-year post-merger income statement, built on a scheme with a retrospective appointed date and a freshly pooled set of assets, is not yet a track record. Some of that margin reflects the mechanical accounting of consolidation and the absence of the loss-making units that were shed or shrunk. The ₹2,752 crore of bookings against a ₹3,000 crore target is a real, verifiable operating metric and a more honest gauge of demand than any margin. The bull would say: a debt-free developer with strong bookings and 39% margins is a compounding machine. The skeptic would say: show me this again in FY2027 and FY2028, on organic execution, before calling it a trend. Both are right, which is exactly why this is the moment the story becomes an investment question rather than a history lesson.

X. The Playbook: Strategic & Investing Lessons

Step back from the blizzard of renamings and schemes, and the Indiabulls saga yields a handful of lessons that generalize well beyond one Haryana engineer's empire.

The first is the power of strategic resignation. Gehlaut's de-promoterisation is a genuine textbook case — rarer than it should be — of a founder concluding that his own presence had become the single largest liability on the balance sheet, and acting on it. Most founders rationalize; he divested, resigned, and reclassified himself out of control of the two businesses he was most identified with. Whether one views this as noble discipline or as a shrewd way to preserve value he still economically benefited from, the mechanism is instructive: sometimes the highest-return capital allocation decision a promoter can make is to allocate himself out of the picture.

The second is the recycling of a brand name, and it is subtler than it looks. Indiabulls demonstrates that a corporate brand is not a fixed asset but a context-dependent one. In banking and mortgage finance — industries where regulators, bondholders, and depositors demand spotless governance — the Indiabulls name had become radioactive, and it was rationally retired. In private real-estate development and consumer financial services — where a customer or a landowner responds to familiarity and heft rather than to a regulator's trust — the same name still carries commercial weight. The group did not save the brand; it relocated it to the one environment where it still functioned. That is a genuinely clever piece of intangible-asset management, and also a slightly uncomfortable one, since it implies the name works best precisely where scrutiny is lightest.

The third lesson is written in Dhani's losses: the high cost of unsecured consumer credit in emerging markets. Customer acquisition is a vanity metric if collections cannot keep pace. Dhani proved, expensively, that hyper-growth fintech lending without robust, on-the-ground underwriting and recovery infrastructure is not a business but a slow-motion charity. The RBI's digital-lending crackdown merely accelerated a reckoning the loan book was already heading toward.

And the fourth is the one the entire 2025 restructuring rests on: conglomerate discount versus holding-company clarity. Seventeen overlapping entities, each opaque, collectively worth less than their parts, were folded into one legible vehicle in an explicit bid to unlock trapped equity value. It is a clean thesis. But it comes with a warning that the very next section is built around: simplification of structure is not the same as simplification of incentives. A single clean vehicle controlled by a returning promoter can trap value just as effectively as a maze — it simply does so more elegantly. Which brings us to the stress test.

XI. The Stress Test: Bull vs. Bear Case & Key KPIs

Every good investment debate is really a debate about durability of advantage, so let us run the new Indiabulls through two classic frameworks before staking out the bull and bear.

Hamilton Helmer's 7 Powers is unkind to most of the business but flattering to one corner of it. The clearest candidate for a cornered resource is the portfolio of elite, well-located development parcels locked up under JDAs in supply-constrained markets like Mumbai and Gurugram — land access that competitors cannot easily replicate. There is a whisper of scale economies and brand in the equation too: the Indiabulls name genuinely lowers the cost of striking a JDA and marketing a project, a real if modest edge. But on the financial-services side, the powers largely evaporate. In discount broking, Indiabulls Securities has no meaningful scale advantage against players an order of magnitude larger, and switching costs are close to zero — a retail trader moves brokers with a few taps. Switching costs are moderate in real estate, mostly via brand stickiness and the sunk trust of a homebuyer mid-purchase, but they are not a fortress.

Porter's Five Forces sharpens the same picture. In real-estate development, the threat of new entrants is theoretically high, but the capital and — increasingly — the regulatory barriers erected by RERA (India's real-estate regulator, which imposes registration, escrow, and disclosure discipline) protect established, trusted brands and punish fly-by-night builders. That favors Indiabulls at the margin. But rivalry is intense on both pillars: in broking, it faces Zerodha, Groww, and Angel One — modern, low-cost, technology-native platforms that have already won the mass market; in real estate, it faces DLF, Godrej Properties, and the fast-rising Signature Global, all with deeper pipelines and, in several cases, stronger balance sheets. Indiabulls is a challenger in both arenas, not an incumbent.

The bull case is coherent and rests on three legs. First, the debt-free, net-cash balance sheet is a real and rare asset in Indian real estate, an industry that periodically incinerates over-leveraged developers; a builder that owes nothing can keep executing through downturns that bankrupt its rivals. Second, the high-margin turnaround is showing up in reported results — 39% net margins and a genuine profit where there were losses — suggesting the asset-light model, if sustained, could compound attractively. Third, the ARC platform is counter-cyclical, positioned to make money precisely when financial markets and credit conditions deteriorate, offering a natural hedge against the cyclicality of the property book.

The bear case is equally coherent and, in the near term, sharper. Start with promoter credibility and dilution. Gehlaut's return as dominant promoter reopens every governance question the de-promoterisation was designed to close — and it does so with concrete, dated evidence, not just history. In June 2026, the board approved a preferential issue of up to ₹1,000.07 crore in convertible warrants, priced at ₹19.40 each, to a set of investor entities, with an EGM convened on July 2, 2026, to seek shareholder approval; Gehlaut himself was reported to be subscribing to over ₹400 crore of it.19 Preferential warrants to a promoter and a handful of named funds, after a stock that had already run up sharply, are exactly the kind of related-party capital raise a skeptical investor scrutinizes hardest — is it a vote of confidence, or dilution of minority holders on favorable terms to insiders? The answer turns entirely on where the money goes and at what return. Second, competitive reality: Indiabulls Securities is a tier-two broker with little visible path to reclaiming share from Zerodha and Groww, and its organic user growth is structurally challenged. Third, execution risk in the JDA model: asset-light means the company depends on third parties for land, on courts for clearing title litigation, and on partners for timelines — it has traded balance-sheet risk for control risk, and delays outside its power can strand a project's value for years.

Which leaves the question of what to actually watch. Three KPIs matter more than any others, and none of them can be spun in a press release for long:

- Quarterly real-estate pre-sales (bookings) value — the single cleanest read on demand and execution, and the honest scorecard against the ₹3,000+ crore annual target. Margins can be manufactured by accounting; bookings cannot.

- Active brokerage clients and market share — the test of whether Indiabulls Securities can stop bleeding share to the discount-broking giants, or whether it is a legacy asset in slow decline.

- Warrant conversion and the return on the raised capital — whether the ₹1,000 crore of new money gets deployed into high-yielding JDA projects that lift return on equity, or gets parked in low-yield assets while diluting existing shareholders. This is the direct, measurable test of whether the returning promoter allocates capital for all owners or primarily for insiders.

XII. Epilogue

Twenty-five years is a long time to spend building, breaking, and rebuilding the same idea. The Indiabulls story has run the full circuit of Indian capitalism: an insurgent online broker that humbled a clubby establishment; a leveraged conglomerate that reached for real estate and power and finance all at once; a shadow-banking heavyweight that nearly drowned when the tide of liquidity went out; a founder who did the almost unthinkable and gave away his most famous companies to save them; a fintech dream that learned the hard way that lending is easy and collecting is everything; and finally, a consolidated, debt-free holding company that has returned, quite literally, home to its name.

There is something almost novelistic about a brand being retired from the industries that made it dangerous and revived in the one place it can still do useful work. But novelistic is not the same as proven. The new Indiabulls Ltd. is, for now, a promising first-year income statement wrapped around an old identity and steered by a promoter whose track record contains both genuine discipline and genuine controversy. The asset-light model is real; so is the competitive weakness in broking. The debt-free balance sheet is real; so is the freshly approved dilution. The turnaround is real; so is the fact that one clean year is not a track record.

The ultimate test is not whether Sameer Gehlaut can tell a good resurrection story — he has proven, repeatedly, that he can. It is whether the streamlined, asset-light Indiabulls can permanently shed the leverage instincts and governance shadows of its past and compound wealth, patiently and cleanly, for the ordinary shareholders now along for the ride. The phoenix has risen. Whether it can simply fly — steadily, unspectacularly, for a decade — is the only question that ultimately matters.

References

-

Indiabulls Housing Finance Limited is now Sammaan Capital Limited — Mediabrief, 2024 ↩↩↩

-

New Name & Old Name of Listed Entity — Embassy Developments Limited (Investor Relations) ↩↩

-

Rajiv Rattan takes control of Indiabulls Power — Business Standard, 2014-09-06 ↩

-

Yaari Digital Integrated Services Completes Major Merger Scheme, Rebrands as Indiabulls Limited — ScanX, 2025 ↩↩↩

-

Zeal to Excel: Sameer Gehlaut | Indiabulls Group — M&A Critique ↩↩↩↩

-

Indiabulls promoters split empire — Business Standard, 2014-07-09 ↩↩↩

-

Delhi HC dismisses plea seeking probe into Indiabulls Housing Finance — Business Standard, 2024-02-04 ↩↩

-

Delhi High Court dismisses petition alleging financial irregularities by Indiabulls Housing Finance — SCC Online, 2024-02-05 ↩

-

Indiabulls Housing Finance Limited rebranded as 'Sammaan Capital Limited' — Exchange4media, 2024 ↩

-

Indiabulls Ltd Completes Name Change, Faces ₹1.46 Lakh Fine — Whalesbook Corporate News, 2025 ↩

-

NCLAT gives go-ahead for Indiabulls Real Estate–Embassy Group merger — Business Standard, 2025-01-12 ↩↩

-

DHANI SERVICES 2023-24 Annual Report Analysis — Equitymaster ↩↩

-

Yaari Digital Integrated Services — Intimation of Scheme Effectiveness and Record Dates, 2025-10-14 (Indiabulls.com) ↩

-

Yaari Digital Integrated Services Completes Massive Share Allotment Under Scheme of Arrangement — ScanX, 2025 ↩

-

Dhani Services–Yaari Digital Merger: Record Date for Share Entitlement — Angel One, 2025 ↩

-

Indiabulls Limited Q4 FY26 Earnings: Revenue ₹418.39 Cr, Real Estate Drives Growth — ScanX, 2026 ↩

-

Indiabulls' Q4 profit jumps 46.4 pc to Rs 194 crore (FY26 results) — The Hans India, 2026-04-29 ↩↩

-

Indiabulls seeks nod for ₹1,000.07 crore warrant issue — ScanX, 2026 ↩

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube