HBL Engineering: The Deep-Tech Powerhouse Behind India's Railways and Defense

I. Introduction & Episode Roadmap

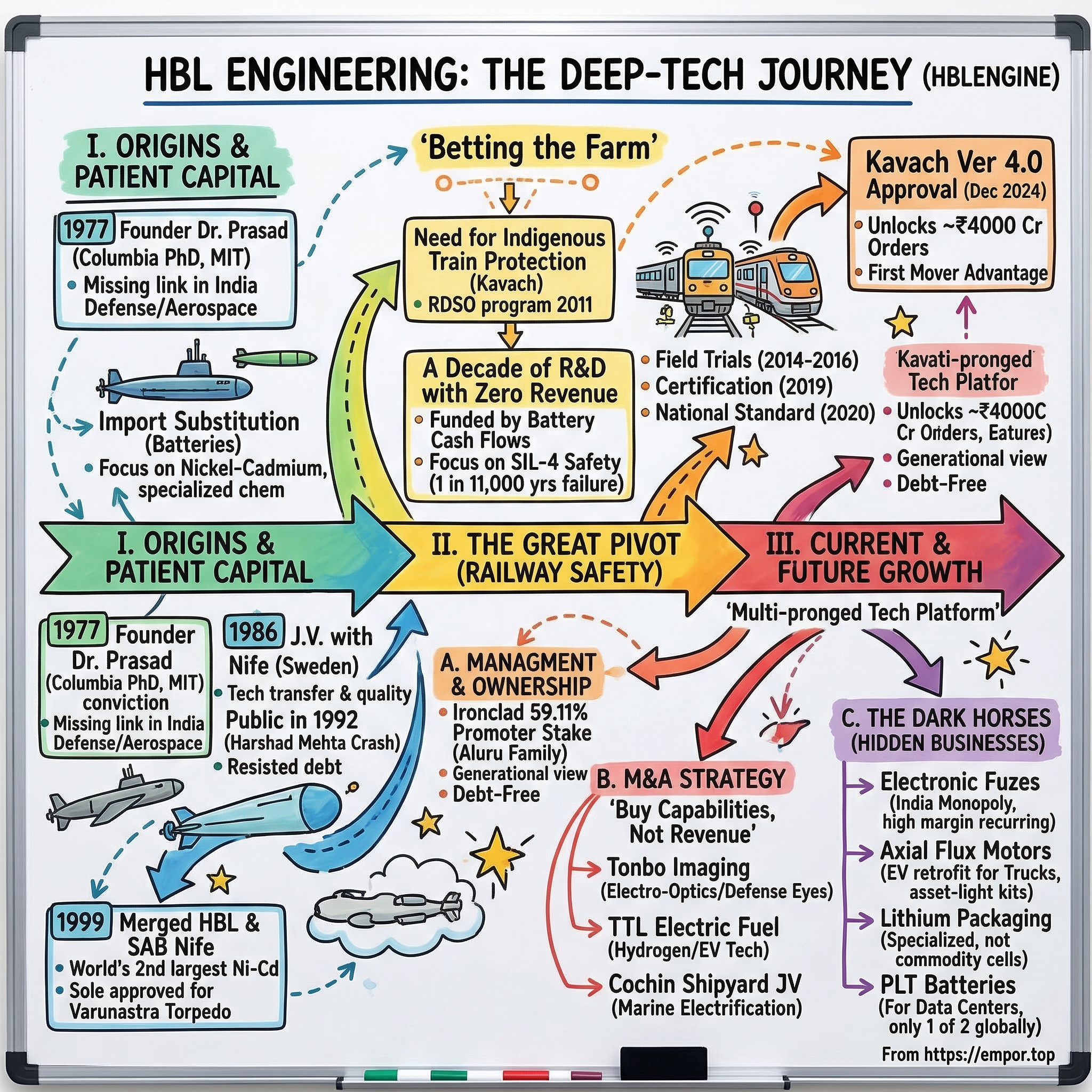

Picture this. It is a sweltering afternoon in December 2024, and somewhere in the labyrinthine corridors of India's Railway Board in New Delhi, a quiet notification lands on a bureaucrat's desk. HBL Engineering Limited—a company most casual investors had never heard of—has just become the first entity in India to receive RDSO approval for Kavach Version 4.0, the most advanced indigenous train collision avoidance system ever certified in the country. The approval unlocked a pipeline worth nearly four thousand crore rupees in pending orders. And with it, a forty-seven-year-old battery company from Hyderabad completed what might be the most improbable corporate metamorphosis in modern Indian industrial history.

How did this happen? How did a company that spent decades making nickel-cadmium batteries for submarines and torpedo propulsion systems end up becoming the indispensable linchpin of India's entire railway safety architecture? And why did nobody—not the sell-side analysts, not the institutional investors, not even most retail shareholders—see it coming until the stock had already multiplied several times over?

The answer lies in a story that is quintessentially Indian in its patience, its ambiguity, and its eventual payoff. It is the story of a founder who earned a doctorate from Columbia University and degrees from MIT and IIT Kharagpur, then returned to Hyderabad in the late 1970s with a singular, almost stubborn thesis: India's defense and aerospace sectors had critical technology gaps, and someone needed to fill them from scratch, without relying on foreign license agreements that could be revoked at geopolitically inconvenient moments. That founder, Dr. Aluru Jagadish Prasad, is still at the helm nearly five decades later, and the company he built is now a roughly eighteen-thousand-crore-rupee enterprise sitting at the intersection of three of the most powerful macro tailwinds in India—railway modernization, defense indigenization, and commercial vehicle electrification.

But perhaps the most telling signal of this transformation came not from any order book or earnings call, but from a seemingly mundane corporate action in November 2024: the company changed its name. HBL Power Systems Limited became HBL Engineering Limited. On paper, it was just a regulatory filing. In practice, it was a declaration of victory—an acknowledgment that the company had outgrown its identity as a battery manufacturer and was now, definitively, an IP-led industrial technology company. When a forty-seven-year-old company bothers to change its name, it is worth paying attention to what it is trying to tell you.

This deep dive will trace the full arc of that transformation. We will start with the origin story—a contrarian founder, Swedish joint ventures, and the painstaking process of becoming one of only two companies on the planet capable of manufacturing certain types of nickel-cadmium batteries at scale. Then we will spend considerable time on the Kavach inflection point, arguably the single most consequential product bet in the company's history, and one that took over a decade of zero-revenue R&D to realize. We will examine the management team, their ownership incentives, and why they have chosen to remain virtually debt-free despite massive capital expenditure requirements. We will unpack an M&A strategy that is surgical rather than scattershot, and we will reveal the "hidden" businesses—electronic fuzes, axial flux motors, electric drivetrain retrofits—that are growing fast but remain largely invisible in the consolidated numbers. Finally, we will stress-test the entire thesis with a rigorous bull-and-bear analysis, and extract the playbook lessons that make HBL a case study in building sovereign industrial capabilities.

Let us begin where all good origin stories begin—with a young man, a conviction, and a city that nobody associated with deep technology.

II. Origins & The "Patient Capital" Era (1977–2000s)

In 1977, Hyderabad was not the gleaming IT hub it would become two decades later. It was a quieter city, known for its Nizami heritage, its biryani, and its sprawling Osmania University campus. India itself was in the grip of the License Raj—the labyrinthine system of industrial permits and government approvals that made starting a manufacturing business an exercise in bureaucratic endurance. The Emergency had ended just months earlier. Capital markets were rudimentary. Foreign exchange was scarce. The idea that this city, in this country, at this moment, would become home to one of the world's most specialized defense battery manufacturers would have seemed absurd to anyone except, perhaps, Dr. Aluru Jagadish Prasad.

Prasad's journey to founding Hyderabad Batteries Limited—the original incarnation of what would become HBL Engineering—is itself a study in the kind of intellectual ambition that defined a particular generation of Indian technologists. After completing his undergraduate studies at IIT Kharagpur, one of India's premier engineering institutions, he went on to earn a graduate degree from MIT and then a doctorate from Columbia University in New York. These were not casual educational pursuits—this was a man who had trained at three of the most demanding technical institutions in the world, absorbing the best of American and Indian engineering traditions. He could have stayed in the United States. Many of his peers did. The brain drain of the 1970s was relentless, and opportunities for deep-tech entrepreneurs in India were, to put it charitably, limited.

But Prasad saw something that most people did not. He recognized that India's defense establishment—the military, the navy, the air force—was almost entirely dependent on imported batteries for its most critical applications. Submarine propulsion batteries, aircraft starting batteries, torpedo power systems—all of these came from foreign suppliers, primarily European ones.

And that dependency created a vulnerability that went far beyond economics. India had learned this lesson painfully during the 1965 and 1971 wars, when arms embargoes by Western nations exposed the country's catastrophic dependence on imported defense equipment. In a world where geopolitical alliances could shift overnight, relying on a Swedish or French company to supply the batteries that powered your submarine fleet was not just expensive—it was strategically dangerous. One diplomatic crisis, one sanctions regime, one export control decision by a foreign government, and your submarine fleet could be grounded for lack of replacement batteries.

So in 1977, with modest capital and enormous conviction, Prasad founded Hyderabad Batteries Limited. The early years were grinding, in ways that are difficult to appreciate from the vantage point of today's startup culture.

Building a battery company is not glamorous work. It involves mastering electrochemistry—understanding how different metals and electrolytes interact at the molecular level to store and release energy. It requires metallurgy—knowing how to alloy, sinter, and plate metals to create electrode structures that can withstand thousands of charge-discharge cycles without degrading. It demands precision manufacturing—tolerances measured in microns, contamination controls that rival semiconductor fabrication, quality assurance processes that must account for the fact that a battery failure in a submarine or a fighter jet could cost lives.

And then, beyond all the technical challenges, there was the uniquely Indian obstacle: navigating the byzantine procurement processes of the Indian Ministry of Defence. The lead times were measured not in quarters but in years. You develop a product, you submit it for testing, you wait for approval, you get rejected, you modify, you resubmit. The cycle could take five to seven years for a single product line. And at the end of that process, your reward was a government contract with thin margins and long payment cycles. This was not a business for anyone seeking quick returns.

The breakthrough came in 1986 with a pivotal joint venture with Nife of Sweden. Nife was one of Europe's leading nickel-cadmium battery manufacturers, and the partnership gave HBL access to critical manufacturing know-how that would have taken years to develop independently. The entity was incorporated as SAB Nife Power Systems Limited, and it represented a classic technology-transfer arrangement of the era: the Swedish partner provided the initial intellectual property and process expertise, while the Indian partner provided the manufacturing base, the labor force, and—crucially—the relationships with Indian defense procurement agencies.

This joint venture was the crucible in which HBL's culture was forged. From Nife, the company absorbed Scandinavian precision in manufacturing processes and quality control. From Prasad's vision, it inherited a relentless focus on import substitution—not as a protectionist exercise, but as a genuine capability-building endeavor. The combination proved formidable.

In February 1992, the company went public to finance its diversification into uninterrupted power systems. The timing of this public issue deserves its own paragraph, because it encapsulates the kind of market chaos that forges a founder's financial philosophy for life.

February 1992 was, arguably, the single best moment in Indian capital market history to sell shares to the public. The Bombay Stock Exchange Sensex had been on a tear, driven by the legendary (and soon-to-be-infamous) stockbroker Harshad Mehta, who was systematically manipulating the market using fraudulent bank receipts to fund massive stock purchases. The euphoria was intoxicating. IPOs were being lapped up by investors with an appetite for risk that bordered on clinical delusion. Industrial companies, technology companies, it did not matter—anything with an IPO document was being subscribed multiple times over. HBL's public issue went through successfully, riding this wave of irrational exuberance.

Then came the crash. By April 1992, investigative journalism had begun exposing Mehta's scheme. By July 1992, the full extent of the scam was public knowledge—roughly five thousand crore rupees in fraudulent transactions, a figure that was staggering for the time. The market collapsed. The Sensex lost nearly half its value. Investor confidence did not just erode—it evaporated. For context, the devastation of July 1992 ranks alongside October 2008 (the Global Financial Crisis) and March 2020 (COVID-19) as one of the three worst periods in Indian market history. Companies that had raised capital at peak valuations suddenly found themselves with furious public shareholders, cratered stock prices, and a market environment that was openly hostile to industrial IPOs for years afterward.

HBL survived. But the experience appears to have permanently imprinted on Prasad a deep-seated conservatism about leverage, external capital, and the fickleness of public markets. It is not coincidental that, three decades later, the company remains virtually debt-free and has never returned to the equity markets for another capital raise. When you have lived through the Harshad Mehta crash as a freshly public company, you learn to fund your own ambitions.

In 1999, the company completed a defining corporate restructuring: the merger of the original Hyderabad Batteries Limited (incorporated in 1977) with SAB Nife Power Systems Limited (incorporated in 1986) into a single consolidated entity. This was not merely an administrative exercise. It eliminated the complexity of running two parallel organizations with overlapping product lines and consolidated all of HBL's battery technology—lead-acid, nickel-cadmium, silver-zinc, and emerging lithium chemistries—under one roof.

By the early 2000s, HBL had quietly achieved something remarkable. It had become the world's second-largest manufacturer of nickel-cadmium batteries, behind only Saft of France. Its products powered some of the most critical defense platforms in India's arsenal: the Sintered Plate Nickel-Cadmium batteries that started Indian Air Force fighter jets, the propulsion batteries for India's Kilo-class submarines (originally Russian-designed boats that formed the backbone of the Indian Navy's conventional submarine fleet), and the silver-zinc batteries that powered the Varunastra—India's indigenously developed heavyweight torpedo. When Varunastra was handed over to the Indian Navy for service induction, HBL's batteries were the only ones approved for use. Not a foreign supplier's. HBL's.

These were not commodity products, and the distinction is critical for understanding HBL's moat.

A submarine battery is not a bigger version of a car battery. It is an engineering marvel that must deliver massive amounts of power—enough to propel a three-thousand-ton vessel through water—reliably, silently, and safely in an enclosed, pressurized environment where any leakage of hydrogen gas (a natural byproduct of battery charging) could cause a catastrophic explosion. The battery must function in extreme temperatures, withstand the shock of depth-charge detonations, tolerate vibrations that would shake most electronic equipment apart, and recover from deep-discharge cycles that would destroy a conventional battery.

The qualification process is correspondingly brutal. A battery designed for submarine use must undergo years of testing under simulated combat conditions. Temperature cycling from minus twenty to plus fifty-five degrees Celsius. Shock resistance testing at forces that would flatten a human body. Vibration tolerance across the full spectrum of frequencies a submarine encounters in operation. And then, after the laboratory testing, there are sea trials—actual deployments on submarines where the battery's performance is monitored under real operational conditions.

The barriers to entry are not just technical; they are institutional. Once a navy qualifies a battery supplier—a process that can take five to eight years from initial sample submission to full qualification—switching costs are enormous. You do not casually replace the power source of a billion-dollar submarine. The incumbent supplier has an almost insurmountable advantage, because the navy would need to repeat the entire multi-year qualification process with a new supplier, during which time it cannot guarantee the reliability of its submarine fleet.

This was the foundation—two decades of patient, unglamorous work in some of the most demanding applications in the world. No venture capital, no frothy tech-market excitement, no media coverage. Just a company in Hyderabad quietly becoming irreplaceable to the Indian defense establishment, one battery chemistry at a time. But by the mid-2000s, Prasad was already looking beyond batteries. He understood, perhaps earlier than anyone in his industry, that batteries were fundamentally a chemical hardware business with natural margin ceilings. Electrochemistry could sustain the company, but it could not transform it. For that, HBL would need to make a bet so large and so risky that it would either define the company's next four decades or destroy the value built in the first three.

That bet was called TCAS. And it would take a decade of faith, frustration, and near-zero revenue before it paid off.

III. The Great Pivot: Betting the Farm on Railway Safety

To understand why HBL's pivot into railway electronics was so audacious, you first need to understand what the company was pivoting away from. By the late 2000s, HBL Power Systems was a profitable, stable, and thoroughly unglamorous company. Its battery business—spanning industrial lead-acid, nickel-cadmium, and specialty defense batteries—generated reliable cash flows but operated in a world of thin margins, intense competition in commodity segments, and long payment cycles from government customers. The company was, to borrow a metaphor, a well-maintained locomotive running on a track that led somewhere comfortable but ultimately limited.

Prasad and his team saw the ceiling. Batteries, no matter how specialized, are physical products governed by the unforgiving economics of raw material costs, manufacturing yields, and commodity pricing cycles. Lead prices go up, your margins go down. A competitor in China scales up nickel-cadmium production, your export pricing comes under pressure. The intellectual property moats in battery chemistry, while real, were eroding as manufacturing techniques became more widely disseminated.

There is a useful analogy here. Think of the difference between a construction company that builds houses and a company that designs the architectural software used to plan those houses. Both are in "construction," but their economics are fundamentally different. The construction company's revenue scales linearly with materials and labor—it earns a fixed margin on every brick laid. The software company's revenue scales with licenses sold—once the code is written, each additional sale is almost pure profit. HBL, in its battery incarnation, was the construction company. It needed to become the software company.

But what software? What IP-intensive product could a battery manufacturer credibly develop?

The answer came from an unlikely place: the Indian Railways.

The Indian Railways is one of the world's largest and most complex rail networks. Over sixty-eight thousand kilometers of track. More than thirteen thousand trains operating daily. Over twenty-three million passengers carried every single day. And a safety record that was, to put it diplomatically, a source of national embarrassment and periodic political crisis.

Train collisions and derailments killed hundreds of people every year. Every major accident triggered a cycle of media outrage, ministerial promises, committee reports, and eventually, nothing. The problem was not a lack of awareness—everyone knew the network needed an automatic train protection system. The problem was that no Indian company had the capability to build one. And importing European systems like ETCS (European Train Control System) was prohibitively expensive for the scale of India's network. ETCS was designed for European rail systems with their relatively contained scale; deploying it across sixty-eight thousand kilometers of Indian track, with its unique gauge, signaling legacy, and operational complexity, would have cost tens of billions of dollars. The government needed an indigenous solution, at a fraction of the cost, that could be manufactured at scale domestically.

In 2011, the Research Designs and Standards Organisation—RDSO, the technical arm of the Indian Railways—initiated a program to develop an indigenous Train Collision Avoidance System, or TCAS.

The choice of RDSO as the lead agency was itself significant. RDSO is not a procurement body; it is a standards and research organization. Its role was to define the specifications, oversee the development process, and ultimately certify the finished product. This meant that the development partners would not be building to a fixed, detailed blueprint—they would be co-developing the specification alongside RDSO, iterating on requirements as field testing revealed new challenges. It was a collaborative, open-architecture development model, more akin to how DARPA works in the United States than how traditional Indian government procurement operates.

Three companies were selected as development partners: HBL Power Systems, Medha Servo Drives, and Kernex Microsystems. All three were Hyderabad-based firms, which tells you something about the concentration of defense and railway electronics expertise in the city—a legacy of institutions like DRDO, ECIL, and BDL that had been based there for decades, creating a dense ecosystem of engineering talent and suppliers. Each company would independently develop its own version of the system, and RDSO would evaluate and certify whichever met its stringent requirements.

For HBL, this was the bet—the single largest strategic wager in the company's history.

The company committed significant R&D resources—engineering talent, capital, management attention—to a project that had no guaranteed revenue, no fixed timeline, and a customer (the Indian Railways) that was notorious for bureaucratic delays, shifting specifications, and political interference. There was no contract guaranteeing that HBL would ever receive a production order. The development program was, in effect, a decade-long job interview with the world's largest railway bureaucracy, and there was no guarantee of getting the job at the end.

The decade that followed was, by any reasonable measure, agonizing.

Consider what TCAS—later renamed Kavach, the Hindi word for "armor"—actually requires. It is not a simple sensor or a single piece of software. It is a complete, integrated ecosystem of technologies that must work in perfect concert.

At the trackside level, Kavach requires radio frequency identification (RFID) tags embedded in the track at regular intervals, acting as digital mile markers that allow onboard systems to know precisely where a train is located. It requires stationary radio towers that continuously broadcast information about signal status, track conditions, and the locations of other trains in the zone.

At the locomotive level, each train must be equipped with an onboard computer that fuses data from multiple sources—GPS positioning, RFID tag readings, radio communications from trackside equipment—to build a real-time picture of its position and the positions of every other train in the vicinity. The computer must continuously calculate whether a collision scenario is developing and, if so, first warn the driver and then, if the driver does not respond, automatically apply the brakes. This override function—taking control of a train away from a human driver—is both the most critical and the most controversial aspect of the system.

All of this must function reliably in the Indian operating environment, which is among the most challenging in the world for electronic systems. Monsoon rains that can dump two hundred millimeters of water in a single day. Summer temperatures that routinely exceed forty-five degrees Celsius. Dust storms that deposit fine particulate matter on every exposed surface. Electromagnetic interference generated by an aging electrical grid, by mobile phone towers, by the electric traction systems of the trains themselves. And it must do all of this with near-zero tolerance for error, because a false negative—a collision that the system fails to prevent—could kill hundreds of people.

This is where the concept of Safety Integrity Level 4, or SIL-4, becomes central to the story, and it is worth explaining in detail because it is the single most important technical barrier protecting HBL's competitive position.

Safety Integrity Levels are defined by international standards used in railway signaling—specifically the CENELEC EN 50126 (which covers specification and demonstration of reliability, availability, maintainability, and safety), EN 50128 (software standards for railway control and protection systems), EN 50129 (safety-related electronic systems for signaling), and EN 50159 (safety-related communication in railway systems). There are four levels, SIL-1 through SIL-4, with SIL-4 being the highest.

Think of it this way. SIL-1 is the level of safety you would expect from a household appliance—a washing machine that stops if the door opens. SIL-4 is the level of safety you demand from a nuclear reactor's emergency shutdown system. To achieve SIL-4 certification, a system must demonstrate a probability of dangerous failure of less than one in one hundred million per hour of operation. In practical terms, this means that if you ran the system continuously for eleven thousand years, you would expect it to have a single dangerous failure. One. In eleven thousand years.

What does this require in practice? It means that every single line of software code must be formally verified—not just tested, but mathematically proven to behave correctly under all possible input conditions. Every hardware component must have redundant backups, and the redundancy architecture must be designed so that no single point of failure can compromise the system. Every communication protocol must be encrypted, authenticated, and designed to fail safely if the communication channel is disrupted. Every possible failure mode—and in a complex electronic system, there are thousands—must be identified, analyzed, and mitigated. The documentation alone for a SIL-4 certification can fill rooms. The testing and validation process takes years. And the entire process must be verified by an independent safety assessor with no commercial relationship to the developer.

For any software engineer accustomed to the "move fast and break things" ethos of Silicon Valley, SIL-4 certification represents an almost incomprehensibly different approach to building technology. You cannot deploy, observe, and iterate. You must get it right the first time, every time, because failure means a train collision.

HBL spent years in the development and testing loop. Field trials commenced in 2014, initially on short sections of track in controlled environments. The first experiments on actual passenger trains came in February 2016—a milestone that sounds routine but represented years of prior engineering work to reach the point where the system was reliable enough to be trusted on a train carrying real people.

Then the cycle of iteration began. The system was tested, and problems were discovered. Communication protocols that worked in the laboratory failed in the field due to electromagnetic interference from overhead power lines. GPS accuracy degraded in tunnels and deep cuttings. Software edge cases that no one had anticipated in the design phase emerged during real-world operation. Each problem required engineering solutions, which required testing, which revealed new problems.

Specifications changed. RDSO added requirements as its own understanding of the system's operational environment deepened. Political priorities shifted—new Railway Ministers, new committees, new mandates, each with slightly different visions of what the system should do. Through it all, HBL's legacy battery business—the "boring" cash cow that generated steady if unspectacular margins—funded the entire R&D effort. This is a pattern worth highlighting: the ability to fund a decade of zero-revenue moonshot R&D using cash flows from an established business is one of the most underappreciated advantages of patient, founder-led companies. Amazon used its e-commerce cash flows to fund AWS. Berkshire Hathaway used its insurance float to fund acquisitions. HBL used its battery cash flows to fund Kavach. The mechanism is the same: a stable, profitable core business provides the financial runway for a transformative bet.

The certification milestone came in 2019, when Kavach received SIL-4 certification, confirming compliance with the full suite of European safety standards. In July 2020, the Ministry of Railways adopted Kavach as the National Automatic Train Protection System. This was the moment the decade of investment began converting into commercial reality.

But the real breakthrough—the moment that separated HBL from its competitors—came with Version 4.0. While all three original development partners had contributed to earlier versions of Kavach, HBL became the first company to receive RDSO approval for Kavach Version 4.0, the latest and most advanced iteration of the system. This approval was not ceremonial; it was the regulatory prerequisite for HBL to begin delivering against its accumulated order book. Without it, orders worth thousands of crores would have remained on paper.

And what an order book it was. The numbers tell the story of a complete financial transformation. In December 2024, HBL secured a landmark order worth approximately fifteen hundred and twenty-two crore rupees from Chittaranjan Locomotive Works for the supply and installation of onboard TCAS equipment in 2,200 locomotives, with an execution timeline of twelve months. This was followed by an eight-hundred-crore-rupee order from Banaras Locomotive Works, a five-hundred-and-seventy-five-crore-rupee order from Integral Coach Factory in Chennai, and a one-hundred-and-thirty-three-crore-rupee contract from South Central Railway for deploying Kavach across the Vijayawada-Ballarshah section. By early 2026, HBL's accumulated Kavach order book had swelled to approximately thirty-eight hundred and sixty-five crore rupees—a staggering figure for a company whose entire annual revenue in FY2024 was around twenty-two hundred crores.

The financial implications are profound, and they illustrate a concept that is worth dwelling on: the difference between selling atoms and selling certified intelligence. A nickel-cadmium battery is, ultimately, a container of chemicals. Its price is bounded by raw material costs on the floor and by competitive alternatives on the ceiling. A Kavach onboard unit is a box of electronics whose value derives not from the silicon and copper inside it, but from the years of R&D, the SIL-4 certification, and the institutional relationships that went into creating it. The bill of materials for a Kavach unit is a fraction of its selling price; the rest is pure intellectual property margin.

Battery manufacturing, even for specialized defense applications, typically operates at EBITDA margins in the low-to-mid teens. Electronics and signaling systems, particularly those with proprietary IP and SIL-4 certification, can command margins in the high teens to low twenties—and in some cases, significantly higher. As Kavach revenue ramps up and becomes a larger share of the consolidated mix, HBL's blended margins are structurally shifting upward. This is not a cyclical improvement driven by favorable commodity prices or a one-time order. It is a permanent change in the company's economic engine, driven by a fundamental shift from selling physical hardware to selling certified intellectual property.

The numbers are already confirming this thesis. In the quarter ending June 2025, HBL reported revenue of approximately six hundred and twenty-one crore rupees—a twenty-nine percent sequential increase from the March quarter. But the real story was in the margins: EBITDA roughly doubled from the prior quarter, and net profit margins expanded to over thirty-one percent. That is not a battery company's margin profile. That is an IP company's margin profile. And it is only the beginning of the mix shift.

The scale of the opportunity ahead remains enormous, and the numbers are worth spelling out because they define the size of HBL's addressable market for the next half-decade.

The Indian government has set an ambitious target: deploying Kavach across approximately forty-four thousand kilometers of railway track by 2030, with an initial batch of ten thousand locomotives to be fitted with onboard equipment and another ten thousand to follow in a phased manner, with all work expected to be completed within four years. This timeline was actually accelerated from the original 2035 target following several high-profile train accidents that generated intense political and public pressure to improve railway safety.

As of early 2026, only about thirteen hundred route kilometers had been commissioned with Kavach Version 4.0, and approximately four thousand locomotives had been fitted with onboard units. The arithmetic is stark: more than forty-two thousand kilometers remain to be covered, and more than sixteen thousand locomotives remain to be fitted. This gap represents years of sustained, high-visibility procurement spending, and HBL—as the first company to receive Kavach 4.0 certification—is positioned as the prime beneficiary of a multi-year deployment cycle that is, for all practical purposes, irreversible.

But the Kavach story was never the only story. Even as the railway safety business was consuming management attention and investor imagination, HBL was quietly building several other businesses that, in their own right, could justify significant value. To understand those, we first need to understand who is actually running this company and what motivates them.

IV. Current Management, Ownership & Incentives

In an era when corporate India is increasingly characterized by professional management teams, revolving-door CEOs, and activist shareholders demanding quarterly results, HBL Engineering represents a throwback to a different model of capitalism—one where the founder is still in charge, the family owns a commanding stake, and the time horizon for strategic decisions is measured in decades rather than quarters.

Dr. Aluru Jagadish Prasad remains the Executive Chairman and Managing Director. At an age when most founders have long since handed over operational control, Prasad continues to be actively involved in the company's strategic direction. But this is not a case of a founder who cannot let go. Rather, Prasad has spent the past decade deliberately architecting the transition from a battery company to an engineering and electronics enterprise, a transformation that required his personal credibility and institutional relationships to execute. When you are asking the Indian Railways to trust your company with a safety-critical system that will protect millions of passengers, the fact that the same person who has been supplying submarine batteries to the Indian Navy for three decades is personally vouching for the product carries enormous weight.

The execution team around Prasad reflects the company's dual identity as both a family enterprise and a professionally managed operation. M.S.S. Srinath serves as a Whole-Time Director and has been instrumental in scaling the electronics and defense segments. His role is particularly important in the current phase, as the company transitions from R&D and certification to high-volume production and delivery—a transition that requires a different set of operational skills than the patient development work that characterized the Kavach journey.

Kavita Prasad Aluru, who represents the next generation of the founding family, was appointed to the board in 2018 and plays a role in driving the execution of the massive railway and defense order books. Her involvement is significant not just operationally but symbolically: it signals that the Aluru family views HBL as a multi-generational enterprise, not a single-founder company that will be sold or wound down when the patriarch retires.

The combination of family continuity and professional depth is a governance model that, when it works well, can be extraordinarily effective—and when it works poorly, can be a disaster. Indian corporate history is littered with examples of both outcomes. In HBL's case, the evidence so far suggests it is working: the company has successfully navigated the most complex product development program in its history (Kavach), maintained financial discipline throughout, and is now executing against its largest-ever order book.

The ownership structure tells you everything about the company's incentive alignment.

The promoters—primarily through the Aluru Family Private Trust, with Kavita Prasad Aluru as the largest individual shareholder at approximately fifty-one percent—hold an ironclad 59.11 percent stake in the company. To put this in context, most Indian mid-cap companies have promoter holdings in the thirty-to-fifty percent range, and many have seen their promoter stakes gradually dilute over the years as founders sell shares to fund personal expenses, family disputes, or diversification into unrelated businesses. The Aluru family has done none of this. Their stake has remained rock-solid for years. This is not a promoter group that is diluting its holding to fund growth or selling shares in block deals to institutional investors. They are in for the long haul—generationally.

What does this mean practically? It means that HBL's management does not optimize for quarterly earnings-per-share growth or worry excessively about short-term stock price movements. When the company decided to fund a decade of Kavach R&D with battery cash flows—a decision that depressed reported profitability for years—that decision was not second-guessed by activist shareholders demanding the capital be returned as dividends.

When HBL chose to remain virtually debt-free—carrying debt at roughly 0.05 times equity, which is essentially zero—despite the temptation to leverage the balance sheet for faster growth, that decision reflected a family's preference for generational resilience over short-term return-on-equity optimization. A finance professor might argue that HBL's capital structure is suboptimal, that some degree of leverage would improve returns on equity and create tax shields. And they would be technically correct. But Prasad, who lived through the Harshad Mehta crash as a freshly public company and has watched countless leveraged Indian industrials blow up over the decades, has clearly concluded that the optionality value of a debt-free balance sheet exceeds the theoretical benefits of optimal leverage. Given the company's current position—sitting on a massive order book that will require significant working capital to execute—that conservatism looks prescient.

The financial discipline is worth emphasizing because it is so rare in Indian mid-cap industrials. Companies with large government order books typically need significant working capital, and the temptation to borrow against those orders is enormous. HBL has resisted this temptation. The company funds its R&D, its capital expenditure, and its working capital requirements primarily from internal accruals. In a business where government payment cycles can stretch to six to nine months, maintaining a near-zero-debt balance sheet while simultaneously funding multiple growth initiatives is a remarkable feat of financial management.

The institutional shareholder base is, as of early 2026, relatively thin—and this is perhaps one of the most interesting aspects of the HBL story from a market dynamics perspective. Foreign institutional investors hold approximately 4.83 percent, and mutual fund schemes collectively own just 0.21 percent. Individual retail investors, collectively holding about thirty percent, constitute the largest non-promoter shareholder group.

To put this in perspective, most Indian companies of similar market capitalization have mutual fund holdings of five to fifteen percent and FII holdings of ten to twenty percent. HBL's institutional ownership is a fraction of what you would expect for a company of its size and quality. Why? Partly because the company never marketed itself aggressively to institutional investors during its battery era—there was simply not much of a story to tell. Partly because the name "HBL Power Systems" did not scream "high-growth technology company" to the fund managers scanning their Bloomberg terminals. And partly because the company's transformation is so recent that most institutional investors have not yet updated their models or visited the company.

This ownership structure suggests that the institutional discovery of HBL Engineering is still in its early stages. As the Kavach revenue ramp becomes visible in quarterly numbers and the company's transformation from a battery manufacturer to an IP-led engineering company becomes undeniable in the financial statements, institutional ownership is likely to increase—potentially providing a secondary tailwind to the stock as mutual funds and FIIs build positions.

The management's recent capital allocation decisions also deserve scrutiny. Rather than pursuing empire-building acquisitions or diversifying into unrelated businesses—a common affliction of founder-led Indian companies—HBL has deployed capital with surgical precision, targeting specific technological capabilities that complement its core businesses. This brings us to what might be the most intellectually interesting part of the HBL story: its M&A playbook.

V. M&A Strategy and Capital Deployment

Most Indian industrial companies, when they grow, do so by acquiring revenue. They buy competitors, they buy market share, they buy distribution networks. The logic is straightforward: if you are a battery company and you want to grow, buy another battery company. Synergies, scale economies, market consolidation. It is the playbook taught in every MBA program and executed, with varying degrees of success, by industrial conglomerates around the world.

HBL does something fundamentally different. It does not buy revenue. It buys capabilities. Specifically, it acquires or invests in companies that possess intellectual property or engineering expertise that HBL cannot develop in-house within an acceptable timeframe, and then integrates those capabilities into its existing defense, mobility, or energy platforms. The M&A strategy is not about getting bigger. It is about getting smarter.

Consider the three major capital deployment decisions of the past few years, and the strategic logic behind each one becomes clear. Each transaction tells a story about what HBL believes it needs to build next—and, equally importantly, what it has decided it cannot build on its own.

The Tonbo Imaging Investment: Buying Eyes for the Defense Portfolio

In February 2023, HBL announced an investment of up to one hundred and fifty crore rupees in Tonbo Imaging India, a Bengaluru-based startup that designs and manufactures electro-optic imaging systems for defense applications. The investment was structured as compulsorily convertible preference shares across three tranches, which upon full conversion would give HBL a stake of approximately thirty-five to thirty-six percent at floor valuation.

Tonbo is not a random startup. It is a company whose products—thermal imaging sights, surveillance cameras, targeting systems—are deployed in over twenty-five countries and are used by India's defense and home ministries. Electro-optics and imaging subsystems are, as HBL's own management described it, "the eyes and the brain of surveillance platforms and weapon systems." They are among the most technically demanding components in modern military hardware, requiring expertise in infrared sensor design, image processing algorithms, and ruggedized optical engineering.

Why did HBL invest rather than build? Because electro-optics is a field where the core competency is software and sensor design—disciplines that are fundamentally different from HBL's strengths in electrochemistry, power electronics, and mechanical systems. Building an electro-optics capability from scratch would have taken years and required hiring a completely different type of engineer. By investing in Tonbo, HBL acquired instant access to world-class imaging technology that it could integrate into its own defense products—creating, for example, complete weapon system packages that include both the power source (HBL's batteries) and the targeting system (Tonbo's optics). The strategic value of being able to offer an integrated, indigenous solution to the Indian military is enormous, particularly in an era where the government's "Make in India" defense procurement policies explicitly favor domestic suppliers.

TTL Electric Fuel: The EV Leapfrog

In FY2024, HBL acquired a sixty percent stake in TTL Electric Fuel Private Limited, making it a subsidiary. This acquisition positioned HBL squarely in the electric vehicle ecosystem, specifically in the domain of hydrogen fuel cell technology and advanced EV components.

Hydrogen fuel cells represent a different bet on the future of mobility than battery-electric vehicles. While batteries dominate the passenger car segment, many transportation experts believe that hydrogen fuel cells will be the preferred technology for long-haul trucking, marine vessels, and other heavy-duty applications where the weight and charging time of large battery packs create operational challenges. A hydrogen fuel cell vehicle can be refueled in minutes, just like a diesel vehicle, and carries its energy in a lightweight tank rather than in hundreds of kilograms of battery cells.

The strategic logic here mirrors the Tonbo investment: HBL identified a technology gap (fuel cell and advanced EV tech), calculated that internal R&D would take too long, and chose to acquire the capability instead. Developing hydrogen fuel cell technology from scratch requires expertise in membrane electrode assembly design, catalyst optimization, and system-level thermal management—none of which are related to HBL's existing competencies. By acquiring a company with a working platform, HBL compressed what would have been a multi-year R&D program into a single transaction. The question investors should ask is not whether HBL overpaid, but what the R&D time savings and strategic option value of early positioning in the hydrogen economy are worth.

The Cochin Shipyard Joint Venture: Maritime Electrification

The most recent capital deployment decision—announced in January 2026—is a proposed joint venture with Cochin Shipyard Limited, one of India's premier shipbuilders and a public-sector enterprise with deep relationships across the Indian Navy. The JV, in which HBL will hold sixty percent and Cochin Shipyard forty percent, is focused on developing electric mobility technology and energy storage solutions for the marine sector: electric and hybrid propulsion systems for ships, boats, and other marine assets.

This JV is strategically brilliant for several reasons.

First, it positions HBL in the maritime electrification market, which is at a nascent stage globally but is expected to grow rapidly as international maritime emissions regulations tighten. The International Maritime Organization has set ambitious targets for reducing greenhouse gas emissions from shipping, and countries around the world are implementing green port and green shipping policies that will increasingly require electric and hybrid propulsion systems. Getting into this market early—before the regulatory wave fully hits—is a classic HBL move: build the capability before the demand arrives.

Second, it pairs HBL's electric drivetrain technology (more on this in the next section) with Cochin Shipyard's shipbuilding expertise and naval procurement relationships. Cochin Shipyard is not a minor player—it is the largest shipbuilding and ship repair facility in India, and it has built everything from aircraft carriers (INS Vikrant, India's first indigenously built aircraft carrier) to offshore patrol vessels. Having Cochin Shipyard as your JV partner is like having a golden key to the Indian Navy's procurement office.

Third, it leverages HBL's existing battery and energy storage capabilities in a new end market. And fourth, by structuring the deal as a JV rather than an acquisition, HBL limits its upfront capital commitment while gaining access to Cochin Shipyard's manufacturing infrastructure and customer base. The sixty-forty split, with HBL holding the majority, ensures operational control without the full capital burden of a standalone subsidiary.

The common thread across all three transactions is a discipline that is rare in Indian corporate M&A: each deal fills a specific, identified capability gap; each is sized appropriately relative to HBL's balance sheet; and each is structured to minimize risk while maximizing strategic optionality. There are no vanity acquisitions here, no empire-building, no "transformative" deals that require massive debt issuance. It is the anti-conglomerate playbook, and it is working.

But M&A, however smart, only creates value if the underlying businesses are strong. And HBL has several underlying businesses that most investors do not even know exist.

VI. "The Dark Horses": HBL's Hidden Businesses

If Kavach is the engine of HBL's current growth narrative, the businesses described in this section are the turbochargers—high-margin, fast-growing segments that are largely invisible in the company's consolidated financials but could, independently, justify significant value. The challenge for investors is that these businesses are buried within broad reporting segments, making it difficult to parse their individual contributions. But the strategic importance—and the margin profile—of each one is worth understanding in detail.

Electronic Fuzes: The Margin Machine

Deep within HBL's defense electronics portfolio lies a business that rarely gets mentioned in analyst reports but may be the company's highest-margin product line: electronic fuzes for ammunition.

For readers unfamiliar with the term, a fuze is the component that detonates a munition—an artillery shell, a rocket, a grenade, a missile—at the correct moment. Traditional fuzes were mechanical devices, essentially sophisticated clockwork mechanisms that armed and detonated based on time delays or impact forces. Electronic fuzes are their modern replacement: microelectronic devices that use accelerometers, gyroscopes, and microprocessors to determine the optimal detonation point with far greater precision and reliability than mechanical fuzes ever could. They can be programmed for airburst detonation (exploding at a specific altitude above the target), proximity detonation (triggering when close to the target), or point-detonation (triggering on impact).

HBL is the only Indian company with one hundred percent indigenous technology for electronic fuzes. Let that sink in. In a country that spends tens of billions of dollars annually on defense, HBL has a monopoly on the domestic production of one of the most critical components in modern ammunition. The company manufactures fuzes for artillery shells, rockets, grenades, and other munitions, and its products have been approved by the Ministry of Home Affairs for use by paramilitary forces.

The economics of this business are extraordinary. Electronic fuzes are small, lightweight, and relatively inexpensive to manufacture on a per-unit basis—but they are sold into a market where the alternative is importing from foreign suppliers at multiples of the domestic price, and where volumes can be enormous because fuzes are consumables. Every artillery shell fired in training or combat consumes a fuze. Every grenade thrown requires one. Unlike a submarine battery that lasts years, fuzes are used once and destroyed. This creates a recurring revenue dynamic that is unusual in defense manufacturing: the more a military trains and the more ammunition it stockpiles, the more fuzes it needs. India's defense establishment fires millions of rounds of ammunition annually in training alone. The margins are, by all indications, significantly higher than HBL's legacy battery business, though exact segment profitability is not disclosed separately.

The growth runway is immense on both domestic and international fronts. Domestically, India is in the midst of a massive ammunition modernization program, transitioning from mechanical to electronic fuzes across its artillery, mortar, and rocket inventory. The government's "positive indigenization lists"—which mandate domestic sourcing for specified defense items—are creating a protected domestic market for exactly the kind of product HBL makes. In November 2025, a Request for Information was issued for 155mm electronic fuzes under the Indian Army's initiative for indigenous manufacturing, with trials expected to follow.

The export potential is equally compelling. Countries in Europe, the Middle East, and Southeast Asia that are upgrading their artillery and rocket systems need electronic fuzes, and India's competitive manufacturing costs—combined with the growing strategic alignment between India and Western democracies on defense supply chains—make HBL an attractive supplier. The company has already begun exhibiting at international defense exhibitions, including DSEI in London, signaling its intent to pursue export markets aggressively. In a world where NATO allies are scrambling to replenish ammunition stockpiles depleted by the conflict in Ukraine, an Indian supplier of 100% indigenous electronic fuzes could find a receptive market.

Axial Flux Permanent Magnet Synchronous Motors (AF-PMSM): A Different Kind of EV Play

When most investors hear "electric vehicle," they think Tesla, Tata Motors, or perhaps some Chinese startup making passenger cars. HBL is not in the passenger EV business. Instead, it has developed something far more interesting: a proprietary axial flux permanent magnet synchronous motor specifically designed for heavy commercial vehicles.

To understand why axial flux motors matter, a brief technical digression is helpful. Most electric motors in the world—including those in Tesla vehicles—are radial flux motors. In a radial flux motor, the magnetic field runs perpendicular to the axis of rotation, like the spokes of a bicycle wheel pushing against the rim. The motor is shaped like a cylinder, and its power output is largely determined by its length. Want more power? Make the cylinder longer.

An axial flux motor flips this geometry. The magnetic field runs parallel to the axis of rotation—imagine two pancakes facing each other with a spinning disc between them. This "pancake" design allows axial flux motors to be dramatically thinner and lighter than radial flux motors of equivalent power output, with higher torque density and better efficiency at low-to-medium speeds. These characteristics make them particularly well-suited for commercial vehicles—trucks, buses, heavy-duty utility vehicles—where weight and space are at a premium, and low-speed torque (for hauling heavy loads up steep Indian highways) is more important than top-end speed.

HBL's motors are not off-the-shelf components. They are proprietary designs, developed in-house, with the motor control electronics designed and manufactured by HBL as well. The complete powertrain—motor, controller, and energy management system—is an integrated product that HBL sells as a package.

The Asset-Light Retrofit Play: Selling Kits, Not Trucks

Here is where HBL's EV strategy gets genuinely clever. Rather than competing with established OEMs to build electric trucks from the ground up—a capital-intensive, fiercely competitive business—HBL is pursuing an asset-light retrofit model. The company sells Electric Drive Train (EDT) kits that can be used to convert existing diesel commercial vehicles to electric or hybrid propulsion.

Think about the size of the addressable market. India has an estimated twelve million trucks on its roads, the vast majority of which are diesel-powered. Many of these trucks are old—India's average truck age is significantly higher than in developed markets—and they are among the most polluting vehicles in the country. Replacing the entire fleet with new electric trucks would take decades and cost trillions of rupees. The truck manufacturing industry simply cannot produce new electric vehicles fast enough to replace the existing fleet within any reasonable timeframe.

But retrofitting existing vehicles with electric drivetrains is faster, cheaper, and creates immediate environmental benefits. Take the engine out of an existing truck chassis—a chassis that might have ten or fifteen years of useful life remaining—and replace it with HBL's electric drivetrain kit. The truck's frame, cabin, suspension, and braking system remain intact. Only the propulsion system changes. The cost is a fraction of buying a new electric truck, the turnaround time is weeks rather than the months-long wait for a new vehicle order, and the environmental impact is immediate.

HBL's retrofit kits include the axial flux motor, the motor controller, and the integration components needed to replace a diesel engine with an electric powertrain. The battery system can be specified by the vehicle owner or supplied by HBL, providing flexibility for fleet operators who may have their own battery sourcing preferences or existing relationships with battery suppliers.

This is a classic "picks and shovels" strategy—the phrase referring to the California Gold Rush observation that the people who made the most reliable money were not the gold miners but the merchants who sold them picks and shovels.

Rather than trying to compete in the brutally competitive end-market of vehicle manufacturing, where margins are thin and capital requirements are massive, HBL is selling the enabling technology—the components that make electrification possible regardless of which OEM or fleet operator ultimately deploys the vehicles. It is asset-light, it is high-margin relative to vehicle manufacturing, and it leverages HBL's core competency in power electronics and motor design.

The retrofit market also has a natural built-in demand floor. As Indian cities impose increasingly stringent emissions restrictions and as fuel costs continue to rise, fleet operators face a stark economic choice: retrofit their existing trucks and extend their useful life by a decade, or scrap them and buy new electric trucks at three to five times the cost. For most fleet operators—particularly the small and medium-sized businesses that dominate India's trucking industry—the retrofit option is not just cheaper, it is the only financially viable path to compliance.

Lithium-Ion Cell Packaging: The Smart Pivot

The fourth hidden business reflects a strategic decision that is worth studying. In the early 2020s, there was enormous excitement—and enormous government subsidy—around lithium-ion cell manufacturing in India. Dozens of companies announced plans to build gigafactories. HBL looked at the competitive landscape and made a deliberate choice: rather than entering the hyper-competitive commodity cell manufacturing business, the company would focus on specialized cell packaging—taking commodity cells and assembling them into highly engineered battery packs optimized for specific applications like data centers and defense arrays.

The logic is compelling, and it reveals a strategic sophistication that belies HBL's modest public profile. Cell manufacturing is a volume game dominated by Chinese, Korean, and Japanese giants—CATL, BYD, LG Energy Solution, Panasonic—with decades of process optimization and massive scale advantages. These companies produce hundreds of gigawatt-hours of cells annually. An Indian entrant starting from scratch would be competing on cost against players who have already invested tens of billions of dollars in manufacturing infrastructure and have decades of yield optimization experience. That is a battle that is very difficult to win.

But cell packaging—the design, thermal management, battery management systems, and integration of cells into application-specific modules—is a fundamentally different business. It is a value-added engineering exercise where the competitive advantage comes not from scale but from deep domain expertise in the application. How do you package lithium-ion cells for a submarine, where they must withstand shock, vibration, and operate in a sealed environment? How do you package them for a data center, where thermal runaway in a single cell could take out millions of dollars of computing infrastructure? These are problems that generic cell manufacturers cannot solve. They are problems that a company with fifty years of experience building batteries for the most demanding applications in the world is uniquely qualified to address.

HBL also occupies a unique position in the Pure Lead Thin Plate (PLT) battery segment that deserves its own spotlight. The company is the sole producer in India and only the second in the world to manufacture these specialized high-power batteries. The technology was developed entirely in-house—not licensed from a foreign partner, not acquired through an acquisition, but built from scratch by HBL's own engineers.

What makes PLT batteries special? They are designed to deliver very high power for short durations—think of them as sprinters rather than marathon runners. While a conventional lead-acid battery is optimized for steady, long-duration discharge (like powering a UPS for thirty minutes), a PLT battery is optimized for intense, short-duration bursts (like starting a large diesel generator in a data center within seconds of a power outage). This makes them ideal for data center applications, where milliseconds of power interruption can cause millions of dollars in lost transactions and data corruption.

In a world increasingly dependent on data center infrastructure—driven by AI workloads, cloud computing, and digital transformation—demand for reliable, high-power backup batteries is growing rapidly. Major technology companies are building massive data centers across India, and each one needs backup power systems that can deliver instantaneous, reliable power. HBL is one of only two companies globally that can supply PLT batteries for these applications. Interestingly, Cummins—the American diesel engine and power generation giant—resells HBL-manufactured batteries under its own brand, a testament to the quality and reliability of HBL's PLT technology.

Each of these hidden businesses shares a common characteristic: they are built on proprietary technology, they serve markets with high barriers to entry, and they carry margins that are structurally higher than HBL's legacy battery business. As these segments scale, they will have a disproportionate impact on the company's consolidated profitability.

VII. Competitive Landscape & Strategic Moats

Every investor who has ever studied competitive strategy knows that moats matter more than momentum. A company can grow revenues at fifty percent a year, but if it has no moat, that growth will attract competitors who will eventually compress margins and destroy returns on capital. The question for HBL is not whether it is growing fast—it clearly is—but whether that growth is defensible.

Evaluating HBL Engineering through the lens of competitive strategy reveals a company that has, whether by design or by decades of incremental accumulation, built an unusually formidable set of moats. Let us apply two of the most rigorous frameworks in competitive analysis.

Hamilton Helmer's 7 Powers

Of the seven strategic powers Helmer identifies—Scale Economies, Network Effects, Counter-Positioning, Switching Costs, Branding, Cornered Resource, and Process Power—HBL's moats are most clearly visible in two.

Cornered Resource: The Kavach 4.0 RDSO Certification. This is the clearest example of a cornered resource in HBL's portfolio. RDSO certification for Kavach Version 4.0 is not something that can be purchased, replicated, or circumvented. It is the product of years of collaborative development with a government agency, extensive field testing, SIL-4 certification from independent safety assessors, and a track record of operational performance. A new entrant cannot simply hire better engineers or invest more capital to leapfrog HBL's position. They must endure the same multi-year certification process, and they must do so against an incumbent that already has a proven product and an established order book. This is a government-mandated oligopoly, and the barriers to entry are measured not in money but in time—which, in a market where the government is impatient to deploy Kavach as fast as possible, is the scarcest resource of all. It is worth noting that in December 2023, Indian Railways did announce that multinational companies Siemens and Japan's Kyosan would be brought in to increase Kavach deployment capacity. But even this expansion of the supplier base does not diminish HBL's advantage: these MNCs are starting from scratch in terms of RDSO certification for their own systems, while HBL is already delivering against its order book.

Switching Costs: Integrated Train Management Systems. Once HBL's Kavach and Train Management System are installed and integrated into a railway zone's infrastructure—the trackside equipment, the onboard locomotive systems, the radio communication towers, the central control centers—the cost and complexity of switching to a different supplier is enormous. This is not like switching from one cloud software provider to another. It involves physical infrastructure deployed across hundreds of kilometers of track, tested and certified as a unified system. Ripping it out and replacing it with a competitor's system would require new certification, new field testing, and—most critically—a period of operational downtime during which the safety system is unavailable. No railway administrator in their right mind would authorize that unless HBL's system were catastrophically failing, which it is not.

Porter's Five Forces

Buyer Power: High But Mitigated. In theory, HBL should be crushed by buyer power. Its primary customers—the Indian Railways for Kavach, the Indian military for defense batteries and fuzes—are monopsony or near-monopsony buyers with enormous purchasing leverage. Governments, as a general rule, are brutal negotiators. They set specifications, control tender processes, and can delay payments with impunity. This dynamic typically decimates margins for defense and railway suppliers. But HBL has partially neutralized this threat through the uniqueness of its IP. When you are the only Indian company with SIL-4 certified Kavach 4.0, or the only Indian company with indigenous electronic fuze technology, the buyer's leverage is diminished. The government needs your product more than you need any individual contract, because the alternative—importing foreign systems—is more expensive and strategically undesirable in the current political environment.

Threat of New Entrants: Virtually Zero in Core Segments. The technical barriers to entry in HBL's core businesses are extraordinary. Developing a SIL-4 certified train protection system requires a decade of collaborative R&D with RDSO and independent safety certification. Manufacturing submarine batteries requires years of qualification testing with the Indian Navy. Producing electronic fuzes with indigenous technology requires mastering the intersection of microelectronics, pyrotechnics, and extreme-environment engineering. None of these capabilities can be acquired quickly, regardless of capital availability. A well-funded new entrant would need ten to fifteen years to build the certifications, relationships, and operational track record that HBL has accumulated over decades.

Threat of Substitutes: Low in the Near Term. For Kavach, there is no substitute—the Indian Railways has mandated it as the national ATP system. For submarine and torpedo batteries, alternative chemistries (such as lithium-ion) are being explored for next-generation platforms, but the qualification cycle for new battery chemistries in submarine applications is measured in decades. For electronic fuzes, the substitute is imported fuzes, which the government is actively trying to eliminate under its indigenization mandate. In each core segment, HBL's products face minimal substitution risk over the next five to seven years.

Supplier Power: Manageable. Battery manufacturing requires raw materials—lead, nickel, cadmium, lithium—whose prices are set by global commodity markets. HBL has limited pricing power over its suppliers. However, the company's diversification across multiple battery chemistries and its growing electronics business (which has a different cost structure) reduces its overall sensitivity to any single raw material. The more the revenue mix shifts toward electronics and IP-based products, the less supplier power matters. For the electronics segments, the key inputs are electronic components—processors, sensors, communication modules—which are sourced from a global supply chain with multiple alternative suppliers.

Industry Rivalry: Segmented. In the Kavach market, rivalry is limited by the small number of certified suppliers. The original development consortium—HBL, Medha Servo Drives, and Kernex Microsystems—constitutes the core domestic supplier base. While Siemens and Kyosan have been invited to participate in Kavach deployment, they are entering a market where HBL has the first-mover advantage of Version 4.0 certification and a proven delivery track record. In specialty defense batteries, rivalry is limited by the extreme qualification requirements—you cannot win a submarine battery contract without years of prior qualification. In commodity industrial batteries, rivalry is intense—but this is precisely the segment that HBL is de-emphasizing as it pivots toward higher-margin electronics and IP-based products. The company is effectively migrating from a high-rivalry segment (commodity batteries) to low-rivalry segments (certified railway safety, defense electronics), which is structurally positive for long-term profitability.

Taken together, the competitive analysis paints a picture of a company that occupies an unusually defended strategic position. The combination of government-mandated demand, SIL-4 certification barriers, decades-long qualification cycles in defense, and indigenous IP monopolies in fuzes creates a multi-layered moat that would be extraordinarily expensive and time-consuming for any competitor to breach. This is not a business where a well-funded private equity firm can simply write a large check and enter the market. The barriers are measured in decades of institutional trust, not dollars of invested capital.

VIII. Bear vs. Bull Case

The Bull Case

The bull case for HBL Engineering rests on three mutually reinforcing tailwinds, each of which is independently powerful and collectively transformative.

First, the Kavach deployment mandate. The Indian Railways has committed to covering approximately forty-four thousand kilometers of track and fitting onboard equipment in twenty thousand locomotives by 2030. As of early 2026, only about thirteen hundred route kilometers have been commissioned and approximately four thousand locomotives fitted. The gap between current deployment and the target represents years of sustained, high-visibility revenue for HBL. Importantly, this is not a discretionary corporate spending decision that can be easily deferred—it is a government mandate driven by political imperative (railway safety is an intensely emotional issue in Indian politics) and backed by dedicated budget allocations. The probability of the mandate being abandoned is effectively zero; the main variable is the pace of execution.

Second, the margin transformation. As Kavach and defense electronics become a larger share of consolidated revenue, EBITDA margins are structurally shifting from the low-to-mid teens toward the eighteen-to-twenty-two percent range. This is not a one-time improvement; it reflects a permanent change in the company's business mix from commodity hardware (batteries) to IP-led systems (Kavach, fuzes, motors). The June 2025 quarter showed a dramatic illustration of this dynamic: EBITDA roughly doubled and net profit margins expanded to over thirty percent, driven primarily by the ramp-up of high-margin electronics revenue.

Third, the optionality in hidden businesses. The electronic fuze segment, the electric drivetrain retrofit business, the Cochin Shipyard maritime JV, and the Tonbo Imaging partnership are all at early stages of revenue contribution. If even one or two of these businesses achieve meaningful scale, they represent incremental growth vectors that are not currently priced into most valuation models.

There is also a less obvious but potentially transformative element to the bull case: the compounding effect of HBL's multiple businesses creating cross-selling opportunities. A defense ministry that buys HBL's submarine batteries is a natural customer for HBL's electronic fuzes. A railway administration that deploys HBL's Kavach system is a natural customer for HBL's train management systems and battery energy storage solutions. And a Cochin Shipyard building electric vessels through the JV is a natural customer for HBL's motors and battery packs. These are not theoretical synergies—they reflect the reality that defense and infrastructure procurement in India tends to favor vendors with proven track records across multiple product categories.

The bull case scenario envisions HBL Engineering as a company that is transitioning from a specialized battery manufacturer with a market capitalization of roughly eighteen thousand crores to a diversified defense and mobility technology platform with multiple high-margin revenue streams, a massive government-backed order book, and a proprietary IP portfolio that creates genuine competitive moats.

The Bear Case

The bear case is equally worth taking seriously, and it centers on three risks.

First, concentration risk. HBL's growth narrative is heavily dependent on the Indian government—specifically, the Indian Railways and the Ministry of Defence. If the Railways delays Kavach tenders, slows capital expenditure, or changes procurement priorities (perhaps due to fiscal constraints or a change in political leadership), HBL's revenue growth could stall significantly. The company has limited ability to diversify its customer base for Kavach, because the product is specifically designed for and certified by the Indian Railways. This is the flip side of having a government-mandated monopoly: your moat is only as strong as the government's commitment to the program.

Second, execution risk. Scaling from a battery manufacturer to a company that must deliver thousands of crores worth of complex electronics systems on tight timelines is an enormous operational challenge. Manufacturing electronic fuzes and assembling TCAS equipment require different skills, different quality control processes, and different supply chains than manufacturing batteries. If HBL struggles with manufacturing yields, component sourcing, or installation timelines, it could face cost overruns, delivery delays, and potential penalties on its government contracts. The FY2025 financial results hinted at some growing pains: despite solid margins, operating cash flow collapsed compared to the prior year—a pattern that bears watching as the company scales its electronics delivery capabilities.

Third, technology obsolescence in legacy segments. HBL's legacy battery business—particularly lead-acid and nickel-cadmium—faces long-term headwinds from advancing battery chemistry. If solid-state batteries, advanced lithium-ion chemistries, or other breakthrough technologies render nickel-cadmium and lead-acid batteries obsolete for defense and aviation applications, HBL's traditional cash-cow business could erode. The qualification cycles for new battery chemistries in defense applications are long (which provides near-term protection), but the direction of technological change is clear.

Additionally, the entry of global players like Siemens and Kyosan into the Kavach ecosystem, while not an immediate threat, introduces the possibility of increased competition over the medium term. If these MNCs successfully certify their own versions of Kavach-compatible systems, HBL's pricing power and market share could come under pressure in future tender cycles. It is worth noting that global railway signaling is dominated by a handful of giants—Siemens, Alstom, Hitachi Rail, Thales—who have decades of experience with ETCS (European Train Control System) deployments worldwide. If the Indian government were to allow ETCS-compatible systems as an alternative to Kavach, these global players could leverage their existing technology base to enter the Indian market at scale. For now, the government's commitment to an indigenous system appears firm, but policy is never permanent.

There is also a valuation consideration that the bear case must acknowledge. At a market capitalization of roughly eighteen thousand crores, HBL trades at a meaningful premium to its historical valuation multiples and to many of its Indian industrial peers. This premium is justified only if the Kavach revenue ramp materializes on schedule and the margin expansion proves sustainable. If either of these assumptions is disappointed—even temporarily—the stock could experience significant volatility as the market re-prices its expectations.

The KPIs That Matter

For investors tracking HBL Engineering's ongoing performance, two metrics stand out as the most important leading indicators.

The first is the Electronics Revenue Mix—specifically, the percentage of total revenue derived from the Electronics segment (which includes Kavach, defense electronics, and fuzes) versus the legacy Battery segments. This ratio is the single best proxy for the company's margin trajectory and strategic transformation. A steadily rising electronics revenue mix confirms that the pivot is working and that margins will continue to expand.

The second is the Order Book-to-Revenue Ratio, particularly for the Electronics segment. An order book that is growing faster than revenue provides visibility into future growth and confirms that the Kavach deployment pipeline is converting into firm orders. As of early 2026, HBL's order book stands at approximately thirty-nine hundred crores against annual revenue of roughly twenty-two hundred crores—an order book-to-revenue ratio of nearly 1.8 times, which provides substantial revenue visibility for the next two years. Conversely, a stagnating or declining order book would be an early warning signal that government procurement is slowing or that competitors are winning a larger share of new tenders.

A third metric worth monitoring, though less frequently discussed, is Cash Conversion—the ratio of operating cash flow to reported net profit. In FY2025, this ratio deteriorated sharply, suggesting that working capital requirements are increasing as the company scales its electronics delivery. If cash conversion does not recover as the order book is executed, it could signal deeper operational issues in inventory management or receivables collection from government customers.

IX. The Playbook: Lessons in Deep Tech & Sovereign Capabilities

HBL Engineering's five-decade journey offers several lessons that extend far beyond the specifics of batteries and railway safety systems. They are lessons about how to build industrial technology companies in emerging markets, and they are worth extracting for anyone studying deep-tech entrepreneurship.

Surviving the Valley of Death

The most obvious lesson is also the most difficult to execute: how to fund a decade of zero-revenue R&D when you are not a Silicon Valley startup with access to patient venture capital.