Happiest Minds Technologies: India's Born-Digital Moonshot

I. Cold Open & Episode Roadmap

The September 2020 IPO announcement should have been routine—another mid-sized Indian IT services company tapping public markets. Instead, something extraordinary happened. When bidding closed on September 9th, Happiest Minds Technologies had been oversubscribed 151 times, with retail investors clamoring for shares at ₹166 apiece. The grey market premium surged to 87%, signaling euphoria rarely seen even in India's frothy IPO markets.

What made investors so euphoric about a company with just ₹714 crores in revenue, competing against IT giants with thousand-crore war chests?

The answer lay in three words emblazoned across every investor presentation: "Born Digital. Born Agile." While Infosys and TCS were retrofitting their legacy businesses for the cloud era, Happiest Minds had never known a world without it. Founded in 2011—the same year Marc Andreessen declared software was eating the world—this wasn't just another IT services firm. It was positioning itself as a digital-native insurgent, unburdened by mainframe contracts or COBOL programmers.

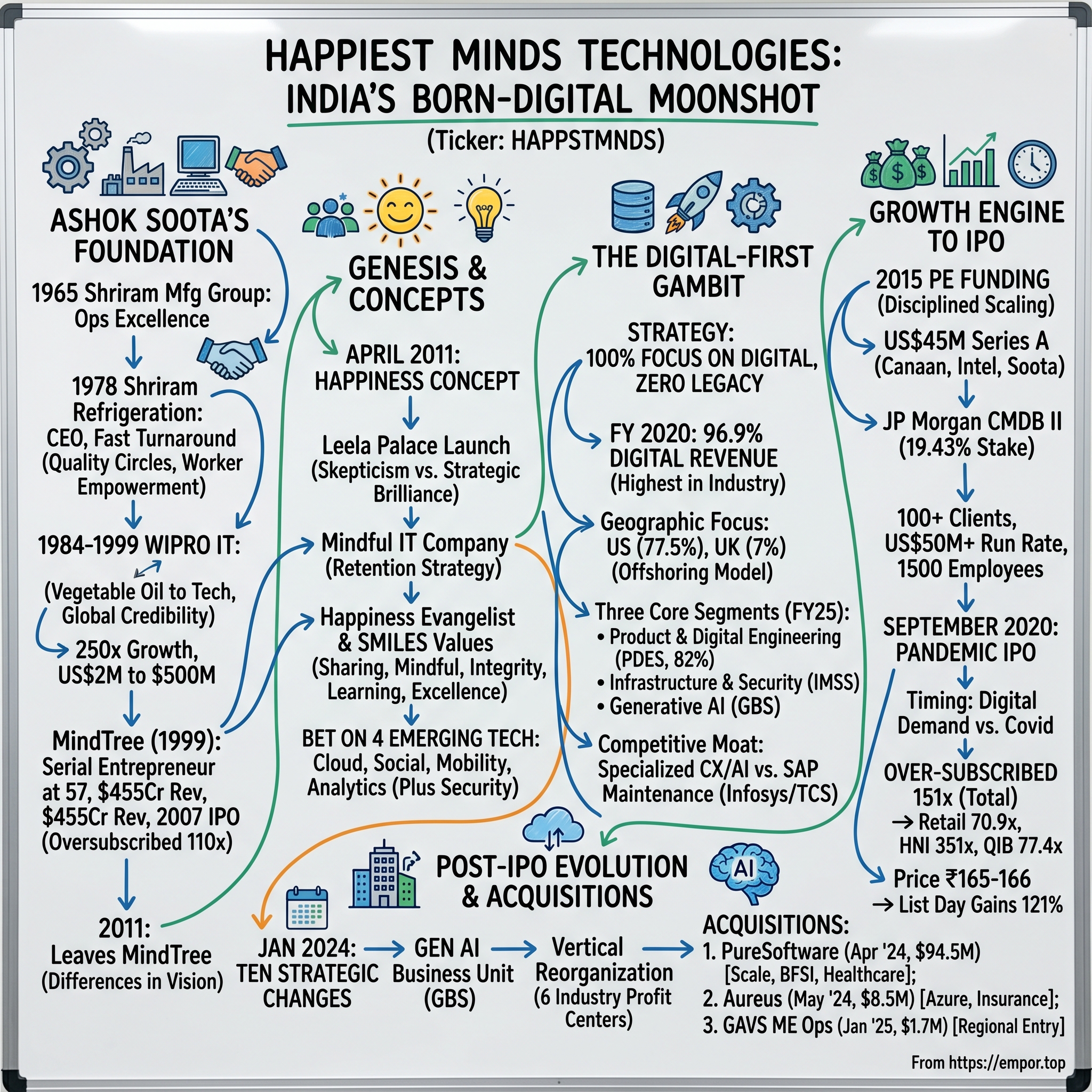

But the real story begins with the man behind the curtain: Ashok Soota, then 68 years old, launching his second entrepreneurial venture after already building MindTree into a billion-dollar enterprise. In an industry obsessed with youth and disruption, here was a septuagenarian betting his legacy on emerging technologies most CEOs couldn't spell—blockchain, AR/VR, edge computing. His previous company, MindTree, had gone public in 2007 to great fanfare. Now he was back, promising to build something even more ambitious: a "Mindful IT Company" that would embed happiness into its very DNA.

The audacity was breathtaking. Soota wasn't just competing on technology or price—he was betting that culture itself could be a competitive moat. The company appointed a "Happiness Evangelist" (yes, really), created core values that spelled SMILES (Sharing, Mindful, Integrity, Learning, Excellence), and measured employee satisfaction as religiously as EBITDA margins. In the cutthroat world of IT services, where attrition rates routinely exceed 20%, this seemed either revolutionary or delusional.

This is the story of how a serial entrepreneur's second act became one of India's most fascinating digital transformation plays—a company that would grow from zero to over ₹1,400 crores in revenue in just over a decade, acquire two companies in rapid succession, and position itself at the forefront of the GenAI revolution. It's about timing markets perfectly, building culture as strategy, and proving that in technology, sometimes the best time to start isn't when you're young and hungry—it's when you're experienced enough to know exactly which rules to break.

II. The Ashok Soota Saga: From Wipro to Serial Entrepreneur

The partition of India in 1947 created millions of refugees, but few would travel as far—literally and metaphorically—as the five-year-old boy born in what is now Pakistan's North-West Frontier Province on November 12, 1942. Ashok Soota's father was a doctor in the British Indian medical service, a detail that would prove formative. The medical profession's emphasis on discipline, continuous learning, and patient care would later manifest in unexpected ways in Soota's approach to building technology companies.

By 1965, armed with an engineering degree, Soota joined the Shriram Group—not in technology, but in industrial manufacturing. For thirteen years, he learned the unglamorous art of operational excellence, supply chain management, and turning around distressed assets. The defining moment came in 1978 when he became CEO of Shriram Refrigeration, a company bleeding red ink for four consecutive years. The board expected a multi-year turnaround. Soota delivered profitability in year one.

How? While others focused on cost-cutting, Soota redesigned the entire value chain—from supplier relationships to dealer networks. He introduced quality circles before they became fashionable, empowered factory workers to suggest improvements, and most importantly, aligned incentives across the organization. These weren't Silicon Valley innovations; they were hard-won lessons from Indian manufacturing floors. But they would prove invaluable when he made his unexpected pivot to technology.

The transition came through Wipro—then still known more for vegetable oil than software. Azim Premji had just begun his audacious transformation of his father's cooking oil company into a technology conglomerate. He needed someone who understood operations, could build at scale, and most importantly, could sell the Wipro story to skeptical Western clients who couldn't understand why an Indian soap company wanted their IT contracts. Between 1984 and 1999, Soota led Wipro's IT business from just US$2 million to US$500 million run-rate—a 250x growth that transformed both the company and the Indian IT industry. Before joining Wipro, he was running Shriram Refrigeration, which was five times larger than Wipro's IT business at the time, turning it from a loss-making company to a profitable market leader. But Soota saw the future: "I could see that the IT business was where the growth would be".

The Wipro years weren't just about scale—they were about establishing credibility for Indian IT on the global stage. Intel's legendary CEO Andy Grove personally recognized his contributions, a validation that mattered immensely when Indian companies were still fighting perception battles in Silicon Valley boardrooms. Under Soota's leadership, Wipro even overtook Infosys to become the number 2 software company in India at one point.

But in 1999, at the peak of his corporate success, Soota did something unexpected. He walked away from one of the most powerful positions in Indian IT to start from scratch. He co-founded Mindtree alongside nine other professionals, embracing the uncertainty of entrepreneurship at 57—an age when most executives are planning their retirement portfolios, not their startup pitch decks.

Mindtree achieved ₹455 crore in revenue within six years and went public in 2007, with its IPO oversubscribed 110 times. The company would eventually reach billion-dollar revenues, validating Soota's belief that Indian IT could spawn successful second-generation companies. But despite the success, Soota eventually stepped away, citing differences in vision and strategy.

By 2011, most would have considered Soota's career complete—two successful companies, an IPO, industry recognition, wealth beyond measure. He had served as President of the Confederation of Indian Industry (CII) and was a member of the Prime Minister's Task Force for IT. His place in Indian IT history was secure.

Yet at 68, an age when his contemporaries were writing memoirs, Soota was sketching business plans. The decision to start Happiest Minds wasn't about money or legacy—it was about unfinished business. The IT services industry he'd helped build was becoming commoditized, trapped in a low-margin race to the bottom. He saw an opening for something different: a company built from day one for the digital age, unencumbered by legacy systems or thinking. The serial entrepreneur was ready for his most audacious bet yet.

III. Genesis: The "Happiest Minds" Concept (2011)

The conference room at the Leela Palace in Bangalore buzzed with skepticism on that April morning in 2011. Journalists had gathered expecting another IT services company launch—India was churning out dozens every month. Instead, Ashok Soota stood before them and announced something that sounded almost absurd: he was building a company around happiness.

"We will measure success not just by revenue or profit, but by creating the Happiest People and Happiest Customers," Soota declared, flanked by his founding team including CEO & MD Vikram Gulati. The room's reaction ranged from bemused smiles to outright confusion. In an industry where "bench strength" and "utilization rates" dominated boardroom discussions, here was a veteran talking about appointing a "Happiness Evangelist."

The cynics missed the strategic brilliance hidden in the feelgood messaging. Happiest Minds was positioning itself as "a mindful IT company" focused on enabling digital transformation for enterprises and technology providers. The happiness framework wasn't corporate fluff—it was a retention strategy in an industry bleeding talent to Silicon Valley startups. The core values—Sharing, Mindful, Integrity, Learning, Excellence—deliberately spelled SMILES, creating a mnemonic device that would stick in employees' minds long after orientation ended.

But the real differentiation lay in the technology bets. While established players were still making fortunes from ERP implementations and mainframe migrations, Soota's team identified four emerging technologies that would define the next decade: cloud computing, social media, mobility, and analytics. Security would be added as a fifth pillar. This wasn't speculation—it was pattern recognition from someone who'd seen multiple technology waves crash and recede.

The founding team composition revealed the strategy. Unlike typical startups founded by young engineers, Happiest Minds assembled industry veterans who brought deep domain expertise and, crucially, existing client relationships. They weren't trying to disrupt the industry; they were planning to outmaneuver it by moving faster into emerging spaces while incumbents protected legacy revenue streams. The founding team that joined Soota included CEO & MD Vikram Gulati, who brought over 23 years of IT industry experience as the former CEO and President of Intelligroup. The broader leadership team included Ramakanth Desai and Puneet Jetli as Co-CEOs of IT Services Business, Salil Godika as Chief Strategy & Marketing Officer, Joseph Anantharaju leading Software Products Engineering, and several other industry veterans who had spent two decades in the industry.

The early funding story defied conventional startup wisdom. Within months of launch, Happiest Minds secured a $45 million Series A investment—led by Canaan Partners, Intel Capital, and Ashok Soota himself. This was the largest first-round funding in Indian IT services history at the time, signaling investor confidence in the team's ability to execute despite being industry newcomers.

Soota articulated the opportunity clearly: "The shifting technology landscape provides opportunities and an entry strategy for new players like Happiest Minds. These new technologies enable IT to become more for transformational enterprises and measurable in terms of its business impact. Happiest Minds will be differentiated by its sharp focus on these technologies, focused solutions, people brand, deep domain expertise and non-linear growth".

The strategy was audacious yet pragmatic. Instead of competing head-on with TCS or Infosys for traditional outsourcing deals, Happiest Minds would focus exclusively on digital technologies where the playing field was more level. They wouldn't maintain armies of COBOL programmers or mainframe specialists. Every hire, every investment, every client engagement would align with the digital-first vision.

By the end of 2011, skeptics were beginning to pay attention. The company that started with a seemingly naive focus on happiness had assembled serious firepower—veteran leadership, substantial funding, and most importantly, a clear thesis about where the industry was heading. The stage was set for what would become one of the most focused digital transformation plays in Indian IT.

IV. The Digital-First Gambit: Building While Others Transform

Picture the typical large Indian IT services company boardroom in 2011: executives staring at PowerPoint slides showing 70% of revenues from legacy maintenance, 20% from package implementation, and maybe—if they were progressive—10% from "emerging technologies." The digital transformation budget was usually a rounding error, hidden somewhere in the "innovation fund." Now picture Happiest Minds' first strategy session: 100% focus on digital, zero legacy, no compromise.

This wasn't bravado—it was calculated positioning. While Infosys and TCS were managing the delicate balance of protecting multi-billion dollar legacy revenues while investing in digital capabilities, Happiest Minds had the luxury of starting fresh. No sacred cows, no quarterly earnings pressure from Wall Street, no thousand-person bench trained in yesterday's technologies. By Fiscal 2020, the numbers validated the strategy: 96.9% of the company's revenues came from digital services which is one of the highest among Indian IT companies. To put this in perspective, most traditional IT giants were struggling to push their digital mix past 30-50% of revenues. Happiest Minds had essentially inverted the industry's revenue pyramid.

The company organized itself into three core segments that would define its growth trajectory. Product & Digital Engineering Services (PDES), which would eventually account for 82% of revenues by FY25, served 6 sectors including BFSI, EdTech, Healthcare, Industrial & Manufacturing, Hi-Tech & Media, and Retail & Logistics. The second pillar, Infrastructure Management & Security Services (IMSS), focused on next-generation infrastructure rather than data center management. The third, which would later evolve into Generative AI Business Services (GBS), positioned the company at the bleeding edge of AI transformation.

The technology stack wasn't accidental—it was architected. Happiest Minds leveraged a spectrum of disruptive technologies: artificial intelligence, blockchain, cloud, digital process automation, internet of things, robotics/drones, security, virtual/augmented reality. Each capability was built not in isolation but as part of an integrated offering. A retail client implementing IoT sensors would naturally need edge computing, real-time analytics, and security—all available from the same vendor.

Geographic focus revealed another strategic choice. 77.5 per cent revenue from the US and follows the offshoring model (77.5 per cent)—the company wasn't trying to be everywhere. It concentrated firepower on markets where digital transformation budgets were largest and decision-making fastest. The UK provided another 7%, with the remaining split between India and emerging markets.

Early client wins demonstrated the model's viability. Unlike traditional outsourcers who started with application maintenance contracts and hoped to upsell, Happiest Minds entered at the transformation layer. For the world's leading beverage maker, Happiest Minds enhanced their sales process through a generative AI enabled chat bot for actionable intelligence and decision making. For a leading American multinational investment bank and financial services company, Happiest Minds was selected to drive their digital transformation program.

The competitive positioning was subtle but effective. When a Fortune 500 company needed someone to maintain their SAP systems, they called Infosys. When they needed to build a mobile-first customer experience powered by AI, Happiest Minds was increasingly on the shortlist. The company wasn't competing for the same deals—it was creating a new category.

Building credibility required more than technical capabilities. The company invested heavily in analyst relations, winning recognition from firms like ISG and Everest Group. Industry certifications, partnerships with cloud providers, and thought leadership became force multipliers. The message was consistent: we're not a cheaper alternative to incumbent vendors; we're a better alternative for digital initiatives.

The financial model reflected the strategy's ambition. While traditional IT services companies optimized for 15-18% EBITDA margins through scale and automation, Happiest Minds targeted 20%+ margins through value-based pricing and IP leverage. Higher margins would fund continued investment in emerging technologies, creating a virtuous cycle of capability building and premium positioning.

By 2020, as the company prepared for its IPO, the digital-first gambit had paid off spectacularly. What started as a contrarian bet on avoiding legacy technologies had become the company's greatest strength. In a world suddenly forced into digital acceleration by a global pandemic, Happiest Minds found itself perfectly positioned for the moment.

V. The Growth Engine: Scaling to IPO (2011-2020)

The conference call with JP Morgan's private equity team in 2015 should have been routine due diligence. Instead, it turned into a three-hour strategic deep dive that would reshape Happiest Minds' trajectory. The PE investors weren't just bringing capital—they were bringing discipline, governance structures, and most importantly, pressure to articulate a path to public markets.

Building from zero to ₹714 crores revenue by FY20 required more than organic growth—it demanded systematic execution across multiple vectors simultaneously. The company's approach resembled a three-dimensional chess game: expanding client relationships vertically, adding new accounts horizontally, and building capabilities in the third dimension.JP Morgan Private Equity Group, along with Intel Capital and Ashok Soota, invested $52.5 million in Series A funding, marking one of the largest early-stage investments in Indian IT services history. JP Morgan Investment Management CMDB II held 19.43% stake and would eventually exit completely through the IPO, making about 40%+ IRR on its 5-year old investment.

The customer concentration challenge plagued most mid-tier IT companies—too few clients contributing too much revenue. Happiest Minds tackled this systematically. By 2015, they had crossed 100 valued customers and reached a $50 million+ annualized revenue run rate with over 1,500 employees. More importantly, no single client accounted for more than 15% of revenues, providing stability that investors craved.

Geographic expansion followed a disciplined playbook. The company established operations in the U.S., UK, The Netherlands, Australia and Middle East, but maintained cost discipline by keeping 77.5% of delivery offshore. This wasn't about planting flags—each location was chosen based on specific client needs or regulatory requirements.

The goal of being on course to achieve US$ 100 million revenue faster than any other Indian IT services company became the North Star metric. Every strategic decision—which clients to pursue, which capabilities to build, which geographies to enter—was evaluated through this lens. Speed mattered as much as scale.

Competition from established players required creative positioning. When Infosys or TCS pitched for a $50 million engagement, Happiest Minds couldn't compete on scale or pricing. Instead, they positioned themselves as specialists—the boutique consulting firm for digital initiatives while the giants handled the commodity work. "What's a small project for big IT firms is big business for us," became the internal mantra.

The leadership team evolved significantly during this period. Vikram Gulati, the founding CEO, departed in 2014 when he couldn't relocate to Bangalore due to personal priorities. Sashi Kumar took over as CEO & MD, bringing stability and operational excellence. The company built a second line of leadership, ensuring no single departure could derail growth momentum.

Culture remained the invisible differentiator. While competitors struggled with 25-30% attrition rates, Happiest Minds maintained industry-leading retention through innovative engagement programs. The "Happiness Evangelist" role, initially mocked by industry observers, proved prescient—engaged employees delivered better client outcomes, creating a virtuous cycle of growth and retention.

Building the IPO narrative required more than just financial performance. The company needed to demonstrate sustainable competitive advantages, scalable business model, and addressable market opportunity. By FY20, with ₹714 crores in revenue and consistent profitability, the story was compelling: a digital-first player perfectly positioned for the coming acceleration in enterprise transformation spending.

The PE funding had served its purpose—providing not just capital but credibility, governance structures, and pressure to perform. As JP Morgan prepared its exit, they had helped transform a startup into an IPO-ready enterprise. The stage was set for public markets.

VI. The IPO Story: Timing the Digital Wave (2020)

March 2020 should have been a disaster for an IPO. The pandemic had frozen capital markets, companies were withdrawing listings, and investors were hoarding cash. Inside Happiest Minds' boardroom, the debate raged: postpone indefinitely or push ahead into the uncertainty? Ashok Soota, now 77, made the call that would define the company's next chapter: "The world is going digital faster than ever. If not now, when?"

The draft red herring prospectus filed with SEBI in June 2020 made Happiest Minds the first company to file for an IPO since the pandemic began. The timing seemed either prescient or foolish—nobody could tell which. The IPO comprised a fresh issue of ₹110 crore and an offer for sale of 3.57 crore shares, with JP Morgan exiting its entire 19.43% stake and promoter Ashok Soota selling 84.14 lakh shares.

The price band was set at ₹165-166 per share, with bidding scheduled from September 7-9, 2020. The pricing raised eyebrows—at the upper band, the company would be valued at over ₹2,300 crores, implying a P/E multiple higher than many established mid-tier IT players. JP Morgan's complete exit was unusual—PE investors rarely sold their entire stake at IPO if they believed in continued growth—but the fund was making about 40%+ IRR on its 5-year old investment.

Then something extraordinary happened. As subscription opened on September 7th, retail investors flooded in. HNIs (High Net Worth Individuals) bid aggressively. Institutional investors, starved of quality tech IPOs, piled in. By the time bidding closed on September 9th, the IPO had been oversubscribed 151 times—one of the most successful IPOs in Indian capital markets history.

The retail portion, despite being limited to just 10% of the issue (versus the typical 35%), was oversubscribed 70.94 times. The QIB (Qualified Institutional Buyer) portion saw 77.43 times subscription, while the HNI portion was oversubscribed an astounding 351.46 times. The grey market premium surged to 87%, indicating shares would likely list at nearly double the IPO price.

What drove this euphoria? Three factors converged perfectly. First, 96.9% of revenue from digital services positioned Happiest Minds as a pure-play digital transformation bet—exactly what investors wanted in a post-COVID world. Second, the founder's track record—Soota had already delivered one successful IPO with MindTree—provided credibility. Third, the small retail allocation created artificial scarcity, driving demand even higher.

The listing day on September 17, 2020, validated the enthusiasm. Shares opened at ₹351 on NSE, a 111% premium to the issue price, and closed the day at ₹366.95, delivering listing gains of 121%. Ashok Soota's shareholding reduced from 61.8% to 53.2% post-IPO, but the value of his remaining stake had more than doubled in a single day.

The promoter's 50% stake that had been pledged against a ₹40 crore loan facility from Avendus since July 2019 was removed post-IPO, eliminating a potential overhang. The fresh capital of ₹110 crore would fund working capital needs and provide dry powder for acquisitions—critical for competing against larger rivals.

The IPO transformed Happiest Minds from a private company into a public entity with new obligations and opportunities. Quarterly earnings calls, analyst coverage, institutional scrutiny—all would require a different level of operational discipline. But it also provided currency for acquisitions, credibility with large clients, and liquidity for employees holding ESOPs.

Market observers noted the irony: while traditional IT giants were trading at depressed valuations due to concerns about legacy revenue cannibalization, a company with less than ₹1,000 crores in revenue commanded premium multiples by positioning itself as "born digital." The message to the industry was clear—narrative matters as much as numbers.

The post-IPO ownership structure revealed interesting dynamics. While Soota remained the dominant shareholder, the entry of marquee institutional investors like Morgan Stanley, Goldman Sachs, and various mutual funds provided validation and liquidity. Employee ownership through ESOPs ensured alignment between company performance and individual wealth creation.

For Ashok Soota, the IPO represented vindication of his digital-first strategy. At an age when most founders would be content with private wealth, he had chosen the scrutiny and pressure of public markets. The successful listing wasn't just about valuation—it was about proving that Indian IT could spawn successful next-generation companies, not just legacy giants.

VII. Post-IPO Evolution: Acceleration & Acquisitions (2020-Present)

The Monday morning leadership meeting in January 2024 felt different. Ashok Soota, now 81, unveiled what he called "ten strategic transformational changes" that would reshape Happiest Minds. The company that had gone public as a digital services provider was about to transform itself again—this time into an AI-first enterprise with aggressive acquisition ambitions.

The establishment of Gen AI business services, BU reorganization with industry groups into profit centers, and two excellent acquisitions have set the foundation for the best performance since IPO. The creation of the Generative AI Business Services (GBS) unit wasn't just organizational reshuffling—it was a bet that GenAI would be as transformational as cloud computing had been a decade earlier. The PureSoftware acquisition in April 2024 for $94.5 million (₹779 crores) represented the company's largest M&A move. PureSoftware with a global presence and headquarters in Noida is a fast-growing Digital Engineering & Transformation Services and solutions provider with deep domain expertise. The 1,200-person company brought not just scale but strategic capabilities in BFSI and Healthcare verticals, plus a near-shore presence in Mexico and offices in Singapore, Malaysia, and Africa. PureSoftware reported revenues of US $ 43 Million (~ ₹351 Crores) for Fiscal 2024.

The Aureus acquisition followed quickly in May 2024 for $8.5 million. The 150-person company headquartered in Denver, Colorado with a development center in Hyderabad partners with Fortune 500 companies including global Insurance and Reinsurance providers and Healthcare & Life Sciences enterprises in their cloud transformation journeys. As a Microsoft Certified Gold & Co-sell Partner, Aureus brought critical Azure expertise and domain depth in insurance and reinsurance.

These weren't opportunistic purchases—they were strategic chess moves. The acquisition of PureSoftware and Aureus, the creation of our GenAI Business Unit (GBS), hiring a senior leader to expand net new (NN Sales), and creating six Industry Groups, each headed by an Industry Manager represented a comprehensive transformation of the company's go-to-market approach.

The reorganization into six industry groups—each operating as profit centers—marked a fundamental shift from horizontal service lines to vertical domain expertise. Banking, Financial Services & Insurance (BFSI), EdTech, Healthcare & Life Sciences, Hi-Tech and Media & Entertainment, Industrial, Manufacturing, Energy & Utilities, and Retail, CPG & Logistics would each have dedicated leadership, P&L responsibility, and specialized capabilities. The financial results validated the strategy. Revenue growth accelerated to 28.2% YoY in constant currency in Q2 FY25, with EBITDA margin of 22.7%—well within the guidance range of 20% to 22%. Year-to-date revenue growth in constant currency reached 26% with EBITDA growing at 26.3%. The company was set to report best performance since the initial public offering (IPO).

Geographic expansion took on new urgency. While maintaining focus on the US (84% of revenue), the company began building presence in Middle East markets through strategic acquisitions. The January 2025 acquisition of GAVS Technologies' Middle East Operations for $1.7M provided entry into a high-growth market with established relationships.

The Arttha banking platform emerged as a flagship intellectual property, winning recognition as 'Best Banking-as-a-Service Platform of the Year' at the Africa Bank 4.0 Summit. This wasn't just professional services anymore—Happiest Minds was building products that could scale beyond linear growth models.

GenAI became the spear tip of the growth strategy. For the world's leading beverage maker, Happiest Minds enhanced their sales process through an generative AI enabled chat bot for actionable intelligence and decision making. For a prominent credit union service organization, Happiest Minds built two highly replicable GenAI solutions that help with training their employees on performance management and customer support.

The workforce expanded dramatically—from 5,168 employees in Q4 FY24 to 6,599 by June 2024, largely through acquisitions. But integration wasn't just about headcount. The company focused on cultural alignment, ensuring PureSoftware's "Customer Delight by Creating Employee Delight" philosophy harmonized with Happiest Minds' happiness-first approach.

Recognition from industry analysts provided external validation. The company achieved "Leadership Zone" ratings from Zinnov Zones in multiple categories, became a "Major Contender" in Everest Group's Cybersecurity Services PEAK Matrix, and was recognized among the '50 Best Firms for Data Scientists to Work For' by Analytics India Magazine.

Looking forward, Ashok Soota articulated an audacious vision: $1 billion in revenues by FY31. For a company that crossed $200 million just recently, this represented 5x growth in seven years. But with the foundation now in place—strategic acquisitions integrated, GenAI capabilities built, industry verticals organized—the path seemed clearer than ever before.

VIII. Playbook: The Happiest Minds Model

Inside the Happiest Minds war room, there's a slide that executives reference constantly: "We don't compete where legacy players are strong; we compete where they're conflicted." This single insight encapsulates the strategic playbook that transformed a 2011 startup into one of India's most valuable mid-tier IT companies.

The "Born Digital" advantage versus digital transformation isn't just marketing—it's fundamental architecture. Traditional IT giants carry the burden of transformation: retraining thousands of mainframe programmers, cannibalizing profitable legacy contracts, managing Wall Street expectations while pivoting business models. Happiest Minds never faced these conflicts. Every hire, every training program, every client engagement started with digital-first thinking.

Global Digital enterprise spend is expected to increase by ~20 per cent for the next five years. With almost 78 per cent of clients being served from India and access to a large IT talent pool, Happiest Minds positioned itself perfectly at the intersection of demand explosion and supply advantage. The company didn't need to be the biggest—it needed to be the most focused.

Culture as competitive advantage sounds soft until you examine the numbers. While industry attrition rates hover around 20-25%, Happiest Minds consistently maintains lower churn through its happiness-first approach. Lower attrition means higher project continuity, deeper client relationships, and reduced recruitment costs—all flowing directly to margins. The "Happiness Evangelist" role that seemed quirky in 2011 now looks prescient as companies globally grapple with employee engagement in hybrid work models.

Managing high growth with profitability requires deliberate choices. The company maintains EBITDA margins of 20-22%, higher than many larger peers, by focusing on value over volume. Instead of competing for commodity application maintenance contracts at 8-10% margins, Happiest Minds targets digital transformation initiatives where clients pay premium rates for specialized expertise. The math is simple: better to have 100 clients paying premium rates than 1,000 clients grinding down prices.

The mid-tier sweet spot—not too big, not too small—provides unique advantages. Large enough to handle enterprise-scale projects, yet nimble enough to make decisions quickly. Important enough to get CEO attention at clients, yet not so large that bureaucracy stifles innovation. This Goldilocks positioning allows Happiest Minds to win deals that are too complex for startups but too specialized for giants focused on billion-dollar contracts.

The dual acquisition strategy reveals sophisticated thinking about inorganic growth. PureSoftware brought scale and domain depth—1,200 employees and established BFSI relationships. Aureus brought specialized capabilities—Azure expertise and insurance domain knowledge with 150 people. Together, they accelerated Happiest Minds' journey by 3-4 years, providing both immediate revenue and long-term capability building.

Building IP while remaining a services company represents the holy grail of IT services—non-linear growth. The Arttha banking platform, recognized globally for innovation, demonstrates this approach. Instead of building products in isolation, Happiest Minds develops IP through client engagements, ensuring market validation and funding while retaining rights to productize solutions. This hybrid model provides the stability of services revenue with the scalability of product offerings.

The focus on emerging technologies—GenAI, blockchain, IoT, AR/VR—before they become mainstream provides first-mover advantages. When enterprises finally allocate budgets for these technologies, Happiest Minds already has trained teams, proven methodologies, and reference clients. This forward-positioning strategy requires investment ahead of revenue, but creates competitive moats that are difficult for followers to breach.

Organizational design reflects strategic priorities. The 2024 reorganization into six industry-focused profit centers wasn't just structural reshuffling—it was acknowledgment that domain expertise matters more than technical skills in winning digital transformation deals. A banker evaluating vendors cares less about your Java expertise and more about your understanding of open banking regulations and neo-bank architectures.

The capital allocation philosophy balances growth and returns. While maintaining investment in organic capability building, the company returns cash to shareholders through consistent dividends—₹5.75 per share in FY24, demonstrating confidence in cash generation. This balanced approach attracts both growth and value investors, broadening the shareholder base.

Geographic concentration in the US (84% of revenue) seems risky until you consider the alternative. Instead of spreading thin across 50 countries, Happiest Minds dominates specific verticals in the world's largest IT services market. This focused approach enables deeper client relationships, better price realization, and efficient resource allocation.

The lesson for competitors is uncomfortable: success in IT services increasingly requires choosing what not to do. Happiest Minds chose not to maintain legacy capabilities, not to chase low-margin contracts, not to expand indiscriminately. These conscious exclusions created space for focused excellence in digital services—a playbook that's easier to admire than replicate.

IX. Analysis: Bear vs. Bull Case

Bull Case: The Digital Acceleration Thesis

The investment thesis for Happiest Minds writes itself in an era where every board meeting includes "digital transformation" as an agenda item. With digital-first positioning in a growing market, the company sits at the intersection of secular tailwinds that could drive growth for the next decade.

The leadership pedigree provides unusual comfort in a sector littered with failed ventures. Ashok Soota isn't learning on the job—he's applying patterns recognized over fifty years in technology. His previous company, MindTree, went from zero to billion-dollar revenues. The playbook is proven; only the scale differs. When a founder has delivered successful IPOs twice before, betting against the third attempt requires particular courage or foolishness.

Recent performance validates the strategy. Year-to-date revenue growth in constant currency of 26% and EBITDA of 26.3% places Happiest Minds among the fastest-growing IT services companies globally. More importantly, this growth comes with expanding margins, demonstrating pricing power rare in a commoditizing industry. The Q2 FY25 acceleration to 28.2% YoY growth suggests momentum building rather than peaking.

The successful M&A integration capabilities demonstrated through PureSoftware and Aureus acquisitions reveal institutional maturity beyond the company's age. While many tech companies destroy value through poor acquisition integration, Happiest Minds has shown ability to identify, acquire, and integrate complementary businesses. This M&A muscle memory becomes increasingly valuable as industry consolidation accelerates.

GenAI and emerging tech capabilities position the company for the next technology wave. While larger competitors debate how to incorporate AI without cannibalizing existing services, Happiest Minds built a dedicated GenAI Business Services unit from scratch. Early client wins in GenAI—from beverage makers to credit unions—demonstrate ability to commercialize emerging technologies before they become commoditized.

The structural advantages of being "born digital" compound over time. No legacy infrastructure to maintain, no obsolete skills to retrain, no conflicted priorities between old and new business models. Every dollar of investment goes toward future capabilities rather than maintaining the past. This efficiency gap versus traditional players widens with each technology transition.

Bear Case: The Scalability Question

Yet serious challenges lurk beneath the growth narrative. 84 per cent of revenue from USA and UK exposes Happiest Minds to concentrated geographic risk at a particularly volatile moment. Rising anti-immigration sentiments, push against outsourcing, and potential policy changes under different administrations could dramatically impact growth. A single piece of legislation restricting H1-B visas or offshore development could crater the business model.

Intense competition from both large and mid-tier players threatens margins and growth. When TCS, Infosys, and Wipro finally complete their digital transformations—and they will—they'll compete directly with Happiest Minds but with 100x the resources. Meanwhile, other mid-tier players like Persistent Systems and Coforge are executing similar digital-first strategies. The competitive moat isn't as wide as it appears.

The market's verdict is sobering: Market cap down -23.2% in 1 year despite strong operational performance. While revenue and profits grow, the stock price declines, suggesting investors either don't believe the growth is sustainable or think it's already priced in. This divergence between operational performance and market valuation often signals concerns about future prospects that aren't yet visible in financial statements.

Dependency on tech spending cycles creates vulnerability to macroeconomic shocks. When enterprises cut discretionary spending, digital transformation projects are often first to be delayed or canceled. Unlike mission-critical maintenance work that continues regardless of economic conditions, Happiest Minds' digital services are more susceptible to budget volatility.

Scale disadvantages versus larger competitors become more pronounced as deals get bigger. While Happiest Minds can win a $10 million digital transformation project, competing for $100 million integrated deals requires global delivery capabilities, financial strength, and risk absorption capacity that favors larger players. The company risks being stuck in the middle—too big to be nimble, too small to compete for mega-deals.

The founder dependency risk looms large. At 81, Ashok Soota remains Executive Chairman and the company's spiritual core. While succession planning exists, the transition from founder-led to professionally-managed company often proves rocky in Indian IT. Investors buying the stock are implicitly betting on successful leadership transition—never a certainty.

Customer concentration, while managed, remains a concern. The top 10 clients contribute significant revenue percentage, and losing even one major account could impact growth trajectories. In enterprise IT services, client relationships can change quickly with CIO transitions or strategic vendor consolidations.

The sustainability of 20%+ EBITDA margins faces pressure from multiple directions: wage inflation in India, competition for digital talent, investment requirements in emerging technologies, and client pressure on pricing. Maintaining premium margins while scaling becomes increasingly difficult as the company grows beyond the $500 million revenue mark.

The Verdict

The bull-bear debate ultimately hinges on whether Happiest Minds can maintain its differentiation as the industry evolves. Bulls see a company perfectly positioned for digital acceleration with proven execution capabilities. Bears see a subscale player in an increasingly competitive market with concentrated risks. The truth, as often happens, likely lies somewhere in between—a solid growth story with real risks that require careful monitoring.

X. Looking Forward: The Next Chapter

The handwritten note on Ashok Soota's desk reads simply: "What's next after digital?" At 81, when most founders would be writing memoirs, Soota is architecting the company's third transformation. The creation of Happiest Health, a knowledge, health & wellness enterprise and SKAN, India's first private sector, non-profit organization for medical research on aging and neurological disorders reveals ambitions beyond IT services.

These aren't vanity projects. Happiest Health represents Soota's belief that the intersection of healthcare and technology will define the next decade. SKAN (Soota Centre for Advanced Knowledge in Ageing and Neurodegeneration) tackles aging and neurological disorders through cutting-edge research. For a founder who started his third company at 68, understanding aging isn't academic—it's personal. The synergies with Happiest Minds' healthcare vertical are obvious, even if the business models remain separate.

The founder's evolving vision beyond IT reflects a broader transformation in Indian technology. The generation that built India's IT services industry is asking what comes next. Soota's answer: apply technology expertise to solve fundamental human problems—health, aging, education. This expansion of ambition from services to solutions, from revenue to impact, could define Happiest Minds' next chapter.

AI and GenAI as the next growth frontier isn't speculation—it's already happening. The company's GenAI Business Services unit, created in 2024, represents more than organizational restructuring. It's a bet that AI will be as transformational as the internet, requiring specialized expertise that traditional IT services companies will struggle to build. Early client wins validate this thesis, but the real test comes when GenAI moves from pilot projects to production systems.

The long-term growth target to be at least 1.5x market growth, which was set even at the time of IPO, seems conservative given recent performance. With the market growing at 10-12% and Happiest Minds growing at 25-30%, the company is already exceeding this target. The real question: can this outperformance continue as the base gets larger? The $1 billion revenue target by FY31 implies 20%+ CAGR—ambitious but achievable if current momentum sustains.

Succession planning and leadership transition represents the elephant in the room. Joseph Anantharaju's elevation to Executive Vice Chairman signals the beginning of transition, but Indian IT has few examples of successful founder succession. The challenge isn't just replacing Soota's strategic vision—it's maintaining the culture and values that differentiate Happiest Minds. The next leader must be both operator and evangelist, strategist and culture carrier.

What would success look like in 5 years? By 2030, Happiest Minds could be a $750 million revenue company with leadership positions in GenAI services, healthcare technology, and digital engineering. The company would have completed 3-5 more strategic acquisitions, expanding geographic presence and capability depth. Employee count could reach 15,000, maintaining the happiness-first culture while operating at scale. The Arttha platform and other IP assets would contribute 15-20% of revenues, providing non-linear growth.

But success might look different than traditional metrics suggest. If Soota's vision materializes, Happiest Minds in 2030 won't just be measured by revenue or market cap. It will be evaluated by impact: healthcare solutions improving patient outcomes, AI systems augmenting human capability, aging research extending productive lifespans. The company that started with happiness as its organizing principle might end up redefining what success means in Indian IT.

The regulatory and policy environment adds complexity to forecasting. Data localization requirements, AI governance frameworks, and cybersecurity regulations will shape service delivery models. Happiest Minds' focus on emerging technologies means navigating uncharted regulatory waters—an advantage for those who get it right, existential risk for those who don't.

Market dynamics suggest continued consolidation in mid-tier IT services. Companies with subscale revenues and undifferentiated offerings will struggle to compete. Happiest Minds could be acquirer or acquired, predator or prey. The company's strong balance sheet and proven M&A capability suggest it will be buyer rather than seller, but in technology, today's hunter often becomes tomorrow's hunted.

The broader question facing all Indian IT services companies: what happens when India is no longer the low-cost destination? As Indian engineering salaries rise and other countries develop technical capability, the labor arbitrage model weakens. Happiest Minds' focus on specialized expertise rather than cost advantage positions it better than commodity players, but the entire industry faces this transition.

For long-term investors, Happiest Minds represents a bet on Indian IT's ability to reinvent itself. The company that started as a digital services provider could evolve into something entirely different—a healthcare technology company, an AI platform provider, or something not yet imagined. The journey from ₹714 crores to potentially ₹7,000 crores won't be linear, but for those who believe in the vision, it might be transformational.

The most intriguing possibility: Happiest Minds becomes the template for next-generation Indian technology companies. Not just service providers but solution creators. Not just executing strategies but setting them. Not just following global trends but defining them. If this vision materializes, the company that started with a focus on happiness might end up showing Indian IT what comes after the services era.

XI. Recent News

The drumbeat of quarterly results tells a story of sustained momentum. Q3 FY25 delivered revenue growth of 28.2% y-o-y in constant currency, with Happiest Minds set to report its best performance since IPO in absolute terms. The numbers validate the strategic transformation initiated in 2024—acquisitions integrated, GenAI capabilities commercialized, industry verticals operationalized.

Executive Vice Chairman Joseph Anantharaju highlighted the company's "continued ability to execute and deliver high-quality digital capabilities," noting that Happiest Minds accelerated its net new growth opportunities while increasing the number of large customers during the quarter. This expansion of the customer base addresses a key concern about concentration risk that had worried investors.

The deal wins reveal the breadth of digital transformation engagements. For a global technology & service major, Happiest Minds is partnering to implement core banking technology to streamline operations for the mortgage division of a large multinational banking and financial services company. For a US logistics tech provider, Happiest Minds is driving their digital transformation agenda and building intelligent conversational dashboards using Gen AI.

The Board's recommendation of a final dividend of ₹3.5 per equity share for FY25 signals confidence in cash generation despite aggressive growth investments. This follows the FY24 total dividend of ₹5.75 per share, demonstrating commitment to returning value to shareholders while funding expansion.

Market sentiment remains mixed despite operational excellence. The market cap of ₹8,649 crores represents a decline of 30.4% over one year, creating a divergence between business performance and stock valuation that often indicates either market skepticism about sustainability or an opportunity for value investors.

The industry recognition continues to accumulate. Happiest Minds was awarded Best DevOps Framework for Scalability and Security at the 6th Edition India DevOps Show 2025, ranked 2nd in "IT Services" category at the ESC Export Excellence Awards 2025, and recognized among 'Inspiring Firms in AI & Analytics' at the 3AI ACME Awards. These accolades provide third-party validation of technical capabilities crucial for winning enterprise deals.

Analyst coverage expanded with Happiest Minds achieving 'Product Challenger' status in ISG Provider Lens Study for Digital Engineering Services, 'Major Contender' in Everest Industry 4.0 PEAK Matrix 2025 and Everest Data and AI Services for Mid-market Enterprises PEAK Matrix 2025, and 'Innovator and Major Player' in NelsonHall's Transforming Core Banking Services NEAT Report. This breadth of coverage across multiple research firms enhances visibility with enterprise buyers who rely on analyst recommendations.

The integration of recent acquisitions progresses smoothly. NCLT Bengaluru approved dispensation for meetings under composite scheme between PureSoftware and Happiest Minds in August 2024, clearing regulatory hurdles for full integration. PureSoftware won two IBSi Digital Banking Awards for Arttha's digital lending and wallet innovation, demonstrating that acquired assets continue winning market recognition.

GenAI solutions are moving from pilots to production, with Happiest Minds building replicable GenAI solutions for a prominent credit union service organization to help with employee training on performance management and customer support, and for a South East Asian Bottling company, building GenAI solutions that allow employees to converse in both local language and English against Enterprise knowledge.

Looking ahead, Chairman Ashok Soota emphasized the company's strategic initiatives have them "well-positioned for strong double-digit organic growth in FY26 and beyond," while noting that despite economists projecting a slowdown in some markets, the company maintains "healthy pipelines of demand" with no recession-driven slowdown visible.

XII. Links & Resources

Company Resources: - Investor Relations: https://www.happiestminds.com/investors/ - Annual Reports: https://www.happiestminds.com/digital-integrated-annual-report-2023-2024/ - Press Releases: https://www.happiestminds.com/news-and-events/press-releases/ - NSE Listing: https://www.nseindia.com/get-quotes/equity?symbol=HAPPSTMNDS

Industry Analysis & Reports: - ISG Provider Lens Digital Engineering Services Studies - Everest Group PEAK Matrix Reports (Cybersecurity, Industry 4.0, Data & AI) - NelsonHall Transforming Core Banking Services NEAT Report - Zinnov Zones Ratings for Digital Engineering Services - AIM Research PeMa Quadrant for MLOps Service Providers

Founder Interviews & Content: - Ashok Soota's autobiography "Entrepreneurial Roller Coaster" - Various leadership talks at CII, NASSCOM events - Earnings call transcripts (quarterly on investor relations page)

Competitive Intelligence: - Mid-tier IT services comparisons (Persistent Systems, Coforge, L&T Infotech) - Digital transformation market reports (Gartner, IDC, Forrester) - Indian IT services industry analysis (NASSCOM reports)

Books & Long-form Articles: - "The MindTree Story" - insights into Soota's first venture - NASSCOM's "Digital Transformation in India" annual reports - Case studies from IIM Bangalore on Indian IT entrepreneurship

Healthcare & Social Ventures: - Happiest Health platform: Focus on health and wellness content - SKAN Research: Medical research on aging and neurological disorders - Corporate social responsibility initiatives and impact reports

Epilogue: The Happiness Dividend

As we close this deep dive into Happiest Minds Technologies, it's worth stepping back to consider what this company represents in the broader arc of Indian technology. This isn't just another IT services firm that successfully went public—it's a meditation on second acts, strategic focus, and the audacious belief that culture can be a competitive advantage in an industry often reduced to cost arbitrage and utilization rates.

The numbers tell one story: from zero to ₹2,000+ crores in revenue in just over a decade, successful IPO at 151x oversubscription, strategic acquisitions integrated, GenAI capabilities built, consistent profitability maintained. By any conventional measure, Happiest Minds has succeeded in carving out a profitable niche in the hypercompetitive IT services landscape.

But the more interesting story lies in what Happiest Minds chose not to be. In an industry where scale is worshipped and companies measure success by headcount, this company deliberately stayed focused. No mainframe modernization practice. No COBOL programmers. No pursuit of billion-dollar outsourcing deals that would require armies of people but generate commodity margins. Every decision—from the clients pursued to the capabilities built—reflected a coherent strategy of digital specialization over diversification.

The cultural experiment deserves particular attention. When Ashok Soota appointed a "Happiness Evangelist" in 2011, the industry snickered. A decade later, with the Great Resignation reshaping workforce dynamics globally, the focus on employee happiness looks prescient. The SMILES values weren't just feel-good corporate speak—they were a retention strategy that directly impacted margins through lower attrition and higher productivity.

The acquisitions of PureSoftware and Aureus in 2024 marked an inflection point. These weren't desperate moves by a struggling company but strategic acceleration by a profitable enterprise. The ability to identify, acquire, and integrate complementary businesses while maintaining cultural coherence demonstrates institutional capability beyond what the company's age would suggest.

Yet challenges remain substantial. The 30% stock price decline despite strong operational performance suggests market skepticism about something—perhaps the sustainability of growth rates, the competitive dynamics as larger players complete their digital transformations, or simply the broader rotation away from mid-cap IT stocks. The concentration in US markets (84% of revenue) creates vulnerability to policy changes, economic cycles, and currency fluctuations that could quickly impact growth trajectories.

The founder transition looms as perhaps the biggest question mark. At 81, Ashok Soota remains the spiritual core of Happiest Minds. While Joseph Anantharaju's elevation to Executive Vice Chairman signals succession planning, the history of founder transitions in Indian IT is mixed at best. The company that built its identity around one man's vision must prove it can thrive beyond his active involvement.

Looking forward, Happiest Minds faces a fascinating set of strategic choices. Does it continue as a specialized digital services player, content with sustainable growth and premium margins? Does it use its public currency to make larger acquisitions, potentially doubling or tripling in size but risking cultural dilution? Does it double down on product development, using the Arttha platform as a template for building IP-driven revenue streams?

The GenAI revolution adds another dimension of both opportunity and risk. Early mover advantage in GenAI services could position Happiest Minds as the go-to partner for enterprises navigating this transformation. But GenAI also threatens to automate many tasks currently performed by IT services companies, potentially disrupting the entire industry's economics. The company betting on emerging technologies must now bet on which technologies will emerge victorious.

The broader lesson from the Happiest Minds story is about the power of strategic clarity in building differentiated businesses. In a world of infinite options, the companies that thrive are often those that make clear choices about what they will and won't do. Happiest Minds chose digital over legacy, culture over commodity, focus over diversification. These choices created a company that, while smaller than the IT giants, generates superior margins and growth rates.

For investors evaluating Happiest Minds, the calculus isn't simple. This is simultaneously a growth story (25%+ revenue growth), a value story (profitable with dividends), and a transformation story (GenAI and platform investments). The company trades at multiples that reflect neither pure growth nor deep value, existing in the uncomfortable middle ground that often represents opportunity or trap, depending on execution.

The ultimate test will be whether Happiest Minds can maintain its differentiation as the industry evolves. Can a company built on happiness maintain that culture at scale? Can digital specialization remain valuable as digital becomes table stakes? Can a mid-tier player continue winning against both nimble startups and resourceful giants? The answers will determine whether Happiest Minds becomes a case study in sustainable differentiation or another reminder that in technology, today's advantages are tomorrow's commodities.

What's certain is that Happiest Minds has already achieved something remarkable: proving that in Indian IT's third decade, there's still room for new stories, new models, and new definitions of success. The company that started with happiness as its organizing principle has delivered substantial returns to shareholders, meaningful careers to employees, and digital transformation to clients. In an industry often criticized for its mechanistic approach to human capital, that itself is a form of disruption worth celebrating.

As this episode concludes, we're left with a profound question that extends beyond Happiest Minds to the entire technology services industry: In a world where AI increasingly handles technical tasks, what's the sustainable value that human-centered IT services companies provide? Happiest Minds' answer—deep domain expertise, cultural alignment, and yes, happiness—might just point the way forward for an industry searching for its next act. Whether that thesis proves correct will determine not just one company's fate but potentially the future trajectory of Indian IT's continued evolution.

The story of Happiest Minds is far from over. But what's been written so far suggests that sometimes the best time to start isn't when you're young and naive—it's when you're experienced enough to know exactly which rules are worth breaking. In building a company around happiness in an industry obsessed with utilization rates, Ashok Soota and his team haven't just built a successful business. They've offered a different vision of what Indian technology companies can become. And in that vision, perhaps, lies the seed of the industry's next transformation.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube