Gravita India: The Circular Economy Champion

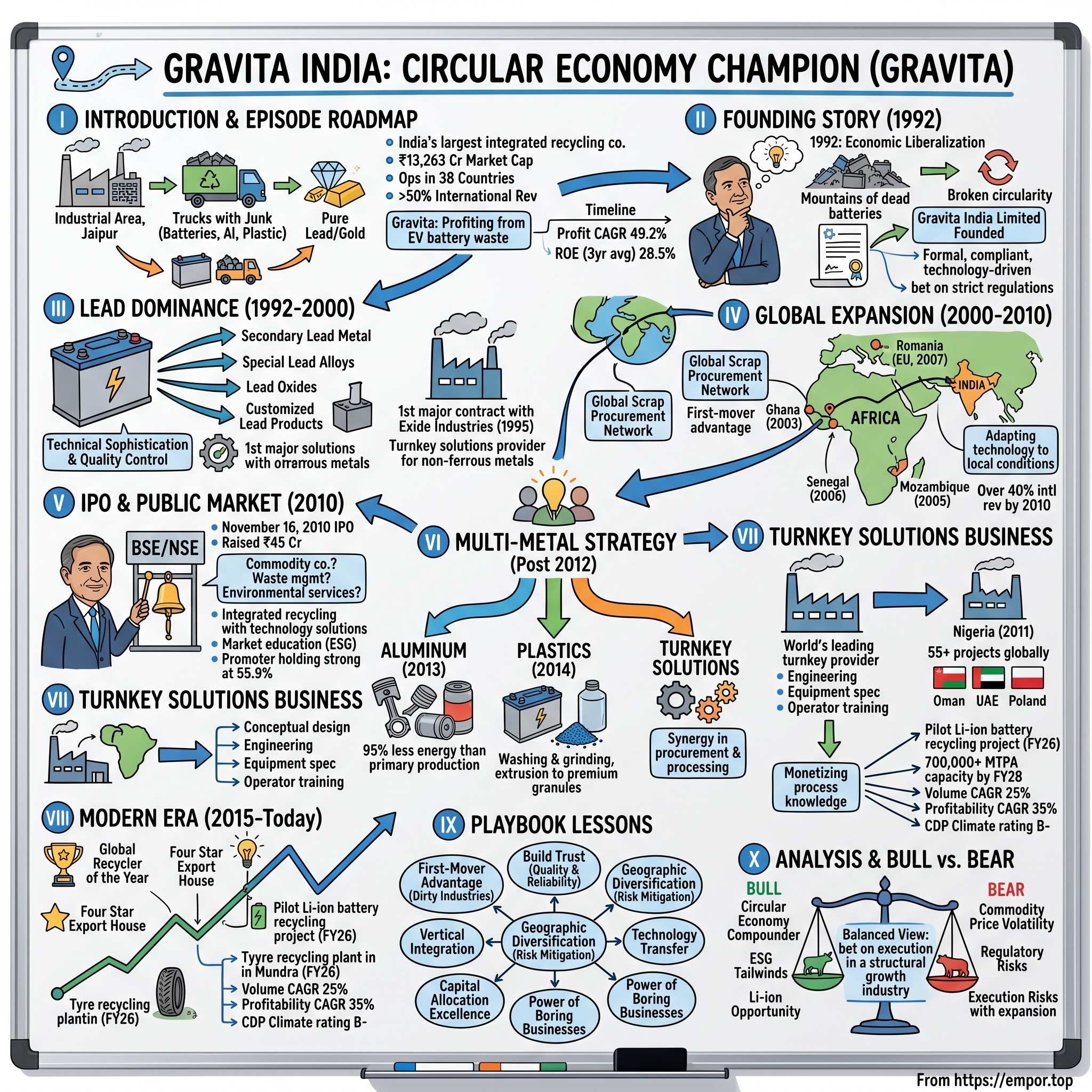

I. Introduction & Episode Roadmap

Picture this: In a nondescript industrial area outside Jaipur, trucks laden with what most would consider worthless junk—dead car batteries, aluminum scrap, plastic waste—roll through the gates of a facility that turns this detritus into pure gold. Not literally, of course, but close enough. This is Gravita India, a company that has quietly built one of the world's most sophisticated recycling empires while most investors were chasing software unicorns.

With a market capitalization of ₹13,263 crores and operations spanning 38 countries, Gravita has become India's largest integrated recycling company. More impressively, over 50% of its revenue flows from international markets—a rare feat for an Indian industrial company. But here's the kicker: while Tesla gets headlines for making electric vehicles, Gravita has positioned itself to profit from every dead battery those EVs will eventually produce.

The question that drives our story today isn't just how a Jaipur-based startup became the world's leading provider of battery recycling solutions. It's how founder Rajat Agrawal saw opportunity where others saw waste, built trust in an industry plagued by fly-by-night operators, and created a business model that turns environmental compliance from a cost center into a competitive moat.

This is a story about patient capital meeting urgent environmental needs. It's about building boring businesses in unsexy industries and discovering they're neither boring nor unsexy when you look at the returns. Over the past five years, Gravita has delivered a profit CAGR of 49.2%—numbers that would make any growth investor salivate, hidden inside a company that literally processes garbage.

Our journey will take us from the liberalizing Indian economy of 1992 through the company's audacious expansion into Africa, its pivot from recycler to technology provider, and its current position at the intersection of two megatrends: the circular economy and the electrification revolution. We'll explore how Gravita built four distinct recycling verticals, why it chose to list publicly in 2010, and what its 28.5% three-year average ROE tells us about the economics of well-run recycling businesses.

But this isn't just a success story. We'll also examine the bear case: commodity price volatility, regulatory risks, and why despite stellar fundamentals, the stock has returned only 21.44% over the past year. We'll dig into what happens when China changes its waste import policies, when environmental regulations tighten, and when new players eye your profitable niche.

The recycling industry sits at a fascinating crossroads. On one side, you have the world drowning in waste—7 billion tonnes annually and growing. On the other, you have governments mandating circular economy practices and manufacturers desperate for raw materials. Gravita has positioned itself right in the middle, with the technology, scale, and geographic reach to capitalize on both sides of this equation.

What makes this story particularly compelling for investors is the contrast between perception and reality. The market often views recyclers as commodity businesses with thin margins and high cyclicality. But Gravita's numbers tell a different story—one of pricing power, technological differentiation, and surprisingly resilient margins. It's a reminder that sometimes the best investments hide in plain sight, disguised as something far less attractive than they actually are.

II. Founding Story & The Recycling Vision (1992)

The year was 1992. India had just embarked on its historic economic liberalization under P.V. Narasimha Rao and Manmohan Singh. License Raj was crumbling, foreign investment was trickling in, and a generation of entrepreneurs was awakening to possibilities that had been locked away for decades. In Jaipur, far from the business corridors of Mumbai and Delhi, a young man named Rajat Agrawal was having an epiphany about garbage.

Agrawal wasn't born into industrial royalty. He didn't have the backing of a business house or access to old-money networks. What he had was an engineer's eye for inefficiency and an entrepreneur's instinct for opportunity. Walking through Jaipur's industrial areas, he noticed something others overlooked: mountains of dead lead-acid batteries piling up at mechanics' shops, scrap dealers hoarding them without proper processing capabilities, and battery manufacturers importing virgin lead at premium prices. The circularity was broken, and in that break, Agrawal saw his future. The India that Rajat Agrawal encountered in 1992 was a nation awakening from decades of socialist slumber. The liberalization process initiated in 1991 was prompted by a balance of payments crisis, dissolution of the Soviet Union, and sharp rise in oil prices from the Gulf War. The old certainties were crumbling, import licenses were being abolished, and entrepreneurs could finally dream beyond the narrow confines of the License Raj.

But Agrawal's vision wasn't about software or services—the glamorous sectors that would soon capture India's imagination. It was about lead, that heavy, toxic metal that powered the country's vehicles through millions of batteries. India's automotive sector was exploding, and with it, a mountain of battery waste was accumulating with no systematic solution. The usual practice was to throw batteries in household dustbins with other waste, with almost nil segregation, ending up in landfills without proper collection or recycling infrastructure.

Rajat Agrawal founded Gravita India Limited in 1992, starting with a simple premise: what if waste could be wealth? What if the toxic sludge that everyone wanted to dispose of could be transformed into pure lead that manufacturers desperately needed? This wasn't just recycling—it was alchemy for the industrial age.

The technical challenges were immense. Lead smelting isn't just melting metal; it's a complex metallurgical process requiring precise temperature control, chemical treatments, and sophisticated pollution control systems. One wrong move and you're either producing substandard metal that no manufacturer will touch, or you're poisoning the environment and facing regulatory shutdown. In 1992, most Indian recyclers operated in the informal sector—backyard operations with minimal safety standards and no environmental controls.

Agrawal's first facility in Jaipur was different. He invested in proper smelting furnaces, emission control systems, and—crucially—trained workers in safe handling procedures. This wasn't the cheapest way to operate, but it was the only way to build a business that could last. While competitors cut corners, Gravita invested in compliance, betting that environmental regulations would only get stricter and that customers would eventually pay a premium for responsibly recycled materials.

The early years were brutal. Banks didn't understand the business model—why would anyone pay good money for garbage? Battery manufacturers were skeptical—could recycled lead really match the quality of virgin metal? Environmental regulators were suspicious—wasn't this just another polluter in disguise? Every stakeholder needed convincing, and Agrawal spent those early years as much in conference rooms and regulatory offices as he did on the factory floor.

What saved Gravita was a combination of timing and technology. The economic liberalization meant Indian manufacturers were suddenly competing globally, and they needed cost advantages wherever they could find them. Recycled lead, when processed correctly, was chemically identical to virgin lead but significantly cheaper. As Gravita refined its processes and consistently delivered quality metal, word spread through India's tight-knit battery manufacturing community.

By the mid-1990s, Gravita had cracked the code on two critical aspects of the recycling business. First, procurement: building a network of scrap dealers and collection points that could deliver steady supplies of battery waste. Second, processing: developing proprietary techniques that maximized metal recovery while minimizing emissions. These weren't revolutionary innovations—similar processes existed in developed countries—but adapting them to Indian conditions, with local materials and labor costs, required significant ingenuity.

The real breakthrough came when Agrawal realized that lead recycling wasn't just about the metal—it was about the entire ecosystem. Batteries contain plastic casings, acid electrolytes, and other materials, all of which have value if processed correctly. Gravita positioned itself as a turnkey solutions provider for lead battery recycling and other non-ferrous metals, able to handle every aspect of the recycling process and extract maximum value from what others considered waste.

This comprehensive approach set Gravita apart from competitors who focused solely on lead extraction. By 1999, the company had developed capabilities in producing not just secondary lead, but also specialized lead alloys for specific battery applications, lead oxides for industrial use, and even recycled plastic granules from battery casings. Each additional product stream meant better economics and stronger relationships with customers who could now source multiple materials from a single, reliable supplier.

The environmental angle, initially a cost center, was becoming a competitive advantage. As India began implementing stricter pollution controls in the late 1990s, Gravita's early investments in compliance paid off. While competitors scrambled to upgrade their facilities or shut down entirely, Gravita was already meeting and exceeding standards. This regulatory moat would prove invaluable as the company began planning its next phase: international expansion.

Looking back, what's remarkable about Gravita's founding story isn't just that Agrawal saw opportunity in waste—plenty of entrepreneurs have that insight. It's that he had the patience and discipline to build a formal, compliant, technology-driven business in an industry dominated by informal players. He understood that in recycling, as in many industries, the race doesn't always go to the swift, but to those who build sustainable competitive advantages brick by brick.

The foundation was set. Gravita had proven that recycling could be both profitable and responsible, that Indian companies could match global standards in complex industrial processes, and that there was serious money to be made in the circular economy—decades before that term became fashionable. The question now was how far this model could scale.

III. Building the Core: Lead Recycling Dominance (1992–2000)

The late 1990s were make-or-break years for Indian manufacturing. The protected markets of the License Raj era were gone, replaced by cutthroat competition from imports and multinational corporations setting up Indian operations. In this environment, Gravita's value proposition—high-quality recycled lead at competitive prices—suddenly looked less like a niche offering and more like a strategic necessity for battery manufacturers fighting for survival.

Gravita's approach to building its lead recycling empire was methodical, almost boring in its consistency. While dot-com entrepreneurs in Bangalore were raising millions on PowerPoint presentations, Agrawal was perfecting the unglamorous art of smelting battery scrap. The company developed four distinct product lines from this single waste stream: secondary lead metal for new battery production, specialized lead alloys with precise chemical compositions, lead oxides for industrial applications, and finally, customized lead products for niche markets.

The technical sophistication required was considerable. Different battery types—automotive, industrial, inverter—contained different lead alloys. A car battery might use antimony-lead alloy for durability, while a UPS battery might use calcium-lead for lower maintenance. Gravita developed processes to not just recover lead, but to analyze, separate, and reconstitute these specific alloys. This wasn't just melting and pouring; it was reverse engineering at an industrial scale.

The real innovation was in quality control. Virgin lead has consistent properties—it comes from mines with known ore compositions. Recycled lead comes from thousands of different sources, each with potential contaminants. Gravita invested heavily in spectrographic analysis equipment and developed strict incoming material standards. They would reject entire truckloads of scrap if contamination levels were too high, even if it meant short-term supply shortages. This discipline paid off in customer trust.

By 1995, Gravita had secured its first major contract with Exide Industries, India's largest battery manufacturer. This wasn't just a customer win; it was a validation of the entire business model. If Exide—with its stringent quality requirements and international partnerships—could rely on Gravita's recycled lead, then the product had truly arrived. Other manufacturers quickly followed, and by 1997, Gravita was supplying to virtually every major battery producer in North India.

The environmental regulatory landscape was evolving rapidly during this period. The Batteries (Management and Handling) Rules came into effect, requiring battery manufacturers and dealers to ensure proper collection and recycling of used batteries. The Ministry of Environment introduced specific rules replacing earlier regulations, creating a formal framework for battery waste management. For Gravita, this wasn't a burden—it was a gift. Every new regulation raised barriers to entry and pushed informal recyclers further to the margins.

Gravita's response was to double down on environmental compliance. They didn't just meet standards; they exceeded them and then publicized that fact. The company began conducting regular environmental audits, publishing emission data, and inviting customers and regulators to inspect their facilities. In an industry plagued by fly-by-night operators and environmental disasters, Gravita positioned itself as the responsible choice.

The human element was crucial to this success. Lead recycling is dangerous work—exposure to lead dust can cause severe health problems. While informal recyclers often employed workers without proper protection, Gravita implemented comprehensive safety protocols. Regular blood lead level testing, mandatory protective equipment, and rotating work schedules to minimize exposure. This not only protected workers but also reduced turnover and built a skilled, loyal workforce that understood the complexities of the recycling process.

Over two decades, the company grew significantly and came to be recognized globally for exceptional customer service and technical expertise. The company's three decades of experience in polymer recycling ran parallel to its lead operations, creating synergies in procurement and processing. A scrap dealer bringing in batteries might also have plastic waste; a customer buying lead might need recycled plastics for other applications. These adjacencies, seemingly minor at first, would later become the foundation for Gravita's multi-vertical strategy.

Financial discipline was another differentiator. The recycling business is working capital intensive—you need to buy scrap upfront, process it, and then wait for customer payment. Many recyclers failed not because their technology was inferior but because they couldn't manage cash flows. Gravita developed sophisticated inventory management systems, negotiated favorable payment terms with suppliers, and maintained strong banking relationships. They treated working capital management as a core competency, not an afterthought.

The trust-building exercise extended beyond customers to suppliers. Gravita established a network of authorized collection centers, training scrap dealers in proper battery handling and offering premium prices for properly sorted materials. They created a win-win ecosystem where everyone from the neighborhood kabadiwala (scrap dealer) to large industrial clients benefited from participating in the formal recycling economy.

By 1998, Gravita was processing over 12,000 metric tons of battery scrap annually, making it one of India's largest formal sector recyclers. But more importantly, they had established a template for how to build a sustainable recycling business: invest in technology, prioritize compliance, build trust through transparency, and create value for all stakeholders. These principles would guide the company as it embarked on its next ambitious phase.

The numbers told the story of transformation. From a single furnace operation in 1992, Gravita had grown to multiple processing lines with sophisticated pollution control systems. Recovery rates had improved from 65% to over 85%, meaning more metal extracted from the same amount of scrap. Customer complaints had dropped to near zero, and the company was generating consistent profits that could fund further expansion.

The stage was set for Gravita's next act. The Indian market was becoming saturated—there were only so many battery manufacturers to supply. But Agrawal had been studying global recycling markets and noticed something interesting: developing countries in Africa and Southeast Asia faced the same battery waste problems India had in 1992, but with even less recycling infrastructure. The question wasn't whether to expand internationally, but how to do it without losing the quality and compliance standards that had made Gravita successful. The answer would reshape the company's destiny.

IV. The Global Expansion Play (2000–2010)

The new millennium brought a new vision for Gravita. While Indian IT companies were following the sun to serve Western markets, Agrawal was looking at a different map entirely—one where the Democratic Republic of Congo's cobalt mines, Ghana's growing automotive sector, and Tanzania's industrial expansion represented not extraction opportunities but recycling goldmines. In 2000, Gravita made its first international foray, a move that would transform it from an Indian recycler into a global circular economy player.

Why Africa? The conventional wisdom would have suggested expansion into developed markets with established recycling industries. But Agrawal saw what others missed: Africa's rapidly growing economies were generating increasing amounts of battery waste with virtually no formal recycling infrastructure. The company built customer presence in more than 50 countries across Europe, America, Asia and Africa, with over 50% of revenue flowing from overseas markets. The regulatory frameworks were nascent, the competition was minimal, and the environmental damage from informal recycling was severe. It was India in 1992 all over again, but with the benefit of Gravita's hard-won expertise.

Ghana became the beachhead. In 2003, Gravita established its first African facility in Tema, Ghana's industrial hub. The challenges were immediate and overwhelming. Everything that could go wrong did. The port clearance for equipment took months instead of weeks. Local contractors didn't understand the specifications for pollution control systems. The power grid was unreliable, requiring expensive backup generators. Finding skilled workers who could handle complex smelting operations safely was nearly impossible.

But Gravita had learned from its Indian experience that building a recycling business wasn't just about installing furnaces—it was about creating an ecosystem. They brought in Indian technicians to train local workers, not just in operating equipment but in understanding the chemistry of lead recycling. They worked with local authorities to develop environmental standards rather than waiting for regulations to be imposed. Most importantly, they built relationships with local scrap dealers, teaching them how to identify and sort different types of batteries.

The Ghana operation became profitable within 18 months, faster than even Agrawal had projected. The reason was simple: pent-up demand. Battery manufacturers across West Africa had been importing virgin lead from overseas at premium prices. Suddenly, here was a local supplier offering quality recycled lead at 30% lower cost. Orders poured in not just from Ghana but from Nigeria, Ivory Coast, and Senegal.

Emboldened by Ghana's success, Gravita accelerated its African expansion. Mozambique came next in 2005, strategically chosen for its proximity to South African markets and Portuguese-speaking African nations. Then Senegal in 2006, serving Francophone West Africa. Manufacturing facilities were established in Romania, Ghana, Mozambique, Togo, Senegal, Tanzania, and Sri Lanka. Each new market brought unique challenges—different languages, currencies, regulatory frameworks, and business cultures—but the core model remained consistent: build trust through quality, ensure environmental compliance, and create value for local stakeholders.

The expansion into Romania in 2007 represented a different kind of ambition. This wasn't a developing market with limited recycling infrastructure; this was the European Union, with stringent environmental standards and established competitors. Gravita's Romanian facility was designed to be a showcase—state-of-the-art technology, zero-discharge systems, and automation levels that exceeded even Indian operations. The message was clear: an Indian company could compete with anyone, anywhere, on quality and environmental standards.

The global scrap procurement network that Gravita built during this period was perhaps its most valuable creation. Battery scrap is a peculiar commodity—it's generated everywhere but has value only if aggregated efficiently. Gravita established collection partnerships with automotive service chains, industrial battery users, and even government agencies across multiple continents. They created a reverse logistics network that could move scrap from collection points in rural Africa to processing facilities with remarkable efficiency.

Cultural navigation was crucial to international success. In Ghana, Gravita learned to work with traditional chiefs who controlled land usage. In Mozambique, they navigated the legacy of civil war and rebuilt trust in industrial development. In Romania, they had to overcome skepticism about an Indian company's ability to meet EU standards. Each market required not just business acumen but cultural sensitivity and patience.

The financial engineering behind this expansion was sophisticated. Rather than funding everything from India, Gravita established local subsidiaries that could access regional banking systems. They used letters of credit from international banks to finance scrap procurement, leveraging their Indian parent company's credibility while building local credit histories. This distributed financial model reduced currency risks and made the company more resilient to regional economic shocks.

Technology transfer became a strategic weapon. Gravita didn't just export Indian recycling technology; they adapted it to local conditions. The furnaces designed for Ghana's humid climate were different from those in Romania's temperate zone. The scrap sorting processes developed for African markets, where manual labor was abundant, differed from the automated systems in European facilities. This localization of technology made Gravita's operations more efficient and harder to replicate.

By 2008, when the global financial crisis hit, Gravita's international diversification proved its worth. While the Indian market contracted and commodity prices crashed, the company's African operations continued growing. The crisis had reduced virgin lead production globally, making recycled lead even more valuable. Gravita's presence across multiple markets allowed it to shift resources to where demand was strongest, maintaining profitability when purely domestic players were struggling.

The human stories from this expansion period are remarkable. Indian engineers who had never left Rajasthan found themselves training workers in Mozambique. Ghanaian technicians became experts in lead metallurgy and were sent to establish operations in Tanzania. A Romanian environmental engineer developed pollution control innovations that were implemented across Gravita's global operations. The company wasn't just recycling batteries; it was creating a global cadre of recycling professionals.

Competition began to notice. International recycling companies that had ignored African markets suddenly saw Gravita's success and tried to enter. But Gravita had first-mover advantages that were hard to overcome: established supplier relationships, trained local workforces, and most importantly, trust built over years of consistent operations. When a Chinese competitor tried to undercut Gravita's prices in Ghana, customers stuck with Gravita because they knew the quality would be consistent and the environmental compliance real.

The regulatory landscape evolved during this period, generally in Gravita's favor. As African governments became more aware of the environmental damage from informal recycling, they implemented stricter standards that favored organized players. Gravita often found itself advising governments on policy, helping draft regulations that would create sustainable recycling industries. This wasn't corporate capture—it was genuine partnership in building environmental frameworks that balanced economic development with ecological protection.

By 2010, Gravita's international operations were contributing over 40% of revenues. The company had facilities in seven countries, employed over 500 people globally, and was processing more than 50,000 metric tons of battery scrap annually. But more than the numbers, Gravita had proven something important: that an Indian company could build a truly global industrial business, not by serving developed markets but by building infrastructure in developing ones.

The lessons from this decade of expansion were clear. First, emerging markets offered better opportunities than developed ones for companies willing to build foundational infrastructure. Second, environmental compliance could be a competitive advantage even in markets with weak regulations. Third, technology and knowledge transfer created more value than simple capital investment. These insights would prove crucial as Gravita prepared for its next transformation: becoming a public company.

V. The IPO and Public Market Journey (2010)

November 16, 2010, marked a watershed moment for Gravita. As Rajat Agrawal rang the ceremonial bell at the Bombay Stock Exchange, he wasn't just taking his company public—he was making a statement about the investability of India's circular economy. The company listed on both BSE and NSE, with the IPO consisting of 36,00,000 equity shares at ₹125 per share, raising ₹45 crores. In a year when investors were chasing technology stocks and retail chains, here was a recycling company asking for public market validation.

The decision to go public wasn't taken lightly. Gravita was profitable, had strong cash flows, and didn't desperately need capital. The existing operations could have been funded through internal accruals and debt. But Agrawal saw the IPO as more than a fundraising exercise—it was about institutionalizing the company, creating currency for acquisitions, and most importantly, signaling that recycling was a serious, scalable business worthy of public investment.

The roadshow for the IPO was an education exercise. Investment bankers initially struggled to position Gravita. Was it a commodity company? A waste management firm? An environmental services provider? The answer was all and none of these. Gravita had created a new category—integrated recycling with technology solutions—that didn't fit neatly into existing sectors. Analysts had to be taught about recovery rates, environmental compliance costs, and the economics of reverse logistics.

The IPO prospectus revealed fascinating details about the business that had been closely guarded. Gross margins of 12-15% might seem thin, but in the commodity recycling business, they were exceptional. The return on capital employed exceeded 20%, remarkable for an asset-heavy business. Most impressively, the company had negative working capital cycles in many markets—customers paid faster than Gravita paid suppliers, generating cash for growth.

Institutional investors were initially skeptical. The concerns were predictable: commodity price volatility, regulatory risks, dependence on informal sector supply chains, and environmental liabilities. Each roadshow presentation became a masterclass in recycling economics. Agrawal explained how Gravita's margins were protected through processing fees rather than commodity speculation, how environmental compliance created barriers to entry, and how the company's technology capabilities provided pricing power.

The retail investor response was more enthusiastic. India's growing environmental consciousness meant individual investors understood and appreciated Gravita's business model. The subscription numbers reflected this divergence—the retail portion was oversubscribed 2.8 times while institutional subscription was modest at 1.2 times. The market was sending a message: Main Street understood recycling's value even if Wall Street remained skeptical.

Post-listing, the challenges of being a public company became apparent immediately. Quarterly earnings pressure conflicted with the long-term nature of building recycling infrastructure. Commodity price movements, over which Gravita had no control, caused earnings volatility that markets punished severely. The stock price gyrated wildly in the first year, testing the conviction of both management and investors.

Gravita's response was to focus on what they could control: operational excellence and transparent communication. They began publishing detailed operational metrics—tons processed, recovery rates, new collection points established—giving investors visibility beyond just financial numbers. Quarterly earnings calls became educational sessions where management explained everything from lead metallurgy to African regulatory changes. Slowly, a dedicated investor base emerged that understood the business's long-term potential.

The capital raised from the IPO was deployed strategically. Rather than just expanding capacity, Gravita invested in technology upgradation across facilities. New furnaces with better heat recovery, automated material handling systems, and sophisticated emission control equipment were installed. The company also established a centralized R&D facility in Jaipur, focusing on improving recovery rates and developing new recycling processes. These investments didn't show immediate returns but positioned Gravita for the next phase of growth.

Being public also forced positive changes in corporate governance. Independent directors brought new perspectives, questioning assumptions and pushing for better capital allocation. The audit committee's scrutiny improved financial controls and risk management. The requirement for regular disclosures created discipline in operations—you can't hide problems when you have to report quarterly results.

The IPO also provided currency for acquisitions, though Gravita was selective in using it. Rather than buying competitors, they acquired strategic capabilities. A small technology company specializing in battery testing equipment was acquired to enhance quality control. A logistics firm with expertise in hazardous material transportation was brought in-house to improve scrap collection efficiency. These tuck-in acquisitions didn't make headlines but strengthened the company's competitive moat.

Market education remained a constant challenge. Sell-side analysts struggled to model the business, often missing the nuances of recycling economics. When lead prices fell, analysts would downgrade the stock, not understanding that lower raw material costs actually improved Gravita's margins as processing fees remained stable. When environmental regulations tightened, markets worried about compliance costs, missing that stricter rules eliminated competition and improved pricing power.

The public market journey also brought unexpected benefits. The listed status opened doors with large customers who wanted supply chain partners with transparent financials and strong governance. International banks became willing to provide working capital facilities at competitive rates. Government contracts, previously difficult to access, became available as Gravita's public company status provided credibility.

Employee motivation transformed with the introduction of stock options. Engineers and plant managers who had built the company now had a direct stake in its success. The ESOP program aligned long-term incentives and helped retain crucial talent. Watching their stock options appreciate as the company grew created an ownership culture that permeated the organization.

Five years post-IPO, by 2015, the transformation was evident. Market capitalization had grown from ₹450 crores at listing to over ₹1,800 crores. The company had used its listed status to raise additional capital through qualified institutional placements, funding international expansion without diluting promoter control. Promoter holding remained strong at 55.9%, signaling continued commitment to the business.

The IPO journey taught Gravita valuable lessons about balancing diverse stakeholder interests. Public market discipline improved operational efficiency and capital allocation. Transparency requirements strengthened the organization's processes and controls. Most importantly, being public provided a platform to evangelize about the circular economy to a broader audience. Every earnings call, every investor presentation, every annual report became an opportunity to demonstrate that sustainability and profitability weren't mutually exclusive.

The public listing also coincided with a global shift in how markets viewed environmental businesses. The 2010s saw the emergence of ESG investing, and suddenly Gravita's environmental credentials became a strength rather than a curiosity. International funds focused on sustainable investing began taking positions. The company that had struggled to explain its business model in 2010 found itself fielded as a pure-play circular economy investment by 2015.

Looking back, the IPO was about more than capital or credibility—it was about validation. It proved that an Indian recycling company could access public markets, deliver returns to shareholders, and maintain its environmental mission. The journey from that November day in 2010 to becoming a multi-thousand-crore market cap company wasn't always smooth, but it demonstrated that patient capital and sustainable business practices could create substantial value. The foundation was now in place for Gravita's next evolution: moving beyond lead into a multi-metal, multi-vertical recycling conglomerate.

VI. Diversification Beyond Lead: The Multi-Metal Strategy

By 2012, Gravita had a decision to make. The company dominated lead recycling in its markets, with limited room for organic growth without taking excessive risks. The easy choice would have been to stay focused, optimize operations, and deliver steady returns. But Agrawal saw a different opportunity: leveraging Gravita's recycling expertise across multiple materials. The question wasn't whether to diversify, but how to do it without losing the focus that had made the company successful.

The diversification strategy emerged from a simple observation: the infrastructure Gravita had built—collection networks, processing facilities, customer relationships—could handle more than just lead batteries. The company expanded into manufacturing and recycling units for lead metal & lead products, aluminium alloys and plastic granules. Scrap dealers who brought batteries also had aluminum waste from automotive parts. Customers who bought recycled lead needed recycled plastics for other applications. The adjacencies were obvious; the challenge was execution.

Aluminum became the first major diversification. The logic was compelling: aluminum recycling uses 95% less energy than primary production, making it economically attractive even at small scales. Gravita's existing relationships with automotive and industrial customers provided immediate market access. But aluminum metallurgy is completely different from lead processing—different furnaces, different temperatures, different alloy compositions. Gravita couldn't just repurpose existing equipment; they needed new capabilities.

The company's approach was characteristic: start small, learn fast, scale carefully. A pilot aluminum recycling line was established at the Jaipur facility in 2013. Rather than trying to process all types of aluminum scrap, Gravita focused on specific grades—automotive castings, extrusion scrap, used beverage cans—where they could ensure quality and consistency. They hired metallurgists from the aluminum industry, licensed technology from European equipment manufacturers, and spent months perfecting their processes before commercial production.

The aluminum business revealed an unexpected advantage: synergy in procurement. The same network that collected battery scrap could gather aluminum waste, reducing collection costs for both materials. Trucks that previously returned empty from battery collection runs now carried aluminum scrap, improving logistics efficiency. The incremental economics were attractive—the fixed costs of the collection infrastructure were already covered by the lead business, making aluminum recycling immediately profitable.

Plastic recycling came next, driven by customer demand rather than strategic planning. Battery manufacturers were asking if Gravita could handle the plastic casings from recycled batteries instead of sending them to other processors. The volumes were significant—every ton of batteries yielded roughly 100 kilograms of plastic. Initially treated as a waste disposal problem, Gravita realized this could become another revenue stream.

The plastic recycling operation started in 2014 with basic washing and grinding equipment to produce recycled flakes. But Gravita quickly moved up the value chain, investing in extrusion lines to produce premium recycled granules. The company focused on specialized grades including polypropylene, polycarbonate, HDPE, and ABS—engineering plastics with higher values and specific applications. Quality was paramount; recycled plastics had to meet the same specifications as virgin materials to gain customer acceptance.

The technical challenges in plastic recycling were different from metals. Contamination was harder to detect and remove. Different plastic types couldn't be mixed without destroying material properties. Color consistency was crucial for customer acceptance. Gravita developed sophisticated sorting technologies, including optical scanners and density separation systems, to ensure pure, consistent output. They also established dedicated supply chains for specific plastic grades, working with industrial users who generated clean, segregated waste.

What made Gravita's diversification successful was the discipline in choosing what not to do. They avoided commodity plastics where margins were thin and competition intense. They stayed away from electronic waste recycling despite its buzz, recognizing that the complexity and regulatory requirements were beyond their capabilities. Every diversification decision was filtered through strict criteria: Could they leverage existing infrastructure? Did they have technical competence? Were the economics attractive? Could they achieve leadership positions?

The turnkey solutions business emerged as an unexpected fourth vertical. As Gravita expanded internationally, governments and companies increasingly asked not just for recycling services but for help establishing their own recycling facilities. Could Gravita design a battery recycling plant for Nigeria? Could they train operators for a facility in Bangladesh? Could they provide ongoing technical support for operations in Vietnam?

Initially, Gravita was reluctant—wouldn't they be creating competitors? But they realized this was actually a higher-margin, capital-light business that leveraged their deepest competitive advantage: process knowledge. The company became the world's leading turnkey solutions provider for lead battery recycling. They began offering complete packages: facility design, equipment procurement, installation supervision, operator training, and ongoing technical support. The margins on these projects exceeded 25%, far higher than physical recycling.

The turnkey business had strategic benefits beyond immediate profits. It positioned Gravita as a technology company rather than just a recycler, commanding higher valuations. It created recurring revenue streams through maintenance contracts and technical support agreements. Most importantly, it generated market intelligence—Gravita knew about new recycling capacity being built globally before anyone else, allowing them to adjust their own expansion plans accordingly.

By 2016, the diversification strategy was showing results. Non-lead revenues had grown to 35% of total sales. More importantly, the diversified portfolio reduced earnings volatility—when lead prices were weak, aluminum might be strong. The different materials had different cycles, providing natural hedging. Customer relationships deepened as Gravita became a one-stop solution for multiple recycling needs.

The operational complexities of managing multiple verticals were significant. Each material required different expertise, equipment, and processes. Quality standards varied across products and markets. Regulatory requirements differed for hazardous materials like lead versus non-hazardous materials like aluminum. Gravita responded by creating dedicated business units with separate P&L responsibility while maintaining shared services for procurement, logistics, and administration.

Human capital became the binding constraint on diversification. Finding people who understood both recycling technology and business management was difficult. Gravita established its own training academy, taking engineering graduates and putting them through 18-month programs covering everything from metallurgy to environmental compliance. They also began hiring from adjacent industries—aluminum smelters, plastic processors, engineering consultancies—bringing in specialized expertise.

The investment in R&D intensified during this period. Gravita established material-specific research teams focused on improving recovery rates and developing new applications for recycled materials. They partnered with academic institutions for fundamental research while keeping applied development in-house. Patents were filed for novel processes, though the real intellectual property was in the accumulated know-how that couldn't be easily replicated.

Market positioning evolved with diversification. Gravita was no longer just a lead recycler but an integrated circular economy company. Marketing messages shifted from emphasizing individual materials to highlighting comprehensive recycling solutions. The company began participating in sustainability conferences, not just metals tradeshows. Customer conversations moved from procurement departments to sustainability teams, opening new commercial opportunities.

The financial metrics validated the strategy. Return on capital employed remained above 20% despite significant growth investments. EBITDA margins improved as higher-margin businesses like turnkey solutions grew. Most remarkably, the company maintained its capital efficiency—revenue per employee and revenue per unit of invested capital actually increased during the diversification period.

By 2018, Gravita had successfully transformed from a single-product company to a diversified recycling conglomerate. The four verticals—lead, aluminum, plastics, and turnkey solutions—each had distinct competitive advantages while sharing common infrastructure. The company could offer customers comprehensive recycling solutions while maintaining leadership in individual categories. The diversification hadn't diluted focus; it had multiplied capabilities.

The lessons from this diversification were nuanced. Success came not from abandoning core competencies but from extending them into adjacent areas. The discipline to say no to attractive but unrelated opportunities was as important as the courage to enter new businesses. Most critically, diversification worked because it was customer-driven rather than strategy-driven—Gravita expanded into areas where existing relationships and capabilities created natural advantages.

VII. Technology & Innovation: The Turnkey Solutions Business

The transformation of Gravita from a recycling operator to a technology provider began with a simple request in 2011. A Nigerian battery manufacturer wanted to establish their own recycling facility but lacked the technical expertise. Could Gravita help? The initial instinct was to decline—why enable potential competition? But Agrawal saw a different angle: what if Gravita could monetize its accumulated knowledge without deploying capital?

The first turnkey project was a modest 5,000-ton-per-year lead recycling facility in Lagos. Gravita provided everything: conceptual design, detailed engineering, equipment specifications, procurement support, installation supervision, and operator training. The project took 18 months and generated revenues of $3 million with EBITDA margins exceeding 30%. More importantly, it proved that Gravita's process knowledge had value independent of its physical operations. Word spread quickly in the global recycling community. Gravita had already executed more than 55 turnkey projects in different countries, establishing itself as the world's leading provider of recycling solutions. The company had developed something unique: the ability to transfer not just technology but entire recycling ecosystems to new markets.

What made Gravita's turnkey offering compelling wasn't just the hardware—anyone could sell furnaces and pollution control equipment. It was the software: the operational know-how accumulated over decades. How do you optimize smelting temperatures for different battery chemistries? How do you manage acid neutralization in tropical climates versus temperate ones? How do you train operators who have never seen industrial equipment? These were questions Gravita could answer with specificity born from experience.

The business model evolved rapidly. Gravita became a design/engineering solution provider for Lead Battery Recycling Plants, providing comprehensive turnkey solutions with cost-effective waste battery recycling process & environment-friendly technology for Lead industries. Projects ranged from small 3,000-ton facilities for local markets to massive 50,000-ton plants for national champions. Each project was customized—the company provided tailor-made solutions for Lead recycling projects and designed the latest state-of-the-art technology equipment as per the customer's specific country environmental norms.

The technology portfolio was comprehensive. Basic services included plant layout and engineering design, equipment specification and procurement, installation supervision and commissioning. Advanced offerings encompassed process optimization, automation integration, and even operational management contracts. The company also provided technical consultation for lead acid battery recycling and smelting, advanced PLC-based control and monitoring systems, and flexible annual maintenance contracts.

Geographic reach expanded dramatically. With over 70 successful recycling projects globally, including Qatar, UAE, Saudi Arabia, Poland and Chile, Gravita wasn't just serving developing markets—they were competing with European technology providers in sophisticated markets. With 12 state-of-the-art manufacturing facilities, the company became the world's leading turnkey recycling solution provider, having delivered 71+ projects to date.

The consulting services division emerged as a natural extension. Gravita's consulting services assisted organizations in complying with government policies such as Extended Producer Responsibility (EPR) and Battery Waste Management. Companies needed help navigating complex regulatory frameworks, designing collection systems, and implementing compliance protocols. Gravita's experience across multiple jurisdictions made them uniquely qualified to provide this guidance.

The intellectual property strategy was nuanced. Rather than relying solely on patents, which could be circumvented or ignored in many markets, Gravita focused on building tacit knowledge—the kind that couldn't be easily copied. They developed proprietary process control software, custom alloy formulations, and specialized training programs. The real moat was the integration of these elements into a coherent system that delivered consistent results.

Training became a differentiator. Gravita established a technical training center in Jaipur where client personnel spent weeks learning not just equipment operation but the underlying science of recycling. They created detailed operating manuals in multiple languages, developed virtual reality training modules for hazardous procedures, and provided ongoing remote support through digital platforms. This comprehensive approach meant that Gravita-designed plants actually operated at promised efficiency levels, unlike many competitor installations.

The financial model for turnkey projects was sophisticated. Projects were structured in phases—feasibility study, detailed engineering, equipment supply, installation, commissioning—with payments tied to milestones. This reduced client risk while ensuring Gravita's cash flows. Maintenance contracts provided recurring revenue streams that could last decades. Some projects included performance guarantees where Gravita's compensation was tied to actual recovery rates and environmental compliance.

Competition emerged from unexpected quarters. Chinese equipment manufacturers offered cheaper alternatives, though often with inferior technology and minimal support. European engineering firms provided sophisticated solutions but at premium prices and without understanding of developing market constraints. Gravita occupied the sweet spot—proven technology at reasonable prices with deep understanding of challenging operating environments.

The strategic value of the turnkey business extended beyond direct revenues. Every project provided market intelligence about global recycling capacity, regulatory trends, and technology evolution. Client relationships often led to other opportunities—equipment upgrades, capacity expansions, or new recycling verticals. The installed base of Gravita-designed plants created a natural market for spare parts and technical services.

Risk management was crucial. Turnkey projects involved multiple risks—technology performance, execution delays, payment defaults, and political instability in some markets. Gravita developed sophisticated risk assessment frameworks, insisted on letter of credit payments, and partnered with export credit agencies for project financing. They also maintained a roster of trusted local partners who could handle civil construction and basic installation, reducing execution risks.

By 2018, the turnkey solutions business was contributing over 15% of Gravita's revenues with EBITDA margins exceeding 35%. But more importantly, it had transformed the company's positioning. Gravita was no longer seen as just a recycler but as a technology company that happened to also operate recycling facilities. This perception shift was reflected in valuation multiples—technology companies commanded higher valuations than commodity processors.

The knowledge transfer went both ways. Insights from turnkey projects improved Gravita's own operations. A novel emission control system developed for a Middle Eastern client was subsequently implemented across Gravita's facilities. A material handling innovation created for a space-constrained Asian plant improved efficiency in Indian operations. The turnkey business became an R&D engine that benefited the entire organization.

Human capital development accelerated through the turnkey business. Engineers who designed plants developed broader perspectives than those who only operated them. Project managers who handled international installations built capabilities in cross-cultural communication and complex stakeholder management. The turnkey division became a leadership development pipeline, producing executives who understood both technology and business.

The ecosystem effects were substantial. Gravita's success in turnkey projects elevated India's reputation in global recycling technology. Indian equipment manufacturers benefited from specifications in Gravita-designed plants. Indian engineering talent found opportunities in international recycling projects. The company had effectively created an export industry around recycling technology, with Gravita as the anchor.

Looking ahead, the turnkey business positioned Gravita perfectly for the next wave of recycling demand. As governments worldwide implemented extended producer responsibility regulations and circular economy mandates, the need for recycling infrastructure would explode. The electric vehicle revolution would require massive lithium-ion battery recycling capacity. E-waste regulations would drive demand for sophisticated recovery systems. In each of these areas, Gravita's proven ability to design, build, and operate recycling facilities would be invaluable.

VIII. Modern Era: Scale, Sustainability & Recognition (2015–Today)

The transformation of Gravita from a successful recycler to a global sustainability champion accelerated dramatically after 2015. The Paris Climate Agreement had just been signed, ESG investing was moving from niche to mainstream, and suddenly, companies that had been quietly building circular economy infrastructure for decades found themselves at the center of the zeitgeist. For Gravita, this wasn't a pivot—it was vindication of a strategy pursued since 1992.The numbers validated everything. Company has delivered good profit growth of 49.2% CAGR over last 5 years, a staggering achievement for a capital-intensive industrial business. Company has a good return on equity (ROE) track record: 3 Years ROE 28.5%—metrics that would make any software company envious, achieved by a company that literally processes garbage. The transformation wasn't just financial; it was philosophical. Gravita had proven that environmental responsibility and shareholder returns weren't mutually exclusive.

Recognition came from unexpected quarters. Mr Rajat Agrawal, Chairman and MD received the prestigious Global Recycler of the Year award from MRAI during IMRC 2025! This wasn't just a personal accolade but validation of Gravita's approach to building a sustainable recycling business. The company achieved "Four Star Export House" status from the Directorate General of Foreign Trade, Ministry of Commerce & Trade, Government of India, acknowledging its contribution to India's export economy.

The scale achieved by 2024 was remarkable. Market Cap: 13,201 Crore with Revenue: 4,001 Cr and Profit: 338 Cr. The company had grown from a single facility in Jaipur to manufacturing facilities in Jaipur (Rajasthan), Kathua (J&K), Mundra (Gujarat), and Chittoor (AP) in India, plus operations in Romania, Ghana, Mozambique, Togo, Senegal, Tanzania, and Sri Lanka. The strategic expansion continued unabated. Gravita India is setting up a pilot project for lithium-ion battery recycling in FY 26, with a total investment of INR 70-100 crore, recognizing the massive opportunity in EV battery recycling. The company is planning to establish tyre recycling plant in Mundra, India, expected to be operational by FY26, with an initial capacity of 9,000 tons per annum. These weren't random diversifications but calculated bets on the future of the circular economy.

The company has outlined a capex plan of over INR 600 crores up to FY27, mostly self-funded without significant new debt—a testament to the cash-generating capability of the business. The target was ambitious: 700,000+ MTPA capacity by FY28, with the company targeting overall volume growth of 25% CAGR and profitability growth of 35% CAGR over the next 3-4 years.

Environmental credentials became increasingly important as ESG investing went mainstream. Gravita India secured a respectable B- grade in its maiden CDP Climate rating, joining the ranks of global companies transparent about their climate impact. The company's commitment went beyond compliance—they were actively reducing their carbon footprint while helping others do the same through recycling.

The recognition extended to industry awards. Gravita was awarded the Best Employer 2024 Award for All Round Performance from The Employers' Association of Rajasthan. The company was honored with the Leading Refined Lead Brand award at the MCX Awards 2024. Each accolade reinforced Gravita's position as not just a recycler but a leader in sustainable business practices.

The human capital story was equally impressive. From a handful of employees in 1992, Gravita had grown to employ over 3,350 people globally by FY24. The company had created an ecosystem of skilled professionals—metallurgists, environmental engineers, logistics experts—all united by the mission of turning waste into wealth. The employee stock ownership program ensured that this workforce was invested, literally and figuratively, in the company's success.

Technology leadership accelerated during this period. Gravita is developing in-house technologies for refining metals from lithium-ion batteries and expanding its R&D capabilities to support its new recycling projects. The company wasn't just adopting existing technologies but creating new ones, filing patents, and developing proprietary processes that would define the next generation of recycling.

The financial performance validated the strategy. In Q1 FY26, Gravita achieved YoY growth of 12% in volumes, 15% in revenue, 22% in EBITDA, and 39% in PAT, with ROIC remaining healthy at 28%. These weren't the numbers of a mature, slow-growth industrial company but of a dynamic business capturing a massive opportunity.

Global operations continued to expand strategically. Gravita has signed an MoU to develop a battery recycling plant via JV in Oman with an annual capacity of 6000 metric ton per annum in Phase I, expanding entry into the Middle East. The company's network spread across 70+ countries with customer presence in 38+ countries, making it a truly global player.

The shift in business mix was deliberate and strategic. Value-added product contribution grew by 47%, moving away from commodity products toward specialized, higher-margin offerings. The non-lead business was targeted to exceed 30% of revenues, reducing dependence on any single material. This wasn't diversification for its own sake but a conscious effort to build multiple growth engines.

Sustainability wasn't just a buzzword but embedded in operations. The company set ambitious targets: utilizing 30%+ renewable energy and continuously improving recovery rates to minimize waste. Every ton of material recycled represented not just revenue but carbon emissions avoided, resources conserved, and environmental damage prevented.

The market positioning evolved significantly. Gravita was no longer competing just with other recyclers but positioning itself as an alternative to mining companies. Why dig new mines when existing materials could be recycled infinitely? This narrative resonated with customers, regulators, and investors increasingly concerned about resource scarcity and environmental impact.

Looking at the competitive landscape, Gravita had built formidable moats. The global scrap procurement network couldn't be replicated quickly. The technical expertise accumulated over decades created barriers to entry. The regulatory compliance track record opened doors that remained closed to newcomers. Most importantly, the trust built with stakeholders—from scrap dealers in African villages to Fortune 500 customers—was irreplaceable.

The integration of digital technologies transformed operations. IoT sensors monitored furnace performance in real-time. AI algorithms optimized material blending for maximum recovery. Blockchain technology was being explored for supply chain transparency. This wasn't your grandfather's recycling company but a modern industrial enterprise leveraging cutting-edge technology.

Customer relationships deepened and evolved. Long-term contracts with minimum volume commitments provided revenue visibility. Technical partnerships for developing new alloys created switching costs. Sustainability reporting services helped customers meet their ESG goals. Gravita wasn't just a supplier but a partner in customers' sustainability journeys.

The regulatory tailwinds strengthened globally. Extended Producer Responsibility regulations expanded to more countries and materials. Carbon pricing made recycling more economically attractive versus primary production. Import restrictions on waste forced countries to develop domestic recycling infrastructure. Each regulatory change reinforced Gravita's business model.

By 2024, Gravita had transformed from a regional recycler to a global circular economy champion. The company that started with a single furnace in Jaipur now operated across continents, recycled multiple materials, provided technology solutions, and was preparing for the next wave of opportunities in lithium-ion batteries and other emerging waste streams. The foundation was set for the next phase of growth, with sustainability not as a constraint but as the core driver of value creation.

IX. Playbook: Business & Investing Lessons

After three decades of building Gravita from a single-furnace operation to a global recycling powerhouse, certain patterns emerge—lessons that transcend the specifics of lead smelting or aluminum processing and speak to fundamental truths about building enduring businesses in challenging industries. These aren't theoretical frameworks but battle-tested principles forged in the furnaces of Jaipur and refined in the markets of Africa.

First-Mover Advantage in Regulated, "Dirty" Industries

The most valuable businesses often hide where others fear to tread. When Gravita entered lead recycling in 1992, the industry was dominated by informal operators with questionable environmental practices. Rather than seeing regulation as a burden, Agrawal recognized it as an opportunity. Every new environmental standard raised barriers to entry and eliminated informal competition. By moving first into compliance—investing in pollution control when it wasn't mandatory, obtaining certifications before they were required—Gravita turned regulatory evolution into competitive advantage. The lesson: in industries heading toward stricter regulation, being ahead of the curve creates a moat that only widens over time.

Building Trust in Commodity Businesses Through Quality and Reliability

Recycled materials face an inherent trust deficit—customers assume virgin materials are superior. Gravita overcame this through relentless focus on quality consistency. They rejected profitable orders if material standards couldn't be guaranteed. They published detailed specifications and stood behind them with warranties. They invited customers to audit facilities. This obsession with quality transformed a commodity into a differentiated product. The broader principle: in commodity businesses, reliability is the ultimate differentiator. When customers can't distinguish your product from competitors' on features, they'll pay premiums for the confidence that you'll deliver exactly what you promise, every time.

Geographic Diversification as Risk Mitigation in Cyclical Markets

Gravita's expansion into Africa wasn't just about growth—it was sophisticated risk management. Different markets have different cycles. When Indian lead demand weakened during economic slowdowns, African markets might be growing. When European environmental regulations tightened, creating opportunities, Asian markets provided stability. This geographic hedging smoothed earnings volatility that plague single-market players. But the key insight goes deeper: Gravita didn't just enter multiple markets; they chose complementary markets with different drivers, regulatory timelines, and competitive dynamics. The lesson: geographic diversification works best when markets are economically uncorrelated.

The Power of Vertical Integration: From Scrap Procurement to Finished Products

Gravita's vertical integration wasn't about controlling the entire value chain for control's sake—it was about capturing value where it accumulated. In recycling, margins are made at two points: procurement (buying scrap below its metal value) and processing (converting scrap to usable materials). By integrating both, Gravita captured the entire margin stack. But more importantly, vertical integration created information advantages. Controlling procurement meant understanding supply dynamics before competitors. Operating processing facilities revealed demand patterns others missed. This information asymmetry enabled better capital allocation and strategic decisions.

Technology Transfer as a Business Model Multiplier

The turnkey solutions business revealed a profound insight: in industrial businesses, process knowledge can be more valuable than physical assets. By packaging their expertise into transferable solutions, Gravita created a capital-light, high-margin revenue stream that actually strengthened their core business. Every turnkey project provided market intelligence, customer relationships, and technology insights that improved their own operations. The broader principle: any company with deep process expertise should consider how to monetize that knowledge without compromising competitive advantage.

Managing Working Capital in the Recycling Business

Recycling is inherently working capital intensive—you buy scrap, process it, then wait for payment. Gravita turned this challenge into competitive advantage through sophisticated working capital management. They negotiated payment terms where customers paid faster than suppliers. They used letters of credit to reduce payment risk. They maintained optimal inventory levels using predictive analytics. Most cleverly, they structured international operations to use local banking relationships, reducing currency exposure and improving terms. The lesson: in capital-intensive businesses, working capital management isn't just treasury function—it's strategic capability that determines competitive position.

Why Sustainability Can Be Profitable at Scale

Gravita proved that environmental responsibility and profitability aren't mutually exclusive—they're mutually reinforcing at scale. Environmental compliance created barriers to entry. Sustainability credentials attracted premium customers. Resource efficiency improved margins. Carbon credits provided additional revenue. ESG positioning attracted patient capital at lower costs. The key insight: sustainability is profitable when it's built into the business model from inception, not bolted on as an afterthought. Companies that view environmental compliance as cost center will always struggle against those who see it as competitive advantage.

The Importance of Patient Capital and Long-Term Thinking

Gravita's journey required extraordinary patience. The first facility took years to reach profitability. International expansions required upfront investments with uncertain returns. Technology development consumed resources without immediate payback. Yet this patient approach created compounding advantages. Early investments in compliance paid off when regulations tightened. Geographic expansion created network effects in procurement. Technology investments enabled the high-margin turnkey business. The lesson: in industrial businesses, competitive advantages compound slowly but surely. Patient capital that can withstand short-term volatility captures long-term value.

Creating Ecosystems, Not Just Businesses

Gravita didn't just build recycling facilities—they created entire ecosystems. They trained scrap dealers, educated customers, worked with regulators, developed local suppliers, and built community relationships. This ecosystem approach created switching costs beyond simple commercial relationships. A competitor might match Gravita's prices or even technology, but they couldn't quickly replicate the entire ecosystem. The principle: sustainable competitive advantage comes from creating interdependencies that make your business essential to stakeholders' success.

The Value of Boring Businesses

Perhaps the most important lesson from Gravita's story is the value of boring businesses. While markets chase exciting narratives—AI, crypto, biotech—enormous value is created in mundane industries like recycling. These businesses have several advantages: less competition for assets and talent, more rational competitive dynamics, stickier customer relationships, and often, better economics than "exciting" industries. Gravita's 49.2% profit CAGR wasn't achieved despite being in a boring industry but because of it.

Operational Excellence as Strategy

In commodity businesses where products are undifferentiated, operational excellence becomes strategy. Gravita's focus on increasing recovery rates, reducing emissions, improving safety, and optimizing logistics wasn't just about efficiency—it was about building competitive advantage one basis point at a time. Small improvements compounded: 1% better recovery rates, 2% lower processing costs, 3% faster working capital turns. Over time, these marginal gains created insurmountable cost advantages.

The Network Effects in Recycling

Gravita discovered powerful network effects in recycling that aren't immediately obvious. The more collection points they established, the lower their procurement costs. The more materials they processed, the better their technology became. The more customers they served, the stronger their brand. The more geographies they entered, the more resilient their supply chain. These network effects created a flywheel where scale begat advantage begat scale.

Risk Management Through Diversification

Gravita's multi-metal, multi-geography, multi-business model strategy wasn't just about growth—it was sophisticated risk management. Lead price crashes were offset by aluminum strength. Indian regulatory changes were balanced by African stability. Technology services revenues smoothed recycling volatility. This diversification wasn't random but carefully orchestrated to create natural hedges. The lesson: in cyclical industries, diversification should be designed to reduce correlation, not just add revenue streams.

The Importance of Founder-Led Vision

Throughout Gravita's journey, founder leadership provided consistency of vision that professional management might have lacked. Agrawal's willingness to sacrifice short-term profits for long-term positioning, to enter difficult markets, to invest in compliance before required—these decisions required conviction that quarterly earnings-focused managers might not have possessed. The principle: in businesses requiring long-term transformation, aligned founder leadership can be invaluable.

Capital Allocation Excellence

Gravita's capital allocation track record is remarkable. They consistently achieved returns on invested capital exceeding 25% while growing rapidly. This wasn't luck but disciplined decision-making. They had clear hurdle rates for new investments. They walked away from acquisitions that didn't meet return thresholds. They reinvested in highest-return opportunities, whether that was geographic expansion, new verticals, or technology development. The lesson: in capital-intensive businesses, capital allocation skill is the ultimate differentiator between value creation and value destruction.

These lessons from Gravita's playbook aren't just applicable to recycling or even industrial businesses. They speak to fundamental principles of building enduring enterprises: the value of patience, the power of compounding advantages, the importance of ecosystem thinking, and the reality that boring businesses solving real problems often create more value than exciting ventures chasing ephemeral opportunities. In a world obsessed with disruption, Gravita's story reminds us that sometimes the best businesses are built not by breaking things but by fixing them, one recycled battery at a time.

X. Analysis & Bear vs. Bull Case

Bull Case: The Circular Economy Compounder

The bull case for Gravita isn't built on hope but on arithmetic. Start with the fundamentals: 49.2% profit CAGR over five years isn't a fluke—it's the result of structural advantages compounding. The 28.5% three-year average ROE demonstrates this isn't growth for growth's sake but profitable expansion. When a capital-intensive industrial business consistently generates returns approaching 30%, something special is happening beneath the surface.

The global leadership position in battery recycling with turnkey capabilities creates a powerful moat. Gravita has already executed more than 55 turnkey projects globally—each one a testament to their technical expertise and a barrier for competitors. When governments want to establish recycling infrastructure, when companies need to meet EPR obligations, when environmental compliance becomes mandatory, Gravita is often the first call. This isn't just market share; it's mind share in a critical, growing industry.

ESG tailwinds are transforming from nice-to-have to must-have. The European Union's Circular Economy Action Plan, India's Battery Waste Management Rules, and similar regulations globally aren't suggestions—they're mandates with penalties. Every new regulation expands Gravita's addressable market and increases barriers to entry. The company isn't riding a trend; it's positioned at the intersection of regulatory necessity and environmental urgency.

Promoter holding at 55.9% signals continued commitment and alignment. The Agrawal family hasn't been sellers but builders, reinvesting profits and maintaining control through decades of growth. This isn't a company being dressed up for sale but one being built for generations. When insiders own majority stakes and aren't selling despite massive appreciation, they're telling you something about future prospects.

Multi-geography, multi-product diversification provides resilience rare in industrial businesses. Operations across 38 countries mean no single market downturn can cripple results. Four distinct verticals—lead, aluminum, plastics, turnkey—create multiple growth engines. This isn't conglomerate complexity but synergistic diversification where capabilities in one area strengthen others.

The lithium-ion battery recycling opportunity could dwarf current operations. With EV adoption accelerating globally and batteries lasting 8-10 years, a tsunami of battery waste is coming. Gravita's pilot project for lithium-ion battery recycling positions them perfectly. They have the infrastructure, the technology, the regulatory expertise—everything except the waste stream, which is about to explode.

Valuation remains reasonable despite massive appreciation. At current levels, the company trades at forward P/E multiples that don't reflect the growth trajectory or quality of the business. Compare Gravita's metrics to global waste management leaders—higher growth, better returns, lower valuations. This disconnect won't persist indefinitely.

Bear Case: The Commodity Trap

The bear case starts with an uncomfortable truth: Gravita is ultimately a price-taker in commodity markets. When lead prices crash, as they do cyclically, margins compress regardless of operational excellence. The company can't control LME prices, and their processing fee model only partially insulates them from commodity volatility. History is littered with well-run commodity processors destroyed by adverse price movements.

Environmental regulation risks cut both ways. While stricter regulations help Gravita competitively, they also increase compliance costs and legal liability. One environmental accident—a fire, a spill, contamination—could result in massive fines, operational shutdowns, and reputation damage. In an industry handling hazardous materials, these aren't theoretical risks but constant threats.

The stock performance—up only 21.44% over the past year despite strong fundamentals—suggests market skepticism. Either investors see risks not reflected in reported numbers, or the market simply doesn't believe the growth story. When a company reports spectacular metrics but the stock languishes, it's worth asking what the market knows that the numbers don't show.

Competition from organized players entering recycling is intensifying. Amara Raja, Exide, and other battery manufacturers are backward integrating into recycling. Global waste management giants are eyeing emerging markets. Chinese recyclers with cost advantages are expanding internationally. Gravita's first-mover advantages are real but not insurmountable.

Dependence on global scrap availability creates vulnerability. Gravita doesn't control waste generation—they depend on others' consumption and disposal patterns. If battery life extends, if recycling at source improves, if consumption patterns change, Gravita's raw material supply could constrict. The company is essentially short innovation in battery longevity.

Working capital intensity remains a structural challenge. Despite excellent management, the business requires significant working capital to function. In credit crunches or banking crises, this dependency becomes a vulnerability. The company's growth is ultimately constrained by their ability to finance working capital efficiently.

Execution risks multiply with expansion. Every new geography brings regulatory complexity, cultural challenges, and operational risks. Every new vertical requires different expertise, equipment, and markets. The company is attempting multiple expansions simultaneously—lithium-ion batteries, rubber recycling, new geographies. Execution stumbles are probable, not just possible.