Heritage Foods: The Pure-Play Dairy Powerhouse

I. Introduction & The "Pure Play" Thesis

Picture a Hyderabad apartment block at 5:30 a.m. The city is still half-asleep, but a small army of men on scooters is already weaving through narrow lanes, depositing one-litre pouches of milk outside thousands of doors before the maids arrive to make the morning filter coffee. By the time the sun is fully up, roughly 1.5 million households across South India will have opened a pouch printed with a familiar green and red logo. The brand is హెరిటేజ్ ఫుడ్స్ Heritage Foods, and that quiet, daily ritual is the foundation of one of the most unusual capital-allocation stories on the Indian stock exchange.

Heritage is, on paper, a deeply unsexy company. It collects perishable liquid from approximately 300,000 dairy farmers, chills it within hours of milking, processes it in plants scattered across nine states, and pushes it into a distribution net of more than 95,000 outlets and around 1,800 Heritage Parlours.1 For the financial year that ended March 31, 2024, the company reported revenue of ₹3,786 crore, profit after tax of ₹118 crore, and a return on equity north of 16% — numbers that, in absolute terms, would barely register on a Mumbai analyst's screen.2

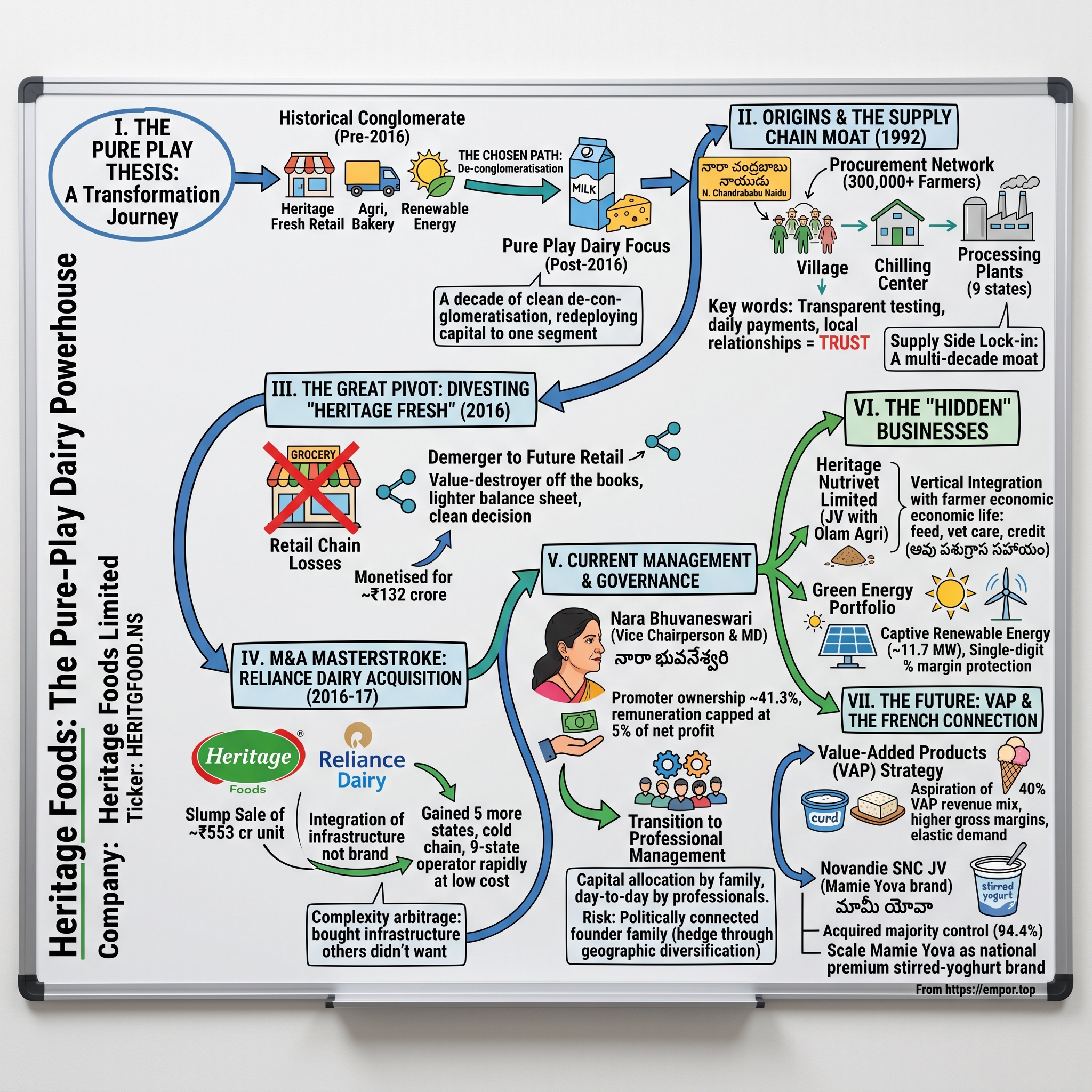

But the story here is not the absolute scale. It is the transformation. A decade ago, Heritage was a confusing little conglomerate. There was a dairy business. There was a retail chain — Heritage Fresh — competing with Reliance and More for the same urban shoppers. There was an agri-business, a bakery operation, a renewable energy arm, and various assorted experiments. The market hated it. The stock traded at a sleepy mid-single-digit multiple of cash flow, and the joke on Banjara Hills was that the family who controlled it was running half a dozen ventures at once because they did not want to choose.

Then they chose.

Between 2016 and 2025, Heritage executed one of the cleanest "de-conglomeratisations" in Indian mid-cap history. The retail chain was sold. The bakery business was wound down. The agri vertical was rationalised. Capital was redeployed into the one segment where the family had genuine procurement advantage and a 30-year head start: liquid milk and its higher-margin cousins — curd, paneer, ghee, lassi, flavoured milk, ice cream, and the new bet, French-style stirred yoghurt. By 2026, dairy contributes more than 95% of revenue, and management talks publicly about Value-Added Products, or VAP, the way a SaaS founder talks about ARR.3

This is the "Pure Play" thesis. The bet is that the Indian market — like every emerging consumer market before it — eventually pays a premium for focus, brand, and balance-sheet discipline over conglomerate sprawl. Heritage took the discount and chose the harder path: doing one thing, in one perishable, politically sensitive category, very well. This article walks through how they got here, who is running the place, and what could still break the story.

II. Origins & The Supply Chain Moat

The founding scene is unusual, because the founder did not stay around to run it. In 1992, a young politician named నారా చంద్రబాబు నాయుడు N. Chandrababu Naidu — at that point a rising figure in the Telugu Desam Party — incorporated Heritage Foods (India) Limited in the still-undivided state of ఆంధ్రప్రదేశ్ Andhra Pradesh.4 Naidu was a farmer's son from Naravaripalle, a village in Chittoor district where most households kept buffaloes for income. He had watched the local milk economy his entire life, and he understood something the urban policy class did not: organising the supply side of milk — getting it cold, getting it tested, getting the farmer paid on time — was a harder problem than selling it.

The timing was almost suspiciously good. The early 1990s were the post-liberalisation moment in India. P. V. Narasimha Rao and Manmohan Singh had just dismantled the licensing raj. The "శ్వేత విప్లవం White Revolution," the great cooperative-led milk surge that Verghese Kurien had engineered through Operation Flood since the 1970s, had pushed India past the United States to become the world's largest milk producer. But the public cooperatives — Andhra Pradesh Dairy Development Cooperative Federation, Gujarat's Amul, Karnataka's Nandini — could not absorb every farmer in every village. There was room, finally, for organised private players who could pay better and run leaner.

Heritage was built for that gap. Naidu and a small group of co-founders set up village-level milk procurement centres, bulk milk coolers, and a small processing plant. The pitch to farmers was simple: bring your morning and evening milk to our chilling centre, we will test it transparently for fat and SNF (solids-not-fat), we will pay you twice a day, and we will not haggle. In a market where the local middleman — the dudhwala — historically clipped a farmer's payment with opaque quality tests, that promise was almost radical.

Within a few years, the trust began to compound. Farmers told other farmers. Village procurement clusters became district networks. Naidu himself became Chief Minister of Andhra Pradesh in 1995 and stepped away from day-to-day management, but the procurement engine kept growing under the operating team and his wife, నారా భువనేశ్వరి Nara Bhuvaneswari, who would eventually take the executive helm.

By the early 2000s, Heritage had built what economists would call a "two-sided platform" without ever using the phrase. On one side, hundreds of thousands of small farmers — most owning two to five animals — were locked in by daily cash payments, veterinary services, and animal feed sold on credit. On the other side, urban consumers in Hyderabad, Bangalore, Chennai, and Visakhapatnam knew the green-and-red pouch as the brand that did not water down the milk. In a category where consumer fear of adulteration is genuinely visceral — Indian households still routinely boil milk to check for froth — that brand-as-trust signal was the first and most durable Power the company built.

The "moat" sounds boring when described in PowerPoint: 8 to 9 states of procurement, 15-plus processing units, hundreds of bulk milk coolers, a fleet of insulated tankers, around 15,000 village-level agents. But every single one of those nodes is a relationship. Every chilling unit is a piece of physical infrastructure that a new entrant would need to replicate, in the local political climate, at the same per-litre cost, while pricing competitively against Amul. That is the back-end problem in Indian dairy, and it took Heritage 30 years to solve it.

That long, patient build-out is what gave the family the option to be aggressive on the other side of the balance sheet — to make the bigger, scarier capital decisions that would define the next decade.

III. The Great Pivot: Divesting "Heritage Fresh"

Walk into a Heritage Fresh store in Bangalore in 2015 and the picture was almost charming: bright yellow signage, a refrigerated aisle of curd and paneer up front, a vegetable section in the back, a smattering of staples and personal care, and a bored cashier handling a queue of three customers. The chain had around 130 stores at its peak, mostly in the south, and on paper it looked like a natural extension of the dairy distribution network — if you are already chilling pouches of milk to the consumer's door, why not capture the rest of the basket?5

Anyone who has tried to run modern trade in India already knows the answer. The store economics were brutal. Rents in tier-1 metros had spiralled. Working capital — fresh produce, inventory, shrinkage — chewed cash. Margins on grocery, especially against the rising tide of Reliance Retail's More chain, BigBasket's online assault, and DMart's hyper-low-cost format, refused to move past low single digits. The category was, in the language of corporate finance, a value-destroyer. And it was sitting on the same balance sheet as a high-return dairy business that was being asked to subsidise it.

The internal debate, by all accounts, was painful. Retail had been a strategic talking point for the company for more than a decade. Senior management had built careers inside it. There was a plausible story that the store fleet could be turned into a captive distribution moat. But by 2016, the numbers refused to behave. The retail segment was loss-making, the brand was sub-scale, and the capital that was being trapped inside it could earn 20%-plus inside the dairy plants.

The decision, when it came, was uncharacteristically clean for an Indian family business. On November 7, 2016, Heritage Foods announced that it had agreed to demerge its retail undertaking into Future Retail Limited — Kishore Biyani's vehicle — in a share-swap deal. Heritage shareholders received Future Retail shares in proportion to their holdings, and Heritage itself was issued a stake equivalent to about 3.65% of Future Retail's enlarged equity base.[^6] In one stroke, the retail vertical was off the books.

There are three things to notice about how this was structured. First, no cash changed hands. That was unusual — Indian promoters typically want their pound of flesh in cash on exit — but it also meant Heritage retained upside if the Future Retail story worked, and avoided crystallising a tax bill on what was, at the time, a low-basis asset. Second, the deal was framed as a "strategic combination" rather than a fire sale, which protected employee morale and brand value during the transition. Third — and this is the part that looks prescient in hindsight — Heritage did not wait to see if Future Retail's later financial troubles played out before monetising the position. By the time Future Retail's later collapse during the COVID era and the subsequent Reliance saga unfolded, Heritage had already substantially exited its stake, ultimately realising around ₹132 crore in cash proceeds.6

The intellectually honest framing is this: it was not a "good price" in any absolute sense. The Future Retail shares Heritage received were worth a fraction of the capital that had been deployed into the retail business over the preceding decade. But it was the right price, because the alternative was continuing to drip-feed losses into a business that the management team had finally concluded they could not win. The discipline was not in extracting maximum value — it was in admitting the trade was over.

That admission cleared the runway. The balance sheet was lighter. Management bandwidth was no longer being burned arguing about lease renewals in Whitefield. And — most importantly — the family had quietly demonstrated to itself that it was willing to cut a sacred cow. Which, as it turned out, was exactly the muscle they needed for what came next.

IV. M&A Masterstroke: The Reliance Dairy Acquisition

To understand the scale of what Heritage attempted in 2016–17, you have to first absorb the asymmetry of the matchup. On one side: Heritage, a roughly ₹1,800 crore South Indian dairy company with no real presence north of Maharashtra. On the other side: Reliance Retail Limited, a subsidiary of Mukesh Ambani's Reliance Industries, which had built a national dairy procurement and packaging network as a feeder for its retail stores under the "Dairy Life" డైరీ లైఫ్ label. By revenue, the Reliance dairy unit was doing approximately ₹553 crore — about a third the size of Heritage's dairy business — but it was spread across five additional states, including Punjab, Uttarakhand, Rajasthan, Haryana, and Maharashtra.[^8]

It was also, by all available reporting, bleeding money.

Strategic logic for Reliance to exit was straightforward. Ambani's group had decided that the future of consumer goods at Reliance ran through retail formats and digital — not through running perishable milk-collection routes in Bathinda. The dairy unit was a sub-scale orphan inside a much larger empire. For Heritage, the question was the mirror image: could a regional company digest a national footprint, in an asset class where every kilometre of cold chain matters, without choking on integration costs?

The deal closed on November 7, 2016 — coincidentally the same day the Future Retail demerger was announced, which itself signalled how tightly the family was sequencing the capital cycle. Heritage acquired the dairy business of Reliance Retail in a "slump sale" — an Indian legal structure where an entire undertaking is transferred as a going concern for a lump-sum consideration, without allocating value to individual assets.[^8] The reported consideration was modest by the standards of branded consumer M&A in India. While the contemporaneous press did not fully break out the exact number, contextual research notes pegged the headline value in the low triple-digit crores — a fraction of what comparable dairy infrastructure was changing hands at in private markets, where listed peers were trading on EBITDA multiples in the high teens to high twenties.7

The genius of the structure was that Heritage was not paying for a brand or a customer base. Reliance Dairy Life was not a beloved consumer label. What Heritage was buying was infrastructure. Bulk milk coolers in Punjab. Procurement relationships with farmers in Rajasthan. Processing capacity in Uttarakhand. A toehold in geographies where Heritage's southern brand could not be parachuted overnight, but where the procurement nodes could immediately be plugged into the existing Heritage operating system — the testing protocols, the payment cycles, the route planning, the cold-chain discipline.

The integration playbook, in retrospect, looks almost academic. Step one: standardise quality testing across the acquired centres to Heritage protocols, which immediately improved farmer trust in the previously chaotic Reliance system. Step two: rationalise overlapping logistics routes, killing duplicate tanker runs and renegotiating fuel contracts at combined volumes. Step three: keep the regional brand names — including "Dairy Life" in northern markets — to avoid a brand-recognition cliff in states where consumers had never heard of Heritage. Step four: very slowly, route higher-margin Value-Added Products (curd, paneer, lassi) into the new geographies using the inherited cold chain.

Did it work? In strict P&L terms, the acquired business stopped being a drag within a couple of years, but the more important answer is structural: Heritage went from a 4-state operator to a 9-state operator in a single transaction, at a fraction of the cost of building those nodes organically. For perspective, building a single bulk milk cooler with farmer onboarding takes 18 to 24 months of fieldwork in a new state. Heritage compressed roughly a decade of geographic expansion into one slump sale.

There is a subtler lesson too. The Reliance deal was a "complexity arbitrage" — Heritage was paying low because the buyer pool for an unbranded, sub-scale, money-losing dairy infrastructure asset was tiny. Most strategic players wanted brand, not pipes. Most financial buyers wanted growth, not turnaround. By being one of the few entities with both the operational competence to integrate the assets and the patience to absorb a couple of years of losses, Heritage created its own bid-ask spread. That is, almost word for word, the Buffett-style "circle of competence" trade — and a rare example in Indian listed mid-caps of management actually executing it.

What this said about management's instincts mattered more than the deal itself. The Reliance acquisition signalled to the market that this was a family willing to act asymmetrically — to sell when others were buying retail, and to buy infrastructure that no one else wanted. Which raises the question of who, exactly, that family is.

V. Current Management & Governance

The first time you meet Nara Bhuvaneswari at a Heritage Foods AGM, you might miss her. She is in her early seventies, dressed in a traditional cotton sari, and tends to speak softly in answers to shareholder questions. There is no Davos-circuit branding, no LinkedIn thought-leadership posts, no business-school case studies built around her. And yet she has, over more than three decades, quietly become one of the longest-serving female executives running a publicly listed Indian consumer staples company.

Bhuvaneswari's path to the corner office was not conventional. She is the wife of the founder, Chandrababu Naidu, and the daughter-in-law of the Telugu cinema legend and former Andhra Pradesh Chief Minister N. T. Rama Rao. When Naidu entered electoral politics full-time in the 1990s, she stepped into operational leadership of Heritage not as a placeholder but as a working executive — by all accounts spending substantial time on plant visits, farmer meetings, and supplier negotiations through the formative decade. Today she serves as Vice Chairperson and Managing Director, a position she has occupied through the company's most consequential capital decisions.[^10]

The promoter group as a whole owns approximately 41.3% of the equity, with Bhuvaneswari individually holding around 24% — a substantial personal economic interest that aligns her wealth far more tightly to Heritage's stock performance than to her cash compensation.[^10] That last point is worth dwelling on. Her managerial remuneration is, by design and disclosure, capped at 5% of the company's net profit, a structure that ties take-home pay directly to bottom-line outcomes rather than top-line growth, headcount, or vanity acquisitions.[^10] An Indian promoter-MD earning a salary linked to net profit, rather than to assets-under-management or revenue, is not as common as it should be. It is the kind of pay structure a passive investor wants to see, because it discourages exactly the empire-building behaviour that destroyed shareholder value at so many Indian conglomerates through the 2010s.

The transition to professional management has been the other quiet story. Bhuvaneswari's son, Nara Lokesh, is a non-executive director, but the day-to-day operating cadence runs through a deep bench of presidents and category heads. Names like J. Sambasiva Rao on the operations side, Srideep Kesavan on the CEO seat (appointed in 2023), and a layered finance and supply-chain leadership team have professionalised what was, two decades ago, very much a family-run operation.8 The split is clean: the family handles capital allocation, board-level strategy, and the long-arc M&A bets. The professionals run the trucks, the plants, the routes, the SKU rationalisations, and the working-capital cycle.

A genuinely interesting governance signal arrived in 2025, when the company restructured its joint venture with the French dairy group Novandie (the Mamie Yova brand) by taking its own stake to 94.4%. The decision-making process around that move — described later — was led by the professional management team with board oversight, not by a unilateral family edict. That is the kind of organisational sophistication you want to see before betting on the next leg of growth.

There are legitimate diligence asides too. Concentrated promoter ownership in a politically connected family is always a risk vector in India — the company's founder was Chief Minister of Andhra Pradesh through multiple terms, including the period from June 2024 onward, and political cycles in the Telugu states have historically correlated with sentiment around the brand in southern markets. Heritage has managed this exposure carefully, but it is the single biggest qualitative risk a long-term investor should keep in their working memory. It is also why the company's deliberate geographic diversification — out of an Andhra-Telangana concentration into northern India through the Reliance deal — was not just a growth move but a governance hedge.

That same hedging instinct — diversifying away from any one fragile dependency — also shows up in two businesses most investors do not even realise Heritage owns.

VI. The "Hidden" Businesses: Nutrivet & Green Energy

Drive out of Hyderabad on the Bangalore highway, past the IT parks of Gachibowli and into Mahbubnagar district, and you eventually arrive at a series of unmarked industrial sheds with sacks of feed pellets stacked outside. This is the operational heart of Heritage Nutrivet Limited, a subsidiary that almost no equity research report bothers to model with any depth, and which may turn out to be one of the most strategically important assets the parent company owns.

The premise of Heritage Nutrivet, or HNL, is elegant. A dairy farmer's two largest expenses are animal feed and veterinary care. If both of those are sold to her by the same company that buys her milk — on credit, deducted from her milk payments automatically — then her relationship to that company becomes structural rather than transactional. She is not just a supplier. She is a customer too. The English word for this is "vertical integration." The Telugu-speaking village agent who runs the chilling centre simply calls it ఆవు పశుగ్రాస సహాయం — cow-feed assistance.

HNL manufactures and distributes cattle feed, mineral mixtures, and nutritional supplements. The product is sold primarily to Heritage's own farmer network, although some volumes go to non-Heritage farmers in dairy-dense pockets. The economics work in three layers simultaneously. First, HNL captures a slice of the farmer's input wallet that would otherwise leak to local feed traders. Second, by improving the quality of the feed, Heritage indirectly improves the milk fat percentage and the daily yield per animal in its procurement zone — which means the parent collects more litres of higher-quality milk per route, lowering per-litre logistics costs. Third, the credit relationship — Nutrivet on credit, deducted from milk payments — raises the switching cost for the farmer dramatically. Walking away from Heritage means settling an outstanding feed account.

According to disclosed operational updates, HNL has been growing in the mid-teens to roughly 20% range year on year, with revenues in the multi-hundred crore range and expanding distribution into newer geographies as the dairy footprint widens.[^12] In a separate financial structuring, the international agribusiness platform Olam Agri took a 50% strategic stake in HNL in 2021, creating a joint venture that combined Heritage's farmer network with Olam's global commodity sourcing and animal-nutrition expertise.9 That deal is a quiet vote of confidence in the unit economics of the feed business from a serious global counterparty.

The second "hidden" lever is even less glamorous: electricity. Run a dairy plant for an hour and the single biggest variable you watch — after raw milk procurement — is your power bill. Pasteurisation, homogenisation, chilling, cold storage, packaging lines, and the entire cold-chain logistics network are electricity-intensive in a way that is almost invisible to the end consumer.

Heritage's response has been to build a captive renewable energy portfolio. As disclosed in its annual reports, the company operates roughly 11.7 MW of combined solar and wind capacity that feeds its own plants under captive consumption arrangements with state grids.1 The mechanism is straightforward: the company generates power at, say, ₹3-4 per unit equivalent and offsets grid drawdowns that would have cost it ₹6-8 per unit. The math, scaled across multiple plants, translates into single-digit-percent margin protection — small in any one year, but compounding meaningfully when input-cost cycles squeeze the rest of the P&L.

The strategic point is that neither Nutrivet nor the captive power business shows up on a casual scan of the company. There is no analyst day spent walking through them. They do not feature in the investor presentation hero charts. But they are precisely the kind of "boring infrastructure" assets that, over a 10-year holding period, separate a 12% compounder from an 18% compounder in a low-margin consumer category. They are also exactly the kind of vertical investments that get harder to replicate for any new entrant trying to disrupt the core franchise.

Together, these two units bookend the cost structure: Nutrivet defends the procurement cost (per litre paid to farmers), and renewable energy defends the conversion cost (per litre processed). Sandwiched between them is the future of the entire company — the part where the milk becomes something more.

VII. The Future: VAP & The French Connection

There is a small, almost cult-favourite product on Heritage's shelf called "Heritage Selectt Probiotic Curd." It comes in a transparent tub. It costs more than twice as much per gram as the loose curd that most South Indian households eat by the bowlful. And it sells, quietly but steadily, in the cold cabinets of urban modern-trade chains across Hyderabad, Bangalore, and Chennai. To understand the next chapter of this company, that tub is a more important artefact than any acquisition.

For most of Heritage's history, the business has been a "white milk" business. Pasteurised, toned, double-toned, full-cream — different fat percentages of essentially the same product, sold by the litre, with gross margins in the single digits and net margins in the very-low single digits. Branded liquid milk is, structurally, one of the worst gross-margin profiles in Indian consumer staples. Every player in the country, from Amul to హాట్సన్ Hatsun Agro to Dodla Dairy to Heritage, fights for the same urban consumer wallet at functionally identical retail prices, with most of the differentiation living in trust and on-time delivery.

VAP — Value-Added Products — is the way out. Curd పెరుగు, paneer పనీర్, ghee నెయ్యి, lassi, flavoured milk, ice cream, cheese, and stirred yoghurt all carry meaningfully higher gross margins than liquid milk, with margin differentials that can run roughly two times the liquid base depending on the product and the geography.3 More importantly, VAP demand is more elastic, more brand-sensitive, and more amenable to premiumisation. A consumer who is indifferent between two pouches of milk is genuinely willing to pay a premium for a probiotic curd with the right brand cue.

Heritage management has, for the last several reporting cycles, talked about steadily lifting VAP's share of revenue from the historical mid-twenties percent range toward a longer-term aspiration of 40%, with VAP growth running well ahead of liquid milk growth in most quarters.3 The transition is mechanically difficult because it requires capital — chilled-display cabinets in retail outlets, separate packaging lines in plants, additional cold-chain logistics — but the unit economics, once a product crosses minimum-efficient scale in a region, reward the patience.

Which brings us to the French connection. In 2019, Heritage entered into a 50-50 joint venture with Novandie SNC, a privately held French dairy specialist controlled by the Andros family, to launch stirred yoghurt and dairy desserts in India under a new brand: మామీ యోవా Mamie Yova.10 Novandie brought the recipe expertise — the company has decades of experience in European fruit yoghurts and dessert formats. Heritage brought the cold chain, the procurement, the distribution, and the regulatory navigation that any foreign entrant in Indian dairy would otherwise spend years on.

For five years, the JV existed as a slow-burn product line, building distribution in modern trade and selectively entering general trade in select metros. By all accounts, the early sales were promising but the structural problem with 50-50 JVs began to assert itself: decisions took longer than they needed to, capital deployment required dual approval, and brand-investment intensity was always a negotiation rather than a strategy. The Acquired.fm canon would have predicted this. Joint ventures in fast-moving consumer categories — particularly between a local operator and a foreign brand owner — almost always end one of two ways: either one party buys the other out, or the venture quietly fades.

Heritage chose to buy. In June 2025, the company announced that it would increase its stake in the Mamie Yova JV to approximately 94.4%, effectively taking operating control while leaving a minority interest with Novandie.11 The transaction was structured as a step-up acquisition rather than a full buyout, preserving the French partnership for ongoing recipe access and innovation pipeline while moving all material commercial decisions to Heritage's side of the table.

The strategic shift here is more important than the headline. By taking control, Heritage signalled that it intends to scale Mamie Yova as a national stirred-yoghurt brand in India — a category that essentially does not exist yet at scale. The Indian consumer eats curd in massive quantities, but western-style fruit yoghurt remains a rounding error in total dairy consumption. Heritage's bet is that demographic and income inflection points — younger urban consumers, fitness-led category creation, the modern-trade and quick-commerce distribution build-out — make the next decade the right window to plant the flag.

If it works, Mamie Yova becomes Heritage's first genuinely premium, pan-India consumer brand — a category-defining play rather than a category-following one. If it does not, Heritage will have spent a manageable amount of capital learning that the Indian consumer was not ready, and the underlying cold chain still finds productive use for the Heritage core curd portfolio. The downside is bounded; the upside is, for the first time in the company's history, structurally non-linear.

That is the conceptual transition the company has been making for nearly a decade now — from being a regional milk-distribution utility to being a focused, branded, value-added dairy platform. The playbook for how they got here is the next thing worth examining.

VIII. Playbook: Business & Strategy Lessons

If you had to teach Heritage's playbook as a single MBA case, the cleanest framing would be: "Three Decisions, Twenty Years."

The first decision was to concentrate. Most Indian family businesses, having achieved early success in one vertical, spent the 2000s sprawling outward into adjacencies that flattered the ego more than the balance sheet. Heritage spent the 2010s doing the opposite. The retail divestment, the agri-business rationalisation, the bakery wind-down — all of these were votes against optionality in favour of focus. The market took years to reward this. Heritage's stock spent extended periods trading flat or down while peers in different categories looked sexier. But the cumulative impact, by the 2020s, was a much higher-quality earnings stream, less working capital intensity, and a return-on-capital profile that finally started to look like a branded consumer business rather than a diversified holding company.

The "Pure Play" premium is a real phenomenon in Indian equity markets. Multiples expand when the story becomes legible. Heritage's transition from a "what does this company actually do" stock to a "this is a dairy compounder" stock unlocked institutional ownership that previously could not justify the position internally. There is a lesson here that goes beyond Heritage: in markets where retail flows are momentum-driven and institutional flows are mandate-driven, narrative clarity is itself a source of multiple expansion.

The second decision was to vertically integrate around procurement, not retail. The intuitive vertical-integration move for a dairy company is forward integration into stores and direct-to-consumer. Heritage tried that with Heritage Fresh and concluded it was the wrong direction. The right direction was backward — deeper into the farmer's economic life through Nutrivet (feed), through veterinary services, through credit. That backward integration is invisible to the consumer but enormously powerful in terms of switching costs on the supply side. Once a farmer is on Heritage Nutrivet on credit, with bi-weekly payment cycles for her milk, leaving Heritage to sell to a local cooperative is not a free decision.

In Indian dairy, the front end — the consumer-facing brand and the urban distribution — is competitive but contestable. The back end — collecting 1.5 million litres of perishable liquid daily across hundreds of thousands of farmers in nine states, with quality testing, payment processing, and cold-chain logistics that survive the Indian monsoon — is the impossible task. Heritage understood that the front-end glamour was a trap and that the back-end grind was the real moat. That is a deeply counter-cultural insight in a market that loves D2C decks.

The third decision was to balance asset-heavy and asset-light deliberately. Heritage owns the plants, the cold chain, the chilling centres, and the renewable energy assets. It does not own the farmers. That separation is the key to the operating model. By owning the conversion infrastructure but renting the raw-material origination through a decentralised farmer network, Heritage gets the cost advantages of scale on the heavy assets without taking on the political and operational nightmare of corporate farming.

This same dichotomy plays out in distribution. Heritage owns the cold-chain trucks and the master warehousing, but the last-mile delivery to households runs through a franchise model — the morning milkman is typically a small entrepreneur with a route, not a Heritage employee. The franchise pays Heritage a margin, takes the consumer-facing risk, and provides the daily customer relationship. Heritage retains the brand, the supply, the working capital, and the data on demand patterns.

The result is a company that, when read superficially, looks like a heavy-asset dairy company, but on closer inspection is something subtler: a chilled-logistics platform with a brand, a captive feed business, and an emerging premium dairy portfolio sitting on top of it. Each layer protects the margin of the one below. The procurement network and Nutrivet defend the input cost. The plants and renewable energy defend the conversion cost. The brand and the franchise distribution defend the realisation. VAP and Mamie Yova create the next leg of growth on top of the stable base.

It is not a glamorous business. It is, in fact, almost aggressively unglamorous. But the discipline of building each layer in the right order — and the patience to wait for the market to recognise it — is the real Acquired.fm-style lesson here.

IX. Analysis: 7 Powers & Porter's Five Forces

A formal Hamilton Helmer's framework applied to Heritage produces an interesting profile, because the company exhibits some Powers strongly, others weakly, and still others in an asymmetric way that matters more than the textbook scoring would suggest.

Scale Economies is the cleanest Power Heritage possesses. The cost per litre of running a procurement route — fuel, refrigeration, testing, payment processing — falls meaningfully as the volume on that route rises. A bulk milk cooler that is running at 60% capacity is functionally cheaper to operate per litre than one running at 30% capacity, because the marginal cost is electricity and labour spread over more units. Heritage's roughly 1.5 million litres per day of processing volume, spread across approximately 300,000 farmers, sits comfortably above the minimum-efficient scale in most of its operating geographies.1 A new entrant trying to enter, say, the Anantapur procurement zone would need to either match Heritage's existing route density (years of fieldwork) or operate at a structurally higher per-litre cost. That is a textbook scale economy.

Branding is real but bounded. In the Telugu states and parts of Karnataka and Tamil Nadu, "Heritage" carries the kind of trust signal that comes from 30 years of not being caught in an adulteration scandal during a market where adulteration scandals are common. Consumer brand strength of that kind translates into pricing power on incremental SKUs — a curd or a paneer launched under the Heritage label gets shelf adoption faster than a generic equivalent. North of the Vindhyas, brand recognition is much thinner, which is why the company kept the "Dairy Life" branding intact in northern markets after the Reliance acquisition. That asymmetry is worth keeping in mind: Heritage is a brand south of Maharashtra and a distribution operator north of it.

Switching Costs are essentially zero on the consumer side — a household can switch milk pouches tomorrow without any friction — but materially high on the supplier side. The combination of Nutrivet credit, daily payment cycles, and veterinary support creates a relationship cost for a farmer leaving Heritage. This inverted switching-cost dynamic, where the supplier is locked in more than the customer, is unusual in consumer staples and is one of the most underappreciated structural advantages the company has.

Cornered Resource, Counter-Positioning, Network Economies, and Process Power are all weak to negligible in Heritage's case. There is no proprietary genetic input. No structurally cheaper business model that incumbents cannot copy without cannibalising themselves. No two-sided network effect. The process expertise is real but not unique — every serious dairy operator in India has comparable testing protocols today.

So Heritage scores high on two Powers (Scale Economies and Supplier-Side Switching Costs), medium on one (Branding, regional), and low on the rest. That is a reasonable competitive profile for a regional consumer category leader, but not for a global-style moat.

Porter's Five Forces sharpens the picture further.

Rivalry is intense and unlikely to ease. Heritage competes with అమూల్ Amul (the Gujarat Cooperative Milk Marketing Federation's national colossus and the price-setter for the entire Indian dairy market), Hatsun Agro Products (Tamil Nadu's larger and more VAP-skewed listed peer), Dodla Dairy (Andhra-based, listed since 2021), and a long tail of state cooperatives — నందిని Nandini in Karnataka, ఆవిన్ Aavin in Tamil Nadu, విజయ Vijaya in Andhra-Telangana, మదర్ డైరీ Mother Dairy in the National Capital Region. Cooperatives compete on price; private players compete on brand and VAP mix. Heritage has historically positioned itself in the premium-to-mass-premium range within its geographies, which is the only profitable place to stand in the long run.

Bargaining Power of Suppliers is structurally medium-high in Indian dairy. Farmers can switch — at the margin and with friction — between Heritage, cooperatives, and informal traders depending on the price offered per litre of fat. Heritage's defence, as discussed, is to convert the transactional supplier relationship into an ecosystem relationship through Nutrivet and credit. This raises the effective switching cost without ever owning the farmer outright.

Bargaining Power of Buyers is bifurcated. Household consumers individually have near-zero power, but the aggregated channel — modern trade chains, quick-commerce platforms like Blinkit and Zepto, and B2B institutional buyers like hotel chains and ice cream brands — does have meaningful negotiating leverage on pricing and margins. As VAP scales and modern-trade penetration grows, this force will tighten over the next decade.

Threat of New Entrants is low for the procurement/processing backbone (a 5-to-10 year build with high failure rates) but moderate for branded VAP, where direct-to-consumer brands, foreign entrants, and well-capitalised cooperatives can credibly enter specific product categories. Heritage's first-mover position in geographies and its captive cold chain are partial defences.

Threat of Substitutes is the most interesting force to watch. Plant-based dairy alternatives — soy milk, oat milk, almond milk — are sub-scale in India today but growing in urban premium pockets. Cultural attachment to cow and buffalo milk remains very strong, but the next generation of urban Indian consumers may be the first to seriously substitute at the margin. Heritage's defence here is to build its own premium VAP and probiotic portfolio that protects the dairy share-of-throat against substitutes positioning themselves as "healthier" alternatives.

The Forces analysis lands roughly where intuition would suggest: a structurally medium-attractiveness industry where execution and scale concentration determine returns, with a long-tail substitution risk that is not urgent today but worth tracking.

X. Conclusion & The Bear/Bull Case

The bull case for Heritage Foods is the compounding bull case, not the multibagger bull case. It rests on four legs.

First, VAP contribution as a share of revenue moves from the mid-twenties percent range toward the company's articulated 40% aspiration over the next several years, driven by curd, paneer, ghee, ice cream, and the new Mamie Yova-led stirred yoghurt category.3 Each percentage point of VAP mix is a margin tailwind. Cumulatively, this is the single largest variable that determines whether Heritage compounds at 12% or at 18% over the next decade.

Second, Mamie Yova scales into a recognised national brand in the premium stirred-yoghurt and dairy-dessert segment, validating the post-2025 strategic decision to take majority control of the JV. The category is small today, but its analogue in other emerging markets (Indonesia, Brazil, Mexico) has scaled meaningfully over similar income-curve windows. If Heritage executes, it owns the category-defining brand in a new India-wide niche.

Third, Heritage Nutrivet continues to grow in the mid-teens to twenty-percent range, eventually generating enough cash flow and brand recognition to be considered as either a B2B animal nutrition business in its own right or — more strategically — to deepen the farmer ecosystem lock-in to a point where the entire procurement moat becomes effectively un-replicable.[^12]

Fourth, the renewable energy and operational efficiency programs continue to defend the conversion margin against electricity-tariff inflation and protect free cash flow.

If those four legs hold, Heritage becomes a meaningfully larger, more profitable, more focused company by the early 2030s — without ever needing a transformative acquisition or a discontinuous strategic pivot.

The bear case is also important, and it deserves equal seriousness.

The first bear risk is raw-material volatility. Cattle feed inputs — maize, soyabean meal, deoiled cakes — are commodities exposed to monsoon outcomes, global crop cycles, and government export policy. A bad fodder year, like the one the industry endured during the post-COVID inflation cycle, can compress dairy industry margins meaningfully. Heritage's vertical integration through Nutrivet provides partial protection but does not eliminate the exposure.

The second bear risk is regulatory and political. Milk procurement prices and consumer milk prices are quasi-regulated in many Indian states, sometimes informally through pressure on private players to "not raise prices" during sensitive electoral windows. Heritage's geographic concentration in the Telugu states historically created an additional political sensitivity given the founder's electoral career, although the geographic diversification of the post-Reliance era has reduced this concentration meaningfully.

The third bear risk is the substitution and modern-trade margin pressure that the Five Forces analysis identified. Quick-commerce platforms in particular have demonstrated, across multiple Indian consumer categories, an ability to compress brand pricing power once they reach a critical share of category sales. Dairy is not immune.

The fourth bear risk is execution risk on Mamie Yova specifically. New category creation in Indian consumer goods is hard. Many capable companies have spent years trying to scale categories — kombucha, oat milk, premium granola — that the Indian consumer ultimately rejected at scale. Heritage is making a thoughtful bet, but it is a bet.

The right way to track this story, for a long-term holder, is to focus on a small number of KPIs rather than the headline P&L.

The first KPI is VAP revenue mix percentage and its sequential trajectory. Whether VAP is growing meaningfully faster than liquid milk in any given reporting period is the single best signal of underlying margin direction. Heritage discloses this metric regularly enough to track.

The second KPI is procurement volume in litres per day, alongside farmer count and per-farmer yield. Procurement growth that comes from per-farmer yield expansion (driven by better Nutrivet penetration and better animal nutrition) is structurally higher-quality than procurement growth that comes from adding more farmers to the network, because yield improvements have higher unit economics and improve route density. A consistent multi-year improvement in litres-per-farmer is the deepest possible signal that the ecosystem strategy is working.

The third KPI worth tracking, even if less frequently disclosed, is Mamie Yova distribution depth and category share — measured by outlets carrying the brand and by the brand's share of the modern-trade stirred-yoghurt segment. This is the optionality KPI, and it indicates whether the post-2025 strategic bet is paying off.

Heritage sits in an unusual place in the Indian consumer staples landscape. It is not the largest. It is not the fastest-growing. It is not the most premium. But it may be the most disciplined — the company that, having tried diversification and decided it was a mistake, spent the next decade systematically cleaning up, going deep on one category, and quietly building the kind of unglamorous infrastructure that compounds when the spotlight is somewhere else. Whether that discipline gets fully rewarded depends on how the next decade of Indian dairy consumption unfolds, and on whether the family and the professional management team can keep choosing focus over sprawl when the next shiny opportunity appears in the boardroom.

In the pantheon of Indian listed dairy plays, Heritage is the focused regional compounder with a national footprint, a quiet governance structure, and a premium-VAP optionality bet. It is, in the truest sense, a pure play. And in a market that has historically penalised conglomerate complexity and rewarded category clarity, the next chapter of this story belongs to that quiet, daily ritual at 5:30 a.m. — the green-and-red pouch left at the door, the morning curd, and the stirred yoghurt that, in time, may join them on the same shelf.

References

References

-

BSE India — Heritage Foods Shareholding Pattern and Company Profile ↩

-

Heritage Foods exits Retail business to Future Retail — Business Standard, 2016-11-07 ↩

-

Heritage Foods Slump Sale Valuation Context — Nuvama Wealth Research ↩

-

Heritage Foods 32nd Annual Report FY 2023-24 — Board & Management Section ↩

-

Heritage Foods Investor Relations — Subsidiaries & Joint Ventures ↩

-

Heritage Foods Investor Presentation Q4 FY24 — Mamie Yova / Novandie JV slides ↩

-

Heritage Foods increases stake in Novandie JV to 94.4% — MarketScreener, 2025-06-16 ↩

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube