Himadri Speciality Chemical: The Carbon King's Electric Pivot

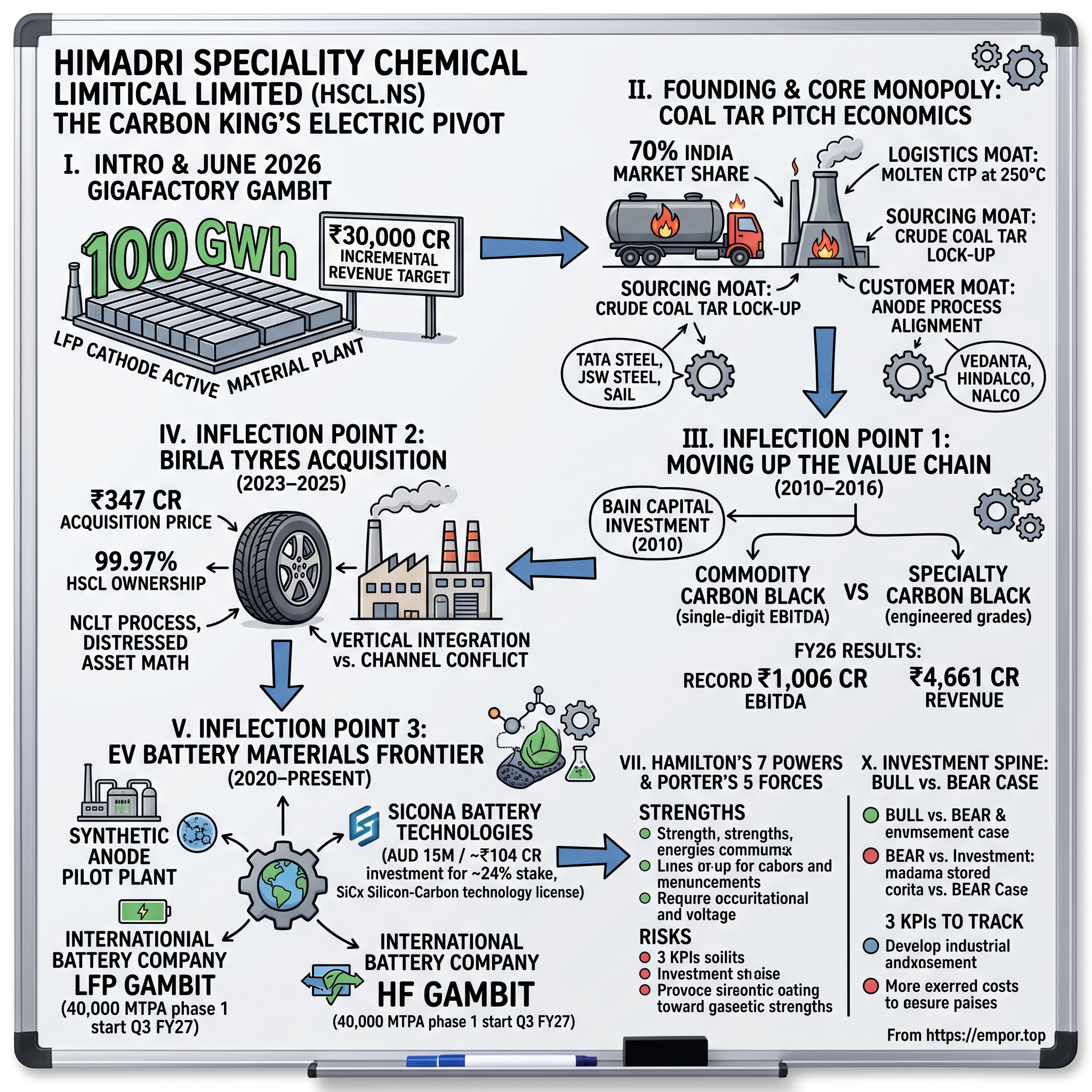

I. Introduction & The June 2026 Gigafactory Gambit

Picture a sprawling industrial yard on the banks of the Hooghly River in West Bengal. The air is thick with the unmistakable, acrid smell of distilling coal tar — a black, viscous, almost medieval substance that has been boiled and fractionated on this site for more than three decades. Fleets of squat, insulated tanker trucks idle in the heat, their cargo held at a scalding 250 degrees Celsius so it does not solidify into rock before it reaches an aluminum smelter a thousand kilometers away. This is the smell of money in heavy industry. It is also, on the face of it, about the least glamorous business imaginable.

Now hold that image, and consider the announcement that landed in the summer of 2026. Himadri Speciality Chemical Limited — the company that owns that pungent yard — laid out a plan to build battery materials capacity equivalent to 100 gigawatt-hours of lithium-ion cells, anchored by what it described as India's first dedicated Lithium Iron Phosphate (LFP) cathode active material plant, with management dangling a target of roughly ₹30,000 crore of incremental revenue over the following five to six years.1 For a company whose entire FY26 revenue was around ₹4,661 crore, that is not a growth plan. That is a proposed reincarnation.2

So here is the question that animates this entire episode: how does a company that spent decades distilling the dirtiest residue of the steel industry end up positioning itself as the would-be backbone of India's clean-energy supply chain? How does a coal tar distiller credibly claim it can build a cathode plant that, if it works, would be one of the first of its scale anywhere outside China?

The honest answer — and we will keep coming back to this — is that nobody knows yet, including Himadri's management. What we can do is trace the logic, separate the proven from the promised, and stress-test the story the way a skeptical long-term investor would.

The roadmap for this episode runs as follows. First, the dirty, boring, deeply profitable B2B core that funds everything else: coal tar pitch (CTP) and carbon black, where Himadri occupies a genuinely fortified position in the Indian market. Second, the two strategic pivots that quietly rewrote the company's financial DNA — the move "up the value chain" into specialty carbon black, and the institutionalization that began when Bain Capital wrote a check in 2010. Third, the controversial capital-allocation calls that make this a debate rather than a victory lap: buying a bankrupt tire maker out of insolvency court, and sprinkling minority bets across battery startups in Australia and the United States. And finally, the big one — the "Himadri Reloaded" thesis — where we ask whether this is a textbook case of using monopoly cash flows to buy asymmetric upside, or a cash-rich industrial company talking itself into a capital-destroying bubble.

Let us be clear about the posture here. Himadri's core business is real, it throws off cash, and its competitive position is unusually defensible for a commodity-adjacent chemical company. None of that automatically means the LFP gamble pays off. Those are two separate claims, and the market in mid-2026 — with the stock trading at record highs above ₹700 — appeared to be pricing in success on both. Our job is to keep them separate.9

To understand whether the electric future is plausible, you first have to understand the carbon kingdom that pays for it. And that story starts not with batteries, but with the foul-smelling byproduct of a coke oven.

II. Founding & The Core Monopoly: Coal Tar Pitch Economics

In 1987, a member of the Choudhary family in Kolkata incorporated a modest enterprise called Himadri Castings Private Limited. The name tells you the original ambition: castings, basic metallurgical work — the kind of small industrial outfit that dotted West Bengal in the late license-raj years. It was not destined for greatness in that form. Within a few years, the family made the pivot that would define everything: around 1990, they turned to coal tar distillation.[^7]

This was not a visionary leap into a hot sector. Coal tar distillation in 1990s India was about as far from a hot sector as you could get. It was capital-intensive, environmentally messy, and dependent on the fortunes of the steel and aluminum industries. But it had one quiet virtue that the family seems to have grasped early: once you are good at it and embedded with your suppliers and customers, almost nobody can dislodge you. The boring business became indispensable. That is the whole story in miniature.

What exactly is coal tar pitch, and why should anyone care?

Let us demystify the product, because the entire moat rests on understanding it. When steel plants run coke ovens — baking coal at high temperatures to make the coke that feeds blast furnaces — they generate a thick, black, foul liquid byproduct called crude coal tar. To the steel mill, this is waste, a nuisance to be sold off. Himadri buys this crude tar and distills it, much as an oil refinery fractionates crude petroleum, separating it into more valuable streams. The heaviest, stickiest fraction left behind is coal tar pitch.

Why does pitch matter? Because it is the indispensable binder in two processes most people never think about. First, aluminum. You cannot smelt aluminum without carbon anodes, and you cannot make carbon anodes without a binder that glues petroleum coke particles together and then bakes into a solid, conductive block. That binder is coal tar pitch. There is a useful way to hold this in your head: no pitch, no anode; no anode, no aluminum. Second, electric-arc-furnace steelmaking and other industries need graphite electrodes — and pitch is again the binder. Himadri's product sits at the literal foundation of two heavy industries, which is precisely why a smelly residue can be a strategically vital input.

The structural near-monopoly

Himadri came to control on the order of 70% of India's coal tar pitch market — a dominance that did not come from a single clever move but from a self-reinforcing logistics-and-sourcing machine that is genuinely hard to copy.[^7]

Start with the logistics nightmare, which is actually the moat. Liquid coal tar pitch has to be kept hot — around 250 degrees Celsius — throughout transport, or it cools and hardens into a useless solid mass inside the tanker. Himadri runs a proprietary fleet of specialized, heated, insulated tankers that carry molten pitch thousands of kilometers across India to smelters. Think about what that means for a would-be competitor: it is not enough to build a distillation plant. You also have to replicate a continent-spanning fleet of custom hot-haul trucks and the operational know-how to keep a temperamental material liquid across India's roads and heat. The product is hard to make and even harder to deliver — and the delivery problem is the part rivals consistently underestimate.

Then there is the sourcing moat, which is arguably the deeper one. Himadri is the single largest buyer of crude coal tar in India, with long-term feedstock arrangements tied to the country's major steel producers — the likes of Tata Steel, JSW Steel, and SAIL. By locking up the raw material at the source, Himadri does something quietly powerful: it doesn't just win customers, it denies competitors their feedstock. A new entrant cannot simply decide to enter the pitch business, because the crude tar it would need is already spoken for. This is the cornered-resource dynamic we will return to in the powers analysis — control the input, and you control the industry.

Finally, the customer side. On the demand end sits a consolidated oligopoly: India's aluminum giants — Vedanta, Hindalco, and the state-owned NALCO — plus graphite-electrode makers like HEG and Graphite India. These are multi-decade relationships, and they are sticky for an unglamorous but powerful reason we will unpack later: smelters calibrate their entire anode process to the specific chemistry of their pitch supplier. Switching is not a procurement decision; it is a production risk.

What does all this mean for an investor? It means the base business is not really a commodity business in the way the smelly product would suggest. It is a logistics-and-relationships business wearing a commodity's clothes. The downside is genuinely protected; the feedstock is locked; the customers are captive for technical reasons. That protected cash flow is the war chest. The interesting question — the one management has been answering for fifteen years — is what to do with it. The first answer was to stop being a pure commodity player at all.

III. Inflection Point 1: Moving Up the Value Chain (2010–2016)

For most of its early life, Himadri was a classic family-run Indian industrial — competent, conservative, and opaque in the way such companies often are. The first jolt toward something more came in 2010, and it came from an unlikely source: a global private equity firm decided this coal tar distiller in West Bengal was worth institutional money.

The Bain Capital catalyst

In 2010, Bain Capital invested roughly ₹250 crore for a minority stake in Himadri — on the order of 15% of the company.[^7] On paper this was just a growth-capital deal. In practice it was a culture transplant. Bain's involvement nudged the family-led structure toward institutional-grade governance, board discipline, and the kind of long-horizon capital allocation thinking that distinguishes a company that compounds from one that merely survives. You can debate how much credit any single investor deserves, but the trajectory afterward — the professionalization, the willingness to make multi-year bets, the eventual courting of public-market investors — is consistent with a company that learned to think in decades rather than quarters.

The commodity trap

To appreciate the next pivot, you have to feel the pain that motivated it. Alongside pitch, Himadri makes carbon black — a fine black powder produced by the controlled, partial combustion of heavy oils. The bread-and-butter version, rubber-grade carbon black, goes into tires as a reinforcing filler. It is essential, it is high-volume, and it is brutally commoditized. Its profitability is hostage to two cycles management cannot control: the price of crude-oil-derived feedstock and the boom-bust of tire manufacturing. In the lean years, this business ran at single-digit EBITDA margins — roughly 5 to 10% — which is the financial equivalent of running on a treadmill.

Management looked at that treadmill and made a decision that, in retrospect, was the most important commercial choice in the company's history before the EV pivot: stop competing on price, and start competing on chemistry.

The pivot to specialty carbon black

Between roughly 2014 and 2016, Himadri leaned into specialty carbon black — grades engineered for demanding, non-tire applications: engineering plastics, synthetic fibers, coatings, and high-end printing inks. These are not sold by the truckload at spot prices; they are qualified into customers' formulations, command meaningful premiums, and carry margins that can run at multiples of the commodity grade. The strategic logic was simple and sound: if you cannot escape a cyclical commodity, change what you sell so the cycle matters less.

The company signaled the seriousness of the shift in its very identity. In 2016 it renamed itself from "Himadri Chemicals & Industries" to "Himadri Speciality Chemical Limited" — putting the word "speciality" in the masthead as both a promise to investors and a discipline on itself.[^7]

The financial proof point

Here is where we test the story against the numbers, because a rebrand is cheap and margin expansion is not. The proof arrived in the FY26 results. Himadri reported record EBITDA of ₹1,006 crore — crossing the ₹1,000-crore threshold for the first time — on revenue of about ₹4,661 crore, with profit after tax of roughly ₹755 crore, up sharply year on year.2 The standout is not the top line, which was essentially flat against FY25's ₹4,613 crore; it is that EBITDA still climbed about 19% and PAT about 36%.2

Read that carefully, because it is the single most important sentence about the legacy business. Profits grew strongly while revenue barely moved. That is the financial signature of a mix shift — the company sold a more valuable basket of products from broadly the same volume, pushing the EBITDA margin up toward the low-20s percent range, against the roughly 12% the blended business earned a few years prior. The engine of that expansion was the ramp of high-margin specialty grades, including the large Mahistikry specialty carbon black facility that management has touted as among the largest single-location plants of its kind.2[^3]

For an investor, the takeaway is concrete and it is the foundation of the bull case: management said it would expand margins by going specialty, and over a multi-year window it did. That earned execution credibility is the asset Himadri is now spending — borrowing against, in a sense — to fund the far riskier chapters. The first place it spent it was not a battery plant. It was a bankruptcy court in Kolkata.

IV. Inflection Point 2: The Birla Tyres NCLT Acquisition (2023–2025)

There is a particular kind of asset that fascinates and terrifies investors in equal measure: the distressed industrial carcass. A factory that someone spent a fortune building, that then went bankrupt, and that now sits half-alive in an insolvency proceeding, available for cents on the rupee — if you are brave enough, or foolish enough, to take it on. In October 2023, Himadri walked into exactly that situation and bought one.

The transaction

The target was Birla Tyres Limited — a once-iconic Indian tire brand that had collapsed into insolvency under India's bankruptcy code. Himadri did not go alone at first; it teamed with Dalmia Bharat Refractories, and the Kolkata bench of the National Company Law Tribunal (NCLT) approved their joint resolution plan in October 2023, after the committee of creditors had signed off with a vote share north of 80%.5 The headline price was ₹347 crore.5 Then, over the following eighteen months, Himadri tightened its grip: by April 2025, having bought out Dalmia's interest and converted debentures, it held essentially the entire company — about 99.97%.[^7]

Benchmarking the capital deployment

Was ₹347 crore a good price? This is where you have to think like a distressed-asset investor rather than a growth investor, and the math is genuinely interesting. The liquidation value of the asset — what you would get by selling off the bricks and machines — was pegged around ₹335 crore, meaning Himadri paid only a sliver above scrap value.5 Birla Tyres had carried admitted debts well above ₹1,100 crore; the lenders, in approving the plan, swallowed a haircut on the order of 70%.5 That is the brutal arithmetic of the insolvency code: someone lost a fortune so that someone else could buy cheap.

Now run the greenfield comparison, which is the real argument for the deal. Building a comparable tire plant from scratch would plausibly cost ₹1,000–1,500 crore and take three to four years of construction and ramp. Himadri instead took physical possession of the Balasore plant in Odisha — including around 190 acres of land, a completed passenger-car-radial (PCR) line, and a recognized domestic brand — for a fraction of replacement cost, and funded it entirely out of internal cash accruals rather than fresh debt or equity.[^7] On a pure dollars-of-asset-per-rupee-spent basis, it is hard to argue this was expensive. The downside is capped near liquidation value; the upside, if the plant can be revived, is leveraged to the gap between scrap value and a functioning factory.

The strategic paradox

So far, so clever. But here is where the skeptic plants a flag, and the question is sharp enough that it deserves to sit unresolved. On paper, Birla Tyres is forward integration — Himadri makes carbon black, tires consume carbon black, so why not capture the downstream margin by making tires yourself? Vertical integration, the analysts nod approvingly.

Except: who buys Himadri's rubber-grade carbon black? India's tire majors — MRF, Apollo, CEAT, JK Tyre. By reviving Birla Tyres, Himadri has made itself a direct competitor to its own customers. This is the textbook channel-conflict trap. A purchasing manager at a major tire company now has to weigh whether buying carbon black from Himadri means feeding a rival's cost structure. Management can argue, plausibly, that Birla Tyres is small relative to the majors and operates in segments where the conflict is limited — but the structural tension is real and is not waved away by a slide deck. The bull frames it as integration; the bear frames it as a few hundred crores of cash quietly poisoning relationships in the much larger carbon black book. Both readings are defensible on today's facts, which is exactly why this remains a live debate rather than a settled win.

What is not in dispute is the pattern it reveals about management's temperament: a willingness to make unconventional, contrarian capital-allocation bets that do not fit the tidy narrative of a focused specialty chemicals company. Hold that thought, because the next set of bets is far larger, far stranger, and far less proven — and it points away from tires and toward the electrons.

V. Inflection Point 3: The EV Battery Materials Frontier (2020–Present)

Every transformation story has a moment where the protagonist looks at what they already own and sees it differently. For Himadri, that moment was the realization that the same coal tar chemistry that binds aluminum anodes also sits one or two refining steps away from the materials inside a lithium-ion battery.

The realization

Strip a modern battery cell down to its two electrochemical halves and you find carbon everywhere. The anode — the negative electrode — is overwhelmingly made of graphite, and increasingly of synthetic graphite produced from needle coke, a high-purity, highly crystalline coke that is itself a derivative of coal tar pitch. The cathode — the positive electrode — is where the chemistry wars are fought, and in 2026 the chemistry winning the volume battle globally for mass-market EVs and storage is LFP, lithium iron phosphate, prized for being cheaper and safer (if less energy-dense) than the nickel-rich alternatives.

Here is the connective tissue that makes Himadri's pivot more than a press release: the company already makes needle coke from coal tar pitch for its existing industrial businesses. If it can purify that coke to battery grade, it has a credible path into synthetic anode material without starting from zero. That is a genuine, asset-backed reason to believe — distinct from the cathode ambition, where Himadri has no comparable incumbency and is essentially building a new competence.

The synthetic anode monopolist-in-waiting

On the anode side, Himadri's claim is the most grounded part of the entire EV story. The company began operating a pilot-scale plant — on the order of a few hundred tonnes of annual capacity — to produce synthetic anode material and, critically, to get it qualified with global cell makers.[^3] That word, qualified, matters more than the tonnage. Battery cell manufacturers do not casually swap anode suppliers; the material has to be tested, validated, and designed into the cell over many months. Clearing qualification is the real barrier, and a pilot line is exactly how you start. Management has framed FY26 as the year it commissioned its first anode material production capability.2 This is the part of the EV thesis where Himadri is competing from a position of existing chemistry strength rather than ambition alone.

The strategic investments

To leapfrog into next-generation technology and secure customers, Himadri spent the 2023–2026 window assembling a portfolio of minority stakes — buying optionality and access rather than building everything in-house.

The first is Sicona Battery Technologies, an Australian developer of silicon-carbon anode materials. Silicon is the holy grail additive for anodes: blended into graphite at roughly 5–20%, Sicona's SiCx material claims to lift energy density by around 20% and charging performance by around 40%, addressing the two things every EV buyer complains about — range and charge time.3 Himadri committed capital — figures cited around AUD 15 million / roughly ₹103.95 crore via cash and convertible notes — for a stake that started near 17.6% and was set to rise toward 24% as notes convert.3 But the more valuable prize was contractual: Himadri secured exclusive rights to localize and manufacture Sicona's anode technology in India.3 That is the structure to watch — a relatively small equity check that buys a technology license and a head start, rather than a controlling ownership position.

The second is International Battery Company (IBC), a US-based cell startup. Himadri built its stake in steps — an initial 16.24% for about USD 4.43 million in May 2025, raised to 20.47% with a further USD 0.66 million by June 2026, bringing the cumulative investment to roughly USD 6.09 million.4 Why a cell maker? Because IBC is building a gigafactory in Bengaluru and is developing an LFP-based cell line — its "Prabal 2000" — designed to use Himadri's cathode and anode materials.4 In other words, Himadri is paying a modest sum to wire in a captive, aligned offtake partner: a customer with a contractual and equity reason to buy the materials Himadri intends to make. For a company about to build a cathode plant with no track record in cathodes, securing a friendly first buyer is not a nicety; it is close to a precondition.

The 100 GWh LFP gamble

Which brings us to the centerpiece, and the single biggest unproven swing in this entire story. Himadri laid out plans for an LFP cathode active material plant in Odisha, beginning with a first phase of 40,000 MTPA at an estimated investment of around ₹1,125 crore, scaling toward 200,000 MTPA over five to six years — the capacity management maps to roughly 100 GWh of battery cells and the ₹30,000-crore revenue aspiration.1 The first milestone capacity is targeted to begin around Q3 FY27, with the full first phase ramping over the following year and FY29 framed as the year of full operations.1

Now the sober read. India produces essentially no LFP cathode material at scale today; China dominates the global supply chain. If Himadri pulls this off, it is genuinely strategic — a domestic, non-Chinese cathode source in a world increasingly anxious about supply-chain concentration. But "first in India" cuts both ways: there is no domestic playbook to copy, the technology and process know-how have to be acquired or developed, and the economics must somehow survive against Chinese producers operating at vastly larger scale and lower cost. The ₹1,125 crore for phase one is real money but, by global cathode standards, a modest entry ticket. Whether that is disciplined staging or bringing a knife to a gunfight is the crux of the bear case — and it depends entirely on execution by a team whose track record is in coal tar, not cathodes. To judge that, we have to look at the people.

VI. Management Profile & Credibility Assessment

In a company attempting three transformations at once, the single most important variable is not the LFP process flow or the carbon black margin — it is the judgment of the person allocating the capital. At Himadri, that person is Anurag Choudhary.

The leader

Anurag Choudhary serves as Chairman, Managing Director, and Chief Executive Officer — a concentration of titles that itself tells you this is a promoter-driven company where one family's judgment steers the ship.6 He has been chairman of the board since July 2022, and he is the public face of the strategic reinvention, the one articulating the battery-materials vision on earnings calls and in investor presentations.6 His style, as it comes through in disclosures and calls, is that of an ambitious owner-operator: comfortable making contrarian bets, willing to deploy the core business's cash into ventures that sit far outside the company's historical competence.

Skin in the game

Here the story is, on balance, reassuring — and it is the strongest single argument that management believes its own narrative. Anurag directly holds about 8.59% of the company; the broader promoter family group owns roughly 51.63%.6 This is not a hired-gun CEO with a sliver of options and a soft landing; this is a family whose collective net worth is overwhelmingly tied to whether the EV pivot succeeds or fails.

The signal sharpened in late 2025. The promoter group converted warrants into equity — with Anurag personally paying out of pocket to pick up an additional 6,000,000 shares.[^7]6 Warrant conversions where insiders write real checks are one of the cleaner alignment signals available to an outside investor: it means the people with the most information chose to increase, not trim, their exposure at the prevailing price. It does not prove the strategy is right — insiders can be wrong with conviction — but it does mean management is eating its own cooking.

Compensation reinforces the picture. Anurag's annual pay sits around ₹4.38 crore, structured heavily toward fixed rather than variable, and modest for a company of Himadri's size and ambition.6 In a market where promoter-CEOs sometimes extract outsized packages regardless of performance, restraint here is a small but real governance positive. The wealth creation, clearly, is meant to come through the equity stake, not the paycheck.

The credibility audit

So how much should we trust the battery story? Weigh both sides honestly.

On the positive ledger: this is a management team that has actually done a hard transformation before. The pivot from commodity to specialty carbon black was not a slide — it was a multi-year operational slog that showed up in the margin line, with the FY26 EBITDA milestone as Exhibit A.2 When Himadri said years ago it would expand margins by moving up the value chain, it eventually delivered. That is the kind of promise-and-deliver track record that earns a management team the benefit of the doubt on the next promise.

On the skeptical ledger: the next promise is an order of magnitude harder. Transitioning from a B2B chemical distiller into, simultaneously, an EV battery-materials technology company and a B2C tire manufacturer is not one transformation — it is three, running in parallel, each capital-hungry, each demanding competencies the company does not historically possess. There is also the uncomfortable question of narrative and valuation. With the stock at record highs above ₹700 in mid-2026, there is a powerful incentive to keep the growth story vivid.9 A disciplined investor should ask whether the ₹30,000-crore battery revenue target functions as a genuine operating plan or partly as a valuation-support narrative — and should watch closely whether management hits the concrete near-term milestones (the Q3 FY27 cathode start, anode qualification wins) or quietly lets dates slip while the vision stays gloriously intact. Execution, not eloquence, is the test.

To frame why this management has any right to attempt such a leap, it helps to be rigorous about where the company's advantages actually come from — and where they run out. For that, two analytical lenses.

VII. Hamilton's 7 Powers & Porter's 5 Forces Applied

It is tempting, in a transformation story, to let the exciting new business dominate the analysis. But durable advantage is best assessed where the cash actually comes from today. So let us war-game Himadri's powers honestly — and note carefully that most of them protect the old kingdom, not the new frontier.

Hamilton Helmer's 7 Powers

Cornered Resource (high power, core business). The strongest of Himadri's advantages is its grip on feedstock. By being the largest buyer of crude coal tar in India and tying up supply with steel producers, Himadri effectively controls access to the raw material any pitch competitor would need.[^7] A would-be rival cannot buy what is already contracted. This is a textbook cornered resource, and it underpins the ~70% pitch share.

Process Power (high power, core business). The operational complexity of handling, storing, and moving liquid pitch at 250 degrees across a subcontinent — in a proprietary fleet of insulated heated tankers — is a capability built over decades that cannot be bought off a shelf. It is embedded in trucks, routes, people, and tacit know-how. New entrants consistently underestimate this, which is precisely what makes it powerful.

Switching Costs (moderate power, core business). Aluminum smelters and graphite-electrode makers tune their kilns and processes to the specific chemical fingerprint of their pitch supplier. Changing suppliers risks production disruption in a continuous, capital-intensive process where downtime is enormously expensive. That technical lock-in keeps customers sticky — though it is "moderate" rather than "high" because large, sophisticated buyers retain negotiating leverage on price.

Scale Economies (moderate power, core business). Himadri runs captive power — on the order of 32 MW — fed partly by waste gases recovered from carbon black manufacturing, lowering production costs in an energy-intensive process.[^7] Turning a waste stream into cheap captive power is a quietly elegant cost advantage, though it is the kind of edge competitors can partially replicate.

Notice the pattern: every one of Himadri's identifiable powers attaches to the legacy carbon business. The battery-materials venture, as of mid-2026, has no proven power of its own — no cornered resource (China controls the cathode supply chain), no demonstrated process power, no entrenched switching costs. Its potential edge is borrowed: feedstock integration from coal tar into needle coke into anode, plus licensed IP from Sicona. That is a hypothesis of future power, not present power, and investors should price it as such.

Porter's 5 Forces

Threat of new entrants — very low (core). Capital intensity, environmental permitting, the transport-logistics barrier, and raw-material lock-in combine to make entry into Indian coal tar pitch extraordinarily difficult. This is the force most favorable to Himadri.

Bargaining power of suppliers — high. The flip side of the cornered resource: crude coal tar comes from a handful of consolidated steel giants. They are the gatekeepers of the input, which gives them leverage over price even as Himadri leverages volume.

Bargaining power of buyers — moderate. Aluminum and graphite customers are consolidated and large, which gives them clout. But they have no viable domestic alternative to Himadri at scale, which blunts it. The balance is an uneasy mutual dependence rather than one-sided power.

Threat of substitutes — split, and this is the crux. For industrial coal tar pitch, substitution risk is low; there is no easy replacement binder for carbon anodes. But for battery materials, substitution risk is high and existential — competing chemistries could route around LFP cathodes or synthetic graphite anodes entirely. The old business is insulated from substitution; the new one is acutely exposed to it. That asymmetry is the single most important thing to hold in mind when valuing the transformation.

The powers analysis, then, delivers a clear verdict: Himadri is fortified where it is today and unproven where it wants to go. To sharpen that further, we have to look at who it is actually fighting.

VIII. Competitor Benchmarking: Who Does Himadri Play Against?

A company's strategy only makes sense against the competitors it has chosen to fight — and Himadri has, remarkably, picked fights on three different battlefields at once, against opponents of wildly different sizes.

The carbon black duel

In Indian carbon black, Himadri is not the heavyweight, and it is important to be honest about that. The scale leaders are PCBL Limited (the RPSG Group company formerly known as Phillips Carbon Black), commanding something like 35–40% of the domestic market, and Birla Carbon (Aditya Birla Group) with roughly 30%.7 Himadri, at around 17%, is the smaller challenger.7 PCBL has pursued scale in tire-grade volume and has diversified — notably acquiring Aquapharm to push into water-treatment specialty chemicals — while Birla Carbon brings global heft.7

Himadri's response to being outgunned on scale is instructive and consistent with its whole history: don't fight the volume war, fight the margin war. By concentrating on specialty grades, Himadri chooses the high-value niche over the price-cutting bulk game it would likely lose to larger rivals. This is a coherent strategy for a number-three player — compete where chemistry and qualification matter more than tonnage. Whether it can sustain that niche premium as the larger players also chase specialty is an open question worth tracking.

The coal tar pitch duel

Here the relevant titan is Rain Industries — a global heavyweight in coal tar pitch and calcined petroleum coke (CPC), operating at a scale Himadri does not approach internationally.8 For years the two coexisted on a kind of geographic truce: Rain dominated globally, Himadri dominated India. That truce is now under pressure. Rain has been moving to commission substantial new CTP capacity in Andhra Pradesh — a quarter-million-tonne-scale facility — which would bring a global-scale competitor directly onto Himadri's home turf for the first time in a serious way.8

This is the most underappreciated near-term competitive risk in the whole story. Himadri's ~70% domestic pitch share is the bedrock that funds the EV adventure. A credible domestic challenger at scale could pressure both volume and price in exactly the business investors are counting on for stable cash flow. It does not break the moat — the logistics and switching-cost barriers remain — but it could compress the returns from the kingdom while management is busy spending in the battery province.

The battery materials competitors

And then there is the battlefield where Himadri is the small one. Domestically, Epsilon Carbon is pursuing a similar integrated carbon-to-anode strategy, so Himadri will not have India's anode opportunity to itself. But the real benchmark is China. Firms like 杉杉股份 Shanshan and 贝特瑞 BTR dominate global anode supply, and LFP cathode is overwhelmingly a Chinese game led by players such as 德方纳米 Dynanonic, with China controlling well over 90% of the global LFP and anode supply chain.

Be blunt about the matchup. These Chinese incumbents enjoy immense scale, mature processes, deep government support, and cost curves refined over a decade of hypergrowth. Himadri's entire battery-materials capital commitment to date is a few hundred crore against rivals operating at a scale measured in tens of billions of dollars. Himadri's only plausible path is not to beat the Chinese on global cost but to win a protected domestic niche — supplying Indian and Western cell makers who want supply-chain diversification away from China, possibly aided by Indian industrial policy and tariffs. That is a real opportunity, but it is a narrower and more policy-dependent thesis than the ₹30,000-crore headline suggests. The competitive reality forces the hard questions a skeptic would press — which is exactly where we go next.

IX. Activist/Skeptical-Investor Stress Test & Current Risk Radar

Imagine a sharp-elbowed activist investor — or a thoughtful short-seller — sitting across from Anurag Choudhary at the AGM. What would they actually challenge? Not the smell of the coal tar, but the architecture of the strategy. Three questions cut deepest.

The activist challenge

Portfolio complexity and the conglomerate discount. "You are simultaneously running a coal tar utility supplying aluminum smelters, a high-tech battery-chemicals lab, and a retail tire factory. What does a specialty chemicals analyst even value you as?" This is the diworsification critique, and it has teeth. Markets tend to apply a discount to businesses that are hard to model as a single coherent entity, because complexity hides underperformance and stretches management attention. The bull answer — that it is all "carbon," from pitch to anode to tire filler — is rhetorically neat but does not erase the reality that these are three different customer bases, cost structures, and competitive dynamics.

Capital destruction risk. "You generate dependable cash from a near-monopoly. You are pouring it into an unproven LFP cathode plant and a distressed tire asset. Why should we trust that reinvestment over returning capital?" The honest rebuttal is the skin-in-the-game point — the promoter family is risking its own majority stake, not just shareholders' money. But alignment is not a guarantee of correctness. A founder can be sincerely, expensively wrong, and the structure of these bets (new competencies, brutal competition) is genuinely high-risk.

Customer alienation. The channel-conflict problem from the Birla Tyres chapter resurfaces here as a standing risk, not a one-time event: every quarter Himadri operates a tire business is a quarter its tire-major carbon black customers have a reason to look for alternative suppliers. It is a slow-burn risk, easy to dismiss in any single period and potentially corrosive over many.

The risk radar

Beyond the strategy critique, two structural risks deserve specific attention because they could undermine the thesis through no fault of management's execution.

LFP technology obsolescence. Himadri is making a large, concentrated bet on LFP cathode chemistry. But battery chemistry is a moving target. If the market tilts decisively toward sodium-ion (cheaper, no lithium), solid-state (a step-change in energy density), or high-nickel NMC for premium segments, a multi-billion-rupee LFP facility risks becoming an expensive white elephant. Management's partial hedge — the silicon-carbon anode bet via Sicona, which is chemistry-agnostic at the cathode level — is sensible, but the headline cathode investment is squarely exposed to chemistry risk. This is the substitute-threat force made concrete.

Feedstock sourcing bottleneck. Here is the elegant, long-tail risk that ties the whole company together. Himadri's entire moat rests on crude coal tar, which is a byproduct of coke-oven, blast-furnace steelmaking. But steelmaking itself is under decarbonization pressure. If Indian steel shifts over time toward hydrogen-based direct reduced iron (DRI) and electric-arc routes that bypass coke ovens, the supply of crude coal tar could structurally decline. The very green transition that Himadri is betting on in batteries could, in a long-horizon irony, erode the feedstock that funds it. This is not a near-term threat — India's coke-based steel capacity is vast and growing — but it is the kind of slow structural risk a thirty-year investor must hold in view.

None of these risks is necessarily fatal. But together they explain why this is a genuinely contested stock rather than an obvious one — and why the bull and bear cases are both internally coherent.

X. The Investment Spine: Bull vs. Bear Case

Strip away the storytelling and the question for a long-term investor reduces to a single tension: you are buying a fortified, cash-generative monopoly that is voluntarily spending its cash on unproven, fiercely competitive new businesses. Whether that is brilliant or reckless depends on which of the following you find more persuasive.

The bull case

The bull case starts from a position of strength that is rare in transformation stories: the core business actually works and actually pays. Himadri is arguably the only vertically integrated, profitable, cash-generating Indian company plausibly positioned to localize the EV battery-materials supply chain — and it is funding that ambition from internal accruals rather than betting the balance sheet.[^7] The downside is genuinely protected by the pitch and specialty carbon monopoly, with its cornered feedstock and switching costs. The FY26 margin expansion proves management can execute a hard pivot.2 And the Sicona and IBC alignments provide early, tangible customer validation and proprietary IP access for a relatively modest outlay.34 In this reading, India is at the start of a structural EV and energy-storage build-out, Himadri has the chemistry adjacency and the cash to seize a protected domestic niche, and you are being handed the optionality on a multi-decade growth wave essentially subsidized by a boring monopoly.

The bear case

The bear case starts from valuation and ends with China. At record highs, the stock appears priced for the transformation to succeed — meaning much of the ₹30,000-crore battery dream is arguably already in the price, even though that target rests on a global EV-adoption curve facing real-world demand wobbles and is, by management's own timeline, years from material revenue.19 Birla Tyres, however cheaply acquired, will absorb management bandwidth and capital to revive while creating channel conflict in the larger carbon black book.5 And in cathodes, Himadri is bringing a few-hundred-crore knife to a gunfight against Chinese giants with government subsidies and scale measured in the tens of billions. The bear's summary: you are paying a premium multiple for an industrial company to win at a high-tech business it has never done, against the most formidable manufacturing competitors on earth, while a global-scale rival (Rain) marches into its home pitch market.8

Holding both

The intellectually honest position is that both cases are correct about different things. The bull is right that the core business is a fortress and the downside is real-but-limited. The bear is right that the upside is unproven and the price assumes a lot of it. The resolution will not come from argument; it will come from execution data over the next several years. Which is why the discipline for a long-term investor is to stop debating and start watching a very small number of things.

The 3 KPIs to track

Forget the dozens of metrics in the quarterly deck. Three signals will tell you whether the thesis is breaking the bull's way or the bear's.

1. LFP cathode plant commissioning, on schedule. Is the first phase (40,000 MTPA, beginning around Q3 FY27) actually starting on time and ramping?1 This is the single cleanest test of execution credibility. A slip — especially an unexplained one — would be the first hard evidence that the vision is outrunning the company's capability.

2. Birla Tyres EBITDA contribution. Is the Balasore plant turning cash-flow positive, or is it a quiet drain on the parent? The distressed-asset bet is validated only if the carcass comes back to life; otherwise it is a bandwidth tax with a side of channel conflict.

3. EBITDA margin stability. Can Himadri hold the low-20s percent margin it reached in FY26 as input prices swing and the (initially lower-margin) new businesses scale?2 The margin line is where the specialty thesis lives or dies, and it is the number that most directly reveals whether the company's pricing power is durable or cyclical.

Watch those three, and the noise resolves into signal. They also happen to encode the deeper lessons of the whole Himadri story.

XI. Playbook Lessons & Epilogue

Step back from the rupees and the chemistry, and Himadri offers a set of transferable lessons about how industrial companies reinvent themselves — and where reinvention curdles into hubris.

The "reloading" strategy. The central move of Himadri's last two decades is the use of a steady, monopolistic, cash-generative industrial business as the funding source for asymmetric, high-tech growth options. This is reloading: you keep firing the reliable old gun to pay for the experimental new arsenal. Done well — staged, internally funded, hedged with options like the Sicona and IBC stakes — it is how a coal tar distiller earns the right to attempt a battery-materials business at all. The discipline lies in never letting the experiments consume the engine that funds them.

The value of feedstock control. The deepest lesson is that in a manufacturing business, control of the raw material is the ultimate moat. Himadri's durable advantage was never the distillation chemistry, which others can learn; it was being the largest buyer of crude coal tar in India and denying rivals their feedstock. The same instinct runs through the entire EV strategy — own the coal tar, make the needle coke, refine the anode, secure the cathode offtake. Whoever controls the input controls the chain. It is the through-line that makes an otherwise scattered-looking portfolio internally logical.

The danger of conglomeration. And yet the same instinct, pushed too far, becomes empire-building. The line between brilliant forward integration and value-destroying diworsification is genuinely thin, and Himadri is walking it in real time — a pitch utility, a specialty chemicals franchise, a battery-materials startup, and a retail tire brand under one roof. The market will reward coherence and punish sprawl, and which one this turns out to be is not yet decided.

So where does that leave the carbon king? Himadri's journey — from a small West Bengal casting outfit in 1987, to the indispensable plumbing of India's aluminum and steel industries, to an aspiring pillar of the country's green-industrial future — is one of the more striking reinventions in Indian manufacturing. The first two acts are written and proven: the monopoly is real, the margins expanded, the cash is flowing. The third act, the electric one, is still being staged, and its reviews will be decided not by the eloquence of the vision but by whether the cathode plant lights up on schedule, the tire factory pays its way, and the margins hold. For now, Himadri is exactly what it has always been at its best — a company quietly betting that the dirtiest business in the room can pay for the cleanest future. Whether that bet compounds or combusts is the story still being written.

References

-

Himadri Speciality Chemical to set up LFP Cathode Active Material plant in Odisha — EVreporter ↩↩↩↩↩

-

Himadri Speciality Chemical Reports Record FY26 Results with ₹1,006 Crore EBITDA — ScanX ↩↩↩↩↩↩↩↩

-

Sicona Signs Transformational Licensing Agreement with Himadri to Scale SiCx Production — PR Newswire, 2025-05 ↩↩↩↩

-

Himadri Speciality Chemical hikes stake in International Battery Company to 20.47% — Business Standard, 2026-06-11 ↩↩↩

-

NCLT approves Himadri, Dalmia Group's joint resolution plan of Birla Tyres — Business Standard, 2023-10-19 ↩↩↩↩↩

-

Anurag Choudhary Biography: Chairman, Managing Director & CEO of Himadri Speciality Chemical — StockLens ↩↩↩↩↩

-

PCBL Limited Corporate Profile and Financial Performance — Moneycontrol ↩↩↩

-

Rain Industries Investor Relations & Advanced Carbon Material Capacity Updates ↩↩↩

-

Himadri Speciality Chemical Stock Profile — NSE India (Symbol: HSCL) ↩↩↩

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube