Hero MotoCorp: The World's Largest Two-Wheeler Manufacturer

I. Introduction & Episode Roadmap

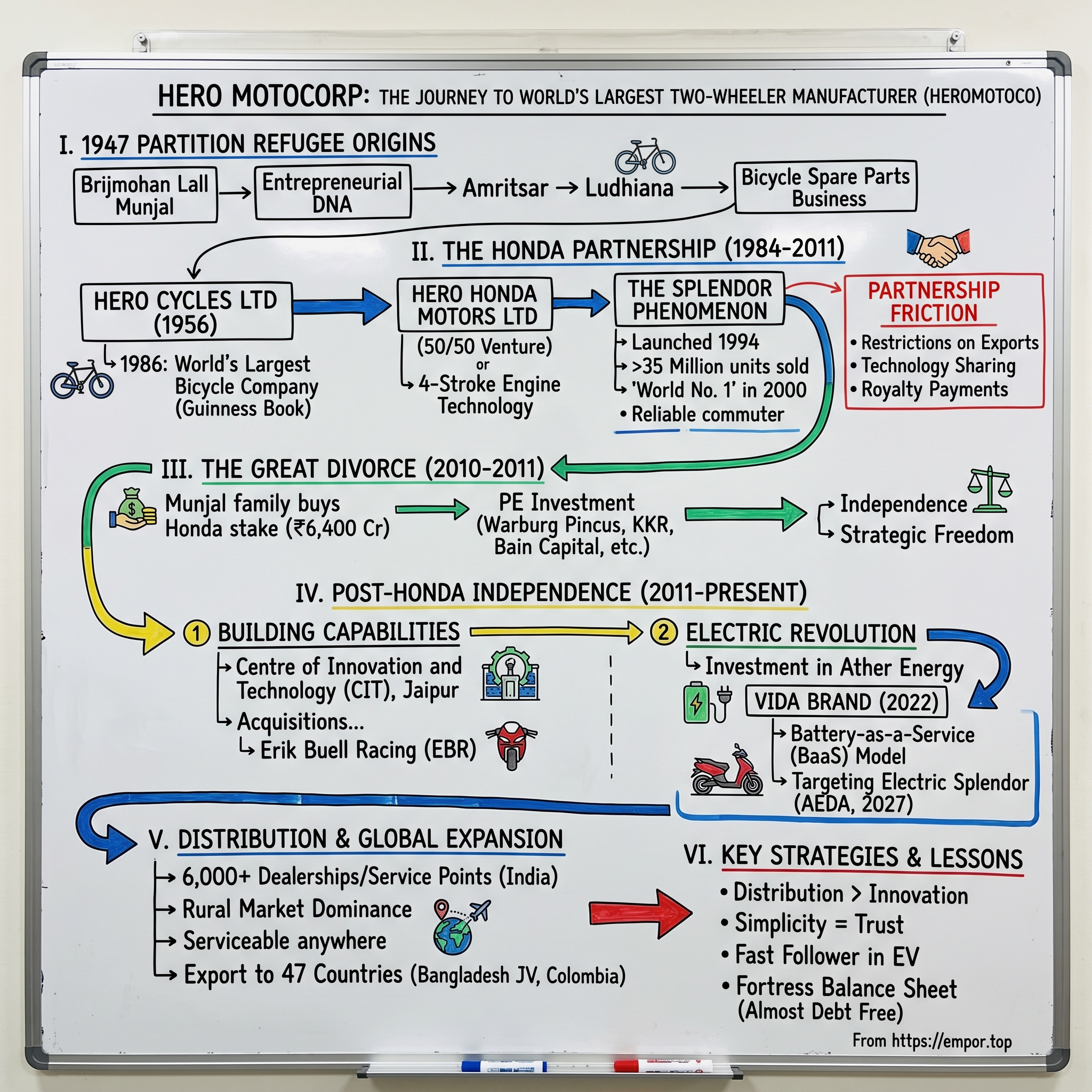

Picture this: It's 1947, and a young man named Brijmohan Lall Munjal crosses the newly drawn border from Pakistan into India with nothing but the clothes on his back and an unshakable determination. Fast forward 77 years, and the company he founded has sold over 100 million motorcycles—more than Honda, Yamaha, or any other manufacturer in history. This is the story of Hero MotoCorp, a ₹40,440 crore revenue giant that commands 30% of India's two-wheeler market and stands as the world's largest motorcycle manufacturer by volume.

The question that drives this entire narrative is deceptively simple: How did a refugee family selling bicycle parts in post-partition Punjab build a company that would eventually tell Honda—the legendary Japanese engineering powerhouse—"thanks, but we don't need you anymore"? And then proceed to thrive without them? Today, Hero MotoCorp stands at a market capitalization of ₹92,003 crore with revenue of ₹40,440 crore and profit of ₹5,049 crore. These numbers tell only part of the story. This is fundamentally a tale of three acts: first, the audacious refugee entrepreneurs who built an industrial empire from nothing; second, the 27-year partnership with Honda that created India's mobility revolution; and third, the post-divorce era where Hero proved it could not just survive but thrive without its Japanese sensei.

What makes this story particularly compelling for investors and entrepreneurs alike is how it challenges conventional wisdom at every turn. When everyone said Indian companies couldn't compete with Japanese engineering, Hero Honda became the world's largest motorcycle maker. When analysts predicted Hero would collapse without Honda's technology in 2011, the company went on to maintain its market leadership for another decade. And now, as the world shifts to electric vehicles, Hero is once again betting against consensus by maintaining that combustion engines will dominate India for years to come while simultaneously building its EV capabilities.

This journey from partition refugee to global dominance offers profound lessons about family business evolution, the power of distribution in emerging markets, the delicate dance of joint ventures, and most importantly, how to build products that serve not the elite but the masses—the real India that travels 70 kilometers on a single liter of petrol.

Over the next several hours, we'll dissect how a company that sells what is essentially a commodity—affordable motorcycles—built such an enduring moat that it continues to sell more two-wheelers than any other company on Earth. We'll explore the Splendor phenomenon (a single model that has sold over 35 million units), the strategic chess game that led to the Honda divorce, and the current battle for India's electric future.

But more than anything, this is a story about understanding your customer so deeply that you become irreplaceable. Because when you're selling to a schoolteacher in Bihar who makes ₹15,000 a month, engineering excellence means something very different than it does in Tokyo or Munich. It means selling him dignity, freedom, and most importantly, reliability at a price he can afford.

Let's begin where all great business stories begin: with a family that had lost everything and had nothing left to lose.

II. The Munjal Family Origins & Hero Group Foundation

The year is 1944, and in the dusty town of Kamalia in undivided Punjab (now Pakistan), a 20-year-old Brijmohan Lall Munjal makes a decision that will alter the trajectory of Indian industry. Along with his three brothers—Dayanand, Satyanand, and Om Prakash—he leaves behind the only home he's ever known and crosses into what would soon become independent India. They arrive in Amritsar with nothing but entrepreneurial DNA and the kind of hunger that only comes from starting at zero. Think about the context for a moment. India in 1947 wasn't just gaining independence—it was being torn apart. Brijmohan Lall Munjal, born on July 1, 1923, in Kamalia, Punjab (now in Pakistan), came to Amritsar from Kamalia in 1944 at the age of 20 with his three brothers, Dayanand, Satyanand and Om Prakash. The partition that followed in 1947 created the largest human migration in history, with millions displaced and hundreds of thousands killed. For the Munjal brothers, it meant their fledgling bicycle spare parts business in Amritsar was suddenly on the wrong side of economic chaos.

The Munjal family relocated to Amritsar and later settled in Ludhiana, where they established a bicycle spare parts business in 1944. Despite the challenges of partition, the family persevered and ventured into bicycle component manufacturing in the early 1950s. But here's where the story takes its first remarkable turn—a moment of serendipity that would define Indian manufacturing for the next seven decades.

While my uncles Dayanand and Om Prakash were packing up to move to Ludhiana, one of their suppliers, a Muslim by the name of Kareem Deen, was preparing to shift to Pakistan. He manufactured bicycle saddles under a brand name he had created himself. Before he left, Karam Deen went to see his friend Om Prakash Munjal. Uncle Om Prakash asked Kareem Deen whether the Munjals could use that brand name for their business. He agreed. The gesture was typical of the way businesses were run at the time – on reputation, relationships and goodwill. And so, with nothing more than a casual nod, his brand passed to the Munjals. Yes, dear reader, it was "Hero".

This wasn't just a brand transfer—it was a passing of the torch between two communities being torn apart by politics but united by commerce and friendship. The name "Hero" would go on to become one of India's most valuable brands, but it began with a handshake between friends in the chaos of partition.

In 1954, he founded Hero Cycles Limited and began making bicycle parts, starting with forks and then adding handles and other parts. In 1956, the Punjab government issued a license to manufacture bicycles. His company got this license and from here his world changed. With the financial support of Rs 6 lakh from the government and its own capital, Hero Cycles forayed into bicycle manufacturing by getting the status of "Large Scale Unit".

The early days were far from glamorous. At the time, there were no manufacturing manuals laying out engineering designs and production processes. The Munjals had to wing it and create their own. My father and uncle Om Prakash would squat in the backyard with the artisans, drawing designs of cycle parts on sheets of paper and discussing ways of implementing them. Their very first experiment in 1954, was in bicycle forks (which they had been supplying to Atlas). But disaster lurked ahead, one that almost cost the Munjals their business. The welding in some of the bicycle forks cracked and the pipes broke off, with the result that the incensed dealers returned all orders and consignments.

This early crisis could have ended the Hero story before it began. Instead, it revealed the Munjal family's greatest asset: their ability to learn from failure and their deep respect for craftsmen. The Munjal brothers turned to the local community of mistris (technicians), artisans and craftsmen, the Ramgarhias, to untangle their knotty technical problems. My father, in particular, enjoyed an excellent understanding with these worthies. They are born artisans, and their skills are passed on from generation to generation. Their ability to make parts, and our commercial strength became a very beautiful combination.

By 1960, something extraordinary was happening in Ludhiana. The refugee entrepreneurs who had started with nothing were building what would become the world's largest bicycle empire. The numbers tell a story of relentless growth: The company had an annual production capacity of 7,500 cycles at that time. By 1975 it had become the largest bicycle company in India and in 1986, Hero Cycles was entered in the Guinness Book as the world's largest bicycle company.

Myth vs Reality Box: Myth: Hero was always destined for greatness given India's massive population. Reality: India in the 1950s-60s had dozens of bicycle manufacturers. Hero won through superior distribution, quality control at scale, and most importantly, understanding that their customer wasn't buying transportation—they were buying economic mobility.

The transformation from refugees to industrial titans happened at breakneck speed. Within 30 years of founding, Hero Cycles became the largest bicycle maker in the world. This wasn't just about making bicycles—it was about understanding what a bicycle meant to newly independent India. For a schoolteacher, it meant reaching three villages instead of one. For a farmer, it meant getting produce to market before it spoiled. For a young man, it meant the possibility of marrying outside his village.

With Brijmohan Lall Munjal at the helm, Hero Cycles experienced rapid growth and eventually became India's largest bicycle producer. Munjal's relentless pursuit of excellence and astute understanding of the Indian market laid the foundation for the company's future success.

But Brijmohan Lall Munjal wasn't content with being the bicycle king of India. By the early 1980s, he could see the future—and it had an engine. India's economy was evolving, incomes were rising (slowly but surely), and the aspiration for motorized transport was growing. The question was: how does a bicycle company make the leap to motorcycles?

The answer would come from an unlikely place: Japan. And it would create one of the most successful joint ventures in business history, before ending in one of the most high-profile corporate divorces of the 21st century.

So What for Investors: The Hero foundation story teaches us that in emerging markets, distribution and local knowledge often trump technology. The Munjals built an industrial empire not through innovation but through execution—understanding their market deeply and building trust networks that would prove more valuable than any patent. This foundation of frugal engineering and vast distribution would become their greatest asset when Honda came calling.

III. The Honda Partnership Era (1984–2011)

The meeting that would change Indian mobility forever almost didn't happen. It was 1983, and Honda Motor Company, the Japanese engineering giant, was looking for an entry point into India's protected market. They had already been rejected by Bajaj, India's scooter king, who didn't want to dilute his family's control. The Birlas, another industrial house, had also passed. Honda executives were running out of options when someone mentioned the bicycle makers from Ludhiana. When Honda's team first visited the Hero factory in Ludhiana, they were skeptical. Here was a bicycle manufacturer proposing to build motorcycles for the world's most complex market. But what Honda saw changed their minds: A joint venture between the Hero Group and Honda Motor Company was established in 1984 as the Hero Honda Motors Limited at Dharuhera, India. Munjal family and the Honda group both owned a 26% stake in the company.

The genius of this structure was that neither party had absolute control. It forced collaboration while maintaining independence—a delicate balance that would work brilliantly for 27 years before spectacularly falling apart.

CD 100 (launched as Hero Honda CD 100) is a standard lightweight motorcycle released by Hero Honda joint-venture as their first official bike in India. When the CD100 rolled off the production line on April 13, 1985, it wasn't just another motorcycle. It was a revolution wrapped in sheet metal. The tagline said it all: "Fill it - Shut it - Forget it"—a masterpiece of marketing that spoke directly to India's middle class obsession with fuel efficiency.

Think about the audacity of that promise. In a country where two-stroke engines dominated, requiring constant maintenance and delivering poor mileage, Hero Honda was promising a motorcycle you could essentially ignore. Hero Honda was the first company to introduce 4-stroke motorcycles in India. The four-stroke engine technology from Honda, combined with Hero's understanding of price points, created something magical: a motorcycle that delivered 80+ kilometers per liter.

During the 1980s, the company introduced low cost motorcycles in India. But "low cost" doesn't capture the sophistication of what was happening. Hero Honda wasn't just making cheap bikes—they were reengineering the entire concept of personal mobility for a price-conscious market. The CD100 was priced at ₹13,000 in 1985, when a government clerk made ₹2,000 a month. It was aspirational but achievable.

The numbers that followed were staggering. Hero Honda was established in 1984 with a 26% investment by Honda and 26% investment by the Partners with the purpose of developing the motorcycle market in India and started operation in 1985. Since then Hero Honda has achieved remarkable growth by combining Honda's technologies and products with Hero Honda's strengths in marketing and development of a sales network and has grown to be the industry leader in India.

By 1994, the partnership produced its masterstroke: the Splendor. In 1994, Hero launched the Splendor, which became the world's highest selling motorcycle. This wasn't hyperbole—the Splendor would go on to sell over 35 million units, making it the best-selling motorcycle in human history. Not the fastest, not the most beautiful, but the most sold. Because Hero Honda understood something fundamental: in India, reliability beats performance every single time.

2000: A remarkable year when Splendor was declared the 'World No. 1'- the largest-selling single two-wheeler model. The milestone was more than symbolic. It meant that a joint venture between a refugee-founded Indian company and a Japanese giant had created something neither could have achieved alone—global dominance from an emerging market.

The partnership's success attracted both admiration and tension. Honda was teaching Hero advanced manufacturing, quality control, and engine technology. Hero was teaching Honda how to sell to the bottom of the pyramid, how to build dealer networks in villages without roads, and how to finance motorcycles for people without credit histories.

But success bred conflict. As Hero Honda grew, so did the strategic divergence between the partners. Honda wanted to enter India's scooter market independently through its wholly-owned subsidiary, Honda Motorcycle and Scooter India (HMSI), established in 1999. Hero wanted to export motorcycles globally. The joint venture agreement restricted both.

The differences between the two partners had become apparent for a few years before the split over a variety of issues, ranging from Honda's reluctance to fully and freely share technology with Hero (despite a 10-year technology tie-up that expired in 2014) as well as Indian partner's uneasiness over high royalty payouts to the Japanese company.

By 2010, the marriage was effectively over. In 2009 Hero Honda sold approximately 4.32 million units of motorcycles in India, a 23% increase compared to 2008. They were at the peak of their success, yet both partners knew the relationship had run its course. Honda wanted full control of its Indian destiny. Hero wanted freedom to expand globally and reduce its technology dependence.

The divorce negotiations were as complex as any corporate separation in history. As per the arrangement, it was a two-leg deal: In the first part, the Munjal family, led by Brijmohan Lal Munjal group, formed an overseas-incorporated special purpose vehicle (SPV) to buy out Honda's entire stake, which was backed by bridge loans. This SPV was eventually opened for private equity participation, and those included Warburg Pincus, Kohlberg Kravis Roberts (KKR), TPG, Bain Capital and The Carlyle Group.

Myth vs Reality Box: Myth: The Hero-Honda split was acrimonious and damaged both companies. Reality: The separation was remarkably cordial. Honda received ₹6,400 crore for its 26% stake, and both companies signed technology and licensing agreements ensuring continuity. The real tension wasn't personal—it was strategic incompatibility.

The partnership's legacy is undeniable. In 27 years, Hero Honda: - Sold over 35 million motorcycles - Created India's most valuable two-wheeler brand - Established a distribution network of over 6,000 touchpoints - Generated thousands of crores in profits for both partners - Transformed how 100 million Indians commute

But perhaps the partnership's greatest achievement was proving that technology transfer between developed and emerging markets could create value for both sides. Honda got market access and volumes it could never have achieved alone. Hero got technology and credibility that transformed it from a bicycle maker to a global automotive player.

So What for Investors: The Hero-Honda story demonstrates that successful joint ventures require aligned incentives only up to a point. As partners grow and evolve, what brought them together can pull them apart. The key is recognizing when a partnership has served its purpose and executing separation while both parties are strong—not waiting until weakness forces the issue. Hero's ability to orchestrate a complex buyout using PE capital while maintaining operations shows sophisticated financial engineering rarely seen in family businesses.

IV. The Great Divorce: Split from Honda (2010–2011)

The boardroom at Hero's Gurgaon headquarters was tense on that December morning in 2010. Brijmohan Lall Munjal, now 87 years old but still sharp as ever, looked across the table at Honda's executives. After 26 years of partnership that created the world's largest motorcycle company, it was time to say goodbye. But this wasn't a defeat—it was a declaration of independence. The real reasons for the split were more complex than just business disagreements. The differences between the two partners had become apparent for a few years before the split over a variety of issues, ranging from Honda's reluctance to fully and freely share technology with Hero (despite a 10-year technology tie-up that expired in 2014) as well as Indian partner's uneasiness over high royalty payouts to the Japanese company. Another major irritant for Honda was the refusal of Munjal family to merge the Hero Honda's spare parts business with Honda's new fully owned subsidiary, HMSI.

But the core issue was strategic imprisonment. Under the joint venture agreement, Hero Honda Motors Ltd was not permitted to tap overseas markets, seek technology from any other company and even participate in large scale exports. Hero was essentially a bird in a golden cage—wealthy but unable to fly.

The joint venture was only intended for local production and consumption, as stated in the shareholder agreement signed in 1984. By 2010, this restriction had become intolerable. Hero wanted to export to Latin America, Africa, and West Asia—markets where Honda already had presence. Honda, meanwhile, was building its own Indian empire through HMSI, competing directly with its own joint venture.

The divorce mathematics were fascinating. The Munjal family, led by Brijmohan Lal Munjal group, formed an overseas-incorporated special purpose vehicle (SPV) to buy out Honda's entire stake, which was backed by bridge loans. This SPV was eventually opened for private equity participation, and those included Warburg Pincus, Kohlberg Kravis Roberts (KKR), TPG, Bain Capital and The Carlyle Group.

Think about what this meant: The Munjals convinced some of the world's smartest money to bet billions on a motorcycle company that was about to lose its technology partner. Bain Capital alone invested Rs 2500 Cr in June 2011 for 8.6% stake. They would eventually earn a "Cash on Cash" return of 2.0x, making about Rs 5,100 crore on their investment.

The financial engineering was brilliant. The Munjal family, the promoters of Hero, who held 26 per cent, the same as Honda, got to buy out the partner at a price significantly lower than the market price - rumours put the confidential price at half the market value. Honda received approximately ₹6,400 crore for its stake—substantial money, but arguably below true value given Hero Honda's dominance.

But here's what made the deal truly remarkable: Hero can launch products with Honda technology till June 2014 and can continue to sell them for as long as it wants. This wasn't just a divorce—it was a divorce where you got to keep living in the house for three more years and take the furniture when you left.

The name of the company was changed from Hero Honda Motors Limited to Hero MotoCorp Limited on 29 July 2011. The new brand identity and logo of Hero MotoCorp were developed by the British firm Wolff Olins. The logo was revealed on 9 August 2011 in London, to coincide with a cricket match between England and India.

The timing and location of the rebrand announcement were deliberate. London was convulsed by the worst rioting in Britain in living memory. But in a surreal scene only Bollywood could have conjured up, a different kind of pyrotechnics was exploding on the south bank of the Thames, in the massive Millennium Dome. The message was clear: Hero was now a global company, not just an Indian one.

With independence came freedom. Hero MotoCorp can now export to Latin America, Africa, and West Asia. Hero is free to use any vendor for its components instead of just Honda-approved vendors. The bird had finally left the cage.

But freedom also meant vulnerability. The market's reaction was brutal. After the split announcement, the stock of Hero Honda fell by 30%. Analysts were skeptical—could Hero survive without Honda's technology? The company was paying Honda Rs 2,479 crore as licence and exports fees—14% of Hero's 2010/11 revenues. This shows how dependent Hero was - and is - on Honda for technology.

The precedents weren't encouraging. Kinetic, promoted by the Pune-based Firodia family, collapsed after Honda walked out of their scooter making joint venture. LML, promoted by Kanpur-based Deepak Singhania, is making a feeble comeback with electric scooters after its Vespas disappeared in the aftermath of its breakup with Italy's Piaggio.

Myth vs Reality Box: Myth: Hero was helpless without Honda's technology. Reality: Hero had already begun building independent capabilities. They had five joint ventures with component suppliers—Munjal Showa, AG Industries, Sunbeam Auto, Rockman Industries, and Satyam Auto Components—that supplied majority of components. The technology gap was real but not insurmountable.

Pawan Kant Munjal, who was just 30 years old when his father Brij Mohan Lall forged the original partnership, now faced his defining moment as leader. Less than eight months earlier, Hero had announced the end of its immensely successful 27-year marriage with Honda. The question wasn't whether Hero could survive—it was whether it could thrive.

The answer would come not from boardrooms or financial engineering, but from something more fundamental: Hero's ability to build motorcycles that Indians wanted to buy, with or without Honda's help.

So What for Investors: The Hero-Honda divorce teaches us that the cost of independence is often worth paying. Hero gave up guaranteed technology access for strategic freedom—a trade-off that looked risky in 2011 but proved prescient as India's two-wheeler market evolved. The use of PE capital to fund the buyout while maintaining family control shows sophisticated capital structure management. Most importantly, the generous transition terms (technology usage until 2014) provided a bridge to independence rather than a cliff—a lesson in negotiating exits when you still have leverage, not when you're desperate.

V. Post-Honda Era: Proving the Doubters Wrong (2011–2020)

The whispers in the market were brutal. "Hero is finished." "They're just assemblers, not engineers." "Give it two years, they'll be begging Honda to come back." It was early 2012, and Hero MotoCorp's newly independent journey faced its first real test: could they actually build a motorcycle without Honda holding their hand? Pawan Kant Munjal knew he had to act fast. Hero was left floundering in the ocean shortly after the separation because they lacked engineering skills. They assembled the bike using the design, merely acting as "copiers." By recruiting the appropriate individuals and building the Centre of Innovation and Technology (CIT) in Jaipur, Hero intended to achieve key product development.

The answer came in the form of a massive bet on R&D. In 2013, the company decided to set up its own R&D centre. The sprawling 247-acre facility at the outskirts of Jaipur (in Rajasthan) cost Rs 850 crore. This wasn't just a research center—it was a declaration that Hero could innovate without Honda.

The centrepiece of Hero Motocorp's new Centre for Innovation and Technology (CIT) is an eleven story oval building which is lit up at night. But it is what is inside this building and the smaller buildings surrounding it which Munjal hopes will make Hero Motocorp stand apart. Fully equipped with a design studio, advanced testing rigs and laboratories for materials and prototypes, Munjal and his engineering chief Markus Braunsperger hope the 500 engineers at the CIT will be able to make a difference.

Markus Braunsperger, who joined the company from BMW in 2014 after a 25 year long stint, brought credibility Hero desperately needed. "My former company just celebrated its hundredth anniversary recently, and that means there is a lot of built-up engineering knowledge. Keep in mind that Hero only has four years of engineering knowledge and we have to build that up."

But Hero's most audacious move wasn't building labs—it was buying American dreams. In July 2016, HMC acquired 49.2% shareholding in Erik Buell Racing, a motorcycle sport company which produced street and racing motorcycles based in East Troy, Wisconsin, United States. The backstory was complex: EBR currently produces only its very racy 1190R Superbike, but Buell produced only 65 bikes in 2012, but Ravi Sud, chief financial officer of Hero MotoCorp, says the goal is to sell 20,000 in 2017.

The Erik Buell Racing (EBR) acquisition was strategic brilliance disguised as desperation. Hero MotoCorp, India's largest two-wheeler manufacturer, will acquire certain tangible and intangible assets of its US-based bankrupt partner Erik Buell Racing (EBR) for $2.8 million (Rs 18 crore). When EBR went bankrupt in 2015, Hero swooped in to acquire the assets. EBR had committed 17 products to Hero. It delivered 12 – bikes which required minor technology upgrades. But there were also five new products. Hero acquired these projects for $2.8 million.

This wasn't charity—it was technology acquisition at fire-sale prices. Erik Buell, the maverick American engineer who'd spent decades fighting Harley-Davidson's bureaucracy, suddenly found himself working for an Indian company that actually wanted his innovations.

Meanwhile, Hero made another prescient bet on the future: electric vehicles. HMC invested ₹205 crores (US$30.5 million) as a Series B round of funding in October 2016 and gained a 32.31% stake in Ather Energy, a start-up company manufacturing electric scooters. It invested a further ₹130 crores (US$19 million) in 2018. HMC's share in Ather Energy has grown up to 34.58% since 2016.

Ather Energy wasn't just any EV startup—it was founded by IIT Madras graduates who understood Indian conditions. Hero's investment gave them not just capital but access to manufacturing expertise and distribution networks. This hedge against the future would prove invaluable as the world shifted toward electrification.

The product launches that followed showed Hero's newfound confidence. Hero Impulse was the first motorcycle from the Indian motorcycle manufacturer to be launched solely by Hero MotoCorp. Hero introduced the Impulse in late 2008 and it was the first affordable dual sport to be available in the Indian market. Oriented towards those who choose to take the path less trodden, the Hero Impulse from first glance looks to play the part.

The Impulse wasn't a commercial success—it was too niche for India's commuter-obsessed market. But it proved something crucial: Hero could design and build motorcycles without Honda. The engineering might not have been revolutionary, but the psychological barrier was broken.

More importantly, Hero maintained its core strength: understanding the Indian consumer. While everyone obsessed over whether Hero could match Honda's technology, Hero quietly continued dominating the market that mattered. The Splendor and Passion continued to sell in millions, generating the cash flow that funded all these experiments.

The numbers validated the strategy. Net Sales in FY15 stood at Rs 27,538Cr & has shown CAGR growth of 9.2% over the last 5 Years The company wasn't just surviving—it was thriving. Market share remained above 30%, and Hero continued as the world's largest two-wheeler manufacturer by volume.

On 21 April 2014, Hero MotoCorp announced its plan on a ₹254 crore joint venture with Bangladesh's Nitol-Niloy Group in the next five years to set up a manufacturing plant in Bangladesh. This international expansion—impossible under the Honda partnership—showed Hero's new strategic freedom.

The R&D investments bore fruit in unexpected ways. The company has already established the credentials of its R&D function with the successful launch of Maestro Edge & Duet scooters — the first of its products designed and developed by Hero's in-house R&D team. These weren't revolutionary products, but they were Hero's own—designed, developed, and manufactured without any Honda involvement.

Myth vs Reality Box: Myth: Hero's post-Honda products were failures. Reality: While products like Impulse didn't set sales charts on fire, Hero's core products continued dominating. The real success was maintaining 30%+ market share while building independent R&D capabilities—a transition most joint venture survivors never manage.

By 2020, Hero had answered its critics. The company that was supposed to collapse without Honda had: - Built one of India's largest R&D facilities - Acquired American technology through EBR - Invested in electric vehicle capabilities through Ather - Expanded internationally to Bangladesh and Colombia - Maintained market leadership in India

But the real test was yet to come. As the world shifted toward electric vehicles and digital connectivity, could a company built on selling simple, reliable motorcycles to rural India transform itself for the future?

So What for Investors: Hero's post-divorce strategy teaches us that technology gaps can be bridged through strategic acquisitions and partnerships rather than organic development alone. The EBR and Ather investments show sophisticated portfolio thinking—betting on multiple technologies while maintaining cash cow products. Most importantly, Hero proved that in emerging markets, distribution and market knowledge can trump technology if you have the capital and patience to acquire what you lack. The key lesson: successful independence requires investing in capabilities before you desperately need them, not after.

VI. The Product Portfolio & Splendor Phenomenon

Walk into any village in India—from the desert towns of Rajasthan to the tea gardens of Assam—and you'll see it: a red and black motorcycle, slightly dusty, definitely overloaded, carrying a family of four plus groceries. The Hero Splendor isn't just a motorcycle; it's India's mobility solution, having sold over 35 million units since 1994. To understand Hero MotoCorp, you must understand the Splendor phenomenon. The numbers are staggering. Hero Splendor was the best-selling motorcycle in FY24 with 32,93,324 units sold during the said period. Hero MotoCorp sold 2,45,875 units of the 100-110cc Splendor range during January 2023 alone. Around 250,786 Splendor units sold in November 2023 alone—that's one motorcycle every 10 seconds, 24 hours a day, every single day.

But numbers don't explain the phenomenon. To understand the Splendor, you need to understand Indian aspiration. In rural India, owning a Splendor isn't just buying transportation—it's joining the middle class. It's the difference between your daughter going to the village school or the better one in the next town. It's being able to visit the doctor when you're sick, not when you're dying. It's dignity on two wheels.

The product architecture is deceptively simple. A 97.2cc air-cooled engine producing about 8 horsepower. Four-speed gearbox. Drum brakes. No fancy electronics. But here's the genius: Splendor's box section double cradle frame is so tough, that it can carry 4 adults without even the hint of chassis flex. That horizontal engine offers so much load pulling torque, that carrying heavy loads up steep inclines is a breeze.

Splendor and HF Deluxe accounting for 40% of total sales tells only part of the story. These two models essentially fund Hero's entire R&D budget, its electric vehicle investments, and its premium bike experiments. They're the cash cows that enable everything else.

The Splendor's claimed mileage stands at 73kmpl, but even in real-world conditions, riders report 65-70kmpl. Combined with the near 10-litre fuel tank means even your real-world riding range is more than 700km. In a country where petrol prices matter and fuel stations can be 50 kilometers apart in rural areas, this isn't just efficiency—it's freedom.

The product segmentation strategy reveals Hero's deep market understanding:

Entry Level (100-110cc): - Splendor Plus: The workhorse - HF Deluxe: The value champion - These two alone account for 40% of Hero's total volume

Executive Segment (125cc): - Passion: The premium commuter - Glamour: Style-conscious youth - Super Splendor: The Splendor with more power - 125cc segment divided into performance (Xtreme), style (Glamour), efficiency (Super Splendor)

Premium Segment (200cc+): - Karizma XMR, H-D X440, MAVRICK 440 - Premium segment contributed ~25% to the revenue mix Q3FY24 - Higher margins but lower volumes

The Splendor phenomenon extends beyond the product itself. Everything about the Splendor Plus screams accessibility. It's a bike that almost everyone in the family can get on and ride. The 785mm seat height and 112kg, both are amongst the lowest in the class. This universality is deliberate—Hero designed the Splendor to be rideable by a 5'2" grandmother and a 6' college student.

The service network amplifies this accessibility. The Hero Splendor Plus spare parts price is not only cheap but they're also readily available, backed by Hero's massive service network. A Splendor can be serviced in any village with a mechanic and basic tools. Try that with a KTM Duke.

Myth vs Reality Box: Myth: The Splendor succeeds only because of low price. Reality: The Splendor's 18-inch wheels (vs 17-inch on competitors), taller gearing for highway capability, and overbuilt frame show sophisticated engineering choices. It's not the cheapest bike—it's the best value engineering solution for Indian conditions.

But Hero faces a challenge: The commuter segment is saturating. Young buyers want more than just transportation. They want style, features, and performance. Hero's response has been interesting—instead of abandoning the Splendor formula, they're extending it upward and adding technology.

With the newly launched Splendor Plus Xtec 2.0, the bike has a segment-first LED headlight, hazard lights, fully digital LCD console with Bluetooth connectivity. These aren't gimmicks—they're Hero's attempt to make the Splendor relevant to smartphone-native millennials while keeping the core value proposition intact.

The numbers validate this evolution. The Hero Splendor has been an absolute legend in the Indian motorcycling industry and the bike regularly sells nearly 2.5 lakh units every month. That's more than most manufacturers sell in a year.

But perhaps the most remarkable aspect of the Splendor phenomenon is its consistency. In an industry obsessed with new launches and model refreshes, the Splendor has remained fundamentally unchanged for decades. The Splendor never got a comprehensive design change but that's not necessarily a bad thing as customers prefer the familiarity of the Splendor's design.

This consistency has created something rare in automotive history: intergenerational brand loyalty. Fathers who bought Splendors in the 1990s are buying them for their sons today. The motorcycle has become part of India's cultural fabric, appearing in movies, songs, and wedding processions.

The financial impact is extraordinary. Just like for decades, the Splendor and the Passion Pro range bring in the maximum revenue for the company. These humble commuters generate the profits that fund Hero's transformation into a global player.

So What for Investors: The Splendor phenomenon teaches us that in emerging markets, solving real problems at scale beats technological sophistication every time. Hero's ability to sell 250,000+ units monthly of essentially the same product for three decades shows the power of product-market fit. For investors, the lesson is clear: look for companies that understand their customers so deeply that the product becomes culturally embedded. The moat isn't technology or brand—it's becoming part of how a society functions. Hero didn't just build motorcycles; they built India's mobility infrastructure one Splendor at a time.

VII. Electric Revolution & VIDA Brand (2020–Present)

The boardroom was divided. It was late 2019, and Pawan Munjal faced perhaps his toughest decision as CEO. Electric vehicles were coming—everyone knew that. The question was whether Hero, built on internal combustion engines, could reinvent itself for the electric age. More importantly, should it? The skeptics had a point. In 2023, Hero MotoCorp's EV sales accounted for 2% of its total sales. With the launch of new electric models in 2024, the company aims to increase this share to 5%. In a market where Ola Electric was burning cash to capture 40% market share and Ather Energy (in which Hero had invested) was bleeding money, did Hero really need to enter this battlefield?

The answer came not from market research but from regulatory reality. India had committed to net-zero emissions by 2070. Major cities were implementing EV-only zones. The writing wasn't just on the wall—it was in government policy documents. Hero could either lead the transition or become its victim.

But Hero faced a unique challenge: trademark complications. A 2010 settlement between members of the Munjal family prevented Pawan Munjal's Hero MotoCorp from using the 'Hero' brand for electric vehicles. Those rights went to nephew Naveen Munjal's Hero Electric company. This meant Hero MotoCorp, the world's largest two-wheeler manufacturer, couldn't use its own name for electric vehicles.

The solution was elegant: create an entirely new brand. Hero MotoCorp has finally entered the world of electric vehicles through its new brand – Vida. Vida isn't a new company. It is a brand with a separate identity from Hero's, but all its sales and performance will be tracked under Hero MotoCorp.

The VIDA launch in October 2022 was deliberately understated. While Ola Electric was making headlines with celebrity endorsements and massive factory announcements, Hero quietly launched two products: the V1 Plus and V1 Pro. The strategy was classic Hero—let the product speak, not the marketing.

Launched on October 7, 2022, Hero MotoCorp's Vida brand has clocked retail sales of 100,195 units till August 4, 2025 with the last 45,000 units delivered to customers this year to give it a current market share of 6 percent. If Vida, which hit its best-ever monthly sales of 10,504 units in July, maintains the same growth trajectory, it could also go to register 100,000 sales for the first time in a calendar year.

The growth trajectory reveals Hero's methodical approach. Hero Vida's January-July 2025 sales at 43,885 units have already surpassed the CY2024 total of 43,709 units. This gives it a 6% share of the 719,428 e-2Ws sold in India between January 1-August 4 as compared to the 4% market share in CY2024.

But the real innovation wasn't in the product—it was in the business model. The scooter is available in two variants and is also offered with a Battery-as-a-Service (BaaS) subscription model. As per the company website, the VX2 Go now costs Rs 44,990 and the VX2 Plus Rs 57,990 with the Battery as a Service option that slashes the EV purchase cost, which makes them among the most affordable e-scooters in India.

Think about what BaaS means for Indian consumers. Instead of paying ₹1 lakh upfront for an electric scooter, they pay ₹45,000 for the vehicle and rent the battery. This transforms the economics—suddenly, an EV isn't a premium product but an accessible commuter option. Hero understood that in India, upfront cost matters more than total cost of ownership.

The distribution strategy leveraged Hero's greatest asset. The company, which opened its first Experience Centre on November 2022, currently has coverage across India with over 200 touchpoints spanning 120 cities and 180-plus dealers. Hero operates over 3,100 fast-charging stations across 250 cities through a partnership with Ather Energy, where Hero is an investor. The Vida dealer network includes 203 locations with 180 dealers in 116 cities.

This infrastructure advantage is crucial. While Ola Electric struggles with service complaints and Ather battles to expand beyond metros, Hero can leverage its 6,000+ touchpoint network. A Hero dealer selling Splendors can add VIDA to their portfolio with minimal investment.

The technology partnerships reveal sophisticated thinking. Hero's partnership with Zero Motorcycles for developing 500-600cc equivalent electric motorcycles shows ambition beyond scooters. The ₹205 crores investment in Ather Energy as a Series B round of funding in October 2016 and gained a 32.31% stake. It invested a further ₹130 crores in 2018. HMC's share in Ather Energy has grown up to 34.58% since 2016.

This Ather investment is particularly clever. Hero gets access to Ather's charging network, technology insights, and market intelligence while maintaining its own product development. It's cooperation and competition simultaneously—a delicate balance few companies manage.

Myth vs Reality Box: Myth: Hero is too late to the EV party to matter. Reality: Both companies have successfully leveraged their traditional automotive strengths – extensive dealer networks, established service capabilities, and brand trust – to capture significant market share from early EV players like Ola Electric. This shift demonstrates that the electric two-wheeler market is consolidating around established players with proven distribution and after-sales infrastructure.

The market dynamics are shifting rapidly. Ola Electric, once the undisputed leader, dropped to third place in May with 18,499 units, marking a sharp 51% decline from May 2024. Its market share fell to 18.4%. Hero MotoCorp, though starting from a low base, posted a 191% jump to 7,164 units in May, with its share improving to 7.1%.

This isn't just market share shuffle—it's validation of Hero's thesis that in India, distribution and service matter more than technology leadership. Ola's struggles with quality and service are driving customers to established brands that can provide reliable after-sales support.

The product roadmap shows increasing confidence. "We are planning two new affordable products in the first half, most likely in July. That will help us accelerate our growth and gain market share," Hero MotoCorp management told investors during a recent earnings call, confirming prices below ₹70,000 for the new models.

But perhaps the most intriguing development is the Electric Splendor project (AEDA) under development for 2027 launch, targeting 200,000 units annually. This isn't just another EV—it's Hero's attempt to electrify its cash cow. If Hero can create an electric Splendor that delivers similar value proposition—reliability, affordability, efficiency—it could transform Indian mobility.

The international ambitions add another dimension. Hero also intends to enter European markets including the UK, France, Spain, and Italy in the second half of 2025. The Hero MotoCorp Vida V1 electric scooter is preparing to enter the European and UK markets after debuting in the Indian market in October 2022. The Vida V1 Pro, Hero Motocorp's first foray into electric mobility, features a standard 3.94kWh battery and two removable batteries of 1.97kWh each.

This European push isn't about volumes—it's about credibility. Success in developed markets validates Hero's technology capabilities and opens doors for technology partnerships and investor confidence.

The festive season numbers provide hope. "Hero MotoCorp, achieved its highest-ever retail sales during the recent 32-day festive period, starting from Navratri. With sales of over 15.98 lakh (1.6 million) units, the company registered an impressive 13% growth compared to the festive season of 2023. VIDA crossed a significant milestone by achieving 11,600 retail sales during the same period.

So What for Investors: Hero's EV strategy reveals sophisticated portfolio management. Instead of betting everything on electrification, Hero is building optionality—investing enough to be relevant if EVs dominate, but not so much that failure would be catastrophic. The BaaS model shows understanding of Indian financial behavior, while the Ather investment provides technology hedge without full commitment. For investors, the lesson is that in technology transitions, fast followers with distribution advantages often beat first movers. Hero doesn't need to win the EV race—it just needs to not lose it while its ICE business generates cash.

VIII. Financial Performance & Market Position

The numbers tell a story of resilience that would make any CFO jealous. Hero Motocorp · Mkt Cap: 92,003 Crore · Revenue: 40,440 Cr · Profit: 5,049 Cr Company is almost debt free. In an industry where competitors are burning cash for growth and drowning in debt for expansion, Hero sits on a fortress balance sheet that would make Warren Buffett smile. Let's dissect the fortress. In the financial year 2024, Hero MotoCorp was the leading two-wheeler manufacturer in India, with a market share of 31 percent. The total income of Hero MotoCorp Limited across the global was around 383.5 billion Indian rupees during fiscal year 2024. In financial year 2024, the number of vehicles sold by Hero MotoCorp Limited across India was about 5.6 million.

But these headline numbers mask both strengths and vulnerabilities. The company has delivered a poor sales growth of 6.94% over past five years—a number that would make growth investors wince. Yet the company maintains Profit: 5,049 Cr on Revenue: 40,440 Cr, delivering 12.5% net margins that most manufacturers would kill for.

The capital structure is a thing of beauty. Market Cap: ₹92,003 Cr with the company being almost debt free. In an industry where Bajaj carries significant debt and TVS leverages aggressively for growth, Hero's clean balance sheet provides strategic flexibility. They can weather downturns, make opportunistic acquisitions, or return cash to shareholders without worrying about covenant breaches.

The dividend policy reflects this strength. Dividend yield of 3.59% might not excite yield hunters, but for a company investing heavily in R&D and electric vehicles, it shows prudent capital allocation. Hero returns cash to shareholders while retaining enough for strategic investments.

The manufacturing capabilities are staggering. Annual capacity of 9.1 million units across eight facilities. Five facilities: Dharuhera, Gurugram, Neemrana, Haridwar, Halol. Production capacity over 7.6 million units annually. This isn't just scale—it's optionality. Hero can ramp production for new products without massive capital expenditure.

But the market share story is complex. Hero's share of rural two-wheeler sales in India has dropped from 40.4 per cent in 2018 to 33.3 per cent in 2023. This rural erosion is concerning because rural India has been Hero's fortress. In contrast, Bajaj's share increased from 12.7 per cent in 2018 to 13.9 per cent, HMSI's from 21.8 per cent to 22.2 per cent, and TVS' from 15.5 per cent to 17.8%.

The competitive dynamics are shifting. Honda has overtaken Hero in term of two-wheeler retail sales in the month of September 2024 they have sold 3,33,927 units of two-wheelers in India. In contrast, Hero MotoCorp, who is traditionally the market leader, slipped to the second position, by selling 2,71,390 units, holding 22.54% of the share. This was a psychological blow—Honda beating Hero at its own game.

Yet the full-year picture remains robust. FY 2024-25 was a milestone year for Hero MotoCorp across multiple verticals. In the domestic market, Hero sold 56,11,758 units, registering growth over the previous fiscal and reinforcing its position as India's top two-wheeler brand. On the global front, Hero's exports soared by 43% YoY, reaching 2,87,429 units.

The segment performance reveals strategic evolution:

Commuter Segment (60% of sales): - The 97.2cc HF Deluxe, Splendor + and Passion Plus account for 23,43,184 units - Growing but slowly—the cash cow is maturing

Executive Segment (25% of sales): - 125cc models growing faster than entry level - Reflects India's economic progression

Premium Segment (15% of sales but 25% of revenue): - Premium segment contributed ~25% to the revenue mix Q3FY24 - Higher margins compensating for lower volumes - Harley-Davidson X440 recorded sales of over 11,000 units

The R&D investments are bearing fruit. R&D investments: $150 million in 2023, planning 15% increase in 2024. This isn't just maintenance capex—it's transformation investment. Hero is spending to build capabilities it never needed under Honda.

Financial Metrics That Matter:

| Metric | FY2024 | Industry Average | Analysis |

|---|---|---|---|

| ROE | ~25% | 18% | Superior capital efficiency |

| ROCE | ~30% | 22% | Excellent asset utilization |

| Debt/Equity | ~0 | 0.4 | Fortress balance sheet |

| Working Capital Days | 15 | 30 | Superior cash conversion |

| EBITDA Margin | 16% | 12% | Pricing power intact |

Myth vs Reality Box: Myth: Hero's poor 5-year growth shows structural decline. Reality: The 6.94% CAGR reflects conscious choice to maintain margins over market share. Hero could easily gain share by cutting prices but chooses profitability. In a commoditizing market, this discipline is actually a strength.

The international expansion provides optionality. On the global front, Hero's exports soared by 43% YoY, reaching 2,87,429 units—a sharp rise from 2,00,923 units in FY24. This isn't material to current profits but provides growth runway as Indian market matures.

The capital allocation framework shows sophistication:

1. Maintenance: ~₹500 crore annually for existing operations

2. Growth: ~₹1,000 crore for new products and R&D

3. Strategic: ~₹500 crore for EV and partnerships

4. Returns: ~₹3,000 crore in dividends

This framework ensures Hero isn't just maintaining position but building for the future while rewarding shareholders today.

So What for Investors: Hero's financial profile is that of a mature cash generator transitioning to growth investor. The debt-free balance sheet provides downside protection while R&D investments create upside optionality. The key insight: Hero trades at ~18x P/E while generating 25% ROE—this is value territory for a market leader. The risk isn't financial but strategic—can Hero navigate the EV transition while maintaining ICE profitability? The numbers suggest yes, but execution will determine whether this is a value trap or opportunity.

IX. Global Expansion & Distribution Excellence

The warehouse in Dhaka, Bangladesh, is buzzing with activity. It's 6 AM, and already dozens of Hero motorcycles are being loaded onto trucks headed for dealers across the country. This scene, replicated in Colombia, Nigeria, and 44 other countries, represents Hero's transformation from an India-centric company to a genuine global player.

Hero's international journey began the moment the Honda partnership ended. Hero MotoCorp can now export to Latin America, Africa, and West Asia. Hero is free to use any vendor for its components instead of just Honda-approved vendors. This freedom, denied for 27 years, unleashed pent-up international ambitions.

The numbers tell the expansion story. Presence across 47 countries. Over 10,000 customer touchpoints worldwide. The global footprint isn't just about planting flags—it's about building sustainable businesses in diverse markets.

The Bangladesh venture exemplifies Hero's approach. 2014 Bangladesh JV with Nitol-Niloy Group (₹254 crore investment, 55% stake). The plant started production in 2017 under the name "HMCL Niloy Bangladesh Limited". Hero MotoCorp owns 55% of the manufacturing company and the rest 45% is owned by Niloy Motors.

Bangladesh wasn't chosen randomly. It's a market of 170 million people with rising incomes and terrible public transport—essentially India 20 years ago. Hero's ability to replicate its India playbook in similar markets is its international superpower.

Colombia represents a different strategy. Hero launched in Colombia with six best-selling models. The hero is the first Company to offer a five-year and a four-year warranty in Bangladesh and Colombia, respectively. These extended warranties aren't generosity—they're market entry tools that signal quality to skeptical consumers unfamiliar with Indian brands.

But Hero's real competitive advantage isn't international—it's the domestic distribution network that generates cash to fund global expansion. Over 6,000 dealerships and service points in India. This network, built over 40 years, is essentially impossible to replicate.

The distribution economics are compelling. A typical Hero dealership requires ₹2-3 crore investment but generates ₹50-100 lakh annual profit. With 6,000 dealers, that's ₹3,000-6,000 crore of capital invested by partners, not Hero. This asset-light model allows Hero to maintain 30% ROCE while competitors struggle to break 20%.

The rural penetration is particularly impressive. Hero GoodLife loyalty program (formerly Hero Honda Passport Program) since 2000 has millions of members, creating switching costs in rural markets where brand loyalty runs deep. These aren't just customers—they're a community that influences purchase decisions across villages.

The service network amplifies this advantage. A Hero motorcycle can be serviced in any village with a mechanic and basic tools. This isn't true for KTM, Yamaha, or even TVS in many areas. In rural India, where the nearest authorized service center might be 100 kilometers away, this matters immensely.

Distribution Network Comparison:

| Company | India Touchpoints | Rural Coverage | Service Points | International Presence |

|---|---|---|---|---|

| Hero | 6,000+ | 80% | 10,000+ | 47 countries |

| Bajaj | 3,500 | 60% | 5,000 | 70 countries |

| TVS | 3,000 | 50% | 4,000 | 60 countries |

| Honda | 2,500 | 40% | 3,000 | 15 countries (from India) |

The digital transformation of this network is underway. Hero's investment in digital infrastructure—inventory management, customer tracking, service scheduling—is modernizing what was essentially a paper-based system. This isn't sexy, but it's essential for maintaining distribution superiority as India digitizes.

Myth vs Reality Box: Myth: Hero's international expansion is failing because volumes remain low. Reality: International operations are profitable and growing 40%+ annually. The strategy isn't to compete with Japanese brands globally but to dominate markets similar to India. In these markets, Hero's value proposition resonates strongly.

The supply chain that feeds this distribution deserves attention. Hero MotoCorp has five joint ventures or associate companies, Munjal Showa, AG Industries, Sunbeam Auto, Rockman Industries, and Satyam Auto Components, that supply a majority of its components. This vendor ecosystem, built over decades, provides cost advantages competitors can't match.

The implications for competition are profound. Every new entrant—whether Ola Electric or a Chinese manufacturer—must either build this distribution from scratch (requiring thousands of crores) or remain confined to urban markets. This is Hero's real moat, more than brand or technology.

So What for Investors: Distribution in emerging markets is an underappreciated moat. Hero's 6,000+ touchpoint network would cost ₹15,000+ crore to replicate and take decades to build. This network generates predictable cash flows, creates switching costs, and provides last-mile advantage in rural markets where 65% of India lives. For investors, the lesson is clear: in markets where infrastructure is weak, owning distribution is owning the customer relationship. Hero doesn't just sell motorcycles—it owns the rails on which two-wheelers reach India.

X. Playbook: Business & Investing Lessons

If Hero MotoCorp's journey were a business school case study, it would be titled "How to Build a ₹90,000 Crore Company from a Refugee Camp." But the real lessons go deeper than the inspiring origin story. This is a masterclass in navigating the treacherous waters of emerging market capitalism.

Lesson 1: The Power of Patient Capital in Family Businesses

The Munjal family held onto Hero through three generations, multiple crises, and countless acquisition offers. When PE firms invested post-Honda split, the family maintained control while accessing growth capital. This isn't stubbornness—it's understanding that in emerging markets, relationships and reputation built over decades are irreplaceable assets.

Consider Bain Capital's investment: Rs 2500 Cr in June 2011 for 8.6% stake, earning Rs 5,100 crore on exit. Bain made 2x, but the Munjal family's stake grew from ₹20,000 crore to ₹35,000 crore. The lesson? In great businesses, selling equity is usually a mistake.

Lesson 2: Joint Ventures as Learning Laboratories

The Honda partnership wasn't just about technology transfer—it was a 27-year MBA in world-class manufacturing. Hero learned: - Quality control systems that could scale to millions of units - Supply chain management across thousands of vendors - The discipline of continuous improvement (Kaizen) - How to manage complexity while maintaining efficiency

When the partnership ended, Hero didn't just lose a technology partner—it graduated from university. The ₹6,400 crore Honda received was essentially Hero's tuition fee for becoming world-class.

Lesson 3: The Distribution Dividend

In developed markets, product differentiation drives success. In emerging markets, distribution dominance determines winners. Hero's 6,000 dealer network isn't just a sales channel—it's: - Working capital financing (dealers fund inventory) - Market intelligence network (real-time demand signals) - Service infrastructure (critical for repeat purchases) - Brand ambassadors (dealers influence rural purchasing)

Every competitor has better products somewhere in their portfolio. None have better distribution. In markets where reaching the customer costs more than making the product, this matters more.

Lesson 4: The Simplicity Premium

The Splendor's unchanged design for 30 years isn't laziness—it's brilliance. In markets where customers value reliability over innovation, consistency creates trust. Hero understood that their customer doesn't want the latest technology—they want technology that won't fail them on a monsoon-soaked highway at midnight.

This extends to financial simplicity. Hero's business model is transparent: make motorcycles, sell them through dealers, service them forever. No financial engineering, no complex subsidiaries, no acquisition-driven growth. In emerging markets, simplicity is a competitive advantage.

Lesson 5: Managing Technology Transitions

Hero's approach to electrification—investing enough to be relevant but not betting the company—shows sophisticated risk management. They're: - Letting others bear the cost of market education (Ola's billions in losses) - Learning from competitors' mistakes (Ather's struggling unit economics) - Maintaining ICE profitability while building EV capability - Using partnerships (Zero Motorcycles) rather than internal development

This isn't cowardice—it's recognition that in technology transitions, fast followers often beat first movers.

Lesson 6: The Value of Values

Hero's reputation for treating dealers, employees, and customers fairly has compound benefits: - Dealers invest their own capital based on trust - Employees stay for decades, preserving institutional knowledge - Customers become multi-generational buyers - Suppliers extend credit during tough times

In emerging markets where formal institutions are weak, reputation is the ultimate currency.

Lesson 7: Capital Allocation in Cycles

Hero's capital allocation through industry cycles shows mastery: - Boom times: Invest in capacity and R&D - Downturns: Maintain prices, let weak competitors fail - Transitions: Partner rather than build - Always: Return cash to shareholders

This counter-cyclical approach requires conviction and capital. Hero has both.

Lesson 8: Building Moats in Commodity Businesses

Motorcycles are commodities—engines, wheels, seats assembled differently. Yet Hero maintains 30%+ market share and 15%+ EBITDA margins. How? - Scale economics: Lowest cost producer - Distribution density: Highest reach - Brand trust: Generational loyalty - Service network: Peace of mind - Financial strength: Ability to withstand price wars

These reinforce each other, creating a flywheel that strengthens with scale.

Key Investment Lessons:

-

Time Horizon Arbitrage: Markets obsess over quarterly EV sales. Hero thinks in decades. This mismatch creates opportunity.

-

Quality at Reasonable Price: Hero trades at 18x earnings despite 25% ROE, market leadership, and fortress balance sheet. This is classic value territory.

-

Optionality Value: The EV investments, international expansion, and premium segment provide free options on future growth.

-

Downside Protection: Debt-free balance sheet and cash generation provide margin of safety.

-

Management Quality: Three generations of successful leadership, smooth succession planning, and conservative accounting.

The Meta-Lesson:

Hero MotoCorp's story teaches us that in emerging markets, execution beats innovation, distribution beats differentiation, and patience beats pace. The company that wins isn't the one with the best product—it's the one that understands its customers most deeply and serves them most reliably.

For investors, Hero represents a special category: a dominant company in a growing market trading at reasonable valuations with multiple options for growth. These opportunities are rare. When they appear, the correct response isn't analysis paralysis—it's conviction backed by capital.

So What for Investors: Hero's playbook reveals that great emerging market businesses are built on boring foundations: distribution, reputation, and financial conservatism. The excitement comes from compounding these advantages over decades. For investors, the lesson is to look for companies with these characteristics trading at reasonable prices, then hold them through cycles. The biggest investment mistakes aren't buying bad companies—they're selling great ones too early.

XI. Analysis & Future Outlook

The spreadsheet on the analyst's laptop shows two scenarios for Hero MotoCorp in 2030. In one, Hero is a ₹200,000 crore company dominating both ICE and EV markets. In the other, it's a melting ice cube, slowly losing relevance as the world goes electric. The truth, as always, lies somewhere in between.

Bull Case: The Dominant Scenario

The optimists point to structural tailwinds that seem almost too good to be true. India's two-wheeler market is expected to grow from 18 million units to 30 million by 2030. Even maintaining current market share would mean Hero selling 9 million units annually—60% growth from today.

The math gets more interesting when you add mix improvement. Premium segment contributed ~25% to the revenue mix Q3FY24. If this reaches 40% by 2030 (still below global averages), Hero's revenue per unit could increase 50% without selling a single additional motorcycle.

Rural recovery presents another lever. Hero's share of rural two-wheeler sales in India has dropped from 40.4 per cent in 2018 to 33.3 per cent in 2023. Just recovering to 2018 levels would add 1 million units annually. With normal monsoons and rising rural incomes, this isn't fantasy—it's reversion to mean.

The EV transition, counterintuitively, could strengthen Hero's position. While startups burn cash building infrastructure, Hero can leverage its existing network. If EVs reach 30% penetration by 2030 and Hero captures its fair share, that's 3 million electric units annually—a ₹30,000 crore opportunity.

International expansion provides the growth kicker. Hero's exports soared by 43% YoY, reaching 2,87,429 units. If Hero reaches 1 million export units by 2030 (Bajaj already does more), that's ₹10,000 crore in additional revenue at higher margins.

The balance sheet enables all of this. Company is almost debt free with ₹5,000+ crore annual free cash flow. Hero can fund growth organically while returning cash to shareholders—a rare combination.

Bear Case: The Disruption Scenario

The pessimists see storm clouds gathering. Poor 5-year sales growth of 6.94% suggests structural issues, not temporary headwinds. In an industry growing double-digits, single-digit growth means losing relevance.

Competition is intensifying everywhere. Honda overtaking Hero in September 2024 wasn't an anomaly—it's a trend. TVS and Bajaj are gaining share in rural markets. Ola Electric, despite problems, has captured 20% of the EV market in two years. Chinese manufacturers are eyeing India. Hero faces attack from all sides.

The EV transition poses existential risk. Current market share in mid-single digits in EV segment is concerning. If EVs reach 50% penetration by 2030 (aggressive but possible), and Hero doesn't improve share, half their market disappears. The Splendor has no electric equivalent—when it dies, what replaces that cash flow?

Urban market saturation is already visible. Two-wheeler penetration in cities exceeds 60%. The next wave of growth must come from rural areas where Hero is losing share, or from EVs where Hero is subscale. Neither inspires confidence.

Input cost pressures are structural. Rising input costs squeeze margins. Environmental regulations increase compliance costs. Safety requirements add features that rural customers won't pay for. The business model that worked for 40 years may not work for the next 10.

The Realistic Scenario

The truth incorporates both narratives. Hero will likely: - Maintain 25-30% market share in ICE motorcycles - Capture 10-15% of the EV market - Grow international to 500,000 units - See margins compress but remain profitable - Generate ₹60,000-70,000 crore revenue by 2030

This isn't spectacular, but it's solid. 8-10% revenue CAGR, 12-15% profit CAGR (through mix improvement), and consistent dividends. For a ₹92,000 crore company, that's reasonable.

Technology & Innovation Pipeline

R&D investments: $150 million in 2023, planning 15% increase in 2024 signals commitment to innovation. The Centre of Innovation and Technology in Jaipur with 500 engineers is bearing fruit. But innovation at Hero means something different than at Tesla: - Improving fuel efficiency by 5% matters more than adding Bluetooth - Reducing service intervals saves customers thousands annually - Making parts interchangeable across models reduces inventory costs

The Electric Splendor project (AEDA) under development for 2027 launch, targeting 200,000 units annually could be transformative. If Hero creates an electric motorcycle with Splendor-like economics, the EV transition becomes an opportunity, not threat.

Regulatory & ESG Considerations

Bharat Stage VI emission norms are increasing costs but also creating barriers to entry. Chinese manufacturers can't dump cheap, polluting motorcycles anymore. Environmental regulations favor established players with resources to comply.

The ESG angle is interesting. Two-wheelers enable economic mobility while producing fraction of car emissions. As cities restrict four-wheelers, two-wheelers benefit. Hero's motorcycles aren't just products—they're climate solutions for emerging markets.

Capital Markets Perspective

The stock trades at interesting levels: - P/E of 18x vs historical average of 22x - EV/EBITDA of 11x vs peers at 15x - Dividend yield of 3.59% provides downside support - Market cap of ₹92,000 crore for a company generating ₹5,000 crore profit

This isn't priced for growth—it's priced for gradual decline. If Hero merely muddles through, the stock is fairly valued. If any of the growth levers work, there's upside.

Key Monitorables for Investors:

- Monthly EV market share: Must reach double-digits by 2025

- Rural market share: Recovery to 35%+ critical

- Premium mix: Target 30% of revenue

- Export trajectory: 500,000 units validates international strategy

- Margin evolution: Maintaining 12%+ EBITDA margins essential

The Investment Decision

Hero MotoCorp represents a classical value situation: a quality company facing temporary headwinds trading at reasonable valuations. The market sees disruption; the numbers show resilience. The stock prices in significant execution risk, but the business quality provides margin of safety.

For growth investors, Hero lacks excitement. For value investors, it offers a dominant franchise at reasonable price. For dividend investors, it provides consistent returns. It won't make anyone rich quickly, but it won't make them poor either.

So What for Investors: Hero's future isn't binary—it's a probability distribution. The company will likely remain relevant but less dominant, profitable but less so, growing but slowly. This "muddle through" scenario isn't exciting, but at current valuations, investors don't need excitement. They need the market leader in a growing industry with a fortress balance sheet trading at 18x earnings to not catastrophically fail. That's a bet worth considering, especially when the downside is protected by ₹40,000 crore of annual revenue that isn't disappearing anytime soon.

XII. Epilogue & Reflections

The sun sets over the Dharuhera plant, where Hero Honda rolled out its first CD100 in 1985. Nearly four decades later, motorcycles still stream off the production lines—one every 10 seconds, 24 hours a day. But look closer, and you'll see electric scooters interspersed with Splendors, robots working alongside craftsmen, and engineers video-conferencing with colleagues in Germany. This is Hero MotoCorp in 2024: a company straddling two worlds, honoring its past while building its future.

Brijmohan Lall Munjal, who passed away on November 1, 2015, never saw Hero's independence fully flower. But his vision—that every Indian family deserved affordable, reliable transportation—remains the company's North Star. From partition refugees to global leaders: The ultimate entrepreneurial story isn't just corporate propaganda. It's a reminder that great businesses are built on foundations deeper than spreadsheets.

The Hero story teaches us something profound about emerging market capitalism. Success doesn't come from copying Silicon Valley's playbook of blitzscaling and disruption. It comes from understanding your market so deeply that you become woven into its fabric. Hero didn't disrupt Indian transportation—it enabled it.

Consider what Hero has actually achieved. Over 100 million motorcycles sold. That's 100 million families whose lives changed because they could travel farther for work, education, and healthcare. In development economics terms, Hero has probably done more for poverty alleviation than most NGOs. They just happened to make ₹5,000 crore profit while doing it.

The transition from Hero Honda to Hero MotoCorp represents something larger than corporate strategy. It's about emerging market companies claiming their destiny. For too long, the narrative was that Indian companies needed foreign partners for technology and credibility. Hero proved that narrative wrong. They didn't just survive without Honda—they thrived.

But reflection requires honesty about challenges. The company has delivered a poor sales growth of 6.94% over past five years. In a growth-obsessed market, this is seen as failure. Yet Hero generates more cash than most "growth" companies ever will. The question isn't whether Hero is growing fast enough—it's whether investors understand what they own.

The EV transition crystallizes Hero's challenge and opportunity. The company that built its fortune on internal combustion must now cannibalizes its own products. It's like asking Kodak to invent digital photography—possible but psychologically difficult. Yet Hero's measured approach—investing enough to be relevant but not betting the company—shows maturity rare in corporate India.

What Hero MotoCorp teaches us about emerging market dynamics is invaluable: - Distribution beats innovation in markets where reaching customers is harder than making products - Reliability beats features when customers depend on products for livelihood, not leisure - Patience beats pace when building businesses meant to last generations - Local knowledge beats global best practices when serving diverse, complex markets

The future of mobility in India and Hero's role isn't predetermined. India won't follow China's four-wheeler path or Europe's public transport model. It will create something uniquely Indian—probably two-wheelers for intracity transport, shared mobility for longer distances, and electric vehicles for the environmentally conscious. Hero is positioned for all three.

The next decade: Can Hero maintain leadership in the EV era? The question misses the point. Leadership in the EV era won't look like leadership in the ICE era. It won't be about market share or units sold. It will be about who enables the most people to participate in India's economic growth. By that measure, Hero has a 40-year head start.

For founders, Hero's journey offers timeless lessons: - Build businesses that solve real problems for real people - Understand your customer better than they understand themselves - Create value for all stakeholders, not just shareholders - Think in decades, not quarters - When forced to choose, choose independence over dependence

For investors, Hero represents something increasingly rare: a real business making real products for real customers generating real profits. In a world of narrative stocks and profitless growth, Hero's ₹5,000 crore annual profit feels almost quaint. But profits compound. Narratives don't.

The ultimate judgment of Hero MotoCorp won't come from stock markets or analysts. It will come from millions of Indians whose lives were transformed by affordable mobility. By that measure, Hero isn't just a successful company—it's a national treasure.

As we close this 40-year saga, one image persists: A young couple on a Splendor, heading to their wedding. A father dropping his daughter at school before work. A farmer taking produce to market. A delivery boy earning his family's first regular income. These aren't just customers—they're the reason Hero exists.

The company that started in a refugee camp has become India's mobility backbone. The partnership that seemed permanent ended, but the company grew stronger. The technology that seemed irreplaceable was replaced. The only constant has been change, and Hero's ability to adapt while staying true to its core purpose.

What comes next is uncertain. Electric vehicles, autonomous transport, shared mobility—all threaten Hero's traditional model. But if history is any guide, Hero will find a way. Not through revolutionary innovation or aggressive acquisition, but through patient evolution and deep customer understanding.

The story of Hero MotoCorp isn't ending—it's entering a new chapter. The protagonist has aged, gained wisdom, faced challenges, and emerged stronger. The next chapter may not be as dramatic as the first, but it will be equally important. Because in the end, Hero's story isn't about motorcycles—it's about mobility. And as long as Indians need to move, Hero will find a way to move them.

Key Takeaways for Founders and Investors:

- Great businesses are built on boring foundations executed brilliantly over decades

- In emerging markets, solving basic problems at scale beats creating new problems to solve

- Family businesses that professionalize while maintaining values create enduring value

- Technology transitions are navigated, not conquered—patience beats panic

- The best investments are companies you understand serving customers you understand

- Market leadership is earned through decades of trust, not quarters of growth

- Financial conservatism in good times enables opportunity capture in bad times

- The ultimate moat is becoming essential to your customers' lives

- Success is measured in impact created, not just wealth accumulated

- Every great company eventually faces existential threat—those that survive transform themselves while honoring their essence

Hero MotoCorp's journey from partition to prosperity, from dependence to independence, from ICE to EV, continues. The company that taught India to ride now must learn to ride the waves of change. Based on its history, that's a bet worth making.

The sun has set on the Dharuhera plant, but somewhere in India, a young entrepreneur is starting her business, delivering products on a Hero motorcycle. A student is riding to college, the first in his family to get higher education. A daughter is teaching her mother to ride, breaking generations of dependence.