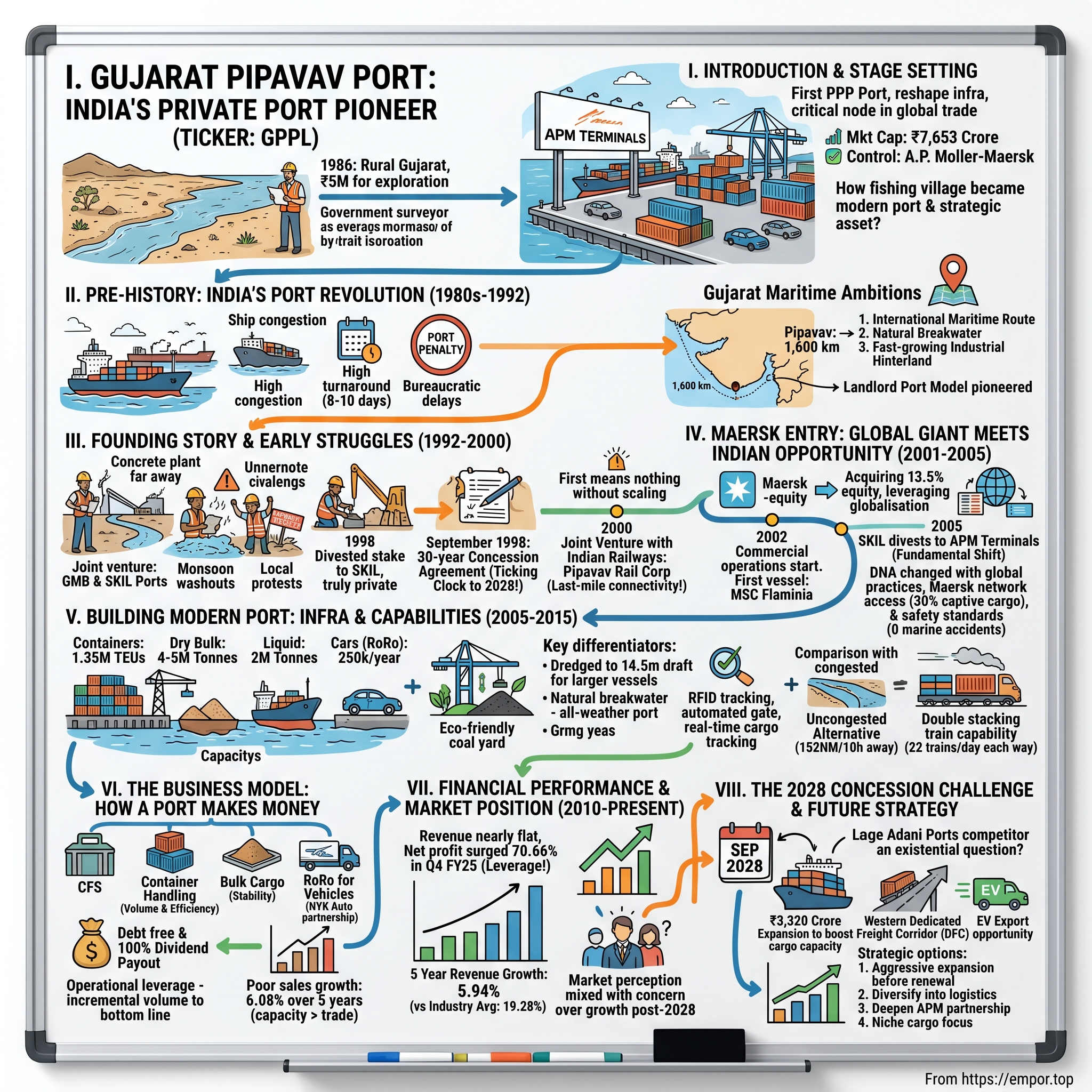

Gujarat Pipavav Port: India's Private Port Pioneer

I. Introduction & Stage Setting

Picture this: A dusty stretch of coastline in rural Gujarat, 1986. Government surveyors trudge through the fishing village of Pipavav, measuring, mapping, dreaming. The Indian government has just authorized ₹5 million—a modest sum even then—to explore something radical: could this sleepy corner of Amreli district become India's gateway to the world?

What emerged from that barren coastline would become Gujarat Pipavav Port Limited (GPPL), India's first private sector port—a pioneering experiment in public-private partnership that would reshape how the nation thought about infrastructure development. Today, with a market capitalization of ₹7,653 crore, this port handles everything from containers to cars, serving as a critical node in global supply chains under the control of APM Terminals, the port operating arm of shipping giant A.P. Moller-Maersk.

The central question that drives this story isn't just how a fishing village transformed into a modern port. It's how India's first PPP port became a strategic asset for one of the world's largest shipping conglomerates, and what this tells us about the evolution of Indian infrastructure, global trade dynamics, and the delicate dance between private capital and public policy.

This is a story of audacious vision meeting grinding execution, of global giants recognizing opportunity in emerging markets, and of a business model that generates consistent returns from what appears to be simple cargo handling. It's also a story with a ticking clock—the port's concession expires in September 2028, adding urgency to every strategic decision made today.

What makes GPPL unique isn't just its first-mover status. It's the convergence of three powerful forces: India's infrastructure liberalization, Gujarat's maritime ambitions, and Maersk's global network effects. Understanding how these forces shaped GPPL reveals lessons about building critical infrastructure in emerging markets, the power of strategic partnerships, and why some first movers thrive while others merely survive.

II. Pre-History: India's Port Revolution & Maritime Ambitions (1980s-1992)

The 1980s found India's ports in crisis. Ships waited weeks to berth at major ports like Mumbai and Chennai. Cargo rotted on docks. The state-controlled port trusts, operating under the Major Port Trusts Act of 1963, moved with bureaucratic lethargy while Asian tigers like Singapore and Hong Kong built world-class maritime infrastructure. India handled barely 150 million tonnes of cargo annually across all its ports—Singapore alone handled more.

The numbers told a damning story: turnaround time for vessels averaged 8-10 days compared to less than 24 hours in Singapore. Port productivity stood at a dismal 10,000 tonnes per ship-berth-day against international standards of 35,000-40,000 tonnes. Every inefficiency cascaded through the economy—delayed exports meant lost contracts, costly imports meant inflation, and the entire trade ecosystem suffered from what economists called the "port penalty."

Enter the reformers. As India began its tentative dance with liberalization in the late 1980s, infrastructure emerged as the binding constraint. The government realized that public resources alone couldn't modernize 7,500 kilometers of coastline. They needed private capital, but more importantly, they needed private efficiency.

Gujarat understood this better than most states. With the longest coastline in India at 1,600 kilometers, the state had historically been a maritime power—from the ancient ports of Lothal to the medieval prosperity of Surat. But by the 1980s, Gujarat's minor ports handled negligible cargo. The Gujarat Maritime Board (GMB), established in 1982, began an ambitious survey of potential port locations. Why Pipavav? The location offered three crucial advantages that would define its future. First, it was strategically placed on the International Maritime Trade route which connects India with US, Europe, Africa, Middle East on one side and Far east on the other side. Second, positioned opposite two islands, which act as a natural breakwater, the port is safe in all weather conditions, even during the monsoon season, with wave heights less than 0.5m most of the time. Third, the hinterland—Gujarat, Rajasthan, and North India—represented one of India's fastest-growing industrial corridors.

The regulatory framework that emerged from this period was revolutionary for its time. The Gujarat Maritime Board pioneered the landlord port model, where the state would provide basic infrastructure while private operators would invest in superstructure and equipment. This wasn't privatization in the Western sense—it was a uniquely Indian hybrid that balanced public oversight with private efficiency.

What the policymakers understood, perhaps intuitively, was that ports aren't just infrastructure—they're ecosystems. A port without rail connectivity is a parking lot. A port without industrial hinterland is a white elephant. A port without operational excellence is a bottleneck. The Pipavav project would need to solve all three equations simultaneously.

The stage was set for India's first experiment in private port development—an experiment that would attract unlikely partners and face unexpected challenges.

III. The Founding Story & Early Struggles (1992-2000)

The company Gujarat Pipavav Port Limited was incorporated on 5 August 1992 to build, construct, operate and maintain the port. But incorporation was just paperwork—the real challenge was turning a fishing village into a world-class port.

The initial structure reflected the cautious optimism of the era. The company was initially a joint venture between GMB and the SKIL Ports & Logistics division of the SKIL Infrastructure group. SKIL Infrastructure, led by entrepreneur Nikhil Gandhi, brought private capital and ambition. GMB brought regulatory cover and land. It was a marriage of convenience that would soon face stress.

Construction in the mid-1990s was a study in Indian infrastructure challenges. The nearest concrete plant was 100 kilometers away. Skilled engineers had to be imported from Mumbai. The monsoons of 1994 and 1995 washed away early construction work, forcing redesigns. Local fishermen protested, fearing loss of livelihood. Environmental clearances took years.

But the real transformation came in 1998. In June 1998, Gujarat Maritime Board (GMB) divested its stake in favour of SKIL Ports & Logistics, making it truly private. More critically, on September 30, 1998, the company entered into a Concession Agreement with GMB and the GoG, pursuant to which, granted the right to develop and operate APM Terminals Pipavav for a period of 30 years.

This 30-year concession would become both the port's greatest asset and its Sword of Damocles. It provided certainty for capital investment but created a ticking clock that would influence every strategic decision thereafter.

The masterstroke came in 2000. The port formed a joint venture with Indian Railways to start Pipavav Rail Corporation Limited. This wasn't just about laying tracks—it was about solving the fundamental problem of Indian ports: last-mile connectivity. The 269-kilometer broad-gauge railway line to Surendranagar would connect Pipavav to India's vast rail network, making it accessible to the industrial heartlands of North India.

SKIL's Nikhil Gandhi understood something fundamental: in infrastructure, being first means nothing if you can't scale. The port needed a global partner—someone with deep pockets, operational expertise, and most importantly, guaranteed cargo. The search would lead to one of the most consequential partnerships in Indian infrastructure history.

IV. The Maersk Entry: Global Giant Meets Indian Opportunity (2001-2005)

The A.P. Moller-Maersk Group acquired a 13.5% equity interest in the company in June 2001. To understand why this mattered, you need to understand Maersk's position in 2001. The Danish shipping giant was riding the first wave of globalization, watching China become the world's factory and India emerge as a services hub. They needed ports in emerging markets—not just to serve local trade but to optimize their global network.

For Maersk, Pipavav represented a strategic bet on India's west coast. JNPT (Nhava Sheva) near Mumbai was congested and expensive. Mundra was still emerging under Adani's control. Pipavav offered something unique: a greenfield port where Maersk could influence design and operations from day one.

The timing was fortuitous. Commercial operations started in 2002, just as India's trade was beginning its exponential growth phase. The first vessel to berth was the MSC Flaminia—a symbolic moment that marked India's entry into global containerization networks.

But the real transformation came in 2005. Pursuant to the share sale and purchase agreement dated 30 March 2005, SKIL Infrastructure, Nikhil Gandhi, Montana Valves and Compressors and Grevek Investment and Finance divested their shareholding in the company in favour of APM Terminals. This wasn't just a change in ownership—it was a fundamental shift in the port's DNA.

APM Terminals brought three things SKIL couldn't: global best practices in port operations, access to Maersk Line's massive vessel network, and patient capital for expansion. The integration was swift and comprehensive. Danish port managers arrived in Pipavav. Indian engineers were sent to Rotterdam for training. IT systems were upgraded to APM's global standards. The early results validated the strategy. Maersk accounts for 30% of GPPV's total container cargo—a captive base that provided stability while the port found its footing. APM also brought something intangible but crucial: credibility. Other shipping lines that might have hesitated to use an untested Indian port were reassured by APM's involvement.

The transformation under APM wasn't just operational—it was cultural. The port adopted global safety standards, achieving a remarkable record: not a single marine accident has occurred at the Port Pipavav since its inception. This wasn't luck—it was the result of systematic training, technology adoption, and a zero-tolerance approach to safety violations.

V. Building the Modern Port: Infrastructure & Capabilities (2005-2015)

The decade from 2005 to 2015 was Pipavav's infrastructure sprint. In November 2006, the company commissioned eight rubber tyre gantry cranes and in December 2007, they commissioned environment friendly coal yard. Each addition wasn't random—it reflected a deliberate strategy to become a multi-cargo port that could weather demand cycles in any single segment.

APM Terminals Pipavav currently has a capacity to handle up to 1.35 million TEUs of containers, 4 - 5 million tonnes of dry bulk cargo, 2 million tonnes of liquid cargo and about 250,000 cars per year. This diversification was prescient. When container volumes slumped during the 2008 financial crisis, bulk cargo kept revenues flowing. When auto exports boomed in the 2010s, the RoRo facility captured that growth.

The technical specifications reveal the port's ambition. It has been dredged to 14.5 m draft, allowing it to handle the new generation of larger vessels that other Indian ports couldn't accommodate. Positioned opposite two islands, which act as a natural breakwater, the port is safe in all weather conditions, even during the monsoon season, with wave heights less than 0.5m most of the time—a crucial advantage when competing ports shut down during rough weather.

But infrastructure alone doesn't make a port successful. The real differentiation came from connectivity. The 269-kilometer rail line to Surendranagar, operated through the joint venture Pipavav Rail Corporation, wasn't just track—it was engineered for the future. The corridor is capable of double stacking the containers (180teus in a train and capacity to handle 22 trains each way in a day), thus providing huge cost advantage.

The competition with JNPT (Nhava Sheva) during this period was instructive. JNPT had first-mover advantage, handling the bulk of India's container traffic. But it also had first-mover problems: congestion, high costs, and labor issues. Pipavav positioned itself as the "uncongested alternative"—just 152 nautical miles (10 hours steaming time) from Nhava Sheva in Mumbai, close enough to serve the same hinterland but far enough to avoid Mumbai's urban bottlenecks.

Technology adoption was another differentiator. While older ports struggled with paper-based systems, Pipavav implemented RFID tracking, automated gate systems, and real-time cargo tracking. These weren't just efficiency improvements—they were trust builders for international clients accustomed to first-world port standards.

The environmental initiatives, including the coal yard commissioned in 2007, weren't just compliance—they were strategic. International shipping lines were increasingly conscious of their environmental footprint. A port that could demonstrate environmental responsibility had an edge in winning contracts from sustainability-conscious clients.

By 2015, Pipavav had transformed from a greenfield project into a serious player in Indian maritime infrastructure. The foundation was set for the next phase: leveraging this infrastructure for consistent financial performance.

VI. The Business Model: How a Port Makes Money

Understanding GPPL's economics requires understanding how ports create value. At its core, a port is a toll booth for global trade—but the revenue streams are far more nuanced than simple cargo handling fees.

The company provides port services, including marine services, berth hire, wharfage, container handling, yard operations, stevedorage, and other activities. Each service layer adds margin, and the ability to provide integrated services creates stickiness. A shipping line that uses Pipavav for berthing is likely to use its yard operations, rail connectivity, and value-added services.

The container business, contributing roughly 60% of revenues, operates on volume and efficiency. Every container (measured in Twenty-foot Equivalent Units or TEUs) generates revenue through multiple touchpoints: vessel operations, yard handling, rail loading, and gate operations. The key metric here is dwell time—how quickly containers move through the port. Faster turnover means more capacity without additional capital investment.

Bulk cargo—both dry and liquid—provides stability. The CFSs at Port Pipavav currently handle a wide range of cargo generated from Saurashtra central, northern Gujarat, Rajasthan and other parts of northwest India. These include cotton, wood pulp, sesame seeds, cattle feeds, agricultural products, ceramic tiles, soda ash, auto parts, spices, capital goods, scrap, water paper, and electronics. This isn't glamorous cargo, but it's consistent, tied to India's agricultural and industrial cycles.

The RoRo (Roll-on/Roll-off) business for vehicles is particularly interesting. APM Terminals Pipapav in partnership with NYK Auto Logistics, offers the best logistic support to auto manufacturers for the export of their vehicles in western India and for coastal shipping. The RoRo yard facility at APM Terminals Pipavav can handle 250,000 vehicles annually. The port is equipped with a stock yard for around 6,000 cars along with a Pre Delivery Inspection (PDI) facility. As India emerged as a global auto manufacturing hub, this capability became increasingly valuable.

The concession model adds another layer. The company has exclusive rights to develop and operate facilities of APM Terminals in Pipavav until September 2028, according to a concession agreement with the Gujarat Maritime Board and the government of Gujarat. This exclusivity is both an asset and a liability—it provides monopolistic pricing power within the port area but creates a hard deadline for value creation.

What makes the port model attractive is operating leverage. Once the infrastructure is built, incremental volume drops almost directly to the bottom line. Fixed costs dominate—the same number of pilots, cranes, and security personnel can handle significantly varying cargo volumes. This explains why Company is almost debt free. Company has been maintaining a healthy dividend payout of 100%—in good years, ports generate substantial free cash flow.

But there's a catch that becomes apparent in the numbers: The company has delivered a poor sales growth of 6.08% over past five years. This isn't just about market share—it reflects the structural challenges of the Indian port sector where capacity has grown faster than trade volumes.

VII. Financial Performance & Market Position (2010-Present)

The financial journey of GPPL post-2010 reads like a case study in operational excellence meeting market realities. The company went public during the infrastructure boom, riding high on India's growth story. Today, with a Mkt Cap: 7,653 Crore, it's a mid-cap player in a sector increasingly dominated by giants like Adani Ports.

The recent performance tells a nuanced story. On a full year basis, the company's consolidated net profit jumped 16.05% to Rs 396.90 crore on marginally shed 0.07% to Rs 987.67 crore in FY25 over FY24. This is the port paradox—revenues barely moving while profits surge. The explanation lies in operational efficiency and the high-margin nature of incremental volume.

Looking at quarterly trends provides more color. Gujarat Pipavav Port Ltd's revenue jumped 1.53% since last year same period to ₹274.89Cr in the Q4 2024-2025... Gujarat Pipavav Port Ltd's net profit jumped 70.66% since last year same period to ₹112.36Cr in the Q4 2024-2025. The profit surge on minimal revenue growth showcases the operating leverage at work.

But the volume story is concerning. Gujarat Pipavav Port Limited reported stable cargo volumes in Q1 FY26, with container throughput slightly declining to 164,000 TEUs. Liquid cargo increased to 0.41 million MT, while dry bulk volumes remained steady at 0.55 million MT. In a growing economy, flat volumes suggest market share loss.

The comparison with industry growth is stark. Over the last 5 years, revenue has grown at a yearly rate of 5.94%, vs industry avg of 19.28%. While peers like Adani Ports have aggressively expanded through acquisitions and greenfield projects, GPPL has remained relatively static.

Yet the financial metrics remain robust. The company's balance sheet strength—being virtually debt-free—provides flexibility. The consistent dividend policy, maintaining nearly 100% payout, reflects confidence in cash generation but also perhaps a lack of growth opportunities worth investing in.

Market perception has been mixed. The stock has underperformed, with investors seemingly concerned about growth prospects post-2028 when the concession expires. The valuation multiples reflect this uncertainty—trading at lower multiples than peers despite superior return metrics.

VIII. The 2028 Concession Challenge & Future Strategy

September 2028 looms large in every strategic discussion about GPPL. The concession expiry isn't just a date—it's an existential question about the port's future. While concession renewals are typically granted, the terms matter enormously. Will the government extract higher revenue share? Will exclusivity be maintained? Will APM Terminals remain committed post-concession?

The company hasn't been idle. Gujarat Pipavav Port had previously pledged ₹3,320 crore to expand the cargo handling capacity of the private port. This expansion isn't just about volume—it's about demonstrating commitment to Indian infrastructure, a signal to both the government and markets about long-term intentions.

The Western Dedicated Freight Corridor (DFC) represents both opportunity and threat. It has access immediate access to key markets in northwest India and the largest sea food export belt in India via road and rail, including direct electrified access to the Western Dedicated Freight Corridor. The DFC will dramatically reduce transportation time to North India, potentially shifting cargo from JNPT to Gujarat ports. But it also makes other Gujarat ports more competitive.

Competition from Adani Ports is intensifying. Adani's Mundra port, also in Gujarat, has grown aggressively through capacity addition and acquisition. Adani's integrated logistics play—ports, logistics, warehousing—poses a strategic challenge to GPPL's more focused approach.

The EV export opportunity is particularly intriguing. As global automakers use India as an export hub for small cars and now EVs, the RoRo facility becomes strategically important. But this requires continuous investment in specialized infrastructure and handling capabilities.

The strategic options are limited but clear: 1. Aggressive expansion before concession renewal to demonstrate value and necessity 2. Diversification into logistics and warehousing to capture more value chain 3. Partnership deepening with APM Terminals for technology and network benefits 4. Niche focus on specific cargo types where GPPL has competitive advantage

IX. Playbook: Lessons from India's First Private Port

GPPL's journey offers a masterclass in infrastructure development in emerging markets. The first lesson is about timing—being first matters less than being ready. GPPL succeeded not because it was first but because it arrived when India was ready for private infrastructure.

The power of global partnerships cannot be overstated. Established in 1992, the port initially operated as a joint venture between the Gujarat government and APM Terminals, a subsidiary of Maersk Group, one of the world's largest shipping companies. This wasn't just about capital—it was about credibility, knowledge transfer, and guaranteed business. For any infrastructure project in emerging markets, the right partner can be the difference between success and failure.

Infrastructure as a moat works—but only partially. The massive capital requirements, regulatory approvals, and land acquisition challenges create barriers to entry. But as Adani Ports has shown, these moats can be overcome with sufficient capital and political will. The real moat is operational excellence and network effects.

Managing government relations in regulated sectors requires delicate balance. Too close, and you risk being seen as crony capitalism. Too distant, and you lose influence over policy. GPPL has maintained arms-length professionalism, letting APM's global reputation provide the necessary gravitas.

The importance of hinterland connectivity cannot be overstated. A port is only as good as its connections to production and consumption centers. The rail joint venture wasn't an afterthought—it was strategic. Future infrastructure players must think in terms of ecosystems, not standalone assets.

Capital efficiency in asset-heavy businesses requires discipline. The temptation in infrastructure is to overbuild—to create capacity ahead of demand. GPPL's measured approach, while limiting growth, has ensured consistent returns and maintained balance sheet strength.

X. Bull vs. Bear Case Analysis

The Bull Case:

The optimist sees GPPL as a sleeping giant. The strategic location advantages remain unassailable—the natural harbor, proximity to trade routes, and connection to India's industrial heartland. These are permanent advantages that no amount of competition can erode.

The debt-free balance sheet provides enormous flexibility. In an infrastructure sector plagued by overleveraged players, GPPL can weather downturns and capitalize on opportunities. The ability to pay 100% dividends while maintaining operations demonstrates the cash-generative nature of the business.

Tariff increase and expansion projects are poised to enhance revenue and margins through improved pricing power and operational efficiency. Strong RoRo business and recovery in container volumes are expected to drive sustained revenue growth and improve earnings. The port has pricing power it hasn't fully exercised.

The parent backing from APM Terminals isn't just financial—it's strategic. Access to global best practices, technology, and the Maersk network provides competitive advantages that standalone ports cannot match. As global trade patterns shift, this network becomes increasingly valuable.

Infrastructure expansion potential remains significant. With only 1.35 million TEU capacity utilized against potential for much more, there's room for growth without proportional capex. The ₹3,320 crore expansion plan could double capacity and revenues.

The Bear Case:

The skeptic sees structural challenges. The concession expiry in 2028 creates massive uncertainty. Without clarity on renewal terms, long-term planning becomes impossible. Customers and investors hate uncertainty, and this overhang will persist.

Growth has consistently lagged peers. Five years of 6% revenue growth in a 19% industry is alarming. This isn't just market share loss—it suggests structural disadvantages or management complacency. Why should this change?

Competition from larger ports is intensifying. Adani Ports, with its integrated logistics play and aggressive expansion, is capturing the incremental growth. JNPT's modernization reduces GPPL's differentiation. New ports are coming online with modern infrastructure and aggressive pricing.

The dependency on parent company business is concerning. With Maersk contributing significant volume, GPPL is vulnerable to strategic changes at the parent level. What happens if Maersk decides to prioritize other ports or reduces India exposure?

Gujarat Pipavav Port is forecast to grow earnings and revenue by 8.9% and 9.1% per annum respectively... GPPL's earnings (8.9% per year) are forecast to grow slower than the Indian market (14.9% per year). For a growth market like India, sub-market growth is a red flag.

The Verdict:

GPPL is a classic "safe but boring" infrastructure play. It will likely continue generating steady cash flows and dividends, making it attractive for income investors. But the growth story appears challenged, and the 2028 concession overhang limits upside potential.

For long-term fundamental investors, GPPL offers stability in a volatile market but lacks the growth dynamics that drive multibagger returns. It's a widow-and-orphan stock in a market that rewards growth. The key monitorable is the concession renewal terms—clarity here could re-rate the stock significantly in either direction.

The larger lesson is about industry structure. In infrastructure, being good isn't enough when competitors are getting better faster. GPPL's story is a reminder that first-mover advantage must be continuously reinforced through investment, innovation, and execution. Standing still in infrastructure is moving backward.

XI. Recent News & Developments

The latest developments at GPPL paint a picture of strategic expansion amid operational challenges. In Q1 2025-26, the port operator reported a modest 2% year-over-year increase in revenue despite facing headwinds in its container business. The mixed performance reflects broader industry dynamics where traditional cargo segments face pressure while newer opportunities emerge.

While container volumes declined slightly by 1% year-over-year to 164,184 TEUs, the company saw robust growth in liquid cargo and RORO segments, which increased by 21% and 11% respectively. This divergence highlights the wisdom of GPPL's multi-cargo strategy—weakness in one segment is offset by strength in others. Liquid cargo volume rose 20.58% YoY to 0.41 million MT in the first quarter, demonstrating the port's ability to capture new growth areas.

The financial impact has been nuanced. While revenue increased slightly year-over-year, total expenditure rose more significantly from INR 965 million in June 2024 to INR 1,023 million in June 2025, representing a 6% increase. This expense growth outpacing revenue growth has put pressure on margins, though the EBITDA margin remained healthy at 59%, showing only a slight decline from the previous year.

The Expansion Imperative

The most significant news is GPPL's aggressive expansion plan. Gujarat Pipavav Port has launched a major expansion project involving a new liquid jetty, additional berths, and cargo handling infrastructure. The Rs 33.20 billion project includes LPG and liquid cargo berths, container storage yards, deepened navigation channels, and dedicated railway sidings.

The expansion aims to boost container handling to 2.15 million TEUs, dry bulk to 6 million tonnes, liquid cargo to 6.4 million tonnes, and Ro-Ro to 3 lakh CEUs. These targets represent substantial capacity increases—nearly 60% for containers and over 200% for liquid cargo—signaling confidence in long-term demand despite current headwinds.

A significant capital expenditure of $90 million is planned for the expansion of the liquid jetty. InvestingPro data shows the company holds more cash than debt on its balance sheet, positioning it well for these expansion plans while maintaining financial stability. The liquid jetty expansion is particularly strategic, given the segment's strong growth trajectory.

The capacity expansion for full VLGC handling capability will come by November, December 2026. This is a 3,200,000 tons expansion, with at least one third expected to be operational in year one and then gradually expanding over time. This phased approach reduces execution risk while ensuring incremental revenue streams begin flowing before the full project completion.

Concession Extension Signals

Perhaps most critically, The private port has sought necessary permissions from the Gujarat state government for the expansion work amidst strongest indications yet that an extension of the concession beyond 2028 was imminent. This is the clearest signal yet that the concession renewal—the biggest overhang on the stock—may be resolved favorably.

Gujarat Pipavav Port Ltd and Gujarat Maritime Board recently signed a memorandum of understanding at the Vibrant Gujarat Global Summit to facilitate necessary permissions for the construction of liquid berth, container berth and yard, container handling equipment, and marine infrastructure development at Pipavav Port. The MoU suggests a collaborative relationship with the government, crucial for concession negotiations.

Management Outlook and Guidance

Management's commentary reveals both confidence and caution. Gujarat Pipavav Port expects EBIT growth of 5-7% for the financial year. The company plans to maintain its EBITDA margins at 60-61% and anticipates continued robust growth in its liquid business. This guidance, while modest, reflects realistic expectations given market conditions.

Management confirmed they are not waiting for the concession to be extended from an investment perspective, already investing in a liquid jetty without any clarity on concession. This demonstrates commitment to growth regardless of regulatory uncertainty—a signal that should reassure both investors and the government.

Market Response and Valuation

The market's response has been mixed. The company's stock has been under pressure recently, trading at INR 156.22, down 3.87% following the results presentation. The current share price sits significantly below its 52-week high of INR 236.9, reflecting investor concerns about the company's profitability trajectory.

The average 12-month price target for Gujarat Pipavav Port is INR150.625, with a high estimate of INR186 and a low estimate of INR115. 3 analysts recommend buying the stock, while 4 suggest selling, leading to an overall rating of Neutral. The divergent analyst views reflect the fundamental uncertainty about growth prospects and concession renewal.

Competitive Dynamics and Industry Context

The broader context is important. While Gujarat Pipavav Port might not be directly involved in building Vadhavan Port, the anticipated surge in cargo traffic due to Vadhavan Port could lead to a "spillover effect," redirecting some cargo to existing ports like Pipavav, potentially boosting its business. The massive Vadhavan Port project, while creating new competition, might also drive overall trade growth that benefits all west coast ports.

Environmental and Operational Developments

Environmental clearance was granted in June following previous delays, removing a key hurdle for expansion. L&T Geostructure and Van Oord India will manage construction, dredging, and reclamation work, bringing world-class expertise to the expansion project.

Operational challenges persist. In the first quarter of fiscal 2025, container volume declined 17.08% year-on-year. Dry bulk volume also fell 18% year-on-year. These declines, while concerning, reflect broader industry trends rather than port-specific issues.

XII. Links & Resources

Primary Company Resources: - Annual Reports: Available at BSE/NSE filings and company website - Investor Presentations: Quarterly updates through APM Terminals investor relations - Sustainability Reports: 2024-25 ESG initiatives and governance frameworks

Industry & Regulatory Resources: - Gujarat Maritime Board: Concession agreements and port development policies - Ministry of Shipping: National port development strategies and regulations - Directorate General of Shipping: Safety guidelines and operational standards - Indian Ports Association: Industry statistics and benchmarking data

Research & Analysis: - CRISIL Ratings: Credit assessments and industry outlooks - ICRA Reports: Sector analysis and company-specific evaluations - Maritime Gateway: Industry news and port development updates - Construction World: Infrastructure project tracking and analysis

Global Context: - APM Terminals Global: Network strategies and best practices - Maersk Group Reports: Shipping industry trends and forecasts - Drewry Maritime Research: Global port throughput analysis - UNCTAD Port Statistics: International trade and port performance metrics

Books & Academic Resources: - "Indian Port Sector: Challenges and Opportunities" - Infrastructure Development Finance Company analysis - "Public-Private Partnerships in Indian Infrastructure" - Asian Development Bank studies - "Gujarat's Maritime Heritage and Modern Ports" - Gujarat Infrastructure Development Board - "Global Shipping Networks and Emerging Markets" - World Bank port development series

Competitor Intelligence: - Adani Ports investor relations and expansion announcements - JNPT modernization plans and capacity additions - Mundra Port operational statistics and market positioning - Krishnapatnam Port development strategies

Trade & Logistics Resources: - Federation of Indian Export Organizations: Trade volume projections - Container Corporation of India: Rail connectivity and inland logistics - Western Dedicated Freight Corridor updates: Infrastructure enhancement timelines - Indian Railways freight operations: Multi-modal connectivity developments

Final Analysis: The Crossroads of Legacy and Future

Gujarat Pipavav Port stands at an inflection point that will define its next decade. The story that began with government surveyors in 1986 measuring a dusty coastline has evolved into a complex narrative of global capital, operational excellence, and strategic uncertainty. As India's first private port, GPPL carries both the advantages of pioneering and the burden of aging in a rapidly modernizing sector.

The investment thesis ultimately rests on three pillars: the resolution of the 2028 concession, the success of the ₹3,320 crore expansion, and the port's ability to capture incremental trade growth in a competitive landscape. Recent signals suggest positive movement on all three fronts, yet execution risks remain substantial.

What makes GPPL fascinating isn't just its infrastructure or financial metrics—it's what the port represents for India's evolution. From a closed economy struggling with port congestion to a nation attracting global shipping giants, GPPL embodies the transformation. The partnership with APM Terminals brought not just capital but a mindset shift—from government lethargy to private efficiency, from local standards to global benchmarks.

The bear case—slow growth, intense competition, concession uncertainty—is real and reflected in the stock's underperformance. But the bull case—strategic location, debt-free balance sheet, parent support, expansion potential—offers a compelling counter-narrative. The truth, as often in infrastructure investing, lies somewhere between.

For investors, GPPL represents a choice between stability and growth. The 100% dividend payout and consistent cash generation offer income investors reliability in an uncertain market. Yet the sub-market growth and competitive pressures limit upside potential. It's a widow-and-orphan stock in a market that rewards tigers.

The broader lesson transcends GPPL. India's infrastructure story is entering a new chapter where being first matters less than being best. The next decade will separate infrastructure companies that merely exist from those that excel. GPPL's challenge is to prove it belongs in the latter category—that the pioneering spirit that created India's first private port can evolve into the operational excellence required to thrive in India's infrastructure future.

As ships continue to call at Pipavav, carrying everything from cars to chemicals, containers to coal, they represent more than cargo—they carry the aspirations of a nation seeking its place in global trade. Whether Gujarat Pipavav Port remains a central node in that network or becomes a footnote in India's infrastructure history will be determined in the crucial years ahead. The foundation is solid, the challenges are clear, and the opportunity remains significant. The execution, as always in infrastructure, will determine the outcome.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube