Healthcare Global Enterprises (HCG): India's Cancer Care Pioneer

I. Introduction & Company Overview

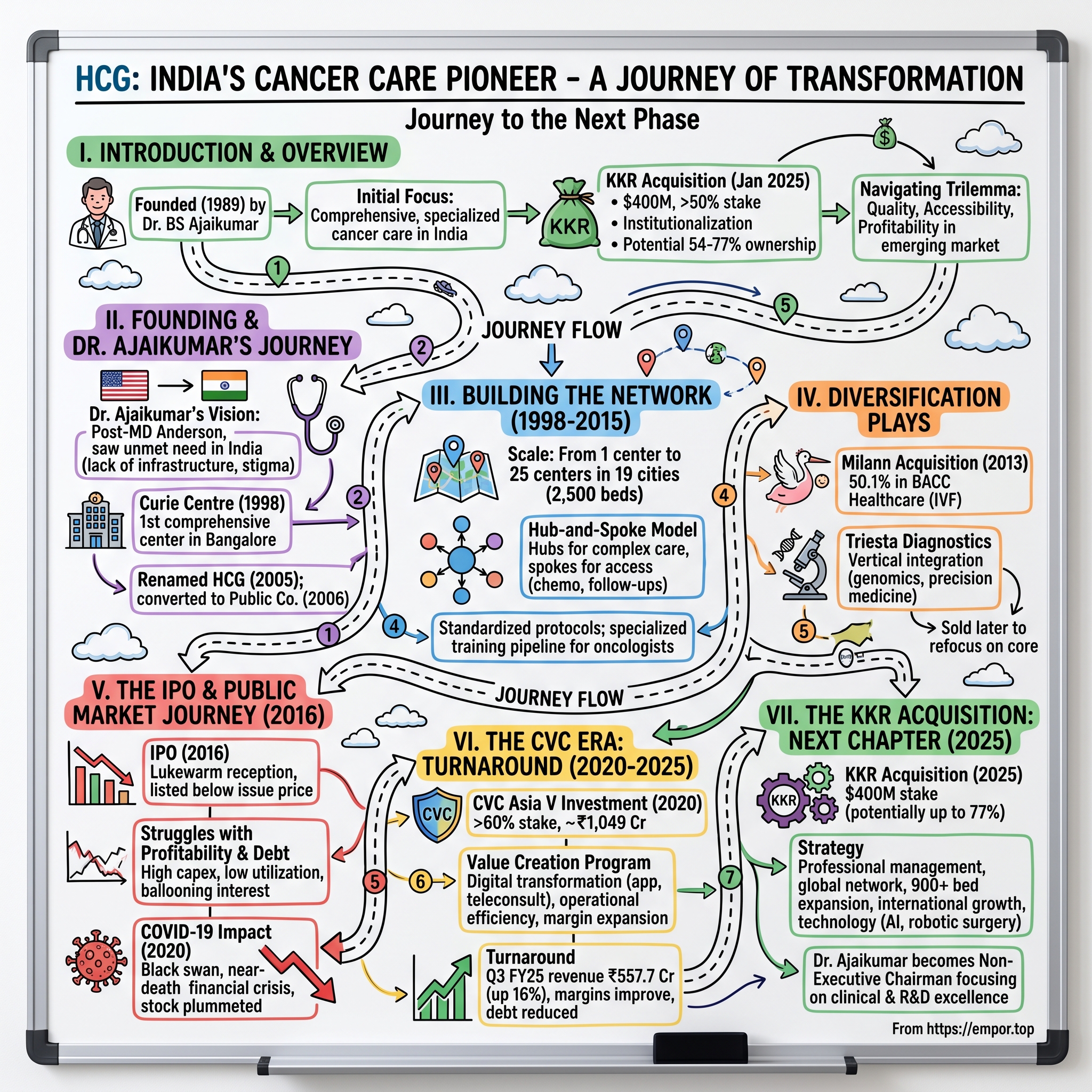

Picture this: It's January 2025, and inside a gleaming boardroom in Mumbai, executives from KKR—one of the world's most sophisticated private equity firms—are signing papers to acquire a controlling stake in an Indian cancer care company for $400 million. The target isn't Apollo or Fortis, household names in Indian healthcare. It's HCG, a company most Indians outside the medical community have never heard of, yet one that treats more cancer patients than any other private network in the country.

The numbers tell a compelling story: HealthCare Global Enterprises commands a market capitalization of approximately ₹9,245 crore, with annual revenues touching ₹2,310 crore. But here's what makes this fascinating—just five years ago, this same company was struggling under a mountain of debt, its stock languishing, its founder-CEO wondering if his three-decade dream of democratizing cancer care in India would survive the pandemic. The February 2025 acquisition sees KKR paying $400 million (approximately ₹3,465 crore) to acquire up to 54% of HCG from CVC Asia V, with an additional mandatory open offer for 26% at ₹445 per share. This positions KKR to potentially own between 54-77% of India's largest private cancer care network—a company that five years ago was gasping for survival.

The central question that frames our story: How did an oncologist's vision, born from watching cancer patients struggle to find quality care in India, transform into a ₹9,000+ crore enterprise that caught the attention of the world's most sophisticated healthcare investors?

This is the story of Dr. BS Ajaikumar, who left a lucrative practice in America to build something that didn't exist in India—a specialized, comprehensive cancer care network. It's a tale of building in an emerging market where the disease was stigmatized, the infrastructure was absent, and the very concept of specialized cancer hospitals was foreign. It's about surviving near-death experiences—both medical and financial—and emerging stronger. And ultimately, it's about how private equity transformed a founder-led Indian healthcare company into an institutional powerhouse.

What makes HCG particularly fascinating for students of business is how it navigated the classic emerging market healthcare trilemma: quality, accessibility, and profitability. Unlike software or consumer goods, you can't iterate quickly in healthcare—mistakes cost lives, not just market share. Yet HCG managed to scale from a single center in Bangalore to 25 medical centers across 19 cities with 2,500 beds, nearly 100 operating theaters, and 40 linear accelerator machines.

As we dive into this journey, we'll explore not just the what but the why—why cancer care specifically, why the hub-and-spoke model, why private equity was both savior and catalyst, and why KKR is betting another $400 million that this story is just beginning. Welcome to the remarkable transformation of Indian cancer care, told through the lens of its most ambitious pioneer.

II. The Founding Story & Dr. BS Ajaikumar's Journey

The year is 1989. Dr. BS Ajaikumar is standing in the oncology ward at MD Anderson Cancer Center in Houston, one of the world's premier cancer institutions. He's been in America for nearly two decades, building a successful practice, publishing research, treating thousands of patients with cutting-edge therapies. By any measure, he's living the Indian-American dream. Yet something gnaws at him—memories of home, of patients in India who would never see the inside of a facility like this.

Dr. Ajaikumar's journey to becoming India's cancer care pioneer began, ironically, with leaving India. After completing his MBBS from the prestigious St. John's Medical College in Bangalore, he did what ambitious Indian doctors did in the 1970s—headed west. His residency at the University of Virginia introduced him to American medical standards. But it was his time at MD Anderson in Houston, earning his MD and practicing oncology, that shaped his vision. Here was cancer care as it should be: multidisciplinary teams, cutting-edge radiation equipment, clinical trials, and most importantly, hope backed by science.

For twenty years, he practiced in the United States, accumulating not just wealth but something more valuable—an understanding of how world-class cancer care operated at scale. He watched Linear Accelerators (LINACs) deliver precise radiation doses. He participated in tumor boards where surgeons, medical oncologists, radiation oncologists, and pathologists collaborated on each case. He saw how protocols and standardization could deliver consistent outcomes across thousands of patients.

But India kept calling. Not through nostalgia, but through numbers. In the late 1980s, India was diagnosing nearly 500,000 new cancer cases annually, yet had fewer than 100 radiation oncologists for a population approaching one billion. Most cancer equipment was concentrated in a handful of government hospitals in metros. The word "cancer" itself was so stigmatized that patients often hid their diagnosis from their own families. Treatment, when available, was often palliative rather than curative.

Founded in 1989, HCG is one of India's largest oncology hospital chains—but the real corporate story begins later. When Dr. Ajaikumar returned to India, he didn't immediately build a corporate empire. He started with a single vision: one comprehensive cancer center in Bangalore that would match international standards. The challenge wasn't just medical—it was everything else.

India in the early 1990s had no ecosystem for specialized healthcare. Banks didn't understand how to value medical equipment as collateral. There were no trained radiation technicians—Dr. Ajaikumar had to create training programs from scratch. The Atomic Energy Regulatory Board (AERB) had just begun licensing private centers to operate radiation equipment, a process fraught with bureaucracy. Even explaining to patients why they needed to come to a specialized center rather than a general hospital was an uphill battle.

The formal corporate structure emerged gradually. Initially incorporated as Curie Centre of Oncology Private Limited in 1998—a name honoring Marie Curie—the company was renamed HealthCare Global Enterprises in 2005, signaling broader ambitions. The conversion to a public company in 2006 marked the transformation from a founder's vision to an institutional entity.

What distinguished Dr. Ajaikumar's approach was his insistence on comprehensive care under one roof. In the US, he'd seen how fragmentation killed patients—not literally, but through delays, miscommunication, and suboptimal treatment sequencing. A patient might see a surgeon who'd recommend immediate surgery, not knowing that neo-adjuvant chemotherapy could shrink the tumor first. In India, with its infrastructure challenges and vast distances, fragmentation would be even deadlier.

Building credibility in those early years meant taking cases others wouldn't touch. When established hospitals referred their "hopeless" cancer cases, Dr. Ajaikumar's team took them on, often achieving remarkable outcomes through aggressive multimodal therapy. Word spread through the most powerful marketing channel in healthcare—patient testimonials. Families who'd been told to "take him home and make him comfortable" instead saw their loved ones achieve remission.

The talent challenge was perhaps the steepest mountain to climb. India's best oncologists were either abroad or concentrated in a few government institutions. Dr. Ajaikumar leveraged his MD Anderson network, recruiting Indian doctors from the US with a compelling pitch: "Come home and build something that matters." He offered not just competitive salaries but equity participation and the chance to shape Indian oncology practice. Many who joined in those early years became millionaires when HCG went public.

By the early 2000s, the foundation was set. HCG had proven that private specialized cancer care could work in India. Patients were willing to pay for quality. Banks began understanding the business model. The AERB streamlined approvals. Most importantly, a new generation of Indian oncologists saw HCG as a place to build careers, not just practice medicine. The stage was set for the next phase—scaling from one center to becoming India's largest cancer care network.

III. Building the Cancer Care Network (1998–2015)

The conference room in HCG's Bangalore headquarters, circa 2003, had a massive map of India on the wall. Red pins marked existing cancer centers—mostly concentrated in metros. Blue pins showed HCG's planned expansion. Dr. Ajaikumar would often stand before this map, explaining to skeptical investors why Nashik, Ahmedabad, and Cuttack were the future of Indian oncology. "Cancer doesn't discriminate by geography," he'd say, "but access to cancer care does."

Building India's largest private cancer care network wasn't just about replicating the Bangalore model elsewhere. Each new center was an exercise in localization, negotiation, and sometimes, improvisation. The hub-and-spoke model that would become HCG's signature wasn't born from strategic consulting frameworks—it emerged from harsh ground realities.

The hub-and-spoke architecture solved multiple problems simultaneously. The "hub" in each region would house expensive equipment like LINACs and PET-CT scanners, subspecialists, and complex surgical facilities. The "spokes"—smaller centers in surrounding towns—would handle chemotherapy, follow-ups, and initial diagnosis. This wasn't just about capital efficiency; it was about making treatment accessible. A farmer from rural Karnataka could get chemotherapy 50 kilometers from home instead of traveling to Bangalore for every session.

Technology acquisition in those years was a delicate dance with suppliers, banks, and regulators. A single LINAC cost upwards of ₹15 crore—more than most Indian hospitals' entire annual equipment budgets. HCG pioneered innovative financing structures, including revenue-sharing agreements with equipment manufacturers who bet on India's long-term cancer care growth. The AERB licensing for each machine took months, requiring proof of adequate radiation safety infrastructure, trained personnel, and quality assurance protocols.

By 2010, HCG had cracked the standardization code. Every center, whether in metropolitan Bangalore or tier-2 Nagpur, followed identical treatment protocols. This wasn't just about clinical quality—it was about brand promise. A patient walking into any HCG center would receive the same evidence-based care. The company developed its own Clinical Management System, digitizing patient records before "digital health" became a buzzword. Tumor boards met via videoconference, allowing a complicated case in Cuttack to benefit from expertise in Bangalore.

The talent multiplication strategy was equally innovative. Instead of trying to recruit hundreds of senior oncologists—which didn't exist—HCG created its own pipeline. The company partnered with medical colleges to offer super-specialty training programs. Young doctors completing their oncology training were offered a deal: join HCG, get trained on cutting-edge equipment, participate in research, and after three years, either stay with equity participation or launch your own practice with HCG's blessing. Many chose to stay.

Founded in 1989, HCG operates 25 medical care centres in 19 cities with 2,500 beds, nearly 100 operating theatres, and 40 linear accelerator machines. But these numbers don't capture the human complexity of this expansion. Each new center meant navigating local politics, recruiting staff who'd never worked in specialized healthcare, and educating communities where cancer was still whispered about, not discussed openly.

The tier-2 and tier-3 city focus, initially seen as risky, proved prescient. These markets had virtually no organized cancer care. HCG didn't face competition from Apollo or Fortis—they faced the choice between HCG and no treatment at all. The company discovered that tier-2 cities had surprising paying capacity. Extended families pooled resources for cancer treatment. State government insurance schemes, launched in the late 2000s, covered many poor patients. Corporate insurance penetration was growing. The unit economics in smaller cities often exceeded metros—lower real estate costs, less staff turnover, and higher patient loyalty.

Clinical excellence remained the north star. HCG published its outcome data publicly—rare for Indian healthcare. Five-year survival rates for common cancers matched international benchmarks. The company participated in global clinical trials, giving Indian patients access to experimental therapies. This wasn't just about marketing; it was about accountability. Every oncologist's performance was tracked, discussed, and improved through continuous medical education programs.

The international collaborations added credibility and capability. HCG partnered with MD Anderson for second opinions on complex cases. They brought international oncologists for training programs. Indian doctors from HCG spent rotations at leading cancer centers globally. This knowledge transfer was bidirectional—HCG's expertise in treating advanced-stage cancers (more common in India due to late detection) became valuable for international partners.

By December 2015, the network had reached critical mass: 14 comprehensive cancer centers including the center of excellence in Bengaluru, three diagnostic centers, and one day-care chemotherapy center. The company was treating over 200,000 patients annually. But expansion had come at a cost. Debt had ballooned to fund new centers. Utilization rates at newer facilities were below plan. Competition was intensifying as large hospital chains recognized oncology's potential. The stage was set for the next phase of HCG's evolution—one that would require fresh capital and new strategic directions.

IV. Diversification Plays: Milann & Triesta

The boardroom discussion in 2013 was heated. HCG was considering its largest acquisition to date—a 50.10% stake in BACC Healthcare, which operated fertility centers under the Milann brand. Some board members questioned the logic: "We're cancer specialists. What do we know about making babies?" Dr. Ajaikumar's response was swift: "We know about giving hope to families facing biological crises. We know about managing complex medical procedures. We know about building trust in sensitive healthcare moments."

The Milann Acquisition Story

The Milann opportunity came through Dr. Kamini Rao, a legend in Indian reproductive medicine with over 25 years of experience. Her Bangalore Assisted Conception Center, established in 1990, had pioneered IVF in South India when most Indians hadn't even heard the term. By 2013, Milann had expanded to multiple centers but faced familiar challenges—capital for expansion, operational standardization, and competing against venture-funded chains.

The strategic rationale went beyond superficial synergies. Both oncology and fertility dealt with time-sensitive, emotionally charged medical journeys. Both required sophisticated equipment and subspecialized talent. Both commanded premium pricing with limited insurance coverage. Most intriguingly, HCG had discovered that fertility preservation for cancer patients—freezing eggs or sperm before chemotherapy—was an underserved need. Young cancer patients often faced the double tragedy of disease and infertility.

The acquisition gave HCG entry into a market growing at 20% annually. India's infertility rates were rising due to lifestyle changes, late marriages, and environmental factors. The social stigma around infertility was declining. Bollywood celebrities openly discussed their IVF journeys. The market was fragmented—thousands of small IVF clinics with varying quality standards. Milann, with its reputation and HCG's operational backbone, could consolidate and scale.

Integration wasn't smooth initially. Fertility specialists had different cultural DNA than oncologists. The patient journey in IVF—often multiple cycles over months or years—differed from cancer care's acute intervention model. The metrics were different too. Success in oncology was measured in survival rates; in IVF, it was pregnancy rates and live births. HCG learned to manage these differences, maintaining Milann's brand identity while implementing back-office standardization.

The financial performance exceeded expectations. Milann's EBITDA margins exceeded 30%, higher than HCG's core cancer business. The cash conversion was superior—IVF patients typically paid upfront, unlike cancer care's insurance-heavy model. By 2016, Milann contributed nearly 8% of HCG's revenues despite being a much smaller operation by infrastructure footprint.

The Triesta Diagnostics Play

While Milann was about adjacency expansion, Triesta represented vertical integration. Launched as HCG's diagnostic arm, Triesta specialized in high-end cancer diagnostics—molecular testing, genomic profiling, liquid biopsies. This wasn't routine blood work; this was precision medicine's cutting edge.

The rationale was compelling. HCG was sending thousands of samples to external labs for specialized tests, facing delays and quality inconsistencies. Cancer treatment increasingly depended on molecular markers—which chemotherapy would work, which wouldn't, which patients needed aggressive treatment, which could be spared toxicity. Controlling diagnostics meant controlling the full patient journey.

Triesta invested heavily in technology. Next-generation sequencing machines, each costing crores, could decode tumor DNA. Liquid biopsy platforms could detect cancer recurrence from blood samples months before traditional scans. The lab achieved NABL and CAP accreditation—gold standards that few Indian diagnostic labs possessed. This wasn't just about serving HCG's internal needs; Triesta began processing samples from other hospitals, creating a new revenue stream.

The intellectual property component was crucial. Triesta's team developed India-specific cancer panels—genetic tests tailored to mutations common in Indian populations. They published research on cancer genomics in Indian patients, building scientific credibility. International pharma companies partnered with Triesta for clinical trial testing, adding high-margin revenue.

However, the diagnostic business proved more challenging to scale than anticipated. The market education burden was heavy—convincing oncologists to order expensive genetic tests, explaining to patients why a ₹50,000 test was worthwhile. Competition from established players like SRL and Metropolis was intense. The capital intensity was higher than expected, with rapid technology obsolescence requiring continuous reinvestment.

The strategic value, though, transcended financial returns. Triesta positioned HCG at oncology's innovation frontier. When immunotherapy and targeted therapy revolutionized cancer treatment, HCG was ready with companion diagnostics. The vertical integration story resonated with investors who saw HCG not just as a hospital chain but as a comprehensive cancer care ecosystem.

The eventual sale of Triesta to HCG NCHRI Oncology for ₹135 crore wasn't a retreat but a strategic refocus. The diagnostics capability remained within the HCG ecosystem while freeing capital for core expansion. The Milann success and Triesta experience taught HCG valuable lessons about diversification—adjacent specialties could work, but vertical integration required careful calibration of ambition versus execution capability.

V. The IPO & Public Market Journey (2016)

The morning of March 16, 2016, was supposed to be triumphant. After weeks of roadshows across Mumbai, Singapore, London, and New York, HCG's IPO was opening for subscription. The offer price was set at ₹218 per share, valuing the company at roughly ₹2,000 crore. Dr. Ajaikumar rang the ceremonial bell at the NSE, surrounded by his team, many of whom had been with him since the early days. Yet within hours, it became clear that the market's reception would be lukewarm at best.

The IPO raised ₹650 crore, with the issue subscribed 1.3 times—respectable but not spectacular. Institutional investors who'd seemed enthusiastic during roadshows turned cautious when writing checks. The concerns were multifaceted: healthcare stocks had underperformed recently, HCG's debt levels worried analysts, and the company's expansion-heavy strategy meant profits were still years away. The stock listed at ₹205, below the issue price—a psychological blow for a company used to exceeding expectations.

The roadshow presentations had been meticulously crafted. HCG's pitch was compelling on paper: India's cancer incidence growing at 11% annually, the company's market leadership, successful track record of entering new geographies, the Milann diversification showing early success. The management team spoke passionately about democratizing cancer care, about the thousands of lives saved, about the massive unmet need in tier-2 and tier-3 India.

But institutional investors asked harder questions. Why were utilization rates at new centers below 40%? How would HCG compete when Apollo and Fortis were aggressively entering oncology? Why was debt-to-EBITDA at 4.5x when peers operated at 2-3x? Most pointedly—when would the company actually generate free cash flow?

The retail investor response revealed another challenge. Unlike consumer companies or banks, healthcare was hard for average investors to understand. HCG's story—specialized care, hub-and-spoke models, AERB licenses—didn't translate into simple narratives. The brand recognition that helped Fortis or Apollo's IPOs was absent. Most retail investors outside South India hadn't heard of HCG.

Building institutional credibility became management's obsession post-IPO. Quarterly earnings calls transformed from perfunctory updates to detailed operational discussions. The company began disclosing granular metrics—bed utilization rates by center, average revenue per patient, clinician productivity. Management met investors regularly, explaining the J-curve of hospital economics—why new centers lost money initially but became cash cows at maturity.

The struggle with profitability was real and visible. Between 2016 and 2019, HCG opened six new centers, each requiring ₹50-100 crore in capital expenditure. The gestation period for profitability—typically 3-4 years for new hospitals—meant accumulated losses even as revenue grew. The company's PAT remained negative or marginally positive, frustrating investors who'd expected post-IPO operational leverage.

Debt became the millstone around HCG's neck. By 2019, total debt exceeded ₹1,000 crore. Interest costs consumed nearly 15% of revenues. Rating agencies expressed concerns. Banks turned cautious about additional lending. The stock price languished between ₹150-200, well below IPO levels. Short sellers circled, betting that HCG's expansion strategy would implode.

Then came COVID-19—a black swan that nearly killed the company. Cancer surgeries, which couldn't be done remotely, plummeted as hospitals became COVID centers. Patients, immunocompromised from chemotherapy, stayed away from hospitals. International patients, a high-margin segment, disappeared. Revenues in Q1 FY2021 crashed by 40%. Fixed costs—salaries, lease rentals, interest—continued. The company burned through cash reserves.

The pandemic exposed the fragility of debt-funded expansion in healthcare. Unlike manufacturing or services, hospitals couldn't simply shut down and restart. Cancer patients needed continuous care. HCG's doctors worked through lockdowns, sometimes treating just handful of patients per day in centers built for hundreds. The human toll was immense—several HCG healthcare workers died from COVID.

By June 2020, the situation was dire. Banks demanded asset sales. The stock touched ₹90, giving HCG a market cap below its book value. Employees worried about salaries. Vendors demanded advance payments. Dr. Ajaikumar, now in his 70s, faced the possibility that his life's work might not survive.

It was in this darkest hour that an unexpected savior emerged. CVC Capital Partners, the global private equity giant, saw opportunity where others saw disaster. They recognized that COVID was temporary, cancer was permanent, and HCG's infrastructure, built over three decades, couldn't be easily replicated. The negotiation that followed would transform HCG from a struggling public company into private equity's next big healthcare bet.

VI. The CVC Era: Turnaround & Transformation (2020–2025)

The Zoom call in May 2020 was surreal. On one side, Dr. Ajaikumar and his CFO, sitting in a nearly empty Bangalore headquarters with masked security guards visible in the background. On the other, CVC's partners, dialing in from London, Hong Kong, and Mumbai, their homes turned into makeshift offices. They were negotiating a deal worth over ₹1,000 crore while India's healthcare system was collapsing around them. CVC's opening statement set the tone: "We don't invest in distress. We invest in transformation opportunities disguised as distress."

Since CVC Asia V invested in 2020, CVC's India team worked closely with HCG on a transformational value creation program to drive revenue growth through and beyond COVID, improve key performance indicators, source and execute acquisitions and digital transformation. The acquisition, completed in June 2020 for approximately ₹1,049 crore, gave CVC a 60.36% controlling stake. The timing seemed either brilliant or insane—buying a hospital chain during a pandemic when hospitals were struggling to survive.

CVC's first 100 days revealed their playbook. Unlike typical private equity cost-cutting, they invested aggressively. Digital infrastructure that HCG had delayed for years—teleconsultation platforms, digital patient records, automated billing systems—was implemented in months. They brought in McKinsey consultants, not to recommend layoffs but to optimize clinical pathways. Every patient journey was mapped, bottlenecks identified, solutions implemented.

The operational improvements were granular but impactful. Chemotherapy chair utilization increased from 60% to 85% through better scheduling algorithms. LINAC machines, previously idle during lunch hours, ran continuously through staggered operator shifts. Inventory management, especially for expensive cancer drugs, was centralized, reducing working capital by 20%. These weren't revolutionary changes—they were the accumulation of hundreds of small optimizations that HCG's management, firefighting through COVID, hadn't had bandwidth to implement.

The margin expansion story was remarkable. Despite COVID headwinds, HCG's EBITDA margins expanded from 12% in FY2020 to over 18% by FY2023. This wasn't through price increases—cancer care pricing remained stable. Instead, it came from operational leverage. Fixed costs were spread across higher patient volumes. Procurement was centralized, negotiating better rates from suppliers. Clinical protocols were standardized, reducing treatment variations that drove up costs.

The acquisition strategy under CVC was selective but transformative. In late 2024, HCG acquired MG Hospital in Vizag, a 196-bed facility with a strong 35% operating margin. Additionally, the company launched a 200-bed cancer care center in Ahmedabad. It is also expanding its North Bengaluru facility by 125 beds. These weren't distress acquisitions but strategic additions filling geographic gaps in HCG's network. Each acquisition was integrated rapidly, with HCG's protocols and systems implemented within quarters, not years.

The digital transformation went beyond operational efficiency. HCG launched India's first comprehensive cancer care app, allowing patients to book appointments, access medical records, and consult doctors remotely. The app became crucial during COVID lockdowns but remained popular post-pandemic, especially for follow-up consultations. International patients from Africa and the Middle East could now get second opinions without traveling to India, opening new revenue streams. The financial turnaround numbers validated CVC's strategy. Q3 FY25 showed operational revenue of Rs 557.7 crore, up from Rs 468.9 crore in the same period last year, with growth driven by increasing volumes across modalities. For the first nine months of FY25, revenue increased by 16 per cent to Rs 1,637 crore, with a 38 per cent year-on-year jump in PAT to Rs 37 crore. Average revenue per occupied bed in Q3 was Rs 44,284, reflecting a 3.5 per cent growth rate.

The cultural transformation was equally important. CVC brought in professional managers for non-clinical roles, freeing doctors to focus on medicine. Performance metrics shifted from activity-based (number of procedures) to outcome-based (patient satisfaction, clinical outcomes). Variable compensation was introduced, aligning individual incentives with organizational goals. This wasn't always smooth—several senior managers who'd been with HCG since early days struggled with the new performance-driven culture.

CVC's network effects strategy was sophisticated. They facilitated partnerships between HCG and their other portfolio companies in healthcare. Medical device companies in CVC's portfolio offered HCG preferential pricing. Healthcare IT companies provided customized solutions. This wasn't just financial engineering—it was operational synergy at scale.

The preparedness for exit was built in from day one. CVC knew they'd eventually sell—that's the private equity model. Every operational improvement was documented, every financial metric tracked, every growth initiative measured. By 2024, when they began exploring exit options, they had a compelling story: a company transformed from COVID-near-death to robust profitability, from operational chaos to clinical excellence, from founder-dependent to institutionally managed.

VII. The KKR Acquisition: Next Chapter (2025)

The Investment Committee meeting at KKR's New York headquarters in December 2024 was unusually animated. The team was debating whether to bid for HCG—their third major Indian healthcare investment in five years. The head of Asia Healthcare made the case: "This isn't just about buying India's largest cancer network. This is about riding three megatrends: aging populations, lifestyle disease explosion, and healthcare infrastructure build-out in emerging markets. HCG is the platform to capture all three."

KKR acquired up to a 54 per cent stake in Healthcare Global Enterprises (HCG) from CVC Asia V for $400 million (approximately Rs 3,465 crore), purchasing shares at Rs 445 apiece and making an open offer to buy an additional 26 per cent. The valuation implied an enterprise value of nearly ₹7,000 crore—a remarkable recovery from the ₹1,500 crore valuation during COVID depths.

The strategic rationale went beyond financial metrics. KKR had generated spectacular returns in Indian healthcare— in August 2022, KKR had sold its stake in Max Healthcare for Rs 9,400 crore, realising a fivefold return on investment over four years. They understood the playbook: operational improvements, strategic acquisitions, technology enablement, and patient volume growth. HCG offered something more—a pure-play oncology platform in a market where cancer incidence was growing at double digits.

Dr. BS Ajaikumar, Founder of HCG, will take on the role of Non-Executive Chairman and be focused on driving clinical, academic and research and development excellence. This transition, negotiated carefully over months, was crucial. At 75, Dr. Ajaikumar recognized the need for professional management while retaining his role as clinical visionary. His new mandate—research, academics, clinical excellence—played to his strengths while freeing him from operational minutiae.

KKR's due diligence revealed opportunities that CVC hadn't fully exploited. The diagnostic business could be scaled dramatically—genetic testing in India was nascent but exploding. The international patient business, disrupted by COVID, could be rebuilt through medical tourism partnerships. Most intriguingly, HCG's data—millions of patient records, treatment outcomes, genetic profiles—could power AI-driven drug discovery and precision medicine initiatives.

The management presentation to KKR highlighted the expansion roadmap. HCG plans to add 900 more beds over the next 4-5 years, focusing on underserved geographies. Each new center would follow the proven hub-and-spoke model, achieving profitability within 36 months. The capital efficiency had improved dramatically—new centers required 30% less investment than five years ago due to standardized designs and centralized procurement.

Akshay Tanna, partner and head of India private equity, KKR, said the investment will support developing medical infrastructure and delivery of critical oncology services. KKR re-entered healthcare by buying controlling stake in Kerala's Baby Memorial Hospital. This wasn't KKR's first rodeo in Indian healthcare—they brought deep operational expertise and global best practices.

The technology roadmap under KKR was ambitious. Plans included AI-powered treatment planning, where algorithms would suggest optimal therapy combinations based on tumor genetics and patient characteristics. Robotic surgery platforms would be introduced in major centers. Digital therapeutics—apps that help manage chemotherapy side effects, provide psychological support, track recovery—would complement physical care. This wasn't technology for technology's sake but tools to improve outcomes and patient experience.

The governance restructuring was carefully orchestrated. KKR would appoint independent directors with global healthcare experience. The board would have dedicated committees for clinical quality, technology, and expansion. Management incentives would be tied to long-term value creation, not just short-term profitability. This institutional framework would ensure HCG's evolution from founder-led to professionally governed continued smoothly.

International expansion featured prominently in KKR's vision. HCG already operated in Kenya—proof of concept for emerging market expansion. The Middle East, with its large Indian diaspora and limited oncology infrastructure, was the logical next frontier. Southeast Asia, particularly Indonesia and Vietnam, offered massive untapped markets. KKR's global network could facilitate these expansions through local partnerships and regulatory navigation.

The competitive response to KKR's entry was swift. Apollo announced a ₹1,000 crore oncology expansion. Fortis accelerated its cancer care investments. Regional players worried about HCG's renewed financial firepower. The consolidation wave that KKR's entry triggered would reshape Indian oncology—smaller centers would either sell or struggle to compete.

What made this acquisition particularly interesting was the timing. Healthcare valuations globally had cooled from pandemic highs. Interest rates were elevated. Yet KKR was making one of its largest Indian healthcare bets. This contrarian move reflected confidence not just in HCG but in the structural growth story of Indian healthcare—a market where demand would outstrip supply for decades.

VIII. Current Operations & Business Model

Walk through HCG's flagship Bangalore center today, and you're seeing the culmination of three decades of evolution. The morning tumor board meeting has 15 specialists on video conference from different cities, discussing a complex case. In the basement, one of 40 LINACs delivers precisely targeted radiation while the patient watches Netflix on ceiling-mounted screens. Upstairs, the day-care chemotherapy unit operates at 95% capacity, with patients receiving treatment while working on laptops. This is cancer care reimagined—efficient, patient-centric, technology-enabled.

HCG operates 25 medical care centres in 19 cities with 2,500 beds, nearly 100 operating theatres, and 40 linear accelerator machines. But these numbers only tell part of the story. The real innovation lies in how these assets are orchestrated to deliver care at scale while maintaining quality.

The business model has evolved into four distinct but synergistic segments. Cancer care remains the core, contributing roughly 80% of revenues. The oncology services span the entire patient journey—from prevention and screening through diagnosis, treatment, and survivorship care. Each comprehensive cancer center offers surgical oncology, medical oncology, radiation oncology, nuclear medicine, and supportive care under one roof. This integration eliminates the coordination failures that plague fragmented healthcare systems.

Milann fertility centers represent the second pillar, contributing approximately 8% of revenues but with disproportionate profitability. The IVF business model is inherently attractive—high margins, cash upfront, limited insurance dependence, and repeat customers (many couples require multiple cycles). The synergy with oncology through fertility preservation for cancer patients adds a unique differentiator that pure-play IVF chains cannot match.

The multispecialty hospitals, primarily in smaller cities, serve as feeders to the cancer network while diversifying revenue streams. These facilities offer general medicine, surgery, and diagnostics, identifying cancer cases early and referring complex cases to HCG's comprehensive centers. This creates a virtuous cycle—the multispecialty presence builds local brand equity, which drives cancer care volumes.

International operations, currently centered in Kenya, represent the fourth segment. The Nairobi center has become East Africa's premier cancer facility, treating patients from Ethiopia, Uganda, Tanzania, and beyond. The model here differs from India—higher prices, significant out-of-pocket payments, longer patient stays due to travel distances. The learnings from Kenya are informing HCG's broader international expansion strategy.

The unit economics reveal why specialized healthcare can be more profitable than general hospitals. The Average Revenue Per Occupied Bed (ARPOB) increased 3.5% YoY to INR 44,284 in Q3 FY25, while the Average Occupancy Rate (AOR) improved to 62.1% from 59.8% in Q3FY24. These metrics significantly exceed general hospital averages due to the complexity and duration of cancer treatment.

The hub-and-spoke efficiency deserves deeper examination. A typical hub requires ₹150-200 crore investment but serves 5-7 spokes, each requiring only ₹20-30 crore. The hub handles complex surgeries and radiation; spokes manage chemotherapy and follow-ups. This topology means 70% of patient touchpoints happen at lower-cost spokes, while high-value procedures concentrate at hubs. The result: better asset utilization and superior returns on capital.

Technology leverage has become a key differentiator. Each LINAC machine, costing ₹15-20 crore, can treat 50-60 patients daily when optimally utilized. HCG's machines run 14-16 hours daily versus industry average of 8-10 hours, achieved through staggered shifts and predictive maintenance. The company's proprietary treatment planning software reduces setup time by 30%, allowing more patients per machine. This operational excellence translates directly to the bottom line.

The clinical talent model has matured into a hybrid structure. Senior oncologists are typically partners with equity stakes, aligning their interests with organizational success. Junior doctors are salaried employees with clear progression paths. Visiting consultants provide specialized expertise without fixed cost burdens. This structure balances quality, cost, and scalability—critical for maintaining margins while expanding rapidly.

The payer mix reveals Indian healthcare's evolution. Approximately 40% of revenues come from insurance (government schemes and private insurance), 50% from out-of-pocket payments, and 10% from corporate contracts. This diversification reduces dependence on any single payment source. The insurance percentage is rising as coverage expands, but out-of-pocket remains significant due to treatment components (like targeted therapy drugs) not covered by insurance.

Working capital management in healthcare is notoriously complex, but HCG has developed sophisticated systems. Insurance claims are processed within 45 days through dedicated teams and automated submission systems. High-cost drugs are managed through consignment inventory models with pharmaceutical companies. Equipment financing is structured to align with revenue generation timelines. These optimizations have reduced working capital requirements by 25% over five years.

The quality metrics that matter in cancer care—five-year survival rates, infection rates, patient satisfaction scores—are tracked obsessively and benchmarked globally. HCG publishes these outcomes transparently, unusual in Indian healthcare. This commitment to measurement and transparency has become a competitive advantage, attracting patients who value evidence-based care over proximity or price alone.

IX. Industry Context & Competitive Landscape

India's cancer care industry is experiencing a paradox: explosive growth amid massive underservice. India's cancer care industry is growing at a compound annual growth rate (CAGR) of 17%, yet the country has just one oncologist per 1,600 cancer patients versus one per 100 in developed markets. This supply-demand mismatch creates both opportunity and responsibility for players like HCG.

The numbers paint a stark picture. India reports 1.4 million new cancer cases annually, projected to reach 2 million by 2030. The disease burden is shifting—while tobacco-related cancers remain prevalent, lifestyle-associated cancers (breast, colorectal, prostate) are rising rapidly. The epidemiological transition mirrors economic development, creating demand for sophisticated treatment modalities that didn't exist a generation ago.

Competition in Indian oncology has intensified dramatically. Apollo Hospitals, with its vast network and deep pockets, has declared oncology a strategic priority, investing ₹1,000 crore in new cancer centers. Fortis Healthcare leverages its urban presence to capture high-value oncology cases. Tata Memorial Hospital, the government's flagship cancer institution, remains the price and quality benchmark. International players like Cancer Treatment Centers of America have explored Indian entry through partnerships.

Yet the competitive dynamics in specialized healthcare differ from general hospitals. Brand matters more when outcomes are life-or-death. Clinical expertise cannot be built overnight—training a competent oncologist takes 10+ years. Equipment requirements create barriers to entry—a basic oncology setup requires ₹50+ crore investment. These factors provide moats for established players like HCG.

The specialized versus multispecialty debate continues to rage. Large hospital chains argue that comprehensive care under one roof offers convenience and better coordination. HCG counters that specialization enables deeper expertise, better outcomes, and paradoxically, lower costs through focused operations. The market seems to be voting for specialization—focused players in oncology, cardiology, and orthopedics are growing faster than generalists.

Technology disruption is reshaping competitive dynamics. Precision medicine—treatment tailored to tumor genetics—advantages players with diagnostic capabilities and data analytics expertise. Immunotherapy, which harnesses the immune system against cancer, requires different infrastructure than traditional chemotherapy. Proton therapy, though expensive, offers superior outcomes for certain cancers. HCG's scale allows investments in these technologies that smaller players cannot match.

Geographic white spaces remain abundant. Tier-3 and tier-4 cities, home to 40% of India's population, have virtually no organized cancer care. State capitals in North-East India, despite high cancer incidence, lack comprehensive treatment facilities. Even in metros, capacity constraints mean weeks-long waiting lists for radiation therapy. HCG's expansion pipeline targets these underserved markets where competition is minimal and impact is maximal.

The regulatory environment adds complexity. The Atomic Energy Regulatory Board (AERB) controls licensing for radiation equipment—a process requiring 6-12 months and substantial documentation. State governments regulate hospital operations with varying standards and requirements. Drug pricing controls affect chemotherapy economics. Clinical trial regulations impact access to innovative therapies. Navigating this regulatory maze advantages experienced operators.

Reimbursement evolution is reshaping the industry. Government insurance schemes like Ayushman Bharat cover basic cancer treatment but not expensive targeted therapies. Private insurance is expanding coverage but with caps and exclusions. Out-of-pocket spending remains substantial, limiting access for middle and lower-income patients. HCG's diversified payer mix and operational efficiency allow it to serve both paying and subsidized patients profitably.

The talent war intensifies as the industry expands. India produces only 75 oncologists annually, far below requirement. Nurses trained in chemotherapy administration are scarce. Radiation physicists and technicians command premium salaries. HCG's training programs and brand equity provide advantages, but talent remains the binding constraint on growth.

International benchmarking reveals both gaps and opportunities. India's five-year cancer survival rates lag developed countries by 20-30 percentage points, primarily due to late detection. Per capita spending on cancer care is 1/50th of the US levels. These gaps represent massive growth potential as awareness increases, incomes rise, and insurance expands. HCG's positioning at the quality-accessibility intersection captures this growth.

New entrants are experimenting with disruptive models. Digital health startups offer second opinions and care coordination. Pharmacy chains are adding chemotherapy day-care centers. Diagnostic chains are backward integrating into treatment. While these models may capture certain segments, the complexity of comprehensive cancer care provides defensibility for integrated players like HCG.

X. Playbook & Investment Lessons

The HCG story offers a masterclass in building specialized healthcare at scale in emerging markets. The playbook that emerged—through trial, error, and iteration—provides lessons that transcend healthcare and geography.

Lesson 1: Focus Beats Diversification (Until It Doesn't)

HCG's laser focus on oncology for its first two decades enabled deep expertise and operational excellence. The company resisted temptations to become another multispecialty chain. This focus created competitive advantages—clinical protocols optimized for cancer, equipment utilization maximized for oncology procedures, talent specialized in cancer care. However, the Milann acquisition showed that adjacent diversification can work when core capabilities translate. The lesson: focus on one vertical until you've achieved clear leadership, then expand into adjacent areas where your capabilities provide advantage.

Lesson 2: Capital Allocation in Capital-Intensive Industries

Healthcare is inherently capital-intensive—equipment, infrastructure, working capital. HCG learned through painful experience that growth must be balanced with returns. The pre-COVID expansion spree, funded primarily through debt, nearly killed the company. The CVC era brought discipline—expansion only when existing centers achieved target utilization, asset-light models where possible, partnerships instead of ownership for non-core assets. The key insight: in capital-intensive industries, return on capital employed (ROCE) matters more than growth rate.

Lesson 3: Managing Through Cycles

Healthcare demand seems non-cyclical—people get sick regardless of economic conditions. Yet HCG discovered healthcare has its own cycles. New center economics follow a J-curve—losses for 2-3 years before profitability. Technology cycles require periodic massive reinvestment. Regulatory cycles alter economics overnight. COVID showed that even essential services face disruption. The companies that survive and thrive build balance sheets for the trough, not the peak. They maintain financial flexibility to capitalize on distress opportunities. They view downturns as chances to gain share from weaker competitors.

Lesson 4: Private Equity as Catalyst, Not Savior

CVC and KKR brought more than capital—they brought operational discipline, governance structure, and strategic clarity. But private equity also brings pressure for exits, financial engineering, and short-term thinking. HCG navigated this by aligning on long-term value creation while delivering short-term wins. The company improved margins without compromising clinical quality. It expanded strategically rather than aggressively. It prepared for exit from day one of investment. The lesson: private equity works when operational improvement, not financial engineering, drives returns.

Lesson 5: Founder Transition as Opportunity

Dr. Ajaikumar's transition from executive chairman to non-executive role could have been traumatic. Instead, it became liberating. Freed from operational responsibilities, he could focus on clinical innovation and research—areas where his expertise added most value. Professional managers brought skills he lacked—financial sophistication, operational excellence, stakeholder management. The lesson: founders who gracefully transition to appropriate roles multiply enterprise value rather than destroy it.

Lesson 6: Technology Adoption Requires Business Model Innovation

HCG discovered that buying advanced equipment doesn't automatically translate to better outcomes or economics. The company had to innovate business models around technology. LINACs run extended hours required new staffing models. Precision medicine required educating doctors and patients about value. Digital health required changing patient behavior and clinical workflows. The insight: in emerging markets, technology adoption succeeds when accompanied by business model innovation that makes the technology accessible and valuable.

Lesson 7: Building Trust in Stigmatized Sectors

Cancer in India carried a stigma—patients hid diagnoses, families avoided discussion, society associated it with death. HCG had to build trust through radical transparency. Publishing outcome data, enabling second opinions, acknowledging limitations, celebrating survivors—these actions slowly changed perceptions. The company learned that in stigmatized sectors, brand building requires patience, authenticity, and consistent delivery. Trust, once earned, becomes an unassailable moat.

Lesson 8: Scaling Quality in Emerging Markets

The conventional wisdom suggests quality and scale are inversely related in emerging markets—grow fast or maintain standards, not both. HCG proved otherwise through systematic approaches. Standardized protocols ensured consistent care across centers. Technology enabled remote supervision and quality control. Training programs created talent pipelines. Outcome measurement created accountability. The playbook: codify excellence, then replicate ruthlessly while measuring obsessively.

Lesson 9: The Power of Ecosystem Thinking

HCG's evolution from hospital operator to ecosystem orchestrator multiplied value. The company didn't just treat cancer—it influenced the entire patient journey from prevention through survivorship. Partnerships with diagnostic companies enabled early detection. Collaboration with pharmaceutical companies improved drug access. Relationships with medical colleges created talent pipelines. Government partnerships expanded reach. This ecosystem approach created network effects that pure hospital operations couldn't achieve.

Lesson 10: Timing Market Evolution

HCG's success came from anticipating, not following, market evolution. The company built oncology capacity before insurance coverage expanded. It entered tier-2 cities before competition recognized opportunity. It invested in precision medicine before India understood personalized treatment. This anticipatory positioning required courage and capital but created first-mover advantages that proved durable. The lesson: in emerging markets, skate to where the puck is going, but be prepared for a longer wait than expected.

XI. Bear vs. Bull Case Analysis

The Bull Case: Riding Structural Tailwinds

The optimistic view on HCG rests on multiple structural growth drivers converging simultaneously. India's cancer incidence is growing at 11% annually, driven by aging demographics, lifestyle changes, and improved detection. With cancer becoming the second-leading cause of death in India, demand for specialized treatment will only accelerate.

HCG's market leadership position provides competitive advantages that compound over time. The company treats more cancer patients than any other private network, generating data and expertise that improve outcomes and attract more patients—a virtuous cycle. HCG works with more than 400 oncologists, creating network effects where the best talent attracts more talent.

KKR's operational expertise and capital access unlock value creation opportunities that were previously constrained. The firm's healthcare portfolio companies can provide synergies—medical device partnerships, technology solutions, operational best practices. KKR's brand equity helps in talent recruitment, partnership negotiations, and geographic expansion. The planned 900-bed expansion over 4-5 years will be executed with institutional rigor rather than entrepreneurial enthusiasm.

The tier-2/tier-3 city expansion strategy taps into India's next consumption wave. These markets offer attractive economics—lower real estate costs, limited competition, growing ability to pay, increasing insurance coverage. HCG's hub-and-spoke model is perfectly suited for these markets, providing sophisticated care without massive capital investment. As these cities grow and prosper, HCG's early presence creates lasting competitive advantages.

Technology leadership in precision oncology positions HCG for medicine's future. As cancer treatment shifts from one-size-fits-all to personalized therapy, HCG's diagnostic capabilities, data analytics, and clinical expertise become increasingly valuable. The company can charge premium prices for superior outcomes while improving cost-effectiveness through targeted treatment.

Rising insurance penetration democratizes access while improving HCG's economics. Government schemes like Ayushman Bharat are expanding coverage. Private insurance is growing at 15% annually. Corporate healthcare benefits are becoming standard. As insurance coverage expands, HCG's addressable market multiplies while payment certainty improves.

The international expansion opportunity remains largely untapped. Africa's cancer burden is growing rapidly with minimal infrastructure. The Middle East's Indian diaspora seeks quality care. Southeast Asia lacks specialized oncology centers. HCG's proven model can be replicated across emerging markets, creating new growth vectors beyond India.

The Bear Case: Structural Challenges Persist

The pessimistic view focuses on fundamental challenges that no amount of operational improvement can overcome. Healthcare in India remains a difficult business—capital-intensive, highly regulated, price-sensitive, and operationally complex. HCG's return on equity has historically been below cost of capital, raising questions about long-term value creation.

Competition from larger, better-capitalized players threatens HCG's market position. Apollo and Fortis have deeper pockets, broader networks, and diversified revenue streams. They can afford to lose money in oncology while subsidizing from profitable segments. International players entering through partnerships bring global best practices and deep expertise. Government hospitals, though inefficient, offer free or subsidized treatment that HCG cannot match.

The capital intensity problem has no easy solution. Each new comprehensive cancer center requires ₹100+ crore investment with 3-4 year payback periods. Medical equipment becomes obsolete quickly, requiring continuous reinvestment. Working capital needs are substantial due to insurance payment delays. This capital intensity limits return on invested capital and constrains growth without dilution or debt.

Execution risk in rapid expansion is substantial. Healthcare expansion isn't like opening retail stores—each hospital requires specialized talent, regulatory approvals, and community trust. HCG's track record shows new centers often take longer than expected to achieve profitability. The planned 900-bed expansion could strain management bandwidth and financial resources.

Regulatory and pricing pressures could compress margins. Government price controls on drugs and procedures limit pricing power. Insurance companies negotiate harder as they gain scale. Regulatory compliance costs keep rising. Any adverse regulatory change could significantly impact profitability.

Geographic concentration creates vulnerability. Despite national presence, HCG generates disproportionate revenues from South India. Cultural differences, language barriers, and regional competition make North and East India expansion challenging. Natural disasters, political instability, or regional economic downturns could disproportionately impact HCG.

The founder transition risk, while managed well so far, remains. Dr. Ajaikumar's vision and relationships built HCG. His transition to non-executive role, while necessary, removes day-to-day involvement from someone who understood the business intimately. Professional managers may optimize financials but lose the mission-driven culture that attracted talent and built trust.

Technology disruption could come from unexpected quarters. AI-powered diagnosis might reduce the need for specialists. Drug innovations might make radiation therapy obsolete. Home-based care models might reduce hospital utilization. While HCG invests in technology, disruptive innovations often come from outside established players.

The debt burden, though reduced, remains substantial. Interest coverage ratios are improving but still concerning. Any economic downturn or operational hiccup could stress debt service. Private equity ownership typically involves leverage, potentially adding more debt despite current improvements.

The Balanced View

Reality likely lies between these extremes. HCG operates in a structurally growing market with genuine competitive advantages, but faces real challenges in execution and competition. The company's success will depend on management's ability to execute expansion while maintaining quality, navigate competition while preserving margins, and adopt technology while controlling costs. KKR's involvement tips the odds toward success, but healthcare remains a difficult business where operational excellence matters more than financial engineering.

XII. Looking Forward & Closing Thoughts

As we stand in early 2025, HCG represents something larger than a corporate success story. It embodies the transformation of Indian healthcare from a cottage industry to institutional excellence. The company that started with one doctor's vision of bringing world-class cancer care to India now treats over 500,000 patients annually, employs thousands, and sets clinical standards that others follow.

The future of cancer care in India will be shaped by three forces, and HCG is positioned at the intersection of all three. First, the epidemiological transition—as India becomes wealthier, cancer shifts from being a disease of the elderly to affecting younger populations, requiring different treatment approaches and longer-term care. Second, the technological revolution—AI, genomics, and immunotherapy are transforming cancer from a death sentence to a manageable chronic disease. Third, the accessibility imperative—making quality cancer care available beyond metros to the 70% of Indians living in smaller cities and rural areas.

HCG's role in democratizing specialty healthcare extends beyond business metrics. In tier-2 cities like Nashik or Cuttack, HCG centers have become anchors of hope. Families that would have given up now have access to the same protocols used in Mumbai or Bangalore. Young oncologists who would have migrated abroad or to metros now build careers in their hometowns. The multiplier effects—economic, social, psychological—ripple through communities.

Post-KKR acquisition, several metrics will determine HCG's trajectory. Utilization rates at new centers—the speed at which they reach 70%+ occupancy—will indicate execution capability. EBITDA margin expansion while maintaining quality will show operational excellence. Success in international markets will demonstrate model portability. Most critically, clinical outcomes—survival rates, patient satisfaction, treatment innovations—will determine whether HCG remains a leader or becomes another hospital chain.

The lessons for healthcare entrepreneurs and investors are profound. Building healthcare businesses in emerging markets requires patient capital, operational excellence, and missionary zeal. The winners won't be those who financialize healthcare but those who solve real problems—access, quality, affordability—at scale. The HCG journey shows that specialized focus, carefully executed, can create more value than diversified approaches.

Looking ahead, several questions will shape HCG's next chapter. Can the company maintain its clinical edge while scaling rapidly? Will international expansion create new growth engines or dilute focus? How will the competitive landscape evolve as healthcare consolidates? Can HCG pioneer new business models that make cancer care truly accessible to all Indians, not just those who can afford it?

The broader implications for Indian healthcare are significant. HCG's success has inspired dozens of entrepreneurs to build specialized healthcare businesses—diabetes chains, dialysis networks, mental health platforms. The institutionalization of healthcare, led by companies like HCG, is professionalizing a sector long dominated by individual practitioners and family-run hospitals. The entry of sophisticated investors like KKR signals healthcare's maturation as an asset class.

Yet challenges remain daunting. India spends just 3.5% of GDP on healthcare versus 8-10% in developed countries. The doctor-to-patient ratio remains abysmal. Insurance penetration, though growing, covers less than 30% of the population. These gaps represent both opportunity and responsibility for companies like HCG.

The ultimate measure of HCG's success won't be financial returns or market capitalization. It will be the millions of lives extended, families kept together, and hope restored. In a country where cancer was once whispered about in hushed tones, HCG has helped make it a disease that can be discussed, treated, and increasingly, survived.

As Dr. Ajaikumar transitions to his new role, focusing on research and clinical excellence, he leaves behind more than a company—he leaves a template for building world-class healthcare in challenging markets. The boy from Karnataka who trained at MD Anderson and returned to transform Indian oncology has proven that with vision, persistence, and the right partners, healthcare in emerging markets can match global standards.

The HCG story is far from over. With KKR's resources, operational expertise, and global network, the company stands poised for its next phase of growth. Whether it becomes India's first truly global healthcare company, pioneers new models of cancer care, or stumbles under the weight of expectations remains to be seen. What's certain is that HCG has already transformed Indian cancer care and will continue shaping its future.

For investors, HCG represents a compelling but complex opportunity. The structural growth drivers are undeniable. The execution challenges are real. The competitive dynamics are intensifying. The regulatory environment remains uncertain. Success requires not just capital but deep understanding of healthcare's unique dynamics—where doing good and doing well must align for sustainable value creation.

The final reflection brings us back to that Mumbai boardroom where KKR signed the deal. This transaction represents more than private equity's next healthcare bet. It symbolizes the maturation of Indian healthcare, the globalization of emerging market companies, and the increasing sophistication of specialized medicine. Most importantly, it represents hope—hope that quality healthcare can be accessible, that Indian companies can achieve global standards, and that business can be a force for social good.

The story of HealthCare Global Enterprises is, ultimately, a human story—of patients fighting disease, doctors battling odds, entrepreneurs building dreams, and investors betting on transformation. It's a story that continues to unfold, shaped by forces larger than any individual or institution. As India rises, as cancer increases, as technology advances, HCG stands at the crossroads, ready to write its next chapter. The question isn't whether the opportunity exists—it's whether the execution can match the ambition. Time, as always in healthcare, will tell.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube