Hindustan Foods: The 'Foxconn' of Indian FMCG

I. Introduction & The "Invisible" Giant

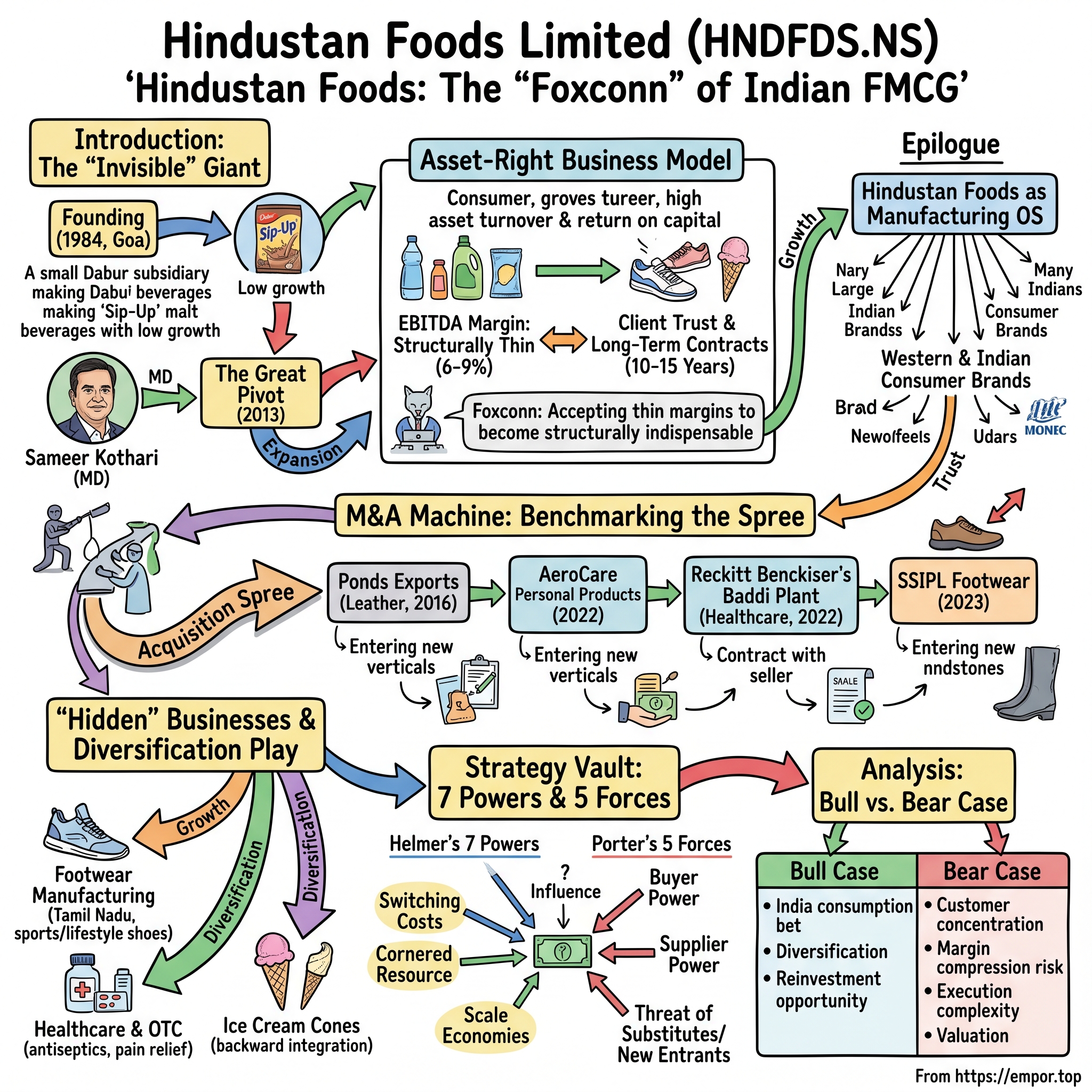

Open the cabinet under your kitchen sink in a middle-class apartment in Andheri, Indore, or Coimbatore. Pull out the dishwashing liquid, the floor cleaner, the toilet cleaner, the laundry pod. Now walk into the bathroom and pick up the mosquito repellent vaporizer, the bar soap, the deodorant, the talcum powder. Wander to the kid's room and check the school sneakers, the rubber-soled sandals, the lunch-box drinking yogurt sitting in the fridge. There is a non-trivial probability—a probability that grows every single quarter—that somewhere between five and ten of those items did not actually emerge from a factory owned by हिंदुस्तान यूनिलीवर Hindustan Unilever, or रेकिट बेंकाइजर Reckitt Benckiser, or डैनोन Danone, or नाइकी Nike, or गोदरेज Godrej. They emerged from a sprawling network of plants run by a Mumbai-headquartered company whose name almost no Indian consumer would recognise if you stopped them on a footpath and asked.

That company is हिन्दुस्तान फूड्स लिमिटेड Hindustan Foods Limited, and the joke, if you can call it that, is that the "Foods" part of the name is no longer even the biggest part of the business. It is the largest dedicated contract manufacturer in Indian fast-moving consumer goods—an enormous, deliberately invisible, deeply embedded supplier to almost every Western and Indian consumer brand that competes for shelf space in the Indian retail aisle.1

The company runs more than two dozen factories across India, manufactures everything from beverage concentrates to leather footwear to coil mosquito repellents to ice cream cones, and reported revenues of roughly ₹3,200 crore for FY24 with a market capitalisation that, as of mid-2026, hovers around the ₹6,500–7,000 crore range.27 In a country where the consumer-goods narrative is almost entirely owned by the brands sitting at the front of the shop, Hindustan Foods has quietly built itself into the manufacturing operating system that powers them.

The analogy that gets thrown around—and we are going to interrogate it carefully later in this story—is that Hindustan Foods is the 富士康 Foxconn of Indian FMCG. Like the Taiwanese giant 鴻海精密 Hon Hai Precision Industry that assembles iPhones for Apple at a single-digit margin and somehow still generates one of the largest electronics businesses on earth, Hindustan Foods has accepted a structurally thin EBITDA margin in exchange for becoming structurally indispensable. The brand makes the design, the marketing, the distribution, the margin. Hindustan Foods makes the product.

Here is the more interesting fact, the one that pulled us into this story in the first place: this is not a brand-new company. Hindustan Foods was founded in 1984 as a small subsidiary set up by डाबर Dabur to manufacture malt-based beverages.[^9] For roughly three decades, it was a sleepy, sub-scale unit with limited ambition and limited shareholder return. Then, in 2013, a Mumbai-based promoter family that had been quietly running contract manufacturing operations for HUL and others for thirty years decided to use Hindustan Foods as the listed vehicle through which to professionalise and institutionalise an entire industry that had, until then, lived in the shadows of Indian capitalism.9

That family was the Kotharis, operating through their privately held वैनिटी केस ग्रुप Vanity Case Group, and the man driving the transformation was समीर कोठारी Sameer Kothari. What happened over the following decade is the central narrative of this story: a sleepy 1984 side-project, picked up cheaply by a strategic operator who understood the industry better than the industry understood itself, was systematically rebuilt into a compounding machine whose stock price has multiplied many times over and whose footprint now extends into businesses—footwear, ice cream cones, healthcare formulations, injection-moulded sandals—that have nothing to do with the company's original name.1

Over the next two hours of reading, we are going to do four things. We will trace how a small malt-beverage factory became a pan-Indian contract-manufacturing platform. We will dissect the "asset-right" business model that makes a 6-to-9 percent EBITDA margin look attractive rather than alarming. We will benchmark the acquisition spree that built the moat. And we will end on the question every long-term investor in this stock eventually has to answer: in a business where your top five customers are bigger than you, smarter than you, and could in theory walk away tomorrow, what exactly is the moat you are paying fifty times earnings for? Let's begin where every good Indian business story begins—with a company that almost died of irrelevance before someone with vision picked it up off the floor.

II. The Great Pivot: From Stagnation to Scale

To understand why 2013 mattered so much for Hindustan Foods, you first have to understand the strange, almost embarrassing position the company occupied at the start of that year. Picture a small, dated manufacturing unit in गोवा Goa, a few state excise licences, one major contract with Dabur to produce a barley-and-malt drink called सिप-अप Sip-Up and various forms of bottled beverage concentrate, a public listing on the BSE that almost no one paid attention to, and an annual revenue figure that, in a country growing nominal GDP at double digits, had effectively flatlined for years.[^9] That was the entirety of Hindustan Foods.

The company had been founded in 1984 by Dabur as a project to produce malt-based beverages near the food-processing hub on the western coast. For almost three decades, it had toggled between being a marginally profitable supplier and a marginally loss-making one. The factory was real, the licences were real, the listed shell was real—but there was no thesis, no roadmap, no second product line, and no obvious reason for the business to exist in 2013 in any form different from how it had existed in 1984. It was, in the politest possible Indian-corporate sense, a candidate for either revival or quiet euthanasia.

Enter समीर कोठारी Sameer Kothari and his cousin शशांक सिन्हा Shashank Sinha. The Kothari family had been quietly operating in the contract-manufacturing space since the early 1980s through वैनिटी केस ग्रुप Vanity Case Group, a privately held collection of factories that produced personal-care products—shampoos, talcum powders, hair oils, deodorants—for major multinational brands operating in India.9 The Kotharis were not glamorous. Their factories were not photographed for business magazines. But for thirty years they had been the back-office of Indian FMCG, the people whose names appeared in tiny font on the back of the bottle next to the words "manufactured by".

What Sameer Kothari understood, sitting in Mumbai in 2012, was something that almost no one outside the contract-manufacturing world fully appreciated. The economics of Indian FMCG manufacturing were on the verge of a structural shift. Multinational brands—एचयूएल HUL, Reckitt, कोलगेट Colgate, नेस्ले Nestlé—were under increasing pressure from their global parents to reduce capital intensity. Building and operating manufacturing plants in tier-three Indian towns to comply with state-level GST and excise differentials was capital-destructive, distracting from the brands' core mission of marketing and distribution, and operationally messy. There was a latent, multi-decade tailwind building: brand owners wanted to outsource manufacturing, but there was no publicly listed, professionally managed, capital-disciplined Indian counterparty capable of accepting that outsourcing at scale.

The Kotharis decided, in essence, to become that counterparty. In 2013, the Vanity Case Group acquired a controlling stake in Hindustan Foods and Sameer Kothari became Managing Director.[^9] The strategic logic was elegant: rather than continue running contract manufacturing through a private partnership where every plant expansion required negotiated bank debt and family capital, they would use a listed company as the consolidated vehicle. Public listing gave them access to equity capital for expansion, a transparent corporate-governance structure that multinational clients trusted, and an institutional platform that could absorb acquisitions without breaking.

But—and this is the critical point that the Indian financial press almost universally missed at the time—Sameer Kothari did not just want to run a bigger contract manufacturer. He wanted to redefine what contract manufacturing was. The historical Indian model was what the industry calls "job work": a brand sends you raw materials, your factory adds labour and machine time, you ship finished product back. It is essentially renting out a factory by the hour. Margins are razor-thin, switching costs for the brand are near zero, and the contract manufacturer carries almost no leverage in the relationship.

The model the Kotharis built at Hindustan Foods is fundamentally different. They call it dedicated manufacturing, and the structure works like this. A brand, say Reckitt, decides it wants to launch a new dishwashing-liquid line for the South Indian market. Instead of building its own greenfield plant, Reckitt signs a long-term contract—often ten to fifteen years—with Hindustan Foods. HFL then builds, owns, and operates a dedicated facility configured exclusively to manufacture that product, often co-located near the brand's distribution hub. Reckitt commits to a minimum volume offtake. In exchange, HFL absorbs the capex and the operational risk.

This sounds simple. The implications are not. Once a Reckitt dishwashing line is running on a custom HFL plant with formulations, batch processes, and quality protocols configured to Reckitt's exact specifications, the cost for Reckitt of switching that production back in-house, or to a rival contract manufacturer, becomes prohibitive. Months of regulatory approvals, weeks of line trials, formulation re-validations—the brand essentially never moves once the line is hot. The contract manufacturer is no longer a vendor. The contract manufacturer is a piece of the brand's own supply chain that just happens to sit on a different balance sheet.

That insight—shifting the value chain from job work to dedicated manufacturing, from vendor to embedded supply-chain partner—is the single most important strategic decision in the history of Hindustan Foods. Everything that follows in this story, every acquisition, every greenfield plant, every diversification into footwear or ice cream cones, is a derivative of that 2013 reframing. The Kotharis did not invent Indian contract manufacturing. They invented the institutional, listed, capital-disciplined version of it.

III. The Business Model: "Asset-Right" and The Power of Trust

If you have ever been on an Indian investor call where an analyst from a domestic mutual fund asks the management about EBITDA margins, you can probably predict exactly how the conversation usually unfolds. The analyst spots a 6-percent EBITDA margin, compares it unfavourably to a 22-percent margin at HUL, asks whether the company has any pricing power. Management protests, talks about asset turnover, talks about return on capital. The analyst nods politely and moves on. The conversation almost always misses the point.

Hindustan Foods runs an EBITDA margin of roughly 6-to-9 percent.27 That is not a margin you want to defend on a glossy presentation slide. But the margin is, in a very real sense, the whole point of the business. A higher margin would imply that Hindustan Foods is extracting more value from its clients than its clients are willing to give up over a fifteen-year contract horizon. A higher margin would imply that, somewhere on the desk of a procurement vice president at HUL or Reckitt, there is an Excel spreadsheet flashing red and asking the question: "Why are we paying our contract manufacturer this much?" The genius of the model is that this spreadsheet does not exist, because the margin is calibrated to live just below the threshold where the brand would consider in-housing again.

Think about the structural logic from the brand's perspective. A multinational brand operating in India has three options for manufacturing. Option one: build and operate its own factory, which requires capex of perhaps ₹100 crore for a mid-sized plant, ongoing maintenance, labour-relations exposure, GST and state-excise compliance across multiple state lines, and the headache of running an industrial operation in a country where running an industrial operation is non-trivial. Option two: use traditional job-work suppliers, which delivers low cost but no quality assurance, no scale, no consistency, and an endless renegotiation cycle. Option three: sign a dedicated long-term contract with Hindustan Foods, which converts an unpredictable capex line into a predictable per-unit variable cost, transfers the operational headache to a professional counterparty, and leaves the brand's balance sheet free to invest in the things that actually drive consumer preference: marketing and distribution.

For a global FMCG company whose parent in London or Amsterdam is measuring its India subsidiary on capital efficiency, the third option is the obvious answer. And once you sign that contract, your CFO can take the next earnings call and tell shareholders that India is now operating on an asset-light model—a phrase that, in the global FMCG lexicon, is gold. The asset-heaviness has not disappeared. It has simply moved onto Hindustan Foods' balance sheet, where the Kotharis are happy to absorb it because their cost of capital is structurally lower than the brand's required return.

This is where the term "asset-right" enters the vocabulary. Hindustan Foods does not pretend to be asset-light. Building factories is capital-intensive, and at any given time the company has a substantial pipeline of greenfield and brownfield construction underway. The "right" in asset-right means that every rupee of capex is tied to a contracted volume commitment from a creditworthy client before the first brick is laid. The take-or-pay structure ensures that even if the brand's product underperforms in the market, the volume guarantee compensates HFL for its capital deployment. Risk does not vanish, but it is redistributed in a way that allows Hindustan Foods to keep building.

The financial output of this model is almost the opposite of what it looks like at first glance. Low margin, high asset turnover, low working-capital intensity. Return on capital employed in the high-teens to low-twenties percent, depending on the year and the mix.27 In the language of long-term compounding investors, this is a beautiful business: predictable, contracted, capital-efficient. In the language of momentum traders looking for margin expansion, it is boring. The disconnect between those two readings is exactly why Hindustan Foods spent its first several public-market years trading at multiples that, with the benefit of hindsight, look extraordinarily generous to anyone who bought early.

There is one more dimension to the model that deserves attention, and it is the one the Kotharis talk about least openly but matters most: trust. Multinational FMCG companies do not casually hand over the manufacturing of their flagship product to a counterparty. The decision goes through procurement, through quality assurance, through brand-protection committees, through global supply-chain governance. By the time a Reckitt or a Danone agrees to run a flagship product through a Hindustan Foods plant, they have audited the management, the financials, the safety protocols, the labour practices, the environmental compliance, and the political stability of the location, often multiple times.

That audit process is itself a moat. Every additional brand that gets comfortable working with HFL adds a reference, an institutional endorsement, a procurement-team comfort that gets carried into the next conversation. A new entrant attempting to compete with Hindustan Foods for a Reckitt contract is not just competing on price. It is competing against a fifteen-year audit trail, a portfolio of multinational reference clients, and a procurement officer's career-risk calculus. In Hamilton Helmer's framework, this is the foundation of what we will later call counter-positioning and process power. For now, the point is simpler. The Kotharis built a business where the entry barrier is not capital. The entry barrier is reputation, accumulated over decades, and there is no shortcut to accumulating it.

That is the foundation on which everything else is built. To understand how the Kotharis turned this foundation into a compounding machine, we have to look at how they spent their capital—because Hindustan Foods, more than almost any other Indian listed company of comparable size, is a story of acquisitions executed with surgical discipline.

IV. The M&A Machine: Benchmarking the Spree

In November 2016, a small filing landed on the BSE corporate-actions page that, on its surface, looked like an industrial sideshow.10 Hindustan Foods, a company most equity analysts could not have placed on a map, had agreed to acquire the leather-products division of Hindustan Unilever—a unit called पॉन्ड्स एक्सपोर्ट्स Ponds Exports based in पॉन्डिचेरी Puducherry, which manufactured leather shoes for export markets, primarily to European retailers.10 The price was modest. The strategic significance was not.

Step back for a moment. Hindustan Foods, the malt-beverage company from गोवा Goa, was buying a leather footwear factory from Unilever. The product had nothing to do with food. The geography was on the opposite coast of India. The customer base was European, not Indian. By any conventional measure of corporate strategy, this was a textbook diversification mistake.

Except it wasn't, and the reason it wasn't tells you everything about how the Kotharis think about acquisitions. The Ponds Exports plant was not a leather business in the conceptual sense. It was a complex manufacturing facility with skilled labour, established export quality protocols, regulatory approvals to ship to multiple European jurisdictions, and—most critically—it was being divested by Unilever at a price that reflected Unilever's view that the asset was non-strategic to the parent. For HUL, the leather division was a stranded asset, an awkward holdover from an earlier era of conglomerate corporate structures. For the Kotharis, who looked at every potential acquisition through the lens of "can we sweat this asset harder than the seller could", it was a discounted entry into a manufacturing vertical with high barriers to scratch-built entry.

The Ponds Exports deal established the template that Hindustan Foods would use repeatedly over the following decade. Step one: identify under-utilised or non-strategic manufacturing assets sitting on the balance sheets of large multinational companies who, for reasons of corporate focus or capital reallocation, are willing to sell at attractive multiples. Step two: structure the acquisition as a slump sale, which in Indian corporate-law terminology means buying the business unit as a going concern at a transactional price typically benchmarked against asset replacement value rather than earnings multiples. Step three: integrate the asset into the broader HFL platform, often by simultaneously signing a long-term manufacturing contract with the seller for the very products the plant was already producing. The seller gets balance-sheet relief, HFL gets a productive asset and a guaranteed revenue stream, and everybody walks away happy except the equity analyst who was trying to model the transaction.

Fast-forward to early 2022, and the next acquisition arrived with even sharper economics. Hindustan Foods agreed to acquire एयरोकेयर AeroCare Personal Products, a contract manufacturer that produced personal-care goods for international brands, for a headline consideration of approximately ₹30 crore.4 The reported impact on the top line was almost immediate: AeroCare contributed roughly ₹100 crore to annualised revenue almost from the first quarter post-acquisition.4 In multiple terms, that is a transaction priced at well under half-times sales, in an industry where comparable contract-manufacturing assets traded at one-to-two times revenue when bought by private-equity. The Kotharis essentially bought a year of operating cash flow for the price of a few months of revenue.

The same pattern repeated again in December 2022, when Hindustan Foods announced the acquisition of रेकिट बेंकाइजर Reckitt Benckiser's healthcare manufacturing facility at बद्दी Baddi in Himachal Pradesh for approximately ₹130 crore.[^5] The strategic logic here was more nuanced than a simple asset purchase. The Baddi facility produced over-the-counter healthcare products—antiseptics, pain relief formulations, household therapeutic items—that sat in a higher-margin segment than HFL's core home-care and food portfolio. By acquiring the plant, Hindustan Foods simultaneously gained a long-term manufacturing contract with Reckitt for the products the plant was already making, expanded into the high-margin OTC and healthcare vertical, and absorbed a workforce already trained to pharmaceutical-grade quality standards.[^5]

If you read the Baddi transaction carefully, you can see the full Kothari thesis in compressed form. The acquisition price of ₹130 crore was, by any standard private-market benchmark, a modest figure for a facility of that scale and regulatory complexity. The plant came with embedded volume commitments from Reckitt, which meant the asset was contracted from day one rather than requiring a multi-year ramp. The product mix expanded HFL's margin profile in a way that pure incremental volume growth could not. And the geography in Baddi sat in a state that, while no longer offering the original excise benefits of the late-2000s tax-holiday era, retained a deep industrial ecosystem of skilled labour and supplier networks.[^5]

The valuation logic across all of these transactions is worth pausing on, because it is the single most under-appreciated piece of the Hindustan Foods investment story. The brands that HFL serves—Reckitt, Unilever, Danone, Nestlé—trade in their respective home markets at price-to-earnings multiples typically in the range of 30x-to-50x or higher. The Indian listed subsidiaries—हिंदुस्तान यूनिलीवर लिमिटेड Hindustan Unilever Limited, नेस्ले इंडिया Nestlé India, कोलगेट-पामोलिव इंडिया Colgate-Palmolive India—trade at even more premium multiples driven by the structural growth narrative of Indian consumption.7 The plants those brands are willing to divest, however, trade at fractions of one-times sales. The arbitrage is straightforward: HFL is using its cost-of-capital advantage and its operational expertise to buy productive assets from sellers who, in their own corporate calculus, are happy to free up the balance sheet at a price that, in transactional terms, is essentially a rounding error against their own market capitalisation.4[^5]

The broader pattern is that Hindustan Foods does not buy companies in the way that a private-equity sponsor buys companies. It buys productive capacity at marginal-cost prices, then layers its own contracting and management discipline on top to extract returns that, for the seller, were never accessible because the asset was non-strategic in the seller's hands. The 2023 acquisitions in the footwear space—including एसएसआईपीएल SSIPL Lifestyle's shoe-manufacturing operations and related transactions in athletic and casual footwear—followed the same logic.5 An under-utilised plant, a contracted offtake partner, and a balance sheet willing to absorb the capital intensity in exchange for a long-tail of stable cash flow.5[^14]

It is worth being honest about the risk. The Kotharis are not infallible buyers. Not every acquisition has turned out as cleanly as the pitch deck suggested. Integrations have taken longer than expected, capacity utilisation in some of the newly acquired plants has ramped more slowly than initial projections implied, and the working-capital requirements of running multiple plants across multiple states have, at times, stressed the balance sheet. The investor presentations talk about gross-block expansion and capex pipelines with a confidence that occasionally needs to be read against the actual reported capacity utilisation numbers from the subsequent annual reports.13 But the strike rate has been high enough, and the discipline on price-per-asset low enough, that the overall portfolio has compounded at a rate that few Indian industrial businesses of comparable scale can match.

Which raises the obvious question: who is actually driving this machine, and how do they think? The answer takes us into the family office in Mumbai where almost all of the decisions that matter for Hindustan Foods get made—the Kotharis themselves.

V. Management Analysis: The Kothari Era

If you spend any time watching समीर कोठारी Sameer Kothari in television interviews or earnings-call recordings, you start to notice something that does not quite fit the conventional Indian-promoter archetype.[^7] He does not perform the kind of bullish, headline-grabbing growth talk that is endemic on Indian business television. He does not promise to double revenue every two years, does not gesture at vague "five-year vision" slides, does not lapse into the corporate-jargon mush of "transformational journeys" and "category disruption". He talks like a chief financial officer who happens to run the company, dwelling on asset turnover, return on capital, gross block, capacity utilisation, and the specific contractual structure of new long-term agreements.[^7]

That tonal restraint is, in itself, a strategy. Hindustan Foods serves the most procurement-disciplined buyers in Indian consumer goods. A loud, promotional management style would set off alarms in the procurement offices of Unilever and Reckitt. A quiet, numbers-first, operationally-focused management style signals exactly the kind of counterparty those buyers want to work with. Sameer Kothari's public persona is, in a real sense, a piece of the company's commercial positioning.

The Kothari family's background helps explain the temperament. Sameer is the third generation of a family that has been in Mumbai-based industrial trading and manufacturing since the early 1980s.9 His grandfather established the family business, his father expanded it into personal-care contract manufacturing through Vanity Case Group, and Sameer inherited not a single legacy company but a multi-decade institutional understanding of how the contract-manufacturing industry operates: who the customers are, what their procurement cycles look like, what their quality protocols demand, and where the structural pricing power sits at each stage of the value chain.9 When he took over Hindustan Foods in 2013, he was not learning the industry. He had spent thirty years watching his family operate inside it from the inside.

That institutional knowledge functions as what Hamilton Helmer would describe as a "cornered resource"—an input to the business that competitors cannot easily replicate even if they have the capital and the ambition to try. A private-equity sponsor wanting to enter Indian contract manufacturing today can buy plants, hire engineers, and finance acquisitions. What it cannot easily buy is thirty years of relationships with the procurement vice presidents of the top twenty Indian FMCG brands, the muscle memory of operating to multinational quality standards across multiple product categories, and the credibility that comes from having delivered through the messy, regulatory-shifting last three decades of Indian industrial policy.

The Kothari shareholding structure in Hindustan Foods reinforces the long-term mindset.6 Through the various promoter entities consolidated under the Vanity Case Group umbrella, the family holds in the region of 60-to-65 percent of the equity.16 Sameer Kothari himself holds a direct stake of around 10 percent.1 That is the kind of concentrated ownership that, in the corporate-finance literature, almost always correlates with longer planning horizons and lower tolerance for short-term financial-engineering shortcuts. When the family owns a controlling stake, every decision is measured against a decadal time frame rather than the quarterly earnings call.

In early 2024, the company announced a scheme of arrangement designed to simplify and consolidate the promoter holding structure.6 The technical mechanics of the scheme involved the merger of certain promoter holding entities to reduce layered ownership and create a more transparent line of sight between the ultimate beneficiaries and the listed company.6 In the abstract this sounds like corporate plumbing, but it matters because it signals an intent on the part of the family to make the promoter structure as legible as possible to external investors, regulators, and potential strategic partners. Opaque promoter structures are a perennial red flag for foreign institutional investors looking at Indian mid-caps. Voluntarily simplifying that structure is the opposite signal—a deliberate move to lower the cost of equity capital available to the company.

The incentive structure for management is also worth understanding. According to the disclosure in the FY24 annual report and the corporate governance filings, performance bonuses for senior leadership are capped at 200 percent of basic pay, with the variable component tied specifically to revenue growth, profit-after-tax growth, and gross block expansion targets.18 The gross-block expansion target is the one that deserves attention—management is explicitly incentivised to grow the asset base of the business, with a long-stated internal target of reaching a gross block in the region of ₹1,800 crore.1 The choice of gross block as a key incentive metric is unusual for an Indian listed company and tells you something about how the Kotharis think. They are not running for margin expansion. They are running for asset accumulation, because asset accumulation in their model is the deterministic path to compounding revenue and earnings over time.

There is a small but meaningful operating-style detail that comes through in the way the Kotharis run the company day to day. They are conservative about leverage. The debt-to-equity ratio has been managed within a band that, by Indian industrial standards, is moderate—high enough to use the tax shield effectively, low enough to absorb a downturn in any single product category without distress.27 The dividend payout has been modest, reflecting the deliberate decision to retain cash for capex rather than return it to shareholders, which is the correct policy for a high-return-on-capital business with a long runway. Working capital has been actively managed through the contractual structure of client agreements, with most major contracts including provisions for raw-material price pass-through and inventory-financing arrangements that minimise the working-capital burden carried by HFL.1

The cumulative picture is of an owner-operator family running a listed company with the seriousness of a 100-year project. That mindset is rarer than it sounds. Many Indian listed companies are run either by detached professional management teams optimising for the next earnings beat or by promoter families who treat the listed entity as a personal piggy-bank. The Kotharis appear to do neither. They run Hindustan Foods like a multi-generational industrial asset that they intend to hand to the next generation in better condition than they received it.

With that operating philosophy established, the next question is where that capital has actually been going. Because the most surprising fact about Hindustan Foods in 2026 is that the largest and fastest-growing segments of the business have almost nothing to do with food.

VI. "Hidden" Businesses & The Diversification Play

Walk through the gates of a Hindustan Foods plant in कोयंबटूर Coimbatore and you can be forgiven for thinking you have arrived at the wrong company. There are no malt-beverage vats here. There are no biscuit-baking lines. What you see instead are sewing machines, rubber-injection presses, leather-cutting stations, and conveyor systems carrying half-finished sports shoes from one workstation to the next.5[^14] The largest single greenfield investment Hindustan Foods has made in the last several years is in fact a footwear-manufacturing complex in Tamil Nadu designed to produce athletic and lifestyle shoes for both domestic and export markets.[^14]

The footwear story did not begin with a single decision. It began with the Ponds Exports leather acquisition in 2016, which planted the seed.10 It expanded materially with the AeroCare deal in 2022, which—despite its name—included not just personal-care but also injection-moulded plastic and rubber capabilities that bridged into footwear and household goods.4 It became a strategic pillar when, in 2023, Hindustan Foods announced an investment of approximately ₹100 crore to build a new dedicated footwear plant in Tamil Nadu, designed to manufacture sports and casual footwear at scale for global brands.[^14] And it accelerated further with related acquisitions and capacity-build-outs across the footwear value chain through 2023 and into 2024, including engagements connected to एसएसआईपीएल SSIPL Lifestyle and parallel build-outs of injection-moulded sandal manufacturing capacity.5

The strategic question is: why footwear? The answer reveals how the Kotharis think about category expansion. Indian footwear, particularly the branded athletic and lifestyle segment, was structurally similar to Indian FMCG in 2013—dominated by multinational brand owners (नाइकी Nike, एडिडास Adidas, पुमा Puma, रीबॉक Reebok), who controlled marketing, distribution, and design, but who increasingly wanted to disaggregate manufacturing from the brand layer. India's footwear manufacturing base had historically been fragmented, low-quality, and concentrated in geographically isolated clusters in आगरा Agra and Tamil Nadu. There was no institutional, listed, capital-disciplined counterparty for brands wanting to scale Indian manufacturing.5[^14]

The Kotharis recognised that the footwear opportunity was a near-perfect rhyme of the FMCG opportunity they had already begun executing on. Same customer archetype (multinational brand owner), same procurement dynamics (long-cycle contracts, audited quality, dedicated lines), same structural tailwind (brand desire to offload capex), and—crucially—an entire decade of HFL's own institutional credibility that could be transferred from the FMCG conversation to the footwear conversation almost frictionlessly. A procurement officer at Reckitt who had spent years working with Hindustan Foods on cleaning products did not need to be sold on the company's capability when the conversation shifted to dishwashing detergents. The same institutional reference travelled into footwear via the parent-company conversations.5[^14]

The second major diversification has been into healthcare and over-the-counter products, anchored by the Reckitt Baddi acquisition discussed earlier but extended through several smaller capacity build-outs.[^5] The healthcare segment for HFL includes manufacturing of antiseptic solutions, pain-relief topicals, household OTC therapeutics, and—through a separate but related relationship—operations connected to medical-device contract manufacturing for brands like शोल Scholl. The strategic logic mirrors the footwear playbook: high-margin category, structurally outsourcing-friendly, and customers (हलियॉन Haleon, Reckitt, others) who have been actively divesting Indian manufacturing capacity over the last several years.[^5]

The third diversification, and the one that most clearly betrays the Kothari obsession with vertical integration, is in ice cream cones. In 2024, Hindustan Foods began ramping up a dedicated facility manufacturing ice cream cones at a scale of approximately one million cones per day, designed primarily to supply the company's own ice cream contract-manufacturing plants that produce branded frozen-dessert products for multinational clients.3 On its surface this is the smallest of the diversifications discussed here. In strategic terms it may be the most important. By integrating backwards into cone manufacturing, HFL captures a meaningful slice of the input-cost structure for the ice cream contracts it is already running. It controls quality, controls supply-chain risk, and—not incidentally—generates an incremental high-margin revenue line from selling cones to third parties when its own ice cream plants do not need the entire output.3

The segment-level economics of the diversified business are worth unpacking, because they reveal a more nuanced picture than the headline numbers suggest. The food-and-beverage segment, which includes the core malt-beverage and beverage-concentrate business plus the newer ice cream and dairy operations, contributes a substantial share of revenue but operates at the lower end of HFL's margin band, largely because the underlying products are commoditised and the brand owners have strong procurement leverage. The home-care segment, which includes household cleaners, laundry products, and air-care, runs at slightly better margins because the product categories are more technologically differentiated. The personal-care segment, including soaps, deodorants, and toiletries, sits in the middle. The healthcare and OTC segment, even though smaller in revenue terms, contributes disproportionately to gross profit because of the higher per-unit pricing and the more demanding quality standards that justify it. And the footwear segment, which is still in its capex-heavy ramp phase, has not yet contributed materially to consolidated profitability but is expected to be a significant gross-profit contributor as capacity utilisation matures.13

The diversification story raises an obvious question that long-term investors should sit with. Is Hindustan Foods diworsifying? Is the company spreading itself thin across too many product categories—FMCG, footwear, healthcare, ice cream cones—and risking the kind of complexity creep that eventually destroys focus and returns? The Kothari answer, articulated repeatedly in investor presentations and management interviews, is no, because every category they have entered shares the same underlying business model: dedicated contract manufacturing on long-term volume contracts with multinational counterparties.3[^7] The product changes. The customer archetype, the contracting structure, the operational discipline, and the capital-allocation framework do not.

Whether that argument holds up over time is, in the end, an empirical question that will be answered by the segment-wise return-on-capital numbers in the FY28 and FY30 annual reports rather than by any management commentary today. For now, the diversification has expanded the addressable market, deepened the relationships with anchor multinational clients, and reduced the company's dependence on any single product category.

That brings us to the strategic frameworks that long-term investors typically use to interrogate exactly this kind of business—the durability of competitive advantage in a structurally low-margin, asset-heavy, customer-concentrated industry.

VII. The Strategy Vault: 7 Powers & 5 Forces

There is a particular intellectual discipline required to analyse a company like Hindustan Foods, because the most superficial reading of the business gets the strategic picture exactly wrong. On the surface, HFL is a low-margin contract manufacturer working for customers many times its size. By that surface reading, the company should have no pricing power, no competitive moat, and no defensible long-term position. The reality is almost the opposite, and to see why, it helps to walk through the business through two of the most useful frameworks in modern strategy literature: Hamilton Helmer's 7 Powers and Michael Porter's 5 Forces.[^9]

Start with 7 Powers. The first power Helmer identifies is scale economies. In contract manufacturing, scale matters because the fixed cost of running quality systems, regulatory compliance infrastructure, procurement teams, and central engineering capability is essentially the same whether you run two plants or twenty-two. As HFL's plant count has grown—through acquisitions and greenfield builds—the per-plant overhead burden has compressed, while the company's bargaining power with raw-material suppliers and equipment vendors has expanded. A smaller contract manufacturer cannot afford to dedicate a full engineering team to optimising line throughput across multiple product categories. Hindustan Foods can.1 Scale economies are real here, though they are nowhere near as pronounced as in semiconductor foundries or hyperscale cloud infrastructure.

The second power, and the one that is most central to the Hindustan Foods story, is switching costs. We touched on this earlier when discussing the dedicated-manufacturing model, but the depth of the lock-in deserves more attention. When a multinational brand runs a flagship product through an HFL dedicated line, the lock-in operates on multiple dimensions simultaneously. There is formulation lock-in: the specific batch process, ingredient sequencing, and quality-control parameters configured for that line are not portable to another facility without weeks or months of re-validation. There is regulatory lock-in: many of HFL's plants hold product-specific approvals from food, drug, and consumer-safety regulators that cannot be replicated quickly elsewhere. There is supply-chain lock-in: the surrounding distribution and inventory infrastructure has been built around the geographic location of the HFL plant. And there is what might be called career-risk lock-in: the procurement officer who originally signed the contract has staked professional credibility on the relationship, and the cost of triggering a manufacturing transition that disrupts shelf availability is, for that officer, asymmetrically high. Switching costs are the most powerful and most durable of the moats Hindustan Foods has constructed, and they are accreting, not eroding, with every new long-term contract that gets added to the book.

The third power that applies here is what Helmer calls cornered resource, which we already touched on in the management section. The Kothari family's three-decade institutional knowledge of Indian contract manufacturing—the relationships, the operational muscle memory, the quality-protocol fluency, the regulatory navigation—is not something a competitor can buy at any price. A new entrant can hire engineers. It cannot hire the institutional memory of having delivered through three decades of Indian industrial-policy shifts.9 This cornered-resource moat is harder to measure than scale economies or switching costs, but it is one of the more durable forms of advantage.

The other Helmer powers apply to varying degrees. Counter-positioning is present in the sense that the multinational FMCG companies that are HFL's customers cannot easily replicate the low-margin, asset-heavy business model HFL operates, because doing so would destroy the capital-light financial profile their own shareholders demand. Process power is present in the operational discipline that has been built across multiple plants and product categories. Network economies and branding are largely absent—this is not a consumer-brand business and HFL's customers are not networked in a way that creates increasing returns to additional customers. So out of the seven powers, three are clearly present (scale, switching costs, cornered resource), two are partially present (counter-positioning, process power), and two are essentially absent (network economies, branding). For a business of this archetype, three durable powers with two supporting ones is a strong moat profile.

Now flip to Porter's Five Forces. The bargaining power of buyers is the obvious concern. HFL's top customers—Reckitt, Unilever, Danone, others—are vastly larger than HFL itself, have global procurement organisations, and in theory could exert significant pricing pressure. In practice, the buyer power is constrained by the switching costs we just described. Buyers can pressure HFL on incremental contract renewals at the margin, but they cannot easily walk away from an existing dedicated line, which means the long-tail of contracted revenue is protected even when individual price negotiations get tough.

The bargaining power of suppliers, by contrast, is moderate and manageable. HFL's main inputs are raw materials—chemicals, packaging materials, agricultural inputs, leather, rubber—that are sourced from competitive supplier markets where no single vendor has structural pricing leverage. Energy and labour are local-cost inputs that, while inflation-exposed, are largely passed through in the contracting structure.1

The threat of new entrants is, on paper, high. There is no patent moat, no proprietary technology, no regulatory entry barrier specific to HFL. In practice, the threat of new entrants is constrained by exactly the same reputational and switching-cost moats described above. A new contract manufacturer trying to enter at scale faces a multi-year process of building references, accumulating audits, and proving operational discipline before any meaningful share of multinational brand procurement budgets becomes accessible. The threat exists, but it operates on a timeline measured in decades, not quarters.

The threat of substitutes is the most subtle of the five forces in this case. The substitute is not another contract manufacturer; the substitute is the brand owner deciding to bring manufacturing back in-house. This is the structural risk that any HFL investor has to model. The countervailing dynamic, however, is the global trend among consumer-brand companies to reduce capital intensity, focus on marketing and distribution, and outsource the asset-heavy parts of the value chain. As long as that meta-trend persists—and there is no obvious reason to expect a reversal—the threat of substitution by in-housing remains manageable.

Industry rivalry, the fifth force, exists but is fragmented. The Indian contract-manufacturing landscape includes other players, including parts of the private operations within the broader Vanity Case Group ecosystem and various smaller domestic and foreign-owned contract manufacturers. None of them have the scale, listed-company governance, and diversified portfolio that HFL has assembled. The rivalry exists at the level of individual contract bids but does not translate into systemic pricing pressure at the industry level.[^9]

The composite reading from these two frameworks is the same. Hindustan Foods operates in a business that looks structurally low-margin and exposed but is actually defended by switching costs and cornered-resource advantages that accumulate over time. The moat is not visible on a single quarterly earnings statement. It is visible only in the trajectory of the contracted revenue book over multiple years and in the persistence of the customer relationships through multiple procurement cycles. For a long-term investor, that is exactly the kind of moat that the market tends to under-price in the short term and over-recognise once the compounding becomes obvious. Which brings us to the bull-bear debate.

VIII. Analysis: The Bull vs. Bear Case

Walk through the analyst notes on Hindustan Foods written in 2026 and you find a strikingly bifurcated set of views. The bulls and the bears are not arguing about the same data. They are arguing about which lens to apply to the data. Understanding that disagreement is the heart of the investment thesis.

The bull case begins with a single observation about the Indian consumer that is almost impossible to dispute: aggregate Indian household consumption of FMCG, footwear, personal-care, and home-care goods is on a multi-decade structural growth path driven by rising disposable income, urbanisation, formalisation of the retail sector, and the slow but steady premiumisation of every category from soap to sneakers. Whether the winner in Indian dishwashing detergent over the next decade is Reckitt or Unilever or गोदरेज Godrej or रिलायंस Reliance Industries or a yet-to-be-launched private label from a domestic retailer is, from Hindustan Foods' perspective, almost irrelevant. HFL manufactures for almost all of them, and the more the category grows, the more volume flows through the contracted plants.[^9] The bull case is, in essence, a bet on the Indian consumption story disaggregated from any specific brand's market share.

The second pillar of the bull case is the diversification trajectory we discussed earlier. As HFL extends from its core FMCG base into footwear, healthcare, and other higher-margin verticals, the consolidated margin profile of the business should structurally expand even without any improvement in pricing power on the legacy contracts. The arithmetic is simple. A growing share of revenue from higher-margin segments, holding the lower-margin segment margins constant, raises the company-level margin. If HFL's blended EBITDA margin has historically sat in the 7-to-9 percent range, the path to a 10-to-12 percent blended margin over the next several years runs through faster growth in healthcare, OTC, and premium personal-care relative to food and household commodities.13

The third pillar of the bull case is the structural reinvestment opportunity. Hindustan Foods has been compounding its gross block at a pace that exceeds most Indian industrial peers, deploying capital into new plants at returns that, based on disclosed contract structures, comfortably exceed the cost of capital. As long as the runway for new dedicated plants continues—and the multinational brand-owner appetite for outsourcing shows no sign of saturation—HFL has a structural mechanism for compounding earnings without needing to expand multiples. This is the textbook profile of a high-quality compounder: incremental capital deployed at attractive return on equity over a long runway.

Now turn to the bear case, which is more nuanced than the bulls tend to acknowledge. The first concern, and the one that gets aired most frequently on Indian sell-side calls, is customer concentration. The top five customers of Hindustan Foods, in aggregate, contribute a majority share of consolidated revenue.1 If any one of those customers decided to bring manufacturing back in-house, or shifted production to a rival contract manufacturer, or—worst case—exited the Indian market entirely, the revenue and earnings impact would be material. The switching-cost moats we discussed in the previous section make this scenario unlikely in any given quarter, but the cumulative tail risk over a multi-decade horizon is not zero.

The second bear-case concern is what might be called the asymmetric power dynamic with multinational counterparties. Even within the framework of long-term contracts, HFL's customers retain meaningful leverage at the margin on contract renewals, price escalation terms, and incremental volume commitments. Over time, the customers may be able to grind down HFL's per-unit margins faster than HFL can expand its asset base and product mix to compensate. This is the slow-bleed bear case—not a sudden customer exit, but a structural margin compression driven by relentless procurement pressure over a decade.

The third concern is execution risk on the diversification strategy. As Hindustan Foods extends into footwear, healthcare, ice cream cones, and other adjacencies, the operational complexity of managing multiple product categories across multiple geographies grows non-linearly. The Kothari management team has, so far, demonstrated impressive operational discipline. But the larger the company gets, and the more diversified its product mix becomes, the more difficult it is to maintain that discipline. The risk is not that any single new business fails; it is that the cumulative drag of managing too many things at once eventually shows up in slipping execution.

The fourth bear-case concern is valuation, and this is the most quantitatively-driven of the bear arguments.7 Hindustan Foods has historically traded at a price-to-earnings multiple in the range of 50x or higher, which is rich by any standard, even allowing for the structural growth runway. The implicit assumption baked into that multiple is that the company will continue compounding earnings at the historical rate for an extended period. If the compounding rate slows—whether due to customer concentration risk, margin compression, execution slippage, or simply the law of larger numbers as the base expands—the multiple compression alone would be a meaningful headwind for the stock even if absolute earnings continue to grow.7

Layering on the strategic-framework view we developed in the previous section, the bull-bear debate ultimately resolves into a question about the durability of the switching-cost moat. The bulls believe the moat is structural and deepens over time. The bears believe the moat is real but slowly eroded by procurement pressure and the long-term competitive evolution of the contract-manufacturing industry. Both views are intellectually defensible, and the honest answer is that the truth probably lies somewhere in between.

A myth-versus-reality check is useful here. The consensus narrative on Hindustan Foods, as expressed in the more enthusiastic Indian financial press, often paints the company as a "no-risk" compounder benefiting from a structural Indian consumption tailwind. The reality is that the business carries real risks—customer concentration, margin compression, execution complexity—that are not always honestly priced into either the narrative or the multiple. Conversely, the consensus narrative among some traditional value investors is that the company is dangerously over-valued at current multiples. The reality there is that the switching-cost moat is more durable than a simple multiple-comparison analysis captures, and the runway for incremental capital deployment at attractive returns is genuinely long.

For investors who want to follow the story without getting trapped in either the bull or the bear narrative, three key performance indicators are worth tracking closely over the next several years. The first is asset turnover—the ratio of revenue to gross block—which captures whether HFL is sweating its expanding asset base at progressively higher utilisation rates. The second is return on equity, which captures whether the incremental capital being deployed into new plants is actually generating attractive returns through the cycle. The third is the growth rate of the non-food segments—footwear, healthcare, personal-care—relative to the food-and-beverage segment, which captures whether the diversification thesis is actually translating into a structurally improving mix. Those three indicators, tracked over multiple years, will tell the real story far more reliably than any quarter-to-quarter beat-or-miss commentary.

IX. Epilogue & Final Thoughts

If you stand back from the entire arc of this story and squint, what you see is a particular kind of Indian capitalist enterprise that the global investment community has only recently begun to take seriously. Hindustan Foods is not a brand. It does not own consumer mindshare. It does not advertise. It does not appear on the front pages of the business press except when it announces an acquisition. But it has positioned itself, deliberately and patiently, at the structural choke point of one of the most important value chains in the Indian economy—the manufacturing of the things that Indian households consume every single day.

The Kothari legacy, if we are going to call it that, is not the construction of a brand. It is the construction of an operating system. Every multinational FMCG company operating in India is, in some material sense, plugged into the manufacturing platform that Hindustan Foods has built over the last decade. The brands write the marketing. The brands own the distribution. The brands collect the consumer margin. And underneath all of that, Hindustan Foods runs the plants that actually make the products. It is, in the original sense of the term, infrastructure.

The Foxconn analogy that has followed the company through its growth years is imperfect but illuminating. Foxconn's relationship with Apple is one of asymmetric dependency: Apple needs Foxconn to ship iPhones, Foxconn needs Apple to keep the assembly lines running. The relationship is mediated by long-term contracts, deep capex commitments, and a level of operational integration that, in practice, makes the two companies a single supply chain organised under two different legal entities. The HFL-with-Reckitt or HFL-with-Unilever relationships have a similar texture. The brand cannot run the plants. The plant operator cannot capture the consumer margin. Neither side can easily walk away. The relationship is not a vendor relationship; it is a supply-chain marriage.[^9]

What happens next for Hindustan Foods is genuinely interesting. The natural next horizon is international expansion. The same logic that has driven HFL's growth in India—multinational brands wanting to disaggregate manufacturing from brand ownership in a high-growth emerging market—applies, with appropriate modifications, to Southeast Asia, parts of Africa, and the Middle East. Whether the Kotharis will actually pursue international expansion, and whether they can do so without diluting the operational discipline that has been the foundation of their domestic success, is one of the most important strategic questions facing the company over the next decade.[^7]

The second open question is what happens when the next generation of the Kothari family takes over. Family-controlled Indian businesses have a famously bimodal track record on generational transitions—some flourish under the second or third generation, others descend into family disputes and value destruction. Sameer Kothari, as the third generation of his family in this industry, is still the active operator. The transition to a fourth generation, when it eventually happens, will be a moment that long-term shareholders should watch with particular attention.

The third open question, and the most interesting one for long-term observers, is whether Hindustan Foods will eventually become the platform on which an entirely new category of Indian consumer business is built—a kind of "white-label private label" infrastructure that allows new entrants to launch consumer brands without ever building manufacturing capacity. The economic logic for such an evolution exists. The execution complexity is substantial. The Kothari management has, so far, focused on serving existing multinational brand owners rather than enabling new entrants, but the boundary between those two strategies is porous, and a future iteration of HFL operating partly as a platform for emerging Indian D2C brands is not implausible.

For now, what Hindustan Foods is can be summarised in a single sentence. It is the listed, professionally managed, capital-disciplined operating system that powers the Indian consumer-goods economy. Its founders built a factory. Its current operators built a platform. The next chapter, like every chapter that came before, will be written one acquisition, one greenfield plant, and one long-term contract at a time. The lesson of the Hindustan Foods story, for any long-term investor watching India, is that some of the most interesting compounders are the companies that have made themselves deliberately invisible. The brands you can see on the shelf are the visible tip of the iceberg. The companies that actually make the products underneath—organised, listed, scaled, professionalised—are the part of Indian capitalism that the next generation of global investors is only now beginning to understand. Hindustan Foods, for better or worse, is the prototype of what that understanding looks like.

References

References

-

Annual Report 2023-24 — Hindustan Foods Limited, 2024-08-14 ↩↩↩↩↩↩↩↩↩↩↩↩↩

-

Annual Report 2022-23 — Hindustan Foods Limited, 2023-08-10 ↩↩↩↩

-

Investor Presentation Q1FY25 — Hindustan Foods Limited, 2024-08-14 ↩↩↩↩↩↩

-

Acquisition of AeroCare Personal Products — BSE/NSE Filing, 2022-02-14 ↩↩↩↩

-

Hindustan Foods to expand footwear manufacturing via acquisitions — Moneycontrol, 2023-11-20 ↩↩↩↩↩↩

-

Detailed Scheme of Arrangement for Promoter Merger — HFL Investor Relations, 2024-03-01 ↩↩↩↩

-

Corporate Governance Report FY24 — National Stock Exchange of India, 2024-07-20 ↩

-

Vanity Case Group: The Parent Entity Strategy — Official Website ↩↩↩↩↩

-

Hindustan Foods acquires Ponds Exports from HUL — Business Standard, 2016-11-04 ↩↩↩

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube