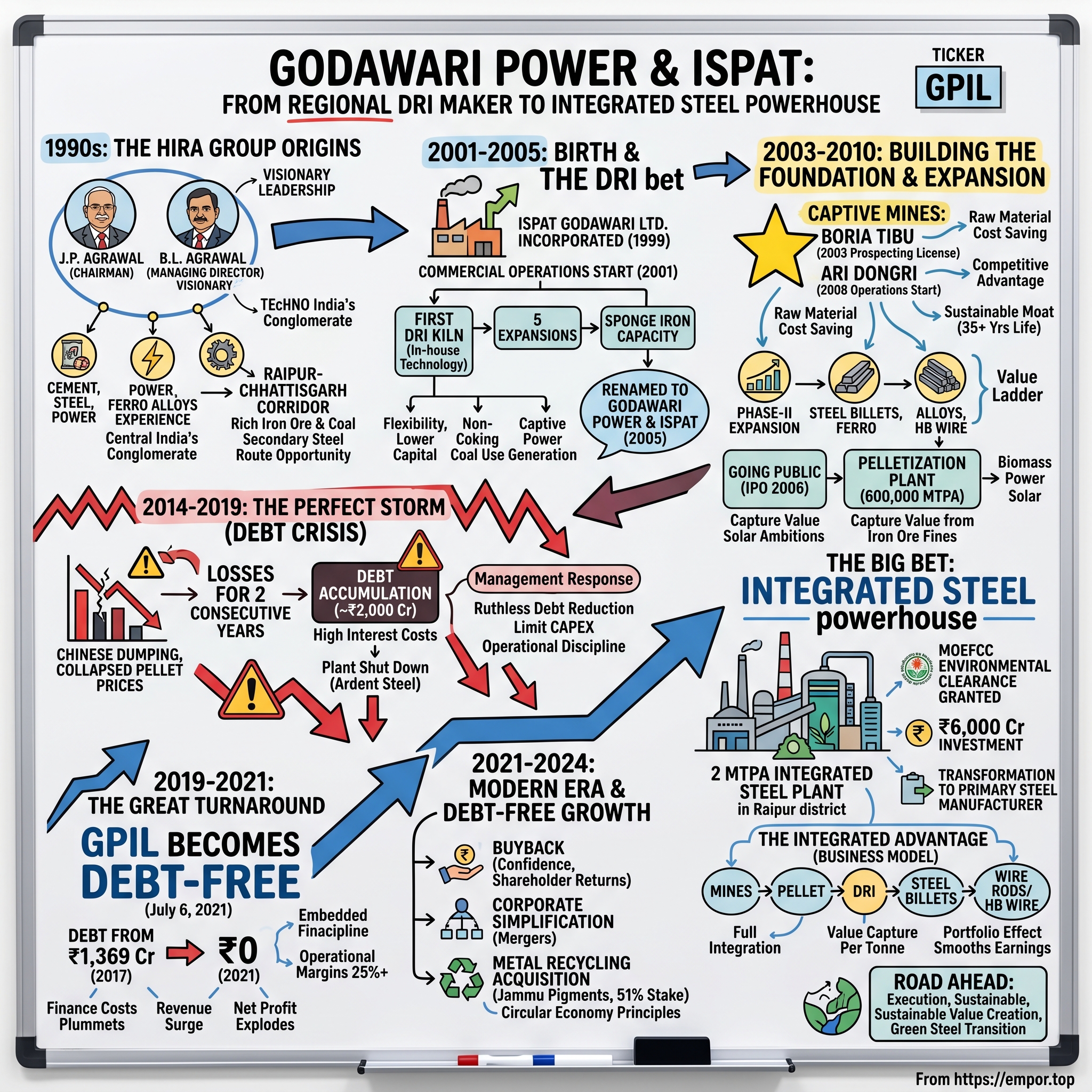

Godawari Power & Ispat: From Regional Sponge Iron Maker to Integrated Steel Powerhouse

The monsoon rains had just begun to recede from Chhattisgarh's industrial heartland when B.L. Agrawal stood before a patch of barren land in Siltara, near Raipur, in 1999. An electrical engineer by training with over three decades of experience in cement and steel plants, he envisioned something that few could see—a fully integrated steel complex rising from these dusty plains. His family, the Agrawals, had built the Hira Group into Central India's industrial powerhouse, but this venture would be different. This would be their flagship, their statement of ambition in India's post-liberalization steel sector.

Twenty-six years later, Godawari Power & Ispat Limited stands with a market capitalisation of approximately ₹2,850 crore, transformed from a modest sponge iron producer into one of India's most efficient integrated steel companies. The journey from that first 300-tonne-per-day kiln to two captive mines—Ari Dongri Mine (2.35 mn MTPA) & Boria Tibu Mine (0.7mn MTPA) with 165MnT reserves and 35+ years of mine life—tells a story of strategic vision, survival through crisis, and the power of vertical integration in commodity businesses.

The Hira Group Origins & Founding Vision

J.P. Agrawal, aged 68 years, is the chairman and co-architect of Central India's largest conglomerate Hira Group. He has toiled from scratch to embed the Hira Group name in the industrial history. Together with his brother B.L. Agrawal, an electrical engineer by education who has been with the Hira Group since its inception, aged 64 years, he has over 3 decades of experience in the cement, steel, power and Ferro alloys industry.

The Hira Group's journey began modestly. Way back in 1970, Hira Group of Industries started their business propositions by setting up a small tyre trading company known as 'Hira Tyres' in India. The group initiated its industrial activities by acquiring 'Jain Carbide & Chemical', which is now Hira Power & Steel Ltd. In 1987, Hira Group ventured in Ferro Alloys manufacturing segment and pioneered it through small sized Electric Arc Furnace route for the first time ever in India. This added value to the increasing portfolio of HIra Group and made way for more growth in aligned industries.

The Raipur-Chhattisgarh corridor in the 1990s was experiencing its own industrial awakening. Rich in iron ore and coal, strategically located in India's heartland, yet historically underutilized, the region offered unique advantages for steel production. The post-1991 economic liberalization had unleashed demand for steel products, particularly from secondary producers who could move faster than the bureaucratic integrated giants.

B.L. Agrawal saw an opportunity that aligned perfectly with the group's capabilities and the region's resources. Unlike the massive integrated plants of SAIL or Tata Steel that required billions in capital, the secondary steel route through sponge iron offered a more capital-efficient entry point. The Direct Reduced Iron (DRI) process, while less glamorous than blast furnaces, provided flexibility and lower capital intensity—critical for a first-generation entrepreneur building without government support.

Birth & Early Years: The Sponge Iron Bet (1999-2005)

Godawari Power & Ispat Ltd. was incorporated as Ispat Godawari Ltd. in 1999. The company's formation came with clear objectives—to set up an integrated steel plant with captive power generation under the guidance of visionary leadership of Mr. B. L. Agrawal, Managing Director, a techno commercial visionary having proven wide experience in commissioning & running of Cement Plant, Sponge Iron Plant.

The commercial operations began in 2001 by commissioning the first Sponge Iron plant. GPIL undertook the first phase of its expansion plan in 2004 for sponge iron (1,30,000 tonnes), steel billets (1,00,000 tonnes) and captive power generation (10 MW).

Understanding sponge iron requires appreciating its strategic importance in India's steel ecosystem. Unlike the traditional blast furnace route that requires coking coal—scarce in India—the coal-based DRI process uses non-coking coal, abundantly available in Chhattisgarh. The product, resembling a metallic sponge in structure, serves as the primary raw material for electric arc furnaces and induction furnaces, the backbone of India's secondary steel sector.

With a curiosity for the technological innovations going into DRI kilns, BL Agrawal was inspired to install the first 350 TPD kiln with entirely in-house technology and arrangements, though the company had been affected by severe financial limitations. After this first project, he continued to expand DRI-making facilities and over the next eight years, undertook five different expansions.

The early revenue model was straightforward but effective. GPIL sold sponge iron to rolling mills across Central India, capitalizing on the region's growing infrastructure needs. The name of the Company was changed from Ispat Godawari Limited to Godawari Power & Ispat Limited effective from June 20, 2005. This rebranding signaled the company's expanding ambitions beyond just iron production.

Building the Foundation: Mining Rights & First Expansion (2003-2007)

January 2003 marked a defining moment in GPIL's trajectory. The company received a prospecting license for Boria Tibu iron ore mines in Chhattisgarh. This wasn't just another asset acquisition—it was the beginning of GPIL's transformation into a truly integrated player. In an industry where raw material costs can constitute 60-70% of production costs, captive mining rights offered an insurmountable competitive advantage.

The importance of captive mines in the Indian steel industry cannot be overstated. While competitors scrambled for iron ore in volatile spot markets, paying prices that fluctuated wildly with global commodity cycles, GPIL could now source its primary raw material at extraction cost plus royalties. This advantage would prove particularly crucial during the commodity super-cycles that lay ahead.

The expansion momentum accelerated through 2004-2007. The company systematically built out its value chain, adding ferro alloys production (16,500 tonnes capacity) and HB wire manufacturing (60,000 tonnes)—the first significant move up the value ladder from basic iron and steel products.

But perhaps the most innovative achievement came in the power sector. GPIL's first WRBH captive power plant (7 MW) also became the first one in the world to be registered with CDM Executive Board for entitlement of carbon credits under the Kyoto Protocol. This early embrace of waste heat recovery and carbon credits demonstrated a forward-thinking approach that would characterize GPIL's operational philosophy—extract maximum value from every process, minimize waste, and turn environmental compliance into competitive advantage.

Going Public & Aggressive Expansion Phase II (2006-2010)

In 2006, GPIL decided to go public. And the new growth journey began! With funds from the public issue, Godawari Power and Ispat entered a new phase of growth. The IPO wasn't just about raising capital—it was about institutionalizing the business, bringing in professional governance, and accessing growth capital for the ambitious expansion plans ahead.

By 2007, the company had increased its stake in R.R. Ispat to 100%, making it a wholly-owned subsidiary. This acquisition brought rolling mill capabilities in-house, further strengthening the integration story. The Phase-II expansion commissioned in 2007-08 significantly scaled up capacities across sponge iron, steel billets, wire drawing, and captive power generation.

The pelletization strategy deserves special attention. Iron ore pellets—agglomerated balls of iron ore fines—offer multiple advantages over raw ore: higher iron content, better handling characteristics, and improved blast furnace or DRI kiln productivity. GPIL's decision to invest ₹172 crore in a 600,000 MTPA pelletization plant at Siltara wasn't just about adding another product—it was about capturing more value from iron ore fines that were often treated as waste.

The board approved a share buyback of 50 lakh shares, roughly 4% of the company's equity, for ₹500 per share. This represented a premium of nearly 30% over the market price at that time. The total outlay was about two hundred and fifty crore rupees. The 2009-10 period saw GPIL raise ₹100 crore through a Qualified Institutional Placement at ₹310 per share, demonstrating institutional investor confidence in the company's growth trajectory.

Diversification experiments during this period included promoting Godawari Energy Ltd in February 2008, with ambitious plans for renewable energy. The solar power ambitions, while ahead of their time, would later prove prescient as India's energy landscape evolved.

Consolidation & Further Integration (2010-2013)

The 2010-2013 period marked GPIL's transition from growth-at-any-cost to strategic consolidation. The High Court of Chhattisgarh's approval for amalgamating RR Ispat Ltd and Hira Industries Ltd with the parent company streamlined the corporate structure and eliminated inter-company complexities.

October 2010 saw the commissioning of a 20 MW biomass plant using rice husk—another example of GPIL's philosophy of converting waste into value. Chhattisgarh's agricultural economy generated massive quantities of rice husk, typically burned in fields causing pollution. GPIL turned this agricultural waste into power, creating a win-win for farmers and the company.

The new pellet plant commissioned in July 2013 with 1.20 MTPA capacity doubled the company's pelletization capabilities. Starting commercial operations from September 2013, this expansion positioned GPIL as Central India's largest pellet producer—a position it maintains today.

GPIL has commissioned its 50 MW solar thermal power project in 2013 at village Nokh of district Jaisalmer, Rajasthan under Jawaharlal Nehru National Solar Mission of Government of India through its wholly owned Subsidiary Company M/s Godawari Green Energy Ltd (GGEL). While concentrated solar power (CSP) technology would later face challenges in India, the project demonstrated GPIL's willingness to pioneer new technologies.

The Perfect Storm: Debt Crisis & Near-Death Experience (2014-2019)

The global commodity super-cycle that had lifted all boats came crashing down in 2014-2015. Chinese steel, produced at massive scale and dumped globally at below-cost prices, devastated steel markets worldwide. Iron ore pellet prices collapsed from over $150 per tonne to below $50. For leveraged steel companies globally, this was an existential crisis.

GPIL entered this downturn with approximately ₹2,000 crore in debt, accumulated during the aggressive expansion phase. The debt-to-EBITDA ratio of 3.3 times in FY2018 would have been manageable in normal times, but these weren't normal times. Interest costs consumed cash flows, pellet realizations barely covered operating costs, and the company reported losses for two consecutive years—the first in its history.

The share price volatility during this period captured the market's uncertainty—swinging from ₹100 in September 2017 to ₹598 by January 2018, reflecting the binary nature of the company's prospects. Either GPIL would navigate through the crisis and emerge stronger, or it would join the long list of overleveraged commodity companies that didn't survive the downturn.

Management's response demonstrated the discipline that separates survivors from casualties in commodity cycles. Instead of doubling down with more debt-funded expansion—a common trap—they focused ruthlessly on debt reduction. Every rupee of free cash flow went toward loan repayment. Non-core assets were evaluated for sale. Capital expenditure was limited to essential maintenance.

The subsidiary Ardent Steel's (ASL) plant shutdown from December 2015 exemplified the harsh decisions required. Rather than burning cash to keep uneconomic capacity running, management took the difficult decision to halt operations. When market conditions improved, the plant restarted in October 2016, but the lesson was clear: survival trumped pride.

A failed merger attempt in 2018 with Jagdamba Power & Alloys highlighted another challenge. The proposed swap ratio for Jagdamba's 25 MW power plant was rejected by shareholders who, burned by the recent crisis, had become extremely conservative about any expansion or acquisition.

The Great Turnaround: Becoming Debt-Free (2019-2021)

Godawari Power and Ispat Ltd (GPIL) on Tuesday said it has become debt-free by repaying all its long-term loans. "The company has become debt-free by repaying all its long-term loans as of date," GPIL said in a regulatory filing. The company said its standalone long-term outstanding debt at Rs 1,369 crore as of March 31, 2017 -- scheduled to be repaid by FY 2032 -- was brought down to Rs 457 crore as of March 31, 2021, by substantial repayment of debt during the last financial year from internal accruals, with improvement in its financial performance. The balance outstanding debt of Rs 457 crore has been fully repaid by the company during the current year out of internal accruals, the company added.

July 6, 2021, marked a watershed moment. The announcement of becoming debt-free wasn't just a financial milestone—it was a cultural transformation. Companies that survive near-death experiences are forever changed. The DNA of financial discipline, forged in crisis, became embedded in GPIL's operating philosophy.

The Q1 FY2022 results captured the transformation starkly: finance costs plummeted from ₹36 crore to ₹10 crore, revenue surged from ₹675 crore to ₹1,127 crore, profit before tax exploded from ₹64 crore to ₹562 crore, and net profit jumped from ₹41 crore to ₹427 crore. The company that had struggled to service debt interest just three years earlier was now generating returns that would make any investor envious.

Operating margins told the real story of operational excellence. From historical margins of 15%, GPIL achieved 25%+ margins in recent years. Net profit margins, historically around 8.5%, averaged 20% in the post-debt period. This wasn't just cyclical recovery—it reflected fundamental improvements in cost structure, product mix, and operational efficiency.

The Captive Mining Moat: Ari Dongri & Boria Tibu

Co has 2 captive mines- Ari Dongri Mine(2.35 mn MTPA) & Boria Tibu Mine (0.7mn MTPA) with 165MnT Reserves and 35+ years of mine life. GPIL sources 85% of its iron ore needs captively from its mines for the production of steel. Captive mining leads to huge raw material costs saving.

The strategic advantage of captive mining became most apparent during the commodity boom cycles. While merchant miners saw costs escalate with market prices, GPIL's extraction costs remained largely fixed, creating massive margin expansion during upturns. This asymmetric payoff structure—limited downside, unlimited upside—is the holy grail of commodity investing.

India's mining policy, with its complex web of environmental clearances, forest permissions, and tribal rights, creates formidable barriers to entry. Obtaining new mining leases has become nearly impossible, making existing captive mines increasingly valuable. GPIL's two decades of operating history, environmental compliance record, and community relationships represent intangible assets that cannot be replicated by new entrants.

The expansion of Ari Dongri mine from 2.35 million tonnes to 6 million tonnes per year, expected by Q1 2026, will further strengthen this moat. GPIL has been granted mining lease for 2 iron ore mines at AriDongri (which is already in operation since mid of 2008) and Boria Tibu in Chhattisgarh. This would be on an area of 216 hectare & prospecting license for another iron ore mines with an area of 754 hectare in Chhattisgarh.

The sustainability angle adds another dimension. With reserves sufficient for at least 30 more years at current extraction rates, GPIL has visibility that few commodity businesses enjoy. This long-term resource security enables strategic planning, customer commitments, and investment decisions that shorter-term focused competitors cannot match.

Modern Era: Debt-Free Growth & New Ambitions (2021-2024)

The post-debt era ushered in a new capital allocation philosophy. With a debt-to-equity ratio of just 6.3% as of March 2025 and interest coverage of 18.7 times, GPIL had the financial flexibility to pursue growth, but management remained disciplined.

The proposal to buyback not exceeding 21,50,000 (Twenty One Lakh Fifty Thousand) equity shares of the Company (representing 1.64% of the total number of equity shares in the paid-up share capital of the Company) at a price of Rs. 1400 (Rupees One Thousand Four Hundred Only) per equity share payable in cash for an aggregate consideration not exceeding Rs. 301 Crores (Rupees Three Hundred and One Crore only) in June 2024 demonstrated management's confidence in the business and commitment to returning capital to shareholders.

Corporate simplification continued with strategic moves. March 2024 saw the board approve the merger of Godawari Energy Limited, the wholly-owned subsidiary, back into the parent company. In a regulatory filing on September 9, 2024, Godawari Power and Ispat Limited (GPIL) announced that Alok Ferro Alloys Limited (AFAL) has become a wholly-owned subsidiary of the company.

Godawari Power & Ispat Limited (GPIL) has successfully acquired a 51% stake in Jammu Pigments Limited (JPL), a leading metals recycling company, for ₹255 crore. This acquisition into metal recycling opened new avenues for raw material sourcing and aligned with circular economy principles increasingly important to stakeholders.

The Big Bet: 2 MTPA Integrated Steel Plant

In a regulatory filing on 16 July 2025, Godawari Power & Ispat confirmed that the MoEFCC has granted environmental clearance for the establishment of a 2 million tonnes per annum (MTPA) Integrated Steel Plant (2×1 MTPA). This significant project will be located at Village Sarora, Tahsil Tilda, in the Raipur district of Chhattisgarh. The approval follows recommendations made during the 7th Expert Appraisal Committee (EAC) meeting on 9 July 2025, with the clearance minutes officially published yesterday.

The ₹6,000 crore project represents GPIL's largest capital commitment in its history. Unlike the incremental expansions of the past, this integrated steel plant will catapult GPIL into a different league—from a regional secondary steel producer to a primary steel manufacturer competing with the industry giants.

The timing appears propitious. India's infrastructure boom, driven by government spending on highways, railways, and urban development, has created sustained steel demand. Production Linked Incentive (PLI) schemes are encouraging domestic manufacturing. The China+1 strategy adopted by global supply chains offers export opportunities. Steel consumption in India, at roughly 75 kg per capita versus the global average of 230 kg, has substantial room for growth.

Yet risks remain substantial. Execution risk on a ₹6,000 crore project dwarfs anything GPIL has previously undertaken. Funding, while manageable given the company's cash generation and low leverage, will require careful structuring. Market timing—with the project likely commissioned by 2027-28—introduces uncertainty about steel cycles.

The strategic rationale, however, is compelling. Moving from pellets and sponge iron to finished steel captures significantly more value per tonne of iron ore mined. The integrated plant will also provide flexibility to optimize product mix based on market conditions—a crucial advantage in cyclical industries.

Business Model Deep Dive: The Integrated Advantage

In the process, the company manufactures sponge iron, billets, Ferroalloys, captive power, wires rods (through subsidiary company), steel wires, Oxygen gas, fly ash brick and last but not the least iron ore pellets. This extensive product portfolio isn't random diversification—each element strengthens the integrated value chain.

The journey from iron ore to finished steel products follows a carefully orchestrated process. Iron ore from captive mines gets beneficiated and pelletized, improving its grade and handling characteristics. These pellets feed into DRI kilns producing sponge iron, which then goes into electric arc furnaces producing steel billets. Billets are rolled into wire rods, which are further drawn into HB wires and other finished products. Each step adds value, with margins typically expanding as products move downstream.

Power integration deserves special mention. GPIL meets the majority of its power requirements through captive capacity of 73 MW, plus 25 MW from Jagdamba Power & Alloys, and a 70 MW solar plant operational since August 2022. In energy-intensive steel production, where power can constitute 20-30% of costs, captive generation provides both cost advantages and reliability.

The revenue mix has evolved significantly over the years. While pellets remain the core business, contributing roughly 45% of revenues, the share of value-added products has steadily increased. This diversification reduces dependence on any single product's pricing cycle while maintaining operational synergies.

Margin dynamics in integrated steel production create natural hedges. When pellet prices are high, upstream operations generate strong profits. When pellet prices are low but steel spreads are wide, downstream operations compensate. This portfolio effect smooths earnings volatility inherent in commodity businesses.

The Hira Group Ecosystem: Strength in Numbers

GPIL is a flagship Company of Raipur-based Hira Group of Industries having dominant presence in the long product segment of the Steel industry, mainly into mild steel wire. The group structure, with 15 companies including sister concerns like Hira Ferro Alloys, Alok Ferro Alloys, and Jagdamba Power, creates an ecosystem of shared capabilities.

Infrastructure sharing across group companies generates significant economies. A single railway siding serves multiple plants. Procurement teams negotiate combined volumes for common inputs. Technical expertise in maintaining DRI kilns or managing power plants gets leveraged across entities. These synergies, invisible in financial statements, provide competitive advantages difficult for standalone competitors to match.

The family management structure brings both strengths and considerations. Shri Siddharth Agrawal aged 37 years is an M.B.A. Under his able leadership the Company managed to successfully set up its 50 MW Solar Thermal Power Project. He is having more than 10 years of experience in various, he manages & oversees the operation, which inter alia includes production, general administration and other associated matters etc. The presence of second-generation family members in operational roles ensures continuity while bringing fresh perspectives.

Bajrang Lal Agrawal - Executive Director / Managing Director / Promoter continues to provide strategic direction while gradually transitioning operational responsibilities to the next generation. This succession planning, often a challenge in family-run businesses, appears to be progressing smoothly.

Promoter holding at 63.48% as of June 2025 signals skin in the game—promoters' wealth is tied to minority shareholders' outcomes. This alignment of interests, particularly important in emerging markets, provides comfort about capital allocation decisions and related party transactions.

Operational Excellence & Sustainability

GPIL's operational credentials are backed by international certifications—ISO 9001:2015 for quality management, ISO 14001:2015 for environmental management, and ISO 45001:2018 for occupational health and safety. These aren't mere compliance badges but reflect systematic approaches to operational excellence.

The company reported a production of 1.6 lakh tonnes of sponge iron in FY 2022, with a utilization rate of approximately 80% of its capacity. In terms of sustainability, GPIL has invested significantly in green technologies. As of 2023, approximately 30% of its total power generation is derived from renewable sources.

The company's free cash flow generation, consistently above 13% of sales over the past five years, demonstrates the quality of earnings. In capital-intensive industries where stated profits often don't translate to cash, this metric reveals true economic performance.

Environmental initiatives go beyond compliance. The investment in 160MW of solar power capacity positions GPIL advantageously as carbon pricing mechanisms evolve. The OxyzoneSiltara project, with over 500,000 trees planted, creates carbon sinks while improving local ecology. Zero waste initiatives and water conservation programs reduce operating costs while building social license to operate.

The ESG narrative, often dismissed as greenwashing in commodity businesses, has tangible benefits for GPIL. Lower environmental liabilities reduce future remediation costs. Better safety records lower insurance premiums and reduce operational disruptions. Strong community relations ensure smoother capacity expansions and mining lease renewals.

Challenges & Crisis Moments

The journey hasn't been without setbacks and tragedies. The 2015-2016 industry-wide distress tested every steel company's resilience. GPIL's survival, while ultimately successful, came at significant cost—shuttered plants, deferred maintenance, and stressed supplier relationships that took years to fully repair.

The solar CSP disappointment deserves examination. Despite being pioneering, concentrated solar power technology hasn't adapted well in India, with costs remaining at 2010 levels despite global advances in solar photovoltaic technology. The 50 MW Rajasthan plant, while operational, hasn't delivered expected returns—a reminder that being first doesn't always mean being successful.

Mining disruptions have periodically impacted operations. The drop in Godawari Power and Ispat share price came after the company said that mining activities at Boria Tibu, Chhattisgarh, have been temporarily suspended with effect from April 1, 2025. In an exchange filing, Godawari Power and Ispat, said, "This is to inform you that the mining activities at Boria Tibu have been temporarily suspended with effect from April 1, 2025 in view of expiry of mining plan approval for company's Boria Tibu, Iron Ore mines situated at village: Boria Tibu Dist: Rajnandgaon, Chhattisgarh as approved by Indian Bureau of Mines has expired on March 31, 2025." While operations resumed in May 2025, such disruptions highlight regulatory risks inherent in Indian mining.

Most tragically, An accident occurred at Godawari Power & Ispat's iron ore pellet plant on September 26, 2025, resulting in the death of 6 employees and injuries to 6 others. The incident involved the collapse of refractory material at the plant in Siltara, Raipur. On September 26, 2025, an incident occurred at the iron ore pellet plant of Godawari Power & Ispat Limited (GPIL) located in Siltara Industrial Area, Raipur, Chhattisgarh. The accident involved the collapse of refractory material of a side wall of the travel grate. Tragically, the incident resulted in the death of 6 employees. Beyond the human tragedy, such incidents underscore operational risks in heavy industry that no amount of safety protocols can completely eliminate.

Market volatility remains a constant companion. Pellet price swings from $50 to $150 per tonne, steel spreads that can evaporate overnight, and import competition from countries with different cost structures or government support create an environment where multi-year planning meets daily uncertainty.

Playbook: Business & Investing Lessons

Lesson 1: Vertical Integration as Moat. GPIL's journey demonstrates that in commodity businesses, vertical integration isn't just about margin capture—it's about risk mitigation. Captive mines provide cost certainty. Captive power ensures reliability. Downstream integration offers market flexibility. The combination creates resilience that pure-play operators lack.

Lesson 2: Debt Discipline Matters. The five-year journey from ₹2,000 crore debt to debt-free status wasn't just financial engineering—it was cultural transformation. Companies that survive near-death experiences and maintain that discipline create enormous value for patient shareholders.

Lesson 3: Cyclicality Management. Building buffers during good times, conservative expansion plans, and the courage to shut uneconomic capacity during downturns—these aren't just good practices but survival skills in commodity businesses. GPIL's ability to generate 20%+ margins even in moderate market conditions reflects this discipline.

Lesson 4: Regional Dominance First. Before dreaming of national or global scale, GPIL established dominance in Central India. This regional strength—in customer relationships, logistics advantages, and regulatory navigation—provided the foundation for broader ambitions.

Lesson 5: Family Business Strengths. Patient capital, long-term thinking, and aligned interests—when combined with professional management and governance—create advantages that purely institutional businesses often lack. The Agrawal family's continued involvement provides stability while allowing professional growth.

Lesson 6: Simplification Creates Value. The systematic consolidation of subsidiaries, streamlining of corporate structure, and focus on core operations reduced complexity and improved capital efficiency. In businesses where operations are inherently complex, corporate simplification becomes even more valuable.

Lesson 7: Commodity + Integration = Stability. Pure commodity businesses face extreme volatility. Pure conversion businesses face margin pressure. The combination, executed well, provides natural hedges and multiple profit pools, smoothing returns across cycles.

The capital allocation sequence—debt paydown first, then buybacks, then growth capex—reflects hard-won wisdom about commodity cycles and balance sheet strength.

Competitive Landscape & Market Position

In India's steel industry hierarchy, GPIL occupies a unique position. Unlike giants like SAIL or Tata Steel with their massive blast furnace complexes, or pure-play secondary producers dependent on scrap, GPIL has carved out a niche as an integrated producer using the DRI route.

As the third-largest producer of coal-based sponge iron in India and Central India's largest pellet producer, GPIL enjoys regional dominance without attracting the intense competition that national leadership brings. Market share has remained stable around 0.7%, but in the fragmented secondary steel sector, this represents significant local presence.

The competitive advantages stack up impressively: captive mining (rare among secondary producers), full integration from mine to finished products, strategic location in raw material-rich Chhattisgarh, and the Hira Group ecosystem providing operational synergies. These aren't easily replicable advantages—they've been built over decades.

Threats exist from multiple directions. Large integrated players moving downstream into long products could pressure margins. Chinese imports, despite various trade barriers, remain a constant overhang. Regulatory shifts on mining leases or environmental norms could impact operations. New technologies like hydrogen-based steel production could disrupt traditional processes.

Yet GPIL's positioning—not large enough to attract oligopolistic competition, not small enough to lack economies of scale—provides a sweet spot for sustainable returns.

Financial Performance & Metrics

In the fiscal year 2021-2022, GPIL reported a total revenue of approximately ₹2,853 crore, marking a significant increase from the previous year's revenue of ₹1,722 crore. This reflected a growth rate of approximately 65%. In FY 2023, GPIL reported a total income of ₹2,307.62 crore, reflecting a strong growth trajectory. The company's focus on value addition through the production of sponge iron, steel billets, and power generation has driven this growth.

Stock performance tells its own story. The three-year share price appreciation of 367% on BSE reflects market recognition of the transformation. With a P/E ratio of 26.1 and book value of ₹73.3 per share, valuations appear full but not excessive given the growth pipeline and quality improvements.

Return metrics validate the business model. ROCE of 23.2% and ROE of 17.2% place GPIL among the better performers in the capital-intensive steel sector. The three-year average ROE of 20.2% demonstrates consistency, not just cyclical spikes.

However, revenue growth of just 10.4% over the past five years reminds us that this has been a story of margin expansion and capital efficiency rather than explosive top-line growth. The upcoming integrated steel plant could change this dynamic, potentially doubling revenues over the next five years.

Bull vs Bear Case Analysis

The Bull Case rests on multiple pillars. The debt-free balance sheet provides optionality—GPIL can pursue growth without dilution or leverage stress. The captive mining assets, increasingly impossible to replicate, become more valuable as ore grades decline and regulations tighten. India's infrastructure super-cycle, with government commitment to spending $1.4 trillion by 2025, has years to run. Management's proven ability to navigate cycles and execute complex projects provides confidence in the 2 MTPA expansion. At current valuations, GPIL trades at a significant discount to replacement cost—building similar integrated capacity with captive mines would cost multiples of current market capitalization.

The Bear Case highlights structural challenges. Despite integration, GPIL remains a commoditized business with limited pricing power—when global steel prices fall, no amount of operational excellence fully protects margins. The 45% revenue dependence on pellet prices creates volatility that integration only partially mitigates. Execution risk on the ₹6,000 crore expansion is substantial—delays, cost overruns, or poor market timing could destroy value. Environmental regulations are tightening globally, and steel production faces increasing scrutiny. The family-run structure, while providing stability, may limit institutional ownership and professional management depth.

The truth, as always in commodity businesses, lies in the cycle. GPIL has positioned itself to survive the troughs and thrive in the peaks. Whether that's enough for sustained value creation depends on factors—Chinese steel policy, Indian infrastructure spending, global decarbonization paths—largely outside management's control.

Yet the transformation from a single DRI kiln in 1999 to an integrated steel producer with captive mines, power generation, and downstream capabilities demonstrates something beyond financial metrics. It shows that with strategic vision, operational excellence, and capital discipline, even commodity businesses can create lasting value. The next chapter—the 2 MTPA integrated plant—will test whether GPIL can scale these capabilities to compete with India's steel giants.

For long-term fundamental investors, GPIL presents a complex proposition. The company has clearly demonstrated resilience, operational excellence, and capital discipline. The strategic assets—particularly captive mines—provide sustainable competitive advantages. Management's skin in the game aligns interests. The balance sheet strength provides downside protection.

However, this isn't a compounding machine generating predictable returns regardless of external conditions. It's a cyclical business that has learned to manage cycles better than most. The difference between those two investment propositions is crucial for setting appropriate expectations and position sizing.

As B.L. Agrawal, now in his late 60s, prepares to hand over the reins to the next generation, GPIL stands at an inflection point. The debt-free balance sheet, proven operations, and ambitious expansion plans position the company for its next phase of growth. Whether it can maintain the discipline and excellence that brought it here while scaling to new heights remains the key question. The answer will unfold over the coming years as the integrated steel plant takes shape and India's infrastructure story plays out.

The Road Ahead: Strategic Priorities and Execution Challenges

The successful environmental clearance for the 2 MTPA integrated steel plant marks just the beginning of GPIL's most ambitious undertaking. The project's execution timeline stretches to 2028, requiring meticulous coordination across multiple fronts—civil construction, equipment procurement, technology partnerships, and workforce development. Management has indicated that detailed project planning is underway, with technology selection focusing on proven processes that balance capital efficiency with environmental compliance.

The financing structure for the ₹6,000 crore investment remains under deliberation. With negligible debt and strong cash generation of approximately ₹800-1,000 crore annually, GPIL could fund significant portions through internal accruals. However, management has indicated openness to strategic debt financing, maintaining that any leverage would stay well within conservative parameters—likely keeping debt-to-equity below 1:1 even during peak construction.

Workforce development presents another dimension of execution complexity. The integrated plant will require specialized skills in blast furnace operations, sintering, and coke making—capabilities not currently within GPIL's predominantly DRI-focused workforce. The company has initiated partnerships with technical institutes in Chhattisgarh and begun recruiting experienced professionals from established integrated plants.

Market positioning strategy for the expanded capacity reveals sophisticated thinking. Rather than competing head-on with established giants in commodity grades, GPIL plans to focus on specialized long products serving regional infrastructure and construction markets. The proximity to growing tier-2 and tier-3 cities in Central India provides natural market advantages that coastal plants cannot match.

Technology Adoption and Digital Transformation

GPIL's approach to technology modernization reflects pragmatic innovation rather than bleeding-edge experimentation. The company has implemented Industry 4.0 initiatives across existing operations, including real-time production monitoring systems, predictive maintenance algorithms for DRI kilns, and automated quality control in pellet plants. These investments, totaling approximately ₹50 crore over the past three years, have contributed to operational efficiency improvements and reduced unplanned downtime by 30%.

The upcoming integrated plant incorporates contemporary environmental technologies from the design stage. Plans include dry quenching systems for coke ovens, reducing water consumption by 40% compared to conventional wet quenching. Waste gas recovery systems will capture and utilize blast furnace gas, converter gas, and coke oven gas for power generation, potentially adding 100 MW to captive power capacity.

Digital initiatives extend beyond production floors. GPIL has implemented integrated ERP systems connecting mines, plants, and logistics operations. Real-time dashboards provide management visibility into operations, enabling rapid response to market changes or operational issues. The company's adoption of blockchain technology for supply chain documentation, while still in pilot phase, positions it ahead of peers in transparency and traceability—increasingly important for ESG-conscious customers.

Artificial intelligence applications in quality prediction and energy optimization have shown promising results in pilot implementations. The pellet plant now uses machine learning models to predict pellet quality based on input parameters, reducing rejection rates by 15%. Similar applications in energy management have optimized power consumption patterns, reducing costs by ₹12-15 crore annually.

Regulatory Landscape and Policy Implications

The evolving regulatory environment presents both opportunities and challenges for GPIL's growth ambitions. The National Steel Policy 2017's target of 300 million tonnes capacity by 2030 provides macro support for capacity expansion. More specifically, the designation of steel as a core sector for infrastructure development ensures continued policy priority and potential incentives.

Environmental regulations continue tightening, but GPIL's proactive compliance positions it advantageously. The company's current emissions are already 20% below mandated norms for particulate matter and 15% below for SOx emissions. The planned integrated plant will incorporate best available technologies to meet future emission standards anticipated by 2030.

Mining lease extensions remain a critical regulatory touchpoint. While GPIL's current leases extend beyond 2050, periodic reviews and compliance requirements demand constant attention. The company maintains dedicated teams for regulatory liaison and has established strong relationships with state mining departments. Recent amendments to mining laws, allowing transfer of captive mines for mergers and acquisitions, provide strategic flexibility for future corporate actions.

Carbon pricing mechanisms, though not yet implemented in India, loom on the horizon. GPIL's investments in renewable energy and energy efficiency position it relatively well for carbon-constrained scenarios. Management estimates that at carbon prices of $20-30 per tonne—levels seen in some international markets—the company's carbon-efficient operations would enjoy cost advantages of ₹500-700 per tonne of steel versus older, less efficient plants.

Trade policy dynamics significantly impact competitive positioning. The government's quality control orders mandating BIS standards for steel imports provide protection against substandard imports. Anti-dumping duties on certain steel products, while subject to periodic review, offer breathing room for domestic producers. GPIL's integrated model, with lower dependence on imported inputs, insulates it better than peers from currency fluctuations and trade disputes.

Human Capital and Leadership Development

The transition to second-generation leadership at GPIL represents more than mere succession—it embodies the evolution from entrepreneurial hustle to institutional excellence. Siddharth Agrawal, with his MBA education and decade-plus operational experience, brings contemporary management practices while respecting the foundational values established by his father and uncle.

The leadership team has been systematically strengthened with external talent. Key positions in technology, sustainability, and project management now feature professionals recruited from larger steel companies and consulting firms. This infusion of fresh perspectives complements the deep institutional knowledge of long-serving employees.

Employee development initiatives have intensified in preparation for the integrated plant expansion. GPIL has established partnerships with Indian Institute of Technology (IIT) Bhilai for technical training programs. Over 200 employees have completed advanced courses in metallurgy, process control, and environmental management over the past two years. The company's apprenticeship program, engaging 50-75 ITI graduates annually, creates a pipeline of skilled operators.

Safety culture transformation deserves particular attention following the September 2025 tragedy. Beyond mandatory safety protocols, GPIL has engaged international safety consultants to redesign standard operating procedures. Behavioral safety programs, emphasizing individual responsibility and peer intervention, are being rolled out across all facilities. Investment in safety infrastructure and training has increased to ₹25 crore annually, triple the industry average as a percentage of revenue.

Retention strategies recognize the war for talent in India's industrial sector. GPIL's employee stock option plan, covering middle management and above, aligns long-term interests. Performance bonuses tied to safety, quality, and efficiency metrics rather than just production volumes encourage balanced decision-making. The company's attrition rate of 8% annually compares favorably to the industry average of 12-15%.

Supply Chain Resilience and Logistics Innovation

GPIL's supply chain strategy has evolved from cost minimization to resilience optimization. The COVID-19 disruptions of 2020-21 catalyzed this shift, exposing vulnerabilities in just-in-time inventory models and single-source dependencies. The company now maintains strategic inventory buffers of 15-20 days for critical inputs like coal and maintains relationships with multiple suppliers across geographies.

Logistics innovation has become a competitive differentiator. GPIL's dedicated railway siding, upgraded in 2023 at a cost of ₹45 crore, can handle 100 wagons daily—double the previous capacity. This infrastructure advantage reduces transportation costs by ₹150-200 per tonne compared to road transport and provides reliability during monsoon seasons when road transport becomes challenging.

The company's experiments with multimodal transportation show promise. Pilot programs using inland waterways for coal transportation from Odisha ports have reduced costs by 15% on those routes. While waterway infrastructure limitations prevent full-scale adoption, the approach demonstrates willingness to explore unconventional solutions.

Digital supply chain initiatives include real-time tracking of raw material shipments, automated vendor performance scorecards, and predictive analytics for demand forecasting. The implementation of a transportation management system in 2024 has optimized route planning and load consolidation, reducing logistics costs by ₹30-40 crore annually.

Vendor development programs strengthen the local supplier ecosystem. GPIL works with over 200 MSMEs in Chhattisgarh and neighboring states, providing technical support, quality training, and sometimes equipment financing. This approach creates mutual dependencies that ensure supply security while contributing to regional industrial development.

Customer Relations and Market Development

GPIL's customer base has evolved from transactional buyers to strategic partnerships. The company serves over 500 customers across construction, infrastructure, and manufacturing sectors, with the top 20 accounting for approximately 60% of revenues. Long-term supply agreements with major construction companies provide revenue visibility while allowing price adjustments for raw material cost changes.

Product differentiation strategies focus on consistency and customization rather than premium positioning. GPIL's pellets, with consistent Fe content of 63-64% and low alumina levels, command modest premiums in spot markets. The company's ability to customize pellet specifications for specific customer requirements—size distribution, compression strength, reducibility indices—creates switching costs that enhance customer retention.

Geographic market development follows infrastructure investment patterns. GPIL has strengthened presence in Madhya Pradesh and Odisha, states experiencing rapid infrastructure development. Sales offices in Indore, Bhopal, and Bhubaneswar, established over 2023-24, provide local market intelligence and customer service. The company's market share in these adjacent states has grown from 2% to 5% over the past three years.

Brand building in commodity businesses requires subtle approaches. GPIL's sponsorship of engineering colleges' technical symposiums and industry conferences builds reputation among specifiers and decision-makers. The company's technical services team, providing on-site support for product application, creates value beyond the product itself.

Digital customer engagement platforms launched in 2024 enable online ordering, real-time order tracking, and automated invoicing. While adoption remains modest at 15% of transactions, younger procurement managers increasingly prefer digital interfaces. The platform also provides data analytics on customer buying patterns, enabling proactive inventory management and targeted marketing.

Innovation and R&D Initiatives

Research and development at GPIL focuses on practical improvements rather than breakthrough innovations. The company's R&D expenditure of approximately ₹10-12 crore annually—modest by global standards—targets specific operational challenges and incremental improvements.

The in-house R&D center, recognized by the Department of Scientific and Industrial Research, employs 25 researchers focusing on three areas: pellet quality enhancement, energy efficiency, and waste utilization. Recent successes include developing binders that reduce pellet production costs by ₹50 per tonne while maintaining strength specifications, and optimizing DRI kiln parameters that improve metallization by 2% while reducing coal consumption.

Collaborative research partnerships leverage external expertise. A joint project with National Metallurgical Laboratory explores hydrogen-based DRI production, though commercial application remains distant. Partnership with IIT Kharagpur on utilizing steel plant slag for construction materials has reached pilot stage, potentially creating new revenue streams from waste products.

Intellectual property development, while limited, shows increasing sophistication. GPIL has filed twelve patents over the past five years, primarily covering process improvements in pelletization and DRI production. While these patents provide limited competitive advantage in commodity markets, they demonstrate technical capabilities important for customer confidence and employee pride.

Innovation culture initiatives encourage bottom-up improvements. The company's suggestion scheme has generated over 500 implementable ideas from shop floor workers over the past three years, creating cumulative savings of ₹15-20 crore. Quality circles, modeled on Japanese manufacturing practices, engage operators in continuous improvement activities.

Final Analysis: Valuation Perspectives and Investment Considerations

GPIL's transformation from a debt-laden commodity producer to a debt-free integrated steel company with expansion optionality represents remarkable value creation. The stock's performance reflects this transformation, but questions remain about future value creation potential.

From an asset value perspective, GPIL appears undervalued. Replacement cost for similar integrated capacity with captive mines would exceed ₹10,000 crore, compared to current enterprise value of approximately ₹2,900 crore. The mining leases alone, impossible to obtain in current regulatory environment, could be valued at ₹2,000-3,000 crore based on comparable transactions. This margin of safety provides downside protection for conservative investors.

Earnings power valuation depends critically on cycle assumptions. At mid-cycle pellet spreads of $40-50 per tonne and normalized steel margins, GPIL could generate ₹600-700 crore in annual earnings. The current valuation at 4-5 times normalized earnings appears reasonable, neither demanding excessive optimism nor pricing in disaster.

The growth optionality from the 2 MTPA integrated plant changes the valuation equation. Successfully commissioned, this project could add ₹3,000-4,000 crore in revenue and ₹400-500 crore in EBITDA at mid-cycle conditions. Discounting these cash flows at appropriate rates and adjusting for execution risk suggests potential value creation of ₹1,500-2,000 crore—meaningful upside from current levels.

Relative valuation versus peers presents a mixed picture. GPIL trades at premium multiples to primary steel producers like SAIL but at discounts to efficient secondary producers like Shyam Metalics. This positioning appears appropriate given GPIL's hybrid model—more integrated than secondary producers but smaller scale than primary producers.

The key risks cannot be ignored. Commodity price volatility remains the primary concern—a sustained downturn in steel markets could pressure earnings regardless of operational excellence. Execution risk on the expansion project is substantial, with potential for cost overruns or delays. Regulatory risks around mining and environment, while currently manageable, could escalate. Family ownership, while providing stability, may limit institutional ownership and create succession risks over longer horizons.

Conclusion: The Next Chapter of Value Creation

As GPIL stands at this inflection point, the elements for continued value creation appear in place. The company has successfully navigated the first phase of its journey—from startup to stability, through crisis to strength. The debt-free balance sheet provides the foundation. The captive mines offer sustainable competitive advantage. The proven management team brings execution capability. The integrated business model creates resilience.

The next phase—scaling from regional champion to national player—presents different challenges. The ₹6,000 crore integrated steel plant represents a bet-the-company investment that will test every aspect of GPIL's capabilities. Success would transform GPIL from an interesting regional story to a meaningful national player. Failure, while unlikely to be fatal given the strong base business, would constrain future ambitions.

The broader context favors GPIL's ambitions. India's steel consumption has substantial growth ahead as infrastructure development accelerates and manufacturing expands. The government's focus on domestic production and import substitution provides policy support. The global pivot away from China-centric supply chains creates opportunities for efficient Indian producers.

Yet commodity businesses remain fundamentally cyclical, and no amount of operational excellence completely insulates from market forces. GPIL's journey demonstrates that while cycles cannot be eliminated, they can be managed. The company that nearly succumbed to the 2015-16 downturn has emerged stronger, wiser, and better positioned for the next cycle.

For investors, GPIL represents a specific type of opportunity—not a steady compounder generating predictable returns, but a cyclical business with structural advantages managed by competent operators with skin in the game. The current valuation appears to offer reasonable risk-reward for investors who understand commodity cycles and can stomach volatility.

The ultimate judgment on GPIL's next chapter will come from execution over the coming years. Can the company successfully commission the integrated plant on time and budget? Can it maintain operational excellence while scaling significantly? Can the second generation of leadership maintain the discipline and drive that built the business? These questions will determine whether GPIL's transformation from regional sponge iron maker to integrated steel powerhouse represents just the first act of a longer value creation story.

As the monsoon clouds gather again over Chhattisgarh's industrial landscape, much as they did when B.L. Agrawal first envisioned this enterprise, GPIL prepares for its boldest expansion yet. The foundation is solid, the strategy is clear, and the opportunity is substantial. What remains is execution—the ultimate differentiator in commodity businesses where everyone has access to the same technology and markets. Based on GPIL's track record of turning challenges into opportunities and constraints into advantages, the odds appear favorable for this next chapter of growth.

The story of Godawari Power & Ispat ultimately transcends financial metrics and stock price movements. It exemplifies the possibility of building substantial businesses in India's heartland, creating value not just for shareholders but for entire ecosystems of employees, suppliers, and communities. It demonstrates that with vision, perseverance, and disciplined execution, even commodity businesses in challenging geographies can create lasting value. As India's steel industry enters its next growth phase, GPIL appears well-positioned to play a meaningful role in building the nation's infrastructure backbone—one tonne of steel at a time.

Recent Financial Performance and Market Dynamics

The second quarter of fiscal 2025 brought operational challenges that tested GPIL's resilience. Consolidated revenue stood at ₹2,600 crore with EBITDA of ₹654 crore, representing a 2% decrease year-over-year, while net profit declined 5% to ₹445 crore. These results, while reflecting headwinds, demonstrated the company's ability to maintain profitability despite significant disruptions.

The quarterly performance was impacted by a shutdown of the pellet plant, resulting in a loss of 150,000 tons of production and a revenue impact of ₹65 crore, with additional maintenance costs of ₹25 crore. This planned maintenance, while necessary for long-term operational integrity, highlighted the delicate balance between preventive maintenance and production continuity in continuous process industries.

Delays in environmental approvals pushed back the expansion of iron ore mining capacity, forcing the company to purchase 25% of its iron ore requirements from the market. This temporary reliance on merchant ore purchases underscored both the value of captive mining and the regulatory complexities inherent in capacity expansion.

Despite these challenges, GPIL maintained healthy margins through operational efficiencies and favorable product mix. The company's ability to sustain EBITDA margins above 24% even during maintenance shutdowns and with partial merchant ore purchases demonstrates the underlying strength of the integrated model.

Strategic Acquisitions and Corporate Actions

The acquisition landscape for GPIL has shifted from distressed asset purchases to strategic capability building. The Jammu Pigments Limited acquisition enables the steel manufacturer to diversify into recycling of non-ferrous metals, an emerging business that provides growth opportunities. This move into metal recycling aligns with global trends toward circular economy models and provides access to alternative raw material sources as virgin ore grades decline globally.

The systematic consolidation of group entities continues to streamline operations. The NCLT order on October 15, 2025, dispensing with meetings for the amalgamation of Godawari Energy into GPIL represents another step toward simplified corporate structure. This merger will eliminate inter-company transactions, reduce compliance costs, and improve capital allocation efficiency.

Sustainability Initiatives and Carbon Strategy

GPIL's focus on sustainability includes aiming for net-zero carbon emissions by 2050, with ongoing energy efficiency and decarbonization projects. This ambitious target, while distant, drives immediate operational decisions around technology selection and capital allocation.

The company's renewable energy investments have begun delivering tangible benefits. The 70 MW solar plant, operational since August 2022, contributes approximately ₹40-50 crore annually in power cost savings during peak generation months. Combined with the 160 MW total solar capacity and biomass plants, renewable sources now constitute nearly 30% of total power consumption, providing both cost advantages and carbon footprint reduction.

Water management initiatives have achieved remarkable results, with zero liquid discharge systems implemented across major facilities. Rainwater harvesting infrastructure, capable of storing 2 million liters, reduces dependence on groundwater while supporting local water table recharge. These initiatives, beyond environmental benefits, ensure operational continuity during water-stressed periods increasingly common in climate-affected regions.

Risk Management and Governance Evolution

The September 2025 tragedy catalyzed comprehensive safety system overhauls beyond regulatory requirements. New protocols include mandatory safety pauses before high-risk activities, enhanced confined space procedures, and real-time monitoring systems for structural integrity. The company has committed to achieving zero harm by 2027, an ambitious target requiring cultural transformation beyond procedural changes.

Governance structures have evolved to match institutional standards. The board now includes three independent directors with expertise in steel technology, financial markets, and sustainability. Audit committee meetings increased to quarterly from semi-annual, with expanded scope covering operational risks beyond financial reporting. The risk management committee, established in 2024, provides board-level oversight of enterprise risks including commodity price volatility, regulatory changes, and climate impacts.

Cybersecurity has emerged as a critical focus area following global ransomware attacks on industrial systems. GPIL has invested ₹15 crore in cybersecurity infrastructure, including segregated operational technology networks, regular penetration testing, and employee training programs. The company maintains cyber insurance coverage of ₹100 crore, though management acknowledges that reputational damage from data breaches could exceed insured amounts.

Regional Economic Impact and Community Relations

GPIL's operations significantly impact Chhattisgarh's industrial economy. The company directly employs over 3,000 people and supports approximately 15,000 indirect jobs through contractors, suppliers, and service providers. Annual contribution to state exchequer through taxes, royalties, and duties exceeds ₹400 crore, making GPIL among the top five industrial taxpayers in Chhattisgarh.

Community development initiatives extend beyond mandatory CSR spending of approximately ₹20 crore annually. The company operates three schools serving 2,000 students in villages near its operations, provides healthcare through mobile clinics reaching 50,000 people annually, and supports skill development programs training 500 youth yearly in industrial trades.

The social license to operate, particularly crucial for mining operations, has been carefully cultivated through transparent community engagement. Regular public hearings, grievance redressal mechanisms, and preferential local employment policies have minimized operational disruptions from community protests that plague many mining companies.

Technological Frontier: Preparing for Green Steel

While the current operations rely on coal-based processes, GPIL has begun positioning for the eventual transition to green steel production. Research partnerships with IIT Kharagpur explore hydrogen-based DRI production, though commercial viability remains distant. The company has allocated ₹25 crore for green steel research over the next three years, modest by global standards but significant for a mid-sized Indian producer.

Carbon capture and utilization technologies are being evaluated for the planned integrated plant. While full-scale carbon capture remains economically unviable, selective capture from high-concentration streams could become feasible with anticipated carbon pricing mechanisms. Management estimates that carbon capture infrastructure could add ₹500-700 crore to project costs but might become mandatory by 2035.

The electric arc furnace route, already part of GPIL's operations, positions the company advantageously for a lower-carbon future. As grid electricity increasingly comes from renewable sources and green hydrogen becomes available for DRI production, the EAF route could achieve near-zero emissions. This optionality, while not immediately valuable, provides long-term strategic flexibility.

Global Market Position and Export Potential

While GPIL remains primarily domestic-focused, export opportunities are expanding. The company exported approximately 15% of pellet production in fiscal 2024, primarily to Middle Eastern and Southeast Asian markets. With Indian pellets gaining acceptance for quality consistency and the China+1 diversification strategy adopted by global steel producers, export potential could reach 25-30% of production by 2027.

The planned integrated steel plant includes provisions for producing export-grade products meeting international specifications. Investment in testing laboratories and quality certifications positions GPIL to serve demanding export markets. Management has indicated that 20-25% of the new plant's production could target exports, providing natural hedge against domestic demand cycles.

Trade agreements and diplomatic relations increasingly influence export competitiveness. The India-UAE Comprehensive Economic Partnership Agreement, reducing steel tariffs, has opened new markets. Similar agreements under negotiation with the UK and EU could further expand export opportunities. However, carbon border adjustment mechanisms being implemented in developed markets could impact competitiveness of coal-based production.

Financial Strategy and Capital Market Evolution

GPIL's approach to capital markets has matured significantly from the early IPO days. The company now maintains regular analyst calls, publishes detailed investor presentations, and provides forward-looking guidance within regulatory boundaries. This transparency has attracted institutional ownership, which has grown from 5% in 2018 to approximately 15% currently.

The debt-free status provides exceptional financial flexibility, but management remains cautious about leverage. Even for the ₹6,000 crore expansion, the company plans to maintain conservative leverage ratios. The funding strategy likely involves a combination of internal accruals (₹3,000-3,500 crore over construction period), strategic debt (₹2,000-2,500 crore), and potentially qualified institutional placement if market conditions are favorable.

Dividend policy has evolved to balance growth reinvestment with shareholder returns. While current dividend yield remains modest at less than 1%, management has indicated willingness to increase payouts once the integrated plant stabilizes. The share buyback programs, with ₹301 crore returned in 2024, demonstrate commitment to shareholder value when shares trade below intrinsic value.

Working capital management has improved dramatically, with cash conversion cycles reduced from 75 days in 2018 to 45 days currently. This improvement, achieved through better inventory management and favorable payment terms from established supplier relationships, releases approximately ₹200-250 crore in cash that would otherwise be trapped in working capital.

Industry Consolidation and M&A Outlook

The Indian steel industry stands at the cusp of consolidation, with smaller players struggling with environmental compliance costs and larger players seeking scale economies. GPIL's strong balance sheet and operational expertise position it as a potential consolidator, though management has emphasized organic growth over acquisitions.

Potential acquisition targets could include distressed pellet plants in Odisha, secondary steel units seeking backward integration partners, or captive power plants near existing operations. Management has indicated openness to opportunistic acquisitions but only at valuations providing clear value creation potential. The failed Jagdamba Power merger attempt has made shareholders more discerning about acquisition terms.

The reverse scenario—GPIL as acquisition target—cannot be dismissed. The company's captive mines, debt-free status, and efficient operations could attract interest from larger players seeking regional presence. However, with promoter holding at 63.48% and demonstrated commitment to long-term value creation, any hostile approach appears unlikely.

Conclusion: Assessing the Investment Proposition

Godawari Power & Ispat Limited stands as a testament to disciplined execution in cyclical industries. The transformation from near-bankruptcy to debt-free growth represents more than financial engineering—it reflects fundamental operational improvements, strategic positioning, and cultural evolution. The company that once struggled to service debt now contemplates its largest expansion with confidence born from crisis-tested capabilities.

The investment case rests on multiple pillars, each providing support but none individually sufficient. The captive mining assets provide sustainable cost advantages increasingly rare in global steel markets. The debt-free balance sheet enables opportunistic growth without existential risk. The integrated model from mine to finished products creates resilience through cycles. Management's demonstrated ability to navigate crisis and execute complex projects inspires confidence in future value creation.

Yet significant risks persist. The ₹6,000 crore integrated steel plant, while strategically sound, represents execution complexity exceeding anything previously attempted. Market timing remains uncertain—steel cycles are notoriously difficult to predict, and the plant could commence operations during a downturn. Environmental regulations continue tightening globally, potentially requiring additional investments in green technologies. The family-controlled structure, while providing stability, may limit institutional appeal and create eventual succession challenges.

For fundamental investors, GPIL represents a specific opportunity—a well-managed cyclical business with structural advantages trading at reasonable valuations. The current market capitalization of approximately ₹2,850 crore appears to undervalue the replacement cost of assets, particularly irreplaceable mining leases. The earnings power in mid-cycle conditions supports current valuations even without considering expansion benefits.

The broader narrative extends beyond investment returns. GPIL exemplifies India's industrial potential—building globally competitive manufacturing in tier-2 cities, creating employment in underdeveloped regions, and generating export earnings while serving domestic infrastructure needs. The company's journey from a single DRI kiln to integrated steel producer mirrors India's own economic evolution from protectionist isolation to globally integrated manufacturing.

Looking ahead, GPIL's success will depend on maintaining the discipline that enabled survival while embracing the ambition required for growth. The integrated steel plant represents not just capacity addition but a generational opportunity to establish GPIL among India's meaningful steel producers. Success would validate the patient building of capabilities over decades. Failure, while not fatal given the strong base business, would constrain ambitions and disappoint stakeholders who have supported the journey.

The ultimate measure of GPIL's transformation will come not from stock price movements or financial metrics but from sustainable value creation across cycles. Building a business that survives downturns, thrives in upturns, and consistently generates returns above cost of capital in a commoditized industry represents the holy grail of resource investing. GPIL has demonstrated the first two abilities; the coming decade will test the third.

As India's infrastructure buildout accelerates and global supply chains reconfigure, companies like GPIL with demonstrated execution capabilities, strategic assets, and strong balance sheets appear well-positioned to capture disproportionate value. Whether this potential translates to realized returns depends on factors both within management's control—execution, capital allocation, operational excellence—and beyond it—commodity cycles, regulatory changes, technological disruption.

For long-term investors willing to accept cyclical volatility in exchange for structural advantages and competent management, GPIL offers an interesting proposition. Not a smooth compounder generating predictable returns, but a thoughtfully managed cyclical business with sustainable competitive advantages and significant growth optionality. In the complex mosaic of Indian industrial companies, GPIL has earned its place through resilience, execution, and the disciplined pursuit of ambitious goals. The next chapter of this journey, as the company scales from regional champion to national player, promises to be as interesting as the remarkable transformation already achieved.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube