Gokaldas Exports: The Private Equity Turnaround Masterclass

I. Introduction & The "Blackstone" Shadow

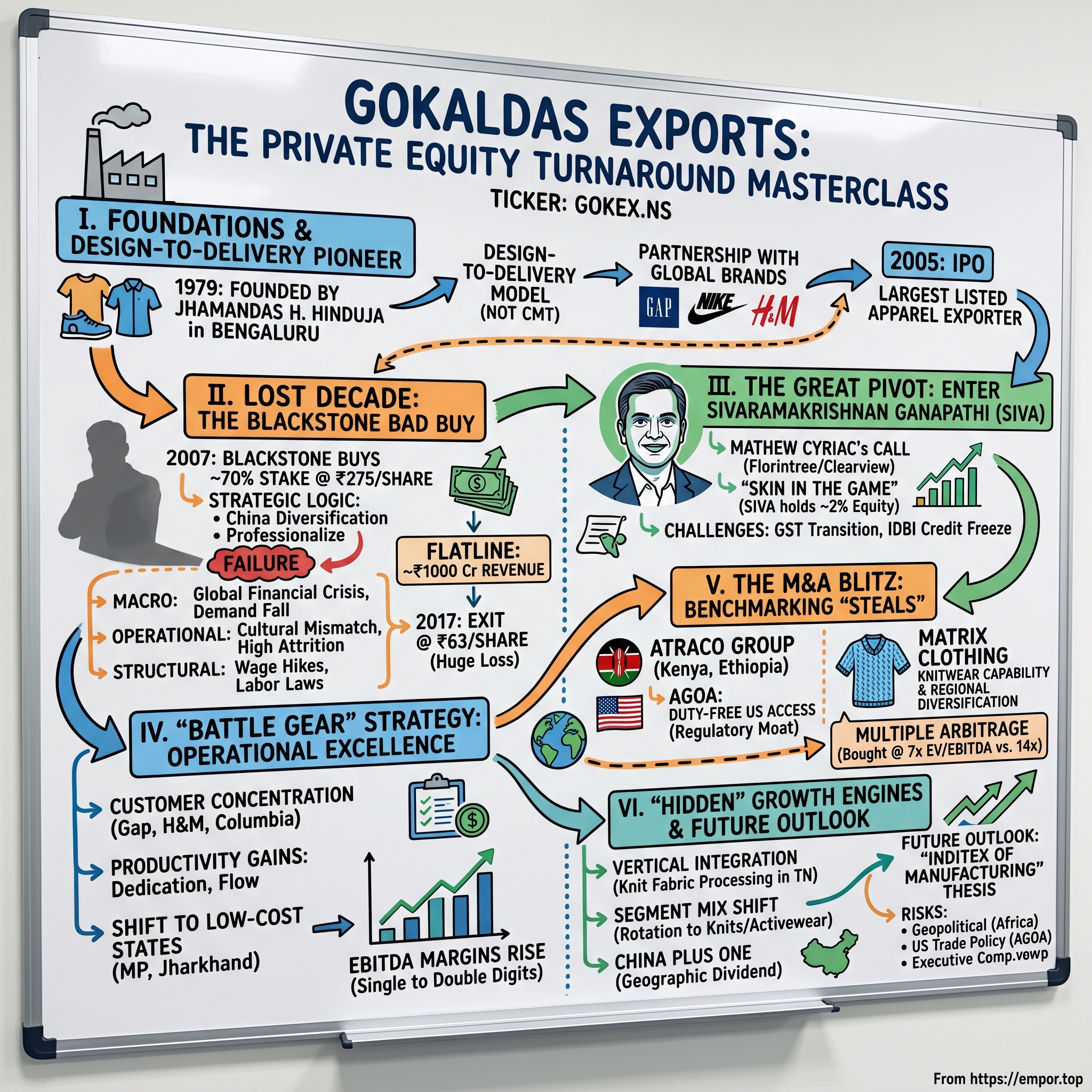

Picture a Bengaluru factory floor in the summer of 2017. Sewing machines hum in long parallel rows. Pattern cutters move with the practiced indifference of people who have been making garments for two decades. Outside, on the company's investor relations page, a quiet press release sits like an admission of defeat: Blackstone, the largest private equity firm in the world, was exiting गोकुलदास एक्सपोर्ट्स लिमिटेड Gokaldas Exports Limited at roughly ₹63 per share — a price that valued the company at about a quarter of what Blackstone had paid for it ten years earlier.[^1]

That is not a typo. The world's most celebrated alternative-asset manager — the firm that had built its reputation on Hilton, Equity Office, and a dozen other textbook leveraged buyouts — had just taken what insiders politely called a "textbook failure" in India.[^1] The deal had been priced in 2007 at ₹275 per share for roughly 70 percent of the company, valuing Gokaldas at around $160 million in equity at the time.1 Blackstone had bought right at the peak of the pre-Lehman euphoria, watched the Global Financial Crisis vaporise discretionary apparel demand, ridden out a decade of muscle-cramped working capital, and ultimately handed the keys to a fund called Clearview Investment Holdings — controlled by Mathew Cyriac, the same banker who, in his earlier Blackstone life, had originally championed the Gokaldas buyout.[^1]

If the story stopped there, this would be a cautionary essay about hubris in emerging-market PE. But it doesn't stop there. From that low base of roughly ₹63 per share in 2017, Gokaldas's stock compounded into a multi-bagger across the next eight years, riding a transformation under a new professional CEO and two transformative cross-border acquisitions.2 The "PE write-off" became, in the language of the trade, a "ten-bagger." A company that the smartest money on the planet had given up on emerged as one of India's most credible global garment platforms.

What changed? Not the sewing machines. Not the customer list — Gap, H&M, Columbia, Nike — most of them were already there in 2007.3 What changed was who sat in the corner office, what the incentive structure looked like, and how capital got deployed.

This is the story of how a third-generation Sindhi family business became a private equity poster child, then a private equity embarrassment, then — through the unlikely hands of a professional manager named Sivaramakrishnan Ganapathi शिवरामकृष्णन गणपति, formerly of Idea Cellular and Wipro — a textbook case in what happens when you finally pair operational obsession with skin in the game.2 It is also a story about India's place in the global apparel supply chain at a moment when 中国加一 the "China Plus One" sourcing thesis is reorganising who makes the world's t-shirts and Columbia ski jackets.

The roadmap: We start with the founding by Jhamandas H. Hinduja in 1979, when "Made in India" garments meant something very different than it does today. We move through the IPO mania of 2004–2005, when Gokaldas became the country's largest listed apparel exporter.4 We sit through the lost decade of the Blackstone years. We watch the 2017 handover, the 2018 near-death experience, and the slow, grinding rebuild. We then accelerate through the Atraco and Matrix Clothing acquisitions of 2024, which doubled the platform overnight and gave Gokaldas duty-free factories in Kenya and Ethiopia at exactly the moment Washington was reaching for tariff levers against China and Bangladesh.56 And we end on the question that every long-term holder is currently asking: in the era of cinematic geopolitical risk, fast fashion, and ESOP proxy fights, can a contract garment maker really compound like an Inditex of manufacturing?

Stick around. The seams are surprisingly load-bearing.

II. Foundations & The "Design-to-Delivery" Pioneer

It is helpful, before getting to the financial engineering, to spend a minute on the founding scene — because Gokaldas's original moat was not a balance sheet at all. It was an attitude.

In the late 1970s, India's garment export industry was, charitably, an embarrassment. The country sold cotton bales and yarn to the world, then watched Hong Kong, Taiwan, and South Korea cut and sew that yarn into the t-shirts and jeans that ended up on American shelves. The Multi-Fibre Arrangement — a brutally complicated quota system that governed global textile trade from 1974 until 2005 — actually protected some of India's mediocre players by capping how much the more efficient East Asian factories could ship to the United States.[^8] In other words, India was running a quota-protected garment sector that had no real reason to get good.

Into that landscape stepped Jhamandas H. Hinduja जमणदास हिन्दूजा, a Sindhi entrepreneur who founded Gokaldas in 1979 in Bengaluru — at the time still spelled and pronounced Bangalore, and very much not yet a tech city.4 Bengaluru was chosen partly because of climate (cotton garments dislike Mumbai humidity), partly because of labor (Karnataka had a deep pool of women who could be trained on sewing lines), and partly because Karnataka's industrial policy was less hostile than Maharashtra's. The Hinduja family — distinct from the much larger London-based Hinduja Group of Srichand and Gopichand Hinduja, despite the shared surname — was a tightly held, traditionally run business clan.

What separated Gokaldas in those first two decades was not capacity. It was that the company decided to design. Most Indian garment exporters lived on what insiders call CMT — "cut, make, trim." A buyer in New York or London sent a pattern, the factory cut fabric to the pattern, sewed it together, trimmed the loose threads, slapped on a label, and shipped it. The factory captured maybe 8–10 percent margin on the cheapest possible part of the value chain. Design — selecting the season's wash, choosing the trims, sketching the silhouette — was done in studios in Manhattan, London, Düsseldorf.

The Hinduja brothers reversed this. By the late 1990s, Gokaldas was operating what the industry called "design-to-delivery." That meant in-house design studios, in-house fabric sourcing teams, in-house wash development, in-house trim engineering. When Gap Inc. ordered 50,000 men's chinos for next spring, Gokaldas didn't wait for a Tech Pack from San Francisco. Gokaldas's own designers — sitting in Bengaluru, watching what was selling on Bond Street and Fifth Avenue — proposed the wash, the rise, the pocket placement, and walked the buyer through the prototypes.[^9] That is the difference between being a vendor and being a partner. Partners get the next season's order book before the spreadsheet competition has been asked to bid.

By the early 2000s, Gokaldas was sewing for essentially every name in Western mass-market apparel: Gap, Old Navy, Banana Republic, Nike, Adidas, Tommy Hilfiger, Marks & Spencer, GAP Body, J.C. Penney.3 The product mix was overwhelmingly woven — pants, shorts, jackets, outerwear — which is the harder, higher-skill end of the garmenting business. (Knits, the soft-jersey t-shirts and polo shirts, are a different industrial process entirely — circular knitting machines, calendaring, very different cut patterns. We will come back to this distinction, because it matters enormously to the modern story.)

Then came the moment that changed everything: the IPO. In March 2005, Gokaldas Exports listed on the NSE and BSE. The price band was set at ₹375–425 per share, the issue was oversubscribed roughly 42 times, and the listing made the Hinduja family one of the wealthiest garment-export clans in India.4 The timing was extraordinary. The Multi-Fibre Arrangement had just expired on January 1, 2005. With quotas dismantled, the question was: which countries would absorb the freed-up global apparel volumes? India seemed an obvious answer — and Gokaldas, as the country's largest and best-known apparel exporter, was the obvious vehicle.

But there were two countries the bulls did not pay enough attention to: Bangladesh and Vietnam. বাংলাদেশ Bangladesh, with wages roughly half of India's and a state structure that bent over backward for garment investors, would shortly overtake India in total garment exports.[^8] Vietnam, with its proximity to Chinese yarn supply and its eventually-very-favorable trade deals with the US and EU, would do the same. India, despite all the quota-expiry hype, would lose share over the next decade.

This is the context Gokaldas walked into. The IPO had crowned them king of a domain that was about to lose its global throne. And waiting in the wings, with a $150 million-plus checkbook and a freshly opened India office, was a buyer who very much wanted to own that crown.

III. The Lost Decade: The Blackstone "Bad Buy"

In the summer of 2007, the smartest people in finance were, on average, the most wrong people in finance. The cheap-debt party was in its final, most euphoric hours. Bear Stearns had just bailed out two of its mortgage hedge funds. Indian PE deal volumes were at all-time highs. Blackstone, fresh off its own blockbuster New York IPO in June 2007, was deploying capital aggressively into India.

In August 2007, Blackstone announced its acquisition of approximately 70 percent of Gokaldas Exports from the Hinduja family at ₹275 per share, valuing the equity check at roughly $165 million — at the time one of the largest private equity deals in Indian apparel.1 Blackstone made an open offer to public shareholders at the same price to comply with SEBI takeover rules. The deal was championed within Blackstone by Mathew Cyriac, then the firm's senior India dealmaker — a fact that will become important again.[^1]

The strategic logic was textbook. Buy India's largest listed garment exporter at a moment when global brands were diversifying away from China, professionalise the management, scale capacity, install systems, and exit at a multiple expansion — perhaps by selling to a strategic buyer like a Crystal Group or Li & Fung, perhaps via a secondary IPO. On a back-of-envelope, this was supposed to be a 3x deal over five years.

What happened next is by now well-documented in the Indian financial press, but worth pulling apart properly. Three things broke at once.

The first was simply macro. Within a year of the deal closing, Lehman Brothers collapsed, US consumer discretionary spending fell off a cliff, and Gap Inc. cut order books across every Asian vendor. Order volumes from Gokaldas's top customers fell sharply in 2008–2009. A garment factory's economics are vicious in a downturn: labor cost is fixed (you cannot fire 30,000 workers in India without massive severance), real estate is fixed, but order volumes flex with global retail. Operating leverage runs in reverse. Margins evaporated.

The second was operational. PE firms are excellent at financial engineering — capital structure, working capital efficiency, cost rationalization, board governance. They are notoriously less good at the daily operational grind of a labor-intensive factory floor. Garmenting is a high-touch, low-margin business where the difference between making 8 percent and making 3 percent is whether your supervisors notice that the seam tolerance on a particular SKU is drifting up by two millimeters. Blackstone parachuted in CEOs from outside the industry. Cultural fit with the legacy Hinduja-trained shop-floor managers was poor. Attrition spiked. Customer relationships, built over twenty years of trust between Hinduja patriarchs and Gap buyers, fell into the hands of executives who would rotate out within eighteen months.

The third was structural. India's labor laws made factory closure or relocation expensive. The rupee strengthened against the dollar in patches, squeezing dollar-billed garment exporters. And the geographies that were eating India's lunch — Bangladesh, Vietnam, eventually Ethiopia — were enjoying favorable duty regimes and lower wage bases.

The result was what the Economic Times in 2017 called a "flatline."[^1] For nearly a decade, Gokaldas revenue oscillated in a tight band around ₹1,000 crore, while operating margins ranged from low single digits to outright losses. Blackstone gradually increased its ownership above 70 percent as it tried to consolidate control, but the company simply would not turn. By 2016, the situation had become embarrassing — for a marquee PE name accustomed to victory laps, owning what one Indian financial journalist termed a "stuck asset" was painful.

Enter Mathew Cyriac. Cyriac had left Blackstone in 2015 to start his own platform, Florintree Advisors, focused on Indian mid-market opportunities. In 2017, through a Florintree-managed vehicle called Clearview Investment Holdings, he agreed to buy Blackstone's stake in Gokaldas — at ₹63 per share, a roughly 77 percent discount to Blackstone's original purchase price.[^1] On a marked-to-market basis, including dividends and the time value of money, Blackstone had effectively lost the substantial majority of its original $160 million-plus investment over a ten-year hold.[^1]

What makes this a particularly cinematic chapter of Indian PE history is the mirror symmetry. The same person who had originally championed the Blackstone buyout in 2007 was now, ten years later, buying it back at a fraction of the price under his own banner. It is hard to invent a more on-the-nose epilogue. There were no public recriminations. Cyriac, by all accounts a thoughtful and self-aware operator, framed the deal in his post-Blackstone interviews not as an indictment of his prior work but as a recognition that the business had been mispriced both ways — that 2007 was too high, but that 2017 was almost certainly too low.[^1]

He was right about the second part. He was also about to make a hiring decision that, in retrospect, mattered far more than the entry price.

IV. The Great Pivot: Enter Sivaramakrishnan Ganapathi

If you had been in the executive lounge of the Indian Institute of Management Bangalore in the mid-1990s and pointed at the two men who, two and a half decades later, would resurrect a public-equity write-off — Mathew Cyriac and Sivaramakrishnan Ganapathi — you would have been laughed at. They were classmates. They were friends. Neither had any obvious connection to garmenting. Cyriac would spend his career in finance. Ganapathi — Siva, to almost everyone in Indian corporate circles — would spend nearly two decades in mobile telephony and consumer durables, rising to Chief Operating Officer of Idea Cellular, the Aditya Birla Group's wireless arm.2

By 2017, when Cyriac took over Blackstone's stake in Gokaldas, Siva was somewhere between assignments. Cyriac picked up the phone. The pitch was unusual: take over a tired, capital-starved, family-history-laden garment business that the world's largest PE firm had failed to turn around. The compensation structure would be unusual too: a meaningful equity stake alongside the cash compensation, so that the new MD's personal balance sheet would rise and fall with shareholder returns.[^9]

Siva accepted. He joined Gokaldas as Vice Chairman and Managing Director in 2017. Today he holds roughly 2 percent of the equity — a figure that sounds modest until one considers that in Indian listed companies it is genuinely unusual for a non-founder, non-family professional manager to hold a stake of that size in his or her own right.7 For context, most Indian listed-company CEOs hired from outside the founding family hold somewhere between 0.05 and 0.3 percent in equity-linked compensation, often in the form of unvested ESOPs. Siva's position was structurally different from day one: he was not a hired hand. He was a co-owner.

That distinction is not academic. The behavior of professional managers in India shifts measurably based on whether they own equity outright. Equity owners — particularly those who paid for their equity in cash — tend to obsess about return on capital. They are reluctant to do empire-building acquisitions that dilute their own holding. They cut underperforming product lines without sentiment. They worry about working capital. Pure salary-plus-options CEOs, by contrast, can sometimes drift toward revenue maximisation, because revenue growth typically drives both their reputation and their option payoff, even when it destroys returns.

Siva, by every account from the people who worked under him, walked in and behaved like an owner. His public communication style is unusually direct for an Indian CEO. He uses precise language in earnings calls — "our customer concentration", "our capital allocation", "our return on capital employed" — not the fluffy verbiage of expansion-for-its-own-sake.[^9] He sets quantitative targets and acknowledges misses without sandbagging.

But before any of this could matter, Siva had to survive his first six months.

In July 2017, the Indian government rolled out the Goods and Services Tax, the largest indirect-tax reform in the country's history. For garment exporters, the GST transition was operationally catastrophic — the input tax credit mechanism for inverted duty structures (where input taxes are higher than output taxes) created enormous refund pile-ups, freezing working capital for months. Around the same time, the Reserve Bank of India placed IDBI Bank, Gokaldas's primary lender, under Prompt Corrective Action (PCA), which severely restricted IDBI's ability to extend new credit.8 For a garment exporter — a business that lives or dies on the float between paying suppliers and getting paid by overseas buyers — a frozen working-capital line is a death sentence.

The crisis story, retold later by Siva in interviews, was almost tragicomic. He spent his first months on the job not redesigning the strategy or visiting customers, but driving between banks in Mumbai, Bengaluru, and Delhi trying to assemble a syndicate of lenders who would replace IDBI's frozen facility.2 He renegotiated supplier terms personally. He flew to San Francisco and to Bentonville, told Gap and other key customers exactly what the company was going through, and asked for accelerated payments on a temporary basis. The customers, perhaps sensing a man who was telling them the truth, agreed.

By the time the working-capital crisis was resolved in 2018, Siva had two assets the previous decade had stripped away: customer goodwill earned in a foxhole, and a management team that had watched the new CEO personally save the company. From that point, the rebuild was on solid foundations.

It is also worth flagging, because the next chapters lean on it, that Siva's compensation has been controversial. Indian proxy advisors — particularly IiAS — have at multiple junctures publicly objected to elements of his pay package, especially the variable component and proposed ESOP grants. In January 2025, an institutional shareholder bloc successfully voted down a proposed ESOP allotment to him, citing what they considered overly generous terms.[^12] Siva's defenders point to the multi-year stock price performance and the equity he has already put at risk; his critics point to absolute compensation levels and to the optics of a manager voting himself further dilution. Reasonable people can disagree. What is undeniable is that "skin in the game" cuts both ways: it incentivises performance, and it can also generate proxy fights.

But to get to a place where shareholders fight about your stock grants, you first have to make the stock worth fighting over. That is what the next chapter is about.

V. The "Battle Gear" Strategy: Operational Excellence

In 2018, after surviving the GST and IDBI gauntlet, Siva and his team made a decision that, in retrospect, was the inflection point: they would stop trying to be everything to everyone.

For decades, Indian garment exporters — Gokaldas included — had operated on what the industry calls the "any-order" model. A buyer's procurement team would email out an RFQ for, say, 80,000 women's blouses in seven sizes and four colorways. Twenty Indian factories would bid. The lowest viable bidder won. Margins on these one-off, "chase-the-order" jobs hovered around 5–7 percent before factory overheads. Every factory floor was a chaotic mosaic of different SKUs, different fabrics, different stitch counts, different buyer requirements. Line balancing was a nightmare. Defect rates were uneven. Workers retrained for new products constantly.

Siva's first strategic call — what the company has internally called the "Battle Gear" strategy in some of its investor presentations — was to deliberately concentrate the customer book on a smaller number of larger relationships, then optimize the factory floor around their specific needs.[^9] The "big three" became Gap (and its sister brands Old Navy and Banana Republic), Columbia Sportswear, and H&M. Together these three customer groups have accounted for over half of Gokaldas's revenue in recent years.9

This sounds risky. Customer concentration is, in fact, one of the most-flagged risks in textile equity research. If Gap pivots its sourcing strategy, your top-line takes a hammering. But concentration also has a powerful flip side. When a factory dedicates entire lines — sometimes entire facilities — to a single buyer's quality system, the productivity gains are extraordinary. Setup times collapse. Worker training is amortised. Defect rates fall. Buyer audits become easier. The buyer's design teams begin sharing prototypes earlier, which lets the factory plan capacity better, which improves on-time-delivery, which earns more share-of-wallet from the buyer. The flywheel turns.

The second move was geographic. Bengaluru, where Gokaldas was born and still headquarters, had become an expensive place to make garments. Karnataka's minimum wages had risen significantly over the 2010s. Bengaluru's labor pool was being pulled into the tech and BPO sectors, raising both wages and attrition for garment workers. Real estate around the older Peenya and Bommasandra industrial areas was no longer competitive.

Siva began deliberately shifting capacity to states with lower wage costs and more aggressive industrial subsidies — particularly Madhya Pradesh and Jharkhand, where state governments had introduced specific garment-park incentive schemes.[^9] New facilities went up in MP. Some Bengaluru lines were consolidated. The company also leaned into the existing units in Karnataka's northern districts and into Tamil Nadu. This was not glamorous work. It involved acquiring land, navigating state-level labor approvals, training fresh workers from scratch, and absorbing the productivity hit of a new facility's first 18 months. But by 2022, the effective average wage cost across the Gokaldas footprint had fallen materially, and capacity had grown.

The third operational lever, less visible from the outside, was inventory and lead-time discipline. Fast fashion had restructured the apparel buyer's expectations. Where in 2007 a buyer might have placed an order six months ahead of season, by 2018 the same buyer expected an eight-week response on a "replenishment" SKU. Gokaldas reorganised its supply chain — fabric pre-positioning, dedicated production blocks, in-house trim warehousing — to compress lead times. Faster turnaround commanded a price premium and locked in repeat business.

The cumulative effect on the P&L was the kind of transformation that, in retrospect, looks obvious but was anything but. EBITDA margins, which had been hovering in the low single digits for most of the Blackstone era, began climbing steadily into the high single digits and then into double digits.9 Revenue, which had been a flatlining ₹1,000–1,200 crore for nearly a decade, broke out and began compounding. By FY2024, the company's annual revenue had crossed ₹2,800 crore, with EBITDA margins materially above the historic average.9 The market, slowly at first and then violently, repriced the stock.

By 2023, Gokaldas was trading at an earnings multiple that put it in the conversation with the better-quality Indian textile mid-caps. The stock had risen by an order of magnitude from its 2017 lows. At that moment, with public-market currency in hand and management confidence restored, Siva did something many turnaround CEOs never do: he put on his M&A hat.

VI. The M&A Blitz: Benchmarking the "Steals"

There is a well-known asymmetry in M&A literature. Companies trading at high multiples can acquire companies trading at low multiples, and the acquisition is mechanically accretive to earnings per share. This is not financial alchemy; it is arithmetic. But the asymmetry only works if the acquired company is not actually broken, and if the integration does not destroy the value the multiple was supposed to capture.

In 2023–2024, with Gokaldas's own EV/EBITDA multiple having expanded toward the mid-teens, Siva and his board went hunting. They closed two transformative deals within a single calendar window.

The Atraco Group acquisition was announced in early 2024 and closed shortly thereafter. Gokaldas paid approximately $55 million for Atraco — a UAE-headquartered manufacturer whose actual factories are in Kenya and Ethiopia — at an enterprise value to EBITDA multiple of roughly 7x.5 On its face, $55 million for a single garment manufacturer is a meaningful check for a company Gokaldas's size. But the strategic logic is where this gets interesting.

Atraco's factories sit inside two trade preference regimes that are extremely difficult to replicate. The African Growth and Opportunity Act (AGOA), enacted by the US Congress in 2000, allows duty-free entry into the United States for apparel manufactured in qualifying sub-Saharan African countries.[^14] Both Kenya and Ethiopia are AGOA beneficiaries. For comparison, apparel shipped directly from India into the US generally faces tariffs in the high single digits to mid-teens, depending on the HS code and fiber composition. That tariff differential — call it 10–12 percentage points on the landed cost — is, in a business where gross margins might be 25–30 percent, the difference between being competitive and being uncompetitive on price-sensitive SKUs.[^14] Atraco also gives Gokaldas duty-free access to the European Union via the EU's "Everything But Arms" preferences for Least Developed Countries (in Ethiopia's case) and various preferential agreements for Kenya.

In other words, Gokaldas didn't just buy 40 million pieces of incremental capacity. It bought a regulatory moat. At a moment when the United States was reaching for tariff levers against China and was selectively raising duty rates on Bangladesh and Vietnam, Gokaldas had quietly secured production geographies that paid zero US import duty on the same SKU.

The Atraco deal also brought operational diversification. The Ethiopian unit at Hawassa Industrial Park is one of the largest single-site garment factories in East Africa. Ethiopia's labor cost base is among the lowest in any meaningful garment-producing geography globally — wages roughly 30–40 percent below even Bangladesh.[^14] Yes, there are political-stability risks (we'll get to those in the bear case). But the cost arithmetic is striking.

The Matrix Clothing acquisition, announced on February 5, 2024, was even larger in rupee terms. Gokaldas agreed to acquire Matrix Clothing for an enterprise value of approximately ₹489 crore, again at roughly 7x EV/EBITDA.6 Matrix is a Delhi-based, knitwear-focused garment exporter with a strong book of UK and European customers. For Gokaldas, which had historically been overwhelmingly a woven house, this was a deliberate strategic acquisition of capability in the knit segment.

Knits matter for two reasons. First, they are typically higher margin than wovens at the equivalent SKU complexity, because the knit fabric supply chain is shorter and the process less labor-intensive once volume scales. Second, knits drive fast-fashion cycles — t-shirts, polos, base-layer wear — which means more orders per year per customer relationship, and therefore higher capacity utilisation than the seasonality of woven outerwear can deliver. Matrix's existing UK and European book — covering retailers like Primark, M&S, and others — also diversified Gokaldas's regional exposure away from the very heavy US/Gap concentration.[^9]

Here is the part that long-term investors should sit with. While Gokaldas itself was trading at roughly 14x EV/EBITDA on the Indian markets in early 2024, the company was acquiring strategic, scale, regulatory-moat assets at 7x EV/EBITDA.56 The multiple arbitrage — roughly two-times — is the kind of capital allocation that, applied consistently over a decade, can compound shareholder returns at rates that pure organic growth cannot match. It is, in spirit, very close to the playbook that Constellation Software, Heico, and a handful of other obsessive serial acquirers have used in adjacent industries.

The question, of course, is whether the integration sticks. Garment M&A has a poor historical track record. Cultural integration in factories — where line supervisors and floor managers run the operation more than the C-suite does — is harder than in software. Currency exposure across India, US dollars, Kenyan shillings, Ethiopian birr, and euros adds complexity. And the proxy-advisory and minority-shareholder concerns about leverage and pay structure (see Section IV) have not gone away.

The early signals on integration, through the first full year of Atraco and Matrix in the reported numbers, were broadly encouraging. Capacity utilisation in Africa rose. Knit capacity in India was expanded and deepened. Margins did not collapse on consolidation. But these acquisitions are still early innings — long-term holders should watch the next several quarterly reports closely for the integration metrics.

The deeper question Siva had asked himself in 2023, before pulling the trigger on Atraco and Matrix, was a different one. The question was: where in this business can we capture margin that the rest of the industry is leaving on the table?

He had an answer.

VII. The "Hidden" Growth Engines

If you walked the floor of an old-school Indian garment exporter in 2015 — including Gokaldas itself in that era — you would have seen a brilliant cut-and-sew operation that started its day by receiving someone else's fabric. Bales of woven cotton would arrive at the loading dock from a fabric mill in Coimbatore, or from a Chinese mill in Zhejiang, or from a Sri Lankan supplier. The fabric had already been dyed, finished, calendered, and rolled by someone else. The garment factory's role was to take it from there: cut it, sew it, wash it, finish it, pack it, ship it.

That structure leaves money on the table. A meaningful fraction of the value in a finished garment lives in the fabric processing stage — the dyeing, the chemical finishing, the dimensional stabilisation. Industry studies suggest that for a typical knit t-shirt, the processing margin can represent 300–400 basis points of gross margin that the garment maker never sees, because that margin is captured by the dyer / processor upstream. Multiply that by tens of millions of garments per year, and you are talking about real money.

Siva's team made the bet that for the knit segment in particular, vertical integration into fabric processing was worth the capital investment. In recent years, Gokaldas announced and built out a dedicated knit fabric processing unit in Tamil Nadu, with the explicit goal of capturing that processing margin in-house for the knit volumes that the Matrix acquisition (and the company's broader knitwear push) would generate.[^9] This is a textbook example of using a strategic acquisition to justify a downstream capex investment that, on its own, would not have had enough volume to clear hurdle rates.

Vertical integration in textiles is a delicate art. Over-integrate and you lose flexibility — you end up running your own captive dye-house at low utilisation when buyer mix shifts. Under-integrate and you cede margin permanently. The discipline is to integrate only where the volume is genuinely captive, the technology is mature, and the processing capability becomes a competitive differentiator. The knit processing unit was, on those tests, the right kind of integration. It also dramatically compresses lead times, because in-house processing eliminates a two-to-three-week link in the supply chain.

The second hidden growth engine is the segment mix shift itself. Gokaldas has been steadily and deliberately rotating its product mix toward knits.9 Wovens are still the larger absolute revenue contributor and remain the company's heritage capability — but the marginal incremental investment dollars over the past three years have flowed disproportionately toward knit capability. The reasons go beyond the basis-point margin advantage. Knits, structurally, give the company faster inventory turnover, more responsiveness to fast-fashion buyers, and exposure to product categories — activewear, athleisure, base layers — that have been the fastest-growing parts of Western apparel retail over the past decade.

The third hidden growth engine, less hidden after the Atraco deal but still under-appreciated in the equity story, is what one might call the China Plus One geographic dividend. The phrase 中国加一 "China Plus One" has been repeated so often in Indian capital-markets media over the past five years that it has become a cliche. But the underlying shift is real, structural, and very much still in its early innings. Western retailers, having spent the 2000s and 2010s building their supply chains around Chinese capacity, have been actively diversifying sourcing toward Vietnam, Bangladesh, India, Indonesia, and increasingly Africa.[^15] Gokaldas's footprint — India, Kenya, Ethiopia — gives it the option to route a customer's order through whichever geography optimises for that customer's specific landed-cost calculus, lead-time requirement, and tariff exposure.

This kind of multi-country sourcing flexibility is something that a single-country competitor — a Bangladeshi factory locked in Dhaka, or an Indian factory tied to Tirupur — cannot offer. And as US trade policy becomes more granular and politicised — selectively raising duties on specific countries, threatening Section 301 investigations, conditioning trade preference renewals on labor and environmental criteria — that flexibility becomes more valuable each year. A retailer in Bentonville staring at a 25 percent surprise tariff on Bangladeshi cotton woven shirts wants a vendor who can within weeks shift that order to a duty-free Kenyan line. Gokaldas can. Most of its peers cannot.

There is a fourth, even quieter engine that deserves a line: customer mix evolution. Over the past three years, Gokaldas has been steadily adding new customer relationships beyond the legacy big-three — including, by management commentary, additional US specialty retailers and European fast-fashion buyers.[^9] The dependence on Gap specifically has been diluting, which materially de-risks the customer concentration story that has long worried analysts.

So what should an investor be watching as a forward indicator? Three KPIs matter more than any others. First, realised EBITDA margin on a consolidated, post-integration basis — because that is the single number that captures whether the acquisitions and the knit-processing capex are actually delivering the promised margin uplift. Second, revenue mix between wovens, knits, and the Africa footprint — because the strategic thesis lives or dies on the rotation toward higher-margin and tariff-advantaged segments. Third, return on capital employed at the consolidated level, because that is what tells you whether the rapid M&A and capex deployment is value-creative or value-destructive.

These three numbers, tracked quarter over quarter, will tell the long-term shareholder more than any earnings call commentary or sell-side note ever will.

VIII. Playbook: Business & Analysis

Step back from the quarterly noise for a moment. What is Gokaldas, fundamentally, as a business? And what frameworks help us understand whether it is structurally advantaged or structurally fragile?

Hamilton Helmer's 7 Powers framework offers a useful lens. Let us walk through which powers actually apply here, and where the company has only mild advantages rather than durable moats.

Cornered Resource. This is probably the strongest of Gokaldas's structural powers. The duty-free trade status enjoyed by its Kenyan and Ethiopian operations under AGOA is a regulatory cornered resource of meaningful economic value.[^14] You cannot simply build a factory in Karnataka and replicate this. You either have AGOA-eligible production geography or you don't. The barrier is policy, not capital. And as Western trade policy has tilted toward bilateralism and selective tariff regimes, the value of that cornered resource has, if anything, grown.

Scale Economies. Gokaldas's combined post-acquisition footprint — across India and East Africa — gives it an annualized capacity of tens of millions of garments across multiple product categories and geographies.59 That kind of scale is genuinely difficult for smaller competitors to match. Western retailers want vendors who can absorb their full Asian-sourced volume of a category without splintering across ten different factories. Gokaldas can be the consolidated vendor on a category in a way that a $50 million-revenue regional competitor cannot.

Switching Costs. Switching costs in apparel manufacturing are higher than they look, and lower than ideal. Higher than they look because once a buyer has integrated a vendor into their design and tech-pack workflow, qualified the vendor on social-compliance audits, established quality history, and locked them into a season's calendar, moving away from that vendor costs the buyer real time and risk. Lower than ideal because there is no exclusive contract; every season, every SKU is theoretically up for rebid. The switching cost is real but soft.

Counter-Positioning, Network Economies, Branding, and Process Power are largely not applicable in this business. There is no two-sided network. There is no consumer brand. Process power exists at the margin — Gokaldas's design-to-delivery capability is a real operational advantage built over decades — but it can be replicated by a well-funded competitor over time.

Now let us run Porter's Five Forces on the industry as a whole, briefly, because the macro-structural picture matters.

Threat of New Entrants at the small-vendor level is high. A new garment factory in Tirupur or Dhaka or Hanoi can be set up in 18 months with reasonable capital. But the threat of new entrants at the scale Gokaldas operates — multi-country, multi-product, multi-buyer-relationship — is much, much lower. The barrier is not capital. It is the qualification and relationship history with global retailers, which takes a decade-plus to build.

Bargaining Power of Buyers is high. Gap, H&M, and Columbia are large, sophisticated, professional procurement organisations. They price every SKU mercilessly. The mitigation is geographic and product diversification on Gokaldas's side — if Gap pushes too hard on price for woven chinos out of India, Gokaldas can refer them to Kenya, or pivot capacity to Columbia's outerwear program. Multi-buyer leverage is real.

Bargaining Power of Suppliers. Cotton and yarn are commoditised globally. Trim suppliers are fragmented. Dye and chemical suppliers have some pricing power but face competition. Net, supplier power is moderate.

Threat of Substitutes. Garments are garments. Substitution at the category level (more synthetics, more athleisure, more secondhand) does occur but slowly. Not a near-term P&L threat.

Rivalry Among Existing Competitors. Intense. Indian, Bangladeshi, Vietnamese, Chinese, and now African manufacturers all chase the same Western retail volumes. Margins are thin. The winners are the ones who deliver service, reliability, lead time, and increasingly, trade-tariff arbitrage. Gokaldas's structural positioning here is good but not unassailable.

Myth versus reality. A common consensus narrative about Gokaldas runs: "this is a cyclical garment business riding the China Plus One wave; once that wave subsides, multiple compression will be brutal." There is a kernel of truth in this — the company is, undeniably, in a cyclical business, and multiple compression in apparel cycles has historically been violent. But the consensus narrative misses two things. First, the duty-free Africa footprint is not a cyclical asset; it is a structural one, and its value rises with every passing trade-policy headline. Second, the multiple arbitrage embedded in the Atraco and Matrix acquisitions — buying at 7x while trading at 14x — is mechanical value creation that does not depend on cycle timing. The cyclical-trader's framing of Gokaldas materially under-appreciates the structural overlay.

The management lesson. There is a broader insight from the Gokaldas story that goes beyond textiles. Indian listed companies have a long history of either being founder-run (Reliance, Bajaj, the Birla group, the Tata-controlled companies) or being run by hired professional CEOs whose ownership is essentially zero. The Gokaldas experiment — a meaningful equity stake in the hands of a non-founder professional MD — is structurally rare in India. The fact that it has worked, at least over the eight-year horizon since Siva took over, is a useful data point for governance theorists. It also raises, of course, the question of what happens when the same equity-owning CEO seeks to expand his ownership through ESOPs, which is precisely the proxy-fight tension that flared up in early 2025.[^12] Skin in the game is a powerful incentive structure. It also requires ongoing governance discipline.

A second-layer diligence note worth flagging: Gokaldas's working-capital intensity and reliance on bank credit lines — a structural feature of the garment-export business — means that any material change in the company's credit rating, or any sudden change in the export-finance environment (such as a re-tightening at IDBI-type lenders, or a US tariff shock that disrupts collections), can transmit fast to operating performance. The 2017 IDBI episode was not a one-off curiosity; it was an early lesson in how working-capital fragility shapes garment exporters globally.

These structural and governance factors set up the question that the next and final section addresses: where does Gokaldas go from here?

IX. Conclusion & Future Outlook

It is 2026, and a long-term shareholder of Gokaldas Exports faces a fundamentally different company from the one that Mathew Cyriac bought out of Blackstone's portfolio nine years ago.

In 2017, the bull case rested almost entirely on a turnaround thesis: bring in professional management, restore EBITDA margins to industry-average levels, and let the multiple re-rate. That thesis has fully played out. The stock has been one of the great Indian small-cap-to-mid-cap migrations of the past decade. The Hinduja-founded business that Blackstone could not turn now sits at the centre of a multi-country, multi-product, multi-buyer platform with structural tariff advantages and a deepening vertical footprint.

The new bull case — the one that matters for the next five years, not the last eight — is more ambitious. It is the "Inditex of Manufacturing" thesis. The argument runs: Gokaldas is one of the very few apparel manufacturers globally that combines (a) genuine scale, (b) multi-geography production flexibility with regulatory advantages, (c) vertical integration into fabric processing, (d) a deep customer book with the leading Western mass-market and specialty retailers, and (e) a management team with both the capital allocation discipline and the operational chops to keep compounding through M&A.[^9]9 Each Atraco-style deal, executed at a 7x multiple while the parent trades at 14x, creates mechanical value. Each integrated processing unit captures basis points of margin that the industry routinely cedes. Each new customer relationship in a new geography deepens the moat against single-country competitors.

The bear case has not gone away, and any honest long-term holder must internalise it. Three risks deserve special attention.

First, geopolitical risk in Africa. The Ethiopia operation, while operationally excellent and tariff-advantaged, sits in a country that has experienced significant internal conflict in recent years. The political stability of Ethiopia and, to a lesser extent, Kenya is not Gokaldas's to control. A disruption to the Ethiopian production base — whether from internal politics, transport disruptions, or workforce instability — would materially hurt the consolidated economics. The mitigation is the multi-country footprint itself: Indian and Kenyan capacity can flex up, but not without lead time.

Second, US trade policy risk. The entire Africa value proposition rests on AGOA. AGOA is not permanent. It requires periodic renewal by the US Congress, and its eligibility criteria are politically reviewed.[^14] If AGOA were not renewed, or if Ethiopia or Kenya were to lose AGOA-beneficiary status due to political or labor criteria, the tariff arbitrage would vanish. This is, in some sense, the same risk that any concentrated-trade-preference business carries; it has been worth taking for the past quarter-century, but it is real.

Third, executive compensation and proxy governance. The early-2025 vote in which institutional shareholders blocked a proposed ESOP grant to the MD is a meaningful signal.[^12] Indian institutional governance is becoming more activist. Compensation structures that worked in earlier turnaround phases — when getting the right CEO at any price was the priority — may face more scrutiny as the company matures into a mid-cap with broader institutional ownership. Skilfully navigating that scrutiny without losing the alignment that has driven the company's transformation is its own management challenge.

Beyond those three named risks, the standard portfolio of apparel-industry concerns — discretionary consumer demand cycles, currency volatility across multi-geography revenue, fashion-trend disruption, labor-cost inflation, ESG and worker-safety scrutiny — all still apply. None of them are unique to Gokaldas, but none of them go away.

Three KPIs to watch, restated for emphasis: consolidated EBITDA margin (the integration test), the revenue mix between wovens, knits, and the African footprint (the strategic-shift test), and consolidated return on capital employed (the capital-allocation test). If those three numbers continue to trend in the right direction over the coming quarters, the structural story stays intact. If any of them inflects materially the wrong way, that is the early-warning system.

And so, what is the final reflection on a business that went from family-founded export workshop to PE-backed disappointment to professionally-run global manufacturer in a single business lifetime?

It is this: in emerging markets, the rarest commodity is not capital. Capital can be raised. Plants can be built. Multiples can be re-rated. The rare commodity is the operationally obsessed owner-manager — the person who runs the factory floor as if their own bank account depends on it, because it actually does. Blackstone, for all its sophistication, was unable to manufacture that ownership mindset by remote control from Mumbai or New York. Mathew Cyriac, by walking up to his college classmate and handing him both the keys and a real piece of the equity, manufactured it on the first try.

That is the Gokaldas masterclass. The factories, the customers, the fabric — they were always there. What changed was who looked after them, and what those people had to lose. From a "textbook failure" in Blackstone's portfolio to a textbook turnaround in someone else's: the cloth was the same the whole time. The hands holding it were different.

The needle keeps moving.

References

References

-

How Gokaldas Exports is weaving a new success story — Forbes India, 2022 ↩↩↩↩

-

Gokaldas Exports to acquire Matrix Clothing for enterprise value of Rs 489 cr — Business Standard, 2024-02-05 ↩↩↩

-

Gokaldas Exports Investor Relations — Annual Reports and Filings ↩

-

Gokaldas Exports FY2024 Annual Report — Financial Statements and MD&A ↩↩↩↩↩↩

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube