Goodluck India: From IIT Dorms to Defense Dreams - The Engineering Conglomerate That Bet on Everything

I. Introduction & Cold Open

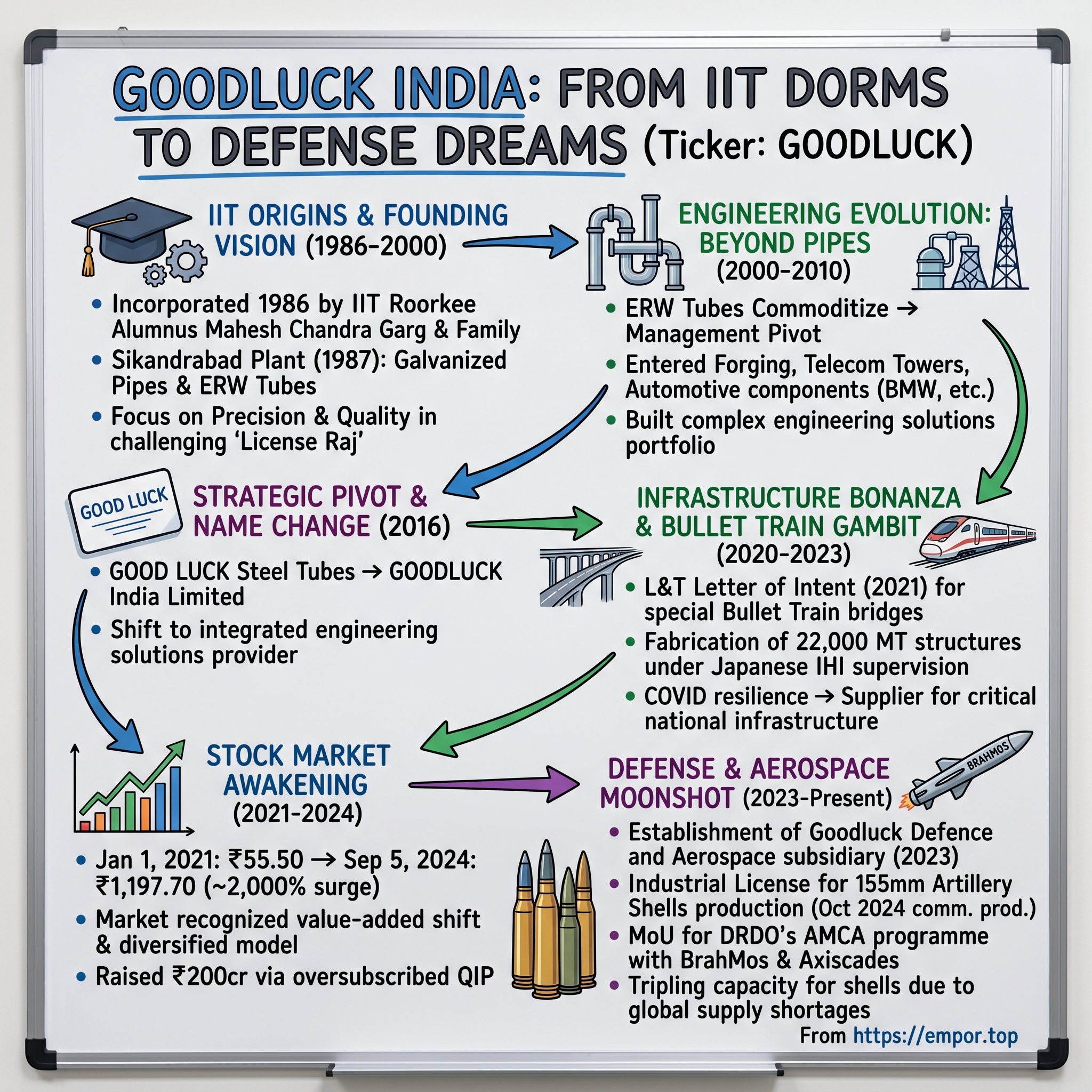

The afternoon of October 3, 2024 was electric at the Bombay Stock Exchange. At 9:36 AM, Goodluck India share price was trading 2.63 per cent higher at ₹1,342 per share, touching yet another all-time high. In the corporate offices of Ghaziabad, three generations of the Garg family watched as their four-decade-old engineering company crossed a watershed moment—the company announced that it has received an industrial licence under the Indian Arms Act, 1959, enabling it to begin production of empty shells.

For Mahesh Chandra Garg, the IIT Roorkee alumnus who had returned from working with multinationals abroad to start making pipes in 1987, this was vindication of a philosophy he'd held since the beginning: never stop evolving, never stop engineering. The company that started with galvanized pipes during the License Raj had just earned the right to manufacture artillery shells for a nation preparing for modern warfare.

How does a small pipe manufacturer transform itself into India's second-largest auto-grade precision steel tubes manufacturer with defense ambitions? How does a company that nearly everyone ignored for decades suddenly see its stock surge over 2,000% in just three years? And perhaps most intriguingly, how did a group of IIT graduates build one of India's most diversified engineering conglomerates by deliberately choosing the unglamorous path of B2B manufacturing?

The answer lies in a uniquely Indian story of patient capital, technical excellence, and the ability to spot infrastructure mega-trends before they become obvious. From irrigation pipes to bullet train bridges, from auto components for BMW to artillery shells for the Indian Army, Goodluck India's journey mirrors the transformation of Indian manufacturing itself.

Today, the company operates six state-of-the-art facilities across Uttar Pradesh and Gujarat with a capacity exceeding 500,000 metric tons per annum. It serves over 600 customers globally, exporting to more than 100 countries. With a market capitalization that has touched Rs 4,279 crore and targeting revenues of Rs 7,000-8,000 crore in the next 3-4 years, Goodluck India represents something rare in Indian markets—a company that built its fortune by making the things that make other things work.

This is that story.

II. The IIT Origins & Founding Vision (1986-2000)

The monsoon of 1986 was particularly harsh in North India, flooding fields and exposing the desperate need for better irrigation infrastructure. It was against this backdrop that Mahesh Chandra Garg, IIT Alumni & who has worked overseas with MNC and came back to India and started business in 1987. The decision seemed counterintuitive—leave a comfortable multinational job to manufacture pipes in Ghaziabad? But Garg saw what others missed: India's water crisis would only intensify, and someone needed to build the infrastructure to manage it.

Goodluck India Limited(Formerly known as Goodluck Steel Tubes Limited) was incorporated in Nov.'86 as a Private Limited Company and was converted into a Public Limited Company in 1994. The Company was promoted by M C Garg, K C Garg, Anil Kumar and K C Agarwal. The founding team wasn't just family—it was a brain trust of engineers who understood both the science of steel and the art of Indian business.

The first plant, commissioned in 1987 in Sikandrabad, was modest—a facility manufacturing galvanised steel tubes and pipes with diameters ranging from 1/2 to 10 at its plant in Sikandrabad. The plant had an installed capacity of 32,000 tonnes per annum (tpa). But what set Goodluck apart wasn't scale—it was precision. In an era when most Indian manufacturers competed on price, the IIT graduates insisted on competing on quality.

At the time, there was a huge demand for irrigation pipes due to a shortage of water supply. Goodluck India Ltd was initially started as a manufacturer of ERW tubes, which were at that time a value-added product and in demand. Electric Resistance Welded (ERW) tubes represented a technical leap from traditional pipes—they were stronger, more reliable, and commanded premium prices.

The License Raj years weren't kind to entrepreneurs. Getting raw materials required navigating bureaucratic mazes, securing working capital meant pledging everything, and finding customers willing to pay for quality over quantity was a daily battle. Yet the company demonstrated remarkable resilience—Despite stiff competition we have been profit making, Income Tax and Dividend paying since inception.

By 1994, sensing opportunity in India's gradual economic opening, the founders made a crucial decision—go public. In 1995, GSTL completed a public issue to part finance an expansion project to raise this capacity to 50,000 tonnes pa. The IPO wasn't just about raising capital; it was about institutionalizing the business, creating governance structures that would outlast the founders.

The late 1990s brought new challenges and opportunities. For the year 1999-2000, the company set up a cold rolling strip plant at its factory with a sales turnover of Rs. 5252.51 Lacs, representing a growth rate of 16%. This wasn't just capacity expansion—it was the beginning of vertical integration, a strategy that would define Goodluck's next two decades.

What distinguished the Garg family's approach was their engineering mindset applied to business strategy. While competitors chased volumes in commoditized products, Goodluck systematically moved up the value chain. They weren't building a pipes company; they were building an engineering solutions platform. Every new product line, every technical capability added, was a deliberate step toward becoming indispensable to India's industrialization.

The foundation laid in these early years—technical excellence, financial discipline, and strategic patience—would prove crucial as India entered a new millennium with ambitious infrastructure dreams.

III. The Engineering Evolution: Beyond Pipes (2000-2010)

The new millennium brought a revelation to Mahesh Garg and his team. Gradually, over a period of time, ERW tubes became commoditized products and soon the management realized this was not a business with technical barriers. Hence Goodluck India Ltd, owing to its engineering background, started entering into other business segments and extended into value-added segments. The business now has offerings across CR sheet and pipes, Precision pipes and auto tubes, Forging, and Engineering structure & fabrication.

The year 2006 marked a pivotal transformation. Rather than simply making tubes, Goodluck commissioned its first forging plant—a bold entry into precision engineering that required entirely different capabilities. Forgings weren't just bent metal; they were the critical components that held together India's growing industrial complex—from power plants to defense equipment.

The timing was prescient. India's telecom revolution was reaching its crescendo. Mobile towers were sprouting across the landscape like mechanical forests, each requiring precisely engineered structures that could withstand monsoons, earthquakes, and the weight of rapidly evolving transmission equipment. Goodluck positioned itself as the backbone of this digital revolution, manufacturing the towers that would connect a billion Indians.

In 2007, the company took another leap, commissioning its first plant for ERW/CDW Precision Tubes. These weren't your grandfather's pipes—they were engineered to tolerances measured in microns, designed for applications in automobiles, hydraulics, and specialized industrial equipment. The shift from commodity pipes to precision tubes was like a musician moving from playing scales to composing symphonies.

The 2008 global financial crisis tested every assumption. Credit markets froze, demand collapsed, and companies across India shuttered factories. Yet Goodluck's diversification strategy proved its worth. When construction slowed, automotive picked up. When telecom investments paused, government infrastructure spending accelerated. The company had engineered its own hedge—a portfolio of products that rarely declined simultaneously.

By 2010, Goodluck had quietly assembled one of India's most comprehensive engineering capabilities under one roof. From basic galvanized pipes to complex forgings for defense applications, from telecom towers to precision automotive components, the company had systematically built competencies that would take competitors decades to replicate.

The transformation wasn't just about products—it was about relationships. To meet challenges of ever increasing quality demand on our products we export 40-50% of our product which enables us to remain in touch with changing trends worldwide in our product basket. By maintaining such high export ratios, Goodluck forced itself to compete with global standards, using international markets as a crucible for continuous improvement.

What emerged from this decade wasn't just a larger company—it was a fundamentally different entity. The pipe manufacturer of 1986 had evolved into an engineering conglomerate capable of solving complex industrial challenges. This evolution positioned Goodluck perfectly for what was coming next: India's infrastructure supercycle.

IV. The Name Change & Strategic Pivot (2016)

June 2016 marked more than a corporate rebranding—it signaled a fundamental shift in ambition. Effective July 05, 2016, Good Luck Steel Tubes Limited will change its name to Goodluck India Limited. For a company that had built its reputation on steel tubes for three decades, dropping "Steel Tubes" from its name was like a caterpillar acknowledging its wings.

The boardroom discussions leading to this decision revealed a deeper strategic insight. India was on the cusp of its largest infrastructure build-out in history. The government's ambitious plans—smart cities, dedicated freight corridors, metro networks, renewable energy installations—all required not just steel tubes but integrated engineering solutions. The old name was becoming a straitjacket.

By 2016, Goodluck's client roster read like a who's who of Indian industry: L&T, Reliance, BHEL, PowerGrid, DRDO, ISRO, HAL. These weren't customers buying commodities; they were partners seeking engineering excellence. The automotive division was supplying precision tubes to BMW, Mercedes-Benz, and Toyota—companies that didn't compromise on quality.

The renamed entity immediately set about proving its expanded vision. The company announced that the company is coming up with new manufacturing facility for its existing line of business eg. steel tubes, pipes, precision tubes etc. at its land situated at village: SikraTaluka-Bhachau (Kachchh), Gujarat. The company's existing manufacturing capacity is 2,30,000 MTPA and presently running at optimal capacity utilization The proposed manufacturing facility of approx 72,000 MTPA will add in the company's total production capacity.

The Gujarat facility wasn't just about capacity—it was about proximity to ports, access to the western industrial corridor, and positioning for the next wave of growth. Unlike the commodity-focused expansions of the past, this facility was designed for flexibility, capable of producing everything from solar mounting structures to specialized forgings for aerospace applications.

The market initially yawned at the name change. The stock continued its sleepy trajectory, trading in a narrow band as investors struggled to understand what exactly Goodluck India was becoming. Was it a steel company? An auto ancillary? An infrastructure player? The answer was yes—to all of the above.

This strategic ambiguity was deliberate. While pure-play companies in each sector fought bloody price wars, Goodluck operated at the intersections, combining capabilities that few could match. Need specialized structures for a solar farm that also required precision tubes for tracking mechanisms? Goodluck could do both. Require forgings for defense equipment along with fabricated structures for the same project? One vendor, multiple solutions.

By late 2016, the company was supplying specialized products across an impossibly diverse range: railway bridges, transmission towers, boiler structures, defense components, automotive parts, and oil & gas equipment. Each vertical supported the others, creating a web of competencies that became increasingly valuable as India's infrastructure complexity grew.

The name change was a declaration: Goodluck was no longer defined by what it made, but by the problems it could solve. This positioning would prove prophetic as India embarked on its most ambitious infrastructure project yet—the bullet train.

V. The Infrastructure Bonanza & Bullet Train Gambit (2020-2023)

November 2021 brought news that would transform Goodluck's trajectory: Ghaziabad-based Goodluck India received a letter of intent (LoI) for an order worth Rs 198.76 crore by L&T for the bullet train project in the country for the supply and fabrication of special bridges. The company told the media that the LoI is awarded for the supply and fabrication of special bridges for the bullet train project on the National high-speed rail track between Mumbai and Vapi. The execution period of the order envisions the completion of the project by 2023.

But this wasn't just another infrastructure contract. It will be executed under the expert supervision of Ishikawajima-Harima Heavy Industries Corporation (IHI) -a Japanese expert in the design and supply area of steel bridges. For a company that started making irrigation pipes, working alongside Japanese engineering giants on India's most technologically advanced rail project was validation of a 35-year journey up the value chain.

The bullet train project revealed Goodluck's evolved capabilities. Goodluck India Ltd has been making fabricated structures for the bullet train project under a joint workshop of L&T, IHI Japan, and Goodluck at Bhuj. In this contract, L&T is giving the raw material and working capital risk and Goodluck India Ltd is only fabricating and supplying, While erection has been done by some other agency, Goodluck India Ltd has an order for 22,000 MT of fabricated structures for the bullet train project.

The scale was staggering—22,000 metric tons of fabricated structures that would carry trains at 320 kilometers per hour. These weren't ordinary steel structures; they required precision measured in millimeters, strength to withstand high-frequency vibrations, and durability to last decades. The margins were attractive, but more importantly, the project positioned Goodluck at the forefront of India's high-speed rail ambitions.

The pandemic years of 2020-2021 initially looked catastrophic. Factories shut, workers returned to villages, and demand evaporated overnight. Yet something remarkable happened at Goodluck—the company used the crisis as an opportunity to recalibrate. While competitors struggled with excess capacity, Goodluck's diversified portfolio provided unexpected resilience.

As the government unleashed unprecedented infrastructure spending to revive the economy, Goodluck found itself perfectly positioned. The company wasn't just a beneficiary of government spending; it had become critical infrastructure itself—supplying to PowerGrid for transmission projects, Indian Railways for modernization, renewable energy companies for solar installations, and now, the prestigious bullet train project.

By November 2024, 65% of this order has been produced with the remaining portion expected to be completed within the next 8 to 12 months. The execution wasn't just about fulfilling an order; it was about proving Indian engineering could meet Japanese standards, opening doors to future high-speed rail projects across Asia.

The bullet train project also brought unexpected benefits. Working with IHI Corporation exposed Goodluck's engineers to Japanese manufacturing philosophies—kaizen, just-in-time, total quality management—approaches that began permeating throughout the organization. The Kutch facility, from where these special structures were supplied, became a laboratory for manufacturing excellence.

Meanwhile, the broader infrastructure boom was accelerating. India's push for renewable energy meant thousands of solar installations requiring mounting structures. The electric vehicle revolution demanded specialized tubes for batteries and chassis. Smart cities needed everything from transmission towers to precision-engineered urban infrastructure. Goodluck was selling shovels in a gold rush, except these shovels were highly engineered, precision-manufactured, and irreplaceable.

VI. The Stock Market Awakening (2021-2024)

January 1, 2021: Goodluck India's stock closed at Rs 55.50, barely noticed by a market obsessed with technology stocks and pandemic darlings. By September 5, 2024, it had touched Rs 1,197.70—a mind-bending return of 2,049%. What happened in these three years wasn't just a stock price movement; it was the market's belated recognition of a transformation decades in the making.

The initial trigger was paradoxically subtle. As global supply chains fractured during COVID, companies worldwide began desperately seeking reliable suppliers. Goodluck's three decades of quiet competence suddenly became invaluable. Orders poured in—not just for pipes or tubes, but for complex engineering solutions that required multiple capabilities under one roof.

For the financial year 2021, the company reported a total income of Rs. 1578 crore. For the financial year 2021, the company reported a total profit of Rs. 300.55 crore after paying tax. But the real story wasn't in the absolute numbers—it was in the margins. As Goodluck shifted its product mix toward value-added products, EBITDA margins expanded from 8% toward 12%, with some divisions like precision tubes achieving 15%+.

The market structure worked in Goodluck's favor. With limited public float and strong promoter holding, every bit of positive news created outsized price movements. Institutional investors, initially skeptical of this "pipe company," began recognizing it as a play on multiple themes: infrastructure, defense, automotive, renewable energy. Why buy four different stocks when one company offered exposure to all of India's growth sectors?

In 2024, management made a strategic move that signaled confidence: raising INR 200 crore through a Qualified Institutional Placement (QIP). The funds weren't for survival—they were for dominance. The capital would fund the defense foray, expand precision tube capacity, and provide working capital for larger infrastructure projects. The QIP was oversubscribed, with marquee institutions fighting for allocation.

Management's communication evolved too. Mahesh Garg, typically conservative with guidance, began articulating a bold vision: Rs 165-170 crore net profit in FY25, with a pathway to Rs 400+ crore PAT in 3-4 years. Revenue targets of Rs 7,000-8,000 crore seemed audacious for a company that had just crossed Rs 4,000 crore, but the building blocks were in place.

The stock market loves narratives, and Goodluck had multiple stories to tell. The infrastructure story resonated with value investors. The defense entry excited growth investors. The consistent dividend payment since inception attracted income investors. The high insider ownership aligned with governance-focused funds. It was a Rorschach test where every investor saw what they wanted.

By late 2024, at a market capitalization exceeding Rs 4,000 crore, Goodluck had graduated from microcap to smallcap, triggering mandatory buying from index funds. The company that had operated in obscurity for decades was suddenly on every research desk's radar. Sell-side analysts scrambled to understand a business model that defied easy categorization.

Yet perhaps the most remarkable aspect of this rally was its sustainability. This wasn't a momentum trade or sectoral rotation; it was a fundamental rerating of a business whose quality had been hidden in plain sight. The market was essentially apologizing for three decades of neglect, and the apology came in the form of extraordinary returns.

VII. The Defense & Aerospace Moonshot (2023-Present)

Goodluck Defence and Aerospace Private Limited, a subsidiary of Good Luck India Limited established on August 31, 2023, is poised to transform India's defence manufacturing landscape with its advanced 155 mm artillery shell production facility. The timing wasn't coincidental—global ammunition supplies were stretched thin, defense budgets were exploding, and India's import dependence had become a strategic vulnerability.

The genesis of this defense pivot traced back to boardroom discussions in early 2023. The Ukraine conflict had exposed a harsh reality: modern warfare consumed artillery shells at rates not seen since World War II. European nations were desperately seeking suppliers, prices had tripled, and delivery timelines stretched to years. Meanwhile, India's own strategic requirements were evolving with tensions on multiple borders.

The license allows it to manufacture medium-caliber artillery shells in sizes 105mm, 120mm, 125mm, 130mm and 155mm, including HE M107 and ERFB variants. This wasn't just a manufacturing license—it was an entry ticket to one of the world's most regulated, most lucrative markets. The range of calibers meant Goodluck could supply ammunition for everything from light howitzers to heavy artillery systems.

The Sikandrabad facility represented a Rs 275 crore bet on India's defense indigenization. The state-of-the-art facility has an initial manufacturing capacity of 150,000 shells per annum, which is planned to be further augmented. But the real ambition was much larger—plans to pump up to ₹500 crore into its Uttar Pradesh facility, aiming to ramp up production of empty M107 155 mm artillery shell casings from 150,000 units to 400,000 units within the next year.

The economics were compelling. These shells, priced between USD 1,000–1,200 for high-grade variants like the 155mm HE, BB AISI 9260, target premium markets, positioning Goodluck as a key supplier to the Indian Army and international defence forces. At full capacity, the defense division could generate Rs 300+ crore in revenues with EBITDA margins exceeding 20%—double the company's traditional businesses.

October 8, 2024 marked a historic milestone: commercial production commenced. In a significant boost to India's 'Atmanirbhar Bharat' initiative, Goodluck India Limited's defence subsidiary Goodluck Defence and Aerospace Ltd has commenced commercial production of artillery Shells at its Sikandrabad in Uttar Pradesh manufacturing facility. The timing was perfect—global ammunition shortages meant order books could fill rapidly.

But Goodluck's defense ambitions extended beyond artillery shells. On September 30, 2025, Goodluck India entered a strategic alliance with BrahMos Aerospace Thiruvananthapuram Ltd (BATL) and Axiscades Technologies Ltd, signing a tripartite Memorandum of Understanding (MoU) to jointly bid for the Defence Research and Development Organisation (DRDO)'s Advanced Medium Combat Aircraft (AMCA) programme. The AMCA program represented India's ambitious fifth-generation fighter aircraft project—a quantum leap from making shells to potentially manufacturing components for stealth fighters.

The strategic logic was impeccable. Goodluck brought precision forging capabilities, established relationships with defense PSUs, and proven execution on complex projects. BrahMos brought missile technology expertise and government relationships. Axiscades brought aerospace engineering and design capabilities. Together, they formed a consortium that could compete for contracts worth thousands of crores.

The geopolitical context amplified the opportunity. The timing couldn't be more opportune. European countries, battered by the protracted Ukraine conflict and disrupted Russian supplies, have been in a frenzy to secure both artillery shells and the explosives that fill them—driving up prices and lead times worldwide. India, traditionally a major importer of defense equipment, was positioning itself as an exporter—and Goodluck intended to ride this wave.

Competition existed, notably from Bharat Forge, which had decades of defense experience. But Goodluck's integrated capabilities—forging, machining, heat treatment, and coating—provided a competitive edge. While others outsourced processes, Goodluck could control quality and timelines end-to-end.

By late 2024, the defense division was already fielding inquiries from multiple countries. The Indian Army's requirements alone could absorb the initial capacity, but export opportunities to Europe, Middle East, and Southeast Asia promised exponential growth. Management's conservative guidance of Rs 250-300 crore defense revenues seemed increasingly like sandbagging.

VIII. Modern Operations & Manufacturing Excellence (2024-Present)

Six manufacturing facilities across two states, 412,000 metric tons of annual capacity, 4,000+ employees, exports to 100+ countries—by 2024, Goodluck India had evolved into an engineering powerhouse that bore no resemblance to the pipe manufacturer of 1986. Yet the transformation was just beginning.

The crown jewel of the expansion was the new hydraulic tube plant in Bulandshahr. INR 250 crore hydraulic tube plant in Bulandshahr, 50,000 tonnes capacity, expected INR 500 crore revenue. This wasn't just another tube plant—it was one of the most advanced facilities of its kind in Asia, producing hydraulic tubes that could replace expensive seamless imports. The timing was perfect: India's construction equipment sector was booming, and every excavator, crane, and hydraulic system needed these specialized tubes.

The Ghaziabad CDW/ERW facility added another 50,000 MTPA, taking total precision tube capacity to 166,000 MTPA. But capacity was just one dimension—the real edge lay in capability. The facility could produce tubes with tolerances that most competitors couldn't achieve, opening doors to aerospace and defense applications where precision was non-negotiable.

Product portfolio diversity had become Goodluck's signature strength. On any given day, the factories might be producing:

- Precision tubes for Tesla's suppliers

- Forged components for BrahMos missiles

- Special steel bridges for the bullet train

- Solar mounting structures for renewable projects

- Crash barriers for highway safety

- Specialized flanges for oil refineries

This diversity wasn't random—it was carefully orchestrated. Each product line shared certain core competencies (metallurgy, precision engineering, quality control) while serving different end markets. When automotive demand slowed, infrastructure picked up. When government spending cycled down, exports compensated. The portfolio had been engineered for resilience.

The workforce evolution was equally remarkable. The company is led by first-generation techpreneur Mr. Mahesh Chandra Garg, an IIT Roorkee alumnus, and supported by three generations of professionally qualified family members, showcasing a legacy of over 37 years of industry excellence. The third generation brought fresh perspectives—digital transformation, sustainability initiatives, and global ambitions—while respecting the engineering-first culture that defined Goodluck.

Modern Goodluck operated with a startup's agility despite its four-decade heritage. When electric vehicle manufacturers needed specialized battery-pack tubes, Goodluck developed them in months, not years. When renewable energy companies required innovative mounting solutions for curved surfaces, Goodluck's engineers delivered custom designs. This responsiveness, rare in traditional manufacturing, became a competitive moat.

Quality certifications told another story of evolution. ISO 9001 was table stakes—Goodluck held specialized certifications for automotive (IATF 16949), aerospace (AS9100), and defense manufacturing. Each certification represented years of process improvement, documentation, and culture change. They were tickets to conversations with global OEMs who wouldn't even consider suppliers without them.

The financial metrics reflected operational excellence. Working capital cycles, traditionally the bane of infrastructure companies, were managed at 100-110 days despite the long-cycle nature of projects. Capacity utilization consistently exceeded 85%, remarkable for such a diversified operation. Return on capital employed had expanded from single digits to mid-teens, validating the value-addition strategy.

By late 2024, Goodluck India had become something unique in Indian manufacturing—a company that could credibly claim expertise from commodity steel products to aerospace components. The journey from pipes to precision had taken four decades, but the company was just getting started.

IX. Playbook: The B2B Conglomerate Strategy

The Goodluck story challenges conventional wisdom about focused strategies and pure plays. In an era where conglomerates trade at discounts and specialization is valorized, how did a company that makes everything from pipes to missile components create spectacular shareholder value? The answer lies in understanding the unique dynamics of Indian B2B manufacturing.

The IIT Advantage

Technical credibility matters immensely in B2B relationships. When Mahesh Garg, an IIT Roorkee alumnus, walked into a client's office, he wasn't a salesman—he was an engineer talking to engineers. This technical DNA permeated the organization. Problems were solved through first principles thinking, not by throwing money or people at them. When DRDO needed specialized forgings, they trusted Goodluck because they knew the company understood metallurgy at a molecular level.

Riding Government Capex Cycles

Goodluck mastered the art of surfing government spending waves. The company didn't just wait for tenders; it anticipated them. Years before the bullet train project was announced, Goodluck was building capabilities in specialized fabrication. Before defense indigenization became policy, the company was investing in forging capabilities. This anticipation required deep understanding of policy directions, budget allocations, and bureaucratic processes—knowledge accumulated over decades.

The Value-Addition Ladder

The journey from commodity pipes (8% margins) to precision tubes (15% margins) to defense products (20%+ margins) wasn't accidental—it was architected. Each step up the value chain built on previous capabilities while adding new ones. The commodity business provided volume and cash flow. The precision business brought technology and quality systems. The defense business leveraged everything that came before while adding regulatory expertise and security clearances.

Working Capital Mastery

Infrastructure projects meant extended working capital cycles—sometimes exceeding 150 days. Lesser companies would have choked on cash flow. Goodluck turned this challenge into competitive advantage. Strong banking relationships, built over decades of conservative financial management, meant access to working capital at competitive rates. More importantly, the diversified portfolio meant cash flows from different businesses offset each other's cycles.

Family Business, Professional Management

The three-generation involvement could have been a recipe for nepotism and stagnation. Instead, it became a source of strength. The first generation brought entrepreneurial energy and technical expertise. The second generation added scale and systems. The third generation is driving digital transformation and global ambitions. Yet the family never exceeded their circle of competence—key positions like CFO and factory heads were held by professionals.

The Timing Paradox

Goodluck's entries into new sectors often seemed late—they weren't first in forgings, precision tubes, or defense. But being second or third had advantages. The pioneers had already educated the market, proven demand, and made expensive mistakes. Goodluck could enter with better technology, refined processes, and established relationships. The bullet train project exemplified this—L&T took the primary contract and risk, while Goodluck captured attractive margins as a specialized supplier.

Trust as Currency

In B2B manufacturing, trust is everything. A single quality failure can destroy decades of relationship building. Goodluck's perfect track record—no major quality issues, no significant delivery failures, consistent dividend payments since inception—became its most valuable asset. When PowerGrid needed critical transmission infrastructure, when the bullet train project required zero-defect components, when BrahMos needed specialized forgings, they chose Goodluck not because it was cheapest, but because it was reliable.

This playbook—technical excellence, patient capital, strategic diversification, operational discipline—created a business model that's both resilient and scalable. It's a uniquely Indian approach to manufacturing, one that acknowledges the country's infrastructure gaps as opportunities rather than obstacles.

X. Bear vs Bull Case & Valuation Analysis

Bull Case: The Infrastructure Supercycle Thesis

The bulls see Goodluck India as perfectly positioned for a multi-decade infrastructure boom. India's infrastructure spending is projected to exceed $1.4 trillion by 2025. The government's ambitious targets—100 GW of solar capacity, 500 km of metro rail annually, modernization of 100 railway stations, three new bullet train corridors—all play directly to Goodluck's capabilities.

The defense opportunity alone could transform the company. With India's defense exports crossing ₹21,000 crore in FY 2024-25 and Europe projected to import over 1 million 155 mm rounds annually through 2027, Goodluck's tripling of capacity could translate into revenues exceeding ₹300 crore from shells alone. If the company captures even 5% of India's growing defense exports, revenues could exceed Rs 1,000 crore from this division alone.

Management's execution track record provides confidence. They've consistently delivered on promises—the bullet train project execution, successful QIP, precision tube plant commissioning. The conservative guidance of Rs 165-170 crore PAT for FY25 seems achievable, with upside from defense production and margin expansion.

The valuation remains reasonable despite the rally. At 21-22x P/E, Goodluck trades at a discount to specialized peers in individual sectors. If one values each division separately—pipes at 15x, precision tubes at 20x, defense at 30x, engineering structures at 18x—the sum-of-parts valuation exceeds Rs 5,000 crore, suggesting 20%+ upside.

Multiple expansion catalysts exist: inclusion in broader indices, discovery by global funds seeking India infrastructure plays, potential defense export breakthroughs, or strategic partnerships with international OEMs. The company's transformation from commodity manufacturer to engineering solutions provider warrants a rerating similar to what happened with companies like Bharat Forge or Motherson Sumi.

Bear Case: The Execution and Cycle Risk

The bears worry about execution complexity. Managing six facilities, four distinct business verticals, and 4,000+ employees while maintaining quality standards across diverse products is enormously challenging. One major quality issue—a defective batch of artillery shells, a failed bullet train component—could destroy decades of reputation.

Working capital requirements remain concerning. Despite management's skill, 100+ day cycles mean enormous capital locked in operations. As the company scales to Rs 7,000-8,000 crore revenue, working capital needs could exceed Rs 1,500 crore. Any disruption in payment cycles—a government budget crisis, client bankruptcy—could create severe stress.

Competition is intensifying across every vertical. In pipes, APL Apollo and Jindal have deeper pockets. In forgings, Bharat Forge has decades more experience. In defense, established players like L&T and newer entrants backed by large conglomerates are aggressively expanding. Goodluck's diversification, while providing resilience, also means competing against specialists in each vertical.

Commodity price volatility poses constant risk. Steel prices can swing 30% in months, and while Goodluck has pricing power in value-added products, the commodity business remains vulnerable. Raw material costs constitute 65-70% of revenues—a 10% adverse movement in steel prices could wipe out a quarter's profits.

Government dependence is structural. Whether it's infrastructure spending, defense procurement, or railway modernization, Goodluck's fortunes are tied to government capex cycles. Political changes, fiscal constraints, or policy shifts could dramatically impact order books. The company's private sector exposure, while growing, isn't sufficient to offset government volatility.

The Valuation Debate

At Rs 4,000+ crore market cap, Goodluck is priced for perfection. The stock's 2,000% rally has already captured much of the obvious upside. Any disappointment—a delayed defense license, execution hiccups, margin compression—could trigger significant correction. The limited float means the stock could fall as dramatically as it rose.

Yet the transformation story may be just beginning. If management delivers on their Rs 400+ crore PAT target, the stock could still double from current levels. The key question isn't whether Goodluck is cheap or expensive—it's whether this engineering conglomerate can successfully navigate its ambitious expansion while maintaining execution excellence.

XI. Lessons & Reflections

The Goodluck India story offers profound lessons for investors, entrepreneurs, and anyone interested in how businesses really get built in India. Strip away the stock charts and press releases, and what emerges is a masterclass in patient company building.

The Power of Patient Capital

In an era of unicorns and rapid exits, Goodluck spent 35 years building capabilities before the market noticed. The Garg family never diluted unnecessarily, never chased vanity metrics, never compromised long-term sustainability for short-term gains. They understood that in manufacturing, competitive advantages compound slowly but surely. The spectacular returns of 2021-2024 weren't created in those three years—they were earned over three decades.

Boring Businesses, Spectacular Returns

While investors chased software companies and platform businesses, Goodluck quietly built a fortune making things nobody thinks about—the tubes in your car's chassis, the towers carrying your phone calls, the structures that will carry bullet trains. These aren't sexy products, but they're essential. And essentiality, combined with execution excellence, creates pricing power that software companies would envy.

First-Mover Disadvantage

Goodluck was rarely first in any market. They weren't the first to make pipes, forgings, or defense products. But being second or third meant learning from others' mistakes, entering with better technology, and capturing markets that pioneers had already educated. The bullet train project exemplified this—Goodluck let others take the headline contracts while capturing the specialized, high-margin work.

Stakeholder Complexity as Moat

Managing relationships with government bureaucrats, Japanese engineers, German automotive companies, and defense establishments simultaneously is enormously complex. This complexity, which would paralyze most companies, became Goodluck's moat. Every additional stakeholder relationship, once established, made the company more indispensable and competitors' entry more difficult.

Trust Compounds

In B2B manufacturing, trust is the ultimate currency. Every on-time delivery, every quality certification, every successfully executed project added to a trust bank that took decades to build. When the artillery shell license was granted, it wasn't just based on manufacturing capability—it was recognition of 37 years of reliable execution. This trust, invisible on balance sheets, may be Goodluck's most valuable asset.

Technical Founders' Enduring Advantage

The IIT founder advantage went beyond the obvious technical competence. It shaped company culture—problems were solved through engineering, not financial engineering. It influenced hiring—engineers were valued over MBAs. It determined strategy—technical difficulty was pursued, not avoided. In a manufacturing business, this engineering-first mindset proved invaluable.

The India Advantage

Goodluck's story is uniquely Indian. The infrastructure gaps that frustrate many became opportunities. The bureaucratic complexity that deters foreign competitors became a moat. The family business structure that seems antiquated to Western investors provided patient capital and long-term thinking. Understanding India's peculiarities and turning them into advantages—this may be the greatest lesson of all.

The Goodluck story isn't finished. With defense production commencing, artillery shell capacity expanding, and management targeting dramatic growth, the next chapter could be even more remarkable than the last. But regardless of what comes next, the journey from a small pipe manufacturer to a diversified engineering conglomerate offers timeless lessons about building enduring businesses.

In the end, Goodluck India represents something increasingly rare—a company that creates real value by making real things, run by people who understand their products at a molecular level, pursuing opportunities others ignore, and doing so with patience that modern markets rarely reward but ultimately must recognize. It's not just a business story; it's a blueprint for how manufacturing excellence can create extraordinary wealth in an economy transitioning from developing to developed.

The pipes that started it all are still being manufactured in Sikandrabad. But today, they're made alongside components that might defend the nation's borders or carry its first high-speed trains. From irrigation to ammunition, from IIT dorms to defense dreams—Goodluck India bet on everything, and increasingly, it looks like everything is paying off.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube