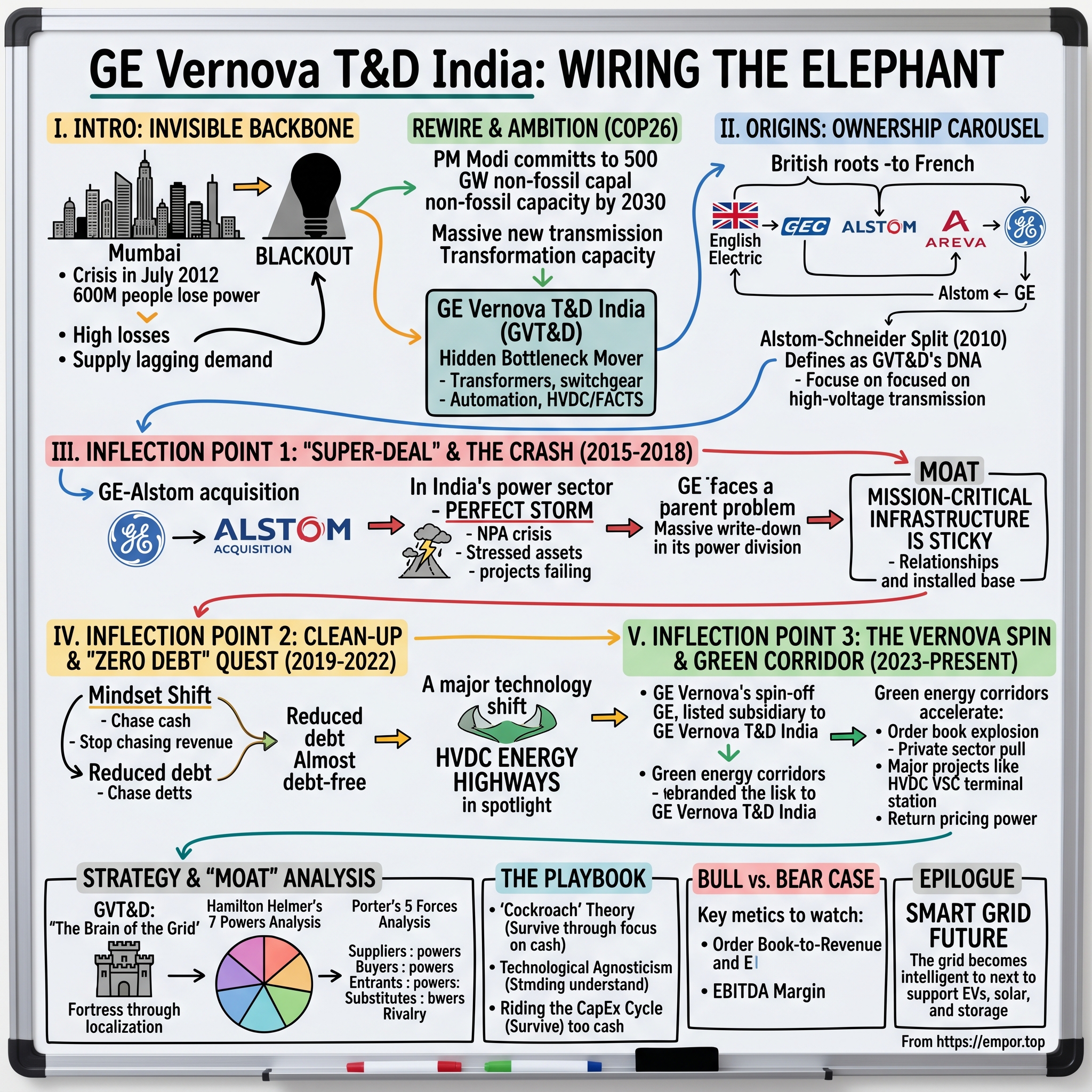

GE Vernova T&D India: Wiring the Elephant

I. Introduction: The Invisible Backbone

Picture Mumbai at 1:33 a.m. on July 30, 2012. Up north, a cascade of circuit breakers trips. Within minutes, the failure spreads—like a digital contagion—across the grid. More than 600 million people across 22 states lose power. Trains grind to a halt. The Delhi Metro suspends service on all six lines, evacuating passengers from cars stopped mid-journey. In one night, India suffers the largest blackout in history, and the lesson is painfully clear: the grid isn’t just infrastructure. It’s the operating system of a modern country.

That outage exposed a brutal truth. The world’s largest democracy was running on a network that, in too many places, was one bad day away from collapse. Around that period, an estimated 27% of electricity was lost in transmission or stolen. Peak supply routinely lagged demand by roughly 9%. For many households and businesses, outages weren’t rare events—they were a daily fact of life, sometimes stretching to 10 hours.

Now fast-forward. India isn’t just fixing the old grid—it’s trying to build the next one, at a scale no one has attempted before. At COP26, Prime Minister Modi committed India to 500 GW of installed capacity from non-fossil sources by 2030, a huge step up from the earlier 175 GW renewables goal for 2022. The Central Electricity Authority then mapped out what that ambition requires on the ground: tens of thousands of circuit-kilometers of new transmission lines and massive additions of transformation capacity, with a projected price tag running into lakhs of crores.

And sitting quietly in the middle of this national project is a company most investors barely recognize: GE Vernova T&D India. Formerly GE T&D India Limited, it’s the listed Indian arm of GE Vernova’s Grid Solutions business, with more than a century of operating history in the country. Its products and projects span the unglamorous but essential guts of the grid: power transformers, circuit breakers, gas-insulated switchgear, instrument transformers, substation automation, digital software, turnkey substations, FACTS and HVDC systems, plus long-tail maintenance and support.

This story is about survival—and timing. A company passed from owner to owner—English Electric, GEC, Alstom, Areva, and now GE Vernova—while riding India’s boom-bust power cycle. It lived through the wreckage of the 2015–2018 NPA crisis and came out not just standing, but positioned for the upside of the green build-out. Because if India is serious about renewable power, the real bottleneck isn’t generating electrons. It’s moving them.

II. Origins: The Ownership Carousel

Long before the GE Vernova badge showed up on factory gates, these plants belonged to Britain’s industrial empire. The company began life as The English Electric Company of India, incorporated on March 13, 1957. Decades later, the name changed to ALSTOM T&D India Limited in April 1993, and then to ALSTOM Limited on July 24, 1998.

But this wasn’t just stationery being updated. Each new owner brought fresh technology, different priorities, and new capital. They also brought the downside of being a faraway subsidiary: disruption, uncertainty, and the constant risk that India would be treated as “non-core” when the parent had bigger fires to fight elsewhere.

The British Foundation (1957-1993)

English Electric set up manufacturing in the Pallavaram and Padappai areas of Chennai, building transformer capacity that would become foundational as India pushed electrification and industrial growth. In 1982–83, the company began manufacturing solid-state generators and transformers, vacuum switches, and electric motors through collaborations with GEC International Controls (UK) and Electroimplex (Bulgaria). In 1984, it signed collaboration agreements with GEC Power Transformers (UK) and Raydne (UK).

The pattern was set early: global know-how flowing into local factories, and local factories quietly becoming indispensable.

The French Nuclear Connection: Areva Era (2004-2010)

On September 23, 2005, ALSTOM Limited became Areva T&D India Limited. The shift mattered. Areva was France’s champion in nuclear and grid technology, and the Indian business was now plugged into a pipeline of ultra-high-voltage expertise—exactly what a country of India’s size needed to move power over long distances.

By then, the company was already doing serious high-voltage work. It successfully commissioned a 315 MVA 400 kV transformer in August 2001. In 2002–03, it tested a new-generation 145 kV circuit breaker as per IEC standards, and commissioned a 420 kV circuit breaker for NTPC’s Talcher Super Thermal Power Plant. This wasn’t “supporting infrastructure.” This was the backbone being poured into place.

The Alstom-Schneider Split (2010): DNA Defined

Then came the moment that most clearly shaped what the company would become. In 2010, after regulatory approvals, Alstom and Schneider Electric closed their joint acquisition of Areva T&D, following a consortium agreement signed in November 2009. The price paid for Areva T&D’s shares amounted to EUR 2.29 billion.

The agreement split the business in a way that effectively defined the company’s future. Transmission—about two thirds of the total—went to Alstom. Distribution—about one third—went to Schneider Electric. Translation: Alstom took the heavy, high-voltage world of big substations, 765 kV transformers, and HVDC systems; Schneider took the medium-voltage distribution side.

In India, 2.9 million shares were acquired by Alstom and Schneider Electric in the tender offer, representing 1.2% of the company’s share capital. Post tender offer, Schneider Electric and Alstom held 73.4% of the share capital of Areva T&D India Ltd.

From there, the company’s identity hardened around transmission: the high-voltage, system-critical equipment and projects that connect power plants to cities, solar parks to industrial centers, and regions of a vast country into a single functioning grid.

And that’s the hidden advantage of the ownership carousel: while letterheads changed from London to Paris, the institutional knowledge stayed put in Chennai—along with the relationships, the factories, and the hard-earned credibility that comes from keeping the lights on.

III. Inflection Point 1: The "Super-Deal" and the Crash (2015-2018)

In GE’s executive suites, CEO Jeff Immelt was placing a once-in-a-generation bet—one that would reshape GE, and drag this small, listed Indian grid company along with it.

GE completed the acquisition of Alstom’s power and grid businesses in November 2015. It was GE’s largest-ever industrial deal. The agreement itself had been struck in 2014, with a headline price of €12.35 billion. After the realities of joint ventures, remedies, closing adjustments, net cash, and currency effects, the effective purchase price landed at about €9.7 billion, roughly $10.6 billion.

The closing required regulatory approvals across more than 20 jurisdictions, including the EU, the U.S., China, India, Japan, and Brazil. When it finally cleared, Immelt framed it as a milestone in GE’s pivot:

"The completion of the Alstom power and grid acquisition is another significant step in GE's transformation," said Jeff Immelt, chairman and CEO of GE. "The complementary technology, global capability, installed base, and talent of Alstom will further our core industrial growth."

On the ground in India, the implications were immediate and very practical. Another parent. Another logo. Another name. On August 2, 2016, the company became GE T&D India Limited.

And the timing could not have been worse.

The Perfect Storm Hits India

Just as GE took over, India’s power sector slid into its ugliest downturn in a decade. The boom years of 2004–2009 had been fueled by easy lending to infrastructure. When the cycle turned, the banking system was left holding the bag.

Raghuram Rajan became RBI Governor in 2013 and pushed the system to stop pretending. Suspecting banks were “ever-greening” bad loans by endlessly restructuring them, he ordered an Asset Quality Review in 2015–16. The result was a sudden, painful recognition of what had been building for years: a wave of NPAs and the provisions to match, hammering bank capital and freezing new lending.

By June 2017, NPAs in the electricity sector were reported at Rs 37,941 crore. A committee examined 34 thermal power projects that had become stressed assets. Private and corporate power generators alone owed loans of more than Rs 1.74 lakh crore that were nearing NPA classification.

For T&D equipment suppliers, this wasn’t an abstract banking statistic. It was the sound of projects dying mid-sentence.

Plants were built without power purchase agreements. Transmission lines were commissioned with little or no power to evacuate. State electricity boards—chronically loss-making even in good times—slowed payments further, or stopped altogether. The investment cycle didn’t just cool; it seized.

Gross NPAs across banks rose from 2.3% of total loans in 2008 to 11.5% in 2017. For GE T&D India, that translated into customers who couldn’t pay, orders that slipped or got cancelled, and a balance sheet suddenly carrying far more stress than a capital goods business can comfortably absorb.

The GE Parent Problem

As brutal as India’s downturn was, it landed at the exact moment GE itself started wobbling. The Alstom acquisition—sold as “transformational”—began to look like an overreach.

GE recorded $17.3 billion of goodwill tied to the deal, reflecting Alstom’s negative book value at acquisition and the purchase premium. Then, in October 2018, GE took a massive $23 billion write-down in its power division, largely attributed to the Alstom purchase.

It was a gut punch: a write-down bigger than the purchase price itself. GE’s stock cratered. Inside the conglomerate, priorities narrowed to survival. And the Indian subsidiary—already dealing with a collapsing domestic cycle—was now tied to a parent in crisis, with less attention, less appetite for risk, and less room for error.

The market treated the Indian stock accordingly. From its earlier highs, shares fell hard as investors stampeded away from what looked like the worst of both worlds: a cyclical industrial business in a broken sector, attached to a parent that suddenly looked anything but invincible. The narrative curdled into something like “old world industrial junk.”

For a while, it wasn’t an unfair description of how it was trading. But it missed what mattered.

Because this period also revealed what doesn’t show up in a glossy acquisition deck: mission-critical infrastructure is sticky. Even when financing froze and customers delayed payments, the installed base still needed service. Utilities couldn’t simply swap out a vendor the way a company switches cloud providers. Decades-long relationships with PGCIL and state utilities mattered precisely because they were built in the unglamorous trenches—commissioning, maintaining, and troubleshooting complex, high-voltage systems like 765 kV substations.

The moat was real. It just wasn’t visible from the stock chart.

IV. Inflection Point 2: The Clean-Up and the "Zero Debt" Quest (2019-2022)

Inside the Chennai offices, the turnaround didn’t arrive with a press release. It arrived with a mindset shift. Management made a decision that sounds obvious in hindsight, but almost nobody follows in the middle of a downturn: stop chasing revenue, and start chasing cash.

The rule was blunt. If a state electricity board wanted to place an order but couldn’t demonstrate it would pay on time, the company would rather walk away. In a capital-goods industry where vendors often say yes to anything just to keep factories busy, that kind of refusal feels like sacrilege. But it was the right kind of discipline for a cycle that had turned toxic.

The results showed up where they always do in this business: in the balance sheet and in working capital. Debt came down sharply, and the company moved to being almost debt-free. Collection efficiency improved too—debtor days reduced from 165 to 125—evidence that this wasn’t just rhetoric. It was execution, over multiple years, with real trade-offs.

At the same time, the business got pickier about what it would do. It rationalized costs, exited contracts that weren’t worth the stress, and focused on the parts of the market where it had a genuine edge—ultra-high-voltage equipment, HVDC systems, and turnkey substation solutions where technology leadership could actually translate into better economics.

The Technology Shift: Enter HVDC

While the financial clean-up was underway, the product story was changing too. High Voltage Direct Current—HVDC—wasn’t just another line item in the brochure. It was a capability that made the company more relevant to the next decade than it had been to the last.

Here’s the intuition. If conventional high-voltage AC transmission is like moving information over old copper lines—fine for shorter distances but inefficient as the haul gets longer—then HVDC is closer to fiber optics for electricity. It’s an efficient, cost-effective way to move huge amounts of power over very long distances to where it’s actually consumed. It also matters politically and practically because it needs less land: 800 kV HVDC requires about four times less right-of-way than comparable HVAC transmission. And for very long schemes—beyond roughly 700 km—HVDC can be more economical than HVAC.

India is basically the perfect use case. Some of the best solar resources sit in places like Rajasthan and Gujarat. Many of the major load centers are far away, including industrial hubs in the west and south. Those distances can run beyond a thousand kilometers. Moving power that far without the right technology means accepting bigger losses and bigger headaches. With HVDC, you can build true “energy highways,” capable of moving multi-gigawatt flows across the country with minimal degradation.

The foundation was already there. Around the time of the Alstom acquisition, the company had delivered India’s first 800 kV HVDC power transformer for the Champa-Kurukshetra project, which used 800 kV HVDC technology to transmit 3,000 MW from Champa in central India to Kurukshetra in northern India.

That capability became more valuable as India’s renewable push picked up speed. Solar generation peaks around midday, often far from demand. Evening demand peaks when people get home. Bridging that mismatch—across both geography and time—meant the grid had to evolve fast. HVDC was one of the key enablers.

By 2019–2022, the transformation was largely internal: from a stressed, leveraged business living with bad-cycle customers to a leaner operation with far tighter cash discipline and more future-proof technology. The stock price didn’t necessarily advertise the shift. But underneath, the company had changed shape.

V. Inflection Point 3: The Vernova Spin and the Green Corridor (2023-Present)

On November 9, 2021, GE announced it would split into three publicly traded companies. The names telegraphed the new reality: GE HealthCare, GE Aerospace, and GE Vernova. GE HealthCare went first, spinning off on January 4, 2023. GE Vernova followed.

On April 2, 2024, GE Vernova (NYSE: GEV) completed its separation from GE and began trading as an independent company on the New York Stock Exchange under the ticker “GEV.”

GE explained the brand this way:

"GE Vernova's mission is embedded in its name—it retains its legacy, 'GE,' as an enduring and hard-earned badge of quality and ingenuity. 'Ver' / 'verde' signal Earth's verdant and lush ecosystems. 'Nova,' from the Latin 'novus,' nods to a new, innovative era of lower carbon energy."

For the Indian business, the spin changed what it meant to be “a subsidiary.” This wasn’t just a new sign on the gate—it was a new parent with a single job: the energy transition. Shareholders approved the name change from GE T&D India Limited to GE Vernova T&D India Limited, effective October 16, 2024. The grid business was no longer sitting inside a conglomerate whose gravitational center was jet engines. It was now aligned with a pure-play electrification and decarbonization platform.

The Macro Tailwinds Arrive

As the corporate structure snapped into focus, India’s grid build-out accelerated.

The diagnosis had been made years earlier. In 2012, a Power Grid Corporation of India Limited (PGCIL) study found that evacuation and transmission infrastructure around many high-potential renewable sites was simply not ready. PGCIL submitted the Green Energy Corridor report in FY 2012–13, implementation began in 2015, and the Inter-State Transmission System (ISTS) Green Energy Corridor project—covering about 3,200 circuit-kilometers of lines and around 17,000 MVA of substation capacity—was commissioned in March 2020.

Then came the next wave. The Cabinet Committee on Economic Affairs approved Green Energy Corridor Phase II for 13 GW renewable energy projects in Ladakh, targeted for completion by FY 2029–30, with an estimated cost of Rs 20,773.70 crore and Central Financial Assistance at 40% of project cost.

All of this sat inside the bigger rewire: India’s Transmission Plan for 500 GW, a roughly Rs 2.4 lakh crore program to connect renewable-rich states to the country’s major demand centers.

And that’s when the “grid problem” flipped. In 2012, the question was capacity: Do we have enough power? By 2024, it was logistics: How do you move solar power generated at noon to cities that need it at night?

The Order Book Explosion

You could see the shift in the numbers before you could feel it in the stock.

GE Vernova T&D India reported a sharp acceleration in demand, with order inflows up 75% year-on-year in the first three quarters of FY25. New order inflow in 9MFY25 was Rs 77,871 million, up from Rs 44,563 million in the same period of FY24.

By December 31, 2024, the outstanding order book stood at Rs 107,809 million. Notably, it skewed private: about 68% of the backlog came from private-sector customers. That matters, because it signals pull from real commercial build-outs—not just policy push.

Big-ticket projects were back too. On December 20, 2025, the company secured an order from AESL Projects Limited to design and establish a 2,500 MW, ± 500 kV HVDC VSC terminal station to evacuate renewable power from Khavda to South Olpad. Nuvama estimated the deal value at around Rs 8,000–10,000 crores—material relative to the company’s order book and its estimated FY26 revenue.

Financials followed. For the year ending March 31, 2025, GE Vernova T&D India generated revenue of INR 4,350 crore. The company also reported strong profitability growth over this period, with EBITDA rising sharply. In 2024, revenue was 42.92 billion rupees, up 35.49% year-on-year, and earnings rose to 6.08 billion, up 236%.

Management leaned into the moment. The company communicated a FY25 revenue target of INR 5,500–6,000 crore, with overall margins expected to remain above 20%, and announced plans to invest INR 806 crore to expand manufacturing capacity across its facilities.

The global parent put more chips on the table as well. GE Vernova announced plans to invest approximately USD $16 million in India to expand its electrification manufacturing and engineering footprint, including a new manufacturing line at its Chennai facility and a new facility in Noida.

After years where suppliers ate risk just to keep plants running, pricing power came roaring back. When the entire country needs transformers, switchgear, and HVDC gear at the same time—and only a handful of qualified players can actually deliver—the economics stop being friendly to the buyer.

VI. Strategy and the "Moat" Analysis

To understand what GVT&D actually sells, you have to look past the metal.

The Brain of the Grid

Yes, the company makes the obvious stuff: power transformers, circuit breakers, gas-insulated switchgear, instrument transformers, and the rest of the substation hardware that physically moves electricity from one place to another. It also delivers turnkey substation engineering and construction, Flexible AC Transmission Systems (FACTS), High Voltage DC (HVDC) projects, and long-tail maintenance support.

But the higher-level story is that GVT&D doesn’t just ship equipment. It helps run the system.

The transformers are the visible part—monumental machines that can weigh hundreds of tons. The less visible part is what turns all that hardware into a controllable network: substation automation, digital software, and the control systems that let grid operators see what’s happening and respond fast.

When PGCIL has to balance power flows across regional grids—reacting in near real time to fluctuations in generation and demand—it depends on SCADA (Supervisory Control and Data Acquisition) systems and load dispatch centers. GVT&D provides these systems. And that creates a different kind of stickiness than hardware alone. Switching isn’t hard because someone can’t build a transformer. Switching is hard because the integration, the commissioning, and the operational know-how become deeply embedded in how the grid is actually run.

Localization as Fortress

A second advantage is far more practical: the company builds in India, at scale.

With five manufacturing sites, GE Vernova T&D India is positioned to meet rising demand for grid equipment and services without waiting on overseas capacity. It manufactures 765 kV class reactors at its Vadodara plant, and has supplied more than 600 transformers and reactors of 765 kV class from that facility to customers in India and abroad.

That footprint buys the company three things that matter in a cycle like this. First, speed—delivery times that are often hard for imports to match. Second, access—eligibility for “Make in India” preferences that government-linked procurement increasingly leans on. And third, resilience—less exposure to trade disruptions and geopolitical flare-ups that can suddenly turn cross-border sourcing into a problem. After 2020, as scrutiny of Chinese imports increased, local manufacturers stood to benefit.

"The notification, once implemented, is expected to support the domestic T&D cycle, curb low-cost dumping by Chinese suppliers, and reduce India's high import dependence, thereby structurally benefiting domestic T&D manufacturers such as CG Power, Siemens Energy, Hitachi Energy, GE Vernova T&D India."

The Competitive Landscape

All of this plays out in a market that’s not crowded—especially at the very top end of voltage and complexity.

India’s high-voltage T&D equipment space has only a handful of companies with the engineering depth, qualification track record, and technology access to execute at the scale utilities require. Much of the cutting-edge capability sits with global majors like Hitachi Energy, Siemens Energy, and GE Vernova, and that reality creates a natural barrier for would-be entrants.

Hitachi Energy India, for example, competes across utilities, renewables, industry, transportation, and data centers against players like GE Vernova, Siemens India, and CG Power. Its revenue grew to Rs 6,442 crore in FY25 from Rs 5,247 crore in FY24, and its order backlog climbed to around Rs 19,246 crore—evidence of just how hard demand has hit the system.

"Siemens is among the few players with a presence in high-voltage lines up to 765kV and is hence expected to benefit from planned investments. We believe that Siemens had adopted a selective stance for HVDC projects."

Put it together and you get something close to an oligopoly—one where the defenses aren’t branding or distribution. They’re time, trust, and qualification. You don’t simply decide to “start up” a 765 kV transformer business. Utilities take years to qualify suppliers, the technology and process expertise are hard-won, and the capital requirements are heavy. In a market where the grid must be built now—not later—those barriers tilt the economics toward the incumbents.

VII. Frameworks: Powers and Forces

Hamilton Helmer's 7 Powers Analysis

Switching Costs (High): When GVT&D installs a 765 kV substation and ties it into automation and control systems, it doesn’t just deliver hardware—it becomes part of how the customer runs the grid. Much of this equipment is built to last for decades. The software is integrated into day-to-day operations. The service work depends on deep familiarity with the installed base. Swapping vendors isn’t like re-tendering a commodity contract; it means years of planning, large capital spend, fresh commissioning risk, and the very real possibility of destabilizing a mission-critical network. In grid infrastructure, nobody “switches” on a whim.

Cornered Resource: There’s also a talent moat that’s easy to miss from the outside: engineers in India who understand both the legacy Alstom-era technology still embedded across the network and the newer GE systems layered on top. That knowledge is earned over years of commissioning, maintenance, and troubleshooting in the real world—specific to India’s grid topology, utility procurement realities, and on-site constraints. Competitors can hire individuals, but they can’t replicate the institutional memory overnight.

Counter-Positioning: The 2019–2022 cleanup revealed a subtle but powerful advantage: GVT&D was willing to walk away from orders that didn’t pay. In a downturn, many suppliers keep factories busy by accepting weak terms and hoping for the best. GVT&D chose the opposite—prioritizing cash collection and balance-sheet resilience. That discipline is a form of counter-positioning against rivals still incentivized to chase top-line growth at any cost.

Scale Economies: With five manufacturing sites serving India and export demand, the company benefits from scale in procurement, production, testing, and service. In a business where qualification standards are strict and delivery reliability matters, scale isn’t just about cost—it’s about throughput and execution capacity that a new entrant can’t easily match.

Porter's 5 Forces Analysis

Supplier Power (Moderate-High): This is a specialized supply chain. Transformers and high-voltage systems depend on inputs like CRGO steel, high-purity copper, bushings, and control electronics—categories where global supply can be tight and vendor concentration is real. GVT&D’s scale and long-term relationships help, but supplier leverage doesn’t disappear when the whole world is trying to build grids at the same time.

Buyer Power (Nuanced): On paper, buyers should dominate: PGCIL, state utilities, and large private developers are massive and concentrated. In normal times, that translates into tough pricing and tough payment terms. But the current cycle isn’t normal. Demand for grid equipment is rising sharply, qualified suppliers are limited, and delivery slots are the real scarce resource. Industry estimates point to a step-change in annual ordering driven by HVDC and exports versus the pre-Covid run-rate. In that kind of shortage economy, bargaining power shifts toward the suppliers who can actually build, test, and deliver.

Threat of New Entrants (Very Low): The National Electricity Plan points to a major build-up of HVDC transmission in the FY28–FY32 period, including significant additions of HVDC line length and transfer capacity. The headline takeaway isn’t just growth—it’s that the clock is ticking. You can’t wake up, decide to enter HVDC and 765 kV infrastructure, and be relevant in time. Qualification takes years, technology access matters, and the capital and engineering requirements are prohibitive.

Threat of Substitutes (Low): There’s no substitute for a functioning grid. Rooftop solar and distributed generation may reduce some incremental demand for centralized power, but they also make balancing and stability harder—raising the need for smarter substations, automation, and grid control. Battery storage helps, but it complements transmission and distribution; it doesn’t replace them.

Competitive Rivalry (Moderate): Rivalry among Hitachi Energy, Siemens Energy, and GE Vernova is real, but it’s not a race to the bottom. When demand exceeds supply and backlogs stretch for years, the market doesn’t reward reckless price cuts. The fight shifts to capability, delivery reliability, qualification history, and who can take on the hardest projects without blowing up timelines.

VIII. The Playbook: Lessons in Corporate Survival

The "Cockroach" Theory

GVT&D’s survival through the 2015–2018 mess is about as close as you get to a corporate cockroach story: the world around it can burn, but it finds a way to keep moving.

GE, the parent, was unraveling—taking a $23 billion write-down in power and cycling through leadership upheaval. India’s power market, meanwhile, was choking on the NPA crisis, with projects stalled and customers stretching payments. In that environment, GVT&D narrowed its focus to the one thing it could actually control: cash.

The lesson is brutally simple and a little heretical in capital goods: cash flow beats revenue growth. Management made the deliberate choice to shrink in order to survive. They walked away from orders that came with bad payment behavior. They exited work that wasn’t worth the risk. They squeezed working capital. The payoff wasn’t a glamorous growth story—it was a company that came out leaner, nearly debt-free, and ready for the cycle to turn.

Technological Agnosticism

Another reason it made it through: it learned how to belong to whoever owned it, without losing itself.

Under Areva, it absorbed French grid expertise. Under GE, it took on a different kind of operational discipline. And through all of it, the core job didn’t change: solve the Indian grid’s problems, in Indian conditions, with Indian customers. The Chennai factories kept building. Local teams kept delivering. Relationships with PGCIL and state utilities survived yet another logo change.

That kind of adaptability is rare. Many subsidiaries become completely dependent on the parent—and wobble when the parent does. Others go so “local” that they lose access to global technology and standards. GVT&D managed the balancing act: it kept pulling in capabilities from each owner while staying operationally grounded in India.

Riding the CapEx Cycle

The final lesson is the oldest one in heavy industry: this is a cycle business, and cycles mess with people’s judgment.

When factories are idle and order books are thin, the market tends to declare the whole enterprise “broken.” That’s what happened in the 2017–2020 period, when the NPA crisis dominated the narrative and the sector looked uninvestable. But the grid doesn’t stop needing maintenance, upgrades, and expansion. And when the cycle turns, capacity and qualification suddenly become scarce—and valuable.

As the order environment improved, the market rerated the story hard. The stock rose sharply over the following years, approaching its 52-week high. The investing takeaway isn’t the exact magnitude of the move—it’s the pattern: learn to separate structural decay (which kills businesses) from cyclical pain (which creates entry points). For GVT&D, the problems were cyclical, even when they looked existential.

IX. Bull vs. Bear

The Bull Case

India’s energy transition is still in the early innings. As of February 28, 2025, India’s installed solar capacity was about 102.57 GW. To get to the country’s 500 GW non-fossil target, solar will likely need to do a disproportionate amount of the heavy lifting—nearly 300 GW by some estimates. And that doesn’t just mean more panels. It means a much bigger, smarter grid to absorb, stabilize, and move all that power.

Then there’s a newer, very modern load showing up at the edge of the grid: data centers. India’s data center capacity is projected to jump from about 1.4 gigawatts to 9 GW by 2030, and could consume roughly 3% of the country’s electricity. AI workloads don’t tolerate “mostly reliable.” They need clean, stable power—exactly the kind of demand that forces upgrades in transmission, substations, and grid automation.

There’s also an export angle. GE Vernova has framed its push as an “Asia for Asia” strategy: build and engineer locally to serve regional demand, while making the supply chain more resilient. If India becomes a meaningful manufacturing base for the broader Asia-Pacific region, GVT&D isn’t just riding India’s capex cycle—it’s tapping into a wider one.

And the domestic pipeline is not subtle. As of May 31, 2025, PGCIL’s transmission network stretched to roughly 180,239 circuit-kilometers of EHV lines, with 283 EHV AC and HVDC substations and transformation capacity of 564,961 MVA. PGCIL has already facilitated evacuation of more than 110 GW of non-fossil capacity. The takeaway isn’t any single figure—it’s that the build-out is real, underway, and structurally tied to national targets.

The Bear Case

Valuation: The stock has priced in near-perfection. After a roughly 2,780% gain over three years, expectations are sky-high. In that setup, even “fine” execution can disappoint. Delayed projects, margin slippage, or losing a few marquee orders can lead to sharp drawdowns.

Raw Material Risk: This is a copper-and-steel business wearing a software-and-electrons costume. Copper and aluminum price moves can compress margins fast if contracts aren’t well-structured or hedged. A spike in CRGO steel or copper prices would pressure profitability.

Parent Royalty: The parent-subsidiary relationship always carries an agency risk. GE Vernova monetized an incremental 8% ownership stake in GE Vernova T&D India Limited for about $0.6 billion of pre-tax proceeds. The stake sale itself may have been value-accretive, but it highlights the underlying question investors can’t ignore: how aggressively does the global parent choose to extract value over time, including through royalty fees for brand and technology?

Chinese Competition: Restrictions have helped domestic players, but policy can change. There have been reports that the Government may allow Chinese companies to bid for government contracts, particularly in infrastructure, power, and manufacturing. Neither the government nor any company has confirmed this, but the market has treated it as a risk worth watching.

Key Metrics to Watch

For investors tracking GVT&D’s performance, two indicators tend to matter more than everything else:

Order Book-to-Revenue Ratio: Currently above 2.0x, which implies strong revenue visibility. If it slides below 1.5x, that’s a meaningful warning sign on demand. If it stays elevated—above 2.5x—it suggests the cycle is still accelerating.

EBITDA Margin: With margins above 20%, the company is operating from a position of strength. A drop below 15% would imply either intensifying competition, unfavorable project mix, or raw material inflation that can’t be passed through.

X. Epilogue: The Smart Grid Future

The next chapter for GVT&D sits under a deceptively simple phrase: the “smart grid.” It’s the shift from merely transmitting electricity to actively managing it—because in a world of renewables, EVs, and storage, the grid can’t just be strong. It has to be intelligent.

GE Vernova has been orienting its India playbook around green and digital solutions that make the grid smarter, more resilient, and more environmentally friendly. In practice, that means preparing the system for electric vehicles—not just as a new class of demand, but potentially as flexible capacity through vehicle-to-grid concepts. It means orchestrating millions of rooftop solar systems that produce in the daytime and lean on the grid after sunset. It means integrating battery storage so power can be shifted across hours, smoothing the mismatch between when energy is generated and when people actually use it.

Zoom out and you can see why the parent matters. GE Vernova says its technologies touch roughly 30% of the world’s electricity generation. That kind of installed base and engineering depth gives it a credible shot at helping solve the “energy trilemma” that every country wrestles with: reliability, affordability, and sustainability—at the same time.

And that brings us back to the investing lens. GE Vernova T&D India is, in many ways, a pick-and-shovel business for India’s growth. If you believe India gets to a $5 trillion economy—and then keeps climbing—you have to believe the grid gets built out alongside it. Every factory, every data center, every EV charging station, every high-rise apartment depends on dependable power. And dependable power depends on the unglamorous infrastructure GVT&D designs, manufactures, installs, and maintains.

GE Vernova describes the segment it serves as a $265 billion industry that could grow to $435 billion by 2030, with electrification and decarbonization driving long-run demand and global generation capacity projected to more than double by 2040. Big numbers, yes—but the takeaway is simpler: the world is entering an era where building and upgrading grids becomes a central economic project, not a background expense.

The 2012 blackout that threw 600 million people into darkness was the alarm bell. The response—a multi-decade rewiring of India’s power system—is now playing out in real time. After surviving the ownership carousel, the NPA crash, and the GE meltdown, GVT&D enters this era in a rare position: battle-tested, deeply embedded, and operating in the exact part of the value chain that suddenly matters most.

For long-term investors, the question isn’t whether India’s grid keeps expanding. That’s about as durable a trend as you get. The real question is whether GVT&D can defend its edge—through raw material swings, competitive pressure, and the sheer execution grind of delivering an enormous order book. Its history argues it can.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube