Groww (Billionbrains): The Platform that Ate Indian Finance

I. Introduction: The "New India" Retail Revolution

In the autumn of 2023, something quietly extraordinary happened on the servers of the National Stock Exchange. A seven-year-old startup, founded by four former Flipkart employees working out of a modest Bengaluru office, overtook Zerodha—the undisputed king of Indian discount broking—to become the country's largest stockbroker by active clients.

Groww had 6.63 million active users on the NSE by the end of September, edging past Zerodha's 6.48 million. The margin was thin, barely two percent, but the symbolism was enormous.

Zerodha had built its throne over more than a decade, pioneering flat-fee trading in India and earning a reputation as the broker that every retail trader trusted. Its founders, Nithin and Nikhil Kamath, had become folk heroes of Indian fintech—bootstrapped billionaires who never raised a rupee of venture capital. Groww had arrived at the same summit in less than half the time, burning through hundreds of millions in venture funding to get there. The question that reverberated through Dalal Street was simple: was this a flash in the pan, or a permanent changing of the guard?

The company behind Groww is formally called Billionbrains Garage Ventures—a name that sounds more like a Bangalore co-working space than the custodian of tens of millions of Indian investment accounts. But the name reflects the founders' self-image: builders, tinkerers, garage-startup romantics who believed they could rewire how an entire nation saves and invests.

Their playbook was deceptively simple, yet fiendishly difficult to replicate. Start with a zero-revenue product—free direct mutual funds—that incumbent banks could not afford to match without destroying their own businesses. Use that product as a customer acquisition funnel of breathtaking efficiency, building trust before building revenue. Layer on stock trading, lending, payments, and asset management once the user base was locked in. And when the time came to go public, pay the United States government a staggering $160 million in exit taxes just for the privilege of moving the parent entity back to India, signaling to the world that this was always going to be an Indian story.

By November 2025, when Billionbrains listed on the NSE at a 30 percent premium to its issue price of one hundred rupees per share—closing its first day at about 131 rupees and nearly doubling within a week—the market was effectively answering a question that had hung over the company for years. Is Groww merely a brokerage? Or is it the first true financial super app for the Indian middle class?

The IPO was subscribed 17.6 times over, with institutional investors bidding 22 times their allocation and retail investors nearly 9.5 times. The valuation at listing crossed $8.9 billion, suggesting the market was betting heavily on the platform thesis rather than the brokerage thesis.

Consider the scale for a moment. With nearly 70 million registered users, over 12 million active demat accounts, a lending arm growing at over 30 percent quarter-on-quarter, a freshly minted asset management company backed by State Street Global Advisors, and a wealth management subsidiary acquired for $150 million, Groww was no longer just a trading app. It was becoming a platform—and the distinction matters enormously for how one ought to think about the next decade of this business.

On the morning of November 12, 2025—listing day—the scene at Groww's Bengaluru headquarters reportedly had the nervous energy of a wedding. Employees gathered around screens. The four founders, who had quit Flipkart nine years earlier with little more than a shared conviction that Indian investing was broken, watched as the ticker symbol GROWW appeared on the NSE for the first time. The stock opened at 128.50 rupees, a healthy premium to the issue price, and kept climbing. By the close of that first week, the stock was trading near 200 rupees. The market was not just pricing a brokerage. It was pricing a possibility.

A brokerage earns transactional revenue that rises and falls with market volumes. A platform earns annuity-like revenue from a deepening relationship with each customer. The difference in terminal value between those two models is vast.

To understand why Groww is positioned to be the latter, one has to go back to the beginning. Not to a boardroom strategy session, but to a village in Madhya Pradesh, to the corridors of IIT Bombay, and to the peculiar culture of India's first great e-commerce company.

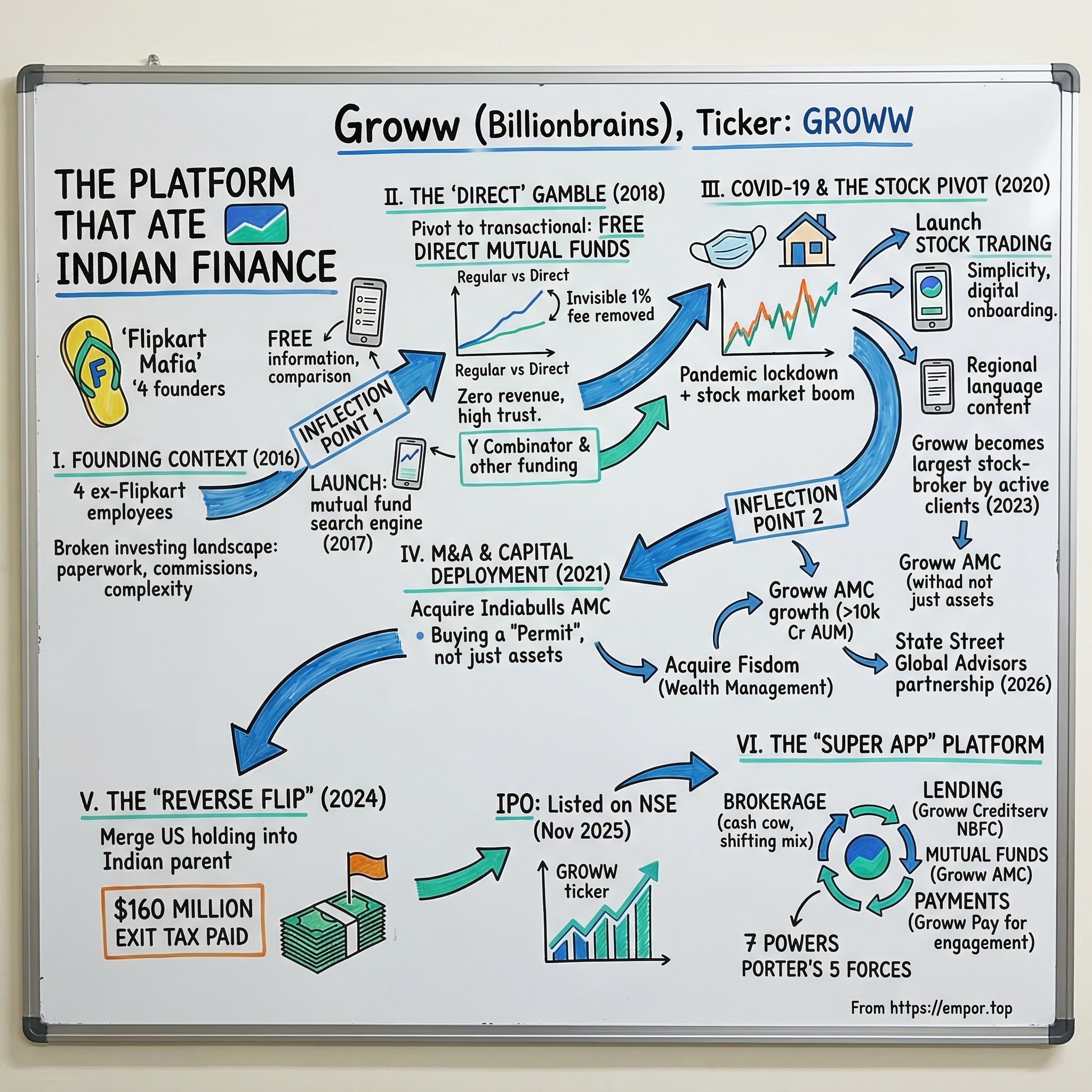

II. The Flipkart Mafia and the Founding Context

Lalit Keshre grew up in Lepa, a remote village in Madhya Pradesh, the son of a farmer. There was no English-medium school in the village, so his parents made the difficult decision to send him to live with his grandparents in the town of Khargone, where the schools were marginally better. It was the kind of sacrifice that millions of Indian families make—uprooting a child from home so they can have a shot at a different kind of life.

Keshre was, by every available account, a relentlessly curious student—the kind who cracks the IIT-JEE entrance exam not because of expensive coaching classes but because of sheer intellectual stubbornness. He made it to IIT Bombay, where he completed both a bachelor's and a master's degree in electrical engineering, specializing in microelectronics. The farmer's son from Lepa had earned a seat at one of the most competitive institutions on earth.

After graduating, Keshre spent seven years at Ittiam Systems, a Bangalore-based semiconductor design company, working on product and engineering. It was solid, respectable work, but the entrepreneurial itch was growing.

In 2011, he tried his hand at building something of his own for the first time, co-founding Eduflix, an edtech platform that aimed to bring video-based learning to Indian students. The timing was brutally poor. India's broadband penetration was still nascent, smartphone adoption was years away from its inflection point, and funding for consumer internet companies was scarce. Eduflix shut down in 2013.

It was a painful education—the kind that leaves scar tissue on the psyche of an entrepreneur—but it left Keshre with a crucial instinct that would later define Groww: the product has to be so simple that the infrastructure almost does not matter. If you are building for India, you cannot assume fast internet, large screens, or financial literacy. You have to assume nothing and design for everything.

He joined Flipkart in 2013, during the company's hypergrowth phase, becoming one of its early product managers. There he helped launch Flipkart Quick and contributed to the Flipkart Marketplace product. But more importantly than any specific project, he absorbed the Flipkart culture—an obsessive focus on user experience, a willingness to subsidize growth with venture capital, and the conviction that if you could make something ten times easier than the existing alternative, the market would come to you.

Flipkart did not merely sell products online; it had to build the entire infrastructure of Indian e-commerce from scratch—logistics, payments, cash-on-delivery, vernacular interfaces. That experience taught Keshre that in India, the product is not just the software. The product is the entire experience, from the first Google search to the moment money settles in your account.

It was at Flipkart that he met the three colleagues who would become his co-founders, and together they formed one of the most complementary founding teams in Indian startup history.

Harsh Jain, who would become Groww's Chief Operating Officer, was part of Flipkart's product management team. He held a B.Tech and a Master's in Information and Communication Engineering from IIT Delhi, and an MBA from UCLA Anderson. Jain brought a rare combination that most startups lack: deep technical product thinking layered with business-school rigor around growth levers, unit economics, and market sizing. He was the kind of operator who could move fluidly between whiteboarding a product feature with engineers and building a financial model for the board.

Neeraj Singh, the future CTO, was an engineering manager at Flipkart who had built the company's customer returns and refund system—one of those unglamorous but mission-critical products that teaches an engineer everything about building for scale, handling edge cases, and maintaining reliability when millions of transactions are flowing through the pipes. Singh held a degree from ITM Gwalior and a postgraduate diploma in advanced computing from CDAC. He was the quiet builder of the group, the one who would make sure the technology never broke even as user growth went parabolic.

Ishan Bansal, the future CFO, came from Flipkart's corporate development team and had also worked in mergers and acquisitions at Naspers, the South African media conglomerate that was one of Flipkart's major investors. A BITS Pilani graduate with an MBA from XLRI Jamshedpur and a CFA charter, Bansal was the financial architect of the group—the one who understood valuation, deal structure, regulatory capital, and the complex dance of raising money from global investors while navigating Indian financial regulations. His M&A experience at Naspers, where he would have seen how large platform businesses are valued and how strategic acquisitions create compounding returns, would prove instrumental in Groww's later capital deployment decisions.

In 2016, all four quit Flipkart. The decision was not made lightly—Flipkart was at the time the most prestigious technology company in India, and all four held senior positions with generous stock options that would later be worth a fortune when Walmart acquired Flipkart for $16 billion in 2018. Walking away from that was a bet not just on an idea, but on each other.

The insight that brought them together was deceptively simple: investing in India was broken.

Opening a brokerage account required physical paperwork that could take weeks. Mutual fund distributors pushed "regular" plans loaded with commissions that ate into returns. The language of finance—NAVs, expense ratios, Sensex points, alpha, beta—was intimidating for anyone who had not grown up around money. Only about four crore Indians had demat accounts at the time, in a country of 1.3 billion. Think about that ratio: roughly three percent of the population had any formal mechanism to participate in the wealth creation that equity markets offer. The gap between the number of people who could benefit from investing and the number who actually did was vast, and it was not a gap of desire but of access and comprehension.

Groww launched in April 2017 with a small team operating out of a co-working space in Koramangala, Bengaluru's startup heartland—the same neighborhood that had incubated Flipkart, Ola, and dozens of other Indian tech companies. But unlike those companies, which launched with ambitious platforms and aggressive growth targets, Groww started with something deliberately modest.

It was not a brokerage. It started as a mutual fund search engine—a simple tool that helped people compare funds, understand what they were looking at, and demystify the jargon. No transactions, just information.

It was the internet equivalent of a friendly neighbor who happens to know about finance, sitting down with you over tea and explaining what an SIP is. Think of it as Yelp for mutual funds—reviews, ratings, comparisons—without the ability to actually make a purchase. The founders understood something that most fintech companies missed: before you can sell someone a financial product, you have to make them feel that they are not stupid for not already understanding it. The emotional barrier to investing in India was not price; it was shame.

The initial traction was modest—the app had between 5,000 and 10,000 downloads in its first months—but the engagement was deep and the ratings were stellar, hitting 4.9 on Google Play. Users kept coming back. They trusted the platform because it was not trying to sell them anything.

And that trust would soon become the most valuable asset the company owned—far more valuable than any brokerage license. What the founders had built, without fully realizing it yet, was a distribution moat disguised as an information product.

III. Inflection Point 1: The "Direct" Gamble

In early 2018, Groww made the decision that would define its trajectory for the next decade. The company pivoted from being a mutual fund information portal to a transactional platform offering direct mutual fund investments. To understand why this was audacious—and why it terrified the incumbents—one has to understand the economics of mutual fund distribution in India, a business model so profitable and so deeply entrenched that disrupting it required a kind of strategic judo.

Here is how mutual fund distribution works in India, stripped to its essentials.

When an investor buys a "regular" mutual fund plan through a bank or distributor, the fund house pays the distributor a trail commission—typically around one percent of the invested amount, every single year, for as long as the investor stays in the fund. On a portfolio of one crore rupees, that is one lakh per year flowing to the distributor for doing essentially nothing after the initial sale. This commission is baked into the fund's expense ratio, which means the investor pays for it through lower returns, but most investors never notice because the fee is invisible—it is deducted from the fund's NAV before the investor ever sees their statement.

India's banks and wealth managers had built enormous, deeply profitable businesses on this model. ICICI Direct, HDFC Securities, Axis Direct, SBI's distribution arm—these institutions earned hundreds of crores annually from mutual fund distribution commissions alone. It was a beautiful business: high margins, recurring revenue, and a customer base that was largely unaware of the toll being extracted.

Direct plans, introduced by SEBI in 2013, eliminated the distributor commission entirely. They were identical to regular plans in every way—same fund manager, same portfolio, same strategy—except that the expense ratio was lower by roughly one percent, because no commission was being paid out.

Here is an analogy that makes the math visceral.

Imagine two identical highway lanes going to the same destination at the same speed, but one has a toll booth that takes one percent of your fuel every kilometer, and the other is completely free. Over a short trip, you barely notice the difference. Over a twenty-year journey, the difference is staggering. And here is the critical detail: the toll booth is invisible. The fuel is deducted from your tank automatically, so you never see the bill. You just arrive at your destination with less fuel than you expected, and you never quite understand why. An investor putting ten thousand rupees per month into a fund earning twelve percent annually would accumulate roughly one crore in a regular plan, but nearly 1.2 crores in a direct plan. That twenty-lakh difference—twenty lakh rupees of wealth that simply evaporated into distributor commissions—was, in effect, the hidden price of the banker's smile.

Groww offered these direct plans for free. No commissions, no platform fees, no hidden charges. The company earned zero revenue from this product. Every single user who invested through Groww was, from a financial perspective, a pure cost center. The founders were spending venture capital money to acquire customers who generated no income.

In January 2018, Y Combinator invested in Groww's seed round, followed by a $1.6 million pre-Series A in July 2018. That capital was being deployed not to build revenue, but to build a user base.

This was, on its face, insane. But it was also brilliant, and the logic reveals the Flipkart DNA in Groww's thinking. What Groww was actually doing was buying relationships at a fraction of the cost that traditional customer acquisition would require. A bank might spend thousands of rupees acquiring a new wealth management client through advertising, branch visits, physical forms, and relationship managers. Groww was acquiring users for almost nothing, because the product itself was the marketing. Tell a friend that they can save one percent per year on their mutual fund investments simply by switching to an app, and that friend tells two more friends. The viral coefficient was extraordinary precisely because the value proposition was so clear and so obviously in the user's interest.

The incumbents—ICICI Direct, HDFC Securities, and the rest—could see what Groww was doing, but they could not respond. Their mutual fund distribution businesses generated real, immediate revenue that flowed directly to the bottom line. Cannibalizing that revenue by promoting direct plans would have been corporate suicide—imagine the wealth management head at ICICI walking into a board meeting and saying, "I'd like to propose that we eliminate a few hundred crores of annual revenue."

It was a textbook case of what Clayton Christensen called the innovator's dilemma: the thing that makes you profitable today prevents you from adapting to the thing that will make you irrelevant tomorrow. The banks were trapped by their own success, paralyzed by an inability to respond without destroying their existing economics.

By the end of 2019, Groww had accumulated millions of users invested in direct mutual funds. The company was burning cash, but the user acquisition cost was plummeting as word-of-mouth drove organic growth. The Groww app had become the default recommendation in personal finance forums, Reddit threads, and YouTube comment sections across India. When someone asked "how do I start investing?" the answer increasingly was: "Download Groww."

The mutual fund product had served its purpose perfectly. It had created an enormous, engaged, trusting user base that was now ready to be offered something with actual revenue potential—stock trading. The bait had been set. The hook was about to follow. And the timing of what came next was, depending on your perspective, either the luckiest break in Indian fintech history or the most prescient bet.

IV. Inflection Point 2: COVID-19 and the Stock Pivot

In the first half of 2020, as India locked down and the world plunged into pandemic uncertainty, Groww launched stock trading on its platform.

Picture the scene: millions of young professionals confined to their apartments, earning full salaries but unable to spend on travel, dining, entertainment, or the weekend chai at the corner stall. Savings accounts were swelling. The stock market, after a terrifying 40 percent crash in March 2020, began a recovery so dramatic and so sustained that it would become the defining financial event for a generation of Indian investors. The Sensex, which had bottomed near 25,600 in March, would cross 50,000 by February 2021 and breach 60,000 by September.

Social media and YouTube exploded with content about investing—some of it genuinely educational, much of it wildly speculative, all of it generating a tidal wave of interest among a demographic that had never seriously considered the stock market before.

India was not unique in this regard—the same phenomenon was playing out in the United States with Robinhood, in South Korea with Kakao Stock, and in Brazil with NuInvest. But the Indian version of this story had a scale that dwarfed its global counterparts. India had 1.4 billion people, a median age of 28, rapidly improving internet infrastructure thanks to Jio's data revolution, and a stock market that was outperforming every major global benchmark. The conditions for a retail investing explosion were more favorable than anywhere else on earth.

Into this perfect storm, Groww launched a stock trading product that was purpose-built for first-time investors. The design philosophy was radical simplicity.

Where Zerodha's Kite platform was designed for serious traders—dense with candlestick charts, order books, technical analysis overlays, and the kind of interface that a day trader would love but a first-timer would find terrifying—Groww looked more like a consumer social app. The colors were softer. The typography was larger. Buying a stock felt as intuitive as ordering food on Swiggy or booking a ride on Uber. The company had deliberately "Tinder-fied" finance: swipe, tap, done.

The onboarding process was entirely digital, completed in minutes using Aadhaar-based eKYC. There were no account opening charges, no annual maintenance fees. Every friction point that legacy brokers had tolerated for decades—because their existing customers tolerated it—was ruthlessly eliminated.

But the product was only half the story. The other half was distribution, and here Groww made a bet that its competitors underestimated: regional-language content.

The insight was that India's next hundred million investors would not come from English-speaking metro cities—those users had largely already been captured by Zerodha and the legacy brokers. The real opportunity was in Tier 2 and Tier 3 cities: Indore, Lucknow, Coimbatore, Jaipur, Patna—places where young people were digitally savvy but financially underserved, comfortable with smartphones but intimidated by stock market jargon delivered exclusively in English.

Groww invested heavily in educational content distributed through YouTube and social media channels in Hindi, Tamil, Telugu, Kannada, and other regional languages, breaking down concepts like SIPs, PE ratios, and index funds into language that felt accessible rather than academic. During the lockdowns, the company moved its educational workshops entirely online, conducting weekly live sessions with fund managers and industry CEOs that attracted hundreds of thousands of viewers. These were not sales pitches; they were genuine educational events that built trust and brand affinity at a scale that traditional advertising could never achieve.

The results were staggering. Groww experienced a 200 percent growth in first-time customers during the pandemic year. Within eight months of launching stock trading, the platform had over 780,000 active demat accounts and more than 8 million total users. In quick succession, the company layered on digital gold, ETFs, intraday trading, and IPO applications—each product designed to feel like a natural extension of what the user was already doing on the app, a philosophy that came directly from the Flipkart playbook of reducing the number of taps between intent and action.

The funding followed the growth with stunning velocity. In September 2020, Groww raised a $21.4 million Series C led by YC Continuity Fund. In April 2021, Tiger Global led an $83 million Series D that pushed the valuation past $1 billion, making Groww a unicorn. Just six months later, in October 2021, the company closed a massive $251 million Series E led by Iconiq Growth, with participation from Alkeon Capital, Lone Pine Capital, Sequoia Capital India, Ribbit Capital, YC Continuity, Tiger Global, and Propel Ventures. The valuation hit $3 billion. In less than two years, Groww had gone from a free mutual fund app with no brokerage revenue to one of India's most valuable fintech startups.

But the pandemic boom also planted a structural challenge that would become apparent later. Many of the millions of new investors flooding into the market were drawn not by long-term wealth-building but by the dopamine rush of short-term trading, particularly in futures and options—financial instruments that allow traders to bet on market movements with leveraged positions. SEBI data would later reveal that roughly nine out of ten individual F&O traders lost money.

This created a user base that was large but potentially shallow—highly engaged in a bull market, potentially transient in a downturn.

For context on just how distorted the F&O market had become: by the peak in late 2023, India's National Stock Exchange was processing more options contracts daily than any exchange on earth—more than the Chicago Board Options Exchange, more than Nasdaq. Much of that volume was coming from retail traders, many of them young, many of them new, many of them treating weekly options expiries like a lottery ticket. The average holding period for an F&O contract on Indian exchanges was measured in hours, not days.

The founders recognized this risk early, which is why even as the brokerage business was exploding, they were already planning the acquisitions and product launches that would diversify the revenue base beyond transactional trading income. The goal was to ensure that when—not if—the regulatory hammer fell on derivatives, Groww would have enough alternative revenue streams to absorb the blow.

V. M&A and Capital Deployment: The Indiabulls "License" Play

In May 2021, while the funding euphoria was still in full swing, Groww announced a deal that puzzled many financial analysts. It agreed to acquire Indiabulls Asset Management Company and its associated trustee company for 175 crore rupees. The immediate reaction was bewilderment.

Indiabulls Mutual Fund was, to put it charitably, a minor player in a market dominated by giants like SBI, HDFC, and ICICI Prudential. Its quarterly average assets under management had shrunk to about 664 crore rupees by March 2021, down from 921 crore just three months earlier. The fund house was bleeding assets, losing investor confidence, and shrinking in an industry that was otherwise growing rapidly.

By the usual valuation benchmarks for AMC acquisitions in India—which typically happen at five to seven percent of AUM—the price should have been somewhere between 33 and 46 crore rupees. Groww was paying more than 25 percent of AUM. By traditional math, they were overpaying by a factor of four or five.

But Groww was not buying assets. It was buying a license. This distinction is absolutely critical to understanding the strategic logic of the deal.

India's mutual fund industry operates under tight regulatory control. The Securities and Exchange Board of India requires any entity that wants to launch and manage mutual fund schemes to hold an AMC license, and obtaining one from scratch requires meeting stringent eligibility criteria for sponsors—criteria that involve minimum capital adequacy, a track record of financial stability, and regulatory approvals that can take years to secure. For a startup—even a well-funded, fast-growing one—the process of obtaining a fresh AMC license was uncertain in both timeline and outcome.

Think of it this way: in a city where building permits take five years and cost a fortune in legal fees, Groww found a dilapidated building with a valid permit and bought the building not for the bricks, but for the permit. The bricks—the shrinking AUM, the underperforming fund schemes, the departing investors—were irrelevant. The permit was everything.

By acquiring Indiabulls' AMC, Groww became the first fintech company to enter the asset management space in India, taking advantage of SEBI's newly liberalized sponsor eligibility criteria. It was a pioneer in a regulatory opening that every other fintech would later try to follow.

The regulatory process was slow even for an acquisition. The Competition Commission of India approved the deal in September 2021, but the transaction did not formally close until May 2023—nearly two years after announcement. During that waiting period, the Indiabulls fund house continued to hemorrhage assets.

But the moment Groww took control, something remarkable happened.

The company activated what one might call its "nudge engine"—the same behavioral design expertise that had made its mutual fund distribution platform so effective at converting browsers into investors. Groww now had over 20 million users on its app, many of them already investing in mutual funds through the distribution platform using third-party fund houses. All Groww had to do was give those users a gentle push toward its own fund house's products.

Not aggressively, not deceptively, but through the subtle architecture of choice: featuring Groww AMC's index funds and Nifty 50 trackers prominently in the app's discovery flow, offering them as default options in SIP recommendations, building thematic funds around concepts—like technology or manufacturing—that resonated with the platform's young, growth-oriented user base.

The results were dramatic. From about 664 crore in AUM at the time of announcement, Groww AMC grew to over 10,000 crore in AUM by 2025—roughly a fifteen-fold increase in just two years of active management. The fund house now runs more than 50 schemes across equity, debt, hybrid, and index categories. It serves over 1.2 million unique investors. What looked like an absurd overpayment in 2021 turned out to be one of the shrewdest acquisitions in Indian fintech history.

The 175 crore was not the price of an asset management company. It was the price of a manufacturing license that allowed Groww to capture the full value chain of an investor's financial life—from discovery to distribution to asset management—and to earn fees at every step of that chain.

In January 2026, that strategic logic was validated in spectacular fashion. State Street Global Advisors—one of the world's largest asset managers with over $4 trillion under management, the firm behind the legendary SPDR family of ETFs—announced it would acquire a 23 percent stake in Groww AMC for 580 crore rupees.

The deal combined 381 crore in secondary share purchases with about 199 crore in fresh primary capital. State Street's voting rights were capped at 4.99 percent, meaning this was a financial and strategic investment rather than a control play. Yie-Hsin Hung, CEO of State Street Investment Management, said the partnership would allow State Street to "participate directly in the growth of India's domestic asset management market" and build a pipeline of Indian investment exposures for global distribution.

The message was unmistakable: a global asset management giant, with more experience in passive investing than perhaps any firm on earth, was betting that Groww's distribution platform was the right vehicle to reach India's next hundred million mutual fund investors.

VI. The "Reverse Flip" and the $160 Million Tax Bill

The story of Groww's corporate structure is one of the most dramatic chapters in the broader narrative of Indian startups coming home—a tale of regulatory pragmatism, painful financial sacrifice, and the ultimate bet on India's capital markets.

When Groww was founded in 2016, the standard playbook for an Indian startup raising venture capital was to incorporate a holding company in the United States—typically in Delaware—and make the Indian operating entity a subsidiary. This was not about tax avoidance or lack of patriotism. It was simply practical.

US-incorporated entities offered legal frameworks that were more familiar to Silicon Valley investors: standardized shareholder agreements, well-understood exit paths through US listings or acquisitions, and Delaware corporate law that had been refined through decades of venture capital practice. Every major Indian startup of that era—Flipkart, Ola, Freshworks, Razorpay—followed the same model. It was the cost of admission to the global venture capital game.

Groww Inc, the US holding company, was the entity that raised capital from Y Combinator, Tiger Global, Sequoia Capital India, and the rest. Billionbrains Garage Ventures, the Indian entity, was the subsidiary that actually built and operated the product, held the regulatory licenses, and served Indian customers. For the first several years, this structure was invisible to users and largely irrelevant to the business.

But as Groww matured and began contemplating a public listing, the structure became a serious problem. Indian regulations, particularly those governing financial services companies, were tightening around foreign ownership structures. SEBI, the RBI, and the government were all signaling that they preferred Indian-domiciled entities for companies operating critical financial infrastructure. An IPO on the NSE or BSE would require the listed entity to be Indian. And Groww's entire future—its regulatory relationships, its user base, its growth trajectory, its identity—was inextricably Indian.

In May 2024, Groww completed its "reverse flip," merging the US holding company into the Indian parent. Billionbrains Garage Ventures became the sole registered entity, headquartered in Bengaluru. The corporate structure now matched the operational reality.

The mechanics of a reverse flip are worth understanding because they explain why so few Indian startups have actually done it, despite years of talk about "coming home." The process involved shareholders of Groww Inc (the US entity) exchanging their shares for equivalent shares in Billionbrains Garage Ventures (the Indian entity). Every investor—Y Combinator, Tiger Global, Sequoia, Iconiq—had to agree to swap their Delaware-incorporated shares, with all their familiar legal protections, for shares in an Indian private limited company governed by Indian corporate law. This required extensive negotiations, legal restructuring, and regulatory approvals from both US and Indian authorities. It was not a form you fill out; it was a multi-month legal operation involving dozens of law firms across two continents.

But the financial cost was what made the headlines.

Under US tax law, the dissolution of a Delaware entity and the transfer of its assets to a foreign successor triggers capital gains tax based on the fair market value of those assets at the time of transfer. Even though Groww's last private-market valuation of $3 billion from the 2021 Series E had likely declined in the subsequent tech downturn—reports suggested the reverse flip was executed at a valuation more than 30 percent lower than the peak—the tax bill was still massive.

Groww paid approximately 1,340 crore rupees, or about $160 million, to the US Internal Revenue Service.

The scale of this payment is worth pausing on because it reveals something important about the founders' conviction. At the time, Groww's annual revenue was roughly 3,100 crore rupees. The tax bill represented more than 40 percent of a full year's revenue—money that generated no assets, no growth, no competitive advantage. It was purely the cost of unwinding a corporate structure that had been necessary to raise the capital that built the company in the first place.

Imagine paying 40 percent of your annual salary to the government of a country you are leaving, just so you can go home. The founders did not flinch. They understood that this was the toll on the bridge to a public listing in India, and that the long-term value of being an Indian-listed company—with access to domestic institutional capital, regulatory credibility, the ability to acquire Indian financial services firms without cross-border complications, and a listing premium that reflected the company's actual market—far exceeded the one-time cost.

The reverse flip also created an accounting quirk that confused some observers. In FY24, Groww reported a net loss of 805 crore rupees, despite underlying operating performance that was strongly profitable. The loss was almost entirely attributable to the one-time tax provision related to the domicile shift. For anyone glancing at the headlines—"Groww reports 805 crore loss"—it looked like a company bleeding money.

The reality was the opposite. Strip out that charge, and the company was generating healthy operating profits. This became immediately apparent in FY25, when reported profit after tax swung dramatically to 1,824 crore on total income of 4,062 crore—a 45 percent net margin that would make most financial services companies envious, and an EBITDA margin of nearly 59 percent that reflected the extraordinary operating leverage of a technology-driven platform.

The reverse flip was the essential precursor to the November 2025 IPO. It was not just an administrative exercise. It was a statement of intent, the most expensive statement of intent in Indian startup history: Groww's future was in India, its capital base would be Indian, and its listing would put it in front of the domestic investors who were, quite literally, its customers.

VII. The "Hidden" Businesses and Segment Analysis

Walk into any gathering of Indian equity analysts, and the conversation about Groww inevitably starts and ends with brokerage. In some ways, this is understandable. Brokerage income accounts for roughly 70 to 72 percent of the company's revenue, and in Q3 FY26—the most recent quarter as of this writing—revenue from operations hit 1,216 crore, up 25 percent year-over-year. Total income including other income reached 1,261 crore.

The brokerage business is the cash cow, the revenue engine, the thing that makes the income statement work. But focusing exclusively on brokerage is like analyzing Amazon in 2005 by looking only at book sales. The interesting parts of Groww are the businesses that most people have not yet bothered to understand—and those businesses are what will determine whether the company's valuation is justified over the next decade.

Start with the brokerage itself, because even here the story is more nuanced than it appears. Groww's market share in cash equities expanded to a record 28.8 percent in Q3 FY26, up from 21.6 percent a year earlier—a seven-percentage-point gain that is remarkable for a market this competitive. Its derivatives market share rose to 18.1 percent from 12.2 percent. Its mutual fund distribution market share climbed from 12.3 percent to 13.7 percent. The transacting user base—meaning people who actually executed at least one trade or investment during the quarter—crossed 2 crore (20 million), growing about 25 percent year-on-year.

But the revenue mix within brokerage is shifting in ways that matter. Equity derivatives, which accounted for 68 percent of total income a year ago, declined to 57 percent in Q3 FY26. Management has explicitly guided that derivatives will slip below 50 percent of the revenue mix over time.

This is partly a strategic choice—the founders do not want to be dependent on a single volatile revenue stream—and partly a regulatory reality. SEBI's crackdown on futures and options trading, which included increasing minimum contract sizes from the five-to-ten lakh range to fifteen lakh, limiting weekly expiry contracts to one per exchange, and encouraging exchanges to eliminate volume-based discounts, removed nearly 200 crore of annualized revenue from Groww's top line. The government's decision in July 2024 to increase the securities transaction tax on F&O trades by approximately 60 percent added further headwinds.

Q3 FY26 profit after tax fell 28 percent year-on-year to 547 crore despite the revenue increase. However, the year-ago quarter had included a one-time long-term incentive payout recognition that inflated the base; adjusting for that, underlying profit grew about 24 percent. This is an important nuance that the headline numbers can obscure.

Now for the hidden businesses.

The most important alternative revenue stream is lending, operated through Groww Creditserv Technology, a non-deposit-taking NBFC that received its RBI license in December 2022. As of March 2025, the loan book stood at approximately 1,093 crore, and more recent figures suggest it has grown to roughly 1,250 crore.

The product mix includes personal loans—the bread and butter—and a newer product called Loans Against Securities, which allows investors to borrow against their stock or mutual fund portfolios without selling them. LAS accounted for nearly a third of new disbursements by Q2 FY26, with around 9,800 customers using the product.

Think of Groww's lending business like this: the company already knows everything about its borrowers—their income patterns (from trading activity), their net worth (from portfolio values), their savings discipline (from SIP consistency), and their risk appetite (from trading behavior).

This is an underwriter's dream. A traditional bank evaluating a personal loan application sees a credit score, a salary slip, and perhaps a bank statement. Groww sees the full financial picture: how much the borrower saves each month, whether they have been disciplined about their SIP contributions, what their portfolio is worth, and whether their trading behavior suggests prudence or recklessness. The result is lower credit costs, higher approval rates, and better portfolio quality compared to traditional personal lending.

The lending NBFC is still small—contributing roughly 6 percent of consolidated revenue—but it is the highest-margin business in the Groww ecosystem and has the longest runway for growth. If Groww can scale this to even 15-20 percent of revenue over the next three to four years, it would meaningfully change the earnings profile of the consolidated entity.

The Margin Trading Facility, launched in April 2024, has already grown to account for about 5 percent of revenue. MTF allows investors to buy stocks with borrowed money, paying interest on the borrowed portion. The MTF loan book stands at roughly 1,668 crore, capturing a 1.7 percent market share in a segment that was previously dominated by established brokers. Volumes surged 60 percent in Q2 FY26.

Groww AMC, discussed in the previous section, now manages over 10,000 crore in assets across more than 50 schemes, with the State Street partnership bringing global expertise in passive and thematic investing. Management fees on mutual funds are individually modest—typically 50 to 100 basis points of AUM annually—but they are annuity-like: they accrue as long as the money stays invested, regardless of whether the market goes up or down.

Then there is Groww Pay—the UPI and bill payment layer that most analysts dismiss as an afterthought. Users can make peer-to-peer transfers, pay utility bills, recharge mobile phones, and handle loan repayments within the Groww app. This generates negligible direct revenue, but it serves a critical strategic purpose: it transforms Groww from an app you open once a month to check your portfolio into an app you open several times a week.

Daily engagement is the moat that makes every other product cross-sell possible. A user who pays their electricity bill on Groww is more likely to start an SIP on Groww. A user who sees their portfolio balance every time they pay a bill is more likely to add to their investments. This is the same playbook that made WeChat indispensable in China—not because any single feature was irreplaceable, but because the aggregate convenience of having everything in one place created a gravitational pull that no specialized competitor could overcome.

The payments space in India is brutally competitive—PhonePe, Google Pay, and Paytm dominate UPI transactions with hundreds of millions of users each. Groww is not trying to win the payments war outright. It is using payments as a strategic wedge to increase the frequency of app opens from "once a month when I check my portfolio" to "several times a week when I pay my bills." That frequency delta is worth far more than whatever interchange revenue the payments product generates directly.

Finally, the acquisition of Fisdom in October 2025 for approximately 961 crore rupees added a wealth management capability targeting high-net-worth individuals and affluent investors. Fisdom brought over 10,000 crore in assets under advisory, more than a million clients, and 500 employees including 180 in sales spread across 15 offices. Groww subsequently injected an additional 104 crore into Fisdom and launched a new wealth management offering called "W" for the affluent segment.

This marked a crucial strategic recognition: the ultra-low-cost digital model that works brilliantly for mass retail may not be sufficient for clients with more complex needs—those with portfolios above 50 lakh who want advisory-driven solutions, tax optimization, and portfolio management services that require a human touch.

The revenue mix today tells one story. The strategic architecture tells another. Groww is building a platform where every financial need of an Indian household—saving, investing, trading, borrowing, paying, insuring, and wealth planning—can be addressed within a single ecosystem. Whether the market prices this as a brokerage or as a platform will be the single biggest driver of shareholder returns over the next five years.

VIII. Management and Incentives

One of the most telling details about Groww's founders is what they did not do at the IPO.

When Billionbrains listed in November 2025 with a fresh issue of 1,060 crore and an offer for sale of approximately 5,572 crore—making it one of India's largest fintech IPOs—the four co-founders collectively sold shares worth only a token amount. On a company valued at $8.9 billion, this was essentially nothing.

All four retained the vast majority of their holdings, collectively owning approximately 27.8 percent of the post-IPO equity. Lalit Keshre held 9.13 percent, Harsh Jain 6.72 percent, Neeraj Singh 6.26 percent, and Ishan Bansal 4.53 percent. Furthermore, the promoters committed 20 percent of their shareholding to a lock-in period of one and a half years post-listing, a period that does not expire until mid-2027.

In a market where founder sell-downs during IPOs have become a frequent source of investor skepticism—where the question "if the founders are selling, why should I be buying?" is asked with increasing frequency—this level of retained ownership sent an unambiguous signal. The founders were not cashing out at the first opportunity. At Keshre's 9.13 percent stake, his holding was worth approximately 9,000 crore at listing—making the farmer's son from Lepa, Madhya Pradesh, a dollar billionaire. And he kept virtually all of it in Groww stock.

The leadership structure reflects a clear and functional division of labor that has remained remarkably stable since founding.

Keshre, as CEO, sets the strategic direction—he is the one who decided to enter mutual fund manufacturing, to pursue the reverse flip, to target the mass-market retail investor, and to pay the $160 million tax bill. He is described by colleagues and journalists who have profiled him as quiet, intensely focused, and obsessively product-oriented—more engineer than salesman, more architect than evangelist. He is not the face of Groww in the way that Nithin Kamath is the face of Zerodha; he is the mind behind the machine.

Harsh Jain, as COO, runs the day-to-day operations and growth machinery—user acquisition, marketing, partnerships, and the commercial side of each product launch. His IIT Delhi engineering background combined with the UCLA MBA gives him a vocabulary that translates between the product team and the board room.

Neeraj Singh, as CTO, owns the technology stack that processes millions of transactions daily with the reliability that a financial services platform demands. When Groww's app handles the rush of an IPO allotment day—when millions of users simultaneously check their allotment status—it is Singh's architecture that keeps the servers from buckling.

And Ishan Bansal, as CFO, manages the financial engineering—the fundraising, the M&A structuring, the regulatory capital allocation, the tax planning around the reverse flip—that has allowed the company to pursue an aggressive expansion strategy without losing financial discipline.

The compensation structure has generated some controversy that investors should understand. In FY24 and FY25, the company recorded significant one-time long-term incentive payouts for the founding team and key employees—expenses that were large enough to significantly distort quarterly comparisons. In January 2026, a proxy advisory firm pushed back on the company's ESOP proposals and board nomination structures, raising governance questions that are typical for newly listed founder-led companies.

The core question is whether these payouts represent a "founder tax"—a one-time recognition of the value created during the pre-IPO years, common in tech companies transitioning to public markets—or a pattern of excessive compensation that will persist and erode shareholder returns.

The founders would argue the former: they built a company worth nearly $9 billion while holding salaries low during the startup years, forgoing the kind of compensation that comparable executives at established financial services firms routinely earned, and the one-time payouts simply aligned their total compensation with value created. This is not an unusual pattern—Meta, Google, and countless other tech companies recorded massive stock-based compensation charges in the years surrounding their IPOs, and in each case the charges normalized over time.

The counter-argument is that public-market investors expect ongoing compensation to be reasonable and tied to forward-looking performance, not backward-looking value creation. The proxy advisory pushback in January 2026 suggests that institutional investors are watching this issue closely. Investors should monitor whether compensation normalizes in FY27 and beyond; if it does, the FY24-25 charges were indeed a one-time transitional event. If outsized compensation continues, it becomes a governance red flag that would warrant a higher discount rate on the company's future cash flows.

The workforce stood at approximately 1,415 employees as of June 2025, a number that has since increased to roughly 1,900 with the Fisdom acquisition. For a company managing 70 million registered users and processing millions of daily transactions, this employee-to-user ratio is remarkably lean—roughly one employee per 35,000 registered users. By comparison, traditional banks employ tens of thousands of people to serve similar customer counts. This speaks to the degree of automation and technology leverage in the platform, and it is one of Groww's most underappreciated competitive advantages.

IX. The Playbook: 7 Powers and Porter's 5 Forces

To assess whether Groww's competitive position is durable—or merely a product of favorable timing and abundant venture capital—it helps to apply two complementary frameworks: Hamilton Helmer's 7 Powers and Michael Porter's 5 Forces.

Begin with Helmer's framework, which asks a deceptively simple question: what is the source of persistent differential returns? In other words, why would Groww earn above-average profits for an extended period, and what prevents competitors from simply copying its model?

Groww exhibits at least three of the seven powers, and arguably a fourth.

Groww's most powerful strategic advantage is counter-positioning—a power that Helmer defines as a situation where the challenger adopts a superior business model that the incumbent cannot copy because doing so would damage their existing business.

When Groww launched free direct mutual funds in 2018, it offered a product that was objectively better for consumers—lower fees, higher long-term returns—that incumbent banks and wealth managers could not match without destroying their own commission revenue. ICICI Direct, HDFC Securities, and Axis Direct were earning hundreds of crores annually from distributing regular mutual fund plans. Matching Groww's free direct offer would have meant forfeiting that revenue overnight, with no guarantee of recapturing it through alternative channels.

This is classic counter-positioning: the incumbent's rational response to the challenger's strategy is to do nothing, because the cost of responding exceeds the cost of losing market share incrementally. It is the same dynamic that allowed Netflix to disrupt Blockbuster, or that allowed Southwest Airlines to take share from legacy carriers. The incumbents were not stupid; they were trapped by a business model that was too profitable to abandon. And by the time the market had shifted enough that they could no longer ignore direct plans, Groww had a multi-year head start and millions of loyal users.

This is perhaps the single most important strategic insight in the entire Groww story, and it explains why the company's early years of zero revenue were not a failure of monetization but a deliberate act of competitive positioning. The founders were not losing money; they were investing it in an advantage that no incumbent could match.

The second power is switching costs—and in financial services, these are both economic and psychological, compounding with every product a customer uses. Once an investor has their mutual fund SIPs running on autopilot, their stock portfolio with years of tax-lot history, their demat account linked to their bank, their personal loan being serviced, and their UPI payments flowing through a single app, the cost of moving is immense.

It is not just the mechanical effort of transferring accounts. It is the cognitive burden of re-establishing an entire financial identity elsewhere. The investment history, the tax records, the CAMS and NSDL linkages, the UPI handles, the nominee information, the auto-debit mandates—all of these create a web of dependencies that make switching feel far more daunting than it actually is. As Groww layers on more products, each additional product deepens the switching cost.

The third relevant power is cornered resources. Groww's founding team—four senior Flipkart alumni with deep expertise in consumer product design, engineering at scale, corporate finance, and growth marketing—represents a talent combination that is genuinely difficult to replicate. India has many capable engineers and many capable finance professionals, but the intersection of Flipkart-grade consumer product thinking with deep financial services domain knowledge is a narrow Venn diagram.

A fourth power—network effects—is emerging but not yet fully developed. As Groww adds more users, it generates more data about investment behavior, which improves its recommendation algorithms and credit underwriting models, which attracts more users and enables better lending decisions. Its AMC benefits from a larger distribution base, which allows it to launch more niche funds with confidence that they will attract sufficient AUM to be viable. The payments product creates a two-sided network where more users make UPI payments, which drives more daily engagement, which makes every other product cross-sell more effective. These network effects are still nascent, but if they compound over the next decade, they could create a self-reinforcing advantage that competitors will find very difficult to dislodge—similar to how Amazon's marketplace flywheel became nearly impossible to replicate once it reached critical mass.

Now apply Porter's 5 Forces.

The rivalry among existing competitors is intense and getting more so.

Zerodha remains a formidable rival—still the most profitable brokerage in India, with nearly 2,900 crore in net profit on roughly 6,900 crore of revenue in FY24, and a fiercely loyal user base that admires Nithin Kamath's bootstrapped, no-nonsense philosophy. Zerodha's Kite platform is still considered the superior tool for active traders, and its Coin platform for mutual funds has its own loyal following. The fact that Zerodha has never raised external capital gives it a different kind of credibility—it does not have to chase growth to satisfy venture investors, which means it can afford to be patient and disciplined in ways that Groww, with its public-market shareholders, cannot.

Angel One is aggressively expanding its user base and product suite, particularly strong in Tier 2 and Tier 3 cities where it has invested heavily in regional marketing. Upstox, backed by Tiger Global, competes on similar low-cost positioning. Newer entrants like Dhan, INDmoney, and Niyo are growing rapidly in niche segments—Dhan in particular has attracted serious traders with advanced charting tools and execution speed.

The threat of new entrants is the most important force to monitor—and potentially the most dangerous for Groww's long-term position.

Jio Financial Services, backed by Reliance Industries and its 470 million telecom subscribers, has launched the JioFinance super-app with ambitions spanning banking, lending, insurance, and investments. Its joint venture with BlackRock—Jio-BlackRock—directly targets the mutual fund manufacturing space. PhonePe, with over 500 million registered users on its UPI platform, is expanding into mutual funds, insurance, and lending.

These are not scrappy startups. They are platform behemoths with distribution advantages that dwarf Groww's 70 million registered users. The question is whether financial services markets are "winner-takes-all" or "winner-takes-most-in-its-niche." History in both India and globally suggests the latter: even in the United States, where Robinhood, Schwab, Fidelity, and Vanguard all compete vigorously, no single platform has captured more than a quarter of retail investors. HDFC Bank, India's largest private bank, still has only single-digit market share in most product categories. Financial services tend to be fragmented because trust is personal.

Buyer power is moderate—individual retail investors can switch platforms with relative ease if a competitor offers a meaningfully better experience or lower costs. The switching cost framework discussed above mitigates this to some extent, but it is worth noting that in a digital world, the "cost" of downloading a new app is zero. The real switching cost is not technical; it is emotional—the inertia of having your financial life organized in one place.

Supplier power is low—the exchanges (NSE, BSE), depositories (NSDL, CDSL), and fund houses are available to all brokers on essentially identical terms, creating a level playing field on the input side.

The threat of substitutes is real but diffuse: bank fixed deposits, real estate, and gold remain deeply ingrained alternatives to equity investing in Indian household portfolios, and in a severe bear market, the flow of new retail investors into equities could slow dramatically as households retreat to the perceived safety of these traditional assets. India's cultural attachment to physical gold, in particular, should not be underestimated—it represents a competing financial behavior that is centuries old and emotionally powerful in ways that a stock portfolio simply is not.

X. Analysis: Bear versus Bull Case

The bear case for Groww begins and ends with three words: regulatory, cyclical, competitive.

Regulation is the "Sword of Damocles" hanging over the entire Indian brokerage industry. SEBI's crackdown on futures and options trading has already taken a meaningful bite out of revenue—roughly 200 crore in annualized terms for Groww alone, with derivatives dropping from 68 percent of income to 57 percent in just one year. The regulatory direction is clear: SEBI believes that retail participation in derivatives is excessive and harmful, citing studies showing that 89 percent of individual F&O traders lose money.

If SEBI continues to tighten—increasing lot sizes further, adding cooling-off periods for retail F&O traders, imposing additional STT hikes, or restricting the number of permitted strikes—the brokerage revenue base could compress further. Management is diversifying, but the diversification is coming from a relatively low base, and it takes time for lending, AMC, and wealth management revenue to scale to offset a structural decline in derivatives income.

The second bear concern is cyclicality. India added a record 41 million demat accounts in FY25, bringing the total to roughly 192 million. Nearly 40 percent of all individual investors were under 30, suggesting a demographic revolution. But there is a crucial distinction between having an account and actively using it. SEBI surveys indicate that while 63 percent of Indian households are aware of stock investing, only 9.5 percent actively participate.

A prolonged bear market—which India has not experienced since the relatively brief COVID crash of 2020—could expose the fragility of a user base acquired during an unprecedented bull run. Many of Groww's newer users have literally never experienced a sustained downturn. Their reaction to one will determine whether Groww's user metrics are durable or cyclical. The company's SIP book provides some cushion, but the F&O and intraday trading cohort could evaporate quickly.

Third, the competitive threat from Jio Financial Services and PhonePe is not hypothetical—it is unfolding in real time. Jio-BlackRock is building a mutual fund business with access to Reliance's retail distribution network and Jio's massive subscriber base. PhonePe is leveraging its UPI dominance to cross-sell investment products to hundreds of millions of users. If the investment experience becomes commoditized—if buying a mutual fund on PhonePe or Jio feels just as easy and trustworthy as on Groww—the competitive moat narrows considerably.

The bull case starts with the sheer magnitude of the addressable market.

India's "financialization of savings" is genuinely in its early stages. The share of equity and mutual funds in annual household financial savings rose from just 2 percent in FY12 to over 15 percent in FY25—a remarkable shift, but still far below the 40-50 percent levels seen in the United States, South Korea, and other mature markets. Domestic household investments in equities stood at 128 lakh crore in FY24, up from 84 lakh crore just a year earlier. India's mutual fund AUM is projected to reach 300 lakh crore by 2035.

More than half of new investors in FY25 were under 30, suggesting that the behavioral shift toward equity investing is generational—baked into how young Indians think about money—not merely cyclical. This is a structural tailwind that no amount of short-term market volatility can reverse.

Second, Groww's platform economics improve with each additional product. A customer who uses Groww only for stock trading might generate 500 rupees per year in brokerage. The same customer, using Groww for mutual funds, stocks, MTF, a personal loan, and UPI payments, might generate 3,000 to 5,000 rupees per year. The Fisdom acquisition opens the high-net-worth segment, where revenue per customer is an order of magnitude higher. Each layer makes the customer relationship more valuable and harder for a competitor to replicate in its entirety.

At the current market capitalization of roughly 99,000 crore rupees, the market is pricing Groww primarily as a brokerage. If the lending, AMC, and wealth management businesses reach meaningful scale over the next three to five years, the embedded optionality in those businesses is substantial.

Third, the operating leverage is striking. With approximately 2,000 employees serving 70 million registered users, the incremental cost of adding the next 10 million users is minimal. The technology platform is already built to handle surge volumes—IPO allotment days, budget-day market swings, election-result mornings—and each new user who joins the platform costs Groww essentially nothing in marginal infrastructure.

Revenue per employee is among the highest in Indian financial services. Compare this to a traditional private bank, which might employ 50,000 people to serve a comparable number of active accounts, with all the associated costs of branches, relationship managers, back-office processing, and compliance teams. Groww's digital-native architecture eliminates most of these costs by design. In a growing market, this kind of operational efficiency translates into margin expansion that can surprise even optimistic forecasts.

There is also a less obvious bull argument around data. Groww sits on one of the richest datasets in Indian consumer finance—the investment behavior, risk appetite, income patterns, savings frequency, and spending habits of 70 million users. This data, properly leveraged (and properly protected), could power increasingly sophisticated credit underwriting, personalized investment recommendations, and insurance product design. The lending business, in particular, benefits from this data advantage in ways that traditional banks simply cannot match.

For investors tracking this company's ongoing trajectory, three KPIs matter above all else.

First, the number of monthly active transacting users—not registered users, not app downloads, but people who actually executed at least one financial transaction in the trailing period. This is the most honest measure of engagement and the leading indicator of revenue durability; if this number stalls even as registered users grow, it signals that the platform is struggling to convert curiosity into commitment.

Second, revenue per active user, which captures the company's ability to deepen monetization through product cross-sell. If this number rises steadily over time, it means the platform strategy is working. If it flatlines, it means Groww is acquiring users but not deepening relationships.

Third, the percentage of revenue derived from non-brokerage sources—lending, AMC fees, MTF income, wealth management—because the long-term thesis depends entirely on whether Groww can transition from a brokerage that happens to have other products to a platform where brokerage is just one of many revenue engines. As of Q3 FY26, non-brokerage revenue accounts for roughly 28-30 percent of the total. Its trajectory over the next eight quarters will tell more about Groww's future than any single earnings report.

XI. Epilogue: The Legacy of Billionbrains

There is a story that gets told about Groww's early days—perhaps apocryphal, perhaps not—about Lalit Keshre sitting in a cramped apartment in Koramangala, Bengaluru's startup heartland, manually calling new users to understand why they had signed up and what confused them about investing.

The CEO of what is now a hundred-thousand-crore company, on the phone with a first-time investor in Jaipur or Lucknow, patiently explaining what an expense ratio is, or why a large-cap fund differs from a small-cap fund, or why an SIP of just 500 rupees per month is a perfectly valid way to start building wealth.

Whether or not the specific anecdote is true, the impulse behind it defined Groww's trajectory. The company's fundamental achievement was not technological—any reasonably competent engineering team can build a trading app. The achievement was cultural.

Groww changed the vibe of Indian investing from something that felt elite, complex, and vaguely intimidating—the province of suited men in South Mumbai and Nariman Point—to something that felt populist, simple, and accessible. It made a twenty-three-year-old in Indore feel as comfortable buying an index fund as ordering a pair of sneakers on Flipkart. It made a schoolteacher in Coimbatore feel that investing was not something only rich people do, but something she could do with 500 rupees and a few taps on her phone.

That cultural shift—the normalization of retail investing among India's young middle class—is arguably irreversible, regardless of what happens to any individual company's stock price.

The numbers bear this out at a macro level. India went from 40 million demat accounts in 2020 to over 212 million by the end of 2025—a five-fold increase in five years. The mutual fund industry, which managed about 27 lakh crore in 2020, crossed 65 lakh crore by 2025. Monthly SIP flows, which were running at about 8,500 crore per month in early 2020, surpassed 25,000 crore per month by late 2025—a tripling that represents millions of ordinary Indians making a monthly commitment to equity investing through disciplined, automated contributions.

Groww did not cause all of this—the pandemic, the bull market, smartphone penetration, UPI infrastructure, and demographic tailwinds all played their part. But it was the single most important catalyst for making this transition feel easy and natural for tens of millions of first-time participants. Before Groww, the phrase "I invest in the stock market" carried a certain weight in Indian middle-class conversation—it implied sophistication, risk tolerance, and a degree of financial privilege. After Groww, it became as unremarkable as "I have a savings account."

The things to watch going forward are the leading indicators of whether Groww can successfully execute its platform ambitions.

The growth of the MTF loan book tells you whether the company can generate meaningful interest income from its existing user base without taking excessive credit risk. The trajectory of Groww AMC's AUM—and particularly the mix between low-cost passive index funds and higher-fee actively managed thematic products—reveals whether the distribution-to-manufacturing strategy is creating durable, high-margin revenue.

The Fisdom-powered wealth management business, branded as "W," will show whether Groww can move upmarket into the affluent and HNI segment without losing its mass-market identity. This is a delicate balance, but in financial services the dynamics differ from consumer brands. A 25-year-old starting their first SIP needs simplicity and zero friction. A 45-year-old with 2 crore in investable assets needs advisory, tax planning, portfolio rebalancing, and estate management. These are fundamentally different products that happen to share the same underlying customer—the same person, at different stages of their financial life.

Groww's bet is that it can serve both, under the same roof, with different products but the same underlying platform and data layer. If the 25-year-old SIP investor stays on Groww for twenty years and accumulates 2 crore, the platform that guided their first 500-rupee investment could also manage their wealth at scale. The lifetime value of that customer relationship—from first SIP to estate planning—is what the platform thesis ultimately rests upon.

The four founders from Flipkart who started with a mutual fund search engine have, in less than a decade, built the largest investment platform in India by active users. They paid $160 million to the US government for the right to be an Indian company. They acquired a dying mutual fund house and grew its assets fifteen-fold. They convinced State Street Global Advisors to become a strategic partner in their tiny AMC. They bought Fisdom for nearly a thousand crore to add wealth management. They took the company public at a $9 billion valuation in an IPO that was subscribed nearly 18 times over.

And they did not sell their shares. In an era of founder cash-outs, quick flips, and SPAC-fueled liquidity events, the Groww founders chose to keep their wealth tied to the very platform they ask 70 million other Indians to trust with theirs. Actions like that speak louder than any investor presentation.

The transition from "The Flipkart Guys" to the "Custodians of India's Wealth" is not yet complete. The competitive threats from Jio and PhonePe are real and intensifying. The regulatory environment around derivatives is uncertain and trending restrictive. The next bear market—whenever it arrives—will test the durability of the entire thesis and reveal whether Groww's users are investors or tourists.

But if the Indian financialization story plays out over the next twenty years the way that similar transitions have played out in the United States, South Korea, and China—where equity market participation grew from single digits to half the population within a generation—then the company that controls the default savings and investment interface for a generation of Indians will be worth far more than what any current valuation model suggests. Groww has positioned itself to be that company. The next decade will reveal whether the positioning translates into destiny.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube