HUDCO: India's Silent Infrastructure Giant

I. Introduction & Setting the Stage

Picture this: A government office building in New Delhi, 1970. The walls are bare concrete, the furniture spartan. Outside, millions of Indians sleep under bridges, in slums, on pavements. Inside, a small team of bureaucrats and engineers are handed an impossible mandate—finance homes for people banks won't touch, build infrastructure where private capital fears to tread, and somehow, make it financially sustainable.

Fast forward five decades. That modest office has quietly engineered the financing of 192 lakh housing units across India. The organization behind it trades on the NSE with a market capitalization of ₹42,122 crores, yet remains virtually unknown outside policy circles and infrastructure finance professionals. This is HUDCO—Housing and Urban Development Corporation Limited—perhaps India's most consequential company that nobody talks about.

The paradox is striking. While private housing finance companies grab headlines and command premium valuations, HUDCO has methodically built one of India's largest infrastructure financing portfolios. It operates in the shadows of India's development story—present at every major urban transformation, yet invisible to most observers. The company that helped build modern India's cities trades at valuations that would make a value investor weep with either joy or despair, depending on their perspective.

What we're about to explore isn't just a corporate history. It's the story of how a socialist-era institution adapted, survived, and thrived through liberalization, privatization, and digitization. It's about the tension between social mandate and commercial viability—a balancing act that defines not just HUDCO, but the entire architecture of development finance in emerging markets.

This journey will take us from the refugee camps of partition-era Delhi to the smart cities of tomorrow, from handwritten loan applications to digital infrastructure platforms, from a ₹2 crore seed capital to financing ₹1,00,000 crore mega-deals. Along the way, we'll decode why government-owned enterprises like HUDCO persist in sectors theory suggests should be fully private, and what their existence tells us about the limits of pure market capitalism in addressing societal needs.

The timing of this analysis couldn't be more relevant. As India stands at the cusp of a $5 trillion economy dream, as urbanization accelerates at unprecedented rates, as climate change demands resilient infrastructure—HUDCO sits at the intersection of every major trend. Yet its stock has declined 28% in the past year, even as profits grew 24.8%. The market clearly doesn't know what to make of this entity. Perhaps by the end of this exploration, we will.

II. Pre-Independence Context & The Housing Crisis (1947-1970)

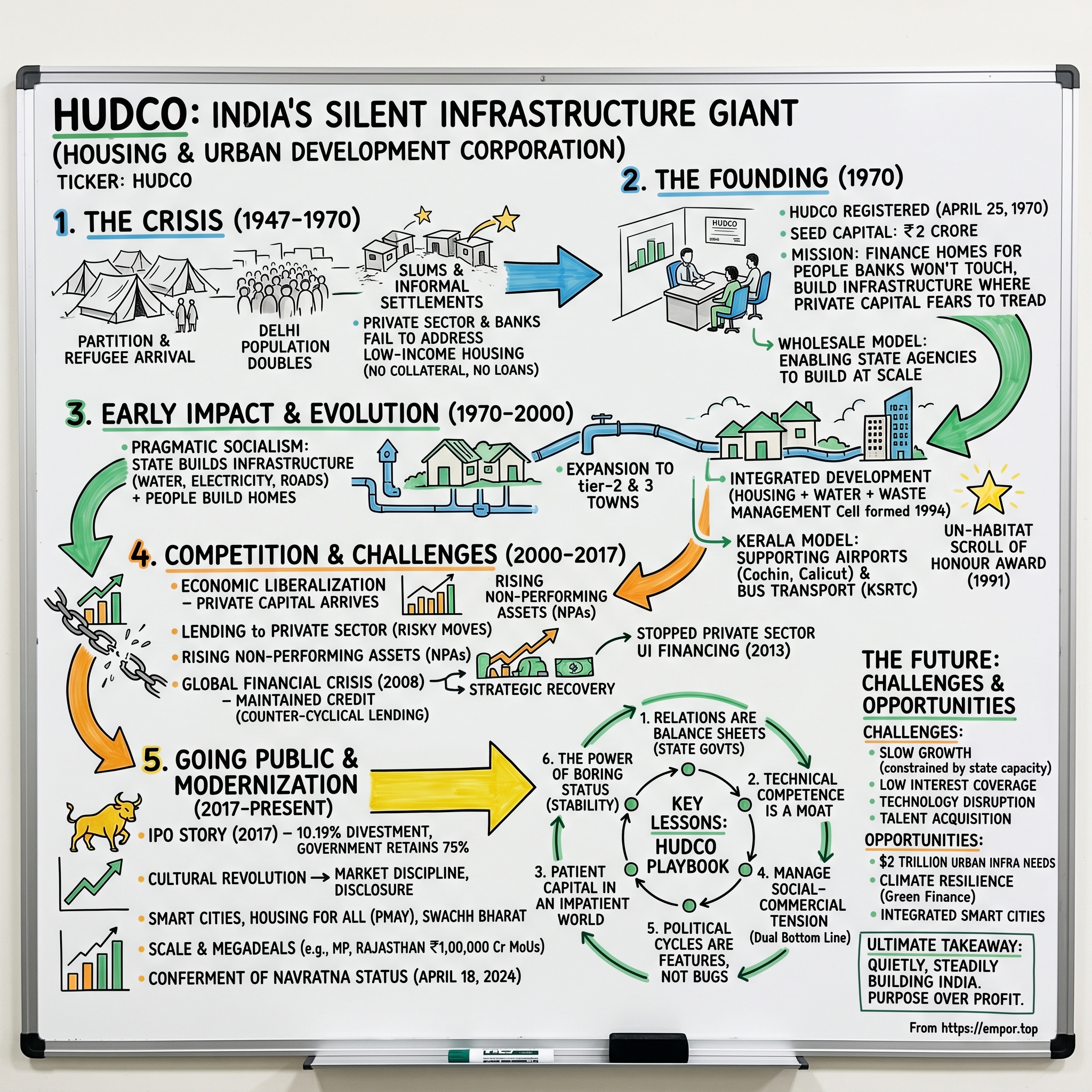

The trains arrived at Delhi's railway stations in 1947 carrying more than just passengers—they carried the architectural blueprint of modern India's first crisis. Partition had created the largest mass migration in human history: 15 million people crossed borders, cities swelled overnight, and makeshift camps became permanent settlements. If you walked through Karol Bagh or Lajpat Nagar in those days, you'd see something that would define Indian cities for generations—the informal settlement, the unauthorized colony, the slum. The demographic catastrophe was staggering. Delhi's population nearly doubled from 917,939 in 1941 to 1,744,072 in 1951, despite significant Muslim outmigration. Refugees were housed in the Purana Qila, Red Fort, and military barracks, with Kingsway Camp alone housing over 35,000 refugees at any given time. The government's initial response was chaotic—by 1950, authorities began allowing squatters to construct houses, creating neighborhoods like Lajpat Nagar and Patel Nagar that retain their refugee character to this day.

But Delhi was just one piece of a continental puzzle. Across India, cities buckled under the weight of displacement. The housing question wasn't academic—it was existential. Where do you put 7 million people who arrive with nothing but trauma? The private sector had no answer. Banks wouldn't lend to refugees without collateral. Developers wouldn't build for people without money. The market, that great allocator of resources, simply shrugged. By the 1960s, the housing crisis had evolved from refugee resettlement to structural urban poverty. India was grappling with finding appropriate solutions to the ever evolving problem of appropriate shelter, starting with more than 6 million people under forced migration led by the division of India. The government's early attempts were piecemeal—the Integrated Subsidised Housing Schemes for Industrial Workers in 1952, the Low Income Group Housing Scheme in 1954, the Slum Clearance and Improvement Schemes in 1956. Each scheme represented a bureaucratic acknowledgment that the market had failed, but none addressed the scale of the problem.

The numbers were brutal. There were 0.9 million homeless people in urban India according to Census 2011, in addition to a slum population of roughly 65 million (or 17% of urban India)—though these figures from decades later only hint at how dire the situation was in the 1960s. Private banks viewed low-income housing as charity, not business. Construction companies saw no profit in building for people who couldn't pay market rates. The poor were caught in a vicious cycle: no collateral meant no loans, no loans meant no homes, no homes meant no address, no address meant no formal employment, and round it went.

It was in this context that a group of bureaucrats and planners began to imagine something radical—a financial institution that would operate where the market wouldn't, lend where banks feared to tread, and somehow make it all sustainable. They weren't trying to replace the market; they were trying to prove that certain markets could exist if someone was willing to take the first risk. This thinking would culminate in 1970 with the birth of HUDCO, but to understand why it succeeded where so many schemes failed, we need to understand the institutional vacuum it was designed to fill.

III. The Founding Story & Early Vision (1970-1980)

On April 25, 1970, in a nondescript government building in New Delhi, a company was registered that would quietly reshape India's urban landscape. The Housing and Urban Development Corporation Limited began life with a capital base of just ₹2 crores—roughly the cost of a modest apartment complex in today's Mumbai. The founding documents were sparse, the mission ambitious: bridge the housing finance gap that private capital refused to touch.

The timing wasn't accidental. India was entering its fourth Five Year Plan, and the planners had finally acknowledged what everyone could see—urban India was breaking. The refugee crisis of partition had morphed into permanent slums. Industrial workers lived in conditions that mocked the nation's socialist ideals. The private sector had made its position clear: there was no money in housing the poor.

But HUDCO's founders understood something the market missed. They saw that the problem wasn't just about individual home loans—it was about financing entire ecosystems. State governments needed capital to build infrastructure. Housing boards needed long-term funding for large projects. Municipalities needed resources for basic services. The retail lending model that banks understood wouldn't work here. What India needed was wholesale transformation.

The organizational structure reflected this vision. Unlike a bank with thousands of branches, HUDCO would operate lean—a handful of offices staffed by engineers and financial specialists who understood both construction and capital. They wouldn't compete with banks for individual customers; they would enable state agencies to build at scale. The average loan tenure would be eight years—an eternity in 1970s India where most commercial loans were measured in months.

The early projects tell the story better than any mission statement. HUDCO's first sanctions went not to Delhi or Mumbai, but to places like Madras (now Chennai) and Calcutta (now Kolkata), financing sites-and-services schemes where the government provided basic infrastructure—water, electricity, sewerage—and let people build their own homes. It was pragmatic socialism: the state would do what individuals couldn't (infrastructure), and individuals would do what the state shouldn't (build homes suited to their needs).

The numbers from those early years seem quaint now—sanctions of a few crores here and there. But each project was a proof of concept. In Hyderabad, HUDCO financed housing for industrial workers near the new public sector factories. In Bhopal, it funded slum improvement that turned unauthorized colonies into legitimate neighborhoods. These weren't just loans; they were experiments in development finance.

What made HUDCO different wasn't just what it financed, but how. Traditional lenders demanded collateral that the poor didn't have. HUDCO accepted government guarantees. Banks wanted quick returns; HUDCO offered moratoriums during construction. Commercial lenders stayed in cities; HUDCO ventured into tier-2 and tier-3 towns where no private financier would go.

The institutional culture that developed in those early years would define HUDCO for decades. This wasn't a place for bankers looking for quick profits or bureaucrats seeking comfortable postings. The early HUDCO officers were a peculiar breed—technically competent enough to evaluate engineering proposals, financially sophisticated enough to structure complex loans, and idealistic enough to believe that public service and financial viability weren't mutually exclusive.

By 1975, five years into its existence, HUDCO had sanctioned projects worth ₹100 crores—fifty times its initial capital. More importantly, it had proved something crucial: there was indeed a market for development finance, but it required patient capital, government backing, and a willingness to measure success differently. Repayment rates were surprisingly high—state governments, whatever their fiscal troubles, prioritized HUDCO dues because they needed continued access to this unique source of funding.

The model was working, but slowly. India's housing shortage was growing faster than HUDCO could finance solutions. The organization needed to evolve, to think bigger, to move beyond just housing into the infrastructure that made housing possible. That evolution would define its next phase, transforming it from a housing finance company into something much more ambitious—an infrastructure bank before India knew it needed one.

IV. Building the Business Model (1980-2000)

The 1980s opened with HUDCO at a crossroads. The experiment had succeeded—the organization was financially viable, its loans were being repaid, and demand far exceeded supply. But success brought scrutiny. Why, critics asked, should a government company enjoy monopoly over development finance? Why not let the market handle it? The answer came not through ideology but through practice, as HUDCO systematically built a business model that private capital couldn't replicate.

The genius lay in the wholesale approach. While banks chased individual mortgages in affluent neighborhoods, HUDCO was financing entire townships. A typical transaction might involve a state housing board seeking ₹50 crores to develop 10,000 housing units for economically weaker sections. HUDCO would structure the loan with a construction period moratorium, a 15-year repayment schedule, and interest rates that made the project viable. The housing board would handle construction and allocation; HUDCO would provide patient capital and technical expertise. The international recognition came in 1991 when HUDCO won UN-Habitat Scroll of Honour Award for the contributions to the development of housing—one of the most prestigious human settlements awards in the world. This wasn't just ceremonial validation; it signaled that HUDCO's model had global relevance. Here was a developing country institution demonstrating that public finance could work where markets failed.

But the real innovation was happening in the field. In 1989, HUDCO began financing infrastructure projects beyond housing—drainage, electricity, water supply, sewerage, solid waste management and roads in the urban areas. This wasn't mission creep; it was recognition that housing without infrastructure was meaningless. You couldn't build homes without water supply, couldn't create neighborhoods without sewerage systems, couldn't develop towns without roads.

In 1994, HUDCO set up a Waste Management Cell for promotion of municipal waste management—prescient timing given that urban India was about to explode in size. The organization was evolving from a housing financier to an urban development catalyst. Each new vertical brought complexity but also synergies. A typical project might now involve housing, water supply, and solid waste management—integrated development that multiplied impact.

The state government partnerships became increasingly sophisticated. HUDCO wasn't just lending money; it was transferring knowledge. Technical teams would work with state agencies on project design, helping them avoid costly mistakes. The consultancy services that developed organically became a formal business line—HUDCO officers who had seen hundreds of projects knew what worked and what didn't.

Consider the Kerala model that emerged in this period. Airport projects of Cochin International Airport and Calicut International Airport in Kerala are supported by HUDCO. The infrastructure for Kerala State Road Transport Corporation and UPSRTC are also funded by them. HUDCO sanctioned ₹100 crore for KSRTC in 2002 for purchasing 550 buses and 350 mini-buses. This was systems thinking—finance the airports that bring economic activity, fund the buses that transport workers, support the housing where they live.

The balance between social mandate and commercial viability was constantly tested. HUDCO's charter required it to allocate 55% of its housing finance to economically weaker sections and low-income groups. This wasn't charity—these loans were structured to be repaid, just over longer periods and at rates that reflected social returns rather than pure financial returns. The other 45% could go to middle and higher-income projects, which generated better margins and cross-subsidized the social lending.

By the mid-1990s, HUDCO had developed what management theorists would later call a "dual bottom line" model—financial sustainability and social impact. The organization was profitable, but profits were means, not ends. Surpluses were plowed back into expanding lending capacity. The dividend paid to the government was modest, reflecting an implicit understanding that HUDCO's real contribution wasn't cash but capability.

The organizational culture that crystallized in these decades was unique in India's public sector. HUDCO officers weren't typical bureaucrats moving paper between departments. They were on construction sites, in municipal offices, at planning meetings. They understood concrete and steel, interest rates and municipal bonds, slum rehabilitation and master plans. This technical competence gave them credibility with both borrowers and policymakers.

But success bred complacency, and complacency invited competition. By the late 1990s, private banks were eyeing the infrastructure finance space. The economy was liberalizing, foreign capital was flowing in, and suddenly everyone wanted to finance India's growth. HUDCO's monopoly was ending. The question was whether an organization built for scarcity could adapt to abundance. The answer would come in the next decade, and it wouldn't be what anyone expected.

V. The Liberalization Era & Strategic Pivot (2000-2013)

The millennium opened with HUDCO facing an existential question it had never needed to ask: Why should we exist? Economic liberalization had unleashed private capital, new housing finance companies were proliferating, and infrastructure had become the new gold rush for investors. The comfortable monopoly over development finance was history. What followed was a decade of experimentation, crisis, and ultimately, clarity about HUDCO's irreplaceable role.

The early 2000s saw HUDCO venture boldly into new territory. The organization expanded its infrastructure portfolio to include power generation projects—a logical extension given that electricity was essential for urban development. Social infrastructure components received new emphasis: primary schools and play grounds, hostels for working women, healthcare centres, police stations and jails, courts. This wasn't random diversification; it was recognition that cities needed more than houses and roads.

The numbers tell a story of rapid growth. By 2012, PAT crossed ₹600 crore mark, and HUDCO raised ₹5000 crore through tax-free bonds. The tax-free bonds were particularly clever—they tapped into retail investors' appetite for tax-efficient instruments while funding social infrastructure. Here was financial engineering with a purpose.

But the aggressive expansion came with a price. HUDCO began lending to private sector entities, competing directly with commercial banks in territories where it had no natural advantage. Private developers promised quick returns and ambitious projects. The officers trained to evaluate government proposals suddenly found themselves assessing private sector business plans. It was like asking a chess player to suddenly play poker—the board was different, the rules had changed, and bluffing was part of the game.

The wake-up call came gradually, then suddenly. Non-performing assets began mounting. Private developers who had painted rosy pictures during the boom found excuses during the slowdown. Projects stalled, loans soured, and HUDCO discovered what banks had long known—private sector lending without private sector capabilities was a recipe for disaster.

The turning point came in March 2013 when HUDCO made a decisive move: it ceased sanctioning new Urban Infrastructure Finance loans to private sector entities. This wasn't retreat; it was strategic clarity. HUDCO recognized that its competitive advantage lay not in competing with banks for private sector business, but in doing what banks couldn't or wouldn't do—patient, long-term development finance for public projects.

The infrastructure boom of this era taught HUDCO valuable lessons. The organization had ring-side seats to India's urbanization acceleration—cities expanding beyond master plans, infrastructure struggling to keep pace, slums growing faster than formal housing. Private capital was indeed flowing, but it was flowing to profitable segments. The old problems HUDCO was created to solve hadn't disappeared; they had simply been obscured by the shine of liberalization.

Consider what was happening on the ground. In Bangalore, IT companies were building gleaming campuses while their workers lived in inadequate housing an hour away. In Gurgaon, private developers created apartment complexes with private water supply and diesel generators because municipal infrastructure hadn't kept pace. The market was solving problems for those who could pay market prices. Everyone else was still waiting.

HUDCO's response was to double down on its core competence. If private banks wanted to finance luxury housing, let them. HUDCO would focus on affordable housing. If infrastructure funds wanted to build toll roads, fine. HUDCO would finance municipal water supply systems. The organization wasn't competing with the market; it was completing it.

The 2004 conferment of Miniratna status—granting greater autonomy in investment decisions—proved crucial during this period. HUDCO could now move faster, structure deals creatively, and respond to opportunities without bureaucratic delays. But autonomy also meant accountability. The government was essentially saying: you have the freedom to succeed or fail on your merits.

The human dimension of this transition is often overlooked. HUDCO's workforce, recruited and trained for public sector lending, had to adapt to a new reality. Some embraced the change, developing new skills in risk assessment and portfolio management. Others struggled with the cognitive dissonance of being asked to think commercially while serving social objectives. The organization that emerged from this period was leaner, more focused, and clearer about its mission.

The financial crisis of 2008 provided unexpected validation. While private lenders retreated, HUDCO maintained its lending to state governments and urban local bodies. Counter-cyclical lending isn't just good economics; it's essential public service. When private capital runs scared, public institutions must step in. HUDCO had the balance sheet strength and institutional mandate to do exactly that.

By 2013, HUDCO had found its equilibrium. It would compete where it had advantages—relationships with state governments, understanding of public sector processes, patience for long-gestation projects. It would avoid areas where private sector capabilities were superior—quick decision-making, aggressive risk-taking, retail customer service. This wasn't admission of defeat; it was strategic positioning for the next phase of growth. And that next phase would begin with something unprecedented—taking this quiet government company public.

VI. The IPO Story & Public Market Entry (2017)

The announcement came quietly, buried in the Union Budget speech of 2016: the government would divest minority stakes in several public sector undertakings. HUDCO was on the list. For an organization that had operated for 47 years away from public scrutiny, the prospect of an IPO was like asking a submarine to surface—necessary perhaps, but profoundly disorienting.

Inside HUDCO's headquarters, the IPO preparation triggered a cultural revolution. Decades of informal practices had to be formalized. Management information systems that had served internal reporting needed to meet market standards. Financial statements that satisfied government auditors had to appeal to equity analysts. The organization hired investment bankers who spoke a language of multiples and comparables that seemed alien to engineers who thought in terms of plinth areas and floor space indices.

The timing was delicate. May 2017 found India's capital markets in a peculiar mood—optimistic about the long-term India story but nervous about near-term disruptions. Demonetization had just roiled the real estate sector. The Real Estate Regulation Act (RERA) was creating new compliance requirements. GST implementation loomed. Into this uncertainty, HUDCO would attempt to convince investors that a 47-year-old government company was worth their money.

The price band was set at ₹56-60 per share—conservative by any measure. The investment bankers had argued for a higher range, pointing to HUDCO's asset base and steady cash flows. But the government, perhaps wisely, chose caution over ambition. This wasn't about maximizing proceeds; it was about ensuring success. A failed IPO would have been more than financial embarrassment—it would have questioned the viability of the entire PSU divestment program. The road show presentations were exercises in translation. HUDCO's management had to explain to fund managers why a company that financed bus depots and sewerage plants deserved their attention. The pitch was straightforward: India needed $2 trillion in infrastructure investment over the next decade, someone had to finance the unglamorous parts, and HUDCO had been doing exactly that for 47 years without a single default to lenders.

When the IPO opened on May 8, 2017, the response exceeded expectations. The issue was oversubscribed 79 times overall—institutional investors bid for 80 times their allocation, retail investors 1.64 times. The grey market premium reached 30-40% of the IPO price. For a government divestment in a PSU, this was remarkable. The market was essentially saying: we understand what you do, and we want in.

The stock listed at Rs 73.45 on BSE and at Rs 73 on NSE, a 22% premium against IPO price of Rs 60. The stock settled at Rs 72.50, a 21% premium to its issue price. In intraday trade, it rallied as much as 30% to Rs 77.80. For HUDCO employees watching from their offices, it was surreal—their quiet government company was now a stock ticker, its value determined every second by anonymous trades.

The IPO allocated 10.19% of the company's stake to public shareholders, with the government retaining 75%. This wasn't full privatization—the government maintained control—but it introduced a new dynamic. HUDCO now had thousands of shareholders who expected quarterly results, investor calls, and most importantly, growth. The organization that had operated for decades with a single shareholder suddenly had to explain itself to mutual funds and retail investors.

The post-IPO period required rapid adjustment. Investor relations became a function, not an afterthought. Quarterly earnings calls introduced a rhythm of disclosure foreign to an organization accustomed to annual reporting. The stock price became a daily report card, rising and falling on news, rumors, and broader market sentiment. HUDCO discovered what every public company knows—the market can be irrational, short-term focused, and unforgiving.

But the IPO also brought unexpected benefits. The market discipline forced operational improvements. Processes that had calcified over decades were reexamined. The need to show quarterly growth pushed HUDCO to be more aggressive in loan recovery, more selective in project sanctions, more efficient in operations. The organization that went public wasn't the same one that came out the other side.

More subtly, the IPO changed HUDCO's relationship with its borrowers. State governments now dealt with a listed company whose stock price reflected, in part, their repayment behavior. Delays in servicing HUDCO loans could trigger analyst downgrades, negative news coverage, stock price declines. The market became an enforcement mechanism more powerful than any government circular.

The IPO also positioned HUDCO for its next phase. With public shareholding came access to capital markets—the ability to raise funds through bonds, rights issues, institutional placements. The organization was no longer dependent solely on government equity infusions and internal accruals. It could now tap the same markets it had watched private players access for years. The student had graduated, even if the curriculum was still being written.

VII. Modern Era: Smart Cities to Housing for All (2017-Present)

The India that HUDCO navigated post-IPO was transforming at unprecedented speed. Smart Cities, Housing for All, Swachh Bharat—ambitious government programs requiring massive capital deployment were launching simultaneously. For an organization that had spent decades in steady-state operations, this was both opportunity and challenge. The question wasn't whether HUDCO was relevant, but whether it could scale fast enough to meet the moment. The conferment of Navratna Status on April 18, 2024, marked a watershed moment. The Department of Public Enterprises (OPE) granted the Navratna Status to Housing and Urban Development Corporation Limited (HUDCO). This wasn't just ceremonial—these organisations are authorised to undertake substantial investments of up to ₹1,000 crore without needing approval from the Centre. For an organization that had operated under tight government control for 54 years, this was liberation.

The timing was perfect. India's infrastructure needs were exploding. The government's Housing for All by 2022 initiative required financing at a scale never before attempted. Smart Cities needed integrated development—not just houses but entire ecosystems of urban infrastructure. HUDCO, with its deep relationships with state governments and urban local bodies, was uniquely positioned to channel this capital. The scale of ambition became clear in July 2025 when HUDCO signed an MoU to provide financial support of Rs 1,00,000 crore over five years for housing and infrastructure projects in Madhya Pradesh. This wasn't just a large loan—it was one of the largest urban development financing agreements at the state level in recent years. Similar agreements followed with Rajasthan (another ₹1,00,000 crore) and commitments to Amaravati's development (₹11,000 crore). HUDCO was operating at a scale that would have been unimaginable a decade earlier.

But scale brought scrutiny. The market noticed concerning trends. Despite profit growth—net profit rose to Rs 630.23 crore in Q1FY26, up 13% from Rs 557.75 crore in Q1FY25—the stock performance was disappointing. Market cap down 28% in 1 year, poor sales growth of 6.38% over past five years. The market was essentially asking: if this is such a great business, why isn't it growing faster?

The answer lay in understanding what HUDCO actually did. This wasn't a typical financial services company chasing retail customers or competing for corporate loans. HUDCO operated in a specific niche—long-term project finance for state governments and urban local bodies. The growth rate was constrained by the absorption capacity of these entities, not HUDCO's lending capacity.

COVID-19 tested this model like never before. State governments' finances collapsed, infrastructure projects stalled, and suddenly everyone questioned whether lending to sub-sovereign entities was prudent. HUDCO's response was textbook counter-cyclical lending—maintaining credit lines when states needed them most, restructuring loans pragmatically, and essentially acting as a financial stabilizer during the crisis.

The recovery vindicated this approach. As states emerged from COVID, infrastructure spending resumed with vengeance. The government's push for capital expenditure as a growth driver meant more projects, more financing needs, more opportunities for HUDCO. But competition had also intensified. Private NBFCs had discovered infrastructure finance, banks were aggressively lending to states, and new institutions like NIIF were entering the space.

HUDCO's competitive response wasn't to match competitors on pricing or terms—a race to the bottom it couldn't win. Instead, it leveraged what competitors couldn't replicate: five decades of relationships, deep understanding of government processes, and most importantly, patience. While private lenders wanted quick exits and high IRRs, HUDCO was comfortable with 15-year loans at modest spreads.

The consultancy business, often overlooked by analysts, became increasingly important. HUDCO wasn't just lending money; it was helping design projects, structure financing, and build capacity. This technical assistance created switching costs—states that worked with HUDCO on project design naturally turned to it for financing.

The challenges remained substantial. Low interest coverage ratio reflected the thin margins in government lending. ROE of 13.5% over 3 years was respectable but not spectacular. The 75% government holding meant decisions were sometimes driven by policy rather than pure commercial logic. The stock market's valuation reflected these realities—HUDCO traded at significant discount to private housing finance companies.

Yet the opportunity was undeniable. India's urban population would double by 2050. Infrastructure investment needs exceeded $1 trillion. Climate resilience required massive capital for retrofitting and green infrastructure. If HUDCO could capture even a fraction of this opportunity while maintaining asset quality, the next decade could dwarf everything that came before. The question was whether a 55-year-old institution had the agility to seize it.

VIII. Financial Architecture & Performance Analysis

The numbers tell a story of conservative excellence wrapped in mediocrity. HUDCO's financial statements read like a paradox—pristine asset quality sitting alongside pedestrian returns, massive scale producing modest profits, government backing generating private sector skepticism. Understanding this requires decoding not just what the numbers say, but what they represent in the unique context of development finance.

Start with the loan portfolio composition: 61% Urban Infrastructure Finance, 39% Housing Finance. This split isn't random—it reflects decades of evolution from pure housing lender to infrastructure financier. The infrastructure portfolio—funding everything from water supply systems to smart city projects—generates lower yields but longer tenures and larger ticket sizes. The housing portfolio, increasingly focused on affordable segments, offers better spreads but higher operational complexity.

The revenue model appears deceptively simple: borrow at X, lend at X+Y, pocket Y as spread. But the reality is far more nuanced. HUDCO's cost of funds benefits from implicit government guarantee—markets price HUDCO bonds almost like sovereign debt. This allows borrowing at rates private NBFCs can only dream of. Yet the lending rates are constrained by the borrowers' paying capacity and political sensitivity around infrastructure costs.

Net Interest Income grew 26% YoY, reaching Rs 962 crore from Rs 761 crore in the same quarter last year. This growth came not from aggressive lending but from portfolio optimization—shifting mix toward higher-yielding segments while maintaining asset quality. The net interest margin of 3.22% might seem thin compared to private housing finance companies' 4-5%, but it's remarkable for infrastructure lending where global benchmarks are often below 2%.

Asset quality presents HUDCO's strongest suit. Gross NPAs dropped to 1.67%, down from 2.71% a year ago. Net NPAs were lower too, coming in at 0.25% versus 0.36% previously. These numbers are extraordinary for any lender, almost unbelievable for one exposed to state governments and municipal bodies often criticized for poor financial management. The secret lies in the lending structure—sovereign guarantees, dedicated revenue streams, and the political impossibility of defaulting on HUDCO.

But low NPAs mask operational inefficiencies. The poor sales growth of 6.38% over past five years reflects structural constraints. HUDCO can't simply open branches and acquire customers like retail banks. Each loan requires months of negotiation with government entities, political clearances, and bureaucratic processes. Growth depends on government capital expenditure cycles, not HUDCO's sales efforts.

The capital adequacy position is comfortable but not fortress-like. With the Navratna status allowing greater operational freedom, HUDCO could leverage its balance sheet more aggressively. But management remains conservative, maintaining buffers well above regulatory requirements. This prudence is both strength and weakness—it ensures stability but limits growth potential.

The dividend policy reveals the government's dual role as promoter and beneficiary. Regular dividends flow back to the exchequer, effectively recycling development finance profits into government revenues. This creates an interesting dynamic—HUDCO must balance retained earnings for growth against the government's fiscal needs. The recent interim dividend of Rs 1.15 per share (11.50% on face value) demonstrates this balancing act.

Regulatory compliance adds another layer of complexity. HUDCO operates under multiple regulators—NHB for housing finance, RBI for NBFC regulations, SEBI for listed company compliance. Each has different requirements, reporting standards, and priorities. Managing this regulatory maze while maintaining operational efficiency is a constant challenge.

The funding mix has evolved significantly post-IPO. While government support remains available, HUDCO increasingly taps bond markets. Tax-free bonds were particularly successful, attracting retail investors seeking efficient returns. The ability to raise ₹5000 crore through such instruments demonstrates market confidence despite the stock price weakness.

Operational metrics reveal interesting patterns. The cost-to-income ratio is low by financial sector standards, reflecting the wholesale model's efficiency. But technology spending remains modest—HUDCO isn't competing on digital platforms or customer experience. The employee cost structure reflects public sector norms rather than market compensation, creating challenges in attracting specialized talent.

The government's 75% holding creates unique dynamics. On one hand, it provides comfort to lenders and borrowers—HUDCO won't be allowed to fail. On the other, it limits strategic flexibility and subjects the company to political priorities. Major decisions require government approval, introducing delays and sometimes non-commercial considerations.

Risk management, often overlooked in analysis, is surprisingly sophisticated. HUDCO's exposure to state governments is diversified across geographies and sectors. Revenue streams are often escrowed, reducing payment risk. The long-term nature of loans provides early warning signals for stress. The bigger risk isn't credit but relevance—whether HUDCO's model remains viable as India's financial markets deepen.

Looking at peer comparison, HUDCO occupies a unique position. Private housing finance companies like HDFC (before merger) or LIC Housing Finance operate in different segments with different risk-return profiles. Infrastructure financiers like PFC or REC focus on power sector. HUDCO's mixed portfolio makes direct comparison difficult, contributing to valuation confusion.

The efficiency paradox is striking—HUDCO is simultaneously highly efficient (low operational costs, minimal NPAs) and highly inefficient (slow growth, modest returns). This isn't contradiction but reflection of its mandate. Efficiency in development finance isn't about maximizing profits but optimizing social impact within financial sustainability. By this measure, HUDCO's performance looks different—192 lakh housing units financed isn't just a number, it's millions of families with homes.

IX. The Playbook: Lessons in Public Sector Excellence

Five decades of navigating Indian bureaucracy, politics, and markets has given HUDCO a playbook that reads like a masterclass in institutional survival. While MBA case studies celebrate private sector disruption, HUDCO's story offers something rarer—how to build enduring capability within government constraints, political cycles, and social mandates. The lessons aren't always intuitive, often contradicting conventional business wisdom.

Lesson 1: Political Cycles Are Features, Not Bugs

Private companies fear political change; HUDCO has learned to surf it. Every new government arrives with new priorities—Housing for All, Smart Cities, AMRUT, Swachh Bharat. Rather than resisting these shifts, HUDCO adapts its lending priorities to align with political mandates. When rural housing is emphasized, HUDCO finances gram panchayat projects. When urban infrastructure becomes priority, it pivots to metro rail and water supply. This isn't opportunism—it's institutional wisdom about working with, not against, democratic politics.

The key insight: political priorities reflect genuine social needs, even if articulated through electoral lenses. By aligning with these priorities, HUDCO ensures relevance while fulfilling its mandate. The organization maintains core competencies—project appraisal, long-term lending, technical assistance—while flexing the application based on political direction.

Lesson 2: Relationships Are Balance Sheets

In development finance, relationships with state governments aren't just important—they're everything. HUDCO has cultivated these relationships over decades, through multiple political parties, bureaucratic reshuffles, and economic cycles. When a new chief secretary takes charge in a state, HUDCO already knows their career trajectory, policy preferences, and administrative style.

This relationship capital compounds. A junior engineer HUDCO worked with in the 1980s might now be a municipal commissioner. A state housing board official who received HUDCO training could become secretary of urban development. These relationships create information advantages, trust networks, and informal communication channels that no amount of technology can replicate.

Lesson 3: Technical Competence as Competitive Moat

HUDCO's edge isn't just financial—it's technical. The organization employs engineers, urban planners, and architects who understand construction costs, project timelines, and implementation challenges. When evaluating a water supply project, HUDCO officers know the difference between surface and groundwater sources, treatment plant technologies, and distribution network designs.

This technical depth serves multiple purposes. It reduces information asymmetry with borrowers, enables better project structuring, and creates value beyond lending. State governments trust HUDCO's technical assessment, often seeking input on project design before formal loan applications. This consultative approach creates switching costs—why go to another lender when HUDCO already understands your project?

Lesson 4: Patient Capital in an Impatient World

While markets obsess over quarterly results, HUDCO operates on generational timescales. A metro rail project financed today might generate returns over 30 years. An affordable housing complex's social impact unfolds over decades as communities develop. This patience isn't just philosophical—it's structural, embedded in funding sources, governance mechanisms, and performance metrics.

The patience extends to relationship building. HUDCO might work with a state for years before sanctioning major loans, building understanding and trust. When projects face delays—inevitable in Indian infrastructure—HUDCO restructures rather than recalls loans. This patience is reciprocated: states prioritize HUDCO dues even during fiscal stress because they know HUDCO will be there during the next crisis.

Lesson 5: The Paradox of Standardization and Flexibility

HUDCO has developed standardized processes refined over decades—loan appraisal formats, risk assessment frameworks, documentation requirements. These standards ensure consistency and reduce errors. Yet within this standardization lies remarkable flexibility. Each state has unique challenges, each project specific requirements. HUDCO adapts its standard products to local contexts without compromising core principles.

Consider how HUDCO finances tribal area housing differently from urban slum rehabilitation, how coastal infrastructure projects account for cyclone risks while hill state projects factor in seismic concerns. This isn't multiple products but one product—development finance—infinitely customized while maintaining standardized risk management.

Lesson 6: Managing the Social-Commercial Tension

Every HUDCO decision involves balancing social mandate with financial viability. Should it finance a marginally viable sewerage project in a poor district? Should lending rates reflect true risk or social priority? These aren't questions with correct answers but tensions to be managed.

HUDCO's approach is portfolio-based. Some projects generate strong returns, others deliver social impact. The portfolio as a whole must be financially sustainable while fulfilling the social mandate. This requires sophisticated cross-subsidization—urban infrastructure loans supporting rural housing, commercial projects enabling social schemes. It's financial engineering with a social purpose.

Lesson 7: Institutional Memory as Strategic Asset

In a country where government officials transfer every few years and private sector employees job-hop frequently, HUDCO's institutional memory is remarkable. Senior officers often spend entire careers at HUDCO, accumulating deep expertise. The organization remembers what worked and what didn't in previous housing schemes, why certain states defaulted in the 1990s, how specific cities managed infrastructure projects.

This memory isn't just archived—it's actively deployed. When Gujarat wants to replicate Tamil Nadu's housing success, HUDCO knows the nuances. When northeastern states seek infrastructure finance, HUDCO understands terrain-specific challenges from previous projects. This institutional memory reduces repeated mistakes and accelerates learning curves.

Lesson 8: The Power of Boring

In a financial sector obsessed with innovation, HUDCO's stability seems boring. Same business model for decades, same types of borrowers, same patient approach. But this boring stability is a feature. States know exactly what HUDCO offers, how it operates, what it expects. This predictability reduces transaction costs and enables long-term planning.

The boringness extends to financial management. No exotic derivatives, no aggressive treasury bets, no complex structuring. Just straightforward lending at reasonable spreads with careful risk management. In a sector littered with spectacular failures from excessive innovation, HUDCO's boring consistency looks like wisdom.

The playbook's meta-lesson might be the most important: excellence in public sector requires different metrics than private sector success. It's not about maximizing profits or growth rates but optimizing social impact within financial sustainability. It's not about disrupting markets but completing them. It's not about individual brilliance but institutional capability. HUDCO's playbook won't produce unicorns or stock market darlings. But it has housed millions, built cities, and proven that public sector excellence, while rare, is possible.

X. Bear vs Bull Case & Competitive Landscape

The investment community remains split on HUDCO, and the arguments on both sides are compelling. The stock return of -28.25% over last year despite 24.8% profit increase encapsulates this confusion—the numbers say one thing, the market believes another. Understanding this disconnect requires examining both the bear and bull cases, then placing HUDCO within India's evolving financial landscape.

The Bear Case: Structural Headwinds

Bears point first to growth—or lack thereof. Sales growth of 6.38% over past five years in an economy growing at 7%+ suggests HUDCO is losing relevance. This isn't cyclical weakness but structural decline as private capital increasingly finances infrastructure. Why would states borrow from HUDCO when bond markets offer competitive rates and banks compete aggressively for government business?

The ROE of 13.5% over 3 years is another red flag. In a financial sector where leading players generate 15-20% ROEs, HUDCO's returns look pedestrian. The low interest coverage ratio suggests thin margins vulnerable to any cost pressure. If funding costs rise or asset quality deteriorates, profitability could evaporate quickly.

Competition is intensifying from every direction. Banks like SBI have massive balance sheets and government relationships. Private NBFCs like Piramal Capital or Edelweiss are aggressively entering infrastructure finance. International institutions like ADB and World Bank offer concessional financing for development projects. New entities like NIIF are purpose-built for infrastructure investment. Where does HUDCO fit in this crowded landscape?

The 75% government holding creates additional concerns. Political interference could direct lending toward unviable projects. Bureaucratic decision-making might miss opportunities that nimbler competitors capture. The talent constraint is real—why would top professionals join HUDCO when private alternatives offer better compensation and career growth?

Technology disruption looms large. While HUDCO processes loans through traditional bureaucratic channels, fintech platforms are reimagining infrastructure finance. Blockchain could revolutionize project monitoring, AI could transform risk assessment, digital platforms could intermediate between projects and capital. HUDCO's minimal technology investment suggests it might be disrupted rather than disruptor.

The market structure is evolving unfavorably. As corporate bond markets deepen, large infrastructure players can access capital directly. State governments are exploring innovative financing mechanisms—land value capture, municipal bonds, PPP structures—that bypass traditional lenders like HUDCO. The intermediation role that justified HUDCO's existence is being questioned.

The Bull Case: Irreplaceable Institution

Bulls see the same facts differently. The steady growth isn't weakness but stability in a volatile sector. While flashy NBFCs have imploded and banks struggle with infrastructure NPAs, HUDCO continues its boring march forward. The low NPAs aren't luck but result of decades of expertise in government lending.

Government backing isn't burden but moat. The implicit sovereign guarantee allows HUDCO to borrow at rates private players can't match. The relationships with state governments, built over 50 years, create switching costs competitors can't overcome. When the next crisis hits—and it will—states will turn to HUDCO, not fair-weather private lenders.

The infrastructure opportunity is massive. India needs $1 trillion in infrastructure investment over the next decade. Even if HUDCO captures a small share, the growth potential is enormous. The focus on affordable housing and urban infrastructure aligns perfectly with government priorities, ensuring policy support and business flow.

The Navratna status allows HUDCO to operate more independently and efficiently. The 'Navratna status' is accorded to Public Sector Undertakings (PSUs) who are authorized to take up investments of up to ₹1,000 crore without Central nod. They have the room to invest up to 30% of their net worth within a year as long they adhere to the ₹1,000 crore threshold. This operational freedom could accelerate decision-making and improve competitiveness.

The valuation discount is opportunity, not warning. HUDCO trades at significant discount to book value and private housing finance companies. Any improvement in perception could drive rerating. The dividend yield provides cushion while waiting for recognition. Patient investors could be rewarded handsomely when the market discovers HUDCO's hidden value.

The balance sheet strength provides optionality. With low NPAs and comfortable capital adequacy, HUDCO could leverage up significantly if opportunities arise. The conservative management might be storing dry powder for the next infrastructure boom. When that comes, HUDCO will be ready while aggressive competitors might be nursing wounds from current excesses.

Competitive Dynamics: The Messy Middle

The reality is that HUDCO operates in an increasingly complex competitive landscape where traditional boundaries are blurring. Banks want to be NBFCs, NBFCs want to be fintech, fintech wants to be everything. In this chaos, HUDCO's focused approach might be advantage, not limitation.

Consider the competitive segments:

Against banks, HUDCO can't match scale but offers specialization. Banks treat infrastructure as one product among many; for HUDCO, it's everything. This focus enables deeper expertise, better project assessment, and patient capital that banks' quarterly-focused management can't provide.

Versus private NBFCs, HUDCO lacks agility but offers stability. Private players might offer better terms during boom times, but they retreat during busts. HUDCO's counter-cyclical lending makes it valuable partner for states that need consistent support across cycles.

Compared to international institutions, HUDCO provides local expertise. While World Bank funding comes with conditions and lengthy processes, HUDCO understands Indian administrative systems, political realities, and implementation challenges. This local knowledge is invaluable for project success.

Against capital markets, HUDCO offers simplicity. Bond issuances require ratings, documentation, and market timing. HUDCO provides straightforward lending with predictable terms. For smaller states or specialized projects, HUDCO's traditional approach might be more practical than capital market alternatives.

The Valuation Puzzle

Why does the market discount HUDCO so heavily? The answer might be that markets don't know how to value institutions that operate outside conventional frameworks. HUDCO isn't trying to maximize profits or growth. It's fulfilling a social mandate while maintaining financial sustainability. Traditional valuation metrics—P/E ratios, P/B multiples, DCF models—struggle to capture this dual objective.

The discount might also reflect time horizon mismatch. Markets focus on next quarter's results; HUDCO's value unfolds over decades. The infrastructure financed today generates returns over 30 years. The affordable housing built now creates social value for generations. Patient capital might recognize this value, but patient capital is increasingly rare in public markets.

XI. The Future: Challenges & Opportunities

The next decade will determine whether HUDCO remains relevant infrastructure financier or becomes anachronistic relic. The forces reshaping India—urbanization, digitization, climate change, demographic transition—create both existential challenges and transformational opportunities. HUDCO's response will define not just its future but the trajectory of infrastructure finance in India.

The $2 Trillion Urban Opportunity

India's urban population will reach 600 million by 2035, requiring unprecedented infrastructure investment. Cities need everything—housing, water supply, sewerage, transportation, solid waste management. The investment requirement exceeds $2 trillion, far beyond government capacity or private sector appetite. This isn't just opportunity; it's necessity. Without adequate infrastructure, urbanization becomes crisis rather than growth driver.

HUDCO is uniquely positioned to capture this opportunity, but positioning isn't enough. The organization needs to scale dramatically—not 6% annual growth but 15-20%. This requires fundamental changes: faster decision-making, larger ticket sizes, innovative products. The comfortable incrementalism of past decades won't suffice when urban infrastructure needs are growing exponentially.

The nature of urban development is also changing. Smart cities require integrated infrastructure—not just physical assets but digital layers. HUDCO must finance not just roads but intelligent transportation systems, not just water supply but smart meters and IoT sensors. This requires new expertise, different risk assessment, and comfort with technology that HUDCO currently lacks.

Climate Resilience: The Unavoidable Imperative

Climate change isn't future risk but present reality. Cities flood annually, water scarcity is chronic, heat waves are deadly. Infrastructure built today must survive climate impacts over 50-year lifespans. This fundamentally changes project economics, design requirements, and financing needs.

HUDCO could become India's green finance champion, but this requires more than rebranding existing products. Green bonds, climate-resilient infrastructure, renewable energy integration—these aren't buzzwords but necessities. International climate finance is available, but accessing it requires sophistication in ESG reporting, climate risk assessment, and green certification that HUDCO must develop.

The opportunity is massive. India's climate adaptation needs exceed $200 billion. Retrofitting existing infrastructure for climate resilience could be even larger. HUDCO's relationships with cities and states position it perfectly to channel climate finance. But competition from international green funds and sustainability-focused NBFCs is intensifying.

Digital Transformation or Digital Disruption

Technology will reshape infrastructure finance whether HUDCO participates or not. Blockchain can revolutionize project monitoring and fund utilization. AI can transform risk assessment and early warning systems. Digital platforms can connect projects with capital more efficiently than traditional intermediation.

HUDCO's technology adoption has been minimal—basic digital operations rather than transformation. This must change. Not because technology is fashionable but because it's essential for competitiveness. States increasingly expect digital interfaces, real-time monitoring, and data-driven insights. Young bureaucrats are digital natives who won't tolerate paper-based processes.

But digital transformation for HUDCO isn't about copying fintech playbooks. It's about enhancing core strengths—using technology to deepen government relationships, improve project assessment, and scale technical assistance. The goal isn't to become tech company but to use technology to be better development financier.

The Talent Challenge

HUDCO's workforce is aging, and attracting young talent is increasingly difficult. Why would talented professionals choose HUDCO over private NBFCs, banks, or startups? Public sector job security isn't attractive to generations valuing growth and impact over stability.

The talent challenge isn't just about compensation—though that matters. It's about purpose, culture, and career development. HUDCO needs to articulate why development finance matters, why public service is meaningful, why building India's infrastructure is exciting. This requires cultural transformation, not just HR policies.

The skill requirements are also evolving. Traditional engineering and finance expertise remains important, but HUDCO needs data scientists, climate specialists, and digital architects. Building this capability requires partnerships with universities, exchange programs with international institutions, and willingness to hire unconventionally.

Competition from New-Age Players

The competitive landscape is evolving rapidly. Fintech platforms are exploring infrastructure finance, seeing opportunity in digitizing traditional processes. International funds are establishing Indian presence, attracted by growth potential. Pension funds and insurance companies are increasing infrastructure allocation, seeking long-term stable returns.

These new competitors bring advantages—technology, capital, and innovation. But they lack what HUDCO has—relationships, expertise, and trust. The question is whether HUDCO can modernize fast enough to remain relevant while these players are still building capabilities.

The collaboration opportunity might be more interesting than competition. HUDCO could partner with fintech for digital capabilities, with international funds for climate finance, with pension funds for long-term capital. Instead of defending turf, HUDCO could become platform that connects various players with infrastructure opportunities.

Regulatory Evolution

The regulatory landscape is shifting. Basel III norms are tightening capital requirements. ESG regulations are mandating climate disclosure. Digital lending regulations are evolving. HUDCO must navigate this changing landscape while maintaining its social mandate.

But regulatory evolution also creates opportunities. The government's infrastructure push might lead to favorable regulations for development finance institutions. Green finance incentives could benefit HUDCO's climate-focused lending. The National Infrastructure Pipeline creates framework for systematic infrastructure development that plays to HUDCO's strengths.

The Strategic Choices

HUDCO faces fundamental strategic choices that will define its future:

Scale vs. Stability: Should HUDCO aggressively grow to capture infrastructure opportunity, accepting higher risks? Or maintain conservative approach, accepting slower growth but ensuring stability?

Specialization vs. Diversification: Should HUDCO deepen focus on core segments—affordable housing and urban infrastructure? Or diversify into new areas like renewable energy and digital infrastructure?

Competition vs. Collaboration: Should HUDCO compete directly with private players? Or position itself as complementary institution focusing on segments others won't serve?

Technology adoption vs. Traditional strengths: Should HUDCO invest heavily in digital transformation? Or focus on enhancing traditional relationship-based model?

These aren't binary choices but spectrums requiring careful calibration. The answers will determine whether HUDCO thrives or merely survives in India's infrastructure finance future.

XII. Closing Thoughts & Key Takeaways

After traversing five decades of HUDCO's journey—from a ₹2 crore experiment to a ₹42,000 crore institution—we arrive at a peculiar conclusion: this might be India's most important company that nobody knows about. Not because of its size or profitability, but because of what it represents: the possibility of effective public sector enterprise in a market economy.

HUDCO's story challenges conventional narratives about Indian business. While we celebrate private sector unicorns and digital disruption, HUDCO has quietly financed the physical infrastructure that makes modern India possible. Those 192 lakh housing units aren't just statistics—they're homes where children study, families gather, and dreams take root. The urban infrastructure financed isn't just pipes and roads—it's the foundation of economic activity that generates livelihoods for millions.

The unsung hero narrative is compelling but incomplete. HUDCO isn't perfect—the slow growth, modest returns, and technological lag are real weaknesses. But these weaknesses stem from the same source as its strengths: the commitment to serving segments that pure market forces ignore. This is the eternal tension of development finance—being commercial enough to sustain operations while being social enough to justify existence.

What HUDCO really offers is proof of concept: patient capital can coexist with quarterly capitalism, public purpose can align with financial discipline, and government ownership doesn't necessarily mean inefficiency. In a world increasingly polarized between state and market fundamentalism, HUDCO represents a middle path—using market mechanisms for public purposes.

The lessons for global development finance are significant. As developing countries grapple with infrastructure gaps, climate adaptation, and inclusive growth, the HUDCO model offers insights. Not as template to copy—every country has unique contexts—but as demonstration that innovative institutional arrangements are possible.

For investors, HUDCO presents a philosophical challenge. How do you value an institution whose success isn't measured in stock price but in social impact? The market's confusion about HUDCO reflects deeper uncertainty about purpose of finance. Is it purely to generate returns? Or to enable development that creates conditions for broader prosperity?

The pragmatic investor might focus on the numbers: steady dividends, improving asset quality, massive infrastructure opportunity. The patient investor might see the rerating potential as markets eventually recognize HUDCO's unique position. The socially conscious investor might value the impact—investing in HUDCO is indirectly financing India's development.

But perhaps the most important takeaway isn't about HUDCO specifically but what it represents for India's development trajectory. As India aspires to developed country status, institutions like HUDCO become crucial. They channel capital to segments that need it most, ensure development is inclusive rather than concentrated, and provide stability during economic turbulence.

The next decade will test whether HUDCO can evolve while maintaining its essence. Can it adopt technology without losing human touch? Can it scale operations without compromising prudence? Can it remain relevant as India's financial markets mature? The answers will determine not just HUDCO's future but the nature of development finance in emerging economies.

The story we've traced—from post-partition housing crisis to smart cities, from government monopoly to public listing, from manual processes to digital aspirations—isn't just corporate history. It's the story of institution building in developing country, of balancing market and state, of serving public purpose while maintaining financial discipline.

As India stands at inflection point—demographic dividend meeting infrastructure deficit, urbanization accelerating amid climate change, digital revolution reshaping everything—HUDCO's role becomes more critical. Not as sole solution but as essential piece of complex puzzle. The boring stability that markets discount might be exactly what India needs as anchor in turbulent times.

The final paradox is that HUDCO's greatest success might be making itself unnecessary. If India develops deep, efficient capital markets that serve all segments, if private capital flows to affordable housing and basic infrastructure, if financial inclusion becomes reality rather than aspiration—then HUDCO's mission is accomplished. But until that distant day, HUDCO remains what it has always been: the institution that does what others won't, finances what others ignore, and builds what India needs.

This isn't story with neat conclusion because it's still being written. Every loan sanctioned, every project financed, every house built adds another line. The stock price might fluctuate, governments might change, technologies might disrupt—but the fundamental need HUDCO addresses remains. As long as India has infrastructure gaps, housing shortages, and excluded populations, HUDCO has purpose.

Perhaps that's the ultimate takeaway: in obsessing over growth rates and stock returns, we might miss the deeper value of institutions that prioritize purpose over profit. HUDCO won't make anyone rich quickly, won't feature in breathless business headlines, won't disrupt anything dramatically. But it will continue doing what it has done for 55 years—quietly, steadily, persistently building the India that should be from the India that is.

For those who measure success differently—in families housed rather than profits earned, in cities built rather than stocks pumped, in inclusive development rather than concentrated wealth—HUDCO offers different kind of return. Not the return on investment that markets track, but return on society that nations need. In the end, that might be the most valuable return of all.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube