Hindustan Unilever: Building India's FMCG Empire

I. Introduction & Episode Roadmap

Nine out of ten Indian households. That's the staggering reach of Hindustan Unilever Limited, a company that has woven itself so deeply into the fabric of Indian daily life that its products—from Surf Excel detergent to Lifebuoy soap, from Brooke Bond tea to Magnum ice cream—have become synonymous with their categories. With revenues exceeding ₹60,000 crore and a market capitalization hovering around ₹6 trillion, HUL stands as India's most valuable FMCG company, a testament to nearly 135 years of evolution from colonial importer to indigenous powerhouse. With revenues exceeding ₹61,400 crore and a market capitalization around ₹5.9 trillion, HUL stands as India's most valuable FMCG company, a testament to nearly 135 years of evolution from colonial importer to indigenous powerhouse.

The central question that frames our exploration is deceptively simple yet profoundly complex: How did a colonial soap importer transform into India's most dominant consumer goods company? This is not merely a story of business expansion—it's a narrative that mirrors India's own economic journey from colonial dependency to emerging market powerhouse, from socialist constraints to liberalized dynamism, from urban concentration to rural penetration.

What unfolds is a masterclass in navigating emerging markets, a blueprint for building consumer empires in complex, diverse, and rapidly evolving economies. We'll trace HUL's evolution through distinct epochs: the colonial foundations when Sunlight soap first arrived at Indian ports, the post-independence era of navigating socialist policies and the License Raj, the transformative moment of 1991's economic liberalization that unleashed unprecedented growth, and the modern challenges of digital disruption and changing consumer preferences.

This analysis reveals three critical themes that define HUL's endurance. First, the power of distribution as a competitive moat—how reaching 9 million retail outlets creates an almost insurmountable barrier to entry. Second, the delicate balance between global sophistication and local adaptation—leveraging Unilever's worldwide R&D while creating products uniquely suited to Indian conditions. Third, the strategic importance of timing—being present before independence, adapting during socialism, and aggressively expanding during liberalization.

For students of business strategy, HUL offers invaluable lessons about building in emerging markets: the importance of patient capital, the necessity of portfolio diversification across price points, the power of acquisition-led growth, and the critical role of talent development in creating sustainable competitive advantages. This is the definitive story of how a foreign company became more Indian than many domestic brands, and how that transformation created one of the most valuable consumer goods enterprises in Asia.

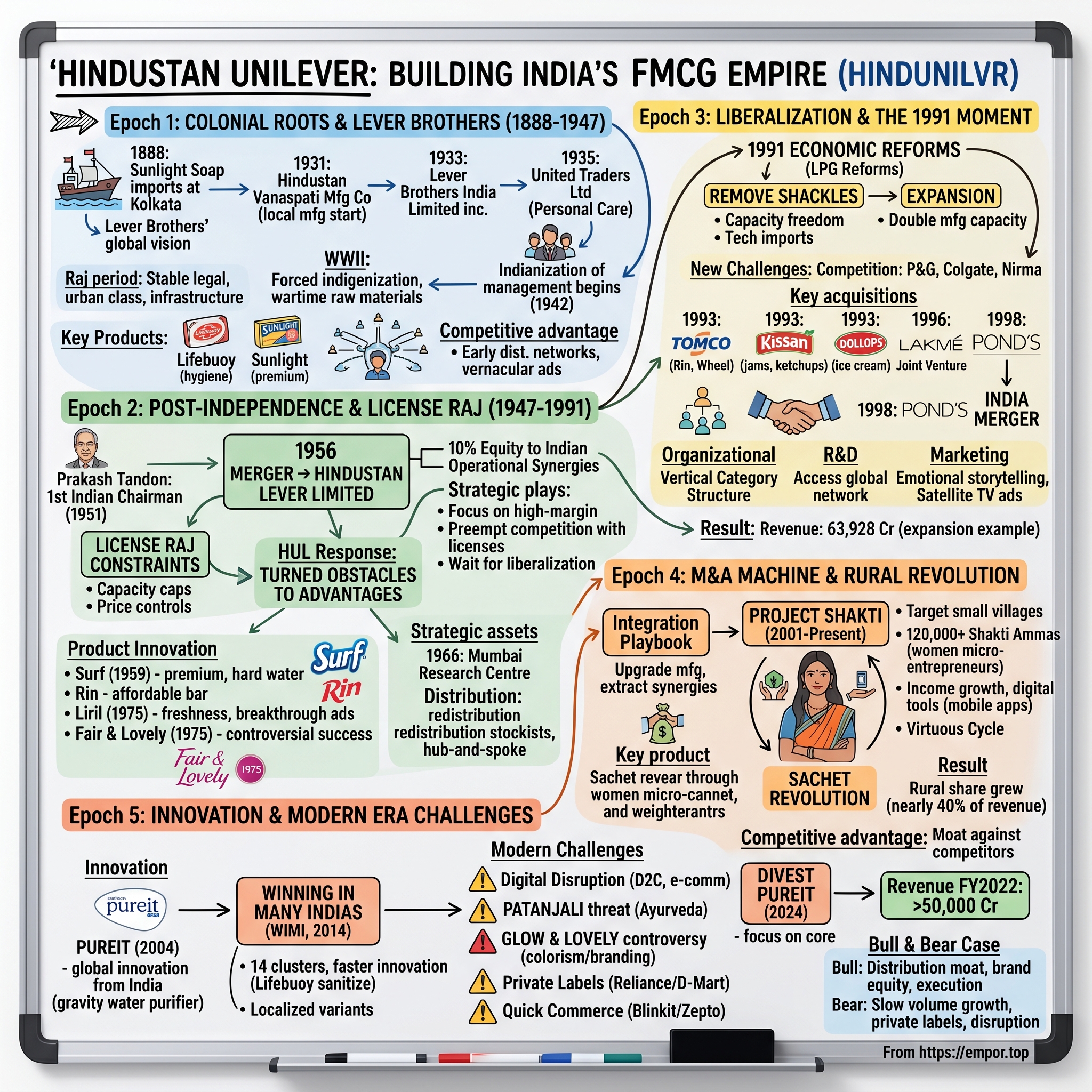

II. Colonial Roots & The Lever Brothers Era (1888–1947)

The year was 1888. At Kolkata's bustling harbor, then the commercial heart of British India, wooden crates marked "Sunlight Soap - Made in England by Lever Brothers" were unloaded from merchant ships. These crates, containing the world's first packaged, branded laundry soap, represented more than just a new product—they embodied the beginning of modern consumer marketing in India. William Hesketh Lever, the visionary founder of Lever Brothers, had identified India not merely as a market for British goods, but as a critical piece in his ambition to build the world's first global consumer goods empire.

Lever's vision for India was both pragmatic and prescient. While other British companies saw the subcontinent primarily as a source of raw materials and a captive market for manufactured goods, Lever recognized the potential for local manufacturing and market development. His philosophy, revolutionary for its time, centered on the belief that soap wasn't just a product but a vehicle for social improvement—a perspective that would later evolve into the concept of "doing well by doing good" that still permeates Unilever's corporate culture today.

The formal establishment of operations began to take shape in the 1930s, a period of significant political and economic transformation in India. In 1931, Lever Brothers took its first major step toward local manufacturing by establishing the Hindustan Vanaspati Manufacturing Company. This wasn't merely about producing vanaspati (hydrogenated vegetable oil)—it was a strategic move to secure a local supply chain for soap production while creating a standalone profitable business. The choice of vanaspati was particularly astute; it addressed a genuine market need for affordable cooking fat while providing the raw materials necessary for soap manufacturing.

Two years later, in 1933, Lever Brothers India Limited was formally incorporated, marking the transition from import-based operations to a locally registered entity. This was followed in 1935 by the establishment of United Traders Limited, which focused on personal care products. The three-company structure—Hindustan Vanaspati, Lever Brothers India, and United Traders—wasn't accidental. It reflected both the regulatory requirements of operating in British India and a sophisticated understanding of market segmentation that was decades ahead of its time.

The Raj period presented unique opportunities and challenges for building a consumer goods business. On one hand, the colonial administration provided a stable legal framework, established transportation infrastructure, and a growing urban middle class familiar with Western products. The British-educated Indian elite in cities like Bombay, Calcutta, and Madras readily adopted products like Sunlight soap and Lifebuoy, viewing them as symbols of modernity and hygiene.

However, the challenges were equally formidable. India's vast geography, diverse languages, and predominantly rural population meant that distribution beyond major cities was extraordinarily difficult. The company had to navigate complex social structures, including the caste system, which influenced consumption patterns in unexpected ways. Religious considerations affected product formulation—soaps couldn't contain tallow in regions with large Hindu populations, while Muslim consumers had their own dietary and purity requirements.

The import substitution strategy that Lever Brothers pioneered during this period would become a template for multinational corporations operating in developing markets for decades to come. Rather than simply importing finished goods from Britain, the company began establishing local manufacturing facilities. The Sewri factory in Bombay, established in the 1930s, became one of the largest soap manufacturing facilities in Asia. This shift from imports to local production wasn't just economically advantageous—it was politically astute, demonstrating commitment to India at a time when nationalist sentiment was rising.

The Second World War marked a crucial inflection point. With shipping lanes disrupted and imports restricted, local manufacturing became not just advantageous but essential. The war years forced rapid indigenization of both production and management. Raw material shortages led to innovative formulations using locally available ingredients. The company developed new supply chains, working directly with Indian farmers for coconut oil and other agricultural inputs. These relationships, forged under wartime necessity, would become enduring competitive advantages in the post-independence era.

Perhaps most significantly, the war years accelerated the Indianization of management—a process that would distinguish Lever Brothers from other British companies in India. In 1942, even before independence was assured, the company began systematically training Indian managers for senior positions. This wasn't tokenism; it was a recognition that long-term success in India would require Indian leadership. Young Indians were sent to Britain for training, exposed to global best practices, and groomed for leadership roles.

The recruitment and development of Indian talent during this period reads like a who's who of future Indian corporate leadership. The company attracted the brightest graduates from Indian universities, offering them career prospects that few other organizations could match. This early investment in Indian talent would pay enormous dividends, creating a pipeline of leaders who understood both global business practices and local market nuances.

The product portfolio during the colonial era was carefully curated to serve different market segments. Sunlight soap targeted the affluent urban households, promising superior cleaning power for fine fabrics. Lifebuoy, launched in India in 1895, was positioned as the hygiene soap for the masses, with its distinctive red color and carbolic odor signifying its germicidal properties. The marketing of these products revealed sophisticated understanding of Indian consumer psychology—Lifebuoy's health platform resonated with traditional Indian emphasis on purity and cleanliness, while Sunlight's premium positioning appealed to aspirational consumers.

Distribution strategies during this period laid the groundwork for what would become HUL's most formidable competitive advantage. The company established a network of distributors and wholesalers that reached deep into tier-2 and tier-3 cities. They pioneered the concept of "direct coverage," where company representatives would visit retailers directly, ensuring product availability and visibility. This distribution architecture, painstakingly built over decades, created relationships and market knowledge that competitors would find nearly impossible to replicate.

The marketing innovations of this era were remarkably prescient. Lever Brothers was among the first to use Indian languages in advertising, recognizing that English-only communication would limit market reach. They sponsored local events, from religious festivals to sports competitions, embedding their brands in Indian cultural life. The company's advertising didn't just sell products; it sold ideas—hygiene, modernity, and progress—that resonated with an India on the cusp of independence.

As 1947 approached and independence became imminent, Lever Brothers faced a critical decision. Many British companies were reducing their Indian exposure, fearful of nationalization or hostile regulation. Lever Brothers chose differently. They accelerated Indianization, increased local investment, and prepared for a post-colonial future. This decision—to double down on India at a moment of maximum uncertainty—would prove to be one of the most consequential in the company's history.

The colonial era had established the foundations: manufacturing capabilities, distribution networks, brand equity, and most importantly, a cadre of Indian managers ready to lead. As the Union Jack was lowered for the last time on August 15, 1947, Lever Brothers was positioned not as a colonial relic but as a company ready to participate in building independent India. The seeds planted during these six decades would flourish in ways that neither William Lever nor his successors could have imagined.

III. Post-Independence Transformation & The License Raj (1947–1991)

The stroke of midnight on August 15, 1947, brought not just political freedom but a fundamental reimagining of India's economic destiny. For Lever Brothers, independence meant navigating an entirely new reality—a socialist-leaning government suspicious of foreign capital, a regulatory framework that would soon crystallize into the License Raj, and a nation determined to build self-reliance through import substitution. The company's response to these challenges would transform it from a foreign subsidiary into an institution that would become inseparable from India's own economic development.

The appointment of Prakash Tandon as the first Indian chairman in 1951 marked more than a symbolic transition—it represented a fundamental shift in how the company would operate in independent India. Tandon, who had joined Lever Brothers in 1939 and trained in Britain, embodied the bicultural competence that would become HUL's hallmark. His appointment sent a powerful signal to both the government and consumers that this was no longer a British company operating in India, but an Indian company with British parentage. Under his leadership, the company would navigate the treacherous waters of economic nationalism while maintaining its connection to global best practices.

The transformative moment came in 1956 with the merger of Hindustan Vanaspati Manufacturing Company, Lever Brothers India Limited, and United Traders Limited into a single entity—Hindustan Lever Limited. This wasn't merely corporate restructuring; it was a masterstroke of political and business acumen. By offering 10% equity to Indian shareholders, the company preempted potential nationalization while creating a constituency of Indian stakeholders invested in its success. The choice of name itself—putting "Hindustan" before "Lever"—signaled where the company's loyalties lay.

The merger created operational synergies that would prove crucial in navigating the License Raj. Under India's Industrial Policy Resolution of 1956, the government controlled virtually every aspect of industrial production—what could be produced, in what quantities, where factories could be located, and at what prices products could be sold. Having a single corporate entity simplified compliance with this byzantine regulatory framework while allowing for more efficient capital allocation across different product categories.

The License Raj, which would dominate Indian economic life until 1991, presented challenges that would have broken less adaptable companies. Production capacity was strictly controlled—if HUL wanted to increase soap production by even a few tons, it needed government permission. Prices were regulated, often below what market dynamics would dictate. Foreign exchange for importing raw materials or technology was scarce and strictly rationed. Yet within these constraints, HUL didn't just survive—it thrived, turning regulatory obstacles into competitive advantages.

The company's strategy during this period was brilliantly counterintuitive. While the License Raj constrained production capacity, it also limited competition. New entrants found it nearly impossible to get licenses, while HUL's established presence gave it preferential access. The company used its limited production capacity strategically, focusing on high-margin products and building brand equity that would pay dividends when restrictions were eventually lifted. They treated licenses not as constraints but as assets, accumulating them whenever possible to preempt competition.

The product launches of this era reveal how HUL adapted global innovations to Indian conditions while navigating regulatory constraints. Surf, launched in 1959, exemplified this approach. While Unilever had developed synthetic detergents for Western markets, the Indian version had to be fundamentally different. It needed to work in hard water, common across India. It had to be effective in cold water, as hot water washing was rare. The formulation used locally available raw materials to navigate import restrictions. Most importantly, it had to deliver visible results at a price point accessible to middle-class Indians.

The marketing of Surf created a template that HUL would use repeatedly—premiumization within reach. The tagline "Surf ki kharidari mein hi samajhdari hai" (Buying Surf is the smart choice) didn't just sell detergent; it sold aspiration wrapped in pragmatism. The Lalitaji campaign, featuring a middle-class housewife who chose quality over false economy, became one of Indian advertising's most iconic creations. This wasn't just advertising; it was cultural anthropology transformed into commercial communication.

Rin, positioned as the affordable alternative to Surf, demonstrated HUL's sophisticated understanding of market stratification. While the License Raj limited overall production, it didn't prevent product differentiation. By offering products at multiple price points, HUL could capture different consumer segments while maximizing returns from limited production capacity. This portfolio approach—premiums for the affluent, popular products for the middle class, and affordable options for the masses—became the cornerstone of HUL's strategy.

The launch of Liril in 1975 represented a different kind of innovation—cultural as much as commercial. In a conservative society where discussion of personal hygiene was taboo, Liril's advertising featuring a woman enjoying a waterfall bath was revolutionary. The lime-fresh positioning and the unforgettable jingle created a new category of freshness soaps. More importantly, it demonstrated HUL's ability to push cultural boundaries while remaining within acceptable limits—a delicate balance that few competitors could achieve.

Fair & Lovely, launched in 1975, would become both HUL's most successful and most controversial product. The fairness cream tapped into deep-seated Indian preferences for lighter skin—a complex legacy of caste, class, and colonial history. While the product would later face criticism for perpetuating colorism, its commercial success was undeniable. It demonstrated HUL's willingness to address consumer needs that others ignored, even when those needs raised uncomfortable questions about social values.

The establishment of the Research Centre in Mumbai in 1966 marked a crucial evolution in HUL's capabilities. This wasn't just about adapting global products to Indian conditions—it was about creating innovations specifically for Indian consumers. The center developed products that addressed uniquely Indian challenges: soaps that worked in hard water, detergents effective at lower temperatures, and foods that retained nutrition despite limited refrigeration. This R&D capability would become increasingly important as India opened up to global competition.

The relationship with Unilever during the License Raj era was complex and sometimes contentious. The Indian government was suspicious of foreign companies repatriating profits and transferring technology at what it considered excessive prices. The Foreign Exchange Regulation Act (FERA) of 1973 required foreign companies to reduce their equity to 40%, threatening Unilever's control. Through careful negotiation and by demonstrating its commitment to India through local R&D and manufacturing, HUL secured an exemption, maintaining Unilever's majority stake.

Technology transfer during this period was carefully managed to satisfy both government requirements and business needs. Unilever shared manufacturing processes, formulations, and management practices, but always with an eye toward maintaining some degree of technological dependence. This delicate balance—transferring enough technology to satisfy regulators while maintaining competitive advantages—required constant negotiation and adjustment.

The distribution innovations of this period laid the groundwork for HUL's future dominance. Recognizing that the License Raj made large-scale manufacturing expansion difficult, the company focused on distribution efficiency. They pioneered the concept of "redistribution stockists" in smaller towns, who would supply retailers in surrounding rural areas. This hub-and-spoke model allowed HUL to reach markets that were economically unviable for direct coverage. By the 1980s, HUL products were available in towns and villages that had never seen other branded products.

The company's approach to talent development during the License Raj era created a competitive advantage that persists to this day. With foreign exchange restrictions limiting the ability to bring in expatriate managers, HUL had no choice but to develop local talent. The company established one of India's most rigorous management training programs, recruiting from the best colleges and providing exposure to global best practices. This investment in human capital created a pipeline of leaders not just for HUL but for Indian industry as a whole.

The social initiatives undertaken during this period weren't just corporate philanthropy—they were strategic investments in market development. Rural development programs improved purchasing power in potential markets. Health and hygiene education created demand for HUL products. These initiatives, while generating goodwill with the government and communities, also built brand awareness and consumer education in markets that would become increasingly important.

As the 1980s drew to a close, cracks in the License Raj system were becoming apparent. The Indian economy was stagnating, foreign exchange reserves were depleting, and the Soviet Union—India's economic model—was collapsing. HUL, constrained for decades by production limits and price controls, had nevertheless built formidable advantages: unmatched distribution, powerful brands, deep consumer understanding, and strong local capabilities.

The company had also developed something intangible but invaluable: the ability to thrive within constraints. This organizational capability—turning regulatory obstacles into competitive moats, finding opportunity within limitation—would prove crucial when the economic liberalization of 1991 suddenly removed the constraints that had defined Indian business for four decades. HUL was like a coiled spring, compressed by regulation but ready to expand explosively when released.

The License Raj era had transformed HUL from a foreign subsidiary into an Indian institution. The company had learned to navigate not just regulations but the deeper currents of Indian society—its aspirations, anxieties, and contradictions. It had built capabilities that no amount of capital could quickly replicate: relationships with millions of retailers, understanding of diverse Indian consumers, and the ability to operate profitably in one of the world's most challenging business environments.

As 1991 approached, India stood on the brink of revolutionary change. The economic crisis that would force liberalization was building, though few recognized its magnitude. HUL, having spent four decades building within constraints, was about to discover what it could achieve without them. The patient investments in brands, distribution, and capabilities made during the License Raj would soon generate returns that would transform HUL from a successful Indian company into one of the emerging world's most valuable corporations.

IV. The 1991 Moment: Liberalization Changes Everything

June 1991. India's foreign exchange reserves had dwindled to barely three weeks of imports. The government, forced to airlift gold to London as collateral for emergency loans, faced its gravest economic crisis since independence. Finance Minister Manmohan Singh, in his budget speech on July 24, quoted Victor Hugo: "No power on earth can stop an idea whose time has come." The idea was economic liberalization, and for Hindustan Lever, it represented the removal of shackles that had constrained its growth for four decades. The liberalization package was revolutionary in its scope. The crisis in 1991 forced the government to initiate a comprehensive reform agenda, including Liberalisation, Privatisation and Globalisation, referred to as LPG reforms. Industrial licensing was abolished for all but 18 industries. The dreaded MRTP Act, which had constrained large companies' expansion, was effectively dismantled. Foreign direct investment limits were raised from 40% to 51% in most sectors, with some allowing 100% foreign ownership. Import restrictions that had protected domestic industry for decades were swept away. The rupee was devalued and made partially convertible. For Hindustan Lever, each of these changes represented the removal of a shackle that had constrained growth for four decades.

The immediate impact on HUL was transformative. Production capacity, frozen for years by licensing requirements, could now be expanded based on market demand rather than bureaucratic approval. The company immediately announced plans to double manufacturing capacity across categories. New product launches, previously delayed by months or years of regulatory approval, could now be fast-tracked. Import of technology and raw materials, once subject to foreign exchange rationing, became a matter of commercial decision rather than government permission.

But liberalization brought a double-edged sword—while removing constraints, it also invited competition. Procter & Gamble, HUL's global arch-rival, entered India in 1991 with ambitious plans. Colgate-Palmolive, previously confined to toothpaste, expanded into soaps and detergents. Nirma, the homegrown detergent manufacturer that had already disrupted HUL's dominance in the 1980s, now had access to technology and capital to mount an even stronger challenge. The comfortable oligopoly of the License Raj era was over; HUL would have to fight for every percentage point of market share.HUL's response was swift and strategic. Rather than defending market share through price wars or incremental innovation, the company embarked on an aggressive consolidation strategy. The crown jewel of this strategy was the acquisition of Tata Oil Mills Company (TOMCO) in 1993. In one of the most visible and talked about events of India's corporate history, the erstwhile Tata Oil Mills Company (TOMCO) merged with HUL, effective from April 1, 1993. This wasn't just any acquisition—TOMCO was HUL's largest competitor in soaps and detergents, holding significant market share with brands like Rin, Wheel, and OK.

The TOMCO acquisition was a masterclass in strategic timing and execution. On March 9, 1993, Tomco and HLL announced their intention to merge, effective April 1, 1993. The merger terms included an exchange ratio of two HLL shares for every 15 Tomco shares. The deal structure was carefully crafted to appeal to TOMCO shareholders while maintaining value for HUL investors. The exchange ratio of 2 HUL shares for every 15 TOMCO shares reflected the relative valuations while offering TOMCO shareholders participation in the combined entity's future growth.

What made the TOMCO acquisition transformative wasn't just its size but its strategic implications. HUL acquired Rin and Wheel, two brands that had successfully competed in the mass market segment where HUL had traditionally been weak. Rin, positioned as an affordable bar soap for clothes washing, complemented HUL's premium Surf detergent powder. Wheel, an even more affordable option, gave HUL entry into the bottom-of-pyramid market that Nirma had so successfully captured. This portfolio approach—premium, popular, and mass market brands under one roof—would become HUL's signature strategy.

The integration of TOMCO revealed HUL's operational excellence. Rather than simply absorbing TOMCO's operations, HUL rationalized manufacturing, optimized distribution networks, and repositioned brands to minimize cannibalization while maximizing market coverage. TOMCO's manufacturing facilities were upgraded to HUL standards, improving quality while reducing costs. The combined distribution network eliminated redundancies while extending reach. Within two years, the acquired brands were contributing significantly to HUL's growth, validating the acquisition strategy.

The Brooke Bond-Lipton merger represented another dimension of HUL's post-liberalization transformation. The beverages market in India was fragmented, with regional players dominating local markets. By combining Brooke Bond's strength in tea with Lipton's global brand equity, HUL created a beverages powerhouse. The merger, effective January 1, 1996, brought together complementary strengths—Brooke Bond's deep distribution in South India, Lipton's strength in packet tea, and both companies' understanding of Indian tea-drinking habits.

The liberalization era also saw HUL expanding beyond its traditional categories through strategic partnerships and acquisitions. The joint venture with Kimberly-Clark in 1994 to market Huggies diapers and Kotex sanitary pads represented entry into new personal care segments. The Lakme acquisition gave HUL a foothold in cosmetics, a category with enormous growth potential as Indian women increasingly entered the workforce. The Kissan acquisition from the UB Group in 1993 strengthened HUL's presence in processed foods, while the Kwality ice cream partnership marked entry into frozen desserts.

Each of these moves reflected a sophisticated understanding of post-liberalization dynamics. With production constraints removed, the game had shifted from capacity utilization to market share capture. With import barriers lowered, the threat wasn't just from domestic competitors but from global giants. With consumers having more choices, brand building and innovation became more critical than ever. HUL's acquisition spree wasn't just about buying brands—it was about preempting competition, filling portfolio gaps, and building scale advantages that would be difficult to replicate.

The capital allocation strategy during this period was equally sophisticated. HUL maintained its dividend payout to shareholders while funding acquisitions through a combination of internal accruals and modest debt. The company's strong cash generation allowed it to be opportunistic—moving quickly when acquisition targets became available while maintaining financial flexibility. This balance between growth investment and shareholder returns would become a hallmark of HUL's financial management.

The organizational transformation required to manage this expanded portfolio was profound. HUL reorganized from a functional structure to a category-focused organization. Separate verticals for Home & Personal Care, Foods & Beverages, and Specialty Chemicals were created, each with its own management team and P&L responsibility. This structure allowed for focused attention on diverse categories while maintaining synergies in procurement, distribution, and corporate functions.

The human capital implications of liberalization were equally significant. With multinationals entering India and Indian companies expanding globally, the war for talent intensified. HUL's response was to strengthen its position as India's premier finishing school for management talent. The company's management trainee program became even more selective and rigorous. Compensation packages were benchmarked globally. Career paths were accelerated, with high performers reaching senior positions faster than ever before.

The R&D response to liberalization reflected the new competitive reality. While the Mumbai research center continued its work on India-specific innovations, HUL now had greater access to Unilever's global R&D network. Technology transfer agreements were liberalized, allowing faster introduction of global innovations. The company established specialized labs for different categories, recognizing that innovation in foods required different capabilities than innovation in detergents. The focus shifted from adaptation to innovation—creating products for India that could potentially be exported to other emerging markets.

The marketing evolution during this period was dramatic. With private television channels proliferating after liberalization, advertising opportunities exploded. HUL was among the first to recognize the power of satellite television, becoming one of the largest advertisers on channels like Zee TV and Star Plus. The company's advertising moved from product functionality to emotional storytelling, recognizing that in a competitive market, emotional connections mattered as much as functional benefits.

The distribution transformation accelerated by liberalization was perhaps most significant. With restrictions on transportation and warehousing removed, HUL could optimize its supply chain like never before. The company invested in IT systems to track inventory and sales in real-time. The traditional "push" system of loading distributors with inventory gave way to a "pull" system responding to actual consumer demand. Direct coverage of retail outlets increased from thousands to hundreds of thousands, ensuring product availability and visibility.

As the 1990s progressed, it became clear that liberalization had fundamentally transformed not just HUL but Indian business itself. The comfortable certainties of the License Raj—guaranteed profits for established players, protection from foreign competition, regulated prices ensuring margins—were gone forever. In their place was a dynamic, competitive marketplace where success required constant innovation, operational excellence, and deep consumer understanding.

For HUL, liberalization had been exactly the catalyst needed to transform from a successful Indian company into a regional powerhouse. Revenue: 63,928 Cr today represents a dramatic expansion from the constrained growth of the pre-liberalization era. The removal of regulatory shackles had allowed HUL to realize its full potential, leveraging decades of patient investment in brands, distribution, and capabilities. The company that emerged from the first decade of liberalization was fundamentally different—larger, more dynamic, more competitive—than the one that had entered 1991. The stage was set for even more dramatic expansion in the decades to come.

V. The M&A Machine: Building Through Acquisitions (1993–2010)

The liberalization of 1991 didn't just remove constraints—it fundamentally rewired the logic of competition in Indian FMCG. Market share, once protected by licensing restrictions, now became a battlefield where only scale and execution excellence could provide sustainable advantage. For Hindustan Lever, this new reality triggered one of the most ambitious acquisition campaigns in Indian corporate history, transforming the company from a large player into an almost omnipresent force across consumer categories.

The post-TOMCO success had proven that HUL could execute complex acquisitions, integrate diverse businesses, and extract synergies that justified premium valuations. This confidence, combined with strong cash generation and Unilever's global support, enabled HUL to embark on a systematic consolidation of the Indian FMCG market. The strategy was multi-pronged: acquire struggling competitors to eliminate threats, buy successful regional brands to accelerate geographic expansion, and purchase niche players to enter new categories quickly. The Kissan acquisition in 1993 exemplified HUL's strategic approach. In 1993, Kissan was acquired by Brooke Bond India and is now an integral part of Hindustan Unilever Limited (HUL). Kissan had been purchased by the UB Group's Vittal Mallya from the Mitchell Brothers in 1950, and by the early 1990s, was a well-established brand in jams, ketchups, and squashes. For HUL, Kissan represented entry into processed foods—a category with enormous growth potential as Indian consumers increasingly adopted convenience foods. The acquisition brought not just brands but also manufacturing expertise in food processing and relationships with farmers for raw material sourcing.

The Dollops ice cream acquisition from Cadbury India, also in 1993, marked HUL's entry into frozen desserts. This was followed by the launch of Wall's in 1994, leveraging Unilever's global ice cream expertise. 1994 witnessed BBLIL launching the Wall's range of Frozen Desserts. By the end of the year, the company entered into a strategic alliance with the Kwality Icecream Group families and in 1995 the Milkfood 100% Icecream marketing and distribution rights too were acquired. The ice cream market in India was nascent but growing rapidly with increasing refrigerator penetration and changing consumption habits. HUL's strategy was to dominate the category early, building distribution infrastructure that would be difficult for competitors to replicate. The Lakme acquisition represented HUL's entry into cosmetics through a particularly strategic route. HUL and yet another Tata company, Lakmé Limited, formed a 50:50 joint venture, Lakmé Unilever Limited, to market Lakmé's market-leading cosmetics and other appropriate products of both the companies in 1996. Subsequently in 1998, Lakmé Limited sold its brands to HUL and divested its 50% stake in the joint venture to the company. The Tatas sold Lakmé to Hindustan Unilever for ₹200 crore. Lakme, established in 1952 by JRD Tata at Prime Minister Nehru's request to reduce foreign exchange spent on imported cosmetics, had become India's premier cosmetics brand. For HUL, this acquisition provided instant leadership in a high-margin, aspirational category that perfectly complemented its personal care portfolio.

The Pond's India merger in 1998 represented internal consolidation rather than external acquisition but was equally strategic. The internal restructuring culminated in the merger of Pond's (India) Limited (PIL) with HUL in 1998. The two companies had significant overlaps in Personal Products, Speciality Chemicals and Exports businesses, besides a common distribution system since 1993 for Personal Products. The two also had a common management pool and a technology base. The amalgamation was done to ensure for the Group, benefits from scale economies both in domestic and export markets and enable it to fund investments required for aggressively building new categories. The Modern Foods acquisition in January 2000 marked a historic milestone—not just for HUL but for India's economic liberalization journey. In January 2000, in a historic step, the government decided to award 74 per cent equity in Modern Foods to HUL, thereby beginning the divestment of government equity in public sector undertakings (PSU) to private sector partners. HUL was the sole bidder for Modern Foods. It paid Rs 10.5 million, as per the valuation exercise undertaken by its valuer ICICI, for 74% of the shares. Later the government exercised its put option to sell the remaining 26% to HUL for Rs 4.4 million in November 2002. Modern Foods had over 40% of the bread market in India.

The Modern Foods acquisition, however, would prove to be one of HUL's rare missteps, illustrating that even the most successful acquirers can stumble. Senior HUL officials said the acquisition was a complete misfit with the HUL culture and systems. The bakery business, with its short shelf life, complex distribution requirements, and unionized workforce from its PSU days, proved difficult to integrate. After struggling for years to make the business viable, HUL eventually divested Modern Foods to Nimman Foods Private Limited in 2015, acknowledging that bread and bakery didn't fit its core competencies.

The acquisition strategy wasn't limited to large deals. HUL systematically acquired regional brands that gave it entry into specific geographies or consumer segments. The Kothari General Foods acquisition in 1992 strengthened HUL's position in instant coffee. The Kwality and Milkfood ice cream brands, acquired in 1994-95, expanded HUL's frozen desserts portfolio. Each acquisition was carefully evaluated not just for its standalone value but for how it would fit into HUL's overall portfolio and distribution system.

The integration playbook that HUL developed during this period became a competitive advantage in itself. The company had a systematic approach: first, stabilize operations and reassure employees; second, integrate the acquired brands into HUL's distribution system; third, upgrade manufacturing to HUL standards; fourth, reposition brands to minimize overlap with existing portfolio; and finally, extract cost synergies through procurement, manufacturing, and overhead optimization. This disciplined approach meant that most acquisitions became accretive to earnings within two to three years.

The financial architecture of these acquisitions was equally sophisticated. HUL typically used a combination of cash and stock, structuring deals to be immediately accretive to earnings per share. The company maintained a conservative balance sheet, ensuring it had the financial flexibility to move quickly when opportunities arose. This financial discipline meant HUL could outbid competitors who might need lengthy approval processes or external financing.

The MRTPC (Monopolies and Restrictive Trade Practices Commission) challenges that followed many of these acquisitions revealed the regulatory complexity of consolidation in India. The TOMCO merger, in particular, faced legal challenges from employee unions and consumer groups who argued it would create a monopoly. HUL successfully defended these acquisitions by arguing that they enhanced efficiency, improved product quality, and ultimately benefited consumers through better products at competitive prices.

The human dimension of these acquisitions was handled with particular care. Unlike many acquirers who immediately downsized acquired companies, HUL typically retained most employees, investing in training to bring them up to HUL standards. This approach not only avoided labor unrest but also preserved valuable institutional knowledge about local markets and consumer preferences. Many executives from acquired companies rose to senior positions within HUL, bringing diverse perspectives to the organization.

The innovation that followed these acquisitions demonstrated the value of consolidation beyond mere market share gains. By combining R&D capabilities, manufacturing expertise, and market knowledge from different companies, HUL could innovate faster and more effectively. Products were reformulated using better technology, packaging was upgraded, and new variants were launched to address unmet consumer needs. The acquired brands often performed better under HUL than they had as independent entities.

The category expansion achieved through acquisitions transformed HUL from primarily a soaps and detergents company into a diversified FMCG conglomerate. By 2010, HUL had significant positions in home care, personal care, foods, beverages, and ice cream. This diversification provided resilience—when one category faced challenges, others could compensate. It also allowed HUL to leverage its distribution system more effectively, spreading fixed costs across a broader product portfolio.

The competitive response to HUL's acquisition spree was mixed. Some competitors, like Godrej and Dabur, also pursued acquisitions to defend their positions. Others, like Nirma, focused on organic growth and cost leadership. International competitors like P&G and Colgate largely avoided major acquisitions in India, preferring to build their businesses organically. This varied response meant that HUL's acquisition strategy effectively changed the structure of the Indian FMCG industry, creating higher barriers to entry and favoring scaled players.

The regulatory environment evolved in response to this consolidation wave. The Competition Commission of India, established in 2003 to replace the MRTPC, brought more sophisticated analysis to merger reviews. Future acquisitions would face greater scrutiny, particularly in categories where HUL already had dominant positions. This regulatory evolution meant that HUL's window for aggressive consolidation was closing, making the acquisitions of the 1993-2010 period even more strategically valuable.

The brand portfolio management capabilities developed during this acquisition phase became a core competency. HUL learned to manage dozens of brands across multiple categories, each with its own positioning, target consumer, and growth strategy. The company developed sophisticated frameworks for resource allocation, ensuring that investment went to brands with the highest growth potential while maintaining cash cows that generated steady profits.

By 2010, the acquisition-led growth phase was largely complete. HUL had consolidated its position as India's largest FMCG company, with leadership positions across multiple categories. The company had a portfolio of over 35 brands, many of which were household names across India. The distribution network had been optimized to handle this diverse portfolio, reaching millions of outlets across urban and rural India.

The lessons from this acquisition spree were profound. HUL had demonstrated that in a fragmented market like India, consolidation could create significant value through scale economies, distribution synergies, and portfolio optimization. The company had also shown that successful acquisition wasn't just about financial engineering—it required operational excellence, cultural sensitivity, and long-term vision.

As the 2010s began, HUL would need to find new sources of growth. The easy wins from acquisition were largely exhausted, competition was intensifying, and consumer preferences were evolving rapidly. The company would need to shift from buying growth to creating it organically, from consolidating existing markets to creating new ones. The capabilities built during the acquisition era—brand management, distribution excellence, innovation, and operational efficiency—would be crucial for this next phase of growth.

VI. Project Shakti & Rural Revolution (2001–Present)

In 2001, as India's urban markets showed signs of saturation and multinational competitors intensified their assault on city consumers, HUL made a counterintuitive strategic pivot that would redefine not just its own growth trajectory but the very conception of rural marketing in emerging economies. Project Shakti was started in 2001. It is a rural initiative that targets small villages populated by less than 5000 individuals. It is a unique win-win initiative that catalyses rural affluence even as it benefits business.

The genesis of Project Shakti lay in a fundamental challenge: how to profitably serve the 600,000 villages that housed 70% of India's population but contributed less than 30% of FMCG consumption. Traditional distribution models broke down in rural India—low population density meant smaller order sizes, poor infrastructure increased transportation costs, and limited purchasing power reduced margins. Most companies had written off rural markets as unviable. HUL saw an opportunity hidden within these constraints. The model was elegantly simple yet revolutionary in its execution. Project Shakti has nearly 120,000 thousand women micro-entrepreneurs across 18 states. The women entrepreneurs, called Shakti Ammas, are trained on basic principles of distribution management. These women are provided with credit facilities, so that they can purchase HUL products at wholesale prices and sell them at retail prices. What made this model transformative wasn't just its scale but its fundamental reimagining of distribution as a tool for social empowerment.

The Shakti Amma—literally "empowered mother"—became the face of HUL in villages where traditional retail infrastructure didn't exist. These women, typically from below-poverty-line families, were selected through partnerships with self-help groups (SHGs) and microfinance institutions. The selection criteria were carefully calibrated: women needed to be literate enough to maintain basic accounts, have the support of their families, and possess the social standing to interact with other villagers. This wasn't charity disguised as business—it was a rigorous commercial operation with social benefits.

The training provided to Shakti Ammas went far beyond product knowledge. HUL's team of Rural Sales Promoters (RSPs) coach these Shakti entrepreneurs by familiarising them with the product range in order to manage their businesses better. They also train them on the basics of sales and troubleshooting and help them enhance their soft skills in areas such as negotiation and communication. This comprehensive training transformed housewives into entrepreneurs, creating a new class of businesswomen in conservative rural societies where women's economic participation had been minimal.

The economics of the Shakti model revealed sophisticated understanding of rural market dynamics. By enabling the average Shakti entrepreneur to earn a sustainable income of about $10 – $14 per month, which is double their average household income, the Project has helped improve the overall standard of living in their families. This income, while modest by urban standards, was transformative in rural contexts where cash income opportunities for women were virtually non-existent. The model created a virtuous cycle—as Shakti Ammas earned income, their purchasing power increased, creating demand for the very products they sold.

The product portfolio for Project Shakti was carefully curated to match rural needs and purchasing patterns. Rural consumers are price sensitive. Sachets and small packs of premium products. Price doesn't exceed Rs.5 per sachet. This sachet revolution—selling shampoo in single-use packets, detergent in small pouches, tea in affordable quantities—wasn't just about affordability. It was about reducing the risk of trying new products for cash-constrained consumers and enabling daily wage earners to purchase quality products with their daily earnings.

The distribution innovation of Project Shakti extended beyond simple door-to-door selling. Shakti Ammas became information nodes in their villages, educating consumers about hygiene, nutrition, and health. The company also initiated a Shakti Vani project to supplement Project Shakti; Under this programme, trained communicators visited schools and village gatherings to impart awareness on sanitation, good hygiene practices and women empowerment. This educational component transformed product selling into a public health intervention, creating demand while improving health outcomes.

The technological evolution of Project Shakti demonstrated HUL's ability to adapt to India's digital revolution. The iShakti programme provides information and services to meet rural needs in medical health and hygiene, agriculture, animal husbandry, education, vocational training and employment and women's empowerment. As smartphones penetrated rural India, HUL equipped Shakti Ammas with mobile apps for ordering, inventory management, and accessing product information. This digital layer improved efficiency while maintaining the human touch that made the model successful.

The pandemic period revealed the resilience and importance of the Shakti network. During the pandemic, the Shakti network played the role of being a crucial part of its distribution channel. Thanks to the efforts put in by these women entrepreneurs, HUL was able to dramatically extend the physical reach of its products to rural households. In several instances, the Shakti entrepreneurs travelled to distributors to pick up stocks, which they subsequently distributed to the households in their vicinity. When traditional supply chains broke down during lockdowns, Shakti Ammas became lifelines for their communities, ensuring availability of essential products.

The social impact of Project Shakti extended far beyond economic empowerment. As most of the Ammas say Project Shakti has provided each of them a new life full of dignity due to financial independence. Women who had never left their villages became confident entrepreneurs, their children stayed in school longer funded by their mothers' earnings, and gender dynamics in families shifted as women became economic contributors. The program challenged deep-seated patriarchal norms, using commerce as a vehicle for social change.

The competitive response to Project Shakti was telling. While competitors attempted to replicate the model, few succeeded at HUL's scale. The success of Shakti wasn't just about the distribution model—it was about the patient investment in training, the partnerships with NGOs and SHGs, the trust built over years, and the integration with HUL's broader rural strategy. Project Shakti has now been replicated in different countries like Pakistan, Sri Lanka, and Vietnam Bangladesh etc. owing to the enormous success it achieved in India.

The criticism of Project Shakti, while limited, raised important questions about corporate involvement in development. Some argued that HUL was exploiting cheap labor, that the incomes generated were insufficient, or that the model created dependency rather than true empowerment. HUL's response was to continuously evolve the program—increasing margins for Shakti Ammas, providing additional training, and creating pathways for the most successful entrepreneurs to become sub-distributors.

The strategic value of Project Shakti for HUL went beyond immediate sales. The program created a moat that competitors found nearly impossible to cross. While anyone could copy HUL's products or match its prices, replicating a network of 160,000 trained, motivated, and loyal rural entrepreneurs required decades of patient investment. The relationships, trust, and social capital embedded in the Shakti network represented an intangible asset more valuable than any physical infrastructure.

The learning from Project Shakti influenced HUL's broader rural strategy. The company recognized that rural India wasn't a monolithic market but a collection of diverse micro-markets, each with unique characteristics. The "Winning in Many Indias" strategy that emerged in the 2010s was directly influenced by insights gathered through the Shakti network. Shakti Ammas became HUL's eyes and ears in rural India, providing real-time market intelligence that no amount of formal market research could replicate.

The financial impact of rural expansion through initiatives like Project Shakti was substantial. Rural markets, which contributed less than 30% of HUL's revenues in 2001, grew to nearly 40% by the 2020s. This growth came with healthy margins, as rural consumers showed strong brand loyalty once trust was established. The rural expansion also provided a hedge against urban market saturation and economic volatility—rural consumption remained resilient even during economic downturns.

The sustainability dimension of Project Shakti aligned with evolving corporate responsibility expectations. What began as a business initiative became a showcase for sustainable and inclusive business models. The program demonstrated that profitability and social impact weren't mutually exclusive—that businesses could "do well by doing good." This narrative became increasingly important as consumers, investors, and regulators demanded greater corporate accountability for social and environmental impact.

The organizational capabilities developed through Project Shakti proved valuable beyond rural distribution. The ability to manage a distributed network of entrepreneurs, to train and motivate a diverse workforce, to adapt products and communication for varied contexts—these capabilities enhanced HUL's overall organizational agility. Managers who cut their teeth on Project Shakti brought valuable perspectives to other parts of the business.

The policy implications of Project Shakti's success influenced government thinking about rural development. The model demonstrated that private sector involvement in rural development could be effective when aligned with business objectives. Policymakers began to see corporations not just as entities to be taxed for development funding but as potential partners in development delivery. This shift in perspective opened doors for HUL and other companies to engage more deeply with government programs.

As Project Shakti matured, HUL faced new challenges. The most successful Shakti Ammas were graduating to become sub-distributors, requiring new entrepreneurs to be recruited and trained. Rural consumers were becoming more sophisticated, demanding greater product variety and better service. Digital commerce was beginning to penetrate rural areas, potentially disrupting the Shakti model. HUL's response was continuous innovation—enhancing training, expanding product portfolios, and integrating digital tools while maintaining the human relationships that made Shakti successful.

The global recognition of Project Shakti validated HUL's approach. Business schools wrote case studies, development organizations cited it as a model for inclusive business, and Unilever replicated elements of the model in other emerging markets. The program won numerous awards for innovation, sustainability, and social impact. This recognition enhanced HUL's reputation, attracting talent and building relationships with stakeholders who valued purpose-driven business.

Looking forward, Project Shakti represents both HUL's greatest achievement in rural marketing and a platform for continued innovation. The network of empowered women entrepreneurs, the deep rural presence, the trust and relationships built over two decades—these assets position HUL uniquely for the next phase of rural growth. As rural India digitalizes, as consumption patterns evolve, as new competitors emerge, the Shakti network provides HUL with the flexibility and reach to adapt and thrive.

The ultimate lesson of Project Shakti is that sustainable business success in emerging markets requires more than just adapting products or prices for poor consumers. It requires reimagining business models to create value for all stakeholders, investing patiently in capabilities and relationships, and recognizing that social impact and business success can be mutually reinforcing. For HUL, Project Shakti wasn't just a rural distribution initiative—it was a transformation of how multinational corporations could operate in developing countries, creating shared value that benefits business and society alike.

VII. The Innovation Engine: R&D and Product Development

In 2004, HUL launched a product that would exemplify its approach to innovation for emerging markets—not adaptation of global products, but ground-up innovation addressing uniquely Indian challenges. Pureit was first launched in Chennai in 2004 with the introduction of Pureit Classic, a first-of-its-kind gravity-based water purifier to provide accessible and safe drinking water to millions. The genesis of Pureit revealed how HUL's R&D had evolved from a support function to a strategic capability driving growth.

The water purifier market in India presented a classic emerging market paradox. The need was enormous—hundreds of millions lacked access to safe drinking water, with waterborne diseases causing thousands of deaths annually. Yet existing solutions were inadequate. Boiling water was time-consuming and expensive. Electric purifiers like Aquaguard were costly, required continuous electricity, and needed running water pressure—luxuries unavailable to most Indians. The market was ripe for disruption, but the technical challenges were formidable.

The development of Pureit took over four years and represented one of HUL's most ambitious R&D projects. The filter was test-marketed in Chennai in 2004, and gradually sold across India over the next four years. The innovation wasn't incremental—it required breakthrough thinking across multiple dimensions. The purification technology needed to work without electricity or running water. It had to remove not just visible impurities but also bacteria, viruses, and parasites. Most challenging, it had to be affordable for lower-middle-class families while being profitable for HUL.

The technical solution was elegant in its simplicity. Pureit puts water through four stages of filtration, in which sediments, dirt, parasites and residues are removed. The device used a combination of physical filtration and chemical treatment to achieve purification standards that met international benchmarks. The "Germkill Kit" indicator was a masterstroke—it automatically shut off water flow after treating a specified volume, ensuring users never drank inadequately purified water. This fail-safe mechanism addressed the critical trust deficit in water purification. The pricing strategy for Pureit was revolutionary for the water purifier category. Unilever priced the entry-level product, Pureit Classic, at Rs 2,350 - less than half the entry level prices of other purifiers. This wasn't predatory pricing but a fundamental reimagining of the cost structure. By eliminating electricity requirements, simplifying manufacturing, and leveraging HUL's scale in procurement and distribution, Pureit could be profitable at price points competitors couldn't match.

The marketing of Pureit demonstrated sophisticated understanding of consumer psychology around health products. "We have offered Rs 1 crore in prize money to anyone who can prove that some other water purifier brand can purify water better than Pureit, and there are still no takers for that money," says Bokey proudly. This bold challenge addressed skepticism head-on while building confidence in the product's efficacy. The advertising showing dirty water being purified in real-time provided visual proof that resonated with consumers accustomed to boiling water as the only trusted purification method.

The global expansion of Pureit validated HUL's reverse innovation capabilities. Today, it also sells in Bangladesh, Brazil, Indonesia, Mexico, Nigeria and Sri Lanka. Products developed for Indian conditions—dealing with inconsistent water quality, unreliable electricity, and price-sensitive consumers—proved relevant across emerging markets. This reversed the traditional flow of innovation from developed to developing markets, positioning HUL as a source of global innovation within Unilever.

The "Winning in Many Indias" (WIMI) strategy launched in 2014 represented a fundamental reconceptualization of the Indian market. In 2014 he launched an initiative called Winning In Many Indias (Wimi), wherein he divided the country into 14 clusters and devolved a lot of authority to each of the clusters. This wasn't just geographic segmentation—it was recognition that India contained multiple distinct markets, each with unique consumer preferences, competitive dynamics, and growth trajectories.

The WIMI framework classified India into consumer clusters based on multiple parameters: income levels, urbanization, cultural preferences, climate, and competitive intensity. These are supported by 16 country category business teams that function as micro-organisations to reduce the time taken to land innovations. This organizational innovation created entrepreneurial units within HUL's large structure, combining the agility of startups with the resources of a multinational corporation.

The product innovations emerging from WIMI revealed the power of localized innovation. For instance, a variant of Rin detergent that consumed less water was launched for water deficient states in the west and south. Karnataka got its own variant of Bru instant coffee, Bru Kannadiga. These weren't superficial customizations but products fundamentally reimagined for local conditions. The success of these variants validated the hypothesis that Indian consumers valued products that addressed their specific needs over generic national offerings.

The speed of innovation under WIMI was transformative. One example of the model's success is how it enabled Lifebuoy to ramp up capacity 30 times and launch 17 hand sanitiser variants in just 100 days during the 2020 pandemic. This rapid response would have been impossible under HUL's previous centralized structure. The pandemic period became a proof point for the WIMI model's effectiveness in crisis response and opportunity capture.

The digital transformation of HUL's innovation process reflected broader technological shifts. The company started launching product variants to suit that particular cluster. Digital tools enabled rapid prototyping, consumer testing through online panels, and real-time market feedback. Social media listening provided insights into emerging consumer needs. E-commerce data revealed purchasing patterns invisible in traditional retail. This digital layer accelerated innovation cycles from years to months.

The sustainability dimension of innovation became increasingly central to HUL's R&D agenda. Products were reformulated to reduce water usage, packaging was redesigned to minimize plastic, and manufacturing processes were optimized for energy efficiency. These sustainability innovations weren't just about corporate responsibility—they addressed real consumer concerns about environmental impact while often reducing costs.

The talent strategy supporting innovation was equally important. HUL established partnerships with Indian Institutes of Technology, recruited specialized talent in areas like data science and digital marketing, and created innovation labs where employees could experiment with new ideas. The company's innovation challenges, hackathons, and startup collaborations brought external perspectives into the organization.

The intellectual property strategy evolved to protect innovations while enabling speed. HUL filed patents for breakthrough innovations while relying on trade secrets and rapid market entry for incremental improvements. The company's legal team worked closely with R&D to identify protectable innovations early in the development process. This IP strategy created barriers to imitation while maintaining innovation velocity.

The collaboration with Unilever's global R&D network provided access to cutting-edge science while maintaining local relevance. HUL could leverage Unilever's basic research in areas like surfactant chemistry or enzyme technology while applying these advances to Indian-specific challenges. This two-way flow—Indian innovations going global and global technologies adapted for India—maximized R&D productivity.

The measurement and metrics around innovation became increasingly sophisticated. HUL tracked not just the number of new products launched but their speed to market, success rates, and contribution to growth. Innovation metrics were cascaded to individual performance objectives, ensuring organizational alignment. The company's innovation dashboard provided real-time visibility into the innovation pipeline, enabling better resource allocation.

The partnerships and collaborations expanded HUL's innovation capabilities beyond internal R&D. Collaborations with startups brought disruptive technologies, partnerships with universities provided access to cutting-edge research, and alliances with suppliers enabled material innovations. HUL's innovation ecosystem extended far beyond its own laboratories, creating a network effect that accelerated innovation.

The cultural transformation required to sustain innovation was profound. HUL had to evolve from a culture of perfection—where products were extensively tested before launch—to one of experimentation where rapid testing and learning were valued. Failure was reframed from something to be avoided to a necessary part of the innovation process. This cultural shift, perhaps more than any technical capability, enabled HUL's innovation acceleration.

Looking forward, HUL's innovation agenda faces new challenges and opportunities. Artificial intelligence and machine learning are opening new possibilities for product development and consumer understanding. The rise of personalized products demands mass customization capabilities. Sustainability requirements are becoming more stringent. Digital-native competitors are setting new standards for innovation speed.

The lessons from HUL's innovation journey are profound. Success in emerging markets requires more than adapting global products—it demands ground-up innovation addressing local challenges. Speed matters as much as quality in rapidly evolving markets. Organizational structures must balance scale with agility. Most importantly, innovation must be embedded in culture, not just confined to R&D departments.

For HUL, innovation has evolved from a functional capability to a strategic imperative. The company that once adapted British soaps for Indian consumers now creates products that define categories globally. This transformation—from innovation follower to innovation leader—represents perhaps the most fundamental change in HUL's long history.

VIII. Modern Era Challenges & Opportunities (2010–Today)

The 2010s dawned with HUL in an enviable position—market leadership across categories, unmatched distribution, powerful brands, and strong financial performance. Yet the decade ahead would prove to be among the most challenging in the company's history, testing every assumption about how to build and sustain competitive advantage in rapidly evolving markets. The convergence of digital disruption, new competition, changing consumer preferences, and social accountability would force HUL to reimagine itself while maintaining its core strengths. The GSK Consumer Healthcare merger completed in April 2020 represented HUL's boldest strategic move of the decade. Hindustan Unilever Limited (HUL), India's largest fast-moving consumer goods company, today announced that it has successfully completed the merger of GlaxoSmithKline Consumer Healthcare Limited (GSKCH) with HUL. The merger of GSK CH India with HUL will be on a basis of an exchange ratio of 4.39 HUL shares for each GSK CH India share, implying a total equity value of Rs 31,700 crore for 100 per cent of GSK CH India. The Board of Directors of HUL today approved HUL acquiring the Horlicks Brand for India from GSK for a consideration of Euro 375.6 mln (INR 3045 Cr).

This wasn't just an acquisition—it was a transformative entry into the health and nutrition space. Horlicks commands a volume market share of around 50% in India. The acquisition brought not just market leadership but also 3,500 employees with deep expertise in nutrition, strong relationships with healthcare professionals, and established presence in pharmacy channels—capabilities HUL had historically lacked.

The strategic rationale for the GSK merger went beyond immediate market share gains. The nutrition and health drinks category remains under-penetrated in India and HUL is well positioned to further develop the market given the extent of its reach and capabilities. With rising health consciousness, aging populations, and increasing lifestyle diseases, the nutrition category represented a secular growth opportunity. HUL's distribution reach could expand category penetration while GSK's product expertise ensured credibility in health-related categories.

The integration challenges highlighted broader issues facing large FMCG companies in the post-merger landscape. Managing complexity across diverse categories, maintaining focus while pursuing scale, and balancing short-term performance with long-term investments became increasingly challenging. The GSK merger, while strategically sound, added another layer of complexity to an already diverse portfolio.

The emergence of Patanjali from 2011 onwards represented perhaps the most significant competitive threat HUL had faced since liberalization. Between 2011-12 and 2015-16, PAL has grown by more than ten times - its revenue grew by 1004 percent in four years to Rs 5,000 crore in FY2016 from Rs 453 crore in FY2012. This wasn't just another competitor—it was a fundamental challenge to the multinational model that HUL represented. Patanjali's positioning around swadeshi (indigenous) values, natural ingredients, and affordable pricing resonated with a growing segment of consumers questioning Western brands.

HUL's response to Patanjali was swift but complex. Months after Baba Ramdev announced in April this year that Patanjali has clocked Rs 5,000 crore in sales during 2015-16, HUL decided to revive Lever Ayush–an ayurvedic brand which was left in the corner some years ago by the company. The relaunch of Lever Ayush represented more than product development—it was an acknowledgment that consumer preferences were shifting toward natural and traditional products. Hindustan Unilever (HUL), the local arm of the Anglo-Dutch multinational, plans to launch 20 new natural and herbal products under its Ayush brand in a bid to win back consumers who flocked to Patanjali's ayurvedic soaps, skin creams, and shampoos.

The competitive dynamics with Patanjali revealed structural challenges in HUL's business model. While HUL had superior distribution, technology, and financial resources, Patanjali had authenticity, lower cost structures, and emotional connection with consumers seeking alternatives to multinational brands. The popularity of PAL brands was giving a tough time to companies such as HUL, P&G, Colgate–Palmolive, Nestle, ITC, GCPL and Dabur India Limited. Colgate sales growth rate in the toothpaste category had decreased from 11 per cent in December 2013 to 1 per cent in December 2015. The Dant Kanti market share grew from 0 per cent to around 5 per cent in the same period (Malviya, 2017).

The Fair & Lovely controversy and subsequent rebranding to Glow & Lovely in 2020 crystallized broader questions about corporate responsibility and brand purpose. In a revolutionary decision taken on June 25, 2020, Hindustan Unilever Limited (HUL) announced that it would rename its age-old product Fair and Lovely to Glow & Lovely. The decision came amid global protests against racial discrimination and growing criticism of products promoting skin lightening. Unilever announced today the next step in the evolution of its skin care portfolio to a more inclusive vision of beauty – which includes the removal of the words 'fair/fairness', 'white/whitening', and 'light/lightening' from its products' packs and communication. As part of this decision, the Fair & Lovely brand name will be changed in the next few months. We recognise that the use of the words 'fair', 'white' and 'light' suggest a singular ideal of beauty that we don't think is right, and we want to address this.

The rebranding, while necessary from a social responsibility perspective, highlighted the challenges of managing legacy brands in evolving social contexts. Critics responded to the rebranding by criticizing the continuing sale of the product and expressing concerns that changing the name of the product does not address how colorism is still prevalent in the community. The controversy damaged brand equity built over decades and raised questions about whether multinational companies could authentically address local social issues while maintaining global standards.

The digital disruption of the 2010s fundamentally altered competitive dynamics. E-commerce platforms like Amazon and Flipkart changed how consumers discovered and purchased products. Direct-to-consumer (D2C) brands could now reach consumers without HUL's distribution advantage. Social media influencers could build brands faster than traditional advertising. Digital-native brands like Mamaearth, Nykaa's private labels, and dozens of others emerged, targeting specific consumer segments with focused propositions.

HUL's digital response involved multiple initiatives but faced structural challenges. The company launched its own D2C platform, invested in digital marketing capabilities, and partnered with e-commerce platforms. However, the fundamental challenge was that digital disruption eroded the competitive advantages—distribution reach, advertising scale, retail relationships—that had sustained HUL for decades. In the digital world, a startup with a good product and smart digital marketing could compete with HUL on relatively equal terms.

The quick commerce revolution, accelerated by the pandemic, presented both opportunities and challenges. Platforms like Blinkit, Zepto, and Swiggy Instamart could deliver products in 10-15 minutes, changing consumer expectations about convenience. While this opened new growth avenues, it also meant that HUL had to manage another complex channel with different economics, competitive dynamics, and consumer behaviors. The traditional trade, modern trade, e-commerce, and now quick commerce—each required different strategies, capabilities, and investments.

The financial milestone of crossing ₹50,000 crore in revenue in FY2022 was significant but came with caveats. In the last financial year, HUL became a Rs 50,000 crore turnover company and also the first pure FMCG firm to achieve this milestone. While topline growth was impressive, it was increasingly driven by price increases rather than volume growth. During the quarter, our turnover grew 10 per cent with flat Underlying Volume Growth. The challenge of driving profitable volume growth in a competitive, fragmented market with changing consumer preferences became increasingly acute.

The premium versus mass market tension intensified during this period. Urban markets demanded premium, differentiated products with superior claims and experiences. Rural markets, while growing, remained price-sensitive and preferred established, trusted brands. HUL needed to simultaneously premiumize for urban markets while maintaining affordability for mass markets—a delicate balance that required different innovation, marketing, and distribution strategies.

The sustainability agenda, from being a peripheral concern, moved to the center of corporate strategy. Consumers, particularly younger ones, increasingly factored environmental and social considerations into purchase decisions. Investors demanded ESG (Environmental, Social, Governance) compliance. Regulators imposed stricter environmental standards. HUL responded with ambitious sustainability targets—reducing plastic usage, achieving carbon neutrality, improving water efficiency. However, implementing these changes while maintaining cost competitiveness proved challenging.

The decision to divest Pureit in 2024 symbolized HUL's strategic recalibration. Hindustan Unilever Limited (HUL) today announced that it has signed an agreement for the sale of its Pureit business in India. The business is being sold to A. O. Smith, a leading global water technology company. Rohit Jawa, CEO & Managing Director of HUL, said: "This move is in line with our strategic intent to focus sharply on our core categories." Despite being an innovative product addressing a critical need, In the financial year 2024 (FY24), the turnover of HUL's water purification business stood at Rs 293 crore, which is less than one per cent of the FMCG giant's total turnover. The divestment acknowledged that success in FMCG required focus, and that not all categories fit HUL's core competencies.

The organizational challenges of managing complexity became increasingly apparent. HUL operated across multiple categories, each with different competitive dynamics, consumer behaviors, and success factors. The company served diverse consumer segments from premium urban to rural bottom-of-pyramid. It managed hundreds of SKUs across dozens of brands. This complexity strained management attention, complicated resource allocation, and sometimes slowed decision-making in a market that increasingly rewarded agility.