HDFC Bank: The Fortress of Indian Finance

I. Introduction and The Golden Standard

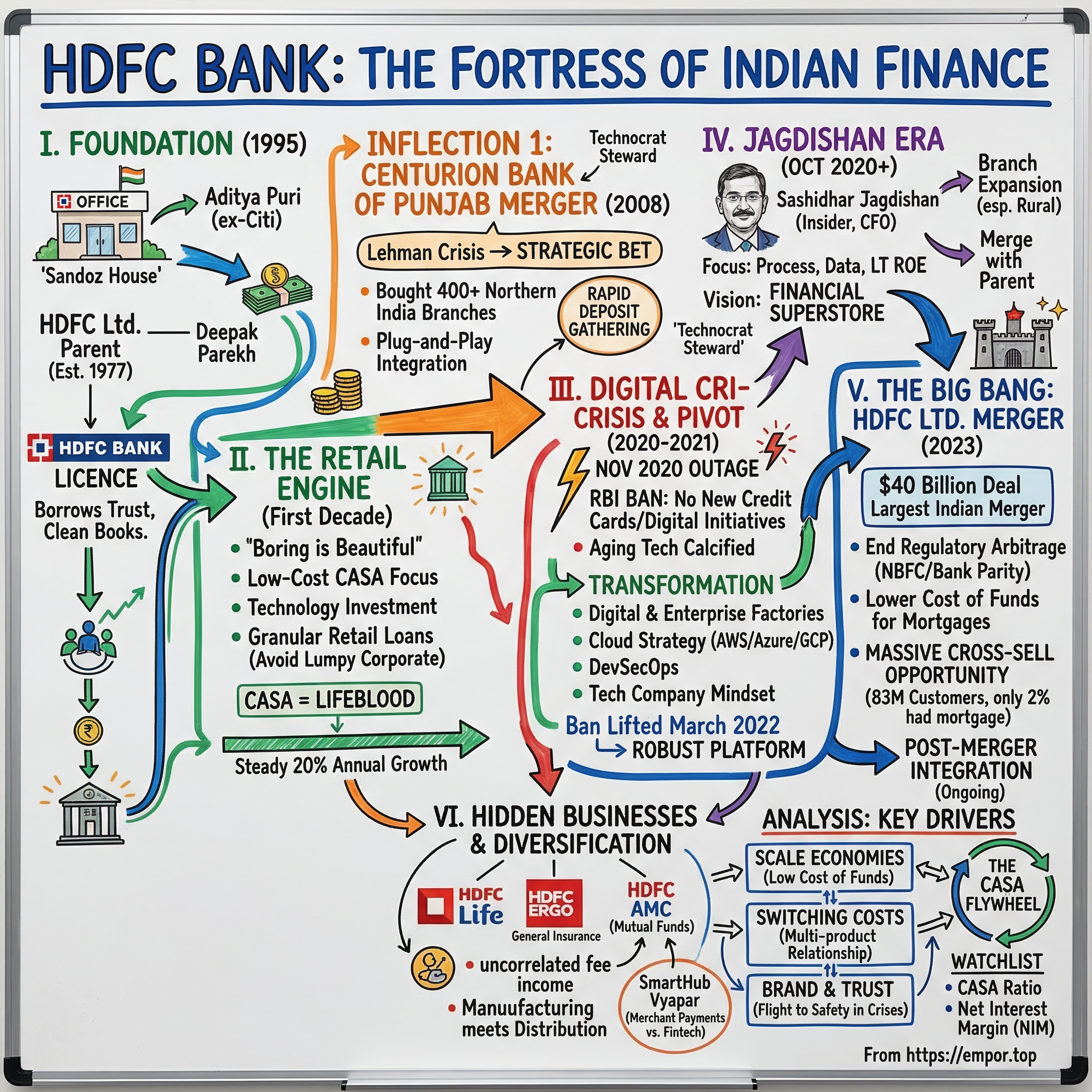

In January 1995, a tiny office on Sandoz House in Mumbai's Worli neighbourhood opened its doors for business. It had no sprawling branch network, no century-old legacy, no government backing. It had a borrowed brand name, a handful of employees, and a managing director who had just walked away from running Citibank's entire Malaysian operations. Thirty-one years later, that startup bank commands a market capitalization north of $170 billion, operates nearly 9,500 branches across India, employs over 214,000 people, and stands among the ten most valuable banks on the planet, having surpassed storied institutions like HSBC, Goldman Sachs, and Morgan Stanley along the way.

HDFC Bank is, at first glance, one of the most boring companies in financial services. It does not trade exotic derivatives. It does not chase moonshot fintech bets. It does not make headlines for billion-dollar write-offs. What it does, quarter after quarter, year after year, for three decades running, is compound. Twenty percent earnings growth. Low single-digit bad loans. A return on equity that most global banks would frame and hang on the wall. And it does this in India, a country where banking crises have toppled institutions with regularity, where state-owned banks sit on mountains of soured loans, and where a new fintech disruptor seems to emerge every month.

The thesis is deceptively simple: HDFC Bank is not really a bank. It is a low-cost-of-funds machine disguised as a technology company, wrapped in the most trusted consumer brand in Indian financial services. Its competitive advantage comes not from brilliant trading desks or complex financial engineering, but from something far more mundane and far more durable: the ability to attract and retain cheap deposits at a scale that no competitor can match.

This is the story of how that machine was built, from the liberalization-era license to the retail banking flywheel, from the "boring is beautiful" philosophy to a wrenching digital crisis that nearly derailed it, and finally to the largest merger in Indian corporate history, a $40 billion deal that fused parent and child into a financial colossus. It is a story about saying no to temptation, about the compounding power of consistency, and about what happens when an emerging-market institution decides it would rather be a fortress than a rocket ship.

II. Founding Context: The Parent and The License

To understand HDFC Bank, you have to start with HDFC Ltd, its parent, and a man named Hasmukhbhai Parekh. In 1977, when India's financial system was dominated by state-run behemoths and the very concept of a private housing mortgage was virtually alien, Parekh did something audacious. At sixty-six years old, having already completed a distinguished career at ICICI, he founded the Housing Development Finance Corporation, India's first specialized mortgage lender. The idea was simple: middle-class Indians deserved access to professional, transparent home loans. At the time, buying a house in India meant navigating a labyrinth of government agencies or borrowing from informal money lenders at exorbitant rates. HDFC Ltd. changed that.

Over the next decade and a half, Hasmukhbhai's nephew Deepak Parekh took the reins and transformed HDFC Ltd. from a niche mortgage shop into India's leading housing finance institution. Deepak Parekh, a chartered accountant who had cut his teeth at Ernst & Young, Grindlays Bank, and JP Morgan before joining his uncle's venture, possessed a rare combination of financial conservatism and institutional ambition. Under his stewardship, HDFC Ltd. built something invaluable: a reputation for clean books, professional management, and unimpeachable credit quality. In a country where financial institutions were routinely plagued by political interference and crony lending, HDFC Ltd. stood apart. That reputation would prove to be the single most important asset the parent could bequeath to its offspring.

The opportunity came in 1993 when Prime Minister P.V. Narasimha Rao's government, continuing the sweeping economic reforms that began in 1991, released guidelines for licensing new private-sector banks. India's banking landscape at the time was a study in stagnation. State-owned banks controlled the overwhelming majority of deposits and loans. Service was abysmal, technology was nonexistent, and non-performing assets were already festering beneath layers of creative accounting. The government recognized that competition from well-capitalized private players could shake the system into modernity.

HDFC Ltd. was among the first to receive an in-principle approval from the Reserve Bank of India. The license was a golden ticket, but what mattered more was what HDFC chose to do with it. While other new licensees like ICICI Bank and UTI Bank (later Axis Bank) pursued aggressive corporate lending strategies to grow quickly, HDFC Bank made a different bet from day one. The strategy was anchored in three principles that would define the institution for decades: maintain a clean balance sheet at all costs, build a dominant retail franchise through CASA deposits, and invest in technology before your competitors realize they need to.

CASA, or Current Account Savings Account deposits, is the lifeblood of any bank's profitability. These are the funds that customers park in their checking and savings accounts, typically earning minimal or zero interest. For the bank, CASA deposits represent the cheapest possible source of funding, far less expensive than wholesale borrowing or term deposits. The bank that wins the CASA war wins the profitability war, because it can lend at competitive rates while maintaining wider margins than rivals who depend on costlier funding. HDFC Bank understood this from its very first day of operations, and building CASA dominance became an obsession that never wavered.

To lead this venture, Deepak Parekh recruited Aditya Puri, a decision that ranks among the most consequential executive appointments in Indian business history. But the man Parekh chose to build his bank was not sitting in some corner office in Mumbai. He was running Citibank Malaysia, eight thousand kilometres away, living the comfortable life of a senior multinational banker.

III. The First Decade: Building the Retail Engine

Aditya Puri was, by any measure, an unusual choice to run a startup bank. Born in 1950, educated at Punjab University in Chandigarh, Puri had spent twenty-one years at Citibank, working across nineteen countries. He had built a reputation as a fiercely competitive commercial banker with a gift for simplifying complexity and an almost allergic reaction to unnecessary risk. Colleagues from his Citibank days described him as blunt, occasionally abrasive, and deeply impatient with bureaucratic nonsense. He smoked cigars, drove German cars, and had zero interest in the kind of political glad-handing that defined Indian banking culture. When Deepak Parekh approached him about leaving Citibank to build a bank from scratch in Mumbai, Puri's friends thought he was mad. He was earning a multinational salary, had a corner office in Kuala Lumpur, and was on track for even bigger roles within the Citi empire. Why would he give that up to start over?

Puri later recounted that the decision came down to a simple calculation. He was forty-four years old, and the Indian banking market was about to be thrown open for the first time in a generation. The opportunity to build something from scratch, to apply everything he had learned at Citibank about technology, risk management, and retail banking to a market of nearly a billion people, was irresistible. He took a pay cut, moved his family back to India, and showed up at a borrowed office in Mumbai with a mandate to build the best bank in the country.

What followed was a masterclass in disciplined execution. While other new private banks were chasing large corporate accounts and infrastructure projects to grow their loan books quickly, Puri focused relentlessly on retail banking. The logic was characteristically straightforward. Corporate loans were lumpy, concentrated, and vulnerable to economic cycles. A single bad infrastructure loan could wipe out years of profits. Retail loans, auto loans, personal loans, credit cards, home loans, were small, diversified, and granular. If one customer defaulted, it barely registered. If a thousand customers defaulted, the losses were still manageable. The strategy was slower, less glamorous, and required enormous upfront investment in technology and branch networks. But it was also far more resilient.

Puri installed technology infrastructure that was, for India in the mid-1990s, almost absurdly advanced. While state-owned banks were still processing transactions on paper ledgers, HDFC Bank deployed core banking software that allowed real-time transaction processing across its entire network. Every branch was connected. Every account was updated instantly. For customers accustomed to waiting days for a check to clear, the experience was transformative. Puri understood something that many of his contemporaries missed: in a market where government banks treated customers as supplicants, simply providing decent service was a massive competitive advantage.

The first major inflection point came in February 2000, when HDFC Bank merged with Times Bank, a smaller private bank promoted by the Bennett Coleman media group. This was India's first-ever voluntary merger between two private banks, and it set the template for HDFC Bank's approach to acquisitions. Times Bank was small, but it had a clean balance sheet and a valuable urban branch network. HDFC Bank shareholders received one share for every 5.75 Times Bank shares, a premium that reflected the quality of what was being acquired. The integration was swift, surgical, and remarkably smooth. Puri's team had studied how Citibank executed acquisitions globally, and they applied those lessons to the Indian context. Within months, Times Bank's branches were fully integrated into HDFC Bank's technology platform, its customers were migrated, and the combined entity was operating as a single, seamless unit.

Through the early 2000s, HDFC Bank grew at a consistent clip of roughly 20 percent annually, a rate that was neither flashy enough to attract accusations of recklessness nor slow enough to disappoint investors. Puri called this the "boring is beautiful" philosophy, and it became the defining ethos of the institution. The bank would not chase growth for growth's sake. It would not lend to politically connected infrastructure projects. It would not compromise on asset quality to hit quarterly targets. It would simply do the basics extraordinarily well, day after day, and let compounding do the rest. When other private banks were extending large corporate loans to steel mills and power plants during the mid-2000s credit boom, HDFC Bank was busy opening branches in tier-two cities and signing up salaried professionals for savings accounts. The discipline would prove prescient. By the time India's NPA crisis erupted a decade later, those aggressive lenders were drowning in bad debts while HDFC Bank sailed through virtually unscathed.

For investors, the lesson from this first decade was unmistakable. In banking, the most valuable quality is not speed, innovation, or even brilliance. It is the ability to say no. HDFC Bank's willingness to walk away from risky but lucrative deals, to sacrifice short-term growth for long-term resilience, created a flywheel of trust, cheap deposits, superior margins, and consistent returns that proved nearly impossible for competitors to replicate.

IV. Inflection Point 1: The Centurion Bank of Punjab Merger

September 2008. Lehman Brothers had just collapsed, global credit markets were seizing up, and banks around the world were fighting for survival. In India, the stock market had cratered, liquidity was evaporating, and the very word "acquisition" had become synonymous with recklessness. It was precisely at this moment that Aditya Puri decided to make the biggest bet of his career.

Centurion Bank of Punjab was, on paper, a middling institution. It had been cobbled together from multiple mergers, first Bank of Punjab merging with Centurion Bank in 2005, and it carried a somewhat chaotic operational legacy. Its financials were unremarkable. Its brand was regional. But it possessed something that HDFC Bank desperately wanted: four hundred branches spread across Northern India, particularly in Punjab, Haryana, and Kerala, states where HDFC Bank had thin presence. In a country where physical branches still mattered enormously for gathering retail deposits, especially in semi-urban and rural areas, those branches represented years of organic expansion compressed into a single transaction.

The deal was structured as an all-stock merger, with Centurion Bank of Punjab shareholders receiving one HDFC Bank share for every twenty-nine CBoP shares. The implied valuation worked out to approximately four times book value, which sent analysts into a minor frenzy. At the time, Indian banking deals were typically priced at two to two and a half times book. Critics argued that Puri was overpaying, that the premium was unjustifiable for a bank with CBoP's modest asset quality and inconsistent profitability.

But Puri was not buying a balance sheet. He was buying distribution. The four hundred-plus branches gave HDFC Bank overnight access to deposit pools in markets where building from scratch would have taken five to seven years. In banking, time is not just money; time is the difference between capturing a generation of customers and watching a competitor lock them in. Every year that HDFC Bank did not have branches in Punjab was a year that State Bank of India and Punjab National Bank were deepening their relationships with millions of potential CASA customers.

The integration was where HDFC Bank truly demonstrated its institutional capability. Drawing on the playbook developed during the Times Bank merger, Puri's team executed what they called a "plug-and-play" approach. CBoP's branches were migrated to HDFC Bank's technology platform within months. Redundant systems were eliminated. Staff were retrained. The CBoP brand was retired and replaced with HDFC Bank's branding. Critically, the process was executed without significant customer attrition. The deposit base was not just retained but grew as former CBoP customers, now under the HDFC Bank umbrella, gained access to a wider product suite and a more reliable technology platform.

Within two years, the CBoP branches were contributing to HDFC Bank's CASA ratio at levels comparable to organically grown branches. The acquisition premium that analysts had lamented was effectively amortized through deposit growth and cross-selling revenue. More importantly, the Northern India footprint gave HDFC Bank a truly national presence for the first time, enabling it to offer nationwide salary account packages to large corporations, a key driver of CASA growth.

The CBoP merger also revealed something important about HDFC Bank's organizational DNA: its ability to absorb and integrate acquisitions without losing operational focus. Many banks stumble after major mergers, distracted by cultural clashes, technology migration headaches, and talent attrition. HDFC Bank treated integration as a core competency, not an afterthought. This capability would prove essential when, fifteen years later, the bank would face an integration challenge orders of magnitude more complex.

The broader context made the CBoP deal look even smarter in retrospect. While HDFC Bank was using the 2008 crisis to expand its franchise at a reasonable price, other Indian banks were beginning to accumulate the infrastructure and corporate loans that would eventually metastasize into the worst NPA crisis in Indian banking history. By 2015, when the Reserve Bank of India's Asset Quality Review forced banks to confront the true scale of their bad debts, the industry's gross NPA ratio would climb toward 11.5 percent. HDFC Bank's? Barely above one percent. The divergence was not luck. It was the accumulated result of twenty years of saying no.

V. Inflection Point 2: The Digital Crisis and Pivot

For two decades, HDFC Bank had cultivated an image of operational excellence, a bank that simply did not make mistakes. Customers trusted it with their money because things worked. ATMs dispensed cash. Mobile apps processed transfers. Credit card transactions cleared without hiccups. This reputation for reliability was, in many ways, as valuable as the bank's financial metrics, because in Indian banking, trust is the ultimate currency.

Then came November 21, 2020, and the carefully constructed image cracked.

A power failure at HDFC Bank's primary data center cascaded into a nationwide outage. Internet banking went dark. Mobile banking crashed. Payment systems froze. Millions of customers, many of whom were mid-transaction, found themselves locked out of their accounts. For a country that was rapidly shifting to digital payments during the COVID-19 pandemic, when physical branch visits were impossible and digital banking was not a convenience but a necessity, the outage was more than an inconvenience. It was a breach of the implicit promise that HDFC Bank had been making for twenty-six years.

What made it worse was that this was not an isolated incident. The November outage was merely the most visible in a series of technology failures that had plagued the bank over the preceding two years. Multiple outages had hit internet banking, mobile banking, and payment systems, each one chipping away at the narrative of infallibility. The Reserve Bank of India, India's banking regulator, had been watching with growing impatience.

On December 2, 2020, the RBI brought down the hammer. In an unprecedented action against India's most valuable private bank, the regulator ordered HDFC Bank to immediately halt all new credit card issuances and freeze all new digital business initiatives under its Digital 2.0 program. For a bank that was adding roughly 400,000 new credit cards per month and had 15 million cards in circulation, the most in the Indian market, this was not a slap on the wrist. It was a body blow.

The irony was sharp. HDFC Bank had built its early competitive advantage on technology, deploying core banking software when state-owned banks were still using paper ledgers. But somewhere along the way, the bank had allowed its technology infrastructure to calcify. The very systems that had been cutting-edge in 1995 had become legacy burdens by 2020. The bank had layered digital products on top of aging monolithic architectures, piling features onto foundations that were never designed to support them. It was as if a racing team had spent twenty years bolting upgrades onto the same chassis without ever building a new car.

The root cause was cultural as much as technical. HDFC Bank had excelled at "branch banking," the art of running a physical distribution network with military precision. But branch banking excellence did not translate to cloud excellence. The skills, mindsets, and organizational structures that made you great at managing thousands of physical locations were fundamentally different from those required to build resilient, scalable digital infrastructure. The bank had underinvested in technology modernization because the branches were still printing money. Why fix what wasn't broken? The outages answered that question definitively.

What followed was a forced transformation that, in hindsight, may have been the best thing that ever happened to HDFC Bank. Unable to issue new credit cards or launch digital products, the bank turned inward with an intensity that peacetime complacency would never have permitted. In June 2021, the bank announced the creation of two new units: a Digital Factory and an Enterprise Factory. The Digital Factory would build new digital products using modern technology stacks, cloud-native infrastructure, APIs, and microservices. The Enterprise Factory would overhaul the bank's core IT infrastructure, migrating from monolithic legacy systems to a distributed, resilient architecture.

The bank adopted a hybrid-cloud strategy, partnering with Amazon Web Services, Microsoft Azure, and Google Cloud Platform. It implemented DevSecOps practices, bringing development, security, and operations together in a way that prioritized system resilience alongside feature velocity. It hired hundreds of engineers, data scientists, and cloud architects, many of them from India's vibrant tech startup ecosystem rather than traditional banking backgrounds. The transformation was not merely technical; it was organizational. The bank was learning to think like a technology company, to treat uptime as a product feature rather than an operational afterthought.

The RBI lifted the credit card ban in March 2022, roughly fifteen months after imposing it. By that point, HDFC Bank had laid the groundwork for a technology platform that was arguably more robust and modern than what it would have built had the crisis never occurred. The bank resumed credit card issuance and quickly regained its position as India's largest credit card issuer by volume. More importantly, the technology transformation positioned it to compete effectively against the fintech insurgents, PhonePe, Paytm, Google Pay, and others, that were reshaping Indian financial services through the Unified Payments Interface, India's revolutionary real-time payments system.

The digital crisis taught HDFC Bank a lesson that applies well beyond banking: operational excellence is not a permanent state. It is a practice that must be continuously reinvested in, especially as the underlying technology landscape shifts. The bank that had built its reputation on being boringly reliable had been reminded, painfully and publicly, that boring is only beautiful when the plumbing actually works.

VI. Current Management: The Jagdishan Era

October 27, 2020. Aditya Puri's last day as managing director and CEO of HDFC Bank. After twenty-six years of unbroken leadership, the longest tenure of any private bank CEO in Indian history, the man who had built the institution from a blank piece of paper was handing over the keys. The succession question had hung over the bank for years, the subject of endless speculation in Mumbai's financial circles. Who could possibly follow a legend?

The answer was Sashidhar Jagdishan, and the choice said everything about what HDFC Bank valued. Jagdishan was not a charismatic dealmaker or a magnetic public speaker. He was an insider, a chartered accountant with a master's degree in economics from the University of Sheffield, who had joined HDFC Bank in 1996, barely a year after it commenced operations. He started as a manager in the finance department and over twenty-four years worked his way up through the organization, serving as CFO and heading the bank's strategic change initiatives before being tapped as Puri's successor.

If Puri was the founder-warrior, the bold personality who willed the institution into existence through sheer force of conviction, Jagdishan was the technocrat-steward, the quiet insider who understood the machinery so intimately that he could tune it without taking it apart. His appointment signaled that HDFC Bank's board believed the institution had matured beyond the founder stage. It no longer needed a visionary builder. It needed a disciplined operator who could manage the enormous complexity of what the bank had become while navigating the existential challenges ahead: the technology overhaul, the regulatory fallout, and the looming mega-merger with the parent company.

Jagdishan inherited the CEO role at perhaps the most turbulent moment in the bank's history. The RBI had just imposed the credit card and digital ban. The COVID-19 pandemic was raging. And the bank's technology reputation lay in tatters. A lesser leader might have been overwhelmed. Jagdishan's response was characteristically methodical. He did not make grand public statements or promise revolutionary change. He assembled teams, set clear priorities, and executed the technology transformation described earlier with a rigor that reflected his finance and operations background.

His management style differs markedly from Puri's. Where Puri led through personal authority and a commanding physical presence, one former executive described him as someone who could fill a boardroom with his voice alone, Jagdishan leads through process, data, and quiet persistence. His incentive structure reflects this orientation. Rather than being evaluated primarily on loan book growth or revenue targets, Jagdishan's compensation is weighted toward long-term return on equity, digital transformation milestones, and customer satisfaction metrics. This is not a CEO optimizing for the next quarter's earnings call. It is a CEO optimizing for the next decade's competitive position.

Under his leadership, HDFC Bank has expanded its branch network from roughly 5,400 when he took over to more than 9,400 by early 2026, with a heavy emphasis on semi-urban and rural locations. He has articulated a vision of transforming HDFC Bank from a "lender" into a "financial superstore," a platform where customers access banking, insurance, investments, and payments through a single integrated relationship. The concept is not new, other banks have used similar language, but Jagdishan has the advantage of the HDFC Ltd. merger, which brought an entire ecosystem of financial services subsidiaries under the bank's roof.

The succession from Puri to Jagdishan has been, by any measure, remarkably smooth. The bank's stock price has performed well, asset quality has remained stable, and the post-merger integration has proceeded without major disruptions. For investors in founder-led companies, this transition offers a case study in how to move from charismatic leadership to institutional management without losing the cultural DNA that made the organization successful in the first place. The answer, it turns out, is to promote someone who absorbed that DNA over twenty-four years of service, someone who does not need to reinvent the culture because he is a product of it.

VII. The Big Bang: The HDFC Ltd. Merger

April 4, 2022. HDFC Bank and HDFC Ltd. jointly announced what would become the largest merger in Indian corporate history: the parent, HDFC Ltd., India's dominant housing finance company, would be absorbed into its child, HDFC Bank. The deal was valued at approximately $40 billion, and when it closed on July 1, 2023, it created a financial institution with a combined asset base of roughly 18 lakh crore rupees, approximately $220 billion, making it the second largest bank in India behind only the state-owned colossus, State Bank of India.

The mechanics of the deal were elegantly simple. For every twenty-five shares of HDFC Ltd. that investors held, they received forty-two shares of HDFC Bank, a swap ratio of 1.68. The ratio was widely regarded as fair to slightly favorable for bank shareholders, effectively pricing HDFC Ltd.'s massive mortgage portfolio at a discount to its standalone value while recognizing the strategic premium of the combination. HDFC Bank allotted over 311 crore new shares to former HDFC Ltd. shareholders, who ended up holding roughly 41 percent of the combined entity. Post-merger, the bank had no identified promoter in the traditional Indian corporate governance sense, making it one of the most widely held financial institutions in the country.

But why merge? For nearly three decades, the HDFC group had operated with a deliberate separation between the bank and the housing finance company. HDFC Ltd. raised money through bonds and wholesale markets, lending it out as mortgages, while HDFC Bank gathered retail deposits and made shorter-term consumer and commercial loans. The structure worked because the two entities faced different regulatory regimes. As a non-banking financial company, HDFC Ltd. operated with lighter regulatory burdens than a commercial bank: no cash reserve ratio requirements, no statutory liquidity ratio mandates, and less stringent capital adequacy norms. This regulatory arbitrage, the gap between what banks had to comply with and what NBFCs could get away with, made the separation profitable.

Then the arbitrage disappeared. The 2018 IL&FS crisis, which exposed the fragility of India's shadow banking system, prompted the Reserve Bank of India to fundamentally rethink how it regulated non-bank financial institutions. In 2021, the RBI introduced the Scale-Based Regulation framework, which brought large NBFCs under essentially the same regulatory requirements as commercial banks. Suddenly, HDFC Ltd. faced bank-like compliance costs without bank-like access to cheap CASA deposits. The math that had justified the separation for three decades no longer worked.

Deepak Parekh, HDFC Ltd.'s chairman, was candid about the logic. Regulatory harmonization between banks and NBFCs had, in his words, "considerably reduced the regulatory arbitrage." Maintaining two separate entities with their own compliance functions, technology platforms, and management teams had become an unnecessary cost. More importantly, the bank needed a larger balance sheet to participate in India's massive infrastructure and housing buildout. With the Indian government targeting 500 million urban residents by 2030 and pushing affordable housing as a national priority, the mortgage opportunity was simply too large to fund through wholesale borrowing alone. HDFC Bank's ocean of CASA deposits could fund mortgages at a cost of capital that HDFC Ltd., relying on bonds and bank borrowings, could never match.

But the financial engineering was only half the story. The real prize was the cross-sell opportunity. At the time of the merger announcement, only about 2 percent of HDFC Bank's customer base had a mortgage from HDFC Ltd. An additional 5 percent had housing loans from other lenders. That meant 93 percent of the bank's roughly 83 million customers had no home loan at all. For a bank that had spent three decades perfecting the art of cross-selling financial products to its existing customer base, this was an enormous untapped reservoir. Every HDFC Ltd. mortgage customer who became a full HDFC Bank relationship, with a savings account, credit card, insurance policy, and mutual fund investment, represented a dramatic increase in lifetime customer value.

The integration, still ongoing as of early 2026, has progressed methodically. The bank has been working to bring down its credit-to-deposit ratio, which spiked after absorbing HDFC Ltd.'s large mortgage portfolio, back toward pre-merger levels. This requires growing deposits faster than loans, a challenge that explains the aggressive branch expansion into semi-urban and rural India. The early signs are encouraging: HDFC Bank's deposit growth has been robust, and the mortgage portfolio has provided a steady stream of high-quality assets with low default rates.

For the Indian financial system, the merger represents a structural shift. It created a universal banking platform that can originate a home loan, fund it with retail deposits, cross-sell insurance and investments on the same relationship, and manage the entire lifecycle through a single technology platform. The competitive implications are significant. Smaller housing finance companies that once competed with HDFC Ltd. on roughly equal regulatory footing now face a rival with access to the cheapest deposits in the Indian private banking system. The moat around HDFC Bank's franchise deepened considerably.

VIII. Hidden Businesses and Segment Analysis

When most investors think of HDFC Bank, they think of its core banking operations: deposits, loans, and the spread between them. But beneath the headline numbers sits a constellation of subsidiaries and strategic initiatives that collectively represent one of the most diversified financial services ecosystems in emerging markets.

Start with insurance. HDFC Life Insurance Company is one of India's leading life insurers, with a product portfolio spanning over sixty offerings and a market position that places it consistently among the top three private life insurers by premium income. The company completed a landmark acquisition of Exide Life Insurance, the first-ever merger and acquisition in the Indian life insurance sector, further consolidating its position. HDFC ERGO General Insurance, originally a joint venture with Munich Re's ERGO International and now a subsidiary of HDFC Bank, offers the full spectrum of general insurance products: motor, health, travel, home, property, marine, and liability coverage. Together, these insurance arms generate substantial fee income for the group without exposing it to credit risk. Insurance distribution through the bank's branch network is a classic "manufacturing meets distribution" model: the bank provides the customer access, the insurance subsidiaries provide the product, and the group captures margins at both ends.

Then there is HDFC Asset Management Company, one of India's largest mutual fund managers by average assets under management. In a country where mutual fund penetration is still in its early innings, with household savings gradually shifting from gold and real estate toward financial assets, HDFC AMC sits at the intersection of India's most powerful secular trend. The mutual fund business generates management fees that are entirely uncorrelated with the bank's credit cycle, providing a valuable earnings diversifier.

The combined value of these subsidiaries is substantial, and it is worth noting that each operates as a publicly listed entity in its own right. HDFC Life and HDFC AMC trade independently on Indian stock exchanges, with their own shareholder bases and governance structures. This visibility provides a natural market check on value creation and management accountability.

Beyond the established subsidiaries, HDFC Bank is investing heavily in new growth vectors. SmartHub Vyapar, the bank's merchant payment platform, serves over 1.6 million merchants and represents the bank's direct response to the fintech disruption reshaping Indian commerce. Rather than ceding the merchant relationship to PhonePe, Google Pay, or Paytm, HDFC Bank is using its existing corporate and SME banking relationships as an on-ramp to build a comprehensive merchant ecosystem that integrates payments, lending, and business analytics. The bank has forged partnerships with fintech firms like KreditPe, ToneTag, and PayU to layer innovative payment solutions on top of its banking infrastructure.

The most strategically consequential initiative, however, may be the least visible. HDFC Bank's Semi-Urban and Rural, or SURU, expansion is arguably the hidden engine that will power the bank's next decade of growth. The bank has been adding branches in rural and semi-urban India at an aggressive pace, pushing its presence to over 4,600 SURU locations covering nearly two-thirds of India's population. These branches are currently loss-making as they build their deposit base and customer relationships, which means they depress near-term profitability. But the long-term logic is compelling. Rural India is where the cheapest deposits live: small savings accounts held by farmers, shopkeepers, and local entrepreneurs who have limited alternatives and high loyalty. As these branches mature over three to five years and their CASA balances grow, they will provide a fresh wave of low-cost funding that competitors who only operate in metro cities cannot access.

The bank has tailored products for this market, including the Pragati Savings Account launched in late 2024, which offers features specifically designed for farmers and rural communities, including partnerships to improve agricultural productivity and credit access. This is not charity; it is strategic customer acquisition at the bottom of the pyramid, where relationship stickiness is highest and lifetime value, once established, is remarkable.

The segment mix of the loan book tells its own story. HDFC Bank has been steadily shifting from wholesale (corporate) lending toward retail and SME lending, where margins are higher and credit risk is more granular. The mortgage portfolio inherited from HDFC Ltd. now sits at the core of the retail franchise, surrounded by auto loans, personal loans, credit cards, and business banking. This diversification means that no single sector or borrower concentration can threaten the bank's earnings stability. It is, in effect, a financial version of the "don't put all your eggs in one basket" principle, executed at continental scale.

IX. Analysis: Porter's Five Forces and Hamilton's Seven Powers

To understand why HDFC Bank commands a persistent premium valuation, it helps to step back from the financial statements and examine the structural forces that define its competitive position.

Switching Costs: The Primary Power. Once a customer establishes their salary account, savings account, credit card, auto loan, home loan, insurance policies, and mutual fund investments with HDFC Bank, the friction involved in moving to a competitor becomes immense. It is not just the paperwork, though there is plenty of that. It is the accumulated convenience: the auto-pay mandates linked to the savings account, the credit card reward points, the pre-approved loan offers calibrated to years of transaction history, the UPI payment links embedded in dozens of apps and merchant relationships. Each additional product deepens the switching cost exponentially. The bank understands this and optimizes ruthlessly for "products per customer" rather than raw customer count. This is why the merger with HDFC Ltd. was so strategically powerful: it added the ultimate high-switching-cost product, a mortgage with a twenty to thirty year tenure, to the cross-sell arsenal.

Scale Economies. HDFC Bank's cost of funds, the blended interest rate it pays on its deposits and borrowings, is structurally lower than virtually every private bank competitor in India. This advantage stems directly from its massive CASA base, which provides funding at near-zero marginal cost. A smaller private bank that relies more heavily on term deposits or wholesale borrowing pays significantly more for every rupee it lends. This cost advantage allows HDFC Bank to underprice competitors on loan rates while simultaneously maintaining higher net interest margins. The scale advantage compounds over time: more branches mean more CASA deposits, which mean lower funding costs, which mean more competitive loan pricing, which attract more customers, who open more CASA accounts. It is a flywheel that accelerates as the bank grows larger, the opposite of the diminishing returns that plague most industries.

Brand and Trust: The Cornered Resource. In Indian banking, trust is not an abstract marketing concept. It is a survival mechanism. When Punjab and Maharashtra Cooperative Bank collapsed in 2019, wiping out depositors' savings, and when Yes Bank teetered on the brink of failure in early 2020, requiring a government-orchestrated rescue, the reaction among Indian depositors was visceral and immediate. Money flowed out of smaller and weaker banks and into institutions perceived as safe. HDFC Bank was a primary beneficiary of this flight to safety, seeing deposit growth accelerate precisely when the broader system was under stress. This dynamic, where crises actually strengthen HDFC Bank's competitive position by driving deposits toward it, is a powerful form of what Hamilton Helmer calls a "cornered resource." The bank's reputation for safety and reliability, built over thirty years of consistent performance, is nearly impossible for a competitor to replicate quickly. Trust, unlike a technology platform or a branch network, cannot be purchased or built overnight.

Threat of New Entrants and Fintech Competition. The most credible competitive threat to HDFC Bank comes not from other banks but from fintech companies. PhonePe, Google Pay, Paytm, and a host of smaller players have already captured significant share of India's payments market through UPI, processing billions of transactions monthly. These companies have advantages in user experience, distribution speed, and engineering talent. However, they face a fundamental constraint: they cannot gather deposits. Payments are a low-margin, high-volume business. The real money in financial services comes from lending and deposit-taking, activities that require a banking license, regulatory capital, and a level of institutional infrastructure that fintechs struggle to build. HDFC Bank's response has been to partner selectively with fintechs, as seen in its credit card partnership with PhonePe, while using its balance sheet power and branch network to compete where fintechs are weakest: in building deep, multi-product customer relationships. Apple Pay is reportedly in talks with HDFC Bank and other major Indian banks for a mid-2026 India launch, suggesting that even global technology giants view established banks as essential partners rather than targets for displacement.

Rivalry Among Incumbents. HDFC Bank's primary banking competitors are ICICI Bank, State Bank of India, Kotak Mahindra Bank, and Axis Bank. ICICI Bank, under CEO Sandeep Bakhshi, has significantly improved its asset quality and digital capabilities in recent years and represents the most formidable peer competitor. State Bank of India, with its enormous branch network and government backing, dominates in absolute size but operates at lower profitability. The competitive dynamic is relatively stable: the top four or five banks continue to gain market share from weaker public-sector banks and small private banks, a trend that the NPA crisis and digital transformation have accelerated.

Bargaining Power of Suppliers and Buyers. Banks operate in a commodity market, money is money, so differentiation comes from service, convenience, and trust rather than product features. Depositors, the bank's "suppliers" of raw material, have relatively low bargaining power individually but can collectively shift deposits during crises, as described above. Borrowers have moderate bargaining power for standardized products like home loans, where comparison shopping is easy, but less power for complex products like working capital facilities where relationship banking matters.

For investors tracking HDFC Bank's ongoing performance, the key metrics to watch are straightforward but revealing. CASA ratio tells you whether the bank is maintaining its low-cost funding advantage, the single most important driver of long-term profitability. Net Interest Margin (NIM) captures the spread between what the bank earns on its assets and what it pays for its funding, the direct financial expression of the cost-of-funds advantage. These two numbers, taken together, provide a real-time signal of whether the bank's core competitive position is strengthening, stable, or eroding. Everything else, loan growth, fee income, credit quality, is downstream of these two drivers.

X. The Playbook: Lessons for Builders

The HDFC Bank story offers several principles that extend well beyond banking, lessons for anyone building a durable institution in a complex, competitive market.

"Boring is a Strategy." In the mid-2000s, when India was in the grip of an infrastructure lending boom and banks were falling over themselves to fund power plants, highways, and steel mills, HDFC Bank conspicuously sat on the sidelines. The deals looked attractive: large loan sizes, government guarantees, and seemingly creditworthy corporate borrowers. Other private banks like ICICI Bank built massive infrastructure loan portfolios, generating impressive short-term growth. HDFC Bank said no. The bank's credit committee, operating under Puri's strict risk guidelines, concluded that infrastructure projects carried concentration risk, political risk, and execution risk that were impossible to fully price. When these loans began souring in 2015 and 2016, as the RBI's Asset Quality Review forced the industry to confront reality, HDFC Bank's restraint was vindicated spectacularly. While peers wrote off billions in bad infrastructure debt, HDFC Bank's gross NPA ratio hovered near 1 percent. The lesson: in a cyclical business, the most valuable decisions are often the deals you do not do. Saying no is not timidity; it is strategy.

The CASA Flywheel. Puri understood from his Citibank days that in banking, the cost of capital is the only metric that matters in the long run. A bank that funds itself cheaply can lend at competitive rates, earn wider margins, generate higher returns, reinvest those returns in better technology and more branches, attract more customers, gather more cheap deposits, and repeat the cycle. Every strategic decision at HDFC Bank, from the relentless focus on salary accounts to the aggressive branch expansion into rural India, serves this flywheel. The CASA ratio is not a financial metric; it is a statement of competitive philosophy. It says: we will do whatever it takes to be the cheapest source of money in the market, and then we will use that advantage to win everywhere else.

Succession Planning as a Core Competency. The transition from Aditya Puri to Sashidhar Jagdishan is one of the cleanest CEO successions in the history of Indian business. Puri ran the bank for twenty-six years, an eternity by global standards. The risk of a personality-dependent institution, one that falters when the founding leader departs, was very real. The board managed this risk by selecting an insider who had spent nearly a quarter century absorbing the institution's values, systems, and risk culture. Jagdishan was not chosen because he was a visionary leader or a charismatic public figure. He was chosen because he was the embodiment of the bank's institutional DNA, someone who would preserve the culture while evolving the strategy. The result has been a seamless transition with no discernible disruption to performance, a rarity among founder-led companies.

Acquisitions as Capability Building. HDFC Bank's three major acquisitions, Times Bank, Centurion Bank of Punjab, and HDFC Ltd., each served a distinct strategic purpose and each was executed with discipline. Times Bank provided an urban footprint. CBoP provided a national footprint. HDFC Ltd. provided a mortgage portfolio and cross-sell opportunity. In each case, the bank paid a fair price, integrated quickly, and extracted value through the flywheel rather than through cost-cutting. The lesson for acquirers is that the best deals are not about buying revenue or earnings. They are about buying capabilities, distribution, or customer access, that amplify your existing competitive advantage.

XI. Epilogue and Conclusion

The question that confronts HDFC Bank as it enters the next phase of its life is whether the fortress can sustain its returns at its current scale. With a balance sheet that now ranks among the largest in Asia, the bank faces the fundamental challenge of every successful growth company: the law of large numbers. Maintaining an 18 to 20 percent return on equity when your asset base exceeds $250 billion is a qualitatively different challenge than doing so at $50 billion. The opportunities must be bigger, the execution must be sharper, and the risks must be managed with even greater precision.

There are reasons for confidence. India's banking system remains deeply underpenetrated relative to developed markets. Credit-to-GDP ratio, at roughly 50 percent, is less than half the levels seen in China or developed Asia. The mortgage market, now central to HDFC Bank's strategy, is in the early stages of a secular growth wave driven by urbanization, rising incomes, and government housing initiatives. The shift of household savings from physical assets like gold and real estate toward financial assets like bank deposits, mutual funds, and insurance is still in its opening chapters. Each of these trends plays directly to HDFC Bank's strengths: its branch network, its deposit franchise, its cross-sell machinery, and the diversified subsidiary ecosystem it now commands.

There are also legitimate concerns. The integration of HDFC Ltd.'s mortgage book has temporarily elevated the bank's credit-to-deposit ratio, requiring aggressive deposit mobilization at a time when competition for deposits across the Indian banking system has intensified. The RBI's evolving regulatory posture, particularly around digital lending, data privacy, and responsible lending practices, introduces ongoing compliance complexity. And the fintech threat, while currently more noise than substance in terms of actual profit pool displacement, is a permanent feature of the competitive landscape that demands continuous technology investment.

Perhaps the most illuminating way to think about HDFC Bank is as a proxy for India itself. If you believe that India will grow, that its middle class will expand, that its urbanization will continue, that its financial system will deepen, and that its economy will reward institutional quality over political connections, then HDFC Bank is the most direct expression of that thesis available in public markets. The bank does not need to do anything extraordinary to grow. It simply needs India to continue doing what India has been doing for the past three decades: getting richer, one family, one savings account, one home loan at a time.

Aditya Puri once said that banking was simple: "You borrow money at a certain price, you lend it at a higher price, and you don't lend it to people who won't return it." Thirty-one years after he walked into that tiny office in Worli, the institution he built remains, at its core, a relentless execution machine built on that deceptively simple premise. The question is not whether HDFC Bank will continue to grow. It is whether any competitor, old or new, can muster the discipline, the patience, and the institutional will to replicate what it took three decades to build. So far, none have come close.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube