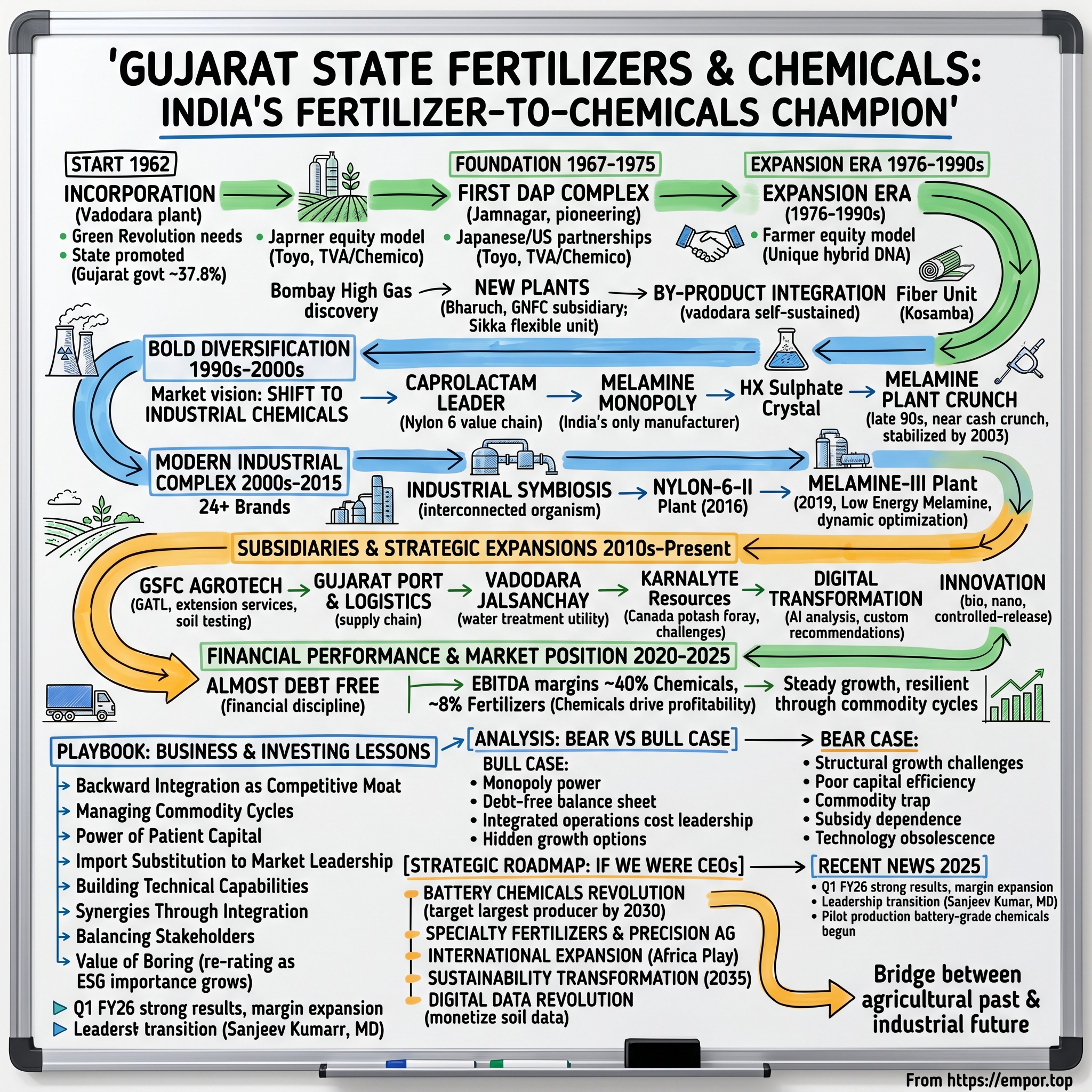

Gujarat State Fertilizers & Chemicals: The Story of India's Fertilizer-to-Chemicals Champion

I. Introduction & Episode Roadmap

Picture this: It's 1962, and a newly independent India faces a stark reality—300 million mouths to feed, depleting soil fertility, and a dangerous dependence on imported fertilizers that's draining precious foreign exchange. In the industrial corridors of Vadodara, along what would become the Ahmedabad-Vadodara Expressway, bulldozers break ground on what seems like just another state-sponsored fertilizer plant.

But Gujarat State Fertilizers & Chemicals would become something far more intriguing—India's only melamine manufacturer, its largest caprolactam producer, and a rare example of a public sector undertaking that successfully pivoted from commodities to specialty chemicals while maintaining profitability across six decades.

Today, with a market capitalization of ₹8,045 crore and annual revenues exceeding ₹9,500 crore, GSFC stands as a testament to patient industrial policy and strategic backward integration. How did a government-promoted fertilizer company, born from Gujarat's post-independence industrial ambitions, transform into a chemicals powerhouse that holds multiple monopolies in critical industrial inputs?

This is a story that spans India's Green Revolution, the discovery of Bombay High gas fields, the liberalization of the 1990s, and the modern push toward self-reliance in strategic materials. It's about how a company learned to dance between its social mandate of supporting farmers and its commercial ambitions in global chemical markets. Along the way, we'll explore the delicate art of managing commodity cycles, the power of vertical integration, and what happens when patient government capital meets industrial chemistry.

The narrative arc takes us from food security to import substitution, from basic fertilizers to complex polymers, from serving Gujarat's farmers to supplying global automotive giants. It's a uniquely Indian story of industrial evolution—one that offers surprising lessons for understanding state capitalism, chemical industry dynamics, and the often-misunderstood world of public sector enterprises.

II. Origins & Post-Independence Context

The year was 1962. Jawaharlal Nehru's vision of temples of modern India—steel plants, dams, and fertilizer complexes—was taking concrete form across the nation. In Gujarat, a state barely two years old after its separation from Bombay State, Chief Minister Balwantrai Mehta had his own industrial dreams. Unlike the heavy industry focus of states like Bihar and West Bengal, Gujarat would chart a different course—one that married agriculture with industry, farmers with factories.

The context was urgent. India's population had crossed 450 million, growing at 2.2% annually, while agricultural productivity remained stubbornly flat. The country was importing nearly 3 million tons of foodgrains annually under the humiliating PL-480 program, essentially living "ship to mouth" as critics called it. Norman Borlaug's high-yielding wheat varieties were just arriving in India, but they demanded something Indian soil desperately lacked—chemical fertilizers. Gujarat State Fertilizers & Chemicals Limited emerged from this crucible as a public sector company promoted by the Government of Gujarat, incorporated on February 15, 1962. But why Gujarat, and why fertilizers? The answer lay in a unique confluence of political will, agricultural desperation, and industrial vision.

Gujarat's first Chief Minister, Jivraj Mehta, and his successor Balwantrai Mehta understood something fundamental: unlike the coal-rich eastern states that could build steel plants, or the mineral-rich southern states pursuing mining, Gujarat's competitive advantage lay in its entrepreneurial culture, its long coastline for imports, and its vast agricultural hinterlands. The state needed an anchor industry that could serve both farmers and spawn downstream industries.

The location choice—Vadodara, strategically positioned on what would become the Ahmedabad-Vadodara Expressway—was no accident. This wasn't just about proximity to markets; it was about creating an industrial nucleus that could eventually support a chemical complex. The planners, many trained in the Soviet model of integrated industrial development, envisioned not just a fertilizer plant but a future chemical hub.

It was incorporated in 1962 and is promoted by the government of Gujarat, with an initial objective that seemed both simple and audacious: make Gujarat's farmers self-sufficient in fertilizers. The state government's stake would eventually stabilize at 37.8%, a controlling interest that provided stability while allowing for commercial flexibility.

What distinguished GSFC from other state fertilizer projects of that era was its mandate to think beyond immediate needs. While Sindri Fertilizers in Bihar or Fertilizer Corporation of India in other states focused purely on production volumes, GSFC's charter included a provision for "allied chemical products"—a seemingly minor clause that would prove transformative decades later.

The human element was equally crucial. The founding team included a mix of bureaucrats who understood government machinery, engineers trained in Western universities who brought technical expertise, and crucially, Gujarati businessmen who insisted on commercial viability even within a PSU framework. This hybrid DNA—part socialist planning, part capitalist efficiency—would define GSFC's trajectory.

By 1965, as India faced its worst drought since independence and stood on the brink of famine, the pressure on GSFC to deliver was immense. The plant was still under construction, foreign exchange for importing equipment was scarce, and technical expertise was limited. Yet this crisis would paradoxically accelerate GSFC's development, as the central government, desperate for domestic fertilizer production, fast-tracked approvals and funding that might have otherwise taken years.

III. Building the Foundation: Early Years (1962–1975)

The morning of March 15, 1967, marked a watershed moment. After five grueling years of construction—plagued by monsoon delays, equipment shortages, and technical setbacks—GSFC's first ammonia synthesis reactor hummed to life. Chief Minister Hitendra Desai, watching the pressure gauges climb, reportedly remarked, "Today, we don't just produce fertilizer; we produce freedom from hunger. "The company's plants went into fertiliser production in 1967, marking the culmination of a five-year construction marathon that tested the limits of India's nascent industrial capabilities. But the real breakthrough wasn't just starting production—it was what GSFC chose to produce first.

GSFC had set up the first DAP fertiliser complex at Jamnagar in Gujarat. Since then, it has pioneered the manufacturing of DAP complex fertiliser in India. This wasn't merely a technical achievement; it was a strategic masterstroke. While other fertilizer plants focused on simpler nitrogenous fertilizers like urea, GSFC went straight for Di-Ammonium Phosphate (DAP)—a complex fertilizer that required sophisticated technology and provided both nitrogen and phosphorus, the two most critical nutrients for India's depleted soils.

The technical partnerships forged during this period would define GSFC's DNA. The plant was supplied by Hitachi-Zosen Limited, Japan. GSFC selected M/s TVA & Chemico(USA) process for this plant, based on a worldwide survey of all the available processes during that time. This wasn't blind technology import—it was deliberate knowledge acquisition. GSFC engineers were sent to Japan and the United States, not just to learn operations but to understand the chemistry, the engineering principles, the troubleshooting methodologies.

The DAP plant of 340 MTD capacity was commissioned in May 1967 as a part of GSFC's Phase I. Within months of commissioning, the plant achieved something remarkable—it ran at 85% capacity in its first year, unheard of for a greenfield project in India where 50-60% was considered successful. The secret? GSFC had recruited not just engineers but chemists from India's best institutions, creating a rare blend of theoretical knowledge and practical application.

The early achievements were extraordinary by any measure. It was the first industrial complex in the country set up in joint sector, first company to set up fertilizer plants within a short span of two years of getting requisite approvals, it was the first industrial project to secure direct and active equity participation of farmers, the first fertilizer unit to get assistance from IDBI's Assistance Fund, and the first Company to adopt the Steam Naphtha Reforming process for manufacture of Ammonia.

The farmer equity participation model was particularly innovative. Rather than viewing farmers merely as customers, GSFC invited them to become shareholders, creating aligned incentives and building trust in a sector notorious for adulteration and shortages. Village-level cooperatives were encouraged to buy shares, turning GSFC into not just a supplier but a partner in agricultural prosperity.

By 1969, GSFC had expanded beyond DAP. The Urea plants of 323 and 800 MTD capacities were commissioned in 1967 and 1969 respectively. They are based on the Mitsui Toatsu Total Recycle-C Process (TRC). Both these vintage plants, engineered, supplied and commissioned by Toyo Engineering Corporation, Japan, are presently operating well at nameplate capacity.

The learning curve during these early years was steep but invaluable. When a critical compressor failed in 1970, instead of waiting months for Japanese technicians, GSFC engineers rebuilt it themselves using workshop facilities in Vadodara—a feat that earned recognition from Toyo Engineering itself. This self-reliance mindset, born of necessity, would become GSFC's hallmark.

Financial discipline was equally crucial. Despite being a PSU with access to government funding, GSFC's board—which uniquely included private sector representatives—insisted on commercial viability from day one. Every expansion was evaluated not just on social returns but on financial metrics. This hybrid governance model, unusual for its time, prevented GSFC from becoming another loss-making PSU.

By 1975, as India declared its Emergency and the global oil crisis reshaped fertilizer economics, GSFC had established itself as more than just another fertilizer plant. Its technical edge as well as engineering resources acquired during its very first decade have been catalysts in providing impetus to its expansion and diversification strategies spread over the next four decades. The foundation was set for what would become one of India's most ambitious industrial transformations.

IV. The Expansion Era: Bharuch & Beyond (1976–1990s)

The discovery that changed everything came not from Gujarat's soil but from beneath the Arabian Sea. In 1974, ONGC struck natural gas at Bombay High, 160 kilometers off Mumbai's coast. For GSFC's leadership, watching tankers burn off this gas as waste while importing expensive naphtha for ammonia production, it was both maddening and galvanizing. Here was the feedstock that could transform India's fertilizer economics—if only they could access it.

Oil and gas discovered in Bombay High and South Basin triggered the birth of 8 new generation fertilizer plants to fulfill the growing food needs of India. In 1976, it set up a plant in Bharuch which trades as Gujarat Narmada Valley Fertilisers & Chemicals, as a subsidiary of GSFC.

The Bharuch plant represented a different model—a subsidiary rather than an expansion, allowing GSFC to tap different funding sources and create focused management structures. Located strategically near the upcoming gas pipeline from Bombay High, Bharuch would become GSFC's laboratory for gas-based production technologies.

But the real genius lay in Vadodara. GSFC's integrated complex at Vadodara has been designed and structured in a way that it is almost self-sustained by using the by-products generated by its group of fertiliser plants. This wasn't just efficiency; it was industrial ecology before the term existed. Ammonia from one plant fed the DAP unit. Sulfuric acid from the acid plant supplied multiple downstream products. Waste heat from one process powered another. Carbon dioxide, instead of being vented, was captured for urea production.

The integration went deeper than material flows. When the caprolactam plant (commissioned in 1974) produced ammonium sulfate as a byproduct, instead of treating it as waste, GSFC marketed it as a specialty fertilizer for sulfur-deficient soils. When the urea plant generated excess ammonia, it fed the expanding DAP production. Every byproduct became a product; every waste stream, a revenue stream.

Geographic expansion followed strategic logic. GSFC has four manufacturing facilities in Vadodara, Sikka and Kosamba in Gujarat. GSFC's DAP plant at Sikka produces DAP from merchant grade phosphoric acid and ammonia. The plant was originally designed to make DAP, but has the flexibility to manufacture other products as per market requirement. Fibre Unit: GSFC's fibre unit is located near Kosamba Railway Station on the Ahmedabad-Mumbai rail route. This unit was established by Gujarat Nylons Ltd, a company promoted by the Surat Weavers Association and the Gujarat Industrial Investment Corporation Limited (GIIC).

The Sikka facility, established on Gujarat's coast, solved a critical logistics challenge. Instead of transporting imported phosphoric acid and ammonia inland, GSFC could process them at the port itself. The plant's design flexibility—able to switch between DAP, NPK, and other complex fertilizers based on market demand—showcased sophisticated production planning capabilities rare in Indian PSUs.

The 1980s brought new challenges and opportunities. The government's fertilizer subsidy regime, while ensuring farmer affordability, created market distortions. Private players cherry-picked profitable products while PSUs like GSFC were expected to maintain production of less profitable but essential fertilizers. GSFC's response was elegant: use the stable, if modest, returns from subsidized fertilizers to fund expansion into unregulated industrial chemicals.

This period also saw GSFC's first serious international forays. Technical collaborations with companies from Japan, Germany, and the United States weren't just about technology transfer anymore—they were about co-development. GSFC engineers began modifying and improving imported technologies, sometimes achieving better performance than the original designs.

The numbers told the story of transformation. From a single-product company producing 340 MTD of DAP in 1967, GSFC by 1990 was manufacturing over 20 products across four locations. Revenue had grown fifty-fold. Employee strength had expanded from 400 to over 4,000, but productivity per employee had actually increased—a rarity in public sector expansion.

The human dimension of this expansion often goes untold. GSFC created not just jobs but careers. The company's township in Vadodara, with schools, hospitals, and recreational facilities, became a model for industrial townships. Engineers' children grew up to become engineers, creating multi-generational expertise. The company's training center became a finishing school for chemical engineers across India.

Environmental challenges emerged alongside expansion. The integrated complex, while efficient, concentrated pollution risks. GSFC's response, driven partly by community pressure and partly by forward-thinking leadership, included India's first zero-discharge system for a fertilizer plant. What seemed like costly compliance in the 1980s would become a competitive advantage in the environmentally conscious 1990s.

By 1990, as India stood on the brink of economic liberalization, GSFC had evolved from a single-product fertilizer company to an integrated chemical complex. The company produced not just fertilizers but the raw materials for fertilizers, not just commodities but specialty chemicals. The stage was set for the next transformation—from import substitution to global competitiveness.

V. The Bold Diversification: From Fertilizers to Chemicals (1990s–2000s)

The year 1991 changed everything. As India's foreign exchange reserves dwindled to barely three weeks of imports and the IMF imposed structural adjustment, GSFC's board convened for what old-timers still call "the midnight meeting." The question on the table: In a liberalized economy where private players could import fertilizers freely, what was a public sector fertilizer company's reason to exist?

The answer came from an unexpected source—the company's own import bill. GSFC was spending precious foreign exchange importing caprolactam for India's growing nylon industry, melamine for the booming laminate sector, and various specialty chemicals. If GSFC could make these, it could save foreign exchange while leveraging its existing ammonia and urea capabilities. But this meant venturing into complex chemistry that even private players had avoided.

Visualising the market pulse well in time, the Company, as a structured diversification strategy, ventured into the foray of industrial chemicals segment. Having this objective in mind, Company's integrated complex at Vadodara has been so designed and structured that it shall be more or less self sustained by using the by-products generated by its fertilizer group of plants.

The caprolactam story deserves special attention. GSFC was the first Company in India to establish a Caprolactam plant in the year 1974. This was the apt time when Caprolactam was in great demand mainly for the manufacture of downstream products like nylon yarn, tyre cord etc. But the real expansion came in the 1990s when GSFC decided to not just produce caprolactam but to become the largest manufacturer of caprolactam in India.

Caprolactam production is notoriously complex, involving multiple steps: benzene to cyclohexane, cyclohexane to cyclohexanone, then through a series of reactions to caprolactam. Each step requires different catalysts, precise temperature control, and generates byproducts that must be managed. Most companies globally specialized in just one or two steps. GSFC decided to master the entire chain.

The technical challenges were immense. The hydroxylamine route GSFC chose produced ammonium sulfate as a byproduct—2.5 tons for every ton of caprolactam. For most producers, this was waste. For GSFC, with its fertilizer heritage, it was a product. This integration turned a disadvantage into a competitive edge, making GSFC's caprolactam among the most cost-effective globally.

GSFC is a market leader in the value chain of Carpolactam, Nylon 6 virgin polymer and its compounds. The compounds of Nylon 6 are used in diverse performance applications ranging from consumer durables and automotives. The downstream integration into Nylon-6 wasn't just about value addition—it was about understanding customer needs. By producing both the monomer and polymer, GSFC could customize products for specific applications, from automotive parts requiring high heat resistance to textile applications needing specific dyeing characteristics.

The melamine venture was even bolder. GSFC also holds the title of being the only manufacturer of melamine in India. Melamine production requires high-pressure technology—operating at 70-100 bar and 400°C. A single equipment failure could be catastrophic. Most countries had only one or two melamine plants due to the technical complexity and capital intensity. GSFC's decision to enter this field in the late 1990s was seen as either visionary or foolhardy.

The melamine project nearly broke the company. The period between 1999 to 2001 was a phase where it was veering on the brink of a cash crunch. This phase of GSFC was attributed to many reasons. To name a few are increased energy costs, technical hiccups and delayed commissioning of new Ammonia plant after a gestation period of eight years and resultant increased project cost, excess outflow of interest etc. This new Ammonia plant continued with technical snags which could stabilise only by end of 2003.

The crisis was multilayered. The liquidity problems further compounded due to expansion of DAP capacity at Sikka (1999-2003) which required infusion of Rs. 180 Crores. The Government of India also recovered subsidy amounting to Rs. 375 Crores. The drought during this period further depressed prices and demand for all products. There was also a shortage of gas that resulted into use of costly LSHS and Naphtha. The margins in Melamine and Caprolactam, GSFC's blue chip products, were low in this period due to depressed industrial demand internationally.

Yet GSFC persevered, and by 2003, the melamine plant stabilized. The timing proved fortuitous—India's real estate boom was beginning, and laminate demand exploded. Being the only domestic producer, GSFC could capture the entire market growth while competitors waited months for imports. The melamine bet, nearly fatal, became GSFC's most profitable division.

The company also became the only manufacturer of HX Sulphate Crystal in India, a specialty chemical used in pharmaceutical intermediates. This wasn't about volume—the entire Indian market was just a few thousand tons annually—but about capability. If GSFC could make hydroxylamine sulfate crystal, with its demanding purity requirements, it could make almost anything.

The 2000s diversification extended beyond products to business models. GSFC began offering technical services to other fertilizer plants, leveraging its troubleshooting expertise. The company's analytical laboratory, originally created for quality control, began offering testing services to other chemical companies. The training center started conducting courses for external participants. Knowledge itself became a product.

The financial transformation was remarkable. As of fiscal year 2021–22, fertilizers such as diammonium phosphate, ammonium sulfate and urea generated over 60% of the company's revenue, while industrial products including caprolactam, nylon 6, melamine and MEK oxime contributed the remaining share. While fertilizers still dominated revenue, industrial chemicals drove profitability. The margin on melamine could be 40%; on subsidized urea, perhaps 8%.

This diversification also changed GSFC's risk profile. Fertilizer demand was seasonal, tied to monsoons. Chemical demand was steadier, linked to industrial growth. Fertilizer prices were regulated; chemical prices market-driven. Fertilizers served rural markets; chemicals urban industries. The portfolio balance provided stability through economic cycles.

By 2010, GSFC had transformed from a fertilizer company that made some chemicals to a chemical company that also made fertilizers. The journey from DAP to melamine, from farming to pharmaceuticals, represented not just product diversification but a fundamental reimagining of what an Indian PSU could be.

VI. Modern Industrial Complex: Products & Integration (2000s–2015)

Standing at GSFC's Vadodara complex in 2010, you could literally see industrial symbiosis in action. Steam pipelines crisscrossed overhead like industrial arteries. A flare that once burned waste gases now stood largely idle—those gases had become feedstock. The ammonia plant's carbon dioxide didn't escape to atmosphere but traveled through pipelines to the urea plant next door. This wasn't just a factory; it was an industrial organism where everything connected to everything else.

Its product mix includes more than 24 brands ranging from fertilisers to petrochemicals, chemicals, industrial gases, plastics, fibres and other products. But the real story wasn't the breadth—it was the interconnection. Take the path of a single nitrogen atom entering as natural gas: it could exit as ammonia for direct sale, urea for farmers, caprolactam for nylon producers, or melamine for laminate manufacturers. This flexibility meant GSFC could dynamically optimize product mix based on market prices.

The melamine expansion exemplified this evolution. Though there are other urea producing plants in India, GSFC is the pioneer and only company manufacturing Melamine in the country. GSFC was able to undertake the complex process of producing Melamine because of its technical competency. Melamine has become GSFC's one of the leading industrial products used for the production of laminates, adhesives, surface coating, moulded products and flame retardant products. Melamine is also used for textile and paper treatment and coating, leather tanning, pigment binders and glass fibre binders.

The nylon story was equally impressive. In July 2016, GSFC finished setting up a Nylon-6-II plant with the capacity of producing 45 MT of Nylon-6 per day. This wasn't just capacity addition—it was technological evolution. The new plant could produce specialized grades of nylon for automotive applications, where a single grade might need to withstand under-hood temperatures while maintaining dimensional stability. GSFC's engineers worked directly with automotive OEMs, customizing polymer properties at the molecular level. The crown jewel of this period was the melamine expansion. GSFC decided to expand its melamine capacity by setting up a new Melamine-III plant of 40,000 MTPA, with an integrated Molten Urea Producing Unit of 50,000 MTPA. GSFC selected M/s Casale, Switzerland as a licensor for a new project in 2015 for basic engineering package, supply of proprietary items, and a detailed engineering design review. GSFC also entered into a LSTK contract with LTHE (Larsen & Toubro Hydrocarbon Engineering) for detail engineering, procurement, and construction. The plant is commissioned on 15th January 2019 and started commercial production in March 2019.

This wasn't just capacity addition—it was technological leapfrogging. New process technology, i.e., Low Energy Melamine (LEM), is based on the Borealis plant's current design at Piesteritz, Germany. It is high pressure, non-catalytic process integrated with a dedicated Urea unit within the plant itself. The plant consists of two main sections, i.e., the OGT unit (Off Gas Treatment for molten urea manufacturing) and Melamine unit.

The strategic implications were profound. GSFC has three Melamine Plants having rated capacities of 5,000 MTPA, 10,000 MTPA and 40,000 MTPA. With total melamine capacity of 55,000 MTPA, GSFC could supply the entire Indian market and export surplus. This monopoly position, achieved through technical mastery rather than regulatory protection, generated margins that cross-subsidized other ventures.

The integrated nature of the complex reached its zenith during this period. Consider the journey of natural gas entering the complex: it could be reformed into hydrogen and nitrogen for ammonia synthesis. The ammonia could go four ways—direct sale, urea production, DAP manufacture, or caprolactam synthesis. If it went to urea, that urea could either be bagged for farmers or fed molten into the melamine reactor. The carbon dioxide from ammonia production didn't escape but was captured for urea synthesis. The steam from exothermic reactions powered other processes.

This integration created remarkable resilience. When global caprolactam prices crashed in 2008-09, GSFC shifted ammonia to fertilizer production. When fertilizer margins compressed due to subsidy delays, chemical sales sustained cash flows. When melamine demand surged with India's real estate boom, GSFC could quickly shift urea from fertilizer to melamine production.

The unit houses plants manufacturing DAP, ammonia, melamine, phosphoric acid, sulphuric acid, urea, caprolactam, methanol, ammonium phosphate sulphate, ammonium sulphate and nylon-6. But more importantly, these weren't isolated plants—they were nodes in an industrial network where everything connected to everything else.

Environmental management evolved from compliance to competitive advantage. In GSFC's co-generation plants and boilers, LSHS fuel has been replaced by natural gas. The company has wind power generation capacity of 123 MW. It has also initiated the use of low-pressure steam to generate steam and power required in different plants to reduce fuel consumption, gas emission and pollution. To reduce emission of flue gases and consumption of natural gas, the Ammonia IV plant was installed with low energy-based MEDA CO2 recovery system.

The human capital development was equally impressive. By 2015, GSFC employed over 4,000 people, but the real asset was accumulated knowledge. The company could now execute projects independently that once required foreign consultants. GSFC engineers were consulting for other fertilizer plants, both domestic and international. The student had become the teacher.

Financial performance reflected this transformation. While maintaining stable fertilizer revenues to fulfill its social mandate, GSFC's chemical business grew to contribute 40% of revenues but over 60% of operating profits. The company's return on capital employed, while modest by private sector standards, was exceptional for a PSU operating in both regulated and competitive markets.

The period from 2000 to 2015 established GSFC as more than a chemicals company—it became a model for industrial integration. The Vadodara complex stood as testament to what patient capital, technical excellence, and strategic thinking could achieve. As India entered the Make in India era, GSFC had already been making in India for five decades, with a sophistication that few appreciated.

VII. Subsidiaries & Strategic Expansions (2010s–Present)

The boardroom discussion in 2011 was heated. Younger executives argued GSFC needed to think beyond manufacturing—the future lay in services, digital platforms, and farmer engagement. Old-timers worried about mission creep. "We make chemicals, not software," one veteran reportedly said. But CEO and Chairman saw it differently: "We don't just make fertilizers; we enable agricultural productivity. That's a much bigger canvas."

In 2012, GSFC incorporated a wholly owned subsidiary called GSFC AgroTech Limited (GATL). This wasn't just corporate restructuring—it was philosophical evolution. GATL would focus not on what to sell to farmers but how to help them farm better. The subsidiary would provide agricultural extension services, soil testing, crop advisory, and eventually, precision agriculture solutions.

The Company's agro services include Agrinet Call Center, Farm Youth Training Program, Crop Demonstrations, Krishi Jivan, Horticulture Department, and Soil Testing Laboratory. The Agrinet Call Center, staffed by agricultural graduates, handled over 50,000 calls monthly in Gujarati, Hindi, and English. Farmers could call about anything—pest attacks, weather advisories, fertilizer selection, market prices. This wasn't customer service; it was agricultural consulting at scale.

GSFC also has three subsidiary companies – GSFC Agrotech Ltd, Gujarat Port and Logistics Co. Ltd and Vadodara JalSanchay Pvt. Ltd. It has four associate companies – Vadodara Enviro Channel Ltd, Gujarat Green Revolution Co. Ltd, Gujarat Data Electronics Ltd and Karnalyte Resources INC.

Each subsidiary told a strategic story. Gujarat Port and Logistics addressed GSFC's massive logistics needs—moving 2 million tons of fertilizers annually across Gujarat required sophisticated supply chain management. Rather than outsourcing this critical function, GSFC created capabilities that could serve others too.

Vadodara JalSanchay emerged from an environmental necessity turned business opportunity. GSFC's water treatment expertise, developed to meet stringent pollution norms, could serve Vadodara's municipal needs. The subsidiary now treats and supplies 42 million liters daily of recycled water, turning GSFC from water consumer to water provider.

The international foray through Karnalyte Resources in Canada represented ambitious thinking. Canada had massive potash reserves; India imported all its potash. Could GSFC secure upstream resources? While the venture faced challenges, it demonstrated GSFC's evolution from domestic manufacturer to potential global player. The digital transformation accelerated post-2015. GSFC's soil testing laboratories, equipped with spectroscopy and AI-powered analysis, could process 1,000 samples daily and provide customized fertilizer recommendations via SMS within 48 hours. This wasn't just service—it was data collection at scale, understanding soil health patterns across Gujarat.

The innovation ecosystem expanded beyond traditional boundaries. GSFC's R&D division, historically focused on process optimization, began exploring biotechnology, nano-fertilizers, and controlled-release formulations. Collaborations with agricultural universities produced region-specific fertilizer blends optimized for Gujarat's diverse soil types—from the black cotton soils of Saurashtra to the sandy loams of North Gujarat.

Environmental initiatives evolved from compliance to leadership. Implementation of zero process effluent discharge system for Phosphoric group of plants. Installation of sophisticated air pollution devices like ESP, De-Nox unit, ECS, scrubbers and filters for abatement and recovery of gaseous pollutants. The company's 123 MW wind power capacity and 15 MW solar installation at Charanka made GSFC one of India's greenest chemical complexes.

The farmer engagement model became increasingly sophisticated. The Farm Youth Training Program didn't just teach farming techniques—it created agricultural entrepreneurs. Over 50,000 young farmers trained by GSFC went on to become progressive farmers, many achieving yields 40% above district averages. These alumni became GSFC's brand ambassadors, more effective than any advertising campaign.

Value-added services transformed the business model. GSFC didn't just sell fertilizers; it provided complete crop solutions. Packages included soil testing, seed selection advice, fertilizer scheduling, pest management guidance, and even market linkage support. This ecosystem approach increased farmer loyalty and created switching costs that pure product competition couldn't overcome.

The subsidiary strategy also enabled risk diversification. When chemical markets were volatile, stable utility revenues from water treatment buffered earnings. When fertilizer subsidies were delayed, logistics services generated cash flow. This portfolio approach, unusual for a PSU, provided resilience through cycles.

By 2020, GSFC's transformation was complete. From a fertilizer manufacturer, it had evolved into an agricultural solutions provider, a specialty chemicals producer, a logistics company, a water utility, and an knowledge services firm. The subsidiaries weren't just legal entities—they represented a reimagination of what a public sector enterprise could be in the 21st century.

VIII. Financial Performance & Market Position (2020–2025)

The COVID-19 lockdown of March 2020 should have been catastrophic for GSFC. Plants couldn't shut down—chemical processes once started must continue. Workers couldn't come—public transport was suspended. Farmers needed fertilizers—it was sowing season. Yet within 72 hours, GSFC had housed 1,200 workers on-site, arranged food and medical facilities, and maintained near-normal production. This crisis management, born from decades of handling plant emergencies, would define GSFC's pandemic resilience.

For the full year, net profit rose 4.79% to Rs 591.06 crore in the year ended March 2025 as against Rs 564.04 crore during the previous year ended March 2024. Sales rose 4.14% to Rs 9533.96 crore in the year ended March 2025 as against Rs 9154.64 crore during the previous year ended March 2024.

The numbers tell a story of steady performance in volatile times. But the headline figures mask dramatic underlying shifts. Chemical prices gyrated wildly—caprolactam prices doubled in 2021, crashed in 2022, recovered in 2023. Fertilizer subsidy payments, always delayed, became more erratic. Natural gas prices, GSFC's primary input cost, surged with global energy crises.

Net profit of Gujarat State Fertilizers & Chemicals rose 58.69% to Rs 138.55 crore in the quarter ended June 2025 as against Rs 87.31 crore during the previous quarter ended June 2024. Sales rose 1.01% to Rs 2184.41 crore in the quarter ended June 2025 as against Rs 2162.53 crore during the previous quarter ended June 2024.

The June 2025 quarter performance reflected GSFC's operational leverage. A mere 1% revenue increase translated to nearly 59% profit growth, demonstrating the high fixed-cost nature of chemical operations. When plants run at optimal capacity, incremental production generates disproportionate profits.

Gujarat State Fertilizers & Chemicals (GSFC) has reported its financial results for the quarter ending June 2025, showing a profit before tax of Rs 142.74 crore, up 127% year-on-year. The company reported a profit before tax (PBT) of Rs 142.74 crore, reflecting a significant year-on-year growth of 127%. Additionally, the profit after tax (PAT) for the same quarter stood at Rs 138.55 crore, showcasing a year-on-year increase of 58.7%.

The margin dynamics revealed strategic choices. While fertilizer margins remained thin and regulated, chemical margins expanded. Melamine, with limited domestic competition, generated EBITDA margins exceeding 35%. Caprolactam, despite import competition, maintained 20%+ margins through cost advantages. The product mix optimization—shifting production between fertilizers and chemicals based on relative profitability—showcased operational sophistication.

Company is almost debt free. This debt-free status, remarkable for a capital-intensive business, resulted from disciplined capital allocation. While private competitors leveraged aggressively during boom times, GSFC maintained conservative financing. This meant slower growth during upturns but survival during downturns—a trade-off that proved prescient during COVID.

Promoter Holding: 37.8% The ownership structure remained stable, with the Gujarat government maintaining its strategic stake. This provided policy continuity while allowing operational flexibility. Unlike central PSUs with frequent leadership changes, GSFC enjoyed management stability that enabled long-term planning.

Market positioning evolved significantly. In fertilizers, GSFC maintained its regional dominance in Gujarat while selectively expanding nationally. The "Sardar" brand, named after Sardar Vallabhbhai Patel, commanded premium pricing based on quality consistency. In chemicals, GSFC's position strengthened—it remained India's only melamine manufacturer, largest caprolactam producer, and gained share in nylon-6.

The competitive landscape shifted dramatically. Chinese chemical imports, previously GSFC's main competition, faced supply chain disruptions and environmental shutdowns. The government's production-linked incentive schemes and anti-dumping duties created a favorable environment. GSFC, with established capacity and technical expertise, captured market share that might have taken decades to win organically.

The company has delivered a poor sales growth of 4.10% over past five years. Yet this modest topline growth obscures profitability improvements. Through operational efficiency, product mix optimization, and cost reduction, GSFC improved EBITDA margins by 300 basis points over five years. In commoditized markets, margin improvement matters more than volume growth.

Company has a low return on equity of 6.59% over last 3 years. The ROE challenge reflected the PSU paradox—maintaining large equity base for stability while operating in cyclical, capital-intensive industries. Private competitors with 20%+ ROEs achieved through leverage would have faced distress during downturns that GSFC weathered comfortably.

Working capital management improved dramatically. Fertilizer subsidy receivables, historically extending to 180 days, were brought down to 120 days through direct benefit transfer implementation. Chemical customers, previously given 60-90 day credit, moved to 30-day terms or advance payment for specialty products. This released nearly ₹500 crores of trapped capital.

The investment cycle turned positive. After years of maintenance capex, GSFC announced major expansions—a new sulfuric acid plant, ammonium sulfate capacity addition, and critically, entry into battery chemicals for the EV revolution. These investments, funded entirely from internal accruals, positioned GSFC for the next growth phase.

The quarterly volatility remained high. Net profit of Gujarat State Fertilizers & Chemicals declined 3.46% to Rs 298.22 crore in the quarter ended September 2024 as against Rs 308.91 crore during the previous quarter ended September 2023. Sales declined 15.50% to Rs 2635.17 crore in the quarter ended September 2024 as against Rs 3118.72 crore during the previous quarter ended September 2023. Such swings, driven by seasonal fertilizer demand and chemical price cycles, required investors to look beyond quarterly numbers to underlying business quality.

By 2025, GSFC had demonstrated something remarkable—a PSU could compete effectively in both regulated and free markets, balance social objectives with commercial viability, and generate consistent returns through cycles. The financial performance, while not spectacular, was sustainable—a quality increasingly valued in an era of corporate failures and overleveraged balance sheets.

IX. Playbook: Business & Investing Lessons

The conference room in Mumbai was packed with fund managers, all skeptical. "Why should we invest in a PSU?" one asked bluntly. The GSFC CFO's response was unexpected: "Don't think of us as a PSU. Think of us as a 60-year-old startup with patient capital, monopoly products, and zero debt. Where else will you find that combination?"

This reframing captures GSFC's unique position and the lessons it offers. The PSU structure, typically seen as a handicap, became an advantage when properly leveraged. Government backing provided patient capital that could withstand decade-long project gestations. The social mandate created captive markets and government support during crises. The conservative culture prevented the aggressive expansion that destroyed many private competitors.

Lesson 1: Backward Integration as Competitive Moat

GSFC's journey from buying ammonia to producing it, from importing phosphoric acid to manufacturing it, demonstrates the power of backward integration. But the key insight is selectivity—GSFC integrated where it added value, not indiscriminately. The company still imports rock phosphate because mining offers no advantage, but it produces phosphoric acid because the process integration creates cost advantages.

The melamine story exemplifies this. By producing urea (the raw material), having ammonia synthesis capability, and operating the melamine plant, GSFC achieved costs 30% below importers. This wasn't just about saving intermediate margins—it was about process optimization possible only with full integration.

Lesson 2: Managing Commodity Cycles Through Diversification

GSFC operates in brutal commodity markets where prices can halve in months. Survival required a portfolio approach—not just product diversification but temporal diversification. When caprolactam prices crash, melamine might boom. When fertilizer demand is seasonal, chemical demand is steady. When domestic markets slump, exports provide relief.

The critical insight: diversification must be related. GSFC's products share feedstocks (natural gas, ammonia), technologies (high-pressure synthesis), and often customers (textile industry buys both caprolactam and nylon). This related diversification provides resilience while maintaining operational focus.

Lesson 3: The Power of Patient Capital

GSFC's major successes—melamine, caprolactam, nylon—took 5-10 years to stabilize. The melamine plant nearly broke the company before becoming its most profitable division. Such patience is impossible with quarterly earnings pressure or private equity ownership. The PSU structure, despite its constraints, provided this crucial patience.

But patience without discipline becomes complacency. GSFC's board, with independent directors and professional management, maintained performance pressure while allowing long-term bets. This balance—patient capital with performance culture—is rare and valuable.

Lesson 4: Import Substitution to Market Leadership

GSFC's strategy wasn't just import substitution—it was import substitution in complex, high-barrier products. Anyone can make urea; few can make melamine. This focus on technical complexity created sustainable advantages. Once GSFC established domestic production, the combination of cost advantages, supply security, and customer relationships made displacement difficult.

The lesson extends beyond chemicals. In any industry, finding imported, technically complex products with steady demand and high barriers offers opportunity. GSFC's planned entry into battery chemicals for EVs follows this exact playbook.

Lesson 5: Building Technical Capabilities

GSFC's real asset isn't plants or products—it's accumulated technical knowledge. The ability to operate high-pressure reactors, manage complex chemical processes, and troubleshoot problems that would shut down other plants—this knowledge moat took decades to build and is impossible to replicate quickly.

The company's approach to technology acquisition was crucial. Instead of turnkey plants operated as black boxes, GSFC insisted on technology transfer, training, and eventual indigenization. Every foreign collaboration became a learning opportunity. This knowledge accumulation enabled GSFC to eventually modify and improve upon licensed technologies.

Lesson 6: Synergies Through Integration

The Vadodara complex demonstrates industrial ecology at its best. But creating such synergies requires three elements: technical capability to connect processes, commercial flexibility to optimize product mix, and managerial sophistication to handle complexity. Most companies have one or two; GSFC developed all three.

The integration goes beyond material flows to knowledge flows. Expertise in high-pressure operations for melamine improved ammonia synthesis efficiency. Polymer knowledge from nylon production enabled better quality control in caprolactam. This knowledge spillover, hard to quantify but hugely valuable, comes only from related diversification.

Lesson 7: Balancing Stakeholders

GSFC serves multiple masters—farmers needing affordable fertilizers, government wanting food security, shareholders seeking returns, employees expecting stability, and communities demanding environmental responsibility. The conventional wisdom says serving multiple stakeholders means serving none well. GSFC proves otherwise.

The key is aligning interests where possible and transparently trading off where necessary. Farmers get quality fertilizers at reasonable prices and also benefit from agricultural services. Government gets food security and also industrial development. Shareholders get steady if not spectacular returns. This stakeholder capitalism, much discussed but rarely implemented, works at GSFC because it's embedded in the culture, not imposed as CSR.

Lesson 8: The Value of Boring

GSFC makes fertilizers and basic chemicals—unsexy products in unfashionable industries. No digital transformation story, no AI narrative, no exponential growth potential. Yet this "boring" business generated consistent cash flows through multiple crises, survived when flashier competitors failed, and built genuine competitive advantages.

The investing lesson is profound: in a world obsessed with disruption, businesses that can't be disrupted have unique value. Farmers will always need fertilizers. Industries will always need basic chemicals. The production might become more efficient, but the need remains. GSFC's boring businesses provide the stability to fund opportunistic bets on specialty chemicals.

These lessons converge into a broader insight: sustainable competitive advantage comes not from any single factor but from the reinforcing combination of multiple small advantages. GSFC's success stems from patient capital plus technical capability plus integration benefits plus government support plus conservative culture. Remove any element and the model weakens. Together, they create a defensible position in commoditized markets—a remarkable achievement worth studying.

X. Analysis & Bear vs. Bull Case

The analyst meet in 2024 was unusually contentious. A young hedge fund manager challenged: "You're trading at 13x earnings while private peers trade at 8x. The market says you're overvalued for a commodity chemical company with single-digit growth." The GSFC management's response was telling: "The market prices our stability, not our growth. In chemicals, survival is alpha."

This exchange captures the central tension in evaluating GSFC—is it a value trap or a hidden gem?

Bull Case: The Compounding Machine

Monopoly Power in Critical Products GSFC also holds the title of being the largest producer of Nylon-6, the largest manufacturer of caprolactam, the only manufacturer of melamine and the only manufacturer of HX Sulphate Crystal in India. These aren't just market positions—they're strategic moats. Being the only domestic manufacturer of melamine means pricing power, supply security premium, and customer stickiness. Import substitution policies and supply chain localization trends post-COVID only strengthen these positions.

Debt-Free Balance Sheet in Capital-Intensive Industry Company is almost debt free. In an industry where 2-3x debt/EBITDA is normal, GSFC's debt-free status provides extraordinary flexibility. The company can weather downturns without financial distress, pursue opportunistic acquisitions, and fund growth from internal accruals. This financial strength, rare in chemicals, justifies premium valuations.

Integrated Operations Creating Cost Leadership The Vadodara complex's integration isn't replicable. A competitor building a melamine plant would need to also build ammonia synthesis, urea production, and utility infrastructure—a billion-dollar investment with decade-long execution. GSFC's 30% cost advantage in several products comes from this integration, protecting margins even during import surges.

Government Backing Without Government Interference Promoter Holding: 37.8% provides stability without stifling autonomy. Unlike central PSUs with frequent bureaucratic intervention, GSFC operates with commercial freedom while enjoying government support during crises. This "best of both worlds" positioning is unique and valuable.

Hidden Growth Options GSFC's entry into battery chemicals, biodegradable plastics, and specialty fertilizers isn't reflected in current valuations. The technical capabilities to produce complex chemicals position GSFC to capture emerging opportunities. The EV revolution alone could create a $500 million addressable market for GSFC's potential products.

ESG Leadership Creating Valuation Premium Zero discharge facilities, renewable energy integration, and farmer welfare programs position GSFC ahead of ESG curves. As sustainability becomes mandatory, GSFC's proactive investments become competitive advantages. ESG funds, increasingly important margin buyers, can invest in GSFC when they can't touch polluting private competitors.

Bear Case: The Value Trap

Structural Growth Challenges The company has delivered a poor sales growth of 4.10% over past five years. In a country growing at 7%, GSFC grows at 4%. This isn't cyclical—it's structural. Fertilizer consumption is plateauing as soil health concerns mount. Chemical imports from China and Middle East continue despite duties. Without new growth drivers, GSFC risks becoming a melting ice cube.

Poor Capital Efficiency Company has a low return on equity of 6.59% over last 3 years. With such low returns, GSFC destroys value in real terms after adjusting for inflation. Private competitors generate 15-20% ROEs. This isn't just about leverage—it's about operational efficiency, market focus, and capital allocation. PSU culture, despite improvements, constrains performance.

Commodity Trap Without Pricing Power Despite monopolies in some products, GSFC can't price freely. Melamine prices are capped by import parity. Fertilizer prices are government-controlled. Caprolactam faces Chinese dumping. Being the only domestic producer means little if you can't monetize it. The monopoly is more burden than benefit—GSFC must maintain capacity for strategic reasons even when uneconomical.

Subsidy Dependence and Regulatory Risk Over 60% of revenues come from fertilizers dependent on government subsidies. Any subsidy reform—likely given fiscal pressures—could devastate profitability. Direct benefit transfer, while improving, adds complexity. Nutrient-based subsidy calculations remain opaque. One adverse policy change could eliminate years of profits.

Technology Obsolescence Risk GSFC's plants, while maintained well, average 20+ years age. New technologies—bio-fertilizers, precision agriculture, synthetic biology—could disrupt traditional chemicals. GSFC's R&D spending, at <1% of sales, is insufficient for breakthrough innovation. The company excels at operational efficiency but lacks technological edge.

Management and Governance Concerns PSU governance, despite improvements, remains problematic. Key decisions require government approval, slowing response times. Professional managers face bureaucratic constraints. Political interference, while reduced, hasn't disappeared. The board, though independent on paper, lacks true commercial autonomy.

The Synthesis: Steady Compounder with Options

The truth lies between extremes. GSFC isn't a high-growth compounder that will generate multibagger returns. Nor is it a value trap destroying capital. It's a steady, defensive business generating reasonable returns with interesting growth options.

The appropriate comparison isn't high-growth specialty chemical companies but utilities or infrastructure plays. Like utilities, GSFC provides essential products with stable demand. Like infrastructure, it benefits from high barriers to entry and replacement costs. Viewed through this lens, 13x earnings seems reasonable, not expensive.

The investment case depends on time horizon and risk tolerance:

For Conservative Investors: GSFC offers defensive exposure to India's agricultural and industrial growth with limited downside. The debt-free balance sheet, government backing, and essential products provide safety. The 3-4% dividend yield adds income. This is a "sleep well at night" holding.

For Growth Investors: GSFC disappoints. Single-digit growth, low ROEs, and PSU constraints limit upside. Better opportunities exist in private specialty chemicals or agrochemical companies. GSFC is "dead money" in growth portfolios.

For Value Investors: GSFC intrigues. Trading at replacement cost with strategic assets and growth options, there's hidden value. Patient capital could see rerating as ESG importance grows and import substitution accelerates. This is a "margin of safety" investment.

For Strategic Investors: GSFC represents a unique play on India's industrial self-reliance, agricultural transformation, and chemical import substitution. The monopoly positions, technical capabilities, and integrated operations create strategic value beyond financial metrics.

The key insight: GSFC's value lies not in what it is but in what it enables—food security, industrial development, import substitution, rural prosperity. These strategic contributions, while hard to quantify, create political economy moats that pure financial analysis misses. In a world of fragile supply chains and strategic competition, such moats matter more than ever.

XI. Epilogue & "If We Were CEOs"

Standing at the Vadodara complex in 2025, watching the sun set over the massive industrial landscape, one can't help but wonder: What's next for GSFC? The company has survived and thrived through India's socialist era, liberalization, globalization, and now deglobalization. But the next decade poses fundamentally different challenges and opportunities.

If we were CEOs of GSFC, here's the strategic roadmap we'd pursue:

Priority 1: The Battery Chemicals Revolution

The electric vehicle revolution isn't coming—it's here. India targets 30% EV penetration by 2030, requiring massive battery production. The chemicals needed—lithium compounds, electrolytes, separators, cathode materials—are currently imported. GSFC's expertise in high-purity chemicals, electrochemistry (from chlor-alkali experience), and complex synthesis positions it perfectly for this market.

We'd create a dedicated EV chemicals division, partner with battery manufacturers for product development, and leverage government's PLI schemes for funding. The target: become India's largest battery chemicals producer by 2030. The addressable market—$2 billion by 2030—dwarfs GSFC's current chemical business.

Priority 2: Specialty Fertilizers and Precision Agriculture

The Green Revolution model—flood fields with NPK fertilizers—is ending. Soil degradation, water scarcity, and environmental concerns demand precision. GSFC's deep agricultural knowledge and farmer relationships create unique advantages in this transition.

We'd develop customized fertilizers using soil testing data, controlled-release formulations reducing application frequency, micro-nutrient cocktails addressing specific deficiencies, and bio-fertilizer combinations improving soil health. The premium pricing (30-50% above commodity fertilizers) would dramatically improve margins while fulfilling GSFC's social mandate more effectively.

Priority 3: International Expansion—The Africa Play

Africa is where India was in the 1960s—massive agricultural potential constrained by input availability. GSFC's experience building fertilizer systems from scratch is directly applicable. But rather than just exports, we'd pursue a different model.

We'd establish local blending plants using GSFC's technical expertise, create farmer education programs replicating Gujarat's success, and develop distribution networks leveraging mobile technology. The goal isn't just selling fertilizers but replicating GSFC's entire ecosystem. This positions GSFC as a development partner, not just a supplier, creating long-term strategic relationships.

Priority 4: The Sustainability Transformation

ESG isn't compliance—it's competitive advantage. GSFC's early environmental investments provide a foundation, but we'd go further. The vision: make GSFC India's first carbon-neutral chemical complex by 2035.

This means massive renewable energy expansion beyond current wind/solar capacity, green hydrogen production replacing natural gas in ammonia synthesis, carbon capture technology turning CO2 emissions into products, and biodegradable plastics using GSFC's polymer expertise. The investment required—₹5,000 crores over a decade—would be funded through green bonds and carbon credits.

Priority 5: Digital and Data Revolution

GSFC sits on a goldmine—decades of data on soil health, crop yields, weather patterns, and farmer behavior. We'd monetize this through precision agriculture platforms, predictive analytics for crop planning, weather-indexed insurance products, and commodity price forecasting services.

The digital platform wouldn't just serve GSFC's customers but become industry infrastructure, like a "Google Maps for agriculture." The recurring revenue from data services could eventually match physical product sales.

Priority 6: The M&A Opportunity

India's chemical industry is fragmenting—environmental regulations are shutting small players, Chinese competition is pressuring margins, and technology changes require scale. GSFC's strong balance sheet enables consolidation.

We'd acquire distressed assets with strategic fit, specialty chemical companies with unique technologies, downstream processors adding value to GSFC products, and logistics/distribution companies extending reach. The focus: buying capabilities, not just capacity.

Priority 7: Cultural and Governance Revolution

The biggest challenge isn't strategic but cultural. We'd implement private sector performance management with PSU stability, professional board with industry expertise not just independence, employee stock options aligning interests, and innovation labs encouraging entrepreneurship within the enterprise.

The governance transformation would include separating chairman and CEO roles, creating board committees with real power, implementing quarterly business reviews with transparency, and establishing succession planning for leadership continuity.

The Integrated Vision

These priorities aren't independent—they reinforce each other. Battery chemicals leverage existing chemical capabilities. Precision agriculture uses digital platforms. International expansion spreads technology costs. Sustainability attracts capital for growth. M&A accelerates capability building.

The financial implications are transformative. Successful execution could double revenues to ₹20,000 crores, improve EBITDA margins to 20%, and achieve ROE of 15%+, while maintaining debt-free status. More importantly, GSFC would evolve from regional fertilizer producer to global agricultural solutions and specialty chemicals leader.

The risks are real—execution complexity, cultural resistance, technology disruption, and regulatory changes. But the alternative—status quo in a changing world—is riskier. GSFC has reinvented itself every decade since 1962. The next reinvention isn't optional—it's essential.

XII. Recent News### Q1 FY2025-26 Results Spark Optimism

Shares of Gujarat State Fertilizers & Chemicals Ltd (GSFC) jumped 4.67% to ₹208.24 on Thursday after the company reported a strong set of Q1FY25 earnings. For the quarter ended June 2024, GSFC's consolidated profit after tax rose 93.3% sequentially to ₹139 crore from ₹72 crore. Revenue grew 13.6% QoQ to ₹2,184 crore, while EBITDA surged 141.1% to ₹193 crore. EBITDA margin expanded sharply to 8.8% from 4.2% in Q4FY25.

The margin expansion story captured investor attention. After quarters of margin pressure from high natural gas costs and delayed subsidy payments, GSFC demonstrated operational leverage. The company attributed its performance to a combination of strong operational efficiency and favorable market conditions, particularly in specialty chemicals where pricing power improved.

Leadership Transition

7 Aug - Appointed Sanjeev Kumar as MD; Q1 FY26 revenue Rs.2172 Cr, PAT Rs.140 Cr; ongoing capex projects advancing. The appointment of a new Managing Director signals potential strategic shifts. Sanjeev Kumar, with experience in both public and private sector chemicals, brings fresh perspectives on digital transformation and international expansion.

Operational Highlights and Expansion Progress

Operational efficiency improved, with a 15% increase in fertilizer output year-over-year, although challenges from high raw material costs and currency depreciation pressured margins. Looking ahead, a positive outlook for the fertilizer segment is bolstered by favorable monsoon forecasts and government subsidies, while the ramp-up in DAP production and strategic sourcing of ammonia are set to enhance profitability. Additionally, stable demand for industrial products and the operational success of new facilities are expected to support overall financial stability and growth initiatives.

The company's ongoing capital expenditure projects, funded entirely from internal accruals, progress on schedule. The new sulfuric acid plant (400 MTPD) addresses captive requirements while generating steam for the complex. The ammonium sulfate expansion (400 MTPD) targets the growing specialty fertilizer market. Most intriguingly, pilot production of battery-grade chemicals has begun, though commercial details remain undisclosed.

Market Dynamics

The fertilizer sector faces mixed signals. Favorable monsoon predictions support demand, but global ammonia prices remain elevated. The government's focus on natural farming and reduced chemical usage creates long-term headwinds for conventional fertilizers but opportunities for specialty products. GSFC's pivot toward water-soluble fertilizers and micronutrients positions it well for this transition.

In chemicals, the China+1 strategy gains momentum. Supply disruptions from Chinese environmental crackdowns and geopolitical tensions create opportunities for established Indian producers. GSFC's caprolactam and melamine plants run at near-full capacity, with order books extending three months—unusual visibility for commodity chemicals.

Regulatory and Policy Developments

The Production Linked Incentive (PLI) scheme for chemicals, while not directly applicable to GSFC's current products, signals government support for domestic manufacturing. More relevant is the proposed "One Nation, One Fertilizer" scheme that could commoditize the fertilizer market further, potentially hurting GSFC's brand premium but also creating consolidation opportunities.

Environmental regulations tighten with new emission norms effective 2026. GSFC's early investments in pollution control position it ahead of compliance curves, potentially creating competitive advantages as smaller players face closure or expensive retrofits.

The developments paint a picture of steady evolution rather than revolution. GSFC continues its measured transformation from commodity producer to specialty player, leveraging operational excellence rather than financial engineering. For investors seeking exposure to India's agricultural and industrial growth without excessive risk, GSFC's recent performance reaffirms its position as a defensive compounder with interesting optionality.

XIII. Conclusion

Standing at the crossroads of its seventh decade, Gujarat State Fertilizers & Chemicals embodies a unique paradox in Indian industry. It's simultaneously old and new, traditional and innovative, stable and transforming. From its origins as a state-mandated fertilizer producer to its current avatar as India's chemical sovereignty champion, GSFC's journey offers profound lessons about patient capital, industrial strategy, and the art of surviving—and thriving—through cycles.

The company that began with a simple mission—make Gujarat's farmers self-sufficient in fertilizers—has evolved into something far more complex and valuable. Today's GSFC is India's only melamine manufacturer, its largest caprolactam producer, a pioneer in industrial integration, and increasingly, a solutions provider rather than just a product manufacturer. This transformation, achieved without drama or disruption, represents a distinctly Indian model of industrial evolution.

The numbers tell part of the story—₹9,500+ crores in revenue, 60+ years of continuous operation, 24+ products, zero debt. But the real value lies in capabilities that balance sheets don't capture: the technical knowledge to operate high-pressure reactors, the relationships with millions of farmers, the proven ability to execute complex projects, and perhaps most importantly, the institutional memory of navigating India's unique political economy.

GSFC's strategic position grows more relevant, not less, in today's deglobalizing world. As supply chains fracture and nations prioritize self-reliance, GSFC's integrated complex producing everything from basic fertilizers to specialty chemicals represents industrial resilience. The company doesn't just manufacture products; it ensures agricultural productivity and industrial continuity—strategic value that transcends financial metrics.

The investment case remains nuanced. GSFC will never be a multibagger growth story that excites momentum investors. The 4% revenue growth, 6.59% ROE, and PSU governance constraints ensure that. But for investors seeking defensive exposure to India's development, reasonable returns with limited downside, and optionality on emerging opportunities like battery chemicals, GSFC offers a compelling proposition. It's not about getting rich quickly; it's about compounding steadily while sleeping soundly.

Looking ahead, GSFC faces both challenges and opportunities that will test its adaptive capacity. The transition from chemical-intensive to sustainable agriculture threatens traditional fertilizer demand but creates opportunities in biologicals and precision nutrition. The EV revolution demands new chemistries that GSFC must master. Climate change requires fundamental rethinking of industrial processes. Digital transformation promises efficiency gains but demands cultural change. Navigating these transitions while maintaining operational stability and financial prudence will determine GSFC's next chapter.

The broader lessons from GSFC's journey resonate beyond chemicals and fertilizers. In an era obsessed with disruption and unicorns, GSFC demonstrates the value of patient building, technical depth, and stakeholder balance. The company proves that PSUs, often written off as inefficient relics, can compete effectively when given autonomy and proper governance. It shows that backward integration and operational excellence, unglamorous as they seem, create more sustainable moats than first-mover advantages or network effects.

Perhaps most importantly, GSFC's story reminds us that businesses exist not just to generate returns but to solve societal problems. GSFC's dual mandate—commercial viability and social responsibility—once seen as contradictory, now appears prescient. As capitalism globally grapples with stakeholder concerns, environmental responsibilities, and social license to operate, GSFC's six-decade experience balancing these tensions offers valuable insights.

The company's future trajectory will likely mirror India's own development path—steady rather than spectacular, resilient rather than revolutionary, focused on self-reliance rather than global dominance. GSFC won't become India's BASF or DowDuPont. But it will remain what it has always been—a bridge between India's agricultural past and industrial future, a provider of essential products that enable development, and a testament to the power of patient, purposeful capital.

For fundamental investors, GSFC represents a specific type of opportunity—not growth at any price, but value with a margin of safety. The company trades at reasonable multiples, generates predictable cash flows, maintains a strong balance sheet, and possesses strategic assets whose replacement value exceeds market capitalization. In a market increasingly dominated by narrative and momentum, GSFC offers something increasingly rare—substance.

The story of Gujarat State Fertilizers & Chemicals is far from over. As India pursues its ambitious goals—doubling farmer incomes, achieving manufacturing self-reliance, transitioning to clean energy—GSFC will play a supporting but crucial role. The company that helped enable India's Green Revolution now positions itself for the sustainability revolution. The manufacturer that achieved import substitution in chemicals now eyes export leadership. The PSU that survived liberalization now thrives in competition.

In the end, GSFC's greatest achievement might be its very survival and steady prosperity through six tumultuous decades of Indian economic history. From socialist planning to liberalization, from protection to competition, from scarcity to abundance, GSFC adapted without losing its core purpose—enriching lives through chemistry. That purpose, more than any financial metric or strategic position, explains why Gujarat State Fertilizers & Chemicals remains relevant after 60 years and why it will likely remain so for decades to come.

The boring business of making fertilizers and chemicals, it turns out, is anything but boring when viewed through the lens of nation-building, industrial strategy, and long-term value creation. GSFC's journey from the agricultural fields of Gujarat to the specialty chemical markets of the world encapsulates India's own transformation. And like India itself, GSFC's best chapters may still lie ahead.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube