G R Infraprojects: From Village Roads to India's Infrastructure Backbone

I. Introduction & Cold Open

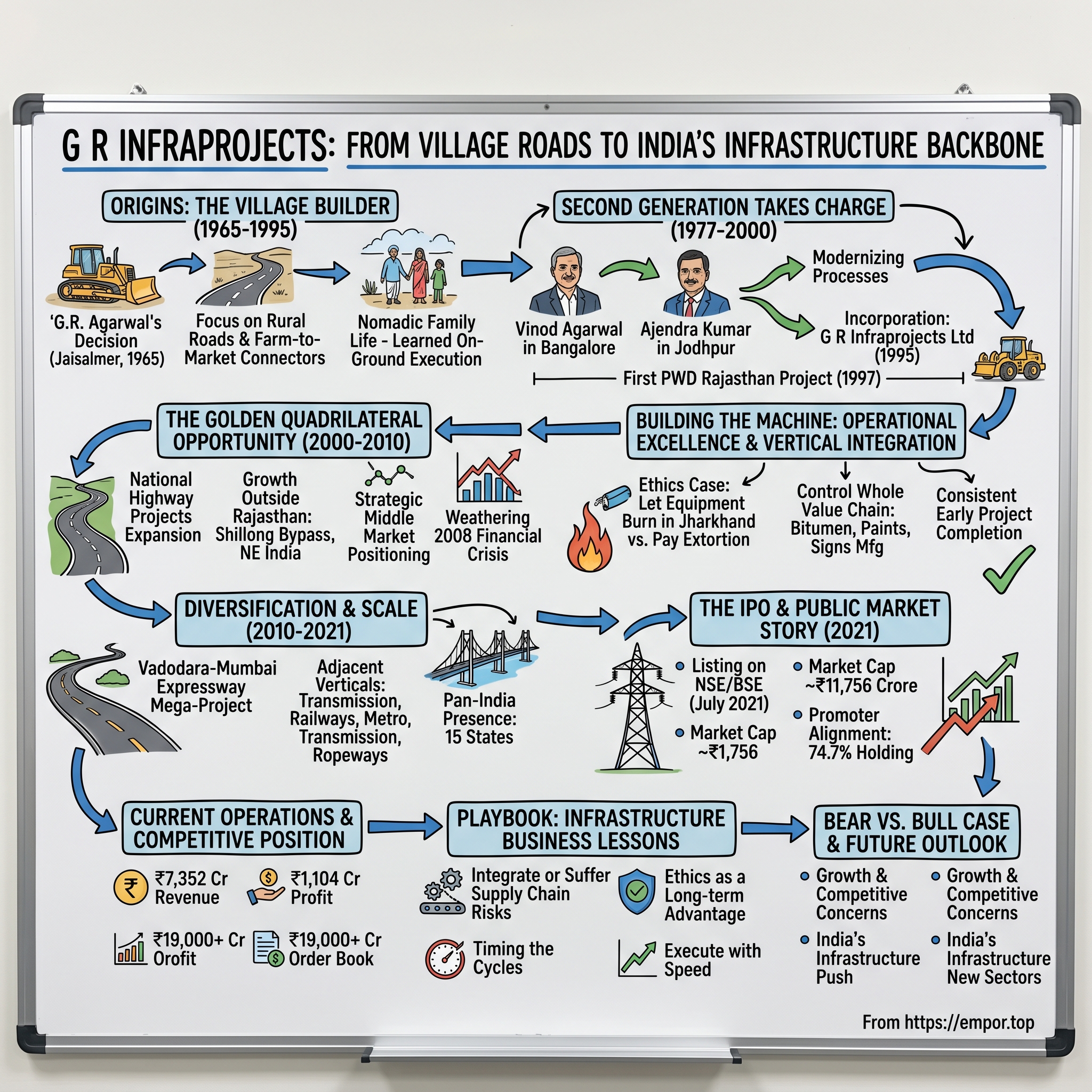

Picture this: A dusty village near Jaisalmer, Rajasthan, 1965. The monsoon has failed again. The few kutcha roads that connected these remote settlements to the outside world have turned to mud, then cracked earth. Government officials in distant Jaipur have bigger priorities—cities need flyovers, state capitals need highways. Who builds roads for villages that don't even appear on most maps?

A young man named G.R. Agarwal decided he would. Not because the government asked him to, not because there was obvious money in it, but because these were his people, his villages. That decision—born of necessity rather than ambition—would eventually create a ₹11,756 crore infrastructure powerhouse that builds some of India's most critical highways, railways, and power transmission lines.

Today, G R Infraprojects Limited stands as one of India's most efficient road construction companies, with ₹7,352 crore in revenue and an order book approaching ₹20,000 crores. When the company went public in July 2021 at ₹837 per share, it wasn't selling a technology platform or a consumer brand. It was selling something far more fundamental: the ability to connect India to itself, one kilometer at a time.

The central question that drives this story isn't just how a small contractor from rural Rajasthan built one of India's premier infrastructure companies. It's about how a family business, operating in one of the most challenging sectors—government contracting—managed to maintain both operational excellence and ethical standards while scaling from ₹2.65 crore projects to ₹2,747 crore mega-highways.

This is a story about timing, about catching the waves of India's infrastructure spending cycles. It's about the unglamorous work of backward integration—manufacturing your own thermoplastic paints and crash barriers because you can't rely on suppliers in remote locations. Most importantly, it's about how three generations of the Agarwal family transformed from nomadic contractors following projects across Rajasthan's desert districts to sophisticated infrastructure engineers managing complex HAM (Hybrid Annuity Model) projects across 15 Indian states.

What makes G R Infraprojects particularly fascinating for students of business is its refusal to follow the typical playbook. While competitors chased prestige projects in metros, GRINFRA built its fortress in Tier-2 and Tier-3 India. While others lobbied for contracts, the Agarwals famously walked away from ₹18 crore worth of machinery—letting Naxals burn it in Jharkhand—rather than pay protection money. "We don't get into business unless it's clean," became more than a tagline; it became the filter through which every opportunity passed.

II. Origins: The Village Builder (1965-1995)

The year 1965 marked more than just another India-Pakistan war or the birth of Bangladesh's independence movement. In a cluster of villages near Jaisalmer, where the Thar Desert begins its march toward Pakistan, it marked the beginning of an infrastructure revolution that no one saw coming.

G.R. Agarwal wasn't an engineer. He wasn't from a business family with capital to deploy. He was simply someone who understood a fundamental truth: without roads, villages die. The milk can't reach the market before it spoils. The sick can't reach hospitals in time. Children can't get to schools that are technically within reach but practically in another world.

Starting with borrowed equipment and family labor, Agarwal began building what the government wouldn't—farm-to-market roads, village connectors, the capillaries of India's transport system that rarely made it into five-year plans. The initial projects were so small they barely qualified as construction work by today's standards. We're talking about leveling dirt paths, laying gravel, building culverts over seasonal streams that became torrents during the monsoon.

But here's what set Agarwal apart from countless other small contractors across India: he understood that infrastructure wasn't just about moving earth and laying tar. It was about understanding the rhythm of rural life. When do farmers need roads most? (Harvest season.) When can you actually build? (Not during monsoons, not during planting.) How do you manage labor when your workforce disappears for weddings, festivals, and agricultural seasons?

The business model, if you could call it that, was beautifully simple. Take small government contracts that bigger players ignored. Complete them faster than promised. Use the reputation to get slightly bigger contracts. Repeat. But execution was anything but simple. The family became nomadic, moving from site to site—Chittor, Dongharpur, Jodhpur, Udaipur—living in temporary accommodations, with children attending whatever local schools would take them for a few months.

This nomadic existence shaped the company's DNA in ways that would only become apparent decades later. First, it created an unusually tight family bond—when you're living in construction site quarters in remote Rajasthan, family is all you have. Second, it built an intimate understanding of on-ground execution that no MBA program could teach. The Agarwal brothers didn't learn construction from textbooks; they learned it from watching their father negotiate with local labor, source materials from skeptical suppliers, and manage cash flows when government payments arrived months late.

By the mid-1970s, as G.R. Agarwal's sons began coming of age, a pattern emerged that would define the family's approach to growth: each son would join the business not out of obligation but out of necessity. Limited educational opportunities in their villages meant that joining the family business wasn't Plan B—it was often the only plan that made sense.

The transformation from individual contractor to actual company was gradual, almost imperceptible. Through the 1970s and 1980s, as India struggled through the Emergency, the License Raj, and economic stagnation, G R Infraprojects (not yet incorporated) quietly built capabilities. They learned to operate concrete mixers, manage hot-mix plants, handle surveying equipment. Each new skill meant they could bid for slightly more complex projects.

What's remarkable about this period is what didn't happen. The Agarwals didn't diversify into real estate, as many contractors did. They didn't chase political connections in state capitals. They didn't even incorporate as a company until 1995, three decades after G.R. Agarwal built his first village road. This wasn't strategic patience—it was simply who they were: road builders from Rajasthan who happened to be very, very good at what they did.

The decision to finally incorporate in 1995 as an integrated Engineering, Procurement, and Construction (EPC) company wasn't driven by ambition but by necessity. The projects were getting bigger, banks needed formal entities to lend to, and government contracts increasingly required corporate structures. But even as they filed the paperwork and opened bank accounts, the family probably didn't imagine that within a decade, they'd be building highways across Northeast India, or that within two decades, they'd be managing one of India's largest infrastructure order books.

III. The Second Generation Takes Charge (1977-2000)

The story of how Vinod Agarwal ended up in Bangalore in 1977-78 tells you everything about how Indian family businesses navigated the pre-liberalization era. His father didn't send him there to get an engineering degree because of some strategic vision about the future of infrastructure. He sent him because Bangalore had one of the few engineering colleges that would accept a student from rural Rajasthan with his academic background, and because someone—a distant relative, a family friend—could provide a place to stay.

Vinod's journey from junior college in Jodhpur to engineering in Bangalore was a culture shock that shaped his worldview. Bangalore in the late 1970s wasn't yet India's Silicon Valley, but it was already different—more cosmopolitan, more systematic, more professional. While his classmates discussed joining Larsen & Toubro or seeking government engineering posts, Vinod knew his destination: back to the family business, but armed with formal knowledge that his father's generation learned through trial and error.

Meanwhile, younger brother Ajendra Kumar was completing his civil engineering degree from Jodhpur University—a more conventional path but no less important. The combination of Vinod's exposure to modern engineering practices and Ajendra's grounding in local realities would prove crucial as the company navigated its first major transition.

The brothers returned to a business that was successful by rural Rajasthan standards but primitive by any modern metric. Accounting meant ledgers maintained in Hindi. Project management meant their father's mental notes. Quality control meant their father personally inspecting every culvert. The challenge wasn't just to modernize these processes but to do so without alienating the old-timers who had built the business with their bare hands.

The 1995 incorporation as G R Infraprojects Limited was less a beginning than a culmination of this modernization process. The company now had systems—rudimentary but real. It had engineers who could read technical drawings, not just implement their father's verbal instructions. Most importantly, it had ambition that extended beyond Rajasthan's borders.

The first Public Works Department (PWD) Rajasthan project in 1997—worth ₹2.65 crore—might seem trivial in today's context. But consider what it represented: a formal government contract with specifications, timelines, and penalties. This wasn't a village panchayat dealing with a local contractor anymore. This was the state government selecting a company through competitive bidding. The winning of that contract validated their transformation. The journey started with first road project that was executed for the PWD (Public Works Department), Rajasthan with a Bid Project Cost of ₹ 26.50 million in 1997, marking their entry into formal government contracting. But what's striking about this period is how measured their growth remained. They didn't immediately chase larger projects or expand geographically. Instead, they methodically built capabilities.

The late 1990s were spent learning the rhythms of formal contracting—how to prepare technical bids, how to manage cash flows when government payments invariably arrived late, how to deal with bureaucratic approvals that could delay projects for months. This wasn't glamorous work, but it was essential. Every delayed payment taught them about working capital management. Every technical specification they struggled to meet taught them about quality standards. Every bureaucratic hurdle taught them patience.

What outsiders often miss about this period is how the License Raj, even in its dying days, shaped companies like G R Infraprojects. The system wasn't designed for efficiency or innovation. It was designed for compliance, for following procedures, for not making waves. But for those who mastered it—who learned to navigate its labyrinthine requirements without compromising their integrity—it provided a moat. When liberalization finally came, they had capabilities their newer, flashier competitors would take years to build.

The Agarwal brothers were also learning something else during this period: the value of saying no. In an industry where corruption was endemic, where getting contracts often meant paying the right people, they were developing their ethical framework. This wasn't some high-minded corporate philosophy developed by consultants. It was practical: corruption was expensive, unpredictable, and ultimately unsustainable. Better to build a reputation for clean dealing and accept slower growth than to play games that could destroy everything they'd built.

As the millennium approached, India stood on the cusp of an infrastructure revolution. The Agarwals, with their newly incorporated company, their engineering degrees, and three decades of on-ground experience, were perfectly positioned to catch the wave. They just didn't know it yet.

IV. The Golden Quadrilateral Opportunity (2000-2010)

The announcement came on January 6, 1999, from Prime Minister Atal Bihari Vajpayee himself: India would build 5,846 kilometers of four and six-lane highways connecting Delhi, Mumbai, Chennai, and Kolkata. The Golden Quadrilateral project, as it came to be known, represented the largest infrastructure initiative in India's history. For a company that had just completed its first ₹2.65 crore PWD project, this should have been irrelevant—like a corner shop owner hearing about Walmart's expansion plans.

But infrastructure doesn't work like retail. When the government decides to build thousands of kilometers of highways, it doesn't just need the L&Ts and the IRBs of the world. It needs hundreds of sub-contractors, specialists, regional players who understand local conditions, can manage local labor, source local materials. The pie was getting bigger, and suddenly there were slices available for companies that knew how to execute.

The Agarwals' first move wasn't to Delhi or Mumbai, where the big contractors were assembling their war rooms. GRIL began its journey outside Rajasthan with Shillong bypass and quickly spread to Manipur, Meghalaya, Bihar, UP, Andhra Pradesh. Think about that choice for a moment. The Northeast in the early 2000s was infrastructure's final frontier—remote, insurgency-affected, with supply chains that made Rajasthan look like Singapore. Why would a Rajasthan-based company make this their breakout move?

The answer reveals the strategic thinking that would define G R Infraprojects' rise. In the Northeast, they weren't competing with established players. The big contractors found these projects too small, too remote, too risky. But for GRINFRA, accustomed to building roads where none existed, dealing with challenging terrain and limited resources, the Northeast was familiar territory with unfamiliar geography. They could charge premium prices for taking on difficult projects while building capabilities that would serve them for decades.

The Shillong bypass project became their calling card. Completed ahead of schedule despite monsoons that could wash away a week's work in an afternoon, despite procurement challenges that required materials to be trucked in from thousands of kilometers away, it announced to the infrastructure establishment that there was a new player who could execute where others couldn't or wouldn't.

This period also saw the family's geographic dispersion—a physical manifestation of the company's growth. Ajendra Kumar became the first family member to settle in Gurugram, establishing their presence in the National Capital Region. This wasn't just about being closer to government ministries and NHAI offices. It was about understanding that infrastructure in the 2000s would be a national game, not a regional one.

The numbers tell only part of the story. Over a span of last 15 years, we have executed more than 100 projects across 23 states. But what those numbers don't capture is the organizational transformation required. Each new state meant understanding new political dynamics, new bureaucratic procedures, new labor markets. It meant building relationships with local suppliers, understanding local construction seasons, adapting to local materials.

The post-2000 infrastructure boom driven by Vajpayee's vision—PMGSY (Pradhan Mantri Gram Sadak Yojana) for rural roads, the Golden Quadrilateral, the East-West and North-South corridors—created opportunities at every level. While headlines focused on the mega-projects, the real work was happening in thousands of smaller contracts that connected this network. GRINFRA positioned itself perfectly in this middle market—too big for local contractors, too small for national giants.

What's particularly instructive about their approach during this period was their resistance to over-leverage. While competitors were raising debt to fund aggressive expansion, the Agarwals maintained their conservative financial approach. They grew with their cash flows, taking on only projects they could fund without stretching their balance sheet. This meant leaving money on the table—passing on projects that looked attractive but would have required significant debt. In the boom years of the mid-2000s, this looked foolishly conservative. By 2008, it looked prescient.

The global financial crisis of 2008 devastated India's infrastructure sector. Companies that had leveraged up to chase growth found themselves with stalled projects, frozen credit lines, and mounting losses. Several prominent infrastructure companies that had been darlings of the stock market in 2007 were fighting for survival by 2009. GRINFRA not only survived but used the crisis to strengthen its position, picking up talent from struggling competitors, acquiring equipment at distressed prices, and most importantly, building trust with government clients by continuing to execute when others were abandoning projects.

By 2010, as India emerged from the crisis and embarked on another infrastructure push, G R Infraprojects had transformed from a regional Rajasthan contractor to a pan-India infrastructure company. They had projects across 15 states, capabilities across multiple types of construction, and most importantly, a reputation for execution that money couldn't buy. The family business from Jaisalmer was ready for its next transformation.

V. Building the Machine: Operational Excellence & Vertical Integration

The moment of truth came in Jharkhand, in the middle of a Naxal-affected forest, when armed insurgents surrounded G R Infraprojects' construction site. The demand was simple: pay protection money or watch your equipment burn. Machinery and equipment valued at over Rs18 crore has been burnt at Hazaribagh in Naxal-hit Jharkhand, but GRIL did not compromise with the extortionists. For most contractors, this would have been a straightforward business decision—pay the money, add it to project costs, move on. The Agarwals chose differently. They let ₹18 crore worth of machinery burn rather than set a precedent of paying extortion.

This decision—financially painful but ethically clear—exemplified the operational philosophy that would distinguish GRINFRA from its peers. "We don't get into business unless it is clean and we do not compromise on ethics at any cost," wasn't just corporate rhetoric. It was the filter through which every operational decision passed.

But ethics alone doesn't build highways. What transformed G R Infraprojects from a good contractor to an exceptional one was their approach to vertical integration—a strategy that sounds boring until you understand what it means in India's infrastructure context.

Consider the problem of thermoplastic road-marking paint. It's a small detail—the white and yellow lines that mark lanes and boundaries. But in remote project sites, getting quality paint delivered on time could delay projects for weeks. The solution? GRINFRA started manufacturing their own. Then road signage. Then metal crash barriers. Then bitumen processing. Each integration solved a specific procurement problem, but together they created something powerful: control over the entire value chain.

The Company has developed in-house resources with key competencies to deliver a project from conceptualization to completion that includes its design and engineering team, 4 manufacturing units situated at Udaipur (Rajasthan), Guwahati (Assam), Sandila (Uttar Pradesh) and Ahmedabad (Gujarat) for manufacturing/ fabrication of bitumen, thermoplastic road-marking paint, road signage, metal crash barriers and electric poles.

This backward integration strategy revealed deep operational insight. In developed markets, specialization makes sense—you focus on your core competency and outsource everything else. But in India's infrastructure sector, especially in remote locations, the opposite is true. Every external dependency is a potential point of failure. Better to control what you can, even if it means lower margins on paper.

The business model evolution during this period was equally sophisticated. GRINFRA didn't just build roads; they structured deals across multiple models—EPC (Engineering, Procurement, Construction), BOT (Build-Operate-Transfer), HAM (Hybrid Annuity Model), DBFOT (Design, Build, Finance, Operate, Transfer), and BOOT (Build, Own, Operate, Transfer). Each model had different risk profiles, cash flow patterns, and return expectations. Mastering all of them meant they could bid for any project, regardless of how the government chose to structure it.

But the real operational excellence showed in execution speed. In an industry where delays are the norm—where completing a project on time is considered an achievement—GRINFRA consistently finished early. The Nagaur-Mukundgarh HAM project, completed 13 months ahead of schedule, wasn't an anomaly. It was the standard. This wasn't about working faster or cutting corners. It was about systematic project management, detailed planning, and most importantly, eliminating dependencies that could cause delays.

The manufacturing integration went beyond solving procurement problems. It created a competitive moat that financial metrics couldn't capture. When you're bidding for a project in remote Arunachal Pradesh, being able to guarantee that you can produce your own bitumen, fabricate your own crash barriers, and manufacture your own signage means you can make commitments that competitors relying on third-party suppliers simply can't match. The operational strategy extended to financial management. In fiscal 2019, the company completed a state HAM project 13 months ahead of schedule and has received early completion bonus in October 2020. These early completion bonuses weren't windfalls—they were engineered outcomes. By controlling their supply chain, maintaining equipment in-house, and operating round-the-clock when necessary, GRINFRA could guarantee completion timelines that competitors treating projects as coordination exercises simply couldn't match.

The scale of this integration becomes clear when you look at the numbers: Our ~11,000 passionate employees, best-in-class assets, latest technology, and 24/7 project execution capability enables us to deliver projects before or on-time with highest standards of quality, safety, financial discipline, and governance. Think about what 24/7 execution means in practical terms. It means having enough equipment to run multiple shifts. It means having maintenance crews that can fix breakdowns at 2 AM. It means having the working capital to pay overtime without waiting for government reimbursements.

This operational excellence created a virtuous cycle. Early completion meant early bonuses, which improved cash flows. Better cash flows meant less dependence on external financing. Less debt meant better bids on new projects. Better bids meant more projects. More projects meant better utilization of their integrated facilities. It was a flywheel that, once spinning, became increasingly difficult for competitors to replicate.

The decision to maintain this level of vertical integration flew in the face of modern management theory about focus and capital efficiency. Why tie up capital in paint manufacturing plants when you could outsource? Why maintain thousands of pieces of equipment when you could rent? The answer lay in understanding the reality of Indian infrastructure: in the places where roads were most needed, traditional supply chains simply didn't exist. You couldn't outsource what wasn't there.

VI. Diversification & Scale (2010-2021)

The Vadodara-Mumbai Expressway project announcement in 2020 represented everything G R Infraprojects had been building toward for 55 years. The Company was incorporated in December 1995 and executed their first projects for the Public Works Department, Rajasthan in 1997 with a Bid Project Cost of ₹ 2.65 Cr, whereas the project recently awarded by NHAI, i.e. Vadodara Mumbai Expressway project in the state of Maharashtra on HAM basis, to the GR Infra IPO in 2020 involves a Bid Project Cost of ₹ 2747 Crores. From ₹2.65 crores to ₹2,747 crores—a thousand-fold increase that tells the story of India's infrastructure transformation and GRINFRA's role in it.

But the real story of this decade wasn't just about bigger projects. It was about systematic diversification into adjacent verticals where their core competencies—project execution, government contracting, managing remote sites—could create value. Railway overbridges, elevated metro lines, transmission lines, multi-modal logistics parks, ropeways—each new vertical wasn't a random diversification but a calculated extension of existing capabilities.

The power transmission business entry deserves particular attention. On the surface, stringing high-voltage lines across the country seems different from building roads. But operationally, the challenges are remarkably similar: acquiring right-of-way across multiple states, managing projects in remote locations, dealing with multiple government agencies, ensuring quality while maintaining speed. GRINFRA didn't need to learn these skills; they'd been perfecting them for decades.

The portfolio by March 2021 told the story: an order book of approximately ₹19,000 crores spread across multiple states and sectors. This wasn't concentration risk; it was systematic de-risking. When highway construction slowed, railway projects picked up. When state governments faced budget constraints, central government projects filled the gap. When traditional infrastructure spending cycled down, new areas like ropeways and logistics parks emerged.

The metro projects marked a particular evolution in capabilities. Building elevated metro lines in cities like Bangalore and Noida required different skills than highway construction—urban project management, minimal disruption to existing infrastructure, coordination with multiple civic agencies. That GRINFRA could win and execute these projects demonstrated that their competence went beyond rural road construction. They had become a full-spectrum infrastructure company.

What's particularly impressive about this diversification is what didn't change: the focus on execution excellence, the emphasis on completing projects ahead of schedule, the insistence on ethical practices. While the projects got more complex and the geographies more diverse, the underlying operational philosophy remained constant.

The financial metrics during this period reflected both the opportunities and challenges of rapid scaling. Revenue grew substantially, but so did working capital requirements. The shift to HAM projects, while reducing construction risk, meant tying up capital for longer periods as the company now had partial ownership of assets during the concession period. This wasn't a problem—GRINFRA had the balance sheet to support it—but it represented a fundamental shift in the business model from pure construction to partial asset ownership.

The scale transformation wasn't just about size; it was about sophistication. The company that once moved from village to village in Rajasthan now managed concurrent projects across 15 states. The family that once maintained ledgers in Hindi now dealt with complex financial structuring across multiple SPVs (Special Purpose Vehicles) for HAM projects. The contractor that once relied on local labor now employed thousands of engineers and technicians.

Yet somehow, through all this growth and transformation, G R Infraprojects maintained its identity as a family business. The Agarwal brothers still visited project sites. Senior family members still knew long-time employees by name. The company still walked away from projects that required compromising their principles. This wasn't nostalgia; it was recognition that their family values—hard work, integrity, long-term thinking—were competitive advantages that no amount of financial engineering could replicate.

VII. The IPO & Public Market Story (2021)

The prospectus filed in June 2021 for G R Infraprojects' initial public offering was notable for what it didn't promise. No disruption narrative. No technology platform story. No asset-light transformation. Just a straightforward proposition: we build infrastructure well, we complete projects on time, and we do it profitably. In an IPO market drunk on new-age business models, GRINFRA was selling something almost quaint—operational excellence in a traditional industry.

The IPO is set to open on Jul 7, 2021, while the closing date is set at Jul 9, 2021. Basis of Allotment finalization is on Jul 14, 2021, refund initiation is on Jul 15, 2021, credit of shares is on Jul 16, 2021, and share listing date is on Jul 19, 2021. Shares of G R Infraprojects shall be listed in the exchanges on Jul 19, 2021. The date, when the listing would be done, is stagnant on Jul 19, 2021.

The numbers were compelling in their conservatism. P/E of 8.5, Industry average is around 18. At a time when loss-making companies were commanding premium valuations based on TAM (Total Addressable Market) slides, GRINFRA was pricing itself at half the industry average. This wasn't modesty; it was strategy. The Agarwals understood that infrastructure is a cyclical business. Better to price conservatively and over-deliver than to burden the company with unrealistic market expectations.

The structure of the offering itself—₹962.37 crores entirely as an offer for sale of 1.15 crore shares—sent a clear message. The company didn't need the money. The objects of the Offer are to achieve the benefits of listing the Equity Shares on the Stock Exchanges and for the offer for sale of up to 11,508,704 Equity Shares by the Selling Shareholders. This was about providing liquidity to early investors and creating a currency for future growth, not about raising capital for operations.

The promoter structure revealed the family's confidence in the business. Promoter Holding: 74.7% Even after the IPO, the Agarwal family retained three-quarters of the company. This wasn't just about maintaining control; it was about alignment. When the family owns 75% of the company, every operational decision affects their wealth directly. There's no agency problem, no misalignment between management and shareholders.

The investor roadshow presentations were refreshingly free of jargon. No talk of disrupting the infrastructure sector or creating platform effects. Instead, slide after slide of completed projects, photos of highways and bridges, graphs showing consistent early completion rates. The message was clear: judge us by what we've built, not by what we promise to build.

What made the IPO particularly interesting from a capital markets perspective was its timing. July 2021 was peak bubble territory for new-age IPOs. Companies with no path to profitability were listing at astronomical valuations. In this environment, a profitable, dividend-paying infrastructure company seemed almost anachronistic. Yet perhaps that was precisely the appeal. In a market full of stories, GRINFRA offered substance.

The leadership structure post-IPO remained unchanged: Vinod Kumar Agarwal as Chairman, Ajendra Kumar Agarwal as Managing Director. No high-profile independent directors brought in to impress markets. No management consultants hired to transform the business. Just the same team that had built the company over decades, now accountable to public shareholders but not fundamentally altered by that accountability.

Market reception was instructive. While the IPO was subscribed, it didn't see the frenzy associated with new-age offerings. Institutional investors appreciated the business quality but were cautious about infrastructure cycles. Retail investors were attracted to the dividend yield but worried about government payment delays. The stock listed at a modest premium and then began its journey of price discovery.

What the public listing did accomplish was validation—not of the business model, which had been proven over decades, but of the family's approach to building a company. In an era of blitzscaling and growth at all costs, G R Infraprojects had shown that patient capital, operational excellence, and ethical practices could create substantial value. The market capitalization of ₹11,756 crores wasn't just a number; it was recognition that what the Agarwals had built in the deserts of Rajasthan had national significance.

VIII. Current Operations & Competitive Position

The numbers tell one story: ₹11,756 crore market cap, ₹7,352 crore revenue, ₹1,104 crore profit. But the reality of G R Infraprojects' current position is more complex than these headlines suggest. The company has delivered a poor sales growth of 3.02% over past five years. In an industry where order books can double overnight with a single project win, this slow growth requires explanation.

The answer lies in a deliberate strategic choice: quality over quantity. While competitors chase revenue growth by bidding aggressively on every available project, GRINFRA maintains strict filters. Project location, payment terms, execution complexity, client credibility—each factor is weighed before bidding. This selective approach means leaving money on the table, but it also means maintaining margins and avoiding problem projects that can destroy years of reputation.

The geographic footprint across 15 states represents both strength and challenge. Unlike companies focused on specific regions, GRINFRA must maintain capabilities across diverse geographies—from the deserts of Rajasthan to the hills of Northeast, from the coastal regions of Andhra Pradesh to the plains of Uttar Pradesh. This requires different equipment, different techniques, different relationships. It's operationally complex but strategically essential for de-risking the business from regional economic cycles.

The organization structure—1,462 employees for a company of this scale—reveals remarkable efficiency. This isn't about keeping headcount low for financial metrics. It's about the leverage that comes from vertical integration and operational excellence. When you manufacture your own materials and maintain your own equipment, when you have systems that prevent rework and delays, you need fewer people to manage the same revenue.

The order book approaching ₹20,000 crores provides visibility but also presents execution challenges. Out of its total order book position of | 17,005.7 crore, orders worth ~| 10,000 crore are currently under execution while the company is awaiting appointed date in balance jobs (8 HAM projects having EPC value of ~| 7,000 crore). Managing this pipeline requires careful capital allocation, precise project scheduling, and most importantly, maintaining execution quality as scale increases.

The competitive landscape has evolved significantly. Chinese construction companies, before recent restrictions, brought different capabilities and pricing aggression. Large conglomerates have entered infrastructure seeking growth. New players backed by private equity promise to disrupt traditional practices. Yet GRINFRA's competitive advantages—deep government relationships built over decades, proven execution in difficult geographies, and the financial strength to weather payment delays—remain difficult to replicate.

What's particularly interesting about their current competitive position is how they've responded to technology changes in the sector. While not leading digital transformation, they've selectively adopted technologies that enhance execution—GPS tracking for equipment, project management software for scheduling, drone surveys for progress monitoring. It's pragmatic modernization rather than transformation for its own sake.

The financial health metrics deserve attention. At the end of Q1 FY23, its gross debt, cash and cash equivalent at the standalone level stood at |1,055 crore, | 295 crore, respectively. The net D/E remained steady at ~0.2x over the past few years. In an industry notorious for leverage-driven disasters, maintaining such conservative debt levels while executing projects worth billions reveals sophisticated working capital management.

The challenge of increased working capital tied up in HAM projects represents the price of evolution. These projects require upfront equity investment, with returns flowing over the concession period. It's a fundamentally different cash flow profile than pure EPC projects. Managing this transition while maintaining growth requires financial sophistication that goes beyond traditional contractor capabilities.

Current operations also reflect the impact of government infrastructure spending cycles. The focus on highways under various programs, the emphasis on last-mile connectivity, the push for logistics infrastructure—each government priority creates opportunities but also competition. GRINFRA must constantly calibrate its capabilities to match evolving government priorities while maintaining its core competencies.

IX. Playbook: Infrastructure Business Lessons

If you wanted to build an infrastructure company in India from scratch, the G R Infraprojects story offers a masterclass—not in what to do, but in how to think. The lessons aren't about copying specific tactics but understanding the principles that guide decisions in this complex sector.

First, the paradox of family business evolution. The Agarwals maintained family control while professionalizing operations. This isn't the typical story of bringing in outside managers to transform a traditional business. Instead, family members acquired formal education, learned modern practices, but retained the value system that defined the company's early days. The lesson: modernization doesn't require abandoning what made you successful; it requires adapting those strengths to new contexts.

The backward integration strategy challenges conventional wisdom about capital efficiency. Three manufacturing units at Udaipur-Rajasthan, Guwahati- Assam and Sandila-Uttar Pradesh, for processing bitumen, thermoplastic road-marking paint and road signage, and a fabrication and galvanization unit at Ahmedabad, Gujarat for manufacturing metal crash barriers and electric poles. Every MBA program teaches focus and outsourcing. GRINFRA did the opposite, and it worked. The lesson: in markets with weak infrastructure, controlling your supply chain isn't inefficiency—it's risk management.

Managing working capital in government contracts requires a different mindset than private sector business. Payment delays aren't exceptions; they're the rule. Building a business model that assumes 180-day payment cycles, that maintains credit lines for these delays, that prices projects to include financing costs—this isn't taught in business school, but it's essential for infrastructure success.

The ethics stance—refusing to pay bribes even when it means losing projects or equipment—seems economically irrational. "We don't get into business unless it is clean and we do not compromise on ethics at any cost," says Tulsyan. Machinery and equipment valued at over Rs18 crore has been burnt at Hazaribagh in Naxal-hit Jharkhand, but GRIL did not compromise with the extortionists. Yet it created a reputation that became its own currency. Government officials knew GRINFRA wouldn't embarrass them with corruption scandals. This reputation meant access to projects that required clean contractors. The lesson: ethics isn't just about doing the right thing; in the long term, it's a competitive advantage.

Geographic diversification as risk mitigation runs counter to the focus strategy most companies follow. GRIL began its journey outside Rajasthan with Shillong bypass and quickly spread to Manipur, Meghalaya, Bihar, UP, Andhra Pradesh. "You cannot remain in one place as roads take you to other states," says Vinod as the company bid for projects in Kerala and Tamil Nadu too. But in infrastructure, where state government finances and priorities vary wildly, geographic concentration is existential risk. The lesson: in government contracting, customer concentration risk manifests geographically.

Timing market cycles requires understanding that infrastructure spending is inherently political. Election cycles, fiscal priorities, and development agendas drive spending patterns. Companies that gear up during boom times often collapse during downturns. GRINFRA's conservative growth during good times and aggressive positioning during downturns reveals deep cycle understanding. The lesson: in cyclical industries, survival requires counter-cyclical thinking.

The importance of execution speed in government contracts goes beyond early completion bonuses. Over a span of last 15 years, we have executed more than 100 projects across 23 states, with an exceptional record of projects being completed on timely basis or before time Fast execution means faster capital recycling. It means reputation that wins more projects. It means avoiding cost escalations from inflation. The lesson: in infrastructure, time isn't just money—it's everything.

Family businesses in public markets face unique challenges. Market quarters demand short-term thinking; infrastructure requires decade-long perspectives. The Agarwals solved this by maintaining majority control and setting expectations appropriately. They didn't promise quarterly growth; they promised long-term value creation. The lesson: going public doesn't mean adopting public market timeframes if your business operates on different cycles.

X. Bear vs. Bull Case & Future Outlook

The bull case for G R Infraprojects writes itself in the arithmetic of India's infrastructure deficit. India needs $1.4 trillion in infrastructure investment by 2025. The government has committed to massive spending across highways, railways, and urban infrastructure. Every budget increases allocation. Every election promises more connectivity. In this context, a company with proven execution capabilities, a ₹20,000 crore order book, and relationships across 15 states seems positioned to capture disproportionate value.

The entry into power transmission deserves special attention in the bull narrative. GRIL is likely to be one of the major recipients of thriving roads, railways and power transmission segments. India's renewable energy push requires massive transmission infrastructure. Unlike roads, where competition is intense, transmission projects require specialized capabilities that few possess. GRINFRA's early moves here could position them for decades of growth.

The operational excellence track record—completing projects ahead of schedule, maintaining quality standards, managing complex stakeholder relationships—creates a moat that's difficult to quantify but impossible to ignore. In a sector where delays are standard and quality issues common, consistent execution becomes its own competitive advantage. Clients pay premiums for certainty.

The reasonable debt-to-equity ratio of 43% provides flexibility that leveraged competitors lack. When the next infrastructure cycle accelerates, GRINFRA can bid aggressively without stretching its balance sheet. When downturns come, they can survive without restructuring. This financial conservatism might limit growth during boom times but ensures survival during busts.

But the bear case has merit too. The company has delivered a poor sales growth of 3.02% over past five years. In a country growing at 6-7% nominally, with infrastructure spending growing faster, this suggests either execution constraints or strategic choices that limit growth. Either explanation raises questions about future potential.

The notable decline in revenue and EBITDA margins points to structural challenges. The lower-than-normalized level of margin is mainly impacted by a) change in project mix with higher contribution from lower margin EPC projects (63% of the total Q1 FY23 revenues), b) early stage of execution in the newly commenced HAM projects (jobs doesn't attract high margin in the initial stage), and c) higher raw material prices. As the company shifts to HAM projects, margins might remain pressured for extended periods.

Working capital intensity has increased substantially. HAM projects require upfront equity investment with returns flowing over 15+ years. This fundamentally different cash flow profile means the company needs more capital to generate the same revenue. It's not a problem if managed well, but it changes the unit economics of the business.

The dependency on government spending cycles represents systematic risk that can't be diversified away. When governments face fiscal constraints—as they periodically do—infrastructure spending is often the first casualty. Unlike consumer businesses that can pivot to different segments, infrastructure companies are structurally tied to government priorities.

Competition has intensified across every segment. Large conglomerates bring financial muscle. International players bring technical expertise. New entrants backed by patient capital can bid irrationally to gain market share. The comfortable oligopoly that existed in Indian infrastructure has given way to intense competition that pressures margins and growth.

The future outlook depends largely on factors outside GRINFRA's control—government spending priorities, interest rate cycles, commodity prices. But within these constraints, the company has options. The push into power transmission, logistics parks, and ropeways represents optionality on new growth vectors. The strong balance sheet provides flexibility to pursue acquisitions or enter new segments. The reputation for execution excellence ensures access to projects regardless of market conditions.

Perhaps most importantly, the alignment between family ownership and public shareholders suggests decisions will be made for long-term value creation rather than short-term market appeasement. In infrastructure, where projects span decades and relationships matter more than quarterly numbers, this alignment might be the most important factor determining future success.

XI. Epilogue & Reflections

Standing at a construction site on the Vadodara-Mumbai Expressway, watching concrete pour for a pillar that will stand for generations, you can't help but reflect on the journey from that first village road in 1965. G R Infraprojects represents something profound about India's development—not the headline-grabbing tech unicorns or consumer brands, but the patient, methodical building of physical infrastructure that connects a nation to itself.

The transformation of the Indian infrastructure landscape over the past three decades has been remarkable. From a country where a four-hour journey between major cities was considered good to one building high-speed expressways and metro systems, the change has been generational. Companies like GRINFRA didn't just benefit from this transformation; they enabled it. Every kilometer of road built created demand for two more. Every project completed on time built confidence for larger projects.

What G R Infraprojects represents for India's development story goes beyond the physical infrastructure built. It's proof that family businesses can professionalize without losing their soul. That ethical practices can coexist with commercial success. That companies from tier-2 India can compete nationally. That patient capital and operational excellence can create more value than financial engineering.

The family business aspect deserves particular reflection. In an era where professional management is valorized and family businesses are seen as anachronistic, the Agarwals have shown a different path. They've proven that family ownership can provide the long-term thinking infrastructure requires. That personal reputation and corporate reputation can reinforce each other. That the values learned building village roads in Rajasthan can scale to national infrastructure projects.

For entrepreneurs, the GRINFRA story offers lessons in building for the long term. The company spent 30 years as a partnership before incorporating, another 16 years as a private company before going public. Each phase built capabilities for the next. There was no rush to scale, no pressure to exit, no pivoting to chase trends. Just consistent focus on getting better at what they did.

For investors, the story challenges conventional frameworks. How do you value a company whose competitive advantage is relationships built over decades? How do you model ethics as a moat? How do you price in the option value of new infrastructure segments? Traditional metrics capture the business but miss the essence of what makes it valuable.

The broader implications for India's infrastructure sector are significant. If a family business from rural Rajasthan can build a ₹11,756 crore company through operational excellence and ethical practices, what does that say about the opportunity ahead? As India pushes toward developed nation status, the infrastructure required is staggering. Companies that can execute—really execute, not just win contracts—will capture enormous value.

Yet challenges remain. Infrastructure is ultimately about state capacity, and corporate execution can only compensate so much for governmental inefficiencies. Payment delays, land acquisition challenges, regulatory uncertainties—these systemic issues limit what even the best companies can achieve. GRINFRA has succeeded despite these challenges, not because they've been solved.

The story also raises questions about the next generation. Can the third generation of Agarwals maintain the values and capabilities that built the company? Can a publicly listed company with institutional shareholders maintain the long-term orientation that infrastructure requires? Can operational excellence survive the pressure for quarterly growth? These questions don't have easy answers.

What's clear is that G R Infraprojects has earned its place in India's infrastructure history. Not through mega-projects or financial innovation, but through something more fundamental: the consistent ability to build what needs building, where it needs building, when it needs building. In a country racing to develop, that capability is invaluable.

The company that started because government wouldn't build roads to remote villages has become one of the government's most trusted partners in building national infrastructure. It's a validation of G.R. Agarwal's original insight: infrastructure isn't about grand visions or complex financing. It's about showing up, day after day, and doing the work. Moving earth. Laying tar. Building bridges. Connecting India, one kilometer at a time.

As India enters what could be its infrastructure decade, companies like G R Infraprojects will determine whether promises become reality. They won't get the headlines that tech companies generate. Their founders won't become celebrity entrepreneurs. But in the villages connected to markets, the cities linked by expressways, the power transmitted across states, their impact will be felt for generations. That's the ultimate measure of infrastructure success—not market capitalization or profit margins, but the permanent transformation of physical and economic geography.

The road from Jaisalmer to the National Stock Exchange has been long, dusty, and occasionally difficult. But it's been built with the same principles that guided that first village road: work hard, deal fairly, complete what you start. In infrastructure, as in life, there are no shortcuts. There's only the road, and those with the patience and capability to build it.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube