Happy Forgings: From Bicycle Pedals to India's Forging Powerhouse

I. Introduction & Episode Teaser

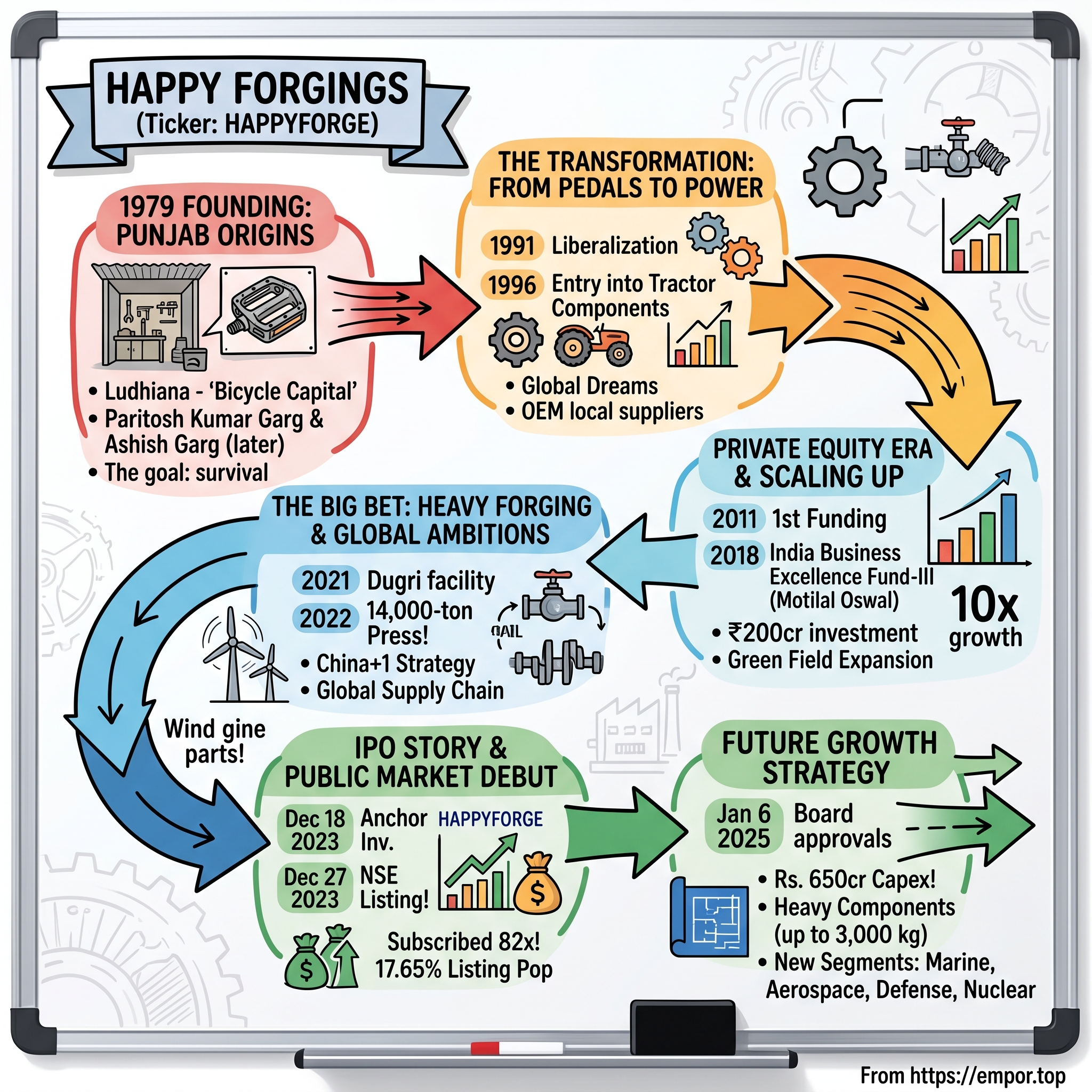

Picture this: A sweltering summer day in 1973 in Ludhiana, Punjab. The air thick with industrial smoke, the rhythmic clanging of metal on metal echoing through narrow lanes. In a modest workshop, two entrepreneurs—Ashish Garg and Paritosh Kumar Garg—are hammering away at what seems like an impossibly simple product: bicycle pedals. Fast forward five decades, and that humble workshop has transformed into Happy Forgings Limited, commanding a market capitalization of ₹9,142 crore and standing as India's fourth-largest manufacturer of complex, safety-critical heavy forged components.

The question that should captivate any student of business history is deceptively simple yet profound: How does a bicycle pedal manufacturer become India's second-largest producer of high-horsepower diesel engine crankshafts? It's a transformation so complete, so audacious, that it reads like industrial fiction—except every ton of forged steel, every precision-machined component, every global OEM partnership is brutally, beautifully real. Today, Happy Forgings stands tall with revenue of ₹1,421 crore and profits of ₹269 crore, wielding the fourth-largest forging capacity in India. The company boasts gross margins of 57.9% and EBITDA margins of 28.6%—numbers that would make any industrial manufacturer envious. But these aren't just numbers on a spreadsheet. They represent decades of calculated risks, strategic pivots, and an almost obsessive focus on precision engineering that transformed a regional workshop into a global supplier to the world's most demanding OEMs.

What makes the Happy Forgings story particularly compelling for investors and business historians alike is its timing. The company's evolution mirrors India's own industrial transformation—from the License Raj era through liberalization, from import substitution to global competitiveness, from family workshops to professionally managed corporations. It's a story of how Indian manufacturing, often dismissed as low-value-add and uncompetitive, can climb the value chain to compete with the best in the world.

The narrative arc we're about to explore isn't just about forging steel—it's about forging relationships that span decades, forging capabilities that took generations to build, and forging a path through India's complex industrial landscape. From bicycle pedals to crankshafts that power the massive engines of commercial vehicles, from a single workshop in Ludhiana to three state-of-the-art facilities with total forging capacity close to 150,000 tonnes, Happy Forgings embodies the audacity of Indian entrepreneurship.

As we dive into this industrial odyssey, we'll uncover the strategic decisions that transformed a commodity business into a precision engineering powerhouse, the capital allocation choices that enabled exponential growth, and the operational excellence that attracted global giants as customers. This is the untold story of how Happy Forgings became happy—and made its investors even happier.

II. The Punjab Origins & Founding Story

The story begins not in boardrooms or venture capital offices, but in the industrial heartland of Punjab in the early 1970s. Ludhiana—the "Manchester of India"—was already earning its reputation as the country's bicycle capital. The city's narrow gullies buzzed with the sound of lathes and hammers, its air thick with metal dust and ambition. It was here that Ashish Garg and Paritosh Kumar Garg saw opportunity where others saw only competition. Paritosh Kumar founded the company in 1979 and continues to provide strategic guidance as Chairman and Managing Director, though some sources cite the founding year as 1973 with both Ashish Garg and Paritosh Kumar Garg as founders. The discrepancy likely reflects the difference between the initial workshop's establishment and formal incorporation.

What's fascinating about the founding story isn't just the timing but the context. The 1970s Punjab was experiencing its own industrial revolution. The Green Revolution had created wealth in rural areas, mechanization was transforming agriculture, and entrepreneurs were rushing to fill the gap in India's industrial capacity. But while others chased quick profits in consumer goods, the Gargs saw opportunity in the unglamorous world of forged components.

The company evolved from humble beginnings as a bicycle pedal manufacturer to become the second-largest producer of high horsepower diesel engine crankshafts in the nation. But in those early days, success meant survival. The workshop operated with basic equipment—manual hammers, simple dies, and the kind of grit that only comes from having everything on the line. Paritosh Kumar, with 45 years of experience in the forging industry, brought technical expertise honed through hands-on work. He understood metal—how it behaved under pressure, how temperature affected its properties, how precision could be achieved even with rudimentary tools.

The choice of Ludhiana wasn't accidental. The city had emerged as India's bicycle capital, producing millions of units annually for a nation that relied on two-wheelers for basic transportation. This created an ecosystem of suppliers, skilled workers, and most importantly, a culture that understood manufacturing. The narrow lanes of Ludhiana's industrial areas were universities of practical engineering, where knowledge passed from master to apprentice, where innovation meant finding a way to make things work with limited resources.

Happy Forgings was founded in 1979 by Managing Director Ashish Garg's father, Paritosh Kumar, to supply forged bicycle pedals in Punjab, India's bicycle hub. In 2006, when Garg joined the business as an executive director, the company had a turnover of US$12.2 million. This generational transition would prove pivotal, but in the 1970s and 80s, the focus was on building credibility one pedal at a time.

The License Raj era added layers of complexity. Every expansion required permits, every import needed approval, and competition was limited by government policy rather than market forces. Yet these constraints bred ingenuity. Unable to import advanced machinery, Happy Forgings learned to modify and maintain equipment far beyond its intended life. Unable to access international markets, they became experts at understanding domestic demand. Unable to raise easy capital, they learned the discipline of self-funded growth.

What set Happy Forgings apart even in these early years was an obsession with quality that seemed almost irrational for a bicycle pedal manufacturer. While competitors focused on volume, the Gargs invested in testing equipment. While others cut corners to improve margins, Happy Forgings maintained specifications that exceeded requirements. This wasn't philanthropy—it was strategic patience. They understood that reputation in industrial manufacturing is built over decades but can be destroyed in days.

The Punjab of that era was also experiencing social transformation. The state that had fed India during the Green Revolution was seeking its next identity. Industrial entrepreneurship offered a path forward, and families like the Gargs became role models. They employed local talent, reinvested profits locally, and proved that Punjab could compete not just in agriculture but in precision manufacturing.

Ashish Garg holds a Master's degree in Manufacturing Systems Engineering and a graduate qualification in Finance from Warwick University in the U.K. This educational foundation would later prove crucial in transforming the company, but the real education happened on the shop floor in Ludhiana. Every failed forging taught a lesson about metal properties. Every satisfied customer built a relationship that would span decades. Every competitor's success provided a benchmark to exceed.

By the late 1980s, Happy Forgings had established itself as a reliable supplier in the bicycle components market. But this was just the foundation. The real transformation was about to begin, as India itself stood on the cusp of economic liberalization. The skills honed in making bicycle pedals—precision forging, quality control, customer relationships—would soon be applied to far more complex and lucrative markets. The stage was set for Happy Forgings to pedal its way into India's automotive revolution.

III. The Transformation Years: From Pedals to Power

The year 1991 changed everything. As India's economy opened up and P.V. Narasimha Rao's government dismantled the License Raj, Happy Forgings faced both an existential crisis and unprecedented opportunity. Global competitors could now enter India, but Indian companies could also dream global dreams. The question for Happy Forgings wasn't whether to transform, but how fast they could do it without losing their soul. The pivotal year was 1996. While India celebrated five years of economic liberalization, Happy Forgings made its boldest strategic move yet—entering the tractor components manufacturing sector. This wasn't just product diversification; it was a complete reimagination of what the company could be. Tractors were the workhorses of India's agricultural economy, and their components required precision and durability that far exceeded bicycle pedals.

The decision to target tractor components was strategic genius disguised as obvious logic. India's tractor market was exploding—from 140,000 units in 1990 to over 250,000 by the mid-1990s. Every major global player wanted in: John Deere, New Holland, Case IH. But they all needed local suppliers who could meet international quality standards while navigating India's complex supply chain realities. Happy Forgings positioned itself perfectly at this intersection.

Between 2010 and 2015, the company gradually ventured into industrial and commercial vehicle segments. This wasn't a rushed expansion but a calculated progression. Each new segment built upon capabilities developed in the previous one. The precision required for tractor components translated directly to commercial vehicle parts. The relationships built with domestic OEMs in one sector opened doors in others.

The transformation required more than new machinery—it demanded a complete cultural shift. Workers who had spent careers making bicycle pedals suddenly needed to understand metallurgy at a different level. Quality standards that were good enough for consumer products wouldn't pass muster for safety-critical automotive components. The company invested heavily in training, bringing in experts from Germany and Japan, sending engineers abroad for education, creating a culture where continuous improvement wasn't a slogan but a survival strategy.

When Ashish Garg joined the business as an executive director in 2006, the company had a turnover of US$12.2 million. "When we decided to go in for OEM business, we invested in an 8,000-metric-ton press line," Garg recalls. "We started forging parts of up to 75–80 kilograms." This wasn't just an equipment upgrade—it was a statement of intent. The 8,000-ton press could forge components that were previously imported, giving Happy Forgings a competitive edge that went beyond cost.

The journey from manufacturing basic forged and machined components to manufacturing complex and safety-critical products with closed tolerances involved expansion of capabilities in both light and heavy forging and machining. The company commissioned its first 8,000-ton forging press, marking its entry into heavy forging—a capability that only a handful of Indian companies possessed.

What's remarkable about this period is how Happy Forgings managed relationships during the transition. They didn't abandon their bicycle component customers overnight. Instead, they maintained these relationships while gradually shifting capacity to higher-value products. This patient approach meant they never faced the cash flow crisis that kills many companies during major pivots. Through over 40 years of business operations, they established long-standing relationships with several Indian and global customers across industries.

The company's evolution during this period also reflected broader changes in Indian manufacturing. The old model of protected markets and guaranteed profits was dead. Global competition meant Indian manufacturers had to match international quality at local costs. Happy Forgings didn't just adapt to this reality—they thrived in it. They understood that in the new India, relationships still mattered, but they had to be backed by world-class capabilities.

By 2015, Happy Forgings had transformed from a bicycle pedal manufacturer to a diversified forging company serving commercial vehicles, farm equipment, and industrial equipment sectors. Beginning with bicycle components, they expanded their scope with three manufacturing facilities producing safety-critical parts for industries such as automotive, railways, agriculture, engine & power generation, oil & gas and construction & mining.

The company's strategic patience during this transformation period would prove invaluable. While competitors rushed to capitalize on India's automotive boom, often overextending themselves, Happy Forgings built capabilities methodically. They understood that in precision manufacturing, reputation takes decades to build but moments to destroy. Every component that left their facility carried not just their name but their future. This obsession with quality over quick profits set the stage for the next phase of their growth—one that would involve private equity partners and ambitions that extended far beyond India's borders.

IV. The Private Equity Era & Scaling Up

The conference room at Happy Forgings' Ludhiana headquarters had seen many meetings, but the one in January 2011 was different. Across the table sat representatives from private equity firms, armed with spreadsheets and growth projections. For a company that had bootstrapped for over three decades, taking outside capital was both an opportunity and a cultural earthquake. The first funding round on January 28, 2011, marked a watershed moment. But it was the September 15, 2018, investment that truly transformed Happy Forgings' trajectory. India Business Excellence Fund - III, funds managed or advised by Motilal Oswal Private Equity (MOPE) has committed Rs 2 billion to Ludhiana-based forging and machining firm Happy Forgings Ltd. This wasn't just capital—it was validation from one of India's most respected financial institutions.

This is the first time the Company has raised private equity capital, making the ₹200 crore (approximately $27.1 million) investment particularly significant. The funds weren't earmarked for financial engineering or debt repayment. The funds will be utilized for Greenfield Expansion and Addition of new forging presses to improve the share of value-added products.

Vishal Tulsyan, managing director and CEO of MOPE, articulated the investment thesis: "Manufacturing has been one of the focus areas of our Fund as it is expected to benefit from strong underlying growth in the Indian economy as well as significant export opportunities." For Happy Forgings, this external validation meant more than money—it meant access to networks, governance improvements, and the discipline that comes with institutional investors.

The private equity partnership catalyzed rapid technological advancement. In 2017 and 2018, the company commissioned a second 8,000-ton forging press, doubling their heavy forging capacity. But the real transformation was in mindset. The presence of PE investors forced Happy Forgings to think in terms of ROCE (Return on Capital Employed), asset turns, and EBITDA margins—metrics that family businesses often overlook in favor of absolute profit numbers.

Ashish Garg, with his master's degree in manufacturing systems engineering from the University of Warwick, became the bridge between old-school manufacturing excellence and modern financial metrics. "The business, which was doing 100 crores [US$12.2 million] in 2007 annually, is now doing over 100 crores monthly," Garg adds. "The growth has been tremendous – almost 12–15 times."

The PE era also brought strategic clarity. Instead of chasing every opportunity, Happy Forgings focused on becoming best-in-class in specific segments. They targeted components where India had a competitive advantage—labor-intensive, precision machining work that was too expensive in developed markets but required quality standards that Chinese manufacturers struggled to consistently meet.

"From 2011–2017, we continuously invested in machining technologies." "We call it the most profitable forging business in the entire industry and in the world today. For the past four years, we have been generating earnings before interest, tax, depreciation and amortization margins of over 26 percent." These weren't empty boasts—the numbers backed them up.

The relationship with Motilal Oswal went beyond capital. He focuses on businesses in the industrials and niche manufacturing sectors, and represents the existing funds on the Board of VVDN Technologies, Happy Forgings, Magicrete and Glass Wall Systems. He also led investments in VVDN Technologies and Happy Forgings from Fund III. Having seasoned PE professionals on the board brought discipline to capital allocation decisions.

This period also saw Happy Forgings develop what would become their competitive moat: the ability to handle both forging and precision machining in-house. "So from a forging background, we entered the machining business and now we are tier-2 suppliers to OEMs. Today, we supply to almost all domestic as well as international OEMs in the farm equipment and commercial vehicles sector, capital equipment, engines and power generation, and oil and gas."

The PE investment also accelerated the company's move up the value chain. Instead of just supplying forged components, they began offering fully machined, ready-to-assemble parts. This transition from a ₹100 per kg forged component to a ₹300 per kg machined component tripled value addition without proportionally increasing costs. It was financial alchemy achieved through engineering excellence.

By 2018, Happy Forgings had emerged as a case study in how private equity, when paired with strong operational management, could transform traditional manufacturing businesses. Established in 1979 by Paritosh Kumar Garg, the company is one of the largest supplier for forged and machined transmission and engine components to the automotive sector. Over the last few years, Happy Forgings has emerged as one of the largest Crankshaft manufacturer in India.

The transformation wasn't without challenges. PE investors demanded quarterly performance reviews, detailed MIS reports, and strategic clarity that family businesses often operate without. Some old-timers in the company struggled with the new pace and accountability. But Ashish Garg navigated these waters skillfully, protecting the company's manufacturing DNA while embracing modern management practices.

As the PE era progressed, Happy Forgings began thinking beyond domestic markets. The capital, credibility, and capabilities built during this period set the stage for their most ambitious move yet—becoming a global supplier capable of competing with established players from Germany, Japan, and the United States. The company that had once made bicycle pedals was now ready to forge its place on the world stage.

V. The Big Bet: Heavy Forging & Global Ambitions

The morning of January 15, 2021, marked a moment of industrial audacity. As the 14,000-ton forging press at Happy Forgings' new Dugri facility thundered to life for the first time, it wasn't just metal being shaped—it was India's manufacturing ambitions taking form. This behemoth of a machine, one of only two in India with such capability, represented a ₹650 crore bet that Happy Forgings could compete not just nationally but globally in the heavy forging space. The expansion in 2021 and 2022 was nothing short of transformative. The commissioning of operations in Dugri, spanning approximately 17 lakh square feet, marked a major leap in manufacturing scale. This period also saw the installation of a 14,000-ton forging press, making Happy Forgings only the second company in India to possess such a capability, paving the way for entry into the industrials segment and global exports.

The 14,000-ton press wasn't just about size—it was about possibilities. It is designed to handle enormous pressures, shaping metal into various forms used in aerospace, automotive, defense, and many other sectors. The press can exert pressure up to 14,000 tons, which is essential for forging large and complex parts. This level of control ensures that each component meets the exact specifications required by industries like aerospace, where precision is paramount.

The decision to invest in such massive capacity during the COVID-19 pandemic, when most companies were cutting capital expenditure, demonstrated either remarkable foresight or remarkable foolishness. As it turned out, it was the former. The global supply chain disruptions had exposed the vulnerability of just-in-time manufacturing and single-source dependencies. Companies worldwide were looking to diversify their supplier base, and Happy Forgings positioned itself perfectly to capture this opportunity.

Entry into wind turbine, oil & gas, and industrial segments wasn't just diversification—it was strategic positioning for the energy transition. Wind turbine components, in particular, represented a massive opportunity. A single wind turbine requires multiple large forged components—main shafts, rotor hubs, tower flanges—each worth significantly more than traditional automotive parts. Happy Forgings was now serving OEMs in commercial vehicles, farm equipment, off-highway and industrial equipment, oil and gas, aerospace, power generation, railways, and wind turbine industries.

The technical capabilities of the 14,000-ton press opened doors that had been firmly shut to Indian manufacturers. Parts such as crankshafts, connecting rods, and suspension components are commonly forged using this press. The ability to create these parts with precise dimensions and enhanced mechanical properties ensures that vehicles are both safe and efficient. But more importantly, it allowed Happy Forgings to bid for contracts that previously went only to established European and Japanese suppliers.

Ashish Garg's master's degree in manufacturing systems engineering from the University of Warwick proved invaluable during this expansion. "Happy Forgings currently has a 14,000 metric ton press line, one of the biggest in India and among the biggest in Asia," he noted with evident pride. This wasn't just about having the biggest toys—it was about having capabilities that few others possessed.

The investment timing proved prescient. As global OEMs accelerated their China+1 strategies post-pandemic, Happy Forgings emerged as a credible alternative. The company's dedication to continuous improvement and customer satisfaction has made it a trusted partner for clients in the automotive, aerospace, and heavy machinery sectors. European customers who had never considered Indian suppliers were suddenly interested.

The Dugri facility represented more than physical expansion—it embodied a new operational philosophy. Happy Forging Ltd. (HFL) is at the forefront of adopting cutting-edge technologies and has a forging press like 14000-ton, 8000-ton, 4000-ton, and 6300-ton mechanical forging presses & 2500-ton forging screw presses. The facility was designed from the ground up for Industry 4.0, with IoT sensors, real-time quality monitoring, and predictive maintenance systems.

By 2022, the company had also installed eight dedicated lines for manufacturing crankshafts, received the IATF 16949:2016 accreditation for manufacture of forged and machined components at the Dugri Facility, and earned recognition with awards like the 'Supplier Excellence Award' for delivery performance at AAM (American Axle Manufacturing) India Supplier Event 2023.

The global ambitions weren't just about exports—they were about becoming part of global supply chains. When a European wind turbine manufacturer sources components from Happy Forgings, they're not just buying parts; they're integrating Happy Forgings into their production planning, quality systems, and long-term strategy. These relationships, once established, create switching costs that protect against competition.

As of September 30, 2023, Happy Forgings' annual aggregate installed capacity for forging and machining had increased to 120,000.00 MT and 47,200.00 MT respectively, with 3,070 employees on its payroll. The transformation from a regional player to a global supplier was complete. The company that had once made bicycle pedals was now forging components for some of the world's most demanding applications.

The massive capacity expansion set the stage for the next chapter in Happy Forgings' evolution—taking the company public and giving investors a chance to participate in India's manufacturing renaissance.

VI. IPO Story & Public Market Debut

The bell rang at the National Stock Exchange at 9:15 AM on December 27, 2023, but for Happy Forgings, the sound had been decades in the making. As the stock began trading, opening at a premium to its issue price, it marked not just a successful IPO but validation of a business model built over 44 years. The IPO journey began long before the official announcement. Happy Forgings IPO was a main-board IPO of 1,18,65,802 equity shares of the face value of ₹2 aggregating up to ₹1,008.59 Crores. The issue was priced at ₹850 per share. The combination of fresh issuance of ₹400 crore and an Offer for Sale of 7,159,920 shares represented a carefully calibrated balance between growth capital and providing exits for early investors.

The Happy Forgings IPO opened from 19th December to 21st December 2023. The size of Happy Forgings IPO was around ₹1008.59 cr. The share allotment date of Happy Forgings IPO was 22nd of December 2023. The Happy Forgings IPO was listed on the 27th of December 2023.

The market response exceeded expectations. The Happy Forgings Ltd IPO was subscribed 82.04 times on 21 December 2023. The public issue subscribed 15.09 times in the retail category, 220.48 times in the QIB category, and 62.17 times in the NII category. This wasn't just oversubscription—it was validation from sophisticated institutional investors who understood the company's unique position in India's manufacturing ecosystem.

JM Financial Limited, Axis Capital Limited, Equirus Capital Private Limited, and Motilal Oswal Investment Advisors Limited were the book-running lead managers for Happy Forgings IPO. The presence of Motilal Oswal, which had been an investor since 2018, as a lead manager sent a strong signal about continuity and confidence.

The use of IPO proceeds revealed strategic priorities. The fresh issue proceeds would be used by the company for: To fund the purchase of equipment, plant and machinery. Prepayment of the debt borrowed by the company. General corporate purpose. This wasn't financial engineering but operational strengthening—exactly what long-term investors want to see.

Happy Forgings IPO raised ₹302.58 crore from anchor investors on December 18, 2023, a day before the public opening. The quality of anchor investors—including mutual funds and insurance companies—provided confidence to retail investors about the company's prospects.

The grey market provided its own verdict. Ahead of its listing, Happy Forgings was commanding a grey market premium (GMP) of Rs 280-300, suggesting about 33-35 per cent listing pop over its issue price of Rs 850 apiece. The premium in the unofficial market had come down a bit. It stood at around Rs 450, ahead of the bidding process.

On listing day, December 27, 2023, the stock delivered. The public issue of Happy Forgings IPO was offered at ₹850.00 per share and the ipo was listed at ₹1000. It delivered listing gain of 17.65%. As the minimum lot size was 17 shares, the IPO offered Rs 2550 per lot return on listing.

The IPO prospectus revealed impressive metrics that justified investor enthusiasm. If you attribute the FY24 annualized earnings to the post-IPO fully diluted paid-up equity capital of the company, the share price of the company would be priced at P/E of 33.56. As this P/E the share price of Happy Forgings is fairly priced if you compare it with its peer group companies. Though owing to some differences in their business models, they all are not comparable on an apple-to-apple basis. But its nearest listed competitors Bharat Forge, Craftsman Auto, Ramkrishna Forgings, and Sona BLW are trading at a P/E of 45.85, 47.01, 47.92, and 68.02 respectively.

The company's financial performance leading up to the IPO was stellar. The revenue from the operation of Happy Forgings in the first six months of FY24 stood at Rs 672.9 crore, while in the full year FY23 it was Rs 1196.53 crore. Its revenue was at Rs 584.96 crore in FY21 which has grown at a CAGR of 43% from FY21 to FY23.

Post-IPO, the shareholding pattern reflected a healthy balance. As per the prospectus documents, Garg Family Trust is the main promoter of the company holding a 42.51% stake in the company. Ashish Garg and Ayush Capital & Financial Services Private Limited, India Business Excellence Fund –III and Paritosh Kumar are the major shareholders of the company having 14.47%, 12.01%, 11.76% and 10% respectively.

The successful IPO validated years of strategic decisions. 2023: A successful IPO and listing validated the company's business model and opened access to capital markets, enabling further value creation and long-term growth. It transformed Happy Forgings from a closely-held family business into a public company with institutional governance standards.

Market perception post-listing remained positive. The company's unique positioning as the fourth largest engineering led manufacturer of complex and safety-critical, and high precision machined components in India with an experience of 40 years. Only the second company in India to have a 14,000 tonne forging press and among four companies in India that possess a 8,000 tonne forging press as of 31 March 2023 provided a competitive moat that investors appreciated.

The IPO wasn't just about raising capital—it was about joining India's elite manufacturing companies. Happy Forgings had successfully made the transition from private to public, from regional to national recognition, from family-owned to professionally managed. The stage was now set for the next phase of growth, with public market accountability driving performance and transparency.

VII. Current Business Model & Market Position

Walk through Happy Forgings' facilities today, and you're witnessing industrial poetry in motion. The rhythmic thunder of the 14,000-ton press, the precision ballet of CNC machines, the organized chaos of a shop floor processing thousands of components daily—this is modern Indian manufacturing at its apex. The numbers tell a story of scale and precision working in harmony. HFL is the 4th largest manufacturer of complex and safety-critical, heavy-forged, and precision-machined components in India by forging capacity. With annual forging capacity of 107,000 tonnes and machining capacity of 46,100 tonnes, Happy Forgings operates at a scale that few Indian manufacturers can match. But it's not just about size—it's about sophistication.

The customer portfolio reads like a who's who of global manufacturing. Ashok Leyland, American Axle, JCB India, Mahindra & Mahindra are among the top clientele who also happen to be the major revenue drivers for FY23. Notably, the largest client contributed an estimated 15 per cent of the total revenue. This customer concentration might worry some investors, but it reflects something deeper—the stickiness of Happy Forgings' relationships.

As of September 30, 2023, its top 10 customers have remained with the company for at least 10 years. In the forging business, where switching costs are enormous and quality failures catastrophic, this longevity speaks volumes. When JCB sources a critical hydraulic component from Happy Forgings, they're not just buying a part—they're buying decades of trust, proven quality systems, and the knowledge that every component will meet specifications.

The revenue mix reveals strategic diversification. "Today, our business is divided into two sectors – automotive and non-automotive. The automotive sector contributes 40 per cent to our business, out of which commercial vehicles hold a major share." The company is known to have entered the commercial vehicle business in 2011 and on boarded clients like Ashok Leyland and American Axle.

But it's the non-automotive segment that showcases Happy Forgings' adaptability. Speaking on the non-auto segment, Garg mentioned that the company commands a 50 per cent market share in the farm equipment sector where it supplies to leading manufacturers like Swaraj, Sonalika, Escort, and Kubota. Furthermore, it has successfully acquired clients such as John Deere and Mahindra in the domain.

The three state-of-the-art facilities operate like a well-orchestrated symphony. The two Kanganwal facilities focus on medium-tonnage components, while the Dugri facility, with its 14,000-ton press, handles the heavy lifting—literally. This geographical concentration in Ludhiana might seem like a risk, but it's actually a strength. The ecosystem of suppliers, skilled workers, and logistics infrastructure makes Ludhiana ideal for heavy manufacturing.

What truly differentiates Happy Forgings is their position in the value chain. They're not just forgers—they're precision machinists. Gross profit improved to ₹205 crore, up 6.3% YoY, with the gross profit margin expanding to 57.9% compared to 56.5% a year earlier. These margins are extraordinary for what many consider a commoditized business. The secret? Value addition through machining.

When Happy Forgings receives an order for a crankshaft, they don't just forge the basic shape. They machine it to tolerances measured in microns, balance it to perfection, and deliver a component that's ready for assembly. This end-to-end capability means they capture value that would otherwise go to multiple suppliers. A forged crankshaft might sell for ₹100 per kg, but a fully machined, ready-to-assemble crankshaft commands ₹300 per kg or more.

The operational metrics reveal world-class execution. Ashish Garg, Managing Director, explained that while forging utilization is around 59% in terms of tonnage, it is closer to 74% in terms of numbers. There is potential to increase utilization by 18-20% as market momentum improves. This could lead to better operational efficiencies and higher EBITDA margins, although quantifying the exact improvement is challenging.

Customer relationships extend beyond transactions. The company's customer base includes AAM India Manufacturing Corporation Private Limited, Ashok Leyland Limited, Bonfiglioli Transmissions Private Limited, Dana India, IBCC Industries (India) Private Limited, International Tractors Limited, JCB India Limited, Liebherr CMCtec India Private Limited, Mahindra & Mahindra Limited, Meritor HVS AB, Meritor Heavy Vehicle Systems Cameri SPA, SML ISUZU Limited, Swaraj Engines Limited and others. The company has served customers in various regions including Brazil, Italy, Japan, Spain, Sweden, Thailand, Turkey, the United Kingdom and the United States of America.

The international footprint is particularly impressive. European customers, known for their exacting standards, source critical components from a company that started making bicycle pedals. This isn't charity or cost-cutting—these are sophisticated buyers who've evaluated suppliers globally and chosen Happy Forgings based on capability and reliability.

Technology integration sets Happy Forgings apart from traditional forgers. Ten robots work alongside human operators, handling repetitive tasks with precision impossible for humans to maintain over eight-hour shifts. IoT sensors monitor press performance in real-time, predicting maintenance needs before failures occur. This isn't Industry 4.0 as buzzword—it's operational excellence through technology.

The financial performance validates the business model. HFL's revenue from operations scaled up by 39.12 per cent to Rs 11,965.30 mn in Fiscal 2023, up from Rs 8,600.46 mn in Fiscal 2022. The restated Profit After Tax (PAT) rose from Rs 1,422.89 mn in Fiscal 2022 to Rs.2,087.01 mn in Fiscal 2023. The revenue from operations for the six months ended September 30, 2023, was Rs.6,729.00 mn with a restated profit of Rs.1,192.99 mn.

Risk management is embedded in the business model. While customer concentration exists, it's mitigated by long-term contracts, high switching costs, and continuous capability building that makes Happy Forgings indispensable to its customers. Raw material price volatility is managed through pass-through mechanisms in contracts. Currency fluctuations on exports are hedged. This isn't a company leaving its fate to market forces.

The competitive moat continues to widen. While competitors struggle to match either Happy Forgings' scale or precision, the company continues investing in both. The 14,000-ton press creates a capability barrier that would cost competitors hundreds of crores to match. The decades of customer relationships create trust barriers even harder to overcome. The combination of forging and machining capabilities creates operational complexity that few can replicate.

As we examine Happy Forgings' current position, we see a company that has successfully transformed from a local supplier to a global player, from a forging company to a precision engineering firm, from a family business to an institutionally-governed corporation. But the journey is far from over. The next chapter—expansion, electrification, and international growth—promises to be even more transformative.

VIII. Future Growth Strategy & Expansion Plans

The boardroom at Happy Forgings' headquarters buzzes with an energy that transcends quarterly earnings calls. Spread across the conference table are blueprints for new facilities, feasibility studies for electric vehicle components, and acquisition targets across Europe and North America. This is a company planning not for the next quarter, but for the next quarter-century. The announcement came on January 6, 2025, sending ripples through the market. Happy Forgings (HFL) has announced that its Board of Directors' has approved a capital investment of up to Rs. 650 crore to establish advanced forging capabilities to serve the non-automotive industrial segment. This new facility will be the first of its kind in Asia and the second largest globally.

The scale of ambition is breathtaking. The capex investment is focused towards heavy forged and machined components such as large crankshafts for industrial and marine applications, as well as other heavy components like axles, gears, oil & gas valves and flanges, spindles, connectors and shafts etc. These components will serve a range of non-automotive industries including, power generation, marine, mining, high-horsepower farm equipment, material handling equipment and cranes, wind energy, oil & gas and specialized segments like aerospace, defense and nuclear.

What makes this expansion particularly strategic is the weight category. The facility will produce components weighing up to 3,000 kilograms, addressing the need for high-weight components in these industries. This isn't just adding capacity—it's entering an entirely new league where only a handful of global players compete.

Ashish Garg, Managing Director of Happy Forgings Limited, stated, "We are pleased to announce this investment of approximately Rs. 650 crores to expand our forging capabilities in the heavyweight components segment. This aligns with our strategy to meet growing demand for large-sized components, particularly in sectors with limited suppliers. We believe this investment will support our growth in the industrial sector, enhance profitability, and strengthen our export presence."

The financing strategy reflects confidence. The total capital expenditure for this facility is expected to span the next 2–3 years, primarily financed through internal accruals and partially through debt. This conservative approach to leverage ensures the company doesn't overextend while pursuing growth.

Beyond organic expansion, Happy Forgings has earmarked around ₹300 crore for potential acquisitions in next three years. This isn't about buying revenue—it's about acquiring capabilities, customer relationships, and geographic presence that would take years to build organically.

The order book provides near-term visibility. Ashish Garg stated that Happy Forgings has secured approximately INR250 crores in new business with a major European farm equipment OEM and is finalizing another significant order. Additionally, they have won a INR300 crores order in the wind sector and are in discussions for further orders in the PV and CV sectors.

The passenger vehicle segment represents untapped potential. Currently at 6% of overall revenues, with expected growth to 8%-10% of total revenues over the next two years. This isn't about competing with established PV component suppliers—it's about finding niches where Happy Forgings' capabilities in heavy forging and precision machining create unique value.

The company's approach to the electric vehicle transition is pragmatic. Ashish Garg expects high single-digit growth in both the CV and farm equipment sectors domestically. The company anticipates outpacing industry growth in the CV segment due to new product launches and sees positive signs in the farm equipment sector, with production levels improving.

While passenger cars might electrify rapidly, commercial vehicles, farm equipment, and industrial machinery will continue using internal combustion engines for decades. Happy Forgings is positioning itself for this reality while gradually building capabilities for EV-specific components.

International expansion despite headwinds shows confidence. Regarding tariffs, Happy Forgings' direct exposure to the US is minimal, and they are not bearing the tariff costs, which are absorbed by the OEMs. The company remains optimistic about its North American business despite potential slowdowns.

The medium-term growth outlook of 15-18% reflects measured optimism. Happy Forgings Ltd is on track with its INR650 crores CapEx plan to enhance production capacities, including the commissioning of new presses, which will increase annual capacity by approximately 20,000 metric tonnes.

Technology integration continues to drive efficiency. The company has invested in advanced technology, research, and development to enhance its manufacturing capabilities and ensure quality standards. Robotic automation, AI-powered quality control, and predictive maintenance aren't buzzwords but operational realities.

Financial metrics support the expansion strategy. For the quarter ended 30 June 2025, revenue from operations came in at ₹354 crore, marking a 3.6% year-on-year (YoY) rise from ₹341 crore in the same period last year. Gross profit improved to ₹205 crore, up 6.3% YoY, with the gross profit margin expanding to 57.9% compared to 56.5% a year earlier.

The projected revenue CAGR of 12% from 2023 to 2026 seems conservative given the expansion plans. With forging capacity set to increase to close to 1 lakh 50,000 tonnes and new high-value segments being targeted, the company could surprise on the upside.

Risk management remains paramount. Customer concentration is being actively addressed through diversification. Raw material volatility is managed through pass-through mechanisms. Export market challenges are mitigated through geographic diversification. The company isn't betting everything on one strategy but building multiple growth engines.

As we look at Happy Forgings' future strategy, we see a company that understands its strengths—precision, scale, relationships—and is leveraging them to enter new, higher-value markets. The journey from bicycle pedals to components for nuclear reactors represents not just growth but transformation. The next five years promise to be the most exciting yet in Happy Forgings' five-decade history.

IX. Playbook: Business & Investing Lessons

If you strip away the machinery, the facilities, and even the products, what remains of Happy Forgings is a masterclass in patient capital allocation and strategic evolution. The lessons embedded in their journey aren't just applicable to manufacturing—they're universal principles of building enduring businesses in emerging markets.

Lesson 1: The Power of Patient Capital

Happy Forgings waited 32 years before taking external capital. This wasn't stubbornness—it was strategic patience. By bootstrapping through the difficult early decades, the founders retained control, learned the business intimately, and built a culture of capital efficiency that persists today. When they finally raised PE funding in 2011 and 2018, they did so from a position of strength, not desperation.

The lesson for investors: Companies that bootstrap successfully often develop DNA that makes them exceptional stewards of capital later. The discipline required to grow without external funding creates habits—cost consciousness, customer focus, operational excellence—that amplify returns when capital becomes available.

Lesson 2: Climbing the Value Chain is a Marathon, Not a Sprint

The progression from bicycle pedals to precision-machined crankshafts took decades. Each step up the value chain—from simple forgings to complex forgings, from forgings to machining, from domestic to global—built upon previous capabilities. Happy Forgings never tried to leap multiple rungs at once.

Consider the numbers: A bicycle pedal might sell for ₹10. A forged automotive component for ₹100 per kg. A precision-machined crankshaft for ₹300 per kg. A specialized industrial component for ₹500 per kg. Each step up required new capabilities, but also provided the cash flow to fund the next ascent.

Lesson 3: Customer Concentration Can Be a Moat, Not Just a Risk

The largest client contributed an estimated 15 per cent of the total revenue. As of September 30, 2023, its top 10 customers have remained with the company for at least 10 years. Traditional finance theory would flag this as a risk, but Happy Forgings turned it into a competitive advantage.

Deep relationships with major OEMs create switching costs that work both ways. When you're integrated into Ashok Leyland's supply chain, with your quality systems aligned with theirs, your production schedule synchronized with their assembly lines, and your engineers collaborating on new product development, you become nearly impossible to replace.

Lesson 4: Manufacturing Excellence in Emerging Markets

Happy Forgings proves that emerging market manufacturers can compete globally not just on cost but on quality and capability. The key is focusing on segments where labor intensity provides an advantage but quality requirements prevent commoditization.

Precision machining of forged components hits this sweet spot perfectly. It requires skilled labor (abundant in India), engineering expertise (increasingly available), and patient capital (provided by family ownership and later PE). But it also demands quality standards that create barriers to entry.

Lesson 5: The Capital Cycle in Cyclical Industries

Happy Forgings' major capacity expansions—2011, 2018, 2021—came during or just after downturns when equipment was cheaper and competitors were retrenching. 2021 & 2022: Marked expansion with the commissioning of operations in Dugri (~17 lakh sq.ft facility), a major leap in manufacturing scale. This period also saw the installation of a 14,000-ton forging press, making Happy Forgings only the second company in India to possess such a capability, paving the way for entry into the industrials segment and global exports.

This countercyclical investment strategy requires two things most companies lack: financial strength to invest during downturns and conviction that demand will return. Happy Forgings had both, partly because their conservative balance sheet gave them flexibility and partly because they understood the long-term drivers of their end markets.

Lesson 6: Technical Capabilities as Competitive Advantage

One of the standout features of a 14000-ton forging press is its ability to apply enormous force with exceptional precision. The machine can exert pressure up to 14,000 tons, which is essential for forging large and complex parts. This level of control ensures that each component meets the exact specifications required by industries like aerospace, where precision is paramount.

In industries where failure isn't an option—aerospace, defense, nuclear—technical capabilities become the primary differentiator. Price becomes secondary to reliability. Happy Forgings understood this and invested accordingly, even when returns weren't immediately apparent.

Lesson 7: Family Business Governance in the Public Markets

The transition from family-owned to professionally-managed while maintaining family control is treacherous. Many Indian companies stumble here. Happy Forgings navigated it by bringing in professional managers for operational roles while family members focused on strategy and capital allocation.

Mr. Ashish Garg is responsible for overseeing its day-to-day operations. He holds a Master's degree in Manufacturing Systems Engineering and a graduate qualification in Finance from Warwick University in the U.K. With over 17 years of experience in Operational Excellence, Business Development, and Finance Management, Ashish brings a wealth of knowledge and expertise to our team.

The combination of Paritosh Kumar's industry experience and Ashish Garg's modern management education created a powerful synthesis—respect for tradition with openness to change.

Lesson 8: The Importance of Picking Your Spots

Happy Forgings doesn't try to be everything to everyone. They don't make small, simple forgings where Chinese competitors dominate. They don't make ultra-large forgings where capital requirements are prohibitive. They found their sweet spot—complex, safety-critical components in the 50-3,000 kg range—and dominated it.

This focused strategy extends to markets too. Talking about the business contributors segment, Garg informed, "Today, our business is divided into two sectors – automotive and non-automotive. The automotive sector contributes 40 per cent to our business, out of which commercial vehicles hold a major share." The company is known to have entered the commercial vehicle business in 2011 and on boarded clients like Ashok Leyland and American Axle.

Lesson 9: Building Trust in B2B Relationships

In B2B manufacturing, trust is everything. A component failure can shut down an assembly line costing millions per day. This creates enormous switching costs—not just economic but psychological. OEM purchasing managers stake their careers on supplier selection.

Happy Forgings built trust through consistency. Same ownership for decades. Same commitment to quality. Same willingness to invest in customer-specific capabilities. This predictability becomes valuable in an unpredictable world.

Lesson 10: The Compound Effect of Continuous Improvement

Gross profit improved to ₹205 crore, up 6.3% YoY, with the gross profit margin expanding to 57.9% compared to 56.5% a year earlier. EBITDA also saw a 3.6% YoY increase, reaching ₹101 crore, supported by healthy operational efficiency and maintaining a strong margin of 28.6%.

Small improvements compound. A 1% improvement in yield. A 2% reduction in rejection rates. A 3% improvement in machine utilization. These seem trivial individually but transformed Happy Forgings from a commodity forger to a precision manufacturer with EBITDA margins that rival software companies.

The Meta-Lesson: Time Arbitrage in Building Industrial Champions

The biggest lesson from Happy Forgings is about time arbitrage. In an era of quarterly earnings obsession, they played a multi-decade game. While competitors optimized for short-term profits, Happy Forgings optimized for long-term competitive position.

This shows up in every major decision: Taking 15 years to move from bicycle pedals to automotive components. Waiting 32 years before raising external capital. Investing in a 14,000-ton press during a pandemic. These aren't the decisions of a company managing to quarterly earnings.

For investors, the lesson is clear: In industrial businesses, competitive advantages compound slowly but surely. The company that seems expensive on next year's earnings might be cheap on next decade's cash flows. Happy Forgings traded at a P/E of 33.9 at IPO—expensive for a manufacturer, cheap for a company building multi-decade moats.

The playbook Happy Forgings has written—patient capital, gradual capability building, deep customer relationships, countercyclical investment—isn't revolutionary. But executing it consistently over decades, through economic cycles, technological changes, and competitive challenges? That's what separates enduring champions from forgotten names.

X. Analysis & Investment Thesis

The investment case for Happy Forgings requires peeling back layers of complexity to reveal a simple truth: this is a company riding multiple structural tailwinds with the operational excellence to capitalize on them. But like any investment thesis worth considering, it comes with risks that demand careful scrutiny.

The Bull Case: Structural Growth Meets Operational Excellence

Start with the financials that make analysts salivate. Gross profit margin expanding to 57.9% and EBITDA margin of 28.6% for a manufacturing company seems almost fantastical. The P/E ratio of 33.9 looks expensive until you realize the company is growing revenues at 15-18% with expanding margins.

But the real bull case goes deeper than spreadsheet metrics. Happy Forgings sits at the intersection of several powerful trends. India's infrastructure build-out requires commercial vehicles. The agricultural mechanization story is still early innings. The global shift away from China creates opportunities for Indian manufacturers. The energy transition—both renewable and traditional—demands specialized components.

Ashish Garg, Managing Director, explained that while forging utilization is around 59% in terms of tonnage, it is closer to 74% in terms of numbers. There is potential to increase utilization by 18-20% as market momentum improves. This utilization dynamic reveals hidden operating leverage. As volumes grow, fixed costs get spread over more units, driving margin expansion.

The competitive advantages compound. Making Happy Forgings only the second company in India to possess such a capability with the 14,000-ton press creates a capability moat. The decades-long customer relationships create switching costs. The combination of forging and machining capabilities creates complexity that competitors struggle to replicate.

Book Value stands at ₹196 with the stock trading significantly higher, but this misses the point. The book value doesn't capture the replacement cost of capabilities built over decades, customer relationships that would take years to replicate, or the scarcity value of being one of two Indian companies with 14,000-ton forging capability.

The Bear Case: Concentration, Cyclicality, and Transition Risks

The bear case starts with customer concentration. The largest client contributed an estimated 15 per cent of the total revenue. If Ashok Leyland sneezes, Happy Forgings catches a cold. In a cyclical industry like commercial vehicles, this concentration amplifies volatility.

The industry itself faces headwinds. Commercial vehicle sales are cyclical, tied to economic growth, infrastructure spending, and freight demand. A economic slowdown would hit Happy Forgings disproportionately. The farm equipment sector faces its own challenges from erratic monsoons and farmer income volatility.

The electric vehicle transition, while distant for commercial vehicles, creates uncertainty. Happy Forgings makes components for internal combustion engines. While heavy commercial vehicles will use diesel engines for decades, the transition to electric in passenger vehicles and light commercial vehicles could pressure volumes and pricing in traditional components.

Raw material volatility presents ongoing challenges. While contracts have pass-through mechanisms, there's typically a lag. In periods of rapid steel price inflation, margins compress before recovering. This creates quarterly volatility that markets often misinterpret as fundamental weakness.

Competition is intensifying. Chinese manufacturers, despite quality perceptions, are moving up the value chain. Other Indian players are adding capacity. Global forging giants are looking at India. Happy Forgings' margins might attract competition like honey attracts bears.

The capital intensity of the business means returns on incremental capital might decline. The ₹650 crore expansion will need to generate ₹100+ crore in annual EBITDA just to maintain current returns. In a competitive market, achieving this without margin pressure will be challenging.

Valuation: Expensive for a Reason

At current valuations, Happy Forgings trades at premiums to established forging companies. The P/E of 33.9 compares to Bharat Forge at 45.85, but Bharat Forge has greater scale and diversification. The question becomes: does Happy Forgings' growth trajectory justify the premium?

The answer depends on execution. If the company delivers 15-18% revenue growth with stable margins, the valuation is reasonable. If margins compress or growth slows, the multiple will contract painfully. This binary outcome makes Happy Forgings a conviction bet rather than a diversification play.

Risk-Reward: Asymmetric but Not Without Peril

The asymmetry in Happy Forgings comes from optionality. The core business provides stability. The expansion into industrial components provides growth. The potential in wind energy, aerospace, and defense provides upside. Acquisitions could accelerate capability building. Each option has value, but quantifying it requires faith in management execution.

The downside is capped by asset value and cash generation. Even in a severe downturn, Happy Forgings' assets—land, machinery, customer relationships—have value. The company's low debt and strong cash generation provide cushion. This isn't a binary bet on survival.

The Variant Perception

The market sees Happy Forgings as an auto ancillary exposed to cyclical end markets. The variant perception is that it's transforming into a diversified precision engineering company serving resilient end markets. The auto exposure is declining as a percentage of revenue. The industrial exposure is growing. The customer base is diversifying.

More subtly, the market underappreciates the value of Happy Forgings' position in the supply chain. As OEMs increasingly focus on assembly and outsource component manufacturing, suppliers with scale, quality, and reliability become strategic partners rather than vendors. Happy Forgings is making this transition.

Catalysts and Milestones

Near-term catalysts include the commissioning of new capacity, announcement of customer wins, and margin expansion from operating leverage. Medium-term milestones include successful entry into new segments, achievement of revenue targets, and potential acquisitions.

The biggest catalyst might be rerating as the market recognizes Happy Forgings' transformation. Industrial engineering companies trade at higher multiples than auto ancillaries. As Happy Forgings' revenue mix shifts, its multiple should expand.

The Investment Decision Framework

For growth investors, Happy Forgings offers exposure to India's manufacturing renaissance with a management team that has demonstrated execution capability. The company fits the quality growth at reasonable price framework.

For value investors, the current valuation requires belief in future growth. This isn't a cigar butt but a growth company at a full price. The margin of safety comes from execution track record rather than valuation.

For income investors, the dividend yield of 0.31% offers little attraction. Happy Forgings is reinvesting for growth rather than returning cash. This will disappoint yield seekers but should excite growth investors.

The Bottom Line

Happy Forgings represents a specific type of investment opportunity: a well-managed company in a growing industry with competitive advantages that should strengthen over time. It's not cheap, carries real risks, and requires patience. But for investors who believe in India's manufacturing story and management's ability to execute, it offers exposure to powerful secular trends with operators who've demonstrated the ability to compound capital over decades.

The investment thesis ultimately rests on a simple question: Can Happy Forgings successfully transform from an auto ancillary to a diversified precision engineering company while maintaining its operational excellence? The company's history suggests yes. The challenges ahead suggest it won't be easy. The current valuation suggests the market is betting on success.

For long-term investors with conviction in India's industrial future and patience to wait for the story to unfold, Happy Forgings offers a way to participate in the country's manufacturing ambitions. Just don't expect the journey to be smooth—forging never is.

XI. Epilogue & Forward Look

As the sun sets over Ludhiana's industrial landscape, casting long shadows across Happy Forgings' sprawling facilities, the hammering of metal continues. Three shifts, round the clock, 365 days a year. The rhythm of industry never stops. Neither does the company's evolution.

The medium-term growth outlook of 15-18% feels conservative when you stand in the Dugri facility, watching the 14,000-ton press shape metal with balletic precision. This isn't just manufacturing—it's industrial choreography, each movement calculated, each outcome precise. The machine that cost hundreds of crores isn't just equipment; it's a statement of intent about Happy Forgings' future.

India's manufacturing renaissance is more than policy slogans and GDP statistics. It's playing out in facilities like Happy Forgings, where components that once came from Germany or Japan are now made in Punjab. The China+1 strategy that consultants theorize about is reality here. When European wind turbine manufacturers source critical components from Ludhiana instead of Shanghai, it's not about cost anymore—it's about capability, reliability, and geopolitical diversification.

The EV transition that keeps auto industry executives awake at night looks different from Happy Forgings' perspective. Yes, passenger vehicles will electrify. But the massive diesel engines that power ships, generators, mining equipment, and heavy trucks? Those will run on internal combustion for decades. And they'll need crankshafts, connecting rods, and other components that Happy Forgings specializes in. The transition risk that worries investors might actually be an opportunity—as competitors focus on EV components, Happy Forgings can dominate the still-massive ICE component market.

The capex investment is focused towards heavy forged and machined components such as large crankshafts for industrial and marine applications, as well as other heavy components like axles, gears, oil & gas valves and flanges, spindles, connectors and shafts etc. These components will serve a range of non-automotive industries including, power generation, marine, mining, high-horsepower farm equipment, material handling equipment and cranes, wind energy, oil & gas and specialized segments like aerospace, defense and nuclear.

The expansion into aerospace, defense, and nuclear segments isn't just diversification—it's moving into markets where price is secondary to quality, where supplier relationships span decades, where barriers to entry aren't just capital but certifications that take years to obtain. These are the markets where 57.9% gross margins aren't anomalies but expectations.

The human story continues to unfold. Paritosh Kumar, who founded the company in 1979, still provides strategic guidance. Ashish Garg, with his Warwick education and modern management approach, bridges tradition and transformation. The 3,070 employees aren't just workers—they're craftspeople, engineers, and operators who've internalized the precision that Happy Forgings demands.

Walking through the facilities, you see the future taking shape. Young engineers from IITs working alongside experienced operators who've spent decades perfecting their craft. Robots working in harmony with humans. Traditional forging techniques enhanced by AI-powered quality control. It's Industry 4.0 with an Indian accent.

The risks remain real. Economic cycles will test resilience. Competition will intensify. Technology will evolve. But Happy Forgings has survived the License Raj, thrived through liberalization, and prospered despite global competition. Each challenge has made them stronger, more focused, more capable.

Garg believes Happy Forgings has a definite edge over competitors simply because the company does not chase the competition. "The engineering solutions designed by us speak for themselves in our financials because we can create a high level of margin today in our business," he explains.

The company that started with bicycle pedals now makes components for wind turbines that power cities. The workshop that once employed a handful now provides livelihoods for thousands. The business that served local customers now supplies global OEMs. This isn't just growth—it's metamorphosis.

Looking forward, the next chapter promises to be even more transformative. The ₹650 crore expansion will create capabilities that few companies globally possess. The push into higher-value segments will improve margins further. The potential acquisitions could accelerate international expansion. The building blocks for a ₹10,000 crore revenue company are falling into place.

But perhaps the most important lesson from Happy Forgings isn't about forging metal—it's about forging a path. In a world obsessed with software and services, they've proven that manufacturing still matters. In an era of quick flips and fast exits, they've shown that patient building creates lasting value. In a business environment that celebrates disruption, they've demonstrated that sometimes, perfecting the basics is the ultimate competitive advantage.

Garg has three key elements in his mantra: being disciplined, taking risks and being constantly on alert. "To run a business with a consistent profit, there should be an unflinching devotion to the business," he states.

As we close this deep dive into Happy Forgings, the overwhelming impression is of a company that knows exactly what it is and where it's going. Not every company needs to be a unicorn. Not every business needs to disrupt industries. Sometimes, the greatest value creation comes from doing difficult things exceptionally well, consistently, over decades.

The story of Happy Forgings is far from over. The company that took 44 years to reach ₹1,000 crore in revenue might add the next ₹1,000 crore in just five years. The transformation from bicycle pedals to aerospace components continues. The journey from Ludhiana workshop to global supplier accelerates.

For investors, employees, customers, and competitors, Happy Forgings represents something important: proof that Indian manufacturing can compete globally not just on cost but on capability. That family businesses can professionalize without losing their soul. That patient capital and operational excellence can create extraordinary value.

The hammers will keep falling. The presses will keep forging. The machines will keep turning. And Happy Forgings will keep transforming metal—and expectations—one component at a time.

This is how industrial champions are built. Not in boardrooms or on spreadsheets, but on shop floors where precision meets persistence, where tradition meets technology, where Indian manufacturing meets global opportunity. The best is yet to come.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube