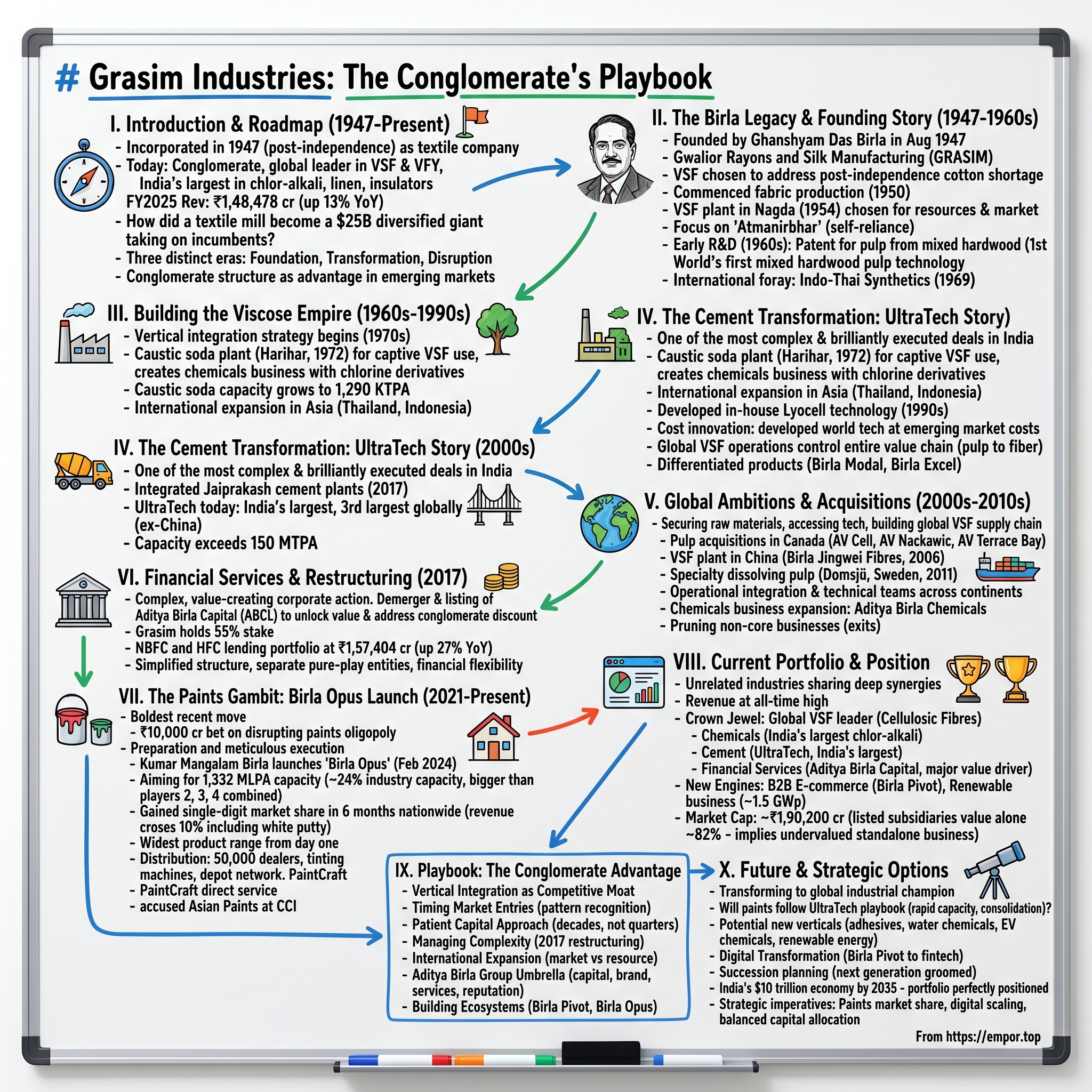

Grasim Industries: The Conglomerate's Playbook

I. Introduction & Episode Roadmap

The monsoon of 1947 brought both promise and peril to a newly independent India. While Jawaharlal Nehru's midnight speech still echoed across the subcontinent, a different kind of nation-building was taking shape in the boardrooms of Indian industrialists. Just days after India attained freedom in August 1947, Grasim Industries was incorporated as a textile company, marking the beginning of what would become one of India's most remarkable corporate transformations.

Today, Grasim stands as a conglomerate with revenue reaching an all-time high of ₹1,48,478 crore in FY2025, up 13% year-over-year. But the journey from a single textile mill to becoming the world's top VSF and VFY maker, India's largest producer of chlor-alkali, linen, and insulators is far more than a story of diversification—it's a masterclass in timing markets, building competitive moats through vertical integration, and knowing when to disrupt established oligopolies.

The central question that frames our exploration: How did a company founded to address India's post-independence cotton shortage evolve into a $25 billion revenue diversified giant that's now taking on Asian Paints' five-decade dominance? The answer lies not just in the Aditya Birla Group's capital strength, but in a uniquely Indian playbook of patient capital allocation, strategic patience spanning generations, and an uncanny ability to identify inflection points in India's economic development.

This episode traces three distinct eras of Grasim's evolution. First, the foundation years (1947-1990s) where viscose staple fiber became the cornerstone of an import substitution strategy. Second, the transformation decade (2000-2010) marked by the audacious UltraTech acquisition that created India's cement behemoth. And third, the current disruption phase where Birla Opus has become India's #3 decorative paints brand within just 6 months of pan-India operations, challenging entrenched players with a ₹10,000 crore war chest.

What makes Grasim particularly fascinating for students of business strategy is its approach to conglomerate management—a model often dismissed in Western markets but thriving in emerging economies. While American conglomerates like GE dismantled themselves, Grasim has proven that in markets with institutional voids, the conglomerate structure can be a competitive advantage rather than a burden.

II. The Birla Legacy & Founding Story (1947-1960s)

The story begins not with spreadsheets and strategy decks, but with vision and cotton—or rather, the lack thereof. In 1947, G.D. Birla envisioned that the country would face an acute shortage of cotton, and man-made fibres would be needed to supplement textile fibre availability for clothing. This wasn't mere speculation; it was prescient analysis of a nation that would soon clothe hundreds of millions while its agricultural sector struggled to modernize.

Ghanshyam Das Birla, already a towering figure in Indian industry and a close confidant of Mahatma Gandhi, understood that political independence meant little without economic self-reliance. Grasim was founded in August 1947, mere days after India attained freedom, as Shri G.D. Birla knew that a newly-independent nation would face an acute shortage of cotton for clothing, and decided to fill this gap with man-made fibres.

The name itself tells a story: Gwalior Rayons and Silk Manufacturing, or GRASIM for short, was incorporated on 25th August 1947. The choice of Gwalior wasn't random—the Maharaja had offered support, and the location provided strategic access to both raw materials and markets. But G.D. Birla's ambitions stretched beyond a single weaving unit.

In 1950, Grasim's first weaving unit successfully commenced fabric production. In 1951, the Maharaja of Gwalior offered land in Nagda to set up a VSF plant, with abundant water resources and proximity to textile markets in Bombay and Ahmedabad making it the right choice. This decision would prove transformational. By 1954, Grasim had set up its second manufacturing plant (15 TPD) at Nagda and began manufacturing viscose staple fibre.

The Nagda facility wasn't just another factory—it represented a philosophy. As India became independent, GD Birla embarked on a journey towards making India 'Atmanirbhar'. The town of Nagda itself became a testament to the Birla approach to industrialization. Nagda's growth is a testament to Grasim's efforts towards transforming the landscape, with quality educational institutions, a modern hospital with state-of-the-art medical facilities, and strong infrastructure, ranking among the cleanest places to live in India.

The real breakthrough came in the 1960s with the establishment of critical R&D capabilities. In the early 1960s, Grasim set up its Pulp and Engineering division at Nagda to boost commercial competitiveness, while the Birla Research Institute for Applied Sciences was established. This wasn't just incremental innovation—it was groundbreaking. The Institute filed the world's first patent to develop pulp from mixed hardwood, which was also the Aditya Birla Group's first-ever patent.

Think about the audacity of this moment: a company in a newly independent, largely agrarian nation was filing world-first patents. This research laid the foundation for technology to be used at Grasim's new plants subsequently set up in Harihar and Mavoor. The mixed hardwood technology solved a critical problem—India didn't have the vast softwood forests of Scandinavia or Canada, but it had abundant mixed hardwood that others considered unsuitable for pulp production.

VSF turned out to be a game-changer for India's textiles industry. While the world saw rayon as a cheap substitute for silk, Grasim positioned VSF as the democratic fiber—affordable, versatile, and perfectly suited for India's tropical climate. The fabric breathed like cotton but had the drape of more expensive materials. It could be blended with other fibers, dyed easily, and most importantly, could be produced at a scale that matched India's enormous domestic demand.

By the end of the 1960s, Grasim had also begun looking beyond India's borders. Indo-Thai Synthetics Company Ltd was incorporated in 1969 in Thailand and started operations in 1970, marking Aditya Birla Group's first foray into international ventures. This wasn't just international expansion for the sake of it—Thailand offered access to ASEAN markets, lower production costs, and importantly, a hedge against the License Raj restrictions that were beginning to constrain growth in India.

The foundation era established three principles that would guide Grasim for decades: First, identify fundamental gaps in India's development trajectory. Second, invest in technology and R&D to create proprietary advantages. Third, think globally even while solving local problems. G.D. Birla hadn't just built a textile company; he had created a platform for industrial expansion that his successors would leverage brilliantly.

III. Building the Viscose Empire (1960s-1990s)

The transformation from a textile manufacturer to a viscose empire represents one of the most underappreciated industrial stories in Indian business history. While software companies and tech unicorns capture headlines today, Grasim's methodical domination of the global VSF market offers timeless lessons in building sustainable competitive advantages.

The 1970s marked a crucial inflection point. In 1972, Grasim set up the world's first mixed hardwood plant at Harihar based on the patented technology, and established a plant to manufacture 33,000 TPA of caustic soda for captive use. This wasn't just vertical integration—it was the beginning of what would become Grasim's signature strategy: controlling the entire value chain from raw material to finished product.

The caustic soda plant decision reveals sophisticated strategic thinking. Caustic soda is essential for VSF production, but it also produces chlorine as a by-product. Rather than treat this as waste, Grasim would eventually build an entire chemicals business around chlorine derivatives. The chemicals business set up in 1972 to manufacture caustic soda for VSF expanded dramatically when Grasim's merger with Aditya Birla Chemicals in 2016 catapulted caustic soda capacity from 452 KTPA to 884 KTPA, with total capacity now at 1,290 KTPA.

The international expansion accelerated through the 1970s and 1980s with remarkable prescience about Asian economic development. Thai Rayon was incorporated in 1974, the second company in Thailand, operating in Viscose Rayon Staple Fiber. P.T Indo Bharat Rayon incorporated in 1980 produces Viscose Staple Fiber in Indonesia. Each facility wasn't just a production unit but a beachhead in rapidly growing Asian markets.

What's fascinating about this period is how Grasim navigated India's License Raj while simultaneously building an international footprint. During an era when getting permission to expand capacity by even 10% required months of bureaucratic wrangling, Grasim was setting up plants across Southeast Asia. This dual strategy—constrained growth at home, aggressive expansion abroad—would prove invaluable when India finally liberalized in 1991.

The technology focus never wavered. In the 1990s, Grasim developed in-house capabilities for Lyocell technology, establishing a 0.5 TPD Lyocell pilot plant in 1993 at 20% of the cost of setting up a similar plant in Europe. This cost innovation would become a hallmark of the Birla approach—achieving developed world technology at emerging market costs.

By the late 1990s, Grasim had quietly built one of the world's largest VSF operations, though few outside the textile industry noticed. The company controlled everything from pulp production to fiber manufacturing to chemical inputs. When competitors bought pulp on volatile global markets, Grasim produced its own. When others struggled with caustic soda availability, Grasim had captive production. This integration provided both cost advantages and supply chain resilience that would prove crucial during market downturns.

The numbers tell the story of dominance: Grasim became the largest exporter of Viscose Rayon Fiber in India with exports to over 50 countries, operating through Grasim Industries in India, Indo Bharat Rayon in Indonesia, Thai Rayon in Thailand, and Birla Jingwei Fibres in China. But what the numbers don't capture is the strategic patience required to build this empire. While tech companies measure progress in quarters, Grasim spent decades perfecting its VSF operations, accumulating advantages that would be nearly impossible for new entrants to replicate.

The viscose empire also demonstrated another crucial aspect of the Grasim playbook: the ability to transform commodity businesses into differentiated products. VSF could have remained a simple cotton substitute, but Grasim continuously innovated—developing specialized fibers for different applications, creating branded products like Birla Modal and Birla Excel, and working with fashion brands to position VSF as a sustainable, premium alternative to conventional fibers.

IV. The Cement Transformation: UltraTech Story (2000s)

The UltraTech acquisition stands as one of the most complex and brilliantly executed deals in Indian corporate history. It's a story of patience, strategic maneuvering, and ultimately, the creation of India's largest cement manufacturer with a capacity of 152.70 million tonnes per annum. But to understand its significance, we need to first understand the context.

The story begins in 2001 with what seemed like an opportunistic investment. Reliance Industries sold its entire 10% stake in L&T to Grasim Industries, when L&T was the largest cement manufacturer in India while Grasim was third-largest. Kumar Mangalam Birla, who had taken over the group in 1995 at age 28, saw something others missed: L&T was a conglomerate trying to be an engineering company, and its cement division, while excellent, was a distraction from its core business.

In 2002, Grasim increased its stake in L&T to 15% and attempted to launch an open offer for an additional 20% stake, which was stayed by SEBI over possible violation of takeover rules. This regulatory hurdle could have killed the deal, but it actually forced a more creative solution. In 2003, L&T announced it would demerge the cement business into UltraTech CemCo, with Grasim agreeing to acquire 8.5% stake from L&T, make an open offer for another 30%, and transfer its 15% stake in L&T to L&T Employees Welfare Foundation.

The structure was elegant: L&T got to focus on engineering, employees were protected, and Grasim gained control of a world-class cement business. The deal was executed in 2004, with Grasim obtaining management control of UltraTech with its 51% stake, while L&T retained 11.5%. The final price represented exceptional value—Grasim paid roughly $500 million for control of assets that would be worth tens of billions within a decade.

But acquiring UltraTech was just the beginning. What followed was a textbook case of value creation through operational excellence and strategic acquisitions. After acquisition, the combined capacity of Grasim and UltraTech went up to 31 million tonnes, making Grasim the largest producer in India and eighth largest in the world.

The integration revealed the power of Grasim's approach. While Grasim was strong in Southern markets, L&T was strong in the rest of India, and L&T's distribution network was vital to push Grasim's own brands. Rather than force immediate integration, Grasim allowed UltraTech to maintain its premium brand positioning, even permitting the use of the L&T brand for over a year post-acquisition.

The real masterstroke came in the subsequent decade of consolidation. In 2017, UltraTech acquired Jaiprakash Associates' six integrated cement plants for ₹16,189 crore—a deal that came when Jayprakash was in financial distress, allowing UltraTech to acquire assets at attractive valuations. This pattern would repeat: patient waiting for opportunities, swift execution when they arose, and meticulous integration afterward.

In 2010, Grasim demerged its cement subsidiary Samruddhi Cement, which contributed 76% of the company's turnover, and later that year merged it into UltraTech. This restructuring simplified the corporate structure and unlocked value by eliminating the holding company discount. It also sent a clear signal: UltraTech would be the vehicle for all cement ambitions.

The numbers validate the strategy. UltraTech today is India's largest manufacturer of cement and world's third-largest cement producer outside China, with total production capacity exceeding 150 MTPA. But beyond size, UltraTech achieved something more valuable: a distributed manufacturing footprint that minimized logistics costs, a premium brand that commanded pricing power, and operational metrics that matched global best practices.

The cement transformation also demonstrated Grasim's ability to manage capital allocation across cycles. Cement is notoriously cyclical, with periods of overcapacity followed by shortages. Many companies destroyed value by expanding at cycle peaks. Grasim/UltraTech consistently did the opposite—acquiring distressed assets during downturns and using strong cash flows during upturns to deleverage rather than chase growth.

What's particularly impressive is how the cement business provided the cash flows and credibility for Grasim's next phase of growth. The steady, predictable earnings from UltraTech gave Grasim the financial firepower to make bold bets like the paints entry, while the operational excellence demonstrated in turning around acquired cement assets gave stakeholders confidence in management's execution abilities.

V. Global Ambitions & Strategic Acquisitions (2000s-2010s)

While UltraTech was transforming Grasim's domestic profile, a parallel story was unfolding on the global stage. The international expansion of the 2000s and 2010s wasn't just about scale—it was about securing raw materials, accessing technology, and building a truly global supply chain for the VSF business.

The Canadian pulp acquisitions marked a strategic pivot. AV Cell Inc., a joint venture with Tembec Canada established in 1998, produced softwood and hardwood pulp for internal consumption, and in 2012, Grasim and Tembec acquired AV Nackawic Inc. for dissolving pulp production. These weren't glamorous deals that made headlines, but they solved a critical problem: securing high-quality pulp supply in an increasingly competitive global market.

In 2006, Grasim acquired a VSF plant in China, leading to the formation of Birla Jingwei Fibres Company. This was audacious—entering China, the world's manufacturing hub, not as a buyer but as a producer. The logic was compelling: be close to the world's largest textile manufacturing base, understand Chinese cost structures, and hedge against potential trade barriers.

The Swedish acquisition added another dimension. In 2011, Grasim acquired a key stake in Domsjö Fabriker AB, Sweden. Domsjö wasn't just any pulp producer—it was a specialty dissolving pulp manufacturer with advanced technology and a reputation for quality. In 2012, the company acquired AV Terrace Bay, Canada, further strengthening its dissolving pulp portfolio.

What's remarkable about these acquisitions is their strategic coherence. Each deal addressed a specific weakness or opportunity in the VSF value chain. Canadian assets provided softwood pulp and geographical diversification. The Swedish acquisition brought technology and access to European markets. The Chinese plant offered proximity to customers and insight into competitive dynamics. Together, they transformed Grasim from an Indian VSF producer into a global player with manufacturing across four continents.

The integration of these global assets showcased operational sophistication often underestimated in Indian companies. Managing plants in Sweden, Canada, Thailand, Indonesia, and China requires not just capital but cultural sensitivity, technological expertise, and supply chain mastery. Grasim developed centralized technical teams that could troubleshoot problems globally, implemented common IT systems across geographies, and created knowledge-sharing platforms that allowed innovations in one plant to be rapidly deployed elsewhere.

The chemicals business underwent similar transformation. Thai Polyphosphates and Chemicals started in 1984 in Thailand merged with other chemical companies to form Aditya Birla Chemicals Ltd, supplying sectors including food, textiles, electrical, electronics, composites, leather, plastics and automobiles. This wasn't just capacity addition—it was about following customers as textile manufacturing shifted to Southeast Asia and building regional supply chains that could serve multinational clients.

Through brownfield expansion, Grasim plans to expand caustic soda capacity to 1,530 KTPA from 1,290 KTPA by 2024. The chemicals business had evolved from a captive unit serving VSF production to a standalone profit center with its own growth trajectory. The business developed a portfolio of chlorine derivatives including Stable Bleaching Powder, Polyaluminium Chloride, Chlorosulphonic Acid, Chlorinated Paraffin Wax, Calcium Chloride, Aluminium Chloride and Chloromethane.

This period also saw strategic exits that were as important as the acquisitions. In 2008, Grasim sold its sponge iron business to Welspun for ₹1,030 crore; in 2015, sold consumer products to Future Group; in 2017, sold Grasim Bhiwani Textiles to Donear; and in 2020, sold its stake in Indo Gulf Fertilisers to Indorama for ₹2,649 crore. These divestments weren't admissions of failure but recognition that capital could be better deployed elsewhere. The discipline to exit non-core businesses is often harder than making acquisitions, and Grasim showed remarkable strategic clarity in pruning its portfolio.

VI. Financial Services & Corporate Restructuring (2017)

The 2017 restructuring represents one of the most complex and value-creating corporate actions in Indian business history. It was a masterclass in financial engineering, stakeholder management, and strategic focus that unlocked billions in shareholder value while maintaining operational continuity.

The backdrop was important: Grasim had become a sprawling conglomerate with interests spanning manufacturing, financial services, retail, and telecom. While each business was substantial, the complexity made it difficult for investors to value the company properly. The conglomerate discount—where the whole trades for less than the sum of its parts—was substantial.

In 2017, Grasim demerged Aditya Birla Capital, its financial services arm including consumer finance, insurance and asset management divisions, while continuing to hold a 55% stake. But this was just part of a larger restructuring. Aditya Birla Nuvo Ltd was merged with Grasim effective July 1, 2017, and subsequently the financial services business was demerged and listed as Aditya Birla Capital Limited on September 1, 2017.

The elegance of the structure was remarkable. Shareholders of Grasim received shares in Aditya Birla Capital, creating a pure-play financial services company that could be valued appropriately by the market. Meanwhile, Grasim retained majority control, ensuring strategic alignment while allowing each entity to pursue its optimal capital structure and growth strategy.

As of March 31, 2025, the overall lending portfolio (NBFC and HFC) stood at highest-ever ₹1,57,404 crore, up 27% YoY, with total AUM (AMC, life insurance and health insurance) at ₹5,11,260 crore, up 17% YoY. The financial services business had become a significant player in its own right, requiring different skills, regulations, and capital than manufacturing businesses.

The restructuring solved multiple problems simultaneously. It simplified Grasim's structure, making it easier for manufacturing-focused investors to understand and value. It gave Aditya Birla Capital the flexibility to raise capital independently without diluting Grasim shareholders. It allowed management teams to focus on their specific industries without the distraction of unrelated businesses. And perhaps most importantly, it demonstrated to the market that the Birla Group understood and was willing to address the conglomerate discount.

The timing was impeccable. India's financial services sector was on the cusp of massive growth, driven by digitization, financial inclusion initiatives, and rising household incomes. As a separately listed entity, Aditya Birla Capital could participate in this growth story without being constrained by the capital allocation priorities of a manufacturing conglomerate. The stock market rewarded this clarity—both Grasim and Aditya Birla Capital saw significant reratings post-demerger.

VII. The Paints Gambit: Birla Opus Launch (2021-Present)

The entry into paints represents the boldest strategic move in Grasim's recent history—a ₹10,000 crore bet on disrupting one of India's most profitable oligopolies. Grasim entered the paints business in 2021, but the preparation and execution that followed reveals a level of strategic sophistication that has stunned incumbents.

The audacity of the move cannot be overstated. The Indian paints industry had been a comfortable oligopoly for decades, with Asian Paints commanding nearly 40% market share and enjoying EBITDA margins that were the envy of global peers. Berger, Kansai Nerolac, and Akzo Nobel had carved out profitable niches. New entrants like JSW had struggled to gain meaningful share despite significant investments. Why would Grasim succeed where others had struggled?

The answer lay in Grasim's unique advantages and meticulous execution. Grasim launched its paints business under the 'Birla Opus' brand in February 2024, expecting to turn profitable once it clocks Rs 10,000 crore in gross revenue within three years of full-scale operations, with investments of Rs 10,000 crore.

The scale of ambition was breathtaking. Kumar Mangalam Birla announced that Birla Opus would transform the paint industry with a 40% addition to current capacity, eyeing 1,332 million litres per annum—bigger than the second, third, and fourth players combined. This wasn't incremental capacity addition; it was shock and awe.

But capacity alone doesn't win markets. The go-to-market strategy leveraged every asset in the Grasim portfolio. With 50,000 dealers and as many tinting machines, Birla Opus built the country's second-largest depot network, leveraging its existing cement business to tap into over 200,000 dealers across India. The cement dealer network provided immediate access to contractors, builders, and architects—the key influencers in paint purchases.

The product strategy was comprehensive from day one. Birla Opus launched with the widest range in the industry—145+ products and 1,200+ SKUs across water-based paints, enamel paints, wood finishes, waterproofing and wallpapers, spanning economy to luxury segments, with 2,300+ tintable colours including 216 iconic Indian colours.

The speed of execution has been remarkable. In its first year, Birla Opus pulled in revenues of around ₹2,600-2,700 crores, becoming India's third-largest decorative paint brand within six months of going nationwide, grabbing a healthy single-digit market share in Q4 FY25. When combining Q4FY25 revenues of Birla Opus and Birla White Putty, the revenue market share has crossed 10% of the organised decorative paints market.

The manufacturing footprint was built with unprecedented speed. Commercial production started at 5 plants with 1,096 MLPA capacity out of total planned 1,332 MLPA across 6 plants, with the 6th plant at Kharagpur expected from H1FY26, giving Birla Opus ~24% of industry capacity in organised decorative paints.

But the real innovation was in distribution and service. Birla Opus introduced PaintCraft direct painting services, a one-stop-shop for products and services that was an industry-first at launch. This addressed a key pain point—the hassle and uncertainty of finding reliable painters and managing the painting process.

The competitive response has been fierce. Grasim accused Asian Paints at the CCI of abusing market dominance through exclusive dealer arrangements, with dealers claiming Asian Paints offered extra discounts and perks for loyalty while cutting credit limits and opening rival dealerships for those stocking Birla Opus. The fact that Asian Paints felt threatened enough to allegedly resort to such tactics validates the seriousness of Grasim's challenge.

The investment community initially questioned the paints entry—why enter a mature market with established players and high marketing costs? But media investments during H2FY25 propelled Birla Opus to become the 2nd most visible paints brand nationwide, with Birla Opus Studios reaching 8 major cities and Paint Gallery building retail footprint across 300+ towns, servicing 6,600+ towns from 137 depots.

The financial commitment has been substantial. Total Capex for the business stood at ₹9,352 crore till March 31, 2025, ~94% of the planned Capex outlay. This front-loaded investment approach—building full capacity before achieving market share—is the opposite of the gradual expansion typically seen in Indian manufacturing. It signals to competitors that Grasim is committed for the long haul and has the financial resources to sustain losses while building market position.

VIII. Current Portfolio & Competitive Position

Today's Grasim is a fascinating study in portfolio management—a collection of leadership positions across seemingly unrelated industries that actually share deep synergies. Revenue reached an all-time high of ₹1,48,478 crore in FY2025, up 13% YoY, though EBITDA stood at ₹20,023 crore, down 4% YoY due to initial investments in Birla Opus.

The VSF business remains the crown jewel. Grasim stands as the world's top VSF and VFY maker, with a total global capacity of 842 KTPA of Cellulosic Staple Fibre. This isn't just about scale—it's about technological leadership, cost advantages from vertical integration, and relationships with global fashion brands increasingly focused on sustainable fibers. The Cellulosic Fibres business delivered its highest ever revenue of ₹15,897 crore, up 6% YoY.

The chemicals business has evolved from a support function to a profit center. Grasim is India's largest producer of chlor-alkali, with caustic soda capacity of 1,290 KTPA and plans to expand to 1,530 KTPA. The business benefits from both internal consumption (for VSF production) and external sales, providing natural hedging against input cost volatility. In Q4FY25, the chemicals segment showed remarkable performance with EBITDA up 52% YoY, demonstrating the value of this often-overlooked division.

Through UltraTech, Grasim controls India's largest cement manufacturer and the world's third-largest producer outside China, with capacity exceeding 150 MTPA. The cement business provides stable cash flows, benefits from India's infrastructure boom, and creates synergies with the new paints business through shared distribution and customer relationships.

The financial services arm, though demerged, remains a significant value driver. With a lending portfolio of ₹1,57,404 crore (up 27% YoY) and total AUM of ₹5,11,260 crore (up 17% YoY), Aditya Birla Capital has emerged as a comprehensive financial services provider. The 55% stake provides Grasim with exposure to India's financial inclusion story without the complexity of direct management.

The new growth engines are particularly exciting. Beyond paints, Birla Pivot, the B2B e-commerce business, crossed an annualized revenue run-rate of ₹5,000 crore, targeting $1 billion revenue by FY27. This platform leverages Grasim's relationships with contractors and builders, offering not just building materials but also financial solutions to MSMEs.

The renewable business expanded to ~1.5 GWp capacity, up 64% from 894 MWp in March 2024, positioning Grasim for the energy transition while providing captive power for its energy-intensive manufacturing operations.

The market capitalization tells a story of value creation. Grasim's market cap stands at approximately ₹1,90,200 crore, but this arguably understates the sum-of-parts value. UltraTech alone has a market cap exceeding ₹2,50,000 crore (Grasim owns ~57%), while Aditya Birla Capital trades at around ₹25,000 crore (Grasim owns 55%). Add the standalone businesses—VSF, chemicals, paints—and the valuation math becomes compelling.

IX. Playbook: The Conglomerate Advantage

The Grasim story challenges conventional wisdom about conglomerates. While Western markets penalize diversification, Grasim has turned it into a competitive advantage. The playbook that emerges from seven decades of evolution offers lessons for emerging market corporations and investors alike.

Vertical Integration as Competitive Moat: Every major business Grasim entered involved controlling critical parts of the value chain. In VSF, it's pulp to fiber to chemicals. In cement, it's limestone mining to manufacturing to distribution. In paints, it's leveraging existing dealer networks while building manufacturing at unprecedented scale. This integration provides cost advantages, supply security, and market intelligence that pure-play competitors can't match.

Timing Market Entries: Grasim's entry timing reveals pattern recognition at its finest. VSF in 1947 addressed post-independence cotton shortages. Cement expansion in the 2000s captured India's infrastructure boom. Paints in 2021 targeted a market ripe for disruption with incumbent complacency. Each entry came not at market peaks but at inflection points where structural changes created opportunities for well-capitalized challengers.

The Patient Capital Approach: Unlike private equity or activist investors demanding quick returns, Grasim measures success in decades. The VSF business took 30 years to achieve global leadership. UltraTech required 20 years of acquisitions and integrations. Birla Opus is planning for profitability in year three but market leadership over a decade. This patience allows for front-loaded investments, acceptance of initial losses, and focus on market share over margins.

Managing Complexity: The 2017 restructuring demonstrated sophisticated thinking about when to integrate versus separate. Manufacturing businesses with operational synergies stayed together. Financial services, requiring different capabilities and regulations, were separated but controlled. The structure provides focus while maintaining strategic flexibility.

International Expansion Strategy: Grasim followed two distinct patterns globally. In VSF, it followed customers—setting up plants in Thailand and Indonesia as textile manufacturing shifted to Southeast Asia. In pulp, it acquired assets in Canada and Sweden for raw material security and technology access. This dual approach—market-seeking versus resource-seeking—optimized capital allocation across geographies.

The Aditya Birla Group Umbrella: The group structure provides advantages often underestimated by critics of conglomerates. Access to patient capital from cash-generating businesses funds new ventures. The Birla brand provides instant credibility with stakeholders. Shared services reduce costs. Management talent rotates across businesses, building versatile leaders. Perhaps most importantly, the group's reputation allows it to attract partners, whether L&T in cement or Tembec in pulp.

Building Ecosystems, Not Just Businesses: Modern Grasim doesn't just manufacture products; it builds ecosystems. Birla Pivot isn't just e-commerce but a platform connecting manufacturers, dealers, contractors, and financiers. Birla Opus isn't just paint but a complete solution including products, services, and design consultation. This ecosystem approach creates switching costs, generates data insights, and opens adjacent revenue streams.

X. Analysis & Investment Case

The investment case for Grasim presents a fascinating puzzle: a company trading at a significant discount to its sum-of-parts value, executing a bold transformation, yet facing skepticism about capital allocation and competitive dynamics.

Sum-of-Parts Valuation: A conservative SOTP analysis reveals significant undervaluation. UltraTech stake (57% of ₹2,50,000 crore market cap) = ₹1,42,500 crore. Aditya Birla Capital stake (55% of ₹25,000 crore) = ₹13,750 crore. These listed subsidiaries alone account for ₹1,56,250 crore, nearly 82% of Grasim's market cap. This implies the standalone businesses—global VSF leadership, chemicals, paints, B2B e-commerce—are valued at just ₹34,000 crore, despite generating over ₹15,000 crore in annual revenue.

The Conglomerate Discount Paradox: Global diversified peers like 3M and Honeywell trade at significant discounts to pure-play competitors. But Indian conglomerates like Reliance and Tata have actually commanded premiums during certain periods. The key difference? Growth rates and market opportunity. While 3M struggles for 3% growth, Grasim's portfolio is exposed to India's GDP-plus growth sectors.

The India Growth Multiplier: Every Grasim business benefits from structural tailwinds. VSF gains from fast fashion and sustainability trends. Cement rides the infrastructure and housing boom. Paints benefits from rising disposable incomes and renovation cycles. Financial services captures financial inclusion. B2B e-commerce digitizes traditional supply chains. Few companies offer such diversified exposure to India's growth story.

Bull Case: The optimistic scenario sees Birla Opus achieving 15% market share in paints within five years, adding ₹15,000 crore in revenue at 15% EBITDA margins. Birla Pivot reaches $2 billion revenue, valued at 2x sales. The VSF business re-rates as sustainable fashion goes mainstream. UltraTech continues consolidating India's cement industry. The conglomerate discount narrows as execution builds credibility. Target: ₹4,000 per share.

Bear Case: Pessimists worry about capital misallocation, with ₹10,000 crore invested in paints potentially earning sub-par returns if market share gains stall at 5-7%. VSF faces pressure from overcapacity and synthetic alternatives. Cement margins compress from new capacity and competitive intensity. The conglomerate structure prevents optimal capital allocation. Target: ₹2,200 per share.

Key Risks: Commodity cycles affecting VSF and chemicals simultaneously could pressure cash flows. Execution on paints remains unproven at scale—gaining initial share is easier than sustaining it. Regulatory changes, particularly environmental norms, could require significant capex. Incumbent retaliation in paints could trigger a price war destroying industry profitability. Technology disruption—bio-based materials, 3D printing in construction—could obsolete traditional products.

Risk Mitigants: Diversification across businesses provides resilience—cement and financial services can fund investments during VSF downturns. The balance sheet remains strong with net debt/EBITDA under 2x despite massive paints investment. Management has demonstrated discipline in exiting non-performing businesses. The controlling stake in listed subsidiaries provides financial flexibility if needed.

XI. The Future & Strategic Options

The next decade will determine whether Grasim transforms from a successful Indian conglomerate into a global industrial champion. The strategic choices ahead are both exciting and existential.

Will Paints Follow the UltraTech Playbook? Early signs suggest Grasim is replicating the cement strategy—rapid capacity building, aggressive market share capture, then consolidation through acquisitions. As smaller paint companies struggle with scale disadvantages, Grasim could acquire regional brands, specialty paint companies, or even international assets. The ₹10,000 crore initial investment is likely just the beginning.

Potential New Verticals: The building materials ecosystem offers adjacent opportunities. Adhesives, waterproofing chemicals, and construction chemicals are logical extensions. The EV revolution could create opportunities in battery chemicals where Grasim's chemical expertise provides an edge. Renewable energy, beyond captive consumption, could become a profit center as India pushes for net-zero emissions.

Digital Transformation Opportunities: Birla Pivot could evolve from a marketplace into a fintech platform, using transaction data to provide working capital loans. The paints business could leverage AR/VR for virtual painting experiences. The VSF business could build direct-to-consumer sustainable fashion brands. Digital isn't just about new businesses but transforming existing ones.

Succession Planning: Kumar Mangalam Birla, at 57, has led the group for three decades. The next generation—Ananya and Aryaman Birla—have joined boards and are being groomed for leadership. The transition will be crucial, particularly as the group becomes more consumer-facing and technology-driven, requiring different skills than traditional manufacturing.

The Next 25 Years: India's economy is expected to reach $10 trillion by 2035. Grasim's portfolio is perfectly positioned for this growth—infrastructure (cement), consumption (paints, financial services), sustainability (renewable energy, sustainable textiles), and digitization (B2B e-commerce). The company that started by clothing newly independent Indians could well become the company that builds, paints, and finances the new India.

Strategic Imperatives: Three critical success factors will determine Grasim's trajectory. First, execution on paints—market share must reach 15%+ to justify the investment. Second, digital transformation—B2B e-commerce must scale to $5 billion to be meaningful. Third, capital allocation—the temptation to enter new businesses must be balanced against optimizing existing portfolios.

XII. Outro & Resources

The Grasim story is ultimately about transformation—of a company, an industry, and a nation. From G.D. Birla's vision of clothing independent India to Kumar Mangalam Birla's ambition to paint its future, the company has consistently identified and addressed fundamental gaps in India's development journey.

Key Takeaways:

First, conglomerates can create value in emerging markets where institutional voids exist and capital is scarce. The ability to cross-subsidize businesses, share infrastructure, and leverage relationships remains valuable in markets like India.

Second, vertical integration, often dismissed as old-fashioned, provides resilience and competitive advantages when executed well. Grasim's control of value chains from raw materials to finished products has proven particularly valuable during supply chain disruptions.

Third, patient capital and long-term thinking enable strategies unavailable to companies focused on quarterly earnings. Grasim's willingness to invest ₹10,000 crore in paints before earning a rupee of profit would be impossible for most listed companies globally.

Fourth, timing matters more than first-mover advantage. Grasim rarely pioneers categories but enters at inflection points with superior resources and execution. This fast-follower strategy reduces risk while maintaining upside.

Lessons for Entrepreneurs: Build businesses that solve fundamental problems rather than incremental improvements. Focus on unit economics and sustainable competitive advantages rather than growth at any cost. Be willing to pivot and exit when businesses no longer fit the portfolio. Most importantly, think in decades, not quarters.

Lessons for Investors: Look beyond simple metrics to understand competitive positioning and strategic options. Conglomerate discounts can create opportunities when businesses are fundamentally strong. Management quality and capital allocation track record matter more than quarterly earnings. In emerging markets, diversification can be a strength, not a weakness.

What Makes Indian Conglomerates Different: Unlike Western conglomerates built through financial engineering, Indian groups grew organically around industrial logic. Family ownership provides continuity and patient capital unavailable to widely held corporations. The social contract—employment, community development, nation-building—remains important alongside shareholder returns. These differences aren't weaknesses but potential sources of sustainable competitive advantage.

The Grasim story continues to unfold. Whether Birla Opus disrupts the paint oligopoly, whether Birla Pivot becomes India's Alibaba for building materials, whether the next generation can maintain the entrepreneurial edge while managing complexity—these questions will define the next chapter. What's certain is that Grasim will remain central to India's industrial story, just as it has been since that August day in 1947 when a newly free nation began building its economic future.

For students of business strategy, Grasim offers a masterclass in portfolio management, market timing, and value creation in emerging markets. For investors, it presents a complex but potentially rewarding opportunity to bet on India's transformation. For competitors, it serves as a warning that patient capital, strategic thinking, and flawless execution remain formidable competitive weapons, even in an age of digital disruption and startup unicorns.

The conglomerate's playbook, refined over seven decades, proves that in markets like India, the question isn't whether diversification destroys value, but how to diversify intelligently, execute relentlessly, and adapt continuously. Grasim has mastered this playbook. The next decade will reveal whether it can teach these old tricks to new businesses, creating value for another generation of stakeholders in an India rushing toward its destiny as a global economic powerhouse.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube