Home First Finance: The Affordable Housing Revolution

I. Introduction & Episode Teaser

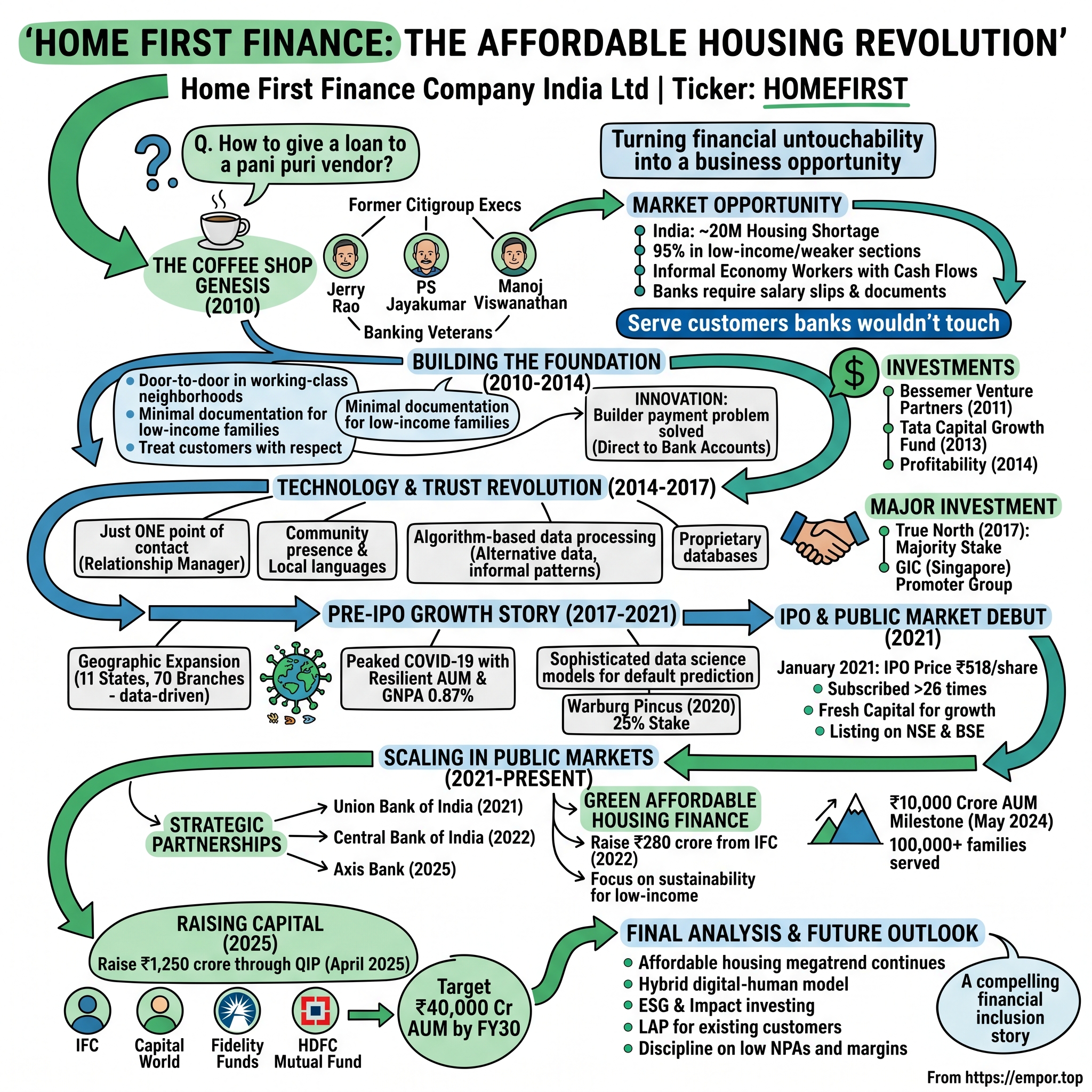

Picture this: A pani puri vendor in suburban Mumbai walks into a bank, hoping to secure a home loan. He has cash income, no formal salary slips, and dreams of owning a 400-square-foot apartment. The bank executive glances at his application, shakes his head, and sends him away. This scene played out millions of times across India until three former Citigroup executives decided to rewrite the script entirely.

The question that drives today's story is deceptively simple yet profoundly transformative: How did three banking veterans build a ₹13,000 crore housing finance company by serving the very customers that traditional banks wouldn't touch? This is the story of Home First Finance Company India Limited—a company that turned financial untouchability into a massive business opportunity. As of today, Home First Finance Company India Ltd (HOMEFIRST) has a market cap of ₹13,241.10 Cr as of 12th August 2025, placing it firmly in the small-cap financial services category. Listed on both the NSE and BSE under the symbol HOMEFIRST, this company represents one of India's most compelling stories of financial inclusion meeting scalable business economics.

What we'll unpack today is how a company built on serving auto-rickshaw drivers, vegetable vendors, and construction workers—customers banks wouldn't touch with a ten-foot pole—became one of India's fastest-growing housing finance companies. It's a story of technology meeting trust, of regulatory navigation meeting market opportunity, and most importantly, of understanding that the biggest markets often lie where traditional players fear to tread.

The roadmap ahead takes us from that fateful coffee shop conversation in 2010 through rapid expansion, private equity deals, a blockbuster IPO, and the company's current position as a digital-first affordable housing finance powerhouse. We'll examine their underwriting innovations, their tech stack that processes loans in 48 hours, and their ability to maintain sub-1% NPAs while serving India's informal economy. Along the way, we'll extract lessons for founders building in regulated markets and investors seeking the next great financial inclusion story.

II. The Coffee Shop Genesis (2010)

The scene opens in a modest coffee shop in Mumbai, circa 2010. The monsoon rains hammer against the windows as three former Citigroup executives lean over steaming cups of chai, sketching out what would become a revolutionary idea in Indian finance. Jerry Rao, former chairman and co-founder of Mphasis; PS Jayakumar, who would later become CEO and MD of Bank of Baroda; and Manoj Viswanathan, previously with Citigroup India, weren't discussing high-yield bonds or private equity deals. They were talking about pani puri vendors.

"How would a pani puri vendor avail a loan and fulfill his dream of buying his own house?" This wasn't an academic exercise—it was the founding question of what would become Home First Finance. The three colleagues, each with decades of experience in retail banking's ivory towers, saw a massive paradox: India's informal economy workers generated real cash flows but couldn't access formal credit. Banks wanted salary slips, IT returns, formal employment letters—documents that auto-rickshaw drivers and vegetable vendors simply didn't have.

Jerry Rao brought extraordinary credentials to this coffee shop brainstorm. The founder and former CEO of software company Mphasis had held several positions in Citibank prior, serving with Citi and Citicorp in various capacities in Asia, Europe, South America, and North America over 20 years, including as Head of the Development Division of Citicorp and Chairman and CEO of Transaction Technologies Inc., based in California. An alumnus of Loyola College Chennai, Indian Institute of Management Ahmedabad and the University of Chicago, he had received Distinguished Alumnus Awards from all three institutions. After selling Mphasis to EDS, Jerry had already proven he could build and exit a billion-dollar company. Now he wanted to solve a different problem.

PS Jayakumar matched Jerry's pedigree with his own banking warfare scars. A Chartered Accountant with a Post Graduate Diploma in Business Management from XLRI Jamshedpur, he was a career banker who had spent over 23 years in Citibank in India and Singapore starting in 1986. His Citibank resume read like a masterclass in consumer banking innovation—he was associated with the first asset securitisation in India in 1991 and the first multi-lingual biometric ATM for the financially excluded in 2006. Later, he would be selected by the Government of India in 2015 to serve as the Managing Director and CEO for Bank of Baroda, the first person from the private sector selected to run a large public sector bank, leading a successful transformation and completing the three-way merger between Bank of Baroda, Vijaya and Dena Bank, earning him the 'Banker of the Year' award by Financial Express for 2018.

The fundamental questions they wrestled with that day cut to the heart of India's financial apartheid: Why is the loan process so complex? Why is there such a gulf in the treatment provided to a premium customer and someone from an informal segment? Why are customers kept in the dark about their own loan process? These weren't just process questions—they were moral imperatives wrapped in a massive business opportunity.

The market opportunity was staggering. India had a housing shortage of over 20 million units, with 95% of the deficit in the economically weaker sections and low-income groups. Traditional banks and housing finance companies focused on the creamy layer—salaried employees of large corporations, professionals, business owners with formal books. Below that lay an ocean of demand: families earning less than ₹50,000 monthly who had stable cash flows but no way to prove them to a traditional underwriter.

What made this moment special wasn't just the identification of the opportunity—plenty of people knew the affordable housing gap existed. It was the combination of three veterans who had the technical skills, industry relationships, and crucially, the patience to build trust in a low-trust market. They weren't fintech cowboys looking for a quick flip; they were institution builders who understood that serving the underserved required reimagining the entire mortgage value chain.

The company commenced operations in August 2010 after registering with the National Housing Bank, the regulatory and licensing body for housing finance companies in India. From day one, their philosophy was radical: treat the pani puri vendor with the same respect as a software engineer, use technology to simplify rather than exclude, and build a business where social impact and profitability weren't at odds but reinforced each other.

III. Building the Foundation (2010–2014)

The early days of Home First Finance looked nothing like a typical financial services startup. While Silicon Valley companies were raising millions on PowerPoint decks, Jerry, Jaya, and Manoj were literally going door-to-door in Mumbai's working-class neighborhoods, sitting with potential customers to understand their financial lives. They discovered that their target customers didn't lack income—they lacked documentation. A tea stall owner might generate ₹40,000 monthly but have no way to prove it to a bank's credit committee.

The first innovation came from an unlikely source: the builder payment problem. In 2010, most housing finance companies would hand over loan proceeds through demand drafts or cheques, creating a maze of paperwork and delays. Home First pioneered disbursing the builders' amount directly into their bank accounts—a simple innovation that seems obvious now but was revolutionary when NEFT and RTGS were still exotic instruments that many builders didn't trust. This single change reduced loan disbursement time from weeks to days and eliminated a major source of fraud and delays. In 2011, validation came from an unexpected quarter. Bessemer Venture Partners bought a minority stake in the company for an undisclosed sum. For context, Bessemer was no ordinary VC—an American venture capital firm headquartered in San Francisco with offices in India, Israel, Hong Kong, and the United Kingdom. Between 2006 and 2011, when they started investing in India, they backed sector leaders across brokerage, lending, and insurance, including being the first institutional investors in Motilal Oswal and investing in non-bank retail lender Shriram City Union Finance. Their investment in Home First signaled that Silicon Valley-style venture capital saw merit in financing India's informal economy.

Two years later, momentum accelerated. In 2013, Tata Capital Growth Fund picked up a minority stake in the company. The Tata name brought more than capital—it brought credibility in conservative Indian financial markets where the Tata brand commanded respect. That same year, the company hit a psychological milestone: approving 1000 loans in March 2013. Each loan represented a family moving from rental to ownership, from uncertainty to stability.

But the real vindication came in 2014: Home First Finance turned profitable. This wasn't supposed to happen. Conventional wisdom held that serving low-income customers meant accepting losses for years, subsidizing financial inclusion with patient capital. Home First proved otherwise. Their model—technology-enabled processing, direct builder payments, and deep community trust—generated positive unit economics from the start.

The core product philosophy was elegantly simple yet revolutionary in execution. While banks required 40+ documents and took 45-60 days to process a home loan, Home First targeted families earning less than ₹50,000 monthly, offering housing loans for home purchases and construction with minimal documentation and rapid turnaround. They understood that their customers' income wasn't irregular—it was just documented differently. A vegetable vendor's daily cash receipts, an auto driver's ride patterns, a construction worker's seasonal employment—all these represented predictable cash flows that traditional underwriting models couldn't capture.

What made Home First different wasn't just whom they served but how they served them. They deployed relationship managers who spoke local languages, understood local businesses, and could assess creditworthiness through community knowledge rather than credit scores. They built technology that could process alternative data—utility payments, mobile recharge patterns, informal chit fund participation—to build credit profiles for the credit-invisible. Most importantly, they treated every customer with dignity, offering the same quality of service whether the loan was for ₹5 lakhs or ₹50 lakhs.

IV. The Technology & Trust Revolution (2014–2017)

The transformation that occurred between 2014 and 2017 would define Home First's trajectory for the next decade. What made the company unique wasn't just technology or trust individually—it was the synthesis of both into something entirely new: a customized, tech-savvy, and customer-centric approach that treated informal sector workers as valued clients rather than charity cases.

Consider the typical loan journey at a traditional bank circa 2015: Multiple visits, different departments, endless photocopies, and most crucially, multiple points of contact who often gave contradictory information. Home First revolutionized this with a simple innovation: just one point of contact for the customer for all loan procedures. Your relationship manager wasn't just a salesperson who disappeared after application—they were your guide through the entire journey, from application to disbursement to repayment.

The technology stack they built was deceptively sophisticated. On the surface, it looked simple—a mobile app for relationship managers, automated document verification, digital payment processing. But underneath lay complex algorithms that could parse informal income patterns, assess property values in undocumented markets, and predict default risk for customers with no credit history. They weren't just digitizing existing processes; they were inventing new ones tailored to their unique customer base.

Building trust with the unorganized sector required more than technology—it required presence. Home First's relationship managers became fixtures in their communities. They attended local festivals, understood seasonal income patterns, knew when the fruit vendor's business peaked and when the construction worker's income dried up. This wasn't corporate social responsibility; it was core business strategy. Trust, they understood, was their primary competitive moat.

The numbers validated the approach. The company reached 5000 disbursals within the next two years after hitting 1000 in 2013—a 5x growth that would make any Silicon Valley startup envious. But unlike typical startups burning cash for growth, Home First maintained profitability throughout this expansion. Each new market they entered, each new customer segment they served, added to their proprietary database of informal economy creditworthiness. The Private Equity inflection point arrived in February 2017. True North acquired a majority stake in Home First Finance for over ₹600 crore. Aether (Mauritius) Limited, an affiliate of the Singaporean sovereign wealth fund GIC, also became part of the company's promoter group. This wasn't just capital injection—it was transformation. True North, founded in 1999 as India Value Fund Advisors, was one of the most experienced private equity firms in India, having invested in over 35 mid-sized profitable businesses. Their involvement brought institutional discipline, governance structures, and crucially, the credibility needed to access larger pools of capital.

The True North deal marked Home First's evolution from startup to scale-up. With patient capital and experienced operators on the board, the company could invest in technology infrastructure that would have been impossible to justify with quarterly earnings pressure. They built automated underwriting models, mobile-first customer interfaces, and most importantly, a data warehouse that captured the financial behavior of India's informal economy at unprecedented granularity.

Credit rating improvements followed naturally. As the company demonstrated consistent asset quality, timely repayments, and robust governance, rating agencies took notice. These weren't just bureaucratic stamps—each rating upgrade meant lower cost of capital, which directly translated to more affordable rates for customers. The virtuous cycle Jerry and team had envisioned was finally spinning at full speed.

V. The Pre-IPO Growth Story (2017–2021)

The four years between the True North investment and the IPO represented Home First's golden expansion era. Geographic expansion followed a deliberate strategy: 11 states, 70 branches, but not random proliferation. Each new market was chosen based on data—construction activity, informal economy concentration, competitive landscape, and regulatory environment. They weren't just opening branches; they were building a national footprint with surgical precision. In October 2020, a watershed moment arrived: Warburg Pincus acquired a 25% stake in Home First Finance for ₹700 crore. The timing was extraordinary—this was peak COVID-19, when the world was in lockdown and financial markets were in turmoil. Yet here was one of the world's most sophisticated private equity firms, with over $53 billion in assets under management, betting big on India's affordable housing story. The investment of approximately INR 700 crore was a combination of primary fund raise and secondary sales by existing shareholders.

The pandemic test revealed Home First's true resilience. While traditional lenders saw NPAs spike as lockdowns destroyed informal economy incomes, Home First maintained GNPA of 0.87% as of March 31, 2020. How? Their deep community relationships meant they understood which customers faced temporary disruption versus permanent income loss. Their technology infrastructure allowed relationship managers to stay connected with customers even during lockdowns. Most importantly, their customers—essential service providers, small shop owners, daily wage earners—showed remarkable repayment discipline even in crisis.

Technology infrastructure underwent radical transformation during this period. The company built sophisticated data science models that could predict default probability based on hundreds of variables—from monsoon patterns affecting construction workers to festival seasons impacting street vendors. They created mobile apps that allowed customers to upload documents, track applications, and make payments without visiting branches. But technology was always the enabler, never the product. The product was trust, speed, and dignity.

Building the underwriting models represented a masterclass in financial innovation. Traditional credit scoring relied on salary slips, tax returns, and credit bureau data—none of which their customers had. Home First built alternative scoring models using proxy data: frequency of mobile recharges (indicating cash flow stability), children's school fees payments (showing financial priorities), and participation in local chit funds (demonstrating savings discipline). Each new customer added to their proprietary database, making the models smarter and risk assessment more precise.

The IPO preparation phase revealed the company's institutional maturity. They upgraded governance structures, formalized processes, and built the financial reporting infrastructure required for public markets. But they never lost sight of their mission. Every board presentation, every investor pitch, started with the same slide: a photo of a customer family standing in front of their new home. The message was clear—financial returns were the outcome, not the purpose. The purpose was transforming lives through homeownership.

VI. The IPO & Public Market Debut (2021)

January 2021 arrived with Home First Finance ready for its public market debut. The IPO, launched at ₹518 per share, aggregated to ₹1,154 crore—a combination of fresh issue of ₹265 crore and an offer for sale of ₹889 crore. The timing seemed counterintuitive: India was still reeling from COVID-19's second wave, economic uncertainty was rampant, and traditional wisdom suggested waiting for calmer waters.

But Home First understood something the market hadn't fully grasped: the pandemic had accelerated, not decelerated, the affordable housing story. Reverse migration had created demand in Tier 2 and Tier 3 cities, work-from-home had made larger homes essential rather than aspirational, and government stimulus had put liquidity in the hands of first-time buyers. The IPO opened on January 21, 2021, and closed on January 25, 2021.

The response was electric: the IPO was subscribed over 26 times. The QIB portion was subscribed 52.53 times, HNI 39.00 times, and even retail investors, typically cautious about financial services IPOs, subscribed 6.59 times. This wasn't just oversubscription—it was validation of a decade-long journey from that coffee shop conversation to public markets credibility.

The pricing debates were fascinating. At ₹518 per share, the company was asking for a P/E of around 42.75 based on annualized earnings—aggressive by traditional lending standards but reasonable for a high-growth fintech play. Critics pointed out that Warburg Pincus had invested just months earlier at ₹334.73 per share, implying a 55% markup. Supporters countered that the pandemic had proven Home First's resilience, justifying the premium.

Equity shares of the company began trading on Bombay Stock Exchange and National Stock Exchange on 3 February 2021. The listing day performance would set the tone for Home First's public market journey. More than share price movements, the IPO enabled three critical transformations: capital for growth without dilutive terms, brand credibility that attracted top talent and partners, and acquisition currency for future consolidation plays.

What the IPO truly enabled was a shift from survival to scale. With ₹265 crore of fresh capital and no immediate pressure for follow-on fundraising, Home First could invest in long-term capabilities—advanced analytics, new product development, geographic expansion—without quarterly earning pressures that plague most public companies. The founders had structured the IPO brilliantly: enough primary capital for growth, enough secondary sale for early investors to realize returns, but retention of sufficient stake to maintain control and alignment.

VII. Scaling in Public Markets (2021–Present)

The post-IPO era revealed Home First's true strategic ambitions. Strategic partnerships became the growth accelerator, starting with a game-changing development in December 2021: Union Bank of India (UBI) and Home First Finance entered into a strategic co-lending partnership. This wasn't just a funding arrangement—it was validation from one of India's largest public sector banks that Home First's underwriting models and customer base were bankable.

Home First Finance signed a similar partnership with Central Bank of India in September 2022 and Axis Bank in 2025. Each partnership brought different strengths: Union Bank's massive rural network, Central Bank's government relationships, Axis Bank's technology infrastructure. These weren't vanilla co-lending deals where banks simply provided capital. Home First structured them as true partnerships where banks gained access to new customer segments while Home First accessed cheaper capital and distribution reach.

The green financing initiative marked Home First's evolution from pure-play lender to impact-focused financial institution. In December 2022, Home First Finance raised ₹280 crore from International Finance Corporation to provide financing for green affordable housing customers. This wasn't greenwashing—it was strategic positioning for the next decade. Green buildings meant lower utility costs for low-income families, better health outcomes from improved ventilation, and access to government subsidies for sustainable construction. The ₹10,000 crore milestone arrived in May 2024, when the company's assets under management crossed this psychological barrier. This wasn't just a number—it represented over 100,000 families who had moved from rental to ownership, from uncertainty to stability. Each loan in that portfolio told a story: the auto-rickshaw driver who now owned a one-bedroom flat, the vegetable vendor whose children had their own study room, the construction worker who had built generational wealth through property ownership.

In April 2025, Home First Finance raised ₹1,250 crore through a qualified institutional placement (QIP), which saw participation from investors including International Finance Corporation, Capital World, Fidelity Funds and HDFC Mutual Fund. The QIP, priced at ₹970 per share, attracted overwhelming response from prominent foreign long-only funds, domestic mutual funds, and insurance companies. This marked the company's first equity fundraise since its IPO in 2021, providing capital to target ₹40,000 crore AUM by FY30—a 27% CAGR from current levels.

Current performance metrics paint a picture of sustainable excellence. The company's market cap stands at ₹12,735 Crore (up 24.2% in 1 year) with revenue of ₹1,647 Cr and profit of ₹413 Cr. The stock trades at 4.40 times book value, reflecting market confidence in future growth. More importantly, the company has maintained its discipline: NPAs remain below 1%, customer acquisition costs continue to decline through digital channels, and net interest margins remain healthy despite competitive pressures.

VIII. Business Model & Unit Economics

The customer acquisition playbook Home First developed represents a masterclass in serving the underserved profitably. Unlike traditional lenders who wait for customers to approach them, Home First goes where their customers are—construction sites, local markets, industrial areas. Their relationship managers aren't just loan officers; they're financial advisors who help customers navigate the complex journey from informal income to formal credit.

The technology-driven approach isn't about replacing human judgment—it's about augmenting it. When a relationship manager meets a street vendor, they input dozens of data points into a mobile app: daily sales patterns, seasonal variations, family size, existing financial commitments. The algorithm processes this information against millions of similar profiles, generating a credit score and suggested loan amount in minutes. But the final decision incorporates the relationship manager's qualitative assessment—does the vendor have a loyal customer base? Is the location stable? These nuances matter.

Risk management and underwriting innovation form the backbone of sustainable growth. Home First discovered that traditional risk metrics often penalized their customers unfairly. A salaried employee who loses their job might default immediately, but a vegetable vendor with 20 years in the same market rarely does. They built models that captured these realities: business vintage matters more than formal employment, community ties predict repayment better than credit scores, and small, frequent income is often more stable than large, monthly salaries.

Collection mechanisms blend technology with empathy. The company uses predictive analytics to identify potential delinquencies before they occur—a customer who usually pays on the 5th but hasn't by the 7th gets a friendly reminder call, not a harsh collection notice. When genuine hardship strikes—illness, accident, seasonal business downturns—the company offers restructuring options that keep customers in their homes while protecting asset quality. This approach explains their sub-1% NPA ratio: customers who feel respected and supported rarely default strategically.

Capital allocation and funding strategy evolved from purely equity-dependent to a sophisticated mix of sources. Bank partnerships provide low-cost capital, the National Housing Bank offers refinancing at preferential rates, and the recent QIP provides growth capital without debt-like obligations. This diversification reduces funding costs, which directly translates to more affordable rates for customers—a virtuous cycle where financial engineering serves social purpose.

The competitive moats run deeper than technology or funding. Trust, built over 15 years of serving communities fairly, can't be replicated with venture capital. The proprietary database of informal economy credit behavior, encompassing hundreds of thousands of loans, provides underwriting insights no competitor can match. The distribution network of relationship managers embedded in local communities creates switching costs—customers won't abandon the institution that helped them achieve homeownership for a marginally better rate elsewhere.

IX. Playbook: Lessons for Founders & Investors

Serving the underserved profitably requires inverting traditional business thinking. Home First didn't ask "How can we adapt our product for poor customers?" They asked "What product would serve these customers best?" The difference is profound. The former leads to stripped-down versions of existing products—"banking for the poor." The latter leads to fundamental innovation—new underwriting models, new distribution channels, new definitions of creditworthiness.

Technology as an enabler, not the product, represents a crucial insight often missed by fintech entrepreneurs. Home First could have positioned itself as a "digital lending platform" or "AI-powered mortgage company." Instead, they understood that their customers valued human relationships, trusted face-to-face interactions, and needed guidance through the complex home-buying process. Technology made this human touch scalable and consistent, but never replaced it.

Building trust in low-trust markets requires extraordinary patience. Home First spent years establishing credibility before scaling. They honored every commitment, never hidden fees in fine print, and treated defaults as opportunities to help rather than punish. This approach seemed inefficient to observers accustomed to Silicon Valley's "move fast and break things" ethos. But in financial services serving vulnerable populations, breaking things means breaking lives. Trust, once lost, is almost impossible to rebuild.

The importance of patient capital cannot be overstated. Home First's journey from founding to profitability took four years, to IPO took eleven. Traditional venture capital, with its 5-7 year fund cycles and IRR pressures, would have forced premature scaling or pivot. Instead, investors like Bessemer, True North, and Warburg Pincus understood they were building infrastructure for India's next phase of development. Their patience was rewarded with returns, but more importantly, with impact.

Regulatory navigation in financial services requires a different mindset than typical startup regulatory arbitrage. Home First never tried to exploit regulatory gaps or operate in gray areas. They engaged proactively with regulators, exceeded compliance requirements, and positioned themselves as partners in financial inclusion. When regulations changed, they adapted quickly rather than fighting. This approach meant slower initial growth but created a sustainable, defensible business model.

The timing question—when to go public—reveals sophisticated thinking about capital markets. Home First could have remained private longer, raising successive rounds at higher valuations. Instead, they went public when they needed permanent capital for growth, when their business model was proven but not yet at scale, and when public markets were receptive to their story. The IPO wasn't an exit but an entry into a new phase of growth with aligned, long-term shareholders.

X. Bear vs. Bull Case

Bull Case:

The massive TAM with government support through "Housing for All by 2022" (now extended to 2025) creates a multi-decade growth runway. India needs 20 million affordable homes, and traditional lenders serve less than 30% of demand. Government subsidies through PMAY (Pradhan Mantri Awas Yojana), interest rate subventions, and tax benefits create a supportive ecosystem where customers, lenders, and policymakers align.

Technology-enabled cost advantages compound over time. While traditional lenders spend 3-4% of loan value on origination and servicing, Home First has driven this below 2% through automation, and it continues to decline. Every basis point saved can either improve margins or reduce customer rates, creating competitive advantage that strengthens with scale.

Strong institutional backing from global investors provides not just capital but credibility. When institutions like IFC, Warburg Pincus, and Fidelity back a company, it signals to regulators, partners, and customers that due diligence has been done, governance is strong, and the business model is sustainable.

Low NPAs and disciplined underwriting through cycles demonstrate that serving low-income customers isn't inherently risky—it requires different risk models. Home First has proven these models through COVID-19, demonetization, and multiple economic cycles. As their database grows and models improve, underwriting becomes more precise, creating a widening moat.

Bear Case:

Concentration risk remains real across multiple dimensions. Geographic concentration in certain states makes the company vulnerable to regional economic shocks or natural disasters. Customer segment concentration in informal economy workers means a formalization drive or economic shift could impact the entire portfolio. Product concentration in home loans limits diversification opportunities.

Competition from banks and larger NBFCs intensifies as the affordable housing opportunity becomes obvious. Banks have lower funding costs, established brands, and regulatory advantages. Larger NBFCs like HDFC have scale advantages and ecosystem plays. As these players move down-market, Home First's niche could get squeezed.

Interest rate sensitivity affects both sides of the balance sheet. Rising rates increase funding costs, which either compress margins or require passing costs to price-sensitive customers. The customers Home First serves have limited ability to absorb rate increases, creating a natural ceiling on pricing power.

Regulatory changes pose constant risk in Indian financial services. Priority sector lending norms, capital requirements, or collection practices could change suddenly. The RBI's increasing focus on consumer protection could limit collection effectiveness or increase compliance costs. Political pressure to provide relief during economic stress could impact profitability.

XI. Final Analysis & Future Outlook

The affordable housing megatrend in India transcends typical sector rotations or economic cycles. It's a structural shift driven by urbanization, formalization, and aspiration. As millions move from villages to cities, from informal to formal employment, from survival to stability, the demand for affordable housing will only intensify. Home First sits at the intersection of these trends, positioned to capture disproportionate value.

Digital transformation of financial services accelerates but doesn't eliminate the human element. The next decade will see hybrid models where technology handles routine processes but humans manage relationships, especially in trust-dependent sectors like housing finance. Home First's early investment in this hybrid model positions them ahead of both traditional lenders (too manual) and neo-banks (too digital).

ESG and impact investing angles make Home First increasingly attractive to a new class of investors. With climate-conscious construction financing, financial inclusion metrics, and governance standards exceeding peers, the company appeals to funds with ESG mandates. As these funds grow from billions to trillions globally, companies with genuine impact stories will command valuation premiums.

Potential expansion opportunities abound: LAP (Loan Against Property) for existing customers needing growth capital, affordable housing development finance, insurance distribution, and even education loans for customers' children. Each expansion leverages the same trust relationships and distribution infrastructure, creating ecosystem effects without venture-style cash burn.

Key metrics to watch include AUM growth rate (target 25%+ annually), NPA trends (maintaining below 1%), cost-to-income ratio (driving toward 30%), and geographic diversification progress. But perhaps the most important metric is one rarely found in analyst reports: number of families moved from rental to ownership. That's the true measure of Home First's success.

The story that began with three bankers in a Mumbai coffee shop wondering how to serve a pani puri vendor has evolved into one of India's most compelling financial inclusion narratives. Home First Finance didn't just build a business—they built a bridge between India's informal economy and formal financial system. In doing so, they proved that purpose and profit aren't opposing forces but complementary energies that, when aligned, create extraordinary value for all stakeholders.

The road ahead promises continued challenges: economic cycles will test asset quality, competition will compress margins, and regulations will evolve. But Home First has something more valuable than capital or technology: they have trust of millions of Indians who see them not as a lender but as a partner in achieving life's most important milestone—owning a home. In a nation where homeownership represents security, status, and success, Home First isn't just financing houses; they're enabling dreams. And that, more than any financial metric, explains why this company's best chapters are still being written.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube